Tremor Tracker [theUltimator5]Tremor Tracker is a volatility monitoring tool that visualizes the "tremors" of price action by measuring and analyzing the average volatility of the current trading range, working on any timeframe. This indicator is designed to help traders detect when the market is calm, when volatility is building, and when it enters a potentially unstable or explosive state by using a lookback period to determine the average volatility and highlights outliers.

🔍 What It Does

Calculates bar-level volatility as the percentage difference between the high and low of each candle.

Applies a user-selected moving average (SMA, EMA, or WMA) to smooth out short-term noise and highlight trends in volatility.

Compares current volatility to its long-term average over a configurable lookback period.

Dynamically colors each volatility bar based on how extreme it is relative to historical behavior:

🟢 Lime — Low volatility (subdued, ranging conditions)

🟡 Yellow — Moderate or building volatility

🟣 Fuchsia — Elevated or explosive volatility

⚙️ Customizable Settings

Low Volatility Limit and High Volatility Limit: Define the thresholds for color changes based on volatility's ratio to its average.

Volatility MA Length: Adjust the smoothing period for the volatility moving average.

Average Volatility Lookback: Set how many bars are used to calculate the long-term average.

MA Type: Choose between SMA, EMA, or WMA for smoothing.

Show Volatility MA Line?: Toggle the display of the smoothed volatility trendline.

Show Raw Volatility Bars?: Toggle the display of raw per-bar volatility with dynamic coloring.

🧠 Use Cases

Identify breakout conditions: When volatility spikes above average, it may signal the onset of a new trend or a news-driven breakout.

Avoid chop zones: Prolonged periods of low volatility often precede sharp moves — a classic “calm before the storm” setup.

Timing reversion trades: Detect overextended conditions when volatility is well above historical norms.

Adapt strategies by volatility regime: Use color feedback to adjust risk, position sizing, or strategy selection based on real-time conditions.

📌 Notes

Volatility is expressed as a percentage, making this indicator suitable for use across different timeframes and asset classes.

The tool is designed to be visually intuitive, so traders can quickly spot evolving volatility states without diving into raw numbers.

Volatilidade Histórica

STDZ - Global Trading Sessions📊 STDZ - Global Trading Sessions (GTS)

STDZ - Global Trading Sessions (GTS) is an indicator that overlays global market session data directly on your intraday charts. It visualizes trading sessions from different time zones, helping intraday traders quickly assess volatility, session ranges, and structural market behavior across global financial centers. The default setting is enough to cover all the major stock markets opening time including:

• Asia: Sydney, Tokyo, Hong Kong

• Europe: Frankfurt, London

• North America: New York

⸻

🚀 Features

• 🔹 Session Visualization: Up to 3 configurable trading sessions with customizable:

• Session time windows

• Time zones (IANA or GMT format)

• Colors

• Session labels

• 🔹 Session Metrics:

• Open, High, Low, and Average lines

• Session range measurement

• 🔹 Statistics Table:

• Live display of each session’s range

• Daily and Weekly True Range / ATR

• 🔹 Session Open Highlights: Vertical lines for weekly changes to contextualize price action

• 🔹 Dynamic Chart Objects: Lines, boxes, and labels update in real time as sessions progress

• 🔹 🕒 Timezone-aware session rendering (supports daylight saving)

ATR % Oscillator - DolphinTradeBot1️⃣ Overview

🔸 This is a simplified version of ATR and TR that shows volatility as percentage changes , making it easier to compare two symbols.

🔸 The indicator compares the volatility of two different assets by calculating the percentage-based price ranges and their moving averages .

📌 This is especially useful for pair traders, as it helps identify which symbol is more volatile, allowing for strategic decisions based on relative movement rather than overall market direction.

2️⃣ How Is It Work?

🔸 For each symbol, it calculates the absolute percentage difference between either:

• Close and Open (net price change), or

• High and Low (daily price range).

🔸 The results are visualized as column bars — the taller the bar, the higher the volatility.

🔸 It also plots a moving average line (SMA) based on the selected range length.

📌 These calculations are independent of the chart you're on — they work purely based on the two selected symbols.

If no symbols are selected, it defaults to using the current chart's symbol.

3️⃣ How to Use It?

With this indicator, you can:

🔸 Compare the volatility between two assets.

🔸 Detect sudden volatility spikes that may signal upcoming momentum.

🔸 Support spread, arbitrage, or correlation-based strategies .

🔸 See which symbol is gaining market attention (a larger difference = more activity).

Example: Compare BTC vs ETH to see which one is dominating in terms of price action or volatility.

4️⃣⚙️ Settings

🔸 Symbol Settings

• Symbol-1 / Symbol-2: Choose the two assets to compare.

• Checkboxes: Enable/disable visibility for each symbol's data.

🔸 Calculation Settings

• Range Average: The number of bars used for the moving average.

• Calculation Source:

- Close-Open: Measures net price movement.

- High-Low: Measures total price range.

(US) Historical Trade WarsHistorical U.S. Trade Wars Indicator

Overview

This indicator visualizes major U.S. trade wars and disputes throughout modern economic history, from the McKinley Tariff of 1890 to recent U.S.-China tensions. This U.S.-focused timeline is perfect for macro traders, economic historians, and anyone looking to understand how America's trade conflicts correlate with market movements.

Features

Comprehensive U.S. Timeline: Covers 130+ years of U.S.-centered trade disputes with historically accurate dates.

Color-Coded Events:

🔴 Red: Marks the beginning of a U.S. trade war or major dispute.

🟡 Yellow: Highlights significant events within a trade conflict.

🟢 Green: Shows resolutions or ends of trade disputes.

Global Partners/Rivals: Tracks U.S. trade relations with China, Japan, EU, Canada, Mexico, Brazil, Argentina, and others.

Country Flags: Uses emoji flags for easy visual identification of nations in trade relations with the U.S.

Major Trade Wars Covered:

McKinley Tariff (1890-1894)

Smoot-Hawley Tariff Act (1930-1934)

U.S.-Europe Chicken War (1962-1974)

Multifiber Arrangement Quotas (1974-2005)

Japan-U.S. Trade Disputes (1981-1989)

NAFTA and Softwood Lumber Disputes

Clinton and Bush-Era Steel Tariffs

Obama-Era China Tire Tariffs

Rare Earth Minerals Dispute (2012-2014)

Solar Panel Dispute (2012-2015)

TPP and TTIP Negotiations

U.S.-China Trade War (2018-present)

Airbus-Boeing Dispute

Usage

Analyze how markets historically responded to trade war initiations and resolutions.

Identify patterns in market behavior during periods of trade tensions.

Use as an overlay with price action to examine correlations.

Perfect companion for macro analysis on daily, weekly, or monthly charts.

About

This indicator is designed as a historical reference tool for traders and economic analysts focusing on U.S. trade policy and its global impact. The dates and events have been thoroughly researched for accuracy. Each label includes emojis to indicate the U.S. and its trade partners/rivals, making it easy to track America's evolving trade relationships across time.

Note: This indicator works best on larger timeframes (daily, weekly, monthly) due to the historical span covered.

Open Range Volatility (High/Low %)Overview

The Open-to-High/Low Movement Indicator helps traders visualize the percentage change between the opening price and the highest & lowest points of each trading session. This indicator is particularly useful for identifying intraday volatility, momentum strength, and potential reversals.

