DC Breakout Strategy | This is simplicity at its finest.As the title already describes: this is a Donchian breakout strategy. This strategy, as of now, only goes long. It goes long when the price close makes a new high and the 8 day moving average is above the 32 day moving average. The strategy exits the trade if the price breaks the atr trailing stop of * 3 or the 8 day moving average crosses below the 32 day moving average.

This is simplicity at its finest.

ATR

UT Bot v5This is an update by request, on someone elses strategy! well more of an edit, but also update from pine v4 to pine v5.

//CREDITS to HPotter for the orginal code. The guy trying to sell this as his own is a scammer lol.

//Edited and converted to @version=5 by SeaSide420 for Paperina

The UT Bot v5 is Movinging average (the MA) vs ATR (the ATR is in the form intended for use as trailing stop loss (ATR_TSL))

Entry logic:

buy = the MA > ATR_TSL and Price > ATR_TSL

sell = the MA < ATR_TSL and Price < ATR_TSL

The Moving average type can be changed in the settings:

options = "SMA", "EMA", "WMA", "HMA"]

the edits i made were:

convert to v5

Add TP and SL

Add Buy only or Sell only option

Add MA type option

Add price source option

Draw MA and ATR_TSL on-chart

DI Crossing Daily Straregy HulkTradingSimple strategy based on crossing DI+ and DI- and Average True Range.

Long entry when DI+ crossover DI-

Short entry when DI+ crossunder DI-

Stop Loss and Take Profits based on Average True Range.

Default values are 1*ATR(14) for stop loss and 2*ATR(14) for Take Profit.

Risk reward 1 to 2 ratio.

Recommended default values, but you can change it if you want.

Recommended timeframe - 1D.

Script was tested on BTCUSDT pair and have a 2.4 profit factor.

Mean Reversion Strategy v2 [KL]Description :

This strategy will enter a position when the following conditions are met:

a) Main signal: When source data (ATR) diverts from its moving average value, and

b) Confirmation: If predicted direction of trend is favorable.

Assumptions :

During periods of high price volatility, ATR diverts from its moving average value. Eventually, ATR should revert. But since just knowing the magnitude of increase/decrease of ATR does not indicate a trend signal, we need to introduce a model to predict the current trend.

In short:

• Trend Prediction : This strategy calculates the expected logarithmic return of the security (the "Drift") and considers prices to be moving in uptrend if the drift curve is upward sloping.

• Assessment of ATR diversion : To determine "yes/no" regarding whether ATR at a given point in time has diverted, this script conducts a two-tailed hypothesis test at each candlestick period. The null hypothesis (H0) is that the fast moving average value should equal the slow moving average value (say, denoted as H0: atr14 == atr28; it is assumed that atr28 is more meaningful for the purpose of describing the current trend because it has a larger sample size). Investopedia has an article summarizing this topic .

Exit Condition :

When trailing stop loss hits.

Previous version :

This strategy is based on Version 1 published back in September . This older version considers +/- one standard deviation to be the critical values relative to average ATR when testing whether ATR has diverted from the mean. This does not take Standard Error ("SE") into account. As a result, the threshold is often too wide and it generates too many entry signals.

Simple Ema_ATR Strategy HulkTradingSimple EMA strategy, based on ema55+ema21 and ATR(Average True Range) and it enters a deal from ema55 when the other entry conditions are met

Basically long and short conditions

If long:

1) close must be less than open (because we are searching for a pullback)

2) emaFast(21) must be bigger than emaSlow(55) - for a trend detection

3) Difference between emaFast and emaSlow must be greater than ATR(14) - for excluding flat

For short conditions are opposite

Stop levels and take profits, based on ATR multiplier.

You can change it in input field.

I recommended values between 1 and 4, not more.

This strategy was tested on pairs BTCUSDT and ETHUSDT and have a nice results.

