Macro & Earnings Dashboard — NY Fed CalendarMacro & Earnings Dashboard — NY Fed Calendar

This is an overlay indicator designed to provide a quick, real-time overview of the most critical upcoming US economic data releases and corporate earnings reports directly on your TradingView chart. It functions as a dynamic dashboard, removing the need to constantly check external calendars.

Key Features

1. Real-Time Economic Calendar (Bottom-Right Table)

The dashboard tracks the time remaining until the next release of five major, high-impact economic indicators. The data for these dates is pre-loaded directly from the New York Fed Economic Indicators Calendar (currently loaded for October through December 2025).

The tracked events include:

CPI (Consumer Price Index)

PPI (Producer Price Index)

Employment Situation (Non-Farm Payrolls / Unemployment Rate)

Interest Rate Decision (FOMC Meetings)

Consumer Sentiment (University of Michigan Survey)

2. Corporate Earnings Tracker (Top-Right Table)

This table uses TradingView's built-in data to calculate the estimated days remaining until the next Earnings Per Share (EPS) report for a curated list of high-profile NASDAQ tickers:

AAPL, NVDA, GOOG, TSLA, MSFT, AMZN, META

3. Color-Coded Urgency

The "Days" column for both macro and earnings tables uses a traffic light system to instantly communicate how soon the event is:

Red: The event is scheduled for Today or Tomorrow (0–1 day away).

Orange: The event is scheduled for the current week (within 6 days).

Teal: The event is more than a week away.

Gray: The date is currently unavailable or outside the loaded calendar range.

Pesquisar nos scripts por "汇洲智能+股票分析+2025年6月5日"

Anchored VWAP (Triple) MYRAXESAnchored VWAP Triple Indicator

The Anchored VWAP Triple indicator is a powerful tool for technical analysis, allowing traders to plot three customizable anchored Volume Weighted Average Price (VWAP) lines on a chart. Unlike traditional VWAP, which resets daily, this indicator lets you anchor each VWAP to a specific date and time, providing a unique perspective on price action relative to key market events.

Features

Three Independent VWAPs: Plot up to three VWAP lines, each anchored to a user-defined date and time.

Customizable Inputs: Set the year, month, day, hour, and minute for each VWAP anchor point. Choose distinct colors for easy identification.

Pure Anchored Design: VWAP lines start only from the anchor point, with no pre-anchor extensions, ensuring a clean and focused analysis.

Debug Mode: Optional display of hour and minute for troubleshooting or educational purposes.

Default Settings: Pre-configured with practical defaults (e.g., September 2025 dates) for immediate use.

How to Use

Add the indicator to your TradingView chart.

Adjust the anchor dates and times for each VWAP (VWAP 1, VWAP 2, VWAP 3) via the input settings.

Select custom colors for each VWAP line to differentiate them on the chart.

Enable Debug Mode if needed to verify time alignment.

Analyze price movements relative to the anchored VWAPs to identify support, resistance, or trend shifts.

Benefits

Ideal for swing traders and long-term analysts who need to anchor VWAP to significant price levels or events.

Enhances decision-making by comparing multiple VWAPs from different anchor points.

Fully compatible with TradingView’s Pine Script v6 for smooth performance.

This indicator is perfect for traders looking to deepen their market analysis with a flexible, multi-VWAP approach. Share your feedback or custom setups in the comments!

CB Charts - GEX MESZ2025/ESZ2025Last Updated: 09/22/2025 6:41 a.m. PST

*DISCLAIMER: Only intended for ESZ2025/MESZ2025 charts.

This indicator plots horizontal levels based on batched GEX levels for ESZ2025/MESZ2025. The batched data is derived from contracts expiring: 0DTE, 1DTE, EoW, EoM, Next Week, Next Month and 3-months out. Labels are available for a high-level view of which levels are which. Hovering (or long-pressing on mobile TV) over the labels will display the nominal values and Rank. This script is manually updated and may not be always updated.

When and what to use:

- Most respected levels come from 1DTE, EoW and EoM.

- 0DTE is included for when this script becomes intraday updated. (CURRENTLY NOT UPDATED INTRADAY)

- Next Week setting is best used only for Friday and Sunday trading

- Next Month setting is best for weeks close to the end of the current month

Powered by the Camels of Wallstreet

Japan Yen Carry Trade to Risk Ratio Sharpe Ratio By UncleBFMStep-by-Step Calculation in the ScriptFetch Rates:Pulls rates dynamically using request.security() from user-specified symbols (e.g., TVC:JP10Y for yen, TVC:US10Y for target). If unavailable (NA), uses fallback inputs (e.g., 0.25% for yen, 4.50% for target).

Converts rates to decimals: (target_rate - yen_rate) / 100.

Calculate Carry:Carry = (Target Rate - Yen Rate) / 100

Example: If US 10Y yield is 4.50% and Japan 10Y is 0.25%, carry = (4.50 - 0.25) / 100 = 0.0425 (4.25% annual yield).

Calculate Daily Log Returns:Log Returns = ln(Close / Close ), where Close is the current price of the pair (e.g., USDJPY) and Close is the previous day's price.

This measures daily percentage changes in a way suitable for volatility calculations.

Calculate Annualized Volatility:Volatility = Standard Deviation of Log Returns over a lookback period (default 63 days, ~3 months) × √252.

