Stdev Breakout StrategyStdev Breakout Strategy

Description:

This script generates a long entry signal when the Standard Deviation crosses over the Simple Moving Average and the Close is greater than the Open, and/or generates a short entry signal when the Standard Deviation crosses under the Simple Moving Average and the Close is less than the Open.

Desvio Padrão (Volatilidade)

CV_VWAP_GMECoefficient of variance GME ‰

Gray area: Regional price variance of GME in per milles

Light gray thick line: NYSE:GME deviation from global mean

1. Select a chart 24-hour ticker like FX_IDC:USDEUR

2. Select a timescale (5 min, 15 min, ...)

3. Monitor the regional price variance

Exchanges included: NYSE, XETR, BMV, FWB, SWB, BITTREX, FTX

Currency conversion: Forex

Adapted from Detecting the great short squeeze on Volkswagen, Godfrey, K. (2016, February 18).

ATR Without OutliersIt is an ATR indicator which filters out outliers.

Outliers are values which are higher than the standard deviation of the true range.

It may be better than normal ATR for stop loss, because it does not keep large values after pump or dump.

It is very useful for high volatile markets like crypto markets.

Cheat Code BandsThese bands are a combination of Fibonacci multiples of standard deviations, combined with specific time-frame moving averages. They are meant to be used similar to a Fibonacci Retracement pull, but with more dynamic and real-time updates on them.

These bands print their next value at the opening mark of a candle, and so will not fake you out.

You can expect to use these bands as support & resistance lines in the market, trading between the 4 different sets (separated via color), and looking for a bounce in the opposite direction if the bands can hold the market.

We oftentimes see price continually fluctuate between the upper-most 3 bands, and the lower-most 3 bands, so looking for a trade in the opposite direction once these bands are being held can be a good idea.

The time frame of the standard deviations, and the moving averages, are different from each-other, and are Fibonacci based as well. Through hours of backtesting, these values seem to hold best, and catch the major pivots in the market nicely.

Use the link below to obtain access to this indicator.

CC - ATR BandsPlots ATR bands around candles at any HTF resolution you desire, taken in through the inputs. The white line represents the open of the HTF, the red and green the expected boundaries. You can use the risk tolerance slider up/down to adjust how risky you want to be with the ATR bands.

I am not responsible for outcomes using this method, indicator or anything else. Please do your own due diligence.

SuperTrendRange by DGTSuperTrendRange study attempts to determine the state of the market

• whether a well-established bull/bear trend is present

• whether the market is trading in a range

SuperTrendRange (STR) takes into account the volatility of the market - further details regarding volatility can be found in the description of “Volatility Bands by DGT” study

Due to its similarities to SupertTrend (ST) and Parabolic SAR (SAR), I will try to explain by stating differences between them

SuperTrendRange uses both the ATR (Average True Range) and STDEV (Standard Deviation) as part of its calculations - unlike ST and SAR where they use only ATR

Sensitivity of the indicator is adjusted using the multiplier setting of both ATR and STDEV

Additionally, unlike ST, the source of the basis of SuperTrendRange can be selected among the assets price value or its moving average

Source and Length are adjustable too

The SuperTrendRange, like Parabolic SAR indicator, appears on a chart as a series of dots, either above, below or unlike Parabolic SAR both above and below of the asset's price

A dot placed

- below the price when the market is trending upward

- above the price when it is trending downward

- both above and below when the price starts moving sideways – this is a feature that both SuperTrend and Parabolic SAR misses, where they are known to produce false signals and losing trades, whereas SuperTrendRange emphasis the zones of the ranges occurring and in most cases are considered no trade recommended zones. Please note that the range width may vary depending on how the market is volatile. It is up to the users to trade if it fits their trading strategies

