Ciclos

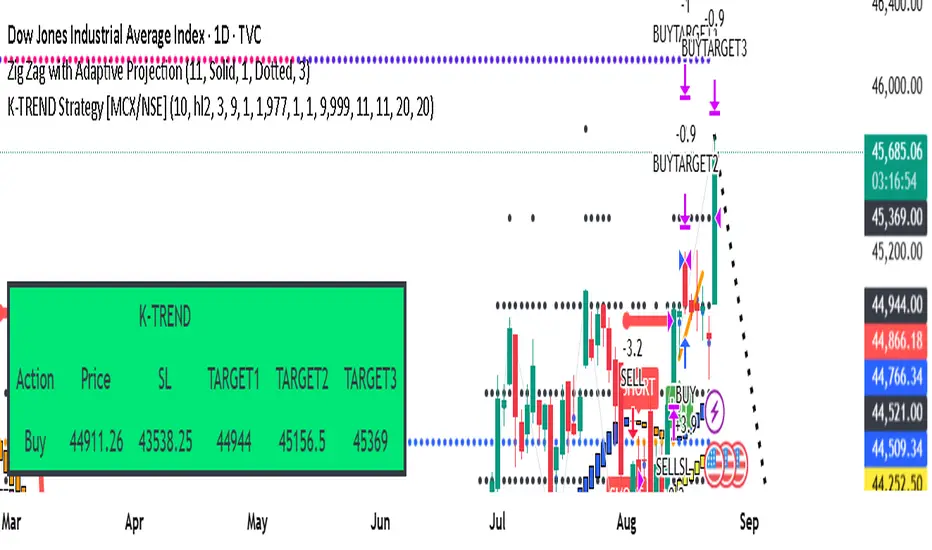

K-TREND Strategy k trend is very useful and high profitablility , it gives entry signals with buy/sell entry signalwith stoploss and targets

Adaptive MVRV & RSI Strategy V6 (Dynamic Thresholds)Strategy Explanation

This is an advanced Dollar-Cost Averaging (DCA) strategy for Bitcoin that aims to adapt to long-term market cycles and changing volatility. Instead of relying on fixed buy/sell signals, it uses a dynamic, weighted approach based on a combination of on-chain data and classic momentum.

Core Components:

Dual-Indicator Signal: The strategy combines two powerful indicators for a more robust signal:

MVRV Ratio: An on-chain metric to identify when Bitcoin is fundamentally over or undervalued relative to its historical cost basis.

Weekly RSI: A classic momentum indicator to gauge long-term market strength and identify overbought/oversold conditions.

Dynamic, Self-Adjusting Thresholds: The core innovation of this strategy is that it avoids fixed thresholds (e.g., "sell when RSI is 70"). Instead, the buy and sell zones are dynamically calculated based on a long-term (2-year) moving average and standard deviation of each indicator. This allows the strategy to automatically adapt to Bitcoin's decreasing volatility and changing market structure over time.

Weighted DCA (Scaling In & Out): The strategy doesn't just buy or sell a fixed amount. The size of its trades is scaled based on conviction:

Buying: As the MVRV and RSI fall deeper into their "undervalued" zones, the percentage of available cash used for each purchase increases.

Selling: As the indicators rise further into "overvalued" territory, the percentage of the current position sold also increases.

This creates an adaptive system that systematically accumulates during periods of fear and distributes during periods of euphoria, with the intensity of its actions directly tied to the extremity of market conditions.

Auction Market Theory: Value Area & VWAP Fade - DashboardAn "Auction Market Theory" dashboard is a visual summary of the market's state according to the principles of Auction Market Theory. It consolidates key metrics like the Value Area (VA), Point of Control (POC), and Volume-Weighted Average Price (VWAP) into a single, easy-to-read panel on your chart.

What a Dashboard Shows

The purpose of the dashboard is to give traders a quick, real-time snapshot of the market's auction process. It helps you answer critical questions like:

Where is the market's "fair value"? This is shown by the Value Area (VA) range.

