Market Cap Landscape 3DHello, traders and creators! 👋

Market Cap Landscape 3D. This project is more than just a typical technical analysis tool; it's an exploration into what's possible when code meets artistry on the financial charts. It's a demonstration of how we can transcend flat, two-dimensional lines and step into a vibrant, three-dimensional world of data.

This project continues a journey that began with a previous 3D experiment, the T-Virus Sentiment, which you can explore here:

The Market Cap Landscape 3D builds on that foundation, visualizing market data—particularly crypto market caps—as a dynamic 3D mountain range. The entire landscape is procedurally generated and rendered in real-time using the powerful drawing capabilities of polyline.new() and line.new() , pushed to their creative limits.

This work is intended as a guide and a design example for all developers, born from the spirit of learning and a deep love for understanding the Pine Script™ language.

---

🧐 Core Concept: How It Works

The indicator synthesizes multiple layers of information into a single, cohesive 3D scene:

The Surface: The mountain range itself is a procedurally generated 3D mesh. Its peaks and valleys create a rich, textured landscape that serves as the canvas for our data.

Crypto Data Integration: The core feature is its ability to fetch market cap data for a list of cryptocurrencies you provide. It then sorts them in descending order and strategically places them onto the 3D surface.

The Summit: The highest point on the mountain is reserved for the asset with the #1 market cap in your list, visually represented by a flag and a custom emblem.

The Mountain Labels: The other assets are distributed across the mountainside, with their rank determining their general elevation. This creates an intuitive visual hierarchy.

The Leaderboard Pole: For clarity, a dedicated pole in the back-right corner provides a clean, ranked list of the symbols and their market caps, ensuring the data is always easy to read.

---

🧐 Example of adjusting the view

To evoke the feeling of flying over mountains

To evoke the feeling of looking at a mountain peak on a low plain

🧐 Example of predefined colors

---

🚀 How to Use

Getting started with the Market Cap Landscape 3D:

Add to Chart: Apply the "Market Cap Landscape 3D" indicator to your active chart.

Open Settings: Double-click anywhere on the 3D landscape or click the "Settings" icon next to the indicator's name.

Customize Your Crypto List: The most important setting is in the Crypto Data tab. In the "Symbols" text area, enter a comma-separated list of the crypto tickers you want to visualize (e.g., BTC,ETH,SOL,XRP ). The indicator supports up to 40 unique symbols.

> Important Note: This indicator exclusively uses TradingView's `CRYPTOCAP` data source. To find valid symbols, use the main symbol search bar on your chart. Type `CRYPTOCAP:` (including the colon) and you will see a list of available options. For example, typing `CRYPTOCAP:BTC` will confirm that `BTC` is a valid ticker for the indicator's settings. Using symbols that do not exist in the `CRYPTOCAP` index will result in a script error. or, to display other symbols, simply type CRYPTOCAP: (including the colon) and you will see a list of available options.

Adjust Your View: Use the settings in the Camera & Projection tab to rotate ( Yaw ), tilt ( Pitch ), and scale the landscape until you find a view you love.

Explore & Customize: Play with the color palettes, flag design, and other settings to make the landscape truly your own!

---

⚙️ Settings & Customization

This indicator is highly customizable. Here’s a breakdown of what each setting does:

#### 🪙 Crypto Data

Symbols: Enter the crypto tickers you want to track, separated by commas. The script automatically handles duplicates and case-insensitivity.

Show Market Cap on Mountain: When checked, it displays the full market cap value next to the symbol on the mountain. When unchecked, it shows a cleaner look with just the symbol and a colored circle background.

#### 📷 Camera & Projection

Yaw (°): Rotates the camera view horizontally (side to side).

Pitch (°): Tilts the camera view vertically (up and down).

Scale X, Y, Z: Stretches or compresses the landscape in width, depth, and height, respectively. Fine-tune these to get the perfect perspective.

#### 🏞️ Grid / Surface

Grid X/Y resolution: Controls the detail level of the 3D mesh. Higher values create a smoother surface but may use more resources.

Fill surface strips: Toggles the beautiful color gradient on the surface.

Show wireframe lines: Toggles the visibility of the grid lines.

Show nodes (markers): Toggles the small dots at each grid intersection point.

#### 🏔️ Peaks / Mountains

Fill peaks volume: Draws vertical lines on high peaks, giving them a sense of volume.

Fill peaks surface: Draws a cross-hatch pattern on the surface of high peaks.

Peak height threshold: Defines the minimum height for a peak to receive the fill effect.

Peak fill color/density: Customizes the appearance of the fill lines.

#### 🚩 Flags (3D)

Show Flag on Summit: A master switch to show or hide the flag and emblem entirely.

Flag height, width, etc.: Provides full control over the dimensions and orientation of the flag on the highest peak.

#### 🎨 Color Palette

Base Gradient Palette: Choose from 13 stunning, pre-designed color themes for the landscape, from the classic SUNSET_WAVE to vibrant themes like NEON_DREAM and OCEANIC .

#### 🛡️ Emblem / Badge Controls

This section gives you granular control over every element of the custom emblem on the flag. Tweak rotation, offsets, and scale to design your unique logo.

---

👨💻 Developer's Corner: Modifying the Core Logic

If you're a developer and wish to customize the indicator's core data source, this section is for you. The script is designed to be modular, making it easy to change what data is being ranked and visualized.

The heart of the data retrieval and ranking logic is within the f_getSortedCryptoData() function. Here’s how you can modify it:

1. Changing the Data Source (from Market Cap to something else):

The current logic uses request.security("CRYPTOCAP:" + syms.get(i), ...) to fetch market capitalization data. To change this, you need to modify this line.

Example: Ranking by RSI (14) on the Daily timeframe.

First, you'll need a function to calculate RSI. Add this function to the script:

f_getRSI(symbol, timeframe, length) =>

request.security(symbol, timeframe, ta.rsi(close, length))

Then, inside f_getSortedCryptoData() , find the `for` loop that populates the `caps` array and replace the `request.security` call:

// OLD LINE:

// caps.set(i, request.security("CRYPTOCAP:" + syms.get(i), timeframe.period, close))

// NEW LINE for RSI:

// Note: You'll need to decide how to format the symbol name (e.g., "BINANCE:" + syms.get(i) + "USDT")

caps.set(i, f_getRSI("BINANCE:" + syms.get(i) + "USDT", "D", 14))

2. Changing the Data Formatting:

The ranking values are formatted for display using the f_fmtCap() function, which currently formats large numbers into "M" (millions), "B" (billions), etc.

If you change the data source to something like RSI, you'll want to change the formatting. You can modify f_fmtCap() or create a new formatting function.

Example: Formatting for RSI.