Dots plotted above and below can be assumed as Support and Resistance levels

Example usages – with trading opportunities

Gold Monthly Chart

Bitcoin Daily Chart

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

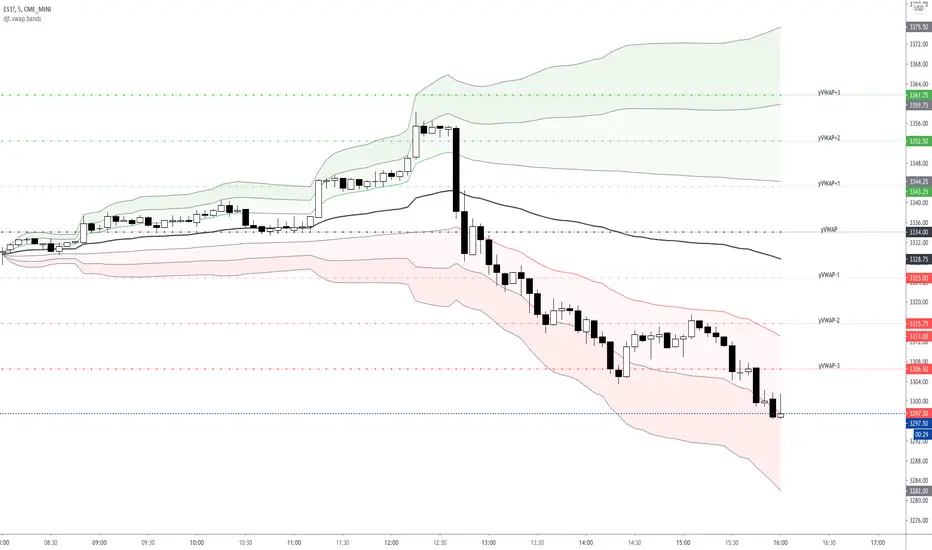

VWAP Standard Deviation Bands w/History & LabelsThis is my bread and butter when trading futures .

- 3 Standard Deviation Bands (Above and Below)

- Yesterday's VWAP and Band Levels

- Labels to help keep track of levels

- Ability to define resolution (I use Daily for my intraday scalping and Weekly/Monthly for context)

Z-Score 'Bollinger Bands'The following script is an application of the Z-Score (previous script).

Z-Scores can be used in place of standard deviation (sigma) in 'Bollinger Bands'.

The average of the sample (x-bar) over 21 days (N)

21 average trading days per month, fixed value

The average of the population (mu) over 63 days (n)

63 days per quarter, default is set to 63

Z-Score is calculated by formula in previous script, and the absolute value is taken of "Z".

Z-High = absolute value of Z + (x-bar).

Z-Low = absolute value of Z - (x-bar).

Will update with Z from mu and Z from avg (working on UX and visualization details).

Portfolio: alpha, beta, stdev, variance, mean, max drawdown...Portfolio Metrics **New**

'returns'

'log returns'

'geometric returns'

portfolio alpha

portfolio beta

portfolio,market correlation

portfolio standard deviation

portfolio variance

mean portfolio returns

maximum drawdown

maximum gain

Portfolio Metrics = α(Jensen's), β, CAPM(Ra), Sharpe, TreynorPortfolio Metrics...

Standard Deviation

Jensen's Alpha

Beta

Expected Return (CAPM, Ra)

