ThinkTech AI SignalsThink Tech AI Strategy

The Think Tech AI Strategy provides a structured approach to trading by integrating liquidity-based entries, ATR volatility thresholds, and dynamic risk management. This strategy generates buy and sell signals while automatically calculating take profit and stop loss levels, boasting a 64% win rate based on historical data.

Usage

The strategy can be used to identify key breakout and retest opportunities. Liquidity-based zones act as potential accumulation and distribution areas and may serve as future support or resistance levels. Buy and sell zones are identified using liquidity zones and ATR-based filters. Risk management is built-in, automatically calculating take profit and stop loss levels using ATR multipliers. Volume and trend filtering options help confirm directional bias using a 50 EMA and RSI filter. The strategy also allows for session-based trading, limiting trades to key market hours for higher probability setups.

Settings

The risk/reward ratio can be adjusted to define the desired stop loss and take profit calculations. The ATR length and threshold determine ATR-based breakout conditions for dynamic entries. Liquidity period settings allow for customized analysis of price structure for support and resistance zones. Additional trend and RSI filters can be enabled to refine trade signals based on moving averages and momentum conditions. A session filter is included to restrict trade signals to specific market hours.

Style

The strategy includes options to display liquidity lines, showing key support and resistance areas. The first 15-minute candle breakout zones can also be visualized to highlight critical market structure points. A win/loss statistics table is included to track trade performance directly on the chart.

This strategy is intended for descriptive analysis and should be used alongside other confluence factors. Optimize your trading process with Think Tech AI today!

Trading!

[COG]S&P 500 Weekly Seasonality ProjectionS&P 500 Weekly Seasonality Projection

This indicator visualizes S&P 500 seasonality patterns based on historical weekly performance data. It projects price movements for up to 26 weeks ahead, highlighting key seasonal periods that have historically affected market performance.

Key Features:

Projects price movements based on historical S&P 500 weekly seasonality patterns (2005-2024)

Highlights six key seasonal periods: Jan-Feb Momentum, March Lows, April-May Strength, Summer Strength, September Dip, and Year-End Rally

Customizable forecast length from 1-26 weeks with quick timeframe selection buttons

Optional moving average smoothing for more gradual projections

Detailed statistics table showing projected price and percentage change

Seasonality mini-map showing the full annual pattern with current position

Customizable colors and visual elements

How to Use:

Apply to S&P 500 index or related instruments (daily timeframe or higher recommended)

Set your desired forecast length (1-26 weeks)

Monitor highlighted seasonal zones that have historically shown consistent patterns

Use the projection line as a general guideline for potential price movement

Settings:

Forecast length: Configure from 1-26 weeks or use quick select buttons (1M, 3M, 6M, 1Y)

Visual options: Customize colors, backgrounds, label sizes, and table position

Display options: Toggle statistics table, period highlights, labels, and mini-map

This indicator is designed as a visual guide to help identify potential seasonal tendencies in the S&P 500. Historical patterns are not guarantees of future performance, but understanding these seasonal biases can provide valuable context for your trading decisions.

Note: For optimal visualization, use on Daily timeframe or higher. Intraday timeframes will display a warning message.

[COG]Nasdaq Weekly Seasonality ProjectionNasdaq Weekly Seasonality Projection

This indicator provides a visualization of Nasdaq seasonality patterns based on historical weekly performance data. It projects price movements for up to 26 weeks ahead, highlighting key seasonal periods that have historically affected tech stocks.

Key Features:

Projects price movements based on historical Nasdaq weekly seasonality patterns

Highlights six key seasonal periods: January Effect, March Lows, April-May Strength, Tech Summer Rally, September Dip, and Q4 Tech Rally

Customizable forecast length from 1-26 weeks with quick timeframe selection buttons

Optional moving average smoothing for more gradual projections

Detailed statistics table showing projected price and percentage change

Seasonality mini-map showing the full annual pattern with current position

Customizable colors and visual elements

How to Use:

Apply to Nasdaq indices or tech-focused instruments (daily timeframe or higher recommended)

Set your desired forecast length (1-26 weeks)

Monitor highlighted seasonal zones that have historically shown consistent patterns

Use the projection line as a general guideline for potential price movement

Settings:

Forecast length: Configure from 1-26 weeks or use quick select buttons (1M, 3M, 6M, 1Y)

Visual options: Customize colors, backgrounds, label sizes, and table position

Display options: Toggle statistics table, period highlights, labels, and mini-map

This indicator is designed as a visual guide to help identify potential seasonal tendencies in Nasdaq and tech stocks. Historical patterns are not guarantees of future performance, but understanding these seasonal biases can provide valuable context for your trading decisions.

Note: For optimal visualization, use on Daily timeframe or higher. Intraday timeframes will display a warning message.

Scalping Entry/Exit Indicator by DiGetImagine having a tool that not only spots high-probability entry signals but also visually marks them on your chart with color-coded cues and automated alerts. The Scalping Entry/Exit Indicator by DiGet does exactly that—by fusing a range of classic candlestick patterns (such as Bullish Hammers, Engulfing patterns, and Morning/Evening Stars) with dynamic risk management levels, this script empowers you to make swift and informed trading decisions. Whether you're an active trader or an algorithm enthusiast, this indicator offers both precision and clarity in identifying scalp opportunities, making your chart analysis more efficient and visually engaging.

Indicator Breakdown

Input Parameters:

The indicator accepts a customizable risk-reward ratio, an ATR period for volatility measurement, and a lookback period to scan for valid candlestick patterns.

ATR & Candle Calculations:

It computes the Average True Range (ATR) to dynamically set stop-loss and take-profit levels. Additionally, it determines the body and wick sizes of each candlestick to help identify key reversal patterns.

Pattern Detection:

Multiple bullish patterns (Hammer, Engulfing, Morning Star) and bearish patterns (Shooting Star, Engulfing, Evening Star) are detected. There’s also a simplified version of the Head & Shoulders pattern, offering further validation for reversal signals.

Signal Generation & Trade Levels:

The script consolidates the pattern signals into combined “buy” and “sell” triggers. It then calculates the respective stop-loss (SL) and take-profit (TP) levels based on the current price and ATR, providing a robust risk management framework.

Visual Aids & Alerts:

To enhance usability, the indicator changes the chart’s background color to green for buy signals and red for sell signals. It also draws labels, lines (representing SL and TP), and markers directly on the chart, along with alert conditions to notify traders of actionable signals.

This indicator is an excellent addition to your TradingView toolkit—ideal for scalpers and short-term traders seeking clarity, precision, and automated signal generation on their charts.

Enjoy trading with confidence and precision!

Lowess Channel + (RSI) [ChartPrime]The Lowess Channel + (RSI) indicator applies the LOWESS (Locally Weighted Scatterplot Smoothing) algorithm to filter price fluctuations and construct a dynamic channel. LOWESS is a non-parametric regression method that smooths noisy data by fitting weighted linear regressions at localized segments. This technique is widely used in statistical analysis to reveal trends while preserving data structure.

