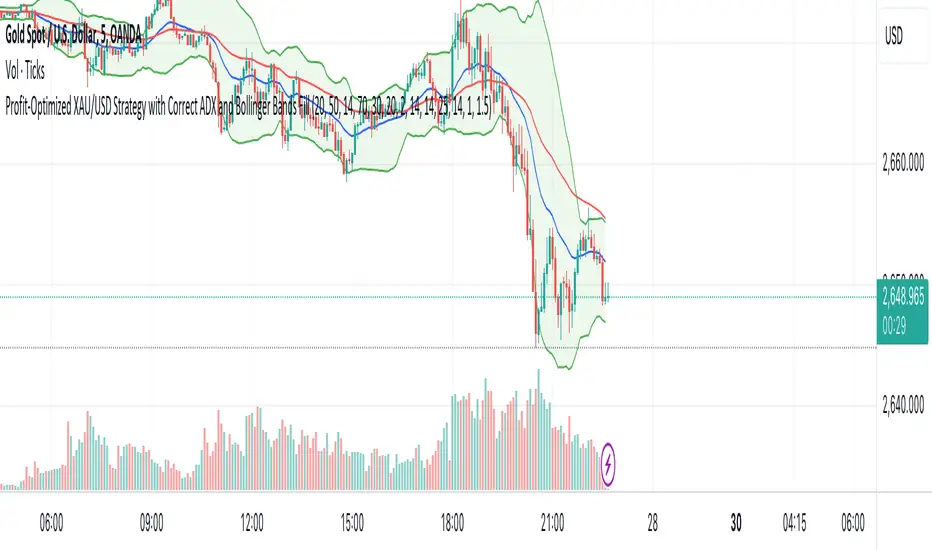

XAU/USD Strategy with Correct ADX and Bollinger Bands Fill1. *Indicators Used*:

- *Exponential Moving Averages (EMAs)*: Two EMAs (20-period and 50-period) are used to identify the trend direction and potential entry points based on crossovers.

- *Relative Strength Index (RSI)*: A momentum oscillator that measures the speed and change of price movements. It identifies overbought and oversold conditions.

- *Bollinger Bands*: These consist of a middle line (simple moving average) and two outer bands (standard deviations away from the middle). They help to identify price volatility and potential reversal points.

- *Average Directional Index (ADX)*: This indicator quantifies trend strength. It's derived from the Directional Movement Index (DMI) and helps confirm the presence of a strong trend.

- *Average True Range (ATR)*: Used to calculate position size based on volatility, ensuring that trades align with the trader's risk tolerance.

2. *Entry Conditions*:

- *Long Entry*:

- The 20 EMA crosses above the 50 EMA (indicating a potential bullish trend).

- The RSI is below the oversold level (30), suggesting the asset may be undervalued.

- The price is below the lower Bollinger Band, indicating potential price reversal.

- The ADX is above a specified threshold (25), confirming that there is sufficient trend strength.

- *Short Entry*:

- The 20 EMA crosses below the 50 EMA (indicating a potential bearish trend).

- The RSI is above the overbought level (70), suggesting the asset may be overvalued.

- The price is above the upper Bollinger Band, indicating potential price reversal.

- The ADX is above the specified threshold (25), confirming trend strength.

3. *Position Sizing*:

- The script calculates the position size dynamically based on the trader's risk per trade (expressed as a percentage of the total capital) and the ATR. This ensures that the trader does not risk more than the specified percentage on any single trade, adjusting the position size according to market volatility.

4. *Exit Conditions*:

- The strategy uses a trailing stop-loss mechanism to secure profits as the price moves in the trader's favor. The trailing stop is set at a percentage (1.5% by default) below the highest price reached since entry for long positions and above the lowest price for short positions.

- Additionally, if the RSI crosses back above the overbought level while in a long position or below the oversold level while in a short position, the position is closed to prevent losses.

5. *Alerts*:

- Alerts are set to notify the trader when a buy or sell condition is met based on the strategy's rules. This allows for timely execution of trades.

### Summary

This strategy aims to capture significant price movements in the XAU/USD market by combining trend-following (EMAs, ADX) and momentum indicators (RSI, Bollinger Bands). The dynamic position sizing based on ATR helps manage risk effectively. By implementing trailing stops and alert mechanisms, the strategy enhances the trader's ability to act quickly on opportunities while mitigating potential losses.

Pesquisar nos scripts por "汇丰股票25"

Larry Conners Vix Reversal II Strategy (approx.)This Pine Script™ strategy is a modified version of the original Larry Connors VIX Reversal II Strategy, designed for short-term trading in market indices like the S&P 500. The strategy utilizes the Relative Strength Index (RSI) of the VIX (Volatility Index) to identify potential overbought or oversold market conditions. The logic is based on the assumption that extreme levels of market volatility often precede reversals in price.

How the Strategy Works

The strategy calculates the RSI of the VIX using a 25-period lookback window. The RSI is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is often used to identify overbought and oversold conditions in assets.

Overbought Signal: When the RSI of the VIX rises above 61, it signals a potential overbought condition in the market. The strategy looks for a RSI downtick (i.e., when RSI starts to fall after reaching this level) as a trigger to enter a long position.

Oversold Signal: Conversely, when the RSI of the VIX drops below 42, the market is considered oversold. A RSI uptick (i.e., when RSI starts to rise after hitting this level) serves as a signal to enter a short position.

The strategy holds the position for a minimum of 7 days and a maximum of 12 days, after which it exits automatically.

Larry Connors: Background

Larry Connors is a prominent figure in quantitative trading, specializing in short-term market strategies. He is the co-author of several influential books on trading, such as Street Smarts (1995), co-written with Linda Raschke, and How Markets Really Work. Connors' work focuses on developing rules-based systems using volatility indicators like the VIX and oscillators such as RSI to exploit mean-reversion patterns in financial markets.

Risks of the Strategy

While the Larry Connors VIX Reversal II Strategy can capture reversals in volatile market environments, it also carries significant risks:

Over-Optimization: This modified version adjusts RSI levels and holding periods to fit recent market data. If market conditions change, the strategy might no longer be effective, leading to false signals.

Drawdowns in Trending Markets: This is a mean-reversion strategy, designed to profit when markets return to a previous mean. However, in strongly trending markets, especially during extended bull or bear phases, the strategy might generate losses due to early entries or exits.

Volatility Risk: Since this strategy is linked to the VIX, an instrument that reflects market volatility, large spikes in volatility can lead to unexpected, fast-moving market conditions, potentially leading to larger-than-expected losses.

Scientific Literature and Supporting Research

The use of RSI and VIX in trading strategies has been widely discussed in academic research. RSI is one of the most studied momentum oscillators, and numerous studies show that it can capture mean-reversion effects in various markets, including equities and derivatives.

Wong et al. (2003) investigated the effectiveness of technical trading rules such as RSI, finding that it has predictive power in certain market conditions, particularly in mean-reverting markets .

The VIX, often referred to as the “fear index,” reflects market expectations of volatility and has been a focal point in research exploring volatility-based strategies. Whaley (2000) extensively reviewed the predictive power of VIX, noting that extreme VIX readings often correlate with turning points in the stock market .

Modified Version of Original Strategy

This script is a modified version of Larry Connors' original VIX Reversal II strategy. The key differences include:

Adjusted RSI period to 25 (instead of 2 or 4 commonly used in Connors’ other work).

Overbought and oversold levels modified to 61 and 42, respectively.

Specific holding period (7 to 12 days) is predefined to reduce holding risk.

These modifications aim to adapt the strategy to different market environments, potentially enhancing performance under specific volatility conditions. However, as with any system, constant evaluation and testing in live markets are crucial.

References

Wong, W. K., Manzur, M., & Chew, B. K. (2003). How rewarding is technical analysis? Evidence from Singapore stock market. Applied Financial Economics, 13(7), 543-551.

Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

Volume Analysis - Heatmap and Volume ProfileHello All!

I have a new toy for you! Volume Analysis - Heatmap and Volume Profile . Honestly I started to work to develop Volume Heatmap then I decided to improve it and add more features such Volume profile, volume, difference in Buy/Sell volumes etc. I tried to put my abilities into this script and tried to use some new Pine Language™ features ( method, force_overlay, enum etc features ). I hope the usage of these new features would be an example for Pine Programmers.

