PowerTrend Pro Strategy – Gold OptimizedTired of false signals on Gold?

PowerTrend Pro combines VWAP, Supertrend, RSI, and smart MA filters with trailing stops & break-even logic to deliver high-probability trades on XAUUSD.

PowerTrend Pro Strategy is a professional-grade trading system designed to capture high-probability swing and intraday opportunities on XAUUSD (Gold) and other volatile markets.

🔑 Core Features

VWAP Anchoring – institutional fair value reference to filter trades.

Supertrend (ATR-based) – adaptive trend filter tuned for Gold’s volatility.

Multi-Timeframe RSI – confirms momentum alignment across intraday and higher timeframe.

EMA + SMA Combo – ensures trades follow strong directional bias, reducing false signals.

Dynamic Risk Management

Adjustable Take Profit / Stop Loss (%)

Trailing Stop that locks in profits on extended moves

Break-Even Logic (stop loss moves to entry once price is in profit)

⚡ Gold-Tuned Presets

XAUUSD 1H → tighter TP/SL & faster entries for active intraday trading.

XAUUSD 4H → wider ATR filter & trailing stops to capture bigger swings.

Generic Mode → works on Forex, Indices, and Crypto (fully customizable).

🎯 Why It Works

Gold is notoriously volatile — quick spikes wipe out weak strategies. PowerTrend Pro solves this by combining:

✅ Institutional bias (VWAP)

✅ Adaptive trend filter (Supertrend)

✅ Momentum confirmation (RSI MTF)

✅ Robust trend structure (EMA + SMA)

✅ Smart exits (TP, SL, trailing & breakeven)

This multi-layer confirmation makes entries stronger and keeps risk under control.

🛠️ Usage

Add the strategy to your chart.

Choose a preset (XAUUSD 1H, 4H, or Generic).

Run Strategy Tester for performance metrics.

Optimize TP/SL and ATR values for your broker & market conditions.

🔥 Pro Tip: Combine this strategy with a session filter (London/NY overlap) or volume confirmation to boost accuracy in Gold.

Strategy!

Multi Channel GRID & DCA LTF [trade_lexx]Multi Channel GRID & DCA LTF

Usage Guide

Part 1: The concept and general possibilities of the "Multi Channel GRID & DCA LTF" strategy

Introduction

Welcome to the guide to "Multi Channel GRID & DCA LTF", a powerful and versatile automated trading strategy for the TradingView platform. This tool was developed for traders who are looking for flexibility, control and a high degree of adaptability to various market conditions.

The strategy is based on a hybrid approach that combines two popular and time-tested techniques.:

1. GRID (grid trading): The classic method of averaging a position is by placing a grid of limit orders.

2. DCA (Dollar Cost averaging): Smart position averaging based on signals from external indicators.

However, "Multi Channel GRID & DCA LTF" goes far beyond the simple combination of these two techniques. The strategy includes a number of unique and innovative features, such as cascading MultiGRID grids for dealing with extreme volatility, Channel Mode range trading mode for profiting from sideways movement, and Low Time Frame analysis (LTF) to achieve surgical accuracy in backtesting. Deep customization options for risk management, capital, take profits, and stop losses allow you to configure a strategy for almost any trading style, asset, and timeframe.

The basic idea: How does it work?

Let's take a detailed look at each of the key concepts embedded in the logic of the strategy.

1. GRID — Automatic placement of buy and sell orders at certain price intervals.

This is a fundamental mode of operation. Its main goal is to systematically improve the average entry price for a position if the market is going against you.

* The principle of operation: After opening the base (first) order (`BO`), the strategy automatically places a series of pending limit orders (here they are called "safety orders" or "SO") at certain price intervals. For a long position, orders are placed below the entry price, and for a short position, orders are placed higher.

* Target: When the price moves against an open position, it consistently hits and executes safety orders. Each such execution adds additional volume to the position at a more favorable price, thereby shifting the overall average entry price (`position_avg_price') closer to the current market price. This means that a much smaller corrective movement will be required to gain ground.

* Flexibility: You have full control over the geometry of the grid: the number of safety orders, the percentage distance between them (`SO Step`), and you can even set a coefficient that will increase this step for each subsequent order (`SO Multiplier`), creating an expanding grid.

2. DCA (Signal Averaging) — Smart Averaging

This mode adds an additional layer of analysis to the averaging process. Instead of just buying/selling at the set price levels, the strategy waits for a confirmation signal.

* Working principle: You can connect any external indicator (for example, RSI, CCI, or even your own complex signal system) to the strategy, which outputs numerical values. As standard, 1 is used for a long signal, and -1 is used for a short signal. The strategy will place the next averaging order only at the moment when it receives the appropriate signal.

* Goal: To average a position not just during a fall (or a rise for a short), but at the moments that your main trading system considers the most favorable for this. This allows you to avoid "catching falling knives" and enter only if there are good reasons.

3. Hybrid Mode (GRID+DCA) is the best of the previous two modes

This mode is designed for maximum filtering and control. It requires two conditions to be fulfilled simultaneously.

* Working principle: The safety order will be executed only if the price has reached the calculated grid level and a confirmation signal has been received from your external indicator. If a confirmation signal is received from an external indicator, the next calculated grid level activates the limit order.

* Goal: To create the most reliable averaging system that protects against premature entries and requires double confirmation (both by price and indicator) before increasing the position size.

4. MultiGRID — Adaptation to extreme volatility

This is one of the most powerful and unique features of a strategy designed to survive and make a profit in the face of strong, protracted trends or "black swans".

* The problem it solves: The usual grid of orders has a limited depth. If the price goes beyond the last safety order, the strategy loses the opportunity to average and becomes vulnerable.

* The principle of operation: The MultiGRID function allows you to create "cascades" — several grids following one another. When all the orders of the first grid are executed, the strategy does not stop. Instead, she can activate the second, third (and so on) a grid of orders. The new grid can be activated by one of two triggers:

1. Offset: The new grid is activated when the price passes another set percentage deviation from the last executed order.

2. Signal: The new grid is activated when a signal is received from an external indicator.

* Goal: To significantly expand the working range of the strategy. This allows it to adapt to strong market movements that would "break" the usual grid, and continue to effectively average a position at a much greater depth of decline or growth.

5. Channel Mode — Trading in the range

This feature turns a standard averaging strategy into a machine for "farming" profits within a price channel that is formed during a sideways market movement.

* The problem it solves: In the standard grid strategy, after partially closing a take profit position, the volume of this part "leaves" the trade until the deal is fully closed. You are missing the opportunity to reuse this capital.

* Operating principle: When Channel Mode is enabled, the following happens. Suppose the price went against you, executed several safety orders, and then turned around and reached one of the partial take profits. At this point, the strategy is:

1. Fixes the profit, as it should be.

2. Instantly places a new limit order to buy (or sell for a short) at exactly the same price level where the last triggered safety order was executed. The volume of this order is equal to the volume of the part that was just closed for take profit.

3. If the price goes down again and executes this "repeat" order, the strategy immediately sets a corresponding take profit for it at the level where the previous profit was taken.

* Goal: To create a continuous buy-sell cycle within the local range (channel). The lower limit of the channel is the price of the last averaging, and the upper limit is the price of a partial take profit. This allows you to repeatedly profit from sideways price fluctuations, without waiting for the full closure of the main, large transaction.

6. LTF (Lower Timeframe Analysis) — Surgical precision of backtesting

This feature is critically important for obtaining reliable results during historical testing (backtesting) of grid strategies.

* The problem it solves: The standard testing mechanism in TradingView has a serious limitation. Working, for example, on a 4-hour chart, he sees only 4 candle points: Open, High, Low and Close. He does not know in what order the price moved within these 4 hours. He could have touched High first and then Low, or vice versa. For grid strategies, this is fatal — the engine can show that a take profit has been executed, although in reality the price first went down, collected the entire grid of orders and only then turned around.

* How it works: When you turn on the LTF mode, the strategy for each candle on your main chart (for example, 4H) requests and analyzes all candles from the lower timeframe you specified (for example, 1-minute). Then it virtually trades the entire price path for these minute candles, executing orders, take profits and stop losses in the sequence in which they would occur in reality. It works in the single take profit mode of the Grid strategy.

* Goal: To provide the most realistic and reliable backtest that reflects the real dynamics of the market. This allows you to avoid false expectations and accurately assess the potential performance of the strategy.

// ------------------------

Part 2: Detailed description of the strategy settings

This section is your main guide to all the switches and options available in the strategy. Understanding each setting is the key to unlocking the full potential of this powerful tool.