// Modify f_fmtCap or create f_fmtRSI

f_fmtRSI(float v) =>

str.tostring(v, "#.##") // Simply format to two decimal places

Remember to update the calls to this function in the main drawing loop where the labels are created (e.g., str.format("{0}: {1}", crypto.symbol, f_fmtCap(crypto.cap)) ).

By modifying these key functions ( f_getSortedCryptoData and f_fmtCap ), you can adapt the Market Cap Landscape 3D to visualize and rank almost any dataset you can imagine, from technical indicators to fundamental data.

---

We hope you enjoy using the Market Cap Landscape 3D as much as we enjoyed creating it. Happy charting! ✨

Ciclos

Adaptive Rolling Quantile Bands [CHE] Adaptive Rolling Quantile Bands

Part 1 — Mathematics and Algorithmic Design

Purpose. The indicator estimates distribution‐aware price levels from a rolling window and turns them into dynamic “buy” and “sell” bands. It can work on raw price or on *residuals* around a baseline to better isolate deviations from trend. Optionally, the percentile parameter $q$ adapts to volatility via ATR so the bands widen in turbulent regimes and tighten in calm ones. A compact, latched state machine converts these statistical levels into high-quality discretionary signals.

Data pipeline.

1. Choose a source (default `close`; MTF optional via `request.security`).

2. Optionally compute a baseline (`SMA` or `EMA`) of length $L$.

3. Build the *working series*: raw price if residual mode is off; otherwise price minus baseline (if a baseline exists).

4. Maintain a FIFO buffer of the last $N$ values (window length). All quantiles are computed on this buffer.

5. Map the resulting levels back to price space if residual mode is on (i.e., add back the baseline).

6. Smooth levels with a short EMA for readability.

Rolling quantiles.

Given the buffer $X_{t-N+1..t}$ and a percentile $q\in $, the indicator sorts a copy of the buffer ascending and linearly interpolates between adjacent ranks to estimate:

* Buy band $\approx Q(q)$

* Sell band $\approx Q(1-q)$

* Median $Q(0.5)$, plus optional deciles $Q(0.10)$ and $Q(0.90)$

Quantiles are robust to outliers relative to means. The estimator uses only data up to the current bar’s value in the buffer; there is no look-ahead.

Residual transform (optional).

In residual mode, quantiles are computed on $X^{res}_t = \text{price}_t - \text{baseline}_t$. This centers the distribution and often yields more stationary tails. After computing $Q(\cdot)$ on residuals, levels are transformed back to price space by adding the baseline. If `Baseline = None`, residual mode simply falls back to raw price.

Volatility-adaptive percentile.

Let $\text{ATR}_{14}(t)$ be current ATR and $\overline{\text{ATR}}_{100}(t)$ its long SMA. Define a volatility ratio $r = \text{ATR}_{14}/\overline{\text{ATR}}_{100}$. The effective quantile is:

Smoothing.

Each level is optionally smoothed by an EMA of length $k$ for cleaner visuals. This smoothing does not change the underlying quantile logic; it only stabilizes plots and signals.

Latched state machines.

Two three-step processes convert levels into “latched” signals that only fire after confirmation and then reset:

* BUY latch:

(1) HLC3 crosses above the median →

(2) the median is rising →

(3) HLC3 prints above the upper (orange) band → BUY latched.

* SELL latch:

(1) HLC3 crosses below the median →

(2) the median is falling →

(3) HLC3 prints below the lower (teal) band → SELL latched.

Labels are drawn on the latch bar, with a FIFO cap to limit clutter. Alerts are available for both the simple band interactions and the latched events. Use “Once per bar close” to avoid intrabar churn.

MTF behavior and repainting.

MTF sourcing uses `lookahead_off`. Quantiles and baselines are computed from completed data only; however, any *intrabar* cross conditions naturally stabilize at close. As with all real-time indicators, values can update during a live bar; prefer bar-close alerts for reliability.

Complexity and parameters.

Each bar sorts a copy of the $N$-length window (practical $N$ values keep this inexpensive). Typical choices: $N=50$–$100$, $q_0=0.15$–$0.25$, $k=2$–$5$, baseline length $L=20$ (if used), adaptation strength $s=0.2$–$0.7$.

Part 2 — Practical Use for Discretionary/Active Traders

What the bands mean in practice.

The teal “buy” band marks the lower tail of the recent distribution; the orange “sell” band marks the upper tail. The median is your dynamic equilibrium. In residual mode, these tails are deviations around trend; in raw mode they are absolute price percentiles. When ATR adaptation is on, tails breathe with regime shifts.

Two core playbooks.

1. Mean-reversion around a stable median.

* Context: The median is flat or gently sloped; band width is relatively tight; instrument is ranging.

* Entry (long): Look for price to probe or close below the buy band and then reclaim it, especially after HLC3 recrosses the median and the median turns up.

* Stops: Place beyond the most recent swing low or $1.0–1.5\times$ ATR(14) below entry.

* Targets: First scale at the median; optional second scale near the opposite band. Trail with the median or an ATR stop.

* Symmetry: Mirror the rules for shorts near the sell band when the median is flat to down.

2. Continuation with latched confirmations.

* Context: A developing trend where you want fewer but cleaner signals.

* Entry (long): Take the latched BUY (3-step confirmation) on close, or on the next bar if you require bar-close validation.

* Invalidation: A close back below the median (or below the lower band in strong trends) negates momentum.

* Exits: Trail under the median for conservative exits or under the teal band for trend-following exits. Consider scaling at structure (prior swing highs) or at a fixed $R$ multiple.

Parameter guidance by timeframe.

* Scalping / LTF (1–5m): $N=30$–$60$, $q_0=0.20$, $k=2$–3, residual mode on, baseline EMA $L=20$, adaptation $s=0.5$–0.7 to handle micro-vol spikes. Expect more signals; rely on latched logic to filter noise.

* Intraday swing (15–60m): $N=60$–$100$, $q_0=0.15$–0.20, $k=3$–4. Residual mode helps but is optional if the instrument trends cleanly. $s=0.3$–0.6.

* Swing / HTF (4H–D): $N=80$–$150$, $q_0=0.10$–0.18, $k=3$–5. Consider `SMA` baseline for smoother residuals and moderate adaptation $s=0.2$–0.4.

Baseline choice.

Use EMA for responsiveness (fast trend shifts) and SMA for stability (smoother residuals). Turning residual mode on is advantageous when price exhibits persistent drift; turning it off is useful when you explicitly want absolute bands.

How to time entries.

Prefer bar-close validation for both band recaptures and latched signals. If you must act intrabar, accept that crosses can “un-cross” before close; compensate with tighter stops or reduced size.

Risk management.

Position size to a fixed fractional risk per trade (e.g., 0.5–1.0% of equity). Define invalidation using structure (swing points) plus ATR. Avoid chasing when distance to the opposite band is small; reward-to-risk degrades rapidly once you are deep inside the distribution.

Combos and filters.

