RSI Signals for Bot (15m close) — JSON FIX v3Bybit Bot RSi:

a lookback indicator that searches for potential short/long plays based on length parameters.

Statistics

VWAP Deviation Oscillator [BackQuant]VWAP Deviation Oscillator

Introduction

The VWAP Deviation Oscillator turns VWAP context into a clean, tradeable oscillator that works across assets and sessions. It adapts to your workflow with four VWAP regimes plus two rolling modes, and three deviation metrics: Percent, Absolute, and Z-Score. Colored zones, optional standard deviation rails, and flexible plot styles make it fast to read for both trend following and mean reversion.

What it does

This tool measures how far price is from a chosen VWAP and expresses that gap as an oscillator. You can view the deviation as raw price units, percent, or standardized Z-Score. The plot can be a histogram or a line with optional fills and sigma bands, so you can quickly spot polarity shifts, overbought and oversold conditions, and strength of extension.

VWAP modes track a session VWAP that resets (4H, Daily, Weekly) or a rolling VWAP that updates continuously over a fixed number of bars or days.

Deviation modes let you choose the lens: Percent, Absolute, or Z-Score. Each highlights different aspects of stretch and mean pressure.

Visual encoding uses a 10-zone color palette to grade the magnitude of deviation on both sides of zero.

Volatility guards compute mode-specific sigma so thresholds are stable even when volatility compresses.

Why this works

VWAP is a high signal anchor used by institutions to gauge fair participation. Deviations around VWAP cluster in regimes: mild oscillations within a band, decisive pushes that signal imbalance, and standardized extremes that often precede either continuation or snapback. Expressing that distance as a single time series adds clarity: bias is the oscillator’s sign, risk context is its magnitude, and regime is the way it behaves around sigma lines.

How to use it

Trend following

Favor the side of the zero line. Bullish when the oscillator is above zero and making higher swing highs. Bearish when below zero and making lower swing lows. Use +1 sigma and +2 sigma in your mode as strength tiers. Pullbacks that hold above zero in uptrends, or below zero in downtrends, are often continuation entries.

Mean reversion

Fade stretched readings when structure supports it. Look for tests of +2 sigma to +3 sigma that fail to progress and roll back toward zero, or the mirror on the downside. Z-Score mode is best when you want standardized gates across assets. Percent mode is intuitive for intraday scalps where a given percent stretch tends to mean revert.

Session playbook

Use Daily or Weekly VWAP for intraday or swing context. Rolling modes help when the asset lacks clean session boundaries or when you want a continuous anchor that adapts to liquidity shifts.

Key settings

VWAP computation

VWAP Mode = 4 Hours, Daily, Weekly, Rolling (Bars), Rolling (Days). Session modes reset the VWAP when a new session begins. Rolling modes compute VWAP over a fixed trailing window.

Rolling (Lookback: Bars) controls the trailing bar count when using Rolling (Bars).

Rolling (Lookback: Days) converts days to bars at runtime and uses that trailing span.

Use Close instead of HLC3 switches the price reference. HLC3 is smoother. Close makes the anchor track settlement more tightly.

Deviation measurement

Deviation Mode

Percent : 100 * (Price / VWAP - 1). Good for uniform scaling across instruments.

Absolute : Price - VWAP. Good when price units themselves matter.

Z-Score : Standardizes the absolute residual by its own mean and standard deviation over Z/Std Window . Ideal for cross-asset comparability and regime studies.

Z/Std Window sets the mean and standard deviation window for Z-Score mode.

Volatility controls

Percent Mode Volatility Lookback estimates sigma for percent deviations.

Absolute Mode Volatility Lookback estimates sigma for absolute deviations.

Minimum Sigma Guard (pct pts) prevents the percent sigma from collapsing to near zero in extremely quiet markets.

Visualization

Plot Type = Histogram or Line. Histogram emphasizes impulse and polarity changes. Line emphasizes trend waves and divergences.

Positive Color / Negative Color define the palette for line mode. Histogram uses a 10-bucket gradient automatically.

Show Standard Deviations plots symmetric rails at ±1, ±2, ±3 sigma in the current mode’s units.

Fill Line Oscillator and Fill Opacity add a soft bias band around zero for line mode.

Line Width affects both the oscillator and the sigma rails.

Reading the zones

The oscillator’s color and height map deviation to nine graded buckets on each side of zero, with deeper greens above and deeper reds below. In Percent and Absolute modes, those buckets are scaled by their mode-specific sigma. In Z-Score mode the bucket edges are fixed at 0.5, 1.0, 2.0, and 2.8.

0 to +1 sigma weak positive bias, usually rotational.

+1 to +2 sigma constructive impulse. Pullbacks that hold above zero often continue.

+2 to +3 sigma strong expansion. Watch for either trend continuation or exhaustion tells.

Beyond +3 sigma statistical extreme. Requires structure to avoid fading too soon.

Mirror logic applies on the negative side.

Suggested workflows

Trend continuation checklist

Pick a session VWAP that matches your timeframe, for example Daily for intraday or Weekly for position trades.

Wait for the oscillator to hold the correct side of zero and for a sequence of higher swing lows in the oscillator (uptrend) or lower swing highs (downtrend).

Buy pullbacks that stabilize between zero and +1 sigma in an uptrend. Sell rallies that stabilize between zero and -1 sigma in a downtrend.

Use the next sigma band or a prior price swing as your target reference.

Mean reversion checklist

Switch to Z-Score mode for standardized thresholds.

Identify tests of ±2 sigma to ±3 sigma that fail to extend while price meets support or resistance.

Enter on a polarity change through the prior histogram bar or a small hook in line mode.

Fade back to zero or to the opposite inner band, then reassess.

Notes on the three modes

Percent is easy to reason about when you care about proportional stretch. It is well suited to intraday and multi-asset dashboards.

Absolute tracks cash distance from VWAP. This is useful when instruments have tight ticks and you plan risk in price units.

Z-Score standardizes the residual and is best for quant studies, cross-asset comparisons, and threshold research that must be scale invariant.

What the alerts can tell you

Polarity changes at zero can mark the start or end of a leg.

Crosses of ±1 sigma identify overbought or oversold in the current mode’s units.

Zone changes signal an upgrade or downgrade in deviation strength.

Troubleshooting and edge cases

If your instrument has long flat periods, keep Minimum Sigma Guard above zero in Percent mode so the rails do not vanish.

In Rolling modes, very short windows will respond quickly but can whip around. Session modes smooth this by resetting at well known boundaries.

If Z-Score looks erratic, increase Z/Std Window to stabilize the estimate of mean and sigma for the residual.

Final thoughts

VWAP is the anchor. The deviation oscillator is the narrative. By separating bias, magnitude, and regime into a simple stream you can execute faster and review cleaner. Pick the VWAP mode that matches your horizon, choose the deviation lens that matches your risk framework, and let the color graded zones guide your decisions.