Av3Based on the ANNE EA v3 for MT4. For use on FOREX.

if ATR is greater than ATR average taken from last 5 candles, then market considered as trending, and so Open(0)>Close(1)=buy Open(0)Close(1)=sell Open(0)

Kifier's MFI/STOCH Hidden Divergence/Trend BeaterMFI/STOCH Hidden Divergence/Trend Beater

General Idea:

My premise around this strategy was to make a general strategy for crypto that would help out with finding entry positions for when you’re bullish on a crypto and want to hold on for a while, and at the same time avoiding massive drops. Essentially a way to mix long term/ swing trading; I somewhat achieved my goal however it still requires a lot of logic tuning of the trend averages.

I’m a huge proponent of volume indicators and coupled with average closing price, I think this gives a really good idea of what is happening with the market. It gives an idea on the market and retail investor sentiment. This generally gives you logical entry positions (Although I don’t know how amazing that will work with all cryptos, there’s a fine line between a good strategy and one that just rides bubble market conditions, some would argue that’s still a success and others not)

How it works:

There are many components to the strategy that try to do different things:

First of all there are two types of entries, a MFI hidden divergence with a STOCH check, essentially it will only fire when a divergence is detected while STOCH is above 50%, however this might be changed in the future as due to the volatile nature of cryptos, the STOCH is not too effective. The second entry is a simple MFI/STOCH trend, if STOCH is above 50% and the trend is detected to be in a trending long, once a MFI crossover over the 50% line is detected an entry is placed, this is designed to get out profit where the divergence would otherwise be less accurate during strongly trending conditions.

-MFI is a great indicator, as a volume weighted momentum indicator I find it the most accurate of all, the STOCH however is a great indicator to get a general picture of simple market conditions and can filter out the emotional noise of retail investors.

-VWMA and an SMA (The bottom oscillator) gives an idea of the trend tacking into account of the volume, this serves as a more short term filter of the trend for filters.

-OBV checks are done between the OBV and an EMA of the OBV, to get the idea of a volume weighted long trend, which is important for crypto as there are massive rallies to go up due to retail greed, it’s great to jump onto it at the beginning, and get off before the stack of cards fall apart.

-ATR is used to detect when the market is relatively just ranging or moving sideways, which is where the hidden divergence entries are done, during predictable and profitable market conditions.

- Stop loss is based on the closest support of the entry, this is a nice medium of room to breath but also an actual stop loss.

Future plans and improvements:

Currently there’s a lot I want to improve, mostly the divergence detection and the overall sharpe ratio could be much better, but the current value of 0.5 gives me hope that the strategy is onto something. I also want to change TP from a percentage stop to something more dynamic but that might be too optimistic. The current plan is to paper trade test this either by manual or by a python bot, to see how it performs with some user input as well.

PMax on Rsi w/T3 *Strategy*Profit Maximizer Indicator on RSI with Tillson T3 Moving Average:

PMax uses ATR calculation inside, for this reason users couldn't manage to use PMax on RSI because RSI indicator doesn't have High and Low values in bars, but ATR needs that values. So I personally calculate RSI in a different way to have High and Low values of RSI wrt price bars.

IMPORTANT:

Because of the sudden movements and divergences on RSI , this indicator must firstly optimized for the charts before using. Optimization can be held by users for the meaningful parameters for each chart.

3 parameters are critical when optimizing:

First: Multiplier

Second: Tillson T3 Length

Third: T3 Volume Factor

Says, Kıvanç Özbilgiç. Here's the strategy version for you to backtest & optimize properly.

Enjoy.

HMA_ATR StrategyATR with HMA experimental minimalist bot for ETHBTC .

A strategy for use by Automated Algorithm systems.

Different from normal ATR as it uses HMA for smoothing.

Example settings result shown here on chart include commission 0.5%

ATR with EOM and VORTEXThis is a strategy, designed for long trends for stock and crypto market.

Its made of ATR for volatility, EOM for volume and VORTEX for the trend direction.

