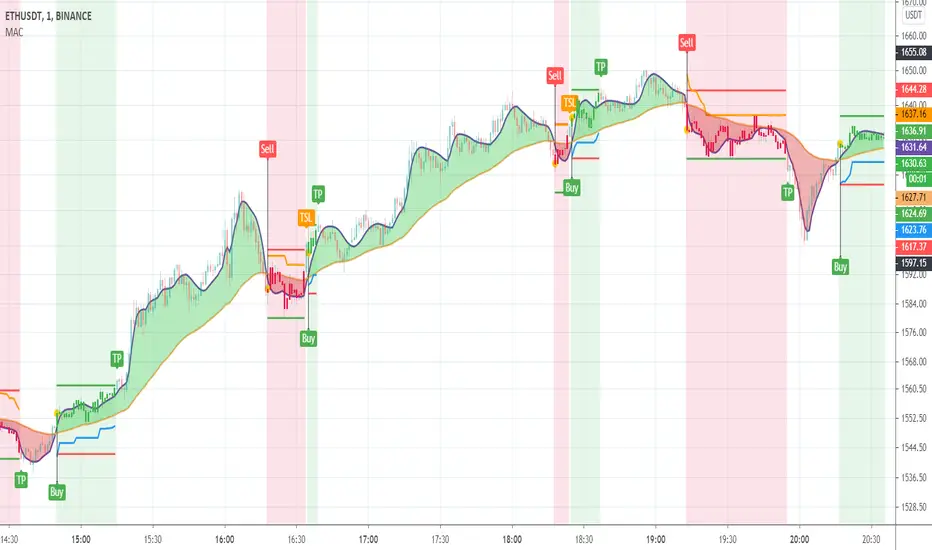

Ghosty's Modded Super Bandpass Filter [DasanC]Very cool Indicator from Ehlers and published originally by @DasanC

I made minor modifications, and added a zero line and changed some values. I use this indicator differently then it is intended to be used for scalping shorter time frames (15 min - 1 hour).

I use it like a cross over, either from the zeroline or when it passes the RMS, for 5-10 pips. While no indicator is 100% this one does a nice job for small scalps.

try it out on a demo and see if you like it.

enjoy.

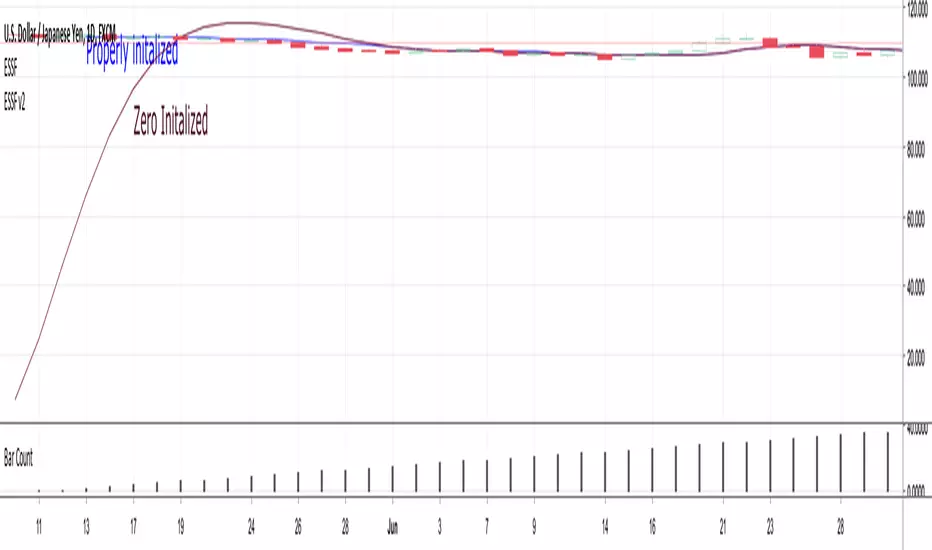

original Indy -

Indicador Pine Script®