Correlation Coefficient - DXY & XAUPublishing my first indicator on TradingView. Essentially a modification of the Correlation Coefficient indicator, that displays a 2 ticker symbols' correlation coefficient vs, the chart presently loaded.. You can modify the symbols, but the default uses DXY and XAU, which have been displaying strong negative correlation.

As with the built-in CC (Correlation Coefficient) indicator, readings are taken the same way:

Positive Correlation = anything above 0 | stronger as it moves up towards 1 | weaker as it moves back down towards 0

Negative Correlation = anything below 0 | stronger moving down towards -1 | weaker moving back up towards 0

This is primarily created to work with the Bitcoin weekly chart, for comparing DXY and Gold (XAU) price correlations (in advance, when possible). If you change the chart timeframe to something other than weekly, consider playing with the Length input, which is set to 35 by default where I think it best represents correlations with Bitcoin's weekly timeframe for DXY and Gold.

The intention is that you might be able to determine future direction of Bitcoin based on positive or negative correlations of Gold and/or the US Dollar Index. DXY has been making peaks and valleys prior to Bitcoin since after March 2020 black swan event, where it peaked just after instead. In the future, it may flip over again and Bitcoin may hit major highs or lows prior to DXY, again. So, keep an eye on the charts for all 3, as well as the indicator correlations.

Currently, we've moved back into negative correlation between Bitcoin and DXY, and positive correlation with Bitcoin and Gold:

Negative Correlation b/w Bitcoin and DXY - if DXY moves up, Bitcoin likely moves down, or if DXY moves down, Bitcoin likely moves up (or if Bitcoin were to move first before DXY, as it did on March 2020, instead)

Positive Correlation b/w Bitcoin and Gold - Bitcoin and Gold will likely move up or down with each other.

DXY is represented by the green histogram and label, Gold is represented by the yellow histogram and label. Again, you can modify the tickers you want to check against, and you can modify the colors for their histograms / labels.

The inspiration from came from noticing areas of same date or delayed negative correlation between Bitcoin and DXY, here is one of my most recent posts about that:

Please let me know if you have any questions, or would like to see updates to the indicator to make it easier to use or add more useful features to it.

I hope this becomes useful to you in some way. Thank you for your support!

Cheers,

dudebruhwhoa :)

Pesquisar nos scripts por "文华财经tick价格"

biased_price_targetLibrary "biased_price_target"

Collection of functions that can be used for the calculation of biased price targets like stop loss and

take profit from a reference price using several methods that are already provided by the "distance_ratio" library plus

the 'HHLL'. Methods supported are percentagewise (PERC), atr-based (ATR), fixed profit (PROF), tick-based (TICKS),

risk reward ratio (RR), and highest high/lowest low (HHLL)

distance_ratioLibrary "distance_ratio"

Collection of types and functions that can be used for the calculation of the ratio of a distance

from a barrier price using several methods. Methods supported are percentagewise (PERC), atr-based (ATR), fixed

profit (PROF), tick-based (TICKS), risk reward ratio (RR) and local extrema (LOC).

This library is meant to replace my previously published "distance_percentile" library since it offers a more intuitive interface by using the method syntax.

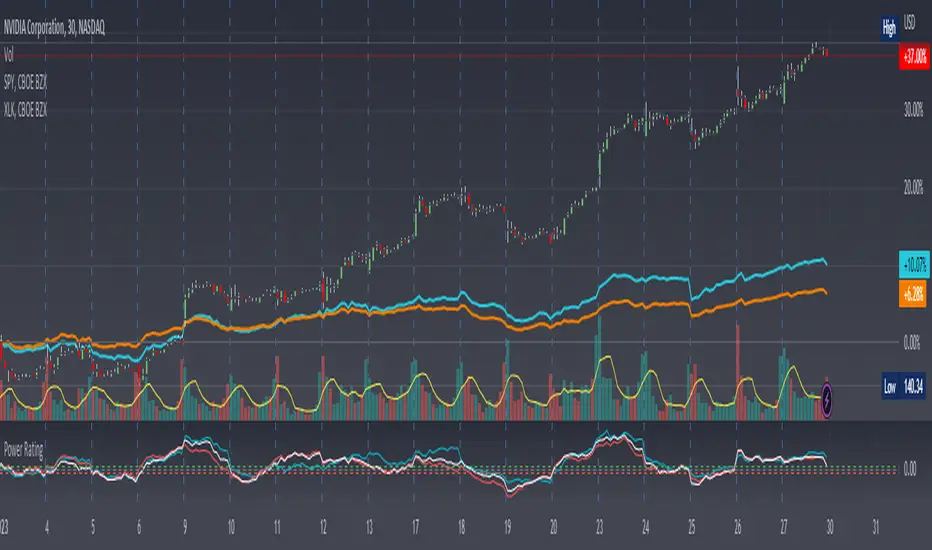

Stock Relative Strength Power IndexAs always, this is not financial advice and use at your own risk. Trading is risky and can cost you significant sums of money if you are not careful. Make sure you always have a proper entry and exit plan that includes defining your risk before you enter a trade.

This idea recently came out of some discussions I stumbled across in a trading group I am a part of regarding Relative Strength and Relative Weakness (shortened to RS and RW from here on out). The whole mechanism behind this trading system is to filter out underperforming securities relative to the current market direction to be in only the strongest or weakest stocks when the market is currently experiencing a bullish or bearish cycle. The idea behind this is there is no point in parking your money into a stock that is treading water or even going down if the market is making strong moves upwards. At that point, you are at worst losing money, and at best trading equal to the index/ETF, in which case the argument is why are you not just trading the index/ETF instead? RS or RW will filter out these sector laggards and allow you to position yourself into strong (or the strongest) stocks at any given time to help improve portfolio performance. Further, not only does it protect your position should the market shift against you briefly, it also often sees exceptional performance in the same cycle. For example, if $SPY makes a 5% move over the course of a month, a stock with RS/RW may make a 10% move, or more, allowing you to see increased profit potential.

