remaLibrary " REMA "

Custom Regional Exponential Moving Average with enhanced sensitivity to recent price action

Description: What Makes REMA Unique?

REMA introduces a dual-region weighting system that intelligently balances short-term responsiveness with long-term trend context, solving the fundamental limitation of standard EMAs where longer periods necessarily sacrifice recent price sensitivity.

Key Differences from Standard EMA:

Adaptive Regional Weighting: Applies stronger exponential decay to recent price data while maintaining appropriate weighting for historical context.

Maintains Responsiveness at Any Length: Unlike standard EMAs where longer periods become progressively less responsive, REMA preserves significant sensitivity to recent price action even at 100+ period lengths.

Mathematically Sound Enhancement: Preserves the core mathematical integrity of exponential averaging while introducing region-specific weighting that better reflects how traders actually interpret price action.

Value to TradingView Community:

Improved Signal Timing: Detects reversals 1-3 bars earlier than traditional EMAs without increasing false signals.

Better Multi-Timeframe Analysis: Provides more consistent behavior across different period settings, reducing conflicting signals between timeframes.

Ideal for Modern Markets: Better handles today's high-volatility, algorithm-driven markets where traditional indicators often lag too much to be effective.

Optimized for Both Trend and Reversal Trading: Simultaneously provides strong trend-following capabilities while remaining sensitive to legitimate reversal signals.

Computation Efficiency: The fast implementation offers enhanced capabilities with minimal computational overhead, making it practical for real-time analysis.

REMA fills a critical gap between lagging long-period EMAs and noisy short-period EMAs, giving traders a single, versatile tool that adapts to market conditions more effectively than standard technical indicators.

Implementation:

rema(src, length, recency_bias, transition_point)

Regional Exponential Moving Average that maintains recent price sensitivity even with long lookback periods

Parameters:

src (float) : Input source series

length (int) : Overall EMA period length

recency_bias (float) : Weighting factor to increase sensitivity to recent prices (1.0-3.0 recommended)

transition_point (float) : Percentage point (0.0-1.0) in the lookback period where weighting shifts from recent to historical

Returns: Custom exponentially weighted moving average with regional bias

rema_fast(src, length, recency_bias)

Simplified Regional EMA that uses a recursive calculation method

Parameters:

src (float) : Input source series

length (int) : Overall EMA period

recency_bias (float) : Factor to increase sensitivity to recent price (1.0-3.0 recommended)

Returns: Computationally efficient regional EMA

Techindicator

AllCandlestickPatternsLibraryAll Candlestick Patterns Library

The Candlestick Patterns Library is a Pine Script (version 6) library extracted from the All Candlestick Patterns indicator. It provides a comprehensive set of functions to calculate candlestick properties, detect market trends, and identify various candlestick patterns (bullish, bearish, and neutral). The library is designed for reusability, enabling TradingView users to incorporate pattern detection into their own scripts, such as indicators or strategies.

The library is organized into three main sections:

Trend Detection: Functions to determine market trends (uptrend or downtrend) based on user-defined rules.

Candlestick Property Calculations: A function to compute core properties of a candlestick, such as body size, shadow lengths, and doji characteristics.

Candlestick Pattern Detection: Functions to detect specific candlestick patterns, each returning a tuple with detection status, pattern name, type, and description.

Library Structure

1. Trend Detection

This section includes the detectTrend function, which identifies whether the market is in an uptrend or downtrend based on user-specified rules, such as the relationship between the closing price and Simple Moving Averages (SMAs).

Function: detectTrend

Parameters:

downTrend (bool): Initial downtrend condition.

upTrend (bool): Initial uptrend condition.

trendRule (string): The rule for trend detection ("SMA50" or "SMA50, SMA200").

p_close (float): Current closing price.

sma50 (float): Simple Moving Average over 50 periods.

sma200 (float): Simple Moving Average over 200 periods.

Returns: A tuple indicating the detected trend.

Logic:

If trendRule is "SMA50", a downtrend is detected when p_close < sma50, and an uptrend when p_close > sma50.

If trendRule is "SMA50, SMA200", a downtrend is detected when p_close < sma50 and sma50 < sma200, and an uptrend when p_close > sma50 and sma50 > sma200.

2. Candlestick Property Calculations

This section includes the calculateCandleProperties function, which computes essential properties of a candlestick based on OHLC (Open, High, Low, Close) data and configuration parameters.

Function: calculateCandleProperties

Parameters:

p_open (float): Candlestick open price.

p_close (float): Candlestick close price.

p_high (float): Candlestick high price.

p_low (float): Candlestick low price.

bodyAvg (float): Average body size (e.g., from EMA of body sizes).

shadowPercent (float): Minimum shadow size as a percentage of body size.

shadowEqualsPercent (float): Tolerance for equal shadows in doji detection.

dojiBodyPercent (float): Maximum body size as a percentage of range for doji detection.

Returns: A tuple containing 17 properties:

C_BodyHi (float): Higher of open or close price.

C_BodyLo (float): Lower of open or close price.

C_Body (float): Body size (difference between C_BodyHi and C_BodyLo).

C_SmallBody (bool): True if body size is below bodyAvg.

C_LongBody (bool): True if body size is above bodyAvg.

C_UpShadow (float): Upper shadow length (p_high - C_BodyHi).

C_DnShadow (float): Lower shadow length (C_BodyLo - p_low).

C_HasUpShadow (bool): True if upper shadow exceeds shadowPercent of body.

C_HasDnShadow (bool): True if lower shadow exceeds shadowPercent of body.

C_WhiteBody (bool): True if candle is bullish (p_open < p_close).

C_BlackBody (bool): True if candle is bearish (p_open > p_close).

C_Range (float): Candlestick range (p_high - p_low).

C_IsInsideBar (bool): True if current candle body is inside the previous candle's body.

C_BodyMiddle (float): Midpoint of the candle body.

C_ShadowEquals (bool): True if upper and lower shadows are equal within shadowEqualsPercent.

C_IsDojiBody (bool): True if body size is small relative to range (C_Body <= C_Range * dojiBodyPercent / 100).

C_Doji (bool): True if the candle is a doji (C_IsDojiBody and C_ShadowEquals).

Purpose: These properties are used by pattern detection functions to evaluate candlestick formations.

3. Candlestick Pattern Detection

This section contains functions to detect specific candlestick patterns, each returning a tuple . The patterns are categorized as bullish, bearish, or neutral, and include detailed descriptions for use in tooltips or alerts.

Supported Patterns

The library supports the following candlestick patterns, grouped by type:

Bullish Patterns:

Rising Window: A two-candle continuation pattern in an uptrend with a price gap between the first candle's high and the second candle's low.

Rising Three Methods: A five-candle continuation pattern with a long green candle, three short red candles, and another long green candle.

Tweezer Bottom: A two-candle reversal pattern in a downtrend with nearly identical lows.

Upside Tasuki Gap: A three-candle continuation pattern in an uptrend with a gap between the first two green candles and a red candle closing partially into the gap.

