HTF Cross Breakout [CHE] HTF Cross Breakout — Detects higher timeframe close crossovers for breakout signals, anchors VWAP for trend validation, and flags continuations or traps with visual extensions for delta percent and stop levels.

Summary

This indicator spots moments when the current chart's close price crosses a higher timeframe close, marking potential breakouts only when the current bar shows directional strength. It anchors a volume-weighted average price line from the breakout point to track trend health, updating labels to show if the move continues or reverses into a trap. Extensions add a dotted line linking the breakout level to the current close with percent change display, plus a stop-loss marker at the VWAP end. Signals gain robustness from higher timeframe confirmation and anti-repainting options, reducing noise in live bars compared to simple crossover tools.

Motivation: Why this design?

Traders often face false breakouts from intrabar wiggles on lower timeframes, especially without higher timeframe alignment, leading to whipsaws in volatile sessions. This design uses higher timeframe close as a stable reference for crossover detection, combined with anchored volume weighting to gauge sustained momentum. It addresses these by enforcing bar confirmation and directional filters, providing clearer entry validation and risk points without overcomplicating the chart.

What’s different vs. standard approaches?

Reference baseline

Standard crossover indicators like moving average crosses operate solely on the chart timeframe, ignoring higher timeframe context and lacking volume anchoring.

Architecture differences

- Higher timeframe data pulls via security calls with optional repainting control for stability.

- Anchored VWAP resets at each signal, accumulating from the breakout bar only.

- Label dynamics update in real-time for continuation checks, with extensions for visual delta and stop computation.

- Event-driven line finalization prunes old elements after a set bar extension.

Practical effect

Charts show persistent lines and labels that extend live but finalize cleanly on new events, avoiding clutter. This matters for spotting trap reversals early via label color shifts, and extensions provide quick risk visuals without manual calculations, improving decision speed in trend trades.

How it works (technical)

The indicator first determines a higher timeframe based on user selection, pulling its close price securely. It checks for crossovers or crossunders of the current close against this higher close, but only triggers on confirmed bars with matching directional opens and closes. On a valid event, a horizontal line and label mark the higher close level, while a dashed VWAP line starts accumulating typical price times volume from that bar onward. During the active phase, the breakout line extends to the current bar, the label repositions and updates text based on whether the current close holds above or below the level for bulls or bears. A background tint warns if the close deviates adversely from the current VWAP. Extensions draw a vertical dotted line at the last bar between the breakout level and close, placing a midpoint label with percent difference; separately, a label at the VWAP end shows a computed stop price. Persistent variables track the active state and accumulators, resetting on new events after briefly extending old elements. Repaint risk from security calls is mitigated by confirmed bar gating or user opt-in.

Parameter Guide

Plateau Length (reserved for future, currently unused): Sets a length for potential plateau detection in extensions; default 3, minimum 1. Higher values would increase stability but are not active yet—leave at default to avoid tuning.

Line Width: Controls thickness of breakout, VWAP, and extension lines; default 2, range 1 to 5. Thicker lines improve visibility on busy charts but may obscure price action—use 1 for clean views, 3 or more for emphasis.

+Bars after next HTF event (finalize old, then delete): Extends old lines and labels by this many bars before deletion on new signals; default 20, minimum 0. Shorter extensions keep charts tidy but risk cutting visuals prematurely; longer aids review but builds clutter over time.

Evaluate label only on HTF close (prevents gray traps intrabar): When true, label updates wait for higher timeframe confirmation; default true. Enabling reduces intrabar flips for stabler signals, though it may delay feedback—disable for faster live trading at repaint cost.

Allow Repainting: Permits real-time security data without confirmation offset; default false. False ensures historical accuracy but lags live bars; true speeds updates but can repaint on HTF closes.

Timeframe Type: Chooses HTF method—Auto Timeframe (dynamic steps up), Multiplier (chart multiple), or Manual (fixed string); default Auto Timeframe. Auto adapts to chart scale for convenience; Multiplier suits custom scaling like 5 times current; Manual for precise like 1D on any chart.

Multiplier for Alternate Resolution: Scales chart timeframe when Multiplier type selected; default 5, minimum 1. Values near 1 mimic current resolution for subtle shifts; higher like 10 jumps to broader context, increasing signal rarity.

Manual Resolution: Direct timeframe string like 60 for 1H when Manual type; default 60. Match to trading horizon—shorter for swing, longer for positional—to balance frequency and reliability.

Show Extension 1: Toggles dotted line and delta percent label between breakout level and current close; default true. Disable to simplify for basic use, enable for precise momentum tracking.

Dotted Line Width: Thickness for Extension 1 line; default 2, range 1 to 5. Align with main Line Width for consistency.

Text Size: Size for delta percent label; options tiny, small, normal, large; default normal. Smaller reduces overlap on dense charts; larger aids glance reads.

Decimals for Δ%: Precision in percent change display; default 2, range 0 to 6. Fewer decimals speed reading; more suit low-volatility assets.

Positive Δ Color: Hue for upward percent changes; default lime. Choose contrasting for visibility.

Negative Δ Color: Hue for downward percent changes; default red. Pair with positive for quick polarity scan.

Dotted Line Color: Color for Extension 1 line; default gray. Neutral tones blend well; brighter for emphasis.

Background Transparency (0..100): Opacity for delta label background; default 90. Higher values fade for subtlety; lower solidifies for readability.

Show Extension 2: Toggles stop-loss label at VWAP end; default true. Turn off for entry focus only.

Stop Method: Percent from VWAP end or fixed ticks; options Percent, Ticks; default Percent. Percent scales with price levels; Ticks suits tick-based instruments.

Stop %: Distance as fraction of VWAP for Percent method; default 1.0, step 0.05, minimum 0.0. Tighter like 0.5 reduces risk but increases stops; wider like 2.0 allows breathing room.

Stop Ticks: Tick count offset for Ticks method; default 20, minimum 0. Adjust per asset volatility—fewer for tight control.

Price Decimals: Rounding for stop price text; default 4, range 0 to 10. Match syminfo.precision for clean display.

Text Size: Size for stop label; options tiny, small, normal, large; default normal. Scale to chart zoom.

Text Color: Foreground for stop text; default white. Ensure contrast with background.

Inherit VWAP Color (BG tint): Bases stop label background on VWAP hue; default true. True maintains theme; false allows custom black base.

BG Transparency (0..100): Opacity for stop label background; default 0. Zero for no tint; up to 100 for full fade.

Reading & Interpretation

Breakout lines appear green for bullish crosses or red for bearish, extending live until a new event finalizes them briefly then deletes. Labels start blank, updating to Bull Cont. or Bear Cont. in matching colors if holding the level, or gray Bull Trap/Bear Trap on reversal. VWAP dashes yellow for bulls, orange for bears, sloping with accumulated volume weight—deviations trigger faint red background warnings. Extension 1's dotted vertical shows at the last bar, with midpoint label green/red for positive/negative percent from breakout to close. Extension 2 places a left-aligned label at VWAP end with stop price and method note, tinted to VWAP for context.

Practical Workflows & Combinations

For trend following, enter long on green Bull Cont. labels above VWAP with higher highs confirmation, filtering via rising structure; short on red Bear Cont. below. Pair with volume surges or RSI above 50 for bulls to avoid traps. For exits, trail stops using the Extension 2 level, tightening on warnings or gray labels—aggressive on continuations, conservative post-trap. In multi-timeframe setups, use default Auto on 15m charts for 1H signals, scaling multiplier to 4 for daily context on hourly; test on forex/stocks where volume is reliable, avoiding low-liquidity assets.