Example: If the standard deviation of USDJPY log returns is 0.005 (0.5% daily), annualized volatility = 0.005 × √252 ≈ 0.0794 (7.94%).

Compute the Ratio:Ratio = Carry / Volatility

Example: Using above, 0.0425 / 0.0794 ≈ 0.535.

If volatility is zero, the ratio is set to NA to avoid division errors.

Plot:Plots the ratio as a line, with optional thresholds (e.g., 0.2 for "high attractiveness") to guide interpretation.

NotesDynamic Rates: Using bond yields (e.g., TVC:JP10Y) or policy rates (e.g., ECONOMICS:JPINTR) makes the indicator responsive to historical and current rate changes, unlike static inputs.

Context: BIS reports use similar ratios to assess carry trade viability. For USDJPY in 2025, with Fed rates around 4.5% and BoJ at 0.25–0.5%, the carry is positive but sensitive to volatility spikes (e.g., during 2024 unwind events).

Usage: Apply to a yen pair chart (e.g., USDJPY, AUDJPY). Adjust symbols for the target currency (e.g., TVC:AU10Y for AUD). The ratio helps compare carry trade profitability across pairs or over time.

Ighodalo Gold - CRT (Candles are ranges theory)This indicator is designed to automatically identify and display CRT (Candles are Ranges Theory) Candles on your chart. It draws the high and low of the identified range and extends them until price breaks out, providing clear levels of support and resistance.

The Candles are Ranges Theory (CRT) concept was originally developed and shared by a trader named Romeotpt (Raid). All credit for the trading methodology goes to him. This indicator simply makes spotting these specific candles easier.

What is a CRT Candle & How Is It Used?

A CRT candle is a single candle that has both the highest high AND the lowest low over a user-defined period. It is identified by analysing a block of recent candles and finding the one candle that contains the entire price range of that block.

Once a CRT candle is formed, its high and low act as an accumulation range.

A break above or below this range is the manipulation phase.

A reclaim of the range (price closing back inside) signifies a potential distribution phase.

On higher timeframes, this sequence can be interpreted as:

Candle 1: Accumulation

Candle 2: Manipulation

Candle 3: Distribution

Reversal (Turtle Soup):

A sweep of the high or low, followed by a quick reclaim (price closing back inside the range), can signify a reversal. According to the theory’s originator, Romeo, this reversal pattern is called “turtle soup.”

After a bearish reversal at the high, the target becomes the CRT low.

After a bullish reversal at the low, the target becomes the CRT high.

How to Use This Indicator

The indicator is flexible and can be adapted to your trading style. The most important settings are:

Max Lookback Period: Number of past candles ("n") the indicator checks within to find a CRT.

CRT Timeframe:

Select a timeframe (e.g., 1H): The indicator will look at the higher timeframe you selected and plot the most recent CRT range from that timeframe onto your current chart. This is useful for multi-timeframe analysis.

Enable Overlapping CRTs:

False (unchecked): Shows only one active CRT range at a time. The indicator won’t look for a new one until the current range is broken.

True (checked): Constantly searches for and displays all CRT ranges it finds, allowing multiple ranges to appear on the chart simultaneously.

Disclaimer & Notes

-This is a visualisation tool and not a standalone trading signal. Always use it alongside your own analysis and risk management strategy.

-All credit for the "Candles are Ranges Theory" (CRT) concept goes to its creator, Romeotpt (Raid).

"On the journey to the opposite side of the range, price often provides multiple turtle soup entry opportunities. Follow their footprints." — Raid, 2025

Relative Strength Comparison-NewShRelative Strength Comparison Script created by Shahbaz on 19th Sep 2025

MEMEC - Meme Coin Market Cap [Da_Prof]For this indicator, the meme coin market cap of the top meme coins are added together to get an estimate of the total meme coin market cap back to the first meme coin, DOGE. Meme.C does this natively on TradingView, but its data only goes back to 19 May 2025. For the indicator, MEME.C supersedes the addition of all the individual meme coins (i.e., from 19 May 2025 to present). The start of MEME.C is labeled on the chart by default, but can be removed by deselecting the label in the settings.

After the creation of DOGE, but before data is available for Meme.C, the highest market cap meme coins are added together to estimate the meme coin market cap. The meme coins used by default are DOGE, SHIB, PEPE, BONK, FLOKI, PENGU, TRUMP, SPX6900, FARTCOIN, WIF, M, BRETT, B, MOG, APE, TURBO, DOG, and POPCAT. Users can select if they wish to disregard any or all of these coins. As of the creation of the indicator, DOGE, SHIB, and PEPE have CRYPTOCAP symbols on TradingView. Therefore, the true market cap of these coins is integrated into this indicator. The other meme coin market caps are estimated using price and the circulating supply as of 09/16/2025. I make no claims as to the indicator's exact accuracy. In fact, it isn't exactly accurate since I utilized the circulating supply on the day it was created, so for meme coins that have a changing supply, the market cap will be at least slightly inaccurate. Use this indicator at your own risk.

To use the indicator, it is best to plot overlayed on the CRYPTOCAP:DOGE chart. You can decide whether or not to hide the DOGE market cap.

Heikin FlowHeikin Flow

by Ben Deharde, 2025

Overview

Heikin Flow is a trend and momentum oscillator built on a smoothed reverse-Heikin-Ashi baseline. It quantifies the distance between price and this baseline, then colors the histogram to reflect both direction and acceleration/deceleration. Use it standalone to read trend energy and shifts, or pair it with Heikin Rider for momentum-aware breakout confirmation.