RS/RW is based on the idea of performance, that is the raw percent change of a security over a given time period relative to a benchmark. This benchmark is often the S&P500 (ES/SPX/SPY and their derivatives). I have to stress that this is not beta, which measures the volatility of a stock over a given period (i.e. if $SPY moves $1, $NVDA will often move $1.74). This is a measurement of the market (i.e. $SPY) has moved 1% over the course of a day, $NVDA has moved 8% over the course of the day. This is very often used as a signal of institutional interest as apart from some very unique moments, retail traders cannot and will not provide enough market pressure to move a market outside of a stock's normal trading range, nor will they outperform the sector or market as a whole consistently over time without some big money to make them move. The problem with running strict performance analysis (i.e. % change from period T ago to period T + n at present) is that while it gives us a baseline of how much the stock has moved, it doesn't overall mean much. For instance, if a $100 stock has moved 5% today, but has been experiencing a period of increased volatility and it's Average True Range (ATR) (the amount a stock will move over X number of periods, on average) is $7, performance seems impressive but is actually generally fairly weak to what the stock has been doing recently. Conversely, if we take a second stock, this time worth $20, and it too has moved 5% in one day but has an ATR of only $0.25, that stock has made an exceptional move and we want to be part of that.

Here, I have created an indicator called the Stock Relative Strength Power Index. This takes the stock's rate of change (ROC) (the % move it has made over X number of periods), the stock's normalized ATR (the ATR represented as a percentage instead of a raw value), and compares these to one another to get the "Power Rating": a representation of the true strength of a stock over X number of periods. The indicator does two things. First, the raw ROC is divided by the stock's normalized ATR to assess whether the stock is moving outside of its normal range of variation or not. Second, since we are interested in trading only stocks with exceptional RS/RW to the market, I have also applied this same calculation to the S&P500 ($SPY) and the various SPDR sector indexes. These comparisons allow for a rapid and accurate assessment of the true strength of a stock at any given time on any given time frame. To cycle back above to our examples, the $100 stock has a Power Rating of only 0.71 (i.e. it is trading less than its current average), while our $20 stock has a Power Rating of 5. If we then compare these to both the market as a whole and the sector that the stock is a part of, we get a much clearer indication of the true buying or selling pressure imposed on the stock at any given time.

Use:

The indicator has 3 lines. The blue line is the security of interest, the red line is the market baseline (i.e. the sector ETF $SPY), and the white line is the sector index. I have given an example above on the semiconductor/tech stock $NVDA on a 30min timeframe. You can see that since the start of 2023, $NVDA has generally been strong to the market and its own sector since the blue line is greater than both the red and white lines over many days. This would have provided some nice day trading opportunities, or even some nice short term swing trades. The values themselves are generally meaningless outside of either the 1 or -1 value lines. All that matters is that the current ticker is surpassing both the market and the sector while being > 1.0 for a long trade or less than -1.0 for a short trade. However, I must stress this indicator gives no trade signals on its own, it is purely a confirmation indicator. An example of a trade would be if you had a trade signal given by either an indicator or by price action suggesting to buy some $NVDA for a trade to the upside, the Power Rating indicator would confirm this by showing if $NVDA was actually showing true strength by being both greater than 1 (the cutoff for it surpassing its ATR) and being above both the red and white lines. Further, you can see $NVDA has been stronger than the market when using the comparison function as well, but the has fluxed in and out of strength intraday when using the actual indicator vs. the static performance ratio chart (plotted as line graphs on the chart).

I have made it possible to change the colour of the plots and the line levels. The adjustment of the line levels gives the trader the flexibility to change their target breakout level (i.e. only trading stocks that have a Power Rating > 2, for example, meaning they are trading at least 2X their normal trading range). The third security comparison is flexible and can be used to compare to the sector ETF (initial intention) or it can be used to compare to other tickers within the same sector, for example. The trader should select the appropriate ETF for the given security of interest to avoid false confirmation if they want to use an ETF as their third input. The proper sector should be readily available on most online websites and accessible in a matter of seconds meaning that the delay is minimal, at worst. If a trader wishes to add additional functionality, such as a crypto trader using BTCUSD as the benchmark instead of $SPY, I encourage them to copy and paste this script and modify as needed since I have made this open source.

This indicator works on all timeframes. The lookback period can be changed, so a day trader who may use a 5min chart (and use a period of 12 to get the hourly Power Rating) will find this equally useful as someone who may be a core trader who wants to look at the performance over the course of years and may use a 60 period on a monthly chart.

Happy trading and I hope this helps!

Crypto Index (DXY) CandlesA modification of @loxx's "Dollar Index (DXY) Candles" allowing for a user selected basket of tickers using the same weights as the standard DXY. Ticker Inputs are in descending order so highest weight is at the top by default, although weighting can be changed manually by modifying the symbol's corresponding weight input in the settings. The Idea was to get a bird's eye view of the crypto space using some of the more relevant names in the space. User's can use the toggle in the settings for viewing the default DXY for comparison. Indicator should be used as a confirmation when looking at long term trend changes in the space, shorter time frames may, or may not be as useful.

Davin's 10/200MA Pullback on SPY Strategy v2.0Strategy:

Using 10 and 200 Simple moving averages, we capitalize on price pullbacks on a general uptrend to scalp 1 - 5% rebounds. 200 MA is used as a general indicator for bullish sentiment, 10 MA is used to identify pullbacks in the short term for buy entries.

An optional bonus: market crash of 20% from 52 days high is regarded as a buy the dip signal.

An optional bonus: can choose to exit on MA crossovers using 200 MA as reference MA (etc. Hard stop on 50 cross 200)

Recommended Ticker: SPY 1D (I have so far tested on SPY and other big indexes only, other stocks appear to be too volatile to use the same short period SMA parameters effectively) + AAPL 4H

How it works:

Buy condition is when:

- Price closes above 200 SMA

- Price closes below 10 SMA

- Price dumps at least 20% (additional bonus contrarian buy the dip option)

Entry is on the next opening market day the day after the buy condition candle was fulfilled.

