Mean Reversion Strategy v2 [KL]Description :

This strategy will enter a position when the following conditions are met:

a) Main signal: When source data (ATR) diverts from its moving average value, and

b) Confirmation: If predicted direction of trend is favorable.

Assumptions :

During periods of high price volatility, ATR diverts from its moving average value. Eventually, ATR should revert. But since just knowing the magnitude of increase/decrease of ATR does not indicate a trend signal, we need to introduce a model to predict the current trend.

In short:

• Trend Prediction : This strategy calculates the expected logarithmic return of the security (the "Drift") and considers prices to be moving in uptrend if the drift curve is upward sloping.

• Assessment of ATR diversion : To determine "yes/no" regarding whether ATR at a given point in time has diverted, this script conducts a two-tailed hypothesis test at each candlestick period. The null hypothesis (H0) is that the fast moving average value should equal the slow moving average value (say, denoted as H0: atr14 == atr28; it is assumed that atr28 is more meaningful for the purpose of describing the current trend because it has a larger sample size). Investopedia has an article summarizing this topic .

Exit Condition :

When trailing stop loss hits.

Previous version :

This strategy is based on Version 1 published back in September . This older version considers +/- one standard deviation to be the critical values relative to average ATR when testing whether ATR has diverted from the mean. This does not take Standard Error ("SE") into account. As a result, the threshold is often too wide and it generates too many entry signals.

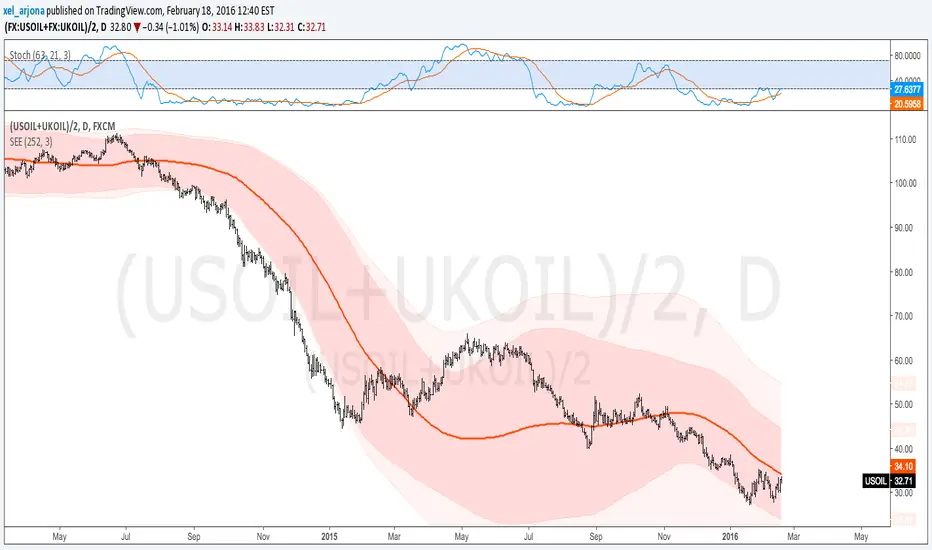

Erro Padrão (EP)

Standard Error of the Estimate -Jon Andersen- V2Original implementation idea of bands by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Standard Error Bands are quite different than Bollinger's.

First, they are bands constructed around a linear regression curve.

Second, the bands are based on two standard errors above and below this regression line.

The error bands measure the standard error of the estimate around the linear regression line.

Therefore, as a price series follows the course of the regression line the bands will narrow , showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands .

Thanks to the work of @glaz & @XeL_arjona

In this version you can change the type of moving averages and the source of the bands.