What It Does

Computes a reverse-HA baseline and optionally smooths it with a selectable MA.

Plots a histogram of distance (price minus baseline) to visualize directional pressure.

Colors the histogram by trend state (above/below baseline) and momentum (accelerating vs. decelerating).

Provides alerts on zero-line crosses to spotlight potential momentum regime changes.

The histogram also helps to spot divergence between price and momentum (e.g., price making new highs while the histogram weakens).

How It Works

Reverse-HA Baseline

Heikin Flow derives a “reverse close” value from Heikin Ashi context (using prior HA open/close with current bar range) to capture underlying pressure. This value is range-bounded to avoid extremes, then optionally smoothed. The resulting line acts as a soft directional baseline.

Smoothing (Noise Control)

Choose SMA/EMA/HMA/VWMA/RMA and a length to control baseline responsiveness. Shorter lengths react faster, longer lengths emphasize trend consistency by filtering noise—useful when pairing with breakout tools like Rider.

Trend & Momentum Logic

Trend: If price is above the baseline, the environment is considered uptrend; below indicates downtrend.

Momentum: The change in distance bar-to-bar distinguishes acceleration (growing distance) from deceleration (shrinking distance).

This dual readout helps you see not just direction, but the quality of that direction—strong push vs. weakening move.

Coloring (Aligned with Heikin Rider Palette)

Deep Blue: Uptrend & accelerating

Light Blue: Uptrend & decelerating

Deep Red: Downtrend & accelerating

Soft Orange: Downtrend & decelerating

This mirrors the palette logic from Heikin Rider for immediate visual consistency across the suite.

How to use

Read the histogram above/below zero (price–baseline) as directional bias; watch color changes for momentum context.

Use zero-line crosses as momentum regime shifts; confirm with price action or Heikin Rider breakout signals.

Watch for divergence between price action and the histogram as an early clue of weakening moves.

Adjust smoothing method/length to fit your market and timeframe—faster for scalping, slower to highlight sustained trends.

Inputs

Smoothing Type & Length for the baseline (SMA/EMA/HMA/VWMA/RMA)

Info Box toggles (display and formatting)

Live Mode option for real-time vs. confirmed-bar behavior (avoids inadvertent lookahead)

Originality

Heikin Flow adapts the HA-driven methodology to an oscillator that focuses on distance-to-baseline and momentum quality, using a reverse-HA construction and flexible MA smoothing—complementing Heikin Rider’s smoothed HA envelope breakout design for a cohesive, momentum-aware workflow.

Alerts

Bullish Heikin Flow Cross — distance crosses above 0 (on bar close)

Bearish Heikin Flow Cross — distance crosses below 0 (on bar close)

Iani SMC Sniper XAU v2.2 (Long+Short + News Countdown, v6)Iani SMC Sniper v2.6 — Anytime • Auto Pip • FVG 50% • OB • News Panel

Smart-Money Concepts made simple for intraday XAU/USD (works on any symbol).

Finds BOS, 50% FVG “sniper” entries, optional Order Blocks, London H/L, news countdown, and a mini info panel.

What it does

BOS (Break of Structure): detects bullish/bearish BOS after London sweep logic.

FVG 50% entries: plots precise long/short entry dots at the midpoint of the gap.

Auto TP/SL: TP = RR × risk, SL below/above recent swing with a small buffer.

Order Blocks (optional): marks the last opposite candle after BOS and alerts on OB revisit.

London High/Low: tracks session range; session filter is optional.

News countdown: shows next event time and minutes left (user-selectable timezone).

Mini Panel: top-left table with Trend (last BOS), Next news, R:R, Pip size.

Inputs (key)

Auto pip size: uses syminfo.mintick. Manual override available.

Risk:Reward (RR): default 2.0.

Pivot length: swing sensitivity.

Sessions: enable if you want signals only 12:00–20:00 (symbol timezone). Off = anytime.

News timezone: pick your own (e.g., Europe/Brussels, America/New_York).

Absolute & daily times: add your events (strings like 2025-09-17 20:00 or 14:30,16:00…).

Show labels/levels/OBs: toggle on/off.

Alerts included

BOS Bullish / BOS Bearish

BUY Entry / SELL Entry (return to 50% FVG)

Bullish OB revisit / Bearish OB revisit

TP Long/Short reached, SL Long/Short hit

NEWS WARNING (warning window only; does not block signals)

To use: Add Alert → Condition: this indicator → choose any of the alertconditions.

Best use

Bias: H1 for structure.

Execution: M15 (standard) or M5 (aggressive).

Works great on XAUUSD, but is symbol-agnostic (auto pip adapts).

Notes

News times display in the timezone you pick in settings.

OBs are a simple implementation meant for quick visual guidance.

Labels: BUY/SELL near entries, TP/SL on set and when hit, BOS up/down.

Risk disclaimer

This tool is for education only. Not financial advice. Backtest and manage risk.

Reference timesThe theory behind this indicator is that sometimes the graph reaches a certain price at at a certain time according to the price it had at the same time and day in any of the previous weeks. If you could easily see what happened a few weeks ago on this day's weekday and half an hour from now, you might theoretically gain more assurance as to where the graph might go in the next half an hour.

