Open Interest RSI [BackQuant]Open Interest RSI

A multi-venue open interest oscillator that aggregates OI across major derivatives exchanges, converts it to coin or USD terms, and runs an RSI-style engine on that aggregated OI so you can track positioning pressure, crowding, and mean reversion in leverage flows, not just in price.

What this is

This tool is an RSI built on top of aggregated open interest instead of price. It pulls futures OI from several major exchanges, converts it into a unified unit (COIN or USD), sums it into a single synthetic OI candle, then applies RSI and smoothing to that combined series.

You can then render that Open Interest RSI in different visual modes:

Clean line or colored line for classic oscillator-style reads.

Column-style oscillator for impulse and compression views.

Flag mode that fills between OI RSI and its EMA for trend/mean reversion blends. See:

Heatmap mode that paints the panel based on OI RSI extremes, ideal for scanning. See:

On top of that it includes:

Aggregated OI source selection (Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit).

Choice of OI units (COIN or USD).

Reference lines and OB/OS zones.

Extreme highlighting for either trend or mean reversion.

A vertical OI RSI meter that acts as a quick strength gauge.

Aggregated open interest source

Under the hood, the indicator builds a synthetic open interest candle by:

Looping over a list of supported exchanges: Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit.

Looping over multiple contract suffixes (such as USDT.P, USD.P, USDC.P, USD.PM) to capture different contract types on each venue.

Requesting OI candles from each venue + contract combination for the same underlying symbol.

Converting each OI stream into a common unit: In COIN mode, everything is normalized into coin-denominated OI. In USD mode, coin OI is multiplied by price to approximate notional OI.

Summing up open, high, low and close of OI across venues into a single aggregated OI candle.

If no valid OI is available for the current symbol across all sources, the script throws a clear runtime error so you know you are on an unsupported market.

This gives you a single, exchange-agnostic open interest curve instead of being tied to one venue. That aggregated OI is then passed into the RSI logic.

How the OI RSI is calculated

The RSI side is straightforward, but it is applied to the aggregated OI close:

Compute a base RSI of aggregated OI using the Calculation Period .

Apply a simple moving average of length Smoothing Period (SMA) to reduce noise in the raw OI RSI.

Optionally apply an EMA on top of the smoothed OI RSI as a moving average signal line.

Key parameters:

Calculation Period – base RSI length for OI.

Smoothing Period (SMA) – extra smoothing on the RSI value.

EMA Period – EMA length on the smoothed OI RSI.

The result is:

oi_rsi – raw RSI of aggregated OI.

oi_rsi_s – SMA-smoothed OI RSI.

ma – EMA of the smoothed OI RSI.

Thresholds and extremes

You control three core thresholds:

Mid Point – central reference level, typically 50.

Extreme Upper Threshold – high-level OI RSI edge (for example 80).

Extreme Lower Threshold – low-level OI RSI edge (for example 20).

These thresholds are used for:

Reference lines or OB/OS zone fills.

Heatmap gradient bounds.

Background highlighting of extremes.

The Extreme Highlighting mode controls how extremes are interpreted:

None – do nothing special in extreme regions.

Mean-Rev – background turns red on high OI RSI and green on low OI RSI, framing extremes as contrarian zones.

Trend – background turns green on high OI RSI and red on low OI RSI, framing extremes as participation zones aligned with the prevailing move.

Reference lines and OB/OS zones

You can choose:

None – clean plotting without guides.

Basic Reference Lines – mid, upper and lower thresholds as simple gray horizontals.

OB/OS Levels – filled zones between:

Upper OB: from the upper threshold to 100, colored with the short/overbought color.

Lower OS: from 0 to the lower threshold, colored with the long/oversold color.

These guides help visually anchor the OI RSI within "normal" versus "extreme" regions.

Plotting modes

The Plotting Type input controls how OI RSI is drawn. All modes share the same underlying OI and RSI logic, but emphasise different aspects of the signal.

1) Line mode

This is the classic oscillator representation:

Plots the smoothed OI RSI as a simple line using RSI Line Color and RSI Line Width .

Optionally plots the EMA overlay on the same panel.

Works well when you want standard RSI-style signals on leverage flows: crosses of the midline, divergences versus price, and so on.

2) Colored Line mode

In this mode:

The OI RSI is plotted as a line, but its color is dynamic.

If the smoothed OI RSI is above the mid point, it uses the Long/OB Color .

If it is below the mid point, it uses the Short/OS Color .

This creates an instant visual regime switch between "bullish positioning pressure" and "bearish positioning pressure", while retaining the feel of a traditional RSI line.

3) Oscillator mode

Oscillator mode renders OI RSI as vertical columns around the mid level:

The smoothed OI RSI is plotted as columns using plot.style_columns .

The histogram base is fixed at 50, so bars extend above and below the mid line.

Bar color is dynamic, using long or short colors depending on which side of the mid point the value sits.

This representation makes impulse and compression in OI flows more obvious. It is especially useful when you want to focus on how quickly OI RSI is expanding or contracting around its neutral level. See:

4) Flag mode

Flag mode turns OI RSI and its EMA into a two-line band with a filled area between them:

The smoothed OI RSI and its EMA are both plotted.

A fill is drawn between them.

The fill color flips between the long color and the short color depending on whether OI RSI is above or below its EMA.

Black outlines are added to both lines to make the band clear against any background.

This creates a "flag" style region where:

Green fills show OI RSI leading its EMA, suggesting positive positioning momentum.

Red fills show OI RSI trailing below its EMA, suggesting negative positioning momentum.

Crossovers of the two lines can be read as shifts in OI momentum regime.

Flag mode is useful if you want a more structural view that combines both the level and slope behaviour of OI RSI. See:

5) Heatmap mode

Heatmap mode recasts OI RSI as a single-row gradient instead of a line:

A single row at level 1 is plotted using column style.

The color is pulled from a gradient between the lower and upper thresholds: Near the lower threshold it approaches the short/oversold color and near the upper threshold it approaches the long/overbought color.

The EMA overlay and reference lines are disabled in this mode to keep the panel clean.

This is a very compact way to track OI RSI state at a glance, especially when stacking it alongside other indicators. See:

OI RSI vertical meter

Beyond the main plot, the script can draw a small "thermometer" table showing the current OI RSI position from 0 to 100:

The meter is a two-column table with a configurable number of rows.

Row colors form an inverted gradient: red at the top (100) and green at the bottom (0).

The script clamps OI RSI between 0 and 100 and maps it to a row index.

An arrow marker "▶" is drawn next to the row corresponding to the current OI RSI value.

0 and 100 labels are printed at the ends of the scale for orientation.

You control:

Show OI RSI Meter – turn the meter on or off.

OI RSI Blocks – number of vertical blocks (granularity).

OI RSI Meter Position – panel anchor (top/bottom, left/center/right).

The meter is particularly helpful if you keep the main plot in a small panel but still want an intuitive strength gauge.

How to read it as a market pressure gauge

Because this is an RSI built on aggregated open interest, its extremes and regimes speak to positioning pressure rather than price alone:

High OI RSI (near or above the upper threshold) indicates that open interest has been increasing aggressively relative to its recent history. This often coincides with crowded leverage and a buildup of directional pressure.

Low OI RSI (near or below the lower threshold) indicates aggressive de-leveraging or closing of positions, often associated with flushes, forced unwinds or post-liquidation clean-ups.

Values around the mid point indicate more balanced positioning flows.

You can combine this with price action:

Price up with rising OI RSI suggests fresh leverage joining the move, a more persistent trend.

Price up with falling OI RSI suggests shorts covering or longs taking profit, more fragile upside.

Price down with rising OI RSI suggests aggressive new shorts or levered selling.

Price down with falling OI RSI suggests de-leveraging and potential exhaustion of the move.

Trading applications

Trend confirmation on leverage flows

Use OI RSI to confirm or question a price trend:

In an uptrend, rising OI RSI with values above the mid point indicates supportive leverage flows.

In an uptrend, repeated failures to lift OI RSI above mid point or persistent weakness suggest less committed participation.

In a downtrend, strong OI RSI on the downside points to aggressive shorting.

Mean reversion in positioning

Use thresholds and the Mean-Rev highlight mode:

When OI RSI spends extended time above the upper threshold, the crowd is extended on one side. That can set up squeeze risk in the opposite direction.

When OI RSI has been pinned low, it suggests heavy de-leveraging. Once price stabilises, a re-risking phase is often not far away.

Background colours in Mean-Rev mode help visually identify these periods.

Regime mapping with plotting modes

Different plotting modes give different perspectives:

Heatmap mode for dashboard-style use where you just need to know "hot", "neutral" or "cold" on OI flows at a glance.

Oscillator mode for short term impulses and compression reads around the mid line. See:

Flag mode for blending level and trend of OI RSI into a single banded visual. See:

Settings overview

RSI group

Plotting Type – None, Line, Colored Line, Oscillator, Flag, Heatmap.

Calculation Period – base RSI length for OI.

Smoothing Period (SMA) – smoothing on RSI.

Moving Average group

Show EMA – toggle EMA overlay (not used in heatmap).

EMA Period – length of EMA on OI RSI.

EMA Color – colour of EMA line.

Thresholds group

Mid Point – central reference.

Extreme Upper Threshold and Extreme Lower Threshold – OB/OS thresholds.