* Pair with a higher-timeframe median slope as a regime filter (trade only in the direction of the HTF median).

* Use band width relative to ATR as a range/trend gauge: unusually narrow bands suggest compression (mean-reversion bias); expanding bands suggest breakout potential (favor latched continuation).

* Volume or session filters (e.g., avoid illiquid hours) can materially improve execution.

Alerts for discretion.

Enable “Cross above Buy Level” / “Cross below Sell Level” for early notices and “Latched BUY/SELL” for conviction entries. Set alerts to “Once per bar close” to avoid noise.

Common pitfalls.

Do not interpret band touches as automatic signals; context matters. A strong trend will often ride the far band (“band walking”) and punish counter-trend fades—use the median slope and latched logic to separate trend from range. Do not oversmooth levels; you will lag breaks. Do not set $q$ too small or too large; extremes reduce statistical meaning and practical distance for stops.

A concise checklist.

1. Is the median flat (range) or sloped (trend)?

2. Is band width expanding or contracting vs ATR?

3. Are we near the tail level aligned with the intended trade?

4. For continuation: did the 3 steps for a latched signal complete?

5. Do stops and targets produce acceptable $R$ (≥1.5–2.0)?

6. Are you trading during liquid hours for the instrument?

Summary. ARQB provides statistically grounded, regime-aware bands and a disciplined, latched confirmation engine. Use the bands as objective context, the median as your equilibrium line, ATR adaptation to stay calibrated across regimes, and the latched logic to time higher-quality discretionary entries.

Disclaimer

No indicator guarantees profits. Adaptive Rolling Quantile Bands is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Best regards

Chervolino

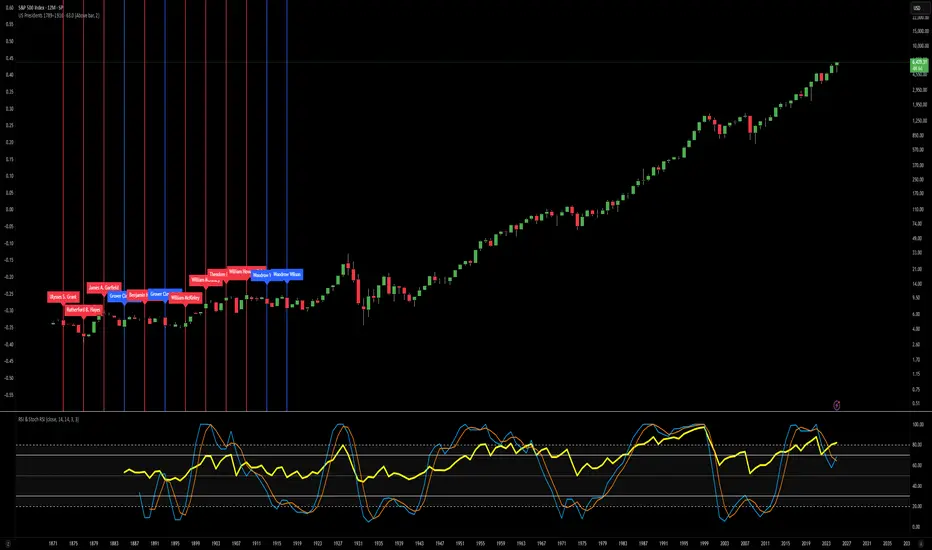

US Presidents 1789–1916Description:

This indicator displays all U.S. presidential elections from 1789 to 1916 on your chart.

Features:

Vertical lines at the date of each presidential election.

Line color by party:

Red = Republican

Blue = Democrat

Gray = Other/None

Labels showing the name of each president.

Historical flag style: All presidents before 1900 are considered historical, providing visual distinction.

Fully overlayed on the price chart for timeline context.

Customizable: Label position (above/below bar) and line width.

Use case: Great for studying historical market behavior around elections or for general reference of U.S. presidents during the early history of the country.

US Presidents 1920–2024Description:

This indicator displays all U.S. presidential elections from 1920 to 2024 on your chart.

Features:

Vertical lines at the date of each presidential election.

Line color by party:

Red = Republican

Blue = Democrat

Gray = Other/None

Labels showing the name of each president.

Modern flag style: Presidents from 1900 onward are highlighted as modern, giving clear historical separation.

Fully overlayed on the price chart for timeline context.

Customizable: Label position (above/below bar) and line width.

Use case: Useful for analyzing modern U.S. presidential cycles, market reactions to elections, or quickly referencing recent presidents directly on charts.

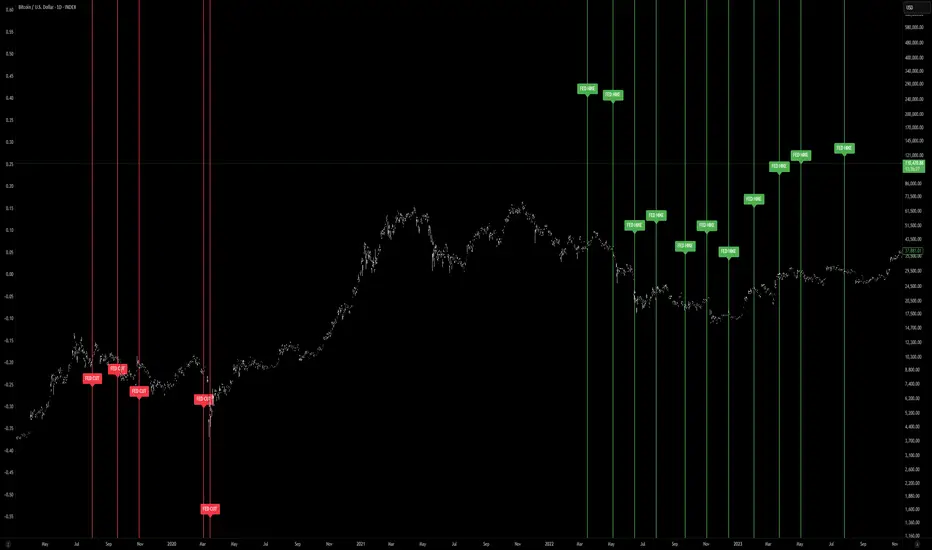

FED Rate Decisions (Cuts & Hikes)This indicator highlights key moments in U.S. monetary policy by plotting vertical lines on the chart for Federal Reserve interest rate decisions.

Features:

Rate Cuts (red): Marks dates when the Fed reduced interest rates.

Rate Hikes (green): Marks dates when the Fed increased interest rates.

Configurable view: Choose between showing all historical decisions or only those from 2019 onwards.

Labels: Each event is tagged with “FED CUT” or “FED HIKE” above or below the bar (adjustable).

Alerts: You can set TradingView alerts to be notified when the chart reaches a Fed decision day.

🔧 Inputs:

Show decisions: Switch between All or 2019+ events.