1. 🛡️ Risk Management 🛡️

This group contains fundamental parameters that determine the basic logic of risk management and the geometry of grid orders.

* Strategy type: Determines the direction of transactions.

* Long: The strategy will only open long positions (buy).

* Short: The strategy will only open short positions (sell).

* Both: The strategy will work both ways, opening long or short depending on the incoming signal.

* SO Count: Sets the maximum number of Safety (averaging) Orders (SO) that the strategy will place within the same grid. If you have MultiGRID enabled, this number applies to each individual grid.

* SO Step (%): This is the base percentage deviation from the entry price at which the first safety order will be placed. For example, at a value of 0.5, the first SO in a long trade will be placed 0.5% lower than the opening price of the base order.

* SO Multiplier: A coefficient that exponentially increases the step for each subsequent safety order. This allows you to create an expanding grid where averaging orders are placed further and further apart, which is effective with strong and accelerating price movements.

* *The step formula for the nth order*: Step(N) = (SO Step) * (SO Multiplier ^(N-1)).

* If the value is 1, all steps will be the same.

* With a value of 1.6, the step of the second SO will be 1.6 times larger than the first, the step of the third will be 1.6 times larger than the second, and so on.

* 1️⃣ TP/SL: These are simplified settings for quick configuration. They allow you to turn on/off the main take profit and stop loss and set basic percentage values for them. More detailed settings for these parameters can be found in the relevant sections below.

// ------------------------

2. 💰 Money Management 💰

Everything related to position size, leverage, and capital is configured here.

* Volume BO (Base Order): Determines the size of the trade's opening order.

* Volume BO: A fixed amount in the quote currency (for example, in USDT).

* USDT (check mark): Manages the information in the comments to the orders. If enabled, the volume of orders in USDT will be displayed in the comments. This is convenient for visual analysis and for sending the amount of USDT by the placeholder {{strategy.order.comment}} via webhooks when connecting the strategy to the exchange or trading terminals.

* or % of deposit: The amount calculated as a percentage of the available capital of the strategy. The check mark to the right of this field enables this mode. Important: using a percentage activates the effect of compounding (compound interest), as the amount of each new transaction will be automatically recalculated based on the current capital (initial capital + profit/loss). If enabled, the percentage of orders will be displayed in the comments. This is convenient for visual analysis and for sending percentages on the placeholder {{strategy.order.comment}} via webhooks when connecting the strategy to the stock exchange, trading terminals, or creating Copy trading.

* Martingale: The coefficient applied to the volume of orders. It increases the size of each subsequent insurance order compared to the base one.

* Volume formula for the nth SO: Volume SO (N) = (Volume BO) * (Martingale^N).

* With a value of 1.2, the volume of the first SO will be 1.2 times greater than the base, the second — 1.44 times (`1.2 * 1.2`) and so on.

* Leverage: Specify the size of your leverage. This parameter is used exclusively for calculating and displaying the approximate liquidation price. It does not affect the size of positions, but it helps to visually assess the risks.

* Liquidation: Enables or disables the calculation and display of the liquidation line on the chart.

* Margin type: Allows you to select a method for calculating the liquidation price, simulating the logic of exchanges:

* Isolated: The liquidation price is calculated based on the size and leverage of the current open position only.

* Cross: The calculation simulates using the entire available balance to maintain a position. In the strategy, the liquidation price is calculated as the level at which the loss on the current transaction is equal to the current capital.

* Commission (%): Specify the percentage of your exchange's commission per transaction. The correct value of this parameter is crucial for obtaining realistic backtest results.

// ------------------------

3. 🕸️ Grid Management 🕸️

This group is responsible for the logic of safety orders and advanced mechanics such as Channel Mode and MultiGRID.

* SO Type: Defines the logic of placing averaging orders.

* GRID: Classic grid. All safety orders are placed in advance as limit orders.

* DCA: Signal averaging. The strategy is waiting for a signal from an external indicator to place a market averaging order.

* GRID+DCA: Hybrid. The strategy waits for a signal, and if it arrives, places a limit order at the appropriate price level of the grid or executes a market order if the signal has arrived below the limit order level.

* Signal for SO: A data source (indicator) that will be used for signals in DCA and GRID+DCA modes.

* ↔️ Channel Mode: When this option is enabled, the strategy tries to trade in a sideways range. After partially closing a take profit position, it immediately places a limit order for re-entry at the price of the last triggered safety order. This creates a buy-sell cycle within the local channel.

* Best Price Only: This filter adds an additional condition for averaging in DCA and MultiGRID modes (when it operates on a signal). The next averaging order or a new grid will be activated only if the current price is more favorable (lower for long, higher for short) than the price of the previous entry.

* 🧩 MultiGRID ⮕ Enables cascading grid mode.

* Grid Count: The total number of grids that can be activated sequentially.

* Offset: Percentage deviation from the price of the last order of the previous grid. When this margin is reached, the following grid of orders is activated (this mode does not require a signal).

* Or signal: Allows you to use the signal from an external indicator as a trigger to activate the next grid. The checkmark on the right turns on this mode.

// ------------------------

4. 🎯 Entry and Stop 🎯

This group of settings allows you to fine-tune the conditions for starting a new trade and all aspects related to protective stop orders, including the complex mechanics of trailing and managing SL after partial take profits.

* 🎯 Signal: A data source (indicator) that will be used to determine when to enter a trade. The strategy expects a value of 1 for the start of a long trade and -1 for a short trade.

* Min Bars: Sets the minimum number of candles that must pass from the moment of opening the previous trade to the moment of opening the next one. A value of 0 disables this filter. This is a useful tool to prevent overly frequent entries in a "noisy" market.

* Non-stop: If this option is enabled, the strategy ignores the Entry Signal and opens a new trade immediately after closing the previous one (taking into account the Min Bars filter, if it is set). This turns the strategy into a constantly working mechanism that is always on the market.

* 🛑 SL Type: Defines the base price from which the stop loss percentage will be calculated. The stop loss in the first section must be enabled for this block of settings to work.

* From the entry point: SL is always calculated from the opening price of the very first base order. It remains static throughout the entire transaction unless it is moved by other functions.

* From breakeven line: SL is dynamically recalculated and shifted each time a safety order is executed. It always follows the average price of the position, being at a given percentage distance from it.

* From last executed SO: SL is recalculated from the price of the last executed order, whether it is a base or a safety order.

* From last SO: SL is calculated from the price of the most recent possible safety order in the grid. This is usually the most remote and conservative type of SL.

* Trailing SL Type: Defines the algorithm by which the stop loss will move after its activation.

* Standard: Classic trailing. After activation, SL will follow the price at a fixed distance.

* ATR: SL will follow the price at a distance equal to the value of the ATR indicator multiplied by the specified multiplier.

* External Source: SL will follow any selected line of the third-party indicator.

* Period and Multiplier: Common parameters for all types of trailing.

* Source: The source of the line for the trailing SL of the third-party indicator.

* Trailing SL after entry: The mode of activation of the trailing SL after entering the transaction

* SL management after TP (sections 1️⃣, 2️⃣, 3️⃣): These three blocks allow you to create a complex stop loss management logic as profits are recorded.

For each take profit level (TP1, TP2, TP3), you can configure:

* SL BE / SL TP1 / SL TP2: When the corresponding TP is reached, the stop loss will be moved to the breakeven point (for TP1), to the TP1 price level (for TP2) or to the TP2 price level (for TP3).

* Trailing SL: When the corresponding TP is reached, the trailing stop loss is activated according to the settings above.

* By ↔️ Signal: A very powerful option. If it is enabled, the above action (SL transfer or trailing activation) will occur when the opposite trading signal is received from an external indicator. This allows you to protect profits or reduce losses if the market turns sharply, even before reaching the target.

* SL Delay ⮕ Allows you to delay the activation of the stop loss.

* Number of Bars: The Stop loss will be physically placed on the market only after the specified number of candles has passed since entering the trade. This can help to avoid "taking out" the stop with a random short movement (squiz) immediately after opening a position.

* SL Block: Unique defensive mechanics for trading both ways (`Strategy Type: Both`).

* Number of SL: If the strategy receives the specified number of stop losses in a row in one direction (for example, 2 stops long), it temporarily blocks the opportunity to open new trades in that direction.

* Lock Reset mode:

* By direction: The lock is lifted if a profitable trade is closed in the allowed direction or if a stop loss is triggered in the opposite direction.

* First profit: The lock is lifted after closing any profitable transaction, regardless of its direction.

// ------------------------

5. ✅ Take Profit ✅

This group of settings provides comprehensive control over profit taking, from a simple take profit to a complex system of partial closures and trailing.

