Average True Range NormalizedIntroduction

This simple script is the normalization of the common ATR indicator. The utility in normalization, in this case, is the contextualization of the absolute movements of the ATR compared to the previous candles. Not finding an indicator that reflected my needs, I created it and decided to make it available to the community.

The oscillator is fully based on the original ATR indicator, once normalized it varies its values between -50 and +50 and has a moving average based on it.

I added alarms:

- crossing of horizontal levels (default +40 -40)

- crossing of the moving average

Settings

ATR period : like a normal ATR indicator, the number of candles on which the ATR calculation is based

Smooth : like normal ATR indicator, type of moving average to smooth true range values

Normalization Period : Number of candles on which ATR normalization is based, it takes the maximum and the minimum values in the last N candles and creates the value -50 and +50, between these two values normalize the others.

MA Period : Period of MA based on ATR, this MA can be used like moving level to find the moment of low volatility

Type : Kind of MA, you can choose only between 3 types ( SMA, EMA, WMA )

Horizontal Lines Value : high and low level for high and low volatility

Alert on crossing Horizontal lines : enable alerts on crossing Horizontal Lines

Alert on crossing MA : enable alerts on crossing Moving Average

How to use

ATR isn't a directional indicator, but volatility is fuel for markets, low ATR values indicate quiet moments or consolidation movements, otherwise high ATR values indicate selling or buying pressure. A reversal in price with an increase in ATR would indicate strength behind that move.

The problem, for me, with normal ATR is that often the values have to be contextualized with older values, on the contrary being normalized you can:

- catch small fluctuations, and anticipate the decline;

- contextualize the values without having to look at the history in the previous candles

So:

- under MA or horizontal line the volatility is too low, it would be advisable to consider not opening positions;

- over MA line the volatility is raising and a reversal in price with an increase in ATR would indicate strength behind that move;

Remember that every statistical indicator is just a tool, it needs to be understood to be used at its best, otherwise, it is just a colored line in a colored graph.

Média de Amplitude de Variação (ATR)

Best delta gridTradingThis indicator help grid traders to chose the best delta in their gridTrading.

The best delta gridTrading indicator is proportional to the Average true range.

Modified ATR Indicator [KL]Modified Average True Range (ATR) Indicator

This indicator displays the ATR with relative highs and relative lows statistically determined.

What is ATR:

To know what ATR is, we need to understand what a True Range (TR) is.

- TR at a given bar is the highest distance between points: a) High vs low, b) High vs Close, and c) Low vs Close.

- ATR is the moving average of TRs over a predefined lookback period; 14 is the most commonly used.

- ATR can be mathematically expressed as:

Why is ATR Important

ATR often used to measure volatility; high volatility is indicated by high ATR, vice versa for low. This is a versatile tool allowing traders to determine entry/exit points, as well as the size of stop losses and when to take profits relative to it.

This is an opinion: Through observations, I have noticed that ATR can also indirectly tell us the levels of relative volume. This intuitively makes sense because in order to increase length of TR, high amounts of capital inflow/outflow is required (graphically speaking, high volume is required in order to make lengths of candle sticks longer). The relationship between ATR and relative volume should hold unless the market is illiquid to the extreme that there is no relationship between volume and price.

That said, knowing the relative lows/highs of ATR is very useful. It can be interpreted as:

- Relative high = high volatility, usually during sell offs

- Relative low = decreasing volume, could indicate price consolidation

Instead of arbitrarily determining whether ATR is high/low, this indicator will determine relative highs and relative lows using a simple statistical model.

How relative high/low is determined by this model

This indicator applies two-tailed hypothesis testing to test whether ATR (ie. say lookback of 14) has greatly deviated from a larger sample size (ie. lookback of 50). Assuming ATR is normally distributed and variance is known, then test statistic (z) can be used to determine whether ATR14 is within the critical area under Null Hypothesis: ATR14 == ATR50. If z falls below/above the left/right critical values (ie. 1.645 for a 90% confidence interval), then this is shown by the indicator through using different colors to plot the ATR line.