Key Features

✅ Real-Time High/Low Percentage Movement – Calculates and plots the percentage movement from the opening price to both the session high (green line) and session low (red line).

✅ Separate Chart Pane – Keeps your main price chart clean while displaying movements in a separate panel.

✅ Zero Reference Line – Helps distinguish upward and downward movements.

✅ +10% and -10% Threshold Lines – Assists in identifying significant price swings.

✅ Customizable & Lightweight – Efficiently tracks market movements without slowing down your chart.

How to Use

When the green line moves higher, it indicates strong buying pressure after the open.

When the red line moves lower, it shows selling pressure from the open price.

If movements stay within a small range, the market is experiencing low volatility.

Extreme movements beyond ±10% can indicate potential breakout or reversal zones.

Best for:

📈 Day traders tracking intraday momentum

📊 Swing traders spotting volatility trends

⚡ Scalpers identifying quick price movements

💡 Volatility-based strategies

This indicator works across all timeframes and asset classes, including stocks, forex, commodities, and crypto.

🚀 Add this to your chart today and stay ahead of the market!

PumpC Opening Range Breakout (ORB) Stretch RangePumpC ORB Stretch

The PumpC ORB Stretch is a volatility-based indicator that helps traders identify potential breakout zones by analyzing how price typically behaves around the open. This tool is inspired by concepts introduced by Toby Crabel in his well-known book “Day Trading with Short-Term Price Patterns and Opening Range Breakout.”

Rather than predicting market direction, this indicator highlights areas where price is likely to expand based on recent volatility. It is designed for traders who prefer dynamic, data-driven breakout levels over static support and resistance zones.

What Is the "Stretch"?

In Toby Crabel’s framework, the Stretch is the average of the smaller of two price moves:

The distance from the open to the high of the bar

The distance from the open to the low of the bar

This smaller value captures the “quiet side” of the candle and reflects recent price compression. Averaged over multiple periods (commonly 10 daily bars), it creates a baseline to assess how far price may move away from the open under typical market conditions.

How the Indicator Works

The PumpC ORB Stretch follows this process:

Uses a higher timeframe (such as daily) to calculate the open, high, and low.

For each bar, measures the smaller of the two distances: open to high or open to low.

Applies a moving average to the result over a user-defined number of bars (default is 10).

Multiplies the average stretch by customizable levels (e.g., 0.382, 1.0, 2.0).

Plots breakout levels above and below the open of the selected timeframe.

The result is a set of adaptive levels that expand or contract with market volatility.

Customization Options

Stretch Timeframe: Choose the timeframe used for stretch calculation (default: Daily).

Stretch Length: Set the number of bars to include in the moving average.

Breakout Levels: Enable or disable individual levels and define multipliers.

Color Settings: Customize colors for each range level for easy visual distinction.

Plot Style: Circular markers are used to reduce chart clutter and improve readability.

How to Use It

Use plotted levels to anticipate possible breakouts from the open.

Adjust stretch length to reflect short-term or longer-term volatility trends.

Combine this tool with momentum indicators, volume, or price action for confirmation.

Use levels to help guide stop placement or profit targets in breakout strategies.

Important Notes

This script is based on an interpretation of Crabel’s concepts and is not affiliated with Crabel Capital or the original author.

The indicator does not predict direction; it is a tool for context and structure.

It is recommended that users test and validate this tool in a simulated environment before applying it to live trading.

This indicator is intended for educational purposes only.

Licensing and Attribution

This script is built entirely in Pine Script v5 and follows TradingView’s open-source standards. It does not include any third-party or proprietary code. If you modify or share it, please credit the original idea and follow all TradingView script publishing rules.

Hourly Volatility Explorer📊 Hourly Volatility Explorer: Master The Market's Pulse

Unlock the hidden rhythms of price action with this sophisticated volatility analysis tool. The Hourly Volatility Explorer reveals the most potent trading hours across multiple time zones, giving you a strategic edge in timing your trades.

🌟 Key Features:

⏰ Multi-Timezone Analysis

• GMT (UTC+0)

• EST (UTC-5) - New York

• BST (UTC+1) - London

• JST (UTC+9) - Tokyo

• AEST (UTC+10) - Sydney

Perfect for tracking major market sessions and their overlaps!

📈 Dynamic Visualization

• Color-gradient hourly bars for instant pattern recognition

• Real-time volatility comparison

• Interactive data table with comprehensive statistics

• Automatic highlighting of peak volatility periods

🎯 Strategic Applications:

Day Trading:

• Identify optimal trading windows

• Avoid low-liquidity periods

• Capitalize on session overlaps

• Fine-tune entry/exit timing

Risk Management:

• Set appropriate stop losses based on hourly volatility

• Adjust position sizes for different market hours

• Optimize risk-reward ratios

• Plan around high-impact hours

Global Market Analysis:

• Track volatility across all major sessions

• Spot institutional trading patterns

• Identify quiet vs. active periods

• Monitor 24/7 market dynamics

💡 Perfect For:

• Forex traders navigating global sessions

• Crypto traders in 24/7 markets

• Day traders optimizing execution times

• Algorithmic traders fine-tuning strategies

• Risk managers calibrating exposure

📊 Advanced Features:

• Rolling 3-month analysis for reliable patterns

• Precise pip movement calculations

• Sample size tracking for statistical validity

• Real-time current hour comparison

• Color-coded visual system for instant insights

⚡ Pro Trading Tips:

• Use during major session overlaps for maximum opportunity

• Compare patterns across different instruments

• Combine with volume analysis for deeper insights

• Track seasonal variations in hourly patterns

• Build trading schedules around peak hours

🎓 Educational Value:

• Understand market microstructure

• Learn global market dynamics

• Master timezone relationships

• Develop timing intuition

🛠️ Customization:

• Adjustable lookback period

• Flexible pip multiplier

• Multiple timezone options

• Visual preference settings

Whether you're scalping the 1-minute chart or managing longer-term positions, the Hourly Volatility Explorer provides the precise timing intelligence needed for today's global markets.

Transform your trading schedule from guesswork to science. Know exactly when markets move, why they move, and how to position yourself for maximum opportunity.

#TechnicalAnalysis #Trading #Volatility #MarketTiming #DayTrading #Forex #Crypto #TradingView #PineScript #MarketAnalysis #TradingStrategy #RiskManagement #GlobalMarkets #FinancialMarkets #TradingTools #MarketStructure #PriceAction #Scalping #SwingTrading #AlgoTrading

Daily Movement AnalysisDaily Volatility Explorer: 7-Day Market Pulse Indicator

Unlock the hidden rhythms of market movements with this powerful analytical tool designed for both traditional and crypto traders. This indicator meticulously tracks and analyzes price volatility patterns across all seven days of the week, giving you a strategic edge in planning your trades.