Where is the most volume concentrated? This is the Point of Control (POC), the price that acts as a gravitational center.

How are market participants currently positioned? The VWAP provides a measure of the average price paid, weighted by volume. Price trading above VWAP suggests a bullish volume bias, while price below suggests a bearish bias.

Is the market in a state of balance or imbalance? The relationship between the current price and these key levels helps to quickly determine if the market is accepting a price range (balance) or rejecting it (imbalance/trend).

How to Interpret the Dashboard

Value Area (VA) & Point of Control (POC)

These metrics are derived from a volume profile and are the foundation of the auction theory dashboard. The dashboard displays the VA's low and high, as well as the POC. These levels define the market's "accepted" price range for a given period.

VWAP

VWAP acts as a real-time moving average that is more responsive to volume than a standard moving average. It's often used as an intraday anchor. When price is significantly stretched from the VWAP (and its standard deviation bands), it's a signal of a potential over-extension and a target for a mean-reversion trade.

Dashboard's Role in Trading

The dashboard is not an entry signal itself, but a contextual tool. It provides the framework for your trading decisions. For a "fade the edge" strategy, you would use the dashboard to:

Identify the edges: See the exact price levels of the VA and VWAP bands.

Wait for the stretch: Look for price to move beyond those edges.

Confirm the reversal: Only then would you look at other indicators (like RSI or volume spikes) for an entry signal.

Manage the trade: Use the POC as a potential take-profit target, as price has a high probability of returning to this point of volume consensus.

Adaptive ATR Guardian [自适应 ATR 守护者]自适应ATR守护者 | Adaptive ATR Guardian

——多品种智能交易防护策略 | Multi-Asset Intelligent Trading Protection Strategy

核心功能 | Core Features

1. 自动识别交易品种| Automatic Asset Detection

• 智能识别BTC/USD、XAU/USD等品种

• Auto-detects assets (e.g., BTC/USD, XAU/USD)

• 动态调整参数:ATR倍数、止盈止损比例

• Dynamic parameter tuning (ATR multipliers, TP/SL ratios)

2. 自适应ATR风控 | Adaptive ATR Risk Control

• 基于真实波动率(ATR)动态计算止盈止损

• TP/SL levels adjust with ATR volatility

• 参数自动优化:BTC(3xTP/1.5xSL) ,黄金(2xTP/1xSL)

• Auto-optimized: BTC (3xTP/1.5xSL), Gold (2xTP/1xSL)

3. 实时动态跟踪 | Real-Time Tracking

• 持仓期间止盈止损线实时更新

• Live TP/SL line updates during trades

• 可视化提示:绿色止盈线、红色止损线

• Visual cues: Green TP line, Red SL line

4. 趋势跟随逻辑 | Trend-Following Logic

• 双均线交叉(9MA & 21MA)触发信号

• Dual MA crossover (9MA & 21MA) for entries

• 金叉做多 / 死叉做空

• Long on Golden Cross, Short on Death Cross

5. 专业可视化界面 | Professional Visualization

• 图表标签显示关键参数

• On-chart label shows settings

• 自适应K线范围展示所有标记

• Auto-adjusts plot ranges for clarity

xauusd:Only suitable for 1 minute, short-term tradingxauusd

:Only suitable for 1 minute, short-term trading

Volume Spike Strategy by CzechroninThis strategy uses VOlume spikes to enter big trades

~

Czechronin

Breakout asia USD/CHF1 — Customizable Parameters

sess1 & sess2: The two time ranges that define the Asian session (e.g., 20:00–23:59 and 00:00–08:00).

Important: format is HHMM-HHMM.

rr: The risk/reward ratio (default = 3.0, meaning TP = 3× risk size).

onePerSess: Toggle to allow only one trade per Asian session or multiple.

bufTicks: Extra margin for the SL beyond the signal candle.