Bjorgum Key Levels

Key Levels Aims to capture 3 of the most significant points in price action

Breakouts

False Breakouts (Traps)

Back Checks

These 3 points alone, if properly identified, can be some of the most significant points of movement in the price history of an asset and bring significant gains to traders, if capitalized on. Here are a few examples of these setups

Breakouts

Breakouts can bring significant rallies as the market swings one sided after key levels are breached. This entry type can bring large trending runs to follow. Momentum is on your side, but the trade off is a higher entry.

False Breakouts

Also known as a bull trap or a bear trap, false breaks can lead to swift and significant reversals and potential for a large and sudden move to the opposite side. When a key level breakout fails to hold, parties entering to capitalize on the "epic breakout" can get left holding the bag forcing them to exit at a loss, which can double the force of pressure. Traps can bring swift gains from good entry prices. However, price is still in a larger trend against you so momentum is weak, so price action is susceptible to roll over.

Backchecks

Back checks are pull backs in trend that find middle ground to the 2 areas already described. Both momentum and entry price are decent, but risk is defined as a key level has flipped offering entry with stops below demand, or above supply.

Combining these 3 methods helps to diversify risk, understand trend development, and bring steady gains. This script helps to identify these points to traders with analysis of key levels, price structure, and trend direction, while providing visual signals and alerts for when they occur.

Best of luck in your coding and trading and thank you for your support

node nirvanaThis indicator is suitable for those who have studied Mr. Nirvana's course, as well as those who work in the style of supply and demand.

ATR Trailing Stop v5 One of my favorite stops is the ATR Trailing Stop-loss. With the implementation of PineScript v5, a code update was needed in order to use this stop/exit-strategy with newer strategy scripts. A timeframe selector that was not featured on earlier versions is also included. This new version can be plugged into PineScript v5 strategies, and also has a simpler/cleaner code that makes the code logic easier to follow than prior versions.

For those that are unfamiliar with the ATR Trailing Stop exit strategy; it is a trailing stop that takes into account the volatility of the underlying asset by trailing the price series using a multiple of the Average True Range (ATR). In practice I’ve found that this exit can be more effective than traditional trailing stops, depending on the volatility of the asset you are trading. More detailed information can be found at www.stockopedia.com

How do I use it? Add it to your chart as an indicator to visualize where the ATR stop would be with your settings. Or, copy and add it to your v5 strategy with the addition of a ta.crossunder(close, ATRTrailingStop) or ta.crossover(close, ATRTrailingStop) function. Special thanks and credit to HPotter who coded an earlier version of this in pine!

Logarithmic Average True Range

In the case of ATR, it is known to represent volatility by simply expressing the price range.

However, of course, as the value of an asset increases, it is not possible to simply compare it with a numerical value, so the ATR was expressed as a percentage using a logarithmic function.

This way we can see the volatility even with ATR.

ATR의 경우 단순하게 가격의 범위만을 표현하여 변동성을 나타낸다고 알려져있습니다.

하지만 당연하게도 자산의 가치가 높아질수록 단순하게 수치만으로 비교할 수는 없고, 따라서 로그함수를 사용해 %로 ATR을 표현하였습니다.

이렇게 표현하면 ATR로도 변동성을 볼 수 있습니다.

ATRSLTPTwo adjustable ATRs are drawn on the screen for gradual stop, the ATR multiplier can be changed in the settings. the green line shows the target point with 5 ATR (cannot be changed)

[CP]Pivot Boss Floor Pivots with ATR Dilation and Dynamic LevelsINTRODUCTION:

Compared to all the Pivot Indicators available on Trading View Public Library, this Floor Pivots Indicator differentiates itself in two major original ways:

Dilates the Pivot Support/Resistance Levels into Support/Resistance Bands based on volatility

Displays the S/R Levels Dynamically , that is, only those levels will be shown that are close enough to the price resulting in much cleaner looking charts.

There were a few features whose logic I had figured out, but I could not implement them due Pine Script’s Limitation (they should really work on increasing Pine Script’s capacity instead of adding more and more features to the language in order to make it look ‘better’):

Showing multiple timeframe pivots at the same time (not possible due to Pine Script’s limitation on the ‘Max Number of Outputs’ )

Automatic Detection of highly profitable Double Hot Pivot Zones (DPZ), also due to the ‘Max Number of Outputs’ limit

GENERAL USER INPUTS:

Most of the settings are self-explanatory, however, a few of them need some explanation:

Show Floor Pivots Dynamically – This will turn ON the dynamic pivot levels, please note that this function will work ONLY IN INTRADAY timeframes.