🎯 Key Features:

• Dynamic 3-month rolling analysis of daily price movements

• Real-time volatility comparison across all trading days

• Clear visual representation through color-coded bar charts

• Detailed statistical table with exact pip movements

• Sample size tracking for statistical reliability

• Works seamlessly on both traditional and crypto markets

💡 Why Traders Need This:

1. Optimal Trade Timing

- Identify the most volatile trading days for maximum opportunity

- Discover the quietest days to avoid choppy markets

- Perfect for swing traders and day traders alike

2. Risk Management Enhancement

- Set smarter stop-losses based on typical daily ranges

- Adjust position sizes according to daily volatility patterns

- Avoid overtrading during historically low-volatility periods

3. Strategic Planning

- Plan your trading week around peak volatility days

- Optimize entry and exit points based on historical movements

- Better time management by focusing on the most active days

4. Market Psychology Insights

- Understand weekly market rhythm and institutional patterns

- Identify how weekend gaps affect crypto markets

- Spot changes in market behavior across different days

🔍 Perfect For:

• Forex traders tracking major currency pairs

• Crypto traders navigating 24/7 markets

• Gold and commodity traders

• Day traders optimizing their trading schedule

• Swing traders planning optimal entry/exit days

📊 Data-Driven Decisions:

The indicator maintains a rolling 3-month window of data, providing fresh, relevant insights while filtering out outdated patterns. Each day's analysis is based on actual market movements, giving you reliable, actionable intelligence for your trading decisions.

⚡ Pro Tip: Use this indicator alongside your existing strategy to enhance your trading plan and improve your timing. The color-coded visual system makes it easy to spot patterns at a glance, while the detailed statistics table provides the hard numbers you need for precise planning.

Remember: Markets evolve, and this indicator helps you stay on top of changing patterns in real-time. Whether you're trading traditional markets or crypto, understanding daily volatility patterns is crucial for consistent trading success.

Risk MeterRisk Meter Indicator for TradingView

The Risk Meter is a powerful market risk assessment tool designed to help traders evaluate the current risk environment using a simple, data-driven score. By analyzing four critical market factors—VIX (volatility index), market breadth, trailing volatility, and credit spreads—the indicator generates a risk score between 0 and 4. This score empowers traders to make informed decisions about hedging, exiting positions, or re-entering the market, with clear visual cues and alerts for intraday monitoring.

What It Does

Calculates a Risk Score: Assigns a score from 0 to 4, where each point reflects an active risk condition based on four market indicators.

Identifies Risk Levels:

A score of 3 or higher indicates a high-risk environment, suggesting traders consider hedging or reducing exposure.

A score of 2 or lower for at least two consecutive days signals a potential opportunity to re-enter the market.

Provides Visual Feedback: Uses color-coded Columns, threshold markers, and a component table for quick interpretation.

Supports Decision-Making: Offers a structured approach to managing risk and timing trades.

How It Works

The Risk Meter aggregates four key risk conditions, each contributing 1 point to the total score when triggered:

Elevated and Rising VIX (Risk 1)

Condition: The VIX is above 18 and higher than it was 20 days ago.

Purpose: Detects increasing market fear or uncertainty.

Market Breadth Dropping (Risk 2)

Condition: Either:

Fewer than 50% of S&P 500 stocks are above their 200-day moving average and fewer than 70% are above their 50-day moving average, or

The 3-day EMA of the 200-day breadth falls below 80% of its 20-day SMA.

Purpose: Identifies weakening participation across the market.

Trailing Volatility (Risk 3)

Condition: The 30-day annualized volatility of the equal-weight S&P 500 (RSP) exceeds 35%.

Purpose: Highlights periods of heightened price instability.

Credit Spreads (Risk 4)

Condition: The price ratio of high-yield bonds (HYG) to Treasuries (TLT or IEF) is lower than it was 20 days ago, indicating widening credit spreads.

Purpose: Signals potential stress in credit markets.

The total risk score is the sum of these conditions (0 to 4). Additionally, the indicator tracks consecutive days with a score of 2 or lower to generate re-entry signals.

How to Read It Intraday

The Risk Meter is built on daily data but can be monitored intraday for real-time insights. Here’s how traders can interpret it:

Risk Score Plot:

Displayed as a step line ranging from 0 to 4.

Colors:

Red: High risk (score ≥ 3) – caution advised.

Green: Re-entry signal – score ≤ 2 for at least two consecutive days (triggered when the count increments from 1 to 2).

Blue: Neutral or low risk (score < 3 without a re-entry signal).

Threshold Lines:

Dashed Gray Line at 3: Marks the high-risk threshold.

Dotted Gray Line at 2: Indicates the low-risk threshold for re-entry signals.

Risk Component Table:

Located in the top-right corner, it lists:

VIX, Breadth, Volatility, and Credit Spreads.

Status: Shows "" (warning, red) if the risk condition is met, or "✓" (safe, blue) if not.

Helps traders pinpoint which factors are driving the score.

Alerts:

High Risk Alert: Triggers when the score moves from < 3 to ≥ 3.

Re-entry Signal Alert: Triggers when the score ≤ 2 for two consecutive days.

Intraday Usage Tips

Check the indicator throughout the day for early signs of risk shifts, especially if the score is near a threshold (e.g., 2 or 3).

Combine with other intraday tools (e.g., price action, volume) since the Risk Meter updates daily but reflects broader market conditions.

How Traders Can Use It

High-Risk Signal (Score ≥ 3):

Consider hedging positions (e.g., with options) or reducing equity exposure to protect against potential downturns.

Re-entry Signal (Score ≤ 2 for 2+ Days):

Look to re-enter the market or increase exposure, as it suggests stabilizing conditions.

Daily Risk Management:

Use the score and table to assess overall market health and adjust strategies accordingly.

Alert-Driven Trading:

Set up alerts to stay notified of critical risk changes without constant monitoring.

Why Use the Risk Meter?

This indicator offers a systematic, multi-factor approach to risk assessment, blending volatility, breadth, and credit market data into an easy-to-read score. Whether you’re an intraday trader or a longer-term investor, the Risk Meter helps you stay proactive, avoid surprises, and time your trades with greater confidence.

Financial Risk Disclaimer for the Risk Meter Tool

Important Notice: The Risk Meter is a market risk assessment tool designed to provide insights into current market conditions based on historical data and predefined indicators. It is intended for informational and educational purposes only and should not be considered financial advice, a recommendation to buy or sell any securities, or a guarantee of future market performance.

Key Considerations

No Guarantee of Accuracy: While the Risk Meter utilizes reliable data sources and established financial metrics, the creators do not guarantee the accuracy, completeness, or timeliness of the information provided. Financial markets are complex and subject to rapid, unpredictable changes, and the tool’s output may not fully reflect all market dynamics.

Market Risks: Trading and investing in financial markets carry significant risks, including the potential loss of principal. Market volatility, economic shifts, and other factors can lead to unexpected outcomes. Past performance is not a reliable indicator of future results, and the Risk Meter’s assessments are based on historical data, not future predictions.

Not a Substitute for Professional Advice: The Risk Meter is not intended to replace personalized financial guidance. Users are strongly encouraged to consult a qualified financial advisor, perform their own research, and evaluate their personal financial situation, risk tolerance, and investment objectives before making any trading or investment decisions.

Limitation of Liability: The creators of the Risk Meter, including any affiliates, developers, or contributors, are not liable for any direct, indirect, incidental, or consequential losses or damages arising from the use of this tool. This includes, but is not limited to, financial losses, missed opportunities, or decisions based on the tool’s output.

User Responsibility: By using the Risk Meter, you accept full responsibility for your trading and investment decisions. You acknowledge that you use the tool at your own risk and that the creators bear no responsibility for any outcomes resulting from its use.

Final Note

The Risk Meter is a supplementary tool designed to enhance your understanding of market risk. It is not a comprehensive solution for investment management. Approach trading and investing with caution, ensuring your decisions align with your personal financial strategy.