* ✅ TP Type: Defines the base price for calculating the percentage deviation of the take profit.

* From entry point: TP is calculated from the base order price.

* From breakeven line: TP dynamically follows the average position price.

* From last executed SO: TP is calculated from the price of the last executed order.

* Filters for closing on signal

* Only ➕: If TP is triggered by a signal, the deal will be closed only if it is in the black relative to the average price.

* Or >TP: If TP is triggered by a signal, the trade will be closed only if the closing price is better than (or equal to) the estimated price of this TP.

* TP type of trailing: Yes, take profit has a trailing too! It works differently than the SL trailing.

* Standard / ATR: After the price touches the "virtual" TP level, the trailing is activated. He does not place a stop order, but begins to move away from the price, dynamically moving the limit order to close further and further in the profitable direction, allowing him to collect the maximum from the impulse movement.

* External Source: TP will follow any selected line of the third-party indicator.

* Period and Multiplier: Parameters for calculating the trailing margin TP.

* Source: The source of the line for the trailing TP of the third-party indicator.

* TP level settings (sections 1️⃣, 2️⃣, 3️⃣, 4️⃣): The strategy supports up to four independent take profit levels, which allows for a flexible system of partial commits.

For each level, you can set:

* TP: Enable the level and set its percentage deviation from the base price.

* Size: What percentage of the current position will be closed when this level is reached. For the last active TP, this parameter is ignored, and 100% of the remaining position is closed.

* Trailing TP: Enable the above-described trailing mechanism for this particular level.

* Signal: Enable closing based on the signal from the external indicator for this level.

* Or take: If both the closing on the signal and the limit order are enabled, then whatever comes first will work.

* After SO: Activate this TP level only after the specified number of safety orders has been executed. This allows you to set closer targets for riskier (deeply averaged) positions.

// ------------------------

6. 🔬 GRID and MultiGrid Analysis on Lower TFs (LTF) 🔬

This group activates one of the most important functions for accurate testing of grid strategies.

* Enable LTF Calculation ⮕ The main switch of the analysis mode on the lower timeframes.

* Timeframe selection: A drop-down list where you can select a timeframe for detailed analysis. For example, if your main schedule is 1 hour, you can select 1 minute here. The strategy will emulate the trading of minute candles within each hour candle.

❗️Important: As mentioned in the first part, the use of this mode is critically necessary to obtain realistic backtest results, especially for strategies with a dense grid of orders. Without it, the results may be overly optimistic and not reflect the real dynamics of the market. It should be remembered that TradingView imposes a limit on the number of intra-bars (minor TF bars) that can be requested. This is usually about 100,000 bars.

// ------------------------

7. 🕘 Backtest Date Range 🕘

This group allows you to focus testing on a specific historical period.

* Limit Date Range: Enables date filtering.

* Start time: The date and time when the strategy will start analyzing and opening deals.

* End time: The date and time after which the strategy will stop opening new deals and complete testing.

// ------------------------

8. 🎨 Visualization 🎨

All the options responsible for the appearance and information content of the chart are collected here.

* Show PnL labels: Enables/disables the display of text labels with the result (profit/loss) after closing each trade.

* Statistics Table: Enables/disables the main dashboard with detailed statistics on the results of the backtest.

* Strategy Settings Table: Enables/disables an additional panel that summarizes all the key parameters of the current configuration.

* Monthly Profit Table: Enables/disables a table with a breakdown of percentage returns by month and year.

* Table settings: For each of the three tables, you can individually adjust the Text size and Table Position on the screen to position them as conveniently as possible.

* Decimal places: Defines how many decimal places will be displayed in numeric values in tables and on labels.

// ------------------------

9. ✉️ Webhook Settings ✉️

This group is intended for traders who want to automate trading on strategy signals using third-party services and exchanges (for example, 3Commas, WunderTrading, Cryptorobotics, Cryptohopper, Bitsgap, Binance, ByBit, OKX, Pionex, Bitget or proprietary solutions).

For each key event in the strategy, there is a separate switch and a text field:

* Webhook for Open: Enable and set a message for the webhook that will be sent when the base order is opened.

* Webhook for Averaging: A message sent when executing any insurance order.

* Webhook for Take Profit: A message sent when closing on take profit (including partial ones).

* Webhook for Stop-Loss: A message sent when a stop loss is closed.

You can insert a JSON code or any other message format that your service requires for automation into the text fields. The strategy supports special placeholders (for example, `{{strategy.order.alert_message}}`), which allow you to dynamically insert the necessary data into the message, such as the amount of USDT or the percentage of the deposit for entry, averaging and take profit orders.

TrendBreaks & MA Divergence v1.3 — couleurs perso (panel)clean and easy predictive mouvements and swing stratagy

FREEDOM - TJR Model\ FREEDOM – TJR Model\ 🚀

\ Automates TJR’s well-known NQ playbook with clean visuals, filters, and alerts—so you can focus on execution.\

\ Core idea\

1. Trade \ NQ\ in the \ New York session\ 🗽

2. Wait for a \ liquidity sweep\ of a \ prior session\ High/Low (Asia or London) ✂️

3. Confirm with \ SMT (NQ vs ES) divergence\ 🔀

4. Act on a \ proprietary entry signal\ 🔒

5. Risk at the swing 🛡️, target \ untapped internal/session liquidity\ 🎯

This indicator draws those session levels for you, tracks sweeps, detects SMT, applies higher-timeframe confluence, and fires alerts that respect your time window and filters.

---

\ What it draws & detects\

\ • Sessions & Liquidity Sweeps\ 🕒

* Plots \ Asia / London / New York\ session bands.

* On session close, it freezes the session’s \ High/Low\ as dotted “previous-session levels” and \ extends them forward\ until price \ crosses\ (choose \ Wicks\ or \ Close\ ).

* When price takes a previous-session \ High\ → \ Buyside sweep\ ; takes a \ Low\ → \ Sellside sweep\ .

* Optional \ Sweep Zones\ expand around the swept level using an \ ATR(21)\ margin; can auto-fade “fake” sweeps.

\ Tip: Keep “Extend previous session High/Low until cross” ON to maintain a clean roadmap into NY open.\

\ • SMT Divergence (NQ vs ES)\ 🔀

* Classic pivot-to-pivot SMT:

* \ Bearish SMT\ = NQ makes a \ higher high\ while ES does \ not\ .

* \ Bullish SMT\ = NQ makes a \ lower low\ while ES does \ not\ .

* Draws \ lines\ from pivot to pivot (no chart spam), with optional inline “SMT” label and optional confidence \ score\ (0–100) based on strength + recency.

* Context aware:

* Only shows \ Bearish SMT\ after a \ buy-side sweep\ (previous-session High taken).

* Only shows \ Bullish SMT\ after a \ sell-side sweep\ (previous-session Low taken).

* Respects your \ NY time window\ if enabled.

\ • Proprietary Entry Signals\ 🔒

* Prints entry lines + arrows only when your rules align (proprietary detection under the hood).

* Respects:

* \ Session-sweep bias\ (optional): Sells only after buy-side sweep; Buys only after sell-side sweep.

* \ Monotonic filter\ : new Sell must be \ higher\ than last Sell; new Buy must be \ lower\ than last Buy (resets each session).

* \ Minimum distance\ to nearest previous-session dotted level (in ticks).

* \ NY time filter\ window.

* \ HTF confluence\ (see below).

---

\ HTF Confluence (optional)\ 📈

* Choose \ MA slope\ (\ EMA/SMA/RMA/WMA\ ) or \ HH/HL structure\ on a higher timeframe (e.g., 60m/240m).

* Entry arrows and alerts can be gated so they only print when HTF bias agrees with the setup.

\ Tip: Start with EMA 50 on 60m for a smooth directional filter; add HH/HL only if you want stricter structure confirmation.\

---

\ Dashboard (bottom-right)\ 🧩

* \ VWAP state\ :

* \ Overbought\ (🔴) if close > VWAP + (mult × stdev)

* \ Oversold\ (🟢) if close < VWAP − (mult × stdev)

* Otherwise \ Neutral\ (⚪️)

* \ Premium / Discount\ vs previous-session 50% midline: Premium = above (red bias), Discount = below (green bias).

* \ SMT row\ : Bullish / Bearish / Neutral with optional score.

---

\ How to use the settings (quick tour)\

\ ENTRY\

* \ Entry Swing Length\ : lower = more signals.

* \ Confirmation\ : \ Candle Close\ or \ Wicks\ for breakout.

