Alpha ADX DI+/DI- V5 by MUNIF SHAIKHMODIFIED ADX DI+/DI- V5

Usage: To use this indicator for entry: when DMI+ crosses over DMI-, there is a bullish sentiment, however ADX also needs to be above 25 to be significant, otherwise the move is not necessarily sustainable.

Inversely, when DMI+ crosses under DMI- and ADX is above 25, then the sentiment is significantly bearish , but if ADX is below 20, the signal should be disregarded.

The line control represents, if the ADX is greater than the line of 25, the price trend is considered strong

Pesquisar nos scripts por "汇丰股票25"

Rob Booker - ADX Breakout updated to pinescript V5Rob Booker - ADX Breakout. The strategy remains unchanged but the code has been updated to pinescript V5. This enables compatibility with all new Tradingview features. Additonally, indicators have been made more easily visible, default cash settings as well as input descriptions have been added.

Rob Booker - ADX Breakout: (Directly taken from the official Tradingview V1 version of the script)

Definition

Rob Booker’s Average Directional Index (ADX) Breakout is a trend strength indicator that affirms the belief that trading in the direction of a trend and continuing to follow its pull is more profitable for traders, while simultaneously reducing risk.

History

ADX was traditionally used and developed to determine a price’s trend strength. It is commonly known as a tool from the arsenal of Rob Booker, experienced entrepreneur and currency trader.

Calculations

Calculations for the ADX Breakout indicator are based on a moving average of price range expansion over a specific period of time. By default, the setting rests at 14 bars, this however is not mandatory, as other periods are routinely used for analysis as well.

Takeaways

The ADX line is used to measure and determine the strength of a trend, and so the direction of this line and its interpretation are crucial in a trader’s analysis. As the ADX line rises, a trend increases in strength and price moves in the trend’s direction. Similarly, if the ADX line is falling, a trend decreases in strength and price then enters a period of consolidation, or retracement.

Traditionally, the ADX is plotted on the chart as a single line that consists of values that range from 0-100. The line is non-directional, meaning that it always measures trend strength regardless of the position of a price’s trend (up or down). Essentially, ADX quantifies trend strength by presenting in both uptrends and downtrends of the line.

What to look for

The values associated with the ADX line help traders determine the most profitable trades and where risk lies in the current trend. It is important to know how to quantify trend strength and distinguish between the varying values in order to understand the differences in trending vs. non-trending conditions. Let’s take a look at ADX values and what they mean for trend strength.

ADX Value:

0-25: Signifies an absent of weak trend

25-50: Signifies a strong trend

50-75: Signifies a very strong trend

75-100: Signifies an extremely strong trend

To delve into this a bit further, let’s assess the meaning of ADX if it is valued below 25. If the ADX line remains below 25 for more than 30 or so bars, price then enters range conditions, making price patterns more distinguishable and visible to traders. Price will move up and down between resistance and support in order to determine selling and buying interest and may then eventually break out into a trend or pattern.

The way in which ADX peaks, ebs, and flows is also a signifier of its overall pattern and trend momentum. The line can clearly indicate to the trader when trend strength is strong versus when it is weak. When ADX peaks are pictured as higher, it points towards an increase in trend momentum. If ADX peaks are pictured as lower - you guessed it - it points towards a decrease in trend momentum. A trend of lower ADX peaks could be a warning for traders to watch prices and manage and assess risk before a trade gets out of hand. Similarly, whenever there is a sudden move that seems out of place or a change in trend character that goes against what you’ve seen before, this should be a clear sign to watch prices and assess risk.

Summary

The ADX Breakout indicator is a trend strength indicator that analyzes price movements relative to trend strength to signal a user when is best for a trade and when is best to manage risk and assess patterns. As long as a trader recognizes strong trends and assesses the risk of each trade properly, they should have no problem using this indicator and utilizing it to work in their favor. In addition, the ADX helps identify trending conditions, but while doing so, also aids traders in finding strong trends to trade. The indicator can even alert traders to specific changes in trend momentum, allowing them to be primed for risk management.

Price Displacement - Candlestick (OHLC) CalculationsA Magical little helper friend for Candle Math.

When composing scripts, it is often necessary to manipulate the math around the OHLC. At times, you want a scalar (absolute) value others you want a vector (+/-). Sometimes you want the open - close and sometimes you want just the positive number of the body size. You might want it in ticks or you might want it in points or you might want in percentages. And every time you try to put it together you waste precious time and brain power trying to think about how to properly structure what you're looking for. Not to mention it's normally not that aesthetically pleasing to look at in the code.

So, this fixes all of that.

Using this library. A function like 'pd.pt(_exp)' can call any kind of candlestick math you need. The function returns the candlestick math you define using particular expressions.

Candle Math Functions Include:

Points:

pt(_exp) Absolute Point Displacement. Point quantity of given size parameters according to _exp.

vpt(_exp) Vector Point Displacement. Point quantity of given size parameters according to _exp.

Ticks:

tick(_exp) Absolute Tick Displacement. Tick quantity of given size parameters according to _exp.

vtick(_exp) Vector Tick Displacement. Tick quantity of given size parameters according to _exp.

Percentages:

pct(_exp, _prec) Absolute Percent Displacement. (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

vpct(_exp, _prec) Vector Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Expressions You Can Use with Formulas:

The expressions are simple (simple strings that is) and I did my best to make them sensible, generally using just the ohlc abreviations. I also included uw, lw, bd, and rg for when you're just trying to pull a candle component out. That way you don't have to think about which of the ohlc you're trying to get just use pd.tick("uw") and now the variable is assigned the length of the upper wick, absolute value, in ticks. If you wanted the vector in pts its pd.vpt("uw"). It also makes changing things easy too as I write it out.

Expression List:

Combinations

"oh" = open - high

"ol" = open - low

"oc" = open - close

"ho" = high - open

"hl" = high - low

"hc" = high - close

"lo" = low - open

"lh" = low - high

"lc" = low - close

"co" = close - open

"ch" = close - high

"cl" = close - low

Candle Components

"uw" = Upper Wick

"bd" = Body

"lw" = Lower Wick

"rg" = Range

Pct() Only

"scp" = Scalar Close Position

"sop" = Scalar Open Position

"vcp" = Vector Close Position

"vop" = Vector Open Position

The attributes are going to be available in the pop up dialogue when you mouse over the function, so you don't really have to remember them. I tried to make that look as efficient as possible. You'll notice it follows the OHLC pattern. Thus, "oh" precedes "ho" (heyo) because "O" would be first in the OHLC. Its a way to help find the expression you're looking for quickly. Like looking through an alphabetized list for traders.

There is a copy/paste console friendly helper list in the script itself.

Additional Notes on the Pct() Only functions:

This is the original reason I started writing this. These concepts place a rating/value on the bar based on candle attributes in one number. These formulas put a open or close value in a percentile of the bar relative to another aspect of the bar.

Scalar - Non-directional. Absolute Value.

Scalar Position: The position of the price attribute relative to the scale of the bar range (high - low)

Example: high = 100. low = 0. close = 25.