Sell Condition is when:

- Prices closes below 10 SMA

- Hard stop at 15% drawdown from entry price (adjustable parameter)

- Hard stop at medium term and long term MA crossovers (adjustable parameters)

So far this strategy has been pretty effective for me, feel free to try it out and let me know in the comments how you found :)

Feel free to suggest new strategy ideas for discussion and indicator building

Volume/Market ProfileVolume/Market Profile is a 2 in 1 Volume Profile and Market Profile Indicator.

This indicator is my own calculations for compiling a volume profile and market profile.

The profile is progressively calculated live as the chart develops.

I have made use of both Boxes AND Lines to allow me to display a finer granularity profile by displaying up to twice the max amount of lines allowed in tradingview.

I have spent a lot of time to make sure the values are getting appended exactly as intended so that I can assure this profile is operating as precisely as possible within the limitations of the data available.

To make my calculations easier to use in other places, I have made my volume profile a function that can be extracted and used whenever you need values from a volume profile.

Feel free to read through the script if you don't understand how this profile is developed. I have made a commentary of my volume profile function to help you understand what exactly happens to compile the profiles.

As mentioned before, This indicator doubles as a market profile. To view both at the same time you will need to add the indicator on your chart twice.

I have built in comprehensive customizations to allow you to display your profiles however fits your needs.

Timeframe: The aggregation period for profiles, to see a 1 week profile, change the timeframe to 1 week.

Note: You can add custom timeframes by adding a custom timeframe in your chart timeframe dropdown menu. When you add timeframes in this area, they appear as options within indicators with the timeframe input.

Sensitivity: Allows for greater or less granularity changes. The calculation method for granularity automatically changes depending on the range of your chart.

Note: Multiply this value by 100 and that will be the max range (in ticks) of your price before the indicator automatically adjusts to make the profile less granular. (ex. If price ranges $1, and 1 tick is $0.01, granularity will be 0.01 with a sensitivity of 1+)

Value Area %: % of total volume to display as the value zone. (_% of total profile values are contained within the value zone)

Calculate as Market Profile: Uses a 1 Instead of the candle volume, to display a Market Profile. (If selected POC -> TPOC)

Display Size: Sets the # of bars from the profile axis to the profile's max value. If set negative, profile will be displayed left of axis, if positive, profile will be displayed to the right of the axis.

Display Offset: Sets the # of bars in front(or behind) the current chart bar to set the axis of the profile. If negative, the axis will be to the left of the current chart bar, if positive the axis will be right of the current chart bar.

Display Historical POC/VAH/VAL: Choose to display historical poc,vah,val lines.

Colors: I'm not explaining colors.

Enjoy!

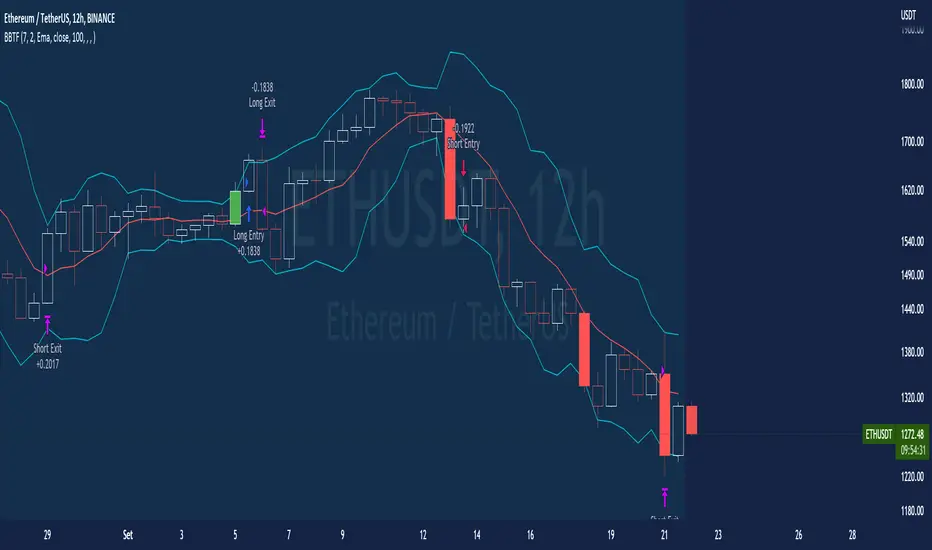

BT-Bollinger Bands - Trend FollowingEsse script foi criado para estudo de Backtest.

O script usa as Bandas de Bollinger para indicar o início de uma tendência, a entrada é configurada quando o preço abre abaixo e fecha acima da banda superior ou para venda quando o preço abre acima e fecha abaixo da banda inferior.

Não há um stop fixo e nem alvo fixo a saída se dá quando o preço toca a média da banda.

Você pode usar uma média móvel como filtro combinado com a estratégia.

O Script também pode ser usado com algum serviço de bot como 3commas.io , basta colocar as mensagens de entrada e saída para o bot.

Autor : Credsonb - Nick: M4TR1X_BR

Neste gráfico estou usando as seguintes configurações:

Bandas Bollinger: 7

Desvio Padrão: 1.5

Time Frame: 12hs

Ticker: ETH

This script was created for Backtest study.

script uses Bollinger Bands to indicate the start of a trend, entry is set when price opens below and closes above the upper band or for short when price opens above and closes below the lower band.

There is no fixed stop and no fixed target, the exit occurs when the price touches the average of the band.

You can use a moving average as a filter combined with the strategy.

The Script can also be used with some bot service like 3commas. io , just put the input and output messages to the bot.