* \ Filter entry by session sweeps\ : enforces “sell after buy-side sweep, buy after sell-side sweep.”

* \ Minimum distance (ticks)\ : blocks entries too close to previous-session dotted levels.

* \ Replay mode\ : keeps entries visible in Bar Replay.

* \ NY Time filter\ : default \ 08:00–14:00 NY\ ; arrows/alerts respect the window.

* \ Arrow offset (ticks)\ : how far above/below the candle to plot the arrow.

\ SESSION SWEEPS\

* Toggle \ Buyside/Sellside zones\ , adjust \ ATR(21)\ margin & length.

* \ Hide Fake Sweep Zones\ (default ON).

* \ Extend H/L until cross\ (Wicks/Close).

* Optional \ daily reset\ for unswept dotted lines.

\ SESSIONS\

* Enable/disable \ Asia, London, NY AM, NY PM\ ; set start/end; choose color; extend midline if desired.

* DST toggles for NY/London.

\ HTF Confluence\

* Turn it ON/OFF; pick timeframe & method (MA slope or HH/HL); set MA type/length or swing length.

\ Dashboard\

* Show/hide table; set VWAP stdev length/multiplier.

* SMT settings: comparison symbol (\ default ES1!\ ), pivot length, show score/labels, recency window, etc.

\ Alerts\ (always last) 🔔

* \ Session line cross\ : choose Highs/Lows and crossing mode (\ Same as extension / Wicks / Close\ ).

* \ Entry alerts\ : \ Filtered / Unfiltered / Both\ .

* \ Filtered\ = respects sweep bias, HTF confluence, minimum distance, monotonic rule, and time window.

* \ Unfiltered\ = ignores sweep bias/HTF/monotonic (still respects minimum distance + time window).

* All entry alerts also respect the \ NY time window\ when enabled.

---

\ Suggested workflow\

* Open NQ on a 1–5m chart.

* Let the dotted \ previous-session H/L\ extend into NY; wait for a \ sweep\ .

* Check \ SMT\ : after buy-side sweep → look for \ bearish SMT\ ; after sell-side sweep → look for \ bullish SMT\ .

* Take the \ proprietary entry\ when filters agree.

* Stop at the swing; aim for \ untapped internal/session liquidity\ .

* Let \ alerts\ handle the monitoring.

---

\ Why traders like it\

* It mirrors the model popularized by \ TJR\ while removing the chart admin: sessions, sweeps, SMT, HTF gating, distances, monotonic sequencing, time windows, and ready-to-use alerts—so your execution stays consistent. ✨

---

\ Disclaimer\ ⚠️

\ This tool is for educational purposes only and does not constitute financial advice. Markets involve risk; always do your own research and test in replay/paper before trading live. FREEDOM – TJR Model is inspired by TJR’s publicly known framework but is not affiliated with, endorsed by, or sponsored by TJR. You are solely responsible for your trading decisions and outcomes.\

Straddle Charts - Live (Enhanced)Track options straddles with ease using the Straddle Charts - Live (Enhanced) indicator! Originally inspired by @mudraminer, this Pine Script v5 tool visualizes live call, put, and straddle prices for instruments like BANKNIFTY. Plotting call (green), put (red), and straddle (black) prices in a separate pane, it offers real-time insights for straddle strategy traders.

Key Features:

Live Data: Fetches 1-minute (customizable) option prices with error handling for invalid symbols.

Price Table: Displays call, put, straddle prices, and percentage change in a top-left table.

Volatility Alerts: Highlights bars with straddle price changes above a user-defined threshold (default 5%) with a yellow background and concise % labels.

Robust Design: Prevents plot errors with na checks and provides clear error messages.

How to Use: Input your call/put option symbols (e.g., NSE:NIFTY250814C24700), set the timeframe, and adjust the volatility threshold. Monitor straddle costs and volatility for informed trading decisions.

Perfect for options traders seeking a simple, reliable tool to track straddle performance. Check it out and share your feedback!

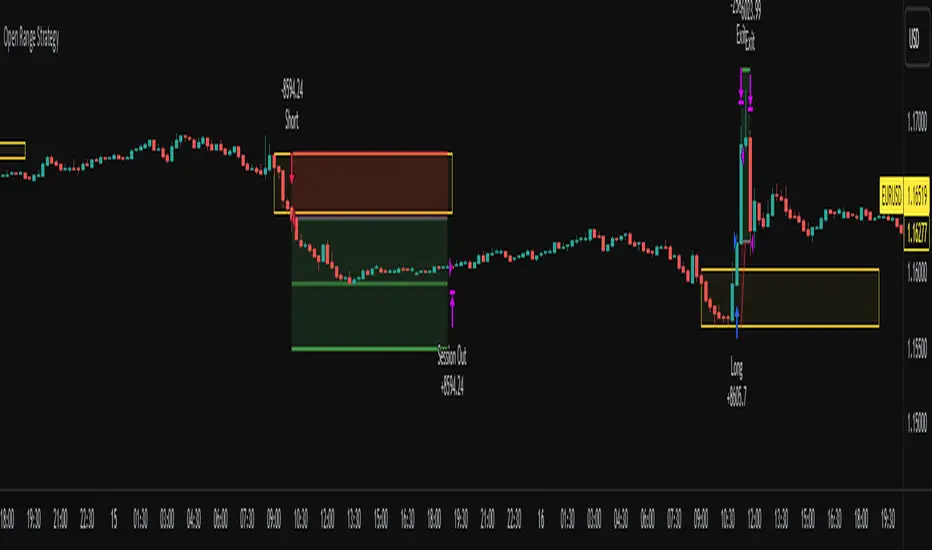

Open Range Breakout Strategy With Multi TakeProfitHello everyone,

For a while, I’ve been wanting to develop new scripts, but I couldn’t decide what to create. Eventually, I came up with the idea of coding traditional and well-known trading strategies—while adding modern features such as multi–take profit options. For the first strategy in this series, I chose the Open Range Strategy .

For those unfamiliar with it, the Open Range Strategy is a trading approach where you define a specific time period at the beginning of a trading session—such as the first 15 minutes, 30 minutes, or 1 hour—and mark the highest and lowest prices within that range. These levels then act as reference points for potential breakouts: if the price breaks above the range, it may signal a long entry; if it breaks below, it may indicate a short entry. This method is popular among day traders for capturing early momentum in the market.

Since this strategy is generally used as an intraday strategy , I added a Trade Session feature. This allows you to define the exact time window during which trades can be opened. Once the session ends, all positions are automatically closed, ensuring trades remain within your chosen intraday period.

Even though it’s a relatively simple concept, I’ve come across many different variations of it. That’s why I created a highly customizable project. Under the Session Settings, you can select the time window you want to define as your range. Whether it’s the first 15-minute candle or the entire first hour, the choice is entirely yours.

For stop-loss placement, there are two different options:

Middle of the Range – The stop loss is placed at the midpoint between the high and low of the defined range, offering a balanced buffer for both bullish and bearish setups.

Top/Bottom of the Range – The stop loss is placed just beyond the range’s high for short trades or just below the range’s low for long trades, providing a more conservative risk approach.

I’ve always been a big fan of the multi take-profit feature, so I added two different take-profit targets to this project. Take profits are calculated based on a Risk-to-Reward Ratio, which you can adjust in the settings. You can also set different position sizes for each target, allowing you to scale out of trades in a way that suits your strategy.

The result is a flexible, user-friendly strategy script that brings together a classic approach with modern risk management tools—ready to be tailored to your trading style

Backtest - Strategy Builder [AlgoAlpha]🟠 OVERVIEW

This script by AlgoAlpha is a modular Strategy Builder designed to let traders test custom trade entry and exit logic on TradingView without writing their own Pine code. It acts as a framework where users can connect multiple external signals, chain them in sequences, and run backtests with built-in leverage, margin, and risk controls. Its main strength is flexibility—you can define up to five sequential steps for entry and exit conditions on both long and short sides, with logic connectors (AND/OR) controlling how conditions combine. This lets you test complex multi-step confirmation workflows in a controlled, visual backtesting environment.

🟠 CONCEPTS

The system works by linking external signals —these can be values from other indicators, and/or custom sources—to conditional checks like “greater than,” “less than,” or “crossover.” You can stack these checks into steps , where all conditions in a step must pass before the sequence moves to the next. This creates a chain of logic that must be completed before a trade triggers. On execution, the strategy sizes positions according to your chosen leverage mode ( Cross or Isolated ) and allocation method ( Percent of equity or absolute USD value]). Liquidation prices are simulated for both modes, allowing realistic margin behaviour in testing. The script also tracks performance metrics like Sharpe, Sortino, profit factor, drawdown, and win rate in real time.

