Realized Volatility (StdDev of Returns, %)Realized Volatility (StdDev of Returns, %)

This indicator measures realized (historical) volatility by calculating the standard deviation of log returns over a user-defined lookback period. It helps traders and analysts observe how much the price has varied in the past, expressed as a percentage.

How it works:

Computes close-to-close logarithmic returns.

Calculates the standard deviation of these returns over the selected lookback window.

Provides three volatility measures:

Daily Volatility (%): Standard deviation over the chosen period.

Annualized Volatility (%): Scaled using the square root of the number of trading days per year (default = 250).

Horizon Volatility (%): Scaled to a custom horizon (default = 5 days, useful for short-term views).

Inputs:

Lookback Period: Number of bars used for volatility calculation.

Trading Days per Year: Used for annualizing volatility.

Horizon (days): Adjusts volatility to a shorter or longer time frame.

Notes:

This is a statistical measure of past volatility, not a forecasting tool.

If you change the scale to logarithmic, the indicator readibility improves.

It should be used for analysis in combination with other tools and not as a standalone signal.

Volatilidade Histórica

Realized Volatility (StdDev of Returns, %)📌 Realized Volatility (StdDev of Returns, %)

This indicator measures realized volatility directly from price returns, instead of the common but misleading approach of calculating standard deviation around a moving average.

🔹 How it works:

Computes close-to-close log returns (the most common way volatility is measured in finance).

Calculates the standard deviation of these returns over a chosen lookback period (default = 200 bars).

Converts results into percentages for easier interpretation.

Provides three key volatility measures:

Daily Realized Vol (%) – raw standard deviation of returns.

Annualized Vol (%) – scaled by √250 trading days (market convention).

Horizon Vol (%) – volatility over a custom horizon (default = 5 days, i.e. weekly).

🔹 Why use this indicator?

Shows true realized volatility from historical returns.

More accurate than measuring deviation around a moving average.

Useful for traders analyzing risk, position sizing, and comparing realized vs implied volatility.

⚠️ Note:

It is best used on the Daily Chart!

By default, this uses log returns (which are additive and standard in quant finance).

If you prefer, you can easily switch to simple % returns in the code.

Volatility estimates depend on your chosen lookback length and may vary across timeframes.

Auto Fib V2Auto Fib V2 — Advanced Fibonacci Mapping Tool

Introduction

Auto Fib V2 is an advanced Fibonacci retracement indicator that automatically adapts to recent market ranges. Rather than manually drawing Fibonacci lines, this script dynamically maps them based on the most recent highs and lows, allowing traders to see the chart as if it were a "navigation map." Its primary purpose is to help identify potential buy and sell zones with greater clarity.

Key Concept

The script is built on a simple but powerful interpretation of Fibonacci retracement:

When the price moves below the 0.236 level, it suggests an oversold zone, where buyers may step in and market reversal potential increases.

When the price rises above the 0.764 level, it highlights an overbought zone, where sellers may become more active and risk of reversal grows.

Between these extremes, the Golden Pocket (0.382–0.618 zone) is highlighted as the area where institutional traders and algorithms often react. Historically, this is one of the most respected Fibonacci areas in technical analysis.

Features & Customization

Automatic Range Detection: The indicator automatically finds the recent high/low (based on user-defined lookback bars) and applies Fibonacci levels.

Flexible Direction Setting: Traders can use Auto Mode to let the script decide direction from price movement, or manually choose upward/downward mapping.

Multiple Levels Display: Beyond the standard levels, extra fractional retracements (0.146, 0.309, 0.441, etc.) are included for more precise mapping.

Golden Pocket Highlighting: Visually emphasizes the 0.382–0.618 retracement zone for quick recognition.

Custom Styles: Switch between line-based and dot-based plotting, with adjustable colors and transparency for improved readability.

Practical Use

Auto Fib V2 is not intended as a direct buy/sell signal generator, but as a contextual guide. Traders can use it to:

Confirm whether the current price area is closer to an overbought or oversold condition.

Combine it with oscillators (RSI, MACD) or trend indicators (EMA, ADX) to strengthen trading decisions.

Identify confluence zones where Fibonacci levels overlap with key supports/resistances.

Quickly adapt to market shifts without the need to redraw Fibonacci retracement lines repeatedly.

Why Use Auto Fib V2?

Manual Fibonacci drawing can be subjective, often depending on the swing points a trader chooses. Auto Fib V2 reduces that subjectivity by using consistent logic, creating a more systematic approach. For intraday traders, it provides rapid context to assess whether the market is stretched or balanced. For swing traders, it offers a map of reaction zones across higher timeframes.

Intelligent Trading SuiteIntelligent Trading Suite

“One script to rule them all.”

Overview

The Intelligent Trading Suite is a professional-grade decision system built in Pine Script. It is a unified engine—not a bundle of indicators—that combines adaptive pattern recognition, historical memory, and multi-context intelligence into one framework. Using a deep historical pattern database and integrating session dynamics, market calendars, holiday effects, and economic events, it filters noise and adapts to conditions. Core emphasis: precise pattern detection with target-price projection that remains stable as new candles print (mitigates target drift) and early detection of forming geometric patterns and divergences/hidden divergences.