Liquidity Market Seeking SwiftEdgeThis indicator is designed to identify potential liquidity levels on the chart by detecting swing highs and lows, which are often areas where stop-loss orders or significant orders accumulate. It visualizes these levels with horizontal lines and labels on the right side of the chart, color-coded based on volume to help traders understand where the market might seek liquidity.

How It Works

Swing Highs and Lows: The indicator uses the ta.pivothigh and ta.pivotlow functions to identify significant swing points over a user-defined lookback period (Swing Length). These points are considered potential liquidity levels where stop-loss orders might be placed.

Volume Analysis: The indicator compares the volume at each swing point to the average volume over a specified period (Volume Average Length). Levels with above-average volume are colored red, indicating higher liquidity, while levels with below-average volume are colored green.

Liquidity Visualization: Horizontal dashed lines are drawn at each identified level, extending across the chart. Labels on the right side display the estimated liquidity amount (simulated based on volume and a multiplier, Volume Multiplier for Liquidity).

Sell Signal: A "SELL NOW" label appears when the price approaches a liquidity level after an uptrend (detected using a simple moving average crossover). This suggests a potential reversal as the market may target liquidity at that level.

Strategy Concept: Market Seeking Liquidity

The indicator is based on the concept that markets often move toward areas of high liquidity, such as clusters of stop-loss orders or significant order accumulations. These liquidity pools are typically found around swing highs and lows, where traders place their stop-losses or large orders. By identifying these levels and highlighting those with higher volume (red lines), the indicator aims to show where the market might move to "grab" this liquidity. For example, after an uptrend, the market may reverse at a swing high to take out stop-losses above that level, providing liquidity for larger players to enter or exit positions.

Settings

Swing Length: The number of bars to look back for detecting swing highs and lows. Default is 20.

Liquidity Threshold: The price threshold for merging nearby levels to avoid duplicates. Default is 0.001.

Volume Average Length: The period for calculating the average volume to compare against. Default is 20.

Volume Multiplier for Liquidity: A multiplier to scale the volume into a simulated liquidity amount (displayed as "K"). Default is 1000.

Usage Notes

Use this indicator on any timeframe, though it may be more effective on higher timeframes (e.g., 1H, 4H) where swing points are more significant.

Red lines indicate levels with higher volume, suggesting stronger liquidity pools that the market might target.

Green lines indicate levels with lower volume, which may be less significant.

The "SELL NOW" signal is a basic example of how to use liquidity levels for trading decisions. It appears when the price approaches a liquidity level after an uptrend, but it should be used in conjunction with other analysis.

Adjust the Volume Multiplier for Liquidity to scale the displayed liquidity amounts based on your instrument (e.g., forex pairs may need a higher multiplier than indices).

Volatility Based Momentum by QTX Algo SystemsVolatility Based Momentum by QTX Algo Systems

Overview

This indicator is designed to determine whether a market trend is genuinely supported by both momentum and volatility. It produces per-candle signals when a smoothed momentum oscillator is above its moving average, a Price – Moving Average Ratio confirms overall trend strength by remaining above a preset level with a positive slope, and when at least one of two distinct volatility metrics is rising. This integrated approach offers traders a consolidated and dynamic view of market energy, delivering more actionable insights than a simple merger of standard indicators.

How It Works

The indicator fuses two complementary volatility measures with dual momentum assessments to ensure robust signal generation. One volatility metric evaluates long-term market behavior by analyzing the dispersion of logarithmic price changes, while the other—derived from a Bollinger Band Width Percentile—captures recent price variability and confirms that market volatility remains above a minimum threshold. A trading signal is generated only when at least one of these volatility measures shows a sustained upward trend over several candles.

For momentum, a double‐smoothed Stochastic Momentum Index provides a refined, short-term view of price action, filtering out market noise. In addition, the PMARP serves as a confirmation tool by comparing the current price to its moving average, requiring that its value remains above a defined level with a positive slope to indicate a strong trend. Together, these elements ensure that a signal is only produced when both the market’s momentum and volatility are in alignment.

Although the components used are based on well-known technical analysis methods, the thoughtful integration of these elements creates a tool that is more than the sum of its parts. By combining long-term volatility assessment with a real-time measure of recent price variability—and by merging short-term momentum analysis with a confirmation of overall trend strength—the indicator delivers a more reliable and comprehensive view of market energy. This holistic approach distinguishes it from standard indicators.

How to Use

Traders can adjust the volatility threshold setting to tailor the indicator to their preferred market or timeframe. The indicator displays per-candle signals when both the refined momentum criteria and the dynamic volatility conditions are met. These signals are intended to be used as part of a broader trading strategy, in conjunction with other technical analysis tools for confirming entries and exits.

Disclaimer

This indicator is for educational purposes only and is intended to support your trading strategy. It does not guarantee performance, and past results are not indicative of future outcomes. Always use proper risk management and perform your own analysis before trading.

Bollinger Bands by Abu ElyasBollinger Bands with Adjustable Stop Loss (Long-Only)

This strategy uses a Bollinger Band breakout approach to enter long positions and incorporates an adjustable stop loss for risk management.

Below is an overview of the logic, parameters, and usage instructions.

1. Bollinger Bands Logic

Basis (Middle Band): A moving average (type selectable by the user) of the chosen source, typically the closing price.

Upper Band: The basis plus a specified number of standard deviations (user-defined multiplier).

Lower Band: The basis minus the same number of standard deviations.

2. Entry Triggers

The strategy enters a long position when the close price rises above the upper Bollinger Band , suggesting a potential bullish breakout.

This logic is only applied within a user-specified date range (adjustable in the strategy’s inputs).

3. Exit Triggers

1. Bollinger Band Exit:

If the close price drops below the lower Bollinger Band , the strategy closes the position, indicating a loss of bullish momentum.

2. Stop Loss Exit:

A default 8% stop loss is set, which automatically exits the trade if the close falls 8% below the entry price.

This stop-loss percentage is adjustable from the strategy’s settings, allowing users to tailor risk based on their preferences.

3. Date Range:

If the current bar is outside of the specified start/end dates, the strategy will also exit any open positions.

4. Position Sizing & Other Settings

1- Position Size:

By default, the script uses 100% of account equity for each trade.

2- Commissions & Slippage:

Commission is set to 0%, and slippage is set to 3 ticks.

3- Timeframe Handling:

You can select a custom timeframe or leave it blank to use the chart’s timeframe.

5. Customization

1. Bollinger Bands Parameters:

Length of the moving average, type of moving average (SMA, EMA, etc.), and the standard deviation multiplier can be adjusted.

2. Stop Loss (%)

The default stop loss of 8% can be changed in the script’s input settings to any percentage you prefer.

3. Date Filter:

Modify the start/end dates to control the historical period over which the strategy executes trades.

6. Notes & Best Practices

1- No Short Trades:

This is a long‐only strategy. It will either be in a long position or flat (no open position).

2- Risk Management:

An 8% stop loss may or may not align with your personal risk tolerance. Always adjust according to market conditions and your own trading style.

3- Market Gaps & Volatility:

In highly volatile markets, slippage or gaps can cause the actual exit price to be worse than the intended stop-loss level.

4- Test Thoroughly:

Backtest on different timeframes and market conditions. No single strategy works in all scenarios.

7. Disclaimer

Educational Use Only: This script is for informational and illustrative purposes and should not be considered financial advice.

No Guarantee of Profit: Past performance does not guarantee future results. Trading involves substantial risk, and it is possible to lose more than your initial investment.