🟠 FEATURES

Up to 5 sequential steps for both long and short entries, each with multiple conditions linked by AND/OR logic.

Two leverage modes ( Cross and Isolated ) with independent long/short leverage multipliers.

Separate multi-step exit triggers for longs and shorts, with optional TP/SL levels or opposite-side triggers for flipping positions.

Position sizing by equity percent or fixed USD amount, applied before leverage.

Realistic liquidation price simulation for margin testing.

Built-in trade gating and validation—prevents trades if configuration rules aren’t met (e.g., no exit defined for an active side).

Full performance dashboard table showing live strategy status, warnings, and metrics.

Configurable bar coloring based on position side and TP/SL level drawing on chart.

Integration with TradingView's strategy backtester, allowing users to view more detailed metrics and test the strategy over custom time horizons.

🟠 USAGE

Add the strategy to your chart. In the settings, under Master Settings , enable longs/shorts, select leverage mode, set leverage multipliers, and define position sizing. Then, configure your Long Trigger and Short Trigger groups: turn on conditions, pick which external signal they reference, choose the comparison type, and assign them to a sequence step. For exits, use the corresponding Exit Long Trigger and Exit Short Trigger groups, with the option to link exits to opposite-side entries for auto-flips. You can also enable TP and/or SL exits with custom sources for the TP/SL levels. Once set, the strategy will simulate trades, show performance stats in the on-chart table, and highlight any configuration issues before execution. This makes it suitable for testing both simple single-signal systems and complex, multi-filtered strategies under realistic leverage and margin constraints.

🟠 EXAMPLE

The backtester on its own does not contain any indicator calculation; it requires input from external indicators to function. In this example, we'll be using AlgoAlpha's Smart Signals Assistant indicator to demonstrate how to build a strategy using this script.

We first define the conditions beforehand:

Entry :

Longs – SSA Bullish signal (strong OR weak)

Shorts – SSA Bearish signal (strong OR weak)

Exit

Longs/Shorts: (TP/SL hit OR opposing signal fires)

Other Parameters (⚠️Example only, tune this based on proper risk management and settings)

Long Leverage: default (3x)

Short Leverage: default (3x)

Position Size: default (10% of equity)

Steps

Load up the required indicators (in this example, the Smart Signals Assistant).

Ensure the required plots are being output by the indicator properly (signals and TP/SL levels are being plotted).

Open the Strategy Builder settings and scroll down to "CONDITION SETUP"; input the signals from the external indicator.

Configure the exit conditions, add in the TP/SL levels from the external indicator, and add an additional exit condition → {{Opposite Direction}} Entry Trigger.

After configuring the entry and exit conditions, the strategy should now be running. You can view information on the strategy in TradingView's backtesting report and also in the Strategy Builder's information table (default top right corner).

It is important to note that the strategy provided above is just an example, and the complexity of possible strategies stretches beyond what was shown in this short demonstration. Always incorporate proper risk management and ensure thorough testing before trading with live capital.

Script pago

EMA Deviation Strategy📌 Strategy: EMA Deviation Strategy

The EMA Deviation Strategy identifies potential reversal points by measuring how far the current price deviates from its Exponential Moving Average (EMA). It dynamically tracks the minimum and maximum deviation levels over a user-defined lookback period, and enters trades when price reaches extreme zones.

🔍 Core Logic:

• Buy Entry: When price deviates significantly below the EMA, approaching the historical minimum deviation — signaling a potential rebound.

• Sell Entry: When price deviates significantly above the EMA, nearing the historical maximum deviation — signaling a possible pullback.

• Optional Take Profit / Stop Loss: Manage risk with customizable exit levels.

⚙️ Customizable Inputs:

• EMA length and lookback period

• Threshold sensitivity for entry signals

• Take profit and stop loss percentages

📈 Best Used For:

• Mean reversion setups

• Assets with cyclical or range-bound behavior

• Identifying short-term overbought/oversold conditions

Mutanabby_AI | Algo Pro Strategy# Mutanabby_AI | Algo Pro Strategy: Advanced Candlestick Pattern Trading System

## Strategy Overview

The Mutanabby_AI Algo Pro Strategy represents a systematic approach to automated trading based on advanced candlestick pattern recognition and multi-layered technical filtering. This strategy transforms traditional engulfing pattern analysis into a comprehensive trading system with sophisticated risk management and flexible position sizing capabilities.

The strategy operates on a long-only basis, entering positions when bullish engulfing patterns meet specific technical criteria and exiting when bearish engulfing patterns indicate potential trend reversals. The system incorporates multiple confirmation layers to enhance signal reliability while providing comprehensive customization options for different trading approaches and risk management preferences.

## Core Algorithm Architecture

The strategy foundation relies on bullish and bearish engulfing candlestick pattern recognition enhanced through technical analysis filtering mechanisms. Entry signals require simultaneous satisfaction of four distinct criteria: confirmed bullish engulfing pattern formation, candle stability analysis indicating decisive price action, RSI momentum confirmation below specified thresholds, and price decline verification over adjustable lookback periods.

The candle stability index measures the ratio between candlestick body size and total range including wicks, ensuring only well-formed patterns with clear directional conviction generate trading signals. This filtering mechanism eliminates indecisive market conditions where pattern reliability diminishes significantly.

RSI integration provides momentum confirmation by requiring oversold conditions before entry signal generation, ensuring alignment between pattern formation and underlying momentum characteristics. The RSI threshold remains fully adjustable to accommodate different market conditions and volatility environments.

Price decline verification examines whether current prices have decreased over a specified period, confirming that bullish engulfing patterns occur after meaningful downward movement rather than during sideways consolidation phases. This requirement enhances the probability of successful reversal pattern completion.

## Advanced Position Management System

The strategy incorporates dual position sizing methodologies to accommodate different account sizes and risk management approaches. Percentage-based position sizing calculates trade quantities as equity percentages, enabling consistent risk exposure across varying account balances and market conditions. This approach proves particularly valuable for systematic trading approaches and portfolio management applications.

Fixed quantity sizing provides precise control over trade sizes independent of account equity fluctuations, offering predictable position management for specific trading strategies or when implementing precise risk allocation models. The system enables seamless switching between sizing methods through simple configuration adjustments.

Position quantity calculations integrate seamlessly with TradingView's strategy testing framework, ensuring accurate backtesting results and realistic performance evaluation across different market conditions and time periods. The implementation maintains consistency between historical testing and live trading applications.

## Comprehensive Risk Management Framework

The strategy features dual stop loss methodologies addressing different risk management philosophies and market analysis approaches. Entry price-based stop losses calculate stop levels as fixed percentages below entry prices, providing predictable risk exposure and consistent risk-reward ratio maintenance across all trades.

The percentage-based stop loss system enables precise risk control by limiting maximum loss per trade to predetermined levels regardless of market volatility or entry timing. This approach proves essential for systematic trading strategies requiring consistent risk parameters and capital preservation during adverse market conditions.

Lowest low-based stop losses identify recent price support levels by analyzing minimum prices over adjustable lookback periods, placing stops below these technical levels with additional buffer percentages. This methodology aligns stop placement with market structure rather than arbitrary percentage calculations, potentially improving stop loss effectiveness during normal market fluctuations.

The lookback period adjustment enables optimization for different timeframes and market characteristics, with shorter periods providing tighter stops for active trading and longer periods offering broader stops suitable for position trading approaches. Buffer percentage additions ensure stops remain below obvious support levels where other market participants might place similar orders.

## Visual Customization and Interface Design

The strategy provides comprehensive visual customization through eight predefined color schemes designed for different chart backgrounds and personal preferences. Color scheme options include Classic bright green and red combinations, Ocean themes featuring blue and orange contrasts, Sunset combinations using gold and crimson, and Neon schemes providing high visibility through bright color selections.

Professional color schemes such as Forest, Royal, and Fire themes offer sophisticated alternatives suitable for business presentations and professional trading environments. The Custom color scheme enables precise color selection through individual color picker controls, maintaining maximum flexibility for specific visual requirements.

Label styling options accommodate different chart analysis preferences through text bubble, triangle, and arrow display formats. Size adjustments range from tiny through huge settings, ensuring appropriate visual scaling across different screen resolutions and chart configurations. Text color customization maintains readability across various chart themes and background selections.

## Signal Quality Enhancement Features

The strategy incorporates signal filtering mechanisms designed to eliminate repetitive signal generation during choppy market conditions. The disable repeating signals option prevents consecutive identical signals until opposing conditions occur, reducing overtrading during consolidation phases and improving overall signal quality.