Core Features

All-Timeframe Operation: Works across every TradingView timeframe—from 1m to 1W—without performance drift.

Pattern Recognition with Targets: Detects triangles, wedges, cup & handle, flags, and H&S; projects targets and stabilizes them against common drift as price evolves.

Early Signal Engine: Flags forming patterns and divergences before completion and notifies when prerequisites align.

Historical Pattern Intelligence: Stores and compares thousands of prior states (Hull, VWAP, RSI, MACD, SMA, CVD) to weight current conditions and calibrate confidence.

Context & Regime Awareness: Adjusts for volatility regimes, liquidity sessions, day-of-week bias, holidays, and macro events.

Unified Signal & Confidence: Fuses all streams into a single Overall signal with calibrated confidence levels (Weak / Neutral / Strong).

Visualization & Alerts

Compact Ultimate Intelligence Table showing each analytical pillar, plus the Overall signal, and an option to show them on the chart as well.

Alerts on table for: new pattern detection, divergence events, volatility shifts, and trend reversals.

Important Notes

-Free plan runtime: TradingView Free accounts may hit platform limits.

Fix: Open settings → switch Mode from Paid to Free → runs within Free limits.

-Heavy computation: The script is calculation- and data-intensive; initial runs can take time.

If a rare runtime error occurs, simply reload the page and continue.

Attributions

Hull Moving Average (Alan Hull)

VWAP (Volume Weighted Average Price)

RSI (Relative Strength Index, J. Welles Wilder Jr.)

MACD (Moving Average Convergence Divergence, Gerald Appel)

Black Flag ATR bands (Jose Azcarate)

Proprietary enhancements, target-stabilization logic, and the nuclear intelligence architecture are original research for this suite.

Compliance

Educational and analytical use only

No financial advice

Ad-free; aligned with TradingView House Rules

Proper attribution included

Access

To get access, please read the Author’s instructions on the script’s page.

Monthly Expected Move (IV + Realized)What it does

Overlays 1-month expected move bands on price using both forward-looking options data and backward-looking realized movement:

IV30 band — from your pasted 30-day implied vol (%)

Straddle band — from your pasted ATM ~30-DTE call+put total

HV band — from Historical Volatility computed on-chart

ATR band — from ATR% extrapolated to ~1 trading month

Use it to quickly answer: “How much could this stock move in ~1 month?” and “Is the market now pricing more/less movement than we’ve actually been getting?”

Inputs (quick)

Implied (forward-looking)

Use IV30 (%) — paste annualized IV30 from your options platform.

Use ATM 30-DTE Straddle — paste Call+Put total (per share) at the ATM strike, ~30 DTE.

Realized (backward-looking)

HV lookback (days) — default 21 (≈1 trading month).

ATR length — default 14.

Note: TradingView can’t fetch option data automatically. Paste the IV30 % or the straddle total you read from your broker (use Mark/mid prices).

How it’s calculated

IV band (±%) = IV30 × √(21/252) (annualized → ~1-month).

Straddle band (±%) = (ATM Call + Put) / Spot to that expiry (≈30 DTE).

HV band (±%) = stdev(log returns, N) × √252 × √(21/252).

ATR band (±%) = (ATR(len)/Close) × √21.

All bands are plotted as upper/lower envelopes around price, plus an on-chart readout of each ±% for quick scanning.

How to use it (at a glance)

IV/Straddle bands wider than HV/ATR → market expects bigger movement than recent actuals (possible catalyst/expansion).

All bands narrow → likely a low-mover; look elsewhere if you want action.

HV > IV → realized swings exceed current pricing (mean-reversion or vol bleed often follows).

Pro tips

For ATM straddle: pick the expiry closest to ~30 DTE, use the ATM strike (closest to spot), and add Call Mark + Put Mark (per share). If the exact ATM strike isn’t quoted, average the two neighboring strikes.

The simple straddle/spot heuristic can read slightly below the IV-derived 1σ; that’s normal.

Keep the chart on daily timeframe—the math assumes trading-day conventions (~252/yr, ~21/mo).

ATR Dynamische Candles 1.2 (by Droes)This script visualizes ATR values as candles to the right of the last candle at today's high and today's low.

ATR Daily Viz V30.0This script visualizes ATR values as candles to the right of the last candle at today's high and low.

This is the first version.

ATR Daily Viz V30.0This script visualizes ATR values as candles to the right of the last candle at today's high and low.

This is the first version.

Institutional HeatmapHeatmap Range - Volume Profile Visualization Indicator

What This Indicator Does

The Heatmap Range indicator provides a sophisticated volume profile visualization that displays price levels with the highest trading activity using color-coded heatmaps directly on your chart. Unlike traditional volume indicators, this tool shows WHERE the most significant trading occurred within specific price ranges over a customizable lookback period.