In this case on the ATR, I applied an EMA to check if current position is above the EMA -> bull trend, below ema -> bear trend

For EOM I am using the positive and negative value scale, if its positive we are in a bull movement, otherwise a bear movement.

Lastly for VORTEX, I took the min and max, and made an average, after that I am using the average and compare it with 1 value. Above 1 -> bull, belowe 1-> bear.

This strategy only goes long.

If you have any questions, let me know.

Trend Surfers - Premium Breakout + AlertsTrend Surfers - Premium Breakout Strategy with Alerts

I am happy today to release the first free Trend Surfers complete Breakout Strategy!

The strategy includes:

Entry for Long and Short

Stoploss

Position Size

Exit Signal

Risk Management Feature

How the strategy works

This is a Trend Following strategy. The strategy will have drawdowns, but they will be way smaller than what you would go through with buy and old.

As a Trend Following strategy, we will buy on strength, when a breakout occurs. And sell on weakness.

The strategy includes a FIX Stoploss determined by an ATR multiple and a trailing Stoploss/Takeprofit also determined by an ATR multiple.

You can also manage your risk by entering the maximum % you are willing to risk on every trade. Additionally, there is an option to enter how many pairs you will be trading with the strategy. This will change your position size in order to make sure that you have enough funds to trade all your favorite pairs.

Use the strategy with alerts

This strategy is alert-ready. All you have to do is:

Go on a pair you would like to trade

Create an alert

Select the strategy as a Trigger

Wait for new orders to be sent to you

Every Entry (Long/Short) will include:

Market Entry (Enter position NOW!)

Stoploss price

Position Size

Leverage

* If you do not wish to use leverage, you can multiply the Position Size by the Leverage. But doing that, you might end up with a position greater than your equity. Trading on Futures is better in order to have accurate risk management.

Exit signals:

When you receive an exit signal, you need to close the position ASAP. If you want to keep your results as close as possible to the backtest results, you need to execute quickly and follow what the strategy is telling you.

Do not try to outsmart the strategy

Leave your emotion out of trading! If you trust the strategy, you will have way better returns than if you try to outsmart it. Follow each signal you receive even if it doesn't seem logical at the moment.

Become a machine that executes. Don't look at fundamentals. Follow the trend! Trust the strategy!

I hope you enjoy it!

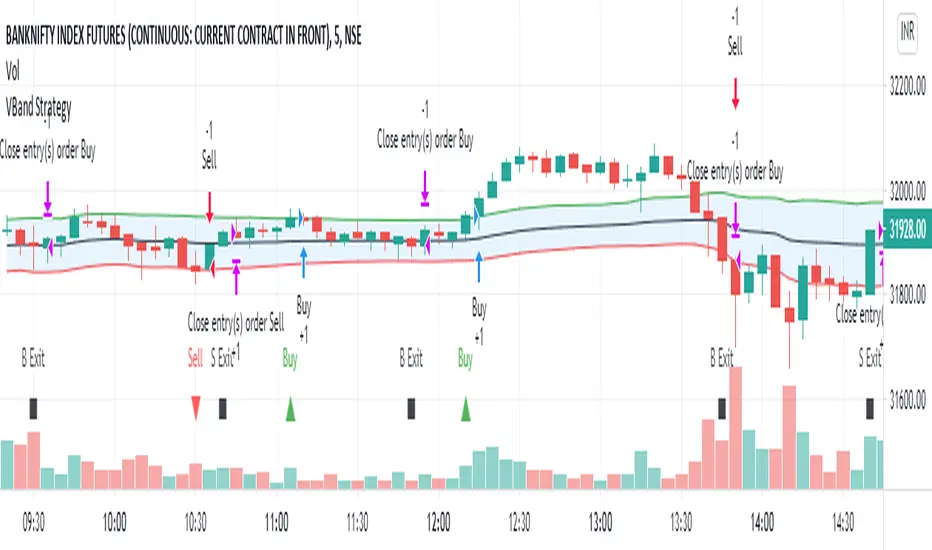

VBand StrategyVBand Strategy is simply used Vwap funcation and atr 14 for find the entry and exit points. This simple Strategy.

