Double CCIThe Commodity Channel Index (CCI) is a momentum oscillator used in technical analysis primarily to identify overbought and oversold levels by measuring an instrument's variations away from its statistical mean. Besides overbought/oversold levels, CCI is often used to find reversals as well as divergences. Originally, the indicator was designed to be used for identifying trends in commodities, however it is now used in a wide range of financial instruments.

There are several steps involved in calculating the CCI. The following example is for a typical 14 Period CCI:

CCI = (Typical Price - 14 Period SMA of TP) / (.015 x Mean Deviation)

Typical Price (TP) = (High + Low + Close)/3

Constant = .015

The Constant is set at .015 for scaling purposes. By including the constant, the majority of CCI values will fall within the 100 to -100 range.

Mean Deviation:

1) Subtract the most recent 14 Period Simple Moving from each typical price (TP) for the Period.

2) Sum these numbers strictly using absolute values.

3) Divide the value generated in step 2 by the total number of Periods (14 in this case).

Overbought and Oversold conditions can be used in their more traditional sense to identify future reversals . Remember true overbought/oversold thresholds values can and often do vary between instruments.

During a Bullish Trend , price crossing above the overbought threshold may indicate strong confidence in the move and price will continue to rise.

During a Bearish Trend , price crossing below the oversold threshold may indicate strong confidence in the move and price will continue to fall.

The first option is a modified CCI indicator that uses the "Arnaud Legoux Moving Average" instead of the SMA, and the source uses the VWAP instead of the HLC3. Added to this version an option to calculate CCI with different types of moving averages:

Green dots mean they are overbought

Orange dots mean they are oversold

Added a "SuperTrend Background" based on the modified CCI indicator:

Bull event = CCI crossing over the 0 line

Bear event = CCI crossing below the 0 line

Added a signal as EMA (modified CCI, signal length)

The second option is a standard CCI indicator that shows a coloured histogram of important levels, giving a good visual of the CCI levels. Added to this version is an extra coloured level +/-200 and an option to use Traditional CCI calculations according to user @JustUncleL

LEVELS:

Aqua: Greater than 200.

Lavender: Greater than 100 and less than 200.

Dark Lavender: Greater than 0 and less than 100.

Dark Coral: Less than 0 and greater than -100.

Coral: Less than -100 and greater than -200.

Light Red: Less than -200.

Pesquisar nos scripts por "美元指数跌破100大关"

Chanu Delta IndicatorThe Chanu Delta Indicator was created as the price difference between the two markets using the principle that the Bitcoin price fluctuations in the BTCUSD market on the BYBIT exchange are greater in the BTCUSDT market. This indicator shows the strength of the current market's buys and sells, and helps in short-term trading.

Chanu Delta Indicator (Δ) = BTCUSD ($) - BTCUSDT ($) (Unit: Dollar, Source: Close)

● Δ > 100 : Strong Buy

● 20 < Δ < 100 : Buy

● -20 < Δ < 20 : Neutral

● -100 < Δ < -20 : Sell

● Δ < -100 : Strong Sell

RedK Volume-Weighted Directional Efficiency Index (DXF)RedK Volume-Weighted Directional Efficiency Index (DXF) is a momentum indicator - that builds on Kaufman's Efficiency Ratio (ER) concept.

DXF utilizes a restricted +100/-100 oscillator to represent the "quality" of a trend, and does a good job in detecting the possibility of an upcoming trend change (in both direction and quality), improving our ability to make decisions on trade entries and exits.

Here's a quick background on Kaufman's Efficiency Ratio (ER)

------------------------------------------------------------------------------- Copied from internet sources -----------------------------

Developed by Perry Kaufman and introduced in his book “New Trading Systems and Methods”, the Efficiency Ratio reflects relative market speed to volatility. There are cases, when it is used as a filter, which helps a trader to avoid ”choppy” markets or trading ranges and to identify smoother trends.

ER is the result of dividing the net change in price movement during n-periods by the sum of all bar-to-bar price changes during the same n-periods. In case the market is trending smoother, then the ratio will be higher. In case the ratio shows readings in proximity to zero, this implies that market movement is inefficient and ”choppy”.

If the Efficiency Ratio shows a reading of +100, this means that the trading instrument is in a bull trend and trending with perfect efficiency.

If the Efficiency Ratio shows a reading of -100, this means that the trading instrument is in a bear trend and trending with perfect efficiency.

It is impossible for any instrument to have a perfect Efficiency ratio, because any movement against the major trend during the examined period of time would cause the ratio to drop.

If the Efficiency Ratio shows a reading above +30 (common setting for the "Significant Level"), this is indicative of a quality bull trend. If the ratio shows a reading below -30, this is indicative of a quality bear trend.

------------------------------------------------------------------------------- End of Copy -------------------------------------------------------------------------------------------------------

Kaufman also used the ER as basis for his famous Kaufman Adaptive Moving Average (KAMA).

Read more on ER & Kama here

How is DXF different from other ER-based indicators?

------------------------------------------------------------------

- Let's get the easy part out of the way: DXF has a "volume-weighting" option ✔

This option is OFF by default (to avoid errors with instruments with no volume data)

- once this option is applied, it provides the benefit of combining the volume effect into the calculation - those who appreciate the effect of volume on price action will hopefully find this option valuable

- The calculation of ER and how it can be "best utilized":

Let's examine the ER concept a bit closer: as a (math) concept, the (original) Efficiency Ratio (ER) takes the positive change of the price of an instrument during a certain period, and divide it by the sum of (absolute) price moves that were observed during that same period.