Author : Credsonb - Nick: M4TR1X_BR

lower_tf█ OVERVIEW

This library is a Pine programmer’s tool containing functions to help those who use the request.security_lower_tf() function. Its `ltf()` function helps translate user inputs into a lower timeframe string usable with request.security_lower_tf() . Another function, `ltfStats()`, accumulates statistics on processed chart bars and intrabars.

█ CONCEPTS

Chart bars

Chart bars , as referred to in our publications, are bars that occur at the current chart timeframe, as opposed to those that occur at a timeframe that is higher or lower than that of the chart view.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 intrabars at the LTF of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This framework exemplifies how authors can determine which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. As there is a 100K limit to the number of intrabars that can be analyzed by a script, a trade-off occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

█ `ltf()`

This function returns a timeframe string usable with request.security_lower_tf() . It calculates the returned timeframe by taking into account a user selection between eight different calculation modes and the chart's timeframe. You send it the user's selection, along with the text corresponding to the eight choices from which the user has chosen, and the function returns a corresponding LTF string.

Because the function processes strings and doesn't require recalculation on each bar, using var to declare the variable to which its result is assigned will execute the function only once on bar zero and speed up your script:

var string ltfString = ltf(ltfModeInput, LTF1, LTF2, LTF3, LTF4, LTF5, LTF6, LTF7, LTF8)

The eight choices users can select from are of two types: the first four allow a selection from the desired amount of chart bars to be covered, the last four are choices of a fixed number of intrabars to be analyzed per chart bar. Our example code shows how to structure your input call and then make the call to `ltf()`. By changing the text associated with the `LTF1` to `LTF8` constants, you can tailor it to your preferences while preserving the functionality of `ltf()` because you will be sending those string constants as the function's arguments so it can determine the user's selection. The association between each `LTFx` constant and its calculation mode is fixed, so the order of the arguments is important when you call `ltf()`.

These are the first four modes and the `LTFx` constants corresponding to each:

Covering most chart bars (least precise) — LTF1

Covers all chart bars. This is accomplished by dividing the current timeframe in seconds by 4 and converting that number back to a string in timeframe.period format using secondsToTfString() . Due to the fact that, on premium subscriptions, the typical historical bar count is between 20-25k bars, dividing the timeframe by 4 ensures the highest level of intrabar precision possible while achieving complete coverage for the entire dataset with the maximum allowed 100K intrabars.

Covering some chart bars (less precise) — LTF2

Covering less chart bars (more precise) — LTF3

These levels offer a stepped LTF in relation to the chart timeframe with slightly more, or slightly less precision. The stepped lower timeframe tiers are calculated from the chart timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

Covering the least chart bars (most precise) — LTF4

Analyzes the maximum quantity of intrabars possible by using the 1min LTF, which also allows the least amount of chart bars to be covered.

The last four modes allow the user to specify a fixed number of intrabars to analyze per chart bar. Users can choose from 12, 24, 50 or 100 intrabars, respectively corresponding to the `LTF5`, `LTF6`, `LTF7` and `LTF8` constants. The value is a target; the function will do its best to come up with a LTF producing the required number of intrabars. Because of considerations such as the length of a ticker's session, rounding of the LTF to the closest allowable timeframe, or the lowest allowable timeframe of 1min intrabars, it is often impossible for the function to find a LTF producing the exact number of intrabars. Requesting 100 intrabars on a 60min chart, for example, can only produce 60 1min intrabars. Higher chart timeframes, tickers with high liquidity or 24x7 markets will produce optimal results.

█ `ltfStats()`

`ltfStats()` returns statistics that will be useful to programmers using intrabar inspection. By analyzing the arrays returned by request.security_lower_tf() in can determine:

• intrabarsInChartBar : The number of intrabars analyzed for each chart bar.

• chartBarsCovered : The number of chart bars where intrabar information is available.

• avgIntrabars : The average number of intrabars analyzed per chart bar. Events like holidays, market activity, or reduced hours sessions can cause the number of intrabars to vary, bar to bar.

The function must be called on each bar to produce reliable results.

█ DEMONSTRATION CODE

Our example code shows how to provide users with an input from which they can select a LTF calculation mode. If you use this library's functions, feel free to reuse our input setup code, including the tooltip providing users with explanations on how it works for them.

We make a simple call to request.security_lower_tf() to fetch the close values of intrabars, but we do not use those values. We simply send the returned array to `ltfStats()` and then plot in the indicator's pane the number of intrabars examined on each bar and its average. We also display an information box showing the user's selection of the LTF calculation mode, the resulting LTF calculated by `ltf()` and some statistics.

█ NOTES

• As in several of our recent publications, this script uses secondsToTfString() to produce a timeframe string in timeframe.period format from a timeframe expressed in seconds.

• The script utilizes display.data_window and display.status_line to restrict the display of certain plots.

These new built-ins allow coders to fine-tune where a script’s plot values are displayed.

• We implement a new recommended best practice for tables which works faster and reduces memory consumption.

Using this new method, tables are declared only once with var , as usual. Then, on bar zero only, we use table.cell() calls to populate the table.

Finally, table.set_*() functions are used to update attributes of table cells on the last bar of the dataset.

This greatly reduces the resources required to render tables. We encourage all Pine Script™ programmers to do the same.

Look first. Then leap.

█ FUNCTIONS

The library contains the following functions:

ltf(userSelection, choice1, choice2, choice3, choice4, choice5, choice6, choice7, choice8)

Selects a LTF from the chart's TF, depending on the `userSelection` input string.

Parameters:

userSelection : (simple string) User-selected input string which must be one of the `choicex` arguments.

choice1 : (simple string) Input selection corresponding to "Least precise, covering most chart bars".

choice2 : (simple string) Input selection corresponding to "Less precise, covering some chart bars".

choice3 : (simple string) Input selection corresponding to "More precise, covering less chart bars".

choice4 : (simple string) Input selection corresponding to "Most precise, 1min intrabars".

choice5 : (simple string) Input selection corresponding to "~12 intrabars per chart bar".

choice6 : (simple string) Input selection corresponding to "~24 intrabars per chart bar".

choice7 : (simple string) Input selection corresponding to "~50 intrabars per chart bar".

choice8 : (simple string) Input selection corresponding to "~100 intrabars per chart bar".

