Liquidation Strategy📈 It enters a long trade when long liquidation spikes above a set threshold.

📉 It enters a short trade when short liquidation drops below the negative threshold.

🧮 It optionally filters entries using an EMA multiplier.

🔁 It exits long when RSI crosses below its smoothed version.

🔄 It exits short when RSI crosses above its smoothed version.

🔗 It requires linking to the Liquidations indicator on Bybit or OKX charts.

Média Móvel Exponencial (MME)

Penguin Volatility State StrategyThe Penguin Volatility State Strategy is a comprehensive technical analysis framework designed to identify the underlying "state" or "regime" of the market. Instead of just providing simple buy or sell signals, its primary goal is to classify the market into one of four distinct states by combining trend, momentum, and volatility analysis.

The core idea is to trade only when these three elements align, focusing on periods of volatility expansion (a "squeeze breakout") that occur in the direction of a confirmed trend and are supported by strong momentum.

Key Components

The strategy is built upon two main engines

The Volatility Engine (Bollinger Bands vs. Keltner Channels)

This engine detects periods of rapidly increasing volatility. It measures the percentage difference (diff) between the upper bands of Bollinger Bands (which are based on standard deviation) and Keltner Channels (based on Average True Range). During a volatility "squeeze," both bands are close. When price breaks out, the Bollinger Band expands much faster than the Keltner Channel, causing the diff value to become positive. A positive diff signals a volatility breakout, which is the moment the strategy becomes active.

The Trend & Momentum Engine (Multi-EMA System)

This engine determines the market's direction and strength. It uses:

A Fast EMA (e.g., 12-period) and a Slow EMA (e.g., 26-period): The crossover of these two moving averages defines the primary, underlying trend (similar to a MACD).

An Ultra-Fast EMA (e.g., 2-period of ohlc4): This is used to measure the immediate, short-term momentum of the price.

The Four Market States

By combining the Trend and Momentum engines, the strategy categorizes the market into four visually distinct states, represented by the chart's background color. This is the most crucial aspect of the system.

💚 Green State: Strong Bullish

The primary trend is UP (Fast EMA > Slow EMA) AND the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This represents a healthy, robust uptrend where both the underlying trend and short-term price action are aligned. It is considered the safest condition for taking long positions.

❤️ Red State: Strong Bearish

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) AND the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This represents a strong, confirmed downtrend. It is considered the safest condition for taking short positions.

💛 Yellow State: Weakening Bullish / Pullback

Condition: The primary trend is UP (Fast EMA > Slow EMA) BUT the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This is a critical warning signal for bulls. While the larger trend is still up, the short-term price action is showing weakness. This could be a minor pullback, a period of consolidation, or the very beginning of a trend reversal. Caution is advised.

💙 Blue State: Weakening Bearish / Relief Rally

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) BUT the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This signals that a downtrend is losing steam. It often represents a short-covering rally (a "bear market rally") or the first potential sign of a market bottom. Bears should be cautious and consider taking profits.

How the Strategy Functions

The strategy uses these four states as its foundation for making trading decisions. The entry and exit arrows (Long, Short, Close) are generated based on a set of rules that can be customized by the user. For instance, a trader can configure the strategy to

Only take long trades during the Green State.

Require a confirmed volatility breakout (diff > 0) before entering a trade.

Use the "RSI on Diff" indicator to ensure that the breakout is supported by accelerating momentum.

Summary

In essence, the Penguin Volatility State Strategy provides a powerful "dashboard" for viewing the market. It moves beyond simple indicators to offer a contextual understanding of price action. By waiting for the alignment of Trend (the State), Volatility (the Breakout), and Momentum (the Acceleration), it helps traders to identify higher-probability setups and, just as importantly, to know when it is better to stay out of the market.

License / disclaimer

© waranyu.trkm — MIT License. Educational use only; not financial advice.

VWAP Trend Strategy (Intraday) [KedarArc Quant]Description:

An intraday strategy that anchors to VWAP and only trades when a local EMA trend gate and a volume participation gate are both open. It offers two entry templates—Cross and Cross-and-Retest—with an optional Momentum Exception for impulsive moves. Exits combine a TrendBreak (structure flips) with an ATR emergency stop (risk cap).

Updates will be published under this script.

Why this merits a new script

This is not a simple “VWAP + EMA + ATR” overlay. The components are sequenced as gates and branches that *change the trade set* in ways a visual mashup cannot:

1. Trend Gate first (EMA fast vs. slow on the entry timeframe)

Counter-trend VWAP crosses are suppressed. Many VWAP scripts fire on every cross; here, no entry logic even evaluates unless the trend gate is open.

2. Participation Gate second (Volume SMA × multiplier)

This gate filters thin liquidity moves around VWAP. Without it, the same visuals would produce materially more false triggers.

3. Branching entries with structure awareness

* Cross: Immediate VWAP cross in the trend direction.

* Cross-and-Retest: Requires a revisit to VWAP vicinity within a lookback window (recent low near VWAP for longs; recent high for shorts). This explicitly removes first-touch fakeouts that a plain cross takes.

* Momentum Exception (optional): A quantified body% + volume condition can bypass the retest when flow is impulsive—intentional risk-timing, not “just another indicator.”

4. Dual exits that reference both anchor and structure

* TrendBreak: Close only when price loses VWAP and EMA alignment flips.

* ATR stop: Placed at entry to cap tail risk.

These exits complement the entry structure rather than being generic stop/target add-ons.

What it does

* Trades the session’s fair value anchor (VWAP), but only with local-trend agreement (EMA fast vs. slow) and sufficient participation (volume filter).

* Lets you pick Cross or Cross-and-Retest entries; optionally allow a fast Momentum Exception when candles expand with volume.

* Manages positions with a structure exit (TrendBreak) and an emergency ATR stop from entry.

How it works (concepts & calculations)

* VWAP (session anchor):

Standard VWAP of the active session; entries reference the cross and the retest proximity to VWAP.

* Trend gate:

Long context only if `EMA(fast) > EMA(slow)`; short only if `EMA(fast) < EMA(slow)`.

A *gate*, not a trigger—entries aren’t considered unless this is true.

* Participation (volume) gate:

Require `volume > SMA(volume, volLen) × volMult`.

Screens out low-participation wiggles around VWAP.

Entries:

* Cross: Price crosses VWAP in the trend direction while volume gate is open.

* Cross-and-Retest: After crossing, price revisits VWAP vicinity within `lookback` (recent *low near VWAP* for longs; recent *high near VWAP* for shorts).

* Momentum Exception (optional): If body% (|close−open| / range) and volume exceed thresholds, enter without waiting for the retest.

Exits:

* TrendBreak (structure):

* Longs close when `price < VWAP` and `EMA(fast) < EMA(slow)` (mirror for shorts).

* ATR stop (risk):

* From entry: `stop = entry ± ATR(atrLen) × atrMult`.

How to use it ?

1. Select market & timeframe: Intraday on liquid symbols (equities, futures, crypto).

2. Pick entry mode:

* Start with Cross-and-Retest for fewer, more selective signals.

* Enable Momentum Exception if strong moves leave without retesting.

3. Tune guards:

* Raise `volMult` to ignore thin periods; lower it for more activity.

* Adjust `lookback` if retests come late/early on your symbol.

4. Risk:

* `atrLen` and `atrMult` set the emergency stop distance.

5. Read results per session: Optional panel (if enabled) summarizes Net-R, Win%, and PF for today’s session to evaluate

behavior regime by regime.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

Gann Fan Strategy [KedarArc Quant]Description

A single-concept, rule-based strategy that trades around a programmatic Gann Fan.

It anchors to a swing (or a manual point), builds 1×1 and related fan lines numerically, and triggers entries when price interacts with the 1×1 (breakout or bounce). Management is done entirely with the fan structure (next/previous line) plus optional ATR trailing.

What TV indicators are used

* Pivots: `ta.pivothigh/ta.pivotlow` to confirm swing highs/lows for anchor selection.

* ATR: `ta.atr` only to scale the 1×1 slope (optional) and for an optional trailing stop.

* EMA: `ta.ema` as a trend filter (e.g., only long above the EMA, short below).

No RSI/MACD/Stoch/Heikin/etc. The logic is one coherent framework: Gann price–time geometry, with ATR as a scale and EMA as a risk filter.

How it works

1. Anchor

* Auto: chooses the most recent *confirmed* pivot (you control Left/Right).

* Manual: set a price and bar index and the fan will hold that point (no re-anchoring).

* Optional Re-anchor when a newer pivot confirms.

