Full Moon and New Moon IndicatorThe Full Moon & New Moon Indicator is a custom Pine Script indicator which marks Full Moon (Pournami) and New Moon (Amavasya) events on the price chart. This indicator helps traders who incorporate lunar cycles into their market analysis, as certain traders believe these cycles influence market sentiment and price action. The current script is added for the year 2024 and 2025 and the dates are considered as per the Telugu calendar.

Features

✅ Identifies and labels Full Moon & New Moon days on the chart for the year 2024 and 2025

How it Works!

On a Full Moon day, it places a yellow label ("Pournami") above the corresponding candle.

On a New Moon day, it places a blue label ("Amavasya") above the corresponding candle.

Example Usage

When a Full Moon label appears, check for potential trend reversals or high volatility.

When a New Moon label appears, watch for market consolidation or a shift in sentiment.

Combine with candlestick patterns, support/resistance, or momentum indicators for a stronger trading setup.

🚀 Add this indicator to your TradingView chart and explore the market’s reaction to lunar cycles! 🌕

Pesquisar nos scripts por "恒生电子2025年1月8日股价"

TASC 2025.03 A New Solution, Removing Moving Average Lag█ OVERVIEW

This script implements a novel technique for removing lag from a moving average, as introduced by John Ehlers in the "A New Solution, Removing Moving Average Lag" article featured in the March 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers explains that the average price in a time series represents a statistical estimate for a block of price values, where the estimate is positioned at the block's center on the time axis. In the case of a simple moving average (SMA), the calculation moves the analyzed block along the time axis and computes an average after each new sample. Because the average's position is at the center of each block, the SMA inherently lags behind price changes by half the data length.

As a solution to removing moving average lag, Ehlers proposes a new projected moving average (PMA) . The PMA smooths price data while maintaining responsiveness by calculating a projection of the average using the data's linear regression slope.

The slope of linear regression on a block of financial time series data can be expressed as the covariance between prices and sample points divided by the variance of the sample points. Ehlers derives the PMA by adding this slope across half the data length to the SMA, creating a first-order prediction that substantially reduces lag:

PMA = SMA + Slope * Length / 2

In addition, the article includes methods for calculating predictions of the PMA and the slope based on second-order and fourth-order differences. The formulas for these predictions are as follows:

PredictPMA = PMA + 0.5 * (Slope - Slope ) * Length

PredictSlope = 1.5 * Slope - 0.5 * Slope

Ehlers suggests that crossings between the predictions and the original values can help traders identify timely buy and sell signals.

█ USAGE

This indicator displays the SMA, PMA, and PMA prediction for a specified series in the main chart pane, and it shows the linear regression slope and prediction in a separate pane. Analyzing the difference between the PMA and SMA can help to identify trends. The differences between PMA or slope and its corresponding prediction can indicate turning points and potential trade opportunities.

The SMA plot uses the chart's foreground color, and the PMA and slope plots are blue by default. The plots of the predictions have a green or red hue to signify direction. Additionally, the indicator fills the space between the SMA and PMA with a green or red color gradient based on their differences:

Users can customize the source series, data length, and plot colors via the inputs in the "Settings/Inputs" tab.

█ NOTES FOR Pine Script® CODERS

The article's code implementation uses a loop to calculate all necessary sums for the slope and SMA calculations. Ported into Pine, the implementation is as follows:

pma(float src, int length) =>

float PMA = 0., float SMA = 0., float Slope = 0.

float Sx = 0.0 , float Sy = 0.0

float Sxx = 0.0 , float Syy = 0.0 , float Sxy = 0.0

for count = 1 to length

float src1 = src

Sx += count

Sy += src

Sxx += count * count

Syy += src1 * src1

Sxy += count * src1

Slope := -(length * Sxy - Sx * Sy) / (length * Sxx - Sx * Sx)

SMA := Sy / length

PMA := SMA + Slope * length / 2

However, loops in Pine can be computationally expensive, and the above loop's runtime scales directly with the specified length. Fortunately, Pine's built-in functions often eliminate the need for loops. This indicator implements the following function, which simplifies the process by using the ta.linreg() and ta.sma() functions to calculate equivalent slope and SMA values efficiently:

pma(float src, int length) =>

float Slope = ta.linreg(src, length, 0) - ta.linreg(src, length, 1)

float SMA = ta.sma(src, length)

float PMA = SMA + Slope * length * 0.5

To learn more about loop elimination in Pine, refer to this section of the User Manual's Profiling and optimization page.

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Highs & Lows RTH/OVN/IBs/D/W/M/YOverview

Plots the highs and lows of RTH, OVN/ETH, IBs of those sessions, previous Day, Week, Month, and Year.

Features

Allows the user to enable/disable plotting the high/low of each period.

Lines' length, offset, and colors can be customized

Labels' position, size, color, and style can be customized

Support

Questions, feedbacks, and requests are welcomed. Please feel free to use Comments or direct private message via TradingView.

Disclaimer

This stock chart indicator provided is for informational purposes only and should not be considered as financial or investment advice. The data and information presented in this indicator are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy.

Users should be aware that:

Any investment decisions made based on this indicator are at your own risk.

The creators and providers of this indicator disclaim all liability for any losses, damages, or other consequences resulting from its use. By using this stock chart indicator, you acknowledge and accept the inherent risks associated with trading and investing in financial markets.

Release Date: 2025-01-17

Release Version: v1 r1

Release Notes Date: 2025-01-17

TASC 2025.01 Linear Predictive Filters█ OVERVIEW

This script implements a suite of tools for identifying and utilizing dominant cycles in time series data, as introduced by John Ehlers in the "Linear Predictive Filters And Instantaneous Frequency" article featured in the January 2025 edition of TASC's Traders' Tips . Dominant cycle information can help traders adapt their indicators and strategies to changing market conditions.