In this indicator, the LOWESS algorithm is used to create a central trend line and deviation-based bands. The midline changes color based on trend direction, and diamonds are plotted when a trend shift occurs. Additionally, an RSI gauge is positioned at the end of the channel to display the current RSI level in relation to the price bands.

lowess_smooth(src, length, bandwidth) =>

sum_weights = 0.0

sum_weighted_y = 0.0

sum_weighted_xy = 0.0

sum_weighted_x2 = 0.0

sum_weighted_x = 0.0

for i = 0 to length - 1

x = float(i)

weight = math.exp(-0.5 * (x / bandwidth) * (x / bandwidth))

y = nz(src , 0)

sum_weights := sum_weights + weight

sum_weighted_x := sum_weighted_x + weight * x

sum_weighted_y := sum_weighted_y + weight * y

sum_weighted_xy := sum_weighted_xy + weight * x * y

sum_weighted_x2 := sum_weighted_x2 + weight * x * x

mean_x = sum_weighted_x / sum_weights

mean_y = sum_weighted_y / sum_weights

beta = (sum_weighted_xy - mean_x * mean_y * sum_weights) / (sum_weighted_x2 - mean_x * mean_x * sum_weights)

alpha = mean_y - beta * mean_x

alpha + beta * float(length / 2) // Centered smoothing

⯁ KEY FEATURES

LOWESS Price Filtering – Smooths price fluctuations to reveal the underlying trend with minimal lag.

Dynamic Trend Coloring – The midline changes color based on trend direction (e.g., bullish or bearish).

Trend Shift Diamonds – Marks points where the midline color changes, indicating a possible trend shift.

Deviation-Based Bands – Expands above and below the midline using ATR-based multipliers for volatility tracking.

RSI Gauge Display – A vertical gauge at the right side of the chart shows the current RSI level relative to the price channel.

Fully Customizable – Users can adjust LOWESS length, band width, colors, and enable or disable the RSI gauge and adjust RSIlength.

⯁ HOW TO USE

Use the LOWESS midline as a trend filter —bullish when green, bearish when purple.

Watch for trend shift diamonds as potential entry or exit signals.

Utilize the price bands to gauge overbought and oversold zones based on volatility.

Monitor the RSI gauge to confirm trend strength—high RSI near upper bands suggests overbought conditions, while low RSI near lower bands indicates oversold conditions.

⯁ CONCLUSION

The Lowess Channel + (RSI) indicator offers a powerful way to analyze market trends by applying a statistically robust smoothing algorithm. Unlike traditional moving averages, LOWESS filtering provides a flexible, responsive trendline that adapts to price movements. The integrated RSI gauge enhances decision-making by displaying momentum conditions alongside trend dynamics. Whether used for trend-following or mean reversion strategies, this indicator provides traders with a well-rounded perspective on market behavior.

MTF Fractals [RunRox]🔽 MTF Fractals is a powerful indicator designed to visualize fractals from multiple timeframes directly on your chart, highlight liquidity sweeps at these fractal levels, and provide several additional features we’ll cover in detail below.

We created this indicator because we couldn’t find a suitable tool that met our specific needs on TradingView. Therefore, we decided to develop a valuable indicator for the entire TradingView community, combining simplicity and versatility.

⁉️ WHAT IS A FRACTALS?

In trading, a fractal is a technical analysis pattern composed of five consecutive candles, typically highlighting local market turning points. Specifically, a fractal high is formed when a candle’s high is higher than the highs of the two candles on either side, whereas a fractal low occurs when a candle’s low is lower than the lows of the two adjacent candles on both sides.

Traders use fractals as reference points for identifying significant support and resistance levels, potential reversal areas, and liquidity zones within price action analysis. Below is a screenshot illustrating clearly formed fractals on the chart.

📙 FRACTAL FORMATION

Here’s how fractals form depending on your chosen setting (3, 5, 7, or 9):

▶️ 3-bar fractal – forms when the central candle is higher (for highs) or lower (for lows) than one candle on each side.

▶️ 5-bar fractal – forms when the central candle is higher or lower than two candles on both sides.

▶️ 7-bar fractal – forms when the central candle is higher or lower compared to the three candles on each side.

▶️ 9-bar fractal – forms similarly but requires four candles on each side, making the fractal significantly more reliable and robust.

A higher number of bars ensures stronger fractal levels, highlighting more significant potential reversal points on the chart.

Now that we’ve covered the theory behind fractal formation, let’s explore the indicator’s functionality in more detail.

Below, I’ll explain each feature clearly and illustrate how you can effectively utilize this indicator in your trading.

🕐 MULTI-TIMEFRAME FRACTALS

We realized that displaying fractals only from the current timeframe isn’t always convenient, so we’ve introduced Multi-Timeframe Fractals into this indicator.

Now you can easily display fractals from higher timeframes directly on your current chart, providing you with broader market context and clearer trading signals.

Fractals from Current Timeframe – Fractals identified directly on the chart’s current timeframe.

Fractals from Higher Timeframes – Fractals sourced from higher timeframes and displayed clearly on your current chart for enhanced market perspective.

📈 FRACTAL LINES

Since fractals represent areas of high liquidity, we’ve added an option to extend fractal levels horizontally as Fractal Lines across your chart.

This feature allows you to clearly visualize critical liquidity areas from higher timeframes, directly on your current timeframe chart, as demonstrated in the screenshot below.

With this approach, you can clearly visualize significant fractal levels from higher timeframes directly on your current chart - for example, projecting fractals from the 1-hour (1H) timeframe onto a 3-minute (3m) chart. ✅ This helps you easily identify critical liquidity areas and potential reversal zones without the need to switch between multiple timeframes.

💰 LIQUDITY SWEEP (LIQUDITY GRAB)

To enhance your trading experience, we’ve introduced a feature that clearly identifies liquidity sweeps of fractal levels.

A Liquidity Sweep occurs when a candle closes beyond a fractal line, leaving a wick that pierces through it, signaling that liquidity has been collected at this level.

Below, you’ll find two examples illustrating this functionality:

▶️ Fractal lines from the current timeframe

▶️ Fractal lines projected from higher timeframes

The first example illustrates liquidity being swept from fractals on the current timeframe .

Here, the candle clearly closes beyond the fractal line, leaving a wick through it. This indicates a liquidity sweep at the fractal level, visually highlighting a potential reversal or continuation opportunity directly on your chart.

In the second example, fractals from the higher timeframe are projected onto your current chart.

When a candle on your current timeframe closes beyond an HTF fractal line - leaving a wick through this level - the indicator highlights it clearly. This signals to traders a potential reversal zone, indicating that liquidity has been swept, and price may reverse or significantly react from this area.

You can also enable the display of additional labels on the chart. These labels clearly mark liquidity sweeps at fractal levels, making it easier to visually identify potential reversal points directly on your chart.

⚙️ SETTINGS

Below are the indicator settings with detailed explanations for each parameter.

🔷 Bars in Fractal – Number of candles to the right and left required to form a fractal.

🔷 Fractal Timeframe – Select the timeframe from which you want to display fractals on the current chart.

🔷 Max Age, bars – Number of bars during which the fractal will remain active.

🔷 Show Fractal Line – Display or hide fractal lines.

🔷 Line Style – Choose the style of the line displayed on the chart.

🔷 Line Width – Thickness of the fractal line.

🔷 High Fractal – Style and color of bearish fractals.

🔷 Low Fractal – Style and color of bullish fractals.

🔷 Fractal Label Size – Select the size of fractal labels.

🔷 Show Sweep Labels – Option to display labels when a liquidity sweep occurs.

🔷 Label Color – Color and transparency of the area marked on the chart during a sweep.

🔷 Shade Sweep Area – Show or hide the sweep area shading.

🔷 Area Color – Color and transparency settings for the sweep area.

🔶 We’d love to hear your feedback and any suggestions for additional features you’d like to see in this indicator. We’ll be happy to consider your ideas and continue improving the indicator!