This of course relies of the premise that some traders choose to enter or exit positions according to historical times they are referencing. Hence the name - Reference times.

Example:

it is now 08:00 ET Wednesday. I want to guess what the graph will do in the next half hour. I enter in the indicator the weekday "Wednesday", the time "8:30", and go to 30 minute candles.

I will then see all the candles the graph has been on historical Wednesdays at 8:30. If the candles are below the 08:00 price, we might guess that the graph might want to descent. If they are above the graph, we might guess that the graph might ascend.

How it works:

The user defines a weekday and time he wants to inquire on.

The script searches for past weekdays and similar hours.

It marks these bars at their wicks.

The user can also inquire "opposite hours" - 12 hours ahead or earlier.

The user can also inquire "opposite days" - Monday<->Wednesday, Tuesday<->Thursday.

In addition, the User may inquire the previous day of his selected weekday, which will mark the most recent previous day existent.

Side note: The Time zone offset is set for Jerusalem time. and so it may need future adjustment.

send debugging instances if you find any

Thank you

Assaf Fogelman 2025

Reference TimesThe theory behind this indicator is that sometime the graph will change its direction at a point that is the point it reached at that weekday on that time in the previous weeks. If you can easily see what happened a few weeks ago on this day's weekday and a half an hour from now, you might theoretically gain more assurance as to where the graph might go in the next half an hour.

This of course relies of the premise that some traders choose to enter or exit positions according to historical times they are referencing. Hence the name - Reference times.

Example:

it is now 08:00 ET Wednesday. I want to guess what the graph will do in half an hour. I enter in the indicator the weekday "Wednesday", the time "8:30", and go to 30 minute candles.

I will then see all the candles the graph has been on historical Wednesdays at 8:30. If the candles are below the 08:00 price, we might guess that the graph might want to descent. If they are above the graph, we would guess the graph might want to ascend.

How it works:

The user defines a weekday and time he wants to inquire on.

The script searches for past weekdays and similar hours.

It marks these bars at their wicks.

The user can also inquire "opposite hours" - 12 hours ahead or earlier.

The user can also inquire "opposite days" - Monday<->Wednesday, Tuesday<->Thursday.

In addition, the User may inquire the previous day of his selected weekday, which will mark the most recent previous day existent.

Side note: The Time zone offset is set for Jerusalem time. and so it may need future adjustment.

send debugging instances if you find any

Thank you

Assaf Fogelman 2025

High and Low - MS - 2.0"Showing the high and low points with numbers.

Micha the leftist didn’t say how it’s called in his video.

#LeftismIsAMentalIllness"

נותן לראות את הנקודות הגבוהות והנמוכות עם מספרים

מיכה השמאלן לא אמר איך קוראים לזה בסרטון שלו

#שמאלנותזומחלתנפש

14/09/2025

FOMC Fund Rate 2022–2025(0.1)This indicator visualizes the Federal Open Market Committee (FOMC) meetings from 2022 through 2025.

It plots vertical lines on the announcement dates and attaches labels showing:

The decision (rate hike ⭡, cut ⭣, or hold ⭤).

The size of the rate change in percentage points.

The cumulative Federal Funds Rate path in parentheses.

Features:

Accurate timestamps for each FOMC meeting (UTC+1).

Customizable line style, width, and color.

Label color and text color options.

Placeholder labels for future meetings to maintain the timeline.

Use this script to keep track of historical Fed policy decisions and visualize the rate path over time directly on your chart.

ICT 00:00, 08:30, 09:30 & 13:30 Opens (NY) — Prior-Day HistoryICT 00:00, 08:30, 09:30 & 13:30 Opens (NY)

This is a derivative of ALPHAICTRADER’s open-source script, republished under the MPL-2.0 with clear attribution and documented changes. It plots four New-York–anchored intraday reference levels—0000, 0830, 0930, 1330—as short, right-padded stubs with clean side labels. Use these time anchors (ICT-style midnight + key US windows) to frame bias, volatility pockets, and intraday trade locations.

What’s original in this version (changes)

Right-padded stubs instead of chart-wide rays — each level ends N bars past the latest candle (configurable).

Side labels at the line tip — text-only labels (0000, 0830, 0930, 1330) that sit at the right end of each stub and update every bar.

Optional prior-day history — show Today only or Today + Prior Day; older lines/labels auto-pruned.

Per-anchor controls — Display, Style, Color, Width, and Show Label for each time.

What it plots (and why)

0000 (NY Midnight): daily session anchor for bias/liquidity context.

0830 (NY): macro data window (CPI/NFP/claims) where volatility often concentrates.

0930 (NY): US cash equity market open; opening-drive structure/acceptance tests.

1330 (NY): early-afternoon anchor for continuation vs. fade.

How it works (under the hood)

Session detection: time("1", session, "America/New_York"); first bar flagged via not na(ts) and na(ts ).

Anchor price: open of that first bar per session/day.

Rendering: lines drawn with xloc=bar_index from start bar to bar_index + Right Pad; x2 updates every bar (no extend.right).

Labels: placed at line.get_x2(line) + Label Pad, soft color variant; updated per bar to stay on the tip.

History: arrays keep either today only or today + yesterday and delete anything older immediately.

How to use

Add to any intraday chart (futures/FX/indices). Anchors are always NY-time; TradingView handles DST.