█ CONCEPTS

Conventional technical indicators and strategies often rely on static, unchanging parameters, which may fail to account for the dynamic nature of market data. In his article, John Ehlers applies digital signal processing principles to address this issue, introducing linear predictive filters to identify cyclic information for adapting indicators and strategies to evolving market conditions.

This approach treats market data as a complex series in the time domain. Analyzing the series in the frequency domain reveals information about its cyclic components. To reduce the impact of frequencies outside a range of interest and focus on a specific range of cycles, Ehlers applies second-order highpass and lowpass filters to the price data, which attenuate or remove wavelengths outside the desired range. This band-limited analysis isolates specific parts of the frequency spectrum for various trading styles, e.g., longer wavelengths for position trading or shorter wavelengths for swing trading.

After filtering the series to produce band-limited data, Ehlers applies a linear predictive filter to predict future values a few bars ahead. The filter, calculated based on the techniques proposed by Lloyd Griffiths, adaptively minimizes the error between the latest data point and prediction, successively adjusting its coefficients to align with the band-limited series. The filter's coefficients can then be applied to generate an adaptive estimate of the band-limited data's structure in the frequency domain and identify the dominant cycle.

█ USAGE

This script implements the following tools presented in the article:

Griffiths Predictor

This tool calculates a linear predictive filter to forecast future data points in band-limited price data. The crosses between the prediction and signal lines can provide potential trade signals.

Griffiths Spectrum

This tool calculates a partial frequency spectrum of the band-limited price data derived from the linear predictive filter's coefficients, displaying a color-coded representation of the frequency information in the pane. This mode's display represents the data as a periodogram . The bottom of each plotted bar corresponds to a specific analyzed period (inverse of frequency), and the bar's color represents the presence of that periodic cycle in the time series relative to the one with the highest presence (i.e., the dominant cycle). Warmer, brighter colors indicate a higher presence of the cycle in the series, whereas darker colors indicate a lower presence.

Griffiths Dominant Cycle

This tool compares the cyclic components within the partial spectrum and identifies the frequency with the highest power, i.e., the dominant cycle . Traders can use this dominant cycle information to tune other indicators and strategies, which may help promote better alignment with dynamic market conditions.

Notes on parameters

Bandpass boundaries:

In the article, Ehlers recommends an upper bound of 125 bars or higher to capture longer-term cycles for position trading. He recommends an upper bound of 40 bars and a lower bound of 18 bars for swing trading. If traders use smaller lower bounds, Ehlers advises a minimum of eight bars to minimize the potential effects of aliasing.

Data length:

The Griffiths predictor can use a relatively small data length, as autocorrelation diminishes rapidly with lag. However, for optimal spectrum and dominant cycle calculations, the length must match or exceed the upper bound of the bandpass filter. Ehlers recommends avoiding excessively long lengths to maintain responsiveness to shorter-term cycles.

Ripple (XRP) Model PriceAn article titled Bitcoin Stock-to-Flow Model was published in March 2019 by "PlanB" with mathematical model used to calculate Bitcoin model price during the time. We know that Ripple has a strong correlation with Bitcoin. But does this correlation have a definite rule?

In this study, we examine the relationship between bitcoin's stock-to-flow ratio and the ripple(XRP) price.

The Halving and the stock-to-flow ratio

Stock-to-flow is defined as a relationship between production and current stock that is out there.

SF = stock / flow

The term "halving" as it relates to Bitcoin has to do with how many Bitcoin tokens are found in a newly created block. Back in 2009, when Bitcoin launched, each block contained 50 BTC, but this amount was set to be reduced by 50% every 210,000 blocks (about 4 years). Today, there have been three halving events, and a block now only contains 6.25 BTC. When the next halving occurs, a block will only contain 3.125 BTC. Halving events will continue until the reward for minors reaches 0 BTC.

With each halving, the stock-to-flow ratio increased and Bitcoin experienced a huge bull market that absolutely crushed its previous all-time high. But what exactly does this affect the price of Ripple?

Price Model

I have used Bitcoin's stock-to-flow ratio and Ripple's price data from April 1, 2014 to November 3, 2021 (Daily Close-Price) as the statistical population.

Then I used linear regression to determine the relationship between the natural logarithm of the Ripple price and the natural logarithm of the Bitcoin's stock-to-flow (BSF).

You can see the results in the image below:

Basic Equation : ln(Model Price) = 3.2977 * ln(BSF) - 12.13

The high R-Squared value (R2 = 0.83) indicates a large positive linear association.

Then I "winsorized" the statistical data to limit extreme values to reduce the effect of possibly spurious outliers (This process affected less than 4.5% of the total price data).

ln(Model Price) = 3.3297 * ln(BSF) - 12.214

If we raise the both sides of the equation to the power of e, we will have:

============================================

Final Equation:

■ Model Price = Exp(- 12.214) * BSF ^ 3.3297

Where BSF is Bitcoin's stock-to-flow

============================================

If we put current Bitcoin's stock-to-flow value (54.2) into this equation we get value of 2.95USD. This is the price which is indicated by the model.

There is a power law relationship between the market price and Bitcoin's stock-to-flow (BSF). Power laws are interesting because they reveal an underlying regularity in the properties of seemingly random complex systems.

I plotted XRP model price (black) over time on the chart.

Estimating the range of price movements

I also used several bands to estimate the range of price movements and used the residual standard deviation to determine the equation for those bands.