Returns: (simple string) A timeframe string to be used with `request.security_lower_tf()`.

ltfStats()

Returns statistics about analyzed intrabars and chart bars covered by calls to `request.security_lower_tf()`.

Parameters:

intrabarValues : (float [ ]) The ID of a float array containing values fetched by a call to `request.security_lower_tf()`.

Returns: A 3-element tuple: [ (series int) intrabarsInChartBar, (series int) chartBarsCovered, (series float) avgIntrabars ].

Correlation with Matrix TableCorrelation coefficient is a measure of the strength of the relationship between two values. It can be useful for market analysis, cryptocurrencies, forex and much more.

Since it "describes the degree to which two series tend to deviate from their moving average values" (1), first of all you have to set the length of these moving averages. You can also retrieve the values from another timeframe, and choose whether or not to ignore the gaps.

After selecting the reference ticker, which is not dependent from the chart you are on, you can choose up to eight other tickers to relate to it. The provided matrix table will then give you a deeper insight through all of the correlations between the chosen symbols.

Correlation values are scored on a scale from 1 to -1

A value of 1 means the correlation between the values is perfect.

A value of 0 means that there is no correlation at all.

A value of -1 indicates that the correlation is perfectly opposite.

For a better view at a glance, eight level colors are available and it is possible to modify them at will. You can even change level ranges by setting their threshold values. The background color of the matrix's cells will change accordingly to all of these choices.

The default threshold values, commonly used in statistics, are as follows:

None to weak correlation: 0 - 0.3

Weak to moderate correlation: 0.3 - 0.5

Moderate to high correlation: 0.5 - 0.7

High to perfect correlation: 0.7 - 1

Remember to be careful about spurious correlations, which are strong correlations without a real causal relationship.

(1) www.tradingview.com

Copy/Paste Levels Creator ToolThis indicator is for making levels to enter into the Copy/Paste Levels Indicator, This description will serve as a guide on how to use this tool to export levels for sharing!

Copy/Paste Levels Indicator:

Once you add this indicator to your chart it will pop up with a confirmation box for quick access to adding levels, You can see a snapshot of the settings UI on the left in the chart in this post.

If you want to just add the indicator to your chart press "apply" and you will be able to add levels by going into the settings for the indicator. Otherwise, Just fill out the settings and only check on the boxes you need (minimum 1).

All values are default, and the only boxes that need to be filled out are the Ticker and Lvls.

In the lvls box, insert your levels separated by commas(,) it is preferred that you do not have any spaces in the lvls box, however in the code, I have a piece to remove spaces from this box.

Now The Important Part!

As you may notice, this indicator does not display anything. Its main function is to export formatted text to be entered into the Copy/Paste Levels Indicator.

The way we do this is through email alerts .

After inputting levels to Export, Go to a live chart and set an alert for this indicator, check the box for "Email Alerts".

This will send the alert message to your email when it fires.

After the alert fires,

Check your email, you will have a message containing the formatted levels, ready to be copy and pasted into the other indicator!

How does the alert fire?

I have the alert function set to fire on every calculation of the indicator because of this,

This indicator will alert immediately , on any LIVE chart.

Note: After the alert fires, it is probably a good idea to immediately delete the alert, or else you will get an alert on ever candle with the same information you have already exported.

What if its after market and the chart is not ticking?

When making levels on off hours, remember to set the alert (for this indicator) on a live chart such as BTC.

Remember: The chart you are on does not have to be the one you are making levels for. This indicator is simple an interface.

Enjoy!

Stock Tech Bot One ViewTechnical indicators are not limited. Hence, here is another indicator with the combination of OBV, RSI, and MACD along with support, and resistance that follows the price while honoring the moving average of 200, 90 & 50.

The default lookback period of this indicator is 21 though it is changeable as per the user's desire.

The highest high and lowest low for the last 21 days lookback period proven to be the perfect Support & Resistance as the price of particular stock values are decided by market psychology. The support and resistance lines are very important to understand the market psychology which is very well proven with price action patterns and the lines are drawn based on,

Lower Extreme = 0.1 (Changeable)

Maximum Range = 21 days highest high - 21 days lowest low.

Support Line = 21 days lowest low + (Maximum Range * Lower Extreme)

Resistance Line = 21 days highest high - (Maximum Range * Lower Extreme)

RSI - Relative strength indicator is very famous to find the market momentum within the range of 0 - 100. Though the lookback period is changeable, the 14 days lookback period is the perfect match as the momentum of market movement for the last 3 weeks will always assist to identify the market regime. Here the momentum is just to highlight the indication (green up arrow under the candle for long and red down arrow above the candle for short) of market movement though it is not very important to consider if the price of the stock respect the support & resistance lines along with volume indicator (* = violet color).

OBV - Momentum:

The on-balance volume is always going indicator on any kind of tickers, which helps to identify the buying interest. Now, applying momentum on OBV with the positive movement for at least two consecutive days gives perfect confirmation for entry. A combination of the price along with this momentum(OBV) in the chart will help us to know the whipsaw in the price.

The Symbol "*" on top of each bar shows the market interest in that particular stock. If your ticker is fundamentally strong then you can see this "*" even when the market falls.

MACD:

One of the favorites and simple indicators widely used, where the thump of the rule is not to change the length even if it is allowed. It's OK to believe blindly in certain indicator and consider it while trading. That's why the indicator changes the bar color by following the MACD histogram.

Volume:

It may be the OBV works based on the open price and close price along with volume movement, it is wise to have the volume that is plotted along with price movement that should help you to decide whether the market is greedy or fearful.

The symbol "-" on top of each bar tells you a lot and don't ignore it.