So, in the trader's language, we will be saying "out of a total of $20 moves (up and down) that MSFT did in the past 10 days, MSFT only made a net change of $5 up during that period" - so the "10-day ER" for MSFT in that case is 5/20 = 25% -- then we continue to observe that ongoing "10-day ER" and if it increases, we can expect that MSFT is going to establish a strong move (trend) up --- right?

the magic word here is to "observe the ongoing ER" - many of the ER based indicators just use the ER as calculated by Kaufman's original method. IMHO, these are just "point-in-time readings" - if we hope to get real insights from the ER, we need to take an average of that reading - for our "time window" we're interested in - and only then we can identify trends and patterns in the ER value as it changes during that windowss- DXF does that - and that allows a trader to say "the (weighted) 5-day average of the 10-day ER for MSFT is increasing, and that why i expect an up-trend" -- makes sense ? both the "Lookback" used to calculate the ER, and the Length of observed "window" for the Average ER are adjustable in DXF settings

Other Uses and Settings :

---------------------------------

- As a momentum indicator, DXF can predict an upcoming change of trend - cause that will reflect on the average ER value. There are few examples in the chart where the price move and ER trend *do not agree* - The trader can see these signs and take decisions accordingly

- DXF can help reveal best entries and exits: assume we are long-term bullish on MSFT, and we want to "buy the dip" - DXF can help reveal the time where price is recovering from extreme weakness - and that would be the ideal buy opportunities for us - exampled marked on the chart

- the Stepping & Smoothing options enable better visualization of the DXF plot. the "raw" DXF is still shown as a silver line.

- The "Significant Levels" option is available and is set to -20/+20 by default .. also adjustable in indicator settings.

- Please use DXF in combination with other trend and volume indicators, and with thorough chart / price action analysis and not in isolation to ensure you get proper signal confirmation for trades. In the chart above, you can see DXF combined with a moving average that can act as a filter and to confirm the price moves.

---------------------------------------------------

As usual, feedback & comments are welcome - if you find this work useful in your trading arsenal, please share a comment - i would be more than happy to learn about that. Good luck!

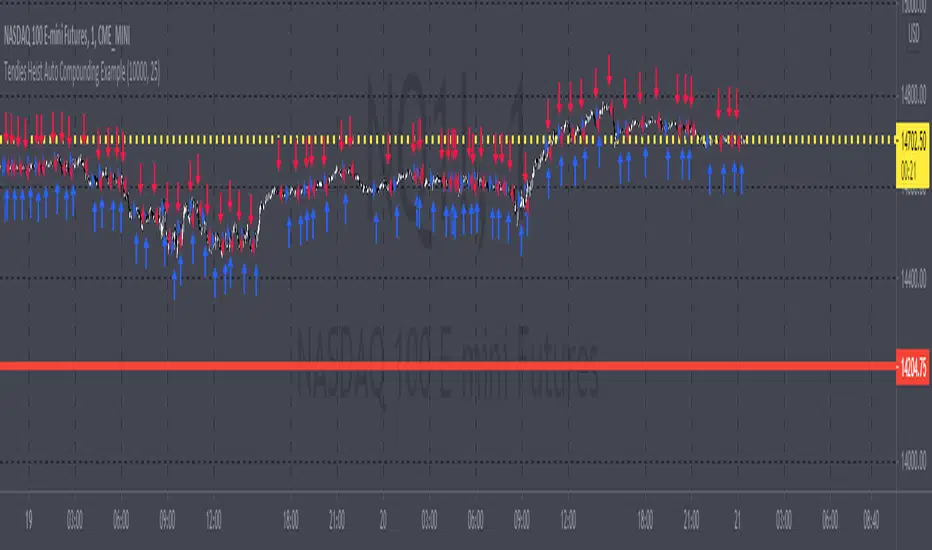

Tendies Heist Auto Compounding ExampleThis is an example of how we can use compounding to control our position size. This example shows how we can automatically add and reduce position size based on account equity. The "initial capital" in properties is the starting account equity. At default its set to 100,000. If our max position size is set to 25 then the very first position that's taken has a position size of 10, IF our leverage is set to 10,000. Account equity divided by leverage equals position size. So in that example 100,000 divided by 10,000 in leverage gives us a max position size of 10. However the max position size was set to 25 meaning we would need 250k in equity for it to open a position size of 25 with the leverage set at 10k. Now if the initial capital was set to 100,000 and the max position size was set to 5 and leverage remained at 10,000, all though 100,000 divided by 10,000 equals 10 it will ONLY open a position size of 5, because the max position size in this example was set at 5. Since this works for strategies you may look through the trade log on the posted back test and check out the position size, you can see in this back test the default 100k is used for the initial capital and the default 10k was used for the leverage. You will be able to see as this logic loses money it takes contracts away and as it gains money it adds contracts. I'm using trading view's basic strategy logic example to provide an example of how the compounding logic works.

Note, don't forget to add the syntax below to your strategy.entry call for this logic to work.

qty = size

Tendies Heist LLC 2021

Cumulative Volume DeltaThis indicator is called Cumulative Volume Delta (CVD), and it is the cumulative difference between buying and selling pressure.

Note, however, that it is not an exact CVD, because Pine Script does not allow you to get the Bid Volume and Ask Volume.

Instead, it uses volume and candlestick length to determine the pressure.

Example: Volume is 100, price change is +1.0% → Buying pressure is 1

Volume is 100, price change is -0.5% → Selling pressure is 0.5

このインジケーターは、Cumulative Volume Delta(CVD)と呼ばれるもので、買い圧力と売り圧力の差を累積したものです。

しかし、Pine Scriptでは買い圧力と売り圧力(Bid VolumeとAsk Volume)を取得することはできないため、正確なCVDではないことに注意してください。

代わりに出来高とローソク足の長さで圧力を判断判断しています。

例:出来高が100、価格の変動が+1.0% → 買い圧力は1

出来高が100、価格の変動が-0.5% → 売り圧力は0.5

SuperTrend Oscillator [LuxAlgo]This oscillator is made of three components, all derived from the SuperTrend indicator. This approach allows the user to easily determine overbought/sold zones, identify whether a retracement is present or if the price is ranging or trending. It also allows for the anticipation of the potential price cross with the SuperTrend.

We provide additional information including whether a signal returned by the SuperTrend was false, as well as the percentage of false signals.