2 — Detecting the Asian Session

The script checks if the candle’s time is inside the first range (sess1) or inside the second range (sess2).

While inside the Asian session, it updates the current high and low.

When the session ends, it locks in these levels as rangeHigh and rangeLow.

3 — Step 1: Detecting the Initial Breakout

Bullish breakout → close above rangeHigh → flag breakoutUp is set to true.

Bearish breakout → close below rangeLow → flag breakoutDown is set to true.

No trade yet — this is just the breakout signal.

4 — Step 2: Waiting for the Retest

If a bullish breakout occurred, wait for the price to return to or slightly below rangeHigh and then close back above it.

If a bearish breakout occurred, wait for the price to return to or slightly above rangeLow and then close back below it.

5 — Entry & Exit

When the retest is confirmed:

strategy.entry() is triggered.

SL = behind the retest confirmation candle (with optional bufTicks margin).

TP = entry price ± RR × risk size.

If onePerSess is enabled, no further trades happen until the next Asian session.

6 — Chart Display

Green line = locked Asian session high.

Red line = locked Asian session low.

Light blue background = active Asian session hours.

Trade entries are shown on the chart when retests occur.

Recovery Zone Hedging [Starbots]Recovery Zone Hedging Strategy — Advanced Adaptive Hedge Recovery System

This strategy introduces an innovative zone-based hedge recovery approach tailored to TradingView’s single-direction trading model. Designed for serious traders and professionals, it combines multiple technical indicators with dynamic position sizing and adaptive take-profit mechanisms to manage drawdowns and maximize recovery efficiency.

How Recovery Zones Are Calculated

The strategy defines recovery zones as a configurable percentage distance from the last executed trade price. This percentage can be adjusted to suit different market volatility environments — wider zones for volatile assets, tighter zones for stable ones. When price moves into a recovery zone against the open position, the strategy places a hedge trade in the opposite direction to help recoup losses.

Dynamic Take-Profit Calculation

Take-profit targets are not fixed. Instead, they increase dynamically based on any accumulated losses from previous hedge trades. For example, if your initial target is 2%, but you have a $5 loss from prior hedges, the next take-profit target adjusts upward to cover both the loss and your profit goal, ensuring the entire hedge sequence closes in net profit.

Originality & Value

Unlike traditional hedging or recovery scripts that rely on static stop losses and fixed trade sizing, this strategy offers:

- Dynamic Hedge Entry Zones: Uses configurable percentage-based recovery zones that adapt to price volatility, allowing precise placement of hedge trades at meaningful reversal levels.

- Multi-Indicator Signal Fusion: Integrates MACD and Directional Movement Index (DMI) signals to confirm trade entries, improving signal accuracy and reducing false triggers.

- Exponential Position Sizing: Each hedge trade’s size grows exponentially using a customizable multiplier, accelerating loss recovery while carefully balancing capital usage.

- Adaptive Take-Profit Logic: The take-profit target adjusts dynamically based on accumulated losses and profit margins, ensuring that the entire hedge sequence closes with a net gain.

- Capital Usage Monitoring: A built-in dashboard tracks real-time equity consumption, preventing over-leveraging by highlighting critical capital thresholds.

- Fail-Safe Exit Mechanism: An optional forced exit beyond the last hedge zone protects capital in extreme market scenarios.

This strategy’s layered design and adaptive mechanisms provide a unique and powerful tool for traders seeking robust recovery systems beyond standard hedge or martingale methods.

How Components Work Together

- Entry Signals: The script listens for MACD line crossovers and DMI directional crosses to open an initial trade.

- Recovery Zones: If the market moves against the initial position, the strategy calculates a recovery zone a set percentage away and places a hedge trade in the opposite direction.

- Position Scaling: Each subsequent hedge trade increases in size exponentially according to the hedge multiplier, designed to recover all previous losses plus a profit.