Inputs

00:00 / 08:30 / 09:30 / 13:30 (NY): Display, Line Style, Color, Width, Show Label

Right Edge: Right Pad (bars) · Label Pad (bars)

History: Show Prior Day (History) — off = today only; on = today + yesterday

Suggested pads: Right Pad 2–5 bars; Label Pad 0–2.

These are context anchors, not signals. Combine with your execution model (market structure, liquidity, FVG/OBs, etc.).

Attribution & License (MPL-2.0)

Original work: “ICT NEW YORK MIDNIGHT OPEN AND 8.30 AM OPEN” by ALPHAICTRADER (MPL-2.0).

This derivative: modifications listed above; source published and kept under MPL-2.0 per license terms.

If you distribute a modified version of this Pine file, you must keep MPL-2.0, retain the copyright/licensing header, publish your modified source, and document your changes.

Notes: Pine v5. Minimalist (no day dividers). Educational tool; not financial advice.

Copyright: © ALPHAICTRADER 2022 · © Funk 2025

License: MPL-2.0

DNSE VN301!, ADX Momentum StrategyDiscover the tailored Pine Script for trading VN30F1M Futures Contracts intraday.

This strategy applies the Statistical Method (IQR) to break down the components of the ADX, calculating the threshold of "normal" momentum fluctuations in price to identify potential breakouts for entry and exit signals. The script automatically closes all positions by 14:30 to avoid overnight holdings.

www.tradingview.com

Settings & Backtest Results:

- Chart: 30-minute timeframe

- Initial capital: VND 100 million

- Position size: 4 contracts per trade (includes trading fees, excludes tax)

- Backtest period: Sep-2021 to Sep-2025

- Return: over 270% (with 5 ticks slippage)

- Trades executed: 1,000+

- Win rate: ~40%

- Profit factor: 1.2

Default Script Settings:

Calculates the acceleration of changes in the +DI and -DI components of the ADX, using IQR to define "normal" momentum fluctuations (adjustable via Lookback period).

Calculates the difference between each bar’s Open and Close prices, using IQR to define "normal" gaps (adjustable via Lookback period).

Entry & Exit Conditions:

Entry Long: Change in +DI or -DI > Avg IQR Value AND Close Price > Previous Close

Exit Long: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI < Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price < Previous Close

Entry Short: Change in +DI or -DI > Avg IQR Value AND Close Price < Previous Close

Exit Short: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI > Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price > Previous Close

Disclaimers:

Trading futures contracts carries a high degree of risk, and price movements can be highly volatile. This script is intended as a reference tool only. It should be used by individuals who fully understand futures trading, have assessed their own risk tolerance, and are knowledgeable about the strategy’s logic.

All investment decisions are the sole responsibility of the user. DNSE bears no liability for any potential losses incurred from applying this strategy in real trading. Past performance does not guarantee future results. Please contact us directly if you have specific questions about this script.

عكفة الماكد المتقدمة - أبو فارس ©// 🔒 Advanced MACD Curve © 2025

// 💡 Idea & Creativity: Engineer Abu Elias

// 🛠️ Development & Implementation: Abu Fares

// 📜 All intellectual rights reserved - Copying, modifying, or redistributing is not permitted

// 🚫 Any attempt to tamper with this code or violate intellectual property rights is legally prohibited

// 📧 For inquiries and licensing: Please contact the developer, Abu Fares

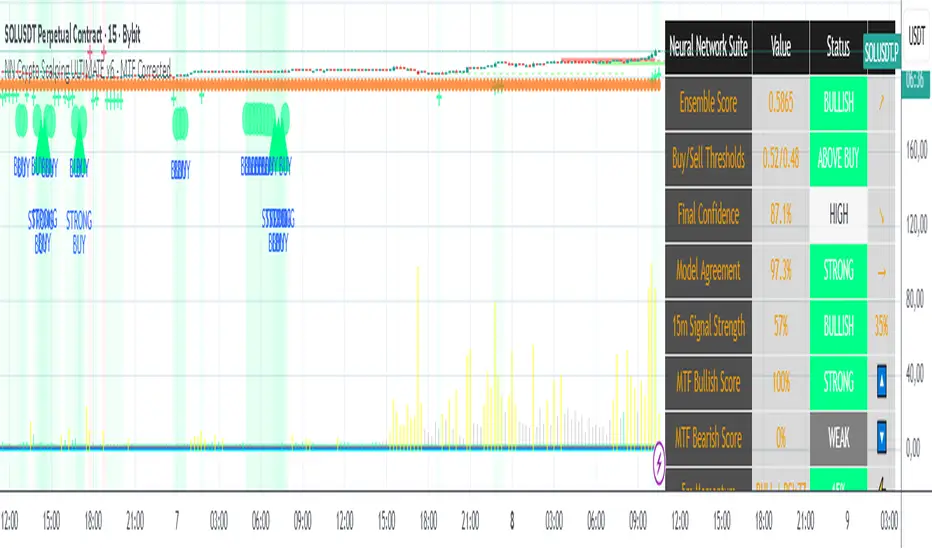

NN Crypto Scalping ULTIMATE v6 - MTF mapercivNeural Network Crypto Trading System v6.1

Complete Technical Documentation

Author

: Neural Network Ensemble Trading System

Version

: 6.1 - MTF Corrected & Bias Fixed

Date

: January 2025

Platform

: TradingView PineScript v6

Executive Summary

The

Neural Network Crypto Trading System v6.1

is an advanced algorithmic trading system that combines three specialized neural networks into an intelligent ensemble to generate cryptocurrency trading signals. The system integrates multi-timeframe analysis, crypto-specific optimizations, dynamic risk management, and continuous learning to maximize performance in highly volatile markets.