2. 1×1 Slope (numeric, not cosmetic)

* ATR mode: `1×1 = ATR(Length) × Multiplier` (adapts to volatility).

* Fixed mode: `ticks per bar` (constant slope).

Because slope is numeric, it doesn’t change with chart zoom, unlike the drawing tool.

3. Fan Lines

Builds classic ratios around the 1×1: 1/8, 1/4, 1/3, 1/2, 1/1, 2/1, 3/1, 4/1, 8/1.

4. Signals

* Breakout: cross of price over/under the 1×1 in the EMA-aligned direction.

* Bounce (optional): touch + reversal across the 1×1 to reduce whipsaw.

5. Exits & Risk

* Take-profit at the next fan line; Stop at the previous fan line.

* If a level is missing (right after re-anchor), a fallback Risk-Reward (RR) is used.

* Optional ATR trailing stop.

Why this is unique

* True numeric fan: The 1×1 slope is calculated from ATR or fixed ticks—not from screen geometry—so it is scale-invariant and reproducible across users/timeframes.

* Deterministic anchor logic: Uses confirmed pivots (with your L/R settings). No look-ahead; anchors update only when the right bars complete.

* Fan-native trade management: Both entries and exits come from the fan structure itself (with a minimal ATR/EMA assist), keeping the method pure.

* Two entry archetypes: Breakout for momentum days; Bounce for range days—switchable without changing the core model.

* Manual mode: Lock a session’s bias by anchoring to a chosen swing (e.g., day’s first major low/high) and keep the fan constant all day.

Inputs (quick guide)

* Auto Anchor (Left/Right): pivot sensitivity. Higher values = fewer, stronger anchors.

* Re-anchor: refresh to newer pivots as they confirm.

* Manual Anchor Price / Bar Index: fixes the fan (turn Auto off).

* Scale 1×1 by ATR: on = adaptive; off = use ticks per bar.

* ATR Length / ATR Multiplier: controls adaptive slope; start around 14 / 0.25–0.35.

* Ticks per bar: exact fixed slope (match a hand-drawn fan by computing slope ÷ mintick).

* EMA Trend Filter: e.g., 50–100; trades only in EMA direction.

* Use Bounce: require touch + reverse across 1×1 (helps in chop).

* TP/SL at fan lines; Fallback RR for missing levels; ATR Trailing Stop optional.

* Transparency/Plot EMA: visual preferences.

Tips

* Range days: larger pivots (L/R 8–12), Bounce ON, ATR Multiplier \~0.30–0.40, EMA 100.

* Trend days: L/R 5–6, Breakout, Multiplier \~0.20–0.30, EMA 50, ATR trail 1.0–1.5.

* Match the TV Gann Fan drawing: turn ATR scale OFF, set ticks per bar = `(Δprice between anchor and 1×1 target) / (bars) / mintick`.

Repainting & testing notes

* Pivots require Right bars to confirm; anchors are set after confirmation (no look-ahead).

* Signals use the current bar close with TradingView strategy mechanics; real-time vs. bar-close can differ slightly, as with any strategy.

* Re-anchoring legitimately moves the structure when new pivots confirm—by design.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

EMA20 Cross Strategy with countertrades and signalsEMA20 Cross Strategy Documentation

Overview

The EMA20 Cross Strategy with Counter-Trades and Instant Signals is a Pine Script (version 6) trading strategy designed for the TradingView platform. It implements an Exponential Moving Average (EMA) crossover system to generate buy and sell signals, with optional trend filtering, session-based trading, instant signal processing, and visual/statistical feedback. The strategy supports counter-trades (closing opposing positions before entering new ones) and operates with a fixed trade size in EUR.

Features

EMA Crossover Mechanism:

Uses a short-term EMA (configurable length, default: 1) and a long-term EMA (default: 20) to detect crossovers.

A buy signal is generated when the short EMA crosses above the long EMA.

A sell signal is generated when the short EMA crosses below the long EMA.

Instant Signals:

If enabled (useInstantSignals), signals are based on the current price crossing the short EMA, rather than waiting for the candle close.

This allows faster trade execution but may increase sensitivity to price fluctuations.

Trend Filter:

Optionally filters trades based on the trend direction (useTrendFilter).

Long trades are allowed only when the short EMA (or price, for instant signals) is above the long EMA.

Short trades are allowed only when the short EMA (or price) is below the long EMA.

Session Filter:

Restricts trading to specific market hours (sessionStart, default: 09:00–17:00) if enabled (useSessionFilter).

Ensures trades occur only during active market sessions, reducing exposure to low-liquidity periods.

Customizable Timeframe:

The EMA calculations can use a higher timeframe (e.g., 5m, 15m, 1H, 4H, 1D, default: 1H) via request.security.

This allows the strategy to base signals on longer-term trends while operating on a shorter-term chart.

Trade Management:

Fixed trade size of €100,000 per trade (tradeAmount), with a maximum quantity cap (maxQty = 10,000) to prevent oversized trades.

Counter-trades: Closes short positions before entering a long position and vice versa.

Trades are executed with a minimum quantity of 1 to ensure valid orders.

Visualization:

EMA Lines: The short EMA is colored based on the last signal (green for buy, red for sell, gray for neutral), and the long EMA is orange.

Signal Markers: Displays buy/sell signals as arrows (triangles) above/below candles if enabled (showSignalShapes).

Background/Candle Coloring: Optionally colors the chart background or candles green (bullish) or red (bearish) based on the trend (useColoredBars).

Statistics Display:

If enabled (useStats), a label on the chart shows:

Total closed trades

Open trades

Win rate (%)

Number of winning/losing trades

Profit factor (gross profit / gross loss)

Net profit

Maximum drawdown

Configuration Inputs

EMA Short Length (emaLength): Length of the short-term EMA (default: 1).

Trend EMA Length (trendLength): Length of the long-term EMA (default: 20).

Enable Trend Filter (useTrendFilter): Toggles trend-based filtering (default: true).

Color Candles (useColoredBars): Colors candles instead of the background (default: true).

Enable Session Filter (useSessionFilter): Restricts trading to specified hours (default: false).

Trading Session (sessionStart): Defines trading hours (default: 09:00–17:00).

Show Statistics (useStats): Displays performance stats on the chart (default: true).

Show Signal Arrows (showSignalShapes): Displays buy/sell signals as arrows (default: true).

Use Instant Signals (useInstantSignals): Generates signals based on live price action (default: false).

EMA Timeframe (emaTimeframe): Timeframe for EMA calculations (options: 5m, 15m, 1H, 4H, 1D; default: 1H).

Strategy Logic

Signal Generation:

Standard Mode: Signals are based on EMA crossovers (short EMA crossing long EMA) at candle close.

Instant Mode: Signals are based on the current price crossing the short EMA, enabling faster reactions.

Trade Execution:

On a buy signal, closes any short position and opens a long position.

On a sell signal, closes any long position and opens a short position.

Position size is calculated as the minimum of €100,000 or available equity, divided by the current price, capped at 10,000 units.

Filters:

Trend Filter: Ensures trades align with the trend direction (if enabled).

Session Filter: Restricts trades to user-defined market hours (if enabled).

Visual Feedback

EMA Lines: Provide a clear view of the short and long EMAs, with the short EMA’s color reflecting the latest signal.

Signal Arrows: Large green triangles (buy) below candles or red triangles (sell) above candles for easy signal identification.

Chart Coloring: Highlights bullish (green) or bearish (red) trends via background or candle colors.

Statistics Label: Displays key performance metrics in a label above the chart for quick reference.

Usage Notes

Initial Capital: €100,000 (configurable via initial_capital).

Currency: EUR (set via currency).

Order Processing: Orders are processed at candle close (process_orders_on_close=true) unless instant signals are enabled.

Dynamic Requests: Allows dynamic timeframe adjustments for EMA calculations (dynamic_requests=true).

Platform: Designed for TradingView, compatible with any market supported by the platform (e.g., stocks, forex, crypto).

Example Use Case

Scenario: Trading on a 5-minute chart with a 1-hour EMA timeframe, trend filter enabled, and session filter set to 09:00–17:00.

Behavior: The strategy will:

Calculate EMAs on the 1-hour timeframe.

Generate buy signals when the short EMA crosses above the long EMA (and price is above the long EMA).

Generate sell signals when the short EMA crosses below the long EMA (and price is below the long EMA).

Execute trades only during 09:00–17:00.

Display green/red candles and performance stats on the chart.

Limitations

Instant Signals: May lead to more frequent signals, increasing the risk of false positives in volatile markets.

Fixed Trade Size: Does not adjust dynamically based on market conditions beyond equity and max quantity limits.