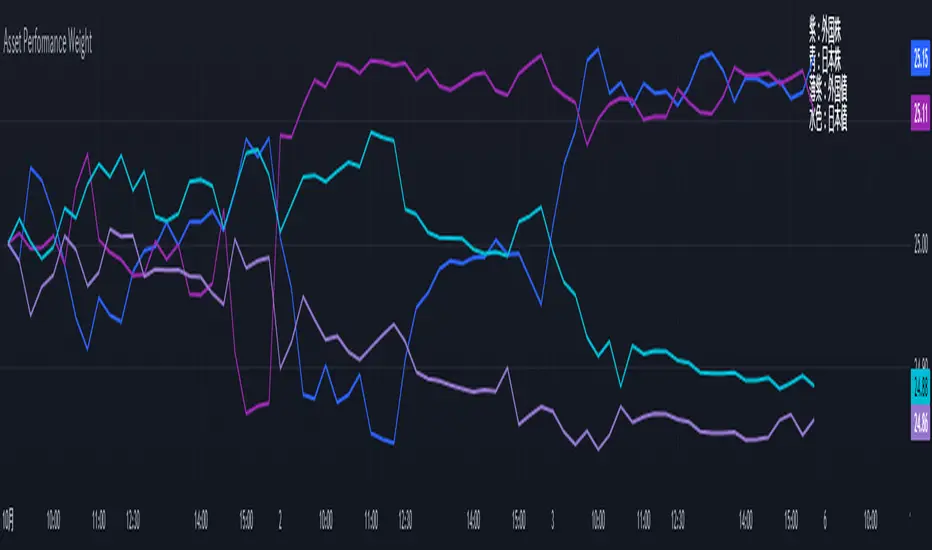

Performance-based Asset Weighting(MTF)**Performance-Based Asset Weighting (MTF/Symbol Free Setting)**

#### Overview

This indicator is a tool that visualizes the relative strength of performance (price change rate) as “weight (allocation ratio)” for **four user-defined stocks**.

By setting any specified past point in time as the baseline (where all symbols are equally weighted at 25%), it aims to provide an intuitive understanding of which symbols outperformed others and attracted capital, or underperformed and saw capital outflows.

**【Default Settings and Application Scenario: Pension Fund Rebalancing Analysis】**

The default settings reference the basic portfolio of Japan's Government Pension Investment Fund (GPIF), configuring four major asset classes: domestic equities, foreign equities, domestic bonds, and foreign bonds. It is known that when market fluctuations cause deviations from this equal-weighted ratio, rebalancing occurs to restore the original ratio (selling assets whose weight has increased and buying assets whose weight has decreased).

Analyzing using this default setting can serve as a reference point for considering **“whether rebalancing sales (or purchases) by pension funds and similar entities are likely to occur in the future.”**

**【Important: Usage Notes】**

The weights shown by this indicator are **theoretical reference values** calculated solely based on performance from the specified start date. Even if large investors conduct significant rebalancing (asset buying/selling) during the period, those transactions themselves are not reflected in this chart's calculations.

Therefore, please understand that the actual portfolio ratios may differ. **Use this solely as a rough guideline. **

#### Key Features

* **Freely configure the 4 assets for analysis:** You can freely set any 4 assets (stocks, indices, currencies, cryptocurrencies, etc.) you wish to compare via the settings screen.

* **Performance-based weight calculation:** Rather than simple price composition ratios, it calculates each asset's price change since the specified start date as a “performance index” and displays each asset's proportion of the total sum.

* **Freely set analysis start date:** You can set any desired starting point for analysis, such as “after the XX shock” or “after earnings announcements,” using the calendar.

* **Multi-Timeframe (MTF) Support:** Independently of the timeframe displayed on the chart, you can freely select the timeframe (e.g., 1-hour, 4-hour, daily) used by the indicator for calculations.

#### Calculation Principle

This indicator calculates weights in the following three steps:

1. **Obtaining the Base Price**

Obtain the closing price for each of the four stocks on the user-set “Start Date for Weight Calculation.” This becomes the **base price** for analysis.

2. **Calculating the Performance Index**

Divide the current price of each stock by the **base price** obtained in Step 1 to calculate the “Performance Index”.

`Performance Index = Current Price ÷ Base Date Price`

This quantifies how many times the current performance has increased compared to the base date performance, which is set to “1”.

3. **Calculating Weights**

Sum the “Performance Indexes” of the four stocks. Then, calculate the percentage contribution of each stock's Performance Index to this total sum and plot it on the chart.

`Weight (%) = (Individual Performance Index ÷ Total Performance Index of 4 Stocks) × 100`

Using this logic, on the analysis start date, all stocks' performance indices are set to “1”, so the weights start equally at 25%.

#### Usage

* **Application Example 1: Market Sentiment Analysis (Using Default Settings)**

Analyze using the default asset classes. By observing the relative strength between “Equities” and “Bonds”, you can assess whether the market is risk-on or risk-off.

* **Application Example 2: Sector/Theme Strength Analysis**

Configure settings for groups like “Top 4 semiconductor stocks” or “4 GAFAM stocks.” Setting the start date to the beginning of the year or earnings season allows you to instantly compare which stocks within the same sector are performing best.

* **Application Example 3: Cryptocurrency Power Map Analysis**

By setting major cryptocurrencies like “BTC, ETH, SOL, ADA,” you can analyze which currencies are attracting market capital.

**【About Legend Display】**

Due to Pine Script specification constraints, the legend on the chart will display fixed names: **“Stock 1” to “Stock 4”. **

Please note that the symbol you entered for “Symbol 1” in the settings corresponds to the “Symbol 1” line on the chart.

#### Settings

* **Symbol 1 to Symbol 4:** Set the four symbols you wish to analyze.

* **Timeframe for Calculation:** Select the timeframe the indicator references when calculating weights.

* **Start Date for Weight Calculation:** This serves as the base date for comparing performance.

#### Disclaimer

This script is solely a tool to assist with market analysis and does not recommend buying or selling any specific financial instruments. Please make all final investment decisions at your own discretion.

-------------------------------------------------------------------------------------------------------------------

**Performance-based Asset Weighting(MTF・シンボル自由設定)**

#### 概要

このインジケーターは、**ユーザーが自由に設定した4つの銘柄**について、パフォーマンス(騰落率)の相対的な強さを「ウェイト(構成比率)」として可視化するツールです。

指定した過去の任意の時点を基準(全銘柄が均等な25%)として、そこからどの銘柄のパフォーマンスが他の銘柄を上回り、資金が向かっているのか、あるいは下回っているのかを直感的に把握することを目的としています。

**【デフォルト設定と活用シナリオ:年金基金のリバランス考察】**

デフォルト設定では、日本の年金積立金管理運用独立行政法人(GPIF)の基本ポートフォリオを参考に、主要4資産クラス(国内株式, 外国株式, 国内債券, 外国債券)が設定されています。市場の変動によってこの均等な比率に乖離が生じると、元の比率に戻すためのリバランス(比率が増えた資産を売り、減った資産を買う)が行われることが知られています。

このデフォルト設定で分析することで、**「今後、年金基金などによるリバランスの売り(買い)が発生する可能性があるか」を考察するための、一つの目安として利用できます。**

**【重要:利用上の注意点】**

このインジケーターが示すウェイトは、あくまで指定した開始日からのパフォーマンスのみを基に算出した**理論上の参考値**です。実際に大口投資家などが途中で大規模なリバランス(資産の売買)を行ったとしても、その取引自体はこのチャートの計算には反映されません。

そのため、実際のポートフォリオ比率とは異なる可能性があることをご理解の上、**あくまで大まかな目安としてご活用ください。**

#### 主な特徴

* **分析対象の4銘柄を自由に設定可能:** 設定画面から、比較したい4つの銘柄(株式、指数、為替、仮想通貨など)を自由に設定できます。

* **パフォーマンス基準のウェイト計算:** 単純な価格の構成比ではなく、指定した開始日からの各銘柄の騰落を「パフォーマンス指数」として算出し、その合計に占める各銘柄の割合を表示します。

* **分析開始日の自由な設定:** 「〇〇ショック後」「決算発表後」など、分析したい任意の時点をカレンダーから設定できます。

* **マルチタイムフレーム(MTF)対応:** チャートに表示している時間足とは別に、インジケーターが計算に使う時間足(1時間足、4時間足、日足など)を自由に選択できます。

