Smart Money Proxy IndexOverview

The Smart Money Proxy Index (SMPI) is an educational tool that attempts to identify potential institutional-style behavior patterns using publicly available market data. This comprehensive tool combines multiple institutional analysis techniques into a single, easy-to-read 0-100 oscillator.

Important Disclaimer

This is an educational proxy indicator that analyzes volume and price patterns. It cannot identify actual institutional trading activity and should not be interpreted as tracking real "smart money." Use for educational purposes and combine with other analysis methods.

Inspiration & Methodology

This indicator is inspired by MAPsignals' Big Money Index (BMI) methodology but uses publicly available price and volume data with original calculations. This is an independent educational interpretation designed to teach smart money concepts to retail traders.

What It Analyzes

SMPI tracks potential "smart money" activity by combining:

Block Trading Detection - Identifies unusual volume surges with significant price impact

Money Flow Analysis - Volume-weighted price pressure using Money Flow Index

Accumulation/Distribution Patterns - Modified On-Balance Volume signals

Institutional Control Proxy - End-of-day positioning and control analysis

Key Features

– Multi-Component Analysis - Combines 4 different institutional detection methods

– BMI-Style 0-100 Scale - Familiar oscillator range with clear extreme levels

– Professional Visualization - Dynamic colors, gradient fills, and clean data table

– Comprehensive Alerts - Buy/sell signals plus divergence detection

– Fully Customizable - Adjust all parameters, colors, and display options

– Non-Repainting Signals - All alerts use confirmed data for reliability

– Educational Focus - Designed to teach institutional flow concepts

How to Interpret

Above 80: Potential smart money distribution phase (bearish pressure)

Below 20: Potential smart money accumulation phase (bullish opportunity)

Signal Generation: Buy signals when crossing above 20, sell signals when crossing below 80

Divergences: Price vs SMPI divergences can signal potential trend changes

Volume Confirmation: Higher volume ratios strengthen signal reliability

Best Practices

Timeframes: Works best on higher timeframes for institutional behavior analysis

Confirmation: Combine with other technical analysis tools and market context

Volume: Pay attention to volume confirmation in the data table

Context: Consider overall market conditions and fundamental factors

Risk Management: Not recommended as standalone trading system

Customizable Parameters

Block Volume Threshold: Sensitivity for unusual volume detection (default: 2.5x average)

SMPI Smoothing Period: Index calculation smoothing (default: 25 bars)

Extreme Levels: Overbought/oversold thresholds (default: 80/20)

Money Flow Length: MFI calculation period (default: 14)

Visual Options: Colors, signals, and display preferences

Available Alerts

Buy Signal: SMPI crosses above oversold level (20)

Sell Signal: SMPI crosses below overbought level (80)

Extreme Levels: Alerts when reaching overbought/oversold zones

Divergence Detection: Bullish and bearish price vs SMPI divergences

Educational Purpose & Limitations

This indicator is designed as an educational proxy for understanding institutional flow concepts. It analyzes publicly available price and volume data to identify potential smart money behavior patterns.

Cannot access actual institutional transaction data

Signals may be slower than day-trading indicators (intentionally designed for institutional timeframes)

Should be used in conjunction with other analysis methods

Past performance does not guarantee future results

What Makes This Different

Unlike simple volume or momentum indicators, SMPI combines multiple institutional analysis techniques into one comprehensive tool. The multi-component approach provides a more robust view of potential smart money activity.

Indicadores e estratégias

AI BUY AND SELL BGThe Gk fundamental is a next gen level ai powered BUY and SELL system engineered for big market moves, it runs an embedded algorithm within a algorithm to detect breakout points before they happen giving traders insane results

works best and only 2h and 4h

SulLaLuna — HTF M2 x Ultimate BB (Fusion) 🌕 **SulLaLuna — HTF M2 x Ultimate BB (Fusion)** 🚀💵

**By SulLaLuna Trading**

(Portions of the Bollinger Band logic adapted with permission/credit from the *Ultimate Buy & Sell Indicator* by its original author — thank you for the brilliance!)

---

🧭 **What This Is**

This is not just another price-following tool.

This is **a macro liquidity detector** — a **Daily Higher Timeframe Hull Moving Average of the Global M2 Money Supply**, smoothed via lower timeframe candles (default 5m, 48 Hull length), overlaid with **Ultimate-style double Bollinger Bands** to reveal *over-extension & mean reversion zones*.

It doesn’t chase candles.

It watches the tides beneath the market — the **money supply currents** that have a **direct correlation** to asset price behavior.

When liquidity expands → risk-on assets tend to rise.

When liquidity contracts → risk-off waves hit.

We ride those waves.

---

🔍 **What It Does**

* **Tracks Global M2** across major economies, FX-adjusted, and scales it to your chart’s price.

* **HTF Hull MA** (Daily, smoothed via 5m base) → gives you the macro liquidity trend.

* **Ultimate BB logic** applied to the HTF M2 Hull → inner/outer bands for volatility envelopes.

* **Pivot Labels** → ideal entry/exit zones on macro turns.

* **Over-Extension Alerts** → when HTF M2 Hull pushes outside the outer bands.

* **Re-Entry Alerts** → mean reversion triggers when liquidity moves back inside the range.

* **Background Paint** from chart TF M2 slope → for confluence on your entry timeframe.

---

📜 **Suggested How-To**

1. **Choose your execution chart** — e.g., 1–15m for scalps, 1H–4H for swings.

2. **Use the background paint** as your *local tide check* (chart TF M2 slope).

3. **Trade in the direction of the HTF M2 Hull** — green line = liquidity rising, red line = liquidity falling.

4. **Watch pivot labels** — these are potential “macro inflection” points.

5. **Confluence stack** — pair with ZLSMA, WaveTrend divergences, VWAP volume, or your favorite price-action setups.

6. **Size down** when HTF M2 Hull is flat/gray (chop zone).

7. **Scale in/out** on over-extension + re-entry alerts for higher probability swings.

---

⚠️ **Important Note**

This indicator **does not predict price** — it tracks macro liquidity flows that *influence* price.

Think of it as your market’s **tide chart**: when the water’s coming in, you can swim out; when it’s going out, you’d better be ready for the undertow.

---

📢 **Alerts Available**

* HTF Pivot HIGH / LOW

* Over-Extension (HTF Hull outside outer BB)

* Re-Entry (return from overbought/oversold)

---

🤝 **Join the SulLaLuna Tribe**

If this indicator helps you capture better entries, follow & share so more traders can learn to trade *math, not emotion*.

We rise together — **and we’ll meet you on the Moon** 🌕🚀💵.

Fibo Channel + MFI LabelOVERVIEW

Fibo Channel + MFI Label plots a logarithmic regression channel with Fibonacci bands and adds a live Money Flow Index (MFI) marker + value at the channel’s right edge. It helps you see where price sits inside the channel while reading volume-weighted momentum from MFI in one glance.

Clean dotted Fibo bands across the log channel (0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0).

Auto labels for each band with % and price.

MFI dot + label that you can offset to the right to keep the chart clear.

PRINCIPLES

Log Regression Channel: Fits price on a log scale and projects a channel that adapts to trend slope.

Fibonacci Bands: Seven equidistant lines between channel bottom/top for quick context of extension/mean reversion.

MFI Overlay: MFI (0–100) is clamped to a 30–70 working band, then mapped vertically inside the right edge of the channel—so momentum is visual, not hidden in a subpane.

HOW TO USE

Context: Treat fibo lines as dynamic zones—reaction near 0.382/0.618 often signals minor pullbacks; 0/1 extremes = stretched.

Momentum Check: The MFI dot gives instant read—rising toward top of the channel with MFI > 50 supports trend continuation; fading toward mid/low warns of loss of pressure.

Clarity: Use the offset inputs to push the dot/label right of the last candle so they don’t overlap price.

FEATURES

Real-time Fibo lines with percentage + price labels.

Adaptive color for the channel (Up/Down) based on regression slope.

Separate X-offsets for the MFI circle and the text label.

Lightweight: no tables, no repainting tricks, just lines + labels.

Fibo line color changes automatically with channel trend direction.

SETTINGS

MFI Length – period for Money Flow Index.

LogReg Lookback / Channel Length / Channel Width – shape and span of the channel.

Up/Down Colors – channel palette.

Fibo Label X Offset – move fibo labels horizontally.

MFI Circle X Offset – move the dot horizontally.

MFI Label X Offset – move the MFI text horizontally.

NOTES

Best on symbols with reliable volume.