Select Reference Lines – none, basic lines or OB/OS zone fills.

Extreme Highlighting – None, Mean-Rev, Trend.

Extra Plotting and UI

RSI Line Color and RSI Line Width .

Long/OB Color and Short/OS Color .

Show OI RSI Meter , OI RSI Blocks , OI RSI Meter Position .

Open Interest Source

OI Units – COIN or USD.

Exchange toggles: Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit.

Notes

This is a positioning and pressure tool, not a complete system. It:

Models aggregated futures open interest across multiple centralized exchanges.

Transforms that OI into an RSI-style oscillator for better comparability across regimes.

Offers several visual modes to match different workflows, from detailed analysis to compact dashboards.

Use it to understand how leverage and positioning are evolving behind the price, to gauge when the crowd is stretched, and to decide whether to lean with or against that pressure. Attach it to your existing signals, not in place of them.

Also, please check out @NoveltyTrade for the OI Aggregation logic & pulling the data source!

Here is the original script:

Análise Fundamentalista

BuLLzEyE_MNQ FVG/IFVG SystemFVG Boxes

These are the main trading zones. The indicator automatically detects Fair Value Gaps and draws boxes on your chart:

• GREEN boxes = Bullish FVG (potential buy zone)

• RED boxes = Bearish FVG (potential sell zone)

• YELLOW boxes = IFVG (Inverse FVG - filled gaps that now act as support/resistance)

• GRAY boxes = Mitigated FVG (gap has been filled)

• WHITE dashed line = 50% level (optimal entry point within the FVG)

Session Boxes

Session boxes show you the high/low range of each major trading session. This helps identify where liquidity sits:

• PURPLE = Asia Session (6:00 PM - 3:00 AM ET)

• BLUE = London Session (3:00 AM - 12:00 PM ET)

• ORANGE = New York Session (9:30 AM - 4:00 PM ET)

• TEAL = Sydney Session (5:00 PM - 2:00 AM ET)

• LIME GREEN = Kill Zone / London-NY Overlap (8:00 AM - 11:00 AM ET) - BEST TRADING TIME

Entry Signals

• GREEN triangle pointing UP = Long entry signal at a Bullish FVG (not 100% reliable)

• RED triangle pointing DOWN = Short entry signal at a Bearish FVG (not 100% reliable)

Liquidity Sweeps

• RED X with 'SWEEP' = Previous Day High (PDH) was swept

• GREEN X with 'SWEEP' = Previous Day Low (PDL) was swept

• Dotted lines = PDH (red) and PDL (green) levels

Information Tables

HTF Bias Table (Top Right): Shows whether the higher timeframe (default 15m) is bullish or bearish, the number of active FVGs, and whether you're in the trading session.

Risk Calculator Table (Bottom Right): Shows your risk amount and calculates how many contracts you can trade for different stop loss sizes (5pt, 10pt, 15pt).

How It Works

What is a Fair Value Gap?

A Fair Value Gap (FVG) is a 3-candle pattern where aggressive buying or selling creates a price void. Specifically, it's when the wick of the first candle doesn't overlap with the wick of the third candle, leaving a gap in between. Price tends to return to these gaps to 'rebalance' before continuing in the original direction.

What is an Inverse FVG?

When an FVG gets filled (price returns and closes through the gap), it becomes an Inverse FVG (IFVG). These zones flip their polarity - a filled Bullish FVG becomes resistance, and a filled Bearish FVG becomes support. The indicator automatically converts mitigated FVGs to yellow IFVG boxes.

The 50% Entry Level

The dashed white line in each FVG represents the 50% level (also called Consequent Encroachment). This is considered the optimal entry point - it's the middle of the imbalance where price is most likely to react.

Suggested Trading Strategy

1. Check HTF Bias (top right table) - only trade in that direction

2. Wait for a liquidity sweep (SWEEP label appears)

3. Look for an FVG to form AFTER the sweep

4. Enter when price returns to the 50% level (dashed line)

5. Place stop loss below/above the FVG (add 2 ticks buffer)

6. Take profit at 1:2 or 1:3 risk-to-reward ratio

Settings Explained

FVG Settings

• Min FVG Size: Minimum gap size in points to be considered valid (default: 2.0)

• Max FVG Age: How many bars until an FVG is removed from chart (default: 50)

• Show 50% Entry Level: Toggle the dashed entry line on/off

Session Settings

• Show Session Boxes: Toggle all session boxes on/off

• Max Sessions to Show: How many historical sessions to display (default: 5)

• Individual Session Toggles: Turn each session (Asia/London/NY/Sydney/Kill Zone) on or off

Risk Calculator Settings

• Account Size: Your trading account balance

• Risk Per Trade: Percentage of account to risk per trade (default: 0.5%)

• Tick Value/Size: Contract specifications for MNQ ($0.50 per tick, 0.25 point tick size)

Tips for Best Results

1. Trade during the Kill Zone (8:00-11:00 AM ET) for best volatility and liquidity

2. Always align trades with HTF bias - don't fight the trend

3. Wait for liquidity sweeps before entering - this confirms smart money activity

4. Use the 50% level for entries - it offers the best risk-to-reward

5. Watch for IFVG zones as additional confluence for entries

6. Use the risk calculator to size positions properly - never risk more than you can afford

7. Session boxes help identify where stops are clustered - sweeps of these levels often precede reversals

Available Alerts

• New FVG Formed (Bullish or Bearish)

• Price Touching 50% Entry Level

• FVG Mitigated (gap filled)

• Long Entry Signal

• Short Entry Signal

• PDH/PDL Liquidity Sweep

─────────────────────────────────────

Created by BullyTrading

Designed for MNQ Prop Firm Trading

One Point Global Net Liquidity The "Fuel" Behind the MarketMost traders look at price action, but price is often just a reflection of the money supply available in the system. This indicator tracks Global Net Liquidity—the actual amount of fiat currency available to flow into risk assets like Crypto and Equities.

Unlike standard "Money Supply" (M2) charts, this indicator focuses on Central Bank Balance Sheets, which is a more direct proxy for "Quantitative Easing" (QE) and "Quantitative Tightening" (QT).

How It Works (The Formula)

This script aggregates the balance sheets of the "Big 4" Central Banks, which represent ~90% of global liquidity. It automatically converts all values to USD Trillions for a standardized view.

{Global Liquidity} = {US Net Liquidity} + {ECB} + {PBoC} + {BoJ}

1. US Net Liquidity (The "Trader's" Formula) We do not just use the Fed's Total Assets. We subtract the money that is "stuck" outside the private economy:

(+) Fed Balance Sheet: Total Assets.

(-) TGA (Treasury General Account): The government's checking account. When this goes up, liquidity is drained from markets.

(-) RRP (Reverse Repo): Money parked by banks at the Fed overnight. When this goes up, liquidity is removed from the system.

2. Global Additions

ECB (Eurozone): Converted to USD.

PBoC (China): Converted to USD.

BoJ (Japan): Converted to USD.

How to Use This Indicator This indicator is designed as an Overlay on the main chart (using the Left Scale).

Correlation: Generally, when the Orange Line (Liquidity) trends up, Bitcoin and the S&P 500 trend up. When Central Banks tighten (line down), risk assets struggle.

The "Divergence" Signal (Alpha):

Bullish: If Price makes a Lower Low but Liquidity makes a Higher Low, it often signals seller exhaustion and a potential bottom.

Bearish: If Price makes a New High but Liquidity fails to follow (or drops), the rally may be unsupported and prone to a reversal.

Settings

Scale: This indicator is pinned to the Scale Left to allow it to overlay price action without distortion.

Data: Uses daily data from ECONOMICS and FRED feeds.

Fabio-Style Order Flow SystemFabio-Style Order Flow System — LVN • Delta • Big Trades • FVG • Order Blocks • Liquidity • Volume Profile

This indicator brings together all major components of Fabio Valentino’s order-flow strategy in one unified tool. It visualizes where smart money is active, where inefficiencies form, and where price is likely to react next.