Show rate cuts / hikes: Toggle visibility separately.

Colors: Customize line and label colors.

Label position: Place labels above or below the bar.

📈 Usage:

This tool helps traders and investors visualize how Fed policy shifts align with market movements. Rate cuts often signal economic easing, while hikes suggest tightening monetary policy. By overlaying these events on price charts, you can analyze historical reactions and prepare for similar scenarios.

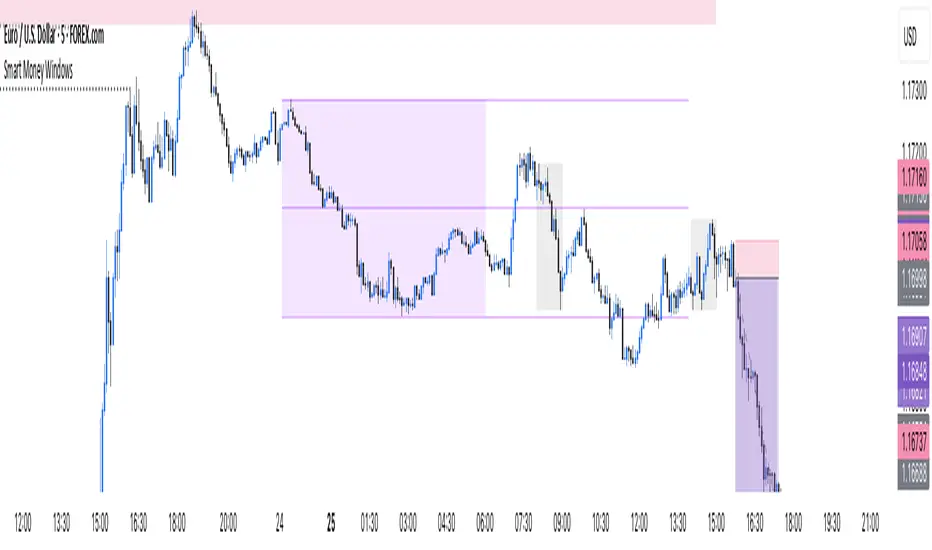

Smart Money Windows- X7Smart Money Windows 📊💰

Unlock the secret moves of the big players! This indicator highlights key liquidity traps, smart money zones, and market kill zones for the Asian, London, and New York sessions. See where the pros hide their orders and spot potential price flips before they happen! 🚀🔥

Features:

Visual session boxes with high/low/mid levels 🟪🟫

NY session shifted 60 mins for precise timing 🕒

Perfect for spotting traps, inducements & smart money maneuvers 🎯

Works on Forex, crypto, and stocks 💹

Get in the “Smart Money Window” and trade like the pros! 💸🔑

By HH

Smart Money Windows- X7Smart Money Windows 📊💰

Unlock the secret moves of the big players! This indicator highlights key liquidity traps, smart money zones, and market kill zones for the Asian, London, and New York sessions. See where the pros hide their orders and spot potential price flips before they happen! 🚀🔥

Features:

Visual session boxes with high/low/mid levels 🟪🟫

NY session shifted 60 mins for precise timing 🕒

Perfect for spotting traps, inducements & smart money maneuvers 🎯

Works on Forex, crypto, and stocks 💹

Get in the “Smart Money Window” and trade like the pros! 💸🔑

By HH

EdgeFlow Pullback [CHE]EdgeFlow Pullback \ — Icon & Visual Guide (Deep Dive)

TL;DR (1-minute read)

⏳ Hourglass = Pending verdict. A countdown runs from the signal bar until your Evaluation Window ends.

✔ Checkmark (green) = OK. After the evaluation window, price (HLC3) is on the correct side of the EMA144 for that signal’s direction.

✖ Cross (red) = Fail. After the evaluation window, price (HLC3) is on the wrong side of the EMA144.

▲ / ▼ Triangles = the actual PB Long/Short signal bar (sequence completed in time).

Small lime/red crosses = visual markers when HLC3 crosses EMA144 (context, not trade signals).

Orange line = EMA144 (baseline/trend filter).

T3 line color = Context signal: green when T3 is below HLC3, red when T3 is above HLC3.

Icon Glossary (What each symbol means)

1) ⏳ Hourglass — “Pending / Countdown”

Appears immediately when a PB signal fires (Long or Short).

Shows `⏳ currentBars / EvaluationBars` (e.g., `⏳ 7/30`).

The label stays anchored at the signal bar and its original price level (it does not drift with price).

During ⏳ you get no verdict yet. It’s simply the waiting period before grading.

2) ✔ Checkmark (green) — “Condition met”

Appears after the Evaluation Window completes.

Logic:

Long signal: HLC3 (typical price) is above EMA144 → ✔

Short signal: HLC3 is below EMA144 → ✔

The label turns green and text says “✔ … Condition met”.

This is rules-based grading, not PnL. It tells you if the post-signal structure behaved as expected.

3) ✖ Cross (red) — “Condition failed”

Appears after the Evaluation Window completes if the condition above is not met.

Label turns red with “✖ … Condition failed”.

Again: rules-based verdict, not a guarantee of profit or loss.

4) ▲ “PB Long” triangle (below bar)

Marks the exact bar where the 4-step Long sequence completed within the allowed window.

That bar is your signal bar for Long setups.

5) ▼ “PB Short” triangle (above bar, red)

Same as above, for Short setups.

6) Lime/Red “+” crosses (tiny cross markers)

Lime cross (below bar): HLC3 crosses above EMA144 (crossover).

Red cross (above bar): HLC3 crosses below EMA144 (crossunder).

These crosses are context markers; they’re not entry signals by themselves.

The Two Clocks (Don’t mix them up)

There are two different time windows at play:

1. Signal Window — “Max bars for full sequence”

A pullback signal (Long or Short) only fires if the 4-step sequence completes within this many bars.

If it takes too long: reset (no signal, no triangle, no label).

Purpose: avoid stale setups.

2. Evaluation Window — “Evaluation window after signal (bars)”

Starts after the signal bar. The label shows an ⏳ countdown.

When it reaches the set number of bars, the indicator checks whether HLC3 is on the correct side of EMA144 for the signal direction.

Then it stamps the signal with ✔ (OK) or ✖ (Fail).

Timeline sketch (Long example):

```

→ ▲ PB Long at bar t0

Label shows: ⏳ 0/EvalBars

t0+1, t0+2, ... t0+EvalBars-1 → still ⏳

At t0+EvalBars → Check HLC3 vs EMA144

Result → ✔ (green) or ✖ (red)

(Label remains anchored at t0 / signal price)

```

What Triggers the PB Signal (so you know why triangles appear)

LONG sequence (4 steps in order):

1. T3 falling (the pullback begins)

2. HLC3 crosses under EMA144

3. T3 rising (pullback ends)

4. HLC3 crosses over EMA144 → PB Long triangle

SHORT sequence (mirror):

1. T3 rising

2. HLC3 crosses over EMA144

3. T3 falling

4. HLC3 crosses under EMA144 → PB Short triangle

If steps 1→4 don’t complete in time (within Max bars for full sequence), the sequence is abandoned (no signal).