Lets talk about how it works:

- It gets number of Rows/Columns from the user for each candle to create heatmap

- It calculates the number of the candles to analyze. Number of the candles may change by number of Rows/columns or if any volume / difference in volumes / volume profile is enabled

- It gets Closing/Opening price, Volume and Time info from lower time frame for each candle ( it can be up to 100K for each candle )

- After getting the data it calculates lower time frame to analyze

- Then it calculates how closing price moves, how much volume on each move and create boxes by the volume/move in each box

- The colors for each box calculated by volume info and closing price movements in the lower time frame

- It shows the boxes on Absolute places or Zero Line optionally

- it shows Volume, Cumulative volume, Difference between Buy/Sell volume for each column

- it changes empty box color by Chart background color, also you can change transparency

- At this time it creates Volume Profile with up to 25 rows

- As a new Pine Language™ feature, it can show Volume Profile in the indicator window or in Main chart, shows Value Area, Value Area High (VAH), Value Area Low (VAL), and draw it and POC (Point Of Control) in the indicator window and/or in the main chart

- Honestly the feature I like is that: For the markets that are not open 24/7, it combines the data from the lower time period without any gaps. For example, if you work for a market that is closed on Saturdays and Sundays, it ensures data integrity by omitting weekends and holidays. so for example if the data is like "ABC---DEF-X---YL-Z" then it makes this data like "ABCDEFXYLZ". In this way, there will be no data breaks in the displayed boxes, there will be no empty colons, and it will appear as if data is coming in at any time.

- Finally it shows Info Panel to give info, its background color automatically changes by the Chart background color

- Important! You should set your "Plan" accordingly, your plan is "Premium or Higher" or "Lower tier". so the script can understand the minimum time frame it can get data!!

I tried to share many screenshots below to explain it much better

How it looks?

it shows Highest Buy/Sell volumes brighter, move volume -> brighter

Volume Profile ( up to 25 row s) ( number of contained candles should be more than 1 )

Volume Profile can be shown in the main chart optionally

How the main chart looks:

Closing price shown and you can enable it, change colors & line width

Can include many candles according to Row&Column number you set

Optionally it can show cumulative volume for each candle

Closing prices from lower time frame

Shows Candle Body by changing background colors

It can shows all included candles on Zero line

You can change the colors of many things

You can set Empty box and border transparency

Table, Empty box Colors adjustment done automatically by chart background color

Sometimes we can not get data from some historical candles if time frame is high such 2days, 1 week etc, and it looks like:

It also checks if Chart time frame and Chart type is suitable

Enjoy!

Artaking 2Components of the Indicator:

Moving Averages:

Short-Term Moving Average (MA): This is a 50-period Simple Moving Average (SMA) applied to the closing price. It is used to track the short-term trend of the market.

Long-Term Moving Average (MA): This is a 200-period SMA used to track the long-term trend.

Day Trading Moving Average: A 20-period SMA is used specifically for day trading signals, focusing on shorter-term price movements.

Purpose:

The crossing of these moving averages (short-term crossing above or below long-term) provides basic buy and sell signals, indicative of potential trend reversals or continuations.

ADX (Average Directional Index) for Trend Strength:

ADX Calculation: The ADX is calculated using a 14-period length with 14-period smoothing. The ADX value indicates the strength of a trend, regardless of direction.

Strong Trend Condition: The indicator considers a trend to be strong if the ADX value is above 25. This threshold helps filter out trades during weak or sideways markets.

Purpose:

To ensure that the strategy only generates signals when there is a strong trend, thus avoiding whipsaws in low volatility or range-bound conditions.

Support Levels:

Support Level Calculation: The indicator calculates the lowest close over the last 100 periods. This level is used to identify significant support zones where the price might find a floor.

Purpose:

Support levels are critical in identifying potential areas where the price might bounce, making them ideal for setting stop losses or identifying buy opportunities.

Volatility Spike (Proxy for News Trading):

ATR (Average True Range) Calculation: The indicator uses a 14-period ATR to measure market volatility. A volatility spike is identified when the ATR is greater than 1.5 times the 14-period SMA of the ATR.

Purpose:

This serves as a proxy for news events or other sudden market movements that could make the market unpredictable. The indicator avoids generating signals during these periods to reduce the risk of being caught in a volatile, potentially news-driven move.

Fibonacci Retracement Levels:

61.8% Fibonacci Level: Calculated from the highest high and lowest low over the long MA period, this retracement level is widely regarded as a significant support or resistance level.

Purpose:

Position traders often use Fibonacci levels to identify potential reversal points. The indicator incorporates the 61.8% level to fine-tune entries and exits.

Candlestick Patterns for Price Action Trading:

Bullish Engulfing Pattern: A bullish reversal pattern where a green candle fully engulfs the previous red candle.

Bearish Engulfing Pattern: A bearish reversal pattern where a red candle fully engulfs the previous green candle.

Purpose:

These patterns are classic signals used in price action trading to identify potential reversals at key levels, especially when they align with other conditions like support/resistance or Fibonacci levels.

Signal Generation:

The indicator generates buy and sell signals by combining the above elements:

Buy Signal:

A buy signal is triggered when:

The short-term MA crosses above the long-term MA (indicating a potential uptrend).

The trend is strong (ADX > 25).

The current price is near or below the 61.8% Fibonacci retracement level, suggesting a potential reversal.

No significant volatility spike is detected, ensuring the market isn’t reacting unpredictably to news.

Sell Signal:

A sell signal is triggered when:

The short-term MA crosses below the long-term MA (indicating a potential downtrend).

The trend is strong (ADX > 25).

The current price is near or above the 61.8% Fibonacci retracement level, suggesting potential resistance.

No significant volatility spike is detected.

Day Trading Signals:

Independent of the main trend signals, the indicator also generates intraday buy and sell signals when the price crosses above or below the 20-period day trading MA.

Price Action Signals:

The indicator can trigger buy or sell signals based purely on price action, such as the occurrence of bullish or bearish engulfing patterns. This is optional and can be enabled or disabled.

Alerts:

The indicator includes built-in alert conditions that notify the trader when a buy or sell signal is generated. This allows traders to act immediately without having to constantly monitor the charts.

Practical Application:

This indicator is versatile and can be used across various trading styles:

Position Trading: The long-term MA, Fibonacci retracement, and ADX provide a solid foundation for identifying long-term trends and potential entry/exit points.

Day Trading: The short-term MA and day trading MA offer quick signals for intraday trading.

Price Action: Candlestick pattern recognition allows for precise entry points based on market sentiment and behavior.

News Trading: The volatility spike filter helps avoid trading during periods of market instability, often driven by news events.

Conclusion:

The Comprehensive Trading Strategy Indicator is a robust tool designed to help traders navigate various market conditions by integrating multiple strategies into a single, coherent framework. It provides clear, actionable signals while filtering out potentially dangerous trades during volatile or weak market conditions. Whether you're a long-term trader, a day trader, or someone who relies on price action, this indicator can be a valuable addition to your trading toolkit.

whookLibrary "whook"

This library provides functions for generating trading alerts for `whook`

check this -> github.com

Currently supported exchanges:

Kucoin futures

Bitget futures

Coinex futures

Bingx

OKX futures ( also its demo mode )

Bybit futures ( also Bybit testnet )

Binance futures ( also Binance futures testnet )

Phemex futures ( also Phemex testnet )

Kraken futures ( also Kraken futures testnet )

# --- Test Cases ---

Note: These test cases are for demonstration purposes only and may not cover all scenarios.

// buy(string account, float amount, string unit = "units", float leverage = 1)

buy("MyAccount", 100, "units", 1)

buy("MyAccount", 1000, "USDT", 5)

buy("MyAccount", 50, "percent", 2)

// sell(string account, float amount, string unit = "units", float leverage = 1)

sell("MyAccount", 50, "units", 1)

sell("MyAccount", 500, "USDT", 3)

sell("MyAccount", 25, "percent", 2)

// set_position(string account, float amount, string unit = "units", float leverage = 1)

set_position("MyAccount", 100, "units", 1)

set_position("MyAccount", 1000, "USDT", 5)

set_position("MyAccount", 50, "percent", 2)

// limit_buy(string account, float amount, float price, string unit = "units", float leverage = 1, string id = "")

limit_buy("MyAccount", 100, 10000, "units", 1, "MyBuyOrder")

limit_buy("MyAccount", 1000, 10500, "USDT", 5)

limit_buy("MyAccount", 50, 11000, "percent", 2)

// limit_sell(string account, float amount, float price, string unit = "units", float leverage = 1, string id = "")

limit_sell("MyAccount", 50, 10000, "units", 1, "MySellOrder")

limit_sell("MyAccount", 500, 9500, "USDT", 3)

limit_sell("MyAccount", 25, 9000, "percent", 2)

// close_percent(string account, float pct = 100)

close_percent("MyAccount", 100)

close_percent("MyAccount", 50)

buy(account, amount, unit, leverage)

Sends a trading alert to execute a market buy order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to buy (can be in USD, units, or percentage).

