Extremum Range MA Crossover Strategy1. Principle of Work & Strategy Logic ⚙️📈

Main idea: The strategy tries to catch the moment of a breakout from a price consolidation range (flat) and the start of a new trend. It combines two key elements:

Moving Average (MA) 📉: Acts as a dynamic support/resistance level and trend filter.

Range Extremes (Range High/Low) 🔺🔻: Define the borders of the recent price channel or consolidation.

The strategy does not attempt to catch absolute tops and bottoms. Instead, it enters an already formed move after the breakout, expecting continuation.

Type: Trend-following, momentum-based.

Timeframes: Works on different TFs (H1, H4, D), but best suited for H4 and higher, where breakouts are more meaningful.

2. Justification of Indicators & Settings ⚙️

A. Moving Average (MA) 📊

Why used: Core of the strategy. It smooths price fluctuations and helps define the trend. The price (via extremes) must cross the MA → signals a potential trend shift or strengthening.

Parameters:

maLength = 20: Default length (≈ one trading month, 20-21 days). Good balance between sensitivity & smoothing.

Lower TF → reduce (10–14).

Higher TF → increase (50).

maSource: Defines price source (default = Close). Alternatives (HL2, HLC3) → smoother, less noisy MA.

maType: Default = EMA (Exponential MA).

Why EMA? Faster reaction to recent price changes vs SMA → useful for breakout strategies.

Other options:

SMA 🟦 – classic, slowest.

WMA 🟨 – weights recent data stronger.

HMA 🟩 – near-zero lag, but “nervous,” more false signals.

DEMA/TEMA 🟧 – even faster & more sensitive than EMA.

VWMA 🔊 – volume-weighted.

ZLEMA ⏱ – reduced lag.

👉 Choice = tradeoff between speed of reaction & false signals.

B. Range Extremes (Previous High/Low) 📏

Why used: Define borders of recent trading range.

prevHigh = local resistance.

prevLow = local support.

Break of these levels on close = trigger.

Parameters:

lookbackPeriod = 5: Searches for highest high / lowest low of last 5 candles. Very recent range.

Higher value (10–20) → wider, stronger ranges but rarer signals.

3. Entry & Exit Rules 🎯

Long signals (BUY) 🟢📈

Condition (longCondition): Previous Low crosses MA from below upwards.

→ Price bounced from the bottom & strong enough to push range border above MA.

Execution: Auto-close short (if any) → open long.

Short signals (SELL) 🔴📉

Condition (shortCondition): Previous High crosses MA from above downwards.

→ Price rejected from the top, upper border failed above MA.

Execution: Auto-close long (if any) → open short.

Exit conditions 🚪

Exit Long (exitLongCondition): Close below prevLow.

→ Uptrend likely ended, range shifts down.

Exit Short (exitShortCondition): Close above prevHigh.

→ Downtrend likely ended, range shifts up.

⚠️ Important: Exit = only on candle close beyond extremes (not just wick).

4. Trading Settings ⚒️

overlay = true → indicators shown on chart.

initial_capital = 10000 💵.

default_qty_type = strategy.cash, default_qty_value = 100 → trades fixed $100 per order (not lots). Can switch to % of equity.

commission_type = strategy.commission.percent, commission_value = 0.1 → default broker fee = 0.1%. Adjust for your broker!

slippage = 3 → slippage = 3 ticks. Adjust to asset liquidity.

currency = USD.

margin_long = 100, margin_short = 100 → no leverage (100% margin).

5. Visualization on Chart 📊

The strategy draws 3 lines:

🔵 MA line (thickness 2).

🔴 Previous High (last N candles).

🟢 Previous Low (last N candles).

Also: entry/exit arrows & equity curve shown in backtest.

Disclaimer ⚠️📌

Risk Warning: This description & code are for educational purposes only. Not financial advice. Trading (Forex, Stocks, Crypto) carries high risk and may lead to full capital loss. You trade at your own risk.