Lines & Colors (quick interpretation)

EMA144 (orange): your baseline trend filter.

T3 (green/red):

Green when T3 < HLC3 (price above the smoothed path; often supportive in up-moves)

Red when T3 > HLC3 (price below the smoothed path; often pressure in down-moves)

HLC3 (gray): the typical price the logic uses ( (H+L+C)/3 ).

Label Behavior (anchoring & cleanup)

Each signal creates one label at the signal bar with ⏳.

The label is position-locked: it stays at the same bar index and y-price it was born at.

After the evaluation check, the label text and color update to ✔/✖, but position stays fixed.

The indicator keeps only the last N labels (your “Show only the last N labels” input). Older ones are deleted to reduce clutter.

What You Can (and Can’t) Infer from ✔ / ✖

✔ OK: Structure behaved as intended during the evaluation window (HLC3 finished on the correct side of EMA144).

Inference: The pullback continued in the expected direction post-signal.

✖ Fail: Structure ended up opposite the expectation.

Inference: The pullback did not continue cleanly (chop, reversal, or insufficient follow-through).

> Important: ✔/✖ is not profit or loss. It’s an objective rule check. Use it to identify market regimes where your entries perform best.

Input Settings — How they change the visuals

T3 length:

Shorter → faster turns, more signals (and more noise).

Longer → smoother turns, fewer but cleaner sequences.

T3 volume factor (0–1, default 0.7):

Higher → more curvature/smoothing.

Typical sweet spot: 0.5–0.9.

EMA length (baseline) default 144:

Smaller → faster baseline, more cross events, more aggressive signals.

Larger → slower, stricter trend confirmation.

Max bars for full sequence (signal window):

Smaller → only fresh, snappy pullbacks can signal.

Larger → allows slower pullbacks to complete.

Evaluation window (after signal):

Smaller → verdict arrives quickly (less tolerance).

Larger → gives the trade more time to prove itself structurally.

Show only the last N labels:

Controls chart clutter. Increase for more history, decrease for focus.

(FYI: The “Debug” toggle exists but doesn’t draw extra overlays in this version.)

Practical Reading Flow (how to use visuals in seconds)

1. Triangles catch your eye: ▲ for Long, ▼ for Short. That’s the setup completion.

2. ⏳ label starts—don’t judge yet; let the evaluation run.

3. Watch EMA slope and T3 color for context (trend + pressure).

4. After the window: ✔/✖ stamps the outcome. Log what the market was like when you got ✔.

Common “Why did…?” Questions

Q: Why did I get no triangle even though T3 turned and EMA crossed?

A: The 4 steps must happen in order and within the Signal Window. If timing breaks, the sequence resets.

Q: Why did my label stay ⏳ for so long?

A: That’s by design until the Evaluation Window completes. The verdict only happens at the end of that window.

Q: Why is ✔/✖ different from my PnL?

A: It’s a structure check, not a profit check. It doesn’t know your entries/exits/stops.

Q: Do the small lime/red crosses mean buy/sell?

A: No. They’re context markers for HLC3↔EMA crosses, useful inside the sequence but not standalone signals.

Pro Tips (turn visuals into decisions)

Entry: Use the ▲/▼ triangle as your trigger, in trend direction (check EMA slope/market structure).

Stop: Behind the pullback swing around the signal bar.

Exit: Structure levels, R-multiples, or a reverse HLC3↔EMA cross as a trailing logic.

Tuning:

Intraday/volatile: shorter T3/EMA + tighter Signal Window.

Swing/slow: default 144 EMA + moderate windows.

Learn quickly: Filter your chart to show only ✔ or only ✖ windows in your notes; see which sessions, assets, and volatility regimes suit the system.

Disclaimer

No indicator guarantees profits. Sweep2Trade Pro \ is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Happy trading

Chervolino

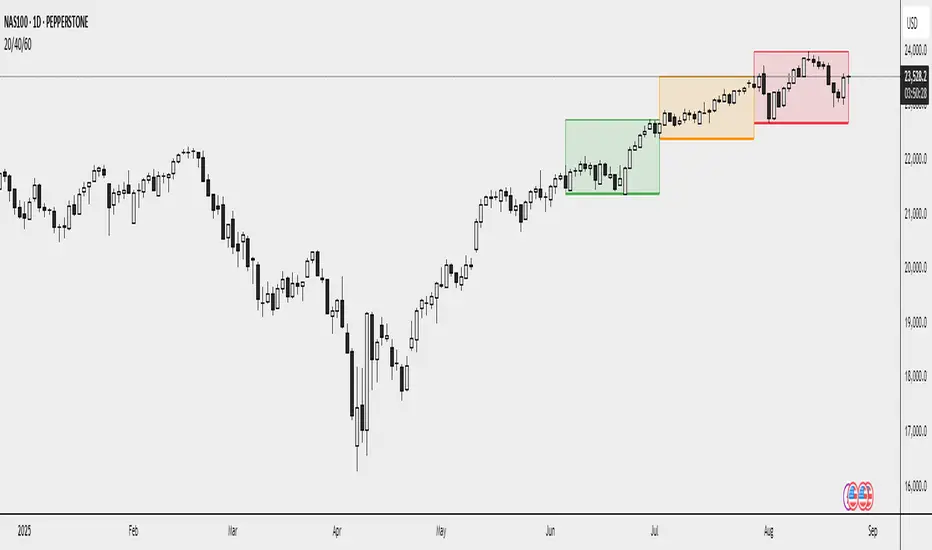

20/40/60Displays three consecutive, connected range boxes showing high/low price ranges for customizable periods. Boxes are positioned seamlessly with shared boundaries for continuous price action visualization.

Features

Three Connected Boxes: Red (most recent), Orange (middle), Green (earliest) periods

Customizable Positioning: Set range length and starting offset from current bar

Individual Styling: Custom colors, transparency, and border width for each box

Display Controls: Toggle borders, fills, and line visibility

Use Cases

Range Analysis: Compare volatility across time periods, spot breakouts

Support/Resistance: Use box boundaries as potential S/R levels

Market Structure: Visualize recent price development and trend patterns

Key Settings

Range Length: Bars per box (default: 20)

Starting Offset: Bars back from current to position boxes (default: 0)

Style Options: Colors, borders, and visibility controls for each box

Perfect for traders analyzing consecutive price ranges and comparing current conditions to recent historical periods.

BB Trading WindowsTrading Windows for Blue Belt Strategy. The windows are as follows:

1:00-02:59

13:00-15:59

22:00-22:59

All in NY timezone.