Session Filter: Simplified and may not account for complex session rules or holidays.

Statistics: Displayed on-chart, which may clutter the view in smaller charts.

Customization

Adjust emaLength and trendLength to suit different market conditions (e.g., shorter for scalping, longer for swing trading).

Toggle useInstantSignals for faster or more stable signal generation.

Modify sessionStart to align with specific market hours.

Disable useStats or showSignalShapes for a cleaner chart.

This strategy is versatile for both manual and automated trading, offering flexibility for various markets and trading styles while providing clear visual and statistical feedback.

Optimized ADX DI CCI Strategy### Key Features:

- Combines ADX, DI+/-, CCI, and RSI for signal generation.

- Supports customizable timeframes for indicators.

- Offers multiple exit conditions (Moving Average cross, ADX change, performance-based stop-loss).

- Tracks and displays trade statistics (e.g., win rate, capital growth, profit factor).

- Visualizes trades with labels and optional background coloring.

- Allows countertrading (opening an opposite trade after closing one).

1. **Indicator Calculation**:

- **ADX and DI+/-**: Calculated using the `ta.dmi` function with user-defined lengths for DI and ADX smoothing.

- **CCI**: Computed using the `ta.cci` function with a configurable source (default: `hlc3`) and length.

- **RSI (optional)**: Calculated using the `ta.rsi` function to filter overbought/oversold conditions.

- **Moving Averages**: Used for CCI signal smoothing and trade exits, with support for SMA, EMA, SMMA (RMA), WMA, and VWMA.

2. **Signal Generation**:

- **Buy Signal**: Triggered when DI+ > DI- (or DI+ crosses over DI-), CCI > MA (or CCI crosses over MA), and optional ADX/RSI filters are satisfied.

- **Sell Signal**: Triggered when DI+ < DI- (or DI- crosses over DI+), CCI < MA (or CCI crosses under MA), and optional ADX/RSI filters are satisfied.

3. **Trade Execution**:

- **Entry**: Long or short trades are opened using `strategy.entry` when signals are detected, provided trading is allowed (`allow_long`/`allow_short`) and equity is positive.

- **Exit**: Trades can be closed based on:

- Opposite signal (if no other exit conditions are used).

- MA cross (price crossing below/above the exit MA for long/short trades).

- ADX percentage change exceeding a threshold.

- Performance-based stop-loss (trade loss exceeding a percentage).

- **Countertrading**: If enabled, closing a trade triggers an opposite trade (e.g., closing a long opens a short).

4. **Visualization**:

- Labels are plotted at trade entries/exits (e.g., "BUY," "SELL," arrows).

- Optional background coloring highlights open trades (green for long, red for short).

- A statistics table displays real-time metrics (e.g., capital, win rates).

5. **Trade Tracking**:

- Tracks the number of long/short trades, wins, and overall performance.

- Monitors equity to prevent trading if it falls to zero.

### 2.3 Key Components

- **Indicator Calculations**: Uses `request.security` to fetch indicator data for the specified timeframe.

- **MA Function**: A custom `ma_func` handles different MA types for CCI and exit conditions.

- **Signal Logic**: Combines crossover/under checks with recent bar windows for flexibility.

- **Exit Conditions**: Multiple configurable exit strategies for risk management.

- **Statistics Table**: Updates dynamically with trade and capital metrics.

## 3. Configuration Options

The script provides extensive customization through input parameters, grouped for clarity in the TradingView settings panel. Below is a detailed breakdown of each setting and its impact.

### 3.1 Strategy Settings (Global)

- **Initial Capital**: Default `10000`. Sets the starting capital for backtesting.

- **Effect**: Determines the base equity for calculating position sizes and performance metrics.

- **Default Quantity Type**: `strategy.percent_of_equity` (50% of equity).

- **Effect**: Controls the size of each trade as a percentage of available equity.

- **Pyramiding**: Default `2`. Allows up to 2 simultaneous trades in the same direction.

- **Effect**: Enables multiple entries if conditions are met, increasing exposure.

- **Commission**: 0.2% per trade.

- **Effect**: Simulates trading fees, reducing net profit in backtesting.

- **Margin**: 100% for long and short trades.

- **Effect**: Assumes no leverage; adjust for margin trading simulations.

- **Calc on Every Tick**: `true`.

- **Effect**: Ensures real-time signal updates for precise execution.

### 3.2 Indicator Settings

- **Indicator Timeframe** (`indicator_timeframe`):

- **Options**: `""` (chart timeframe), `1`, `5`, `15`, `30`, `60`, `240`, `D`, `W`.

- **Default**: `""` (uses chart timeframe).

- **Effect**: Determines the timeframe for ADX, DI, CCI, and RSI calculations. A higher timeframe reduces noise but may delay signals.

### 3.3 ADX & DI Settings

- **DI Length** (`adx_di_len`):

- **Default**: `30`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for calculating DI+ and DI-. Longer periods smooth trends but reduce sensitivity.

- **ADX Smoothing Length** (`adx_smooth_len`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Smooths the ADX calculation. Longer periods produce smoother ADX values.

- **Use ADX Filter** (`use_adx_filter`):

- **Default**: `false`.

- **Effect**: If `true`, requires ADX to exceed the threshold for signals to be valid, filtering out weak trends.

- **ADX Threshold** (`adx_threshold`):

- **Default**: `25`.

- **Range**: Minimum `0`.

- **Effect**: Sets the minimum ADX value for valid signals when the filter is enabled. Higher values restrict trades to stronger trends.

### 3.4 CCI Settings

- **CCI Length** (`cci_length`):

- **Default**: `20`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for CCI calculation. Longer periods reduce noise but may lag.

- **CCI Source** (`cci_src`):

- **Default**: `hlc3` (average of high, low, close).

- **Effect**: Defines the price data for CCI. `hlc3` is standard, but users can choose other sources (e.g., `close`).

- **CCI MA Type** (`ma_type`):

- **Options**: `SMA`, `EMA`, `SMMA (RMA)`, `WMA`, `VWMA`.

- **Default**: `SMA`.

- **Effect**: Determines the moving average type for CCI signal smoothing. EMA is more responsive; VWMA weights by volume.

- **CCI MA Length** (`ma_length`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for the CCI MA. Longer periods smooth the MA but may delay signals.

### 3.5 RSI Filter Settings

- **Use RSI Filter** (`use_rsi_filter`):

- **Default**: `false`.

- **Effect**: If `true`, applies RSI-based overbought/oversold filters to signals.

- **RSI Length** (`rsi_length`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for RSI calculation. Longer periods reduce sensitivity.

- **RSI Lower Limit** (`rsi_lower_limit`):

- **Default**: `30`.

- **Range**: `0` to `100`.

- **Effect**: Defines the oversold threshold for buy signals. Lower values allow trades in more extreme conditions.

- **RSI Upper Limit** (`rsi_upper_limit`):

- **Default**: `70`.

- **Range**: `0` to `100`.

- **Effect**: Defines the overbought threshold for sell signals. Higher values allow trades in more extreme conditions.

### 3.6 Signal Settings

- **Cross Window** (`cross_window`):

- **Default**: `0`.

- **Range**: `0` to `5` bars.

- **Effect**: Specifies the lookback period for detecting DI+/- or CCI crosses. `0` requires crosses on the current bar; higher values allow recent crosses, increasing signal frequency.

- **Allow Long Trades** (`allow_long`):

- **Default**: `true`.

- **Effect**: Enables/disables new long trades. If `false`, only closing existing longs is allowed.

- **Allow Short Trades** (`allow_short`):

- **Default**: `true`.

- **Effect**: Enables/disables new short trades. If `false`, only closing existing shorts is allowed.

- **Require DI+/DI- Cross for Buy** (`buy_di_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a DI+ crossover DI- for buy signals; if `false`, DI+ > DI- is sufficient.

- **Require CCI Cross for Buy** (`buy_cci_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a CCI crossover MA for buy signals; if `false`, CCI > MA is sufficient.

- **Require DI+/DI- Cross for Sell** (`sell_di_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a DI- crossover DI+ for sell signals; if `false`, DI+ < DI- is sufficient.

- **Require CCI Cross for Sell** (`sell_cci_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a CCI crossunder MA for sell signals; if `false`, CCI < MA is sufficient.

- **Countertrade** (`countertrade`):

- **Default**: `true`.

- **Effect**: If `true`, closing a trade triggers an opposite trade (e.g., close long, open short) if allowed.

- **Color Background for Open Trades** (`color_background`):

- **Default**: `true`.

- **Effect**: If `true`, colors the chart background green for long trades and red for short trades.