Dynamic Pivot ATR Period – Period over which the ATR value is calculated to show the pivots dynamically.

ATR Threshold for Dynamic Floor Pivots – Simply put, the indicator will start displaying Pivot Levels if they fall within the 2*ATR distance (default value) of the price. You can increase this number if the volatility increases and vice-versa.

Use ATR to Dilate Intraday Pivot Levels – This will turn ON Floor Pivot Dilation, turning pivot ‘lines’ into ‘bands’ .

ATR Dilation Factor – This number decides the width of the Pivot bands. Larger this number, thicker the bands. Typically, high volatility stocks will require a higher number.

ATR Period – Same as Dynamic Pivot ATR Period, but for Pivot Level Dilation.

INDICATOR USAGE EXAMPLES:

This indicator works great in conjunction with my Pivot Boss Candlestick Scanner indicator.

There are a lot of optimizations I have done in the code, although it looks trivial at first glance, but it's fairly complex.

Feel free to use it and modify it as you wish.

Here are a few examples where the indicator has shown great entries and exits, with the default settings:

NIFTY 5m Chart

Reliance 5m Chart

Tesla 5m Chart

Bitcoin-USDT 15m Chart

FINAL WORDS:

Please understand that I have Cherry Picked the examples to showcase the capability of the indicator and its usage.

DO NOT conflate the accuracy of examples with the accuracy of this indicator.

Once you start using floor pivots, you will realize that a lot of days simply don’t give any high probability setups and you will simply sit out of the market and do nothing (which is a good thing).

If you really want to learn how to use Pivots, read the book ’Secrets of a Pivot Boss’ . This book can change your life.

RSI c/w MA, ADX and ATR data I have added 3 items to the RSI indicator which helps me to get more information at the same time.

1) ADX value - when ADX is above 25 we have a strong trend

2) ATR Value - helps me to calculate my daily targets and stop-loss levels at a glance.

3) A simple moving average - This shows me the trend of RSI. If the price breaks a trend line and at the same time RSI crosses above the MA, it shows me a breakout has happened. In longer timeframes, it can show you in advance if you should expect a reversal in the trend.

You can turn on or off the MA as well as the ADX line.

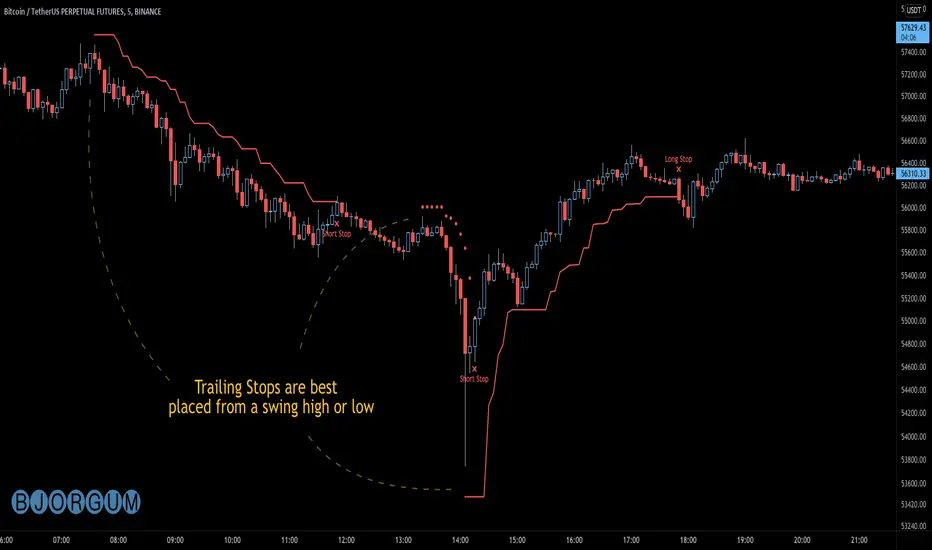

Bjorgum AutoTrailOne Time Trade Risk Management

Incorporating the new interactive feature, this script is meant as a one time trailing stop for the active trader to manage positional risk of an ongoing trade. As a crypto trader or Fx trader, many may find themselves in a position late into the evening, or perhaps daily life is calling while a trade progresses in their favor. Adding a trailing stop to a position thats trending can help to keep you in the trade and lock in gains if things turn around when you are unable to react.