(LES/SES) Compliment Net Volume(LES/SES) Compliment Net Volume

(LES/SES) Compliment Net Volume is a volume-based confirmation tool designed to show whether buyers or sellers are truly in control behind the candles. It acts as a compliment to the Long Elite Squeeze (LES) and Short Elite Squeeze (SES) frameworks, giving traders a clearer view of momentum strength.

Note! {Short Elite Squeeze (SES) Will be released in the Future}

-Designed to take shorts opposite of the long trades from LES

🔹 Core Logic

Net Volume Calculation – Positive volume when price closes higher, negative when price closes lower.

Cumulative Smoothing – Uses a rolling SMA of cumulative differences to remove noise.

Color Coding –

Green → Buyer dominance

Red → Seller dominance

Gray → Neutral pressure

🔹 How to Use

Above zero (green) → Buyers dominate → supports long setups (LES).

Below zero (red) → Sellers dominate → supports short setups (SES).

Flat/gray → No clear pressure → signals caution or chop.

This makes it easier to confirm when market participation aligns with a potential entry or exit.

🔹 Credit

The Compliment Net Volume was developed by Hunter Hammond (Elite x FineFir) as part of the LES/SES system.

The concept builds on classic Net Volume and cumulative volume analysis principles shared by the TradingView community, but has been uniquely adapted into the LES/SES framework.

⚠️ Disclaimer: This is a framework tool, not financial advice. Use with proper risk management.

YoY Gain till current yearYoy gains that helps you build your data base. You can see all the gains from the past 20 years and thus helps you analyze the stock movement and expected gain over the period of time, com bine this information with market cap of the stock and you can know its future potential combined with current and past earnings analysis.

Long Elite Squeeze (LES) — H.H 22 Lindsay (AI)LES (Long Elite Squeeze)

LES (Long Elite Squeeze) is a trading framework designed to capture the highest-probability long setups. It’s not just another signal script — it’s a structured system built to filter noise, manage risk, and keep you aligned with real momentum.

🔹 Core Logic

Breakout Confirmation – Ensures moves have structure, not just random spikes.

Relative Volume (RVOL) – Confirms participation and fuel behind the move.

RSI Alignment – Avoids overextended traps and fakeouts.

Squeeze Momentum – The backbone of LES. Signals fire only after a defined squeeze pattern shift (6+ dark green bars followed by a light green bar).

🔹 Trade Management Built In

Automated Sell Signals – Trigger on either:

2 consecutive dark green bars on Squeeze Momentum

WaveTrend cross down

(only valid after a Buy signal — no random shorts)

HUD Entry Checklist – Live conditions shown on chart.

Status Tracker HUD – Flips between “Waiting for Entry” and “In Trade” for clear context.

🔹 Flexibility

3 switchable squeeze versions (V1, V2, V3) for different market conditions.

Customizable EMA & ATR settings (with color options).

Session-aware logic — filter signals to prime trading hours.

🔹 Blueprint & Credits

LES is a fusion of proven concepts, standing on the shoulders of respected creators:

-Squeeze Momentum – LazyBear

-WaveTrend Oscillator – LazyBear

-Relative Volume – LonesomeTheBlue

Breakout/structural logic – refined from classic frameworks

Their work laid the foundation — LES expands and integrates them into a complete trading system.

⚡ Why LES Stands Out

LES wasn’t coded overnight. It’s the result of countless hours of live testing, rebuilding, and refining. Every feature earned its place by proving value in real trading, not theory.

LES is more than an indicator. It’s a disciplined framework — crafted to turn chaos into structure, randomness into probability, and noise into clarity.

⚠️ Disclaimer: This is a trading framework, not financial advice. Performance depends on trader discipline, risk management, and market conditions.

Infinite EMA with Alpha Control♾️ Infinite EMA with Alpha Control

What Makes This EMA "Infinite"?

Unlike traditional EMA indicators that are limited to typical periods (1-5000), this Infinite EMA breaks all boundaries. You can create EMAs with periods of 1,000, 10,000, or even 1,000,000 bars - that's why it's called "infinite"! Also Infinite EMA starts working immediately from the very first bar on your chart

Why This EMA is "Infinite":

1. Mathematically: When N → ∞, alpha → 0, meaning infinitely long "memory"

2. Practically: You can set any period - even 100,000 bars

3. Flexibility: Alpha allows precise control over the "forgetting speed"

How Does It Work?

The magic lies in the Alpha parameter. While regular EMAs use fixed formulas, this indicator gives you direct control over the EMA's "memory" through Alpha values:

• High Alpha (0.1-0.2): Fast reaction, short memory

• Medium Alpha (0.01-0.05): Balanced response

• Low Alpha (0.0001-0.001): Extremely slow reaction, very long memory

• Ultra-low Alpha (0.000001): Almost frozen in time

The Mathematical Formula:

Alpha = 2 / (Period + 1)

This means you can achieve any EMA period by adjusting Alpha, giving you infinite flexibility!

Expanded "Infinite EMA" Table:

Period EMA (N) - Alpha (Rounded) - Alpha (Exact) - Description

10 - 0.1818 - 0.181818... - Fast EMA

20 - 0.0952 - 0.095238... - Short-term

50 - 0.0392 - 0.039215... - Medium-term

100 - 0.0198 - 0.019801... - Long-term

200 - 0.0100 - 0.009950... - Standard long-term

500 - 0.0040 - 0.003996... - Very long-term

1,000 - 0.0020 - 0.001998... - Super long-term

2,000 - 0.0010 - 0.000999... - Ultra long-term

5,000 - 0.0004 - 0.000399... - Mega long-term

10,000 - 0.0002 - 0.000199... - Giga long-term

25,000 - 0.00008 - 0.000079... - Century-scale EMA

50,000 - 0.00004 - 0.000039... - Practically motionless

100,000 - 0.00002 - 0.000019... - "Glacial" EMA

500,000 - 0.000004 - 0.000003... - Geological timescale

1,000,000 - 0.000002 - 0.000001... - Approaching constant

5,000,000 - 0.0000004 - 0.0000003... - Virtually static

10,000,000 - 0.0000002 - 0.0000001... - Nearly flat line

100,000,000 - 0.00000002 - 0.00000001... - Mathematical infinity

Formula: Alpha = 2/(N+1) where N is the EMA period

Key Features:

Dual EMA System: Run fast and slow EMAs simultaneously

Crossover Signals: Automatic buy/sell signals with customizable alerts

Alpha Control: Direct mathematical control over EMA behavior

Infinite Periods: From 1 to 100,000,000+ bars

Visual Customization: Colors, fills, backgrounds, signal sizes

Instant Start: Works accurately from the very first bar

Update Intervals: Control calculation frequency for noise reduction

Why Choose Infinite EMA?