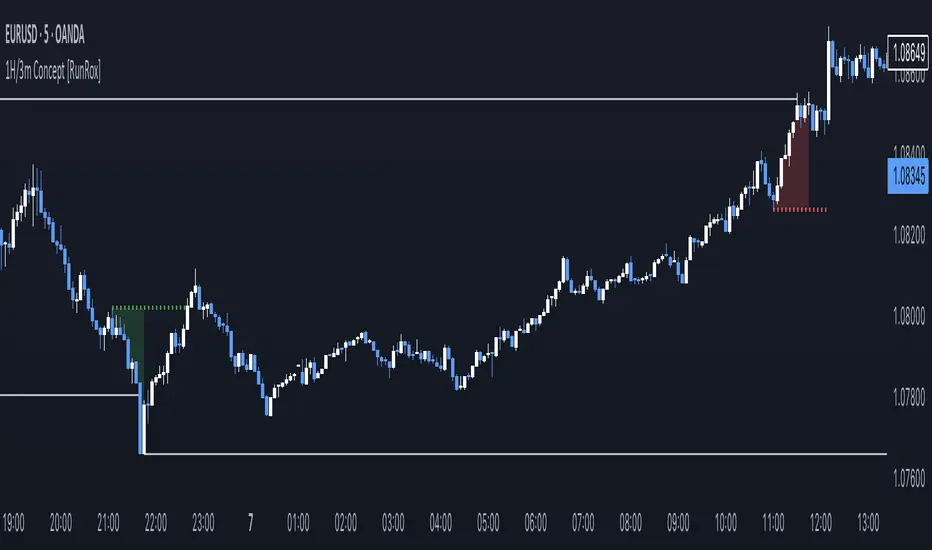

1H/3m Concept [RunRox]🕘 1H/3m Concept is a versatile trading methodology based on liquidity sweeps from fractal points identified on higher timeframes, followed by price reversals at these key moments.

Below, I will explain this concept in detail and provide clear examples demonstrating its practical application.

⁉️ WHAT IS A FRACTALS?

In trading, a fractal is a technical analysis pattern composed of five consecutive candles, typically highlighting local market turning points. Specifically, a fractal high is formed when a candle’s high is higher than the highs of the two candles on either side, whereas a fractal low occurs when a candle’s low is lower than the lows of the two adjacent candles on both sides.

Traders use fractals as reference points for identifying significant support and resistance levels, potential reversal areas, and liquidity zones within price action analysis. Below is a screenshot illustrating clearly formed fractals on the chart.

📌 ABOUT THE CONCEPT

The 1H/3m Concept involves marking Higher Timeframe (HTF) fractals directly onto a Lower Timeframe (LTF) chart. When a liquidity sweep occurs at an HTF fractal level, we remain on the same LTF chart (since all HTF fractals are already plotted on this lower timeframe) and wait for a clear Market Structure Shift (MSS) to identify our potential entry point.

Below is a schematic illustration clearly demonstrating how this concept works in practice.

Below is another 💡 real-chart example , showing liquidity in the form of a 1H fractal, swept by a rapid impulse move. Immediately afterward, a clear Market Structure Shift (MSS) occurs, signaling a potential entry point into the trade.

Another example is shown below, where we see our hourly fractal, from which price clearly reacts, providing an opportunity to search for an entry point.

As illustrated on the chart, the fractal levels from the higher timeframe are clearly displayed, but we’re working directly on the 5-minute chart. This allows us to remain on one timeframe without needing to switch back and forth between charts to spot such trading setups.

🔍 MTF FRACTALS

This concept can be applied across various HTF-LTF timeframe combinations. Although our examples illustrate 1H fractals used on a 5-minute chart, you can effectively utilize many other timeframe combinations, such as:

30m HTF fractals on 1m chart

1H HTF fractals on 3m chart

4H HTF fractals on 15m chart

1D HTF fractals on 1H chart

The key idea behind this concept is always the same: identify liquidity at fractal levels on the higher timeframe (HTF), then wait for a clear Market Structure Shift (MSS) on the lower timeframe (LTF) to enter trades.

⚙️ SETTINGS

🔷 Trade Direction – Select the preferred trading direction (Long, Short, or Both).

🔷 HTF – Choose the higher timeframe from which fractals will be displayed on the current chart.

🔷 HTF Period – Number of candles required on both sides of a fractal candle (before and after) to confirm fractal formation on the HTF.

🔷 Current TF Period – Sensitivity to the impulse that sweeps liquidity, used for identifying and forming the MSS line.

🔷 Show HTF – Enable or disable displaying HTF fractal lines on your chart. You can also customize line style and color.

🔷 Max Age (Bars) – Number of recent bars within which fractals from the selected HTF will be displayed.

🔷 Show Entry – Enable or disable displaying the MSS line on the chart.

🔷 Enable Alert – Activates TradingView alerts whenever the MSS line is crossed.

You can also enable 🔔 alerts, which notify you whenever price crosses the MSS line. This significantly simplifies the process of identifying these setups on your charts. Simply configure your preferred timeframes and wait for notifications when the MSS line is crossed.

🔶 We greatly appreciate your feedback and suggestions for improving the indicator!

Order Blocks-[B.Balaei]Order Blocks -

**Description:**

The Order Blocks - indicator is a powerful tool designed to identify and visualize Order Blocks on your chart. Order Blocks are key levels where significant buying or selling activity has occurred, often acting as support or resistance zones. This indicator supports multiple timeframes (MTF), allowing you to analyze Order Blocks from higher timeframes directly on your current chart.

**Key Features:**

1. **Multi-Timeframe Support**: Choose any timeframe (e.g., Daily, Weekly) to display Order Blocks from higher timeframes.

2. **Customizable Sensitivity**: Adjust the sensitivity to detect more or fewer Order Blocks based on market conditions.

3. **Bullish & Bearish Order Blocks**: Clearly distinguishes between bullish (green) and bearish (red) Order Blocks.

4. **Alerts**: Get notified when price enters a Bullish or Bearish Order Block zone.

5. **Customizable Colors**: Personalize the appearance of Order Blocks to match your chart style.

**How to Use:**

1. Add the indicator to your chart.

2. Select your desired timeframe from the "Multi-Timeframe" settings.

3. Adjust the sensitivity and colors as needed.

4. Watch for Order Blocks to form and use them as potential support/resistance levels.

**Ideal For:**

- Swing traders and position traders looking for key levels.

- Traders who use multi-timeframe analysis.

- Anyone interested in understanding market structure through Order Blocks.

**Note:**

This indicator is for educational and informational purposes only. Always conduct your own analysis before making trading decisions.

**Enjoy trading with Order Blocks - !**

Ivan Gomes StrategyIG Signals+ - Ivan Gomes Strategy

This script is designed for scalping and binary options trading, generating buy and sell signals at the beginning of each candle. Although it is mainly optimized for short-term operations, it can also be used for medium and long-term strategies with appropriate adjustments.

How It Works

• The indicator provides buy or sell signals at the start of the candle, based on a statistical probability of candle patterns, depending on the timeframe.

• It is essential to enter the trade immediately after the signal appears and exit at the end of the same candle.

• If the first operation results in a loss (Loss), the script will send another trade signal at the start of the next candle. However, if the first trade results in a win (Gain), no new signal will be generated.

• The signals follow cycles of 3 candles, regardless of the timeframe. However, if a Doji candle appears, the cycle is interrupted, and no signals will be generated until the next valid cycle starts.

