Combo Strategy 123 Reversal & FSK (Fast and Slow Kurtosis) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the Fast & Slow Kurtosis. The Kurtosis is a market

sentiment indicator. The Kurtosis is constructed from three different parts.

The Kurtosis, the Fast Kurtosis(FK), and the Fast/Slow Kurtosis(FSK).

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategy!

Inferential Statistics And Quick Metrics For Strategy Analysis.Part of this script is used to calculate inferential statistics and metrics not available through the built in variables in the strategy tester.

A label will be created on the last bar displaying important strategy results, so you can test and analyze strategies quicker.

The built in strategy itself is just an example. You can copy and paste the metrics into any existing version 4 strategy and instantly use it**

**Just be sure all the variable names are unique in your target script.

I am looking for critique and would appreciate input on the statistical functions. I am aware that some of these functions are based on the assumption that the data is normally distributed. It's not meant to be perfect, but it is meant to be helpful. So if you think I can add or improve something to make it more helpful, let me know.

Cycles StrategyThis is back-testable strategy is a modified version of the Stochastic strategy. It is meant to accompany the modified Stochastic indicator: "Cycles".

Modifications to the Stochastic strategy include;

1. Programmable settings for the Stochastic Periods (%K, %D and Smooth %K).

2. Programmable settings for the MACD Periods (Fast, Slow, Smoothing)

3. Programmable thresholds for %K, to qualify a potential entry strategy.

4. Programmable thresholds for %D, to qualify a potential exit strategy.

5. Buttons to choose which components to use in the trading algorithm.

6. Choose the month and year to back test.

The trading algorithm:

1. When %K exceeds the upper/lower threshold and then hooks down/up, in the direction of the Moving Average (MA). This is the minimum entry qualification.

2. When %D exceeds the lower/upper threshold and angled in the direction of the trade, is the exit qualification.

3. Additional entry filters include the direction of MACD, Signal and %D. Also, the "cliff", being a long entry is a higher high or a short entry is a lower low.

4. Strategy can only go "Long" or "Short" depending on the selected setting.

5. By matching the settings in the "Cycles" indicator, you can (almost) see what the strategy is doing.

6. Be sure to select the "Recalculate" buttons, to recalculate on every new Tick, for best results.

Please click the Like button and leave a comment if you appreciate this script. Improvements will be implemented as time goes on.

I am not a licensed trade advisor. This strategy is for entertainment only. Use at your own risk!

Combo Strategy 123 Reversal & Fractal Chaos OscillatorThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The value of Fractal Chaos Oscillator is calculated as the difference between

the most subtle movements of the market. In general, its value moves between

-1.000 and 1.000. The higher the value of the Fractal Chaos Oscillator, the

more one can say that it follows a certain trend – an increase in prices trend,

or a decrease in prices trend.

Being an indicator expressed in a numeric value, traders say that this is an

indicator that puts a value on the trendiness of the markets. When the FCO reaches

a high value, they initiate the “buy” operation, contrarily when the FCO reaches a

low value, they signal the “sell” action. This is an excellent indicator to use in

intra-day trading.

WARNING:

- For purpose educate only

- This script to change bars colors.

RSI on VWAP Upgraded strategyFirst of all, the idea of apply RSI to VWAP was inspired by XaviZ; at least, that where I first saw that.

I simply applied the idea and searched for apply this on lower timeframe (M15) to increase the number of positions and improve the profit factor.

The conditions to enter are the same :

long : enter on RSI crossover oversold level

short : enter on RSI crossunder oversell level

To close position, I found a little change to apply :

long : close position when RSI(VWAP) went in overbought zone and crossunder the overbought level OR after being at least x bars in the overbought zone (parameter is 28 by default) => when the first condition happens

short : close position when RSI(VWAP) went in oversold zone and crossover the oversold level OR after being at least x bars in the oversell zone (parameter is 28 by default) => when the first condition happens

With this change, I got better results specially on BTCUSDTPERP (M15) where I reach a 6.8 profit factor with 119 trades closed. Not BAD !

The defaults parameters are the best found for BTCUSDTPERP (M15), but the strategy works fine for other pairs if you take time to find the rights combinations.