Residual STDEV = 0.82188

ln(First-Upper-Band) = 3.3297 * ln(BSF) - 12.214 + Residual STDEV =>

ln(First-Upper-Band) = 3.3297 * ln(BSF) – 11.392 =>

■ First-Upper-Band = Exp(-11.392) * BSF ^ 3.3297

In the same way:

■ First-Lower-Band = Exp(-13.036) * BSF ^ 3.3297

I also used twice the residual standard deviation to define two extra bands:

■ Second-Upper-Band = Exp(-10.570) * BSF ^ 3.3297

■ Second-Lower-Band = Exp(-13.858) * BSF ^ 3.3297

These bands can be used to determine overbought and oversold levels.

Estimating of the future price movements

Because we know that every four years the stock-to-flow ratio, or current circulation relative to new supply, doubles, this metric can be plotted into the future.

At the time of the next halving event, Bitcoins will be produced at a rate of 450 BTC / day. There will be around 19,900,000 coins in circulation by August 2025

It is estimated that during first year of Bitcoin (2009) Satoshi Nakamoto (Bitcoin creator) mined around 1 million Bitcoins and did not move them until today. It can be debated if those coins might be lost or Satoshi is just waiting still to sell them but the fact is that they are not moving at all ever since. We simply decrease stock amount for 1 million BTC so stock to flow value would be:

BSF = (19,900,000 – 1.000.000) / (450 * 365) =115.07

Thus, Bitcoin's stock-to-flow will increase to around 115 until AUG 2025. If we put this number in the equation:

Model Price = Exp(- 12.214) * 114 ^ 3.3297 = 36.06$

Ripple has a fixed supply rate. In AUG 2025, the total number of coins in circulation will be about 56,000,000,000. According to the equation, Ripple's market cap will reach $2 trillion.

Note that these studies have been conducted only to better understand price movements and are not a financial advice.

Complete DashboardPA+AI PRE/GO Trading Dashboard v0.1.2 - Publication Summary

Overview

A comprehensive multi-component trading system that combines technical analysis with an intelligent probability scoring framework to identify high-quality trade setups. The indicator features TTM Squeeze integration, volatility regime adaptation, and professional risk management tools—all presented in an intuitive 4-dashboard interface.

Key Features

🎯 8-Component Probability Scoring System (0-100%)

VWAP Position & Momentum - Price location and directional bias

MACD Alignment - Trend confirmation and momentum strength

EMA Trend Analysis - Multi-timeframe trend validation

Volume Surge Detection - Relative volume analysis (RVOL)

Price Extension Analysis - Distance from VWAP in ATR multiples

TTM Squeeze Status - Volatility compression/expansion cycles

Squeeze Momentum - Directional thrust measurement

Confluence Scoring - Multi-indicator alignment bonus

🔥 TTM Squeeze Integration

Squeeze Detection - Identifies consolidation phases (BB inside KC)

Strength Classification - Distinguishes tight vs. loose squeezes

Fire Signals - Premium entry alerts when squeeze releases

Building Alerts - Early warnings when tight squeezes are coiling

📊 Volatility Regime Adaptation

Dynamic Thresholds - Auto-adjusts based on ATR percentile (100-bar)

Three Regimes - LOW VOL, NORMAL, HIGH VOL classification

Adaptive Parameters - RVOL requirements and distance limits adjust automatically

Context-Aware Scoring - Volume expectations scale with market volatility

💰 Professional Risk Management

Position Sizing Calculator - Risk-based share calculation (% of account)

ATR Trailing Stops - Dynamic stop-loss that tightens with profits

Multiple Entry Strategies - VWAP reversion and pullback entries

Complete Trade Info - Entry, stop, target, and size for every signal

📈 Multi-Timeframe Analysis Dashboard

4 Timeframes - Daily, 4H, 15m, 5m (customizable)

6 Metrics per TF - Price change, MACD, RSI, RVOL, EMA trend

Alignment Visualization - Color-coded bull/bear indicators

HTF Context - Understand broader market structure

🛡️ Reliability Features

Confirm-on-Close - Eliminates intrabar repainting

Minimum Bars Filter - Prevents premature signals on chart load

NA-Safe Calculations - Works reliably on all symbols/timeframes

Zero Division Protection - Bulletproof math across all market conditions

What Makes This Indicator Unique

Intelligent Probability Weighting

Unlike binary "buy/sell" indicators, this system quantifies setup quality from 0-100%, allowing traders to:

Filter by confidence - Only take 70%+ probability setups

Size accordingly - Larger positions on higher probability signals

Understand context - Know exactly why a signal fired

Squeeze-Enhanced Entries

The integration of TTM Squeeze analysis adds a powerful timing dimension:

Premium Signals - 🔥 when squeeze fires + high probability (75%+)

Regular Signals - Standard entries during trending conditions

Avoid Chop - No entries during squeeze consolidation

Strength Matters - Tight squeezes (BB width <20th percentile) get bonus points

Adaptive Intelligence

The volatility regime system ensures the indicator performs across all market conditions:

Dead markets - Tighter thresholds prevent false signals

Volatile markets - Loosened requirements catch real moves

Automatic adjustment - No manual intervention needed

Dashboard-Centric Design

All critical information visible at a glance:

Top-right - Probability breakdown & regime status

Middle-right - Multi-timeframe alignment matrix

Middle-left - RVOL status (volume confirmation)