Settings

Length: Period of the "average true range" used in the calculation of the SuperTrend

Mult: Multiplicative factor for the "average true range"

Smooth: Determines the degree of smoothing of the histogram

Misc:

Fixed Transparency: Use a fixed transparency for the main oscillator

Show Lines: Show the lines displayed by the indicator

Show Labels: Show the labels displayed by the indicator

Usage

The indicator is in a range of (-100,100) with values closer to 100/-100 indicating a stronger trend. The main oscillator value above 0 indicates that the price is above the SuperTrend.

It is possible to identify when a retracement is present in a trend. This is often indicated by an oscillator value moving within 50/-50.

Each overbought/oversold level can be used to determine potential exit points.

The indicator also includes two additional oscillators derived from the main oscillator. A smoothed version of the main oscillator (Signal), and a smoothed version of the difference between the Main and Signal oscillators (Histogram), thus making the oscillator part of the indicator more similar to MACD.

One can use the histogram to anticipate when the price might cross the SuperTrend by comparing the sign between the main and histogram. Potential false signals can also be filtered with this method.

Certain crosses between the price and SuperTrend can be filtered out when the histogram and main oscillator have a different sign (here main = 1, histogram = -1).

We include various indications in order to analyze the signals returned by the SuperTrend. The indicator displays symbols indicating whether a signal was false or not.

A cross symbol will be displayed at the top of the displayed lines when the previous Buy signal was false, else a checkmark is displayed. Symbols displayed at the bottom of the lines are referring to sell signals. We also provide a percentage of false signals, calculated over the entire chart history.

Details

The scaling method used is similar to max-min normalization. We first compute the difference between the price and SuperTrend and divide the result by the difference between the upper and lower extremity used to compute the SuperTrend. Values higher than (1,-1) can occur when price crosses the SuperTrend and as such we use the max and min functions to attenuate these.

The filter used to compute the signal line is based on exponential averaging and is fully adaptive. The smoothing factor used for its computation is the squared value of the main oscillator, divided by length . Since higher values of the oscillator are associated with trending markets, the filter will be closer to the main oscillator when the market is ranging.

Price Action IndexI've created a simple oscillator which I think does a good job of easily showing you when price is worth watching or not. I think all too often you get stuck looking at something like an RSI and end up trading noise.

From my observations and experiences, I've found that there are 2 major catalysts for price movement--

Price is either trending and reaches a top or bottom, or

Price is consolidating and ready to make a move in some direction

These movements can be seen quite well from a Bollinger Band, which is what mostly gave me the inspiration. When I watch a chart with a BB on it I see that either you're looking to trade price moving out of a squeeze or riding price up/down the band until it crosses over and makes a move to the moving average.

My solution was to multiply the direction of price by the strength of its deviation.

Price gets converted into a signal between -1.0 (bottom of the range) and 1.0 (top of the range)

Standard Deviation gets converted into a stochastic signal between 0 (next to no deviation from mean) and 100 (highest deviation in lookback)

These 2 get multiplied by each other

The result tells you if price action is trending bullish and if its approaching max strength (perhaps Overbought), example: Price is hitting highs (1.0) and deviation is also at its highest (100) = 100, opposite for bearish

Result can also tell you if price is at the top of the range but the deviation is so tiny and we're mostly pinned to the mean (1.0 * 5 = only 5)

How to Trade this Indicator--

If the indicator is stuck near the middle and purple:

- Don't make directional trades or you'll be eaten alive by the chop

- Good idea to sell options, Iron Condors/Butterflies, etc

- Wait for a move to breakout --> the purple will fade away and give way to a direction

--- As in all trading scenarios, be mindful of fakeouts/short moves to one direction that very quickly get reversed

If the indicator is heading higher:

- This would indicate there is a bull trend going on, get long

- If we are reaching the overbought area, this is an ideal place to take profits or look at spreads like Bearish Call Spreads (sell calls)

- I think you can make your own determination of when to sell by either selling when we're in the overbought area (if it reaches there) or staying bullish so long as it is above the zone

If the indicator is heading lower:

- Bear trend, shorting is possible

- Can use this as a contrarian signal to buy lows

A couple of charts with the indicator and a purple squeeze box I've drawn (can sometimes get noisy in real-time, but hindsight is 20/20)--

Bitcoin on Daily with default 20 length

Gamestop on 30 minute time frame with 100 length

Please feel free to use this indicator for your trading or your own indicators. This particular script is very stripped down/bare bones from what I have been working on as an ongoing project. If TradingView ever returns scripts you can sell, I would probably open that up for a small premium.

LPS PLSY INDICATOR for VSA( Google translation from Russian.)

Signal conditions:

1. There is a bar with an increased volume

2. The next bar after the bar with increased volume closes in the other direction

Arguments:

Comparison period - the period during which the volumes are compared with each other to calculate the bars with the increased volume.

sensitivity of increased volumes - according to the percentrank indicator - the border above which the volume will be considered large, the same as in the Volume on bar VSA indicator - indicator V2 - for clarity of how it works, I recommend looking at it.

efficiency of the next bar - (efficiency of the next bar from 0 to 100) ") - the efficiency of buying or selling on the next bar, bar field with a large volume. If the value is closer to 100, then the bars whose spread corresponds to the inserted volume will be taken into account, if closer to 0, then bars with a small spread and a large volume can be taken into account.

This argument is calculated similarly to the efficiency of bulls and bears for VSA

Attention.

In its original form, this indicator can give a large number of false signals. To filter out false signals, it should be used after studying the theory of VSA.

Russian language

Условия для сигнала:

1. Имеется бар с повышенным объёмом

2. Следующий бар после бара с повышенным объемом закрывается в другую сторону

Аргументы:

период для сравнения – период, на котором сравниваются между собой объёмы, для вычисления баров с повышенным объемом.

чувствительность повышенных объемов – согласно индикатору percentrank – граница выше которой̆ объем будет считаться большим, то же самое, что в индикаторе Volume on bar VSA - indicator V2 – для наглядности как это работает рекомендую посмотреть его.