Doji Star (Bullish): A two-candle reversal pattern in a downtrend with a long red candle followed by a doji gapping down.

Morning Doji Star: A three-candle reversal pattern with a long red candle, a doji gapping down, and a long green candle.

Piercing: A two-candle reversal pattern in a downtrend with a red candle followed by a green candle closing above the midpoint of the first.

Hammer: A single-candle reversal pattern in a downtrend with a small body and a long lower shadow.

Inverted Hammer: A single-candle reversal pattern in a downtrend with a small body and a long upper shadow.

Morning Star: A three-candle reversal pattern with a long red candle, a short candle gapping down, and a long green candle.

Marubozu White: A single-candle pattern with a long green body and minimal shadows.

Dragonfly Doji: A single-candle reversal pattern in a downtrend with a doji where open and close are at the high.

Harami Cross (Bullish): A two-candle reversal pattern in a downtrend with a long red candle followed by a doji inside its body.

Harami (Bullish): A two-candle reversal pattern in a downtrend with a long red candle followed by a small green candle inside its body.

Long Lower Shadow: A single-candle pattern with a long lower shadow indicating buyer strength.

Three White Soldiers: A three-candle reversal pattern with three long green candles in a downtrend.

Engulfing (Bullish): A two-candle reversal pattern in a downtrend with a small red candle followed by a larger green candle engulfing it.

Abandoned Baby (Bullish): A three-candle reversal pattern with a long red candle, a doji gapping down, and a green candle gapping up.

Tri-Star (Bullish): A three-candle reversal pattern with three doji candles in a downtrend, with gaps between them.

Kicking (Bullish): A two-candle reversal pattern with a bearish marubozu followed by a bullish marubozu gapping up.

Bearish Patterns:

On Neck: A two-candle continuation pattern in a downtrend with a long red candle followed by a short green candle closing near the first candle's low.

Falling Window: A two-candle continuation pattern in a downtrend with a price gap between the first candle's low and the second candle's high.

Falling Three Methods: A five-candle continuation pattern with a long red candle, three short green candles, and another long red candle.

Tweezer Top: A two-candle reversal pattern in an uptrend with nearly identical highs.

Dark Cloud Cover: A two-candle reversal pattern in an uptrend with a green candle followed by a red candle opening above the high and closing below the midpoint.

Downside Tasuki Gap: A three-candle continuation pattern in a downtrend with a gap between the first two red candles and a green candle closing partially into the gap.

Evening Doji Star: A three-candle reversal pattern with a long green candle, a doji gapping up, and a long red candle.

Doji Star (Bearish): A two-candle reversal pattern in an uptrend with a long green candle followed by a doji gapping up.

Hanging Man: A single-candle reversal pattern in an uptrend with a small body and a long lower shadow.

Shooting Star: A single-candle reversal pattern in an uptrend with a small body and a long upper shadow.

Evening Star: A three-candle reversal pattern with a long green candle, a short candle gapping up, and a long red candle.

Marubozu Black: A single-candle pattern with a long red body and minimal shadows.

Gravestone Doji: A single-candle reversal pattern in an uptrend with a doji where open and close are at the low.

Harami Cross (Bearish): A two-candle reversal pattern in an uptrend with a long green candle followed by a doji inside its body.

Harami (Bearish): A two-candle reversal pattern in an uptrend with a long green candle followed by a small red candle inside its body.

Long Upper Shadow: A single-candle pattern with a long upper shadow indicating seller strength.

Three Black Crows: A three-candle reversal pattern with three long red candles in an uptrend.

Engulfing (Bearish): A two-candle reversal pattern in an uptrend with a small green candle followed by a larger red candle engulfing it.

Abandoned Baby (Bearish): A three-candle reversal pattern with a long green candle, a doji gapping up, and a red candle gapping down.

Tri-Star (Bearish): A three-candle reversal pattern with three doji candles in an uptrend, with gaps between them.

Kicking (Bearish): A two-candle reversal pattern with a bullish marubozu followed by a bearish marubozu gapping down.

Neutral Patterns:

Doji: A single-candle pattern with a very small body, indicating indecision.

Spinning Top White: A single-candle pattern with a small green body and long upper and lower shadows, indicating indecision.

Spinning Top Black: A single-candle pattern with a small red body and long upper and lower shadows, indicating indecision.

Pattern Detection Functions

Each pattern detection function evaluates specific conditions based on candlestick properties (from calculateCandleProperties) and trend conditions (from detectTrend). The functions return:

detected (bool): True if the pattern is detected.

name (string): The name of the pattern (e.g., "On Neck").

type (string): The pattern type ("Bullish", "Bearish", or "Neutral").

description (string): A detailed description of the pattern for use in tooltips or alerts.

For example, the detectOnNeckBearish function checks for a bearish On Neck pattern by verifying a downtrend, a long red candle followed by a short green candle, and specific price relationships.

Usage Example

To use the library in a TradingView indicator, you can import it and call its functions as shown below:

//@version=6

indicator("Candlestick Pattern Detector", overlay=true)

import CandlestickPatternsLibrary as cp

// Calculate SMA for trend detection

sma50 = ta.sma(close, 50)

sma200 = ta.sma(close, 200)

= cp.detectTrend(true, true, "SMA50", close, sma50, sma200)

// Calculate candlestick properties

bodyAvg = ta.ema(math.max(close, open) - math.min(close, open), 14)

= cp.calculateCandleProperties(open, close, high, low, bodyAvg, 5.0, 100.0, 5.0)

// Detect a pattern (e.g., On Neck Bearish)

= cp.detectOnNeckBearish(downTrend, blackBody, longBody, whiteBody, open, close, low, bodyAvg, smallBody, candleRange)

if onNeckDetected

label.new(bar_index, low, onNeckName, style=label.style_label_up, color=color.red, textcolor=color.white, tooltip=onNeckDesc)

// Detect another pattern (e.g., Piercing Bullish)

= cp.detectPiercingBullish(downTrend, blackBody, longBody, whiteBody, open, low, close, bodyMiddle)

if piercingDetected

label.new(bar_index, low, piercingName, style=label.style_label_up, color=color.blue, textcolor=color.white, tooltip=piercingDesc)

Steps in the Example

Import the Library: Use import CandlestickPatternsLibrary as cp to access the library's functions.

Calculate Trend: Use detectTrend to determine the market trend based on SMA50 or SMA50/SMA200 rules.

Calculate Candlestick Properties: Use calculateCandleProperties to compute properties like body size, shadow lengths, and doji status.

Detect Patterns: Call specific pattern detection functions (e.g., detectOnNeckBearish, detectPiercingBullish) and use the returned values to display labels or alerts.

Visualize Patterns: Use label.new to display detected patterns on the chart with their names, types, and descriptions.

Key Features

Modularity: The library is designed as a standalone module, making it easy to integrate into other Pine Script projects.

Comprehensive Pattern Coverage: Supports over 40 candlestick patterns, covering bullish, bearish, and neutral formations.

Detailed Documentation: Each function includes comments with @param and @returns annotations for clarity.