1. Unlimited Flexibility: Any period you can imagine

2. Mathematical Precision: Direct alpha control for exact behavior

3. Professional Grade: Suitable for all trading styles

4. Easy to Use: Simple settings with powerful results

5. No Warm-up Period: Accurate values from bar #1

Simple Explanation:

Think of EMA as a "memory system":

• High Alpha = Short memory (forgets quickly, reacts fast)

• Low Alpha = Long memory (remembers everything, moves slowly)

With Infinite EMA, you can set the "memory length" to anything from seconds to centuries!

⚡ Instant Start Feature - EMA from First Bar

Immediate Calculation from Bar #1

Unlike traditional EMA indicators that require a "warm-up period" of N bars before showing accurate values, Infinite EMA starts working immediately from the very first bar on your chart.

How It Works:

Traditional EMA Problem:

• Standard 200-period EMA: Needs 200+ bars to become accurate

• First 200 bars: Shows incorrect/unstable values

• Result: Large portions of historical data are unusable

Infinite EMA Solution:

Bar #1: EMA = Current Price (perfect starting point)

Bar #2: EMA = Alpha × Price + (1-Alpha) × Previous EMA

Bar #3: EMA = Alpha × Price + (1-Alpha) × Previous EMA

...and so on

Key Benefits:

No Warm-up Period: Start trading signals from day one

Full Chart Coverage: Every bar has a valid EMA value

Historical Accuracy: Backtesting works on entire dataset

New Markets: Works perfectly on newly listed assets

Short Datasets: Effective even with limited historical data

Practical Impact:

Scenario Traditional EMA Infinite EMA

New cryptocurrency Unusable for first 200 days ✅ Works from day 1

Limited data (< 200 bars) Inaccurate values ✅ Fully functional

Backtesting Must skip first 200 bars ✅ Test entire history

Real-time trading Wait for stabilization ✅ Trade immediately

Technical Implementation:

if barstate.isfirst

EMA := currentPrice // Perfect initialization

else

EMA := alpha × currentPrice + (1-alpha) × previousEMA

This smart initialization ensures mathematical accuracy from the very first calculation, eliminating the traditional EMA "ramp-up" problem.

Why This Matters:

For Backesters: Use 100% of available data

For Live Trading: Get signals immediately on any timeframe

For Researchers: Analyze complete datasets without gaps

Bottom Line: Infinite EMA is ready to work the moment you add it to your chart - no waiting, no warm-up, no exceptions!

Unlike traditional EMAs that require a "warm-up period" of 200+ bars before showing accurate values, Infinite EMA starts working immediately from bar #1.

This breakthrough eliminates the common problem where the first portion of your chart shows unreliable EMA data. Whether you're analyzing a newly listed cryptocurrency, working with limited historical data, or backtesting strategies, every single bar provides mathematically accurate EMA values.

No more waiting periods, no more unusable data sections - just instant, reliable trend analysis from the moment you apply the indicator to any chart.

🔄 Update Interval Bars Feature

The Update Interval feature allows you to control how frequently the EMA recalculates, providing flexible noise filtering without changing the core mathematics.

Set to 1 for standard behavior (updates every bar), or increase to 5-10 for smoother signals that update less frequently. Higher intervals reduce market noise and false signals but introduce slightly more lag. This is particularly useful on volatile timeframes where you want the EMA's directional bias without every minor price fluctuation affecting the calculation.

Perfect for swing traders who prefer cleaner, more stable trend lines over hyper-responsive indicators.

Conclusion

The Infinite EMA transforms the traditional EMA from a fixed-period tool into a precision instrument with unlimited flexibility. By understanding the Alpha-Period relationship, traders can create custom EMAs that perfectly match their trading style, timeframe, and market conditions.

The "infinite" nature comes from the ability to set any period imaginable - from ultra-fast 2-bar EMAs to glacially slow 10-million-bar EMAs, all controlled through a single Alpha parameter.

________________________________________

Whether you're a beginner looking for simple trend following or a professional researcher analyzing century-long patterns, Infinite EMA adapts to your needs. The power of infinite periods is now in your hands! 🚀

Go forward to the horizon. When you reach it, a new one will open up.

- J. P. Morgan

ALTSEASON Monitor: Macro vs Crypto (normalized)ALTSEASON Monitor: Macro vs Crypto (normalized)

Set 1W or 1M timeframe for the macro picture.

If your provider does not have some symbols, change the tickers in the script settings (for example, ETHBTC from another exchange).

For detailed trading, keep this monitor on the second window and watch local entries on individual charts.

Mikula's Master 360° Square of 12Mikula’s Master 360° Square of 12

An educational W. D. Gann study indicator for price and time. Anchor a compact Square of 12 table to a start point you choose. Begin from a bar’s High or Low (or set a manual start price). From that anchor you can progress or regress the table to study how price steps through cycles in either direction.

What you’re looking at :

Zodiac rail (far left): the twelve signs.

Degree rail: 24 rows in 15° steps from 15° up to 360°/0°.

Transit rail and Natal rail: track one planet per rail. Each planet is placed at its current row (℞ shown when retrograde). As longitude advances, the planet climbs bottom → top, then wraps to the bottom at the next sign; during retrograde it steps downward.

Hover a planet’s cell to see a tooltip with its exact longitude and sign (e.g., 152.4° ♌︎). The linked price cell in the grid moves with the planet’s row so you can follow a planet’s path through the zodiac as a path through price.

Price grid (right): the 12×24 Square of 12. Each column is a cycle; cells are stepped price levels from your start price using your increment.

Bottom rail: shows the current square number and labels the twelve columns in that square.

How the square is read

The square always begins at the bottom left. Read each column bottom → top. At the top, return to the bottom of the next column and read up again. One square contains twelve cycles. Because the anchor can be a High or a Low, you can progress the table upward from the anchor or regress it downward while keeping the same bottom-to-top reading order.

Iterate Square (shifting)

Iterate Square shifts the entire 12×24 grid to the next set of twelve cycles.

Square 1 shows cycles 1–12; Square 2 shows 13–24; Square 3 shows 25–36, etc.

Visibility rules

Pivot cells are table-bound. If you shift the square beyond those prices, their highlights won’t appear in the table.

A/B levels and Transit/Natal planetary lines are chart overlays and can remain visible on the table as you shift the square.

Quick use

Choose an anchor (date/time + High/Low) or enable a manual start price .

Set the increment. If you anchored with a Low and want the table to step downward from there, use a negative value.

Optional: pick Transit and Natal planets (one per rail), toggle their plots, and hover their cells for longitude/sign.

Optional: turn on A/B levels to display repeating bands from the start price.

Optional: enable swing pivots to tint matching cells after the anchor.

Use Iterate Square to shift to later squares of twelve cycles.