Behavior, Constraints & Performance

Signals confirm on bar close with HTF gating when strict mode active, but live bars may update if repainting enabled—opt false for backtest fidelity, true for intraday speed. Security calls risk minor repaints on HTF closes, mitigated by confirmation offsets. Resources cap at 1000 bars back, 50 lines/labels total, with event prunes to stay under budgets—no loops, minimal arrays. Limits include VWAP lag in low-volume periods and dependency on accurate HTF data; gaps or holidays may skew anchors.

Sensible Defaults & Quick Tuning

Defaults suit 5m-1H charts on liquid assets: Auto HTF, no repaint, 1% stops. For choppy markets with excess signals, enable strict eval and bump multiplier to 10 for rarer triggers. If sluggish in trends, shorten extend bars to 10 and allow repainting for quicker visuals. On high-vol like crypto, widen stop % to 2.0 and use Ticks method; for stables like indices, tighten to 0.5% and keep Percent.

What this indicator is—and isn’t

This is a signal visualization layer for breakout confirmation and basic risk marking, best as a filter in discretionary setups. It isn’t a standalone system or predictive oracle—combine with price structure, news awareness, and sizing rules for real edges.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Pesquisar nos scripts por "文华财经tick价格"

BOCS Channel Scalper Indicator - Mean Reversion Alert System# BOCS Channel Scalper Indicator - Mean Reversion Alert System

## WHAT THIS INDICATOR DOES:

This is a mean reversion trading indicator that identifies consolidation channels through volatility analysis and generates alert signals when price enters entry zones near channel boundaries. **This indicator version is designed for manual trading with comprehensive alert functionality.** Unlike automated strategies, this tool sends notifications (via popup, email, SMS, or webhook) when trading opportunities occur, allowing you to manually review and execute trades. The system assumes price will revert to the channel mean, identifying scalp opportunities as price reaches extremes and preparing to bounce back toward center.

## INDICATOR VS STRATEGY - KEY DISTINCTION:

**This is an INDICATOR with alerts, not an automated strategy.** It does not execute trades automatically. Instead, it:

- Displays visual signals on your chart when entry conditions are met

- Sends customizable alerts to your device/email when opportunities arise

- Shows TP/SL levels for reference but does not place orders

- Requires you to manually enter and exit positions based on signals

- Works with all TradingView subscription levels (alerts included on all plans)

**For automated trading with backtesting**, use the strategy version. For manual control with notifications, use this indicator version.

## ALERT CAPABILITIES:

This indicator includes four distinct alert conditions that can be configured independently:

**1. New Channel Formation Alert**

- Triggers when a fresh BOCS channel is identified

- Message: "New BOCS channel formed - potential scalp setup ready"

- Use this to prepare for upcoming trading opportunities

**2. Long Scalp Entry Alert**

- Fires when price touches the long entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "LONG scalp signal at 24731.75 | TP: 24743.2 | SL: 24716.5"

**3. Short Scalp Entry Alert**

- Fires when price touches the short entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "SHORT scalp signal at 24747.50 | TP: 24735.0 | SL: 24762.75"

**4. Any Entry Signal Alert**

- Combined alert for both long and short entries

- Use this if you want a single alert stream for all opportunities

- Message: "BOCS Scalp Entry: at "

**Setting Up Alerts:**

1. Add indicator to chart and configure settings

2. Click the Alert (⏰) button in TradingView toolbar

3. Select "BOCS Channel Scalper" from condition dropdown

4. Choose desired alert type (Long, Short, Any, or Channel Formation)

5. Set "Once Per Bar Close" to avoid false signals during bar formation

6. Configure delivery method (popup, email, webhook for automation platforms)

7. Save alert - it will fire automatically when conditions are met

**Alert Message Placeholders:**

Alerts use TradingView's dynamic placeholder system:

- {{ticker}} = Symbol name (e.g., NQ1!)

- {{close}} = Current price at signal

- {{plot_1}} = Calculated take profit level

- {{plot_2}} = Calculated stop loss level

These placeholders populate automatically, creating detailed notification messages without manual configuration.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This indicator is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Indicator**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the indicator ideal for active day traders who want continuous alert opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased signal frequency also means higher potential commission costs and requires disciplined trade selection when acting on alerts.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The indicator normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The indicator uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The indicator tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The indicator uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. Visual markers (arrows and labels) appear on chart, and configured alerts fire immediately.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents alert spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long alert will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The indicator includes a multi-timeframe ATR filter to avoid alerts during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while viewing 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Alerts enabled

- If ATR < threshold: No alerts fire

This prevents notifications during dead zones where mean reversion is unreliable due to insufficient price movement. The ATR status is displayed in the info table with visual confirmation (✓ or ✗).

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. These levels are displayed as visual lines with labels and included in alert messages for reference when manually placing orders.

### Stop Loss Placement:

Stop losses are calculated just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. SL levels are displayed on chart and included in alert notifications as suggested stop placement.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

## INPUT PARAMETERS:

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long alert generation on/off

- **Enable Short Scalps**: Toggle short alert generation on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between alerts (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for alert enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time indicator status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Long Color**: Customize long signal color (default: darker green for readability)

- **Short Color**: Customize short signal color (default: red)

- **TP/SL Colors**: Customize take profit and stop loss line colors

- **Line Length**: Visual length of TP/SL reference lines (5-200 bars)

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short alerts

- **TP/SL reference lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing channel status, last signal, entry/TP/SL prices, risk/reward ratio, and ATR filter status

- **Visual confirmation** when alerts fire via on-chart markers synchronized with notifications

## HOW TO USE:

### For 1-3 Minute Scalping with Alerts (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars to reduce alert spam

- **Alert Setup**: Configure "Any Entry Signal" for combined long/short notifications

- **Execution**: When alert fires, verify chart visuals, then manually place limit order at entry zone with provided TP/SL levels

### For 5-15 Minute Day Trading with Alerts:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- **Alert Setup**: Configure separate "Long Scalp Entry" and "Short Scalp Entry" alerts if you trade directionally based on bias

- **Execution**: Review channel structure on alert, confirm ATR filter shows ✓, then enter manually

### For 30-60 Minute Swing Scalping with Alerts:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- **Alert Setup**: Use "New Channel Formation" to prepare for setups, then "Any Entry Signal" for execution alerts

- **Execution**: Larger timeframes allow more analysis time between alert and entry

### Webhook Integration for Semi-Automation:

- Configure alert webhook URL to connect with platforms like TradersPost, TradingView Paper Trading, or custom automation

- Alert message includes all necessary order parameters (direction, entry, TP, SL)

- Webhook receives structured data when signal fires

- External platform can auto-execute based on alert payload

- Still maintains manual oversight vs full strategy automation

## USAGE CONSIDERATIONS:

- **Manual Discipline Required**: Alerts provide opportunities but execution requires judgment. Not all alerts should be taken - consider market context, trend, and channel quality

- **Alert Timing**: Alerts fire on bar close by default. Ensure "Once Per Bar Close" is selected to avoid false signals during bar formation

- **Notification Delivery**: Mobile/email alerts may have 1-3 second delay. For immediate execution, use desktop popups or webhook automation

- **Cooldown Necessity**: Without cooldown, rapidly touching price action can generate excessive alerts. Start with 3-bar cooldown and adjust based on alert volume

- **ATR Filter Impact**: Enabling ATR filter dramatically reduces alert count but improves quality. Track filter status in info table to understand when you're receiving fewer alerts

- **Commission Awareness**: High alert frequency means high potential trade count. Calculate if your commission structure supports frequent scalping before acting on all alerts

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features are not included in this indicator version. Multi-timeframe ATR requires higher-tier TradingView subscription for request.security() functionality on timeframes below chart timeframe.