In this strategy you can change (with defaults in () ):

RSI length (28)

RSI overbought level (85)

RSI oversell level (30)

Number of bars before leaving as explain above (28)

The choice to take longs only, shorts only or both

The number of coin/token by position

The start date for backtesting

Please note that the script use a pyramiding parameter of 3 (can be changed in the first line of the script); that means that you can take up to 3 positions before closing. It lets you improve average enter price but increase the risk. 3 is the best I found to improve profit factor without expose myself too much.

This script would be better if automated because of the conditions of buy and sell.

It's only for educative purpose, not an advice to invest.

All my free scripts here : fr.tradingview.com

Leave a message and don't forget to follow me ;) !

Lagged Donchian Channel + EMAThis strategy is based on a lagged 24 periods Donchian Channel and a 200 periods EMA .

The enter positions are calculated this way :

Bull entry

1. we wait for the close of a candle below the channel and it must be below the 200 EMA

2. the following candle must be a green one and close in the lagged channel

3. we put a long order at the close of the second candle, a stop loss at the low of last 3 candles and a x3 take profit

Bear entry

1. we wait for the close of a candle above the channel and it must be above the 200 EMA

2. the following candle must be a red one and close in the lagged channel

3. we put a short order at the close of the second candle, a stop loss at the high of last 3 candles and a x3 take profit

For both long or short positions :

If the order is not filled, it's cancelled if the price reach 50% of the TP or if the price reach the stop loss level

The position is closed if a new bear/bull condition appears in the other side of the position (if a bear appears when you're long and inversement)

Features :

Position calculator's included with leverage option

Labels of position can be plotted or not

Bull/Bear channels can be plotted with red and green filled

All parameters can be changed for backtesting

Better results have been got with defaults parameters on LTCUSDTPERP in H1 timeframe => profit factor of 2.84 with almost 100 positions.

Hope this strategy will be useful and it would be cool if I could get feedback, comments or better combinations of parameters !!

Don't hesitate to like and leave a comment ;)

@Mysteriown

Super Guppy StrategyCM Super Guppy with Long/Short signals, backtesting, and additional options. Updated for PineScript v4.

COINBASE:BTCUSD

Features 2 primary modes, depending on your risk profile. These options are available in the settings:

"Early Signals" ON (default):

Prints a "long" on grey to green transitions AND red to gray transitions.

Prints a "short" on green to grey transitions AND gray to red transitions.

Will not print back-to-back repeated positions (i.e. green → grey → red will only print the first green → gray "short" signal and not print "short" twice).

Rotates long and short positions with no delay.

"Early Signals" OFF

Will close trades, but never open new ones, when guppy transitions to from any color to gray.

Open long: guppy transitions gray to green.

Close long: guppy transitions green to gray.

Open short: guppy transitions gray to red.

Close short: guppy transitions red to gray.

Does not rotate long and short positions back to back.

Additionally:

Can toggle on/off the 200EMA. Default is off.

Can toggle on/off short positions. Default is on.