Phoenix085-Strategies==>MTF - Average True Range + MovAvgFIRSTLY, Here are a few who have influenced my pinescripting immensely recently:

@JustUncleL

@BigBitsIO

@TheArtofTrading

@QuantNomad

@SquigglesNiggles and many many many more.

Overview:

> This indicator is a simple crossover of Moving Averages.

> In addition I am using ATR rising as an indication for Trending Price.

> The entry is made once the smaller moving average crosses the bigger moving average, and also the Closes above the Smaller moving average.

> but the only twist here is,

- the ATR source is One timeframe Higher(In this case same as the session).whereas the source for the Moving averages is one Timeframe Lower.

>i.e., if the Session is 1D, the Indicator checks if the ATR is rising in the DAILY TIMEFRAME,

*_* the trade entry is made once the MOVING AVERAGE crossover happens on ONE TIME FRAME lower, as per example, ATR --> 1D = MA -->4H.

> Moving Average ->

- Thick -> Bigger MA,

- Thin and Transparent -> Smaller MA,

> Also, the Color of the Thicker MOVING AVERAGE Changes as Below:

- When LongCondition is satisfied --> Color=Lime

- When ShortCondition is satisfied --> Color=Red

- When neither condition is satisfied --> Color=Gray

NOTE:

1) There is a limitation in using the Securities function for FREE USERS --> Only 500 bars are allowed. So to use the indicators with more data, you need an upgraded TV account.

2) Strategy still needs Fine tuning, but for now, use the Thicker moving average color LIME FOR LONG ENTRIES and RED FOR SHORT ENTRIES.

This is Free for Use and share

MACD Strategy with trailing ATR stopThis is a trend based strategy that uses EMA and SMA intersection for determining the direction of the trend and MACD for the entry signal. At the same time, the strategy uses ATR, which is working as a trailing stop.

The strategy entry will work when the Trend ribbon will turn green and MACD line will crossover the signal line. This strategy also takes into account the pyramiding and allows to enter the second time if the signal will repeat itself.

There are 3 exit points. The first 10% of the position will be closed when the price will increase by 1%. The second portion of 50% will be closed when the price reaches 5% Take profit target. The remaining 40 % of the position will wait for the exit signal which will occur when the price closes below the ATR line.

The strategy is using a fixed amount in dollars, each time the entry occurs the strategy will enter with 100$ in the order.

The strategy can be applied to other crypto assets. However, they will require input changes.

Best of luck with your trading.

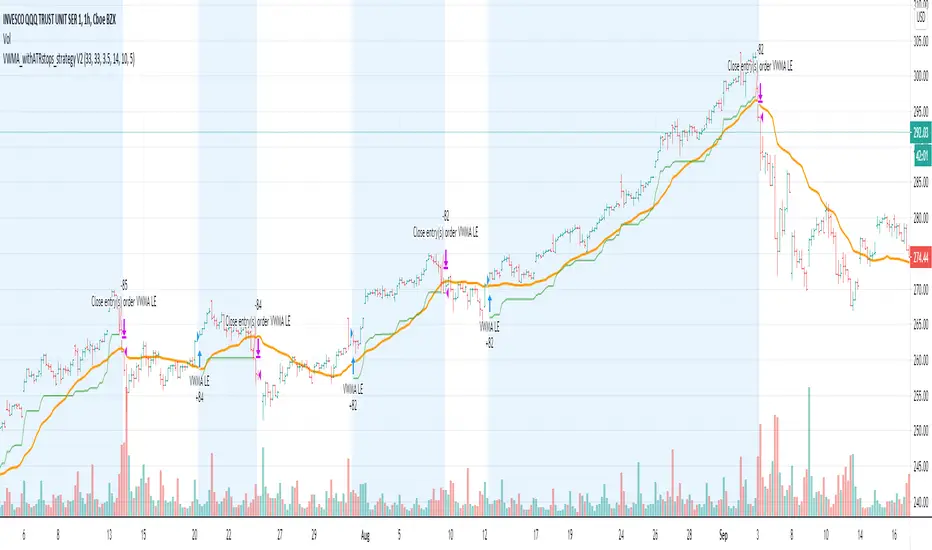

VWMA_withATRstops_strategyThis strategy follows the trend when price is above VWMA indicator. I have modified entry and exit rules to get most out of it.