To use the trail, the user would add the script to the chart. Once added, a set of crosshairs will appear allowing the user to choose a point to begin. Often choosing to start a trail from a swing high/ low can be an ideal option. This tends to provide some protection for a stop by placing it under support for a long trade or above resistance for a short trade.

Price based trail

The trail will automatically plot and the offset is a factor of the distance from price action selected by the crosshairs. If placed above price action the script will plot a short trail, if placed below it will trail for a long position.

Additionally, there are several other trail types other than price based. There is also percent based, which offsets the trail as a percent from close. A hard stop is placed at the cross hair value, then once the distance is exceeded by the percentage specified, the trail begins.

There are 2 more volatility based trails. There is a PSAR trail which can provide quicker and tighter stops that accelerate with the trend locking in gains faster, and an ATR trail that keeps a distance from price action as a function of volatility. Volatility levels can be adjusted from the menu.

Volatility based trail (ATR)

Volatility based trail (PSAR)

Lastly, within the code for more the more technical savvy, is some starting setups for string alerts to be sent to exchanges via 3rd party or custom API applications. Some string manipulation is required for specific providers to meet their requirements, but there is some building block alerts that will take the ticker symbol, recognize the asset your trading (Fx, Crypto, etc) and take input quantity or exchange names from the settings via inputs.

Complex strings can be built to perform almost any trade related task when to comes to alerts via web hook. A little setup this way with some technology to back your system can mean a semi-automated half man, half machine setup that actually manages your trail stop while you cannot. For those that don’t go this far, there is some basic alert functionality that well trigger when a trail is hit so you can react and make a decision.

Please note that for now, interactive mode is engaged only when the script is added to the chart. Additional stops, or for adjustments to be made it is best to add a new version. Also as real trades could be at play managing an actual position, alerts are designed to go off only once to ensure no duplicate orders are sent meaning alerts are not reoccurring. Once an alert is triggered, a new trail is to be set up.

A modified version of the TradingView built in SAR equation was used in this script. To provide the value of the SAR on the stop candle, it was necessary to alter the equation to extract this value as the regular SAR “flips” at this point. Thank you to TradingView for supplying access to the built in formula so that this SAR could behave the same as the built-in function outside of these alterations

Example of SAR value maintained in trigger candle

Cheers and happy trading.

ADR PercentUses past 5 day's daily average ranges and calculates average ADR percentage with respect to latest day's open

Acknowledgement - Uses code from another excellent indicator from critian.d

Weekly Put SaleWeekly Put Sale

This study is a tool I use for selling weekly puts at the suggested strike prices.

1. The suggested strike prices are based on the weekly high minus an ATR multiple which can be adjusted in the settings

2. You can also adjust the settings to Monthly strike prices if you prefer selling options further out

3. I suggest looking for Put sale premium that is between 0.25% to 0.75% of the strike price for weekly Puts and 1% to 3% of the strike price for monthly Puts

Disclaimers: Selling Puts is an advanced strategy that is risky if you are not prepared to acquire the stock at the strike price you sell at on the expiration date. You must make your own decisions as you will bear the risks associated with any trades you place. To sum it up, trading is risky, and do so at your own risk.

RSI Trend LineI took a concept similar to the "Adaptive RSI" to get the RSI overlaid on a price chart. The problem I have with the Adaptive RSI is to me it sticks too closely to price. I wanted something much more visually helpful that can provide actual tradable signals and strategies.

The orange line you are seeing is the "RSI Trend Line"

The further the RSI moves away from a value of 50 (the "zero line"), the more you see this orange line move away from price. This helps visualize the strength of price pushing away from a neutral value to a position of strength or weakness-- if orange is below price then relative strength is high; if orange is above price then relative strength is low. When price is equal to the orange RSI line, the RSI is at a value of 50.