## KNOWN LIMITATIONS:

- **Indicator does not execute trades** - alerts are informational only; you must manually place all orders

- **Alert delivery depends on TradingView infrastructure** - delays or failures possible during platform issues

- **No position tracking** - indicator doesn't know if you're in a trade; you must manage open positions independently

- **TP/SL levels are reference only** - you must manually set these on your broker platform; they are not live orders

- **Immediate touch entry can generate many alerts** in choppy zones without adequate cooldown

- **Channel deletion at 10-tick breaks** may be too aggressive or lenient depending on instrument tick size

- **ATR filter from lower timeframes** requires TradingView Premium/Pro+ for request.security()

- **Mean reversion logic fails** in strong breakout scenarios - alerts will fire but trades may hit stops

- **No partial closing capability** - full position management is manual; you determine scaling out

- **Alerts do not account for gaps** or overnight price changes; morning alerts may be stale

## RISK DISCLOSURE:

Trading involves substantial risk of loss. This indicator provides signals for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Mean reversion strategies can experience extended drawdowns during trending markets. Alerts are not guaranteed to be profitable and should be combined with your own analysis. Stop losses may not fill at intended levels during extreme volatility or gaps. Never trade with capital you cannot afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Always verify alerts against current market conditions before executing trades manually.

## ACKNOWLEDGMENT & CREDITS:

This indicator is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based alert generation, comprehensive alert condition system with customizable notifications, multi-timeframe ATR volatility filtering, cooldown period for alert management, dual TP methods (fixed points vs channel percentage), visual TP/SL reference lines, and real-time status monitoring table. This indicator version is specifically designed for manual traders who prefer alert-based decision making over automated execution.

Support and Resistance levels from Options DataINTRODUCTION

This script is designed to visualize key support and resistance levels derived from options data on TradingView charts. It overlays lines, labels, and boxes to highlight levels such as Put Walls (gamma support), Call Walls (gamma resistance), Gamma Flip points, Vanna levels, and more.

These levels are intended to help traders identify potential areas of price magnetism, reversal, or breakout based on options market dynamics. All calculations and visualizations are based on user-provided data pasted into the input field, as Pine Script cannot directly fetch external options data due to platform limitations (explained below).

For convenience, my website allows users to interact with a bot that will generate the string for up to 30 tickers at once getting nearly real-time data on demand (data is cached for 15min). With the output string pasted into this indicator, it's a bliss to shuffle through your portfolio and see those levels for each ticker.

The script is open-source under TradingView's terms, allowing users to study, modify, and improve it. It draws inspiration from common options-derived metrics like gamma exposure and vanna, which are widely discussed in financial literature. No external code is copied without rights; all logic is original or based on standard mathematical formulas.

How the Options Levels Are Calculated

The levels displayed by this script are not computed within Pine Script itself—instead, they rely on pre-calculated values provided by the user (via a pasted data string). These values are derived from options chain data fetched from financial APIs (e.g., using libraries like yfinance in Python). Here's a step-by-step overview of how these levels are generally calculated externally before being input into the script:

Fetching Options Data:

Historical and current options chain data for a ticker (e.g., strikes, open interest, volume, implied volatility, expirations) is retrieved for near-term expirations (e.g., up to 90 days).

Current stock price is obtained from recent history.

Gamma Support (Put Wall) and Resistance (Call Wall):

Gamma Calculation: For each option, gamma (the rate of change of delta) is computed using the Black-Scholes formula:

gamma = N'(d1) / (S * sigma * sqrt(T))

where S is the stock price, K is the strike, T is time to expiration (in years), sigma is implied volatility, r is the risk-free rate (e.g., 0.0445), and N'(d1) is the normal probability density function.

Weighted gamma is multiplied by open interest and aggregated by strike.

The Put Wall is the strike below the current price with the highest weighted gamma from puts (acting as support).

The Call Wall is the strike above the current price with the highest weighted gamma from calls (acting as resistance).

Short-term versions focus on strikes closer to the money (e.g., within 10-15% of the price).

Gamma Flip Level:

Net dealer gamma exposure (GEX) is calculated across all strikes:

GEX = sum (gamma * OI * 100 * S^2 * sign * decay)

where sign is +1 for calls/-1 for puts, and decay is 1 / sqrt(T).

The flip point is the price where net GEX changes sign (from positive to negative or vice versa), interpolated between strikes.

Vanna Levels:

Vanna (sensitivity of delta to volatility) is calculated:

vanna = -N'(d1) * d2 / sigma

where d2 = d1 - sigma * sqrt(T).

Weighted by open interest, the highest positive and negative vanna strikes are identified.

Other Levels:

S1/R1: Significant strikes with high combined open interest and volume (80% OI + 20% volume), below/above price for support/resistance.

Implied Move: ATM implied volatility scaled by S * sigma * sqrt(d/365) (e.g., for 7 days).

Call/Put Ratio: Total call contracts divided by put contracts (OI + volume).

IV Percentage: Average ATM implied volatility.

Options Activity Level: Average contracts per unique strike, binned into levels (0-4).

Stop Loss: Dynamically set below the lowest support (e.g., Put Wall, Gamma Flip), adjusted by IV (tighter in low IV).

Fib Target: 1.618 extension from Put Wall to Call Wall range.

Previous day levels are stored for comparison (e.g., to detect Call Wall movement >2.5% for alerts).

Effect as Support and Resistance in Technical Trading

Options levels like gamma walls influence price action due to market maker hedging:

Put Wall (Gamma Support): High put gamma below price creates a "magnet" effect—market makers buy stock as price falls, providing support. Traders might look for bounces here as entry points for longs.

Call Wall (Gamma Resistance): High call gamma above price leads to selling pressure from hedging, acting as resistance. Rejections here could signal trims, sells or even shorts.

Gamma Flip: Where gamma exposure flips sign, often a volatility pivot—crossing it can accelerate moves (bullish above, bearish below).

Vanna Levels: Positive/negative vanna indicate volatility sensitivity; crosses may signal regime shifts.

Implied Move: Shows expected range; prices outside suggest overextension.

S1/R1 and Fib Target: Volume/OI clusters act as classic S/R; Fib extensions project upside targets post-breakout.

In trading, these are not guarantees—combine with TA (e.g., volume, trends). High activity levels imply stronger effects; low CP ratio suggests bearish sentiment. Alerts trigger on proximities/crosses for awareness, not advice.

Limitations of the TradingView Platform for Data Pulling

TradingView's Pine Script is sandboxed for security and performance:

No direct internet access or API calls (e.g., can't fetch yfinance data in-script).

Limited to chart data/symbol info; no real-time options chains.

Inputs are static per load; updates require manual pasting.

Caching isn't persistent across sessions.

This prevents dynamic data pulling, ensuring scripts remain lightweight but requiring external tools for fresh data.

Creative Solution for On-Demand Data Pulling

To overcome these limitations, users can use external tools or scripts (e.g., Python-based) to fetch and compute levels on demand. The tool processes tickers, generates a formatted string (e.g., "TICKER:level1,level2,...;TIMESTAMP:unix;"), and users paste it into the script's input. This keeps data fresh without violating platform rules, as computation happens off-platform. For example, run a local script to query APIs and output the string—adaptable for any ticker.