🔍 FEATURES

1. Order Flow & Delta

Smoothed delta to show true market imbalance

Background color shifts to bullish/bearish delta dominance

Alerts for delta spikes & order-flow flips

2. Big Trade Detection

Highlights Big Buy and Big Sell prints (relative to average volume)

Helps identify institutional aggression on both sides

3. Low Volume Nodes (LVNs)

Automatically detects low-volume zones

Flags retests of LVNs for high-probability reactions

Uses dynamic volume thresholds for accuracy

4. Volume Profile (Lightweight)

Bucket-based intrabar profile across user-defined lookback

Highlights volume distribution without heavy TradingView CPU load

Auto-scales bucket density & transparency

5. Fair Value Gaps (FVGs)

Detects both bullish & bearish three-bar imbalances

Marks gaps visually using colored boxes

Updates dynamically with a user-set lookback

6. Order Blocks (OBs)

Identifies valid displacement bars and their origin OB

Plots clean, minimalist rectangles around key OB zones

Uses ATR-based impulse filtering

7. Liquidity Grabs

Detects wick-based liquidity sweeps

Highlights both equal high/low and stop-run type wicks

Useful for spotting reversals & trap setups

8. Strategy Dashboard

Shows real-time order flow state

Displays delta strength, big trades, LVNs, and last directional impulse

Auto-positions in all corners

🎯 PERFECT FOR

Traders who use:

Order Flow

Smart Money Concepts (SMC)

ICT / FVG / Liquidity models

Market Structure + Volume

Fabio Valentino-style analysis

⚙️ PERFORMANCE

All elements optimized

Uses automatic box-clearing to avoid array overload

Works on all timeframes & markets (crypto, FX, indices, stocks)

RSL Screener Column//@version=5

indicator("RSL Screener Column", shorttitle="RSL", overlay=false)

sma26 = ta.sma(close, 26)

rsl = close / sma26

plot(rsl)

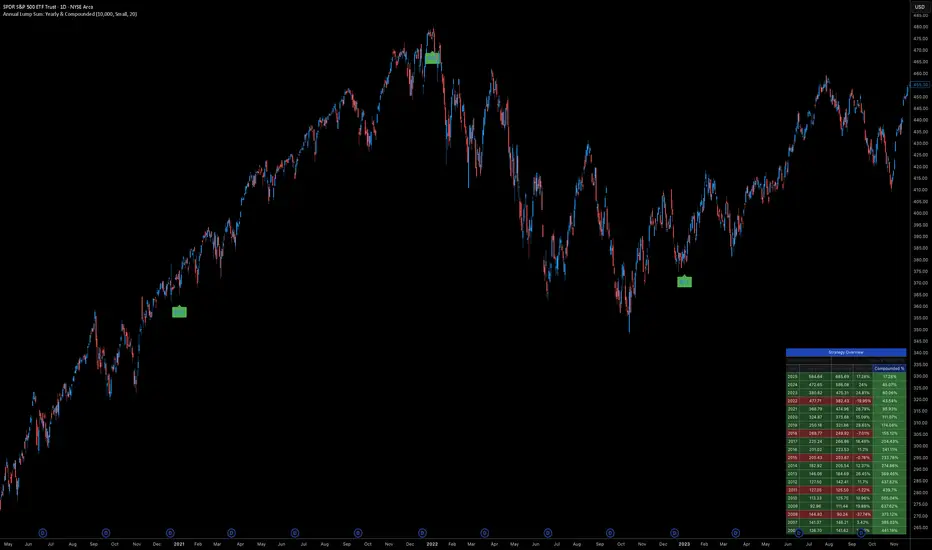

Annual Lump Sum: Yearly & CompoundedAnnual Lump Sum Investment Analyzer (Yearly vs. Compounded)

Overview

This Pine Script indicator simulates a disciplined "Lump Sum" investing strategy. It calculates the performance of buying a fixed dollar amount (e.g., $10,000) on the very first trading day of every year and holding it indefinitely.

Unlike standard backtesters that only show a total percentage, this tool breaks down performance by "Vintage" (the year of purchase), allowing you to see which specific years contributed most to your wealth.

Key Features

Automated Execution: Automatically detects the first trading bar of every new year to simulate a buy.

Dual-Yield Analysis: The table provides two distinct ways to view returns:

Yearly %: How the market performed specifically during that calendar year (Jan 1 to Dec 31).

Compounded %: The total return of that specific year's investment from the moment it was bought until today.

Live Updates: For the current year, the "End Price" and "Yields" update in real-time with market movements.

Portfolio Summary: Displays your Total Invested Capital vs. Total Current Value at the top of the table.

Table Column Breakdown

The dashboard in the bottom-right corner displays the following:

Year: The vintage year of the investment.

Buy Price: The price of the asset on the first trading day of that year.

End Price: The price on the last trading day of that year (or the current price if the year is still active).

Yearly %: The isolated performance of that specific calendar year. (Green = The market ended the year higher than it started).

Compounded %: The "Diamond Hands" return. This shows how much that specific $10,000 tranche is up (or down) right now relative to the current price.

How to Use

Add the script to your chart.

Crucial: Set your chart timeframe to Daily (D). This ensures the script correctly identifies the first trading day of the year.

Open the Settings (Inputs) to adjust:

Annual Investment Amount: Default is $10,000.

Table Size: Adjust text size (Tiny, Small, Normal, Large).

Max Rows: Limit how many historical years are shown to keep the chart clean.

Use Case

This tool is perfect for investors who want to visualize the power of long-term holding. It allows you to see that even if a specific year had a bad "Yearly Yield" (e.g., buying in 2008), the "Compounded Yield" might still be massive today due to time in the market.

SMC Pre-Trade Checklist (Mozzys)Here is a **clean, professional description** you can use when publishing your TradingView script.

It clearly explains what the indicator does and why traders use it—perfect for the public library.

---

# **📌 Script Description (for Publishing)**

**SMC Pre-Trade Checklist (Compact Edition)**

This indicator provides a **smart, compact on-chart checklist** designed for traders who use **Smart Money Concepts (SMC)**.

Instead of guessing or rushing entries, the checklist helps you confirm the essential SMC conditions *before* taking a trade.

The checklist displays as a **small 3-column panel** in the corner of your chart, making it easy to scan without covering price action.

All items are controlled through indicator settings, where you can tick each condition as you validate it in your analysis.

---

## **🔥 What This Tool Helps You Do**

This script helps you stay disciplined by verifying the core components of an SMC setup:

### **1. Higher-Timeframe (HTF) Bias**

* Market direction clarity

* Premium vs. discount zones

* HTF POIs and liquidity targets

### **2. Liquidity Conditions**

* Liquidity sweeps

* Liquidity-based take-profit targets

### **3. Market Structure**

* BOS/CHOCH confirmation

* Displacement

* Clean pullback into POI

### **4. Entry Validation**

* Quality POI

* LTF confirmation

* Logical SL/TP and RR

### **5. Risk Management**

* Correct position sizing

* Avoiding high-impact news

* Spread/volatility conditions

### **6. Trader Discipline**

* Trade matches your model

* No revenge or emotional trading

---

## **🎯 Why Traders Love This**

Most losses come from **breaking rules**, not market randomness.

This checklist forces consistency, clarity, and patience—especially in fast environments like FX, indices, and crypto.

* Prevents emotional entries

* Reduces impulsive trades

* Keeps you aligned with your SMC plan

* Works with any strategy or SMC style

* Clean, minimal, non-intrusive layout

---

## **📌 Features**

* Compact 3-column layout

* Customizable from the indicator settings

* Works on all timeframes and assets

* Zero chart clutter

* Perfect for rule-based traders

---

## **🚀 Who This Indicator Is For**

* SMC traders

* ICT-style traders

* Liquidity-based traders

* Anyone who wants more discipline & consistency

* Backtesters who want structured trade evaluation

--

Scalp Boost LONG✦ Overview

Scalp Boost LONG is a visual tool designed to highlight potential short-term upward impulses.

A signal is generated only when multiple market conditions align at the candle close, combining momentum dynamics, local probability shifts, and abnormal volume behavior.

The indicator does not repaint.

✦ Concept

The tool focuses on selective situations where the market shows signs of micro-breakout potential.

If all internal conditions are confirmed — a LONG event is displayed.

If not — the chart remains clean.

This builds a low-noise signal model, prioritizing quality over frequency.

✦ Signal Logic

The LONG signal requires confirmation of all core conditions:

• Local impulse dynamics

Identifies short-term acceleration suggesting a breakout from a compressed price structure.

• Probability beyond a statistical zone

Uses relative breakout probability instead of fixed levels, checking whether price exceeds expected local ranges.

• Abnormal volume activity

Highlights candles with monetary flow above a custom threshold, signaling increased market interest.

• Anti-overheat filter

Conditions avoiding exhausted or low-momentum phases where continuation is less likely.

Only when all filters are aligned a LONG marker appears.

✦ Visual Structure

The chart display is intentionally minimal:

• ROC Curve

Subdued line, showing short-term momentum without distraction.

• LONG Marker

Green triangle below the candle on confirmed events.

• Candle Highlight

Soft background highlight on the signal bar.

• Volume Marker

Small red dot at the bottom of candles with abnormal monetary flow.

All visual elements appear only on candle close.

✦ Alerts

A clean event structure is available for notifications:

LONG Signal

This allows receiving alerts during chart analysis or in automated workflows while keeping full control over decision-making.

✦ Notes & Guidelines

This tool:

is not a trading system,

does not provide targets or stops,

may trigger against the dominant trend,

should be combined with the user’s own methodology.

Signals are rare by design.

Do not interpret each event as a trend continuation — it highlights conditions, not outcomes.

✦ Suggested Use

-(Non-mandatory ideas for advanced users)

-identifying potential micro-breakouts,

-timing entries around volume spikes,

-adding context to scalping models,

-filtering impulsive moves from noise.

-suitable for a 5-minute timeframe

The indicator can be helpful as a confirmation layer, not a standalone decision tool.

Altcoin Relative Macro StrengthAltcoin Relative Macro Strength

Overview

The Altcoin Relative Macro Strength indicator measures the altcoin market's price performance relative to global macroeconomic conditions. By comparing TOTAL3ES (total altcoin market capitalization excluding Bitcoin, Ethereum and stable coins) against a composite macro trend, the indicator identifies periods of relative overvaluation and undervaluation.