#### 計算の原理

このインジケーターは、以下の3ステップでウェイトを算出しています。

1. **基準価格の取得**

ユーザーが設定した「ウェイト計算の開始日」における、4つの各銘柄の終値を取得し、これを分析の**基準価格**とします。

2. **パフォーマンス指数の算出**

現在の各銘柄の価格を、ステップ1で取得した**基準価格**で割ることで、「パフォーマンス指数」を算出します。

`パフォーマンス指数 = 現在の価格 ÷ 基準日の価格`

これにより、基準日のパフォーマンスを「1」とした場合、現在のパフォーマンスが何倍になっているかが数値化されます。

3. **ウェイトの算出**

4つの銘柄の「パフォーマンス指数」の合計値を算出します。そして、合計値に占める各銘柄のパフォーマンス指数の割合(%)を計算し、チャートに描画します。

`ウェイト (%) = (個別のパフォーマンス指数 ÷ 4銘柄のパフォーマンス指数の合計) × 100`

このロジックにより、分析開始日には全銘柄のパフォーマンス指数が「1」となるため、ウェイトは均等に25%からスタートします。

#### 使用方法

* **応用例1:市場のセンチメント分析(デフォルト設定利用)**

デフォルト設定の資産クラスで分析し、「株式」と「債券」の力関係を見ることで、市場がリスクオンなのかリスクオフなのかを判断する材料になります。

* **応用例2:セクター・テーマ別の強弱分析**

設定画面で、例えば「半導体関連の主要4銘柄」や「GAFAMの4銘柄」などを設定します。開始日を年初や決算時期に設定することで、同セクター内でどの銘柄が最もパフォーマンスが良いかを一目で比較できます。

* **応用例3:仮想通貨の勢力図分析**

「BTC, ETH, SOL, ADA」など、主要な仮想通貨を設定することで、市場の資金がどの通貨に向かっているのかを分析できます。

**【凡例の表示について】**

Pine Scriptの仕様上の制約により、チャート上の凡例は**「銘柄1」〜「銘柄4」という固定名で表示されます。**

お手数ですが、設定画面でご自身が「銘柄1」に入力したシンボルが、チャート上の「銘柄1」のラインに対応する、という形でご覧ください。

#### 設定項目

* **銘柄1〜銘柄4:** 分析したい4つのシンボルをそれぞれ設定します。

* **計算に使う時間足:** インジケーターがウェイトを計算する際に参照する時間足を選択します。

* **ウェイト計算の開始日:** パフォーマンスを比較する上での基準日となります。

#### 免責事項

このスクリプトはあくまで市場分析を補助するためのツールであり、特定の金融商品の売買を推奨するものではありません。投資の最終的な判断は、ご自身の責任において行ってください。

ATT Numbers Header (Movable)For anybody that trades with ATT (Advanced Time Technique) And can't remember the numbers and want's to have them on their chart at all time with full customizability as well this indicator is for you.

MF_Average_Seasonal_MovementYou can chose a date range and see the average, min and max movement within that time.

n addition it shows how many longs or shorts would have won in that time frame.

To quikly look at the time periods in the past it markes the chosen dates each year with two horizontal lines.

You can utilize the election year cycle and look only at post election years for example

Anchored Session Volume Profile • Heatmap Profiles • Asia/EU/US Description

This indicator builds Anchored Session Volume Profiles for Asia, EU, and US sessions on intraday charts and renders them as right-docked line histograms (heatmap or classic style). Each session computes its own POC, VAH, VAL and optional Session High/Low lines. An optional per-price-bin Delta overlay estimates buy/sell pressure inside the profile rows for quick order-flow context.

What’s unique

Three independent session anchors (Asia/EU/US) with custom start/end times, bin size in ticks, and Value Area %.

Right-fixed live rendering or post-close persistence (draw levels only after the session closes).

Adaptive width: profile width scales with elapsed session length (anchor → now/end) within user limits.

Heatmap profile: row tint scales by relative volume; or Classic single-color with optional gradient.

Per-row Delta ticks (outside/inside, configurable direction) derived from bar delta and overlap with each price bin.

Clean POC/VAH/VAL line styling, optional ray extension, and Session High/Low rays per session.

How it works (technical)

Binning: Rows are built with a user-defined bin height in ticks. Arrays expand/shrink as price extends; the base is shifted when new lows appear to keep bins aligned.

Accumulation: For each bar within the active session window, traded volume is distributed to intersecting bins proportionally to the price overlap with that bin.

Value Area: POC is the highest-volume bin. VA is grown symmetrically around the POC until the selected coverage (VA%) is reached.

Delta per bin (optional): A bar-level delta proxy volume * (close − open) / range (clamped) is split into buy/sell and allocated to bins proportionally to the same overlap share, producing a per-row delta magnitude for rendering ticks.

Rendering modes:

Right fixed: refreshes each bar; lines/histogram are docked at the anchor X-position.

Draw Levels after Session Close: on close, only POC/VAH/VAL (and optional Session High/Low) are persisted.

No lookahead: All computations use confirmed bars; levels are deterministic on close.

How to use

Use the Asia/EU/US profiles to read participation hand-offs and session-driven rotations.

Trade off POC/VAH/VAL as acceptance/rejection references; confluence with session High/Low often marks responsive flows.

Employ Delta ticks per row to spot absorption, one-sided stacking, or fading participation inside the profile without leaving TradingView.

Prefer right-fixed during live trading and post-close when you want persistent session levels.

Key settings

General per session: Start/End (hh:mm), Bin size (ticks), Value Area %, toggle POC/VAH/VAL lines.

Rendering: Heatmap vs. Classic, orientation (Left/Right), gradient on/off, row thickness, right offset, adaptive width limits.

Delta (per price bin): global on/off, per-session on/off, tick width, max tick length (bars), outside/inside placement, direction (sign-based / always left / always right), colors.

Levels: POC/VAH/VAL styles (solid/dashed/dotted), widths, colors, extend right (ray).

Session High/Low: per-session on/off, style, width, colors, optional right-ray extension.

Notes & limitations

Designed for intraday data; accuracy depends on the feed’s volume granularity.

Large histories + small bins + delta ticks can be heavy; tune bin size, adaptive width, and delta max length for performance.

Timezone for anchors is set internally to Europe/Berlin.

Educational tool — not a signal generator.

Disclaimer

For educational and informational purposes only. Not financial advice.

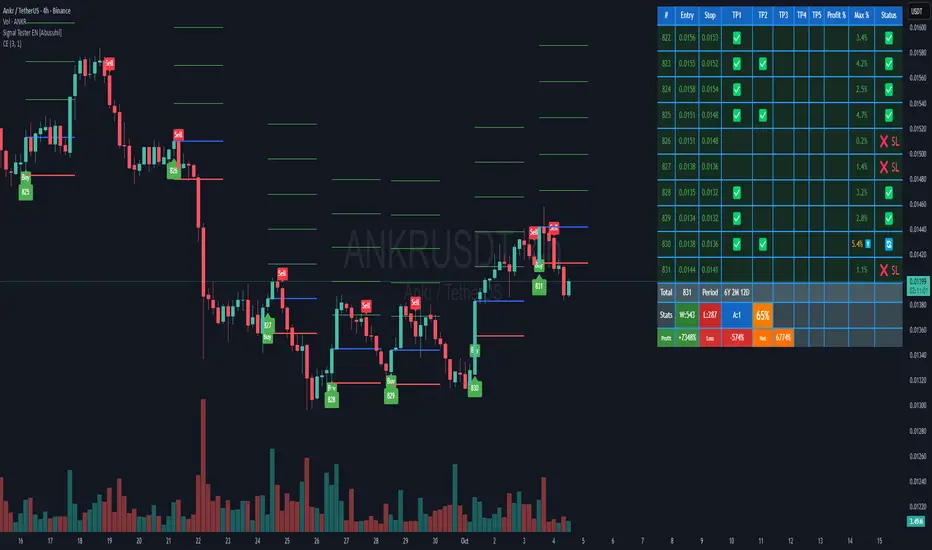

Signal Tester EN [Abusuhil]Signal Tester - Complete Description

Overview

Signal Tester is a comprehensive trading tool designed to backtest and analyze external trading signals with advanced risk management capabilities. The indicator provides seven different calculation methods for stop-loss and take-profit levels, along with detailed performance statistics and real-time tracking of active trades.