Reusability: Can be used in indicators, strategies, or alerts by importing the library and calling its functions.

Extracted from All Candlestick Patterns: The library is derived from the All Candlestick Patterns indicator, ensuring it inherits a well-tested foundation for pattern detection.

Notes for Developers

Pine Script Version: The library uses Pine Script version 6, as specified by //@version=6.

Parameter Naming: Parameters use prefixes like p_ (e.g., p_open, p_close) to avoid conflicts with built-in variables.

Error Handling: The library has been fixed to address issues like undeclared identifiers (C_SmallBody, C_Range), unused arguments (factor), and improper comment formatting.

Testing: Developers should test the library in TradingView to ensure patterns are detected correctly under various market conditions.

Customization: Users can adjust parameters like bodyAvg, shadowPercent, shadowEqualsPercent, and dojiBodyPercent in calculateCandleProperties to fine-tune pattern detection sensitivity.

Conclusion

The Candlestick Patterns Library, extracted from the All Candlestick Patterns indicator, is a powerful tool for traders and developers looking to implement candlestick pattern detection in TradingView. Its modular design, comprehensive pattern support, and detailed documentation make it an ideal choice for building custom indicators or strategies. By leveraging the library's functions, users can analyze market trends, compute candlestick properties, and detect a wide range of patterns to inform their trading decisions.

WhispererRealtimeVolumeLibrary "WhispererRealtimeVolume"

▮ Overview

The Whisperer Realtime Volume Library is a lightweight and reusable Pine Script® library designed for real-time volume analysis.

It calculates up, down, and neutral volumes dynamically, making it an essential tool for traders who want to gain deeper insights into market activity.

This library is a simplified and modular version of the original "Realtime Volume Bars w Market Buy/Sell/Neutral split & Mkt Delta" indicator by the_MarketWhisperer , tailored for integration into custom scripts.

How bars are classified

- Up Bars

If the current bar’s closing price is higher than the previous bar’s closing price, it is classified as an up bar.

Volume handling:

The increase in volume for this bar is added to the up volume.

This represents buying pressure.

- Down Bars

If the current bar’s closing price is lower than the previous bar’s closing price, it is classified as a down bar.

Volume handling:

The increase in volume for this bar is added to the down volume.

This represents selling pressure.

- Neutral Bars

If the current bar’s closing price is the same as the previous bar’s closing price, it is classified as a neutral bar.

Volume handling:

If neutral volume is enabled, the volume is added to the neutral volume.

If neutral volume is not enabled, the volume is assigned to the same direction as the previous bar (up or down). If the previous direction is unknown, it is added to the neutral volume.

▮ What to look for

Real-Time Volume Calculation : Analyze up, down, and neutral volumes in real-time based on price movements and bar volume.

Customizable Start Line : Add a visual reference line to your chart for better context by viewing the starting point of real-time bars.

Ease of Integration : Designed as a library for seamless use in other Pine Script® indicators or strategies.

▮ How to use

Example code:

//@version=6

indicator("Volume Realtime from Whisperer")

import andre_007/WhispererRealtimeVolume/4 as MW

MW.displayStartLine(startLineColor = color.gray, startLineWidth = 1, startLineStyle = line.style_dashed,

displayStartLine = true, y1=volume, y2=volume + 10)

= MW.mw_upDownVolumeRealtime(true)

plot(volume, style=plot.style_columns, color=color.gray)

plot(volumeUp, style=plot.style_columns, color=color.green)

plot(volumeDown, style=plot.style_columns, color=color.red)

plot(volumeNeutral, style=plot.style_columns, color=color.purple)

▮ Credits

This library is inspired by the original work of the_MarketWhisperer , whose "Realtime Volume Bars" indicator served as the foundation.

Link to original indicator :

reversalchartpatternsLibrary "reversalchartpatterns"

User Defined Types and Methods for reversal chart patterns - Double Top, Double Bottom, Triple Top, Triple Bottom, Cup and Handle, Inverted Cup and Handle, Head and Shoulders, Inverse Head and Shoulders

method delete(this)

Deletes the drawing components of ReversalChartPatternDrawing object

Namespace types: ReversalChartPatternDrawing

Parameters:

this (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object

Returns: current ReversalChartPatternDrawing object

method delete(this)

Deletes the drawing components of ReversalChartPattern object. In turn calls the delete of ReversalChartPatternDrawing

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: current ReversalChartPattern object

method lpush(this, obj, limit, deleteOld)

Array push with limited number of items in the array. Old items are deleted when new one comes and exceeds the limit

Namespace types: array

Parameters:

this (array) : array object

obj (ReversalChartPattern) : ReversalChartPattern object which need to be pushed to the array

limit (int) : max items on the array. Default is 10

deleteOld (bool) : If set to true, also deletes the drawing objects. If not, the drawing objects are kept but the pattern object is removed from array. Default is false.

Returns: current ReversalChartPattern object

method draw(this)

Draws the components of ReversalChartPatternDrawing

Namespace types: ReversalChartPatternDrawing

Parameters:

this (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object

Returns: current ReversalChartPatternDrawing object

method draw(this)

Draws the components of ReversalChartPatternDrawing within the ReversalChartPattern object.

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: current ReversalChartPattern object

method scan(zigzag, patterns, errorPercent, shoulderStart, shoulderEnd, allowedPatterns, offset)

Scans zigzag for ReversalChartPattern occurences

Namespace types: zg.Zigzag

Parameters:

zigzag (Zigzag type from Trendoscope/Zigzag/11) : ZigzagTypes.Zigzag object having array of zigzag pivots and other information on each pivots

patterns (array) : Existing patterns array. Used for validating duplicates

errorPercent (float) : Error threshold for considering ratios. Default is 13

shoulderStart (float) : Starting range of shoulder ratio. Used for identifying shoulders, handles and necklines

shoulderEnd (float) : Ending range of shoulder ratio. Used for identifying shoulders, handles and necklines

allowedPatterns (array) : array of int containing allowed pattern types

offset (int) : Offset of zigzag to consider only confirmed pivots

Returns: int pattern type

method createPattern(zigzag, patternType, patternColor, properties, offset)

Create Pattern from ZigzagTypes.Zigzag object

Namespace types: zg.Zigzag

Parameters:

zigzag (Zigzag type from Trendoscope/Zigzag/11) : ZigzagTypes.Zigzag object having array of zigzag pivots and other information on each pivots

patternType (int) : Type of pattern being created. 1 - Double Tap, 2 - Triple Tap, 3 - Cup and Handle, 4 - Head and Shoulders

patternColor (color) : Color in which the patterns are drawn

properties (ReversalChartTradeProperties)

offset (int)

Returns: ReversalChartPattern object created

method getName(this)

get pattern name of ReversalChartPattern object

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: string name of the pattern

method getDescription(this)

get consolidated description of ReversalChartPattern object

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: string consolidated description

method init(this)

initializes the ReversalChartPattern object and creates sub object types

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: ReversalChartPattern current object