### 3.7 Exit Settings

- **Use MA Cross for Exit** (`use_ma_exit`):

- **Default**: `true`.

- **Effect**: If `true`, closes trades when the price crosses the exit MA (below for long, above for short).

- **MA Length for Exit** (`ma_exit_length`):

- **Default**: `20`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for the exit MA. Longer periods delay exits.

- **MA Type for Exit** (`ma_exit_type`):

- **Options**: `SMA`, `EMA`, `SMMA (RMA)`, `WMA`, `VWMA`.

- **Default**: `SMA`.

- **Effect**: Determines the MA type for exit signals. EMA is more responsive; VWMA weights by volume.

- **Use ADX Change Stop-Loss** (`use_adx_stop`):

- **Default**: `false`.

- **Effect**: If `true`, closes trades when the ADX changes by a specified percentage.

- **ADX % Change for Stop-Loss** (`adx_change_percent`):

- **Default**: `5.0`.

- **Range**: Minimum `0.0`, step `0.1`.

- **Effect**: Specifies the percentage change in ADX (vs. previous bar) that triggers a stop-loss. Higher values reduce premature exits.

- **Use Performance Stop-Loss** (`use_perf_stop`):

- **Default**: `false`.

- **Effect**: If `true`, closes trades when the loss exceeds a percentage threshold.

- **Performance Stop-Loss (%)** (`perf_stop_percent`):

- **Default**: `-10.0`.

- **Range**: `-100.0` to `0.0`, step `0.1`.

- **Effect**: Specifies the loss percentage that triggers a stop-loss. More negative values allow larger losses before exiting.

## 4. Visual and Statistical Output

- **Labels**: Displayed at trade entries/exits with arrows (↑ for buy, ↓ for sell) and text ("BUY," "SELL"). A "No Equity" label appears if equity is zero.

- **Background Coloring**: Optionally colors the chart background (green for long, red for short) to indicate open trades.

- **Statistics Table**: Displayed at the top center of the chart, updated on timeframe changes or trade events. Includes:

- **Capital Metrics**: Initial capital, current capital, capital growth (%).

- **Trade Metrics**: Total trades, long/short trades, win rate, long/short win rates, profit factor.

- **Open Trade Status**: Indicates if a long, short, or no trade is open.

## 5. Alerts

- **Buy Signal Alert**: Triggered when `buy_signal` is true ("Cross Buy Signal").

- **Sell Signal Alert**: Triggered when `sell_signal` is true ("Cross Sell Signal").

- **Usage**: Users can set up TradingView alerts to receive notifications for trade signals.

EMA 1/8 Cross - Fixed Pip TP/SLEMA 1/8 Cross – Fixed Pip TP/SL

This strategy is based on the crossover between EMA 8 and EMA 14 as trading signals:

Long entry → when EMA 1 crosses above EMA 8

Short entry → when EMA 1 crosses below EMA 8

Features:

Fixed pip Take Profit (TP) and Stop Loss (SL), fully adjustable in the settings.

Customizable EMA Fast/Slow lengths for optimization.

Pip size input to match different broker definitions (e.g., XAUUSD often uses 0.10 as one pip).

Suitable for testing scalping or swing trading across multiple timeframes.

⚠️ Disclaimer:

This script is intended for backtesting and educational purposes only. Please optimize parameters and apply proper risk management before using it on live accounts.

AltCoin & MemeCoin Index Correlation [Eddie_Bitcoin]🧠 Philosophy of the Strategy

The AltCoin & MemeCoin Index Correlation Strategy by Eddie_Bitcoin is a carefully engineered trend-following system built specifically for the highly volatile and sentiment-driven world of altcoins and memecoins.

This strategy recognizes that crypto markets—especially niche sectors like memecoins—are not only influenced by individual price action but also by the relative strength or weakness of their broader sector. Hence, it attempts to improve the reliability of trading signals by requiring alignment between a specific coin’s trend and its sector-wide index trend.

Rather than treating each crypto asset in isolation, this strategy dynamically incorporates real-time dominance metrics from custom indices (OTHERS.D and MEME.D) and combines them with local price action through dual exponential moving average (EMA) crossovers. Only when both the asset and its sector are moving in the same direction does it allow for trade entries—making it a confluence-based system rather than a single-signal strategy.

It supports risk-aware capital allocation, partial exits, configurable stop loss and take profit levels, and a scalable equity-compounding model.

✅ Why did I choose OTHERS.D and MEME.D as reference indices?

I selected OTHERS.D and MEME.D because they offer a sector-focused view of crypto market dynamics, especially relevant when trading altcoins and memecoins.

🔹 OTHERS.D tracks the market dominance of all cryptocurrencies outside the top 10 by market cap.

This excludes not only BTC and ETH, but also major stablecoins like USDT and USDC, making it a cleaner indicator of risk appetite across true altcoins.

🔹 This is particularly useful for detecting "Altcoin Season"—periods where capital rotates away from Bitcoin and flows into smaller-cap coins.

A rising OTHERS.D often signals the start of broader altcoin rallies.

🔹 MEME.D, on the other hand, captures the speculative behavior of memecoin segments, which are often driven by retail hype and social media activity.

It's perfect for timing momentum shifts in high-risk, high-reward tokens.

By using these indices, the strategy aligns entries with broader sector trends, filtering out noise and increasing the probability of catching true directional moves, especially in phases of capital rotation and altcoin risk-on behavior.

📐 How It Works — Core Logic and Execution Model

At its heart, this strategy employs dual EMA crossover detection—one pair for the asset being traded and one pair for the selected market index.

A trade is only executed when both EMA crossovers agree on the direction. For example:

Long Entry: Coin's fast EMA > slow EMA and Index's fast EMA > slow EMA

Short Entry: Coin's fast EMA < slow EMA and Index's fast EMA < slow EMA

You can disable the index filter and trade solely based on the asset’s trend just to make a comparison and see if improves a classic EMA crossover strategy.

Additionally, the strategy includes:

- Adaptive position sizing, based on fixed capital or current equity (compound mode)

- Take Profit and Stop Loss in percentage terms

- Smart partial exits when trend momentum fades

- Date filtering for precise backtesting over specific timeframes

- Real-time performance stats, equity tracking, and visual cues on chart

⚙️ Parameters & Customization

🔁 EMA Settings

Each EMA pair is customizable:

Coin Fast EMA: Default = 47

Coin Slow EMA: Default = 50

Index Fast EMA: Default = 47

Index Slow EMA: Default = 50

These control the sensitivity of the trend detection. A wider spread gives smoother, slower entries; a narrower spread makes it more responsive.

🧭 Index Reference

The correlation mechanism uses CryptoCap sector dominance indexes:

OTHERS.D: Dominance of all coins EXCLUDING Top 10 ones

MEME.D: Dominance of all Meme coins

These are dynamically calculated using:

OTHERS_D = OTHERS_cap / TOTAL_cap * 100

MEME_D = MEME_cap / TOTAL_cap * 100

You can select:

Reference Index: OTHERS.D or MEME.D

Or disable the index reference completely (Don't Use Index Reference)

💰 Position Sizing & Risk Management

Two capital allocation models are supported:

- Fixed % of initial capital (default)

- Compound profits, which scales positions as equity grows

Settings:

- Compound profits?: true/false

- % of equity: Between 1% and 200% (default = 10%)

This is critical for users who want to balance growth with risk.

🎯 Take Profit / Stop Loss

Customizable thresholds determine automatic exits:

- TakeProfit: Default = 99999 (disabled)

- StopLoss: Default = 5 (%)

These exits are percentage-based and operate off the entry price vs. current close.

📉 Trend Weakening Exit (Scale Out)

If the position is in profit but the trend weakens (e.g., EMA color signals trend loss), the strategy can partially close a configurable portion of the position:

- Scale Position on Weak Trend?: true/false

- Scaled Percentage: % to close (default = 65%)

This feature is useful for preserving profits without exiting completely.

📆 Date Filter

Useful for segmenting performance over specific timeframes (e.g., bull vs bear markets):

- Filter Date Range of Backtest: ON/OFF

- Start Date and End Date: Custom time range

OTHER PARAMETERS EXPLANATION (Strategy "Properties" Tab):

- Initial Capital is set to 100 USD

- Commission is set to 0.055% (The ones I have on Bybit)

- Slippage is set to 3 ticks

- Margin (short and long) are set to 0.001% to avoid "overspending" your initial capital allocation

📊 Visual Feedback and Debug Tools

📈 EMA Trend Visualization

The slow EMA line is dynamically color-coded to visually display the alignment between the asset trend and the index trend:

Lime: Coin and index both bullish

Teal: Only coin bullish

Maroon: Only index bullish

Red: Both bearish

This allows for immediate visual confirmation of current trend strength.