In addition to the trend line, you can enable bands which reflect Overbought and Oversold levels . If you leave the responsiveness to a value of 1.0 and removed any smoothing, these should pretty accurately reflect an actual RSI chart topping the OB and OS lines (default 70 and 30, respectively). (They're still very close with different responsiveness and smoothing values)

The conversion or scaling of RSI value onto price comes with a bit of a quirk which I decided to leave to the user to determine how they want it applied. So the setting "Responsiveness" will impact the sort of aggressiveness of the RSI trend line as well as the the size of the bands. You could think of this in some ways as the OPPOSITE of the multiple setting on a Bollinger or Keltner band-- 1.0 will make for the widest band, 2.0 is the default and my preference, and you can move it up to a value of 5.0.

Here are some examples of how you could use the indicator for trade signals--

And here's my thought on the current state (as of 10/06) on indices with regards to this indicator-

ATR Trailing Stops S/R [LM]Hello Traders,

I would like to introduce you ATR Trailing Stops S/R . The idea is to look for important levels that are identified by trailing stop line, where it usualy spents a lot of time without any move usualy turns out to be good level for bounces.

Script for atr trailing line is originaly taken from: script made by @dgmoon

It has various setting

Timeframe and atr settings

Show lines

Extend lines

Line count - how many lines will be rendered

Candle count - how many candles has to trailing line spend at the same level

Colors - controls color of plot and lines

I hope you will enjoy it, as I enjoyed to write it.

Lukas

+ ATR Support and ResistanceThis, a very different script from most of mine, is my attempt at making a useful, and not messy, support and resistance indicator. If you've never looked into trader xkavalis, and his scripts and discord, I would highly recommend it. He talks about "pay attention candles" a lot. It got me thinking about what those are. Best as I can tell all he means by that phrase is large, impulsive candles. Sometimes these lead to break outs of ranges, or they may signal tops, bottoms, or near-tops and bottoms. The only way I could make sense of this in a mathematical way was by using the average true range. Basically, any candle's true range outside of the ATR is considered a "pay attention candle," by my definition.

This script originally began as just a candle coloring exercise with some optional shapes plotted above/below certain candles, but I quickly realized I wanted to draw lines or zones from these candles, so eventually, after many hours spent figuring out and learning 'line.new' and 'box.new' I got things sorted.

Essentially, my line of thinking is that on impulsive candles down, the origin of the impulse is more important than the close (not always of course, as there are no unbreakable rules in what markets can do), and with impulsive candles up, the same theory applies.

So, for upward impulsive candles I've marked out the zone from the open to the low as a support (until broken, in which case it may become resistance). For downward impulsive candles the zone encompasses the open to the high. I've given the option to plot a line from the close for all of these. It's turned off by default as it's just less stuff on the chart, but you may like it.

The line length is customizable in a menu. It does funny things on low timeframes on forex and stock charts (long lines that result in chart compression), but for some reason very rarely on crypto charts. If someone who is smart (not me) and has much experience with pinescript could perhaps help me out with a fix for this, that would be great. I suspect it has something to do with my "bar_index_duration" that I defined using the time function, but I'm not sure how or why.

Line length on time frames of one hour and up it is typically fine.

Use the ATR multiple to change the sensitivity of the indicator. This is basically the determination of when a candle is beyond the ATR. A multiple of two is two times the ATR. With lower volatile pairs you can maybe make this lower. On lower time frames or with more volatile pairs (illiquid alts in particular) a higher multiple might serve better. I find the default 1.75 is mostly acceptable.

As I started this I also thought adding some sort of volume information to the candles might be useful as well, so I added a simple candle coloring feature referencing the OBV and a 21 period EMA. Candles are colored based on the OBV's relation to its moving average.

I added some plot shapes and candle coloring utilizing the RSI as well. Options to turn on or off shapes plotted for overbought and oversold across the top of the chart. The most interesting feature that I implemented here is a support/resistance zone around the centerline of the RSI. If the RSI is between 49 and 51 then you can have optional candle coloring, shapes plotted above the candles, and s/r zones drawn on the chart. In trending markets the centerline of the RSI will frequetly act as support or resistance, so by being alerted of this condition on the chart you can use that with actual levels marked off in order to help make a judgement on a trade. I think it's a nice addition, and an oft overlooked aspect of the usefulness of the RSI.