Sharpe Ratio

Treynor Ratio

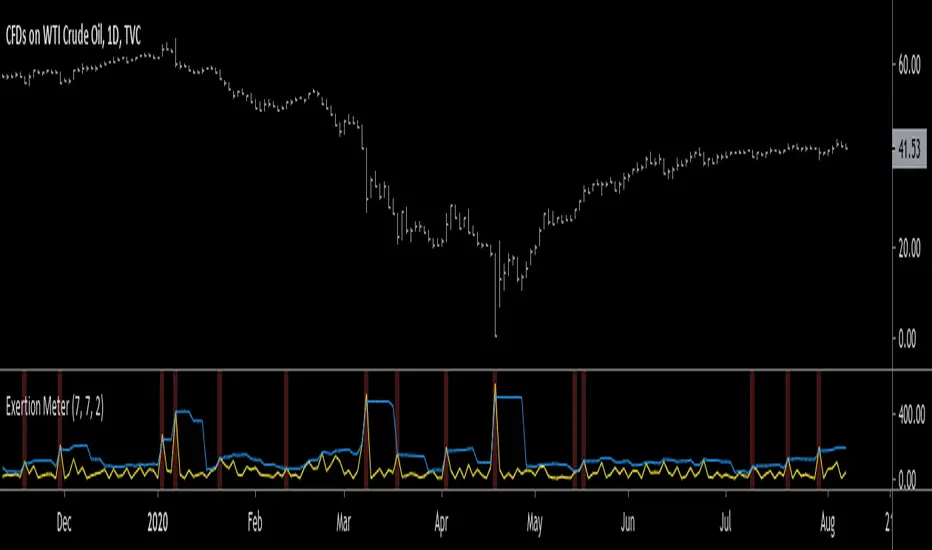

Exertion MeterHello traders, today I wanted to present you something special. I present you the Exertion Meter!

Created from scratch, this idea is based on a theory of mine called "Exertion".

Exertion occurs when price moves beyond the previous bar's range thus it has "exerted itself".

The idea is that when price moves a lot, it exerts a lot of energy which eventually leads to calmer motion, usually in the direction price has exerted itself.

Now, when price has exerted itself a lot in a particular direction, it's telling you that it will likely continue in that direction.

Once this happens, it will gradually calm down until price begins the cycle again, exerting itself in either the same or opposite direction.

This theory is similar to the theory of expansion & contraction phases.

This indicator attempts to show you where price has exerted itself by giving you a two lines cross signal.

The default settings are recommended, but experimentation is encouraged to fit your own personal system.

Both settings control the standard deviation line ( aka . Upper Bollinger Band ).

Enjoy, and hit the follow button to get easy access to all my indicators and to follow my latest publications!

Volatility based Standarde Deviation and Fib. Pivot PointsThis indicator plots Standard deviation levels and Fib. Pivot Points. I prefer to use only SD levels but Fib. levels also come handy in providing support and resistance.

How to use this indicator:

You have to manually enter instrument's Closing Price / Settlement Price and VIX closing price to draw each day's levels.

For NQ, I use VXN closign price and for ES or RTY, I use VIX closing price.

This indicator can be used on individual stocks and forex pairs.

DVI BandsA new idea of mine that I am presently experimenting on for my trades.

The DVI bands is based on my previously published DVI script:

The Directional Volume Index (DVI) is defined as follows:

DVI = VWMA (len1) - SMA (len2), where by default, len1==len2

The position of the DVI above/below the current price provides volume confirmation of the direction of the price trend.

The magnitude of the DVI above/below the current price provides the volume confirmation of the strength of the price trend.

The stdev band is derived from the DVI where:

The DVI piercing the Stdev boundary suggests a significant move in the corresponding direction.

Tightening of the DVI-Stdev bands can suggest the possible incoming of major move ahead.

The novel aspects and principles of this indicator and this source code are the property of © cybernetwork.

VAMA Volume Adjusted Moving Average BandsThis indicator is standard deviation bands using a live analysis adaptation of Richard Arms' Volume Adjusted Moving Average as their basis. VAMA utilizes a period length that is based on volume increments rather than time.

• SampleN - N volume bars used as sample to calculate average volume , 0 equals all bars.

• VAMA Source - Price used for volume weighted calculations.

• VAMA Length - Specified number of volume ratio buckets to be reached.

• VAMA VI Fct - Size of volume ratio buckets.

• VAMA Strict - Must meet desired volume requirements, even if number of bars has to exceed VAMA Length to do it.

• STDV Factor - Standard Deviation multiplier.

• STDV Length - Standard Deviation period.

• Brightness - Color opaqueness for the band fills.

Please see previous published example here for more details on VAMA's usage and inability to redraw the past on time based charts.