💬 Real-Time PnL Labels

When a trade closes, a label shows:

Previous trade return in % (first value is the effective PL)

Green background for profit, Red for losses.

📑 Summary Table Overlay

This table appears in a corner of the chart (user-defined) and shows live performance data including:

Trade direction (yellow long, purple short)

Emojis: 💚 for current profit, 😡 for current loss

Total number of trades

Win rate

Max drawdown

Duration in days

Current trade profit/loss (absolute and %)

Cumulative PnL (absolute and %)

APR (Annualized Percentage Return)

Each metric is color-coded:

Green for strong results

Yellow/orange for average

Red/maroon for poor performance

You can select where this appears:

Top Left

Top Right

Bottom Left

Bottom Right (default)

📚 Interpretation of Key Metrics

Equity Multiplier: How many times initial capital has grown (e.g., “1.75x”)

Net Profit: Total gains including open positions

Max Drawdown: Largest peak-to-valley drop in strategy equity

APR: Annualized return calculated based on equity growth and days elapsed

Win Rate: % of profitable trades

PnL %: Percentage profit on the most recent trade

🧠 Advanced Logic & Safety Features

🛑 “Don’t Re-Enter” Filter

If a trade is closed due to StopLoss without a confirmed reversal, the strategy avoids re-entering in that same direction until conditions improve. This prevents false reversals and repetitive losses in sideways markets.

🧷 Equity Protection

No new trades are initiated if equity falls below initial_capital / 30. This avoids overleveraging or continuing to trade when capital preservation is critical.

Keep in mind that past results in no way guarantee future performance.

Eddie Bitcoin

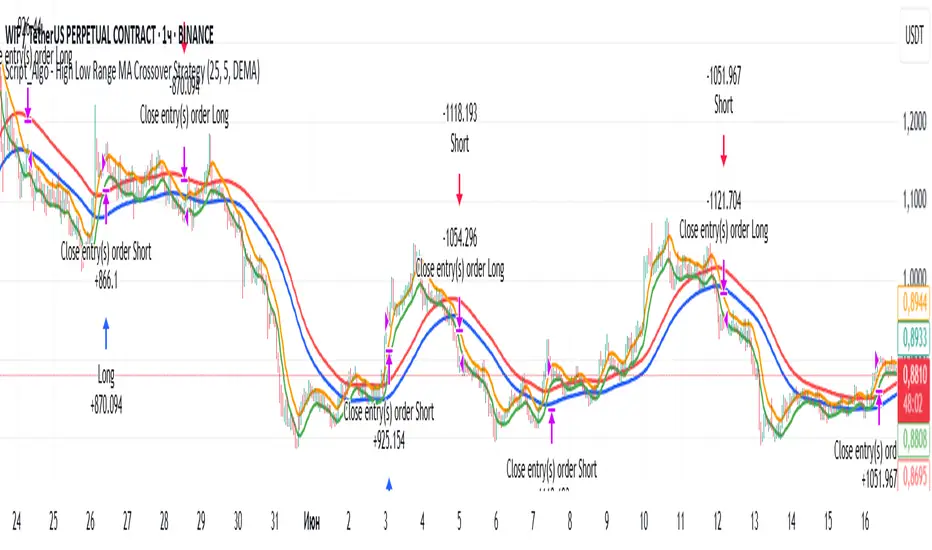

Script_Algo - High Low Range MA Crossover Strategy🎯 Core Concept

This strategy uses modified moving averages crossover, built on maximum and minimum prices, to determine entry and exit points in the market. A key advantage of this strategy is that it avoids most false signals in trendless conditions, which is characteristic of traditional moving average crossover strategies. This makes it possible to improve the risk/reward ratio and, consequently, the strategy's profitability.

📊 How the Strategy Works

Main Mechanism

The strategy builds 4 moving averages:

Two senior MAs (on high and low) with a longer period

Two junior MAs (on high and low) with a shorter period

Buy signal 🟢: when the junior MA of lows crosses above the senior MA of highs

Sell signal 🔴: when the junior MA of highs crosses below the senior MA of lows

As seen on the chart, it was potentially possible to make 9X on the WIFUSDT cryptocurrency pair in just a year and a half. However, be careful—such results may not necessarily be repeated in the future.

Special Feature

Position closing priority ❗: if an opposite signal arrives while a position is open, the strategy first closes the current position and only then opens a new one

⚙️ Indicator Settings

Available Moving Average Types

EMA - Exponential MA

SMA - Simple MA

SSMA - Smoothed MA

WMA - Weighted MA

VWMA - Volume Weighted MA

RMA - Adaptive MA

DEMA - Double EMA

TEMA - Triple EMA

Adjustable Parameters

Senior MA Length - period for long-term moving averages

Junior MA Length - period for short-term moving averages

✅ Advantages of the Strategy

🛡️ False Signal Protection - using two pairs of modified MAs reduces the number of false entries

🔄 Configuration Flexibility - ability to choose MA type and calculation periods

⚡ Automatic Switching - the strategy automatically closes the current position when receiving an opposite signal

📈 Visual Clarity - all MAs are displayed on the chart in different colors

⚠️ Disadvantages and Risks

📉 Signal Lag - like all MA-based strategies, it may provide delayed signals during sharp movements

🔁 Frequent Switching - in sideways markets, it may lead to multiple consecutive position openings/closings

📊 Requires Optimization - optimal parameters need to be selected for different instruments and timeframes

💡 Usage Recommendations

Backtest - test the strategy's performance on historical data

Optimize Parameters - select MA periods suitable for the specific trading instrument

Use Filters - add additional filters to confirm signals

Manage Risks - always use stop-loss and take-profit orders.

You can safely connect to the exchange via webhook and enjoy trading.

Good luck and profits to everyone!!

Script_Algo - Fibo Correction Strategy🔹 Core Concept

The strategy is built on combining Fibonacci retracement levels, candlestick pattern confirmation, and trend filtering for trade selection. It performs well on the 1-hour timeframe across many cryptocurrency pairs. Particularly on LINKUSDT over the past year and a half, despite the not very optimal 1:1 risk/reward ratio.

The logic is simple: after a strong impulse move, the price often retraces to key Fibonacci levels (specifically, the 61.8% level). If a confirming candlestick (pattern) appears at this moment, the strategy looks for an entry in the direction of the main trend.

🔹 Indicators Used in the Strategy

ATR (Average True Range) — Used to calculate the stop-loss and take-profit levels.

EMA (9 and 21) — Additional moving averages for assessing the direction of movement (not directly used in entry conditions, but the logic can be expanded to include them).

SMA (Trend Filter, 20 by default) — The trend direction filter. Trades are only opened in its direction.

Fibonacci Levels — The 61.8% retracement level is calculated based on the high and low of the previous candle.

🔹 Entry Conditions

🟢 Long (Buy):

Previous Candle:

Must be green (close higher than open).

Must have a body not smaller than a specified minimum.

The upper wick must not exceed 30% of the body size.

→ This filters out "weak" or "indecisive" candles.

Current Candle:

Price touches or breaches the Fibonacci 61.8% retracement level from the previous range.

Closes above this level.

Closes above the Trend Filter (SMA) line.

A position is opened only if there are no other open trades at the moment.

🔴 Short (Sell):

Previous Candle:

Must be red (close lower than open).

Must have a body not smaller than a specified minimum.

The lower wick must not exceed 30% of the body size.

Current Candle:

Price touches or breaches the Fibonacci 61.8% retracement level from the previous range.

Closes below this level.

Closes below the Trend Filter (SMA) line.

A trade is opened only if there are no other open positions.

🔹 Risk Management

Stop-Loss = ATR × multiplier (default is 5).

Take-Profit = ATR × the same multiplier.

Thus, the default risk/reward ratio is 1:1, but it can be easily adjusted by changing the coefficient. Although, strangely enough, this ratio has shown the best results on some assets on the 1-hour timeframe.

🔹 Chart Visualization

Fibonacci level for Long — Green line with circles.

Fibonacci level for Short — Red line with circles.

Trend Filter line (SMA) — Blue.

🔹 Strengths of the Strategy

✅ Utilizes a proven market pattern — retracement to the 61.8% level.

✅ Further filters entries using trend and candlestick patterns.

✅ Simple, transparent logic that is easy to expand (e.g., adding other Fib levels, an EMA filter, etc.).

🔹 Limitations

⚠️ Performs better in trending markets; can generate false signals during ranging (sideways) conditions.