- Take-Profit Target: Rather than a fixed target, the TP level is dynamically calculated considering current drawdown and desired profit margin, ensuring the entire hedge sequence closes profitably.

- Cycle Management: Trades alternate direction following the recovery zones until profit is realized or a maximum hedge count is reached. If needed, a forced stop-out limits risk exposure.

Key Benefits for Professional Traders

- Enhanced Risk Management: Real-time capital usage visualization helps maintain safe exposure levels.

- Strategic Hedge Recovery: The adaptive recovery zones and exponential sizing accelerate loss recoupment more efficiently than traditional fixed-step systems.

- Multi-Indicator Confirmation: Combining MACD and DMI reduces false signals and improves hedge timing accuracy.

- Versatility: Suitable for multiple timeframes and asset classes with adjustable parameters.

- Comprehensive Visuals: On-chart recovery zones, hedge levels, dynamic take-profits, and equity usage tables enable informed decision-making.

Recommended Settings & Use Cases

- Initial Position Size: 0.1–1% of account equity

- Recovery Zone Distance: 2–5% price movement

- Hedge Multiplier: 1.5–1.85x growth per hedge step

- Max Hedge Steps: 5–10 for controlled risk exposure

Ideal for trending markets where price retracements create viable recovery opportunities. Use caution in sideways markets to avoid extended hedge sequences.

Important Notes

- TradingView’s single-direction model means hedging is simulated via alternating trades.

- Position sizes grow rapidly—proper parameter tuning is essential to avoid over-leveraging.

This script is designed primarily for professional traders seeking an advanced, automated hedge recovery framework, offering superior capital efficiency and loss management.

Nova Futures PRO (SAFE v6) — HTF + Choppiness + CooldownNova Futures PRO (SAFE v6) — HTF + Choppiness + Cooldown

Estrategia de NY ORB por CPThis strategy marks the New York market opening range during the first 15 minutes and confirms a buy or sell entry once the price returns and retests that range. It’s designed to capture trades of 60 points or more after the range has been retested. I suggest complementing the strategy with an indicator that highlights FVGs (Fair Value Gaps) or order blocks to better understand what price is doing and where it’s heading.

esta estrategia te marca el rango de apertura del mercado de ny de los primeros 15 minutos y te confirma entrada en venta o compra una vez que el precio regrese y retestee el rango. esta diseñada para tener trades de 60 puntos o mas una vez que el rango sea retesteado. sugiero acompañar la estrategia con algun indicador que marque fvg o order blocks para tener una mejor de lo que el precio esta haciendo y hacia donde se dirige.

CP Strat ORBnew york opening range breakout and retest allows you to enter a trade with a better clarity if the price comes back and retest the range

ETH/SOL 1D Dynamic Trend Core - STRATEGY v 45Overview

The Dynamic Trend Core is a sophisticated, multi-layer trading engine designed to identify high-probability, trend-following opportunities. Its core philosophy is rooted in confluence, meaning it requires multiple conditions across trend, momentum, and volume to align before generating a signal. This approach aims to filter out market noise and provide a clearer view of the underlying trend.

The script includes a comprehensive backtesting engine for strategy optimization and a rich, intuitive visual interface for real-time analysis.

How It Works: Core Logic

The engine validates signals through several sequential layers:

Primary Trend Analysis (SAMA): The foundation is a Self-Adjusting Moving Average (SAMA) that dynamically determines the primary market direction (Bullish, Bearish, or Consolidation).

Momentum Confirmation: Signals are then qualified using a blend of the Natural Market Slope and a Cyclic RSI to ensure momentum is firmly aligned with the established trend.

Advanced Filtering Suite: A suite of optional filters provides robust confirmation and allows for deep customization:

Volume & ADX: Confirms that trades are supported by sufficient market participation and trend strength.

Market Regime: Gauges broad market health (e.g., using TOTAL market cap) to avoid trading against the entire market.