In development: alerts

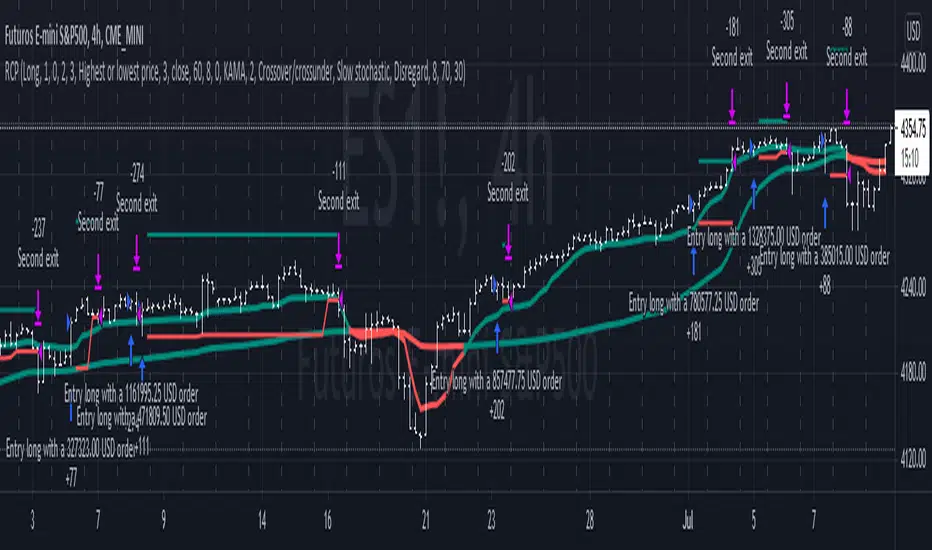

Reversal closing priceThe reversal closing price (RCP) is a candlestick pattern which follows two simples rules:

the low price of current candle needs to be lower than the low price of the last 2 candles

the closing price of current candle needes to be higher than the closing price of the last candle

This generates a signal for a long position. For a short position, the conditions are inverted:

the high price of current candle needs to be higher than the high price of the last 2 candles

the closing price of current candle needes to be lower than the closing price of the last candle

Since RCP is a trend follower indicator, the strategy is programmed in such a way that long positions are only placed if the short period EMA is above the long period EMA, and short positions are only placed if the short EMA is bellow the long EMA. Both periods are configurable, and should be ajusted for each asset.

This strategy uses a fixed stop loss and take profit, and the it's ratio is configurable. The stop price is one tick lower than the lowest price of X candles prior to the order execution for long positions, while in short positions it's one tick higher than the higher price. The amount of candles to lookback (X) is configurable. Both stop and take profit prices are displayed, the first as a red line, and the second as a green line.

This is the setting that I've found to work best with TVC:SPX , but you may find a better setting. While the RCP is universal, it's placement depends on the trend and it's strenght, something that is very heterogeneous among assets.

I really wish that I was able to place images, but I don't have PRO, so text will have to do.

This strategy was designed by Alexandre Wolwacz, a.k.a. Stormer.

The Strategy - Ichimoku Kinko Hyo and moreThe purpose of this strategy is to make the signals from my scripts available for verification by backtests. Different signal and filter combinations can be created and specific manual parameter optimization can be carried out.

In detail, this strategy includes:

23 entry signals

two entry filters with each 9 filters

two exit filters with each 9 filters

take profit and stop loss

time period for backtesting

Combo Strategy 123 Reversal & Fractal Chaos Bands This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Stock market moves in a highly chaotic way, but at a larger scale, the movements

follow a certain pattern that can be applied to shorter or longer periods of time

and we can use Fractal Chaos Bands Indicator to identify those patterns. Basically,

the Fractal Chaos Bands Indicator helps us to identify whether the stock market is

trending or not. When a market is trending, the bands will have a slope and if market

is not trending the bands will flatten out. As the slope of the bands decreases, it

signifies that the market is choppy, insecure and variable. As the graph becomes more

and more abrupt, be it going up or down, the significance is that the market becomes

trendy, or stable. Fractal Chaos Bands Indicator is used similarly to other bands-indicator

(Bollinger bands for instance), offering trading opportunities when price moves above or

under the fractal lines.

The FCB indicator looks back in time depending on the number of time periods trader selected

to plot the indicator. The upper fractal line is made by plotting stock price highs and the

lower fractal line is made by plotting stock price lows. Essentially, the Fractal Chaos Bands

show an overall panorama of the price movement, as they filter out the insignificant fluctuations

of the stock price.

WARNING:

- For purpose educate only

- This script to change bars colors.

STRATEGY TESTER ENGINE - ON CHART DISPLAY - PLUG & PLAYSo i had this idea while ago when @alexgrover published a script and dropped a nugget in between which replicates the result of strategy tester on chart as an indicator.

So it seemed fair to use one of his strategy to display the results.

This strategy tester can now be used in replay mode like an indicator and you can see what happen at a particular section of the chart which was is not possible in default strategy tester results of TV.

Please read how each result is calculated so you will know what you are using.