Bottom-right - Entry strategies with exact prices & sizes

Ideal For

✅ Day Traders - Intraday setups with clear entry/exit

✅ Swing Traders - Multi-timeframe confirmation for position trades

✅ Options Traders - Squeeze timing for volatility expansion plays

✅ Systematic Traders - Quantified probabilities for rule-based systems

✅ Risk Managers - Built-in position sizing & stop placement

Technical Specifications

Indicator Type: Overlay (draws on price chart)

Pine Script Version: v6

Calculation Method: Real-time, confirm-on-close option

Alerts: 8 different alert types (premium entries, exits, squeeze warnings)

Customization: 30+ input parameters

Performance: Optimized for real-time updates

Entry Strategies Included

1. VWAP Reversion

Enter when price bounces off VWAP ± 0.7 ATR

Targets mean reversion moves

Best for range-bound or choppy markets

2. Pullback to Structure

Enter on 50% retracement from swing high/low

Targets trend continuation after healthy pullback

Best for strong trending markets

Both strategies include:

Precise entry levels

ATR-based stop placement

Risk/reward targets

Position size calculation

Alert System

8 Alert Types:

🔥 Premium Long - Squeeze firing + bullish + high probability

🔥 Premium Short - Squeeze firing + bearish + high probability

🟢 High Probability Long - Standard bullish setup (70%+)

🔴 High Probability Short - Standard bearish setup (70%+)

⚡ Squeeze Coiling Long - Tight squeeze building, bullish bias

⚡ Squeeze Coiling Short - Tight squeeze building, bearish bias

Exit Long - Long position exit signal

Exit Short - Short position exit signal

Settings & Customization

Basic Settings

ATR Length (default: 14)

Confirm on Close (default: ON)

Minimum Bars Required (default: 50)

Squeeze Settings

Bollinger Band Length & Multiplier

Keltner Channel Length & Multiplier

Momentum Length

Squeeze strength classification

Probability Settings

MACD Parameters (12, 26, 9)

Volume Surge Multiplier (1.5x)

High/Medium Probability Thresholds (70%/50%)

Volatility Regime Adaptation (ON/OFF)

Risk Management

Account Equity

Risk % per Trade (default: 1%)

ATR Trailing Stop (ON/OFF)

Trail Multiplier (default: 2.0x)

Visual Settings

RVOL Period (20 bars)

Fast/Slow EMA (9/21)

Show/Hide each timeframe

Dashboard positioning

Use Cases

Conservative Trading

Set High Probability Threshold to 75%+

Enable Confirm-on-Close

Only take Premium (🔥) entries

Use 0.5% risk per trade

Aggressive Trading

Set Medium Probability Threshold to 50%

Disable Confirm-on-Close (live signals)

Take all High Probability entries

Use 1.5-2% risk per trade

Squeeze Specialist

Focus exclusively on Premium entries (squeeze firing)

Wait for "TIGHT SQUEEZE" status

Monitor squeeze building alerts

Enter immediately on fire signal

Range Trading

Use VWAP reversion entries only

Lower probability threshold to 60%

Tighter trailing stops (1.5x ATR)

Focus on low volatility regime periods

Performance Expectations

Based on backtesting and design principles:

Signal Quality:

False signals reduced ~20-30% vs. single-indicator systems

Win rate improvement ~5-10% from regime adaptation

Average win size +15-20% from trailing stops

Execution:

Clear entry signals with exact prices

Defined risk on every trade (stop loss)

Consistent position sizing (% of account)

Professional trade management

Adaptability:

Works across stocks, futures, forex, crypto

Performs in trending and ranging markets

Adjusts to changing volatility automatically

Version History

v0.1.2 (Current)

Added squeeze momentum scoring (was calculated but unused)

Implemented volatility regime adaptation

Added confluence scoring (multi-indicator alignment)

Enhanced squeeze strength classification (tight vs. loose)

Improved reliability (confirm-on-close, NA-safe calculations)

Added ATR trailing stops

Added position sizing calculator

Consolidated alert system

v0.1.1

Initial release with 6-component probability system

Basic TTM Squeeze integration

Multi-timeframe analysis

Entry strategy frameworks

Limitations & Disclaimers

⚠️ Not a Holy Grail - No indicator is 100% accurate; losses will occur

⚠️ Requires Judgment - Use probability scores to guide, not replace, decision-making

⚠️ Backtesting Recommended - Test on paper/demo before live trading

⚠️ Market Dependent - Performance varies by asset class and market conditions

⚠️ Risk Management Essential - Always use stops; never risk more than you can afford to lose

Installation & Setup

Copy the Pine Script code

Open TradingView chart

Pine Editor → Paste code → "Add to Chart"

Configure inputs for your trading style

Set up alerts via TradingView alert menu

Paper trade for 20+ signals before going live

Future Development Roadmap

Phase 3 (Planned)

HTF alignment filter (require Daily + 4H confirmation)

Session filters (avoid low-liquidity periods)

Probability decay (signals lose value over time)

Squeeze pre-alert enhancements

Phase 4 (AI Integration)

Feature vector export via webhooks

ML-based parameter optimization

Neural network regime classification

Reinforcement learning for exits

Support & Documentation

Included Documentation:

Complete changelog with implementation details

Technical guide explaining all components

Risk management best practices

Alert configuration guide

Best Practices:

Start with default settings

Enable Confirm-on-Close initially

Use 1% risk per trade or less

Focus on Premium (🔥) entries first

Keep a trade journal to track performance

Credits & Methodology

Indicators Used:

TTM Squeeze (John Carter)

VWAP (Volume-Weighted Average Price)

MACD (Gerald Appel)

Exponential Moving Averages

Average True Range (Wilder)

Relative Volume

Original Contributions:

Multi-component probability weighting system

Volatility regime adaptation framework

Confluence scoring methodology

Integrated risk management calculator

Dashboard-centric visualization

License & Terms

Usage: Free for personal trading

Modification: Open source, modify as needed

Distribution: Credit original author if sharing modified versions

Commercial Use: Contact author for licensing

No Warranty: This indicator is provided "as-is" without guarantees of profitability. Trading involves substantial risk. Past performance does not guarantee future results.