MFI is clamped to 30–70 before mapping inside the channel for cleaner placement.

Requires at least Channel Length bars before drawing.

SUMMARY

Fibo Channel + MFI Label combines a logarithmic regression channel with Fibonacci levels and an on-chart Money Flow Index marker. The channel provides dynamic support/resistance zones based on price’s log-scale trend, while the fibo bands give clear percentage retracement levels. The MFI dot and label display live volume-weighted momentum directly on the price chart, with adjustable offsets for optimal visibility. This tool is designed for traders who want quick visual confirmation of trend direction, price location, and momentum strength without switching between multiple indicators.

DISCLAIMER

For educational purposes only. This is not financial advice. Trading involves risk.

Global Bond Yields Monitor [MarktQuant]Global Bond Yields Monitor

The Global Bond Yields Monitor is designed to help users track and compare government bond yields across major economies. It provides an at-a-glance view of short- and long-term interest rates for multiple countries, enabling users to observe shifts in global fixed-income markets.

Key Features:

Multi-Country Coverage: Includes major advanced and emerging economies such as the United States, China, Japan, Germany, United Kingdom, Canada, Australia, and more.

Multiple Maturities: Displays yields for the 2-year, 5-year, 10-year, and 30-year maturities (20-year for Russia).

Dynamic Yield Data: Plots real-time yields for the selected country directly from TradingView’s data sources.

Weekly Change Tracking: Calculates and displays the yield change from one week ago ( ) for each maturity.

Table Visualization: Option to display a compact data table showing current yields and weekly changes, color-coded for easier interpretation.

Visual Yield Curve Comparison: Plots yield lines for short- and long-term maturities, with shaded areas between curves for visual clarity.

Customizable Display: Choose table placement and whether to show or hide the weekly change table.

Use Cases

This script is intended for analysts, traders, and investors who want to monitor shifts in sovereign bond markets. Changes in yields can reflect adjustments in monetary policy expectations, inflation outlook, or broader macroeconomic trends.

❗Important Note❗

This indicator is for market monitoring and educational purposes only. It does not generate trading signals, and it should not be interpreted as financial advice. All data is sourced from TradingView’s available market feeds, and accuracy may depend on the source data.

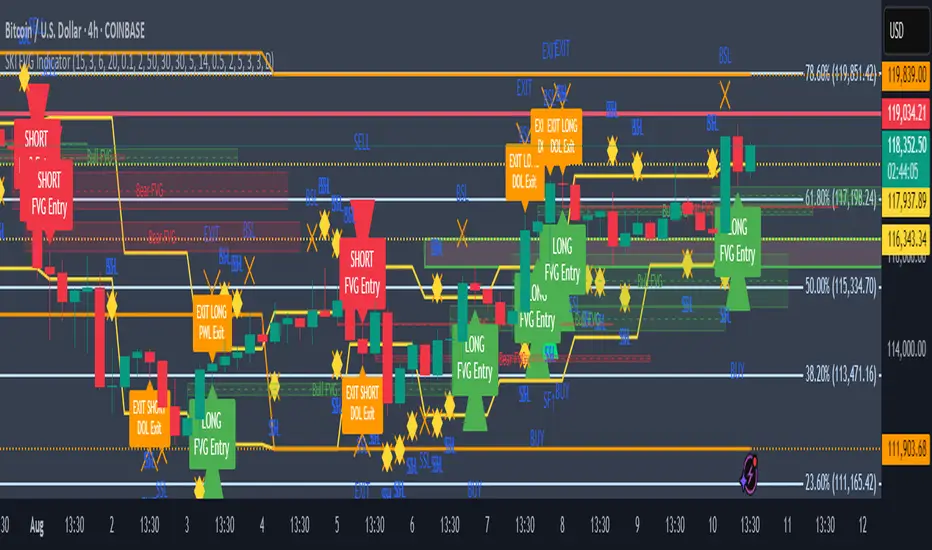

SKI FVG IndicatorIt uses ICT concepts and takes entries and exits. Identifies good FVG and shows an entry to buy or short and also exits at swing high or low , discount areas, primary areas, DOL (draw on liquidity)

Engulfing + Sweep (Confirmed Only) v6 — bars onlyMarks bullish/bearish engulfing candles with liquidity sweeps and confirms them on the next candle — no repaint.

✳️ Features:

• 🟩 Bullish Engulfing + Low Sweep

• 🟥 Bearish Engulfing + High Sweep

• 🎛 Require opposite-color previous candle (optional)

• 📏 Min body-to-range filter

• 🔔 Alerts on confirmation candle

🎯 Best for:

• Price action & reversal traders

• Liquidity sweep confluence setups

Minimal S/R Zones with Volume StrengthHow it works

Pivot Detection

A pivot high is a candle whose high is greater than the highs of a certain number of candles before and after it.

A pivot low is a candle whose low is lower than the lows of a certain number of candles before and after it.

Parameters like Pivot Left Bars and Pivot Right Bars control how sensitive the pivots are.

Zone Creation

Pivot High → creates a Resistance zone.

Pivot Low → creates a Support zone.

Each zone is defined as a price range (top and bottom) and drawn horizontally for a given lookback length.

Volume Strength Filter

Volume Strength (%) = (Volume at Pivot / Volume SMA) × 100.

If the strength is below the minimum threshold (Min Strength %), the zone is ignored.

This ensures only pivots with significant trading activity create zones.

Zone Management

The indicator stores zones in arrays.

Max Zones per side prevents too many zones from being displayed at once.

Older zones are removed when new ones are added beyond the limit.

Visuals

Support zones → green label with Volume Strength %.

Resistance zones → red label with Volume Strength %.

Zones have semi-transparent boxes so price action remains visible.

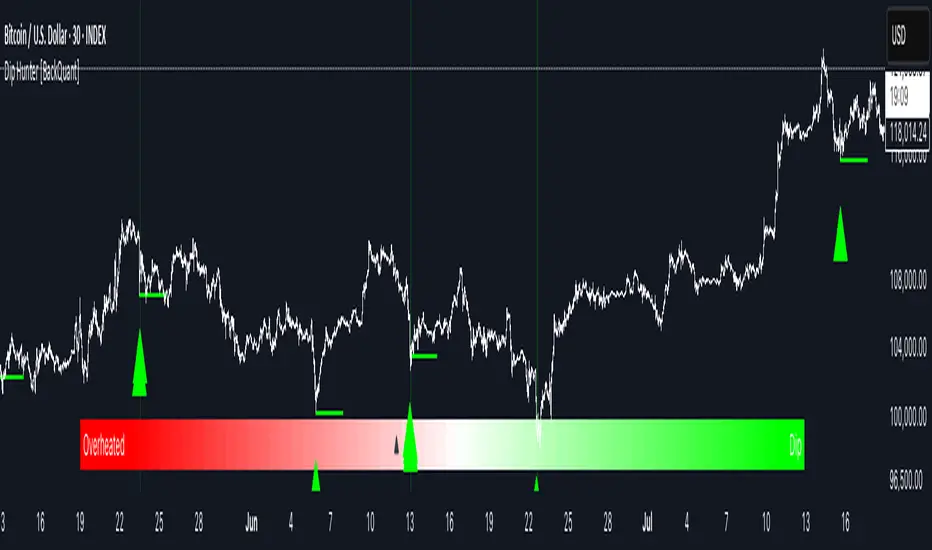

Dip Hunter [BackQuant]Dip Hunter

What this tool does in plain language

Dip Hunter is a pullback detector designed to find high quality buy-the-dip opportunities inside healthy trends and to avoid random knife catches. It watches for a quick drop from a recent high, checks that the drop happened with meaningful participation and volatility, verifies short-term weakness inside a larger uptrend, then scores the setup and paints the chart so you can act with confidence. It also draws clean entry lines, provides a meter that shows dip strength at a glance, and ships with alerts that match common execution workflows.

How Dip Hunter thinks

It defines a recent swing reference, measures how far price has dipped off that high, and only looks at candidates that meet your minimum percentage drop.

It confirms the dip with real activity by requiring a volume spike and a volatility spike.

It checks structure with two EMAs. Price should be weak in the short term while the larger context remains constructive.

It optionally requires a higher-timeframe trend to be up so you focus on pullbacks in trending markets.

It bundles those checks into a score and shows you the score on the candles and on a gradient meter.

When everything lines up it paints a green triangle below the bar, shades the background, and (if you wish) draws a horizontal entry line at your chosen level.