ReversalChartPatternDrawing

Type which holds the drawing objects for Reversal Chart Pattern Types

Fields:

patternLines (array type from Trendoscope/Drawing/2) : array of Line objects representing pattern

entry (Line type from Trendoscope/Drawing/2) : Entry price Line

targets (array type from Trendoscope/Drawing/2)

stop (Line type from Trendoscope/Drawing/2) : Stop price Line

patternLabel (Label type from Trendoscope/Drawing/2)

ReversalChartTradeProperties

Trade properties of ReversalChartPattern

Fields:

riskAdjustment (series float) : Risk Adjustment for calculation of stop

useFixedTarget (series bool) : Boolean flag saying use fixed target type wherever possible. If fixed target type is not possible, then risk reward/fib ratios are used for calculation of targets

variableTargetType (series int) : Integer value which defines whether to use fib based targets or risk reward based targets. 1 - Risk Reward, 2 - Fib Ratios

variableTargetRatios (array) : Risk reward or Fib Ratios to be used for calculation of targets when fixed target is not possible or not enabled

entryPivotForWm (series int) : which Pivot should be considered as entry point for WM patterns. 0 refers to the latest breakout pivot where as 5 refers to initial pivot of the pattern

ReversalChartPattern

Reversal Chart Pattern master type which holds the pattern components, drawings and trade details

Fields:

pivots (array type from Trendoscope/Zigzag/11) : Array of Zigzag Pivots forming the pattern

patternType (series int) : Defines the main type of pattern 1 - Double Tap, 1 - Triple Tap, 3 - Cup and Handle, 4 - Head and Shoulders, 5- W/M Patterns, 6 - Full Trend, 7 - Half Trend

patternColor (series color) : Color in which the pattern will be drawn on chart

properties (ReversalChartTradeProperties)

drawing (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object which holds the drawing components

trade (Trade type from Trendoscope/TradeTracker/1) : TradeTracker.Trade object holding trade components

CandlestickUtilitiesThis library provides essential functions for candlestick chart analysis and pattern recognition in Pine Script®.

It includes:

• Candle structure analysis (bodies, shadows, lengths)

• Trend detection using EMAs

• Common candlestick pattern recognition

This library is under construction.

Designed to support strategy development and improve signal accuracy for traders.

Created by @xprophetx — under MPL-2.0 license.

tafirstlibGeneral Purpose: Starts by stating it's a collection of utility functions for technical analysis.

Core Functionality Areas: Mentions key categories like:

Extrema detection (isMin, isMax, etc.)

Condition checking over time (isMachedInRange, isContinuous, etc.)

Rate of change analysis (isSlowDown)

Moving average calculation (getMA)

Advanced Features: Highlights the more complex functions:

Visualization helpers (getColorNew)

Moving Regression (mr) for smoothing/trend

Cycle analysis (bpDom)

Overall Goal: Concludes by stating the library's aim – simplifying development and enabling complex analysis.

Library "tafirstlib"

TODO: add library description here

isSlowDown(data)

isSlowDown

Parameters:

data (float) : array of numbers

Returns: boolean

isMin(data, maeLength)

isMin

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isMax(data, maeLength)

isMax

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isMinStopped(data, maeLength)

isMinStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isMaxStopped(data, maeLength)

isMaxStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

Returns: boolean

isLongMinStopped(data, maeLength, distance)

isLongMinStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

distance (int) : number

Returns: boolean

isLongMaxStopped(data, maeLength, distance)

isLongMaxStopped

Parameters:

data (float) : array of numbers

maeLength (int) : number

distance (int) : number

Returns: boolean

isMachedInRangeSkipCurrent(data, findRange, findValue)

isMachedInRangeSkipCurrent

Parameters:

data (bool) : array of numbers

findRange (int) : number

findValue (bool) : number

Returns: boolean

isMachedInRange(data, findRange, findValue)

isMachedInRange

Parameters:

data (bool) : array of numbers

findRange (int) : number

findValue (bool) : number

Returns: boolean

isMachedColorInRange(data, findRange, findValue)

isMachedColorInRange isMachedColorInRange(series color data, int findRange, color findValue)

Parameters:

data (color) : series of color

findRange (int) : int

findValue (color) : color

Returns: boolean

countMachedInRange(data, findRange, findValue)

countMachedInRange

Parameters:

data (bool) : array of numbers

findRange (int) : number

findValue (bool) : number

Returns: number

getColor(data)

getColor

Parameters:

data (float) : array of numbers

Returns: color

getColorNew(data)

getColorNew

Parameters:

data (float) : array of numbers

Returns: color

isColorBetter(color_data)

isColorBetter

Parameters:

color_data (color) : array of colors

Returns: boolean

isColorWorst(color_data)

isColorWorst

Parameters:

color_data (color) : array of colors

Returns: boolean

isColorBetter2(color_data)

isColorBetter2

Parameters:

color_data (color) : array of colors

Returns: boolean

isColorWorst2(color_data)

isColorWorst2

Parameters:

color_data (color) : array of colors

Returns: boolean

isDecreased2Bar(data)

isDecreased2Bar

Parameters:

data (float) : array of numbers

Returns: boolean

isContinuousAdvance(targetSeries, range2Find, howManyException)

isContinuousAdvance

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

howManyException (int) : number

Returns: boolean

isContinuous(targetSeries, range2Find, truefalse)

isContinuous

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

truefalse (bool) : boolean

Returns: boolean

isContinuousNotNow(targetSeries, range2Find, truefalse)

isContinuousNotNow

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

truefalse (bool) : boolean

Returns: boolean

isContinuousTwoFactors(targetSeries, range2Find, truefalse)

isContinuousTwoFactors

Parameters:

targetSeries (bool) : array of booleans

range2Find (int) : number

truefalse (bool) : boolean

Returns: boolean

findEventInRange(startDataBarIndex, neededDataBarIndex, currentBarIndex)

findEventInRange

Parameters:

startDataBarIndex (int) : number

neededDataBarIndex (int) : number

currentBarIndex (int) : number

Returns: boolean

findMin(firstdata, secondata, thirddata, forthdata)

findMin

Parameters:

firstdata (float) : number

secondata (float) : number

thirddata (float) : number

forthdata (float) : number

Returns: number

findMax(firstdata, secondata, thirddata, forthdata)

findMax

Parameters:

firstdata (float) : number

secondata (float) : number

thirddata (float) : number

forthdata (float) : number

Returns: number

getMA(src, length, mav)

getMA

Parameters:

src (float) : number

length (simple int) : number

mav (string) : string

Returns: number

mr(mrb_src, mrb_window, mrb_degree)

Parameters:

mrb_src (float)

mrb_window (int)

mrb_degree (int)

bpDom(maeLength, bpw, mult)

Parameters:

maeLength (int)

bpw (float)

mult (float)