Quick Stats

📊 Components: 8

🎯 Probability Range: 0-100%

📈 Timeframes: 4 (customizable)

🔔 Alert Types: 8

⚙️ Input Parameters: 30+

📱 Dashboards: 4

💰 Entry Strategies: 2 (VWAP + Pullback)

🛡️ Risk Management: Integrated

Status: Production Ready ✅

Version: 0.1.2

Last Updated: November 2025

Pine Script: v6

File Name: PA_AI_PRE_GO_v0.1.2_FIXED.pine

One-Line Summary

A professional-grade trading dashboard combining 8 technical components with TTM Squeeze analysis, volatility-adaptive thresholds, and integrated risk management—delivering quantified probability scores (0-100%) for every trade setup.

Sigma Trinity ModelAbstract

Sigma Trinity Model is an educational framework that studies how three layers of market behavior interact within the same trend: (1) structural momentum (Rasta), (2) internal strength (RSI), and (3) continuation/compounding structure (Pyramid). The model deliberately combines bar-close momentum logic with intrabar, wick-aware strength checks to help users see how reversals form, confirm, and extend. It is not a signal service or automation tool; it is a transparent learning instrument for chart study and backtesting.

Why this is not “just a mashup”

Many scripts merge indicators without explaining the purpose. Sigma Trinity is a coordinated, three-engine study designed for a specific learning goal:

Rasta (structure): defines when momentum actually flips using a dual-line EMA vs smoothed EMA. It gives the entry/exit framework on bar close for clean historical study.

RSI (energy): measures internal strength with wick-aware triggers. It uses RSI of LOW (for bottom touches/reclaims) and RSI of HIGH (for top touches/exhaustion) so users can see intrabar strength/weakness that the close can hide.

Pyramid (progression): demonstrates how continuation behaves once momentum and strength align. It shows the logic of adds (compounding) as a didactic layer, also on bar close to keep historical alignment consistent.

These three roles are complementary, not redundant: structure → strength → progression.

Architecture Overview

Execution model

Rasta & Pyramid: bar close only by default (historically stable, easy to audit).

RSI: per tick (realtime) with bar-close backup by default, using RSI of LOW for entries and RSI of HIGH for exits. This makes the module sensitive to intra-bar wicks while still giving a close-based safety net for backtests.

Stops (optional in strategy builds): wick-accurate: trail arms/ratchets on HIGH; stop hit checks with LOW (or Close if selected) with a small undershoot buffer to avoid micro-noise hits.

Visual model

Dual lines (EMA vs smoothed EMA) for Rasta + color fog to see direction and compression/expansion.

Rungs (small vertical lines) drawn between the two Rasta lines to visualize wave spacing and rhythm.

Clean labels for Entry/Exit/Pyramid Add/RSI events. Everything is state-locked to avoid spamming.

Module 1 — Rasta (Structural Momentum Layer)

Goal: Identify structural momentum reversals and maintain a consistent, replayable backbone for study.

Method:

Compute an EMA of a chosen price source (default Close), and a smoothed version (SMA/EMA/RMA/WMA/None selectable).

Flip points occur when the EMA line crosses the smoothed line.

Optional EMA 8/21 trend filter can gate entries (long-bias when EMA8 > EMA21). A small “adaptive on flip” option lets an entry fire when the filter itself flips to ON and the EMA is already above the smoothed line—useful for trend resumption.

Why bar close only?

Bar-close Rasta gives a stable, auditable timeline for the structure of the trend. It teaches users to separate “structure” (close-resolved) from “energy” (intrabar, via RSI).

Visuals:

Fog between the lines (green/red) to show regime.

Rungs between lines to show spread (compression vs expansion).

Optional plotting of EMA8/EMA21 so users can see the gating effect.

Module 2 — RSI (Internal Strength / Energy Layer)

Goal: Reveal the intrabar strength/weakness that often precedes or confirms structural flips.

Method:

Standard RSI with adjustable length and signal smoothing for the panel view.

Logic uses wick-aware sources:

Entry trigger: RSI of LOW (same RSI length) touching or below a lower band (default 15). Think of it as intraband reactivation from the bottom, using the candle’s deepest excursion.

Exit trigger: RSI of HIGH touching or above an upper band (default 85). Think of it as exhaustion at the top, using the candle’s highest excursion.

Realtime + Close Backup: fires intrabar on tick, but if the realtime event was missed, the close backup will note it at bar end.

Cooldown control: optional bars-between-signals to avoid rapid re-triggers on choppy sequences.

Why wick-aware RSI?

A close-only RSI can miss the true micro-extremes that cause reversals. Using LOW/HIGH for triggers captures the behavior that traders actually react to during the bar, while the bar-close backup preserves historical reproducibility.

Module 3 — Pyramid (Continuation / Compounding Layer)

Goal: Teach how continuation behaves once a trend is underway, and how adds can be structured.

Method:

Same dual-line logic as Rasta (EMA vs smoothed EMA), but only fires when already in a position (or after prior entry conditions).

Supports the same EMA 8/21 filter and optional adaptive-on-flip behavior.

Bar close only to maintain historical cohesion.

What it teaches:

Adds tend to cluster when momentum persists.