Inputs and what they mean

Dip Hunter Settings

• Vol Lookback and Vol Spike : The script computes an average volume over the lookback window and flags a spike when current volume is a multiple of that average. A multiplier of 2.0 means today’s volume must be at least double the average. This helps filter noise and focuses on dips that other traders actually traded.

• Fast EMA and Slow EMA : Short-term and medium-term structure references. A dip is more credible if price closes below the fast EMA while the fast EMA is still below the slow EMA during the pullback. That is classic corrective behavior inside a larger trend.

• Price Smooth : Optional smoothing length for price-derived series. Use this if you trade very noisy assets or low timeframes.

• Volatility Len and Vol Spike (volatility) : The script checks both standard deviation and true range against their own averages. If either expands beyond your multiplier the market confirms the move with range.

• Dip % and Lookback Bars : The engine finds the highest high over the lookback window, then computes the percentage drawdown from that high to the current close. Only dips larger than your threshold qualify.

Trend Filter

• Enable Trend Filter : When on, Dip Hunter will only trigger if the market is in an uptrend.

• Trend EMA Period : The longer EMA that defines the session’s backbone trend.

• Minimum Trend Strength : A small positive slope requirement. In practice this means the trend EMA should be rising, and price should be above it. You can raise the value to be more selective.

Entries

• Show Entry Lines : Draws a horizontal guide from the signal bar for a fixed number of bars. Great for limit orders, scaling, or re-tests.

• Line Length (bars) : How far the entry guide extends.

• Min Gap (bars) : Suppresses new entry lines if another dip fired recently. Prevents clutter during choppy sequences.

• Entry Price : Choose the line level. “Low” anchors at the signal candle’s low. “Close” anchors at the signal close. “Dip % Level” anchors at the theoretical level defined by recent_high × (1 − dip%). This lets you work resting orders at a consistent discount.

Heat / Meter

• Color Bars by Score : Colors each candle using a red→white→green gradient. Red is overheated, green is prime dip territory, white is neutral.

• Show Meter Table : Adds a compact gradient strip with a pointer that tracks the current score.

• Meter Cells and Meter Position : Resolution and placement of the meter.

UI Settings

• Show Dip Signals : Plots green triangles under qualifying bars and tints the background very lightly.

• Show EMAs : Plots fast, slow, and the trend EMA (if the trend filter is enabled).

• Bullish, Bearish, Neutral colors : Theme controls for shapes, fills, and bar painting.

Core calculations explained simply

Recent high and dip percent

The script finds the highest high over Lookback Bars , calls it “recent high,” then calculates:

dip% = (recent_high − close) ÷ recent_high × 100.

If dip% is larger than Dip % , condition one passes.

Volume confirmation

It computes a simple moving average of volume over Vol Lookback . If current volume ÷ average volume > Vol Spike , we have a participation spike. It also checks 5-bar ROC of volume. If ROC > 50 the spike is forceful. This gets an extra score point.

Volatility confirmation

Two independent checks:

• Standard deviation of closes vs its own average.

• True range vs ATR.

If either expands beyond Vol Spike (volatility) the move has range. This prevents false triggers from quiet drifts.

Short-term structure

Price should close below the Fast EMA and the fast EMA should be below the Slow EMA at the moment of the dip. That is the anatomy of a pullback rather than a full breakdown.

Macro trend context (optional)

When Enable Trend Filter is on, the Trend EMA must be rising and price must be above it. The logic prefers “micro weakness inside macro strength” which is the highest probability pattern for buying dips.

Signal formation

A valid dip requires:

• dip% > threshold

• volume spike true

• volatility spike true

• close below fast EMA

• fast EMA below slow EMA

If the trend filter is enabled, a rising trend EMA with price above it is also required. When all true, the triangle prints, the background tints, and optional entry lines are drawn.

Scoring and visuals

Binary checks into a continuous score

Each component contributes to a score between 0 and 1. The script then rescales to a centered range (−50 to +50).

• Low or negative scores imply “overheated” conditions and are shaded toward red.

• High positive scores imply “ripe for a dip buy” conditions and are shaded toward green.

• The gradient meter repeats the same logic, with a pointer so you can read the state quickly.

Bar coloring

If you enable “Color Bars by Score,” each candle inherits the gradient. This makes sequences obvious. Red clusters warn you not to buy. White means neutral. Increasing green suggests the pullback is maturing.

EMAs and the trend EMA

• Fast EMA turns down relative to the slow EMA inside the pullback.

• Trend EMA stays rising and above price once the dip exhausts, which is your cue to focus on long setups rather than bottom fishing in downtrends.

Entry lines

When a fresh signal fires and no other signal happened within Min Gap (bars) , the indicator draws a horizontal level for Line Length bars. Use these lines for limit entries at the low, at the close, or at the defined dip-percent level. This keeps your plan consistent across instruments.

Alerts and what they mean

• Market Overheated : Score is deeply negative. Do not chase. Wait for green.

• Close To A Dip : Score has reached a healthy level but the full signal did not trigger yet. Prepare orders.

• Dip Confirmed : First bar of a fresh validated dip. This is the most direct entry alert.

• Dip Active : The dip condition remains valid. You can scale in on re-tests.

• Dip Fading : Score crosses below 0.5 from above. Momentum of the setup is fading. Tighten stops or take partials.

• Trend Blocked Signal : All dip conditions passed but the trend filter is offside. Either reduce risk or skip, depending on your plan.

How to trade with Dip Hunter

Classic pullback in uptrend

Turn on the trend filter.

Watch for a Dip Confirmed alert with green triangle.

Use the entry line at “Dip % Level” to stage a limit order. This keeps your entries consistent across assets and timeframes.

Initial stop under the signal bar’s low or under the next lower EMA band.

First target at prior swing high, second target at a multiple of risk.

If you use partials, trail the remainder under the fast EMA once price reclaims it.

Aggressive intraday scalps

Lower Dip % and Lookback Bars so you catch shallow flags.

Keep Vol Spike meaningful so you only trade when participation appears.

Take quick partials when price reclaims the fast EMA, then exit on Dip Fading if momentum stalls.

Counter-trend probes

Disable the trend filter if you intentionally hunt reflex bounces in downtrends.

Require strong volume and volatility confirmation.

Use smaller size and faster targets. The meter should move quickly from red toward white and then green. If it does not, step aside.

Risk management templates

Stops

• Conservative: below the entry line minus a small buffer or below the signal bar’s low.

• Structural: below the slow EMA if you aim for swing continuation.

• Time stop: if price does not reclaim the fast EMA within N bars, exit.

Position sizing

Use the distance between the entry line and your structural stop to size consistently. The script’s entry lines make this distance obvious.

Scaling

• Scale at the entry line first touch.

• Add only if the meter stays green and price reclaims the fast EMA.

• Stop adding on a Dip Fading alert.

Tuning guide by market and timeframe

Equities daily

• Dip %: 1.5 to 3.0

• Lookback Bars: 5 to 10

• Vol Spike: 1.5 to 2.5

• Volatility Len: 14 to 20

• Trend EMA: 100 or 200

• Keep trend filter on for a cleaner list.

Futures and FX intraday

• Dip %: 0.4 to 1.2

• Lookback Bars: 3 to 7

• Vol Spike: 1.8 to 3.0

• Volatility Len: 10 to 14

• Use Min Gap to avoid clusters during news.

Crypto

• Dip %: 3.0 to 6.0 for majors on higher timeframes, lower on 15m to 1h

• Lookback Bars: 5 to 12

• Vol Spike: 1.8 to 3.0

• ATR and stdev checks help in erratic sessions.

Reading the chart at a glance

• Green triangle below the bar: a validated dip.

• Light green background: the current bar meets the full condition.

• Bar gradient: red is overheated, white is neutral, green is dip-friendly.

• EMAs: fast below slow during the pullback, then reclaim fast EMA on the bounce for quality continuation.

• Trend EMA: a rising spine when the filter is on.

• Entry line: a fixed level to anchor orders and risk.

• Meter pointer: right side toward “Dip” means conditions are maturing.

Why this combination reduces false positives

Any single criterion will trigger too often. Dip Hunter demands a dip off a recent high plus a volume surge plus a volatility expansion plus corrective EMA structure. Optional trend alignment pushes odds further in your favor. The score and meter visualize how many of these boxes you are actually ticking, which is more reliable than a binary dot.

Limitations and practical tips

• Thin or illiquid symbols can spoof volume spikes. Use larger Vol Lookback or raise Vol Spike .

• Sideways markets will show frequent small dips. Increase Dip % or keep the trend filter on.

• News candles can blow through entry lines. Widen stops or skip around known events.