Key Features:

Ensemble of 3 specialized Neural Networks

(Primary, Momentum, Volatility)

Multi-Timeframe Analysis

with 5 timeframes (5m, 15m, 1h, 4h, 1D)

22 Advanced Features

for each model

Anti-repainting

guaranteed with confirmed data

8 Market Regime

automatic detections

6 Signal Levels

(Strong/Moderate/Weak Buy/Sell)

Professional dashboard

with 15+ real-time metrics

Intelligent alert system

with webhook integration

Fury by Tetrad on TESLA v2Fury by Tetrad — TSLA v2 (Free Version)

📊 Fury v2 on TSLA — Financial Snapshot

First trade: August 11, 2010

Last trade: September 5, 2025

Net Profit: $10,549.10 (≈ +10,549%)

Gross Profit: $10,554.36

Gross Loss: $5.26

Commission Paid: $86.95

⚖️ Risk/Return Ratios

Sharpe Ratio: 0.42

Sortino Ratio: 17.63

Profit Factor: 2005.38

🔄 Trade Statistics

Total Trades: 37

Winning Trades: 37

Losing Trades: 0

Win Rate: 100%

Fury is a momentum-reversion hybrid designed for Tesla (TSLA) on higher-liquidity timeframes. It combines Bollinger Bands (signal extremes) with RSI (exhaustion filter) to time mean-reversion pops/drops, then exits via price multipliers or optional time-based stops. A Market Direction toggle (Market Neutral / Long Only / Short Only) lets you align with macro bias or risk constraints. Intrabar simulation is enabled for realistic stop/limit behavior, and labeled entries/exits improve visual auditability.

How it works

Entries:

• Long when price pierces lower band and RSI is below the long threshold.

• Short when price pierces upper band and RSI is above the short threshold.

Exits:

• Profit targets via entry×multiplier (independent for long/short).

• Optional price-based stop factors per side.

• Optional time stop (N days) to cap trade duration.

Controls:

• Market Direction switch (Neutral / Long Only / Short Only).

• Tunable BB length/multiplier, RSI length/thresholds, exit multipliers, stops.

Intended use

Swing or position trading TSLA; can be adapted to other high-beta equities with parameter retuning. Use on liquid timeframes and validate with robust out-of-sample testing.

Disclaimers

Backtests are approximations; past performance ≠ future results. Educational use only. Not financial advice.

Stay connected

Follow on TradingView for updates • Telegram: t.me • Website: tetradprotocol.com

Bitcoin Power Law with Cycle BandsBitcoin Power Law with Cycle Bands DescriptionUnlock the power of Bitcoin’s long-term trends with the Bitcoin Power Law with Cycle Bands script, exclusively available through Bitcoin Wealth Edge! This custom TradingView indicator, built for Pine Script v6, models Bitcoin’s price behavior using a 96% R² power law trendline, derived from days since its genesis (January 3, 2009). Designed to predict cycle tops and bottoms, it features:Power Law Trendline: A cyan line representing fair value (e.g., ~$111,000 as of September 2025), based on a logarithmic regression with adjustable coefficients (a = -17.02, b = 5.83).

Cycle Bands: Adjustable red (upper) and green (lower) bands, defaulting to 3.5x and -3.5x multipliers, aligning with historical peaks (e.g., $69K in 2021) and troughs (e.g., $16K in 2022).

Dynamic Labels: Real-time labels displaying fair value, upper limit ($180K), and lower limit ($40K), updated on the last bar for quick insights.

Follow @HodlerRanch

for updates!

FNGAdataDates_Part1FNGAdataDates_Part1 provides historical trading dates for a financial instrument (e.g., FNGA index or related asset) from May 23, 2025, to approximately mid-2021, covering 950 trading days. The dates are organized into 19 chunks (dates_0 to dates_18), each containing 50 timestamps representing trading days (excluding weekends and possibly holidays). This library is part one of a two-part set due to Pine Script token limits and must be used with FNGAdataDates_Part2 for the complete dataset (1,846 dates). It is designed to align with the FNGAopenPrices and FNGAclosePrices libraries for backtesting, technical analysis, or visualization in Pine Script.

Savitzky-Golay Hampel Filter | AlphaNattSavitzky-Golay Hampel Filter | AlphaNatt

A revolutionary indicator combining NASA's satellite data processing algorithms with robust statistical outlier detection to create the most scientifically advanced trend filter available on TradingView.