Moving Average:

Moving average is a very good trend indicator as everyone considers seeing along with the price in the chart which is not omitted while we gauge the price movement alone with volume in this indicator. The 200, 90 & 50 MA's are everyone's favorite, and the same is plotted on the chart.

As explained above, the combination of all four indicators with price movement will give us very good confidence to take entry.

Candlestick Pattern:

You should admire the techniques of the candlestick pattern as you navigate the chart from right to left. Though there are a lot of patterns that exist, it is easy to enable and disable to view the signal as the label.

Further, last but not least, the exit always depends on individual conviction and how often the individual watch the price movement, if your conviction is strong then follow the down arrow red indication. If not, then exit with a trailing stop that indicates the bar with orange color.

Happy investing

Note: It is just a combination of multiple indicators and patterns to get one holistic view. So, the credit goes to all wise developers who publically published.

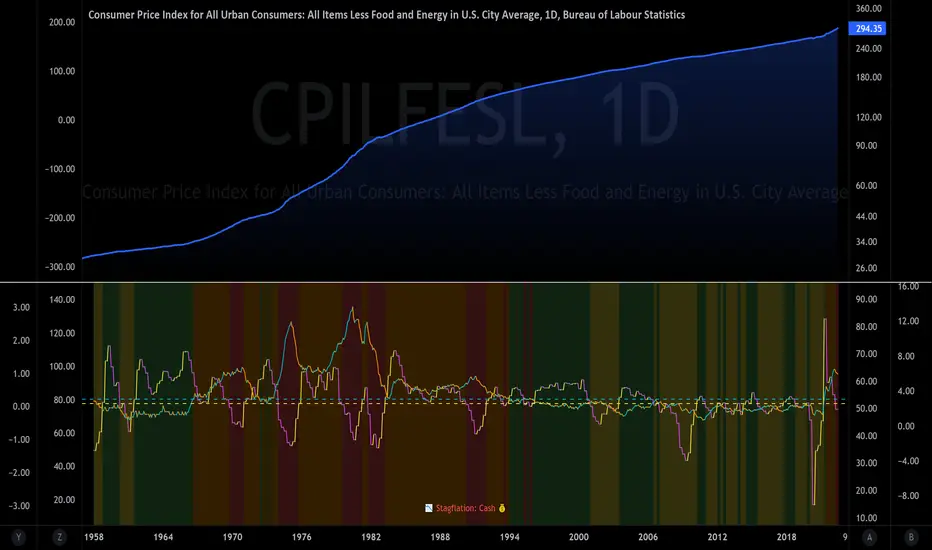

The Investment ClockThe Investment Clock was most likely introduced to the general public in a research paper distributed by Merrill Lynch. It’s a simple yet useful framework for understanding the various stages of the US economic cycle and which asset classes perform best in each stage.

The Investment Clock splits the business cycle into four phases, where each phase is comprised of the orientation of growth and inflation relative to their sustainable levels:

Reflation phase (6:01 to 8:59): Growth is sluggish and inflation is low. This phase occurs during the heart of a bear market. The economy is plagued by excess capacity and falling demand. This keeps commodity prices low and pulls down inflation. The yield curve steepens as the central bank lowers short-term rates in an attempt to stimulate growth and inflation. Bonds are the best asset class in this phase.

Recovery phase (9:01 to 11:59): The central bank’s easing takes effect and begins driving growth to above the trend rate. Though growth picks up, inflation remains low because there’s still excess capacity. Rising growth and low inflation are the Goldilocks phase of every cycle. Stocks are the best asset class in this phase.

Overheat phase(12:01 to 2:59): Productivity growth slows and the GDP gap closes causing the economy to bump up against supply constraints. This causes inflation to rise. Rising inflation spurs the central banks to hike rates. As a result, the yield curve begins flattening. With high growth and high inflation, stocks still perform but not as well as in recovery. Volatility returns as bond yields rise and stocks compete with higher yields for capital flows. In this phase, commodities are the best asset class.

Stagflation phase (3:01 to 5:59): GDP growth slows but inflation remains high (sidenote: most bear markets are preceded by a 100%+ increase in the price of oil which drives inflation up and causes central banks to tighten). Productivity dives and a wage-price spiral develops as companies raise prices to protect compressing margins. This goes on until there’s a steep rise in unemployment which breaks the cycle. Central banks keep rates high until they reign in inflation. This causes the yield curve to invert. During this phase, cash is the best asset.

Additional notes from Merrill Lynch:

Cyclicality: When growth is accelerating (12 o'clock), Stocks and Commodities do well. Cyclical sectors like Tech or Steel outperform. When growth is slowing (6 o'clock), Bonds, Cash, and defensives outperform.

Duration: When inflation is falling (9 o'clock), discount rates drop and financial assets do well. Investors pay up for long duration Growth stocks. When inflation is rising (3 o'clock), real assets like Commodities and Cash do best. Pricing power is plentiful and short-duration Value stocks outperform.

Interest Rate-Sensitives: Banks and Consumer Discretionary stocks are interest-rate sensitive “early cycle” performers, doing best in Reflation and Recovery when central banks are easing and growth is starting to recover.

Asset Plays: Some sectors are linked to the performance of an underlying asset. Insurance stocks and Investment Banks are often bond or equity price sensitive, doing well in the Reflation or Recovery phases. Mining stocks are metal price-sensitive, doing well during an Overheat.

About the indicator:

This indicator suggests iShares ETFs for sector rotation analysis. There are likely other ETFs to consider which have lower fees and are outperforming their sector peers.

You may get errors if your chart is set to a different timeframe & ticker other than 1d for symbol/tickers GDPC1 or CPILFESL.

Investment Clock settings are based on a "sustainable level" of growth and inflation, which are each slightly subjective depending on the economist and probably have changed since the last time this indicator was updated. Hence, the sustainable levels are customizable in the settings. When I was formally educated I was trained to use average CPI of 3.1% for financial planning purposes, the default for the indicator is 2.5%, and the Medium article backtested and optimized a 2% sustainable inflation rate. Again, user-defined sustainable growth and rates are slightly subjective and will affect results.