I've also included a calculation, with candle coloring and/or plot shapes, for something like a stop run on high volume. The calculation for that is in its section below, and should be pretty self explanatory.

Lastly, typing this as I'm posting it, this indicator could also be useful for helping to find placement for trailing a stop. Just a thought!

Volume Power Flow - Taylor V1Combination of Volume Average Trend & Volume Power Range

Able to Change Average Moving Type & Length = Depending on How Volatility /Smooth is Require on your Strategy

1# Color Green = The Volume On Trend Up

2# Color Red = The Volume On Trend Down

3# Spiking Higher Volume = End of the Top/ Bottom

Rate Of Change ATRThis is a very basic, but powerful script.

It gives you the ratio between the rate of change of the last x days and the average true range of the last y days.

---> ROC-ATR Ratio = ROC/ATR

Therefore, you can see how much the price has moved relative to the prices in the past.

This is important because (in my opinion) the basic ROC indicator is not very meaningful if you don't look at the average volatility of recent history.

For example, a ROC of 5% over the last 3 days might be very high for Forex but very small for some crypto.

Consequently, this indicator makes it possible to compare (and be used on) every instrument in every industry the same way.

Generally speaking, it makes more sense if the ATR length is larger than the ROC length.

HPH's SuperKeltnerThis indicator combines the Supertrend (to determine the main trend direction) with two Keltner channels (used for add and take profit signals) to construct a trend trading system.

These are the available settings:

General

UseTrendChange ➞ toggle trend change alerts and labels

UseAdds ➞ toggle add to position alerts and labels

UseTakeProfits ➞ toggle take profit alerts and labels

PrematureAdds ➞ toggle adding to position as soon as the add channels are left (default is false, so the add signal will only fire once the channels are re-entered)

PrematureTakeProfits ➞ toggle taking profit as soon as the tp channels are left (default is false, so the tp signal will only fire once the channels are re-entered)

Visualization

Show Add Keltner ➞ toggle display of the channels used for adding to the position

Show TP Keltner ➞ toggle display of the channels used for taking profit

Show SuperTrend ➞ toggle display of the Supertrend

Keltner

Standard Keltner channels settings except for the fact that there are two different multipliers. The Keltner TP Multiplier should generally be bigger than the Keltner Add Multiplier , as the channels are hit differently in trending markets. I recommend you to use the visualization settings to show the channels and adjust the settings to your liking.

Supertrend

Standard Supertrend settings, nothing to add here.

Alerts

Use the alert messages to customize what alert text the indicator will send. This makes it possible to use the script to automate trading bots.

By default, the alerts are sent after the candle has closed. This ensures that no repainting is happening. If you like the risk, you can toggle the corresponding WaitFor Confirmation if you wish to receive the signals earlier (max. once per bar).

Enjoy!

Berzerker IndexSome pairs have their own distinct behavior. That includes volatility, news reactiveness, trend x chop day discrepancy, and other qualities.

At first, I tried to measure this with the Choppiness Index, but it looks pretty much alike when you compare symbols like EURNZD and GBPCAD, but my testing shows some major behavioral differences between the two. Hence, I decided to build my own measurement which I later decided to call Berzerker Index.

• The calculation takes the previous value and adds 1, 3, 7, or 15 depending on how many standard deviations the price beats.

• Deviations use Jurik Moving Average as a central line. If there is no new penetration, the total value will not be increased.

• At the end of the value update, the result will decay whether it is changed or not. The readings decay significantly faster if the price is between the bands.

• The beginning of the calculation is the beginning of the chart. There isn't any period for the calculation.

As you can see, from the beginning of the year, the maximum readings on EURNZD are 49.8 and 73.6 for GBPCAD. This is what I wanted to achieve - find some way to clearly differentiate the pairs. Later, I went on EURUSD to confirm the results. EURUSD should be a calmer pair and it shows 33.5 which supports the theory.