• The strategy consists of up to two trades per cycle: if the first trade is not successful, the second trade serves as an additional attempt to recover.

Key Points to Consider

1. Avoid trading in sideways markets – If price levels do not fluctuate significantly, the accuracy of the signals may decrease.

2. Trade in the direction of the trend – Using Ichimoku clouds or other trend indicators can help confirm trend direction and improve signal reliability. If the market is in an uptrend (bullish trend) and the indicator generates a sell signal, the most prudent decision would be to wait for a buy signal that aligns with the main trend. The same applies to downtrends, where buy signals may be riskier.

These decisions should be based on chart reading and supported by other technical analysis tools, such as support and resistance levels, which indicate zones where price might face obstacles or reverse direction. Additionally, Fibonacci retracement levels can help identify possible pullback points within a trend. Moving averages are also useful for visualizing the general market direction and confirming whether an indicator signal aligns with the overall price structure. Combining these tools can increase trade accuracy and prevent unnecessary trades against the main trend, reducing risks.

3. Works based on probability statistics – The algorithm analyzes candle formations and their statistical probabilities depending on the timeframe to optimize trade entries.

4. Best suited for scalping and binary options – This strategy performs best in 1-minute and 5-minute timeframes, allowing for multiple trades throughout the day.

Technical Details

• The script detects the candle cycle and assigns an index to each candle to identify patterns and possible reversals.

• It recognizes reference candles, stores their colors, and compares them with subsequent candles to determine if a signal should be triggered.

• Doji candle rules are implemented to avoid false signals in indecisive market conditions. When a Doji appears, the script does not generate signals for that cycle.

• The indicator displays visual alerts and notifications, ensuring fast execution of trades.

Disclaimer

The IG Signals+ indicator was created to assist traders who struggle to analyze the market by providing objective trade signals. However, no strategy is foolproof, and this script does not guarantee profits.

Trading involves significant financial risk, and users should test it in a demo account before trading with real money. Proper risk management is crucial for long-term success.

Multi-Timeframe VWAP Master ProThe Multi-Timeframe VWAP Suite is a comprehensive and highly customizable indicator designed for traders who rely on Volume-Weighted Average Price (VWAP) across multiple timeframes and periods. This tool provides a complete suite of VWAP calculations, including daily, weekly, monthly, quarterly, yearly, and custom VWAPs, allowing traders to analyze price action and volume trends with precision. Whether you're a day trader, swing trader, or long-term investor, this indicator offers unparalleled flexibility and depth for your trading strategy.

Multi-Timeframe VWAPs:

Daily, Weekly, Monthly, Quarterly, and Yearly VWAPs: Track VWAP across various timeframes to identify key support and resistance levels.

Customizable Timeframes: Use the SMA timeframe input to adjust the period for moving averages and other calculations.

Previous Period VWAPs:

Previous Daily, Weekly, Monthly, and Quarterly VWAPs: Analyze historical VWAP levels to understand past price behavior and identify potential reversal zones.

Previous Year Quarterly VWAPs: Compare current price action to VWAP levels from specific quarters of the previous year.

Custom VWAPs:

Custom Start Date and Timeframe: Define your own VWAP periods by specifying a start date and timeframe, allowing for tailored analysis.

Dynamic Custom VWAP Calculation: Automatically calculates VWAP based on your custom inputs, ensuring flexibility for unique trading strategies.

Seasonal and Yearly VWAPs:

April, July, and October VWAPs: Analyze seasonal trends by tracking VWAP levels for specific months.

Yearly VWAP: Get a broader perspective on long-term price trends with the yearly VWAP.

SMA Integration:

SMA Overlay: Combine VWAP analysis with a Simple Moving Average (SMA) for additional confirmation of trends and reversals.

Customizable SMA Length and Timeframe: Adjust the SMA settings to match your trading style and preferences.

User-Friendly Customization:

Toggle Visibility and Labels: Easily enable or disable the display of specific VWAPs and their labels to keep your chart clean and focused.

Color Customization: Each VWAP line and label is color-coded for easy identification and can be customized to suit your preferences.

Dynamic Labeling:

Automatic Labels: Labels are dynamically placed on the last bar, providing clear and concise information about each VWAP level.

Customizable Label Text: Labels include detailed information, such as the timeframe or custom period, for quick reference.

Flexible Timeframe Detection:

Automatic Timeframe Detection: The indicator automatically detects new days, weeks, months, and quarters, ensuring accurate VWAP calculations.

Support for Intraday and Higher Timeframes: Works seamlessly on all chart timeframes, from 1-minute to monthly charts.

Previous Year Quarterly VWAPs:

Q1, Q2, Q3, Q4 VWAPs: Compare current price action to VWAP levels from specific quarters of the previous year.

User-Selectable Year: Choose the year for which you want to calculate previous quarterly VWAPs.

Persistent Monthly VWAPs:

Option to Persist Monthly VWAPs Year-Round: Keep monthly VWAP levels visible even after the month ends for ongoing analysis.

Comprehensive Analysis: Combines multiple VWAP timeframes and periods into a single tool, eliminating the need for multiple indicators.

Customizable and Flexible: Tailor the indicator to your specific trading strategy with customizable timeframes, periods, and settings.

Enhanced Decision-Making: Gain deeper insights into price action and volume trends across different timeframes, helping you make more informed trading decisions.

Clean and Organized Charts: Toggle visibility and labels to keep your chart clutter-free while still accessing all the information you need.

Ideal For:

Day Traders: Use daily and intraday VWAPs to identify intraday support and resistance levels.

Swing Traders: Analyze weekly and monthly VWAPs to spot medium-term trends and reversals.

Long-Term Investors: Leverage quarterly and yearly VWAPs to understand long-term price behavior and key levels.

Seasonal Traders: Track April, July, and October VWAPs to capitalize on seasonal trends.

The Multi-Timeframe VWAP Suite is a powerful and versatile tool for traders of all styles and timeframes. With its comprehensive suite of VWAP calculations, customizable settings, and user-friendly design, it provides everything you need to analyze price action and volume trends with precision and confidence. Whether you're looking to fine-tune your intraday strategy or gain a broader perspective on long-term trends, this indicator has you covered.

Window Seasonality IndicatorThis is a time window seasonal returns indicator. That is, it will provide the mean returns for a given time window based on a given number of lookbacks set by the user. The script finds matching time windows, e.g., 1st week of March going back 5 years or 9:00-10:00 window of every day going 50 days, and then calculates an average return for that window close price with respect to the close price in the immediately preceding time window, e.g. last week of February or 8:00-9:00 close price, respectively.

There are 4 input options:

1) Historical Periods to Average: Set the number of matching historical windows with which to calculate an average price. The max is 730 lookback windows. Note: for monthly or weekly windows, setting too large a number will cause the script to error out.

2) Use Open Price: calculates the seasonal returns using the open price rather than close price.

3) Show Bands: select from 1 Gaussian standard deviation or a nonparamateric ranked confidence interval. As a rough heuristic, the Gaussian band requires at least 30 lookback periods, and the ranked confidence interval requires 50 or more.

4) Upper Percentile: set the upper cutoff for ranked confidence interval.

5) Lower Percentile: set the lower cutoff for ranked confidence interval.

Please be aware, this indicator does not use rigorous statistical methodology and does not imply predictive power. You'll notice the range bands are very wide. Do not trade solely based on this indicator! Certain time windows, such as weekly and monthly, will make more sense applied to commodities, where annual cycles play a role in its supply and demand dynamics. Hourly windows are more useful in looking at equities markets. I like to look at equities with 1-hr windows to see if there is some pattern to overnight behavior or for market open and close.

Trading ChecklistTrading Checklist Indicator - Your Trading Plan Companion

A clean and efficient visual checklist to maintain trading discipline and consistency. This indicator helps traders follow their trading plan systematically by providing an easy-to-use checklist of key confirmation points.

Features:

- Visual checklist with clear green/red status indicators

- Clean, non-intrusive interface

- Real-time status updates

- Easy toggle controls for each item

Key Checkpoints:

1. HTF Structure Analysis

2. Order Flow Confirmation

3. SD/OB/FVG (HTF POI) Identification

4. Liquidity Grab Verification

5. Reversal Alignment Check

Final Confirmations:

- Trade Validity Check

- POI & Stop Loss Safety

- Set and Forget Status

How to Use:

1. Add the indicator to your chart

2. Use the Settings panel to toggle each condition

3. Green dots indicate confirmed conditions

4. Red dots show pending confirmations

5. Verify all conditions before executing trades

Note: This indicator helps maintain trading discipline but should be used alongside proper technical and fundamental analysis.

Tags: #TradingChecklist #RiskManagement #TradingPlan #Trading #Technical #Strategy #Discipline

Ultimate Volatility Scanner by NHBprod - Requested by Client!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto and stock trading! This strategy is for BITCOIN but can be used on any stock or crypto. This was requested by a client so I thought I should create it and hopefully build off of it and build variants!

This script gets and compares the 14-day volatility using the ATR percentage for a list of cryptocurrencies and stocks. Cryptocurrencies are preloaded into the script, and the script will show you the TOP 5 coins in terms of volatility, and then compares it to the Bitcoin volatility as a reference. It updates these values once per day using daily timeframe data from TradingView. The coins are then sorted in descending order by their volatility.

If you don't want to use the preloaded set of coins, you have the option of inputting your own coins AND/OR stocks!

Let me know your thoughts.

RVMM IndicatorRVMM Indicator

RVMM Indicator combines four indicators: RSI, VWAP, MFI, and Momentum to provide comprehensive technical analysis. This indicator helps traders identify potential market conditions based on the interaction of these indicators.

Components of the RVMM Indicator

1. RSI (Relative Strength Index)

RSI is a momentum indicator that measures the speed and change of price movements. RSI oscillates between 0 and 100 and is used to identify overbought and oversold conditions in the market.

Buy Level: Set at 30. When RSI falls below 30, the market is considered oversold, which may suggest a potential upward trend reversal.

Sell Level: Set at 70. When RSI rises above 70, the market is considered overbought, which may suggest a potential downward trend reversal.

2. VWAP (Volume Weighted Average Price)

VWAP is an indicator that combines price and volume to calculate the average price weighted by volume. VWAP is used to identify support and resistance areas and assess the strength of price movements.

Interpretation: If the price is above the VWAP line, the market is likely in an uptrend. If the price is below the VWAP line, the market is in a downtrend.

3. MFI (Money Flow Index)

MFI is a momentum indicator that considers both price and volume. MFI oscillates between 0 and 100 and is used to identify overbought and oversold conditions in the market.

Oversold Level: Set at 20. When MFI falls below 20, the market is considered oversold.

Overbought Level: Set at 80. When MFI rises above 80, the market is considered overbought.

4. Momentum

Momentum is an indicator that measures the speed of price changes. This indicator is used to identify the strength of a trend.

Interpretation: High momentum values indicate a strong uptrend, while low momentum values indicate a strong downtrend.

How to Use the RVMM Indicator

Interpreting Market Conditions:

RSI : Check RSI values below 30 to identify oversold conditions, and above 70 to identify overbought conditions.

VWAP : Observe whether the price is above or below the VWAP line to determine if the market is in an uptrend or downtrend.

MFI : Check if MFI is below 20 to identify oversold conditions, and above 80 to identify overbought conditions.

Momentum : Analyze momentum values to gauge the strength of the current trend.

Confirming Market Conditions:

Use VWAP, MFI, and Momentum to confirm market conditions identified by RSI.

If the price is above the VWAP line, and MFI and Momentum indicate the strength of the uptrend, the market may be in a bullish phase.

If the price is below the VWAP line, and MFI and Momentum indicate the strength of the downtrend, the market may be in a bearish phase.

Risk Management:

Set stop-loss and take-profit levels based on technical analysis and your trading preferences.

Monitor the market and adjust stop-loss and take-profit levels as market conditions change.

Example of Application

Here is an example of how to use the RVMM Indicator in practice:

Bullish Phase: When the price is above the VWAP line, RSI is below 30, and MFI and Momentum indicate the strength of the uptrend, the market is likely in a bullish phase.

Bearish Phase: When the price is below the VWAP line, RSI is above 70, and MFI and Momentum indicate the strength of the downtrend, the market is likely in a bearish phase.

Ultimate T3 Fibonacci for BTC Scalping. Look at backtest report!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto trading! This strategy is for BITCOIN on the 30 minute chart since I designed it to be a scalping strategy. I calculated for trading fees, and use a small amount of capital in the backtest report. But feel free to modify the capital and how much per order to see how it changes the results:)

It is called the "Ultimate T3 Fibonacci Indicator by NHBprod" that computes and displays two T3-based moving averages derived from price data. The t3_function calculates the Tilson T3 indicator by applying a series of exponential moving averages to a combined price metric and then blending these results with specific coefficients derived from an input factor.

The script accepts several user inputs that toggle the use of the T3 filter, select the buy signal method, and set parameters like lengths and volume factors for two variations of the T3 calculation. Two T3 lines, T3 and T32, are computed with different parameters, and their colors change dynamically (green/red for T3 and blue/purple for T32) based on whether the lines are trending upward or downward. Depending on the selected signal method, the script generates buy signals either when T32 crosses over T3 or when the closing price is above T3, and similarly, sell signals are generated on the respective conditions for crossing under or closing below. Finally, the indicator plots the T3 lines on the chart, adds visual buy/sell markers, and sets alert conditions to notify users when the respective trading signals occur.

The user has the ability to tune the parameters using TP/SL, date timerames for analyses, and the actual parameters of the T3 function including the buy/sell signal! Lastly, the user has the option of trading this long, short, or both!

Let me know your thoughts and check out the backtest report!

Statistical Arbitrage Pairs Trading - Long-Side OnlyThis strategy implements a simplified statistical arbitrage (" stat arb ") approach focused on mean reversion between two correlated instruments. It identifies opportunities where the spread between their normalized price series (Z-scores) deviates significantly from historical norms, then executes long-only trades anticipating reversion to the mean.

Key Mechanics:

1. Spread Calculation: The strategy computes Z-scores for both instruments to normalize price movements, then tracks the spread between these Z-scores.

2. Modified Z-Score: Uses a robust measure combining the median and Median Absolute Deviation (MAD) to reduce outlier sensitivity.

3. Entry Signal: A long position is triggered when the spread’s modified Z-score falls below a user-defined threshold (e.g., -1.0), indicating extreme undervaluation of the main instrument relative to its pair.

4. Exit Signal: The position closes automatically when the spread reverts to its historical mean (Z-score ≥ 0).

Risk management:

Trades are sized as a percentage of equity (default: 10%).

Includes commissions and slippage for realistic backtesting.