I have not been trained or even had much experience with MetaTrader code, which is how this indicator was originally coded. See the original Medium article that inspired this indicator if you want to audit & compare code.

Hover over info panel for detailed information.

Features: Advanced info panel that performs Investment Clock analysis and offers additional hover info such as sector rotation suggestions. Customizable sustainable levels, growth input, and inflation input. Phase background coloring.

⚠ DISCLAIMER: Not financial advice. Not a trading system. DYOR. I am not affiliated with Medium, Macro Ops, iShares, or Merrill Lynch.

About the Author: I am a patent-holding inventor, a futures trader, a hobby PineScripter, and a former FINRA Registered Representative.

Upvol and DownvolThis is a tweaked version of

What's Added?

- No negative graph lines (I want to see the crossovers in volume)

- Added NQ

- Adjusted enabled tickers (ES and the current ticker are enabled)

- Adjusted the moving average to better fit the strategy I was backtesting

How to use?

I watch it with other indicators for the cross over in positive delta/negative delta of the volume

- short volume crossing above long? consider going long

- long volume crossing below short consider going short

Also watching the total volume to see if it's going up or down (don't enter if it's dropping or consider getting out)

Historical US Bond Yield CurvePreface: I'm just the bartender serving today's freshly blended concoction; I'd like to send a massive THANK YOU to all the coders and PineWizards for the locally-sourced ingredients. I am simply a code editor, not a code author. Many thanks to these original authors!

Source 1 (Aug 8, 2019):

Source 2 (Aug 11, 2019):

About the Indicator: The term yield curve refers to the yields of U.S. treasury bills, notes, and bonds in order from shortest to longest maturity date. The yield curve describes the shapes of the term structures of interest rates and their respective terms to maturity in years. The slope of the yield curve tells us how the bond market expects short-term interest rates to move in the future based on bond traders' expectations about economic activity and inflation. The best use of the yield curve is to get a sense of the economy's direction rather than to try to make an exact prediction. This indicator plots the U.S. yield curve as maturity (x-axis/time) vs yield (y-axis/price) in addition to historical yield curves and advanced data tickers . The visual array of historical yield curves helps investors visualize shifts in the yield curve that are useful when identifying & forecasting economic conditions. The bond market can help predict the direction of the economy which can be useful in crafting your investment strategy. An inverted 10y/2y yield curve for durations longer than 5 consecutive trading days signals an almost certain recession on the horizon. An inversion happens when short-term bonds pay better than longer-term bonds. There is Federal Reserve Board data that suggests the 10y3m may be a better predictor of recessions.

Features: Advanced dual data ticker that performs curve & important spread analysis, plus additional hover info. Advanced yield curve data labels with additional hover info. Customizable historical curves and color theme.

‼ IMPORTANT: Hover over labels/tables for advanced information. Chart asset and timeframe may affect the yield curve results; I have found consistently accurate results using BINANCE:BTCUSDT on 1d timeframe. Historical curve lookbacks will have an effect on whether the curve analysis says the curve is bull/bear steepening/flattening, so please use appropriate lookbacks.

⚠ DISCLAIMER: Not financial advice. Not a trading system. DYOR. I am not affiliated with the original authors, TradingView, Binance, or the Federal Reserve Board.

About the Editor: I am a former FINRA Registered Representative, inventor/patent holder, futures trader, and hobby PineScripter.

Volume Value per UnitThis script will plot the result of Volume / Close.

This is meant to normalize the volume of tickers with exponential growth, for example a ticker like $BTC that went from $1 to $50k. Having the volume divided by the close will normalize the volume for when the price was $1 and $50k.

SPX Scalping StrategyThis strategy points out good entries and exits to go with the direction of SPY

Used with:

Ticker: SPX 500 USD

Heiken Ashi Candles

1, 3, 5 min timeframe

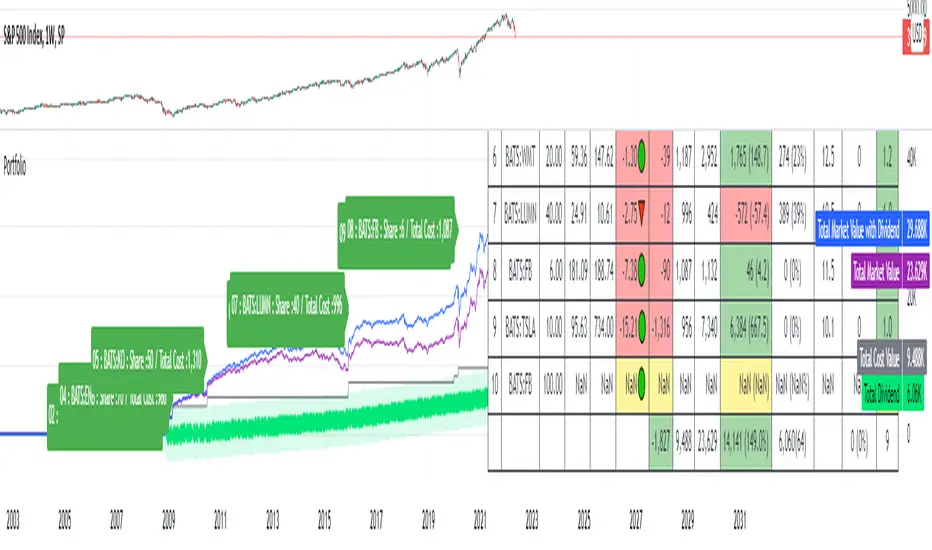

Portfolio SummaryThe stocks in my portfolio has very poor performance since the FED hiked the rate.

since the covid-19, i came to the stock market and buy a stock that i ever heard the name which i don't even know its fundamental.