эффективность следующего бара от 0 до 100 - эффективность покупок или продаж на следующем баре, поле бара с большим объемом. Если значение ближе к 100 то будут учитываться бары у которых спред соответствует вложенному объему, если ближе к 0 то могут учитываться бары у которых спред маленький а объем большой.

Расчёт этого аргумента производится аналогично индикатору efficiency of bulls and bears for VSA

Примечание

В исходном виде этот индикатор может давать большое количество ложных сигналов. Для отсеивания ложных сигналов его следует применять после изучения теории VSA.

CRYPTO HA Strategy money maker long termToday I bring you another amazing strategy.

Its made of 2 EMA in this case 50 and 100.

At the same time, internaly for candles we calculate the candles using the HA system ( while still using in live the normal candles). This way we can assure that even if we use HA candles, we avoid repainting, and its legit.

We first calculate the HA candles based on the EMA 50 values, and after that , we use that candle properties to apply to EMA 100.

Once we have that, for entries we have the next conditions :

sell = o2 > c2 and o2 < c2 and time_cond

buy = o2 < c2 and o2 > c2 and time_cond

For sell : Our open from HA 100 is bigger than Close from ha 100, and the previous open is smaller than previous close

For long : Our open from ha 100 is smaller than close from ha 100 and the previous open is bigger than previous close.

Then we have 2 options :

If we wnat to go only long , which is my prefered version ,or the original one where we go both long and short.

I found that the best results are in general around bigger timeframes, 1h+ , 3h works the best so far on my tests.

For exit we have 2 versions :

1 lets say we had a long signal, as soon as we have a short signal we close the trade. Viceversa for short.

2. Is based on price % movement. In this case I use 7.5% price movement of asset.

We have no TP in use for this system.

For the purpose of this test I use 10.000 $ account. For test I use 100% of it, without any leverage.

I use the SL based on price movement , which is a very risky tool, since it can fluctuate even at 20-30% of our capital.

For comission I used 0.1% for each deal, and a slippage of 5 points.

Be cautious with this system !

If you have any questions , message me.

Easy Loot Golden CrossGolden/Death Cross Moving Average Indicator

30, 100 & 200 period Simple Moving Average (SMA).

30 = Yellow

100 = Green

200 = Black

Black crosses mark the 'golden crosses' as well as the 'death crosses'. These black crosses appear when the 30 crosses the 100 & when the 100 crosses the 200. These black crosses don't tell you when to buy/sell, but simply indicate interest in the market.

This code is open-source so feel free to add this indicator to your chart and play around with the different moving average timeframes & color schemes.

Golden Cross

The golden cross occurs when a short-term moving average crosses over a major long-term moving average to the upside and is interpreted by analysts and traders as signaling a definitive upward turn in a market. Basically, the short-term average trends up faster than the long-term average, until they cross.

There are three stages to a golden cross:

A downtrend that eventually ends as selling is depleted

A second stage where the shorter moving average crosses up through the longer moving average

Finally, the continuing uptrend, hopefully leading to higher prices

Death Cross

Conversely, a similar downside moving average crossover constitutes the death cross and is understood to signal a decisive downturn in a market. The death cross occurs when the short term average trends down and crosses the long-term average, basically going in the opposite direction of the golden cross.

The death cross preceded the economic downturns in 1929, 1938, 1974, and 2008.

VPoC per barThis study prints the current bar VPoC as an horizontal line.

It's aimed originally at BTCUSDT pair and 15m timeframe.

HOW IT WORKS

Zoom In mode: This is the default mode.

The study zooms in into the latest 15 1-minute bar candles in order to calculate the 15 minute candle VPoC.

Zoom Out mode: The VPoC from the last n bars from the current timeframe that match desired timeframe is shown on each bar.

In either case you are recommended to click on the '...' button associated to this study

and select 'Visual Order. Bring to Front.' so that it's properly shown in your chart.

HOW IT WORKS - Zoom In mode

Make sure that '(VP) Zoom into the VP timeframe' setting is set to true.

Choose the zoomed in timeframe where to calculate VPoC from thanks to the '(VP) Zoomed timeframe {1 minute}' setting.

Change '(VP) Zoomed in timeframe bars per current timeframe bar {15}' to its appropiated value. You just need to divide the current timeframe minutes per the zoomed in timeframe minutes per bar. E.g. If you are in 60 minute timeframe and you want to zoom in into 5 minute timeframe: 60 / 5 = 12 . You will write 12 here.

HOW IT WORKS - Zoom Out mode

Make sure that '(VP) Zoom into the VP timeframe' setting is set to false.

If you are using the Zoom out mode you might want to set '(VP) Print VPoC price as discrete lines {True}' to false.

Either choose the zoommed out timeframe where to calculate VPoC from thanks to the '(VP) Zoomed timeframe {1 minute}' setting or turn on the '(VP) Use number of bars (not VP timeframe)' setting in order to use '(VP) Number of bars {100}' as a custom number of bars.

WARNING - Zoom In mode last bar

The way that PineScript handles security function in last bar might result on the last bar not being accurate enough.

SETTINGS

__ SETTINGS - Volume Profile

(VP) Zoomed timeframe {1 minute}: Timeframe in which to zoom in or zoom out to calculate an accurate VPoC for the current timeframe.

(VP) Zoomed in timeframe bars per current timeframe bar {15}: Check 'HOW IT WORKS - Zoom In mode' above. Note : It is only used in 'Zoom in' mode.

(VP) Number of bars {100}: If 'Use number of bars (not VP timeframe)' is turned on this setting is used to calculate session VPoC. Note : It is only used in 'Zoom out' mode.

(VP) Price levels {24}: Price levels for calculating VPoC.