(A) Measure price distance C-L. How high above the low did the candle close (e.g. close - low = 25)

(B) Divide by bar range (high - low). 25 / (100 - 0) = .25

Explaination: The candle closed at the 25th percentile of the bar range given the bar range low = 0 and bar range high = 100.

Formula: scp = (close - low) / (high - low)

Vector = Directional.

Vector Position: The position of the price attribute relative to the scale of the bar midpoint (Vector Position at hl2 = 0)

Example: high = 100. low = 0. close = 25.

(A) Measure Price distance C-L: How high above the low did the candle close (e.g. close - low = 25)

(B) Measure Price distance H-C: How far below the high did the candle close (e.g. high - close = 75)

(C) Take Difference: A - B = C = -50

(D) Divide by bar range (high - low). -50 / (100 - 0) = -0.50

Explaination: Candle close at the midpoint between hl2 and the low.

Formula: vcp = { / (high - low) }

Thank you for checking this out. I hope no one else has already done this (because it took half the day) and I hope you find value in it. Be well. Trade well.

Library "PD"

Price Displacement

pt(_exp) Absolute Point Displacement. Point quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Point size of given expression as an absolute value.

vpt(_exp) Vector Point Displacement. Point quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Point size of given expression as a vector.

tick(_exp) Absolute Tick Displacement. Tick quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Tick size of given expression as an absolute value.

vtick(_exp) Vector Tick Displacement. Tick quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Tick size of given expression as a vector.

pct(_exp, _prec) Absolute Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Parameters:

_exp : (string) Expression

_prec : (int) Overload - Place value precision definition

Returns: Percent size of given expression as decimal.

vpct(_exp, _prec) Vector Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Parameters:

_exp : (string) Expression

_prec : (int) Overload - Place value precision definition

Returns: Percent size of given expression as decimal.

Multi-Timeframe (MTF) Dashboard by RiTzMulti-Timeframe Dashboard

Shows values of different Indiactors on Multiple-Timeframes for the selected script/symbol

VWAP : if LTP is trading above VWAP then Bullish else if LTP is trading below VWAP then Bearish.

ST(21,1) : if LTP is trading above Supertrend (21,1) then Bullish , else if LTP is trading below Supertrend (21,1) then Bearish.

ST(14,2) : if LTP is trading above Supertrend (14,2) then Bullish , else if LTP is trading below Supertrend (14,2) then Bearish.

ST(10,3) : if LTP is trading above Supertrend (10,3) then Bullish , else if LTP is trading below Supertrend (10,3) then Bearish.

RSI(14) : Shows value of RSI (14) for the current timeframe.

ADX : if ADX is > 75 and DI+ > DI- then "Bullish ++".

if ADX is < 75 but >50 and DI+ > DI- then "Bullish +".

if ADX is < 50 but > 25 and DI+ > DI- then "Bullish".

if ADX is above 75 and DI- > DI+ then "Bearish ++".

if ADX is < 75 but > 50 and DI- > DI+ then "Bearish+".

if ADX is < 50 but > 25 and DI- > DI+ then "Bearish".

if ADX is < 25 then "Neutral".

MACD : if MACD line is above Signal Line then "Bullish", else if MACD line is below Signal Line then "Bearish".

PH-PL : "< PH > PL" means LTP is trading between Previous Timeframes High(PH) & Previous Timeframes Low(PL) which indicates Rangebound-ness.

"> PH" means LTP is trading above Previous Timeframes High(PH) which indicates Bullish-ness.

"< PL" means LTP is trading below Previous Timeframes Low(PL) which indicates Bearish-ness.

Alligator : If Lips > Teeth > Jaw then Bullish.

If Lips < Teeth < Jaw then Bearish.

If Lips > Teeth and Teeth < Jaw then Neutral/Sleeping.

If Lips < Teeth and Teeth > Jaw then Neutral/Sleeping.

Settings :

Style settings :-

Dashboard Location: Location of the dashboard on the chart

Dashboard Size: Size of the dashboard on the chart

Bullish Cell Color: Select the color of cell whose value is showing Bullish-ness.

Bearish Cell Color: Select the color of cell whose value is showing Bearish-ness.

Neutral Cell Color: Select the color of cell whose value is showing Rangebound-ness.

Cell Transparency: Select Transparency of cell.

Column Settings :-

You can select which Indicators values should be displayed/hidden.

Timeframe Settings :-

You can select which timeframes values should be displayed/hidden.

Note :- I'm not a pro Developer/Coder , so if there are any mistakes or any suggestions for improvements in the code then do let me know!

Note :- Use in Live market , might show wrong values for timeframes other than current timeframe in closed market!!

Nifty / Banknifty Dashboard by RiTzNifty / Banknifty Dashboard :

Shows Values of different Indicators on current Timeframe for the selected Index & it's main constituents according to weightage in index.

customized for Nifty & Banknifty (You can customize it according to your needs for the markets/indexes you trade in)

Interpretation :-

VWAP : if LTP is trading above VWAP then Bullish else if LTP is trading below VWAP then Bearish.

ST(21,1) : if LTP is trading above Supertrend (21,1) then Bullish , else if LTP is trading below Supertrend (21,1) then Bearish.

ST(14,2) : if LTP is trading above Supertrend (14,2) then Bullish , else if LTP is trading below Supertrend (14,2) then Bearish.

ST(10,3) : if LTP is trading above Supertrend (10,3) then Bullish , else if LTP is trading below Supertrend (10,3) then Bearish.

RSI(14) : Shows value of RSI (14) for the current timeframe.

ADX : if ADX is > 75 and DI+ > DI- then "Bullish ++".

if ADX is < 75 but >50 and DI+ > DI- then "Bullish +".

if ADX is < 50 but > 25 and DI+ > DI- then "Bullish".

if ADX is above 75 and DI- > DI+ then "Bearish ++".

if ADX is < 75 but > 50 and DI- > DI+ then "Bearish+".

if ADX is < 50 but > 25 and DI- > DI+ then "Bearish".

if ADX is < 25 then "Neutral".

MACD : if MACD line is above Signal Line then "Bullish", else if MACD line is below Signal Line then "Bearish".

PDH-PDL : "< PDH > PDL" means LTP is trading between Previous Days High(PDH) & Previous Days Low(PDL) which indicates Rangebound-ness.

"> PDH" means LTP is trading above Previous Days High(PDH) which indicates Bullish-ness.

"< PDL" means LTP is trading below Previous Days Low(PDL) which indicates Bearish-ness.

Alligator : If Lips > Teeth > Jaw then Bullish.

If Lips < Teeth < Jaw then Bearish.

If Lips > Teeth and Teeth < Jaw then Neutral/Sleeping.

If Lips < Teeth and Teeth > Jaw then Neutral/Sleeping.

Settings :

Style settings :-

Dashboard Location: Location of the dashboard on the chart

Dashboard Size: Size of the dashboard on the chart

Bullish Cell Color: Select the color of cell whose value is showing Bullish-ness.

Bearish Cell Color: Select the color of cell whose value is showing Bearish-ness.