Add a few studies of @dgtrd

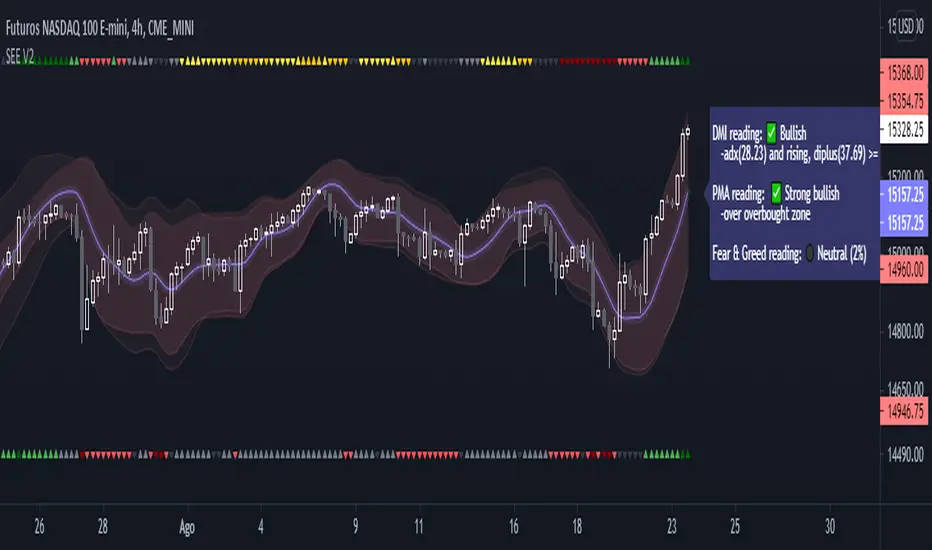

1- ADX Colored Directional Movement Line

Directional Movement (DMI) (created by J. Welles Wilder ) consists of the Average Directional Index ( ADX ), to define whether or not there is a trend present, and Plus Directional Indicator (+D I) and Minus Directional Indicator (-D I) serve the purpose of determining trend direction

ADX Colored Directional Movement Line is custom interpretation of Directional Movement (DMI) with aim to present all 3 DMI indicator components with SINGLE line and ability to be added on top of the price chart (main chart)

How to interpret :

* triangle shapes:

▲- bullish : diplus >= diminus

▼- bearish : diplus < diminus

* colors:

green - bullish trend : adx >= strongTrend and di+ > di-

red - bearish trend : adx >= strongTrend and di+ < di-

gray - no trend : weekTrend < adx < strongTrend

yellow - week trend : adx < weekTrend

* color density:

darker : adx growing

lighter : adx falling

2- Volatility Colored Price/MA Line

Custom interpretation of the idea “Prices high above the moving average (MA) or low below it are likely to be remedied in the future by a reverse price movement”. Further details can be found under study “Price Distance to its MA by DGT”

How to interpret :

-▲ – Bullish , Price Action above Moving Average

-▼ – Bearish , Price Action below Moving Average

-Gray/Black - Low Volatility

-Green/Red – Price Action in Threshold Bands

-Dark Green/Red – Price Action Exceeds Threshold Bands

3- Volume Weighted Bar s

Volume Weighted Bars, a study of Kıvanç Özbilgiç, aims to present whether volume supports price movements. Volume Weighted Bars are calculated based on volume moving average.

How to interpret :

-Volume high above the volume moving average be displayed with red/green colors

-Average volume values will remain as they are and

-Volume low below the volume moving average will be indicated with darker colors

4- Fear & Greed index value, using technical anlysis approach calculated based on :

⮩1 - Price Momentum : Price Distance to its Moving Average

⮩2 - Strenght : Rate of Return, price movement over a period of time

⮩3 - Money Flow : Chaikin Money Flow, quantify changes in buying and selling pressure. CMF calculations is based on Accumulation/Distribution

⮩4 - Market Volatility : CBOE Volatility Index ( VIX ), the Volatility Index, or VIX , is a real-time market index that represents the market's expectation. It provides a measure of market risk and investors' sentiments

⮩5 -Safe Haven Demand: in this study GOLD demand is assumed

Kirshenbaum BandsThis indicator was originally developed by Paul Kirshenbaum, a mathematician with a Ph.D. in economics from New York University.

It uses the standard error of linear regression lines of the closing price to determine band width. This has the effect of measuring volatility around the current trend, rather than measuring volatility for changes in trend.

Good luck!

Standard Error of the Estimate -Composite Bands-Standard Error of the Estimate - Code and adaptation by @glaz & @XeL_arjona

Ver. 2.00.a

Original implementation idea of bands by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

This code is a former update to previous "Standard Error Bands" that was wrongly applied given that previous version in reality use the Standard Error OF THE MEAN, not THE ESTIMATE as it should be used by Jon Andersen original idea and corrected in this version.

As always I am very Thankfully with the support at the Pine Script Editor chat room, with special mention to user @glaz in order to help me adequate the alpha-beta (y-y') algorithm, as well to give him full credit to implement the "wide" version of the former bands.

For a quick and publicly open explanation of this truly statistical (regression analysis) indicator, you can refer at Here!

Extract from the former URL:

Standard Error Bands are quite different than Bollinger's. First, they are bands constructed around a linear regression curve. Second, the bands are based on two standard errors above and below this regression line. The error bands measure the standard error of the estimate around the linear regression line. Therefore, as a price series follows the course of the regression line the bands will narrow, showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands.

Standard Error Bands by @XeL_arjonaStandard Error Bands - Code by @XeL_arjona

Original implementation by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Version 1

For a quick and publicly open explanation of this Statistical indicator, you can refer at Here!

Extract from the former URL:

Standard Error bands are quite different than Bollinger's. First, they are bands constructed around a linear regression curve. Second, the bands are based on two standard errors above and below this regression line. The error bands measure the standard error of the estimate around the linear regression line. Therefore, as a price series follows the course of the regression line the bands will narrow, showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands.