1H/3m Concept [RunRox]🕘 1H/3m Concept is a versatile trading methodology based on liquidity sweeps from fractal points identified on higher timeframes, followed by price reversals at these key moments.

Below, I will explain this concept in detail and provide clear examples demonstrating its practical application.

⁉️ WHAT IS A FRACTALS?

In trading, a fractal is a technical analysis pattern composed of five consecutive candles, typically highlighting local market turning points. Specifically, a fractal high is formed when a candle’s high is higher than the highs of the two candles on either side, whereas a fractal low occurs when a candle’s low is lower than the lows of the two adjacent candles on both sides.

Traders use fractals as reference points for identifying significant support and resistance levels, potential reversal areas, and liquidity zones within price action analysis. Below is a screenshot illustrating clearly formed fractals on the chart.

📌 ABOUT THE CONCEPT

The 1H/3m Concept involves marking Higher Timeframe (HTF) fractals directly onto a Lower Timeframe (LTF) chart. When a liquidity sweep occurs at an HTF fractal level, we remain on the same LTF chart (since all HTF fractals are already plotted on this lower timeframe) and wait for a clear Market Structure Shift (MSS) to identify our potential entry point.

Below is a schematic illustration clearly demonstrating how this concept works in practice.

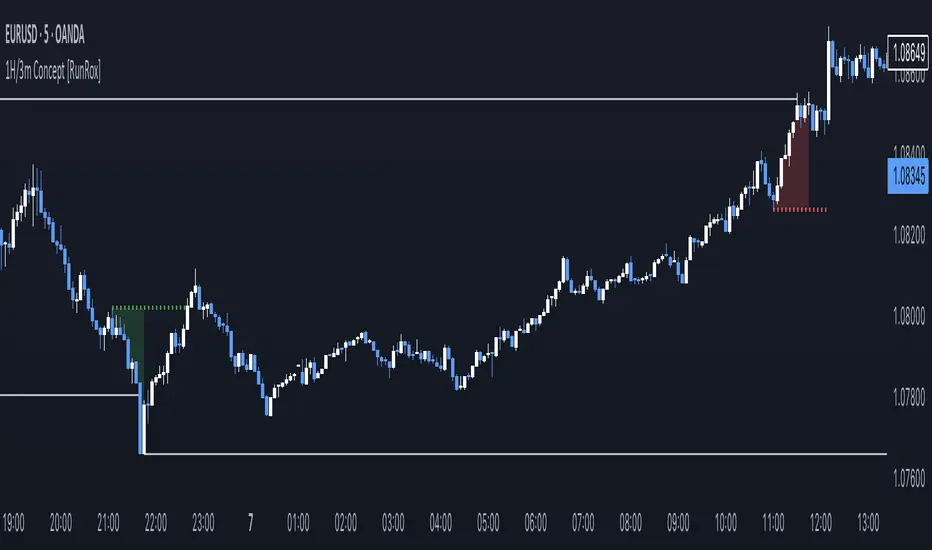

Below is another 💡 real-chart example , showing liquidity in the form of a 1H fractal, swept by a rapid impulse move. Immediately afterward, a clear Market Structure Shift (MSS) occurs, signaling a potential entry point into the trade.

Another example is shown below, where we see our hourly fractal, from which price clearly reacts, providing an opportunity to search for an entry point.

As illustrated on the chart, the fractal levels from the higher timeframe are clearly displayed, but we’re working directly on the 5-minute chart. This allows us to remain on one timeframe without needing to switch back and forth between charts to spot such trading setups.

🔍 MTF FRACTALS

This concept can be applied across various HTF-LTF timeframe combinations. Although our examples illustrate 1H fractals used on a 5-minute chart, you can effectively utilize many other timeframe combinations, such as:

30m HTF fractals on 1m chart

1H HTF fractals on 3m chart

4H HTF fractals on 15m chart

1D HTF fractals on 1H chart

The key idea behind this concept is always the same: identify liquidity at fractal levels on the higher timeframe (HTF), then wait for a clear Market Structure Shift (MSS) on the lower timeframe (LTF) to enter trades.

⚙️ SETTINGS

🔷 Trade Direction – Select the preferred trading direction (Long, Short, or Both).

🔷 HTF – Choose the higher timeframe from which fractals will be displayed on the current chart.

🔷 HTF Period – Number of candles required on both sides of a fractal candle (before and after) to confirm fractal formation on the HTF.

🔷 Current TF Period – Sensitivity to the impulse that sweeps liquidity, used for identifying and forming the MSS line.

🔷 Show HTF – Enable or disable displaying HTF fractal lines on your chart. You can also customize line style and color.

🔷 Max Age (Bars) – Number of recent bars within which fractals from the selected HTF will be displayed.

🔷 Show Entry – Enable or disable displaying the MSS line on the chart.

🔷 Enable Alert – Activates TradingView alerts whenever the MSS line is crossed.

You can also enable 🔔 alerts, which notify you whenever price crosses the MSS line. This significantly simplifies the process of identifying these setups on your charts. Simply configure your preferred timeframes and wait for notifications when the MSS line is crossed.

🔶 We greatly appreciate your feedback and suggestions for improving the indicator!

Indicador Pine Script®