Signal confirmation requirements ensure all technical criteria align before trade execution, reducing false signal occurrence while maintaining reasonable trading frequency for active strategies. The multi-layered approach balances signal quality against opportunity frequency through adjustable parameter optimization.

Entry and exit visualization provides clear trade identification through customizable labels positioned at relevant price levels. Stop loss visualization displays active risk levels through colored line plots, ensuring complete transparency regarding current risk management parameters during live trading operations.

## Implementation Guidelines and Optimization

The strategy performs effectively across multiple timeframes with optimal results typically occurring on intermediate timeframes ranging from fifteen minutes through four hours. Higher timeframes provide more reliable pattern formation and reduced false signal occurrence, while lower timeframes increase trading frequency at the expense of some signal reliability.

Parameter optimization should focus on RSI threshold adjustments based on market volatility characteristics and candlestick pattern timeframe analysis. Higher RSI thresholds generate fewer but potentially higher quality signals, while lower thresholds increase signal frequency with corresponding reliability considerations.

Stop loss method selection depends on trading style preferences and market analysis philosophy. Entry price-based stops suit systematic approaches requiring consistent risk parameters, while lowest low-based stops align with technical analysis methodologies emphasizing market structure recognition.

## Performance Considerations and Risk Disclosure

The strategy operates exclusively on long positions, making it unsuitable for bear market conditions or extended downtrend periods. Users should consider market environment analysis and broader trend assessment before implementing the strategy during adverse market conditions.

Candlestick pattern reliability varies significantly across different market conditions, with higher reliability typically occurring during trending markets compared to ranging or volatile conditions. Strategy performance may deteriorate during periods of reduced pattern effectiveness or increased market noise.

Risk management through stop loss implementation remains essential for capital preservation during adverse market movements. The strategy does not guarantee profitable outcomes and requires proper position sizing and risk management to prevent significant capital loss during unfavorable trading periods.

## Technical Specifications

The strategy utilizes standard TradingView Pine Script functions ensuring compatibility across all supported instruments and timeframes. Default configuration employs 14-period RSI calculations, adjustable candle stability thresholds, and customizable price decline verification periods optimized for general market conditions.

Initial capital settings default to $10,000 with percentage-based equity allocation, though users can adjust these parameters based on account size and risk tolerance requirements. The strategy maintains detailed trade logs and performance metrics through TradingView's integrated backtesting framework.

Alert integration enables real-time notification of entry and exit signals, stop loss executions, and other significant trading events. The comprehensive alert system supports automated trading applications and manual trade management approaches through detailed signal information provision.

## Conclusion

The Mutanabby_AI Algo Pro Strategy provides a systematic framework for candlestick pattern trading with comprehensive risk management and position sizing flexibility. The strategy's strength lies in its multi-layered confirmation approach and sophisticated customization options, enabling adaptation to various trading styles and market conditions.

Successful implementation requires understanding of candlestick pattern analysis principles and appropriate parameter optimization for specific market characteristics. The strategy serves traders seeking automated execution of proven technical analysis techniques while maintaining comprehensive control over risk management and position sizing methodologies.

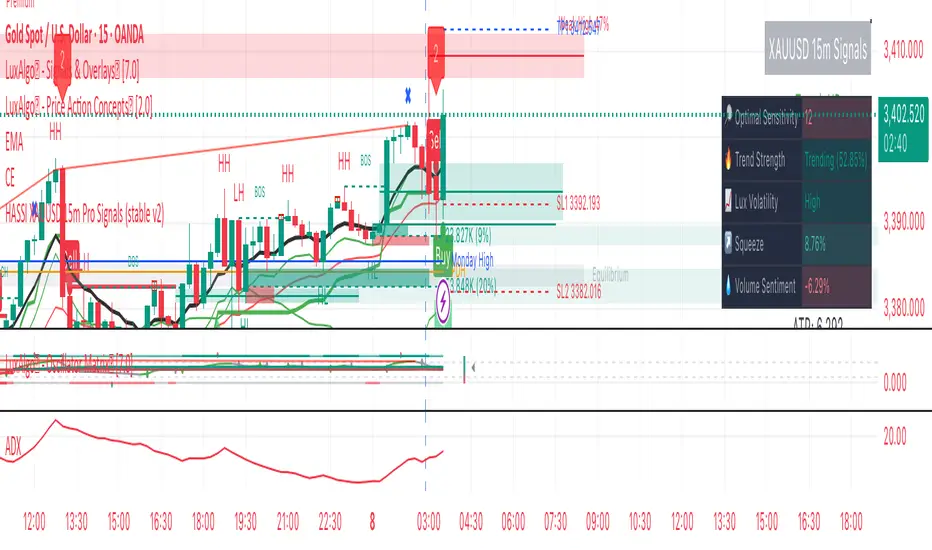

Hassi XAUUSD STRATEGY BOTGold (XAUUSD) 15m trend+momentum based signals with EMA(9/21/200), RSI, custom ADX, ATR-based SL/TP & alerts

Works on XAUUSD 15m.

Entry: EMA9/21 cross + price relative to EMA200 + RSI filter + custom ADX trend strength.

Risk: default SL=1.5×ATR, TP=2×ATR (editable).

Notes: No financial advice. Backtest before live use. Avoid high-impact news whipsaws.

Backtest [OptAlgo]This backtest script is designed to convert ideas or indicators into backtest results. The script creates buy/sell signals by comparing price sources against fixed values or other imported plots using many comparison methods. It has many features including multiple exit systems: TP/SL, custom plot-based stops and more. It supports full trading automation through webhook alerts with live signal processing.

🔢 Signal Creation System

→ Values Group : Compare price sources against fixed numerical values

→ Plots Group : Compare two different price sources/indicators against each other

→ Flexible Comparisons : 15+ comparison methods (equal, crossover, rising...)

→ Signal Types : Long, Short, Close All, Block signals, and combination signals

→ Merge Rules : Minimum condition requirements for signal activation

🔀 Advanced Signal Logic

→ Counter Signals : Choose between reversing positions or closing them

→ Signal Inversion : Flip all buy/sell signals with one toggle

→ External Signal Import : Import coded signals (1=Long, -1=Short, 0=Close)

→ Day Blocker : Enable/disable trading on specific weekdays

→ Session Control : Limit trading to specific market sessions

⚙️ Strategy Settings

→ Position Sides : All Ways, Long Only, or Short Only modes

→ Signal Control : Individual enable/disable for long and short signals

→ Counter Signal Mode : Reverse Open Position vs Close Open Position

→ Signal Reversal : Global signal inversion capability

🔰 Risk Management (Limiter Settings)

→ Leverage Control : Leverage with liquidation warnings

→ Drawdown Limit : Auto-halt strategy at specified drawdown percentage

→ Tradable Ratio : Use portion of available balance (0.01-1.0)

→ Contract Limit : Cap maximum contract size regardless of balance

🎯 TP/SL System

→ Fixed TP/SL : Set percentage-based take profit and stop loss

→ Custom Plot Stops : Use any indicator/plot as dynamic stop loss

→ ATR-Based Exits : Volatility-adjusted TP/SL using Average True Range

→ Realistic Protection : Prevents unrealistic TP/SL prices in live trading

→ Stop Modes : Instant (Sudden) vs Candle Close execution

→ ATR Stop Loss : Override fixed SL with volatility-based calculations

→ ATR Take Profit : Dynamic TP based on market volatility

→ Trailing Options : Safe, Normal, or Aggressive trailing methods

→ Calculation Modes : Normal, Volume-weighted, or Limited (with max %) options

→ Volume Integration : ATR levels adjust based on volume influx

🤖 Automation & Alerts

→ Webhook Integration : Send JSON alerts for automated execution

→ Live Signals : Real-time signal processing (every tick vs bar close)

→ Strategy Key : Unique identifier for automated systems

→ Early Entry : Send alerts X seconds before candle close

→ Fast Execution : Prevent signal lag in automated trading

🐞 Development Tools

→ Alert Plotting : Visualize signals directly on chart (disable for live alerts)

→ Professional Mode : Remove UI controls for faster calculation

→ Debug : Metrics are plotted in data window.

📊 Key Advantages

→ Multi-Condition Logic : Combine multiple indicators with flexible rules

→ Risk-First Design : Built-in drawdown and leverage protection

→ Automation Ready : Full webhook and alert system integration

⚠️ Important Warnings

→ High leverage combined with high SL may adjust to liquidation price

→ Use consistent leverage across all strategies on same trading isolated margin pair

→ Live signals require "Calculate on every tick" enabled in settings

→ Disable alert plotting when creating actual alerts to prevent latency

Dynamic DCA Envelope – Beta V1.1Dynamic DCA Envelope-Beta V1.1 is a preview version of a Dollar-Cost Averaging (DCA) strategy designed for trending or volatile markets.