Examples

These are exploratory examples to spark ideas:

Overview layout (zodiac & degree rails, Transit/Natal rails, price grid)

A-levels plotted, pivots tinted on the table, real-time price highlighted

Drawing angles from the anchor using price & time read from the table

Using a TradingView Gann box along the A-levels to study reactions

Attribution & originality

This script is an original implementation (no external code copied). Conceptual credit to Patrick Mikula, whose discussion of the Master 360° Square of 12 inspired this study’s presentation.

Further reading (neutral pointers)

Patrick Mikula, Gann’s Scientific Methods Unveiled, Vol. 2, “W. D. Gann’s Use of the Circle Chart.”

W. D. Gann’s Original Commodity Course (as provided by WDGAN.com).

No affiliation implied.

License CC BY-NC-SA 4.0 (non-commercial; please attribute @Javonnii and link the original).

Dependency AstroLib by @BarefootJoey

Disclaimer Educational use only; not financial advice.

Sessions [New_ProfitEfex]This script is use for displaying session in a very attractive an clarity way

You can give it a try for free

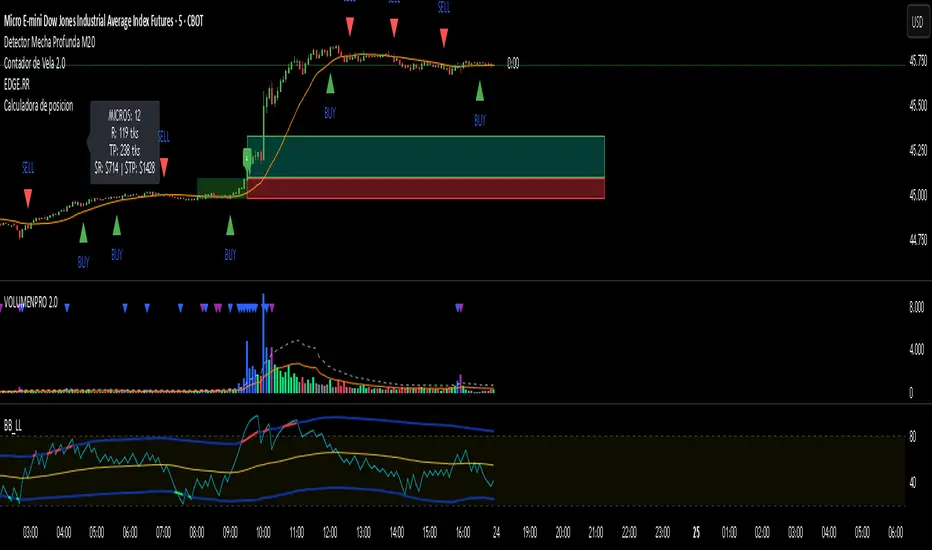

Calculadora de posicion)Position Size Calculator is a simple tool that helps traders instantly know how many contracts or lots to use based on their risk.

Just set your account size, risk percentage, and stop loss distance — the calculator does the rest.

Stay disciplined, control your risk, and trade with confidence.

BBCONLL(100)BBLL helps you quickly spot market extremes and potential turning points.

By combining the Relative Volatility Index with fixed Bollinger Bands, it gives a clear view of when momentum is stretched too far — making it easier to time entries, exits, or confirm trends.

Simple, visual, and effective for traders who want a sharper edge in decision-making.

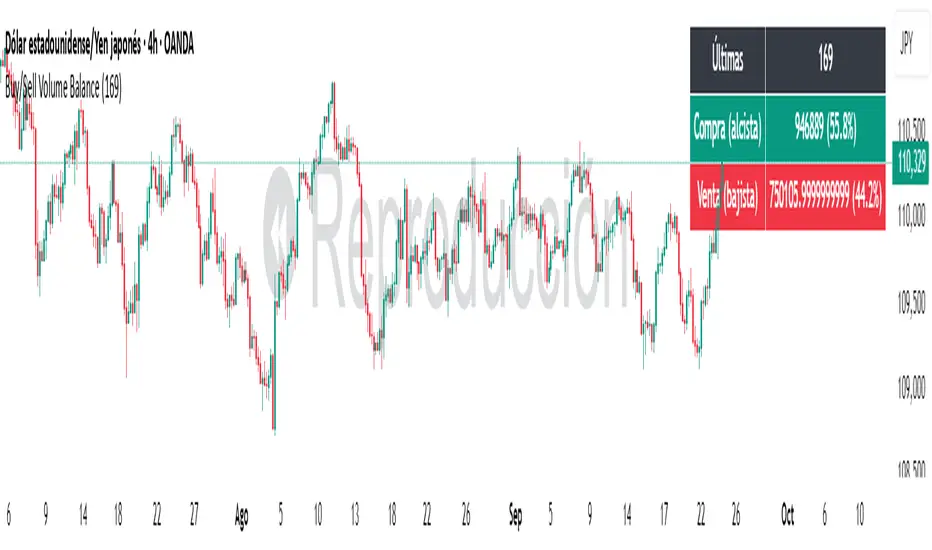

Buy/Sell Volume BalanceDESCRIPTION

Buy/Sell Volume Balance is a simple yet powerful indicator designed to measure and visualize the balance between buying and selling volume over a customizable number of recent candles. It helps traders quickly assess market pressure during consolidation phases or ranges, in order to anticipate the most likely breakout direction.

How it works

The indicator analyzes the last N candles (default = 100, user-editable).

Each candle’s total volume is classified as:

Bullish volume (Buy volume): if the candle closes above or equal to its open.

Bearish volume (Sell volume): if the candle closes below its open.

The volumes are summed separately to calculate:

Total Buy Volume

Total Sell Volume

The percentage of each side relative to the total is also displayed.

All results are shown in a fixed table at the top of the chart for quick interpretation.

Purpose

This tool is specifically designed to help traders evaluate the internal battle between buyers and sellers during a range or sideways market. By understanding which side is accumulating more volume within the range, traders can anticipate which direction is more likely when the price breaks out.

If Buy volume dominates → potential bullish breakout.

If Sell volume dominates → potential bearish breakout.

If both sides are nearly balanced, it signals indecision and a higher chance of false breakouts.

Imbalance Threshold

In practice, traders often consider a clear imbalance when one side reaches at least 55–60% of the total volume.

Above this threshold, the dominant side is more likely to dictate the breakout direction.

Below this threshold, the market is usually in indecision and further confirmation is needed before acting.

How to use it

Add the indicator to your chart and choose the lookback period (number of candles).

Focus on ranges or consolidation zones where price is moving sideways.

Observe the balance of Buy vs Sell volume in the top-right box:

A clear imbalance (>55–60%) suggests the stronger side is more likely to push the breakout.

A balanced ratio (<55–60%) indicates indecision and possible false breakouts.

Use it in combination with support/resistance zones, breakout patterns, or volume spikes for best results.

✅ In summary: This indicator does not give direct buy/sell signals, but it provides valuable context about market pressure, helping you to align your trades with the most probable breakout direction.