This engine shows most common results of strategy tester in a single screen, which are as follows:

1. Starting Capital

2. Current Profit Percentage

3. Max Profit Percentage

4. Gross Profit

5. Gross Loss

6. Total Closed Trades

7. Total Trades Won

8. Total Trades Lost

9. Percentage Profitable

10. Profit Factor

11. Current Drawdown

12. Max Drawdown

13. Liquidation

So elaborating on what is what:

1. Starting Capital - This stays 0, which signifies your starting balance as 0%. It is set to 0 so we can compare all other results without any change in variables. If set to 100, then all the results will be increased by 100. Some users might find it useful to set it to 100, then they can change code on line 41 from to and it should show starting balance as 100%.

2. Current Profit Percentage - This shows your current profit adjusted to current price of the candle, not like TV which shows after candle is close. There is a comment on the line 38 which can be removed and your can see unrealized profit as well in this section. Please note that this will affect Draw-down calculations later in this section.

3. Max Profit Percentage - This will show you your max profit achieved during your strategy run, which was not possible yet to see via strategy tester. So, now you can see how much profit was achieved by your strategy during the run and you can compare it with chart to see what happens during bull-run or bear-run, so you can further optimize your strategy to best suit your desired results.

4. Gross Profit - This is total percentage of profit your strategy achieved during entire run as if you never had any losses.

5. Gross Loss - This is total percentage of loss your strategy achieved during entire run as if you never had any profits.

6. Total Closed Trades - This is total number of trades that your strategy has executed so far.

7. Total Trades Won - This is the total number of trades that your strategy has executed that resulted in positive increase in equity.

8. Totals Trades Lost - This is the total number of trades that your strategy has executed that resulted in decrease in equity.

9. Percentage Profitable - This is the ratio between your current total winning trades divided by total closed trades, and finally multiplied by 100 to get percentage results.

10. Profit Factor - This is the ratio between Gross Profit and Gross Loss, so if profit factor is 2, then it indicates that you are set to gain 2 times per your risk per trade on average when total trades are executed.

11. Current Drawdown - This is important section and i want you to read this carefully. Here draw-down is calculated very differently than what TV shows. TV has access to candle data and calculates draw-down accordingly as per number of trades closed, but here DD is calculated as difference between max profit achieved and current profit. This way you can see how much percentage you are down from max peak of equity at current point in time. You can do back-test of the data and see when peak was achieved and how much your strategy did a draw-down candle by candle.

12. Max Drawdown - This is also calculated differently same as above, current draw-down. Here you can see how much max DD your strategy did from a peak profit of equity. This is not set as max profit percentage is set because you will see single number on display, while idea is to keep it custom. I will explain.

So lets say, your max DD on TV is 30%. Here this is of no use to see Max DD , as some people might want to see what was there max DD 1000 candles back or 10 candle back. So this will show you your max DD from the data you select. TV shows 25000 candle data in a chart if you go back, you can set the counter to 24999 and it will show you max DD as shown on TV, but if you want custom section to show max DD , it is now possible which was not possible before.

Also, now let's say you put DD as 24999 and open a chart of an asset that was listed 1 week ago, now on 1H chart max DD will never show up until you reach 24999 candle in data history, but with this you can now enter a manual number and see the data.

13. Liquidation - This is an interesting feature, so now when your equity balance is less than 0 and your draw-down goes to -100, it will show you where and at what point in time you got liquidated by adding a red background color in the entire section. This is the most fun part of this script, while you can only see max DD on TV.

------------------------------------------------------------------------------

How to Use -

1 word, plug and play. Yes. Actual codes start from line 33.

select overlay=false or remove it from the title in your strategy on first line,

Just copy the codes from line 33 to 103,

then go to end section of your strategy and paste the entire code from line 33 to line 103,

see if you have any duplicate variable, edit it,

Add to chart.

What you see above is very contracted view. Here is how it looks when zoomed in.

imgur.com

----------------------------------------------------------------------------------

Feel free to edit and share and use. If you use it in your scripts, drop me tag. Cheers.

Combo Strategy 123 Reversal & Floor Pivot Points This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The name ‘Floor-Trader Pivot,’ came from the fact that Pivot points can

be calculated quickly, on the fly using price data from the previous day

as an input. Although time-frames of less than a day can be used, Pivots are

commonly plotted on the Daily Chart; using price data from the previous day’s

trading activity.