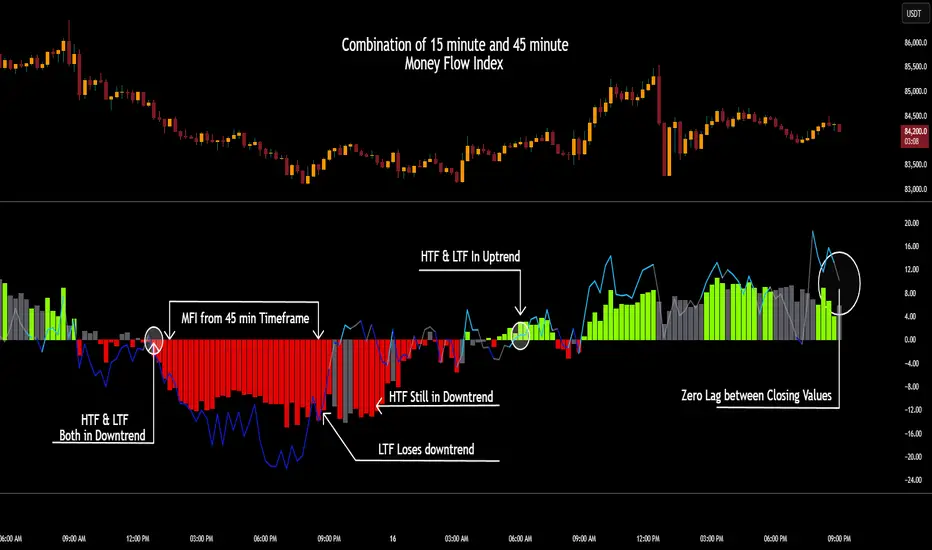

CSCMultiTimeframeToolsLibrary "CSCMultiTimeframeTools"

Calculates instant higher timeframe values for higher timeframe analysis with zero lag.

getAdjustedLookback(current_tf_minutes, higher_tf_minutes, length)

Calculate adjusted lookback period for higher timeframe conversion.

Parameters:

current_tf_minutes (int) : Current chart timeframe in minutes (e.g., 5 for 5m).

higher_tf_minutes (int) : Target higher timeframe in minutes (e.g., 15 for 15m).

length (int) : Base length value (e.g., 14 for RSI/MFI).

Returns: Adjusted lookback period (length × multiplier).

Purpose and Benefits of the TimeframeTools Library

This library is designed to solve a critical pain point for traders who rely on higher timeframe (HTF) indicator values while analyzing lower timeframe (LTF) charts. Traditional methods require waiting for multiple candles to close—for example, to see a 1-hour RSI on a 5-minute chart, you’d need 12 closed candles (5m × 12 = 60m) before the value updates. This lag means missed opportunities, delayed signals, and inefficient decision-making.

Why Traders Need This

Whether you’re scalping (5M/15M) or swing trading (1H/4H), this library bridges the gap between timeframes, giving you HTF context in real time—so you can act faster, with confidence.

How This Library Eliminates the Waiting Game

By dynamically calculating the adjusted lookback period, the library allows:

Real-time HTF values on LTF charts – No waiting for candle closes.

Accurate conversions – A 14-period RSI on a 1-hour chart translates to 168 periods (14 × 12) on a 5-minute chart, ensuring mathematical precision.

Flexible application – Works with common indicators like RSI, MFI, CCI, and moving averages (though confirmations should be done before publishing under your own secondary use).

Key Advantages Over Manual Methods

Speed: Instantly reflects HTF values without waiting for candle resolutions.

Adaptability: Adjusts automatically if the user changes timeframes or lengths.

Consistency: Removes human error in manual period calculations.

Limitations to Note

Not a magic bullet – While it solves the lag issue, traders should still:

Validate signals with price action or additional confirmations.

Be mindful of extreme lookback lengths (e.g., a 200-period daily SMA on a 1-minute chart requires 28,800 periods, which may strain performance).

PineVersatilitiesBundleLibrary "PineVersatilitiesBundle"

Versatilities (aka, Versatile Utilities) Pack includes:

- Eighteen Price Variants bundled in a Map,

- Nine Smoothing Variants bundled in a Map,

- Visualisations that indicate on both - pane and chart.

price_variants(lb)

Computes Several different averages using current and previous OHLC values

Parameters:

lb (int) : - lookback distance for combining OHLC values from the past with the present

Returns: Map of Eighteen Uncommon Combinations of single and two-bar OHLC averages (rounded-to-mintick)

dynamic_MA(masrc, malen, lsmaoff, almasgm, almaoff, almaflr)

Dynamically computes Eight different MAs and returns a Map containing Nine MAs

Parameters:

masrc (float) : source series to compute MA

malen (simple int) : lookback distance for MA

lsmaoff (simple int) : optional LSMA offset - default is 0

almasgm (simple float) : optional ALMA sigma - default is 5

almaoff (simple float) : optional ALMA offset - default is 0.5

almaflr (simple bool) : optional ALMA floor flag - default is false

Returns: Map of MAs - 'ALMA', 'EMA', 'HMA', 'LSMA', 'RMA', 'SMA', 'SWMA', 'WMA', 'ALL' (rounded-to-mintick)

PivotLabelsLibrary "PivotLabels"

drawPivots(qtyLabels, leftLegs, rightLegs)

Displays a label for each of the last `qtyLabels` pivots.

Colors high pivots in green, low pivots in red, and breached pivots in gray.

Parameters:

qtyLabels (int) : (simple int) Quantity of last labels to display.

leftLegs (int) : (simple int) Left pivot legs.

rightLegs (int) : (simple int) Right pivot legs.

Returns: Nothing.

bollingerBandsV2Library "bollingerBandsV2"

Bollinger bands related functions

get_multiple_bollinger_bands(stdv1, stdv2, stdv3, stdv4, stdv5, stdv6, stdv7, length, source)

: Calculates 7 sets of bollinger bands, with 7 different standard deviations

Parameters:

stdv1 (float) : (simple int): standard deviation 1

stdv2 (float) : (simple int): standard deviation 2

stdv3 (float) : (simple int): standard deviation 3

stdv4 (float) : (simple int): standard deviation 4

stdv5 (float) : (simple int): standard deviation 5

stdv6 (float) : (simple int): standard deviation 6

stdv7 (float) : (simple int): standard deviation 7

length (simple int) : (simple int): Length for the bands

source (float) : (simple float): source for the calculation

Returns: : Returns 8 levels plus the range of all the levels.

get_bb_volatility(bb_highest, bb_lowest, ma_length, lookback)

: Provides a volatility indicator based on Bollinger Bands, and indicates wheather the volatility is increasing or decreasing.

Parameters:

bb_highest (float) : (simple float): Top Bollinger Band on which to calculate the range.

bb_lowest (float) : (simple float): Bottom Bollinger Band on which to calculate the range.

ma_length (simple int) : (simple int): Length to use in the smoothing of Bollinger Bands range.

lookback (int) : (simple int): Lookback period to identify a change in the Bollinger Bands range.