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

sell(account, amount, unit, leverage)

Sends a trading alert to execute a market sell order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to sell (can be in USD, units, or percentage).

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

set_position(account, amount, unit, leverage)

Sends a trading alert to set a position.

Parameters:

account (string) : The account ID.

amount (float) : The amount to set the position to (can be in USD, units, or percentage).

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

limit_buy(account, amount, price, unit, leverage, id)

Sends a trading alert to place a limit buy order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to buy (can be in USD, units, or percentage).

price (float) : The limit price.

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

id (string) : An optional custom ID for the limit order.

limit_sell(account, amount, price, unit, leverage, id)

Sends a trading alert to place a limit sell order.

Parameters:

account (string) : The account ID.

amount (float) : The amount to sell (can be in USD, units, or percentage).

price (float) : The limit price.

unit (string) : The unit of the amount (optional, defaults to "units").

leverage (float) : The leverage to use (optional, defaults to 1x).

id (string) : An optional custom ID for the limit order.

close_percent(account, pct)

Sends an alert to close a position on Phemex.

Parameters:

account (string) : The account ID.

pct (float) : The percentage of the position to close (optional, defaults to 100%).

TechniTrend RSI (11TF)Multi-Timeframe RSI Indicator

Overview

The Multi-Timeframe RSI Indicator is a sophisticated tool designed to provide comprehensive insights into the Relative Strength Index (RSI) across 11 different timeframes simultaneously. This indicator is essential for traders who wish to monitor RSI trends and their moving averages (MA) to make informed trading decisions.

Features

Multiple Timeframes: Displays RSI and RSI MA values for 11 different timeframes, allowing traders to have a holistic view of the market conditions.

RSI vs. MA Comparison: Indicates whether the RSI value is above or below its moving average for each timeframe, helping traders to identify bullish or bearish momentum.

Overbought/Oversold Signals:

Marks "OS" (OverSell) when RSI falls below 25, indicating a potential oversold condition.

Marks "OB" (OverBuy) when RSI exceeds 75, signaling a potential overbought condition.

Real-Time Updates: Continuously updates in real-time to provide the most current market information.

Usage

This indicator is invaluable for traders who utilize RSI as part of their technical analysis strategy. By monitoring multiple timeframes, traders can:

Identify key overbought and oversold levels to make entry and exit decisions.

Observe the momentum shifts indicated by RSI crossing above or below its moving average.

Enhance their trading strategy by integrating multi-timeframe analysis for better accuracy and confirmation.

How to Interpret the Indicator

RSI Above MA: Indicates a potential bullish trend. Traders may consider looking for long positions.

RSI Below MA: Suggests a potential bearish trend. Traders may look for short positions.

OS (OverSell): When RSI < 25, the market may be oversold, presenting potential buying opportunities.

OB (OverBuy): When RSI > 75, the market may be overbought, indicating potential selling opportunities.

KillZones + ACD Fisher [TradingFinder] Sessions + Reversal Level🔵 Introduction

🟣 ACD Method

"The Logical Trader" opens with a thorough exploration of the ACD Methodology, which focuses on pinpointing particular price levels associated with the opening range.

This approach enables traders to establish reference points for their trades, using "A" and "C" points as entry markers. Additionally, the book covers the concept of the "Pivot Range" and how integrating it with the ACD method can help maximize position size while minimizing risk.

🟣 Session

The forex market is operational 24 hours a day, five days a week, closing only on Saturdays and Sundays. Typically, traders prefer to concentrate on one specific forex trading session rather than attempting to trade around the clock.

Trading sessions are defined time periods when a particular financial market is active, allowing for the execution of trades.

The most crucial trading sessions within the 24-hour cycle are the Asia, London, and New York sessions, as these are when substantial money flows and liquidity enter the market.

🟣 Kill Zone

Traders in financial markets earn profits by capitalizing on the difference between their buy/sell prices and the prevailing market prices.

Traders vary in their trading timelines.Some traders engage in daily or even hourly trading, necessitating activity during periods with optimal trading volumes and notable price movements.

Kill zones refer to parts of a session characterized by higher trading volumes and increased price volatility compared to the rest of the session.

🔵 How to Use

🟣 Session Times

The "Asia Session" comprises two parts: "Sydney" and "Tokyo." This session begins at 23:00 and ends at 06:00 UTC. The "Asia KillZone" starts at 23:00 and ends at 03:55 UTC.

The "London Session" includes "Frankfurt" and "London," starting at 07:00 and ending at 14:25 UTC. The "London KillZone" runs from 07:00 to 09:55 UTC.

The "New York" session starts at 14:30 and ends at 19:25 UTC, with the "New York am KillZone" beginning at 14:30 and ending at 22:55 UTC.

🟣 ACD Methodology

The ACD strategy is versatile, applicable to various markets such as stocks, commodities, and forex, providing clear buy and sell signals to set price targets and stop losses.

This strategy operates on the premise that the opening range of trades holds statistical significance daily, suggesting that initial market movements impact the market's behavior throughout the day.

Known as a breakout strategy, the ACD method thrives in volatile or strongly trending markets like crude oil and stocks.

Some key rules for employing the ACD strategy include :

Utilize points A and C as critical reference points, continually monitoring these during trades as they act as entry and exit markers.

Analyze daily and multi-day pivot ranges to understand market trends. Prices above the pivots indicate an upward trend, while prices below signal a downward trend.

In forex trading, the ACD strategy can be implemented using the ACD indicator, a technical tool that gauges the market's supply and demand balance. By evaluating trading volume and price, this indicator assists traders in identifying trend strength and optimal entry and exit points.

To effectively use the ACD indicator, consider the following :

Identifying robust trends: The ACD indicator can help pinpoint strong, consistent market trends.

Determining entry and exit points: ACD generates buy and sell signals to optimize trade timing.

Bullish Setup :

When the "A up" line is breached, it’s wise to wait briefly to confirm it’s not a "Fake Breakout" and that the price stabilizes above this line.

Upon entering the trade, the most effective stop loss is positioned below the "A down" line. It's advisable to backtest this to ensure the best outcomes. The recommended reward-to-risk ratio for this strategy is 1, which should also be verified through backtesting.

Bearish Setup :

When the "A down" line is breached, it’s prudent to wait briefly to ensure it’s not a "Fake Breakout" and that the price stabilizes below this line.

Upon entering the trade, the most effective stop loss is positioned above the "A up" line. Backtesting is recommended to confirm the best results. The recommended reward-to-risk ratio for this strategy is 1, which should also be validated through backtesting.

Advantages of Combining Kill Zone and ACD Method in Market Analysis :

Precise Trade Timing : Integrating the Kill Zone strategy with the ACD Method enhances precision in trade entries and exits. The ACD Method identifies key points for trading, while the Kill Zone focuses on high-activity periods, together ensuring optimal timing for trades.

Better Trend Identification : The ACD Method’s pivot ranges help spot market trends, and when combined with the Kill Zone’s emphasis on periods of significant price movement, traders can more effectively identify and follow strong market trends.

Maximized Profits and Minimized Risks : The ACD Method's structured approach to setting price targets and stop losses, coupled with the Kill Zone's high-volume trading periods, helps maximize profit potential while reducing risk.

Robust Risk Management : Combining these methods provides a comprehensive risk management strategy, strategically placing stop losses and protecting capital during volatile periods.

Versatility Across Markets : Both methods are applicable to various markets, including stocks, commodities, and forex, offering flexibility and adaptability in different trading environments.

Enhanced Confidence : Using the combined insights of the Kill Zone and ACD Method, traders gain confidence in their decision-making process, reducing emotional trading and improving consistency.

By merging the Kill Zone’s focus on trading volumes and the ACD Method’s structured breakout strategy, traders benefit from a synergistic approach that enhances precision, trend identification, and risk management across multiple markets.

Directional Movement Index DEThis script uses the existing built-in DMI indicator but adds two lines indicating strength of the ADX trend. The original author J. Welles Wilder, indicated a ADX trending strongly above 25 (yellow by default), and ADX trending weaker at a threshold of 20 or below (dashed yellow by default).