Instead of entering LONG when price crosses above VWMA, I have used RSI(14) of VWMA . that way it skips the false signals. (some extent)

ENTRY

========

1. VWMA setting is 33

2. When RSIofVwma is above 30 enter Long ( and also checks if price already broke the ATR Stop above line )

Stop Loss and Exits

==================

1. Exit is when price breaks the ATR stop loss

2. ATR setting is set as same VWMA Length and multiplier is 3.5

3. STOP Loss that I mentioned in the settings is being used to calculate the how many units can be purchased based on risk of capital value.

Note: There is NO hard stop loss. having above ATR stop loss works as Trailing stop loss

Warning

=======

For the educational purposes only

Wilder's Volatility Trailing Stop Strategy with various MA'sFor Educational Purposes. Results can differ on different markets and can fail at any time. Profit is not guaranteed.

This only works in a few markets and in certain situations. Changing the settings can give better or worse results for other markets. This strategy is based on Wilder's Volatility System. It is an ATR trailing stop that is used for long term trends. This strategy focuses on the trailing stop alone and goes long and short only when it goes above or below the trailing line. It is similar to Donchian channels except it does not include the certain period channel breakout, only the trailing signal. This is only the trailing stop and an attempt to show how well it works standalone as Wilder described.

In his book, Wilder recommends a multiplier of 2.8-3.1 and an ATR lookback of 7 periods along with a running moving average or otherwise known as Wilder's moving average. The calculation and programming part for the trailing stop varies everywhere. I opted to keep it as simple and accurate as I could think of and interpret from the book. The variations to these types of indicators are numerous unfortunately, but Wilder seems to be the original author of ATR and this ATR-based trailing stop. In his book he says to use the significant closing price or highest/lowest closing price for the calculation part but I also included the option of choosing the highest high and lowest low, and the option to choose various moving averages in case anyone wants to experiment.

Comparing this and Donchian channels, it seems that a 2.5 multiplier is somewhat similar to the middle band of DCs and a 3.0 multiplier is somewhat similar to a double length middle band of DCs. It's hard to say which is the better trailing stop for a long term strategy. It's hard to beat the simplicity of DCs but maybe some might find a need for more inputs in a trailing stop or maybe an ATR based one like Wilder's can work better depending on what setting or strategy it's used in.

Profit Maximizer PMax Strategy - Long-ShortI developed a different strategy perspective for the Profit Maximizer PMax indicator prepared by Kıvanç Özbilgiç.

When you come to the settings section;

- You will see 2 options as Straregy Type. You can test the price and pmax intersections as different strategies.

- I added the Long-Short option for spot traders to calculate the profitability rate correctly. Spot traders should not choose this option.

Here you can set alarms on the original indicator with the parameters you find successful.

Türkçe:

Kıvanç Özbilgiç tarafından hazırlanan Profit Maximizer PMax indikatör için farklı bir strateji bakış açısı geliştirdim.

Ayarlar bölümüne geldiğinizde;

- Straregy Type olarak 2 seçenek göreceksiniz. Fiyat kesişimi ve pmax kesişimlerini, farklı stratejiler olarak test edebilirsiniz.

- Spot işlem yapanlar için karlılık oranını doğru hesaplayabilmeleri için Long-Short seçeneği ekledim. Spot işlem yapanların bu seçeneği seçmemeleri gerekmektedir.