Returns: : Returns 8 levels plus the range of all the levels.

get_bbVolatility_data(source, length, stdv1, stdv2, stdv3, stdv4, stdv5, stdv6, stdv7, trend_direction)

: Generates Bollinger Bands Volatility

Parameters:

source (float) : (float): Source for Bollinger Bands

length (simple int) : (int): Length for Bollinger Bands

stdv1 (int) : (int): Standard Deviation 1

stdv2 (int) : (int): Standard Deviation 2

stdv3 (int) : (int): Standard Deviation 3

stdv4 (int) : (int): Standard Deviation 4

stdv5 (int) : (int): Standard Deviation 5

stdv6 (int) : (int): Standard Deviation 6

stdv7 (int) : (int): Standard Deviation 7

trend_direction (string) : (string): Current direction of the trend

Returns: : Returns a map with the levels, plus direction flag and the data table

ZigZag█ Overview

This Pine Script™ library provides a comprehensive implementation of the ZigZag indicator using advanced object-oriented programming techniques. It serves as a developer resource rather than a standalone indicator, enabling Pine Script™ programmers to incorporate sophisticated ZigZag calculations into their own scripts.

Pine Script™ libraries contain reusable code that can be imported into indicators, strategies, and other libraries. For more information, consult the Libraries section of the Pine Script™ User Manual.

█ About the Original

This library is based on TradingView's official ZigZag implementation .

The original code provides a solid foundation with user-defined types and methods for calculating ZigZag pivot points.

█ What is ZigZag?

The ZigZag indicator filters out minor price movements to highlight significant market trends.

It works by:

1. Identifying significant pivot points (local highs and lows)

2. Connecting these points with straight lines

3. Ignoring smaller price movements that fall below a specified threshold

Traders typically use ZigZag for:

- Trend confirmation

- Identifying support and resistance levels

- Pattern recognition (such as Elliott Waves)

- Filtering out market noise

The algorithm identifies pivot points by analyzing price action over a specified number of bars, then only changes direction when price movement exceeds a user-defined percentage threshold.

█ My Enhancements

This modified version extends the original library with several key improvements:

1. Support and Resistance Visualization

- Adds horizontal lines at pivot points

- Customizable line length (offset from pivot)

- Adjustable line width and color

- Option to extend lines to the right edge of the chart

2. Support and Resistance Zones

- Creates semi-transparent zone areas around pivot points

- Customizable width for better visibility of important price levels

- Separate colors for support (lows) and resistance (highs)

- Visual representation of price areas rather than just single lines

3. Zig Zag Lines

- Separate colors for upward and downward ZigZag movements

- Visually distinguishes between bullish and bearish price swings

- Customizable colors for text

- Width customization

4. Enhanced Settings Structure

- Added new fields to the Settings type to support the additional features

- Extended Pivot type with supportResistance and supportResistanceZone fields

- Comprehensive configuration options for visual elements

These enhancements make the ZigZag more useful for technical analysis by clearly highlighting support/resistance levels and zones, and providing clearer visual cues about market direction.

█ Technical Implementation

This library leverages Pine Script™'s user-defined types (UDTs) to create a robust object-oriented architecture:

- Settings : Stores configuration parameters for calculation and display

- Pivot : Represents pivot points with their visual elements and properties

- ZigZag : Manages the overall state and behavior of the indicator

The implementation follows best practices from the Pine Script™ User Manual's Style Guide and uses advanced language features like methods and object references. These UDTs represent Pine Script™'s most advanced feature set, enabling sophisticated data structures and improved code organization.

For newcomers to Pine Script™, it's recommended to understand the language fundamentals before working with the UDT implementation in this library.

█ Usage Example

//@version=6

indicator("ZigZag Example", overlay = true, shorttitle = 'ZZA', max_bars_back = 5000, max_lines_count = 500, max_labels_count = 500, max_boxes_count = 500)

import andre_007/ZigZag/1 as ZIG

var group_1 = "ZigZag Settings"

//@variable Draw Zig Zag on the chart.

bool showZigZag = input.bool(true, "Show Zig-Zag Lines", group = group_1, tooltip = "If checked, the Zig Zag will be drawn on the chart.", inline = "1")

// @variable The deviation percentage from the last local high or low required to form a new Zig Zag point.

float deviationInput = input.float(5.0, "Deviation (%)", minval = 0.00001, maxval = 100.0,

tooltip = "The minimum percentage deviation from a previous pivot point required to change the Zig Zag's direction.", group = group_1, inline = "2")

// @variable The number of bars required for pivot detection.

int depthInput = input.int(10, "Depth", minval = 1, tooltip = "The number of bars required for pivot point detection.", group = group_1, inline = "3")

// @variable registerPivot (series bool) Optional. If `true`, the function compares a detected pivot

// point's coordinates to the latest `Pivot` object's `end` chart point, then

// updates the latest `Pivot` instance or adds a new instance to the `ZigZag`

// object's `pivots` array. If `false`, it does not modify the `ZigZag` object's

// data. The default is `true`.

bool allowZigZagOnOneBarInput = input.bool(true, "Allow Zig Zag on One Bar", tooltip = "If checked, the Zig Zag calculation can register a pivot high and pivot low on the same bar.",

group = group_1, inline = "allowZigZagOnOneBar")

var group_2 = "Display Settings"

// @variable The color of the Zig Zag's lines (up).

color lineColorUpInput = input.color(color.green, "Line Colors for Up/Down", group = group_2, inline = "4")

// @variable The color of the Zig Zag's lines (down).

color lineColorDownInput = input.color(color.red, "", group = group_2, inline = "4",

tooltip = "The color of the Zig Zag's lines")

// @variable The width of the Zig Zag's lines.

int lineWidthInput = input.int(1, "Line Width", minval = 1, tooltip = "The width of the Zig Zag's lines.", group = group_2, inline = "w")

// @variable If `true`, the Zig Zag will also display a line connecting the last known pivot to the current `close`.

bool extendInput = input.bool(true, "Extend to Last Bar", tooltip = "If checked, the last pivot will be connected to the current close.",

group = group_1, inline = "5")

// @variable If `true`, the pivot labels will display their price values.

bool showPriceInput = input.bool(true, "Display Reversal Price",

tooltip = "If checked, the pivot labels will display their price values.", group = group_2, inline = "6")

// @variable If `true`, each pivot label will display the volume accumulated since the previous pivot.

bool showVolInput = input.bool(true, "Display Cumulative Volume",

tooltip = "If checked, the pivot labels will display the volume accumulated since the previous pivot.", group = group_2, inline = "7")

// @variable If `true`, each pivot label will display the change in price from the previous pivot.

bool showChgInput = input.bool(true, "Display Reversal Price Change",

tooltip = "If checked, the pivot labels will display the change in price from the previous pivot.", group = group_2, inline = "8")

// @variable Controls whether the labels show price changes as raw values or percentages when `showChgInput` is `true`.

string priceDiffInput = input.string("Absolute", "", options = ,

tooltip = "Controls whether the labels show price changes as raw values or percentages when 'Display Reversal Price Change' is checked.",

group = group_2, inline = "8")

// @variable If `true`, the Zig Zag will display support and resistance lines.

bool showSupportResistanceInput = input.bool(true, "Show Support/Resistance Lines",

tooltip = "If checked, the Zig Zag will display support and resistance lines.", group = group_2, inline = "9")

// @variable The number of bars to extend the support and resistance lines from the last pivot point.

int supportResistanceOffsetInput = input.int(50, "Support/Resistance Offset", minval = 0,

tooltip = "The number of bars to extend the support and resistance lines from the last pivot point.", group = group_2, inline = "10")

// @variable The width of the support and resistance lines.

int supportResistanceWidthInput = input.int(1, "Support/Resistance Width", minval = 1,

tooltip = "The width of the support and resistance lines.", group = group_2, inline = "11")

// @variable The color of the support lines.

color supportColorInput = input.color(color.red, "Support/Resistance Color", group = group_2, inline = "12")

// @variable The color of the resistance lines.

color resistanceColorInput = input.color(color.green, "", group = group_2, inline = "12",

tooltip = "The color of the support/resistance lines.")