The default colours have been changed so that ADX is yellow, +DI is green, and -DI is red.

Calculation

Calculating the DMI can actually be broken down into two parts. First, calculating the +DI and -DI, and second, calculating the ADX. To calculate the +DI and -DI you need to find the +DM and -DM (Directional Movement). +DM and -DM are calculated using the High, Low and Close for each period. You can then calculate the following:

Current High - Previous High = UpMove

Previous Low - Current Low = DownMove

If UpMove > DownMove and UpMove > 0, then +DM = UpMove, else +DM = 0

If DownMove > Upmove and Downmove > 0, then -DM = DownMove, else -DM = 0

Once you have the current +DM and -DM calculated, the +DM and -DM lines can be calculated and plotted based on the number of user defined periods.

+DI = 100 times Exponential Moving Average of (+DM / Average True Range)

-DI = 100 times Exponential Moving Average of (-DM / Average True Range)

Now that -+DX and -DX have been calculated, the last step is calculating the ADX.

ADX = 100 times the Exponential Moving Average of the Absolute Value of (+DI - -DI) / (+DI + -DI)

The basics

DMI has a value between 0 and 100 and is used to measure the strength of the current trend. +DI and -DI are then used to measure direction. When combined, the indicator can provide some valuable insight. A general interpretation would be that during a strong trend (ADX above 25 but dependent on the analyst's interpretation), when the +DI is above the -DI, then a Bullish Market is defined. When -DI is above +DI, then a Bearish Market is at hand.

One thing to be considered is that what DMI values determine, strength or a potential signal, is up to the trader's interpretation. Acceptable values may change depending on the financial instrument being examined, therefore some historical analysis of the instrument in question would be prudent. A technical analyst can make better decisions based on what has occurred in historical examples.

All credit goes to the original script .

Trend Momentum Strength Indicator, Built for Pairs TradingOverview:

This script combines multiple indicators to provide a comprehensive analysis of both trend strength and trend momentum. It is tailored specifically for pairs trading strategies but can also be used for other trading strategies.

Benefit of Comprehensive Analysis:

Having an indicator that evaluates both trend strength and trend momentum is crucial for traders looking to make informed decisions. It allows traders to not only identify the direction and intensity of a trend but also gauge the momentum behind it. This dual capability helps in confirming potential trade opportunities, whether for entering trades with strong trends or considering reversals during overbought or oversold conditions. By integrating both aspects into one tool, traders can gain a holistic view of market dynamics, enhancing their ability to time entries and manage risk effectively.

Features:

* Trend Strength:

Enhanced ADX Formula: The script includes modifications to the standard ADX formula along with DI+ and DI- to provide more responsive trend strength readings.

Directional Indicators: DI+ (green line) indicates positive directional movement, while DI- (red line) indicates negative directional movement.

Trend Momentum:

Modified Stochastic Indicators: The script uses %K and %D indicators, modified and combined with ADX to give a clear indication of trend momentum.

Momentum Strength: This helps determine the strength and direction of the momentum.

Trading Signals:

Combining Indicators: The script combines ADX, DI+, DI-, %K, and %D to generate comprehensive trading signals.

Optimal Entry Points: Designed to identify optimal entry points for trades, particularly in pairs trading.

Colored Area at Bottom:

This area provides two easy-to-read functions:

Color:

Green: Upward momentum (ratio above 1)

Red: Downward momentum (ratio below 1)

Height:

Higher in green: Stronger upward momentum

Lower in red: Stronger downward momentum

Legend:

Green Line: DI+ (Positive)

Red Line: DI- (Negative)

Black Line: ADX

How to Read This Indicator:

1) Trend Direction:

DI+ above DI-: Indicates an upward trend.

DI- above DI+: Indicates a downward trend.

2) Trend Strength:

ADX below 20: Indicates a neutral trend.

ADX between 20 and 25: Indicates a weak trend.

ADX above 25: Indicates a strong trend.

Trading Signals in Pairs Trading:

Neutral Trend: Ideal for pairs trading when no strong trend is detected.

Overbought/Oversold: Uses %K and %D to identify overbought/oversold conditions that support trade decisions.

Entry Signals: Green signals for long positions, red signals for short positions, based on combined criteria of neutral trend strength and supportive momentum.

Application in Pairs Trading:

Neutral trend: In pairs trading strategies, where neutral movement is often sought, this indicator provides signals that are especially relevant during periods of neutral trend strength and supportive momentum, aiding traders in identifying optimal entry

Risk Management: Combining signals from ADX, DI+, DI-, %K, and %D helps traders make more informed decisions regarding entry points, enhancing risk management.

Example Chart (The indicator is on the upper right corner):

Clean Presentation: The chart only includes the necessary elements to demonstrate the indicator’s functionality.

Demonstrates: Overbought/oversold conditions, upward/downward/no momentum, and trading signals with/without specific scenarios.

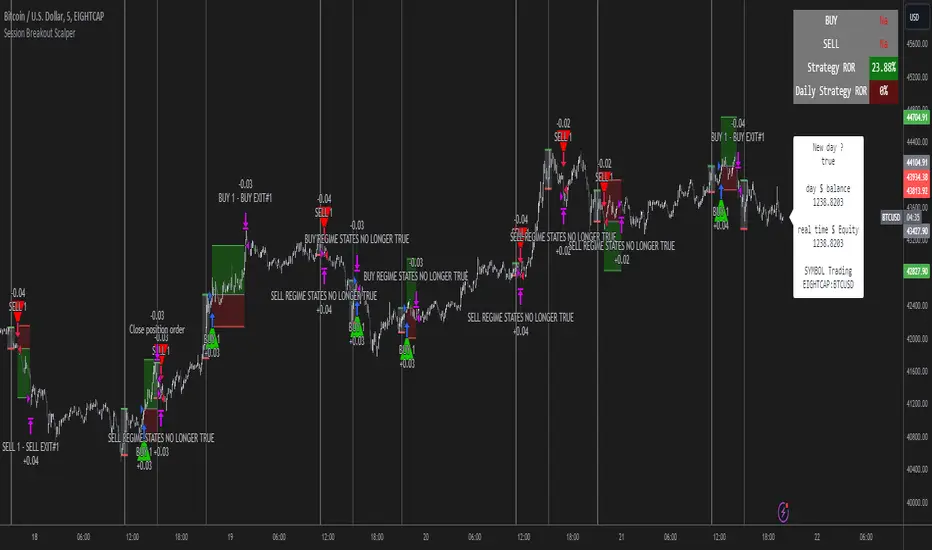

Session Breakout Scalper Trading BotHi Traders !

Introduction:

I have recently been exploring the world of automated algorithmic trading (as I prefer more objective trading strategies over subjective technical analysis (TA)) and would like to share one of my automation compatible (PineConnecter compatible) scripts “Session Breakout Scalper”.

The strategy is really simple and is based on time conditional breakouts although has more ”relatively” advanced optional features such as the regime indicators (Regime Filters) that attempt to filter out noise by adding more confluence states and the ATR multiple SL that takes into account volatility to mitigate the down side risk of the trade.

What is Algorthmic Trading:

Firstly what is algorithmic trading? Algorithmic trading also known as algo-trading, is a method of using computer programs (in this case pine script) to execute trades based on predetermined rules and instructions (this trading strategy). It's like having a robot trader who follows a strict set of commands to buy and sell assets automatically, without any human intervention.

Important Note:

For Algorithmic trading the strategy will require you having an essential TV subscription at the minimum (so that you can set alerts) plus a PineConnecter subscription (scroll down to the .”How does the strategy send signals” headings to read more)

The Strategy Explained:

Is the Time input true ? (this can be changed by toggling times under the “TRADE MEDIAN TIMES” group for user inputs).

Given the above is true the strategy waits x bars after the session and then calculates the highest high (HH) to lowest low (LL) range. For this box to form, the user defined amount of bars must print after the session. The box is symmetrical meaning the HH and LL are calculated over a lookback that is equal to the sum of user defined bars before and after the session (+ 1).

The Strategy then simultaneously defines the HH as the buy level (green line) and the LL as the sell level (red line). note the strategy will set stop orders at these levels respectively.

Enter a buy if price action crosses above the HH, and then cancel the sell order type (The opposite is true for a stop order).

If the momentum based regime filters are true the strategy will check for the regime / regimes to be true, if the regime if false the strategy will exit the current trade, as the regime filter has predicted a slowing / reversal of momentum.