Testing: Always backtest & demo test first. Past results ≠ future profits.

Responsibility: Author of this strategy & description is not responsible for your trading decisions or losses.

Tradingstrategy

Fibonacci Counter-Trend TradingOverview:

The Fibonacci Counter-Trend Trading strategy is designed to capitalize on price reversals by utilizing Fibonacci levels calculated from the standard deviation of price movements. This strategy opens a sell order when the closing price crosses above a specified upper Fibonacci level and a buy order when the closing price crosses below a specified lower Fibonacci level. By leveraging the principles of Fibonacci retracement and volatility, this strategy aims to identify potential reversal points in the market.

How It Works:

Fibonacci Levels Calculation:

The strategy calculates upper and lower Fibonacci levels based on the standard deviation of the price over a specified moving average length. These levels are derived from the Fibonacci sequence, which is widely used in technical analysis to identify potential support and resistance levels.

The upper levels are calculated by adding specific Fibonacci ratios (0.236, 0.382, 0.5, 0.618, 0.764, and 1.0) multiplied by the standard deviation to the basis (the volume-weighted moving average).

The lower levels are calculated by subtracting the same Fibonacci ratios multiplied by the standard deviation from the basis.

Trade Entry Rules:

Sell Order: A sell order is triggered when the closing price crosses above the selected upper Fibonacci level. This indicates a potential reversal point where the price may start to decline.

Buy Order: A buy order is initiated when the closing price crosses below the selected lower Fibonacci level. This suggests a potential reversal point where the price may begin to rise.

Trade Management:

The strategy includes stop-losses based on the Fibonacci levels to protect against adverse price movements.

How to Use:

Users can customize the moving average length and the multiplier for the standard deviation to suit their trading preferences and market conditions.

The strategy can be applied to various financial instruments, including stocks, forex, and cryptocurrencies, making it versatile for different trading environments.

Pros:

The Fibonacci Counter-Trend Trading strategy combines the mathematical principles of the Fibonacci sequence with the statistical measure of standard deviation, providing a unique approach to identifying potential market reversals.

This strategy is particularly useful in volatile markets where price swings can lead to significant trading opportunities.

The use of Fibonacci levels can help traders identify key support and resistance areas, enhancing decision-making.

Cons:

The strategy may generate false signals in choppy or sideways markets, leading to potential losses if the price does not reverse as anticipated.

Relying solely on Fibonacci levels without considering other technical indicators or market conditions may result in missed opportunities or increased risk.

The effectiveness of the strategy can vary depending on the chosen parameters (e.g., moving average length and standard deviation multiplier), requiring users to spend time optimizing these settings for different market conditions.

As with any counter-trend strategy, there is a risk of significant drawdowns during strong trending markets, where the price continues to move in one direction without reversing.

By understanding the mechanics of the Fibonacci Counter-Trend Trading strategy, along with its pros and cons, traders can effectively implement it in their trading routines and potentially enhance their trading performance.

Iron Bot Statistical Trend Filter📌 Iron Bot Statistical Trend Filter

📌 Overview

Iron Bot Statistical Trend Filter is an advanced trend filtering strategy that combines statistical methods with technical analysis.

By leveraging Z-score and Fibonacci levels, this strategy quantitatively analyzes market trends to provide high-precision entry signals.

Additionally, it includes an optional EMA filter to enhance trend reliability.

Risk management is reinforced with Stop Loss (SL) and four Take Profit (TP) levels, ensuring a balanced approach to risk and reward.

📌 Key Features

🔹 1. Statistical Trend Filtering with Z-Score

This strategy calculates the Z-score to measure how much the price deviates from its historical mean.

Positive Z-score: Indicates a statistically high price, suggesting a strong uptrend.

Negative Z-score: Indicates a statistically low price, signaling a potential downtrend.

Z-score near zero: Suggests a ranging market with no strong trend.

By using the Z-score as a filter, market noise is reduced, leading to more reliable entry signals.