WARNING:

- For purpose educate only

- This script to change bars colors.

ATR Trailing Stop Strategy by ceyhunSame coding only coloring and strategy version added

//Barcolor

Green = Trail1 > Trail2 and close > Trail2 and low > Trail2

Blue = Trail1 > Trail2 and close > Trail2 and low < Trail2

Red = Trail2 > Trail1 and close < Trail2 and high < Trail2

Yellow = Trail2 > Trail1 and close < Trail2 and high > Trail2

//It gives White color where there is deterioration.

Let's not use InfoPanel in strategy, it would be wrong as it signals the next day.

ATR Trailing Stoploss StrategyI am sharing the strategy version of the indicator used before. It is very simple to use.

These are the settings I use, you can change, test and use as you wish.

Atr Period 5

Highest High Period 10

Multiplier 2.5

It can generate more signals in shorter time frames.

The success rate will be higher in longer time frames.

The Lazy Trader - Index (ETF) Trend Following Robot50/150 moving average, index (ETF) trend following robot. Coded for people who cannot psychologically handle dollar-cost-averaging through bear markets and extreme drawdowns (although DCA can produce better results eventually), this robot helps you to avoid bear markets. Be a fair-weathered friend of Mr Market, and only take up his offer when the sun is shining! Designed for the lazy trader who really doesn't care...

Recommended Chart Settings:

Asset Class: ETF

Time Frame: Daily

Necessary ETF Macro Conditions:

a) Country must have healthy demographics, good ratio of young > old

b) Country population must be increasing

c) Country must be experiencing price-inflation

Default Robot Settings:

Slow Moving Average: 50 (integer) //adjust to suit your underlying index

Fast Moving Average: 150 (integer) //adjust to suit your underlying index

Bullish Slope Angle: 5 (degrees) //up angle of moving averages

Bearish Slope Angle: -5 (degrees) //down angle of moving averages

Average True Range: 14 (integer) //input for slope-angle formula

Risk: 100 (%) //100% risk means using all equity per trade

ETF Test Results (Default Settings):

SPY (1993 to 2020, 27 years), 332% profit, 20 trades, 6.4 profit factor, 7% drawdown

EWG (1996 to 2020, 24 years), 310% profit, 18 trades, 3.7 profit factor, 10% drawdown

EWH (1996 to 2020, 24 years), 4% loss, 26 trades, 0.9 profit factor, 36% drawdown

QQQ (1999 to 2020, 21 years), 232% profit, 17 trades, 3.6 profit factor, 2% drawdown

EEM (2003 to 2020, 17 years), 73% profit, 17 trades, 1.1 profit factor, 3% drawdown

GXC (2007 to 2020, 13 years), 18% profit, 14 trades, 1.3 profit factor, 26% drawdown

BKF (2009 to 2020, 11 years), 11% profit, 13 trades, 1.2 profit factor, 33% drawdown

A longer time in the markets is better, with the exception of EWH. 6 out of 7 tested ETFs were profitable, feel free to test on your favourite ETF (default settings) and comment below.

Risk Warning:

Not tested on commodities nor other financial products like currencies (code will not work), feel free to leave comments below.

Moving Average Slope Angle Formula:

Reproduced and modified from source:

Tilson T3 and MavilimW Triple Combined StrategyInspired by truly greatful Kivanç Ozbilgic (www.tradingview.com).

The strategy tries to combined three different moving average strategies into one.

Strategies covered are:

1. Tillson T3 Moving Average Strategy

Developed by Tim Tillson, the T3 Moving Average is considered superior to traditional moving averages as it is smoother, more responsive and thus performs better in ranging market conditions as well. However, it bears the disadvantage of overshooting the price as it attempts to realign itself to current market conditions.