Advanced Volume Analysis

Volume-Weighted Price Levels: Calculates and displays up to 20 price levels based on actual trading volume

Customizable Time Period: Analyze volume distribution over 10-500 bars (default: 180 bars)

Smart Bin Sizing: Adjustable pip range (0.1-50 pips) for precise level identification

Peak Detection: Automatically identifies and centers display around highest volume areas

Visual Customization

3 Color Patterns:

Inverted Heat (Orange to Dark Red)

Inverted Cool (Orange to Dark Blue)

Inverted Purple (Light Pink to Dark Purple)

Transparency Control: 0-95% transparency for optimal chart readability

Adaptive Display: Shows most relevant levels centered around peak volume

Multi-Asset Support

Forex Pairs (EUR/USD, GBP/USD, etc.)

Precious Metals (Gold/XAUUSD, Silver/XAGUSD)

Futures (NQ, ES, YM, etc.)

Cryptocurrencies

Stock Indices

Customizable Parameters

Histogram Period (10-500, Default: 180) Bars to analyze for volume distribution

Bin Range (0.1-50 pips, Default: 5.0) Price range for each volume level

Color Pattern (1-3, Default: 1) Visual color scheme selection

Average Volume Period (10-200, Default: 100) Period for volume normalization

Max Display Levels (5-20, Default: 20) Maximum price levels to show

Transparency (0-95%, Default: 50%) Opacity of heatmap display

How to Use

For Day Traders

Identify key support/resistance levels based on actual volume

Spot high-probability reversal zones

Plan entries/exits around significant volume levels

For Swing Traders

Analyze longer-term volume distribution patterns

Identify major accumulation/distribution zones

Confirm breakout levels with volume validation

For Scalpers

Quick identification of intraday volume hotspots

Real-time volume level updates

Precise entry/exit timing around volume clusters

Visual Interpretation

Darker Colors: Higher volume concentration (stronger levels)

Lighter Colors: Lower volume concentration

Color Intensity: Directly correlates to volume strength at that price level

Level Positioning: Automatically centers around peak volume areas

Technical Specifications

Pine Script Version: v5

Chart Overlay: Yes

Max Bars Back: 1000

Performance Optimized: Limited to 200 bins for smooth operation

Real-time Updates: Dynamic calculation on each bar close

Getting Started

Add to Chart: Apply indicator to any supported timeframe

Adjust Period: Set histogram period based on your trading style

Choose Colors: Select color pattern that suits your chart theme

Fine-tune Levels: Adjust bin range and max levels for optimal display

Set Transparency: Balance visibility with chart clarity

Important Notes

Minimum Data Requirement: Needs at least 10 bars of history to function

Performance: Higher periods and smaller bin ranges require more processing

Volume Dependency: Most effective on instruments with consistent volume data

Timeframe Agnostic: Works on all timeframes from 1-minute to monthly

Status Information

The indicator includes a real-time information table showing:

Current settings (Period, Bin Range, Color Pattern, Transparency)

Indicator status (Active/Loading)

Disclaimer: This indicator is for educational and informational purposes only. Past performance does not guarantee future results. Always conduct your own analysis and risk management before making trading decisions.

Compatible with TradingView's Pine Script v5 | Optimized for all market conditions | Professional-grade volume analysis

Sudden MOVE Spikes Buy SignalThis Pine Script indicator, titled "Sudden MOVE Spikes Buy Signal", is designed for TradingView charts to identify potential buy opportunities in risk assets (e.g., BTC, stocks, or any charted symbol) based on spikes in the MOVE index (a measure of U.S. Treasury bond volatility, often called the "VIX for bonds"). It leverages the observation that sharp MOVE spikes above a threshold (indicating bond market stress or illiquidity) have historically preceded liquidity injections from the Fed or Treasury, leading to rallies in risk assets post-2020 (e.g.,

March 2020 COVID crash, October 2022 rate hike volatility, March 2023 banking crisis). The indicator filters out false positives, like the February 2022 geopolitical spike from the Russia-Ukraine invasion, using WTI crude oil price surges as a proxy.Key features:Signal Detection: Fires a "Buy" label when the daily MOVE index crosses above the threshold (default 130) with a sudden rate of change (ROC > 27% over 5 days), signaling potential liquidity-driven bottoms.

Geopolitical Filter: Excludes signals if oil ROC exceeds 20% over 5 days, to avoid non-macro events.

Time Restriction: Only shows signals from January 1, 2020, onward, as the strategy is tuned to the post-COVID regime.

Visuals: Plots a green "Buy" label below the bar on the chart and optionally highlights the bar with a green background (85% opacity) for emphasis.

Alerts: Supports alerts for new signals via TradingView's alert system.

The indicator is versatile and can be applied to any asset chart, though it's optimized for risk assets like cryptocurrencies or equities. Backtesting shows high hit rates for rallies in S&P 500 and BTC after valid signals, but it's a heuristic tool—combine with other analysis for trading decisions.

Synthetic VX3! & VX4! continuous /VX futuresTradingView is missing continuous 3rd and 4th month VIX (/VX) futures, so I decided to try to make a synthetic one that emulates what continuous maturity futures would look like. This is useful for backtesting/historical purposes as it enables traders to see how their further out VX contracts would've performed vs the front month contract.

The indicator pulls actual realtime data (if you subscribe to the CBOE data package) or 15 minute delayed data for the VIX spot (the actual non-tradeable VIX index), the continuous front month (VX1!), and the continuous second month (VX2!) continually rolled contracts. Then the indicator's script applies a formula to fairly closely estimate how 3rd and 4th month continuous contracts would've moved.