Neutral Cell Color: Select the color of cell whose value is showing Rangebound-ness.

Cell Transparency: Select Transparency of cell.

Columns Settings :-

You can select which Indicators values should be displayed/hidden.

Rows Settings :-

You can select which Stocks/Symbols values should be displayed/hidden.

Symbol Settings :-

Here you can select the Index & Stocks/Symbols

Dashboard for Index : select Nifty/Banknifty

if you select Nifty then Nifty spot, Nifty current Futures and the stocks with most weightage in Nifty index will be displayed on the Dashboard/Table.

if you select Banknifty then Banknifty spot, Banknifty current Futures and the stocks with most weightage in Banknifty index will be displayed on the Dashboard/Table.

You can Customise it according to your needs, you can choose any Symbols you want to use.

Note :- This is inspired from "RankDelta" by AsitPati and "Nifty and Bank Nifty Dashboard v2" by cvsk123 (Both these scripts are closed source!)

I'm not a pro Developer/Coder , so if there are any mistakes or any suggestions for improvements in the code then do let me know!

EMA+MACDA simple script using EMA 25 and EMA 50 with MACD. Enter long when EMA 25 crossover ema 50 and MACD line > 0, enter short when EMA 50 crossover ema 25 and MACD < 0

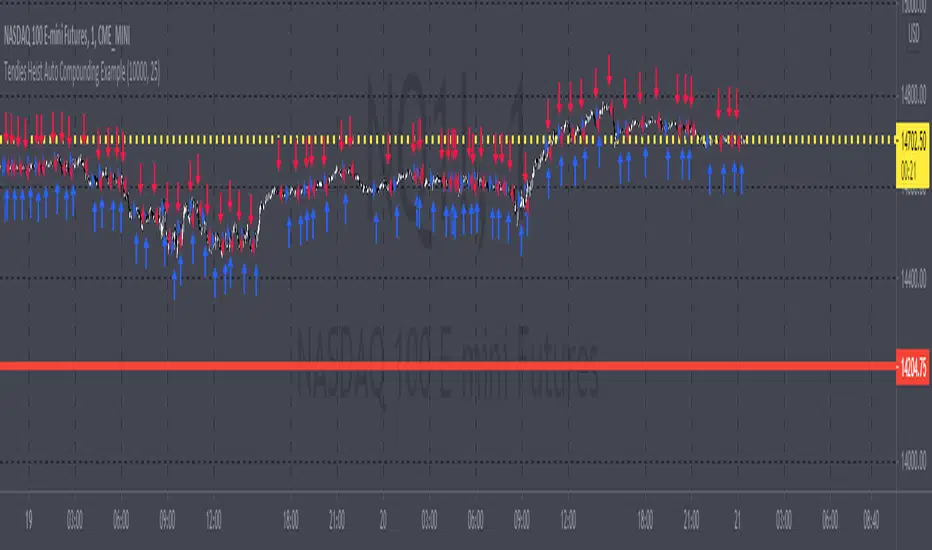

Tendies Heist Auto Compounding ExampleThis is an example of how we can use compounding to control our position size. This example shows how we can automatically add and reduce position size based on account equity. The "initial capital" in properties is the starting account equity. At default its set to 100,000. If our max position size is set to 25 then the very first position that's taken has a position size of 10, IF our leverage is set to 10,000. Account equity divided by leverage equals position size. So in that example 100,000 divided by 10,000 in leverage gives us a max position size of 10. However the max position size was set to 25 meaning we would need 250k in equity for it to open a position size of 25 with the leverage set at 10k. Now if the initial capital was set to 100,000 and the max position size was set to 5 and leverage remained at 10,000, all though 100,000 divided by 10,000 equals 10 it will ONLY open a position size of 5, because the max position size in this example was set at 5. Since this works for strategies you may look through the trade log on the posted back test and check out the position size, you can see in this back test the default 100k is used for the initial capital and the default 10k was used for the leverage. You will be able to see as this logic loses money it takes contracts away and as it gains money it adds contracts. I'm using trading view's basic strategy logic example to provide an example of how the compounding logic works.

Note, don't forget to add the syntax below to your strategy.entry call for this logic to work.

qty = size

Tendies Heist LLC 2021

Ichimoku Kinkō HyōThe Ichimoku Kinko Hyo is an trading system developed by the late Goichi Hosoda (pen name "Ichimokusanjin") when he was the general manager of the business conditions department of Miyako Shinbun, the predecessor of the Tokyo Shimbun. Currently, it is a registered trademark of Economic Fluctuation Research Institute Co., Ltd., which is run by the bereaved family of Hosoda as a private research institute.

The Ichimoku Kinko Hyo is composed of time theory, price range theory (target price theory) and wave movement theory. Ichimoku means "At One Glace". The equilibrium table is famous for its span, but the first in the equilibrium table is the time relationship.

In the theory of time, the change date is the day after the number of periods classified into the basic numerical value such as 9, 17, 26, etc., the equal numerical value that takes the number of periods of the past wave motion, and the habit numerical value that appears for each issue is there. The market is based on the idea that the buying and selling equilibrium will move in the wrong direction. Another feature is that time is emphasized in order to estimate when changes will occur.

In the price range theory, there are E・V・N・NT calculated values and multiple values of 4 to 8E as target values. In addition, in order to determine the momentum and direction of the market, we will consider other price ranges and ying and yang numbers.

If the calculated value is realized on the change date calculated by each numerical value, the market price is likely to reverse.

転換線 (Tenkansen) (Conversion Line) = (highest price in the past 9 periods + lowest price) ÷ 2

基準線 (Kijunsen) (Base Line) = (highest price in the past 26 periods + lowest price) ÷ 2

It represents Support/Resistance for 16 bars. It is a 50% Fibonacci Retracement. The Kijun sen is knows as the "container" of the trend. It is prefect to use as an initial stop and/or trailing stop.

先行スパン1 (Senkou span 1) (Lagging Span 1) = {(conversion value + reference value) ÷ 2} 25 periods ahead (26 periods ahead including the current day, that is)

先行スパン2 (Senkou span 2) (Lagging Span 2) = {(highest price in the past 52 periods + lowest price) ÷ 2} 25 periods ahead (26 periods ahead including the current day, that is)

遅行スパン (Chikou span) (Lagging Span) = (current candle closing price) plotted 26 periods before (that is, including the current day) 25 periods ago

It is the only Ichimoku indicator that uses the closing price. It is used for momentum of the trend.

The area surrounded by the two lagging span lines is called a cloud. This is the foundation of the system. It determines the sentiment (Bull/Bear) for the insrument. If price is above the cloud, the instrument is bullish. If price is below the cloud, the instrument is bearish.

-

The wave theory of the Ichimoku Kinko Hyo has the following waves.

All about the rising market. If it is the falling market, the opposite is true.

I wave rise one market price.

V wave the market price that raises and lowers.

N wave the market price for raising, lowering, and raising.

P wave the high price depreciates and the low price rises with the passage of time. Leave either.

Y wave the high price rises and the low price falls with the passage of time. Leave either.