Important Disclaimer: This indicator is a tool for analysis and education purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Always conduct your own research and consider seeking advice from a qualified financial advisor before making trading decisions.

Key Features

7 Calculation Methods for customizable risk management

External Signal Integration via any oscillator or indicator

Real-time Trade Tracking with visual entry/exit points

Comprehensive Statistics Table showing win rate, profit/loss, and active trades

Date Filtering for focused backtesting periods

Custom Alerts for new buy signals

Multi-Target System with up to 5 take-profit levels

How to Use

Step 1: Connect External Signal

The indicator requires an external signal source to generate buy signals.

Add your preferred indicator to the chart (RSI, MACD, Stochastic, custom indicator, etc.)

In Signal Tester settings, locate "External Indicator" input

Click the input and select your indicator's plot line

Buy signals are generated when the external source crosses above zero

Example: If using RSI, connect the RSI line. A buy signal triggers when RSI crosses above the zero reference (if plotted as oscillator).

Step 2: Choose Your Calculation Method

Select one of seven methods under "Calculation Method":

1. Percentage %

The simplest method using fixed percentage values.

Settings:

Stop Loss %: Distance from entry to stop-loss (default: 2%)

Target 1-5 %: Distance from entry to each take-profit level

Example: Entry at $100

Stop Loss (2%): $98

Target 1 (2%): $102

Target 2 (4%): $104

Best For: Beginners, markets with consistent volatility

2. ATR Multiplier

Uses Average True Range for dynamic levels based on market volatility.

Settings:

ATR Period: Calculation period (default: 14)

Stop Multiplier: ATR multiplier for stop-loss (default: 1.5)

Target Multipliers: ATR multipliers for each take-profit

Example: Entry at $100, ATR = $2

Stop Loss (1.5x ATR): $100 - $3 = $97

Target 1 (2x ATR): $100 + $4 = $104

Best For: Volatile markets, adapting to changing conditions

3. Risk:Reward Ratio

Calculates targets based on risk-to-reward ratios.

Settings:

Stop Loss %: Initial risk percentage

Target Ratios: R:R ratio for each target (1:1.5, 1:2, 1:3, etc.)

Example: Entry at $100, Stop at $98 (2% risk = $2)

Target 1 (1:1.5): $100 + ($2 × 1.5) = $103

Target 2 (1:2): $100 + ($2 × 2) = $104

Target 3 (1:3): $100 + ($2 × 3) = $106

Best For: Traders focused on risk management and position sizing

4. Swing High/Low

Places stop-loss at recent swing low with targets as multiples of the risk.

Settings:

Swing Lookback Candles: Number of bars to find swing low (default: 5)

Stop Safety Distance %: Buffer below swing low

Target Multipliers: Risk multiples for each target

Example: Entry at $105, Swing Low at $100

Stop Loss: $100 - 0.1% = $99.90 (risk = $5.10)

Target 1 (1.5x): $105 + ($5.10 × 1.5) = $112.65

Best For: Swing traders, respecting market structure

5. Partial Take Profit

Sells portions of the position at each target level, moving stop to entry after first target.

Settings:

Stop Loss %: Initial stop distance

Target 1-5 %: Price levels for partial exits

Sell % at TP1-4: Percentage of position to close at each level

Example: 100% position, 50% sell at each target

TP1 hit: Sell 50%, remaining 50%, stop moves to entry

TP2 hit: Sell 25% (50% of remaining), remaining 25%

TP3 hit: Sell 12.5%, remaining 12.5%

Best For: Conservative traders, locking in profits gradually

6. Trailing Stop

Similar to Partial Take Profit but trails the stop-loss to each achieved target.

Settings:

Stop Loss %: Initial stop distance

Target 1-5 %: Price levels for trailing stops

Sell % at TP1-4: Percentage to close at each level

Example:

TP1 ($102) hit: Sell 50%, stop trails to $102

TP2 ($104) hit: Sell 25%, stop trails to $104

Price retraces to $104: Exit with locked profits

Best For: Trend followers, maximizing profit in strong moves

7. Smart Exit

Advanced method that moves stop to entry after first target, then exits based on technical conditions.

Settings:

Stop Loss %: Initial stop distance

First Target %: When hit, stop moves to breakeven

Exit Method: Choose from 8 exit strategies

Exit Methods:

Close < EMA 21: Exits when price closes below 21-period EMA

Close < MA 20: Exits when price closes below 20-period Moving Average

Supertrend Flip: Exits when Supertrend indicator flips bearish

ATR Trailing Stop: Dynamic trailing stop based on ATR

MACD Crossover: Exits on MACD bearish crossover

RSI < 50: Exits when RSI drops below specified level

Parabolic SAR Flip: Exits when SAR flips above price

Bollinger Bands: Exits when price closes below middle or lower band

Best For: Advanced traders, letting winners run with protection

Date Filtering

Control which trades are included in backtesting.

Filter Types:

Specific Date: Only trades after selected date

Number of Weeks: Last X weeks (default: 12)

Number of Months: Last X months (default: 3)

How to Enable:

Check "Enable Date Filter"

Select filter type

Set the date or number of weeks/months

Use Case: Test strategy performance in recent market conditions or specific periods

Understanding the Statistics Table

The table displays the last 10 trades plus comprehensive statistics:

Trade Columns:

#: Trade number

Entry: Entry price

Stop: Current stop-loss level

TP1-TP5: Checkmarks (✅) when targets are hit

Profit %: Realized profit for the trade

Max %: Maximum unrealized profit reached (⬆️ indicates active trade)

Status:

🔄 Active trade

✅ Closed winner

❌ SL - Stopped out

Summary Row:

Total: Number of trades executed

Period: Duration of trading period (Years, Months, Days)

Statistics Row:

W: Number of winning trades

L: Number of losing trades

A: Number of active (open) trades

Win Rate %: (Wins / Total Trades) × 100

Performance Row:

Profit: Total profit from all winning trades

Loss: Total loss from all losing trades

Net: Net profit/loss (Profit - Loss)

Visual Elements

When a buy signal triggers, the indicator draws:

Blue Line: Entry price

Red Line: Stop-loss level

Green Lines: Take-profit levels (up to 5)

Green Label: Trade number below the entry bar

Green Triangle: Buy signal marker

Alerts

The indicator includes customizable alerts for new buy signals.

Setting Up Alerts:

Click the "⏰" icon in TradingView

Select "Signal Tester "

Choose condition: "Buy"

Configure notification preferences (popup, email, webhook)

Click "Create"

Alert Message Format:

🚀 New Buy Signal!

Price:

Trade #:

Best Practices

Backtest First: Test each calculation method on historical data before live trading

Match Timeframe: Use the indicator on the timeframe you plan to trade

Combine with Analysis: Use alongside support/resistance, trend analysis, and other tools

Risk Management: Never risk more than 1-2% of capital per trade

Review Statistics: Regularly check win rate and profit/loss metrics

Adjust Settings: Optimize parameters based on the asset's volatility and your risk tolerance

Limitations

Requires external signal source (does not generate signals independently)

Backtesting assumes perfect entry/exit execution (real trading includes slippage)

Past performance does not guarantee future results

Should be used as one component of a complete trading strategy

Version Information

Version: 1.0

Pine Script Version: v5

Type: Overlay Indicator

Author: Abusuhil

Support and Updates

This indicator is provided as-is for educational and analytical purposes. Users are responsible for their own trading decisions and should thoroughly test any strategy before implementing it with real capital.

Risk Warning: Trading financial instruments carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk appetite. Only trade with money you can afford to lose.