Burada başarılı bulduğunuz parametreler ile orijinal indikatör üzerinde alarmlar kurabilirsiniz.

ATR Stop Buy StrategyThis strategy trial is let you to giving sell and buy orders with ATR (average true range) and an coefficent for them. it is my first strategy work, needs to be upgraded. USE IT WITH YOUR OWN RISK. IT IS NOT EVEN GUARANTEED TO WORK.

2 Candles Inside ATR2 agitated candles falling inside ATR range, awaiting possibly a big move.

Buy / Sell signals at combined high / low can be used as order with other as stop loss.

Counter trade, when this minimal stop loss is hit, is also as useful. However, wait till the SL candle closes, before opening position on the other side.

Works quite well on 15 mins chart, with settings of ATR duration 25 and multiplier 0.6. These settings are configurable, so feel free.

ATR Trailing Stop Strategy by ceyhunSame coding only coloring and strategy version added

//Barcolor

Green = Trail1 > Trail2 and close > Trail2 and low > Trail2

Blue = Trail1 > Trail2 and close > Trail2 and low < Trail2

Red = Trail2 > Trail1 and close < Trail2 and high < Trail2

Yellow = Trail2 > Trail1 and close < Trail2 and high > Trail2

//It gives White color where there is deterioration.

Let's not use InfoPanel in strategy, it would be wrong as it signals the next day.

ATR Trailing Stoploss StrategyI am sharing the strategy version of the indicator used before. It is very simple to use.

These are the settings I use, you can change, test and use as you wish.

Atr Period 5

Highest High Period 10

Multiplier 2.5

It can generate more signals in shorter time frames.

The success rate will be higher in longer time frames.

Full strategy AllinOne with risk management MACD RSI PSAR ATR MAHey, I am glad to present you one of the strategies where I put a lot of time in it.

This strategy can be adapted to all type of timecharts like scalping, daytrading or swing.

The context is the next one :

First we have the ATR to calculate our TP/SL points. At the same time we have another rule once we enter(we enter based on % risk from total equity, in this example 1%, at the same time, lowest ammount for this example is 0.1 lots, but can be modified to 0.01), so we can exit both by tp/sl points, or by losing 1% of our equity or winning 1% of our total equity. It's dinamic.

The strategy is made from

Trend direction :

PSAR

First confirmation point :

Crossover between 10EMA and Bollinger bands middle point

Second confirmation

MACD histogram

Third confirmation

RSI overbought/oversold levels

For entries : we check trend with psar, then once ema cross bb middle point, we confirm together with rsi level for overbought/oversold and macd histogram ( > 0 or <0).

We exit, when we have opposite sign, like from buy to sell or sell to buy, or when we reach tp/sl points, or when we reach % basaed equity points.

It can be changed to be fixed lots, or fixed tp/sl , you just have to uncomment the size from entries, and tp/sl lines.

At the same time, it has the possibility if one desires, to trade only concrete forex session like european, asian and so on for intraday trading.

Hope you enjoy it.

Let me know how it goes.

Trend trader StrategyFirst I would like to thank to @JustUncleL since this strategy started from one of his scalper strategies

This strategy can be adapted to all time charts .

First it has the session where we want to trade, for this example I choosed the EURUSD so I only take in consideration london/neywork session.

Its made from 3 EMA :

normal

slow

ultra slow

It has has the capacity to use HA candles into consideration if its needed.

At the same time we have a price channel made from faster MAs, that act like a bollinger band .

Together with all of them, we establish which trend we have if its uptrend or downtrend

Then we check the candles if they are below or above the MA , and based on the condition if they crossed recently we can suggest if its a buy or a long condition

At the same time we have 2 options of stop conditions:

Through a trailing stop made from ATR or % based

And second, a SL/TP made from pip points or % based.

For this example I used % based.

Let me know what you think about it, and if you found some nice settings for it. So far I only adapted to EURUSD 1 min time.