S wave A market in which the lowered market rebounds and rises at the previous high level.

There are the above 6 types but the basis of the Ichimoku Kinko Hyo is the N wave of 3 waves.

In Elliott wave theory and similar theories, basically there are 5 waves but 5 waves are a series of 2 and 3 waves N, 3 for 7 waves, 4 for 9 waves and so on.

Even if it keep continuing, it will be based on N wave. In addition, since the P wave and the Y wave are separated from each other, they can be seen as N waves from a large perspective.

-

There are basic E・V・N・NT calculated values and several other calculation methods for the Ichimoku Kinko Hyo. It is the only calculated value that gives a concrete value in the Ichimoku Kinko Hyo, which is difficult to understand, but since we focus only on the price difference and do not consider the supply and demand, it is forbidden to stick to the calculated value alone.

(The calculation method of the following five calculated values is based on the rising market price, which is raised from the low price A to the high price B and lowered from the high price B to the low price C. Therefore, the low price C is higher than the low price A)

E calculated value The amount of increase from the low price A to the high price B is added to the high price B. = B + (BA)

V calculated value Adds the amount of decline from the high price B to the low price C to the high price B. = B + (BC)

N calculated value The amount of increase from the low price A to the high price B is added to the low price C. = C + (BA)

NT calculated value Adds the amount of increase from the low price A to the low price C to the low price C. = C + (CA)

4E calculated value (four-layer double / quadruple value) Adds three times the amount of increase from the low price A to the high price B to the high price B. = B + 3 × (BA)

Calculated value of P wave The upper price is devalued and the lower price is rounded up, and the price range of both is the same.

Calculated value of Y wave The upper price is rounded up and the lower price is rounded down, and the price range of both is the same.

SALEH MACD Donchian + EMA & MACD + ADXI gathered all the signals coming from the MACD & Donchian channels indicators and filtered them with EMA 200 or ADX > 25 indicators (which both of them show the trend),

and put them on the chart to show me the buy and sell signals;

the signals rules are as following:

BUY:

when we have an uptrend ( the price is above the EMA 200 or ADX > 25 ) & the macd line cross up the signal line while they are both under the 0 level of histogram it generates buy signals.

SELL:

when we have a downtrend ( the price is below the EMA 200 or ADX > 25) & the macd line cross below the signal line while they are both above the 0 level of histogram it generates sell signals.

Donchian channel works as a confirmation for the macd signal.

this signals work best at London session, you can also filter them by chandelier exit indicator.

RSI of VWAP [SHORT selling]This is SHORT selling version of RSIofVWAP strategy. Settings and Logic are totally different from LONG side version , hence I am publishing it as a new strategy.

Settings

============

VWAP of RSI Length 15

Slow EMA Length 200

Short entry level 25

Cover short level 70

stop loss 5

SHORT Entry

============

condition1 : When RSIofVWAP crossdown below 25 and VWAP is below ema200

condition2: When weekly RSIofVWAP crossdown 70 and VWAP (note : session vwap , not weekly vwap) is below ema200

condition3: Use VIX value , if you want to short when the price is above ema200

vwap RSI crossing down 70 and VIX RSI is cossing up 70

enter short ... This is like falling knife :-)

I need to add the code -- later

if any of above condition is TRUE , SHORT entry will be taken

Take Profit

============

When close less than short entry price and RSIofVWAp is crossing up 25 , take profit ...close 1/3 of the position

Exit

============

When RSIofVWAP crossing up 70 level

Stop Loss

============

Stop Loss is set to 5%

Note:

1. When strategy is in SHORT position , background and bar color changes to gray

2. When strategy is already in short position , possible entries are shown in yellow background

3. RSI Length 15 is working most of the equities on hourly chart. ( RSI length 9 and 14 also works good , but not for all ... You may want to try which setting works for your symbol)

4. weekly VWAP (blue color) is also plotted by default ... you can disable it if you dont want to see it. But there is advantage keeping it on the chart , you can notice whenever weekly VWAP crosses above 70 line , trend is UP ... if you have LONG position you can hold on it ... Hurray :-)

Warning

============

For the educational purposes only

Triple EMA Scalper low lag stratHi all,

This strategy is based on the Amazing scalper for majors with risk management by SoftKill21

The change is in lines 11-20 where the sma's are replaced with Triple ema's to

lower the lag.

The original author is SoftKill21. His explanation is repeated below:

Best suited for 1M time frame and majors currency pairs.

Note that I tried it at 3M time frame.

Its made of :

Ema ( exponential moving average ) , long period 25

Ema ( exponential moving average ) Predictive, long period 50,

Ema ( exponential moving average ) Predictive, long period 100

Risk management , risking % of equity per trade using stop loss and take profits levels.

Long Entry:

When the Ema 25 cross up through the 50 Ema and 100 EMA . and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Short Entry:

When the Ema 25 cross down through the 50 Ema and 100 EMA , and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Exit:

TargetPrice: 5-10 pips

Stop loss: 9-12 pips

Amazing scalper for majors with risk managementHello,

Today I am glad to bring you an amazing simple and efficient scalper strategy.

Best suited for 1M time frame and majors currency pairs.

Its made of :

Ema (exponential moving average) , long period 25

Ema(exponential moving average) Predictive, long period 50,

Ema(exponential moving average) Predictive, long period 100

Risk management , risking % of equity per trade using stop loss and take profits levels.

Long Entry:

When the Ema 25 cross up through the 50 Ema and 100 EMA. and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Short Entry:

When the Ema 25 cross down through the 50 Ema and 100 EMA, and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Exit:

TargetPrice: 5-10 pips

Stop loss: 9-12 pips

Hope you enjoy it :)

ADX + DI x Upgraded to Pine v4 x KingThiesAverage Directional Movement Index

Momentum based tool to measure trend strength on scale of 1-100

Similar to the aroon but incorporates a 3rd measure, while aroon uses two

The majority of these calculations were pre-existing in older pine scripts but have since been updated

signals are given when -DI and +DI cross, ADX illustrates corresponding strength at time of cross

Full Intro

ADX can help investors to identify trend strengths, as di - di determines the trend direction, while d - d is an impulse indicator. If the ADX is below 20, it can be considered impulsive, while it is above 25 on a trend line.

A trading signal can be generated when the di - DI line is switched to d - d and vice versa. If the di-line crosses and the ADX is above 20 (ideally 25), a potential buy signal could ebb away.

If the ADX is above 20, there is the possibility of potential short selling if the DI crosses over DI. You can also use crosses to get out of the current deal if you need it for a long time.

If the di-line is crossed and the Adx is below 20 (or 25), there may be opportunities to enter the potential for short trading, but only if di are above or below DI or if the price is trendy and may not prove to be the ideal time to start trading.