-Long Positions Only

-Intended for Cryptocurrency, but can be used in any market

-1 and 4 hour timeframe

-Average Commissions 0.1%-0.3% per trade (Cryptocurrency)

What it does:

This strategy identifies buying opportunities when price closes below a dynamic envelope (based on EMA). After 3 consecutive closes below the lower envelope, the system arms a buy condition. A DCA buy-in is triggered when price bounces by a configurable percentage from the trailing low. The strategy supports up to 3 buy-ins, each equally sized, and closes the entire position at a fixed take profit or stop loss.

How it works:

-Entry logic is based on price deviation from an EMA envelope

-Waits for 3 closes below the envelope to detect weakness

-Uses bounce percentage from the lowest point to trigger each buy

-Includes cooldown logic between buys to avoid clustering

-All positions are closed when TP or SL is hit

How to use it:

-Use on trending assets with volatility (e.g., crypto, tech stocks)

-Adjust inputs to match asset behavior:

-EMA Length

-Envelope Offset %

-Bounce % (Trailing DCA)

-Take Profit / Stop Loss

-View strategy performance in the Strategy Tester tab

What’s unique:

Unlike most DCA scripts that immediately average down, this version includes:

-Trigger logic requiring multiple closes below trend

-Bounce-based entry to avoid catching a falling knife

-Cooldown resets to prevent overtrading

-A true entry–wait–buy–reset loop mimicking disciplined execution

*This is a beta version intended as a preview. A full Pro version is in development, which includes:

-SmartScaling logic

-Trailing take profit

-Multi-symbol scanning

-Backtest range limits

-Risk-adjusted filtering

SAFE Leverage x50Description:

Safe Leverage x50 is an indicator designed to help traders choose prudent, realistic, and dynamic leverage, adapted to the timeframe and volatility of the asset they are trading.

Based on rigorous statistical and practical observation, this indicator does not propose fixed rules, but rather provides a visual estimate of the maximum leverage a typical trade can tolerate without being liquidated, based on the current candle's movement range. At the same time, it automatically suggests a more conservative leverage (by default, half of the maximum) for more controlled risk management.

SwingTrade ADX Strategy v6This is a swing trading strategy that combines VWAP (Volume Weighted Average Price), ADX (Average Directional Index) for trend strength, and volume ratios to generate long/short entry and exit signals. It's designed for daily charts but can be adapted.

#### Key Features:

- **Entries**: Based on VWAP crossovers, rising/falling delta (price deviation from VWAP), ADX trend confirmation, and volume ratios.

- **Exits**: Dynamic exits when VWAP delta reverses after a peak.

- **Filters**: Optional toggles for VWAP signals, ADX, and volume. Backtest date range for custom periods.

- **Visuals**: VWAP line, signal shapes/labels, and an info panel showing key metrics (VWAP Delta %, ADX, Volume Ratio).

- **Alerts**: Built-in alerts for buy/sell entries and exits.

#### How to Use:

1. Apply to your chart (e.g., stocks, forex, crypto).

2. Adjust parameters in the settings (e.g., ADX threshold, volume period).

3. Enable/disable indicators as needed.

4. Backtest using the date filters and review equity curve.

**Disclaimer**: This is for educational purposes only. Past performance is not indicative of future results. Not financial advice—trade at your own risk. Backtest thoroughly and use with proper risk management.

Feedback welcome! If you find it useful, give it a like.

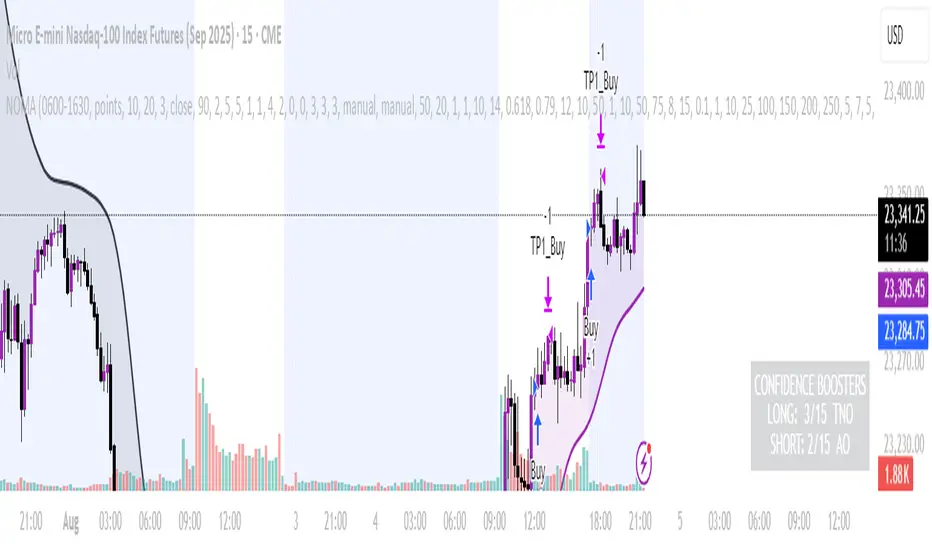

NOMANOMA Adaptive Confidence Strategy —

What is NOMA?

NOMA is a next-generation, confidence-weighted trading strategy that fuses modern trend logic, multi-factor market structure, and adaptive risk controls—delivering a systematic edge across futures, stocks, forex, and crypto markets. Designed for precision, adaptability, and hands-off automation, NOMA provides actionable trade signals and real-time alerts so you never miss a high-conviction opportunity.

Key Benefits & Why Use NOMA?

Trade With Confidence, Not Guesswork:

NOMA combines over 11 institutional-grade confirmations (market structure, order flow, volatility, liquidity, SMC/ICT concepts, and more) into a single “confidence score” engine. Every trade entry is filtered through customizable booster weights, so only the strongest opportunities trigger.

Built-In Alerts:

Get instant notifications on all entries, take-profits, trailing stop events, and exits. Connect alerts to your mobile, email, or webhook for seamless automation or just peace of mind.

Advanced Position Management:

Supports up to 5 separate take-profit levels with adjustable quantities, plus dynamic and stepwise trailing stops. Protects your gains and adapts exit logic to market movement, not just static targets.

Anti-Chop/No Trade Zones:

Eliminate low-probability, sideways market conditions using the “No Chop Zone” filter, so you only trade in meaningful, trending environments.

Full Market Session Control:

Restrict trades to custom sessions (e.g., New York hours) for added discipline and to avoid overnight risk.

— Ideal for day traders and prop-firm requirements.

Multi-Asset & Timeframe Support:

Whether you trade micro futures, stocks, forex, or crypto, NOMA adapts its TP/SL logic to ticks, pips, or points and works on any timeframe.

How NOMA Works (Feature Breakdown)

1. Adaptive Trend Engine

Uses a custom NOMA line that blends classic moving averages with dynamic momentum and a proprietary “Confidence Momentum Oscillator” overlay.

Visual trend overlay and color fill for easy chart reading.

2. Multi-Factor Confidence Scoring

Each trade is scored on up to 11 confidence “boosters,” including:

Market Manipulation & Accumulation (detects smart money traps and true range expansions)

Accumulation/Distribution (AD line)

ATR Volatility Rank (prioritizes trades when volatility is “just right”)

COG Cross (center of gravity reversal points)

Change of Character/Break of Structure (CHoCH/BOS logic, SMC/ICT style)

Order Blocks, Breakers, FVGs, Inducements, OTE (Optimal Trade Entry) Zones

You control the minimum score required for a trade to trigger, plus the weight of each factor (customize for your asset or style).

3. Smart Trade Management

Step Take-Profits:

Up to 5 profit targets, each with individual contract/quantity splits.

Step Trailing Stop:

Trail your stop with a ratcheting logic that tightens after each TP is hit, or use a fully dynamic ATR-based trail for volatile markets.

Kill-Switch:

Instant trailing stop logic closes all open contracts if price reverses sharply.

4. Session Filter & Cooldown Logic

Restricts trading to key sessions (e.g., NY open) to avoid low-liquidity or dead zones.

Cooldown bars prevent “overtrading” or rapid re-entries after an exit.

5. Chop Zone Filter

Optionally blocks trades during flat/choppy periods using a custom “NOMA spread” calculation.

When enabled, background color highlights no-trade periods for clarity.