Multi-Timeframe (MTF) Analysis: Aligns signals with the dominant trend on a higher timeframe (e.g., Weekly).

BTC Cycle Analysis: Positions trades within the context of historical Bitcoin cycles using models like the Halving Cycle or Mayer Multiple.

On-Chart Visuals & Features

The script provides full transparency into its logic with a powerful on-chart interface.

IMPORTANT: For the live visual elements to function correctly, you must enable "Recalculate on every tick" in the script's settings (Settings > Properties).

Power Core Gauge: Located at the bottom-center of the chart, this gauge is the heart of the system. It displays the number of filter conditions currently met (e.g., 5/6) and "powers up" by glowing brighter as more conditions align, indicating a fully confirmed signal is ready.

Live Conditions Panel: This panel in the bottom-right corner acts as a real-time pre-flight checklist. It shows the status (pass/fail) of every individual filter, so you know exactly why a signal is, or is not, being generated.

Energized Trendline: The primary SAMA trendline changes color and intensity based on the strength and direction of the trend, offering immediate visual context.

BTC Halving Cycle Visualizer: Provides a background color guide to the different phases of the Bitcoin halving cycle for macro context.

How to Use & Configure

Select Operation Mode:

Backtest Mode: Use this to test different settings on historical data and find optimal configurations for a specific asset and timeframe.

Alerts-Only Mode: Use this for live trading to generate alert signals without cluttering the chart with backtest data. (Contact publisher for access to this version)

Configure Your Filters:

Start with the default filter settings.

If a potential setup is missed, check the Live Conditions Panel to see which specific filter blocked the signal.

Enable, disable, or adjust filters in the script's settings to match your trading style and the asset's characteristics.

Manage Your Risk:

Go to the "Risk & Exit" settings to configure your Stop Loss and Take Profit parameters to match your personal risk tolerance.

Disclaimer: This script is for educational and informational purposes only. It is not financial advice. All trading involves risk, and past performance is not indicative of future results. Please conduct your own research and backtesting before making any trading decisions.

MNQ Gap-Fade (ETH) — RTH 08:30–15:00 CT, +/-3m refsStrategy overview

This strategy tests a gap-fade idea on MNQ when trading an ETH chart but referencing RTH timing. It measures the overnight move from 3 minutes before the prior RTH close (14:57 CT) to 3 minutes after today’s RTH open (08:33 CT). If that gap is big enough, it bets on mean reversion at the open:

Short after a large gap up

Long after a large gap down

How it works

Sampling windows (RTH, Chicago time):

Prev close sample: the 14:57 bar (3 min before 15:00 close)

Open sample: the 08:33 bar (3 min after 08:30 open)

These offsets help avoid opening/closing bar noise and ensure the bars have formed.

Overnight % move:

(OpenSample−PrevCloseSample)/PrevCloseSample × 100

Signals (at 08:33 pulse):

If gap % ≥ Gap-Up threshold → enter SHORT

If gap % ≤ −Gap-Down threshold → enter LONG

Risk management:

Per-trade TP and SL as percentages from entry (both adjustable)

If still in a position at 14:57, the strategy forces flat (closes all) before the RTH close

Plots & visibility:

Plots the computed Overnight Gap % line

Horizontal lines at your Gap-Up and Gap-Down thresholds for quick visual checks

Alerts:

alertcondition() events fire on:

the open-sample ready pulse,

gap-up short, and gap-down long conditions

(Pine requires static alert messages; the % gap itself is visible on the chart.)

Inputs you can adjust

Times (CT): RTH open/close and the ±3 min offsets (use different values if desired)

Gap thresholds (%): separate values for gap-up (short) and gap-down (long)

Take-profit / Stop-loss (%): per-side percentage targets from average entry price

Instrument & session notes

Designed for MNQ; works on an ETH chart while internally referencing CME/Chicago (CT) RTH times via 1-minute sampling.

If you prefer different markets or exact ET timestamps, change the time inputs accordingly.