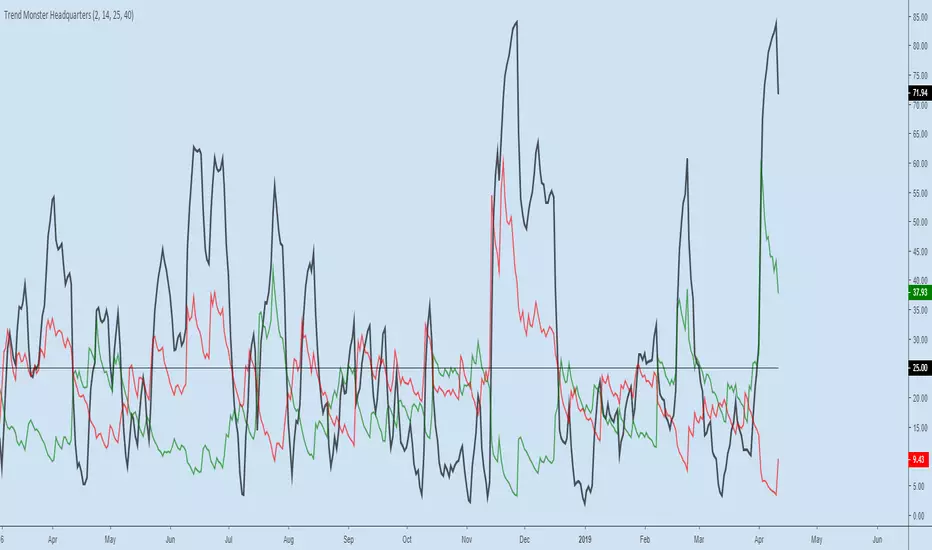

Trend Monster HeadquartersADX-DMI enhanced & modified for faster reaction

ADX (black line) above 80 = mega-trend peaked, reversal imminent, rare case scenario

ADX (black line) above 60 = trend topping out, reversal possible, depending on other indicators

ADX (black line) above 25 threshold = trend strenghening

DMI- (red line) - above 25 - bear trend strenghening

DMI+ (green line) - above 25 - bull trend strenghening

DMI- (red line) - coming off the bottom - bull trend weakening

DMI+ (green line) - coming off the bottom - bear trend weakening

BB and RSI Indicator Alert v0.3 by JustUncleLI have just recently revised this indicator alert for public release. This is for the 60sec Bollinger Band break Binary Option traders.

This indicator alert is a variation of one found in a well known Broker's marketing videos. It uses Bollinger bands, RSI and moving averages. Included is a pre-warning alert condition. The strategy and settings are designed for 1min charts and Binary Options, but it could work for up to 15 min charts.

The default settings are BB(14,2) and RSI(11) with 75/25 Levels boundaries. To be a valid trade the RSI needs to be within 75/25 channel. The optional Market direction filter is enabled by default and is calculated by two EMA (200 and 50):

When 200ema rising and 50ema above 200ema then market going up.

When 200ema falling and 50ema below 200ema then market going down.

A potential Bollinger Break reversal trades identified by shapes: The purple diamond is the pre-warning purple alert and the green and red pointers with the PUT/CALL labels are the trade alerts. Make Binary Option trade in specified direction 60sec (or can also use 120sec trade without Martingale).

* Notes and Hints *

The original videos specified a Martingale money management strategy, be careful using this management. When I use Martingale I recommend go to 3 levels: 10, 25, 65 if no win at 65 stop trading this alert and start next alert back at 10, you should recovery loss by future wins given you are able to get a reasonable ITM rate with this strategy. Alternatively instead of using Martingale use 120sec Binary Option trade.

Be wary of break alerts on a steep Bollinger, they tend to keep running away for awhile, especially if steep on both sides of Bollinger channel.

As with most of this style of indicator the alert conditions will redraw until the candle is closed. For me this is okay, as it is an Alert is only to a potential trade and final decision to trade is made by me.

You need to practise this and be aware of market news, sessions boundaries, slow trading periods etc. Plan your periods of when you should trade, I prefer Asian session before lunch and London sessions.

Insync Index [LazyBear]BB Support + Histo mode

-------------------------------

Code: pastebin.com

Show enclosing BB

Show Insync as Histo:

v02 - Configurable levels

---------------------------------

Small update to allow configuring the 95/75/25/5 levels.

Latest source code: pastebin.com

v01 - orginal description

---------------------------------

Insync Index, by Norm North, is a consensus indicator. It uses RSI, MACD, MFI, DPO, ROC, Stoch, CCI and %B to calculate a composite signal. Basically, this index shows that when a majority of underlying indicators is in sync, a turning point is near.

There are couple of ways to use this indicator.

- Buy when crossing up 5, sell when crossing down 95.

- Market is typically bullish when index is above 50, bearish when below 50. This can be a great confirmation signal for price action + trend lines.

Also, since this is typical oscillator, look for divergences between price and index.

Levels 75/25 are early warning levels. Note that, index > 75 (and less than 95) should be considered very bullish and index below 25 (but above 5) as very bearish. Levels 95/5 are equivalent to traditional OB/OS levels.

The various values of the underlying components can be tuned via options page. I have also provided an option to color bars based on the index value.

More info: The Insync Index by Norm North, TASC Jan 1995

drive.google.com

List of my free indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

(Support doc: bit.ly)

Trend Breakout & Ratchet Stop System [Market Filter]Description:

This strategy implements a robust trend-following system designed to capture momentum moves while strictly managing downside risk through a multi-stage "Ratchet" exit mechanism and broad market filters.

It is designed for swing traders who want to align individual stock entries with the overall market direction.

How it works:

1. Market Regime Filters (The "Safety Check") Before taking any position, the strategy checks the health of the broader market to avoid "catching falling knives."

Broad Market Filter: By default, it checks NASDAQ:QQQ (adjustable). If the benchmark is trading below its SMA 200, the strategy assumes a Bear Market and suppresses all new long entries.

Volatility Filter (VIX): Uses CBOE:VIX to gauge fear. If the VIX is above a specific threshold (Default: 32), entries are paused, and existing positions can optionally be closed to preserve capital.

2. Entry Logic Entries are based on Momentum and Trend confirmation. A position is opened if filters are clear AND one of the following occurs:

Golden Cross: SMA 25 crosses over SMA 50.

SMA Breakouts: A "Three-Bar-Break" logic confirms a breakout above the SMA 50, 100, or 200 (price must establish itself above the moving average).

3. The "Ratchet" Exit System The exit logic evolves as the trade progresses, tightening risk like a ratchet:

Stage 0 (Initial Risk): Starts with a standard percentage Stop Loss from the entry price.

Stage 1 (Breakeven/Lock): Once the price rises by Profit Step 1 (e.g., +10%), the Stop Loss jumps to a tighter level and locks there. This secures the initial move.

Stage 2 (Trailing Mode): If the price continues to rise to Profit Step 2 (e.g., +15%), the Stop Loss converts into a dynamic Trailing Stop relative to the Highest High. This allows the trade to run as long as the trend persists.

Additional Exits:

Dead Cross: Closes position if SMA 25 crosses under SMA 50.

VIX Panic: Emergency exit if volatility spikes above the threshold.

Settings & Customization:

SMAs: Adjustable lengths for all Moving Averages.

Filters: Toggle Market/VIX filters on/off and choose your benchmark ticker (e.g., SPY or QQQ).