It uses an exponential mean‑reversion to a long‑run level formula using:

σ(T) = θ+(σ0−θ)e−kT

You can expect it to be off by ~5% or so (in times of backwardation it might be less accurate).

Adaptive Squeeze Momentum +Adaptive Squeeze Momentum+ (Auto-Timeframe Version)

Overview

Adaptive Squeeze Momentum+ is an enhanced volatility and momentum indicator designed to identify compression and expansion phases in price action. It is inspired by the classic Squeeze Momentum Indicator by LazyBear but introduces automatic parameter adaptation to any timeframe, making it simpler to use across different markets without manual configuration.

Concepts and Methodology

The script combines Bollinger Bands (BB) and Keltner Channels (KC) to detect periods when volatility contracts (squeeze) or expands (release).

A squeeze occurs when BB are inside KC, suggesting low volatility and potential breakout scenarios.

A squeeze release is detected when BB expand outside KC.

Momentum is derived using a linear regression applied to the difference between price and a midrange reference level.

Original Improvements

Compared to the original Squeeze Momentum Indicator, this version offers several enhancements:

Automatic Adaptation: BB and KC lengths and multipliers are dynamically adjusted based on the chart’s timeframe (from 1 minute up to 1 month), removing the need for manual tuning.

Simplified Visualization: A clean, minimalist histogram and clear squeeze state cross markers allow for faster interpretation.

Flexible Application: Designed to work consistently on intraday, daily, and higher timeframes across crypto, forex, stocks, and indices.

Features

Dynamic Squeeze Detection:

Gray Cross: Neutral (no squeeze detected)

Blue Cross: Active squeeze

Yellow Cross: Squeeze released

Momentum Histogram:

Positive/negative momentum shown with slope-based coloring.

Timeframe-Aware Parameters:

Automatically sets optimal BB/KC configurations.

Usage

Watch for blue crosses indicating an active squeeze phase that may precede a directional move.

Use the histogram color and slope to gauge momentum strength and direction.

Combine squeeze release signals with momentum confirmation for potential entries or exits.

Credits and Licensing

This script was inspired by LazyBear’s OLD “Squeeze Momentum Indicator” (). The implementation here significantly expands upon the original by introducing auto-adaptive parameters, restructured logic, and a new visualization approach. Published under the Mozilla Public License 2.0.

Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Use at your own risk.

THE HISTORY By [VXN]

THE HISTORY By - Monthly Seasonal Analysis Indicator

Development Status: This indicator is currently in the development phase and is not yet finished. Features and functionality may change as development continues.

Overview:

This indicator provides comprehensive historical analysis of monthly price patterns, designed to help traders identify recurring seasonal behaviors and market tendencies for the current month across multiple years of data.

Key Features:

Historical Data Analysis:

- Analyzes up to 10 years of historical performance for the current month

- Calculates monthly returns, win rates, and statistical metrics

- Tracks maximum drawdowns and runups for risk assessment

- Requires daily timeframe for accurate monthly calculations

Pattern Recognition:

- Implements a three-period classification system that breaks each month into segments

- Uses visual indicators (🟢🔴🟡) to represent bullish, bearish, and neutral periods

- Helps identify recurring intra-month behavior patterns

Statistical Display:

- Presents historical data in an organized table format

- Shows year-by-year performance comparisons

- Calculates average returns, best/worst performance, and confidence levels

- Displays overall market bias (bullish/bearish tendency) for the current month

Dynamic Zone Overlays:

- Projects Fibonacci-based support/resistance levels based on historical volatility

- Adjusts zone positioning based on the month's historical bias

- Provides visual reference points for potential price targets or reversal areas

Practical Applications:

- Seasonal trading strategy development

- Risk management through historical context

- Understanding market cyclicality and recurring patterns

- Educational tool for studying price behavior over time

Note: This indicator is designed for analysis and education purposes, helping traders understand historical market patterns rather than providing direct trading signals. The data should be used in conjunction with other forms of analysis and proper risk management. As this is still under development, please expect updates and refinements to functionality.

volatility-adjusted breakout envelopethis indicator is designed to help traders visually identify potential entry and exit points based on volatility-adjusted price thresholds. it works by calculating a dynamic expected price move around the previous close using historical volatility data smoothed by exponential moving averages to reduce noise and present a clear range boundary on the chart.

the indicator first computes the logarithmic returns over a user-defined lookback period and calculates the standard deviation of these returns, which represents raw volatility. it annualizes this volatility according to the chart timeframe selected, then uses it to estimate an expected price movement for the current timeframe. this expected move is smoothed to avoid sudden spikes or drops that could cause confusing signals.

using this expected move, the indicator generates two key threshold lines: an upper threshold and a lower threshold. these lines create a volatility-based range around the smoothed previous close price. the thresholds themselves are further smoothed with exponential moving averages to produce smooth, easy-to-interpret lines that adapt to changing market conditions without being choppy.

the core trading signals are generated when the price closes outside of these smoothed threshold ranges. specifically, a long entry signal is indicated when the price closes above the upper threshold for the first time, signaling potential upward momentum beyond normal volatility expectations. a short entry signal occurs when the price closes below the lower threshold for the first time, indicating potential downward momentum.

once an entry signal is triggered, the indicator waits for the price to close back inside the threshold range before signaling an exit. when this occurs, an exit marker is displayed to indicate that the price has returned within normal volatility bounds, which may suggest that the previous trend is losing strength or the breakout has ended.

these signals are visually represented on the chart using small shapes: triangles pointing upwards mark the initial long entries, triangles pointing downwards mark short entries, and x shapes mark the exits for both long and short positions. the colors of these shapes are customizable to suit user preferences.

to use this indicator effectively, traders should watch for the first close outside the smoothed volatility range to consider entering a position in the breakout direction. the exit signals help identify when price action reverts back into the expected range, which can be used to close or reduce the position. this method emphasizes trading breakouts supported by statistically significant moves relative to recent volatility while providing a clear exit discipline.

this indicator is best applied to intraday or daily charts with consistent volatility and volume characteristics. users should adjust the volatility lookback period, smoothing factor, and trading session times to match their specific market and trading style. because it relies on price volatility rather than fixed price levels, it can adapt to changing market conditions but should be combined with other analysis tools and proper risk management.

overall, this indicator provides a smoothed, dynamic volatility envelope with clear visual entry and exit cues based on first closes outside and back inside these envelopes, making it a helpful assistant for manual traders seeking to capture statistically significant breakouts while maintaining disciplined exits.

VWAP Deviation Channels with Probability (Lite)VWAP Deviation Channels with Probability (Lite)

Version 1.2

Overview

This indicator is a powerful tool for intraday traders, designed to identify high-probability areas of support and resistance. It plots the Volume-Weighted Average Price (VWAP) as a central "value" line and then draws statistically-based deviation channels around it.

Its unique feature is a dynamic probability engine that analyzes thousands of historical price bars to calculate and display the real-time likelihood of the price touching each of these deviation levels. This provides a quantifiable edge for making trading decisions.

Core Concepts Explained

This indicator is built on three key concepts:

The VWAP (Volume-Weighted Average Price): The dotted midline of the channels is the session VWAP. Unlike a Simple Moving Average (SMA) which only considers price, the VWAP incorporates volume into its calculation. This makes it a much more significant benchmark, as it represents the true average price where the most business has been transacted during the day. It's heavily used by institutional traders, which is why price often reacts strongly to it.

Standard Deviation Channels: The channels above and below the VWAP are based on standard deviations. Standard deviation is a statistical measure of volatility.

- Wide Bands: When the channels are wide, it signifies high volatility.

- Narrow Bands: When the channels are tight and narrow, it signifies low volatility and

consolidation (a "squeeze").

The Conditional Probability Engine: This is the heart of the indicator. For every deviation level, the script displays a percentage. This percentage answers a very specific question:

"Based on thousands of previous bars, when the last candle had a certain momentum (bullish or bearish), what was the historical probability that the price would touch this specific level?"

The probabilities are calculated separately depending on whether the previous candle was green (bullish) or red (bearish). This provides a nuanced, momentum-based edge. The level with the highest probability is highlighted, acting as a "price magnet."

How to Use This Indicator

Recommended Timeframes:

This indicator is designed specifically for intraday trading. It works best on timeframes like the 1-minute, 5-minute, and 15-minute charts. It will not display correctly on daily or higher timeframes.

Recommended Trading Strategy: Mean Reversion

The primary strategy for this indicator is "Mean Reversion." The core idea is that as the price stretches to extreme levels far away from the VWAP (the "mean"), it is statistically more likely to "snap back" toward it.

Here is a step-by-step guide to trading this setup:

1. Identify the Extreme: Wait for the price to push into one of the outer deviation bands (e.g., the -2, -3, or -4 bands for a buy setup, or the +2, +3, or +4 bands for a sell setup).

2. Look for the High-Probability Zone: Pay close attention to the highlighted probability label. This is the level that has historically acted as the strongest magnet for price. A touch of this level represents a high-probability area for a potential reversal.

3. Wait for Confirmation: Do not enter a trade just because the price has touched a band. Wait for a confirmation candle that shows momentum is shifting.

- For a Buy: Look for a strong bullish candle (e.g., a green engulfing candle or a hammer/pin

bar) to form at the lower bands.

- For a Sell: Look for a strong bearish candle (e.g., a red engulfing candle or a shooting star)

to form at the upper bands.

Define Your Exit:

- Take Profit: A logical primary target for a mean reversion trade is the VWAP (midLine).

- Stop Loss: A logical place for a stop-loss is just outside the next deviation band. For

example, if you enter a long trade at the -3 band, your stop loss could be placed just

below the -4 band.

Disclaimer: This indicator is a tool for analysis and should not be considered a standalone trading system. Trading involves significant risk, and past performance is not indicative of future results. Always use this indicator in conjunction with other forms of analysis and sound risk management practices.

ATR Screener with Labels and ShapesWeekly Daily ATR Pine Scanner

To find out tightness or contraction in a stock we needs to check if volatality is decreasing as well as compared to previous 14 or 10 bars volatility . we check this for weekly and then for Daily , so that we can enter in a stock which is tightest in recent times.