It incorporates a smoothing technique which allows it to plot curves more gradual than ordinary moving averages and with a smaller lag. Its smoothness is derived from the fact that it is a weighted sum of a single EMA, double EMA, triple EMA and so on. When a trend is formed, the price action will stay above or below the trend during most of its progression and will hardly be touched by any swings. Thus, a confirmed penetration of the T3 MA and the lack of a following reversal often indicates the end of a trend. Here is what the calculation looks like:

T3 = c1*e6 + c2*e5 + c3*e4 + c4*e3, where:

– e1 = EMA (Close, Period)

– e2 = EMA (e1, Period)

– e3 = EMA (e2, Period)

– e4 = EMA (e3, Period)

– e5 = EMA (e4, Period)

– e6 = EMA (e5, Period)

– a is the volume factor, default value is 0.7 but 0.618 can also be used

– c1 = – a^3

– c2 = 3*a^2 + 3*a^3

– c3 = – 6*a^2 – 3*a – 3*a^3

– c4 = 1 + 3*a + a^3 + 3*a^2

T3 MovingThe T3 Moving Average generally produces entry signals similar to other moving averages and thus is traded largely in the same manner.

Strategy for Tillson T3 is if the close crossovers T3 line and for at least five bars the close was under the T3

2. Tillson T3 Fibonacci Cross

Kivanc Ozbilgic added a second T3 line with a volume factor of 0.618 (Fibonacci Ratio) and length of 3 (fibonacci number) which can be added by selecting the T3 Fibonacci Strategy input box.

Strategy for Tillson T3 Fibo is when the Fibo Line crossover the T3 it gives long signal vice versa.

3. MavilimW

MavilimW is originally a support and resistance indicator based on fibonacci injected weighted moving averages.

Strategy for MavilimW is is if the close crossovers T3 line and for at least five bars the close was under the T3

Hope you enjoy

Combo Strategy 123 Reversal & Future Lines of Demarcation This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

An FLD is a line that is plotted on the same scale as the price and is in fact the

price itself displaced to the right (into the future) by (approximately) half the

wavelength of the cycle for which the FLD is plotted. There are three FLD's that can be

plotted for each cycle:

An FLD based on the median price.

An FLD based on the high price.

An FLD based on the low price.

WARNING:

- For purpose educate only

- This script to change bars colors.

365 Day High Breakout StrategySCRIPT NOTES

- Strategy consists of 3 parameters :-

1. BUY on 365 day breakout (250 days taken in back-testing instead of 365 days considering weekends and other holidays in a year)

2. Moving averages (Noise Filtering condition )

3. RELATIVE STRENTH indicator (Original Author - tradingview.com ) (Noise Filtering condition )

- Strategy works better on low volatile stocks.

- This strategy is for self improvement and concept sharing purpose only.

- Trading (including profit/loss) using this strategy is completely user's responsibility.

Random entry pointsIt is profitable strategy with random entry points.

A simple strategy involving random opening of trades. But such a strategy on large samples will demonstrate profit. Because the strategy adheres to the golden rule of trading: "Let profits rise and quickly stop losses."

Remember, exit points are very important. Many traders make the mistake of focusing all their attention on entry points.

Combo Strategy 123 Reversal & Fisher Transform Indicator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Market prices do not have a Gaussian probability density function

as many traders think. Their probability curve is not bell-shaped.

But trader can create a nearly Gaussian PDF for prices by normalizing

them or creating a normalized indicator such as the relative strength

index and applying the Fisher transform. Such a transformed output

creates the peak swings as relatively rare events.

Fisher transform formula is: y = 0.5 * ln ((1+x)/(1-x))

The sharp turning points of these peak swings clearly and unambiguously

identify price reversals in a timely manner.

WARNING:

- For purpose educate only

- This script to change bars colors.

Bollinger Bands Breakout StrategyBollinger Bands Breakout Strategy is the strategy version of Bollinger Bands Filter study version, which can be found under my scripts page. The strategy goes long when price closes above the upper band and goes short signal when price closes below the lower band.

Bollinger Bands is a classic indicator that uses a simple moving average of 20 periods, along with plots of upper and lower bands that are 2 standard deviations away from the basis line. These bands help visualize price volatility and trend based on where the price is, in relation to the bands.

The strategy doesn't take into account any other parameters such as Volume / RSI / Fundamentals etc, so user must use discretion based on confirmations from another indicator or based on fundamentals. The strategy results are based on purely long and short trades and doesn't take into account any user defined targets or stop losses.

The strategy works great when the price closes above/below upper/lower bands with continuation on next bar. It is definitely useful to have this strategy or the Bollinger Bands filter along with other indicators to get early glimpse of breach/fail of bands on candle close during BB squeeze or based on volatility .