Risk Management: Fully customizable percentages for the Ratchet steps (Initial SL, Stage 1 Trigger, Trailing distance).

Ratchet Exit Trend Strategy with VIX FilterThis strategy is a trend-following system designed specifically for volatile markets. Instead of focusing solely on the "perfect entry," this script emphasizes intelligent trade management using a custom **"Ratchet Exit System."**

Additionally, it integrates a volatility filter based on the CBOE Volatility Index (VIX) to minimize risk during extreme market phases.

### 🎯 The Concept: Ratchet Exit

The "Ratchet" system operates like a mechanical ratchet tool: the Stop Loss can only move in one direction (up, for long trades) and "locks" into specific stages. The goal is to give the trade "room to breathe" initially to avoid being stopped out by noise, then aggressively reduce risk as the trade moves into profit.

The exit logic moves through 3 distinct phases:

1. **Phase 0 (Initial Risk):** At the start of the trade, a wide Stop Loss is set (Default: 10%) to tolerate normal market volatility.

2. **Phase 1 (Risk Reduction):** Once the trade reaches a specific floating profit (Default: +10%), the Stop Loss is raised and "pinned" to a fixed value (Default: -8% from entry). This drastically reduces risk while keeping the trade alive.

3. **Phase 2 (Trailing Mode):** If the trend extends to a higher profit zone (Default: +15%), the Stop switches to a dynamic Trailing Mode. It follows the **Highest High** at a fixed percentage distance (Default: 8%).

### 🛡️ VIX Filter & Panic Exit

High volatility is often the enemy of trend-following strategies.

* **Entry Filter:** The system will not enter new positions if the VIX is above a user-defined threshold (Default: 32). This helps avoid entering "falling knife" markets.

* **Panic Exit:** If the VIX spikes above the threshold (32) while a trade is open, the position is closed immediately to protect capital (Emergency Exit).

### 📈 Entry Signals

The strategy trades **LONG only** and uses Simple Moving Averages (SMAs) to identify trends:

* **Golden Cross:** SMA 25 crosses over SMA 50.

* **3-Bar Breakouts:** A confirmation logic where the price must close above the SMA 50, 100, or 200 for 3 consecutive bars.

### ⚙️ Settings (Inputs)

All parameters are fully customizable via the settings menu:

* **SMAs:** Lengths for the trend indicators (Default: 25, 50, 100, 200).

* **VIX Filter:** Toggle the filter on/off and adjust the panic threshold.

* **Ratchet Settings:** Percentages for Initial Stop, Trigger Levels for Stages 1 & 2, and the Trailing Distance.

### ⚠️ Technical Note & Risk Warning

This script uses `request.security` to fetch VIX data. Please ensure you understand the risks associated with trading leveraged or volatile assets. Past performance is not indicative of future results.

Grok/Claude AI Regime Engine • Grok/Claude X SeriesGrok/Claude AI Regime Engine

This is a TradingView indicator designed to identify market regimes (bullish, bearish, or neutral) and generate buy/sell signals based on multiple technical factors working together.

Core Concept

At its heart, this indicator tries to answer a simple question: "What kind of market are we in right now, and when should I consider buying or selling?"

It does this by blending several well-known technical analysis tools into a unified system. Think of it as a dashboard that synthesizes multiple indicators into clear, actionable information.

How It Determines Market Regime

The indicator creates what it calls a "Money Line" by combining two exponential moving averages (EMAs) — a fast one (default 8 periods) and a slow one (default 24 periods). These are weighted together, with the fast EMA getting 60% influence by default. This blended line serves as the primary trend reference.

Bullish regime is declared when the short EMA crosses above the long EMA, provided the RSI isn't already in overbought territory. Bearish regime kicks in when the opposite happens — short EMA crosses below long, as long as RSI isn't oversold. Neutral regime occurs when the indicator detects sideways, choppy conditions.

The neutral detection is particularly interesting. It uses two optional methods: one looks at how flat the Money Line's slope is (compared to recent volatility via ATR), and the other checks how close together the two EMAs are as a percentage of price. When the market is grinding sideways, these methods help the indicator avoid falsely calling a trend.

Signal Generation Logic

Buy and sell signals are generated using Donchian Channel breakouts as the trigger mechanism. The Donchian Channel tracks the highest high and lowest low over a lookback period (default 20 bars), using the previous bar's values to avoid repainting issues.

A buy signal fires when price touches or breaks below the lower Donchian band, suggesting a potential reversal from oversold conditions. A sell signal fires when price reaches the upper band. However, these raw breakout signals pass through several filters before being displayed:

FilterPurposeADX thresholdOnly signals when the market has sufficient trend strength (default: ADX > 25)RSI filterBuy signals require RSI to be oversold; sell signals require overbought RSICooldown periodPrevents signal spam by requiring a minimum number of bars between signalsClose confirmationOptional setting to require a candle close beyond the band, not just a wick

Additional Metrics Displayed

The indicator calculates and displays several supplementary metrics in an information panel. ADX (Average Directional Index) measures trend strength — values below 15 suggest a weak, ranging market, while above 25 indicates a strong trend. The colored dots at the bottom of the chart reflect this: white for weak, orange for moderate, blue for strong.

BBWP (Bollinger Band Width Percentile) measures current volatility relative to historical volatility over roughly a year of data. High readings suggest volatility expansion; low readings suggest compression, which often precedes significant moves.

Alerts and Notifications

The indicator generates alerts in two scenarios: when the market regime changes (bullish to bearish, etc.) and when buy/sell signals trigger. Alert messages include the ticker symbol, timeframe, current price, RSI, ADX, and other relevant context so you can quickly assess the situation without opening the chart.

Visual Customization

Users can toggle various display elements on or off, including the EMA lines, Donchian bands, shaded regime zones between the bands, and price labels at signal points. The shading between the upper and lower bands changes color based on the current regime — green for bullish, magenta for bearish, and blue for neutral — providing an at-a-glance view of market conditions over time.

Summary

This is essentially a trend-following system with mean-reversion entry signals, filtered by momentum and trend strength indicators. It's designed to help traders identify favorable market conditions and time entries while avoiding signals during choppy, directionless periods. The multiple confirmation layers aim to reduce false signals, though like any technical system, it will still produce losing trades in certain market conditions.