Consult a Professional: Always consult a qualified financial advisor before making investment decisions.

Use this script as a foundation and personalize it based on your trading style, tolerance for drawdowns, and market conditions.

Volatility Price FlowCapitalize on market volatility with our new volatility price flow indicator. We have designed this indicator to process historical price movements and indicate when price may have reached exhaustion in the context of current volatility.

This is achieved by taking the price deviation from a user defined moving average, and applying a weighting to the deviations from the candle body and candle wick on both buy side and sell side, over a user defined period. The period of the base moving average, type of moving average and the period of the historical price deviations can all be modified. This creates a typical 'band' style indicator, though with a unique characteristic that the buy and sell side vary independently as well as the band expansion being based on weighted variables tied to the actual price changes, rather than just a standard deviation the moves uniformly.

Additionally, these bands can be merged with an anchored vwap - we do this so that the deviations of price from the moving average can include a more volume based approach to identifying potential pivots.

The end result is an indicator that reflects the current market price movements, identifies and capitalizes on impulsive or beginning moves to indicate potential tops / bottoms / reversals.

The signals are simple - anytime price closes within a band, having been outside the band, a signal is displayed. As a basic guide to setting the indicator up for the first time, we suggest reducing all of the multipliers to a value less than 1. Then gradually increase each one, until the signals reduce in quantity and improve in quality, starting with the price deviation multiplier, then the volatility multiplier and finally the expansion multiplier.

Last of all, alerts can be created based on the current chart timeframe and indicator settings, simply by adding an alert that uses the built in buy or sell signal.

Note: We cannot guarantee the accuracy of the signals provided, since the user creates the signals by modifying the settings, and as such we can take no responsibility for any trading losses incurred using the indicator and highly encourage all users to manage their risk and only risk what you can afford to lose.

Power Play Signal Indicator [Masky18]Power Play Signal Indicator

The Power Play Signal Indicator is a sophisticated custom trading strategy designed to identify high-probability breakout and breakdown opportunities by combining consolidation detection, trend alignment, volume analysis, and relative strength ranking. Unlike simple mashups of existing indicators, this script integrates multiple technical concepts into a cohesive strategy that helps traders capitalize on market momentum with precision.

What Makes This Indicator Unique?

The PowerPlay Signal Indicator is not just a combination of existing indicators; it is a custom-built strategy that uses original logic to filter out low-probability setups and focus on high-quality trading opportunities. Here’s how it works:

Consolidation Detection:

The script identifies consolidation zones by analyzing price action over a user-defined period (default: 6 bars). It calculates the high, low, and midpoint of the consolidation range and ensures the price stays within a specified percentage range (default: 13%).

Consolidations are classified as Tight, Loose, or Okay, helping traders gauge the strength of the potential breakout or breakdown.

Breakout & Breakdown Logic:

Breakouts and breakdowns are confirmed using a combination of:

Price Action: The script checks if the price closes above the consolidation high (breakout) or below the consolidation low (breakdown).

Volume Analysis: A significant volume spike (default: 20% increase) is required to confirm the move.

MACD & Moving Averages: The script uses MACD and moving averages (50-day and 200-day) to ensure the breakout/breakdown aligns with the prevailing trend.

Trend Alignment:

The script ensures trades are aligned with the long-term trend by using:

50-day SMA and 200-day SMA to confirm uptrends or downtrends.

150-day SMA as an additional filter to ensure the trend is strong.

52-week high/low conditions to ensure the price is in a favorable position relative to its historical range.

Relative Strength Ranking:

The script compares the asset’s performance against a benchmark asset (e.g., SPY) to ensure it is outperforming the market. This is done using a customizable Relative Strength (RS) Threshold (default: 70).

Golden Candle Signals:

For high-probability setups, the script identifies Golden Candles—strong breakout or breakdown candles with:

Large price movement (default: 7.5% to 12.5% candle size).

High volume (default: 2x the average consolidation volume).

Alignment with MACD and moving averages.

Risk Management:

The script provides stop loss, trailing stop, and take profit levels based on:

ATR (Average True Range): Dynamic stop loss levels are calculated using ATR (default: 14-period ATR with a 2x multiplier).

Trailing Stop Percentage: User-defined trailing stop (default: 2%).

Take Profit Percentage: User-defined take profit (default: 5%).

Performance Tracking:

The script includes a Performance Table that tracks:

Total breakouts and breakdowns.

Successful and failed trades.

Win rates for breakouts and breakdowns.

Golden candle signals.

How Does It Work?

The PowerPlay Signal Indicator combines the following key components to generate signals:

Consolidation Detection:

The script calculates the high, low, and midpoint of the consolidation range over a user-defined period.

It ensures the price stays within a specified percentage range (default: 13%) to confirm consolidation.

Breakout/Breakdown Confirmation:

A breakout is confirmed when:

The price closes above the consolidation high.

Volume increases by at least 20%.

MACD is positive and above the signal line.

The price is above the 50-day and 200-day SMAs.

A breakdown is confirmed when:

The price closes below the consolidation low.

Volume increases by at least 20%.

MACD is negative and below the signal line.

The price is below the 50-day and 200-day SMAs.

Golden Candle Signals:

Golden Candles are identified when:

The candle size is between 7.5% and 12.5%.

Volume is at least 2x the average consolidation volume.

The candle aligns with the prevailing trend and MACD.

Risk Management:

Stop loss levels are calculated using ATR (default: 14-period ATR with a 2x multiplier).

Trailing stop and take profit levels are based on user-defined percentages.

How to Use the Indicator

Input Parameters:

Consolidation Periods: Set the number of bars to analyze for consolidation (default: 6).

Maximum Consolidation Range: Define the maximum percentage range for consolidation (default: 13%).

Stop Loss Factor: Adjust the stop loss multiplier based on the midpoint of the consolidation range (default: 0.985).

RS Threshold: Set the relative strength threshold for trend alignment (default: 70).

Comparison Asset: Enable comparison with a benchmark asset (e.g., SPY) to ensure the asset is outperforming the market.

Trailing Stop Percentage: Set the trailing stop percentage (default: 2%).

Take Profit Percentage: Set the take profit percentage (default: 5%).

Time Exit Bars: Define the maximum number of bars to hold a trade (default: 10).

Interpreting Signals:

Breakout Signal: A green label ("BO") appears when a breakout is detected.

Breakdown Signal: A red label ("BD") appears when a breakdown is detected.

Golden Candle Signal: A gold medal icon (🥇) appears for high-probability setups.

Performance Table:

The performance table displays the number of trades, successful trades, failed trades, and win rates for breakouts and breakdowns.

Alerts:

Enable alerts for breakouts, breakdowns, and golden candles to stay informed about potential trading opportunities.

Why Choose the PowerPlay Signal Indicator?

Original Logic: Combines consolidation detection, trend alignment, volume analysis, and relative strength ranking into a unique strategy.

High-Probability Signals: Focuses on high-quality setups with strong volume and trend alignment.

Risk Management: Built-in stop loss, trailing stop, and take profit options help you manage risk effectively.

Performance Tracking: Tracks trade outcomes and win rates to help you refine your strategy.

Customizable: Fully adjustable inputs allow you to adapt the indicator to your trading style and market conditions.