Script Functionality Breakdown

Inputs: Custom data string (parsed for levels/timestamp); toggles for short-term/previous/Vanna/stop loss; style options (colors, transparency).

Parsing: Extracts levels for the chart symbol; gets timestamp for "updated ago" display.

Drawing: Lines/labels for levels; boxes for gamma zones/implied move; clears old elements on updates.

Info Panel: Top-right summary with metrics (CP ratio, IV, distances, activity); emojis for quick status.

Alerts: Conditions for proximities, crosses, bounces (e.g., 0.5% bounce from Put Wall).

Performance: Uses vars for persistence; efficient for real-time.

This script is educational—test thoroughly. Not financial advice; past performance isn't indicative of future results. Feedback welcome via TradingView comments.

TREV Candles - Range-Based Trend ReversalTREV Candles - Range-Based Trend Reversal Chart Implementation

What is a Trend Reversal (TREV) Chart?

A Trend Reversal chart, also known as a Point & Figure chart variation, is a unique charting method that focuses on price movement thresholds rather than time intervals. Unlike traditional candlestick charts where each candle represents a fixed time period, TREV candles form only when price moves by predefined amounts in ticks.

TREV charts eliminate time-based noise and focus purely on significant price movements, making them ideal for identifying genuine trend changes and continuation patterns.

How TREV Candles Work

This indicator implements true TREV logic with two critical thresholds:

Trend Size: The number of ticks price must move in the current direction to form a trend continuation candle

Reversal Size: The number of ticks price must move against the current direction to form a reversal candle and change the overall trend direction

Key TREV Rules Enforced:

Direction Changes Only Through Reversals: You cannot go from bullish trend directly to bearish trend - a reversal candle must occur first

Threshold-Based Formation: Candles form only when price thresholds are breached, not on time

Logical Wick Placement: Wicks only appear on the "open" side of candles where price temporarily moved against the formation direction

Multiple Candles Per Bar: When price moves significantly, several TREV candles can form within a single time-based bar

Four Distinct Candle Types

Bullish Trend (Green): Continues upward movement when trend threshold is hit

Bearish Trend (Red): Continues downward movement when trend threshold is hit

Bullish Reversal (Blue): Changes from bearish to bullish direction when reversal threshold is breached

Bearish Reversal (Orange): Changes from bullish to bearish direction when reversal threshold is breached

Practical Trading Applications

Trend Identification: Clear visual representation of when trends are continuing vs. reversing

Noise Reduction: Filters out insignificant price movements that don't meet threshold requirements

Support/Resistance: TREV levels often act as significant support and resistance zones

Breakout Confirmation: When price forms multiple trend candles in succession, it confirms strong directional movement

Reversal Signals: Reversal candles provide early warning of potential trend changes

Technical Implementation Features

Intelligent Price Path Processing: Analyzes the assumed price path within each bar (Low→High→Close for bullish bars, High→Low→Close for bearish bars)

Automatic Tick Size Detection: Works with any instrument by automatically detecting the correct tick size

Manual Override Option: Allows manual tick size specification for custom analysis

Impossible Scenario Prevention: Built-in logic prevents impossible wick configurations and direction changes

PineScript Optimization: Efficient state management and drawing limits handling for smooth performance

Comprehensive Styling Options

Each of the four candle types offers complete visual customization:

Body Colors: Independent color settings for each candle type's body

Border Colors: Separate border color customization

Border Styles: Choose from solid, dashed, or dotted borders

Wick Colors: Individual wick color settings for each candle type

Default Color Scheme:

🟢 Bullish Trend: Green body and wicks

🔵 Bullish Reversal: Blue body and wicks

🔴 Bearish Trend: Red body and wicks

🟠 Bearish Reversal: Orange body and wicks

Configuration Guidelines

Trend Size: Larger values create fewer, more significant trend candles. Smaller values increase sensitivity

Reversal Size: Should typically be smaller than trend size. Controls how easily the trend direction can change

Tick Size: Use "auto" for most instruments. Manual override useful for custom point values or backtesting

Ideal Use Cases

Swing Trading: Identify major trend changes and continuation patterns

Scalping: Use smaller thresholds to catch quick reversals and momentum shifts

Position Trading: Use larger thresholds to filter noise and focus on major trend moves

Multi-Timeframe Analysis: Compare TREV patterns across different threshold settings

Support/Resistance Trading: TREV close levels often become significant price zones

Why This Implementation is Superior

True TREV Logic: Enforces proper trend reversal rules that many implementations ignore

No Impossible Scenarios: Prevents wicks on both sides of candles and impossible direction changes

Professional Visualization: Clean, customizable appearance suitable for serious analysis

Performance Optimized: Handles large datasets without lag or drawing limit issues

Educational Value: Helps traders understand the difference between time-based and threshold-based charting

Perfect for traders who want to see beyond time-based noise and focus on what price is actually doing - moving in significant, measurable amounts that matter for trading decisions.

Volume Stack US Top 40 [Pt]█ Overview

Volume Stack US Top 40 is a versatile TradingView indicator designed to give you an at-a-glance view of market sentiment and volume dynamics across the top 40 U.S. large-cap stocks. Inspired by the popular Saty Volume Stack, this enhanced version aggregates essential volume and price strength data from major tickers on both the NYSE and NASDAQ, and works seamlessly on all timeframes.

█ Key Features

Dynamic Buy / Sell Volume Stack: This indicator dynamically stacks the volume bars so that the side with higher volume appears on top. For example, green over red signals more buy-side volume, while red over green indicates greater sell-side volume.

Cross-Market Analysis: Easily toggle between NYSE and NASDAQ to analyze the most influential U.S. stocks. The indicator automatically loads the correct set of tickers based on your selection.

Flexible Coverage: Choose from Top 10, Top 20, Top 30, or Top 40 tickers to tailor the tool to your desired scope of analysis.

Dynamic Table Display: A neat on-chart table lists the selected ticker symbols along with visual cues that reflect each stock’s strength. You can even remove exchange prefixes for a cleaner look.

█ Inputs & Settings

Market Selector: Choose whether to view data from the NYSE or NASDAQ; the indicator automatically loads the corresponding list of top tickers.

Number of Tickers: Select from ‘Top 10’, ‘Top 20’, ‘Top 30’, or ‘Top 40’ stocks to define the breadth of your analysis.

Color Options: Customize the colors for bullish and bearish histogram bars to suit your personal style.

Table Preferences: Adjust the on-chart table’s display style (grid or one row), text size, and decide whether to show exchange information alongside ticker symbols.

█ Usage & Benefits

Volume Stack US Top 40 is ideal for traders and investors who need a clear yet powerful tool to gauge overall market strength. By combining volume and price action data across multiple major stocks, it helps you:

Quickly assess whether the market sentiment is bullish or bearish.

Confirm trends by comparing volume patterns against intraday price movements.

Enhance your trading decisions with a visual representation of market breadth and dynamic buy/sell volume stacking.

Its intuitive design means you spend less time adjusting complex settings and more time making confident, informed decisions.

ICT Power Of Three | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ICT Power Of Three Indicator! This indicator is built around the ICT's "Power Of Three" strategy. This strategy makes use of these 3 key smart money concepts : Accumulation, Manipulation and Distribution. Each step is explained in detail within this write-up. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new ICT Power Of Three Indicator :

Implementation of ICT's Power Of Three Strategy

Different Algorithm Modes

Customizable Execution Settings

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

The "Power Of Three" comes from these three keywords "Accumulation, Manipulation and Distribution". Here is a brief explanation of each keyword :

Accumulation -> Accumulation phase is when the smart money accumulate their positions in a fixed range. This phase indicates price stability, generally meaning that the price constantly switches between up & down trend between a low and a high pivot point. When the indicator detects an accumulation zone, the Power Of Three strategy begins.