This can be used on Heikin Ashi candles for spotting trends, but HA candles are not recommended for trade entries as they don't reflect true price of the asset.

The strategy settings default is 55 SMA and 1 standard deviation for Bollinger Bands filter, but these can be changed from settings.

It is definitely worth reading the 22 rules of Bollinger Bands written by John Bollinger if interested in trading Bollinger Bands successfully.

Grid System With Fake MartingaleThe proposed strategy is based on a grid system with a money management that tries to replicate the effect of a martingale without having to double your position size after each loss, hence the name "fake martingale". Note that a balance using this strategy is still subject to exponential decay, the risk is not minimized, as such, it would be dangerous to use this strategy.

For more information on the martingale and grid systems see:

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the security you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, generating fewer trades as a result.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after each win.

How It Works

Let's illustrate how we replicate a martingale without doubling our exposure with a simple casino example. Imagine you are playing roulette, and that you are betting on colors (black/red), your payout is 1 to 1, in the case you win, you will have your initial stake back plus a profit equal to your initial stake.

If your strategy is to recover any previous losses, you can double your stake each time you lose, once you win you will get back the previous losses plus a profit equal to your original stake, this is the martingale system. So how can we win back previous losses without having to double our stake? We could do that by doubling the payout ratio after a loss, so after a loss, we must use a payout ratio of 2:1, if we lose once again we must use a payout of 4:1...etc, our payout ratio would be subject to exponential growth instead of our stake.

Of course, the payout ratio is fixed with casino games, but in trading, we can manipulate the position of our take profit in order to replicate such effect, this is what this strategy is doing. So after a loss, we place our take profit such that a win recover our losses back plus generate a profit.

Advantages

The advantage of this approach is that unlike the martingale we don't double our position size, which instead can remain constant, this is a huge advantage as a martingale will require a significant capital in order to tank a series of losses.

Disadvantages

The main disadvantage of this method is that the price might never reach our take profit after a long losing streak, our balance would remain in the red and we couldn't do anything about it except reset the strategy.

Frictional costs are still a disadvantage, as such, we would need to place our take profits in order to account for them, while this is still better than purchasing additional shares, it minimizes the chances of the price reaching the take profit.

Conclusions

An alternative money management system replicating the effect of a martingale as been presented, we can see that such a system is far from being perfect, and it would be foolish to use it, however, it stills offer a convenient alternative to less aggressive progressive position sizing systems.

I have been receiving some messages from users criticizing me for exposing the martingale money management system, and I understand why but I can't agree, talking about it allow me to warn users against it, the grid-martingale methodology is will create more harm than anything else, the reward is only one side of the story and should always be compared against the risk, so always take a look at all the statics in a backtest.

Thanks for reading!

Shout-Out

This post was made possible thanks to my patrons:

@Happymono, @AmariMars, @kkhaial, @Nugehe, @LucF, @Nosmok, @iflostio, @DankBeans, @ecletv, @Neverstorm, @alex.crown.jr, @uk503, @xkingshotss, @vsov, @jbelka, @yatrader2, @hughza, @ganh

Geometric Brownian Motion BandIf you are an option trader, who are constantly searching opportunities to set up inverse iron condor position or other strategies, you must be familiar in estimating the range induced by Geometric Brownian Motion (GBM), or Lognormal distribution someone may call.

The theory behind is adopted in the Black Scholes Option Pricing model, this assumes the asset price follows the GBM, shown below, and estimates the range where the price will fall into on the specific date and probability.

dS = a dt + v dW

Assuming the drift term is zero, this GBM Band applies the same model and helps you to quickly assess the suitable range to set up your option strategies with simple setting:

Length – number of bars covered

Vol Multiple - the z-score of the probability

Default values of the Length and Vol Multiple are set to 20 bars and 2.0 z-score respectively.

You can find an example how the GMB Band work.

You can also applies this GMB Band like how Bollinger's Band does for swing trade or breakaway trade.

If you find this indicator is useful to you, Star it, Follow, Donate, Like and Share.

Your support is a highly motivation for me.