__ SETTINGS - MAIN TURN ON/OFF OPTIONS

(VP) Print VPoC price {True}: Show VPoC price

(VP) Zoom into the VP timeframe: When set to true the VPoC is calculated by zooming into the lower timeframe. When set to false a higher timeframe (or number of bars) is used.

(VP) Realtime Zoom in (Beta): Enable real time zoom for the last bar. It's beta because it would only work with zoomed in timeframe under 60 minutes. And when ratio between zoomout and zoomin is less than 60. Note : It is only used in 'Zoom in' mode.

(VP) Use number of bars (not VP timeframe): Uses 'Number of bars {100}' setting instead of 'Volume Profile timeframe' setting for calculating session VPoC. Note : It is only used in 'Zoom out' mode.

(VP) Print VPoC price as discrete lines {True}: When set to true the VPoC is shown as an small line in the center of each bar. When set to the false the VPoC line is printed as a normal line.

__ SETTINGS - EXTRA

(VP) VPoC color: Change the VPoC color

(VP) VPoC line width {1}: Change VPoC line width (in pixels).

(VP) Use number of bars (not VP timeframe): Uses 'Number of bars {100}' setting instead of 'Volume Profile timeframe' setting for calculating session VPoC. Note : It is only used in 'Zoom out' mode.

(VP) Print VPoC price as discrete lines {True}: When set to true the VPoC is shown as an small line in the center of each bar. When set to the false the VPoC line is printed as a normal line.

CREDITS

I have reused and adapted some code from

"Poor man's volume profile" study

which it's from TradingView IldarAkhmetgaleev user.

[Strategy] Simple Golden CrossSimple Golden Cross Strategy.

Works best on a daily chart on "Blue Chip" cryptos such as BTC, ETH, and LTC.

Entry Signal:

-50 day moving average crosses over the 100 day moving average.

Exit Signal:

-50 day moving average crosses under the 100 day moving average.

-Daily candle closes under the 100 day moving average (support).

-100 day moving average crosses under the 200 day moving average.

STRATEGY TESTER ENGINE - ON CHART DISPLAY - PLUG & PLAYSo i had this idea while ago when @alexgrover published a script and dropped a nugget in between which replicates the result of strategy tester on chart as an indicator.

So it seemed fair to use one of his strategy to display the results.

This strategy tester can now be used in replay mode like an indicator and you can see what happen at a particular section of the chart which was is not possible in default strategy tester results of TV.

Please read how each result is calculated so you will know what you are using.

This engine shows most common results of strategy tester in a single screen, which are as follows:

1. Starting Capital

2. Current Profit Percentage

3. Max Profit Percentage

4. Gross Profit

5. Gross Loss

6. Total Closed Trades

7. Total Trades Won

8. Total Trades Lost

9. Percentage Profitable

10. Profit Factor

11. Current Drawdown

12. Max Drawdown

13. Liquidation

So elaborating on what is what:

1. Starting Capital - This stays 0, which signifies your starting balance as 0%. It is set to 0 so we can compare all other results without any change in variables. If set to 100, then all the results will be increased by 100. Some users might find it useful to set it to 100, then they can change code on line 41 from to and it should show starting balance as 100%.

2. Current Profit Percentage - This shows your current profit adjusted to current price of the candle, not like TV which shows after candle is close. There is a comment on the line 38 which can be removed and your can see unrealized profit as well in this section. Please note that this will affect Draw-down calculations later in this section.

3. Max Profit Percentage - This will show you your max profit achieved during your strategy run, which was not possible yet to see via strategy tester. So, now you can see how much profit was achieved by your strategy during the run and you can compare it with chart to see what happens during bull-run or bear-run, so you can further optimize your strategy to best suit your desired results.

4. Gross Profit - This is total percentage of profit your strategy achieved during entire run as if you never had any losses.

5. Gross Loss - This is total percentage of loss your strategy achieved during entire run as if you never had any profits.

6. Total Closed Trades - This is total number of trades that your strategy has executed so far.

7. Total Trades Won - This is the total number of trades that your strategy has executed that resulted in positive increase in equity.

8. Totals Trades Lost - This is the total number of trades that your strategy has executed that resulted in decrease in equity.

9. Percentage Profitable - This is the ratio between your current total winning trades divided by total closed trades, and finally multiplied by 100 to get percentage results.

10. Profit Factor - This is the ratio between Gross Profit and Gross Loss, so if profit factor is 2, then it indicates that you are set to gain 2 times per your risk per trade on average when total trades are executed.

11. Current Drawdown - This is important section and i want you to read this carefully. Here draw-down is calculated very differently than what TV shows. TV has access to candle data and calculates draw-down accordingly as per number of trades closed, but here DD is calculated as difference between max profit achieved and current profit. This way you can see how much percentage you are down from max peak of equity at current point in time. You can do back-test of the data and see when peak was achieved and how much your strategy did a draw-down candle by candle.

12. Max Drawdown - This is also calculated differently same as above, current draw-down. Here you can see how much max DD your strategy did from a peak profit of equity. This is not set as max profit percentage is set because you will see single number on display, while idea is to keep it custom. I will explain.

So lets say, your max DD on TV is 30%. Here this is of no use to see Max DD , as some people might want to see what was there max DD 1000 candles back or 10 candle back. So this will show you your max DD from the data you select. TV shows 25000 candle data in a chart if you go back, you can set the counter to 24999 and it will show you max DD as shown on TV, but if you want custom section to show max DD , it is now possible which was not possible before.

Also, now let's say you put DD as 24999 and open a chart of an asset that was listed 1 week ago, now on 1H chart max DD will never show up until you reach 24999 candle in data history, but with this you can now enter a manual number and see the data.

13. Liquidation - This is an interesting feature, so now when your equity balance is less than 0 and your draw-down goes to -100, it will show you where and at what point in time you got liquidated by adding a red background color in the entire section. This is the most fun part of this script, while you can only see max DD on TV.