The image below shows the strategy executing these trading rules ( Regime filters, "Trades on chart", "Signal & Label" and "Quantity" have been omitted. "Strategy label plots" has been switched to true)

Other Strategy Rules:

If a new session (time session which is user defined) is true (blue vertical line) and the strategy is currently still in a trade it will exit that trade immediately.

It is possible to also set a range of percentage gain per day that the strategy will try to acquire, if at any point the strategy’s profit is within the percentage range then the position / trade will be exited immediately (This can be changed in the “PERCENT DAY GAIN” group for user inputs)

Stops and Targets:

The strategy has either static (fixed) or variable SL options. TP however is only static. The “STRAT TP & TP” group of user inputs is responsible for the SL and TP values (quoted in pips). Note once the ATR stop is set to true the SL values in the above group no longer have any affect on the SL as expected.

What are the Regime Filters:

The Larry Williams Large Trade Index (LWLTI): The Larry Williams Large Trade Index (LWTI) is a momentum-based technical indicator developed by iconic trader Larry Williams. It identifies potential entries and exits for trades by gauging market sentiment, particularly the buying and selling pressure from large market players. Here's a breakdown of the LWTI:

LWLTI components and their interpretation:

Oscillator: It oscillates between 0 and 100, with 50 acting as the neutral line.

Sentiment Meter: Values above 75 suggest a bearish market dominated by large selling, while readings below 25 indicate a bullish market with strong buying from large players.

Trend Confirmation: Crossing above 75 during an uptrend and below 25 during a downtrend confirms the trend's continuation.

The Andean Oscillator (AO) : The Andean Oscillator is a trend and momentum based indicator designed to measure the degree of variations within individual uptrends and downtrends in the prices.

Regime Filter States:

In trading, a regime filter is a tool used to identify the current state or "regime" of the market.

These Regime filters are integrated within the trading strategy to attempt to lower risk (equity volatility and/or draw down). The regime filters have different states for each market order type (buy and sell). When the regime filters are set to true, if these regime states fail to be true the trade is exited immediately.

For Buy Trades:

LWLTI positive momentum state: Quotient of the lagged trailing difference and the ATR > 50

AO positive momentum state: Bull line > Bear line (signal line is omitted)

For Sell Trades:

LWLTI negative momentum stat: Quotient of the lagged trailing difference and the ATR < 50

AO negative momentum state: Bull line < Bear line (signal line is omitted)

How does the Strategy Send Signals:

The strategy triggers a TV alert (you will neet to set a alert first), TV then sends a HTTP request to the automation software (PineConnecter) which receives the request and then communicates to an MT4/5 EA to automate the trading strategy.

For the strategy to send signals you must have the following

At least a TV essential subscription

This Script added to your chart

A PineConnecter account, which is paid and not free. This will provide you with the expert advisor that executes trades based on these strategies signals.

For more detailed information on the automation process I would recommend you read the PineConnecter documentation and FAQ page.

Dashboard:

This Dashboard (top right by defualt) lists some simple trading statistics and also shows when a trade is live.

Important Notice:

- USE THIS STRATEGY AT YOUR OWN RISK AND ALWAYS DO YOUR OWN RESEARCH & MANUAL BACKTESTING !

- THE STRATEGY WILL NOT EXHIBIT THE BACKTEST PERFORMANCE SEEN BELOW IN ALL MARKETS !

Mike's Crossover BotGreetings! As a newcomer to coding, I've developed a simple trading bot for experimentation purposes. However, it's important to note that this bot has not undergone rigorous testing, so please exercise caution and use it at your own risk.

Bot Overview:

The bot operates by leveraging two technical indicators: Moving Average Convergence Divergence (MACD) with 7-day and 25-day parameters, and the Relative Strength Index (RSI). These indicators help identify potential buying and selling opportunities in the market.

MACD Crossovers:

The MACD is a trend-following momentum indicator that compares short-term and long-term moving averages. In our bot, we look for crossovers between the 7-day and 25-day MACD lines. A crossover occurs when these lines intersect, suggesting a potential change in market direction.

RSI Confirmation:

To refine our signals, we incorporate the Relative Strength Index (RSI). When a MACD crossover happens, the bot checks if the RSI is below 40. If it is, a buy signal is generated, indicating a potential undervalued condition. Conversely, when the RSI is above 60 during a crossover, a sell signal is triggered, suggesting a potentially overvalued condition.

Important Considerations:

New Coder Disclaimer: This bot is designed for educational purposes, especially for those who are new to coding. It serves as a learning tool and is not intended for live trading without proper testing.

Risk Awareness: Trading always involves risks, and the bot's performance has not been thoroughly tested in live market conditions. It's crucial to exercise caution and be aware of the inherent risks associated with financial markets.

Continuous Learning: Coding and algorithmic trading are dynamic fields. As you explore this bot, consider it a starting point for learning and continuously seek to enhance your understanding and skills in coding and trading strategies.

Remember, the success of any trading strategy depends on various factors, and past performance is not indicative of future results. Always conduct thorough testing before considering any automated strategy for live trading.

Adaptive MFT Extremum Pivots [Elysian_Mind]Adaptive MFT Extremum Pivots

Overview:

The Adaptive MFT Extremum Pivots indicator, developed by Elysian_Mind, is a powerful Pine Script tool that dynamically displays key market levels, including Monthly Highs/Lows, Weekly Extremums, Pivot Points, and dynamic Resistances/Supports. The term "dynamic" emphasizes the adaptive nature of the calculated levels, ensuring they reflect real-time market conditions. I thank Zandalin for the excellent table design.

---

Chart Explanation:

The table, a visual output of the script, is conveniently positioned in the bottom right corner of the screen, showcasing the indicator's dynamic results. The configuration block, elucidated in the documentation, empowers users to customize the display position. The default placement is at the bottom right, exemplified in the accompanying chart.

The deliberate design ensures that the table does not obscure the candlesticks, with traders commonly situating it outside the candle area. However, the flexibility exists to overlay the table onto the candles. Thanks to transparent cells, the underlying chart remains visible even with the table displayed atop.

In the initial column of the table, users will find labels for the monthly high and low, accompanied by their respective numerical values. The default precision for these values is set at #.###, yet this can be adjusted within the configuration block to suit markets with varying degrees of volatility.

Mirroring this layout, the last column of the table presents the weekly high and low data. This arrangement is part of the upper half of the table. Transitioning to the lower half, users encounter the resistance levels in the first column and the support levels in the last column.

At the center of the table, prominently displayed, is the monthly pivot point. For a comprehensive understanding of the calculations governing these values, users can refer to the documentation. Importantly, users retain the freedom to modify these mathematical calculations, with the table seamlessly updating to reflect any adjustments made.

Noteworthy is the table's persistence; it continues to display reliably even if users choose to customize the mathematical calculations, providing a consistent and adaptable tool for informed decision-making in trading.

This detailed breakdown offers traders a clear guide to interpreting the information presented by the table, ensuring optimal use and understanding of the Adaptive MFT Extremum Pivots indicator.

---

Usage:

Table Layout:

The table is a crucial component of this indicator, providing a structured representation of various market levels. Color-coded cells enhance readability, with blue indicating key levels and a semi-transparent background to maintain chart visibility.

1. Utilizing a Table for Enhanced Visibility:

In presenting this wealth of information, the indicator employs a table format beneath the chart. The use of a table is deliberate and offers several advantages:

2. Structured Organization:

The table organizes the diverse data into a structured format, enhancing clarity and making it easier for traders to locate specific information.

3. Concise Presentation:

A table allows for the concise presentation of multiple data points without cluttering the main chart. Traders can quickly reference key levels without distraction.

4. Dynamic Visibility:

As the market dynamically evolves, the table seamlessly updates in real-time, ensuring that the most relevant information is readily visible without obstructing the candlestick chart.

5. Color Coding for Readability:

Color-coded cells in the table not only add visual appeal but also serve a functional purpose by improving readability. Key levels are easily distinguishable, contributing to efficient analysis.

Data Values:

Numerical values for each level are displayed in their respective cells, with precision defined by the iPrecision configuration parameter.