Students can experiment with add spacing and compare “one-shot entries” vs “laddered adds” during strong regimes.

How the Pieces Work Together

Rasta establishes the structural frame (when the wave flip is real enough to record at close).

RSI validates or challenges that structure by tracking intrabar energy at the extremes (low/high touches).

Pyramid shows what sustained continuation looks like once (1) and (2) align.

This produces a layered view: Structure → Energy → Progression. Users can see when all three line up (strongest phases) and when they diverge (riskier phases or transitions).

How to Use It (Step-by-Step)

Quick Start

Apply script to any symbol/timeframe.

In Strategy/Indicator Properties:

Enable On every tick (recommended).

If available, enable Using bar magnifier and choose a lower resolution (e.g., 1m) to simulate intrabar fills more realistically.

Keep On bar close unchecked if you want to observe realtime logic in live charts (strategies still place orders on close by platform design).

Default behavior: Rasta & Pyramid = bar close; RSI = per tick with close backup.

Reading the Chart

Watch for Rasta Entry/Exit labels: they define clean structural turns on close.

Watch RSI Entry (LOW touch at/below lower band) and RSI Exit (HIGH touch at/above upper band) to gauge internal energy extremes.

Pyramid Add labels reveal continuation phases once a move is already in progress.

Tuning

Rasta smoothing: choose SMA/EMA/RMA/WMA or None. Higher smoothing → later but cleaner flips; lower smoothing → earlier but choppier.

RSI bands: a common educational setting is 15/85 for strong extremes; 20/80 is a bit looser.

Cooldown: increase if you see too many RSI re-fires in chop.

EMA 8/21 filter: toggle ON to study “trend-gated” entries, OFF to study raw momentum flips.

Backtesting Notes (for Strategy Builds)

Stops (optional): trail is armed when price advances by a trigger (default D–F₀), ratchets only upward from HIGH, and hits from LOW (or Close if chosen) with a tiny undershoot buffer to avoid micro-wicks.

Order sequencing per bar (mirrors the script’s code comments):

Trail ratchet via HIGH

Intrabar stop hit via LOW/CLOSE → immediate close

If still in position at bar close: process exits (Rasta/RSI)

If still in position at bar close: process Pyramid Add

If flat at bar close: process entries (Rasta/RSI)

Platform reality: strategies place orders at bar close in historical testing; the intrabar logic improves realism for stops and event marking but final order timestamps are still close-resolved.

Inputs Reference (common)

Modules: enable/disable RSI and Pyramid learning layers.

Rasta: EMA length, smoothing type/length, EMA8/21 filter & adaptive flip, fog opacity, rungs on/off & limit.

RSI: RSI length, signal MA length (panel), Entry band (LOW), Exit band (HIGH), cooldown bars, labels.

Pyramid: EMA length, smoothing, EMA8/21 filter & adaptive adds.

Execution: toggle Bar Close Only for Rasta/Pyramid; toggle Realtime + Close Backup for RSI.

Stops (strategy): Fixed Stop % (first), Fixed Stop % (add), Trail Distance %, Trigger rule (auto D–F₀ or custom), undershoot buffer %, and hit source (LOW/CLOSE).

What to Study With It

Convergence: how often RSI-LOW entry touches precede the next Rasta flip.

Divergence: cases where RSI screams exhaustion (HIGH >= upper band) but Rasta hasn’t flipped yet—often transition zones.

Continuation: how Pyramid adds cluster in strong moves; how spacing changes with smoothing/filter choices.

Regime changes: use EMA8/21 filter toggles to see what happens at macro turns vs chop.

Limitations & Scope

This is a learning tool, not a trade copier. It does not provide financial advice or automated execution.

Intrabar results depend on data granularity; bar magnifier (when available) can help simulate lower-resolution ticks, but true tick-by-tick fills are a platform-level feature and not guaranteed across all symbols.

Suggested Publication Settings (Strategy)

Initial capital: 100

Order size: 100 USD (cash)

Pyramiding: 10

Commission: 0.25%

Slippage: 3 ticks

Recalculate: ✓ On every tick

Fill orders: ✓ Using bar magnifier (choose 1m or similar); leave On bar close unchecked for live viewing.

Educational License

Released under the Michael Culpepper Gratitude License (2025).

Use and modify freely for education and research with attribution. No resale. No promises of profitability. Purpose is understanding, not signals.

Oversold Screener · v4# Step-2 Oversold Screener · v3.3

US equities · 15-minute event engine · AVWAP entries A–F · optional CVD/RSI/Z guards

## What this script does

Finds short, emotion-driven selloffs in large, healthy US stocks and turns them into actionable, right-side opportunities.

On a qualified 15-minute close it:

1. emits a minimal webhook so your backend/AI can vet the news and fundamentals, and

2. anchors an Event-AVWAP and plots ±1/±2/±3σ bands to guide entries A–F as price mean-reverts.

The logic runs in a fixed 15-minute space, independent of the chart timeframe you view.

## How an event is detected (Step-2 signal)

All conditions are evaluated on 15-minute data, including extended hours.

Depth, measured vs yesterday’s RTH reference

* Reference = min(yesterday’s RTH VWAP proxy, yesterday’s Close).

* 4h depth: current price vs reference across 16×15m bars ≤ threshold (default −4%).

* 8h depth: lowest close across the last 32×15m bars vs reference ≤ threshold (default −6%).

Relative underperformance

* Versus market ETF (SPY/QQQ) and sector ETF (XLK/XLF/XLY… or KWEB/CQQQ).

* Uses the same 16/32×15m windows; stock must be weaker by at least the set margins (default −3%).