Manipulation -> When the smart money needs to increase their position sizes, they need retail traders' positions for liquidity. So, they manipulate the market into the opposite direction of their intended direction. This will result in retail traders opening positions the way that the smart money intended them to do, creating liquidity. After this step, the real move that the smart money intended begins.

Distribution -> This is when the real intention of the smart money comes into action. With the new liquidity thanks to the manipulation phase, the smart money add their positions towards the opposite direction of the retail mindset. The purpose of this indicator is to detect the accumulation and manipulation phases, and help the trader move towards the same direction as the smart money for their trades.

Detection Methods Of The Indicator :

Accumulation -> The indicator detects accumulation zones as explained step-by-step :

1. Draw two lines from the lowest point and the highest point of the latest X bars.

2. If the (high line - low line) is lower than Average True Range (ATR) * accumulationConstant

3. After the condition is validated, an accumulation zone is detected. The accumulation zone will be invalidated and manipulation phase will begin when the range is broken.

Manipulation -> If the accumulation range is broken, check if the current bar closes / wicks above the (high line + ATR * manipulationConstant) or below the (low line - ATR * manipulationConstant). If the condition is met, the indicator detects a manipulation zone.

Distribution -> The purpose of this indicator is to try to foresee the distribution zone, so instead of a detection, after the manipulation zone is detected the indicator automatically create a "shadow" distribution zone towards the opposite direction of the freshly detected manipulation zone. This shadow distribution zone comes with a take-profit and stop-loss layout, customizable by the trader in the settings.

The X bars, accumulationConstant and manipulationConstant are subject to change with the "Algorithm Mode" setting. Read the "Settings" section for more information.

This indicator follows these steps and inform you step by step by plotting them in your chart.

🚩UNIQUENESS

This indicator is an all-in-one suite for the ICT's Power Of Three concept. It's capable of plotting the strategy, giving signals, a backtesting dashboard and alerts feature. Different and customizable algorithm modes will help the trader fine-tune the indicator for the asset they are currently trading. The backtesting dashboard allows you to see how your settings perform in the current ticker. You can also set up alerts to get informed when the strategy is executable for different tickers.

⚙️SETTINGS

1. General Configuration

Algorithm Mode -> The indicator offers 3 different detection algorithm modes according to your needs. Here is the explanation of each mode.

a) Small Manipulation

This mode has the default bar length for the accumulation detection, but a lower manipulation constant, meaning that slighter imbalances in the price action can be detected as manipulation. This setting can be useful on tickers that have lower liquidity, thus can be manipulated easier.

b) Big Manipulation

This mode has the default bar length for the accumulation detection, but a higher manipulation constant, meaning that heavier imbalances on the price action are required in order to detect manipulation zones. This setting can be useful on tickers that have higher liquidity, thus can be manipulated harder.

c) Short Accumulation

This mode has a ~70% lower bar length requirement for accumulation zone detection, and the default manipulation constant. This setting can be useful on tickers that are highly volatile and do not enter accumulation phases too often.

Breakout Method -> If "Close" is selected, bar close price will be taken into calculation when Accumulation & Manipulation zone invalidation. If "Wick" is selected, a wick will be enough to validate the corresponding zone.

2. TP / SL

TP / SL Method -> If "Fixed" is selected, you can adjust the TP / SL ratios from the settings below. If "Dynamic" is selected, the TP / SL zones will be auto-determined by the algorithm.

Risk -> The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails. This setting is has a crucial effect on the performance of the indicator, as different tickers may have different volatility so the indicator may have increased performance when this setting is correctly adjusted.

3. Visuals

Show Zones -> Enables / Disables rendering of Accumulation (yellow) and Manipulation (red) zones.

4H RangeThis script visualizes certain key values based on a 4-hour timeframe of the selected market on the chart. These values include the High, Mid, and Low price levels during each 4-hour period.

These levels can be helpful to identify inside range price action, chop, and consolidation. They can sometimes act as pivots and can be a great reference for potential entries and exits if price continues to hold the same range.

Here's a step-by-step overview of what this indicator does:

1. Inputs: At the beginning of the script, users are allowed to customize some inputs:

Choose the color of lines and labels.

Decide whether to show labels on the chart.

Choose the size of labels ("tiny", "small", "normal", or "large").

Choose whether to display price values in labels.

Set the number of bars to offset the labels to the right.

Set a threshold for the number of ticks that triggers a new calculation of high, mid, and low values.

* Tick settings may need to be increased on equity charts as one tick is usually equal to one cent.

For example, if you want to clear the range when there is a close one point/one dollar above or below the range high/low then on ES

that would be 4 ticks but one whole point on AAPL would be 100 ticks. 100 ticks on an equity chart may or may not be ideal due to

different % change of 100 ticks might be too excessive depending on the price per share.

So be aware that user preferred thresholds can vary greatly depending on which chart you're using.

2. Retrieving Price Data: The script retrieves the high, low, and closing price for every 4-hour period for the current market.

The script also calculates the mid-price of each 4-hour period (the average of the high and low prices).

3. Line Drawing: At the start of the script (first run), it draws three lines (high, mid, and low) at the levels corresponding to the high,

mid, and low prices. Users can also change transparency settings on historical lines to view them. Default setting for historical lines

is for them to be hidden.

4. Updating Lines and Labels: For each subsequent 4-hour period, the script checks whether the close price of the period has gone

beyond a certain threshold (set by user input) above the previous high or below the previous low. If it has, the script deletes the

previous lines and labels, draws new lines at the new high, mid, and low levels, and creates new labels (if the user has opted to

show labels).

5. Displaying Values in the Data Window: In addition to the visual representation on the chart, the script also plots the high, mid, and

low prices. These plotted values appear in the Data Window of TradingView, allowing users to see the exact price levels even when

they're not directly labeled on the chart.

6. Updating Lines and Labels Position: At the end of each period, the script moves the lines and labels (if they're shown) to the right,

keeping them aligned with the current period.

Please note: This script operates based on a 4-hour timeframe, regardless of the timeframe selected on the chart. If a shorter timeframe is selected on the chart, the lines and labels will appear to extend across multiple bars because they represent 4-hour price levels. If a longer timeframe is selected, the lines and labels may not accurately represent high, mid, and low levels within that longer timeframe.

Multi Yield CurveAn inversion between the 2 year and 10 year US treasury yield generally means a recession within 2 years. But the yield curve has more to it than that. This script helps analysis of the current and past yield curve (not limited to US treasury) and is very configurable.

"A yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity." (Investopedia)

When the slope is upward (longer maturity bonds have a higher interest rate than shorter maturity bonds), it generally means the economy is doing well and is expanding. When the slope is downward it generally means that there is more downside risk in the future.

The more inverted the curve is, and the more the inversion moves to the front, the more market participants are hedging against downside risk in the future.

The script draws up to 4 moments of a yield curve, which makes it easy to compare the current yield curve with past yield curves. It also draws lines in red when that part of the curve is inverted.

The script draws the lines with proper length between maturity (which most scripts do not) in order to make it more representative of the real maturity duration. The width cannot be scaled because TradingView does not allow drawing based on pixels.

This script is the only free script at time of writing with proper lengths, showing multiple yield curves, and being able to show yield curves other than the US treasury.

█ CONFIGURATION

(The following can be configured by clicking "Settings" when the script is added to a chart)

By default the script is configured to show the US treasury (government bond) yields of all maturities, but it can be configured for any yield curve.