TVMC - Composite Indicator with Technical RatingsDescription:

The TVMC (Trend, Volume, Momentum, Composite) indicator is a powerful multi-component tool designed to provide traders with a comprehensive understanding of market conditions. By combining four essential technical analysis components—trend, momentum, volume, and volatility—this indicator offers clear and actionable insights to assist in decision-making.

Key Features:

1. Trend Component (TC):

* Based on MACD (Moving Average Convergence Divergence), this component analyzes the relationship between two exponential moving averages (fast and slow) to determine the prevailing market trend.

* The MACD signal is normalized to a range of -1 to +1 for consistency and clarity.

2. Momentum Component (MC):

* Utilizes RSI (Relative Strength Index) to measure the strength and speed of price movements.

* This component highlights overbought or oversold conditions, which may indicate potential market reversals.

3. Volume Confirmation (VC):

* Compares the current trading volume to its moving average over a specified period.

* High volume relative to the average confirms the validity of the current trend.

4. Volatility Filter (VF):

* Uses ATR (Average True Range) to gauge market volatility.

* Adjusts and smooths signals to reduce noise during periods of high volatility.

5. Technical Ratings Integration:

* Incorporates TradingView’s Technical Ratings, allowing users to validate signals using moving averages, oscillators, or a combination of both.

* Users can choose their preferred source of ratings for enhanced signal confirmation.

How It Works:

The TVMC indicator combines the weighted contributions of the Trend, Momentum, and Volume components, further refined by the Volatility Filter. Each component plays a specific role:

* Trend: Identifies whether the market is bullish, bearish, or neutral.

* Momentum: Highlights the strength of price action.

* Volume: Confirms whether the current price action is supported by sufficient trading activity.

* Volatility: Filters out excessive noise in volatile market conditions, providing a smoother and more reliable output.

Visualization:

1. Bullish Signals:

* The indicator line turns green and remains above the zero line, indicating upward momentum.

2. Bearish Signals:

* The indicator line turns red and falls below the zero line, signaling downward momentum.

3. Neutral Signals:

* The line is orange and stays near zero, indicating a lack of strong trend or momentum.

4. Zones:

* Horizontal lines at +30 and -30 mark strong bullish and bearish zones, respectively.

* A zero line is included for clear separation between bullish and bearish signals.

Recommended Usage:

* Best Timeframes: The indicator is optimized for higher timeframes such as 4-hour (H4) and daily (D1) charts.

* Trading Style: Suitable for swing and positional trading.

* Customization: The indicator allows users to adjust all major parameters (e.g., MACD, RSI, volume, and ATR settings) to fit their trading preferences.

Customization Options:

* Adjustable weights for Trend, Momentum, and Volume components.

* Fully configurable settings for MACD, RSI, Volume SMA, and ATR periods.

* Timeframe selection for multi-timeframe analysis.

Important Notes:

1. Originality: The TVMC indicator combines multiple analysis methods into a unique framework. It does not replicate or minimally modify existing indicators.

2. Transparency: The description is detailed enough for users to understand the methodology without requiring access to the code.

3. Clarity: The indicator is explained in a way that is accessible even to users unfamiliar with complex technical analysis tools.

Compliance with TradingView Rules:

* The indicator is written in Pine Script version 5, adhering to TradingView’s language standards.

* The description is written in English to ensure accessibility to the global community, with a clear explanation of all components and functionality.

* No promotional content, links, or unrelated references are included.

* The chart accompanying the indicator is clean and demonstrates its intended use clearly, with no additional indicators unless explicitly explained.

Enhanced Cumulative Volume Delta + MAThe Enhanced Cumulative Volume Delta (CVD) indicator is designed to help traders analyze the cumulative buying and selling pressure in the market by examining the delta between the up and down volume. By tracking this metric, traders can gain insights into the strength of a trend and potential reversals. This indicator uses advanced volume analysis combined with customizable moving averages to provide a more detailed view of market dynamics.

How to Use This Indicator:

Volume Delta Visualization:

The indicator plots the cumulative volume delta (CVD) using color-coded candles, where teal represents positive delta (buying pressure) and soft red represents negative delta (selling pressure).

Moving Averages:

Use the moving averages to smooth the CVD data and identify long-term trends. You can choose between SMA and EMA for each of the three available moving averages. The first and third moving averages are typically used for short-term and long-term trend analysis, respectively, while the second moving average can serve as a medium-term filter.

Arrow Markers:

The indicator will display arrows (green triangle up for crossing above, red triangle down for crossing below) when the CVD volume crosses the 3rd moving average. You can control the visibility of these arrows through the input parameters.

Volume Data:

The indicator provides error handling in case no volume data is available for the selected symbol, ensuring that you're not misled by incomplete data.

Practical Applications:

Trend Confirmation: Use the CVD and moving averages to confirm the overall trend direction and strength. Positive delta and a rising CVD can confirm an uptrend, while negative delta and a falling CVD indicate a downtrend.

Volume Breakouts: The arrows marking when the CVD crosses the 3rd moving average can help you spot potential volume breakouts or reversals, making them useful for entry or exit signals.

Volume Divergence: Pay attention to divergences between price and CVD, as these can often signal potential trend reversals or weakening momentum.

RShar Seasonal RSISeasonal RSI

This indicator, Seasonal RSI, is designed to enhance trading decisions by combining the **Relative Strength Index (RSI)** with insights derived from historical **seasonality patterns**. It not only calculates RSI but also overlays seasonality data for the current week of the year, providing traders with a more contextualized view of market conditions.

---

### **Key Features**

#### 1. **Relative Strength Index (RSI) Calculation**

- The script calculates the RSI for a user-defined period (`RSI Length`), which is an oscillator used to measure the speed and magnitude of price changes.

- RSI values are plotted on the chart, helping traders identify **overbought** and **oversold** conditions.

- Thresholds for **Overbought** and **Oversold** levels are customizable, with default values of 70 and 30, respectively.

---

#### 2. **Dynamic RSI Coloring Based on Seasonality**

- The color of the RSI line dynamically adjusts based on historical **win rates** for the current week of the year:

- **Bright Green** for win rates > 65%.

- **Green** for win rates between 50-65%.

- **Red** for win rates between 35-50%.

- **Dark Red** for win rates < 35%.

- This feature gives traders a quick visual cue about whether the historical performance of the current week tends to be bullish, neutral, or bearish.

---

#### 3. **Overbought and Oversold Level Visualization**

- Overbought and oversold levels are displayed as dotted horizontal lines on the RSI chart.

- These levels act as visual guides for potential price reversals:

- **Overbought (default 70)**: Indicates potential selling pressure.

- **Oversold (default 30)**: Indicates potential buying pressure.

---

#### 4. **Seasonality Data Integration**

- Historical **seasonality data** is used to analyze price performance patterns for each week of the year:

- **Win Rate**: The percentage of years in which prices closed higher during the current week.

- **Average Weekly Change**: The average price percentage change during the current week over historical data.

- This data provides additional context to RSI readings, helping traders align their strategies with seasonal tendencies.

---

#### 5. **Information Table Overlay**

- A table is displayed in the **top-right corner** of the chart, summarizing seasonality data for the current week:

- **Week Win Rate**: Displays the percentage of historical years where prices rose during this week.

- **Avg Weekly Change**: Shows the average percentage price change for the current week. Positive values are displayed in green, and negative values are shown in red.

- This overlay provides actionable insights without cluttering the chart.

---

### **How It Works**

1. **Seasonality Data**:

- A function (`getSeasonalityForWeek`) fetches or uses predefined mock seasonality data for each week of the year.