⚠️ The fixed 1:1 risk/reward ratio is not always optimal and could be refined.

⚠️ Performance depends on the selected timeframe and ATR parameters.

📌 Summary:

The strategy seeks corrective entries in the direction of the trend, confirmed by candlestick patterns. It is versatile and can be applied to forex pairs, cryptocurrencies, and stocks.

⚠️ Not financial advice. Pay close attention to risk management to avoid blowing your account. The strategy is not repainting — I have personally verified it through real testing — but it may not necessarily replicate the same results in the future, as the market is constantly changing. Test it, profit, and good luck to everyone!

PowerTrend Pro Strategy – Gold OptimizedTired of false signals on Gold?

PowerTrend Pro combines VWAP, Supertrend, RSI, and smart MA filters with trailing stops & break-even logic to deliver high-probability trades on XAUUSD.

PowerTrend Pro Strategy is a professional-grade trading system designed to capture high-probability swing and intraday opportunities on XAUUSD (Gold) and other volatile markets.

🔑 Core Features

VWAP Anchoring – institutional fair value reference to filter trades.

Supertrend (ATR-based) – adaptive trend filter tuned for Gold’s volatility.

Multi-Timeframe RSI – confirms momentum alignment across intraday and higher timeframe.

EMA + SMA Combo – ensures trades follow strong directional bias, reducing false signals.

Dynamic Risk Management

Adjustable Take Profit / Stop Loss (%)

Trailing Stop that locks in profits on extended moves

Break-Even Logic (stop loss moves to entry once price is in profit)

⚡ Gold-Tuned Presets

XAUUSD 1H → tighter TP/SL & faster entries for active intraday trading.

XAUUSD 4H → wider ATR filter & trailing stops to capture bigger swings.

Generic Mode → works on Forex, Indices, and Crypto (fully customizable).

🎯 Why It Works

Gold is notoriously volatile — quick spikes wipe out weak strategies. PowerTrend Pro solves this by combining:

✅ Institutional bias (VWAP)

✅ Adaptive trend filter (Supertrend)

✅ Momentum confirmation (RSI MTF)

✅ Robust trend structure (EMA + SMA)

✅ Smart exits (TP, SL, trailing & breakeven)

This multi-layer confirmation makes entries stronger and keeps risk under control.

🛠️ Usage

Add the strategy to your chart.

Choose a preset (XAUUSD 1H, 4H, or Generic).

Run Strategy Tester for performance metrics.

Optimize TP/SL and ATR values for your broker & market conditions.

🔥 Pro Tip: Combine this strategy with a session filter (London/NY overlap) or volume confirmation to boost accuracy in Gold.

Nifty Power -> Nifty 50 chart + EMA of RSI + avg volume strategyThis strategy works in 1 hour candle in Nifty 50 chart. In this strategy, upward trade takes place when there is a crossover of RSI 15 on EMA50 of RSI 15 and volume is greater than volume based EMA21. On the other hand, lower trade takes place when RSI 15 is less than EMA50 of RSI 15. Please note that there is no stop loss given and also that the trade will reverse as per the trend. Sometimes on somedays, there will be no trades. Also please note that this is an Intraday strategy. The trade if taken closes on 15:15 in Nifty 50. This strategy can be used for swing trading. Some pine script code such as supertrend and ema21 of close is redundant. Try not to get confused as only EMA50 of RSI 15 is used and EMA21 of volume is used. I am using built-in pinescript indicators and there is no special calculation done in the pine script code. I have taken numbars variable to count number of candles. For example, if you have 30 minuite chart then numbars variable will count the intraday candles accordingly and the same for 1 hour candles.

Supertrend EMA Vol Strategy V5### Supertrend EMA Strategy V5

**Overview**

This is a trend-following strategy designed for cryptocurrency markets like BTC/USD on daily timeframes, combining the Supertrend indicator for dynamic trailing stops with an EMA filter for trend confirmation. It aims to capture strong uptrends while avoiding counter-trend trades, with optional volume filtering for high-conviction entries and ATR-based stop-loss to manage risk. Ideal for long-only setups in bullish assets, it visually highlights trends with green/red bands and fills for easy interpretation. Backtested on BTC from 2024-2025, it shows potential for outperforming buy-and-hold in trending markets, but always use with proper risk management—past performance isn't indicative of future results.

**Key Features**

- **Supertrend Core**: Uses ATR to plot adaptive uptrend (green) and downtrend (red) lines, flipping on closes beyond prior bands for buy/sell signals.

- **EMA Trend Filter**: Entries require price above the EMA (default 21-period) for longs, ensuring alignment with the broader trend.

- **Volume Confirmation**: Optional filter only allows entries when volume exceeds its EMA (default 20-period), reducing false signals in low-activity periods.

- **Risk Controls**: Built-in ATR-multiplier stop-loss (default 2x) to cap losses; exits on Supertrend flips for trailing profits.

- **Visuals**: Green/red lines and highlighter fills for up/down trends, plus buy/sell labels and circles for signals.

- **Customizable Inputs**: Tweak ATR period (default 10), multiplier (default 3), EMA length, start date, long/short toggles, SL, and volume filter.

- **Alerts**: Built-in for buy/sell and direction changes.

**How to Use**

1. Add to your TradingView chart (e.g., BTC/USD 1D).

2. Adjust inputs: Start with defaults for trend-following; increase multiplier for fewer trades/higher win rate. Enable volume filter for volatile assets.

3. Monitor signals: Green "Buy" for long entries (if close > EMA and conditions met); red "Sell" for exits.

4. Backtest in Strategy Tester: Focus on equity curve, win rate (~50-60% in tests), and drawdown (<15% with SL).

5. Live Trading: Use small position sizes (1-2% risk per trade); combine with your analysis. Shorts disabled by default for bull-biased markets.

Trend Impulse Tester | Trend–Impulse–No-Chop (In development) Trend strategy. Regulate your entry and make the drawdown less than 3%, entry at % of capital. Currently under development.

Used on cryptocurrency. The 30 min timeframe was used. Adjust the values yourself, settings are provided

Options Strategy V2.0📈 Options Strategy V2.0 – Intraday Reversal-Resilient Momentum System

Overview:

This strategy is designed specifically for intraday SPY, TSLA, MSFT, etc. options trading (0DTE or 1DTE), using high-probability signals derived from a confluence of technical indicators: EMA crossovers, RSI thresholds, ATR-based risk control, and volume spikes. The strategy aims to capture strong directional moves while avoiding overtrading, thanks to a built-in cooldown logic and optional time/session filters.

⚙️ Core Concept

The strategy executes trades only in the direction of the prevailing trend, determined by short- and long-term Exponential Moving Averages (EMA). Entry signals are generated when the Relative Strength Index (RSI) confirms momentum in the direction of the trend, and volume spikes suggest institutional activity.

To increase adaptability and user control, it includes a highly customizable parameter set for both long and short entries independently.

📌 Key Features

✅ Trend-Following Logic

Long entries are only allowed when EMA(short) > EMA(long)

Short entries are only allowed when EMA(short) < EMA(long)

✅ RSI Confirmation

Long: Requires RSI crossover above a configurable threshold

Short: Requires RSI crossunder below a configurable threshold

Optional rejection filters: Entry blocked above/below specific RSI extremes

✅ Volume Spike Filter

Confirms institutional participation by comparing current volume to an average multiplied by a user-defined factor.

✅ ATR-Based Risk Management

Both Stop Loss (SL) and Take Profit (TP) are dynamically calculated using ATR × a multiplier.

TP/SL ratio is fully configurable.

✅ Cooldown Control

After every trade, the system waits for a set number of bars before allowing new entries.

This prevents overtrading and increases signal quality.

Optionally, cooldown is ignored for reversal trades, ensuring the system can react immediately to a confirmed trend change.

✅ Candle Body Filter (Noise Control)

Avoids trades on candles with too small bodies relative to wicks (often noise or indecision candles).

✅ VWAP Confirmation (Optional)

Ensures price is trading above VWAP for long entries, or below for short entries.

✅ Time & Session Filters

Trades only during regular market hours (09:30–16:00 EST).

No-trade zone (e.g., 14:15–15:45 EST) to avoid low-liquidity traps or late-day whipsaws.

✅ End-of-Day Auto Close

All open positions are force-closed at 15:55 EST, protecting against overnight risk (especially relevant for 0DTE options).