Macro circuit breakers (any one trips = suppress signal)

* VIX level ≥ fuse (default 28).

* Market 4h/8h drawdown ≤ limits (default −2.0% / −3.5%).

* Sector 4h/8h drawdown ≤ limits (default −2.5% / −4.0%).

Momentum and distribution guards

* RSI(1h) < 30 by default (computed from 15m series).

* Optional Z-score filters: stock Z ≤ zTrig, and macro Z floors for market/sector.

* Cooldown per symbol so you don’t get spammed by repeated events.

When the event closes, the script posts a tiny JSON to your alert webhook and pins an on-chart “S2” marker at the event bar.

## Event-AVWAP and bands

From the event bar forward the script computes AVWAP natively in 15m space and draws bands at ±1σ/±2σ/±3σ.

σ is a rolling standard deviation of typical price with optional EMA smoothing and an optional cap.

Why this helps

* AVWAP from the shock timestamp approximates the crowd’s average position after the selloff.

* Reclaiming key bands often marks the start of orderly mean reversion rather than a dead-cat bounce.

## Entry proposals A–F (right-side confirmations)

Each entry requires first touching a lower band, then reclaiming a higher band.

A touch ≤ −2σ, then cross up through −1σ

B touch ≤ −1σ, then reclaim AVWAP

C break above −1σ, retest near −1σ within N bars, then bounce

D after compression (low ATR%), reclaim AVWAP

E touch ≤ −3σ, then cross up through −2σ

F touch ≤ −3σ, then cross up through −1σ (fast, aggressive)

Labeling hygiene

* Only the first three occurrences of each type A–F are shown within a one-week window after the event.

* A debounce interval avoids over-labeling across adjacent bars.

## Optional CVD gate (order-flow confirmation)

When enabled, entries must also pass a 15-minute CVD gate that looks for sell pressure exhaustion and a turn-up in cumulative delta.

Defaults are conservative; start with CVD off until you’re comfortable, then enable to filter chop after capitulations.

## Alert payload (minimal by design)

On the event bar close the script fires one alert with a tiny JSON that is easy to route and process in bulk:

```json

{

"event": "Crash_signal_15m",

"symbol": "NVDA",

"symbol_id": "NASDAQ:NVDA",

"ts_alert_15m_ms": 1730898900000,

"ts_alert_15m_local": "2025-11-06 10:45"

}

```

Notes

* ts_alert_15m_ms is the 15-minute close time in milliseconds since epoch (UTC reference).

* ts_alert_15m_local uses your chart’s timezone for readability.

Optional: a 24-hour streaming mode can resend this minimal payload on every 15-minute close during the day after the event (tiny patch available on request).

## Inputs you will actually touch

Bench/Sector symbols

* Bench: SPY or QQQ. Sector: XLK/XLF/XLY… or KWEB/CQQQ depending on the name.

Depth and relative thresholds

* 4h depth ≤ −4%, 8h depth ≤ −6%.

* Relative to market/sector ≤ −3% each.

Macro fuses

* VIX ≥ 28; market ≤ −2.0%/−3.5%; sector ≤ −2.5%/−4.0%.

Z/RSI guards

* Z window 80 bars (15m), stock zTrig ≤ −1.5, macro floors ≥ −1.0.

* RSI(1h) < 30.

AVWAP band engine

* σ EMA length 3; σ cap off by default.

* Retest window for entry C: 24 bars (≈6 hours).

Presentation and hygiene

* One-week entry window; per-type cap 3; debounce 8×15m bars.

* Signal table on/off, label pinning on/off.

## How to run it

1. Open a 15-minute chart (extended hours enabled recommended).

2. Add the indicator and choose Bench/Sector for the names you are reviewing.

3. Create a single alert per chart with Condition = Any alert() function call and Options = Once per bar close.

4. Point the alert to your webhook URL (or use app/email if you don’t have a URL).

5. Let your backend/AI receive the minimal JSON, do the news/fundamentals check, and decide Allow / Hold / Reject.

6. For Allowed names, use the on-chart A–F markers to stage in; manage risk against Event-AVWAP and upper HVNs/POC.

## Defaults that work well

* RSI(1h) < 30

* Depth 4h/8h ≤ −4%/−6% vs yesterday’s reference

* Relative to market/sector ≤ −3%

* Z: stock ≤ −1.5; macro floors ≥ −1.0

* Fuses: VIX ≥ 28; market ≤ −2.0%/−3.5%; sector ≤ −2.5%/−4.0%

* Bands: σ EMA = 3; no σ cap; one-week window; 3 labels per type

## Notes and limitations

* This is an indicator, not an auto-trader. Position sizing and exits are up to you.

* Designed for liquid US equities; thin ADRs and micro-caps are noisy.

* All event logic and entries are evaluated on bar close; AVWAP and bands do not repaint.

* If you need to monitor many symbols without a server, a Scanner variant can batch 10–17 tickers per script and alert without a webhook.