Configuration:

// User configuration: You can modify this part without code understanding

// Table location configuration

// Position: Table

const string iPosition = position.bottom_right

// Width: Table borders

const int iBorderWidth = 1

// Color configuration

// Color: Borders

const color iBorderColor = color.new(color.white, 75)

// Color: Table background

const color iTableColor = color.new(#2B2A29, 25)

// Color: Title cell background

const color iTitleCellColor = color.new(#171F54, 0)

// Color: Characters

const color iCharColor = color.white

// Color: Data cell background

const color iDataCellColor = color.new(#25456E, 0)

// Precision: Numerical data

const int iPrecision = 3

// End of configuration

The code includes a configuration block where users can customize the following parameters:

Precision of Numerical Table Data (iPrecision):

// Precision: Numerical data

const int iPrecision = 3

This parameter (iPrecision) sets the precision of the numerical values displayed in the table. The default value is 3, displaying numbers in #.### format.

Position of the Table (iPosition):

// Position: Table

const string iPosition = position.bottom_right

This parameter (iPosition) sets the position of the table on the chart. The default is position.bottom_right.

Color preferences

Table borders (iBorderColor):

// Color: Borders

const color iBorderColor = color.new(color.white, 75)

This parameters (iBorderColor) sets the color of the borders everywhere within the window.

Table Background (iTableColor):

// Color: Table background

const color iTableColor = color.new(#2B2A29, 25)

This is the background color of the table. If you've got cells without custom background color, this color will be their background.

Title Cell Background (iTitleCellColor):

// Color: Title cell background

const color iTitleCellColor = color.new(#171F54, 0)

This is the background color the title cells. You can set the background of data cells and text color elsewhere.

Text (iCharColor):

// Color: Characters

const color iCharColor = color.white

This is the color of the text - titles and data - within the table window. If you change any of the background colors, you might want to change this parameter to ensure visibility.

Data Cell Background: (iDataCellColor):

// Color: Data cell background

const color iDataCellColor = color.new(#25456E, 0)

The data cells have a background color to differ from title cells. You can configure this is a different parameter (iDataColor). You might even set the same color for data as for the titles if you will.

---

Mathematical Background:

Monthly and Weekly Extremums:

The indicator calculates the High (H) and Low (L) of the previous month and week, ensuring accurate representation of these key levels.

Standard Monthly Pivot Point:

The standard pivot point is determined based on the previous month's data using the formula:

PivotPoint = (PrevMonthHigh + PrevMonthLow + Close ) / 3

Monthly Pivot Points (R1, R2, R3, S1, S2, S3):

Additional pivot points are calculated for Resistances (R) and Supports (S) using the monthly data:

R1 = 2 * PivotPoint - PrevMonthLow

S1 = 2 * PivotPoint - PrevMonthHigh

R2 = PivotPoint + (PrevMonthHigh - PrevMonthLow)

S2 = PivotPoint - (PrevMonthHigh - PrevMonthLow)

R3 = PrevMonthHigh + 2 * (PivotPoint - PrevMonthLow)

S3 = PrevMonthLow - 2 * (PrevMonthHigh - PivotPoint)

---

Code Explanation and Interpretation:

The table displayed beneath the chart provides the following information:

Monthly Extremums:

(H) High of the previous month

(L) Low of the previous month

// Function to get the high and low of the previous month

getPrevMonthHighLow() =>

var float prevMonthHigh = na

var float prevMonthLow = na

monthChanged = month(time) != month(time )

if (monthChanged)

prevMonthHigh := high

prevMonthLow := low

Weekly Extremums:

(H) High of the previous week

(L) Low of the previous week

// Function to get the high and low of the previous week

getPrevWeekHighLow() =>

var float prevWeekHigh = na

var float prevWeekLow = na

weekChanged = weekofyear(time) != weekofyear(time )

if (weekChanged)

prevWeekHigh := high

prevWeekLow := low

Monthly Pivots:

Pivot: Standard pivot point based on the previous month's data

// Function to calculate the standard pivot point based on the previous month's data

getStandardPivotPoint() =>

= getPrevMonthHighLow()

pivotPoint = (prevMonthHigh + prevMonthLow + close ) / 3

Resistances:

R3, R2, R1: Monthly resistance levels

// Function to calculate additional pivot points based on the monthly data

getMonthlyPivotPoints() =>

= getPrevMonthHighLow()

pivotPoint = (prevMonthHigh + prevMonthLow + close ) / 3

r1 = (2 * pivotPoint) - prevMonthLow

s1 = (2 * pivotPoint) - prevMonthHigh

r2 = pivotPoint + (prevMonthHigh - prevMonthLow)

s2 = pivotPoint - (prevMonthHigh - prevMonthLow)

r3 = prevMonthHigh + 2 * (pivotPoint - prevMonthLow)

s3 = prevMonthLow - 2 * (prevMonthHigh - pivotPoint)

Initializing and Populating the Table:

The myTable variable initializes the table with a blue background, and subsequent table.cell functions populate the table with headers and data.

// Initialize the table with adjusted bgcolor

var myTable = table.new(position = iPosition, columns = 5, rows = 10, bgcolor = color.new(color.blue, 90), border_width = 1, border_color = color.new(color.blue, 70))

Dynamic Data Population:

Data is dynamically populated in the table using the calculated values for Monthly Extremums, Weekly Extremums, Monthly Pivot Points, Resistances, and Supports.

// Add rows dynamically with data

= getPrevMonthHighLow()

= getPrevWeekHighLow()

= getMonthlyPivotPoints()

---

Conclusion:

The Adaptive MFT Extremum Pivots indicator offers traders a detailed and clear representation of critical market levels, empowering them to make informed decisions. However, users should carefully analyze the market and consider their individual risk tolerance before making any trading decisions. The indicator's disclaimer emphasizes that it is not investment advice, and the author and script provider are not responsible for any financial losses incurred.

---

Disclaimer:

This indicator is not investment advice. Trading decisions should be made based on a careful analysis of the market and individual risk tolerance. The author and script provider are not responsible for any financial losses incurred.

Kind regards,

Ely

Captain Backtest Model [TFO]Created by @imjesstwoone and @mickey1984, this trade model attempts to capture the expansion from the 10:00-14:00 EST 4h candle using just 3 simple steps. All of the information presented in this description has been outlined by its creators, all I did was translate it to Pine Script. All core settings of the trade model may be edited so that users can test several variations, however this description will cover its default, intended behavior using NQ 5m as an example.

Step 1 is to identify our Price Range. In this case, we are concerned with the highest high and the lowest low created from 6:00-10:00 EST.

Step 2 is to wait for either the high or low of said range to be taken out. Whichever side gets taken first determines the long/short bias for the remainder of the Trade Window (i.e. if price takes the range high, bias is long, and vice versa). Bias must be determined by 11:15 EST, otherwise no trades will be taken. This filter is intended to weed out "choppy" trading days.

Step 3 is to wait for a retracement and enter with a close through the previous candle's high (if long biased) or low (if short biased). There are a couple toggleable criteria that we use to define a retracement; one is checking for opposite close candles that indicate a pullback; another is checking if price took the previous candle's low (if long biased) or high (if short biased).

This trade model was initially tested for index futures, particularly ES and NQ, using a 5m chart, however this indicator allows us to backtest any symbol on any timeframe. Creators @imjesstwoone and @mickey1984 specified a 5 point stop loss on ES and a 25 point stop loss on NQ with their testing.

I've personally found some success in backtesting NQ 5m using a 25 point stop loss and 75 point profit target (3:1 R). Enabling the Use Fixed R:R parameter will ensure that these stops and targets are utilized, otherwise it will enter and hold the position until the close of the Trade Window.

Dip & Rip Patterns - The Quant Science🇺🇸

GENERAL OVERVIEW

This indicator detects Dip and Rip patterns by quickly highlighting them on the chart.

These patterns have become popular during the pandemic period mainly in the stock, ETF and cryptocurrency markets on which traders use two interesting strategies:

Buy The Dip

Sell The Rip

Before going into the merits of this technical indicator, let's understand what these two patterns mean and what they identify precisely.

Rip (Rise In Price) : wants to identify a market condition in which the price rises rapidly, for example from $100 to $110 in a few minutes or hours.

Dip (Drop In Price) : wants to identify a market condition in which the price drops rapidly, for example from $100 to $90 in a few minutes or hours.

HOW TO USE

For a better user experience, we recommend choosing a neutral colour for the candles while analysing with this indicator. You can quickly change the colour in Chart Settings > Symbol > Candles .

Depending on the configuration set by the user, the indicator will show Dip (Dip In Price) patterns in red and Rip (Rise In Price) patterns in green.

When the pattern forms, a circle will be displayed and a vertical line will be coloured on the chart along with the body of the candle. The user will then be able to quickly and easily track the configured market conditions.