A ticker represents yield data for a specific maturity of a bond.

To configure different tickers, go to the "TICKERS" section. Tickers in this section must be ordered from low maturity to high maturity.

• Enable: draw the ticker on the chart.

• Ticker: ticker symbol on TradingView to fetch data for.

• Months: amount of months of bond maturity the ticker represents.

To configure general settings, go to the "GENERAL" section.

• Period: used for calculating how far back to look for data for past yield curve lines. See "Times back" further in this description for more info.

• Min spacing: minimum amount of spacing between labels. Depending on the size of the screen, value labels can overlap. This setting sets how much empty space there must be between labels.

• Value format: how the value at that part of the line should be written on the label. For example, 0.000 means the value will have 3 digits precision.

To configure line settings per yield curve, each has its own "LINE" section with the line number after it.

• Enable: whether to enable drawing of this line.

• Times back: how many times period to go back in time. When period is D, and times value is 2, the line will be of data from 2 days ago.

• Color: color of the line when not inverted.

• Style: style of the line. Possible values: sol, dsh, dot

• Inversion color: color of the line when the curve inverses between the two maturities at that part of the curve.

• Thickness: thickness of the line in pixels.

• Labels: whether to draw value labels above the line. By default, this is only enabled for the first line.

• Label text color: text color of value label.

• Label background color: background color of value label.

To configure the durations axis at the bottom of the chart, go to the "DURATIONS" section.

• Durations: whether to show maturity term duration labels below the chart.

• Offset: amount to offset durations label to be below chart.

█ MISC

Script originally inspired by the US Treasury Yield Curve script by @longfiat but has been completely rewritten and changed.

Multi Asset + Correlation OverlayFrom time to time, you may want to overlay multiple assets on the same chart instead of using multi-chart views. This can be a much cleaner way of viewing and comparing multiple assets. There is some functionality built into TradingView that lets you do this to a certain extent, but I wanted additional options, correlation labeling and ways to adjust the overlay location. So, today I am releasing to the community my Multi-Asset + Correlation Overlay script / indicator.

What is does: This script allows you to overlay the price of any ticker onto your chart. It also labels the line with the ticker name, and calculates / labels the correlation coefficient of your newly overlayed asset.

How to use it: Add the indicator to your chart. Then, go into the indicator settings to set the ticker of the asset you want to pull in along with how you want to "offset" it. Your 2 tickers may not be priced near each-other, so the offset setting allows you to pull the ticker you added up/down to better visually align with your chart's price range/layout. For instance, if the asset you added is priced $400 higher than the underlying chart price, you may want to set the offset to -400.

If you would like to add multiple tickers and multiple overlays, you can do that by just adding the indicator to your chart more than once. The color is adjustable, and the ticker of the asset will print to the right of the line representing the asset price. The script also calculates the correlation coefficient between the ticker overlay and the underlying chart asset. The correlation coefficient prints to the right of the ticker.

Crypto Volume/Strength ComparatorHello Traders,

Here is an attempt to perform comparative analysis between top cryptos based on strength (oscillator) and volume. Methodology used here is similar to Magic Number formula described in the post : Enhanced Magic Formula for fundamental analysis . But, instead of using fundamentals, we are making use of few technicals to derive similar outcome. Usage of the available stats will not be same as Magic number since we are using technicals.

⬜ Process

▶ Get crypto exchange based on prefix of instrument being used.

▶ For the given exchange, get data for all the tickers available in input fields.

▶ Calculate Oscillator, Momentum based on price for each tickers.

▶ Calculate Oscillator, Momentum based on volume for each tickers.

▶ Calculate Volatility for each tickers.

▶ Rank Price-Oscillator, Price-Momentum, Volume-Oscillator, Volume-Momentum, Volatility for each tickers.

▶ Calculate combined rank by adding up individual ranks.

▶ Calculate movement of rankings from bar to bar

▶ Sort tickers based on rank and populate them on table. Display direction of rankings.

⬜ Components

Display components are as follows:

⬜ Settings

Settings are pretty simple and straightforward

⬜ Calculations

▶ Oscillators : High values of oscillators are considered as ideal as the process is intended towards finding trend.

▶ Momentum : Momentum is calculated on the basis of Squeeze Momentum Indicator by @LazyBear.

▶ Volatility : Volatility is calculated on the basis of Williams Vix Fix by @ChrisMoody. Here too since we are in trend following mode, lower vix fix is considered ideal.

⬜ Few Notes

Tickers will show data only if selected exchange has them. Some tickers are not available in all exchanges. In that case, it will show NAN. This is kind of unavoidable as we need to have fixed size arrays for any calculations.

Indicator works only on crypto tickers which has valid exchange.

Tickers move through the rankings in real time. Background of all stats are based on gradient from green to red.

Tickers on top may not always have better long opportunity or tickers at bottom may not always be optimal for shorting. We need to consider how long the instrument may stay in the position or how fast it is moving in opposite direction. Hence, directions of the ranking movement are also shown on the table.

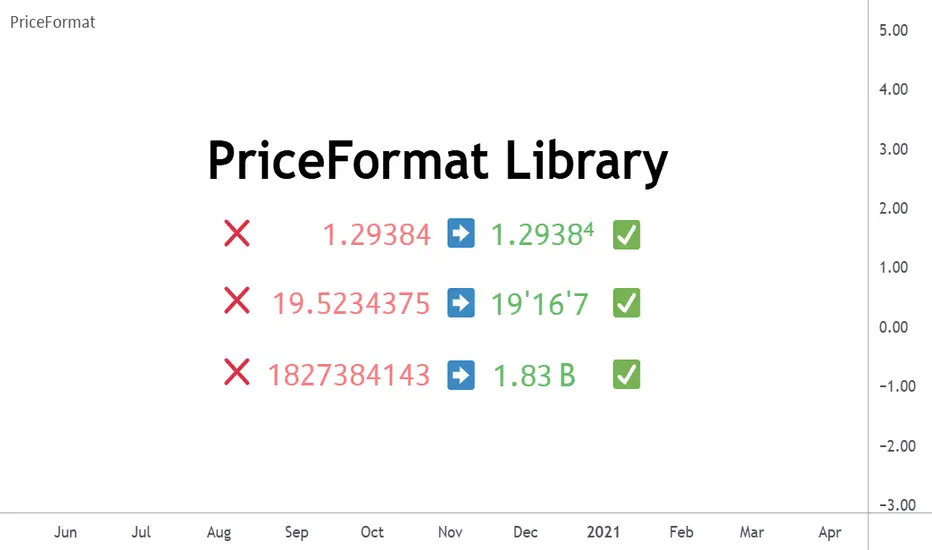

PriceFormatLibrary for automatically converting price values to formatted strings

matching the same format that TradingView uses to display open/high/low/close prices on the chart.

█ OVERVIEW

This library is intended for Pine Coders who are authors of scripts that display numbers onto a user's charts. Typically, 𝚜𝚝𝚛.𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐() would be used to convert a number into a string which can be displayed in a label / box / table, but this only works well for values that are formatted as a simple decimal number. The purpose of this library is to provide an easy way to create a formatted string for values which use other types of formats besides the decimal format.