Square Root Price Calculator By ABPinescript to Calculate Square root of Price usefull for Gann Lover

% Change & Range (With SMA)- Calculates the % range and change for each candle

- uses SMA over "n" bars to show the average % range and the average % change for green days and red days

- optional standard deviation line (k bands)

Tchwella Stocks Custom WatermarkThis Pine Script v5 indicator adds a customizable watermark to TradingView charts, displaying key stock information while allowing for flexible positioning and formatting.

📌 Features & Functionality:

✅ Custom Positioning:

• Fixed to the top-left corner.

• Adjustable spacing ensures the text is properly aligned.

✅ Displayed Information (Configurable):

• Company Name & Market Cap (Optional: Shows dynamically calculated market cap)

• Stock Ticker & Timeframe

• Industry & Sector

✅ Customization Options:

• Font Size: Huge, Large, Normal, Small

• Text Color & Transparency: Adjustable

• Proper Left Alignment for a clean, structured display

• Vertical Offset Tweaks to move text down for better visibility

✅ Optimized Table Layout:

• Uses table.new() for persistent placement.

• Added an empty row to fine-tune positioning, ensuring the watermark doesn’t overlap key chart areas.

🔧 Use Case:

Designed for traders who want a clear, customizable stock watermark to enhance their charting experience without obstructing price action.

Feb 1

Release Notes

Updated version: now you can decide your location for the watermark

Micha Stocks Custom Watermark (MSWM) – TradingView Script

This Pine Script v5 indicator adds a customizable watermark to TradingView charts, displaying key stock information while allowing for flexible positioning and formatting.

📌 Features & Functionality:

✅ Custom Positioning:

• Fixed to the top-left corner.

• Adjustable spacing ensures the text is properly aligned.

✅ Displayed Information (Configurable):

• Company Name & Market Cap (Optional: Shows dynamically calculated market cap)

• Stock Ticker & Timeframe

• Industry & Sector

✅ Customization Options:

• Font Size: Huge, Large, Normal, Small

• Text Color & Transparency: Adjustable

• Proper Left Alignment for a clean, structured display

• Vertical Offset Tweaks to move text down for better visibility

✅ Optimized Table Layout:

• Uses table.new() for persistent placement.

• Added an empty row to fine-tune positioning, ensuring the watermark doesn’t overlap key chart areas.

🔧 Use Case:

Designed for traders who want a clear, customizable stock watermark to enhance their charting experience without obstructing price action.

Feb 7

Release Notes

Micha Stocks Custom Watermark – Updated Version 🚀

This updated Micha Stocks Custom Watermark script enhances your TradingView experience by adding an ATR-based volatility signal alongside the existing customizable stock watermark.

🆕 New Features & Improvements:

✅ ATR (14-Day) with Dynamic Volatility Indicator

• Displays the ATR value and its percentage relative to price.

• Includes a color-coded volatility signal:

• 🔴 High Volatility (Above user-defined Red Threshold)

• 🟡 Moderate Volatility (Between Red & Yellow Thresholds)

• 🟢 Low Volatility (Below user-defined Yellow Threshold)

✅ Fully Customizable ATR Thresholds

• Users can set their own ATR % levels for Red, Yellow, and Green signals.

✅ Improved Watermark Customization

• Users can still adjust the position, size, and color of the watermark.

• Includes Company Name, Ticker, Market Cap, Industry, and Sector.

• ATR can be turned on/off in settings for flexibility.

🔧 How to Use:

1️⃣ Go to Indicator Settings → Enable or Disable ATR Display

2️⃣ Adjust ATR % Thresholds to fit your volatility preference

3️⃣ Customize Text Position, Color, and Size to match your chart setup

This update makes it easier to quickly assess market volatility while keeping a clean and professional chart layout.

💡 Why Use This Indicator?

• Effortlessly track key stock info without cluttering your chart.

• Quickly identify volatile conditions using ATR percentage signals.

• Adjust settings on the fly to match your trading strategy.

📢 Update Now & Enjoy a Smarter Charting Experience!

Round Number Analyzer v3Round Number Analyzer v3 is an indicator designed to analyze how price interacts with round number levels (levels spaced at fixed intervals in points or pips).

The indicator does not generate entry/exit signals, but provides detailed statistics to better understand market dynamics around these key levels.

✨ Key Features

Cross Counting: detects every time the price crosses a round number level (up = Long, down = Short).

Continuations & Reversals: classifies each cross as:

Continuation: the move continues in the same direction as the previous sequence.

Reversal: the move changes direction compared to the previous sequence.

Sequence Classification (L1…L5+): each level is labelled based on its position within the consecutive cross sequence:

L1 = first level of the sequence,

L2 = second consecutive,

…

L5+ = fifth or higher.

Comprehensive Stats Table (top right corner):

Total crosses (Long, Short, Totals).

Total continuations + breakdown by L1…L5+.

Total reversals + breakdown by L1…L5+.

Percentages calculated against the proper denominator, displayed directly inside the cells next to the absolute values.

Date range of analysis (user-defined).

Customizable Step: Works in both points and pips, making the indicator suitable for indices and forex.

⚙️ Main Inputs

Start date / End date → sets the analysis period.

Step mode → Points or Pips.

Step value → distance between round levels.

Pip size → pip size (default = 0.0001, typical for forex).

📈 How to Interpret

A high continuation percentage after L1–L2 suggests the market tends to extend multiple times beyond the first breakout levels.

Higher reversal percentages at advanced levels (L4–L5+) may signal trend exhaustion.

The analysis helps estimate the probability of continuation or reversal depending on how many consecutive levels have already been crossed.

🔎 Practical Applications

Support for breakout or mean-reversion strategies.

Comparative analysis across different markets (e.g. indices vs forex) or different time periods.

📝 Notes

The indicator is timeframe-robust, as it accounts for multiple steps within the same candle, ensuring results do not depend on the selected timeframe (except for TradingView’s historical data limits).

It does not provide automatic trading signals, but serves as a quantitative analysis tool to refine your strategies.

---

Round Number Analyzer v3 è un indicatore pensato per analizzare come il prezzo interagisce con i livelli di round number (livelli a distanza fissa in punti o pips).

L’indicatore non genera segnali di ingresso/uscita, ma fornisce statistiche dettagliate utili per comprendere la dinamica del mercato attorno a questi livelli.

✨ Funzionalità principali

Conteggio dei Cross: rileva ogni volta che il prezzo attraversa un livello round (verso l’alto = Long, verso il basso = Short).

Continuations & Reversals: classifica ogni attraversamento come:

Continuation: il movimento prosegue nella stessa direzione della sequenza precedente.

Reversal: il movimento inverte la direzione rispetto alla sequenza precedente.

Classificazione per sequenza (L1…L5+): ogni livello è etichettato in base alla sua posizione nella sequenza di cross consecutivi:

L1 = primo livello della sequenza,

L2 = secondo consecutivo,

…

L5+ = quinto o superiore.

Statistiche complete in tabella (in alto a destra):

Cross totali (Long, Short, Totals).

Continuations totali + breakdown per L1…L5+.

Reversals totali + breakdown per L1…L5+.

Percentuali calcolate sul denominatore corretto, mostrate direttamente dentro le celle accanto ai valori assoluti.

Date range di analisi (impostabile dall’utente).

Step personalizzabile: puoi lavorare sia in punti che in pips, così l’indicatore è adatto sia per indici che per forex.

⚙️ Input principali

Start date / End date → imposta l’intervallo temporale di analisi.

Step mode → punti o pips.

Step value → ampiezza tra i livelli round.

Pip size → dimensione del pip (default = 0.0001, tipico per il forex).

📈 Come interpretarlo

Una percentuale di continuation molto alta dopo L1–L2 indica che il mercato tende a proseguire più volte oltre i primi livelli di breakout.