In this example, we decided to use a 4H timeframe on the BTC/USDT pair (Binance).

Set in the user interface:

Period: 20

Dip (%): -25

Rip (%): 20

Price falls by 25% or more in 80 hours (Dip Pattern).

Price rise by 25% or more in 80 hours (Rip Pattern).

The user can easily configure the parameters via the user interface in the Inputs section (A) and change the indicator design in the Properties section (B).

🇮🇹

PANORAMICA GENERALE

Questo indicatore rileva i Dip e Rip patterns evidenziandoli velocemente sul grafico.

Questi patterns sono diventati famosi durante il periodo pandemico principalmente nel mercato delle azioni, ETF e Criptovalute su cui i trader utilizzano due interessanti strategie:

Buy The Dip

Sell The Rip

Prima di entrare nel merito di questo indicatore tecnico, comprendiamo il significato di questi due pattern e cosa identificano precisamente.

Rip (Rise In Price) : vuole identificare una condizione di mercato in cui il prezzo sale rapidamente, per esempio passando da 100$ a 110$ in pochi minuti o poche ore.

Dip (Drop In Price) : vuole identificare una condizione di mercato in cui il prezzo cala rapidamente, per esempio passando da 100$ a 90$ in pochi minuti o poche ore.

UTILIZZO

Per una migliore esperienza utente consigliamo di scegliere un colore neutro per le candele mentre si analizza con questo indicatore. Puoi cambiare velocemente il colore in Chart Settings > Symbol > Candles .

In base alla configurazione impostata dall'utente l'indicatore mostrerà in rosso i pattern Dip (Dip In Price) e in verde i pattern Rip (Rise In Price).

Quando il pattern si forma verrà visualizzato un cerchio e una linea verticale sul grafico che sarà colorata insieme al corpo della candela. L'utente quindi potrà tracciare facilmente e velocemente le condizioni di mercato configurate.

In questo esempio abbiamo deciso di utilizzare un timeframe 4H con l'obbiettivo di ricercare i patterns sul pair BTC/USDT (Binance).

Impostiamo nell'interfaccia utente:

Period: 20

Dip (%): -25

Rip (%): 20

Il prezzo diminuisce del 25% o più in 80 ore (Dip Pattern).

Il prezzo aumenta del 25% o più in 80 ore (Rip Pattern).

L' utente può configurare facilmente i parametri attraverso l'interfaccia utente nella sezione Inputs (A) e modificare il design dell'indicatore nella sezione Properties (B).

lib_profileLibrary "lib_profile"

a library with functions to calculate a volume profile for either a set of candles within the current chart, or a single candle from its lower timeframe security data. All you need is to feed the

method delete(this)

deletes this bucket's plot from the chart

Namespace types: Bucket

Parameters:

this (Bucket)

method delete(this)

Namespace types: Profile

Parameters:

this (Profile)

method delete(this)

Namespace types: Bucket

Parameters:

this (Bucket )

method delete(this)

Namespace types: Profile

Parameters:

this (Profile )

method update(this, top, bottom, value, fraction)

updates this bucket's data

Namespace types: Bucket

Parameters:

this (Bucket)

top (float)

bottom (float)

value (float)

fraction (float)

method update(this, tops, bottoms, values)

update this Profile's data (recalculates the whole profile and applies the result to this object) TODO optimisation to calculate this incremental to improve performance in realtime on high resolution

Namespace types: Profile

Parameters:

this (Profile)

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

method tostring(this)

allows debug print of a bucket

Namespace types: Bucket

Parameters:

this (Bucket)

method draw(this, start_t, start_i, end_t, end_i, args, line_color)

allows drawing a line in a Profile, representing this bucket and it's value + it's value's fraction of the Profile total value

Namespace types: Bucket

Parameters:

this (Bucket)

start_t (int) : the time x coordinate of the line's left end (depends on the Profile box)

start_i (int) : the bar_index x coordinate of the line's left end (depends on the Profile box)

end_t (int) : the time x coordinate of the line's right end (depends on the Profile box)

end_i (int) : the bar_index x coordinate of the line's right end (depends on the Profile box)

args (LineArgs type from robbatt/lib_plot_objects/24) : the default arguments for the line style

line_color (color) : the color override for POC/VAH/VAL lines

method draw(this, forced_width)

draw all components of this Profile (Box, Background, Bucket lines, POC/VAH/VAL overlay levels and labels)

Namespace types: Profile

Parameters:

this (Profile)

forced_width (int) : allows to force width of the Profile Box, overrides the ProfileArgs.default_size and ProfileArgs.extend arguments (default: na)

method init(this)

Namespace types: ProfileArgs

Parameters:

this (ProfileArgs)

method init(this)

Namespace types: Profile

Parameters:

this (Profile)

profile(tops, bottoms, values, resolution, vah_pc, val_pc, bucket_buffer)

split a chart/parent bar into 'resolution' sections, figure out in which section the most volume/time was spent, by analysing a given set of (intra)bars' top/bottom/volume values. Then return price center of the bin with the highest volume, essentially marking the point of control / highest volume (poc) in the chart/parent bar.

Parameters:

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

resolution (int) : amount of buckets/price ranges to sort the candle data into (analyse how much volume / time was spent in a certain bucket/price range) (default: 25)

vah_pc (float) : a threshold percentage (of values' total) for the top end of the value area (default: 80)

val_pc (float) : a threshold percentage (of values' total) for the bottom end of the value area (default: 20)

bucket_buffer (Bucket ) : optional buffer of empty Buckets to fill, if omitted a new one is created and returned. The buffer length must match the resolution

Returns: poc (price level), vah (price level), val (price level), poc_index (idx in buckets), vah_index (idx in buckets), val_index (idx in buckets), buckets (filled buffer or new)

create_profile(start_idx, tops, bottoms, values, resolution, vah_pc, val_pc, args)

split a chart/parent bar into 'resolution' sections, figure out in which section the most volume/time was spent, by analysing a given set of (intra)bars' top/bottom/volume values. Then return price center of the bin with the highest volume, essentially marking the point of control / highest volume (poc) in the chart/parent bar.

Parameters:

start_idx (int) : the bar_index at which the Profile should start drawing

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

resolution (int) : amount of buckets/price ranges to sort the candle data into (analyse how much volume / time was spent in a certain bucket/price range) (default: 25)

vah_pc (float) : a threshold percentage (of values' total) for the top end of the value area (default: 80)

val_pc (float) : a threshold percentage (of values' total) for the bottom end of the value area (default: 20)

args (ProfileArgs)

Returns: poc (price level), vah (price level), val (price level), poc_index (idx in buckets), vah_index (idx in buckets), val_index (idx in buckets), buckets (filled buffer or new)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (int)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (float)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (bool)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (string)

len (int)

offset (int)

Bucket

Fields:

idx (series int) : the index of this Bucket within the Profile starting with 0 for the lowest Bucket at the bottom of the Profile

value (series float) : the value of this Bucket, can be volume or time, for using time pass and array of 1s to the update function

top (series float) : the top of this Bucket's price range (for calculation)

btm (series float) : the bottom of this Bucket's price range (for calculation)

center (series float) : the center of this Bucket's price range (for plotting)

fraction (series float) : the fraction this Bucket's value is compared to the total of the Profile

plot_bucket_line (Line type from robbatt/lib_plot_objects/24) : the line that resembles this bucket and it's valeu in the Profile