Cypto Oscillator with Sortino-like VolatilityEnhanced Inverted Ultimate Oscillator with Sortino-like Volatility

This indicator combines the power of the Ultimate Oscillator with a unique Sortino-like volatility calculation to provide a comprehensive view of market dynamics. It's designed to help traders identify potential turning points and assess the risk associated with price movements.

**Core Components:**

* **Ultimate Oscillator (UO):** The UO is a momentum indicator that incorporates short, medium, and long-term price action to identify overbought and oversold conditions. This indicator inverts and normalizes the UO to a 0-10 scale, providing a clear view of momentum shifts.

* **Sortino-like Volatility:** Instead of a standard deviation, this indicator uses a downside deviation calculation. This focuses specifically on *negative* price movements, offering a more relevant measure of risk for most traders. By not penalizing upside volatility, it avoids giving false signals during strong bull runs. The downside deviation is scaled as a percentage of the closing price for cross-asset comparability.

* **Volatility Signal:** The inverted UO is multiplied by the downside deviation to create a combined volatility signal. This signal reflects both momentum and downside risk, providing a more nuanced market perspective.

**Key Features and Uses:**

* **Identifying Potential Turning Points:** Divergences between the UO and price action can signal potential trend reversals. Look for the UO to make higher lows while price makes lower lows (bullish divergence) or the UO to make lower highs while price makes higher highs (bearish divergence).

* **Assessing Downside Risk:** The Sortino-like volatility component helps traders gauge the potential for downside price swings. Higher volatility suggests greater risk.

* **Dynamic Volatility Thresholds:** The indicator includes adjustable upper and lower volatility thresholds, based on a moving average of the volatility signal. These thresholds can be used to identify periods of unusually high or low volatility.

* **Customizable Lookback Periods:** Traders can adjust the lookback periods for the UO and the standard deviation calculation to fine-tune the indicator to their specific trading style and market conditions.

* **Visualizations:** The indicator provides several visual aids, including:

* A histogram of the volatility signal, colored dynamically based on its relationship to the moving average of volatility. Red indicates volatility above the upper bound, orange between the bounds and green below the lower bound.

* A line plot of the volatility signal.

* An optional moving average of the volatility signal.

* Optional upper and lower volatility threshold lines with a filled range for visual clarity.

* **Alerts:** The indicator includes alert conditions for when the volatility signal crosses above the upper threshold (high volatility) or below the lower threshold (low volatility).

**How to Use:**

1. **Inputs:** Adjust the input parameters to optimize the indicator for your chosen asset and timeframe.

2. **Divergences:** Look for divergences between the UO and price to identify potential trend reversals.

3. **Volatility:** Use the volatility signal and thresholds to assess downside risk.

4. **Alerts:** Enable alerts to be notified of high or low volatility events.

**Disclaimer:** This indicator is for informational purposes only and should not be considered financial advice. Always conduct your own thorough analysis before making any trading decisions.

Key improvements in this description:

Clear and concise language: Easy for traders to understand.

Focus on benefits: Highlights how the indicator can help traders.

Detailed explanation of features: Covers all the important aspects.

How-to-use section: Provides practical guidance.

Disclaimer: Includes a necessary disclaimer.

Emphasis on the Sortino-like approach: This is a unique selling point of your indicator.

Well-structured and formatted: Easy to read and digest.

This description should be a great starting point for sharing your indicator with the TradingView community. You can further customize it by adding screenshots of the indicator in action or linking to a chart where it's being used. Remember to respond to comments and questions from other users to build engagement and improve your indicator over time.

Relative Volume Index [PhenLabs]Relative Volume Index (RVI)

Version: PineScript™ v6

Description

The Relative Volume Index (RVI) is a sophisticated volume analysis indicator that compares real-time trading volume against historical averages for specific time periods. By analyzing volume patterns and statistical deviations, it helps traders identify unusual market activity and potential trading opportunities. The indicator uses dynamic color visualization and statistical overlays to provide clear, actionable volume analysis.

Components

• Volume Comparison: Real-time volume relative to historical averages

• Statistical Bands: Upper and lower deviation bands showing volume volatility

• Moving Average Line: Smoothed trend of relative volume

• Color Gradient Display: Visual representation of volume strength

• Statistics Dashboard: Real-time metrics and calculations

Usage Guidelines

Volume Strength Analysis:

• Values > 1.0 indicate above-average volume

• Values < 1.0 indicate below-average volume

• Watch for readings above the threshold (default 6.5x) for exceptional volume

Trading Signals:

• Strong volume confirms price moves

• Divergences between price and volume suggest potential reversals

• Use extreme readings as potential reversal signals

Optimal Settings:

• Start with default 15-bar lookback for general analysis

• Adjust threshold (6.5x) based on market volatility

• Use with multiple timeframes for confirmation

Best Practices:

• Combine with price action and other indicators

• Monitor deviation bands for volatility expansion

• Use the statistics panel for precise readings

• Pay attention to color gradients for quick assessment

Limitations

• Requires quality volume data for accurate calculations

• May produce false signals during pre/post market hours

• Historical comparisons may be skewed during unusual market conditions

• Best suited for liquid markets with consistent volume patterns

Note: For optimal results, use in conjunction with price action analysis and other technical indicators. The indicator performs best during regular market hours on liquid instruments.

Implied and Historical VolatilityAbstract

This TradingView indicator visualizes implied volatility (IV) derived from the VIX index and historical volatility (HV) computed from past price data of the S&P 500 (or any selected asset). It enables users to compare market participants' forward-looking volatility expectations (via VIX) with realized past volatility (via historical returns). Such comparisons are pivotal in identifying risk sentiment, volatility regimes, and potential mispricing in derivatives.

Functionality

Implied Volatility (IV):

The implied volatility is extracted from the VIX index, often referred to as the "fear gauge." The VIX represents the market's expectation of 30-day forward volatility, derived from options pricing on the S&P 500. Higher values of VIX indicate increased uncertainty and risk aversion (Whaley, 2000).

Historical Volatility (HV):

The historical volatility is calculated using the standard deviation of logarithmic returns over a user-defined period (default: 20 trading days). The result is annualized using a scaling factor (default: 252 trading days). Historical volatility represents the asset's past price fluctuation intensity, often used as a benchmark for realized risk (Hull, 2018).

Dynamic Background Visualization:

A dynamic background is used to highlight the relationship between IV and HV:

Yellow background: Implied volatility exceeds historical volatility, signaling elevated market expectations relative to past realized risk.

Blue background: Historical volatility exceeds implied volatility, suggesting the market might be underestimating future uncertainty.

Use Cases

Options Pricing and Trading:

The disparity between IV and HV provides insights into whether options are over- or underpriced. For example, when IV is significantly higher than HV, options traders might consider selling volatility-based derivatives to capitalize on elevated premiums (Natenberg, 1994).

Market Sentiment Analysis:

Implied volatility is often used as a proxy for market sentiment. Comparing IV to HV can help identify whether the market is overly optimistic or pessimistic about future risks.

Risk Management:

Institutional and retail investors alike use volatility measures to adjust portfolio risk exposure. Periods of high implied or historical volatility might necessitate rebalancing strategies to mitigate potential drawdowns (Campbell et al., 2001).

Volatility Trading Strategies:

Traders employing volatility arbitrage can benefit from understanding the IV/HV relationship. Strategies such as "long gamma" positions (buying options when IV < HV) or "short gamma" (selling options when IV > HV) are directly informed by these metrics.