• If you see many back-to-back triangles, raise Min Gap to keep only the best setups.

Quick setup recipes

• Clean swing trader: Trend filter on, Dip % 2.0 to 3.0, Vol Spike 2.0, Volatility Len 14, Fast 20 EMA, Slow 50 EMA, Trend 100 EMA.

• Fast intraday scalper: Trend filter off, Dip % 0.7 to 1.0, Vol Spike 2.5, Volatility Len 10, Fast 9 EMA, Slow 21 EMA, Min Gap 10 bars.

• Crypto swing: Trend filter on, Dip % 4.0, Vol Spike 2.0, Volatility Len 14, Fast 20 EMA, Slow 50 EMA, Trend 200 EMA.

Summary

Dip Hunter is a focused pullback engine. It quantifies a real dip off a recent high, validates it with volume and volatility expansion, enforces corrective structure with EMAs, and optionally restricts signals to an uptrend. The score, bar gradient, and meter make reading conditions instant. Entry lines and alerts turn that read into an executable plan. Tune the thresholds to your market and timeframe, then let the tool keep you patient in red, selective in white, and decisive in green.

Buy and Sell Signals Based on Price Channel BreakoutsThis indicator generates clear Buy and Sell signals by detecting breakouts from a price channel defined by the highest highs and lowest lows over a user-defined period.

A Buy signal triggers when the price closes above the previous bar’s channel high, indicating potential upward momentum.

A Sell signal triggers when the price closes below the previous bar’s channel low, signaling potential downward momentum.

The indicator maintains the position until an opposite breakout occurs, reducing noise and false signals common in scalping strategies.

Ideal for intraday scalpers using 1-minute or 5-minute charts who want to trade breakout momentum with simple, visual signals.

Includes alert conditions for Buy and Sell signals to keep you notified in real-time.

IU Indicators DashboardDESCRIPTION

The IU Indicators Dashboard is a comprehensive multi-stock monitoring tool that provides real-time technical analysis for up to 10 different stocks simultaneously. This powerful indicator creates a customizable table overlay that displays the trend status of multiple technical indicators across your selected stocks, giving you an instant overview of market conditions without switching between charts.

Perfect for portfolio monitoring, sector analysis, and quick market screening, this dashboard consolidates critical technical data into one easy-to-read interface with color-coded trend signals.

USER INPUTS

Stock Selection (10 Configurable Stocks):

- Stock 1-10: Customize any symbols (Default: NSE:CDSL, NSE:RELIANCE, NSE:VEDL, NSE:TCS, NSE:BEL, NSE:BHEL, NSE:TATAPOWER, NSE:TATASTEEL, NSE:ITC, NSE:LT)

Technical Indicator Parameters:

- EMA 1 Length: First Exponential Moving Average period (Default: 20)

- EMA 2 Length: Second Exponential Moving Average period (Default: 50)

- EMA 3 Length: Third Exponential Moving Average period (Default: 200)

- RSI Length: Relative Strength Index calculation period (Default: 14)

- SuperTrend Length: SuperTrend indicator period (Default: 10)

- SuperTrend Factor: SuperTrend multiplier factor (Default: 3.0)

Visual Customization:

- Table Size: Choose from Normal, Tiny, Small, or Large

- Table Background Color: Customize dashboard background

- Table Frame Color: Set frame border color

- Table Border Color: Configure border styling

- Text Color: Set text display color

- Bullish Color: Color for positive/bullish signals (Default: Green)

- Bearish Color: Color for negative/bearish signals (Default: Red)

LOGIC OF THE INDICATOR

The dashboard employs a multi-timeframe analysis approach using five key technical indicators:

1. Triple EMA Analysis

- Compares current price against three different EMA periods (20, 50, 200)

- Bullish Signal: Price above EMA level

- Bearish Signal: Price below EMA level

- Provides short-term, medium-term, and long-term trend perspective

2. RSI Momentum Analysis

- Uses 14-period RSI with 50-level threshold

- Bullish Signal: RSI > 50 (upward momentum)

- Bearish Signal: RSI < 50 (downward momentum)

- Identifies momentum strength and potential reversals

3. SuperTrend Direction

- Utilizes SuperTrend with configurable length and factor

- Bullish Signal: SuperTrend direction = -1 (uptrend)

- Bearish Signal: SuperTrend direction = 1 (downtrend)

- Provides clear trend direction with volatility-adjusted signals

4. MACD Histogram Analysis

- Uses standard MACD (12, 26, 9) histogram values

- Bullish Signal: Histogram > 0 (bullish momentum)

- Bearish Signal: Histogram < 0 (bearish momentum)

- Identifies momentum shifts and trend confirmations

5. Real-time Data Processing

- Implements request.security() for multi-symbol data retrieval

- Uses barstate.isrealtime logic for accurate live data

- Processes data only on the last bar for optimal performance

WHY IT IS UNIQUE

Multi-Stock Monitoring

- Monitor up to 10 different stocks simultaneously on a single chart

- No need to switch between multiple charts or timeframes

Highly Customizable Interface

- Full color customization for personalized visual experience

- Adjustable table size and positioning

- Clean, professional dashboard design

Real-time Analysis

- Live data processing with proper real-time handling

- Instant visual feedback through color-coded signals

- Optimized performance with smart data retrieval

Comprehensive Technical Coverage

- Combines trend-following, momentum, and volatility indicators

- Multiple timeframe perspective through different EMA periods

- Balanced approach using both lagging and leading indicators

Flexible Configuration

- Easy symbol switching for different markets (NSE, BSE, NYSE, NASDAQ)

- Adjustable indicator parameters for different trading styles

- Suitable for both swing trading and position trading

HOW USERS CAN BENEFIT FROM IT

Portfolio Management

- Quick Portfolio Health Check: Instantly assess the technical status of your entire stock portfolio

- Diversification Analysis: Monitor stocks across different sectors to ensure balanced exposure

- Risk Management: Identify which positions are showing bearish signals for potential exit strategies

- Rebalancing Decisions: Spot strongest performers for potential position increases

Market Screening and Analysis

- Sector Rotation: Compare different sector stocks to identify rotation opportunities

- Relative Strength Analysis: Quickly identify which stocks are outperforming or underperforming

- Market Breadth Assessment: Gauge overall market sentiment by monitoring diverse stock selections

- Trend Confirmation: Validate market trends by observing multiple stock behaviors

Time-Efficient Trading

- Single-Glance Analysis: Get complete technical overview without chart-hopping

- Pre-Market Preparation: Quickly assess overnight changes across multiple positions

- Intraday Monitoring: Track multiple opportunities simultaneously during trading hours

- End-of-Day Review: Efficiently review all watched stocks for next-day planning

Strategic Decision Making

- Entry Point Identification: Spot stocks showing bullish alignment across multiple indicators

- Exit Signal Recognition: Identify positions showing deteriorating technical conditions

- Swing Trading Opportunities: Find stocks with favorable technical setups for swing trades

- Long-term Investment Guidance: Use 200 EMA signals for long-term position decisions

Educational Benefits

- Pattern Recognition: Learn how different indicators behave across various market conditions

- Correlation Analysis: Understand how stocks move relative to each other

- Technical Analysis Learning: Observe multiple indicator interactions in real-time

- Market Sentiment Understanding: Develop better market timing skills through multi-stock observation

Workflow Optimization

- Reduced Chart Clutter: Keep your main chart clean while monitoring multiple stocks

- Faster Analysis: Complete technical analysis of 10 stocks in seconds instead of minutes

- Consistent Methodology: Apply the same technical criteria across all monitored stocks

- Alert Integration: Easy visual identification of stocks requiring immediate attention

This indicator is designed for traders and investors who want to maximize their market awareness while minimizing analysis time. Whether you're managing a portfolio, screening for opportunities, or learning technical analysis, the IU Indicators Dashboard provides the comprehensive overview you need for better trading decisions.

DISCLAIMER :

This indicator is not financial advice, it's for educational purposes only highlighting the power of coding( pine script) in TradingView, I am not a SEBI-registered advisor. Trading and investing involve risk, and you should consult with a qualified financial advisor before making any trading decisions. I do not guarantee profits or take responsibility for any losses you may incur.