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

BBPCTIndicator tracks percentage distance between current price and its historical deviations, to produce premium and discount zones, suggest mean reversions,cooldowns and pullbacks

Script so far is traditional,simple, and straight forward ,tinkered it real quick on friend request after failing to find properly done and intuitive work on Bollinger Bands % in pine library

It might or might not be re-published as open source or study protected script , really depends on how future updates goes,how much work will be put in and how unique end result will be.

//Input Options in first release

Option to switch between small (6) variety of filters

(This time no non-traditional filters to avoid overwhelming and confusing users ,current list still yields good diversity for changing indicators behavior and pinpointing best suited filtering direction, in future current types will be swapped with more advanced ones and consolidated into three options tailored for different market conditions - trending,ranging, and balanced(?) - jack of all trades master of none.)

Option to toggle basic warnings about possible reversals,option for colored bars(candles) and/or arrow plots

OB/OS levels can be adjusted via inputs

Note: Current default compiling will lack traditional values as i ditched them and set to personal preference, set to 100 0 for traditional look

Sigma can be changed in inputs,length obviously can be changed too

Source can be changed

//Upcoming updates

Polishment- algorithmic change for cores logic

Attempt to build logic to differentiate pullbacks from reversals

More complex reversal recognition and their confirmations

Proper color coding

//Screencaps

Dont use comment section for asking access , got two warnings already from tradingview moderators because people flood the comment section and apparently its offence from my end to not provide directions for access.

If u are willing to test indicator and actually deliver feedback,ideas, params - Dm(direct message) and we add u ,expiration timer will be set in place to clean up in case no feedback is delivered.

P.S its not likely i will add more people to testing after people count reach 40-50 or script becomes older than week

StDev Based Trendlines - JDAs a second alternatively based trendline script this is the Standard Deviation vesrion.

This script draws trendlines from the pivot points in the price chart.

The angle of the trendlines is determined by (a percentage of) the Standard Deviation.

The angle follows the change in price, compared to the StDev at the moment where the pivot point is detected

The StDev percentage determines if the trendline follows the rate of change of the StDev or a fraction ( value < 100) or a multiple ( value > 100) of that

JD.

#NotTradingAdvice #DYOR

Disclaimer.

I AM NOT A FINANCIAL ADVISOR.

THESE IDEAS ARE NOT ADVICE AND ARE FOR EDUCATION PURPOSES ONLY.

ALWAYS DO YOUR OWN RESEARCH!

VWAP Standard Deviation Multi-Time FrameVWAP Standard Deviation Multi-Time Frame indicator shows VWAP , 1 standard deviation price from the VWAP, 2 standard deviation price from the VWAP and 3 standard deviation price from the VWAP

These lines are value regions and usually act as great support and resistance .

For best results allow the VWAP to develop in the beginning of the time frame, for almost about 20% of the total time period

For example, in a daily time frame, wait for about 4hrs for VWAP to develop before using the VWAP and Standard devaitions of VWAP as support and resistance zones

Change the values in timeframe input to use it for intraday, swing and long term trades.

Possible values are based on standard timeframe values 5,15,D,W,M, 12M etc

Trend Analysis IndicatorThe Trend Analysis Indicator was created by Adam White (Stocks & Commodities V. 10:8 (358-360)) and this is not to be confused with the Trend Analysis Index which was also created by Adam White. The stock is trending when it is above the signal and loses steam when it falls below the signal. Generally you should buy when it is above it's signal and sell when it goes below the signal.

Let me know if you would like me to write more scripts!

Variable Length Moving AverageThe Variable Length Moving Average was created by George R. Arrington Ph.D. (Stocks & Commodities V. 9:6 (219-223)) and I'm really loving this indicator. It is a great moving average that hugs the price very closely and it is fully adjustable to your needs. It detects signals extremely well and I have color coded the moving average line to make it very easy to interpret.

This is not to be confused with the Variable Moving Average created by Tushar S. Chande and as of now I haven't seen any other script for this moving average out there yet.