Methodology

Global Macro Trend Calculation:

The macro trend synthesizes three primary components:

- ISM PMI – A proxy for the business cycle phase

- Global Liquidity – An aggregate measure of major central bank balance sheets and broad money supply

- IWM (Russell 2000) – Small-cap equity exposure, reflecting risk-on/risk-off market sentiment

Global Liquidity is calculated as:

Fed Balance Sheet - Reverse Repo - Treasury General Account + U.S. M2 + China M2

The final Global Macro Trend is:

ISM PMI × Global Liquidity × IWM

Theoretical Framework:

The global macro trend integrates liquidity expansion/contraction with business cycle dynamics and small-cap equity performance. The inclusion of IWM reflects altcoins' tendency to behave as high-beta risk assets, exhibiting sensitivity similar to small-cap equities. This composite exhibits strong directional correlation with altcoin market movements, capturing the risk-on/risk-off dynamics that drive altcoin performance.

Interpretation

Primary Signal:

The histogram displays the rolling percentage change of TOTAL3ES relative to the global macro trend (default: 21-period average). Positive divergence indicates altcoins are outperforming macro conditions; negative divergence suggests underperformance relative to the underlying economic and risk environment.

Data Tables:

Alts/Macro Change – Percentage deviation of the altcoin market's average value from the Global Macro Trend's average over the specified period

Macro Trend – Directional assessment of the macro trend based on slope and trend agreement:

🔵 BULLISH ▲ – Positive slope with upward trend

⚪ NEUTRAL → – Slope and trend direction disagree

🟣 BEARISH ▼ – Negative slope with downward trend

Macro Slope – Percentage rate of change in the global macro trend

Altcoin Valuation – Relative valuation category based on TOTAL3/Macro deviation:

🟢 Extreme Discount / Deep Discount / Discount

🟡 Fair Value

🔴 Premium / Large Premium / Extreme Premium

TOTAL3ES Mcap – Current total altcoin market capitalization (in billions)

Visual Components:

📊 Histogram: Alts/Macro Change

🟢 Green = Positive deviation (altcoins outperforming)

🔴 Red = Negative deviation (altcoins underperforming)

📈 Macro Slope Line

Color-coded to match trend assessment

Scaled for visibility (adjustable in settings)

Application

This indicator is designed to identify mean reversion opportunities by highlighting periods when the altcoin market materially diverges from fundamental macro and risk conditions. Extreme positive values may indicate overvaluation; extreme negative values may signal undervaluation relative to the prevailing economic and risk appetite backdrop.

Strategy Considerations:

- Identify extremes: Look for periods when the histogram reaches elevated positive or negative levels

- Assess valuation: Use the Altcoin Valuation reading to gauge relative over/undervaluation

Confirm with risk sentiment: Check whether macro conditions and risk appetite support or contradict current price levels

- Mean reversion: Consider that significant deviations from trend historically tend to revert

Note: This indicator identifies relative valuation based on macro conditions and risk sentiment—it does not predict price direction or timing.

Settings

Lookback Period – 21 bars (default) – Number of bars for calculating rolling averages

Macro Slope Scale – 3.0 (default) – Multiplier for macro slope line visibility

FAIRPRICE_VWAP_RDFAIRPRICE_VWAP_RD

This script plots an **anchored VWAP (Volume Weighted Average Price)** that resets

based on the user-selected anchor period. It acts as a dynamic “fair value” line

that reflects where the market has actually transacted during the chosen period.

FEATURES

- Multiple anchor options: Session, Week, Month, Quarter, Year, Decade, Century,

Earnings, Dividends, or Splits.

- Intelligent handling of the “Session” anchor so it works correctly on both 1m

(resets each new day) and 1D (continuous, non-resetting VWAP).

- Manual VWAP calculation using cumulative(price * volume) and cumulative(volume),

ensuring the line is stable and works on all timeframes.

- Optional hiding of VWAP on daily or higher charts.

- Offset input for horizontal shifting if desired.

- VWAP provides a true “fair price” reference for trend, mean-reversion,

and institutional-level analysis.

PURPOSE

This indicator solves the common problem of VWAP behaving incorrectly on higher

timeframes, on synthetic data, or with unusual anchors. By implementing VWAP

manually and allowing flexible reset conditions, it functions reliably as

an institutional-style fair value benchmark across any timeframe.

BTC – LEVR: Leverage Efficiency & Volume RatioLEVR: Leverage Efficiency & Volume Ratio

Observation-only. Data: IntoTheBlock.

Overview

The Leverage Efficiency & Volume Ratio (LEVR) is a market structure oscillator designed to detect "Paper Bubbles" and "Organic Bottoms" by separating speculative greed from network utility. While most indicators analyze price action, LEVR analyzes market fragility. It operates on the thesis that Sustainable Rallies are driven by Spot/Network Activity, while Fragile Rallies are driven by Derivatives Leverage.

Synergy

How it works with VERI

LEVR is designed to be the tactical counterpart to the fundamental VERI Indicator (Valuation & Entity Ratio Index).

Use VERI for Strategy: To identify Value. (Is Bitcoin cheap? Are Whales buying?)

Use LEVR for Risk: To identify Structure. (Is the current price move real, or is it a leverage bubble about to pop?)

The "Perfect Setup"

The strongest buy signals occur when VERI is in the Accumulation Zone (Whales buying) AND LEVR is in the Organic Zone (Leverage is flushed out) (as it was the case in the Dec 2022 Bear Market Bottom).

Why LEVR is Unique

Standard indicators often fail to contextualize Open Interest:

vs. Raw Open Interest: Raw OI always trends up over time as the market grows. LEVR solves this by normalizing OI against Active Addresses. This reveals when leverage is outpacing actual adoption.

vs. ELR (Estimated Leverage Ratio): Classic ELR divides Open Interest by Exchange Reserves. However, Exchange Reserves are notoriously difficult to track accurately. LEVR uses Active Addresses (Network Utility) as a cleaner, more reliable denominator for network health.

Methodology

The Mathematics: The indicator calculates a normalized Z-Score ratio between two IntoTheBlock datasets:

The Numerator (Greed): Perpetual Open Interest. The total dollar value of all open futures contracts. This represents the "Gambling" capital.

The Denominator (Utility): Active Addresses. The number of unique addresses transacting on-chain. This represents the "Real" user base.

The Formula : LEVR = Z-Score ( Perpetual Open Interest / Active Addresses )

How to Interpret the Visuals

The line color changes dynamically to reflect the current risk regime:

🟥 Speculative Premium (Red Line > 2.0) :

Signal: "Leverage Bubble."

Context: Open Interest is rising significantly faster than User Growth. The rally is fueled by debt.

Risk: High probability of a "Long Squeeze" or liquidation cascade.

🟦 Organic Base (Blue Line < -1.5) :

Signal: "Spot Driven Market."

Context: Speculators have been flushed out, but active network usage remains high. The line turns Blue to signal a healthy opportunity zone.

Risk: Low. Historically marks robust bottoms where hands are strong.

🟧 Neutral (Orange Line) :

The market is in a transition phase between organic growth and speculation.

Settings & Inputs

Users can customize the sensitivity of the Z-Score to fit their trading style (in brackets their current standard value):

Lookback Period (365) : The rolling window used to establish the "Baseline." A 365-day window captures the yearly trend.

Signal Smoothing (7) : A short moving average to reduce daily data noise.

Bubble Zone Top/Bottom (3.0 / 2.0) : The thresholds for the Red Zone. Raising the "Top" value will only show the most extreme, generational leverage bubbles.

Organic Zone Top/Bottom (-1.5 / -2.5) : The thresholds for the Green Zone. Lowering these values requires a deeper "flush" to trigger a signal.

Optimization

This indicator is mathematically optimized for the Daily (1D) timeframe. Using it on lower timeframes may result in noise due to the daily resolution of on-chain data.

Important Note on Historical Data

Please be aware that aggregated global Perpetual Open Interest data only becomes reliable and widely available starting around 2020-2021.

Pre-2021: The indicator will show a flat line or empty values. This is not a bug; it reflects the lack of historical derivatives market data for that period.

2021-Present: The indicator functions fully as intended.

Credits

Concept inspired by the "Estimated Leverage Ratio" (ELR) popularised by CryptoQuant and analysts like Willy Woo. LEVR adapts this concept for TradingView by substituting Exchange Reserves with Network Activity for better reliability.

Disclaimer

This tool is for research purposes only. It visualizes market structure data and does not constitute financial advice.

Tags

bitcoin, btc, open interest, leverage, on-chain, intotheblock, risk, derivatives, levr, veri

BTC Price Prediction Model [Global PMI]V2🇺🇸 English Guide

1. Introduction

This indicator was created by GW Capital using Gemini Vibe Coding technology. It leverages advanced AI coding capabilities to reconstruct complex macroeconomic models into actionable trading tools.

2. Credits

Special thanks to the original model author, Marty Kendall. His research into the correlation between Bitcoin's price and macroeconomic factors lays the foundation for this algorithm.

3. Model Principles & Formula

This model calculates the "Fair Value" of Bitcoin based on four key macroeconomic pillars. It assumes that Bitcoin's price is a function of Global Liquidity, Network Security, Risk Appetite, and the Economic Cycle.

💡 Unique Insight: PMI & The 4-Year Cycle

A key distinguishing feature of this model is the hypothesis that Bitcoin's famous "4-Year Halving Cycle" may be intrinsically linked to the Global Business Cycle (PMI), rather than just supply shocks.