Scientific Basis

The indicator leverages established financial principles:

Implied Volatility: Derived from the Black-Scholes-Merton model, implied volatility reflects the market's aggregate expectation of future price fluctuations (Black & Scholes, 1973).

Historical Volatility: Computed as the realized standard deviation of asset returns, historical volatility measures the intensity of past price movements, forming the basis for risk quantification (Jorion, 2007).

Behavioral Implications: IV often deviates from HV due to behavioral biases such as risk aversion and herding, creating opportunities for arbitrage (Baker & Wurgler, 2007).

Practical Considerations

Input Flexibility: Users can modify the length of the HV calculation and the annualization factor to suit specific markets or instruments.

Market Selection: The default ticker for implied volatility is the VIX (CBOE:VIX), but other volatility indices can be substituted for assets outside the S&P 500.

Data Frequency: This indicator is most effective on daily charts, as VIX data typically updates at a daily frequency.

Limitations

Implied volatility reflects the market's consensus but does not guarantee future accuracy, as it is subject to rapid adjustments based on news or events.

Historical volatility assumes a stationary distribution of returns, which might not hold during structural breaks or crises (Engle, 1982).

References

Black, F., & Scholes, M. (1973). "The Pricing of Options and Corporate Liabilities." Journal of Political Economy, 81(3), 637-654.

Whaley, R. E. (2000). "The Investor Fear Gauge." The Journal of Portfolio Management, 26(3), 12-17.

Hull, J. C. (2018). Options, Futures, and Other Derivatives. Pearson Education.

Natenberg, S. (1994). Option Volatility and Pricing: Advanced Trading Strategies and Techniques. McGraw-Hill.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (2001). The Econometrics of Financial Markets. Princeton University Press.

Jorion, P. (2007). Value at Risk: The New Benchmark for Managing Financial Risk. McGraw-Hill.

Baker, M., & Wurgler, J. (2007). "Investor Sentiment in the Stock Market." Journal of Economic Perspectives, 21(2), 129-151.

Machine Learning RSI Bands V3The Machine Learning RSI Bands V3 is a cutting-edge trading tool designed to provide actionable insights by combining the strength of machine learning with a traditional RSI framework. It adapts dynamically to changing market conditions, offering traders a robust, data-driven approach to identifying opportunities.

Let’s break down its functionality and the logic behind each input to give you a clear understanding of how it works and how you can use it effectively.

RSI Parameters RSI Source (rsisrc): Choose the data source for RSI calculation, such as the closing price. This allows you to focus on the specific price data that aligns with your trading strategy. RSI Length (rsilen): Set the number of periods used for RSI calculation. A shorter length makes the RSI more reactive to price changes, while a longer length smooths out volatility. These inputs allow you to customize the foundational RSI calculations, ensuring the indicator fits your style of trading.

Band Limits Lower Band Limit (lb): Defines the RSI value below which the market is considered oversold. Upper Band Limit (ub): Defines the RSI value above which the market is considered overbought. These settings give you control over the thresholds for market conditions. By adjusting the band limits, you can tailor the indicator to be more or less sensitive to market movements.

Sampling and Reaction Settings Target Reaction Size (l): Determines the number of bars used to define pivot points. Smaller values react to shorter-term price movements, while larger values focus on broader trends. Backtesting Reaction Size (btw): Sets the number of bars used to validate signal performance. This ensures signals are only considered valid if they perform consistently within the specified range. Data Format (version): Choose between Absolute (ignoring direction) and Directional (incorporating directional price changes). Sampling Method (sm): Select how the data is analyzed—options include Price Movement, Volume Movement, RSI Movement, Trend Movement, or a Hybrid approach. These settings empower you to refine how the indicator processes and interprets data, whether focusing on short-term price shifts or broader market trends.

Signal Settings Signal Confidence Method (cm): Choose between: Threshold: Signals must meet a confidence limit before being generated. Voting: Requires a majority of 5 signal components to confirm a trade. Confidence Limit (cl): Defines the confidence threshold for generating signals when using the Threshold method. Votes Needed (vn): Sets the number of votes required to confirm a trade when using the Voting method. Use All Outputs (fm): If enabled, signals are generated without filtering, providing an unfiltered view of potential opportunities. This section offers a balance between precision and flexibility, enabling you to control the rigor applied to signal generation.

How It Works

The script uses machine learning models to adaptively calculate dynamic RSI bands. These bands adjust based on market conditions, providing a more responsive and nuanced interpretation of overbought and oversold levels.

Dynamic Bands: The lower and upper RSI bands are recalibrated using machine learning to reflect current market conditions. Signals: Long and short signals are generated when RSI crosses these bands, with additional filters applied based on your chosen confidence method and sampling settings. Transparency: Real-time success rates and profit factors are displayed on the chart, giving you clear feedback on the indicator's performance.

Why Use Machine Learning RSI Bands V3?

This indicator is built for traders who want more than static thresholds and generic signals. It offers:

Adaptability: Machine learning dynamically adjusts the indicator to market conditions. Customizability: Each input serves a specific purpose, giving you full control over its behavior. Accountability: With built-in performance metrics, you always know how the tool is performing.

This is a tool designed for those who value precision and adaptability in trading.

Ultra Volume High Breakoutser Inputs:

length: Defines the period to calculate the moving average of volume.

multiplier: Sets the threshold above the moving average to consider as "Ultra Volume."

breakoutMultiplier: Allows for customization of breakout sensitivity.

Volume Calculation:

The script calculates a simple moving average (SMA) of the volume for a defined period (length).

It then detects if the current volume is higher than the moving average multiplied by the user-defined multiplier.

Breakout Condition:

The script checks if the price has moved above the highest close of the previous length periods while the volume condition for "Ultra Volume" is true.

Visuals:

The script marks the breakout with an upward label below the bar (plotshape), colored green for easy identification.

Ultra volume is highlighted with a red histogram plot.

Alert Condition:

An alert condition is included to trigger whenever an ultra volume high breakout occurs.

Customization:

You can adjust the length, multiplier, and breakoutMultiplier to fit your strategy and asset volatility.

Alerts can be set in TradingView to notify you when this condition is met.

Let me know if you'd like further customization or explanation!

Hourly Change Table (UTC Adjustable)### Indicator Description: Hourly Change Table (UTC Adjustable)

The **Hourly Change Table (UTC Adjustable)** is a powerful tool designed for analyzing **hourly average price changes** across financial instruments. By calculating and sorting these averages, the indicator identifies the hours with the most significant positive and negative price movements. It also provides visual highlights directly on the chart for easier decision-making.

---

### What Does This Indicator Do?

1. **Analyzes Hourly Average Price Changes**:

- It calculates the **average percentage price change** for each hour based on the selected lookback period.

2. **Displays a Ranked Table**:

- The indicator generates a table ranking hourly averages from the highest to the lowest, allowing you to see which hours are the most impactful.

3. **Highlights Max and Min Hours on the Chart**:

- The hour with the highest average price change is highlighted in **green**.

- The hour with the lowest average price change is highlighted in **red**.

4. **Adjusts for Time Zones**:

- A customizable **UTC Offset** ensures the indicator aligns with your preferred time zone.

---

### Key Features

1. **Customizable Lookback Period**:

- Define how many bars the indicator analyzes to calculate meaningful trends.

2. **Time Zone Adjustment**:

- Adjust the UTC offset to match your local trading hours or preferred analysis window.