6. Real-Time Alerts

Receive alerts for:

Trade entries (long & short, with confidence score)

Every take-profit target hit

Trailing stop exits or full position closes

Easy setup: Create alerts for all conditions and get notified instantly.

Customization & Inputs

TP/SL Modes: Choose between manual, ATR-multiplied, or hybrid take-profit and trailing logic.

Position Sizing: Fixed contracts/quantity per trade, with customizable splits for scaling out.

Session Settings: Restrict to any time window.

Confidence Engine: User-controlled weights and minimum score—tailor for your asset.

Risk & Volatility Filters: ATR length/multiplier, min/max range, and more.

How To Use

Add NOMA to your chart.

Customize your settings (session, TPs, confidence scores, etc.).

Set up TradingView alerts (“Any Alert() function call”) to receive notifications.

Monitor trade entries, profit targets, and stops directly on your chart or in your inbox.

Adjust confidence weights as you optimize for your favorite asset.

Pro Tips

Start with default settings—they are optimized for NQ micro futures, 15m timeframe.

Increase the minimum confidence score or weights for stricter filtering in volatile or low-liquidity markets.

Adjust your take-profit and trailing stop settings to match your trading style (scalping vs. swing).

Enable “No Chop Zone” during sideways conditions for cleaner signals.

Test in strategy mode before trading live to dial in your risk and settings.

Disclaimer

This script is for educational and research purposes only. No trading system guarantees future results.

Performance will vary by symbol, timeframe, and market regime—always test settings and use at your own risk. Not investment advice.

If alerts or strategy entries are not triggering as expected, try lowering the minimum confidence score or disabling certain boosters.

This will come with a user manual please do not hesitate to message me to gain access. TO THE MOON AND BEYOND

Kairos BarakahTrade with precision during high-probability windows using this advanced Pine Script indicator, designed specifically for Indian Standard Time (IST). The tool identifies key reversal opportunities within a user-defined trading session, combining time-based reference levels, sequence-validated signals, and multi-factor win probability analysis for confident decision-making.

Key Features

1. Time-Based Reference Levels

Automatically sets high/low reference levels at a customizable start time (default: 19:00 IST).

Active trading window with adjustable duration (default: 135 minutes).

Clear visual reference lines for easy tracking.

2. Intelligent Signal Generation

Initial Signals:

Buy (B): Triggered when price closes above the reference high.

Sell (S): Triggered when price closes below the reference low.

Reversal Signals (R):

Valid only after an initial signal, ensuring proper sequence.

Buy Reversal: Price closes above reference high (after a Sell signal).

Sell Reversal: Price closes below reference low (after a Buy signal).

3. Multi-Dimensional Win Probability

Body Strength: Measures candle conviction (body size / total range).

Volume Confirmation: Compares current volume to 20-period average.

Trend Alignment: Uses EMA crosses (9/21) and RSI (14) for momentum.

Composite Score: Weighted blend of all factors, color-coded for quick interpretation:

🟢 >70%: High-confidence signal.

🟠 40-69%: Moderate confidence.

🔴 <40%: Weak signal.

4. Professional Visualization

Clean labels (B/S/R) at signal points.

Real-time reference table showing levels, active signal, and probabilities.

Customizable alerts for all signal types.

Why Use This Indicator?

IST-Optimized: Tailored for Indian market hours.

Rules-Based Reversals: Avoids false signals with strict sequence checks.

Data-Driven Confidence: Win probability metrics reduce guesswork.

Flexible Setup: Adjust time windows and parameters to fit your strategy.

Institutional Sessions Overlay (Asia/London/NY)Institutional Sessions Overlay is a professional TradingView indicator that visually highlights the main trading sessions (Asia, London, and New York) directly on your chart.

Customizable: Easily adjust session start and end times (including minutes) for each market.

Timezone Alignment: Shift session boxes using the timezone offset parameter so sessions match your chart’s timezone exactly.

Clear Visuals: Colored boxes and optional labels display session opens and closes for fast institutional market structure reference.

Toggle Labels: Show or hide session open/close labels with a single click for a clean or detailed look.

Intuitive UI: User-friendly grouped settings for efficient configuration.

This tool is designed for day traders, institutional traders, and anyone who wants to instantly recognize global session timing and ranges for SMC, ICT, and other session-based strategies.

How to use:

Set your chart to your local timezone.

Use the "Session timezone offset" setting if session boxes do not match actual session opens on your chart.

Adjust the hours and minutes for each session as needed.

Enable or disable labels in the “Display” settings group.

Tip: Use the overlay to spot session highs and lows, volatility windows, and institutional liquidity sweeps.

KST Strategy [Skyrexio]Overview

KST Strategy leverages Know Sure Thing (KST) indicator in conjunction with the Williams Alligator and Moving average to obtain the high probability setups. KST is used for for having the high probability to enter in the direction of a current trend when momentum is rising, Alligator is used as a short term trend filter, while Moving average approximates the long term trend and allows trades only in its direction. Also strategy has the additional optional filter on Choppiness Index which does not allow trades if market is choppy, above the user-specified threshold. Strategy has the user specified take profit and stop-loss numbers, but multiplied by Average True Range (ATR) value on the moment when trade is open. The strategy opens only long trades.

Unique Features

ATR based stop-loss and take profit. Instead of fixed take profit and stop-loss percentage strategy utilizes user chosen numbers multiplied by ATR for its calculation.

Configurable Trading Periods. Users can tailor the strategy to specific market windows, adapting to different market conditions.

Optional Choppiness Index filter. Strategy allows to choose if it will use the filter trades with Choppiness Index and set up its threshold.

Methodology

The strategy opens long trade when the following price met the conditions:

Close price is above the Alligator's jaw line

Close price is above the filtering Moving average

KST line of Know Sure Thing indicator shall cross over its signal line (details in justification of methodology)

If the Choppiness Index filter is enabled its value shall be less than user defined threshold

When the long trade is executed algorithm defines the stop-loss level as the low minus user defined number, multiplied by ATR at the trade open candle. Also it defines take profit with close price plus user defined number, multiplied by ATR at the trade open candle. While trade is in progress, if high price on any candle above the calculated take profit level or low price is below the calculated stop loss level, trade is closed.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.5, number of ATRs to calculate stop-loss level)

ATR Take Profit (by default = 3.5, number of ATRs to calculate take profit level)

Filter MA Type (by default = Least Squares MA, type of moving average which is used for filter MA)

Filter MA Length (by default = 200, length for filter MA calculation)

Enable Choppiness Index Filter (by default = true, setting to choose the optional filtering using Choppiness index)

Choppiness Index Threshold (by default = 50, Choppiness Index threshold, its value shall be below it to allow trades execution)

Choppiness Index Length (by default = 14, length used in Choppiness index calculation)

KST ROC Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #2 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #3 (by default = 20, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #4 (by default = 30, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #2 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #3 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #4 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST Signal Line Length (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is KST, Williams Alligator, Moving Average, ATR and Choppiness Index.

The KST (Know Sure Thing) is a momentum oscillator developed by Martin Pring. It combines multiple Rate of Change (ROC) values, smoothed over different timeframes, to identify trend direction and momentum strength. First of all, what is ROC? ROC (Rate of Change) is a momentum indicator that measures the percentage change in price between the current price and the price a set number of periods ago.

ROC = 100 * (Current Price - Price N Periods Ago) / Price N Periods Ago

In our case N is the KST ROC Length inputs from settings, here we will calculate 4 different ROCs to obtain KST value:

KST = ROC1_smooth × 1 + ROC2_smooth × 2 + ROC3_smooth × 3 + ROC4_smooth × 4

ROC1 = ROC(close, KST ROC Length #1), smoothed by KST SMA Length #1,

ROC2 = ROC(close, KST ROC Length #2), smoothed by KST SMA Length #2,

ROC3 = ROC(close, KST ROC Length #3), smoothed by KST SMA Length #3,

ROC4 = ROC(close, KST ROC Length #4), smoothed by KST SMA Length #4

Also for this indicator the signal line is calculated:

Signal = SMA(KST, KST Signal Line Length)

When the KST line rises, it indicates increasing momentum and suggests that an upward trend may be developing. Conversely, when the KST line declines, it reflects weakening momentum and a potential downward trend. A crossover of the KST line above its signal line is considered a buy signal, while a crossover below the signal line is viewed as a sell signal. If the KST stays above zero, it indicates overall bullish momentum; if it remains below zero, it points to bearish momentum. The KST indicator smooths momentum across multiple timeframes, helping to reduce noise and provide clearer signals for medium- to long-term trends.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.