Therefore, the model incorporates PMI as a valuation "Amplifier".

Note: Due to TradingView data limitations, US PMI is currently used as the proxy for the global cycle.

The Formula

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

Global Liquidity (M2): Sum of M2 supply from US, China, Eurozone, and Japan (converted to USD). Represents the pool of fiat money available to flow into assets.

Network Security (Hashrate): Bitcoin's hashrate, representing the physical security and utility of the network.

Risk Appetite (S&P 500): Used as a proxy for global risk sentiment.

Economic Cycle (PMI Z-Score): US Manufacturing PMI is used to amplify or dampen the valuation based on where we are in the business cycle (Expansion vs. Contraction).

4. How to Use

The indicator plots the Fair Value (White Line) and four sentiment bands based on statistical deviation (Z-Score).

Sentiment Zones

🚨 Extreme Greed (Red Zone): Price > +0.3 StdDev. Historically indicates a market top or overheated sentiment.

⚠️ Greed (Orange Zone): Price > +0.15 StdDev. Bullish momentum is strong but caution is advised.

⚖️ Fair Value (White Line): The theoretical "correct" price based on macro data.

😨 Fear (Teal Zone): Price < -0.15 StdDev. Undervalued territory.

💎 Extreme Fear (Green Zone): Price < -0.3 StdDev. Historically a generational buying opportunity.

Sentiment Score (0-100)

100: Maximum Greed (Top)

50: Fair Value

0: Maximum Fear (Bottom)

5. Usage Recommendations

Timeframe: Daily (1D) or Weekly (1W) ONLY.

Reason: The underlying data sources (M2, PMI) are updated monthly. The S&P 500 and Hashrate are daily. Using this indicator on intraday charts (e.g., 15m, 1h, 4h) adds no value because the fundamental data does not change that fast.

Long-Term View: This is a macro-cycle indicator designed for identifying cycle tops and bottoms over months and years, not for day trading.

6. Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. The model relies on historical correlations which may not hold true in the future. All trading involves risk. GW Capital and the creators assume no responsibility for any trading losses.

7. Support Us ❤️

If you find this indicator useful, please Boost 👍, Comment, and add it to your Favorites! Your support keeps us going.

🇨🇳 中文说明 (Chinese Version)

1. 简介

本指标由 GW Capital 使用 Gemini Vibe Coding 技术制作。利用先进的 AI 编程能力,将复杂的宏观经济模型重构为可执行的交易工具。

2. 致谢

特别感谢模型原作者 Marty Kendall。他对这一算法的研究奠定了基础,揭示了比特币价格与宏观经济因素之间的深层联系。

3. 模型原理与公式

该模型基于四大宏观经济支柱计算比特币的“公允价值”。它假设比特币的价格是全球流动性、网络安全性、风险偏好和经济周期的函数。

💡 独家洞察:PMI 与 4年周期

本模型的一个核心独特之处在于:我们认为比特币著名的“4年减半周期”背后的真正驱动力,可能与全球商业周期 (PMI) 高度同步,而不仅仅是供应减半。

因此,模型特别引入 PMI 作为估值的“放大器” (Amplifier)。

注:由于 TradingView 数据源限制,目前采用历史数据最详尽的美国 PMI 作为全球周期的代理指标。

模型公式

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

全球流动性 (M2): 美、中、欧、日四大经济体的 M2 总量(折算为美元)。代表可流入资产的法币资金池。

网络安全性 (Hashrate): 比特币全网算力,代表网络的物理安全性和实用价值。

风险偏好 (S&P 500): 作为全球风险情绪的代理指标。

经济周期 (PMI Z-Score): 美国制造业 PMI 用于根据商业周期(扩张 vs 收缩)来放大或抑制估值。

4. 指标用法

指标会在图表上绘制 公允价值 (白线) 以及基于统计偏差 (Z-Score) 的四条情绪带。

情绪区间

🚨 极度贪婪 (红色区域): 价格 > +0.3 标准差。历史上通常预示市场顶部或情绪过热。

⚠️ 一般贪婪 (橙色区域): 价格 > +0.15 标准差。多头动能强劲,但需谨慎。

⚖️ 公允价值 (白线): 基于宏观数据的理论“正确”价格。

😨 一般恐惧 (青色区域): 价格 < -0.15 标准差。进入低估区域。

💎 极度恐惧 (绿色区域): 价格 < -0.3 标准差。历史上通常是代际级别的买入机会。

情绪评分 (0-100)

100: 极度贪婪 (顶部)

50: 公允价值

0: 极度恐惧 (底部)

5. 使用建议

周期: 仅限日线 (1D) 或周线 (1W)。

原因: 底层数据源(M2, PMI)是月度更新的。标普500和算力是日度更新的。在日内图表(如15分钟、1小时、4小时)上使用此指标没有任何意义,因为基本面数据不会变化得那么快。

长期视角: 这是一个宏观周期指标,旨在识别数月甚至数年的周期顶部和底部,而非用于日内交易。

6. 免责声明

本指标仅供教育和参考使用,不构成任何财务建议。该模型依赖于历史相关性,未来可能不再适用。所有交易均涉及风险。GW Capital 及制作者不对任何交易损失承担责任。

Global M2(USD) V2This indicator tracks the total Global M2 Money Supply in USD. It aggregates economic data from the world's four largest central banks (Fed, PBOC, ECB, BOJ). The script automatically converts non-USD money supplies (CNY, EUR, JPY) into USD using real-time exchange rates to provide a unified view of global liquidity.

Usage

Macro Analysis: Overlay this on assets like Bitcoin or the S&P 500 to see if price appreciation is driven by fiat currency debasement ("money printing").

Liquidity Trends: A rising orange line indicates expanding global liquidity (generally bullish for risk assets), while a falling line suggests monetary tightening.

Real-time Data: A label at the end of the line displays the exact raw total in USD for precise tracking.

该脚本旨在追踪以美元计价的全球 M2 货币供应总量。它聚合了四大央行(美联储、中国央行、欧洲央行、日本央行)的经济数据,并通过实时汇率将非美货币(人民币、欧元、日元)统一折算为美元,从而构建出一个标准化的全球流动性指标。

用法

宏观对冲: 将其叠加在比特币或股票图表上,用于判断资产价格的上涨是否由全球法币“大放水”推动。

趋势研判: 橙色曲线向上代表全球流动性扩张(通常利好风险资产),向下则代表流动性紧缩。

数据直观: 脚本会在图表末端生成一个标签,实时显示当前全球 M2 的具体美元总额。

BTC Price Prediction Model [Global PMI]🇨🇳 中文说明 (Chinese Version)

1. 简介

本指标由 GW Capital 使用 Gemini Vibe Coding 技术制作。利用先进的 AI 编程能力,将复杂的宏观经济模型重构为可执行的交易工具。

2. 致谢

特别感谢模型原作者 Marty Kendall。他对这一算法的研究奠定了基础,揭示了比特币价格与宏观经济因素之间的深层联系。

3. 模型原理与公式

该模型基于四大宏观经济支柱计算比特币的“公允价值”。它假设比特币的价格是全球流动性、网络安全性、风险偏好和经济周期的函数。

模型公式

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

全球流动性 (M2): 美、中、欧、日四大经济体的 M2 总量(折算为美元)。代表可流入资产的法币资金池。

网络安全性 (Hashrate): 比特币全网算力,代表网络的物理安全性和实用价值。

风险偏好 (S&P 500): 作为全球风险情绪的代理指标。

经济周期 (PMI Z-Score): 美国制造业 PMI 用于根据商业周期(扩张 vs 收缩)来放大或抑制估值。

4. 指标用法

指标会在图表上绘制 公允价值 (白线) 以及基于统计偏差 (Z-Score) 的四条情绪带。

情绪区间

🚨 极度贪婪 (红色区域): 价格 > +0.3 标准差。历史上通常预示市场顶部或情绪过热。

⚠️ 一般贪婪 (橙色区域): 价格 > +0.15 标准差。多头动能强劲,但需谨慎。

⚖️ 公允价值 (白线): 基于宏观数据的理论“正确”价格。

😨 一般恐惧 (青色区域): 价格 < -0.15 标准差。进入低估区域。

💎 极度恐惧 (绿色区域): 价格 < -0.3 标准差。历史上通常是代际级别的买入机会。

情绪评分 (0-100)

100: 极度贪婪 (顶部)

50: 公允价值

0: 极度恐惧 (底部)

5. 使用建议

周期: 仅限日线 (1D) 或周线 (1W)。

原因: 底层数据源(M2, PMI)是月度更新的。标普500和算力是日度更新的。在日内图表(如15分钟、1小时、4小时)上使用此指标没有任何意义,因为基本面数据不会变化得那么快。

长期视角: 这是一个宏观周期指标,旨在识别数月甚至数年的周期顶部和底部,而非用于日内交易。

6. 免责声明

本指标仅供教育和参考使用,不构成任何财务建议。该模型依赖于历史相关性,未来可能不再适用。所有交易均涉及风险。GW Capital 及制作者不对任何交易损失承担责任。

🇺🇸 English Guide (英文说明)

1. Introduction

This indicator was created by GW Capital using Gemini Vibe Coding technology. It leverages advanced AI coding capabilities to reconstruct complex macroeconomic models into actionable trading tools.