- For each week, it calculates:

- The **Win Rate** (percentage of years with positive performance).

- The **Mean Change** (average price percentage change).

2. **RSI Plot**:

- The RSI line is plotted on the chart.

- The line's color is determined by the win rate for the current week, providing a visual representation of historical performance trends.

3. **Threshold Visualization**:

- Horizontal lines for overbought and oversold levels are drawn to assist in identifying potential reversal points.

4. **Information Table**:

- The table summarizes the current week's seasonality data for quick reference, helping traders make data-driven decisions.

---

### **Use Cases**

- **Short-Term Traders**:

Use the dynamic RSI colors and seasonality table to align short-term trades with historical patterns of weekly performance.

- **Swing Traders**:

Identify whether a stock or market is in an overbought/oversold condition while considering the seasonal tendency for the week.

- **Contextual Decision-Making**:

Combine traditional RSI signals with historical data to reduce false signals and improve timing.

---

### **Limitations**

- The script uses **mock seasonality data** in its default state. To make it fully functional, replace the mock data with actual historical performance metrics for your specific ticker or market.

- The indicator does not fetch real-time external data due to Pine Script’s limitations, so all seasonality data must be manually updated or hardcoded.

---

This indicator provides a powerful way to combine technical analysis with historical trends, offering a unique edge to traders by adding seasonal context to RSI signals.

Adaptive Fourier Transform Supertrend [QuantAlgo]Discover a brand new way to analyze trend with Adaptive Fourier Transform Supertrend by QuantAlgo , an innovative technical indicator that combines the power of Fourier analysis with dynamic Supertrend methodology. In essence, it utilizes the frequency domain mathematics and the adaptive volatility control technique to transform complex wave patterns into clear and high probability signals—ideal for both sophisticated traders seeking mathematical precision and investors who appreciate robust trend confirmation!

🟢 Core Architecture

At its core, this indicator employs an adaptive Fourier Transform framework with dynamic volatility-controlled Supertrend bands. It utilizes multiple harmonic components that let you fine-tune how market frequencies influence trend detection. By combining wave analysis with adaptive volatility bands, the indicator creates a sophisticated yet clear framework for trend identification that dynamically adjusts to changing market conditions.

🟢 Technical Foundation

The indicator builds on three innovative components:

Fourier Wave Analysis: Decomposes price action into primary and harmonic components for precise trend detection

Adaptive Volatility Control: Dynamically adjusts Supertrend bands using combined ATR and standard deviation

Harmonic Integration: Merges multiple frequency components with decreasing weights for comprehensive trend analysis

🟢 Key Features & Signals

The Adaptive Fourier Transform Supertrend transforms complex wave calculations into clear visual signals with:

Dynamic trend bands that adapt to market volatility

Sophisticated cloud-fill visualization system

Strategic L/S markers at key trend reversals

Customizable bar coloring based on trend direction

Comprehensive alert system for trend shifts

🟢 Practical Usage Tips

Here's how you can get the most out of the Adaptive Fourier Transform Supertrend :

1/ Setup:

Add the indicator to your favorites, then apply it to your chart ⭐️

Start with close price as your base source

Use standard Fourier period (14) for balanced wave detection

Begin with default harmonic weight (0.5) for balanced sensitivity

Start with standard Supertrend multiplier (2.0) for reliable band width

2/ Signal Interpretation:

Monitor trend band crossovers for potential signals

Watch for convergence of price with Fourier trend

Use L/S markers for trade entry points

Monitor bar colors for trend confirmation

Configure alerts for significant trend reversals

🟢 Pro Tips

Fine-tune Fourier parameters for optimal sensitivity:

→ Lower Base Period (8-12) for more reactive analysis

→ Higher Base Period (15-30) to filter out noise

→ Adjust Harmonic Weight (0.3-0.7) to control shorter trend influence

Customize Supertrend settings:

→ Lower multiplier (1.5-2.0) for tighter bands

→ Higher multiplier (2.0-3.0) for wider bands

→ Adjust ATR length based on market volatility

Strategy Enhancement:

→ Compare signals across multiple timeframes

→ Combine with volume analysis

→ Use with support/resistance levels

→ Integrate with other momentum indicators

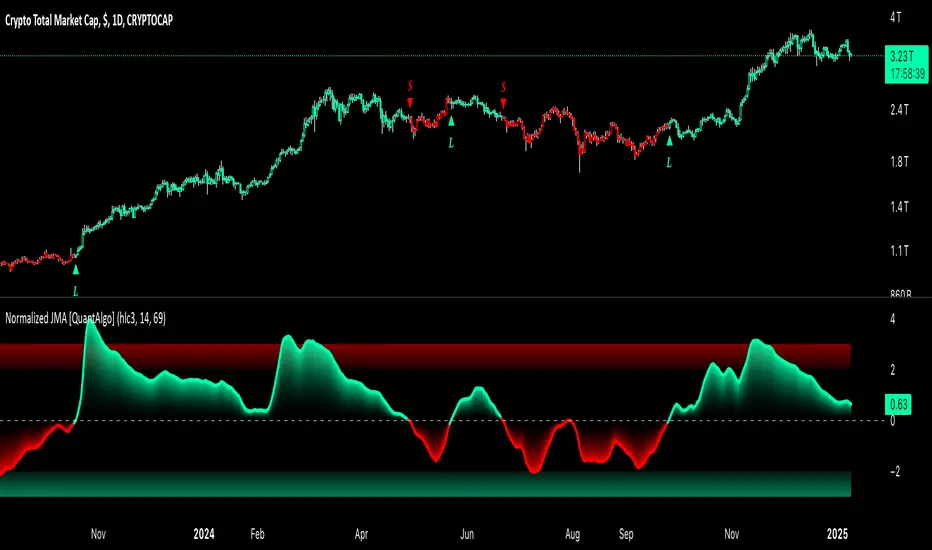

Normalized Jurik Moving Average [QuantAlgo]Upgrade your investing and trading strategy with the Normalized Jurik Moving Average (JMA) , a sophisticated oscillator that combines adaptive smoothing with statistical normalization to deliver high-quality signals! Whether you're a swing trader looking for momentum shifts or a medium- to long-term investor focusing on trend validation, this indicator's statistical approach offers valuable analytical advantages that can enhance your trading and investing decisions!

🟢 Core Architecture

The foundation of this indicator lies in its unique dual-layer calculation system. The first layer implements the Jurik Moving Average, known for its superior noise reduction and responsiveness, while the second layer applies statistical normalization (Z-Score) to create standardized readings. This sophisticated approach helps identify significant price movements while filtering out market noise across various timeframes and instruments.