Non-Repainting Buy/Sell Oscillator B Dadasaheb//@version=5

indicator("Non-Repainting Buy/Sell Oscillator", overlay=false, max_labels_count=500)

// Inputs

fastLen = input.int(9, "Fast EMA Length", minval=1)

slowLen = input.int(21, "Slow EMA Length", minval=1)

// EMA Calculation

fastEMA = ta.ema(close, fastLen)

slowEMA = ta.ema(close, slowLen)

// Non-Repaint Conditions: Check crossover on previous bar

buySignal = ta.crossover(fastEMA , slowEMA )

sellSignal = ta.crossunder(fastEMA , slowEMA )

// Oscillator value: 1 for buy, -1 for sell

oscValue = fastEMA > slowEMA ? 1 : fastEMA < slowEMA ? -1 : 0

// Colors

oscColor = oscValue > 0 ? color.green : oscValue < 0 ? color.red : color.gray

// Plot Oscillator

plot(oscValue, title="Buy/Sell Oscillator", color=oscColor, linewidth=2, style=plot.style_histogram)

hline(0, "Zero Line", color=color.gray)

hline(1, "Buy Zone", color=color.green, linestyle=hline.style_dotted)

hline(-1, "Sell Zone", color=color.red, linestyle=hline.style_dotted)

// Buy/Sell Labels (non-repainting)

plotshape(buySignal, title="Buy Label", location=location.bottom, style=shape.labelup, text="BUY", color=color.green, textcolor=color.white, size=size.tiny)

plotshape(sellSignal, title="Sell Label", location=location.top, style=shape.labeldown, text="SELL", color=color.red, textcolor=color.white, size=size.tiny)

// Alerts

alertcondition(buySignal, title="Buy Alert", message="BUY: Fast EMA crossed above Slow EMA (confirmed)")

alertcondition(sellSignal, title="Sell Alert", message="SELL: Fast EMA crossed below Slow EMA (confirmed)")

Multi-Timeframe RSIRSI Divergence (Time-Based Engine)

This script is a powerful and highly customizable tool designed to automatically detect and display RSI divergences from up to three independent, user-defined timeframes directly on your chart. It eliminates the need to manually switch between timeframes to find these critical trading signals, allowing you to see long-term and short-term divergences all in one place.

The engine is built to be flexible, supporting both regular (reversal) divergences and hidden (trend-continuation) divergences. It's designed for traders who rely on divergence analysis as a core part of their strategy.

Key Features

Multi-Timeframe (MTF) Analysis: Configure and display divergences from up to three different timeframes simultaneously (e.g., show 4-Hour, Daily, and Weekly divergences on your 1-Hour chart). Each timeframe operates independently with its own settings.

Regular & Hidden Divergence: The script can detect both standard regular divergences that signal potential reversals and hidden divergences that suggest a trend may continue.

Configurable Pivot Strength: You have full control over the sensitivity of pivot detection. The 'Left Strength' and 'Right Strength' settings allow you to define what qualifies as a significant price pivot, filtering out market noise.

Bar Count Filter: Refine your signals by setting the minimum and maximum number of bars allowed between two pivots. This ensures you only see divergences that fit your specific strategic timeframe.

Dedicated Alerts: Each of the three timeframes has its own "Enable Alerts" toggle. When a new divergence line is drawn on the chart for a specific timeframe, a corresponding alert can be triggered, ensuring you never miss a potential setup.

Full Visual Customization: Tailor the look and feel of the indicator to your preference. Each timeframe has unique color settings for its bullish and bearish lines, allowing for easy visual identification. You can also toggle the visibility of various chart markers to keep your view clean.

How to Use

1. Add the indicator to your chart.

2. Open the Settings panel.

3. For each timeframe you wish to use (1, 2, or 3), check the "Enable Timeframe" box.

4. Select the desired Timeframe, RSI Length, and Pivot Strength for each active engine.

5. Adjust the Min/Max Bars filter to match your trading style.

6. If you want to receive notifications, check the "Enable Alerts" box for the desired timeframe(s). Then, create an alert using TradingView's alert manager, selecting the indicator and choosing the "Any alert() function call" option.

Support & Resistance Breakouts with TPThis indicator identifies key support and resistance levels based on recent highs and lows over a customizable lookback period. It visually marks breakout signals when price crosses these levels and optionally displays take profit (TP) points after a set number of bars following a breakout.

Features:

Dynamic calculation of support and resistance with adjustable length

ATR-based buffer zones with gradient fills for clear visualization

Multiple line thickness options for personal preference

Breakout signals indicated by arrows on the chart

Optional TP labels to highlight exit points

Alert conditions for breakout and TP events for automated trading alerts

Pivot Points HL DetailedThis indicator marks important turning points in the market, showing you the most recent swing high and swing low as horizontal lines across the chart. Each pivot line has a price label where it formed and a small counter that updates whenever the market touches that level again. The line’s color reflects the prevailing trend, determined by an EMA filter, so you can quickly see if the level is likely acting as support or resistance in the current market environment.

It works by scanning recent bars for points where price made a local high higher than several bars to its left and right, or a local low lower than several bars to its left and right. These pivots are calculated directly from price action using the ta.pivothigh and ta.pivotlow functions. Once identified, the level is tracked in real time, counting every time price crosses it. The EMA provides context: if price is above the EMA, the market is considered in an uptrend and the pivots are colored to match; if price is below, they’re marked as part of a downtrend.

For traders, this offers a clean way to see where the market has turned before and whether those levels are still relevant. Strong levels often show multiple touches, which can be used for entries, exits, or risk management. The built-in alert system can notify you when price approaches either the most recent swing high or swing low, so you can react quickly.

This tool can be applied in almost any market — forex, stocks, indices, commodities, or crypto — because price tends to respect recent swing points regardless of the asset class. It tends to be most effective in liquid markets, where many traders see and react to the same key levels, and it’s valuable in both trending and ranging conditions, though the EMA trend filter adds extra clarity when the market is moving directionally.

Range Detector- LEMAZZEIt looks like you've shared a Pine Script code for a "Range Detector" indicator. This indicator identifies price ranges on a chart and visually represents them with boxes and lines. Here's a breakdown of what it does:

Key Features:

Range Detection:

Uses a moving average (SMA) and ATR (Average True Range) to define price ranges

A range is identified when price stays within ± (ATR × multiplier) of the SMA for a specified length of bars

Visual Elements:

Draws boxes around the detected ranges

Plots a dotted midline within the range

Changes color when the range is broken (up/down)

User Inputs:

Adjustable minimum range length

Range width multiplier

ATR length for volatility calculation

Color customization for different states (broken upward, broken downward, unbroken)

Dynamic Behavior:

Extends ranges if new price action continues within bounds

Changes color when price breaks out of the range

Can merge adjacent ranges if they overlap

How to Use:

When price consolidates within a range, you'll see a box with a dotted midline

If price breaks above, the box turns green (upward break)

If price breaks below, the box turns red (downward break)

The unbroken range remains blue

This indicator could be useful for identifying consolidation periods and potential breakout opportunities in price action trading. The ATR-based range width makes it adaptive to current market volatility.

Source-indicatorsSource Indicators – A premium TradingView tool combining automated support/resistance levels, dynamic trendlines, and breakout alerts.

Perfect for spotting key market zones and trend shifts in real-time.

Market Clarity Pro Market Clarity Pro — See Key Zones, Trend & Volume Signals

Spot yesterday’s High (Supply) and Low (Demand) instantly — and know exactly where big buyers and sellers are likely waiting.

Red zones = strong selling pressure.

Green zones = strong buying pressure.

Plus, a built-in trend line keeps you trading in the right direction and away from sudden reversals.

You’ll also see:

🔴 Red arrow — not a sell signal, but a sign of heavy sellers stepping in, with volume confirmation and a candle breaking the previous one.

🔵 Blue arrow — not a buy signal, but a sign of strong buyers stepping in, with volume confirmation and a candle breaking the previous one.

These arrows highlight potential volume spikes and breakouts for confirmation only — you still confirm with the higher time frame for more market clarity.

Break above supply. Possible uptrend.

Break below demand. Possible downtrend.

📌 Before using this tool, watch the tutorial video to learn exactly how to apply it and how to spot profitable trades with confidence.

S/R Clouds Overview

The S/R Clouds Indicator is a sophisticated TradingView tool designed to visualize support and resistance levels through dynamic cloud formations. Built on the principles of Keltner Channels, it employs a central moving average enveloped by volatility-based bands to highlight potential price reversal zones. This indicator enhances chart analysis with customizable aesthetics and practical alerts, making it suitable for traders across various strategies and timeframes.

Key Features

Dynamic Bands: Calculates upper and lower bands using a configurable moving average (SMA or EMA) offset by multiples of the average true range (derived from high-low ranges), capturing volatility deviations for precise S/R identification.