ProfileArgs

Fields:

show_poc (series bool) : whether to plot a POC line across the Profile Box (default: true)

show_profile (series bool) : whether to plot a line for each Bucket in the Profile Box, indicating the value per Bucket (Price range), e.g. volume that occured in a certain time and price range (default: false)

show_va (series bool) : whether to plot a VAH/VAL line across the Profile Box (default: false)

show_va_fill (series bool) : whether to fill the 'value' area between VAH/VAL line (default: false)

show_background (series bool) : whether to fill the Profile Box with a background color (default: false)

show_labels (series bool) : whether to add labels to the right end of the POC/VAH/VAL line (default: false)

show_price_levels (series bool) : whether add price values to the labels to the right end of the POC/VAH/VAL line (default: false)

extend (series bool) : whether extend the Profile Box to the current candle (default: false)

default_size (series int) : the default min. width of the Profile Box (default: 30)

args_poc_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the poc line plot

args_va_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the va line plot

args_poc_label (LabelArgs type from robbatt/lib_plot_objects/24) : arguments for the poc label plot

args_va_label (LabelArgs type from robbatt/lib_plot_objects/24) : arguments for the va label plot

args_profile_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the Bucket line plots

args_profile_bg (BoxArgs type from robbatt/lib_plot_objects/24)

va_fill_color (series color) : color for the va area fill plot

Profile

Fields:

start (series int) : left x coordinate for the Profile Box

end (series int) : right x coordinate for the Profile Box

resolution (series int) : the amount of buckets/price ranges the Profile will dissect the data into

vah_threshold_pc (series float) : the percentage of the total data value to mark the upper threshold for the main value area

val_threshold_pc (series float) : the percentage of the total data value to mark the lower threshold for the main value area

args (ProfileArgs) : the style arguments for the Profile Box

h (series float) : the highest price of the data

l (series float) : the lowest price of the data

total (series float) : the total data value (e.g. volume of all candles, or just one each to analyse candle distribution over time)

buckets (Bucket ) : the Bucket objects holding the data for each price range bucket

poc_bucket_index (series int) : the Bucket index in buckets, that holds the poc Bucket

vah_bucket_index (series int) : the Bucket index in buckets, that holds the vah Bucket

val_bucket_index (series int) : the Bucket index in buckets, that holds the val Bucket

poc (series float) : the according price level marking the Point Of Control

vah (series float) : the according price level marking the Value Area High

val (series float) : the according price level marking the Value Area Low

plot_poc (Line type from robbatt/lib_plot_objects/24)

plot_vah (Line type from robbatt/lib_plot_objects/24)

plot_val (Line type from robbatt/lib_plot_objects/24)

plot_poc_label (Label type from robbatt/lib_plot_objects/24)

plot_vah_label (Label type from robbatt/lib_plot_objects/24)

plot_val_label (Label type from robbatt/lib_plot_objects/24)

plot_va_fill (LineFill type from robbatt/lib_plot_objects/24)

plot_profile_bg (Box type from robbatt/lib_plot_objects/24)

MACDVMACDV = Moving Average Convergence Divergence Volume

The MACDV indicator uses stochastic accumulation / distribution volume inflow and outflow formulas to visualize it in a standard MACD type of appearance.

To be able to merge these formulas I had to normalize the math.

Accumulation / distribution volume is a unique scale.

Stochastic is a 0-100 scale.

MACD is a unique scale.

The normalized output scale range for MACDV is -100 to 100.

100 = overbought

-100 = oversold

Everything in between is either bullish or bearish.

Rising = bullish

Falling = bearish

crossover = bullish

crossunder = bearish

convergence = direction change

divergence = momentum

The default input settings are:

7 = K length, Stochastic accumulation / distribution length

3 = D smoothing, smoothing stochastic accumulation / distribution volume weighted moving average

6 = MACDV fast, MACDV fast length line

color = blue

13 = MACDV slow, MACDV slow length line

color = white

4 = MACDV signal, MACDV histogram length

color rising above 0 = bright green

color falling above 0 = dark green

color falling below 0 = bright red

color rising below 0 = dark red

2 = Stretch, Output multiplier for MACDV visual expansion

Horizontal lines:

100

75

50

25

0

-25

-50

-75

-100

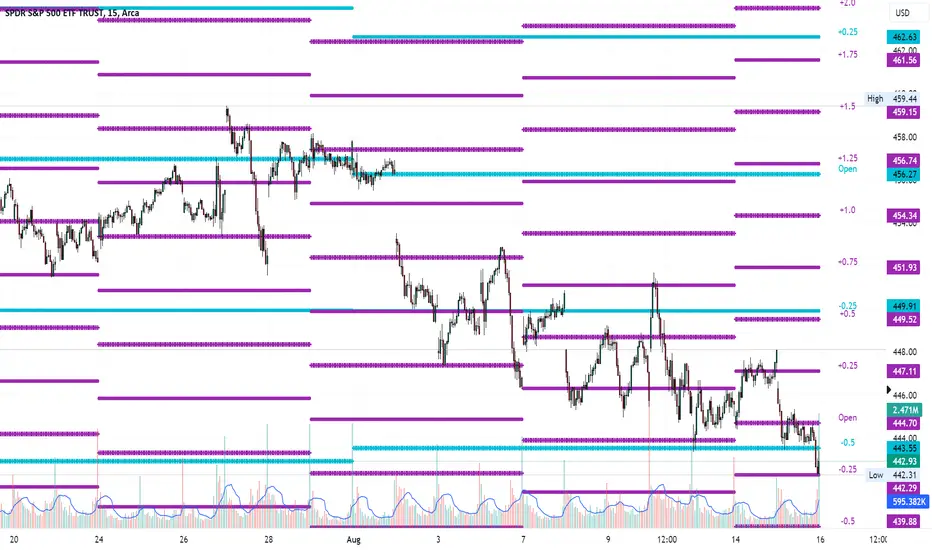

Average Range LinesThis Average Range Lines indicator identifies high and low price levels based on a chosen time period (day, week, month, etc.) and then uses a simple moving average over the length of the lookback period chosen to project support and resistance levels, otherwise referred to as average range. The calculation of these levels are slightly different than Average True Range and I have found this to be more accurate for intraday price bounces.

Lines are plotted and labeled on the chart based on the following methodology:

+3.0: 3x the average high over the chosen timeframe and lookback period.

+2.5: 2.5x the average high over the chosen timeframe and lookback period.

+2.0: 2x the average high over the chosen timeframe and lookback period.

+1.5: 1.5x the average high over the chosen timeframe and lookback period.

+1.0: The average high over the chosen timeframe and lookback period.

+0.5: One-half the average high over the chosen timeframe and lookback period.

Open: Opening price for the chosen time period.

-0.5: One-half the average low over the chosen timeframe and lookback period.

-1.0: The average low over the chosen timeframe and lookback period.

-1.5: 1.5x the average low over the chosen timeframe and lookback period.

-2.0: 2x the average low over the chosen timeframe and lookback period.

-2.5: 2.5x the average low over the chosen timeframe and lookback period.

-3.0: 3x the average low over the chosen timeframe and lookback period.

Look for price to find support or resistance at these levels for either entries or to take profit. When price crosses the +/- 2.0 or beyond, the likelihood of a reversal is very high, especially if set to weekly and monthly levels.

This indicator can be used/viewed on any timeframe. For intraday trading and viewing on a 15 minute or less timeframe, I recommend using the 4 hour, 1 day, and/or 1 week levels. For swing trading and viewing on a 30 minute or higher timeframe, I recommend using the 1 week, 1 month, or longer timeframes. I don’t believe this would be useful on a 1 hour or less timeframe, but let me know if the comments if you find otherwise.

Based on my testing, recommended lookback periods by timeframe include:

Timeframe: 4 hour; Lookback period: 60 (recommend viewing on a 5 minute or less timeframe)

Timeframe: 1 day; Lookback period: 10 (also check out 25 if your chart doesn’t show good support/resistance at 10 days lookback – I have found 25 to be useful on charts like SPX)

Timeframe: 1 week; Lookback period: 14

Timeframe: 1 month; Lookback period: 10

The line style and colors are all editable. You can apply a global coloring scheme in the event you want to add this indicator to your chart multiple times with different time frames like I do for the weekly and monthly.

I appreciate your comments/feedback on this indicator to improve. Also let me know if you find this useful, and what settings/ticker you find it works best with!

Also check out my profile for more indicators!

Kernel Regression ToolkitThis toolkit provides filters and extra functionality for non-repainting Nadaraya-Watson estimator implementations made by @jdehorty. For the sake of ease I have nicknamed it "kreg". Filters include a smoothing formula and zero lag formula. The purpose of this script is to help traders test, experiment and develop different regression lines. Regression lines are best used as trend lines and can be an invaluable asset for quickly locating first pullbacks and breaks of trends.

Other features include two J lines and a blend line. J lines are featured in tools like Stochastic KDJ. The formula uses the distance between K and D lines to make the J line. The blend line adds the ability to blend two lines together. This can be useful for several tasks including finding a center/median line between two lines or for blending in the characteristics of a different line. Default is set to 50 which is a 50% blend of the two lines. This can be increased and decreased to taste. This tool can be overlaid on the chart or on top of another indicator if you set the source. It can even be moved into its own window to create a unique oscillator based on whatever sources you feed it.

Below are the standard settings for the kernel estimation as documented by @jdehorty:

Lookback Window: The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars. Recommended range: 3-50