The main functions exported by this library are:

𝚏𝚘𝚛𝚖𝚊𝚝𝙿𝚛𝚒𝚌𝚎() - creates a formatted string from a price value

𝚖𝚎𝚊𝚜𝚞𝚛𝚎𝙿𝚛𝚒𝚌𝚎𝙲𝚑𝚊𝚗𝚐𝚎() - creates a formatted string from the distance between two prices

𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐() - an alternative to the built-in 𝚜𝚝𝚛.𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐(𝚟𝚊𝚕𝚞𝚎, 𝚏𝚘𝚛𝚖𝚊𝚝)

This library also exports some auxiliary functions which are used under the hood of the previously mentioned functions, but can also be useful to Pine Coders that need fine-tuned control for customized formatting of numeric values:

Functions that determine information about the current chart:

𝚒𝚜𝙵𝚛𝚊𝚌𝚝𝚒𝚘𝚗𝚊𝚕𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝚅𝚘𝚕𝚞𝚖𝚎𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝙿𝚎𝚛𝚌𝚎𝚗𝚝𝚊𝚐𝚎𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝙳𝚎𝚌𝚒𝚖𝚊𝚕𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝙿𝚒𝚙𝚜𝙵𝚘𝚛𝚖𝚊𝚝()

Functions that convert a 𝚏𝚕𝚘𝚊𝚝 value to a formatted string:

𝚊𝚜𝙳𝚎𝚌𝚒𝚖𝚊𝚕(), 𝚊𝚜𝙿𝚒𝚙𝚜(), 𝚊𝚜𝙵𝚛𝚊𝚌𝚝𝚒𝚘𝚗𝚊𝚕(), 𝚊𝚜𝚅𝚘𝚕𝚞𝚖𝚎()

█ EXAMPLES

• Simple Example

This example shows the simplest way to utilize this library.

//@version=6

indicator("Simple Example")

import n00btraders/PriceFormat/1

var table t = table.new(position.middle_right, 2, 1, bgcolor = color.new(color.blue, 90), force_overlay = true)

if barstate.isfirst

table.cell(t, 0, 0, "Current Price: ", text_color = color.black, text_size = 40)

table.cell(t, 1, 0, text_color = color.blue, text_size = 40)

if barstate.islast

string lastPrice = close.formatPrice() // Simple, easy way to format price

table.cell_set_text(t, 1, 0, lastPrice)

• Complex Example

This example calls all of the main functions and uses their optional arguments.

//@version=6

indicator("Complex Example")

import n00btraders/PriceFormat/1

// Enum values that can be used as optional arguments

precision = input.enum(PriceFormat.Precision.DEFAULT)

language = input.enum(PriceFormat.Language.ENGLISH)

// Main library functions used to create formatted strings

string formattedOpen = open.formatPrice(precision, language, allowPips = true)

string rawOpenPrice = PriceFormat.tostring(open, format.price)

string formattedClose = close.formatPrice(precision, language, allowPips = true)

string rawClosePrice = PriceFormat.tostring(close, format.price)

= PriceFormat.measurePriceChange(open, close, precision, language, allowPips = true)

// Labels to display formatted values on chart

string prices = str.format("Open: {0} ({1})\n\nClose: {2} ({3})", formattedOpen, rawOpenPrice, formattedClose, rawClosePrice)

string change = str.format("Change (close - open):\n\n{0} / {1}", distance, ticks)

label.new(chart.point.now(high), prices, yloc = yloc.abovebar, textalign = text.align_left, force_overlay = true)

label.new(chart.point.now(low), change, yloc = yloc.belowbar, style = label.style_label_up, force_overlay = true)

█ NOTES

• Function Descriptions

The library source code uses Markdown for the exported functions. Hover over a function/method call in the Pine Editor to display formatted, detailed information about the function/method.

• Precision Settings

The Precision option in the chart settings can change the format of how prices are displayed on the chart. Since the user's selected choice cannot be known through any Pine built-in variable, this library provides a 𝙿𝚛𝚎𝚌𝚒𝚜𝚒𝚘𝚗 enum that can be used as an optional script input for the user to specify their selected choice.

• Language Settings

The Language option in the user menu can change the decimal/grouping separators in the prices that are displayed on the chart. Since the user's selected choice cannot be known through any Pine built-in variable, this library provides a 𝙻𝚊𝚗𝚐𝚞𝚊𝚐𝚎 enum that can be used as an optional script input for the user to specify their selected choice.

█ EXPORTED FUNCTIONS

method formatPrice(price, precision, language, allowPips)

Formats a price value to match how it would be displayed on the user's current chart.

Namespace types: series float, simple float, input float, const float

Parameters:

price (float) : The value to format.

precision (series Precision) : A Precision.* enum value.

language (series Language) : A Language.* enum value.

allowPips (simple bool) : Whether to allow decimal numbers to display as pips.

Returns: Automatically formatted price string.

measurePriceChange(startPrice, endPrice, precision, language, allowPips)

Measures a change in price in terms of both distance and ticks.

Parameters:

startPrice (float) : The starting price.

endPrice (float) : The ending price.

precision (series Precision) : A Precision.* enum value.

language (series Language) : A Language.* enum value.

allowPips (simple bool) : Whether to allow decimal numbers to display as pips.

Returns: A tuple of formatted strings: .

method tostring(value, format)

Alternative to the Pine `str.tostring(value, format)` built-in function.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : (series float) The value to format.

format (string) : (series string) The format string.

Returns: String in the specified format.

isFractionalFormat()

Determines if the default behavior of the chart's price scale is to use a fractional format.

Returns: True if the chart can display prices in fractional format.

isVolumeFormat()

Determines if the default behavior of the chart's price scale is to display prices as volume.

Returns: True if the chart can display prices as volume.

isPercentageFormat()

Determines if the default behavior of the chart's price scale is to display percentages.

Returns: True if the chart can display prices as percentages.

isDecimalFormat()

Determines if the default behavior of the chart's price scale is to use a decimal format.

Returns: True if the chart can display prices in decimal format.

isPipsFormat()

Determines if the current symbol's prices can be displayed as pips.

Returns: True if the chart can display prices as pips.

method asDecimal(value, precision, minTick, decimalSeparator, groupingSeparator, eNotation)

Converts a number to a string in decimal format.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

precision (int) : Number of decimal places.

minTick (float) : Minimum tick size.

decimalSeparator (string) : The decimal separator.

groupingSeparator (string) : The thousands separator, aka digit group separator.

eNotation (bool) : Whether the result should use E notation.

Returns: String in decimal format.

method asPips(value, priceScale, minMove, minMove2, decimalSeparator, groupingSeparator)

Converts a number to a string in decimal format with the last digit replaced by a superscript.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

priceScale (int) : Price scale.

minMove (int) : Min move.

minMove2 (int) : Min move 2.

decimalSeparator (string) : The decimal separator.

groupingSeparator (string) : The thousands separator, aka digit group separator.

Returns: String in decimal format with an emphasis on the pip value.

method asFractional(value, priceScale, minMove, minMove2, fractionalSeparator1, fractionalSeparator2)

Converts a number to a string in fractional format.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

priceScale (int) : Price scale.

minMove (int) : Min move.

minMove2 (int) : Min move 2.

fractionalSeparator1 (string) : The primary fractional separator.

fractionalSeparator2 (string) : The secondary fractional separator.

Returns: String in fractional format.

method asVolume(value, precision, minTick, decimalSeparator, groupingSeparator, spacing)

Converts a number to a string in volume format.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

precision (int) : Maximum number of decimal places.

minTick (float) : Minimum tick size.

decimalSeparator (string) : The decimal separator.

groupingSeparator (string) : The thousands separator, aka digit group separator.

spacing (string) : The whitespace separator.

Returns: String in volume format.