Percentuali di reversal più elevate nei livelli avanzati (L4–L5+) possono suggerire esaurimento della spinta.

L’analisi permette di stimare la probabilità che un movimento in corso continui o si inverta in base a quanti livelli sono già stati attraversati consecutivamente.

🔎 Applicazioni pratiche

Supporto per strategie di breakout o mean reversion.

Analisi comparativa tra mercati (es. indici vs forex) o tra periodi temporali diversi.

📝 Note

L’indicatore è timeframe-robust: il conteggio tiene conto di multipli step dentro la stessa candela, così i risultati non dipendono dal timeframe scelto (salvo i limiti di caricamento storico di TradingView).

Non fornisce segnali operativi automatici, ma è un tool di analisi quantitativa per affinare le proprie strategie.

Regular Trading Hours Opening Range Gap (RTH ORG)### Regular Trading Hours (RTH) Gap Indicator with Quartile Levels

**Overview**

Discover overnight gaps in index futures like ES, YM, and NQ, or stocks like SPY, with this enhanced Pine Script v6 indicator. It visualizes the critical gap between the previous RTH close (4:15 PM ET for futures, 4:00 PM for SPY) and the next RTH open (9:30 AM ET), helping traders spot potential price sensitivity formed during after-hours trading.

**Key Features**

- **Standard Gap Boxes**: Semi-transparent boxes highlight the gap range, with optional text labels showing day-of-week and "RTH" identifier.

- **Midpoint Line**: A customizable dashed line at the 50% level, with price labels for quick reference.

- **New: Quartile Lines (25% & 75%)**: Dotted lines (default width 1) mark the quarter and three-quarter points within the gap, ideal for finer intraday analysis. Toggle on/off, adjust style/color/width, and add labels.

- **High-Low Gap Variant**: Optional boxes and midlines for gaps between the prior close's high/low and the open's high/low—perfect for wick-based overlaps on lower timeframes (5-min or below recommended).

- **RTH Close Lines**: Extend previous close levels with dotted lines and price tags.

- **Customization Galore**: Extend elements right, limit historical displays (default: 3 gaps), no-plot sessions (e.g., avoid weekends), and time offsets for non-US indices.

**How to Use**

Apply to 15-min or lower charts for best results. Toggle "extend right" for ongoing levels. SPY auto-adjusts for its 4 PM close.

Tested on major indices—enhance your gap trading strategy today! Questions? Drop a comment.

Thanks to twingall for supplying the original code.

Thanks to The Inner Circle Trader (ICT) for the logical and systematic application.

Brownian Motion Probabilistic Forecasting (Time Adaptive)Probabilistic Price Forecast Indicator

Overview

The Probabilistic Price Forecast is an advanced technical analysis tool designed for the TradingView platform. Instead of predicting a single future price, this indicator uses a Monte Carlo simulation to model thousands of potential future price paths, generating a cone of possibilities and calculating the probability of specific outcomes.

This allows traders to move beyond simple price targets and ask more sophisticated questions, such as: "What is the probability that this stock will increase by 5% over the next 24 hours?"

Core Concept: Geometric Brownian Motion

The indicator's forecasting model is built on the principles of Geometric Brownian Motion (GBM) , a widely accepted mathematical model for describing the random movements of financial asset prices. The core idea is that the next price step is a function of the asset's historical trend (drift), its volatility, and a random "shock."

The formula used to project each price step in the simulation is:

next_price = current_price * exp( (μ - (σ²/2))Δt + σZ√(Δt) )

Where:

μ (mu) represents the drift , which is the average historical return.

σ (sigma) represents the volatility , measured by the standard deviation of historical returns.

Z is a random variable from a standard normal distribution, representing the random "shock" or new information affecting the price.

Δt (delta t) is the time step for each projection.

How It Works

The indicator performs a comprehensive analysis on the most recent bar of the chart:

**Historical Analysis**: It first analyzes a user-defined historical period (e.g., the last 240 hours of price data) to calculate the asset's historical drift (μ) and volatility (σ) from its logarithmic returns.

**Monte Carlo Simulation**: It then runs thousands of simulations (e.g., 2000) of future price paths over a specified forecast period (e.g., the next 24 hours). Each path is unique due to the random shock (Z) applied at every step.

**Probability Distribution**: After all simulations are complete, it collects the final price of each path and sorts them to build a probability distribution of potential outcomes.

**Visualization and Signaling**: Finally, it visualizes this distribution on the chart and generates signals based on the user's criteria.

Key Features & Configuration

The indicator is highly configurable, allowing you to tailor its analysis to your specific needs.

Time-Adaptive Periods

The lookback and forecast periods are defined in hours , not bars. The script automatically converts these hour-based inputs into the correct number of bars based on the chart's current timeframe, ensuring the analysis remains consistent across different chart resolutions.

Forecast Quartiles

You can visualize the forecast as a "cone of probability" on the chart. The indicator draws lines and a shaded area representing the price levels for different quartiles (percentiles) of the simulation results. By default, this shows the range between the 25th and 95th percentiles.

Independent Bullish and Bearish Signals

The indicator allows you to set independent criteria for bullish and bearish signals, providing greater flexibility. You can configure:

A bullish signal for an X% confidence of a Y% price increase.

A bearish signal for a W% confidence of a Z% price decrease.

For example, you can set it to alert you for a 90% chance of a 2% drop, while simultaneously looking for a 60% chance of a 10% rally.

How to Interpret the Indicator

The Forecast Cone : The blue shaded area on the chart represents the probable range of future prices. The width of the cone indicates the expected volatility; a wider cone means higher uncertainty. The price labels on the right side of the cone show the calculated percentile levels at the end of the forecast period.

Green Signal Label : A green "UP signal" label appears when the probability of the price increasing by your target percentage exceeds your defined confidence level.

Red Signal Label : A red "DOWN signal" label appears when the probability of the price decreasing by your target percentage exceeds your confidence level.

This tool provides a statistical edge for understanding future possibilities but should be used in conjunction with other analysis techniques.

Aggregated Scores Oscillator [Alpha Extract]A sophisticated risk-adjusted performance measurement system that combines Omega Ratio and Sortino Ratio methodologies to create a comprehensive market assessment oscillator. Utilizing advanced statistical band calculations with expanding and rolling window analysis, this indicator delivers institutional-grade overbought/oversold detection based on risk-adjusted returns rather than traditional price movements. The system's dual-ratio aggregation approach provides superior signal accuracy by incorporating both upside potential and downside risk metrics with dynamic threshold adaptation for varying market conditions.

🔶 Advanced Statistical Framework

Implements dual statistical methodologies using expanding and rolling window calculations to create adaptive threshold bands that evolve with market conditions. The system calculates cumulative statistics alongside rolling averages to provide both historical context and current market regime sensitivity with configurable window parameters for optimal performance across timeframes.

🔶 Dual Ratio Integration System

Combines Omega Ratio analysis measuring excess returns versus deficit returns with Sortino Ratio calculations focusing on downside deviation for comprehensive risk-adjusted performance assessment. The system applies configurable smoothing to both ratios before aggregation, ensuring stable signal generation while maintaining sensitivity to regime changes.

// Omega Ratio Calculation

Excess_Return = sum((Daily_Return > Target_Return ? Daily_Return - Target_Return : 0), Period)

Deficit_Return = sum((Daily_Return < Target_Return ? Target_Return - Daily_Return : 0), Period)

Omega_Ratio = Deficit_Return ≠ 0 ? (Excess_Return / Deficit_Return) : na

// Sortino Ratio Framework

Downside_Deviation = sqrt(sum((Daily_Return < Target_Return ? (Daily_Return - Target_Return)² : 0), Period) / Period)

Sortino_Ratio = (Mean_Return / Downside_Deviation) * sqrt(Annualization_Factor)

// Aggregated Score

Aggregated_Score = SMA(Omega_Ratio, Omega_SMA) + SMA(Sortino_Ratio, Sortino_SMA)

🔶 Dynamic Band Calculation Engine

Features sophisticated threshold determination using both expanding historical statistics and rolling window analysis to create adaptive overbought/oversold levels. The system incorporates configurable multipliers and sensitivity adjustments to optimize signal timing across varying market volatility conditions with automatic band convergence logic.