The symbols with small bars and explosions on events and bank meetings will reach high values, whereas those that are more predictable with less extreme movements will be found below 45.

Lastly, you may identify long periods of continuous descend on the indicator as setting up for a large explosion. This is not the original idea but could work nevertheless.

Of course, I will further update this indicator if I get improvement ideas...

FAQ:

► Does this repaint?

• No.

► Where is the buy signal?

• There isn't one. The purpose is to study repeated behavioral patterns of different symbols, not to drink from the holy grail.

► Why is it called the 'Berzerker' Index?

• I don't know.

I used @everget's version of Jurik's Moving Average with his consent.

What do ya thing?

Wavy Tunnel + Trend ATR Buy Sell Signal by PaRnWavy Tunnel + Trend ATR Buy Sell Signal by PaRn

Originality by PaRn

First Combination of Wavy Tunnel + Trend ATR Buy Sell Signal by PaRn

"Buy Sell Signal" is base on Volatility Stop 20, Multiplier 2.5

"Trend Signal" is based on EMA crossover between EMA12(Close) and EMA26(Close)

Take Profit Line is EMA15(Default)

Wavy line Base on EMA34(high,close,low)

Tunnel line Base on EMA144(close),EMA169(close)

Green Candle Bar = "Uptrend"

Red Candle Bar = "Downtrend"

Buy when "Buy" Signal present

Follow Trend till the end of the trend : "Sell" Signal present

Buy More (Optional) = Green Arrow present on Uptrend

How to use Wavy Tunnel + Trend ATR Buy Sell Signal by PaRn

- Wavy Tunnel + Trend Signal can be used in any timeline from 5 Minutes to Weeks

- Price above both Wavy & Tunnel = "Uptrend"

- Green Candle Bar = Uptrend

- Buy when "Buy" Signal present

- Buy More (Optional) = Green Arrow present on Uptrend

- Hold your possition and Follow Trend till the end of the trend : "Sell" Signal present, It's time to sell all position

NOT RECOMMEND TO USE ON SIDEWAY MARKET

Ticker SummaryTicker Summary provides at-a-glance summary information about a ticker near the current bar on the chart:

P/E ratio

Fwd P/E ratio

PEG ratio

Floating shares vs. total shares outstanding

% of trading volume that was short over the last 3 days

Average True Range (ATR) over last 14 days

There are a few less common items of information:

How many ATR multiples the ATR is extended over the last 10 bars. This gives an idea of how far the stock is currently extended.

"R-frequency", explained below.

An optional "ATR Reticule" is shown near the price. This is useful for traders that use ATR as a guideline for price targets and stop losses. On the left is the # of ATRs the stock is currently above the session open. On the right is the # of ATRs the stock is extended above the 10-bar moving average.

R-frequency: a measure of liquidity relevant to your own trading size. It is the frequency at which 1-R of your trading account is traded for a stock. Formula:

(1-R worth of shares) / (average dollar value traded per second), where:

"1-R worth of shares" is how many shares you would buy for a stop loss of -1 ATR, with max risk dollar value based on the Balance and Max Risk % indicator options.

"Average dollar value traded per second" is the 14-day average of (avg(high, low and close) * daily volume)

R-frequency of a second or less is very liquid. If the value is higher (for example, over 60 seconds) the stock is less liquid and you may have some trouble filling limit orders quickly.

NNFX ATRBefore I begin I want to mention:

1. This is an indicator specially made for NNFX traders who use the ATR rule of ATR1x for Take Profit and ATR1.5x for Stop Loss

2. It is a product of combining the in-built ATR and Dillon Grech's ATR ()

The indicator:

1. It can be used for a quick look using the lines to see instead of calculating whether price hit a TP or SL. However I have kept the Main ATR for those who want to record the ATR into the spreadsheet when back testing or forward testing

2. When placing a buy/long order, TP is blue and appears above price, SL is red and appears below price

3. When placing a sell/short order, TP is blue and appears below price, SL is red and appears above price

4. The Main ATR, which is yellow, is way below price because I didn't want the chart to be overwhelmed by a 5th line in the middle of 2 TPs and SLs aka make the chart look claustrophobic