3. **Graphical Chart Highlights**:

- Instantly identify the most significant hours with color-coded chart backgrounds.

4. **Sorted Data Table**:

- View a ranked list of hourly averages with the maximum and minimum values highlighted for quick reference.

---

### How to Use This Indicator?

1. **Add to Your Chart**:

- Apply the indicator to any financial instrument and time frame on TradingView.

2. **Set the Lookback Period**:

- Configure the "Lookback Bars" setting to define how many bars the indicator should analyze.

3. **Configure the UTC Offset**:

- Align the indicator with your preferred time zone by setting the appropriate UTC offset (e.g., `2` for UTC+2).

4. **Enable Background Highlighting (Optional)**:

- Turn on "Enable Background Highlighting" to visually highlight the max and min hours on the chart.

5. **Analyze the Table**:

- Use the table to identify consistent hourly trends and make informed trading decisions based on historical data.

---

### Practical Use Cases

- **Volatility Analysis**:

- Identify the hours of highest activity or price movement to create a more effective trading plan.

- **Market Timing**:

- Optimize entry and exit points by focusing on the hours with the highest or lowest average changes.

- **Custom Strategy Development**:

- Incorporate hourly averages into your trading strategies for greater precision.

---

### Example (BTC/USD)

1. You are analyzing the **BTC/USD pair** and set the **UTC Offset** to `2` (UTC+2) to match your local time zone.

2. The indicator calculates and identifies:

- **10:00-11:00 (UTC+2)** as the hour with the highest average price increase (e.g., +0.85%).

- **14:00-15:00 (UTC+2)** as the hour with the lowest average price change (e.g., -0.65%).

3. Based on this information:

- You decide to **closely monitor 10:00-11:00** for potential bullish activity or upward momentum.

- You prepare for **14:00-15:00** to act cautiously or position for potential bearish movements.

---

### Important Notes

- **This indicator does not provide financial or investment advice.**

- It is intended solely for **educational purposes** to assist traders in analyzing historical price data.

- Always consider additional market factors, perform your own research, and consult with a financial advisor before making trading or investment decisions.

---

This description emphasizes that the indicator calculates **hourly averages**, while also including a disclaimer clarifying its educational purpose. It’s suitable for publication on TradingView.

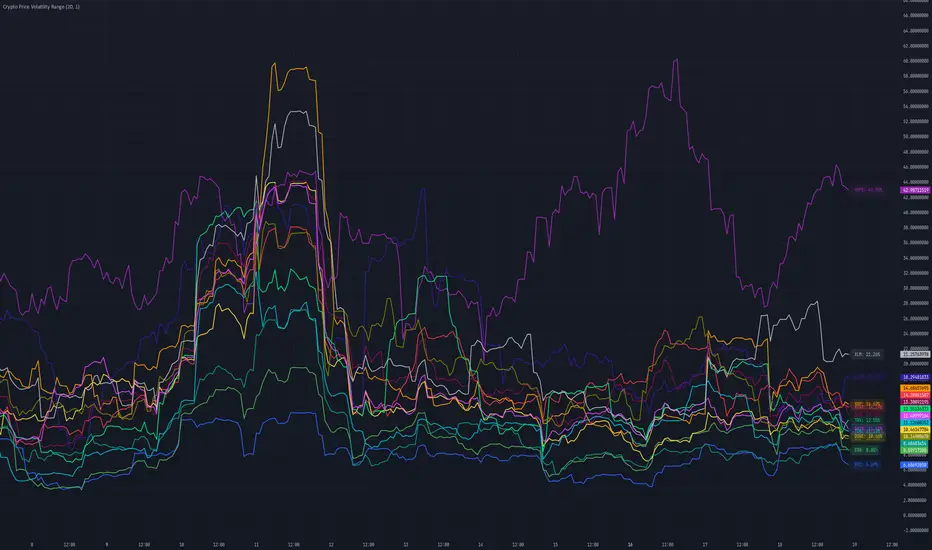

Crypto Price Volatility Range# Cryptocurrency Price Volatility Range Indicator

This TradingView indicator is a visualization tool for tracking historical volatility across multiple major cryptocurrencies.

## Features

- Real-time volatility tracking for 14 major cryptocurrencies

- Customizable period and standard deviation multiplier

- Individual color coding for each currency pair

- Optional labels showing current volatility values in percentage

## Supported Cryptocurrencies

- Bitcoin (BTC)

- Ethereum (ETH)

- Avalanche (AVAX)

- Dogecoin (DOGE)

- Hype (HYPE)

- Ripple (XRP)

- Binance Coin (BNB)

- Cardano (ADA)

- Tron (TRX)

- Chainlink (LINK)

- Shiba Inu (SHIB)

- Toncoin (TON)

- Sui (SUI)

- Stellar (XLM)

## Settings

- **Period**: Timeframe for volatility calculation (default: 20)

- **Standard Deviation Multiplier**: Multiplier for standard deviation (default: 1.0)

- **Show Labels**: Toggle label display on/off

## Calculation Method

The indicator calculates volatility using the following method:

1. Calculate daily logarithmic returns

2. Compute standard deviation over the specified period

3. Annualize (multiply by √252)

4. Convert to percentage (×100)

## Usage

1. Add the indicator to your TradingView chart

2. Adjust parameters as needed

3. Monitor volatility lines for each cryptocurrency

4. Enable labels to see precise current volatility values

## Notes

- This indicator displays in a separate window, not as an overlay

- Volatility values are annualized

- Data for each currency pair is sourced from USD pairs

Ultimate Volatility RateUltimate Volatility Rate

This indicator measures the volatility of price movements.

Support and Resistance Identification:

High volatility periods indicate larger price movements, which can be useful in assessing the potential for support and resistance levels to be broken.

Stop Loss (SL) and Take Profit (TP) Calculations:

The average volatility can be used to calculate dynamic Stop Loss (SL) and Take Profit (TP) levels:

SL: Placing it at a certain volatility multiplier below/above the entry price.

TP: Setting it at a certain volatility multiplier below/above the entry price.

For example:

SL: Entry price +/- (UVR × 1.5)

TP: Entry price +/- (UVR × 2)

Market Condition Analysis:

When the indicator value is high, it suggests that the market is volatile (active).

When the value is low, it indicates the market is in consolidation (sideways movement).

This information helps traders decide whether to take trend-following or consolidation-based positions.

Trend Reversal Monitoring:

A sudden increase in volatility often signals the start of a strong trend.

Conversely, a decrease in volatility can signal the slowing down or end of a trend.

Conditional Volatility Explosion/ContractionThis indicator identifies zones of potential volatility expansion by analyzing the contraction and expansion of volatility bands, which are conditioned by the relationship of the price to moving averages

Volatility Squeeze: When the bands contract, it indicates a potential buildup in market tension, often preceding a significant price movement.

Volatility Expansion: When the bands expand, it signals the release of built-up tension, often resulting in increased volatility.

Trend Confirmation: The bands are active only when the price aligns with the moving average condition, helping to filter out less relevant signals during non-trending markets.

Upper Band: Displays as a red band when the volatility condition is met.

Represents the upper boundary of potential price action during high volatility.

Lower Band: Displays as a green band when the volatility condition is met.

Represents the lower boundary of potential price action during high volatility.

Fill Areas: The areas between the EMA and the bands are filled with transparent colors:

Red for the upper fill.

Green for the lower fill.

These highlights help visualize zones of potential volatility explosion.