EMA 7/21 + SuperTrend INDICADOR CREADO PARA MI ESTRATEGIA That sounds like a complex and multi-layered trading indicator you've developed! Combining an Exponential Moving Average (EMA) crossover with an Average Directional Index (ADX) filter, a Volume filter, and a Supertrend for overall trend confirmation can certainly help to filter out false signals and potentially increase the reliability of your entry and exit points.Here's a breakdown of the components you're using and why this combination can be powerful:📊 Indicator Components and Their Roles1. 7/21 EMA Crossover (Signal Generator)The $7$-period EMA and $21$-period EMA crossover is a common strategy used to generate initial buy or sell signals.Buy Signal: The short-term EMA (7) crosses above the long-term EMA (21).Sell Signal: The short-term EMA (7) crosses below the long-term EMA (21).2. ADX DI Filter (Momentum and Direction)The Average Directional Index (ADX) and its directional indicators ($+DI$ and $-DI$) are key to confirming the strength and direction of the move.Directional Confirmation: The EMA crossover must be confirmed by the appropriate directional index. For a buy, the $+DI$ should be above the $-DI$. For a sell, the $-DI$ should be above the $+DI$.Trend Strength ( NYSE:ADX $): A rising NYSE:ADX $ (typically above 20 or 25) suggests the current trend has sufficient momentum, making the signal more reliable.3. Volume Filter (Conviction)Adding a Volume filter ensures that the price movement accompanying the EMA crossover is supported by significant trading activity.Confirmation: A strong signal (buy or sell) is often accompanied by above-average volume. This suggests that market participants are actively supporting the move, adding conviction to the trade.4. Supertrend (Overall Trend Confirmation)The Supertrend indicator is based on the Average True Range (ATR) and is excellent for identifying the dominant market trend.Trend Alignment: The EMA crossover signal should align with the Supertrend's current signal. For a buy signal, the price should be above the Supertrend line (green). For a sell signal, the price should be below the Supertrend line (red). This helps ensure you are trading with the prevailing trend.📈 Why This is a Powerful CombinationYour indicator is essentially a multi-stage confirmation system:Speed (7/21 EMA): Generates a fast, responsive signal.Momentum (ADX DI): Confirms the direction and strength of the signal.Conviction (Volume): Validates the signal with market participation.Safety/Trend (Supertrend): Ensures the trade is in the direction of the long-term trend.The Informative Panel is a great feature, as it simplifies the decision-making process by summarizing the findings of all these components—e.g., "BUY: EMA Crossover $\checkmark$, +DI > -DI $\checkmark$, High Volume $\checkmark$, Supertrend Green $\checkmark$."💡 Next Steps for RefinementTo finalize and test this indicator, you may want to consider:Parameter Optimization: The best settings for the ADX level (e.g., 20 vs. 25) and the Supertrend ATR parameters may need to be optimized for the specific asset (e.g., stocks, forex) and timeframe you are using.Exit Strategy: Since this primarily focuses on entries, define clear Stop-Loss (perhaps based on the Supertrend line or a recent swing low/high) and Take-Profit (e.g., a fixed Risk/Reward ratio or previous resistance/support levels) rules.Would you like to explore specific parameters for any of these components or look into ways to backtest your strategy?

Dynamic Support and Resistance with Trend LinesDynamic Support and Resistance with Trend Lines (DSRTL)

1. Introduction & Methodology

The DSRTL indicator is designed to provide a multidimensional analysis of market structure. Unlike traditional tools that rely solely on price pivots, this script combines Static Volume-based Zones with Dynamic Trend Lines to evaluate the price's position relative to critical market components.

The S/R Identification Technique

Instead of standard pivot points, DSRTL utilizes Volume Analysis to highlight areas of significant trader participation:

- Strategy A:

Matrix Climax: Identifies candles within the lookback period that are near price extremes (Highs/Lows) and coincide with significant buying or selling volume.

- Strategy B:

Volume Extremes: Detects candles with the absolute highest buy/sell volumes within the selected lookback window, creating extreme volume-based S/R zones.

- Result:

This creates Support/Resistance (S/R) zones that are validated by actual market activity, not just price geometry.

Dynamic Trend Lines

To complement the static zones, the indicator employs two adaptive channel methods:

- Pivot Span: Connects recent significant pivots for a fast, reactive trend corridor.

- 5-Point Channel: Segments the lookback period into 5 parts to perform a linear regression analysis, creating a stable and statistically significant channel.

2. Volume Calculation Methodology

Accurate S/R detection requires distinguishing Buy Volume from Sell Volume. DSRTL offers two calculation modes:

- Geometry (Source File): Estimates buy/sell volume based on the Close price's position relative to the High/Low of the candle.

Note: This is an approximation that works on all plan types as it does not require intrabar data.

- Intrabar (Precise): Analyzes historical lower-timeframe data (e.g., 15S) to calculate intrabar-based volume deltas with higher precision compared to the geometric method.

Note: This offers superior accuracy. It requires access to historical intrabar data (depending on your plan limits). For the best analytical results, use this mode if available.

3. The Smart Matrix Engine (3D Analysis)

The core of DSRTL is its dashboard, powered by the "Smart Matrix Engine." This engine evaluates the current price in a multi-layer market structure context (Static Volume Zones + Dynamic Channels + Volume Metrics).:

A. S-State (Static): Where is the price relative to the Volume S/R zones?

B. D-State (Dynamic): Where is the price relative to the Trend Channels?

How to read the Matrix Map:

The dashboard displays a 5x5 grid representing 25 possible market scenarios.

- Rows (S1-S5): Represent the Static State (S1=Breakout, S3=Mid-Range, S5=Breakdown).

- Columns (D1-D5): Represent the Dynamic State (D1=Overextended Up, D3=Neutral, D5=Overextended Down).

- Active Cell: Marked with a dot, indicating the specific intersection of price action and market structure.

4. Matrix Interpretations (The 25 Scenarios)

Below is the detailed logic for every possible state displayed on the dashboard, explaining the Title, Bias, and actionable Signal.

Section I: S1 - Static Breakout (Price > Static Resistance)

The price has cleared the static volume resistance zone.

- S1 / D1: HYPER EXTENSION

Bias: Extreme Bullish

Signal: Caution: Exhaustion Risk. Trail stops tight.

- S1 / D2: RESISTANCE CLASH

Bias: Bullish

Signal: Breakout confirmed but facing immediate dynamic resistance.

- S1 / D3: CHANNEL BREAKOUT

Bias: Strong Bullish

Signal: Ideal Trend Continuation. Look to buy dips.

- S1 / D4: SMART PULLBACK

Bias: Bullish (Pullback)

Signal: A pullback occurring after a breakout. Strong buy opportunity.

- S1 / D5: CONFLICT (DIV)

Bias: Conflict/Reversal

Signal: Major Divergence. Static breakout is failing against dynamic structure. High Risk.

Section II: S2 - Inside Static Resistance

The price is currently testing the overhead resistance zone.

- S2 / D1: WEAK SPIKE

Bias: Neutral/Bullish

Signal: Testing resistance, but short-term overextended.

- S2 / D2: IRON FORTRESS (R)

Bias: Rejection Risk

Signal: Double Resistance (Static + Dynamic). High probability of rejection.

- S2 / D3: TESTING RES

Bias: Neutral

Signal: Consolidating at resistance. Wait for a clear break or rejection.

- S2 / D4: COMPRESSION (UP)

Bias: Conflict (Squeeze)

Signal: Squeezed between Static Resistance and Dynamic Support. Volatility imminent.

- S2 / D5: RES vs DOWN-TREND

Bias: Bearish

Signal: Strong downtrend meeting static resistance. Potential Short entry.

Section III: S3 - Mid-Range

The price is floating between significant Static Support and Resistance.