🔹 2. Fibonacci Levels for Trend Reversal Detection

The strategy integrates Fibonacci retracement levels to identify potential reversal points in the market.

High Trend Level (Fibo 23.6%): When the price surpasses this level, an uptrend is likely.

Low Trend Level (Fibo 78.6%): When the price falls below this level, a downtrend is expected.

Trend Line (Fibo 50%): Acts as a midpoint, helping to assess market balance.

This allows traders to visually confirm trend strength and turning points, improving entry accuracy.

🔹 3. EMA Filter for Trend Confirmation (Optional)

The strategy includes an optional 200 EMA (Exponential Moving Average) filter for trend validation.

Price above 200 EMA: Indicates a bullish trend (long entries preferred).

Price below 200 EMA: Indicates a bearish trend (short entries preferred).

Enabling this filter reduces false signals and improves trend-following accuracy.

🔹 4. Multi-Level Take Profit (TP) and Stop Loss (SL) Management

To ensure effective risk management, the strategy includes four Take Profit levels and a Stop Loss:

Stop Loss (SL): Automatically closes trades when the price moves against the position by a certain percentage.

TP1 (+0.75%): First profit-taking level.

TP2 (+1.1%): A higher probability profit target.

TP3 (+1.5%): Aiming for a stronger trend move.

TP4 (+2.0%): Maximum profit target.

This system secures profits at different stages and optimizes risk-reward balance.

🔹 5. Automated Long & Short Trading Logic

The strategy is built using Pine Script®’s strategy.entry() and strategy.exit(), allowing fully automated trading.

Long Entry:

Price is above the trend line & high trend level.

Z-score is positive (indicating an uptrend).

(Optional) Price is also above the EMA for stronger confirmation.

Short Entry:

Price is below the trend line & low trend level.

Z-score is negative (indicating a downtrend).

(Optional) Price is also below the EMA for stronger confirmation.

This logic helps filter out unnecessary trades and focus only on high-probability entries.

📌 Trading Parameters

This strategy is designed for flexible capital management and risk control.

💰 Account Size: $5000

📉 Commissions and Slippage: Assumes 94 pips commission per trade and 1 pip slippage.

⚖️ Risk per Trade: Adjustable, with a default setting of 1% of equity.

These parameters help preserve capital while optimizing the risk-reward balance.

📌 Visual Aids for Clarity

To enhance usability, the strategy includes clear visual elements for easy market analysis.

✅ Trend Line (Blue): Indicates market midpoint and helps with entry decisions.

✅ Fibonacci Levels (Yellow): Highlights high and low trend levels.

✅ EMA Line (Green, Optional): Confirms long-term trend direction.

✅ Entry Signals (Green for Long, Red for Short): Clearly marked buy and sell signals.

These features allow traders to quickly interpret market conditions, even without advanced technical analysis skills.

📌 Originality & Enhancements

This strategy is developed based on the IronXtreme and BigBeluga indicators,

combining a unique Z-score statistical method with Fibonacci trend analysis.

Compared to conventional trend-following strategies, it leverages statistical techniques

to provide higher-precision entry signals, reducing false trades and improving overall reliability.

📌 Summary

Iron Bot Statistical Trend Filter is a statistically-driven trend strategy that utilizes Z-score and Fibonacci levels.

High-precision trend analysis

Enhanced accuracy with an optional EMA filter

Optimized risk management with multiple TP & SL levels

Visually intuitive chart design

Fully customizable parameters & leverage support

This strategy reduces false signals and helps traders ride the trend with confidence.

Try it out and take your trading to the next level! 🚀

Gold Friday Anomaly StrategyThis script implements the " Gold Friday Anomaly Strategy ," a well-known historical trading strategy that leverages the gold market's behavior from Thursday evening to Friday close. It is a backtesting-focused strategy designed to assess the historical performance of this pattern. Traders use this anomaly as it captures a recurring market tendency observed over the years.

What It Does:

Entry Condition: The strategy enters a long position at the beginning of the Friday trading session (Thursday evening close) within the defined backtesting period.

Exit Condition: Friday evening close.

Backtesting Controls: Allows users to set custom backtesting periods to evaluate strategy performance over specific date ranges.

Key Features:

Custom Backtest Periods: Easily configurable inputs to set the start and end date of the backtesting range.

Fixed Slippage and Commission Settings: Ensures realistic simulation of trading conditions.

Process Orders on Close: Backtesting is optimized by processing orders at the bar's close.

Important Notes:

Backtesting Only: This script is intended purely for backtesting purposes. Past performance is not indicative of future results.

Live Trading Recommendations: For live trading, it is highly recommended to use limit orders instead of market orders, especially during evening sessions, as market order slippage can be significant.

Default Settings:

Entry size: 10% of equity per trade.

Slippage: 1 tick.

Commission: 0.05% per trade.

TSI w SuperTrend decision - Strategy [presentTrading]This strategy aims to improve upon the performance of Traidngview's newly published "Trend Strength Index" indicator by incorporating the SuperTrend for better trade execution and risk management. Enjoy :)

█ Introduction and How it is Different

The "TSI with SuperTrend Decision - Strategy" combines the Trend Strength Index (TSI) with SuperTrend indicators to determine entry and exit points. Unlike traditional strategies that rely solely on one indicator, this method leverages the strengths of both TSI and SuperTrend to provide a more nuanced and adaptive trading strategy.

This dual approach allows for capturing trends more effectively, especially in volatile markets.

BTCUSD 8h LS Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Trend Strength Index (TSI)

The TSI is a momentum oscillator that shows both the direction and strength of a trend. It is calculated by comparing the price movement with the bar index over a specified period. The formula for TSI is as follows:

```

TSI = (PC / |PC|)

where:

PC = Change in price over the period

```

In this strategy, TSI is calculated using the closing prices and a default period of 64 bars. The TSI values help identify overbought and oversold conditions, providing signals for potential market reversals.

🔶 SuperTrend Indicator

The SuperTrend is a trend-following indicator based on the average true range (ATR). It helps in identifying the direction of the market trend. The SuperTrend calculation involves:

```

SuperTrend = HLC3 ± (Factor * ATR)

where:

HLC3 = (High + Low + Close) / 3

Factor = User-defined multiplier

ATR = Average True Range over a period

```

The SuperTrend settings in this strategy include a length of 10 bars and a factor of 3.0.

Last Bull Cycle of BTC

🔶 Entry and Exit Conditions

The strategy uses the TSI and SuperTrend together to determine entry and exit points:

- Long Entry: When the SuperTrend indicates a downward trend (st.d < 0) and the TSI is above the oversold level (-0.241).

- Long Exit: When the SuperTrend indicates an upward trend (st.d > 0) and the TSI is below the overbought level (0.241).

- Short Entry: When the SuperTrend indicates an upward trend (st.d > 0) and the TSI is below the overbought level (0.241).

- Short Exit: When the SuperTrend indicates a downward trend (st.d < 0) and the TSI is above the oversold level (-0.241).

█ Trade Direction

The strategy allows users to select the trade direction through the `tradeDirection` input. The options are:

- Both: Enables both long and short trades.

- Long: Enables only long trades.

- Short: Enables only short trades.

█ Default Settings

- TSI Length: 64

- SuperTrend Length: 10

- SuperTrend Factor: 3.0

- Trade Direction: Both

- Take Profit (%): 30.0

- Stop Loss (%): 20.0

Impact of Default Settings

- TSI Length: A longer TSI period smooths out noise but may lag in identifying trends. A shorter period is more responsive but can generate false signals.

- SuperTrend Length: A shorter length provides quicker signals but can be prone to whipsaws. A longer length is more reliable but may delay entries and exits.

- SuperTrend Factor: A higher factor increases the distance of the SuperTrend from the price, reducing sensitivity to minor price fluctuations.

- Trade Direction: Allows flexibility in trading strategies by enabling both long and short trades based on market conditions.

- Take Profit and Stop Loss: These settings manage risk by automatically closing trades at predefined profit or loss levels. Higher percentages provide larger potential gains but also higher risk.

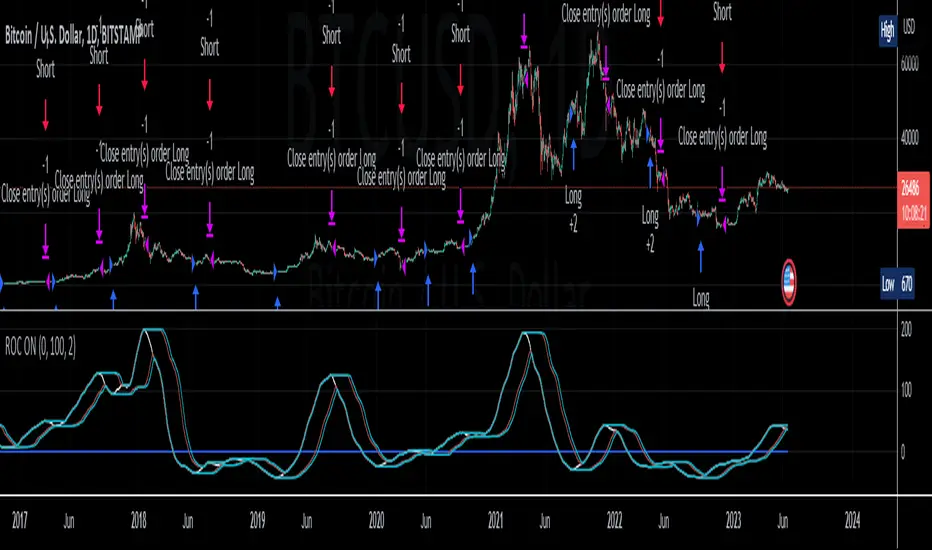

Heikin Ashi ROC Percentile Strategy**User Guide for the "Heikin Ashi ROC Percentile Strategy"**

This strategy, "Heikin Ashi ROC Percentile Strategy", is designed to provide an easy-to-use framework for trading based on the Heikin Ashi Rate of Change (ROC) and its percentiles.

Here's how you can use it:

1. **Setting the Start Date**: You can set the start date for the strategy in the user inputs at the top of the script. The variable `startDate` defines the point from which the script begins executing trades. Simply input the desired date in the format "YYYY MM DD". For example, to start the strategy from March 3, 2023, you would enter `startDate = timestamp("2023 03 03")`.

2. **Adjusting the Midline, Lookback Period, and Stop Loss Level**: The `zerohLine`, `rocLength`, and `stopLossLevel` inputs allow you to adjust the baseline for ROC, the lookback period for the SMA and ROC, and the level at which the strategy stops the loss, respectively. By tweaking these parameters, you can fine-tune the strategy to better suit your trading style or the particular characteristics of the asset you are trading.

3. **Understanding the Trade Conditions**: The script defines conditions for entering and exiting long and short positions based on crossovers and crossunders of the ROC and the upper and lower "kill lines". These lines are defined as certain percentiles of the ROC's highest and lowest values over a specified lookback period. When the ROC crosses above the lower kill line, the script enters a long position; when it crosses below the upper kill line, it exits the position. Similarly, when the ROC crosses below the upper kill line, the script enters a short position; when it crosses above the lower kill line, it exits the position.

In my testing, this strategy performed best on a day and hour basis. However, I encourage you to experiment with different timeframes and settings to see how the strategy performs under various conditions. Remember, there's no one-size-fits-all approach to trading; what works best will depend on your specific circumstances, goals, and risk tolerance.

If you find other useful applications for this strategy, please let me know in the comments. Your feedback is invaluable in helping to refine and improve this tool. Happy trading!