// @variable If `true`, the support and resistance lines will be drawn as zones.

bool showSupportResistanceZoneInput = input.bool(true, "Show Support/Resistance Zones",

tooltip = "If checked, the support and resistance lines will be drawn as zones.", group = group_2, inline = "12-1")

// @variable The color of the support zones.

color supportZoneColorInput = input.color(color.new(color.red, 70), "Support Zone Color", group = group_2, inline = "12-2")

// @variable The color of the resistance zones.

color resistanceZoneColorInput = input.color(color.new(color.green, 70), "", group = group_2, inline = "12-2",

tooltip = "The color of the support/resistance zones.")

// @variable The width of the support and resistance zones.

int supportResistanceZoneWidthInput = input.int(10, "Support/Resistance Zone Width", minval = 1,

tooltip = "The width of the support and resistance zones.", group = group_2, inline = "12-3")

// @variable If `true`, the support and resistance lines will extend to the right of the chart.

bool supportResistanceExtendInput = input.bool(false, "Extend to Right",

tooltip = "If checked, the lines will extend to the right of the chart.", group = group_2, inline = "13")

// @variable References a `Settings` instance that defines the `ZigZag` object's calculation and display properties.

var ZIG.Settings settings =

ZIG.Settings.new(

devThreshold = deviationInput,

depth = depthInput,

lineColorUp = lineColorUpInput,

lineColorDown = lineColorDownInput,

textUpColor = lineColorUpInput,

textDownColor = lineColorDownInput,

lineWidth = lineWidthInput,

extendLast = extendInput,

displayReversalPrice = showPriceInput,

displayCumulativeVolume = showVolInput,

displayReversalPriceChange = showChgInput,

differencePriceMode = priceDiffInput,

draw = showZigZag,

allowZigZagOnOneBar = allowZigZagOnOneBarInput,

drawSupportResistance = showSupportResistanceInput,

supportResistanceOffset = supportResistanceOffsetInput,

supportResistanceWidth = supportResistanceWidthInput,

supportColor = supportColorInput,

resistanceColor = resistanceColorInput,

supportResistanceExtend = supportResistanceExtendInput,

supportResistanceZoneWidth = supportResistanceZoneWidthInput,

drawSupportResistanceZone = showSupportResistanceZoneInput,

supportZoneColor = supportZoneColorInput,

resistanceZoneColor = resistanceZoneColorInput

)

// @variable References a `ZigZag` object created using the `settings`.

var ZIG.ZigZag zigZag = ZIG.newInstance(settings)

// Update the `zigZag` on every bar.

zigZag.update()

//#endregion

The example code demonstrates how to create a ZigZag indicator with customizable settings. It:

1. Creates a Settings object with user-defined parameters

2. Instantiates a ZigZag object using these settings

3. Updates the ZigZag on each bar to detect new pivot points

4. Automatically draws lines and labels when pivots are detected

This approach provides maximum flexibility while maintaining readability and ease of use.

LinearRegressionLibrary "LinearRegression"

Calculates a variety of linear regression and deviation types, with optional emphasis weighting. Additionally, multiple of slope and Pearson’s R calculations.

calcSlope(_src, _len, _condition)

Calculates the slope of a linear regression over the specified length.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period for the linear regression.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast for efficiency.

Returns: (float) The slope of the linear regression.

calcReg(_src, _len, _condition)

Calculates a basic linear regression, returning y1, y2, slope, and average.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) An array of 4 values: .

calcRegStandard(_src, _len, _emphasis, _condition)

Calculates an Standard linear regression with optional emphasis.

Parameters:

_src (float) : (series float) The source data series.

_len (int) : (int) The length of the lookback period.

_emphasis (float) : (float) The emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegRidge(_src, _len, lambda, _emphasis, _condition)

Calculates a ridge regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

lambda (float) : (float) The ridge regularization parameter.

_emphasis (float) : (float) The emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegLasso(_src, _len, lambda, _emphasis, _condition)

Calculates a Lasso regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

lambda (float) : (float) The Lasso regularization parameter.

_emphasis (float) : (float) The emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcElasticNetLinReg(_src, _len, lambda1, lambda2, _emphasis, _condition)

Calculates an Elastic Net regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

lambda1 (float) : (float) L1 regularization parameter (Lasso).

lambda2 (float) : (float) L2 regularization parameter (Ridge).

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegHuber(_src, _len, delta, iterations, _emphasis, _condition)

Calculates a Huber regression using Iteratively Reweighted Least Squares (IRLS).

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

delta (float) : (float) Huber threshold parameter.

iterations (int) : (int) Number of IRLS iterations.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegLAD(_src, _len, iterations, _emphasis, _condition)

Calculates a Least Absolute Deviations (LAD) regression via IRLS.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

iterations (int) : (int) Number of IRLS iterations for LAD.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegBayesian(_src, _len, priorMean, priorSpan, sigma, _emphasis, _condition)

Calculates a Bayesian linear regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

priorMean (float) : (float) The prior mean for the slope.

priorSpan (float) : (float) The prior variance (or span) for the slope.

sigma (float) : (float) The assumed standard deviation of residuals.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRFromLinReg(_src, _len, _slope, _average, _y1, _condition)

Calculates the Pearson correlation coefficient (R) based on linear regression parameters.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_average (float) : (float) The average value of the source data series.

_y1 (float) : (float) The starting point (y-intercept of the oldest bar) for the linear regression.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast for efficiency.

Returns: (float) The Pearson correlation coefficient (R) adjusted for the direction of the slope.

calcRFromSource(_src, _len, _condition)

Calculates the correlation coefficient (R) using a specified length and source data.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast for efficiency.

Returns: (float) The correlation coefficient (R).

calcSlopeLengthZero(_src, _len, _minLen, _step, _condition)

Identifies the length at which the slope is flattest (closest to zero).

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length to consider (minimum of 2).

_minLen (int) : (int) The minimum length to start from (cannot exceed the max length).