2. Credits

Special thanks to the original model author, Marty Kendall. His research into the correlation between Bitcoin's price and macroeconomic factors lays the foundation for this algorithm.

3. Model Principles & Formula

This model calculates the "Fair Value" of Bitcoin based on four key macroeconomic pillars. It assumes that Bitcoin's price is a function of Global Liquidity, Network Security, Risk Appetite, and the Economic Cycle.

The Formula

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

Global Liquidity (M2): Sum of M2 supply from US, China, Eurozone, and Japan (converted to USD). Represents the pool of fiat money available to flow into assets.

Network Security (Hashrate): Bitcoin's hashrate, representing the physical security and utility of the network.

Risk Appetite (S&P 500): Used as a proxy for global risk sentiment.

Economic Cycle (PMI Z-Score): US Manufacturing PMI is used to amplify or dampen the valuation based on where we are in the business cycle (Expansion vs. Contraction).

4. How to Use

The indicator plots the Fair Value (White Line) and four sentiment bands based on statistical deviation (Z-Score).

Sentiment Zones

🚨 Extreme Greed (Red Zone): Price > +0.3 StdDev. Historically indicates a market top or overheated sentiment.

⚠️ Greed (Orange Zone): Price > +0.15 StdDev. Bullish momentum is strong but caution is advised.

⚖️ Fair Value (White Line): The theoretical "correct" price based on macro data.

😨 Fear (Teal Zone): Price < -0.15 StdDev. Undervalued territory.

💎 Extreme Fear (Green Zone): Price < -0.3 StdDev. Historically a generational buying opportunity.

Sentiment Score (0-100)

100: Maximum Greed (Top)

50: Fair Value

0: Maximum Fear (Bottom)

5. Usage Recommendations

Timeframe: Daily (1D) or Weekly (1W) ONLY.

Reason: The underlying data sources (M2, PMI) are updated monthly. The S&P 500 and Hashrate are daily. Using this indicator on intraday charts (e.g., 15m, 1h, 4h) adds no value because the fundamental data does not change that fast.

Long-Term View: This is a macro-cycle indicator designed for identifying cycle tops and bottoms over months and years, not for day trading.

6. Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. The model relies on historical correlations which may not hold true in the future. All trading involves risk. GW Capital and the creators assume no responsibility for any trading losses.

BTC - VERI - Valuation & Entity Ratio IndexVERI: Valuation & Entity Ratio IndexObservation-only.

Data: IntoTheBlock.

Overview & Philosophy

The name VERI is derived from the Latin Veritas (Truth). In a crypto market often driven by deceptive speculative noise, this indicator seeks to establish the "On-Chain Truth" of a price trend.

It operates on the thesis that price action is only sustainable when verified by high-conviction capital flows.VERI is a fundamental composite oscillator that fuses Entity Behavior (Who is holding?) with Network Valuation (Is the price fair?) to identify Bitcoin market cycle extremes.

The "Alpha"

Why this Composite stands out: on-chain metrics often tell only half the story.

MVRV tells you if the price is cheap, but not if anyone is actually buying.

Whale Activity tells you if large players are moving, but not if they are accumulating at a value discount.

VERI fuses these two dimensions into a single Z-Score. It identifies the rare, high-probability moments where Smart Money Conviction intersects with Deep Value.

Methodology

The Mathematics of VERI: The indicator constructs a composite index using three fundamental metrics from IntoTheBlock:

The "Who" (Entity Ratio) : We calculate the flow ratio between Whales (>1% supply holders) and Retail (<0.1% supply holders). A rising ratio indicates supply is transferring from weak hands to strong hands.

The "Why" (Valuation Multiplier) : We utilize the MVRV (Market Value to Realized Value) ratio. To isolate value opportunities, we use the inverse (1 / MVRV).

The Fusion : These factors are multiplied to create the raw VERI index.

Normalization & Inversion

We apply a rolling Z-Score (standard deviation from the mean) and invert the result.

How to Interpret the Indicator

Because the output is inverted, the visual logic matches price action intuitively:

🟥 Distribution Zone (High Values > 1.5):

The Signal: "Low Conviction Overvaluation."

Context: The price is historically expensive relative to the cost basis (High MVRV), and Whales are distributing coins to Retail.Implication: Historically precedes macro tops or deep corrections.

🟩 Accumulation Zone (Low Values < -1.5):

The Signal: "High Conviction Undervaluation."Context: The price is historically cheap (Low MVRV), and Whales are aggressively accumulating relative to Retail.

Implication: Historically precedes macro bottoms and generational entry points.

Zero Line : Represents the historical baseline. A crossover of the zero line often confirms a regime shift (e.g., from Bear to Bull).

Visual Guide & Features

Dynamic Coloring: The line turns Red in the Distribution Zone, Blue in the Accumulation Zone, and Orange during neutral trends.

Zone Labels: Static labels are pinned to the left side of the chart for immediate context.

The "Data Check" Monitor (Status Table): Since this indicator relies on third-party fundamental data, we have included a diagnostic table in the bottom-right corner.

Data Check Monitor Guide

STATUS: LIVE (Green): The indicator is functioning correctly. All data feeds (Whales, Retail, MVRV) are being retrieved successfully.

STATUS: WAIT (Red): The indicator cannot retrieve data. This might happen for some reasons, e.g. your TradingView plan may not support IntoTheBlock integration.

Settings

Lookback Period (Default: 365): The window used for Z-Score normalization. We use a full year to smooth out seasonal volatility.

Smoothing (Default: 7): A 7-day smoothing is applied to the signal to filter out daily noise.

Zone Thresholds: Users can customize the specific Z-Score levels for the Distribution and Accumulation bands.

Disclaimer

This script is for research and educational purposes only. It uses historical on-chain data to visualize market structure and does not constitute financial advice. Past performance of whale entities does not guarantee future results.

Tags

bitcoin, btc, on-chain, mvrv, whales, valuation, fundamentals, cycle, oscillator, veri

Buffett Quality Filter (TTM)//@version=6

indicator("Buffett Quality Filter (TTM)", overlay = true, max_labels_count = 500)

// 1. Get financial data (TTM / FY / FQ)

// EPS (TTM) for P/E

eps = request.financial(syminfo.tickerid, "EARNINGS_PER_SHARE_BASIC", "TTM")

// Profitability & moat (annual stats)

roe = request.financial(syminfo.tickerid, "RETURN_ON_EQUITY", "FY")

roic = request.financial(syminfo.tickerid, "RETURN_ON_INVESTED_CAPITAL", "FY")

// Margins (TTM – rolling 12 months)

grossMargin = request.financial(syminfo.tickerid, "GROSS_MARGIN", "TTM")

netMargin = request.financial(syminfo.tickerid, "NET_MARGIN", "TTM")

// Balance sheet safety (quarterly)

deRatio = request.financial(syminfo.tickerid, "DEBT_TO_EQUITY", "FQ")

currentRat = request.financial(syminfo.tickerid, "CURRENT_RATIO", "FQ")

// Growth (1-year change, TTM)

epsGrowth1Y = request.financial(syminfo.tickerid, "EARNINGS_PER_SHARE_BASIC_ONE_YEAR_GROWTH", "TTM")

revGrowth1Y = request.financial(syminfo.tickerid, "REVENUE_ONE_YEAR_GROWTH", "TTM")

// Free cash flow (TTM) and shares to build FCF per share for P/FCF

fcf = request.financial(syminfo.tickerid, "FREE_CASH_FLOW", "TTM")

sharesOut = request.financial(syminfo.tickerid, "TOTAL_SHARES_OUTSTANDING", "FQ")

fcfPerShare = (not na(fcf) and not na(sharesOut) and sharesOut != 0) ? fcf / sharesOut : na

// 2. Valuation ratios from price

pe = (not na(eps) and eps != 0) ? close / eps : na

pFcf = (not na(fcfPerShare) and fcfPerShare > 0) ? close / fcfPerShare : na

// 3. Thresholds (Buffett-style, adjustable)

minROE = input.float(15.0, "Min ROE %")

minROIC = input.float(12.0, "Min ROIC %")

minGM = input.float(30.0, "Min Gross Margin %")

minNM = input.float(8.0, "Min Net Margin %")

maxDE = input.float(0.7, "Max Debt / Equity")

minCurr = input.float(1.3, "Min Current Ratio")

minEPSG = input.float(8.0, "Min EPS Growth 1Y %")

minREVG = input.float(5.0, "Min Revenue Growth 1Y %")

maxPE = input.float(20.0, "Max P/E")

maxPFCF = input.float(20.0, "Max P/FCF")

// 4. Individual conditions

cROE = not na(roe) and roe > minROE

cROIC = not na(roic) and roic > minROIC

cGM = not na(grossMargin) and grossMargin > minGM

cNM = not na(netMargin) and netMargin > minNM

cDE = not na(deRatio) and deRatio < maxDE

cCurr = not na(currentRat) and currentRat > minCurr

cEPSG = not na(epsGrowth1Y) and epsGrowth1Y > minEPSG

cREVG = not na(revGrowth1Y) and revGrowth1Y > minREVG

cPE = not na(pe) and pe < maxPE

cPFCF = not na(pFcf) and pFcf < maxPFCF

// 5. Composite “Buffett Score” (0–10) – keep it on ONE line to avoid line-continuation errors

score = (cROE ? 1 : 0) + (cROIC ? 1 : 0) + (cGM ? 1 : 0) + (cNM ? 1 : 0) + (cDE ? 1 : 0) + (cCurr ? 1 : 0) + (cEPSG ? 1 : 0) + (cREVG ? 1 : 0) + (cPE ? 1 : 0) + (cPFCF ? 1 : 0)