NASDAQ VWAP Distance Histogram (Multi-Symbol)📊 VWAP Distance Histogram (Multi-Symbol)

This custom indicator plots a histogram of price strength relative to the VWAP (Volume-Weighted Average Price).

The zero line is VWAP.

Histogram bars above zero = price trading above VWAP (strength).

Histogram bars below zero = price trading below VWAP (weakness).

Unlike a standard VWAP overlay, this tool lets you monitor multiple symbols at once and aggregates them into a single, easy-to-read histogram.

🔑 Features

Multi-Symbol Support → Track up to 10 different tickers plus the chart symbol.

Aggregation Options → Choose between average or median deviation across enabled symbols.

Percent or Raw Values → Display distance from VWAP as % of price or raw price points.

Smoothing → Apply EMA smoothing to calm intraday noise.

Color-Coded Histogram → Green above VWAP, red below.

Alerts → Trigger when the aggregate crosses above/below VWAP.

Heads-Up Table → Shows number of symbols tracked and current aggregate reading.

⚡ Use Cases

Market Breadth via VWAP → Monitor whether your basket of stocks is trading above or below VWAP.

Index Substitution → Create your own “mini index” by tracking a hand-picked set of tickers.

Intraday Confirmation → Use aggregate VWAP strength/weakness to confirm entries and exits.

Relative Strength Spotting → Switch on/off specific tickers to see who’s holding above VWAP vs. breaking down.

🛠️ Settings

Include Chart Symbol → Toggle to include the current chart’s ticker.

Smoothing → EMA length (set to 0 to disable).

Percent Mode → Show results as % of price vs. raw difference.

Aggregate Mode → Average or median across all active symbols.

Symbol Slots (S1–S10) → Enter tickers to track alongside the chart.

⚠️ Notes

Works best on intraday charts since VWAP is session-based.

Designed for confirmation, not as a standalone entry/exit signal.

Ensure correct symbol format (e.g., NASDAQ:AAPL if needed).

✅ Tip: Combine this with your regular price action strategy. For example, if your setup triggers long and the histogram is well above zero, that’s added confirmation. If it’s below zero, caution — the basket shows weakness.

Yelober - Market Internal direction+ Key levelsYelober – Market Internals + Key Levels is a focused intraday trading tool that helps you spot high-probability price direction by anchoring decisions to structure that matters: yesterday’s RTH High/Low, today’s pre-market High/Low, and a fast Value Area/POC from the prior session. Paired with a compact market internals dashboard (NYSE/NASDAQ UVOL vs. DVOL ratios, VOLD slopes, TICK/TICKQ momentum, and optional VIX trend), it gives you a real-time read on breadth so you can choose which direction to trade, when to enter (breaks, retests, or fades at PMH/PML/VAH/VAL/POC), and how to plan exits as internals confirm or deteriorate. On top of these intraday decision benefits, it also allows traders—in a very subtle but powerful way—to keep an eye on the VIX and immediately recognize significant spikes or sharp decreases that should be factored in before entering a trade, or used as a quick signal to modify an existing position. In short: clear levels for the chart, live internals for the context, and a smarter, rules-based path to execution.

# Yelober – Market Internals + Key Levels

*A TradingView indicator for session key levels + real‑time market internals (NYSE/NASDAQ TICK, UVOL/DVOL/VOLD, and VIX).*

**Script name in Pine:** `Yelober - Market Internal direction+ Key levels` (Pine v6)

---

## 1) What this indicator does

**Purpose:** Help intraday traders quickly find high‑probability reaction zones and read market internals momentum without switching charts. It overlays yesterday/today’s **automatic price levels** on your active chart and shows a **market breadth table** that summarizes NYSE/NASDAQ buying pressure and TICK direction, with an optional VIX trend read.

### Key features at a glance

* **Automatic Price Levels (overlay on chart)**

* Yesterday’s High/Low of Day (**yHoD**, **yLoD**)

* Extended Hours High/Low (**yEHH**, **yEHL**) across yesterday AH + today pre‑market

* Today’s Pre‑Market High/Low (**PMH**, **PML**)

* Yesterday’s **Value Area High/Low** (**VAH/VAL**) and **Point of Control (POC)** computed from a volume profile of yesterday’s **regular session**

* Smart de‑duplication:

* Shows **only the higher** of (yEHH vs PMH) and **only the lower** of (yEHL vs PML) to avoid redundant bands

* **Market Breadth Table (on‑chart table)**

* **NYSE ratio** = UVOL/DVOL (signed) with **VOLD slope** from session open

* **NASDAQ ratio** = UVOLQ/DVOLQ (signed) with **VOLDQ slope** from session open

* **TICK** and **TICKQ**: live cumulative ratio and short‑term slope

* **VIX** (optional): current value + slope over a configurable lookback/timeframe

* Color‑coded trends with sensible thresholds and optional normalization

---

## 2) How to use it (trader workflow)

1. **Mark your reaction zones**

* Watch **yHoD/yLoD**, **PMH/PML**, and **VAH/VAL/POC** for first touches, break/retest, and failure tests.

* Expect increased responsiveness when multiple levels cluster (e.g., PMH ≈ VAH ≈ daily pivot).

2. **Read the breadth panel for context**

* **NYSE/NASDAQ ratio** (>1 = more up‑volume than down‑volume; <−1 = down‑dominant). Strong green across both favors long setups; red favors short setups.

* **VOLD slopes** (NYSE & NASDAQ): positive and accelerating → broadening participation; negative → persistent pressure.

* **TICK/TICKQ**: cumulative ratio and **slope arrows** (↗ / ↘ / →). Use the slope to gauge **near‑term thrust or fade**.

* **VIX slope**: rising VIX (red) often coincides with risk‑off; falling VIX (green) with risk‑on.

3. **Confluence = higher confidence**

* Example: Price reclaims **PMH** while **NYSE/NASDAQ ratios** print green and **TICK slopes** point ↗ — consider break‑and‑go; if VIX slope is ↘, that adds risk‑on confidence.

* Example: Price rejects **VAH** while **VOLD slopes** roll negative and VIX ↗ — consider fade/reversal.

4. **Risk management**

* Place stops just beyond key levels tested; if breadth flips, tighten or exit.

> **Timeframes:** Works best on 1–15m charts for intraday. Value Area is computed from **yesterday’s RTH**; choose a smaller calculation timeframe (e.g., 5–15m) for stable profiles.

---

## 3) Inputs & settings (what each option controls)

### Global Style

* **Enable all automatic price levels**: master toggle for yHoD/yLoD, yEHH/yEHL, PMH/PML, VAH/VAL/POC.

* **Line style/width**: applies to all drawn levels.

* **Label size/style** and **label color linking**: use the same color as the line or override with a global label color.

* **Maximum bars lookback**: how far the script scans to build yesterday metrics (performance‑sensitive).

### Value Area / Volume Profile

* **Enable Value Area calculations** *(on by default)*: computes yesterday’s **POC**, **VAH**, **VAL** from a simplified intraday volume profile built from yesterday’s **regular session bars**.

* **Max Volume Profile Points** *(default 50)*: lower values = faster; higher = more precise.

* **Value Area Calculation Timeframe** *(default 15)*: the security timeframe used when collecting yesterday’s highs/lows/volumes.

### Individual Level Toggles & Colors

* **yHoD / yLoD** (yesterday high/low)

* **yEHH / yEHL** (yesterday AH + today pre‑market extremes)

* **PMH / PML** (today pre‑market extremes)

* **VAH / VAL / POC** (yesterday RTH value area + point of control)

### Market Breadth Panel

* **Show NYSE / NASDAQ / VIX**: choose which series to display in the table.