Assumptions & limitations

This is a research/backtest tool for a simple gap-fade rule, not a complete trading system.

Slippage, fills, and overnight liquidity may differ from backtest assumptions.

Mean reversion can fail on trend days and during news events; use filters or wider thresholds if needed.

That should be everything reviewers and users need to understand what it does and how to tune it. Want me to add a short “Suggested defaults” block (e.g., 0.75–1.25% gaps, 1% TP/SL) or a “Known gotchas” section for ETH vs. RTH charts?

Ask ChatGPT

ORB 15m – First 15min Breakout (Long/Short)ORB 15m – First 15min Breakout (Long/Short)

Apply on SPY, great returns

MomentumSync-PSAR: RSI·ADX Filtered 3-Tier Exit StrategyTriSAR-E3 is a precision swing trading strategy designed to capitalize on early trend reversals using a Triple Confirmation Model. It triggers entries based on an early Parabolic SAR bullish flip, supported by RSI strength and ADX trend confirmation, ensuring momentum-backed participation.

Exits are tactically managed through a 3-step staged exit after a PSAR bearish reversal is detected, allowing gradual profit booking and downside protection.

This balanced approach captures trend moves early while intelligently scaling out, making it suitable for directional traders seeking both agility and control.

Martin Strategy - No Loss Exit v3Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0

Parabolic SAR with Early Buy & MA-Based Exit Strategy📝 Strategy Description (Max SEO Impact)

This advanced Parabolic SAR-based trading strategy is designed to capture early trend reversals and exit intelligently using a dynamic moving average filter. It enters long trades when a PSAR reversal occurs, and exits only when the PSAR moves above price and the price falls below the 11-period SMA, helping avoid premature exits during volatile swings.

📌 Features:

• Custom Parabolic SAR calculation for refined trend tracking

• Background highlights during buy zones (SAR below price)

• Exit signals only when trend weakens (PSAR above + price under SMA)

• Red flag plotted on chart at exit bars for clear visual identification

• Works on all timeframes and instruments

Ideal for swing traders, trend followers, and strategy testers looking for smart PSAR-based entries with smoother exits.

Parabolic SAR with Early Buy & MA-Based Exit Strategy📝 Strategy Description (Max SEO Impact)

This advanced Parabolic SAR-based trading strategy is designed to capture early trend reversals and exit intelligently using a dynamic moving average filter. It enters long trades when a PSAR reversal occurs, and exits only when the PSAR moves above price and the price falls below the 11-period SMA, helping avoid premature exits during volatile swings.

📌 Features:

• Custom Parabolic SAR calculation for refined trend tracking

• Background highlights during buy zones (SAR below price)

• Exit signals only when trend weakens (PSAR above + price under SMA)

• Red flag plotted on chart at exit bars for clear visual identification

• Works on all timeframes and instruments

Ideal for swing traders, trend followers, and strategy testers looking for smart PSAR-based entries with smoother exits.

Parabolic SAR Strategy with MACD Confirmation & Trend Zone Highl📝 Description (SEO + Follower-Friendly):

🚀 Powerful Trend Strategy Using Parabolic SAR + MACD

This advanced Pine Script combines the classic Parabolic SAR trend-following system with MACD crossover confirmation, improving entry precision and filtering out false signals. The script also features:

✅ Dynamic trend zone background highlighting when SAR is below price

✅ MACD filter ensures trades align with market momentum

✅ Custom SAR logic with adaptive acceleration

✅ Clean visual SAR plots for easy trend tracking

✅ Fully backtestable with strategy.entry logic

🔎 Ideal for traders seeking early trend entries, momentum confirmation, and visual clarity.

📈 Works on all timeframes and pairs — perfect for swing traders, scalpers, and crypto enthusiasts.

💡 Use it as a base strategy or combine with your favorite indicators.

❤️ If you find this helpful, don't forget to like, comment, and follow for more premium strategies!