// Strictness

minScoreForPass = input.int(7, "Min score to pass (0–10)", minval = 1, maxval = 10)

passes = score >= minScoreForPass

// 6. Visuals

bgcolor(passes ? color.new(color.green, 80) : na)

plot(score, "Buffett Score (0–10)", color = color.new(color.blue, 0))

// Info label on last bar

var label infoLabel = na

if barstate.islast

if not na(infoLabel)

label.delete(infoLabel)

infoText = str.format(

"Buffett score: {0} ROE: {1,number,#.0}% | ROIC: {2,number,#.0}% GM: {3,number,#.0}% | NM: {4,number,#.0}% P/E: {5,number,#.0} | P/FCF: {6,number,#.0} D/E: {7,number,#.00} | Curr: {8,number,#.00}",

score, roe, roic, grossMargin, netMargin, pe, pFcf, deRatio, currentRat)

infoLabel := label.new(bar_index, high, infoText,

style = label.style_label_right,

color = color.new(color.black, 0),

textcolor = color.white,

size = size.small)

BTC / XAU Calculator/Hesaplayıcı

USER GUIDE

BTC/XAU Calculator is a table-based indicator that displays Bitcoin price, Gold price (XAU/USD), and the BTC/XAU ratio simultaneously. It pulls real-time market data and calculates values based on your manual inputs.

⸻

Features

• Automatically fetches live BTCUSD and XAUUSD prices.

• Supports two-way manual calculations:

• BTC price → Ratio calculation

• Ratio → BTC price calculation

• Clear table layout showing Market vs Calculated values.

• Compatible with Binance, OANDA, and all brokers.

⸻

1. Settings

Gold Price (XAU/USD)

• When “Use live XAU price” is enabled, the indicator uses real-time XAU/USD.

• If disabled, you can enter your own gold price manually.

⸻

2. Calculation Modes

A) Calculate BTC from Ratio

BTC = Ratio × Gold price

Example:

XAU = 4200

Ratio = 19.08

→ BTC = 4200 × 19.08 = 80,136 USD

⸻

B) Calculate Ratio from BTC

Ratio = BTC price ÷ Gold price

Example:

BTC = 90,000

XAU = 4250

→ Ratio = 90,000 / 4,250 = 21.18

3. Suggested Uses

• Evaluate BTC as cheap/expensive relative to gold

• BTC target projections based on gold

• Macro hedge and correlation analysis

• BTC/XAU ratio-based scenario modeling

⸻

Notes

• This indicator does not generate trading signals.

• It is intended for numerical comparison and scenario building only.

Source: The design and calculation logic of this indicator were created in collaboration with OpenAI’s ChatGPT model.

MCX GOLD1! SpotHelps convert MCX gold rolling contract symbol to spot price.

Note: It cant accurately infer the contract role date, so it makes some assumptions, use the rolldays to adjust where needed

Bollinger Bands Delta Matrix Analytics [BDMA] Bollinger Bands Delta Matrix Analytics (BDMA) v7.0

Deep Kinetic Engine – 5x8 Volatility & Delta Decision Matrix

1. Introduction & Concept

Bollinger Bands Delta Matrix Analytics (BDMA) v7.0 is an analytical framework that merges:

- Spatial analysis via Bollinger Bands (%B location),

- with a 4-factor Deep Kinetic Engine based on:

• Total Volume

• Buy Volume

• Sell Volume

• Delta (Buy – Sell) Z-Scores

and converts them into an expanded 5×8 decision matrix that continuously tracks where price is trading and how the underlying orderflow is behaving.

BDMA is not a trading system or strategy. It does not generate entry/exit signals.

Instead, it provides a structured contextual map of volatility, volume, and delta so traders can:

- identify climactic extensions vs. fakeouts,

- distinguish strong initiative moves vs. passive absorption,

- and detect squeezes, traps, and liquidity voids with a unified visual dashboard.

2. Spatial Engine – Bollinger S-States (S1–S5)

The spatial dimension of BDMA comes from classic Bollinger Bands.

Price location is expressed as Percent B (%B) and mapped into 5 spatial states (S-States):

S1 – Hyper Extension (Above Upper Band)

Price has pushed beyond the upper Bollinger Band.

Often associated with parabolic or blow-off behavior, late-stage momentum, and elevated reversal risk.

S2 – Resistance Test (Upper Zone)

Price trades in the upper Bollinger region but remains inside the bands.

Represents a sustained test of resistance, typically within an established or emerging uptrend.

S3 – Neutral Zone (Middle)

Price hovers around the mid-band.

This is the mean reversion gravity field where the market often consolidates or transitions between regimes.

S4 – Support Test (Lower Zone)

Price trades in the lower Bollinger region but inside the bands.

Represents a sustained test of support within range or downtrend structures.

S5 – Hyper Drop (Below Lower Band)

Price extends below the lower Bollinger Band.

Often aligned with panic, forced liquidations, or capitulation-type behavior, with increased snap-back risk.

These 5 S-States define the vertical axis (rows) of the BDMA matrix.

3. Deep Kinetic Engine – 4-Factor Z-Score & D-States (D1–D8)

The Deep Kinetic Engine transforms raw volume and delta into standardized Z-Scores to measure how abnormal current activity is relative to its recent history.

For each bar:

- Raw Buy Volume is estimated from the candle’s position within its range

- Raw Sell Volume is complementary to buy volume

- Raw Delta = Buy Volume – Sell Volume

- Total Volume = Buy Volume + Sell Volume

These 4 series are then normalized using a unified Z-Score lookback to produce:

1. Z_Vol_Total – overall activity and liquidity intensity

2. Z_Vol_Buy – aggression from buyers (attack)

3. Z_Vol_Sell – aggression from sellers (defense or attack)

4. Z_Delta – net victory of one side over the other

Thresholds for Extreme, Significant, and Neutral Z-Score levels are fully configurable, allowing you to tune the sensitivity of the kinetic states.

Using Z_Vol_Total and Z_Delta (plus threshold logic), BDMA assigns one of 8 Deep Kinetic states (D-States):

D1 – Climax Buy

Extreme Total Volume + Extreme Positive Delta → Buying climax or blow-off behavior.

D2 – Strong Buy

High Volume + High Positive Delta → Confirmed bullish initiative activity.

D3 – Weak Buy / Fakeout

Low Volume + High Positive Delta → Bullish delta without commitment, low-liquidity breakout risk.

D4 – Absorption / Conflict

High Volume + Neutral Delta → Aggressive two-way trade, strong absorption, war zone behavior.

D5 – Neutral

Low Volume + Neutral Delta → Low-energy environment with low conviction.

D6 – Weak Sell / Fakeout

Low Volume + High Negative Delta → Bearish delta without commitment, low-liquidity breakdown risk.

D7 – Strong Sell

High Volume + High Negative Delta → Confirmed bearish initiative activity.

D8 – Capitulation

Extreme Volume + Extreme Negative Delta → Panic selling or capitulation regime.

These 8 D-States define the horizontal axis (columns) of the BDMA matrix.

4. The 5×8 BDMA Decision Matrix

The core of BDMA is a 5×8 matrix where:

- Rows (1–5) = Spatial S-States (S1…S5)

- Columns (1–8) = Kinetic D-States (D1…D8)

Each of the 40 possible combinations (SxDy) is pre-computed and mapped to:

- a Status or Regime Title (for example: Climax Breakout, Bear Trap Spring, Capitulation Breakdown),

- a Bias (Climactic Bull, Neutral, Strong Bear, Conflict or Reversal Risk, and similar labels),

- and a Strategic Signal or Consideration (for example: High reversal risk, Wait for confirmation, Low probability zone – avoid).

Internally, BDMA resolves all 40 regimes so the current state can be displayed on the dashboard without performance overhead.

5. Key Regime Families (How to Read the Matrix)

5.1. Breakouts and Breakdowns

Climax Breakout (Top-side)

Spatial S1 with Kinetic D1 or D2

Bias: Explosive or Extreme Bull

Signal:

- Strong or climactic upside extension with abnormal bullish orderflow.

- Trend continuation is possible, but reversal risk is extremely high after blow-off phases.

Low-Conviction Breakout (Fakeout Risk)

S1 with D3 (Weak Buy, low liquidity)

Bias: Weak Bull – Caution

Signal:

- Breakout not supported by volume.

- Elevated risk of failed auction or bull trap.

Capitulation Breakdown (Bottom-side)

Spatial S5 with Kinetic D8

Bias: Climactic Bear (panic)

Signal:

- Capitulation-type selling or forced liquidations.

- Trend can still proceed, but snap-back or violent short-covering risk is high.

Initiative Breakdown vs. Weak Breakdown

- Strong, high-volume breakdown typically corresponds to D7 (Strong Sell).

- Low-volume breakdown often corresponds to D6 (Weak Sell or Fakeout) with potential for failure.