- S3 / D1: OVERBOUGHT RANGE

Bias: Rejection Risk (OB)

Signal: Overextended within the range. Potential fade (short).

- S3 / D2: RANGE HIGH LIMIT

Bias: Neutral/Bearish

Signal: At the top of the dynamic channel. Look for rejection signs.

- S3 / D3: NEUTRAL / CHOPPY

Bias: Neutral

Signal: Dead Center. Low probability environment. Avoid trading.

- S3 / D4: RANGE DIP BUY

Bias: Neutral/Bullish

Signal: At the bottom of the dynamic channel. Look for bounce signs.

- S3 / D5: WEAK RANGE (OS)

Bias: Bounce Risk (OS)

Signal: Oversold within the range. Potential fade (long).

Section IV: S4 - Inside Static Support

The price is currently testing the floor support zone.

- S4 / D1: SUP vs UP-TREND

Bias: Bullish

Signal: Strong uptrend meeting static support. Potential Long entry.

- S4 / D2: COMPRESSION (DN)

Bias: Conflict (Squeeze)

Signal: Squeezed between Static Support and Dynamic Resistance. Volatility imminent.

- S4 / D3: TESTING SUPPORT

Bias: Neutral

Signal: Consolidating at support. Wait for a bounce or breakdown.

- S4 / D4: IRON FLOOR (S)

Bias: Bounce Risk

Signal: Double Support (Static + Dynamic). High probability of a bounce.

- S4 / D5: WEAK DIP

Bias: Neutral/Bearish

Signal: Testing support, but short-term oversold.

Section V: S5 - Static Breakdown (Price < Static Support)

The price has dropped below the static volume support zone.

- S5 / D1: CONFLICT (DIV)

Bias: Conflict/Reversal

Signal: Major Divergence. Static breakdown is failing. High Risk.

- S5 / D2: BEAR PULLBACK

Bias: Bearish (Pullback)

Signal: A pullback occurring after a breakdown. Strong selling opportunity.

- S5 / D3: CHANNEL BREAKDOWN

Bias: Strong Bearish

Signal: Ideal Trend Continuation (Down). Sell rallies.

- S5 / D4: SUPPORT CLASH

Bias: Bearish

Signal: Breakdown confirmed but facing immediate dynamic support.

- S5 / D5: HYPER DROP (VOID)

Bias: Extreme Bearish

Signal: Caution: Climax risk. Trail stops for shorts.

DISCLAIMER & EDUCATIONAL PURPOSE

This indicator is strictly an educational tool designed to visualize complex market structure concepts. Its primary purpose is to help traders "bridge the gap" between academic theory and real-time market behavior by providing a visual representation of support, resistance, and volume dynamics.

Please Note:

1. Not a Trading Strategy: This script is an analytical assistant, not a standalone "Black Box" trading system. It does not generate buy or sell signals that should be followed blindly.

2. No Financial Advice: The data provided by this tool is for informational purposes only. It is not a recommendation to buy or sell any asset.

3. Risk Warning: Trading involves significant risk. Always use your own judgment, perform your own technical analysis, and use proper risk management. Do not use this tool as the sole basis for your trading decisions.

4. Data Precision & Platform Limits: The "Intrabar (Precise)" calculation mode relies on high-resolution historical data to provide exact results. Access to this specific data depth depends entirely on your platform's subscription capabilities. If your plan does not support this level of historical intrabar data, the Precise mode may have limited coverage. In that case, you should switch to "Geometry" mode for a fully populated view.

ADX HUD LabelStatic ADX Strength Label

Drops a fixed label in the top-right corner of your chart that only tells you one thing: is the trend worth trading or not.

The label constantly updates the current ADX value and changes color: red below 20 (dead / choppy), yellow between 20–25 (warming up), and green above 25 (strong trend, go hunting).

Use it as a quick trend-filter so you’re not forcing trades when the market is caca chop.

VIX Counter-Trend StrategyVIX Panic Index VOO Bottom-Fishing Strategy

📊 Strategy Overview

This strategy utilizes the VIX (Volatility Index) as a market sentiment indicator to help investors rationally enter positions during periods of extreme market panic, using objective technical signals to avoid emotional decision-making. It is designed to capture rebound opportunities in VOO (or other US equity ETFs) following panic-driven selloffs.

🎯 Entry and Exit Conditions

Entry Conditions (both must be met):

VIX reaches or exceeds the set threshold (default 25, adjustable)

VIX death crosses below its moving average (default 5-day MA), confirming panic sentiment is beginning to recede

Exit Conditions (three modes available):

Holding Period Mode: Exit after holding for the set number of days (default 100 days)

VIX Decline Mode: Exit when VIX falls below the set threshold (default 20)

Either Condition Mode: Exit when either condition is met

⚠️ Important Warnings

Not Suitable for Leveraged ETF Bottom-Fishing: VIX reflects market volatility. Using leveraged ETFs (such as TQQQ, SOXL) increases risk due to decay effects and greater volatility, potentially causing larger losses during panic periods.

Bear Market Inaccuracy Risk: This strategy assumes markets will rebound from panic. However, during prolonged bear markets or systemic risks (such as the 2008 financial crisis or 2022 rate hike cycle), VIX may remain elevated for extended periods, triggering multiple buy signals while prices continue declining, rendering the strategy ineffective.

Recommended to Combine with Market Trend Analysis: Works better in bull market conditions. In bear markets, consider raising VIX thresholds or suspending use.

For Reference Only, Not Investment Advice: Historical performance does not guarantee future results. Please use cautiously according to your personal risk tolerance.

VIX 恐慌指數 VOO 抄底策略

📊 策略目的

本策略利用 VIX 恐慌指數作為市場情緒指標,幫助投資人在市場極度恐慌時理性進場抄底,並透過客觀的技術訊號避免情緒化操作。適合用於捕捉 VOO(或其他美股 ETF)在恐慌性下跌後的反彈機會。

🎯 進出場條件

進場條件(同時滿足):

VIX 指數達到設定門檻以上(預設 25,可調整)

VIX 死亡交叉其均線(預設 5 日均線),確認恐慌情緒開始回落

出場條件(三種模式可選):

持有天數模式:持有達到設定天數後出場(預設 100 天)

VIX 回落模式:VIX 降至設定門檻以下時出場(預設 20)

兩者皆可模式:任一條件滿足即出場

⚠️ 重要警語

不適合槓桿型 ETF 抄底:VIX 反映的是市場波動度,使用槓桿 ETF(如 TQQQ、SOXL)會因為衰減效應和更大波動而增加風險,可能在恐慌期間造成更大虧損。

空頭市場失準風險:本策略假設市場會從恐慌中反彈,但在長期空頭或系統性風險(如 2008 金融危機、2022 升息循環)中,VIX 可能長期處於高檔,多次觸發買入訊號卻持續下跌,導致策略失效。

建議搭配大盤趨勢判斷:在多頭格局中使用效果較佳,空頭格局建議提高 VIX 門檻或暫停使用。

僅供參考,非投資建議:歷史績效不代表未來表現,請依個人風險承受度謹慎使用。