Cloud Visualization: Renders semi-transparent clouds between primary and extended bands, providing a clear, layered view of support (lower) and resistance (upper) areas.

Trend Detection: Incorporates a trend state logic based on price position relative to bands and moving average direction, aiding in bullish/bearish market assessments.

Customization Options:

Select from multiple color themes (e.g., Neon, Grayscale) or use custom colors for bands.

Enable glow effects for enhanced visual depth and adjust opacity for chart clarity.

Volatility Insights: Monitors band width to detect squeezes (low volatility) and expansions (high volatility), signaling potential breakouts.

Alerts System: Triggers notifications for price crossings of bands, trend changes, and other key events to support timely decision-making.

How It Works

At its core, the indicator centers on a user-defined period moving average. Volatility is measured via an exponential moving average of the high-low range, multiplied by adjustable factors to form the bands. This setup creates adaptive clouds that expand/contract with market volatility, offering a more responsive alternative to static S/R lines. The result is a clean, professional overlay that integrates seamlessly with other technical tools.

This high-quality indicator prioritizes usability and visual appeal, ensuring traders can focus on analysis without distraction.

Kelly Position Size CalculatorThis position sizing calculator implements the Kelly Criterion, developed by John L. Kelly Jr. at Bell Laboratories in 1956, to determine mathematically optimal position sizes for maximizing long-term wealth growth. Unlike arbitrary position sizing methods, this tool provides a scientifically solution based on your strategy's actual performance statistics and incorporates modern refinements from over six decades of academic research.

The Kelly Criterion addresses a fundamental question in capital allocation: "What fraction of capital should be allocated to each opportunity to maximize growth while avoiding ruin?" This question has profound implications for financial markets, where traders and investors constantly face decisions about optimal capital allocation (Van Tharp, 2007).

Theoretical Foundation

The Kelly Criterion for binary outcomes is expressed as f* = (bp - q) / b, where f* represents the optimal fraction of capital to allocate, b denotes the risk-reward ratio, p indicates the probability of success, and q represents the probability of loss (Kelly, 1956). This formula maximizes the expected logarithm of wealth, ensuring maximum long-term growth rate while avoiding the risk of ruin.

The mathematical elegance of Kelly's approach lies in its derivation from information theory. Kelly's original work was motivated by Claude Shannon's information theory (Shannon, 1948), recognizing that maximizing the logarithm of wealth is equivalent to maximizing the rate of information transmission. This connection between information theory and wealth accumulation provides a deep theoretical foundation for optimal position sizing.

The logarithmic utility function underlying the Kelly Criterion naturally embodies several desirable properties for capital management. It exhibits decreasing marginal utility, penalizes large losses more severely than it rewards equivalent gains, and focuses on geometric rather than arithmetic mean returns, which is appropriate for compounding scenarios (Thorp, 2006).

Scientific Implementation

This calculator extends beyond basic Kelly implementation by incorporating state of the art refinements from academic research:

Parameter Uncertainty Adjustment: Following Michaud (1989), the implementation applies Bayesian shrinkage to account for parameter estimation error inherent in small sample sizes. The adjustment formula f_adjusted = f_kelly × confidence_factor + f_conservative × (1 - confidence_factor) addresses the overconfidence bias documented by Baker and McHale (2012), where the confidence factor increases with sample size and the conservative estimate equals 0.25 (quarter Kelly).

Sample Size Confidence: The reliability of Kelly calculations depends critically on sample size. Research by Browne and Whitt (1996) provides theoretical guidance on minimum sample requirements, suggesting that at least 30 independent observations are necessary for meaningful parameter estimates, with 100 or more trades providing reliable estimates for most trading strategies.

Universal Asset Compatibility: The calculator employs intelligent asset detection using TradingView's built-in symbol information, automatically adapting calculations for different asset classes without manual configuration.

ASSET SPECIFIC IMPLEMENTATION

Equity Markets: For stocks and ETFs, position sizing follows the calculation Shares = floor(Kelly Fraction × Account Size / Share Price). This straightforward approach reflects whole share constraints while accommodating fractional share trading capabilities.

Foreign Exchange Markets: Forex markets require lot-based calculations following Lot Size = Kelly Fraction × Account Size / (100,000 × Base Currency Value). The calculator automatically handles major currency pairs with appropriate pip value calculations, following industry standards described by Archer (2010).

Futures Markets: Futures position sizing accounts for leverage and margin requirements through Contracts = floor(Kelly Fraction × Account Size / Margin Requirement). The calculator estimates margin requirements as a percentage of contract notional value, with specific adjustments for micro-futures contracts that have smaller sizes and reduced margin requirements (Kaufman, 2013).

Index and Commodity Markets: These markets combine characteristics of both equity and futures markets. The calculator automatically detects whether instruments are cash-settled or futures-based, applying appropriate sizing methodologies with correct point value calculations.

Risk Management Integration

The calculator integrates sophisticated risk assessment through two primary modes:

Stop Loss Integration: When fixed stop-loss levels are defined, risk calculation follows Risk per Trade = Position Size × Stop Loss Distance. This ensures that the Kelly fraction accounts for actual risk exposure rather than theoretical maximum loss, with stop-loss distance measured in appropriate units for each asset class.

Strategy Drawdown Assessment: For discretionary exit strategies, risk estimation uses maximum historical drawdown through Risk per Trade = Position Value × (Maximum Drawdown / 100). This approach assumes that individual trade losses will not exceed the strategy's historical maximum drawdown, providing a reasonable estimate for strategies with well-defined risk characteristics.

Fractional Kelly Approaches

Pure Kelly sizing can produce substantial volatility, leading many practitioners to adopt fractional Kelly approaches. MacLean, Sanegre, Zhao, and Ziemba (2004) analyze the trade-offs between growth rate and volatility, demonstrating that half-Kelly typically reduces volatility by approximately 75% while sacrificing only 25% of the growth rate.

The calculator provides three primary Kelly modes to accommodate different risk preferences and experience levels. Full Kelly maximizes growth rate while accepting higher volatility, making it suitable for experienced practitioners with strong risk tolerance and robust capital bases. Half Kelly offers a balanced approach popular among professional traders, providing optimal risk-return balance by reducing volatility significantly while maintaining substantial growth potential. Quarter Kelly implements a conservative approach with low volatility, recommended for risk-averse traders or those new to Kelly methodology who prefer gradual introduction to optimal position sizing principles.

Empirical Validation and Performance

Extensive academic research supports the theoretical advantages of Kelly sizing. Hakansson and Ziemba (1995) provide a comprehensive review of Kelly applications in finance, documenting superior long-term performance across various market conditions and asset classes. Estrada (2008) analyzes Kelly performance in international equity markets, finding that Kelly-based strategies consistently outperform fixed position sizing approaches over extended periods across 19 developed markets over a 30-year period.

Several prominent investment firms have successfully implemented Kelly-based position sizing. Pabrai (2007) documents the application of Kelly principles at Berkshire Hathaway, noting Warren Buffett's concentrated portfolio approach aligns closely with Kelly optimal sizing for high-conviction investments. Quantitative hedge funds, including Renaissance Technologies and AQR, have incorporated Kelly-based risk management into their systematic trading strategies.

Practical Implementation Guidelines

Successful Kelly implementation requires systematic application with attention to several critical factors:

Parameter Estimation: Accurate parameter estimation represents the greatest challenge in practical Kelly implementation. Brown (1976) notes that small errors in probability estimates can lead to significant deviations from optimal performance. The calculator addresses this through Bayesian adjustments and confidence measures.

Sample Size Requirements: Users should begin with conservative fractional Kelly approaches until achieving sufficient historical data. Strategies with fewer than 30 trades may produce unreliable Kelly estimates, regardless of adjustments. Full confidence typically requires 100 or more independent trade observations.

Market Regime Considerations: Parameters that accurately describe historical performance may not reflect future market conditions. Ziemba (2003) recommends regular parameter updates and conservative adjustments when market conditions change significantly.

Professional Features and Customization

The calculator provides comprehensive customization options for professional applications:

Multiple Color Schemes: Eight professional color themes (Gold, EdgeTools, Behavioral, Quant, Ocean, Fire, Matrix, Arctic) with dark and light theme compatibility ensure optimal visibility across different trading environments.

Flexible Display Options: Adjustable table size and position accommodate various chart layouts and user preferences, while maintaining analytical depth and clarity.

Comprehensive Results: The results table presents essential information including asset specifications, strategy statistics, Kelly calculations, sample confidence measures, position values, risk assessments, and final position sizes in appropriate units for each asset class.