5.2. Absorption, Traps and Springs

Absorption at Resistance (Top-side conflict)

S1 or S2 with D4 (Absorption or Conflict)

Bias: Conflict – Extreme Tension

Signal:

- Heavy two-way trade near resistance.

- Potential distribution or reversal if sellers begin to dominate.

Bull Trap or Failed Auction

Typically S1 with D6 (Weak Sell breakdown behavior after a top-side attempt)

Indicates a breakout attempt that fails and reverses, often after poor liquidity structure.

Absorption at Support and Bear Trap (Spring)

S4 or S5 with D4 or D3

Bias: Conflict or Weak Bear – Reversal Risk

Signal:

- Aggressive buying into lows (spring or shakeout behavior).

- Potential bear trap if price reclaims lost territory.

5.3. Trend Phases

Strong Uptrend Phases

Typically seen when S2–S3 combine with strong bullish kinetic behavior.

Bias: Strong or Extreme Bull

Signal:

- Pullbacks into S3 or S4 with supportive kinetic states often act as trend continuation zones.

Strong Downtrend Phases

Typically seen when S3–S4 combine with strong bearish kinetic behavior.

Bias: Strong or Extreme Bear

Signal:

- Rallies into resistance with strong bearish kinetic backing may act as continuation sell zones.

5.4. Neutral, Exhaustion and Squeeze

Exhaustion or Liquidity Void

S1 or S5 with D5 (Neutral kinetics)

Bias: Neutral or Exhaustion

Signal:

- Spatial extremes without kinetic confirmation.

- Often marks the end of a move, with poor follow-through.

Choppy, Low-Activity Range

S3 with D5

Bias: Neutral

Signal:

- Low volume, low conviction market.

- Typically a low-probability environment where standing aside can be logical.

Squeeze or High-Tension Zone

S3 with D4 or tightly clustered kinetic values

Bias: Conflict or High Tension

Signal:

- Hidden battle inside a volatility contraction.

- Often precedes large directionally-biased moves.

6. Dashboard Layout & Reading Guide

When Show Dashboard is enabled, BDMA displays:

1. Title and Status Line

Name of the current regime (for example: Climax Breakout, Bear Trap Spring, Mean Reversion).

2. Bias Line

Plain-language summary of directional context such as Climactic Bull, Strong Bear, Neutral, or Conflict and Reversal Risk.

3. Signal or Strategic Notes

Concise guidance focused on risk and context, not entries. For example:

- High reversal risk – aggressive traders only

- Wait for confirmation (break or rejection)

- Low probability zone – avoid taking new positions

4. Kinetic Profile (4-Factor Z-Score)

Shows the current Z-Scores for Total Volume (Activity), Buy Volume (Attack), Sell Volume (Defense), and Delta (Net Result).

5. Matrix Heatmap (5×8)

Visual representation of S-State vs. D-State with color coding:

- Bullish clusters in a green spectrum

- Bearish clusters in a red spectrum

- Conflict or exhaustion zones in yellow, amber, or neutral tones

The dashboard can be repositioned (top right, middle right, or bottom right) and its size can be adjusted (Tiny, Small, Normal, or Large) to fit different layouts.

7. Inputs & Customization

7.1. Core Parameters (Bollinger and Z-Score)

- Bollinger Length and Standard Deviation define the spatial engine.

- Z-Score Lookback (All Factors) defines how many bars are used to normalize volume and delta.

7.2. Deep Kinetic Thresholds

- Extreme Threshold defines what is considered climactic (D1 or D8).

- Significant Threshold distinguishes strong initiative vs. weak or fakeout behavior.

- Neutral Threshold is the band within which delta is treated as neutral.

These thresholds allow you to tune the sensitivity of the kinetic classification to fit different timeframes or instruments.

7.3. Calculation Method (Volume Delta)

Geometry (Approx)

- Fast, non-repainting approach based on candle geometry.

- Suitable for most users and real-time decision-making.

Intrabar (Precise)

- Uses lower-timeframe data for more precise volume delta estimation.

- Intrabar mode can repaint and requires compatible data and plan support on the platform.

- Best used for post-analysis or research, not blind automation.

7.4. Visuals and Interface

- Toggle Bollinger Bands visibility on or off.

- Switch between Dark and Light color themes.

- Configure dashboard visibility, matrix heatmap display, position, and size.

8. Multi-Language Semantic Engine (Asia and Middle East Focus)

BDMA v7.0 includes a fully integrated multi-language layer, targeting a wide geographic user base.

Supported Languages:

English, Türkçe, Русский, 简体中文, हिन्दी, العربية, فارسی, עברית

All dashboard labels, regime titles, bias descriptions, and signal texts are dynamically translated via an internal dictionary, while semantic meaning is kept consistent across languages.

This makes BDMA suitable for multi-language communities, study groups, and educational content across different regions.

However, due to the heavy computational load of the Deep Kinetic Engine and TradingView’s strict Pine Script execution limits, it was not possible to expand support to additional languages. Adding more translation layers would significantly increase memory usage and exceed runtime constraints. For this reason, the current language set represents the maximum optimized configuration achievable without compromising performance or stability.

9. Practical Usage Notes

BDMA is most powerful when used as a contextual overlay on top of market structure (HH, HL, LH, LL), higher-timeframe trend, key levels, and your own execution framework.

Recommended usage:

- Identify the current regime (Status and Bias).

- Check whether price location (S-State) and kinetic behavior (D-State) agree with your trade idea.

- Be especially cautious in climactic and absorption or conflict zones, where volatility and risk can be elevated.

Avoid treating BDMA as an automatic green equals buy, red equals sell tool.

The real edge comes from understanding where you are in the volatility or kinetic spectrum, not from forcing signals out of the matrix.

10. Limitations & Important Warnings

BDMA does not predict the future.

It organizes current and recent data into a structured context.

Volume data quality depends on the underlying symbol, exchange, and broker feed.

Forex, crypto, indices, and stocks may all behave differently.

Intrabar mode can repaint and is sensitive to lower-timeframe data availability and your plan type.

Use it with extra caution and primarily for research.

No indicator can remove the need for clear trading rules, disciplined risk management, and psychological control.

11. Disclaimer

This script is provided strictly for educational and analytical purposes.

It is not a trading system, signal service, financial product, or investment advice.

Nothing in this indicator or its description should be interpreted as a recommendation to buy or sell any asset.

Past behavior of any indicator or market pattern does not guarantee future results.

Trading and investing involve significant risk, including the risk of losing more than your initial capital in leveraged products.

You are solely responsible for your own decisions, risk management, and results.

By using this script, you acknowledge that you understand these risks and agree that the author or authors and publisher or publishers are not liable for any loss or damage arising from its use.

SCOTTGO - Day Trade Stock Quote V4This Pine Script indicator, titled "SCOTTGO - Day Trade Stock Quote V4," is a comprehensive, customizable dashboard designed for active traders. It acts as a single, centralized reference point, displaying essential financial and technical data directly on your chart in a compact table overlay.

📊 Key Information Provided

The indicator is split into sections, aggregating various critical data points to provide a holistic picture of the stock's current state and momentum:

1. Ownership & Short Flow

This section provides fundamental context and short-interest data:

Market Cap, Shares Float, and Shares Outstanding: Key figures on the company's size and publicly tradable shares.

Short Volume %: Indicates the percentage of trading activity driven by short sellers.

Daily Change %: Shows the day's price movement relative to the previous close.

2. Price & Volatility

This tracks historical and immediate price levels:

Previous Close, Day High/Low: Key daily reference prices.

52-Week High/Low: Important long-term boundaries.

Earnings Date: A crucial fundamental date (currently displayed as a placeholder).

3. Momentum & Volume

These metrics are essential for understanding intraday buying and selling pressure:

Volume & Average Volume: The current trade volume compared to its historical average.

Relative Volume (RVOL): Measures how much volume is currently trading compared to the average rate for that time period (shown for both Daily and 5-Minute rates).

Volume Buzz (%): A percentage representation of how much current volume exceeds or falls below the average.

ADR % & ATR %: Measures of volatility.

RSI, U/D Ratio, and P/E Ratio: Momentum and valuation indicators.

4. Context

This provides background information on the security:

Includes the Symbol, Exchange, Industry, and Sector (note: some fields use placeholder data as this information is not always available via Pine Script).

⚙️ Customization

The dashboard is highly customizable via the indicator settings:

You can control the visibility of every single metric using the Section toggles.

You can change the position (Top Left, Top Right, etc.), size, and colors of the entire table.

In summary, this script is a powerful tool for day traders who need to monitor a large number of fundamental, technical, and volatility metrics simultaneously without cluttering the main chart area.

LJ Parsons Adjustable expanding MRT Fibpapers.ssrn.com

Market Resonance Theory (MRT) reinterprets financial markets as structured multiplicative, recursive systems rather than linear, dollar-based constructs. By mapping price growth as a logarithmic lattice of intervals, MRT identifies the deep structural cycles underlying long-term market behaviour. The model draws inspiration from the proportional relationships found in musical resonance, specifically the equal temperament system, revealing that markets expand through recurring octaves of compounded growth. This framework reframes volatility, not as noise, but as part of a larger self-organising structure.

Algo ۞ Halo 7MAs WonderA complete trend following and important MA crossing tool.

The indicator is self-explanatory. You decide where you want the triggers to go.

Enjoy!