Some stock, i bought them at the hilltop (and sell at the bottom, hehe).

Everyone is a genius in a bull market ; and now i realized i am gonna loss money.

I have to do something, so i looked for an indicator that allow me to manage my portfolio.

unfortunately, i cannot find one that fit me.

so i make this indicator.

How you can get the benefit from this indicator

This indicator will summarize the gain/loss since you bought the stock.

it also include the dividend.

So that you can see how much you gain and loss, and make a decision as you wish.

How to use it

1. Input some neccessary data like ticker/stock (up to 20 tickers, yeah i know, it is too much), share, average price which you can input manually or depend on your entry date.

2. The indicator will calculate gain/loss, dividend, % of your portfolio.

3. You can select how to display based on "Index" or "Market Value".

4. You can toggle on/off both label and table.

Disclaimer

This indicator may display inaccurate and need a lot of improvement.

pls use carefully.

if you have any suggestion, pls dont hersitate to comment below.

Enjoy.

Symbol ViewerView another symbol!

Symbol Viewer allows you to display a ticker of your choice in an indicator box below your current chart.

You no longer need to split your layout to view 2 (or more) tickers at the same time!

The data from your symbol of choice is accurately displayed and updated live.

Percentage Levels by TimeframePlots the positive and negative percentage levels from a selection of timeframes and sources for any ticker. You can use this within a pullback trading system. For example, if you historically look at the average pullback of large cap stocks and ETF's, you can use this indicator to plot the levels it could pullback to for an entry to go long. It can be used as potential targets when trading a ticker short. Another use for this is to backtest the set percentage targets using TradingView's bar replay feature to see how ETF's and large cap stocks have reacted at these levels. Note: This is intended to be used at timeframes equal to higher than the chart's as it may cause re-painting issues.

Currently percentage levels are statically set to 1, 3, 5, 10, 15, 20, 25, and 30% levels above and below the chosen source (open, high, low, close). You can also display the data based on timeframes from Daily (1D) all the way up to Yearly (12M)

*Not financial advice but in my opinion the current percentage levels set (see above) are best used for ETF's and Large Cap Stocks.

Jan 2

Release Notes: Added the ability to select the historical bars to look back when plotting levels

Jan 2

Release Notes: To get a better display or proper resolution on your charts, change the view settings to "Scale Price Chart Only"

Jan 2

Release Notes: To add % labels for this indicator on the price axis, change your chart settings to include "Indicator Name Label" & "Indicator Last Value". You can find this under the Label section after hitting the gear icon in the bottom right of your chart.

Jan 2

Release Notes: Added: Custom Line Plot Extension Settings. Ideally both values should be equal to display optimal extended lines. To return to a base setting: '1' = Historical Lookback & '0' = Offset Lines. Also note this is dependent on the timeframe you are viewing on the chart.

Jan 2

Release Notes: Removed indicator from example chart that was not needed.

Jan 2

Release Notes: Updated some comments in the Pine Script

Jan 2

Release Notes: Update: Added commentary and instructions in the indicator settings to address recommended line plot settings for Stocks/ETF's vs Futures

Jan 2

Release Notes: Changed title from "Calculation Method" to "Calculation Source"

Jan 4 2021

Normal use of security() dictates that it only be used at timeframes equal to or higher than the chart's as it may cause re-painting

Rolling CAGRCompound Annual Growth Rate

This indicator is the compound annual growth rate to be used on any ticker.

How to use

Add indicator to your chart

Specify a data source (default is the close for the selected ticker)

Specify how many trading days are in a year (252 for stocks & 365 for crypto)

Restrictions

This is only accurate on the daily timeframe. So to avoid confusion, I disabled the plotting of the CAGR on any timeframe other than daily

MAROC Fast/SlowNot sure if a similar indicator already exist, so I created my own. After creating this indicator, I realize it looks very similar to MACD. However, it strictly uses Hull moving average in its calculation for the lines.

MAROC is simply Moving Average Rate of Change. This is a trend-following indicator that calculates the rate of change on two Hull moving averages. By default it calculates the ROC on 60-period HMA (green and red) and 180-period HMA (blue and orange). The zero line represents the confirmation of change in trend. Above zero is up trend and below zero is down trend. Note the difference between the "trend reversal" and the "confirmation of a trend". I like to define trend reversal by the change in direction

The colored squares on the zero line has 4 colors that represents the overall trend. Here I include the slowdown of MAROC as the start of a trend.

- bright green = when both the slow and fast MA are trending up

- faded green = when slow MA trending up, but fast MA trending down

- faded red = when slow MA trending down, but fast MA trending up

- bright red = when both the slow MA and fast MA are trending down

Trend changes triangles are shown to signal the change in trend direction (trend reversal). Green and blue triangles are trend reversal to the upside. Red and orange triangles are trend reversal to the downside.

This indicator includes the option of displaying buy(long) and sell(short) signals that follows these rules. Use at your own discretion, as it may not apply well with your market or ticker.

- Long = Bright green square and either fast or slow MAROC changes trend direction to the upside

- Short = Bright red square and either fast or slow MAROC changes trend direction to the downside

Enjoy~! Please let me know if you find this useful and which market / ticker and timeframe you are using it on~ :)

All-Time High with Percentage Drops for ETF's and Large CapsPlots the percentage drop levels from the All-Time High of any ticker. You can use this within a pullback trading system. For example, if you historically look at the average pullback of large cap stocks and ETF's, you can use this indicator to plot the levels it could pullback to for an entry to go long. It can be used as potential targets when trading a ticker short. Another use for this is to backtest the set percentage targets using TradingView's bar replay feature to see how ETF's and large cap stocks have reacted at these levels.

Currently percentage levels are statically set to 1, 2, 3, 5, 7, 10, & 20% levels below the All-Time High.

*Not financial advice but in my opinion the current percentage levels set (see above) are best used for ETF's and Large Cap Stocks.