🔶 Signal Generation Framework

Generates overbought conditions when aggregated score exceeds adjusted upper threshold and oversold conditions below lower threshold, with neutral zone identification for range-bound markets. The system provides clear binary signal states with background zone highlighting and dynamic oscillator coloring for intuitive market condition assessment.

🔶 Enhanced Visual Architecture

Provides modern dark theme visualization with neon color scheme, dynamic oscillator line coloring based on signal states, and gradient band fills for comprehensive market condition visualization. The system includes zero-line reference, statistical band plots, and background zone highlighting with configurable transparency levels.

snapshot

🔶 Risk-Adjusted Performance Analysis

Utilizes target return parameters for customizable risk assessment baselines, enabling traders to evaluate performance relative to specific return objectives. The system's focus on downside deviation through Sortino analysis provides superior risk-adjusted signals compared to traditional volatility-based oscillators that treat upside and downside movements equally.

🔶 Multi-Timeframe Adaptability

Features configurable calculation periods and rolling windows to optimize performance across various timeframes from intraday to long-term analysis. The system's statistical foundation ensures consistent signal quality regardless of timeframe selection while maintaining sensitivity to market regime changes through adaptive band calculations.

🔶 Performance Optimization Framework

Implements efficient statistical calculations with optimized variable management and configurable smoothing parameters to balance responsiveness with signal stability. The system includes automatic band adjustment mechanisms and rolling window management for consistent performance across extended analysis periods.

This indicator delivers sophisticated risk-adjusted market analysis by combining proven statistical ratios in a unified oscillator framework. Unlike traditional overbought/oversold indicators that rely solely on price movements, the ASO incorporates risk-adjusted performance metrics to identify genuine market extremes based on return quality rather than price volatility alone. The system's adaptive statistical bands and dual-ratio methodology provide institutional-grade signal accuracy suitable for systematic trading approaches across cryptocurrency, forex, and equity markets with comprehensive visual feedback and configurable risk parameters for optimal strategy integration.

Volume Based Sampling [BackQuant]Volume Based Sampling

What this does

This indicator converts the usual time-based stream of candles into an event-based stream of “synthetic” bars that are created only when enough trading activity has occurred . You choose the activity definition:

Volume bars : create a new synthetic bar whenever the cumulative number of shares/contracts traded reaches a threshold.

Dollar bars : create a new synthetic bar whenever the cumulative traded dollar value (price × volume) reaches a threshold.

The script then keeps an internal ledger of these synthetic opens, highs, lows, closes, and volumes, and can display them as candles, plot a moving average calculated over the synthetic closes, mark each time a new sample is formed, and optionally overlay the native time-bars for comparison.

Why event-based sampling matters

Markets do not release information on a clock: activity clusters during news, opens/closes, and liquidity shocks. Event-based bars normalize for that heteroskedastic arrival of information: during active periods you get more bars (finer resolution); during quiet periods you get fewer bars (coarser resolution). Research shows this can reduce microstructure pathologies and produce series that are closer to i.i.d. and more suitable for statistical modeling and ML. In particular:

Volume and dollar bars are a common event-time alternative to time bars in quantitative research and are discussed extensively in Advances in Financial Machine Learning (AFML). These bars aim to homogenize information flow by sampling on traded size or value rather than elapsed seconds.

The Volume Clock perspective models market activity in “volume time,” showing that many intraday phenomena (volatility, liquidity shocks) are better explained when time is measured by traded volume instead of seconds.

Related market microstructure work on flow toxicity and liquidity highlights that the risk dealers face is tied to information intensity of order flow, again arguing for activity-based clocks.

How the indicator works (plain English)

Choose your bucket type

Volume : accumulate volume until it meets a threshold.

Dollar Bars : accumulate close × volume until it meets a dollar threshold.

Pick the threshold rule

Dynamic threshold : by default, the script computes a rolling statistic (mean or median) of recent activity to set the next bucket size. This adapts bar size to changing conditions (e.g., busier sessions produce more frequent synthetic bars).

Fixed threshold : optionally override with a constant target (e.g., exactly 100,000 contracts per synthetic bar, or $5,000,000 per dollar bar).

Build the synthetic bar

While a bucket fills, the script tracks:

o_s: first price of the bucket (synthetic open)

h_s: running maximum price (synthetic high)

l_s: running minimum price (synthetic low)

c_s: last price seen (synthetic close)

v_s: cumulative native volume inside the bucket

d_samples: number of native bars consumed to complete the bucket (a proxy for “how fast” the threshold filled)

Emit a new sample

Once the bucket meets/exceeds the threshold, a new synthetic bar is finalized and stored. If overflow occurs (e.g., a single native bar pushes you past the threshold by a lot), the code will emit multiple synthetic samples to account for the extra activity.

Maintain a rolling history efficiently

A ring buffer can overwrite the oldest samples when you hit your Max Stored Samples cap, keeping memory usage stable.

Compute synthetic-space statistics

The script computes an SMA over the last N synthetic closes and basic descriptors like average bars per synthetic sample, mean and standard deviation of synthetic returns, and more. These are all in event time , not clock time.

Inputs and options you will actually use

Data Settings

Sampling Method : Volume or Dollar Bars.

Rolling Lookback : window used to estimate the dynamic threshold from recent activity.

Filter : Mean or Median for the dynamic threshold. Median is more robust to spikes.

Use Fixed? / Fixed Threshold : override dynamic sizing with a constant target.

Max Stored Samples : cap on synthetic history to keep performance snappy.

Use Ring Buffer : turn on to recycle storage when at capacity.

Indicator Settings

SMA over last N samples : moving average in synthetic space . Because its index is sample count, not minutes, it adapts naturally: more updates in busy regimes, fewer in quiet regimes.

Visuals

Show Synthetic Bars : plot the synthetic OHLC candles.

Candle Color Mode :

Green/Red: directional close vs open

Volume Intensity: opacity scales with synthetic size

Neutral: single color

Adaptive: graded by how large the bucket was relative to threshold

Mark new samples : drop a small marker whenever a new synthetic bar prints.

Comparison & Research

Show Time Bars : overlay the native time-based candles to visually compare how the two sampling schemes differ.

How to read it, step by step

Turn on “Synthetic Bars” and optionally overlay “Time Bars.” You will see that during high-activity bursts, synthetic bars print much faster than time bars.

Watch the synthetic SMA . Crosses in synthetic space can be more meaningful because each update represents a roughly comparable amount of traded information.

Use the “Avg Bars per Sample” in the info table as a regime signal. Falling average bars per sample means activity is clustering, often coincident with higher realized volatility.

Try Dollar Bars when price varies a lot but share count does not; they normalize by dollar risk taken in each sample. Volume Bars are ideal when share count is a better proxy for information flow in your instrument.

Quant finance background and citations

Event time vs. clock time : Easley, López de Prado, and O’Hara advocate measuring intraday phenomena on a volume clock to better align sampling with information arrival. This framing helps explain volatility bursts and liquidity droughts and motivates volume-based bars.

Flow toxicity and dealer risk : The same authors show how adverse selection risk changes with the intensity and informativeness of order flow, further supporting activity-based clocks for modeling and risk management.

AFML framework : In Advances in Financial Machine Learning , event-driven bars such as volume, dollar, and imbalance bars are presented as superior sampling units for many ML tasks, yielding more stationary features and fewer microstructure distortions than fixed time bars. ( Alpaca )

Practical use cases

1) Regime-aware moving averages

The synthetic SMA in event time is not fooled by quiet periods: if nothing of consequence trades, it barely updates. This can make trend filters less sensitive to calendar drift and more sensitive to true participation.