Limitations and Considerations

Like any analytical tool, the Kelly Criterion has important limitations that users must understand:

Stationarity Assumption: The Kelly Criterion assumes that historical strategy statistics represent future performance characteristics. Non-stationary market conditions may invalidate this assumption, as noted by Lo and MacKinlay (1999).

Independence Requirement: Each trade should be independent to avoid correlation effects. Many trading strategies exhibit serial correlation in returns, which can affect optimal position sizing and may require adjustments for portfolio applications.

Parameter Sensitivity: Kelly calculations are sensitive to parameter accuracy. Regular calibration and conservative approaches are essential when parameter uncertainty is high.

Transaction Costs: The implementation incorporates user-defined transaction costs but assumes these remain constant across different position sizes and market conditions, following Ziemba (2003).

Advanced Applications and Extensions

Multi-Asset Portfolio Considerations: While this calculator optimizes individual position sizes, portfolio-level applications require additional considerations for correlation effects and aggregate risk management. Simplified portfolio approaches include treating positions independently with correlation adjustments.

Behavioral Factors: Behavioral finance research reveals systematic biases that can interfere with Kelly implementation. Kahneman and Tversky (1979) document loss aversion, overconfidence, and other cognitive biases that lead traders to deviate from optimal strategies. Successful implementation requires disciplined adherence to calculated recommendations.

Time-Varying Parameters: Advanced implementations may incorporate time-varying parameter models that adjust Kelly recommendations based on changing market conditions, though these require sophisticated econometric techniques and substantial computational resources.

Comprehensive Usage Instructions and Practical Examples

Implementation begins with loading the calculator on your desired trading instrument's chart. The system automatically detects asset type across stocks, forex, futures, and cryptocurrency markets while extracting current price information. Navigation to the indicator settings allows input of your specific strategy parameters.

Strategy statistics configuration requires careful attention to several key metrics. The win rate should be calculated from your backtest results using the formula of winning trades divided by total trades multiplied by 100. Average win represents the sum of all profitable trades divided by the number of winning trades, while average loss calculates the sum of all losing trades divided by the number of losing trades, entered as a positive number. The total historical trades parameter requires the complete number of trades in your backtest, with a minimum of 30 trades recommended for basic functionality and 100 or more trades optimal for statistical reliability. Account size should reflect your available trading capital, specifically the risk capital allocated for trading rather than total net worth.

Risk management configuration adapts to your specific trading approach. The stop loss setting should be enabled if you employ fixed stop-loss exits, with the stop loss distance specified in appropriate units depending on the asset class. For stocks, this distance is measured in dollars, for forex in pips, and for futures in ticks. When stop losses are not used, the maximum strategy drawdown percentage from your backtest provides the risk assessment baseline. Kelly mode selection offers three primary approaches: Full Kelly for aggressive growth with higher volatility suitable for experienced practitioners, Half Kelly for balanced risk-return optimization popular among professional traders, and Quarter Kelly for conservative approaches with reduced volatility.

Display customization ensures optimal integration with your trading environment. Eight professional color themes provide optimization for different chart backgrounds and personal preferences. Table position selection allows optimal placement within your chart layout, while table size adjustment ensures readability across different screen resolutions and viewing preferences.

Detailed Practical Examples

Example 1: SPY Swing Trading Strategy

Consider a professionally developed swing trading strategy for SPY (S&P 500 ETF) with backtesting results spanning 166 total trades. The strategy achieved 110 winning trades, representing a 66.3% win rate, with an average winning trade of $2,200 and average losing trade of $862. The maximum drawdown reached 31.4% during the testing period, and the available trading capital amounts to $25,000. This strategy employs discretionary exits without fixed stop losses.

Implementation requires loading the calculator on the SPY daily chart and configuring the parameters accordingly. The win rate input receives 66.3, while average win and loss inputs receive 2200 and 862 respectively. Total historical trades input requires 166, with account size set to 25000. The stop loss function remains disabled due to the discretionary exit approach, with maximum strategy drawdown set to 31.4%. Half Kelly mode provides the optimal balance between growth and risk management for this application.

The calculator generates several key outputs for this scenario. The risk-reward ratio calculates automatically to 2.55, while the Kelly fraction reaches approximately 53% before scientific adjustments. Sample confidence achieves 100% given the 166 trades providing high statistical confidence. The recommended position settles at approximately 27% after Half Kelly and Bayesian adjustment factors. Position value reaches approximately $6,750, translating to 16 shares at a $420 SPY price. Risk per trade amounts to approximately $2,110, representing 31.4% of position value, with expected value per trade reaching approximately $1,466. This recommendation represents the mathematically optimal balance between growth potential and risk management for this specific strategy profile.

Example 2: EURUSD Day Trading with Stop Losses

A high-frequency EURUSD day trading strategy demonstrates different parameter requirements compared to swing trading approaches. This strategy encompasses 89 total trades with a 58% win rate, generating an average winning trade of $180 and average losing trade of $95. The maximum drawdown reached 12% during testing, with available capital of $10,000. The strategy employs fixed stop losses at 25 pips and take profit targets at 45 pips, providing clear risk-reward parameters.

Implementation begins with loading the calculator on the EURUSD 1-hour chart for appropriate timeframe alignment. Parameter configuration includes win rate at 58, average win at 180, and average loss at 95. Total historical trades input receives 89, with account size set to 10000. The stop loss function is enabled with distance set to 25 pips, reflecting the fixed exit strategy. Quarter Kelly mode provides conservative positioning due to the smaller sample size compared to the previous example.

Results demonstrate the impact of smaller sample sizes on Kelly calculations. The risk-reward ratio calculates to 1.89, while the Kelly fraction reaches approximately 32% before adjustments. Sample confidence achieves 89%, providing moderate statistical confidence given the 89 trades. The recommended position settles at approximately 7% after Quarter Kelly application and Bayesian shrinkage adjustment for the smaller sample. Position value amounts to approximately $700, translating to 0.07 standard lots. Risk per trade reaches approximately $175, calculated as 25 pips multiplied by lot size and pip value, with expected value per trade at approximately $49. This conservative position sizing reflects the smaller sample size, with position sizes expected to increase as trade count surpasses 100 and statistical confidence improves.

Example 3: ES1! Futures Systematic Strategy

Systematic futures trading presents unique considerations for Kelly criterion application, as demonstrated by an E-mini S&P 500 futures strategy encompassing 234 total trades. This systematic approach achieved a 45% win rate with an average winning trade of $1,850 and average losing trade of $720. The maximum drawdown reached 18% during the testing period, with available capital of $50,000. The strategy employs 15-tick stop losses with contract specifications of $50 per tick, providing precise risk control mechanisms.

Implementation involves loading the calculator on the ES1! 15-minute chart to align with the systematic trading timeframe. Parameter configuration includes win rate at 45, average win at 1850, and average loss at 720. Total historical trades receives 234, providing robust statistical foundation, with account size set to 50000. The stop loss function is enabled with distance set to 15 ticks, reflecting the systematic exit methodology. Half Kelly mode balances growth potential with appropriate risk management for futures trading.

Results illustrate how favorable risk-reward ratios can support meaningful position sizing despite lower win rates. The risk-reward ratio calculates to 2.57, while the Kelly fraction reaches approximately 16%, lower than previous examples due to the sub-50% win rate. Sample confidence achieves 100% given the 234 trades providing high statistical confidence. The recommended position settles at approximately 8% after Half Kelly adjustment. Estimated margin per contract amounts to approximately $2,500, resulting in a single contract allocation. Position value reaches approximately $2,500, with risk per trade at $750, calculated as 15 ticks multiplied by $50 per tick. Expected value per trade amounts to approximately $508. Despite the lower win rate, the favorable risk-reward ratio supports meaningful position sizing, with single contract allocation reflecting appropriate leverage management for futures trading.

Example 4: MES1! Micro-Futures for Smaller Accounts

Micro-futures contracts provide enhanced accessibility for smaller trading accounts while maintaining identical strategy characteristics. Using the same systematic strategy statistics from the previous example but with available capital of $15,000 and micro-futures specifications of $5 per tick with reduced margin requirements, the implementation demonstrates improved position sizing granularity.

Kelly calculations remain identical to the full-sized contract example, maintaining the same risk-reward dynamics and statistical foundations. However, estimated margin per contract reduces to approximately $250 for micro-contracts, enabling allocation of 4-5 micro-contracts. Position value reaches approximately $1,200, while risk per trade calculates to $75, derived from 15 ticks multiplied by $5 per tick. This granularity advantage provides better position size precision for smaller accounts, enabling more accurate Kelly implementation without requiring large capital commitments.