📊 Visual Aids

EMA plots show trend direction

VWAP line provides real-time mean-reversion context

Stop Loss and Take Profit lines appear dynamically with each trade

Alerts notify of entry signals and exit triggers

🔧 Customization Panel

Nearly every element of the strategy can be tailored:

EMA lengths (short and long, for both sides)

RSI thresholds and length

ATR length, SL multiplier, and TP/SL ratio

Volume spike sensitivity

Minimum EMA distance filter

Candle body ratio filter

Session restrictions

Cooldown logic (duration + reversal exception)

This makes the strategy extremely versatile, allowing both conservative and aggressive configurations depending on the trader’s profile and the market context.

📌 Example Use Case: SPY Options (0DTE or 1DTE)

This system was designed and tested specifically for SPY and other intraday options trading, where:

Delta is around 0.50 or higher

Trades are short-lived (often 1–5 candles)

You aim to trade 1–3 signals per day, filtering out weak entries

🚫 Important Notes

It is not a scalping strategy; it relies on confirmed breakouts with trend support

No pyramiding or re-entries without cooldown to preserve risk integrity

Should be used with real-time alerts and manual broker execution

📈 Alerts Included

📈 Long Entry Signal

📉 Short Entry Signal

⚠️ Auto-closed all positions at 15:55 EST

✅ Proven Settings – Real Trades + Backtest Results

The current version of the strategy includes the optimal settings I’ve arrived at through extensive backtesting, as well as 3 months of real trading with consistent profitability. These results reflect real-world execution under live market conditions using 0DTE SPY options, with disciplined trade management and risk control.

🧠 Final Thoughts

Options Strategy V2.0 is a robust, highly tunable intraday strategy that blends momentum, trend-following, and volume confirmation. It is ideal for disciplined traders focused on SPY or other 0DTE/1DTE options, and it includes guardrails to reduce false signals and improve execution timing.

Perfect for those who seek precision, flexibility, and risk-defined setups—not blind automation.

Combo 2/20 EMA & Bandpass Filter by TamarokDescription:

This strategy combines a 2/20 exponential moving average (EMA) crossover with a custom bandpass filter to generate buy and sell signals.

Use the Fast EMA and Slow EMA inputs to adjust trend sensitivity, and the Bandpass Filter Length, Delta, and Zones to fine-tune momentum turns.

Signals occur when both EMA and BPF agree in direction, with optional reversal and time filters.

How to use:

1. Add the script to your chart in TradingView.

2. Adjust the EMA and BP Filter parameters to match your asset’s volatility.

3. Enable ‘Reverse Signals’ to trade counter-trend, or use the time filter to limit sessions.

4. Set alerts on Long Alert and Short Alert for automated notifications.

Inspiration:

Based on HPotter’s original combo strategy (Stocks & Commodities Mar 2010).

Updated to Pine Script v6 with streamlined code and alerts.

WARNING:

For purpose educate only

EMA Grid + Martingale Strategy (Long-Only) with CooldownTitle:

EMA Grid + Martingale Strategy (Long-Only) with Cooldown

Short Summary:

A long-only strategy combining EMA trend filters, grid-based entries, optional martingale sizing, and a cooldown feature to manage position timing and exits.

Full Description:

This strategy uses a 4-EMA trend confirmation system to detect bullish momentum, then deploys a grid-style entry method with optional martingale position sizing. It includes a cooldown mechanism to prevent reentry too soon after a completed trade cycle.

How It Works

1. Trend Confirmation: Two EMA groups (fast/slow) determine whether market conditions are bullish.

2. Initial Entry: A new position is entered when both EMA groups confirm an uptrend and no position is currently active.

3. Grid Entries: Additional long entries are placed when price drops by a defined pip distance from the last entry, respecting the maximum number of entries.

4. Martingale Sizing (Optional): Grid orders can increase in size with each level using a customizable multiplier.

5. Weighted-Average Exit: All positions close once price reaches or exceeds the average entry price plus a buffer.

6. Cooldown Timer: After closing a position set, the strategy waits a defined number of bars before opening a new grid.

Key Features

• 4 customizable EMAs for trend confirmation.

• Dynamic grid-style long entries based on pip intervals.

• Optional martingale-style position sizing.

• Weighted-average price exit logic with buffer control.

• Cooldown bar period to limit overtrading.

• Suitable for optimization and backtesting with full control over inputs.

Use Cases

• Designed for trending markets where pullbacks present entry opportunities.

• Helps manage staged entries while avoiding premature reentry.

• Ideal for testing martingale and grid-based strategies with exit precision.

Note: This strategy is for testing and educational purposes only. It does not guarantee profits and is not financial advice.

Refined MA + Engulfing (M5 + Confirmed Structure Break)I would like to start by saying that this strategy was put together using ChatGPT, some past trades from myself and some backtested trades, and from my time as a student in Wallstreet Academy under Cue Banks.

I am not profitable yet. I am too jumpy and blow accounts. I'm hoping this strategy (and it's indicator twin) can help me spend less time on the charts, so that I'm not tempted to press buttons as much.

It does fire quite a bit. But, the Strategy Tester tab shows a 30% win rate with our wins being significant to our losses. So, in theory, if you followed the rules of this strategy STRICTLY, you COULD BE profitable.

With that being said, there are times that this strategy has shown to trigger and I ask, "Why?".

I just want to help myself and others, and maybe make some decent\cool stuff along the way. Enjoy

KR

EMA and Dow Theory Strategies🌐 Strategy Description

📘 Overview

This is a hybrid strategy that combines EMA crossovers, Dow Theory swing logic, and multi-timeframe trend overlays. It is suitable for intraday to short-term trading on any asset class: crypto, forex, stocks, and indices.

The strategy provides precise entry/exit signals, dynamic stop-loss and scale-out, and highly visual trade guidance.

🧠 Key Features

・Dual EMA crossover system (applied to both symbol and external index)

・Dow Theory-based swing high/low detection for trend confirmation

・Visual overlay of higher timeframe swing trend (htfTrend)

・RSI filter to avoid overbought/oversold entries

・Dynamic partial take-profit when trend weakens

・Custom stop-loss (%) control

・Visualized trade PnL labels directly on chart

・Alerts for entry, stop-loss, partial exit

・Gradient background zones for swing zones and trend visualization

・Auto-tracked metrics: APR, drawdown, win rate, equity curve

⚙️ Input Parameters

| Parameter | Description |

| ------------------------- | -------------------------------------------------------- |

| Fast EMA / Slow EMA | Periods for detecting local trend via EMAs |

| Index Fast EMA / Slow EMA | EMAs applied to external reference index |

| StopLoss | Maximum loss threshold in % |

| ScaleOut Threshold | Scale-out percentage when trend changes color |

| RSI Period / Levels | RSI period and overbought/oversold levels |

| Swing Detection Length | Number of bars used to detect swing highs/lows |

| Stats Display Options | Toggle PnL labels and position of statistics table |

🧭 About htfTrend (Higher Timeframe Trend)

The script includes a higher timeframe trend (htfTrend) calculated using Dow Theory (pivot highs/lows).

This trend is only used for visual guidance, not for actual entry conditions.

Why? Strictly filtering trades by higher timeframe often leads to missed opportunities and low frequency.

By keeping htfTrend visual-only, traders can still refer to macro structure but retain trade flexibility.

Use it as a contextual tool, not a constraint.

ストラテジー説明

📘 概要

本ストラテジーは、EMAクロスオーバー、ダウ理論によるスイング判定、**上位足トレンドの視覚表示(htfTrend)**を組み合わせた複合型の短期トレーディング戦略です。

仮想通貨・FX・株式・指数など幅広いアセットに対応し、デイトレード〜スキャルピング用途に適しています。

動的な利確/損切り、視覚的にわかりやすいエントリー/イグジット、統計表示を搭載しています。

🧠 主な機能

・対象銘柄+外部インデックスのEMAクロスによるトレンド判定

・ダウ理論に基づいたスイング高値・安値検出とトレンド判断

・上位足スイングトレンド(htfTrend)の視覚表示

・RSIフィルターによる過熱・売られすぎの回避

・トレンドの弱まりに応じた部分利確(スケールアウト)

・**損切り閾値(%)**をカスタマイズ可能

・チャート上に損益ラベル表示

・アラート完備(エントリー・決済・部分利確)