"This is the same mathematics that processes signals from the Hubble Space Telescope and analyzes data from the Large Hadron Collider - now applied to financial markets."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 SCIENTIFIC PEDIGREE

Savitzky-Golay Filter Applications:

NASA: Satellite telemetry and space probe data processing

CERN: Particle physics data analysis at the LHC

Pharmaceutical: Chromatography and spectroscopy analysis

Astronomy: Processing signals from radio telescopes

Medical: ECG and EEG signal processing

Hampel Filter Usage:

Aerospace: Cleaning sensor data from aircraft and spacecraft

Manufacturing: Quality control in precision engineering

Seismology: Earthquake detection and analysis

Robotics: Sensor fusion and noise reduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🧬 THE MATHEMATICS

1. Savitzky-Golay Filter

The SG filter performs local polynomial regression on data points:

Fits a polynomial of degree n to a sliding window of data

Evaluates the polynomial at the center point

Preserves higher moments (peaks, valleys) unlike moving averages

Maintains derivative information for true momentum analysis

Originally published in Analytical Chemistry (1964)

Mathematical Properties:

Optimal smoothing in the least-squares sense

Preserves statistical moments up to polynomial order

Exact derivative calculation without additional lag

Superior frequency response vs traditional filters

2. Hampel Filter

A robust outlier detector based on Median Absolute Deviation (MAD):

Identifies outliers using robust statistics

Replaces spurious values with polynomial-fitted estimates

Resistant to up to 50% contaminated data

MAD is 1.4826 times more robust than standard deviation

Outlier Detection Formula:

|x - median| > k × 1.4826 × MAD

Where k is the threshold parameter (typically 3 for 99.7% confidence)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 WHY THIS IS SUPERIOR

vs Moving Averages:

Preserves peaks and valleys (critical for catching tops/bottoms)

No lag penalty for smoothness

Maintains derivative information

Polynomial fitting > simple averaging

vs Other Filters:

Outlier immunity (Hampel component)

Scientifically optimal smoothing

Preserves higher-order features

Used in billion-dollar research projects

Unique Advantages:

Feature Preservation: Maintains market structure while smoothing

Spike Immunity: Ignores false breakouts and stop hunts

Derivative Accuracy: True momentum without additional indicators

Scientific Validation: 60+ years of academic research

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

1. Polynomial Order (2-5)

2 (Quadratic): Maximum smoothing, gentle curves

3 (Cubic): Balanced smoothing and responsiveness (recommended)

4-5 (Higher): More responsive, preserves more features

2. Window Size (7-51)

Must be odd number

Larger = smoother but more lag

Formula: 2×(desired smoothing period) + 1

Default 21 = analyzes 10 bars each side

3. Hampel Threshold (1.0-5.0)

1.0: Aggressive outlier removal (68% confidence)

2.0: Moderate outlier removal (95% confidence)

3.0: Conservative outlier removal (99.7% confidence) (default)

4.0+: Only extreme outliers removed

4. Final Smoothing (1-7)

Additional WMA smoothing after filtering

1 = No additional smoothing

3-5 = Recommended for most timeframes

7 = Ultra-smooth for position trading

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Signal Recognition:

Cyan Line: Bullish trend with positive derivative

Pink Line: Bearish trend with negative derivative

Color Change: Trend reversal with polynomial confirmation

1. Trend Following Strategy

Enter when price crosses above cyan filter

Exit when filter turns pink

Use filter as dynamic stop loss

Best in trending markets

2. Mean Reversion Strategy

Enter long when price touches filter from below in uptrend

Enter short when price touches filter from above in downtrend

Exit at opposite band or filter color change

Excellent for range-bound markets

3. Derivative Strategy (Advanced)

The SG filter preserves derivative information

Acceleration = second derivative > 0

Enter on positive first derivative + positive acceleration

Exit on negative second derivative (momentum slowing)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Strengths:

Outlier Immunity: Ignores stop hunts and flash crashes

Feature Preservation: Catches tops/bottoms better than MAs

Smooth Output: Reduces whipsaws significantly

Scientific Basis: Not curve-fitted or optimized to markets

Considerations:

Slight lag in extreme volatility (all filters have this)

Requires odd window sizes (mathematical requirement)

More complex than simple moving averages

Best with liquid instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 SCIENTIFIC BACKGROUND

Savitzky-Golay Publication:

"Smoothing and Differentiation of Data by Simplified Least Squares Procedures"

- Abraham Savitzky & Marcel Golay

- Analytical Chemistry, Vol. 36, No. 8, 1964

Hampel Filter Origin:

"Robust Statistics: The Approach Based on Influence Functions"

- Frank Hampel et al., 1986

- Princeton University Press

These techniques have been validated in thousands of scientific papers and are standard tools in:

NASA's Jet Propulsion Laboratory

European Space Agency

CERN (Large Hadron Collider)

MIT Lincoln Laboratory

Max Planck Institutes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 ADVANCED TIPS

News Trading: Lower Hampel threshold before major events to catch spikes

Scalping: Use Order=2 for maximum smoothness, Window=11 for responsiveness

Position Trading: Increase Window to 31+ for long-term trends

Combine with Volume: Strong trends need volume confirmation

Multiple Timeframes: Use daily for trend, hourly for entry

Watch the Derivative: Filter color changes when first derivative changes sign

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTICES

Not financial advice - educational purposes only

Past performance does not guarantee future results

Always use proper risk management

Test settings on your specific instrument and timeframe

No indicator is perfect - part of complete trading system

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The Savitzky-Golay Hampel Filter represents the pinnacle of scientific signal processing applied to financial markets. By combining polynomial regression with robust outlier detection, traders gain access to the same mathematical tools that:

Guide spacecraft to other planets

Detect gravitational waves from black holes

Analyze particle collisions at near light-speed

Process signals from deep space

This isn't just another indicator - it's rocket science for trading .