------------------------------------------------------------------------------

How to Use -

1 word, plug and play. Yes. Actual codes start from line 33.

select overlay=false or remove it from the title in your strategy on first line,

Just copy the codes from line 33 to 103,

then go to end section of your strategy and paste the entire code from line 33 to line 103,

see if you have any duplicate variable, edit it,

Add to chart.

What you see above is very contracted view. Here is how it looks when zoomed in.

imgur.com

----------------------------------------------------------------------------------

Feel free to edit and share and use. If you use it in your scripts, drop me tag. Cheers.

EulerMethod: CryptoCapEN

Shows the cryptocurrency market capitalization balance for the period

Initial data

Bitcoin Capitalization - CRYPTOCAP: BTC

Altcoin Capitalization - CRYPTOCAP: TOTAL2

Money circulates from fiat to bitcoin, from bitcoin to altcoins, from altcoins to fiat

This indicator applies the RSI algorithm to changes in capitalization

The divergence of indices shows an imbalance

Balance level: 0, Maximum: +100, Minimum: -100

(!) Artifacts of indicator readings may occur due to incorrect input data

RU

Показывает баланс капитализации крипторынка за период

Исходные данные

Капитализация Биткоина — CRYPTOCAP:BTC

Капитализация Альткоинов — CRYPTOCAP:TOTAL2

Деньги циркулируют из фиата в биткоин, из биткоина в альткоины, из альткоинов в фиат

В этом индикаторе применяется алгоритм RSI к изменениям капитализации

Расхождения индексов показывают дисбаланс

Балансовый уровень: 0, Максимум: +100, Минимум: -100

(!) Могут возникать артефакты показаний индикатора из-за неправильных исходных данных

Correlation MatrixIn financial terms, 'correlation' is the numerical measure of the relationship between two variables (in this case, the variables are Forex pairs).

The range of the correlation coefficient is between -1 and +1. A correlation of +1 indicates that two currency pairs will flow in the same direction.

A correlation of -1 indicates that two currency pairs will move in the opposite direction.

Here, I multiplied correlation coefficient by 100 so that it is easier to read. Range between 100 and -100.

Color Coding:-

The darker the color, the higher the correlation positively or negatively.

Extra Light Blue (up to +29) : Weak correlation. Positions on these symbols will tend to move independently.

Light Blue (up to +49) : There may be similarity between positions on these symbols.

Medium Blue (up to +75) : Medium positive correlation.

Navy Blue (up to +100) : Strong positive correlation.

Extra Light Red (up to -30) : Weak correlation. Positions on these symbols will tend to move independently

Light Red (up to -49) : There may be similarity between positions on these symbols.

Dark Red: (up to -75) : Medium negative correlation.

Maroon: (up to -100) : Strong negative correlation.

BO - CCI Arrow with AlertBO - CCI Arrow with Alert base on CCI indicator to get signal for trade Binary Option.

Rules of BO - CCI Arrow with Alert below:

A. Setup Menu

1. cciLength:

* Default CCI lenght = 14

2. Linear Regression Length:

* Periods to calculate Linear Regression of CCI,

* Default value = 5

3. Extreme Level:

* Default top extreme level = 100

* Default bottom extreme level = -100

4. Filter Length:

* Periods to define highest or lowest Linear Regression

* Default value = 6

B. Rule Of Alert Bar

1. Put Alert Bar

* Current Linear Regression Line created temporrary peak

* Peak of Linear Regression Line greater than Top Extreme Level (100)

* Previous Linear Regression is highest of Filter Length (6)

* Previous Linear Regression is greater than previous peak of Linear Regression Line

* Current price greater than previous low

* CCI(14) less than Linear Regression Line

2. Call Alert Bar

* Current Linear Regression Line created temporrary bottom

* Bottom of Linear Regression Line less than Bottom Extreme Level (-100)

* Previous Linear Regression is lowest of Filter Length (6)

* Previous Linear Regression is less than previous bottom of Linear Regression Line

* Current price less than previous lhigh

* CCI(14) greater than Linear Regression Line

B. Rule Of Entry Bar and Epiry.

1. Put Entry with expiry 3 bars:

* After Put Alert Bar close with signal confirmed, put Arrow appear, and after 3 bars, result label will appear to show win trade, loss trade or draw trade

2. Call Entry with expiry 3 bars:

* After Call Alert Bar close with signal confirmed, call Arrow appear, and after 3 bars, result label will appear to show win trade, loss trade or draw trade.

3. While 1 trade is opening no more any signal

C. Popup Alert/Mobile Alert

1. Signal alert: Put Alert or Call Alert will send to mobile or show popup on chart

2. Put Alert: only Put Alert will send to mobile or show popup on chart

3. Call Alert: only Call Alert will send to mobile or show popup on chart

Point and Figure (PnF) CCIThis is live and non-repainting Point and Figure Chart Commodity Channel Index - CCI tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

Commodity Channel Index – CCI was developed by Donalt Lambert. CCI can be used to identify overbought or oversold, a new trend or warn of extreme conditions. CCI measures the difference between a security's price change and its average price change. High positive readings indicate that prices are well above their average, which is a show of strength. Low negative readings indicate that prices are well below their average, which is a show of weakness.

The Formula for the Commodity Channel Index ( CCI ) Is:

CCI = (Typical Price – L-period SMA of TP) / (0.015 * Mean Deviation)

Mean Deviation = (SumOf 1->L ( |TP – MA| )) / L

L = Length

TP = Typical Price

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Upper Band : as default, Upper band is 100

Lower Band : as default, Lower band is -100

There are alerts when P&F CCI moves above Upper Band or moves below Lower Band.

Double MA CCI"What is the Commodity Channel Index (CCI)?

Developed by Donald Lambert, the Commodity Channel Index (CCI) is a momentum-based oscillator used to help determine when an investment vehicle is reaching a condition of being overbought or oversold. It is also used to assess price trend direction and strength. This information allows traders to determine if they want to enter or exit a trade, refrain from taking a trade, or add to an existing position. In this way, the indicator can be used to provide trade signals when it acts in a certain way.