🟢 Technical Foundation

Three key components power this indicator are:

Jurik Moving Average (JMA): An advanced moving average calculation that provides superior smoothing with minimal lag

Statistical Normalization: Z-Score based scaling that creates consistent, comparable readings across different market conditions

Dynamic Zone Detection: Automatically identifies overbought and oversold conditions based on statistical deviations

🟢 Key Features & Signals

The Normalized JMA delivers market insights through:

Color-adaptive oscillator line that reflects momentum strength and direction

Statistically significant overbought/oversold zones for trade validation

Smart gradient fills between signal line and zero level for enhanced visualization

Clear long (L) and short (S) markers for validated momentum shifts

Intelligent bar coloring that highlights the current market state

Customizable alert system for both bullish and bearish setups

🟢 Practical Usage Tips

Here's how to maximize your use of the Normalized JMA:

1/ Setup:

Add the indicator to your favorites, then apply it to your chart ⭐️

Begin with the default smoothing period for balanced analysis

Use the default normalization period for optimal signal generation

Start with standard visualization settings

Customize colors to match your chart preferences

Enable both bar coloring and signal markers for complete visual feedback

2/ Reading Signals:

Watch for L/S markers - they indicate validated momentum shifts

Monitor oscillator line color changes for direction confirmation

Use the built-in alert system to stay informed of potential trend changes

🟢 Pro Tips

Adjust Smoothing Period based on your trading style:

→ Lower values (8-12) for more responsive signals

→ Higher values (20-30) for more stable trend identification

Fine-tune Normalization Period based on market conditions:

→ Shorter periods (20-25) for more dynamic markets

→ Longer periods (40-50) for more stable markets

Optimize your analysis by:

→ Using +2/-2 zones for primary trade signals

→ Using +3/-3 zones for extreme market conditions

→ Combining with volume analysis for trade confirmation

→ Using multiple timeframe analysis for strategic context

Combine with:

→ Volume indicators for trade validation

→ Price action for entry timing

→ Support/resistance levels for profit targets

→ Trend-following indicators for directional bias

Relative Performance Indicator by ComLucro - 2025_V01The "Relative Performance Indicator by ComLucro - 2025_V01" is a powerful tool designed to analyze an asset's performance relative to a benchmark index over multiple timeframes. This indicator provides traders with a clear view of how their chosen asset compares to a market index in short, medium, and long-term periods.

Key Features:

Customizable Lookback Periods: Analyze performance across three adjustable periods (default: 20, 50, and 200 bars).

Relative Performance Analysis: Calculate and visualize the difference in percentage performance between the asset and the benchmark index.

Dynamic Summary Label: Displays a detailed breakdown of the asset's and index's performance for the latest bar.

User-Friendly Interface: Includes customizable colors and display options for clear visualization.

How It Works:

The script fetches closing prices of both the asset and a benchmark index.

It calculates percentage changes over the selected lookback periods.

The indicator then computes the relative performance difference between the asset and the index, plotting it on the chart for easy trend analysis.

Who Is This For?:

Traders and investors who want to compare an asset’s performance against a benchmark index.

Those looking to identify trends and deviations between an asset and the broader market.

Disclaimer:

This tool is for educational purposes only and does not constitute financial or trading advice. Always use it alongside proper risk management strategies and backtest thoroughly before applying it to live trading.

Chart Recommendation:

Use this script on clean charts for better clarity. Combine it with other technical indicators like moving averages or trendlines to enhance your analysis. Ensure you adjust the lookback periods to match your trading style and the timeframe of your analysis.

Additional Notes:

For optimal performance, ensure the benchmark index's data is available on your TradingView subscription. The script uses fallback mechanisms to avoid interruptions when index data is unavailable. Always validate the settings and test them to suit your trading strategy.

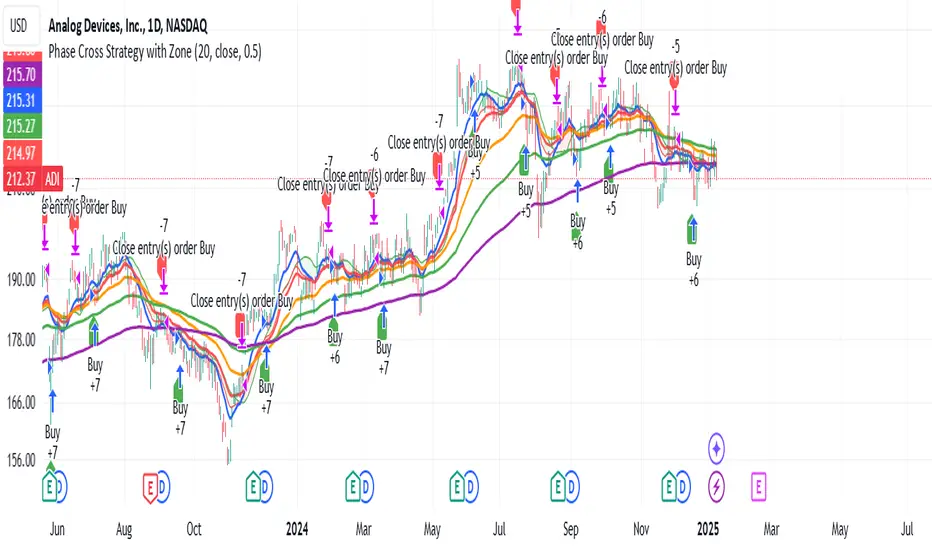

Phase Cross Strategy with Zone### Introduction to the Strategy

Welcome to the **Phase Cross Strategy with Zone and EMA Analysis**. This strategy is designed to help traders identify potential buy and sell opportunities based on the crossover of smoothed oscillators (referred to as "phases") and exponential moving averages (EMAs). By combining these two methods, the strategy offers a versatile tool for both trend-following and short-term trading setups.

### Key Features

1. **Phase Cross Signals**:

- The strategy uses two smoothed oscillators:

- **Leading Phase**: A simple moving average (SMA) with an upward offset.

- **Lagging Phase**: An exponential moving average (EMA) with a downward offset.

- Buy and sell signals are generated when these phases cross over or under each other, visually represented on the chart with green (buy) and red (sell) labels.

2. **Phase Zone Visualization**:

- The area between the two phases is filled with a green or red zone, indicating bullish or bearish conditions:

- Green zone: Leading phase is above the lagging phase (potential uptrend).

- Red zone: Leading phase is below the lagging phase (potential downtrend).

3. **EMA Analysis**:

- Includes five commonly used EMAs (13, 26, 50, 100, and 200) for additional trend analysis.

- Crossovers of the EMA 13 and EMA 26 act as secondary buy/sell signals to confirm or enhance the phase-based signals.

4. **Customizable Parameters**:

- You can adjust the smoothing length, source (price data), and offset to fine-tune the strategy for your preferred trading style.

### What to Pay Attention To

1. **Phases and Zones**:

- Use the green/red phase zone as an overall trend guide.

- Avoid taking trades when the phases are too close or choppy, as it may indicate a ranging market.

2. **EMA Trends**:

- Align your trades with the longer-term trend shown by the EMAs. For example:

- In an uptrend (price above EMA 50 or EMA 200), prioritize buy signals.

- In a downtrend (price below EMA 50 or EMA 200), prioritize sell signals.

3. **Signal Confirmation**:

- Consider combining phase cross signals with EMA crossovers for higher-confidence trades.

- Look for confluence between the phase signals and EMA trends.

4. **Risk Management**:

- Always set stop-loss and take-profit levels to manage risk.

- Use the phase and EMA zones to estimate potential support/resistance areas for exits.

5. **Whipsaws and False Signals**:

- Be cautious in low-volatility or sideways markets, as the strategy may generate false signals.

- Use additional indicators or filters to avoid entering trades during unclear market conditions.

### How to Use

1. Add the strategy to your chart in TradingView.

2. Adjust the input settings (e.g., smoothing length, offsets) to suit your trading preferences.

3. Enable the strategy tester to evaluate its performance on historical data.

4. Combine the signals with your own analysis and risk management plan for best results.

This strategy is a versatile tool, but like any trading method, it requires proper understanding and discretion. Always backtest thoroughly and trade with discipline. Let me know if you need further assistance or adjustments to the strategy!