Condition is :

1. Weekly Candle ATR x 0.8 < 10 Week ATR

2. Daily Candle ATR x 0.6 < 14 Day ATR

When both of the conditions are met then they signifies that the stock has tightened in weekly and daily aswell . so now we can find ways to enter during max squeeze.

How to scan in Pine Scanner ?

FIrst add indicator as favourite and Go to pine scanner page in trading view and then scan your watchlist and there you will see 3 columns 1 with only Weekly conditions met , 2 with only Daily and 3rd with Both conditions met .

Select stocks and move to new watchlist and now you have those stocks which has contracted the most in recent times .

Volatility Barometer (VB)Volatility Barometer (VB)

The Volatility Barometer (VB) is a comprehensive market sentiment indicator designed to measure aggregate stress and fear in the equity market. It consolidates three critical volatility metrics into a single, easy-to-interpret score, providing a broader view of market conditions than any single metric alone.

Core Components

The barometer synthesizes information from:

VIX Index (VIX): The standard measure of implied 30-day stock market volatility.

VVIX Index (VVIX): The volatility of the VIX itself, often seen as the "volatility of volatility." High VVIX readings can signal uncertainty about the VIX's future path.

VIX Futures Term Structure (VX1!−VX2!): The spread between the front-month and second-month VIX futures. A positive spread (contango) is typical, while a negative spread (backwardation) often signals imminent market stress.

How It Works

To create a unified view, the indicator normalizes each of these three components using a Z-score. The Z-score measures how many standard deviations a value is from its historical mean over a user-defined period (defaulting to 252 days, or one trading year).

These three standardized Z-scores are then combined into a final VB Score using a weighted average. Users can customize these weights in the indicator's settings to emphasize the components they find most important.

How to Interpret

The VB Score is plotted as a single line that oscillates around a zero level, with its color changing to reflect the prevailing market regime:

High Stress (Red Line): When the score rises above the "High stress threshold" (default: 1.5), it indicates heightened market fear and risk-off sentiment. This is a period of significant stress, often associated with market downturns.

Low Stress (Green Line): When the score falls below the "Low stress threshold" (default: -1.0), it signals complacency and low perceived risk in the market. Extreme low readings can sometimes precede volatility spikes.

Neutral (Blue Line): Scores between the high and low thresholds represent normal market conditions.

By providing a weighted, multi-faceted view of volatility, the Volatility Barometer helps traders and investors identify market regimes, confirm trading biases, and anticipate potential shifts in market sentiment.

Improved Historical Volatility Calculator (No Options)Improved Historical Volatility Calculator (No Options)

Description

The "Improved Historical Volatility Calculator (No Options)" is a Pine Script indicator designed to calculate the historical volatility (HV) of assets without relying on options data. This tool is particularly useful for markets like forex, indices, or stocks where options trading might be limited or unavailable. It provides a customizable way to measure volatility based on historical price movements, with options to adjust the calculation period, trading days per year, and use an exponentially weighted moving average (EWMA) for enhanced sensitivity to recent data.

This indicator can be used standalone to visualize volatility trends or integrated with other scripts (e.g., option pricing models) to provide a manual input for implied volatility (IV).

Features

Customizable Period: Adjust the number of days (5 to 365) for volatility calculation.

Flexible Annualization: Set the number of trading days per year (default 252) to suit different markets (e.g., 365 for forex).

EWMA Option: Toggle between standard deviation and EWMA for a more responsive volatility measure.

Trend Adjustment: Removes the influence of price trends using an EMA-based detrending method.

Visual Output: Displays volatility as a histogram and labels the latest value on the chart.

How to Use

Add the Indicator: Load the indicator onto your chart via the Pine Script editor or the Indicators menu.

Configure Settings:

Period for Calculation: Set the lookback period (e.g., 30 days) to calculate volatility.

Trading Days per Year: Adjust for your market (e.g., 252 for stocks, 365 for continuous markets).

Use EWMA: Enable for a weighted approach focusing on recent volatility.

Interpret the Results: The histogram shows volatility in decimal form (e.g., 0.03136 = 3.136%), and the label displays the percentage on the last bar.

Integration: Use the calculated volatility value (in decimal form) as a manual IV input in other scripts, such as option pricing models.

Example

For the DXY index, with a 60-day period and 252 trading days per year, the indicator might output a volatility of 0.03136 (3.136%). You can input this value into an options model to estimate standard deviation levels, adjusting for the days to expiry.

Notes

Accuracy: The indicator provides a reliable estimate of historical volatility, with improvements like trend removal and EWMA. For precision, use a period that matches your trading horizon (e.g., 30-90 days).

Limitations: Volatility is based on historical data and may not reflect future market conditions or implied volatility from options.

Compatibility: Tested on TradingView as of June 16, 2025. Ensure sufficient historical data is available for the chosen period.

Suggestions

Increase the period for volatile assets to smooth out noise.

Share feedback or request enhancements in the comments!

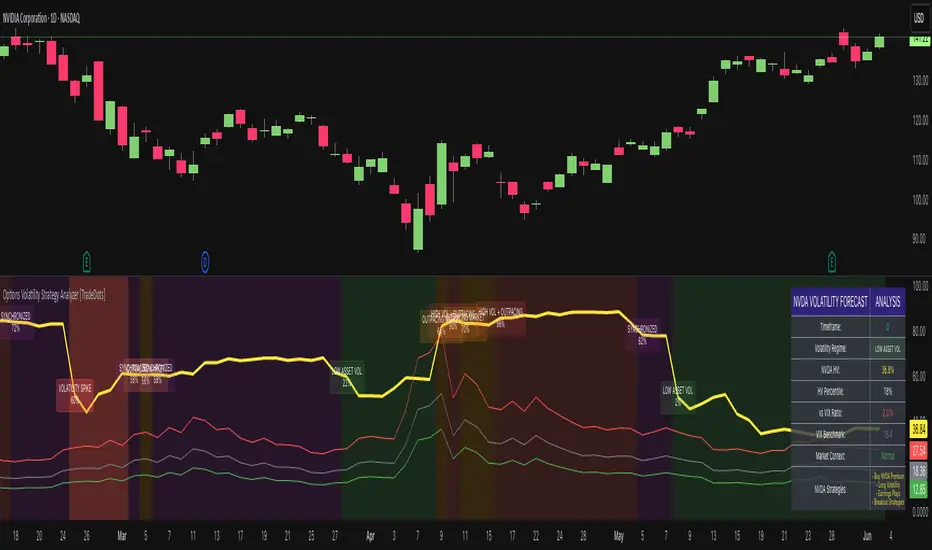

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Support and Resistance Profile with Volatility ClusteringThe indicator begins by looking at recent volatility behavior in the market: it measures the average true range over your chosen “Length” and compares it to the average true range over ten times that period. When volatility over the short window is high relative to longer-term volatility, we mark that period as a “cluster.” As price moves through these clusters—whether in a quiet period or a sudden burst of activity—the script isolates each cluster and examines the sequence of closing prices within it.

Within every cluster, the algorithm next finds the points along the price path that matter most to a human eye, smoothing out minor wobbles and highlighting the peaks and valleys that define the cluster’s shape. It does this by drawing a straight line between the beginning and end of the cluster, then repeatedly snapping the single point that deviates most from that line back onto it and re-interpolating, until it has identified a fixed number of perceptually important points. Those points capture where price really turned or accelerated, stripping away noise so that you see the genuine memory-markers in each volatility episode.

Each of those important points inherits a “weight” based on the cluster’s normalized volatility—essentially how large the average true range in that cluster was relative to its average close. Over your “Main Length for Profile” window, every time one of these weighted points occurs at a particular price level, it adds to a running total in that level’s bin. At the end of the window you see a silhouette of boxes extending to the right of the chart: where boxes are wide, many important points (with high volatility weight) have happened there in the past; where boxes are thin or absent, price memory is light.

For a trader, the value of this profile lies in spotting zones where the market has repeatedly “remembered” price extremes during volatile episodes—those are areas where support or resistance is likely to be strongest. Conversely, gaps in the profile—price levels with little weighted history—suggest frictionless zones. If price enters such a gap, it may move swiftly until it encounters another region of heavy memory. You can use this in several ways: as a filter on breakouts and breakdowns (only trade through a gap when you see sufficient momentum), as a guide for scaling into positions (add when price enters a low-memory zone and tighten stops where memory boxes thicken), or to anticipate where price might pause or reverse (when it reaches a band of wide boxes). By turning raw volatility clusters into a human-readable map of price memory, this tool helps you see at a glance where the market is likely to push or pause—and plan entries, exits, and risk targets accordingly.

Statistical Reliability Index (SRI)Statistical Reliability Index (SRI)

The Statistical Reliability Index (SRI) is a professional financial analysis tool designed to assess the statistical stability and reliability of market conditions. It combines advanced statistical methods to gauge whether current market trends are statistically consistent or prone to erratic behavior. This allows traders to make more informed decisions when navigating trending and choppy markets.

Key Concepts:

1. Extrapolation of Cumulative Distribution Functions (CDF)

What is CDF?

A Cumulative Distribution Function (CDF) is a statistical tool that models the probability of a random variable falling below a certain value.

How it’s used in SRI:

The SRI utilizes the 95th percentile CDF of recent returns to estimate the likelihood of extreme price movements. This helps identify when a market is experiencing statistically significant changes, crucial for forecasting potential breakouts or breakdowns.

Weight in SRI:

The weight of the CDF extrapolation can be adjusted to emphasize its impact on the overall reliability index, allowing customization based on the trader's preference for tail risk analysis.

2. Bias Factor (BF)

What is the Bias Factor?

The Bias Factor measures the ratio of the current market price to the expected mean price calculated over a defined period. It represents the deviation from the typical price level.

How it’s used in SRI:

A higher bias factor indicates that the current price significantly deviates from the historical average, suggesting a potential mean reversion or trend exhaustion.

Weight in SRI:

Adjusting the Bias Factor weight lets users control how much this deviation influences the SRI, balancing between momentum trading and mean reversion strategies.

3. Coefficient of Variation (CV)

What is CV?

The Coefficient of Variation (CV) is a statistical measure that expresses the ratio of the standard deviation to the mean. It indicates the relative variability of asset returns, helping gauge the risk-to-return consistency.

How it’s used in SRI:

A lower CV indicates more stable and predictable price behavior, while a higher CV signals increased volatility. The SRI incorporates the inverse of the normalized CV to reflect price stability positively.

Weight in SRI:

By adjusting the CV weight, users can prioritize consistent price movements over erratic volatility, aligning the indicator with risk tolerance and strategy preferences.

Interpreting the SRI:

1. SRI Plot:

The SRI plot dynamically changes color to reflect market conditions:

Aqua Line: Indicates uptrend stability, signaling statistically consistent upward movements.

Fuchsia Line: Indicates downtrend stability, where statistically reliable downward movements are present.

The overlay background shifts between colors:

Aqua Background: Signifies statistical stability, where trends are historically consistent.

Fuchsia Background: Indicates statistical instability, often associated with trend uncertainty.

Yellow Background: Marks choppy periods, where statistical data suggests that market conditions are not conducive to reliable trading.

2. SRI Volatility Plot:

Displays the volatility of the SRI itself to detect when the indicator is stable or unstable:

Blue Area Fill: Signifies that the SRI is stable, indicating trending conditions.

Yellow Area Fill: Represents choppy or unstable SRI movements, suggesting sideways or unreliable market conditions.

A Chop Threshold Line (dotted yellow) highlights the maximum acceptable SRI volatility before the market is considered too unpredictable.

3. Stability Assessment:

Stable Trend (No Chop):

The SRI is smooth and consistent, often accompanied by aqua or fuchsia lines.

Volatility remains below the chop threshold, indicating a low-risk, trend-following environment.

Chop Mode:

The SRI becomes erratic, and the volatility plot spikes above the threshold.

Marked by a yellow shaded background, indicating uncertain and non-trending conditions.

[Trend Identification:

Use the color-coded SRI line and background to determine uptrend or downtrend reliability.

Be cautious when the SRI volatility plot shows yellow, as this signals trading conditions may not be reliable.

Practical Use Cases:

Trend Confirmation:

Utilize the SRI plot color and background to confirm whether a detected trend is statistically reliable.

Chop Mode Filtering:

During yellow chop periods, it is advisable to reduce trading activity or adopt range-bound strategies.

Strategy Filter:

Combine the SRI with trend-following indicators (like moving averages) to enhance entry and exit accuracy.

Volatility Monitoring:

Pay attention to the SRI volatility plot, as spikes often precede erratic price movements or trend reversals.

Disclaimer:

The Statistical Reliability Index (SRI) is a technical analysis tool designed to aid in market stability assessment and trend validation. It is not intended as a standalone trading signal generator. While the SRI can help identify statistically reliable trends, it is essential to incorporate additional technical and fundamental analysis to make well-informed trading decisions.

Trading and investing involve substantial risk, and past performance does not guarantee future results. Always use risk management practices and consult with a financial advisor to tailor strategies to your individual risk profile and objectives.

Daily Price RangeThe indicator is designed to analyze an instrument’s volatility based on daily extremes (High-Low) and to compare the current day’s range with the typical (median) range over a selected period. This helps traders assess how much of the "usual" daily movement has already occurred and how much may still be possible during the trading day.

[NIC] Volatility Anomaly Indicator (Inspired by Jeff Augen)Volatility Anomaly Indicator (Inspired by Jeff Augen)

The Volatility Anomaly Indicator, inspired by Jeff Augen’s The Volatility Edge in Options Trading, helps traders spot price distortions by analyzing volatility imbalances. It compares short-term (10-day) and long-term (30-day) historical volatility (HV), plotting the ratio in a subgraph with clusters of dots to highlight anomalies—red for volatility spikes (potential sells) and green for calm periods (potential buys).

Originality: This indicator uniquely adapts Augen’s volatility concepts into a visual tool, focusing on relative volatility distortions rather than absolute levels, making it ideal for volatile assets like $TQQQ.

Features:

Calculates the ratio of short-term to long-term volatility.

Detects spikes (ratio > 1.5) and calm periods (ratio < 0.67) with customizable thresholds.

Plots volatility ratio as a blue line, with red/green dots for anomalies.

Includes optional buy/sell signals on the main chart (if overlay is enabled).

How It Works

The indicator computes historical volatility using log returns, then calculates the short-term to long-term volatility ratio. Spikes and calm periods are marked with dots in the subgraph, and threshold lines (1.5 and 0.67) provide context. Buy signals (green triangles) trigger during calm periods, and sell signals (red triangles) during spikes.

How to Use

Apply to any chart (e.g., NASDAQ:TQQQ daily).

Adjust inputs: Short Volatility Period (10), Long Volatility Period (30), Volatility Spike Threshold (1.5).

Watch for red dot clusters (spikes, potential sells) and green dot clusters (calm, potential buys).

Combine with price action or RSI for confirmation.

Why Use This Indicator?

Focuses on volatility-driven price inefficiencies.

Clear visualization with dot clusters.

Customizable for different assets and timeframes.

Limitations

Not a standalone system; requires confirmation.

May give false signals in choppy markets.