KEY TAKEAWAYS

• The CCI measures the difference between the current price and the historical average price.

• When the CCI is above zero it indicates the price is above the historic average. When CCI is below zero, the price is below the hsitoric average.

• High readings of 100 or above, for example, indicate the price is well above the historic average and the trend has been strong to the upside.

• Low readings below -100, for example, indicate the price is well below the historic average and the trend has been strong to the downside.

• Going from negative or near-zero readings to +100 can be used as a signal to watch for an emerging uptrend.

• Going from positive or near-zero readings to -100 may indicate an emerging downtrend.

• CCI is an unbounded indicator meaning it can go higher or lower indefinitely. For this reason, overbought and oversold levels are typically determined for each individual asset by looking at historical extreme CCI levels where the price reversed from." ----> 1

SOURCE

1: (SINCE IM NOT A "PRO" MEMBER I C'ANT POST THE SOUCRE URL..., webpage consulted at : 8:50 GMT -5 ; the 2020-01-18)

I- Added a 2nd MA length and changed the default values of the source type and switched the SMA to a MA.

II- In process to add analytic MACD histogram correlation and if possible, ploting a relative histogram between the CCI upper and lower band.

P.S.:

Don't set your moving averages lengths to far from each other... This could result in fewer convergence and divergence, also in fewer crossing MA's.

Have a good year 2020 !!

//----CODER----//

R.V.

Multi momentum indicatorScript contains couple momentum oscillators all in one pane

List of indicators:

RSI

Stochastic RSI

MACD

CCI

WaveTrend by LazyBear

MFI

Default active indicators are RSI and Stochastic RSI

Other indicators are disabled by default

RSI, StochRSI and MFI are modified to be bounded to range from 100 to -100. That's why overbought is 40 and 60 instead 70 and 80 while oversold -40 and -60 instead 30 and 20.

MACD and CCI as they are not bounded to 100 or 200 range, they are limited to 100 - -100 by default when activated (extras are simply hidden) but there is an option to show full indicator.

In settings there are couple more options like show crosses or show only histogram.

Default source for all indicators is close (except WaveTrend and MFI which use hlc3) and it could be changed but for all indicators.

There is an option for 2nd RSI which can be set for any timeframe and background calculated by Fibonacci levels.

Open Interest Rank-BuschiEnglish:

One part of the "Commitment of Traders-Report" is the Open Interest which is shown in this indicator (source: Quandl database).

Unlike my also published indicator "Open Interest-Buschi", the values here are not absolute but in a ranking system from 0 to 100 with individual time frames-

The following futures are included:

30-year Bonds (ZB)

10-year Notes ( ZN )

Soybeans (ZS)

Soybean Meal (ZM)

Soybean Oil (ZL)

Corn ( ZC )

Soft Red Winter Wheat (ZW)

Hard Red Winter Wheat (KE)

Lean Hogs (HE)

Live Cattle ( LE )

Gold ( GC )

Silver (SI)

Copper (HG)

Crude Oil ( CL )

Heating Oil (HO)

RBOB Gasoline ( RB )

Natural Gas ( NG )

Australian Dollar (A6)

British Pound (B6)

Canadian Dollar (D6)

Euro (E6)

Japanese Yen (J6)

Swiss Franc (S6)

Sugar ( SB )

Coffee (KC)

Cocoa ( CC )

Cotton ( CT )

S&P 500 E-Mini (ES)

Russell 2000 E-Mini (RTY)

Dow Jones Industrial Mini (YM)

Nasdaq 100 E-Mini (NQ)

Platin (PL)

Palladium (PA)

Aluminium (AUP)

Steel ( HRC )

Ethanol (AEZ)

Brent Crude Oil (J26)

Rice (ZR)

Oat (ZO)

Milk (DL)

Orange Juice (JO)

Lumber (LS)

Feeder Cattle (GF)

S&P 500 ( SP )

Dow Jones Industrial Average Index (DJIA)

New Zealand Dollar (N6)

Deutsch:

Ein Bestandteil des "Commitment of Traders-Report" ist das Open Interest, das in diesem Indikator dargestellt wird (Quelle: Quandl Datenbank).

Anders als in meinem ebenfalls veröffentlichten Indikator "Open Interest-Buschi" werden hier nicht die absoluten Werte dargestellt, sondern in einem Ranking-System von 0 bis 100 mit individuellen Zeitrahmen.

Folgende Futures sind enthalten:

30-jährige US-Staatsanleihen (ZB)

10-jährige US-Staatsanleihen ( ZN )

Sojabohnen(ZS)

Sojabohnen-Mehl (ZM)

Sojabohnen-Öl (ZL)

Mais( ZC )

Soft Red Winter-Weizen (ZW)

Hard Red Winter-Weizen (KE)

Magerschweine (HE)

Lebendrinder ( LE )

Gold ( GC )

Silber (SI)

Kupfer(HG)

Rohöl ( CL )

Heizöl (HO)

Benzin ( RB )

Erdgas ( NG )

Australischer Dollar (A6)

Britisches Pfund (B6)

Kanadischer Dollar (D6)

Euro (E6)

Japanischer Yen (J6)

Schweizer Franken (S6)

Zucker ( SB )

Kaffee (KC)

Kakao ( CC )

Baumwolle ( CT )

S&P 500 E-Mini (ES)

Russell 2000 E-Mini (RTY)

Dow Jones Industrial Mini (YM)

Nasdaq 100 E-Mini (NQ)

Platin (PL)

Palladium (PA)

Aluminium (AUP)

Stahl ( HRC )

Ethanol (AEZ)

Brent Rohöl (J26)

Reis (ZR)

Hafer (ZO)

Milch (DL)

Orangensaft (JO)

Holz (LS)

Mastrinder (GF)

S&P 500 ( SP )

Dow Jones Industrial Average Index (DJIA)

Neuseeland Dollar (N6)