Please let me know if you would like me to write any other scripts for indicators you would like to see!

McMillan Volatility Bands w/ Buy & Sell Signals [optstrategist]BACKGROUND

McMillan Volatility Bands are an alternative approach to John Bollinger's "Bollinger Band" study and developed by world-renowned options trader and author Lawrence G. McMillan. Given his background in options trading, it was natural for Lawrence to approach any volatility-based study in the same manner options are priced --using Black-Scholes model. This model of pricing assumes a financial asset's volatility should be measured in percentage change rather than absolute value change.

OVERVIEW

The McMillan Volatility Bands indicator for TradingView will plot the 3 and 4-standard deviation bands around a 20-day moving average. This is how Larry has always used this system. The user can, however, change the standard deviation value as well as the moving average length to their preferred setting. This indicator can be used on any asset and on any timeframe.

Furthermore, the indicator will plot buy and sell signals based on a trading system used by Larry in his flagship newsletter publication The Daily Strategist. The system gives a signal when price closes outside the 4-sigma band and then closes back within the 3-sigma band. That 'signal bar' will be colored red or green for a sell or buy signal setup, respectively.

Finally, an arrow will be plotted on the chart where the system would actually enter the trade. This is determined when price trades a little beyond the extreme of the 'signal bar'. The level by which price has to go beyond the 'signal bar' is an input parameter and can be adjusted by the user. We've chosen the default value of 0.34. This means, the indicator will not give a buy or sell entry until the price moves: 1/3 x beyond the extreme signal bar. This is to prevent getting whipsawed by some setups that never really move in your favor. We've found it successfully removes the less-valuable trade setups.

PARAMETERS

ma_length => length of the moving average that the volatility bands work off of

outside_sigma => standard deviation of outer volatility band

inside_sigma => standard deviation of inner volatility band

entry_trigger_cushion => this refers to the percentage of the signal bar's range. The default value is 0.34. This means price will need to move 1/3 (~34%) of the signal bar's range beyond the high (for a buy) or low (for a sell) of the signal bar to trigger a buy/sell entry. This entry plots the arrow on the chart. We have found requiring this extra move in price eliminates many of the less-desirable signals at the expense of entering the better signals a little later.

WANT TO PURCHASE OR NEED MORE INFORMATION ON McMILLAN VOLATILITY BANDS?

Visit the link below to see purchasing options as well as screenshots of the indicator and how we trade it at McMillan Analysis Corp.

Corrected Moving AverageThis moving average was originally developed by professor Andreas Uhl in 2005 (The paper in German: www.buero-uhl.de). Here is the guy himself: wavelab.at

The strength of the CMA is that the current value of the time series must exceed the current volatility-dependent threshold, so that the filter increases or falls, avoiding false signals in weak phases.

The straight line of CMA can be used for a ranging market identification

[e2] Bitcoin Halving Key & AvwapThis indicator shows a Key Level Support & Resistance level and VWAP that reset on your choice of the Bitcoin's halving date.

Optional Key Calculation Mode:

- Start with first (2012) or second (2016) halving date.

- Start with first and reset on the second (Halving to halving mode)

- Start with every next halving simultaneously (Halving + halving mode)

Labels show the Market Capitalization, total minted Bitcoins and Bitcoin's close price on the halving's date.

A maximum of 5 bands calculated using a factor of the anchored VWAP's standard deviation can be displayed.

Note

- The script is designed for Bitcoin markets only.

- Estimated 3rd halving, script will be updated when next halving occurs.

[e2] EDS Key & AvwapThis indicator shows a Key Level Support & Resistance level and VWAP that resets on your choice of the stock's Earnings , Dividends or Splits release date.

A maximum of 8 bands calculated using a factor of the anchored VWAP's standard deviation can be displayed.

Note

The script is designed for stock-trading only.

Credits

Inspired by timwest , LazyBear 's Earnings S/R Levels and MichelT 's Earnings, Splits, Dividends scripts.