_step (int) : (int) The increment step for lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the slope is flattest.

calcSlopeLengthHighest(_src, _len, _minLen, _step, _condition)

Identifies the length at which the slope is highest.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the slope is highest.

calcSlopeLengthLowest(_src, _len, _minLen, _step, _condition)

Identifies the length at which the slope is lowest.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the slope is lowest.

calcSlopeLengthAbsolute(_src, _len, _minLen, _step, _condition)

Identifies the length at which the absolute slope value is highest.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the absolute slope value is highest.

calcRLengthZero(_src, _len, _minLen, _step, _condition)

Identifies the length with the lowest absolute R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the lowest absolute R value.

calcRLengthHighest(_src, _len, _minLen, _step, _condition)

Identifies the length with the highest R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the highest R value.

calcRLengthLowest(_src, _len, _minLen, _step, _condition)

Identifies the length with the lowest R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the lowest R value.

calcRLengthAbsolute(_src, _len, _minLen, _step, _condition)

Identifies the length with the highest absolute R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the highest absolute R value.

calcDevReverse(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the regressive linear deviation in reverse order, with optional emphasis on recent data.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevForward(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the progressive linear deviation in forward order (oldest to most recent bar), with optional emphasis.

Parameters:

_src (float) : (float) The source data array, where _src is oldest and _src is most recent.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept of the linear regression (value at the most recent bar, adjusted by slope).

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevBalanced(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the balanced linear deviation with optional emphasis on recent or older data.

Parameters:

_src (float) : (float) Source data array, where _src is the most recent and _src is the oldest.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept of the linear regression (value at the oldest bar).

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevMean(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the mean absolute deviation from a forward-applied linear trend (oldest to most recent), with optional emphasis.

Parameters:

_src (float) : (float) The source data array, where _src is the most recent and _src is the oldest.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevMedian(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the median absolute deviation with optional emphasis on recent data.

Parameters:

_src (float) : (float) The source data array (index 0 = oldest, index _len - 1 = most recent).

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns:

calcDevPercent(_y1, _inputDev, _condition)

Calculates the percent deviation from a given value and a specified percentage.

Parameters:

_y1 (float) : (float) The base value from which to calculate deviation.

_inputDev (float) : (float) The deviation percentage.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevFitted(_len, _slope, _y1, _emphasis, _condition)

Calculates the weighted fitted deviation based on high and low series data, showing max deviation, with optional emphasis.

Parameters:

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The Y-intercept (oldest bar) of the linear regression.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevATR(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates an ATR-style deviation with optional emphasis on recent data.

Parameters:

_src (float) : (float) The source data (typically close).

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The Y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcPricePositionPercent(_top, _bot, _src)

Calculates the percent position of a price within a linear regression channel. Top=100%, Bottom=0%.

Parameters:

_top (float) : (float) The top (positive) deviation, corresponding to 100%.

_bot (float) : (float) The bottom (negative) deviation, corresponding to 0%.

_src (float) : (float) The source price.

Returns: (float) The percent position within the channel.

plotLinReg(_len, _y1, _y2, _slope, _devTop, _devBot, _scaleTypeLog, _lineWidth, _extendLines, _channelStyle, _colorFill, _colUpLine, _colDnLine, _colUpFill, _colDnFill)

Plots the linear regression line and its deviations, with configurable styles and fill.

Parameters:

_len (int) : (int) The lookback period for the linear regression.

_y1 (float) : (float) The starting y-value of the regression line.

_y2 (float) : (float) The ending y-value of the regression line.

_slope (float) : (float) The slope of the regression line (used to determine line color).

_devTop (float) : (float) The top deviation to add to the line.

_devBot (float) : (float) The bottom deviation to subtract from the line.

_scaleTypeLog (bool) : (bool) Use a log scale if true; otherwise, linear scale.

_lineWidth (int) : (int) The width of the plotted lines.

_extendLines (string) : (string) How lines should extend (none, left, right, both).

_channelStyle (string) : (string) The style of the channel lines (solid, dashed, dotted).

_colorFill (bool) : (bool) Whether to fill the space between the top and bottom deviation lines.

_colUpLine (color) : (color) Line color when slope is positive.

_colDnLine (color) : (color) Line color when slope is negative.

_colUpFill (color) : (color) Fill color when slope is positive.

_colDnFill (color) : (color) Fill color when slope is negative.

ootaLibrary "oota"

Collection of all custom and enhanced TA indicators - Object oriented methods implementation

method tr(c, useTrueRange)

returns true range of the candle

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc data

useTrueRange (bool) : Use true range for atr calculation instead of just high/low difference

method ma(maType, length, source)

returns custom moving averages

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

source (float) : Moving Average Source

Returns: moving average for the given type and length

method atr(maType, length, useTrueRange, c)

returns ATR with custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

useTrueRange (bool) : Use true range for atr calculation instead of just high/low difference

c (Candle) : Candle object containing ohlc

Returns: ATR for the given moving average type and length

method atrpercent(maType, length, useTrueRange, c)

returns ATR as percentage of close price

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

useTrueRange (bool) : Use true range for atr calculation instead of just high/low difference

c (Candle) : Candle object containing ohlc

Returns: ATR as percentage of close price for the given moving average type and length

method bb(maType, length, multiplier, sticky, c)

returns Bollinger band for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Bollinger band with custom moving average for given source, length and multiplier

method bbw(maType, length, multiplier, sticky, c)

returns Bollinger bandwidth for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Bollinger Bandwidth for custom moving average for given source, length and multiplier

method bpercentb(maType, length, multiplier, sticky, c)

returns Bollinger Percent B for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Bollinger Percent B for custom moving average for given source, length and multiplier

method kc(maType, length, multiplier, useTrueRange, sticky, c)

returns Keltner Channel for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Keltner Channel for custom moving average for given souce, length and multiplier

method kcw(maType, length, multiplier, useTrueRange, sticky, c)

returns Keltner Channel Width with custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Keltner Channel Width for custom moving average

method kpercentk(maType, length, multiplier, useTrueRange, sticky, c)

returns Keltner Channel Percent K Width with custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Keltner Percent K for given moving average, source, length and multiplier

method dc(c, length, sticky)

returns Custom Donchian Channel

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc

length (simple int) : - donchian channel length

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel

method dcw(c, length, sticky)

returns Donchian Channel Width

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc

length (simple int) : - donchian channel length

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel width

method dpercentd(c, length, sticky)

returns Donchian Channel Percent of price

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc

length (simple int) : - donchian channel length

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel Percent D

method supertrend(maType, length, multiplier, useTrueRange, waitForClose, delayed, c)

supertrend Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom Series

length (simple int) : ATR Length

multiplier (simple float) : ATR Multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

delayed (simple bool) : : if set to true lags supertrend atr stop based on target levels.

c (Candle) : Candle object containing ohlc

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

method oscillatorRange(seriesType, source, highlowLength, rangeLength, sticky)

oscillatorRange - returns Custom overbought/oversold areas for an oscillator input

Namespace types: simple CustomSeries

Parameters:

seriesType (simple CustomSeries) : - Custom series type

source (float) : - Osillator source such as RSI, COG etc.

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

rangeLength (simple int) : - length used for calculating oversold/overbought range - usually same as oscillator length