"When NASA needs to separate signal from noise in billion-dollar missions, they use these exact algorithms. Now you can too."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt

Version: 1.0

Release: 2025

Pine Script: v6

"Where Space Technology Meets Market Analysis"

Not financial advice. Always DYOR

Laguerre-Kalman Adaptive Filter | AlphaNattLaguerre-Kalman Adaptive Filter |AlphaNatt

A sophisticated trend-following indicator that combines Laguerre polynomial filtering with Kalman optimal estimation to create an ultra-smooth, low-lag trend line with exceptional noise reduction capabilities.

"The perfect trend line adapts to market conditions while filtering out noise - this indicator achieves both through advanced mathematical techniques rarely seen in retail trading."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 KEY FEATURES

Dual-Filter Architecture: Combines two powerful filtering methods for superior performance

Adaptive Volatility Adjustment: Automatically adapts to market conditions

Minimal Lag: Laguerre polynomials provide faster response than traditional moving averages

Optimal Noise Reduction: Kalman filtering removes market noise while preserving trend

Clean Visual Design: Color-coded trend visualization (cyan/pink)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 THE MATHEMATICS

1. Laguerre Filter Component

The Laguerre filter uses a cascade of four all-pass filters with a single gamma parameter:

4th order IIR (Infinite Impulse Response) filter

Single parameter (gamma) controls all filter characteristics

Provides smoother output than EMA with similar lag

Based on Laguerre polynomials from quantum mechanics

2. Kalman Filter Component

Implements a simplified Kalman filter for optimal estimation:

Prediction-correction algorithm from aerospace engineering

Dynamically adjusts based on estimation error

Provides mathematically optimal estimate of true price trend

Reduces noise while maintaining responsiveness

3. Adaptive Mechanism

Monitors market volatility in real-time

Adjusts filter parameters based on current conditions

More responsive in trending markets

More stable in ranging markets

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ INDICATOR SETTINGS

Laguerre Gamma (0.1-0.99): Controls filter smoothness. Higher = smoother but more lag

Adaptive Period (5-100): Lookback for volatility calculation

Kalman Noise Reduction (0.1-2.0): Higher = more noise filtering

Trend Threshold (0.0001-0.01): Minimum change to register trend shift

Recommended Settings:

Scalping: Gamma: 0.6, Period: 10, Noise: 0.3

Day Trading: Gamma: 0.8, Period: 20, Noise: 0.5 (default)

Swing Trading: Gamma: 0.9, Period: 30, Noise: 0.8

Position Trading: Gamma: 0.95, Period: 50, Noise: 1.2

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 TRADING SIGNALS

Primary Signals:

Cyan Line: Bullish trend - price above filter and filter ascending

Pink Line: Bearish trend - price below filter or filter descending

Color Change: Potential trend reversal point

Entry Strategies:

Trend Continuation: Enter on pullback to filter line in trending market

Trend Reversal: Enter on color change with volume confirmation

Breakout: Enter when price crosses filter with momentum

Exit Strategies:

Exit long when line turns from cyan to pink

Exit short when line turns from pink to cyan

Use filter as trailing stop in strong trends

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✨ ADVANTAGES OVER TRADITIONAL INDICATORS

Vs. Moving Averages:

Significantly less lag while maintaining smoothness

Adaptive to market conditions

Better noise filtering

Vs. Standard Filters:

Dual-filter approach provides optimal estimation

Mathematical foundation from signal processing

Self-adjusting parameters

Vs. Other Trend Indicators:

Cleaner signals with fewer whipsaws

Works across all timeframes

No repainting or lookahead bias

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎓 MATHEMATICAL BACKGROUND

The Laguerre filter was developed by John Ehlers, applying Laguerre polynomials (used in quantum mechanics) to financial markets. These polynomials provide an elegant solution to the lag-smoothness tradeoff that plagues traditional moving averages.

The Kalman filter, developed by Rudolf Kalman in 1960, is used in everything from GPS systems to spacecraft navigation. It provides the mathematically optimal estimate of a system's state given noisy measurements.

By combining these two approaches, this indicator achieves what neither can alone: a smooth, responsive trend line that adapts to market conditions while filtering out noise.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 TIPS FOR BEST RESULTS

Confirm with Volume: Strong trends should have increasing volume

Multiple Timeframes: Use higher timeframe for trend, lower for entry

Combine with Momentum: RSI or MACD can confirm filter signals

Market Conditions: Adjust noise parameter based on market volatility

Backtesting: Always test settings on your specific instrument

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTES

No indicator is perfect - always use proper risk management

Best suited for trending markets

May produce false signals in choppy/ranging conditions

Not financial advice - for educational purposes only

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 CONCLUSION

The Laguerre-Kalman Adaptive Filter represents a significant advancement in technical analysis, bringing institutional-grade mathematical techniques to retail traders. Its unique combination of polynomial filtering and optimal estimation provides a clean, reliable trend-following tool that adapts to changing market conditions.

Whether you're scalping on the 1-minute chart or position trading on the daily, this indicator provides clear, actionable signals with minimal false positives.

"In the world of technical analysis, the edge comes from using better mathematics. This indicator delivers that edge."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Professional Quantitative Trading Tools

Version: 1.0

Last Updated: 2025

Pine Script: v6

License: Open Source

Not financial advice. Always DYOR

US Elections Democrate-Republicain (1920-2025)This script shows the different U.S. presidents and indicates whether each was Democratic or Republican. It allows users to analyze the market based on the president in office.