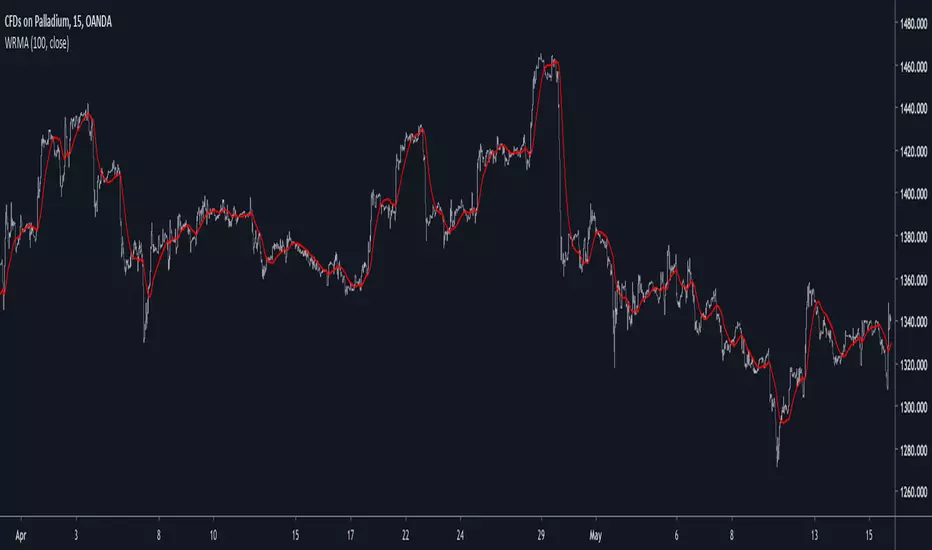

Well Rounded Moving AverageIntroduction

There are tons of filters, way to many, and some of them are redundant in the sense they produce the same results as others. The task to find an optimal filter is still a big challenge among technical analysis and engineering, a good filter is the Kalman filter who is one of the more precise filters out there. The optimal filter theorem state that : The optimal estimator has the form of a linear observer , this in short mean that an optimal filter must use measurements of the inputs and outputs, and this is what does the Kalman filter. I have tried myself to Kalman filters with more or less success as well as understanding optimality by studying Linear–quadratic–Gaussian control, i failed to get a complete understanding of those subjects but today i present a moving average filter (WRMA) constructed with all the knowledge i have in control theory and who aim to provide a very well response to market price, this mean low lag for fast decision timing and low overshoots for better precision.

Construction

An good filter must use information about its output, this is what exponential smoothing is about, simple exponential smoothing (EMA) is close to a simple moving average and can be defined as :

output = output(1) + α(input - output(1))

where α (alpha) is a smoothing constant, typically equal to 2/(Period+1) for the EMA.

This approach can be further developed by introducing more smoothing constants and output control (See double/triple exponential smoothing - alpha-beta filter) .

The moving average i propose will use only one smoothing constant, and is described as follow :

a = nz(a ) + alpha*nz(A )

b = nz(b ) + alpha*nz(B )

y = ema(a + b,p1)

A = src - y

B = src - ema(y,p2)

The filter is divided into two components a and b (more terms can add more control/effects if chosen well) , a adjust itself to the output error and is responsive while b is independent of the output and is mainly smoother, adding those components together create an output y , A is the output error and B is the error of an exponential moving average.

Comparison

There are a lot of low-lag filters out there, but the overshoots they induce in order to reduce lag is not a great effect. The first comparison is with a least square moving average, a moving average who fit a line in a price window of period length .

Lsma in blue and WRMA in red with both length = 100 . The lsma is a bit smoother but induce terrible overshoots

ZLMA in blue and WRMA in red with both length = 100 . The lag difference between each moving average is really low while VWRMA is way more precise.

Hull MA in blue and WRMA in red with both length = 100 . The Hull MA have similar overshoots than the LSMA.

Reduced overshoots moving average (ROMA) in blue and WRMA in red with both length = 100 . ROMA is an indicator i have made to reduce the overshoots of a LSMA, but at the end WRMA still reduce way more the overshoots while being smoother and having similar lag.

I have added a smoother version, just activate the extra smooth option in the indicator settings window. Here the result with length = 200 :

This result is a little bit similar to a 2 order Butterworth filter. Our filter have more overshoots which in this case could be useful to reduce the error with edges since other low pass filters tend to smooth their amplitude thus reducing edge estimation precision.

Conclusions

I have presented a well rounded filter in term of smoothness/stability and reactivity. Try to add more terms to have different results, you could maybe end up with interesting results, if its the case share them with the community :)

As for control theory i have seen neural networks integrated to Kalman flters which leaded to great accuracy, AI is everywhere and promise to be a game a changer in real time data smoothing. So i asked myself if it was possible for a neural networks to develop pinescript indicators, if yes then i could be replaced by AI ? Brrr how frightening.

Thanks for reading :)

Quadruple Kaufman Adaptive Moving AverageFour Kaufman Adaptive Moving Averages in one script. Useful for identifying trends and setting points to add to positions / exit trades. KAMA's are great for keeping you in trending markets and avoiding sideways chops and ranges. Try them out by tweaking the fast/slow ma's and lengths to get the right set for your charts that removes the thinking about whether to be long or short and when to add to positions.

A suggested trading strategy is to tweak the ma's (often you'll want larger values) until they span the price action well on past trends. Then each time price action closes and crosses one of your KAMA lines is an opportunity to add to your position. Once all lines are cleared and you've loaded up your position, hopefully your average price of entry falls short of the highest KAMA line's value. Once this happens you don't need to get out the trade until such time as a price close crosses again that largest KAMA line. For eager profit takers, close positions once any KAMA line is crossed once you're successfully loaded up on a direction.

I use this script with a renko chart and values -> 26 length 6 fast ma 100 slow ma, 26 8 100, 26 10 100, 26 12 100 and it's good to see these moving averages, unlike regular moving averages, bend around choppy action that come when trends pause, keeping me successfully in winning trades. Give it a try.