2) Breakout logic on “equal-information” samples

The script exposes simple alerts such as breakout above/below the synthetic SMA . Because each bar approximates a constant amount of activity, breakouts are conditioned on comparable informational mass, not arbitrary time buckets.

3) Volatility-adaptive backtests

If you use synthetic bars as your base data stream, most signal rules become self-paced : entry and exit opportunities accelerate in fast markets and slow down in quiet regimes, which often improves the realism of slippage and fill modeling in research pipelines (pair this indicator with strategy code downstream).

4) Regime diagnostics

Avg Bars per Sample trending down: activity is dense; expect larger realized ranges.

Return StdDev (synthetic) rising: noise or trend acceleration in event time; re-tune risk.

Interpreting the info panel

Method : your sampling choice and current threshold.

Total Samples : how many synthetic bars have been formed.

Current Vol/Dollar : how much of the next bucket is already filled.

Bars in Bucket : native bars consumed so far in the current bucket.

Avg Bars/Sample : lower means higher trading intensity.

Avg Return / Return StdDev : return stats computed over synthetic closes .

Research directions you can build from here

Imbalance and run bars

Extend beyond pure volume or dollar thresholds to imbalance bars that trigger on directional order flow imbalance (e.g., buy volume minus sell volume), as discussed in the AFML ecosystem. These often further homogenize distributional properties used in ML. alpaca.markets

Volume-time indicators

Re-compute classical indicators (RSI, MACD, Bollinger) on the synthetic stream. The premise is that signals are updated by traded information , not seconds, which may stabilize indicator behavior in heteroskedastic regimes.

Liquidity and toxicity overlays

Combine synthetic bars with proxies of flow toxicity to anticipate spread widening or volatility clustering. For instance, tag synthetic bars that surpass multiples of the threshold and test whether subsequent realized volatility is elevated.

Dollar-risk parity sampling for portfolios

Use dollar bars to align samples across assets by notional risk, enabling cleaner cross-asset features and comparability in multi-asset models (e.g., correlation studies, regime clustering). AFML discusses the benefits of event-driven sampling for cross-sectional ML feature engineering.

Microstructure feature set

Compute duration in native bars per synthetic sample , range per sample , and volume multiple of threshold as inputs to state classifiers or regime HMMs . These features are inherently activity-aware and often predictive of short-horizon volatility and trend persistence per the event-time literature. ( Alpaca )

Tips for clean usage

Start with dynamic thresholds using Median over a sensible lookback to avoid outlier distortion, then move to Fixed thresholds when you know your instrument’s typical activity scale.

Compare time bars vs synthetic bars side by side to develop intuition for how your market “breathes” in activity time.

Keep Max Stored Samples reasonable for performance; the ring buffer avoids memory creep while preserving a rolling window of research-grade data.

Total Points Range by exp3rtsThis indicator measures and displays the true intraday movement of a market by approximating tick-level activity using 1-second data aggregation. Instead of only looking at net candle movement, it sums every price change during a session, giving traders a more accurate picture of market effort and volatility.

Total Points Moved (TPM) – Captures the full distance traveled by price, not just the net gain/loss.

Bullish vs. Bearish Movement – Separates upward and downward moves so you can see who dominated the session.

Custom Sessions – Define your own session start/end times and time zone for precise tracking.

End-of-Session Summary – Automatically plots a label at session completion with totals for TPM, bullish, and bearish movement.

Visual Session Highlighting – Background shading makes it easy to see when the chosen session is active.

This tool is useful for:

Understanding the true effort vs. result of price movement

Comparing volatility across sessions

Identifying whether bulls or bears contributed more to market swings

Supporting order flow and tick-based trading strategies

Portfolio Simulator & BacktesterMulti-asset portfolio simulator with different metrics and ratios, DCA modeling, and rebalancing strategies.

Core Features

Portfolio Construction

Up to 5 assets with customizable weights (must total 100%)

Support for any tradable symbol: stocks, ETFs, crypto, indices, commodities

Real-time validation of allocations

Dollar Cost Averaging

Monthly or Quarterly contributions

Applies to both portfolio and benchmark for fair comparison

Model real-world investing behavior

Rebalancing

Four strategies: None, Monthly, Quarterly, Yearly

Automatic rebalancing to target weights

Transaction cost modeling (customizable fee %)

Key Metrics Table

CAGR: Annualized compound return (S&P 500 avg: ~10%)

Alpha: Excess return vs. benchmark (positive = outperformance)

Sharpe Ratio: Return per unit of risk (>1.0 is good, >2.0 excellent)

Sortino Ratio: Like Sharpe but only penalizes downside (better metric)

Calmar Ratio: CAGR / Max Drawdown (>1.0 good, >2.0 excellent)

Max Drawdown: Largest peak-to-trough decline

Win Rate: % of positive days (doesn't indicate profitability)

Visualization

Dual-chart comparison - Portfolio vs. Benchmark

Dollar or percentage view toggle

Customizable colors and line width

Two tables: Statistics + Asset Allocation

Adjustable table position and text size

🚀 Quick Start Guide

Enter 1-5 ticker symbols (e.g., SPY, QQQ, TLT, GLD, BTCUSD)

Make sure percentage weights total 100%

Choose date range (ensure chart shows full period - zoom out!)

Configure DCA and rebalancing (optional)

Select benchmark (default: SPX)

Analyze results in statistics table

💡 Pro Tips

Chart data matters: Load SPY or your longest-history asset as main chart

If you select an asset that was not available for the selected period, the chart will not show up! E.g. BTCUSD data: Only available from ~2017 onwards.

Transaction fees: 0.1% default (adjust to match your broker)

⚠️ Important Notes

Requires visible chart data (zoom out to show full date range)

Limited by each asset's historical data availability

Transaction fees and costs are modeled, but taxes/slippage are not

Past performance ≠ future results

Use for research and education only, not financial advice

Let me know if you have any suggestions to improve this simulator.

ITM SMA Crossover Strategy (Positioned Labels)This strategy tries to find the crossover of 10 sma in relation to 200 sma. Golden cross over is when 10 sma crosses above 200 sma. Death cross over is opposite.

As per the author - Heather Cullen ITM strategy - 'Buy' when the Golden cross is seen and 'exit' when Death cross is seen.

Lot Calculator EditableEdit the value of point to use it. Honnestly idk what can I say so don't read it.It's just an indicator to calculate your lot. Editable on the TP, SL and more

Time Range by exp3rtsTime Window highlights a custom time range directly on your chart, helping you focus on specific market sessions or trading hours.

Key Features:

Highlights a custom time range with a shaded background

Fully adjustable start and end time (hour & minute)

Supports multiple time zones (e.g., GMT, UTC, Europe/Berlin)

Optional market color shading inside the window (bull/bear neutral tone)

Use Cases:

Mark London Open, New York Session, or any session overlap

Focus on high-probability trading hours

Visualize your backtesting timeframe or algo activity window

Track premarket or after-hours activity for futures or indices

Customization:

Set the beginning and end time in your local or exchange time zone

Choose your timezone string (e.g., "GMT", "Etc/UTC", "America/New_York")

Automatically colors candles in the time window for easy visibility

Total Points Moved by exp3rtsThis lightweight utility tracks the total intraday range of price movement, giving you real-time insight into market activity.

It calculates:

🟩 Bullish Points – Total range from bullish candles (close > open)

🟥 Bearish Points – Total range from bearish candles (close < open)

🔁 Total Points Moved (TPM) – Sum of all high–low ranges for the day

Values are pulled from the 1-second chart for high precision and displayed in a compact tag in the top-right corner.