・トレンドゾーンを可視化する背景グラデーション

・勝率・ドローダウン・APR・資産増加率などの自動表示

| 設定項目名 | 説明内容 |

| --------------------- | -------------------------- |

| Fast EMA / Slow EMA | 銘柄に対して使用するEMAの期間設定 |

| Index Fast / Slow EMA | 外部インデックスのEMA設定 |

| 損切り(StopLoss) | 損切りラインのしきい値(%で指定) |

| 部分利確しきい値 | トレンド弱化時にスケールアウトする割合(%) |

| RSI期間・水準 | RSI計算期間と、過熱・売られすぎレベル設定 |

| スイング検出期間 | スイング高値・安値の検出に使用するバー数 |

| 統計表示の切り替え | 損益ラベルや統計テーブルの表示/非表示選択 |

🧭 上位足トレンド(htfTrend)について

本スクリプトには、上位足でのスイング高値・安値の更新に基づく**htfTrend(トレンド判定)が含まれています。

これは視覚的な参考情報であり、エントリーやイグジットには直接使用されていません。**

その理由は、上位足を厳密にロジックに組み込むと、トレード機会の損失が増えるためです。

このスクリプトでは、**判断の補助材料として「表示のみに留める」**設計を採用しています。

→ 裁量で「利確を早める」「逆張りを避ける」判断に活用可能です。

LANZ Strategy 5.0 [Backtest]🔷 LANZ Strategy 5.0 — Rule-Based BUY Logic with Time Filter, Session Limits and Auto SL/TP Execution

This is the backtest version of LANZ Strategy 5.0, built as a strategy script to evaluate real performance under fixed intraday conditions. It automatically places BUY and SELL trades based on structured candle confirmation, EMA trend alignment, and session-based filters. The system simulates real-time execution with precise Stop Loss and Take Profit levels.

📌 Built for traders seeking to simulate clean intraday logic with fully automated entries and performance metrics.

🧠 Core Logic & Strategy Conditions

✅ BUY Signal Conditions:

Price is above the EMA200

The last 3 candles are bullish (close > open)

The signal occurs within the defined session window (NY time)

Daily trade limit has not been exceeded

If all are true, a BUY order is executed at market, with SL and TP set immediately.

🔻 SELL Signal Conditions (Optional):

Exactly inverse to BUY (below EMA + 3 bearish candles). Disabled by default.

🕐 Operational Time Filter (New York Time)

You can fully customize your intraday window:

Start Time: e.g., 01:15 NY

End Time: e.g., 16:00 NY

The system evaluates signals only within this range, even across midnight if configured.

🔁 Trade Management System

One trade at a time per signal

Trades include a Stop Loss (SL) and Take Profit (TP) based on pip distance

Trade result is calculated automatically

Each signal is shown with a triangle marker (BUY only, by default)

🧪 Backtest Accuracy

This version uses:

strategy.order() for entries

strategy.exit() for SL and TP

strategy.close_all() at the configured manual closing time

This ensures realistic behavior in the TradingView strategy tester.

⚙️ Flow Summary (Step-by-Step)

On every bar, check:

Is the time within the operational session?

Is the price above the EMA?

Are the last 3 candles bullish?

If conditions met → A BUY trade is opened:

SL = entry – X pips

TP = entry + Y pips

Trade closes:

If SL or TP is hit

Or at the configured manual close time (e.g., 16:00 NY)

📊 Settings Overview

Timeframe: 1-hour (ideal)

SL/TP: Configurable in pips

Max trades/day: User-defined (default = 99 = unlimited)

Manual close: Adjustable by time

Entry type: Market (not limit)

Visuals: Plotshape triangle for BUY entry

👨💻 Credits:

💡 Developed by: LANZ

🧠 Strategy logic & execution: LANZ

✅ Designed for: Clean backtesting, clarity in execution, and intraday logic simulation

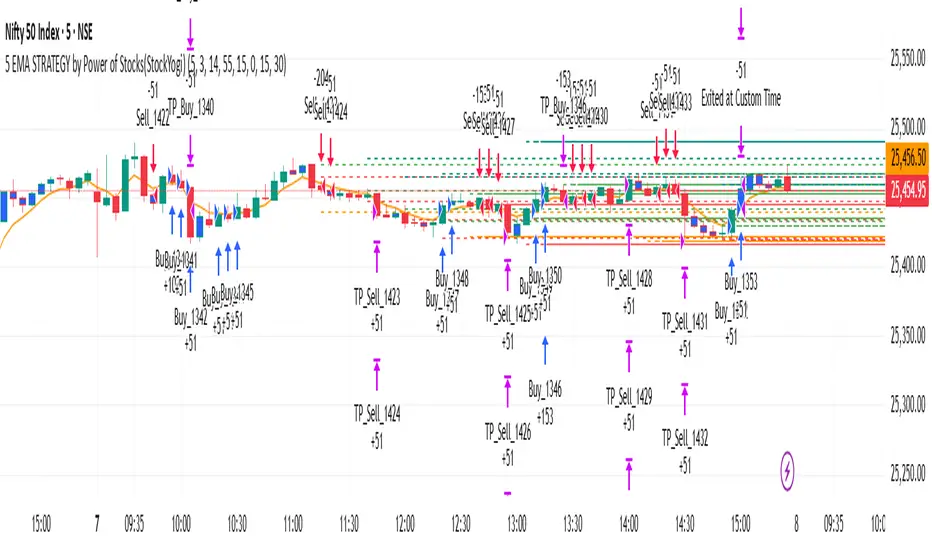

5 EMA STRATEGY by Power of Stocks(StockYogi)5 EMA STRATEGY by Power of Stocks(StockYogi)

This is a 5 EMA Breakout Strategy inspired by the trading principles taught by Shubhashi Pani, founder of the Power of Stocks (POS) community.

The strategy is designed to:

• Detect breakout setups when price breaks the high/low of a signal candle (based on EMA conditions)

• Enter trades only if the breakout occurs within the next 3 candles

• Allow multiple trades in the same direction without closing the earlier one

• Use independent stop-loss (SL) and take-profit (TP) targets for each trade based on a user-defined risk-reward ratio

• Optionally enter trades only at candle close

• Optionally avoid trades during a custom time window (e.g., 3:00 PM to 3:30 PM IST)

• Optionally close all open positions at a defined time (e.g., 3:30 PM IST)

The goal of this strategy is to provide greater flexibility and realism for intraday or short-term traders following structured breakout systems.

Disclaimer: This script is an implementation of technical ideas for educational purposes only. It is not financial advice. All trading involves risk, and past performance does not guarantee future results.

Strategy Credits:

This strategy is based on publicly known breakout rules taught by Shubhashi Pani (Power of Stocks). This is not an official POS script, and I am not affiliated with the Power of Stocks team. This implementation was developed independently to follow the logic shared for educational use.

Feel free to use, backtest, and modify according to your needs. Constructive feedback is welcome!

Options Strategy V1.3📈 Options Strategy V1.3 — EMA Crossover + RSI + ATR + Opening Range

Overview:

This strategy is designed for short-term directional trades on large-cap stocks or ETFs, especially when trading options. It combines classic trend-following signals with momentum confirmation, volatility-based risk management, and session timing filters to help identify high-probability entries with predefined stop-loss and profit targets.

🔍 Strategy Components:

EMA Crossover (Fast/Slow)

Entry signals are triggered by the crossover of a short EMA above or below a long EMA — a traditional trend-following method to detect shifts in momentum.

RSI Filter

RSI confirms the signal by avoiding entries in overbought/oversold zones unless certain momentum conditions are met.

Long entry requires RSI ≥ Long Threshold

Short entry requires RSI ≤ Short Threshold

ATR-Based SL & TP

Stop-loss is set dynamically as a multiple of ATR below (long) or above (short) the entry price.

Take-profit is placed as a ratio (TP/SL) of the stop distance, ensuring consistent reward/risk structure.

Opening Range Filter (Optional)

If enabled, the strategy only triggers trades after price breaks out of the 09:30–09:45 EST range, ensuring participation in directional moves.

Session Filters

No trades from 04:00 to 09:30 and from 16:00 to 20:00 EST, avoiding low-liquidity periods.

All open trades are closed at 15:55 EST, to avoid overnight risk or expiration issues for options.

⚙️ Built-in Presets:

You can choose one of the built-in ticker-specific presets for optimal conditions:

Ticker EMAs RSI (Long/Short) ATR SL×ATR TP/SL

SPY 8/28 56 / 26 14 1.4× 4.0×

TSLA 23/27 56 / 33 13 1.4× 3.6×

AAPL 6/13 61 / 26 23 1.4× 2.1×

MSFT 25/32 54 / 26 14 1.2× 2.2×

META 25/32 53 / 26 17 1.8× 2.3×

AMZN 28/32 55 / 25 16 1.8× 2.3×

You can also choose "Custom" to fully configure all parameters to your own market and strategy preferences.

📌 Best Use Case:

This strategy is especially suited for intraday options trading, where timing and risk control are critical. It works best on liquid tickers with strong trends or clear breakout behavior.