Example 5: Bitcoin Swing Trading

Cryptocurrency markets present unique challenges requiring modified Kelly application approaches. A Bitcoin swing trading strategy on BTCUSD encompasses 67 total trades with a 71% win rate, generating average winning trades of $3,200 and average losing trades of $1,400. Maximum drawdown reached 28% during testing, with available capital of $30,000. The strategy employs technical analysis for exits without fixed stop losses, relying on price action and momentum indicators.

Implementation requires conservative approaches due to cryptocurrency volatility characteristics. Quarter Kelly mode is recommended despite the high win rate to account for crypto market unpredictability. Expected position sizing remains reduced due to the limited sample size of 67 trades, requiring additional caution until statistical confidence improves. Regular parameter updates are strongly recommended due to cryptocurrency market evolution and changing volatility patterns that can significantly impact strategy performance characteristics.

Advanced Usage Scenarios

Portfolio position sizing requires sophisticated consideration when running multiple strategies simultaneously. Each strategy should have its Kelly fraction calculated independently to maintain mathematical integrity. However, correlation adjustments become necessary when strategies exhibit related performance patterns. Moderately correlated strategies should receive individual position size reductions of 10-20% to account for overlapping risk exposure. Aggregate portfolio risk monitoring ensures total exposure remains within acceptable limits across all active strategies. Professional practitioners often consider using lower fractional Kelly approaches, such as Quarter Kelly, when running multiple strategies simultaneously to provide additional safety margins.

Parameter sensitivity analysis forms a critical component of professional Kelly implementation. Regular validation procedures should include monthly parameter updates using rolling 100-trade windows to capture evolving market conditions while maintaining statistical relevance. Sensitivity testing involves varying win rates by ±5% and average win/loss ratios by ±10% to assess recommendation stability under different parameter assumptions. Out-of-sample validation reserves 20% of historical data for parameter verification, ensuring that optimization doesn't create curve-fitted results. Regime change detection monitors actual performance against expected metrics, triggering parameter reassessment when significant deviations occur.

Risk management integration requires professional overlay considerations beyond pure Kelly calculations. Daily loss limits should cease trading when daily losses exceed twice the calculated risk per trade, preventing emotional decision-making during adverse periods. Maximum position limits should never exceed 25% of account value in any single position regardless of Kelly recommendations, maintaining diversification principles. Correlation monitoring reduces position sizes when holding multiple correlated positions that move together during market stress. Volatility adjustments consider reducing position sizes during periods of elevated VIX above 25 for equity strategies, adapting to changing market conditions.

Troubleshooting and Optimization

Professional implementation often encounters specific challenges requiring systematic troubleshooting approaches. Zero position size displays typically result from insufficient capital for minimum position sizes, negative expected values, or extremely conservative Kelly calculations. Solutions include increasing account size, verifying strategy statistics for accuracy, considering Quarter Kelly mode for conservative approaches, or reassessing overall strategy viability when fundamental issues exist.

Extremely high Kelly fractions exceeding 50% usually indicate underlying problems with parameter estimation. Common causes include unrealistic win rates, inflated risk-reward ratios, or curve-fitted backtest results that don't reflect genuine trading conditions. Solutions require verifying backtest methodology, including all transaction costs in calculations, testing strategies on out-of-sample data, and using conservative fractional Kelly approaches until parameter reliability improves.

Low sample confidence below 50% reflects insufficient historical trades for reliable parameter estimation. This situation demands gathering additional trading data, using Quarter Kelly approaches until reaching 100 or more trades, applying extra conservatism in position sizing, and considering paper trading to build statistical foundations without capital risk.

Inconsistent results across similar strategies often stem from parameter estimation differences, market regime changes, or strategy degradation over time. Professional solutions include standardizing backtest methodology across all strategies, updating parameters regularly to reflect current conditions, and monitoring live performance against expectations to identify deteriorating strategies.

Position sizes that appear inappropriately large or small require careful validation against traditional risk management principles. Professional standards recommend never risking more than 2-3% per trade regardless of Kelly calculations. Calibration should begin with Quarter Kelly approaches, gradually increasing as comfort and confidence develop. Most institutional traders utilize 25-50% of full Kelly recommendations to balance growth with prudent risk management.

Market condition adjustments require dynamic approaches to Kelly implementation. Trending markets may support full Kelly recommendations when directional momentum provides favorable conditions. Ranging or volatile markets typically warrant reducing to Half or Quarter Kelly to account for increased uncertainty. High correlation periods demand reducing individual position sizes when multiple positions move together, concentrating risk exposure. News and event periods often justify temporary position size reductions during high-impact releases that can create unpredictable market movements.

Performance monitoring requires systematic protocols to ensure Kelly implementation remains effective over time. Weekly reviews should compare actual versus expected win rates and average win/loss ratios to identify parameter drift or strategy degradation. Position size efficiency and execution quality monitoring ensures that calculated recommendations translate effectively into actual trading results. Tracking correlation between calculated and realized risk helps identify discrepancies between theoretical and practical risk exposure.

Monthly calibration provides more comprehensive parameter assessment using the most recent 100 trades to maintain statistical relevance while capturing current market conditions. Kelly mode appropriateness requires reassessment based on recent market volatility and performance characteristics, potentially shifting between Full, Half, and Quarter Kelly approaches as conditions change. Transaction cost evaluation ensures that commission structures, spreads, and slippage estimates remain accurate and current.

Quarterly strategic reviews encompass comprehensive strategy performance analysis comparing long-term results against expectations and identifying trends in effectiveness. Market regime assessment evaluates parameter stability across different market conditions, determining whether strategy characteristics remain consistent or require fundamental adjustments. Strategic modifications to position sizing methodology may become necessary as markets evolve or trading approaches mature, ensuring that Kelly implementation continues supporting optimal capital allocation objectives.

Professional Applications

This calculator serves diverse professional applications across the financial industry. Quantitative hedge funds utilize the implementation for systematic position sizing within algorithmic trading frameworks, where mathematical precision and consistent application prove essential for institutional capital management. Professional discretionary traders benefit from optimized position management that removes emotional bias while maintaining flexibility for market-specific adjustments. Portfolio managers employ the calculator for developing risk-adjusted allocation strategies that enhance returns while maintaining prudent risk controls across diverse asset classes and investment strategies.

Individual traders seeking mathematical optimization of capital allocation find the calculator provides institutional-grade methodology previously available only to professional money managers. The Kelly Criterion establishes theoretical foundation for optimal capital allocation across both single strategies and multiple trading systems, offering significant advantages over arbitrary position sizing methods that rely on intuition or fixed percentage approaches. Professional implementation ensures consistent application of mathematically sound principles while adapting to changing market conditions and strategy performance characteristics.

Conclusion

The Kelly Criterion represents one of the few mathematically optimal solutions to fundamental investment problems. When properly understood and carefully implemented, it provides significant competitive advantage in financial markets. This calculator implements modern refinements to Kelly's original formula while maintaining accessibility for practical trading applications.

Success with Kelly requires ongoing learning, systematic application, and continuous refinement based on market feedback and evolving research. Users who master Kelly principles and implement them systematically can expect superior risk-adjusted returns and more consistent capital growth over extended periods.

The extensive academic literature provides rich resources for deeper study, while practical experience builds the intuition necessary for effective implementation. Regular parameter updates, conservative approaches with limited data, and disciplined adherence to calculated recommendations are essential for optimal results.

References

Archer, M. D. (2010). Getting Started in Currency Trading: Winning in Today's Forex Market (3rd ed.). John Wiley & Sons.

Baker, R. D., & McHale, I. G. (2012). An empirical Bayes approach to optimising betting strategies. Journal of the Royal Statistical Society: Series D (The Statistician), 61(1), 75-92.

Breiman, L. (1961). Optimal gambling systems for favorable games. In J. Neyman (Ed.), Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability (pp. 65-78). University of California Press.

Brown, D. B. (1976). Optimal portfolio growth: Logarithmic utility and the Kelly criterion. In W. T. Ziemba & R. G. Vickson (Eds.), Stochastic Optimization Models in Finance (pp. 1-23). Academic Press.

Browne, S., & Whitt, W. (1996). Portfolio choice and the Bayesian Kelly criterion. Advances in Applied Probability, 28(4), 1145-1176.

Estrada, J. (2008). Geometric mean maximization: An overlooked portfolio approach? The Journal of Investing, 17(4), 134-147.