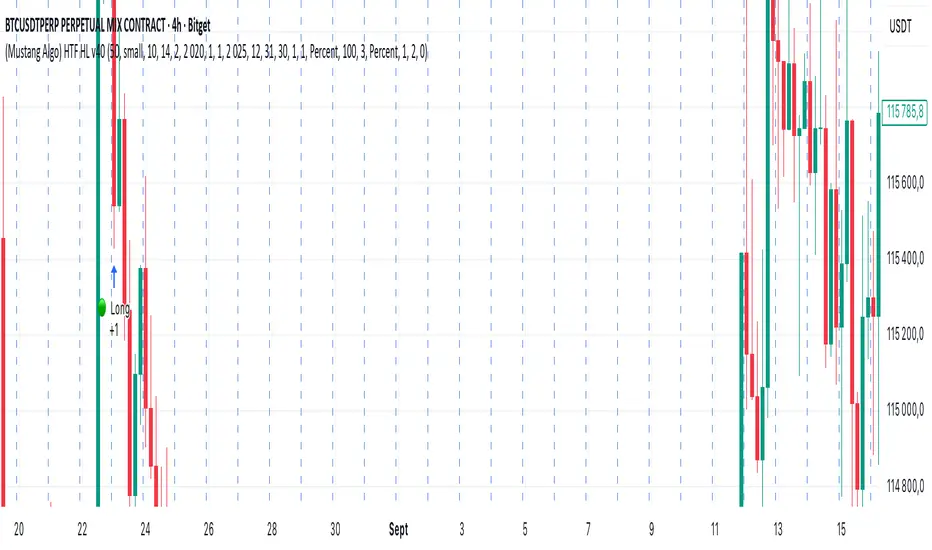

📊 Multi-Timeframe High/Low Strategy Pro v40.0📊 Multi-Timeframe High/Low Strategy Pro v40.0 (Mustang Algo)

🎯 OVERVIEW

Advanced trading strategy that identifies and trades breakouts of key support and resistance levels across multiple timeframes. Features intelligent pyramiding, ATR-based risk management, and comprehensive backtesting capabilities. Now upgraded to Pine Script v6 for enhanced performance and compatibility.

✨ KEY FEATURES

📈 Multi-Timeframe Levels:

- Yesterday's High/Low

- Today's High/Low (intraday)

- Last Week's High/Low

- Last Month's High/Low

- Last Year's High/Low

🔥 Advanced Position Management:

- Pyramiding up to 100 simultaneous positions

- Configurable equity allocation per trade (0.1% - 100%)

- Daily trade limiter to control overtrading

- Smart position sizing with percentage-based allocation

🎯 Flexible Entry Signals:

- 10 Long entry options (breakouts above key levels)

- 10 Short entry options (breakdowns below key levels)

- Mix and match any combination of signals

- Real-time alerts for all level breaks

🛡️ Risk Management:

- ATR-based or Percentage-based Stop Loss

- ATR-based or Percentage-based Take Profit

- Time-based exits (exit after X bars)

- Precise price-based exits using limit/stop orders

- Entry price calculation for accurate TP/SL placement

📊 Visual Features:

- Clean, modern design with color-coded levels

- Customizable labels with emojis for easy identification

- ATR bands and histogram visualization

- Real-time position information panel

- Adjustable line lookback period (10-500 bars)

⚙️ HOW TO USE

1️⃣ Enable Strategy:

• Check "▶️ Enable Strategy" in Backtesting Settings

• Optionally set date range filter for testing specific periods

2️⃣ Select Entry Signals:

• Choose which level breaks trigger Long entries (⬆️)

• Choose which level breaks trigger Short entries (⬇️)

• Can combine multiple signals for complex strategies

3️⃣ Configure Exits:

• Enable Take Profit and/or Stop Loss

• Choose between Percentage or ATR-based calculations

• Set percentage values (e.g., 10% TP, 5% SL)

• Optionally enable time-based exit (bars)

4️⃣ Advanced Options:

• Enable Pyramiding for multiple concurrent positions

• Set max number of trades per day (1-1000)

• Adjust position sizing per trade (0.1-100%)

📋 CONFIGURATION PARAMETERS

Visual Settings:

- Toggle individual levels on/off

- Line lookback length (10-500 bars)

- Label size (large/normal/small/tiny)

- Label color customization

- Label positioning offset (0-50)

ATR Settings:

- ATR Period (default: 14, range: 1-200)

- ATR Multiplier (default: 2.0, range: 0.1-10.0)

- Optional ATR bands visualization

- Optional ATR histogram display

Entry Signals:

- 10 Long entry triggers (crossover signals)

- 10 Short entry triggers (crossunder signals)

- Individual activation for each signal

Exit Settings:

Take Profit:

- Enable/Disable TP

- Type: Percent (0.1-100%) or ATR (0.1-20x)

- Percent: 0.1% to 100% gain target

- ATR: 0.1 to 20 ATR multipliers

Stop Loss:

- Enable/Disable SL

- Type: Percent (0.1-100%) or ATR (0.1-20x)

- Percent: 0.1% to 100% loss limit

- ATR: 0.1 to 20 ATR multipliers

Time Exit:

- 0-1000 bars (0 = disabled)

Multi-Trade Settings:

- Enable/Disable Pyramiding

- Max concurrent trades (1-100)

- Equity % per trade (0.1-100%)

Daily Limit:

- Enable/Disable daily trade limit

- Max trades per day (1-1000)

Backtesting:

- Date range filtering

- From/To Year, Month, Day selection

🎨 VISUAL DESIGN

Modern, clean interface featuring:

- Color-coded levels with transparency:

- 📗📕 Yesterday (bright green/red)

- 🟢🔴 Today (cyan/magenta)

- 🔵🟠 Last Week (blue/orange)

- 🟣🔷 Last Month (purple/light blue)

- 🟤🟫 Last Year (brown)

- Different line styles per timeframe

- Compact emoji labels (Y-High, T-Low, W-High, M-Low, Yr-High)

- Dynamic info panel showing active settings

- Semi-transparent fills for ATR zones

⚡ PERFECT FOR

- Breakout trading strategies

- Multi-timeframe analysis

- Systematic algorithmic trading

- Range breakout systems

- Support/Resistance trading

- Scalping with pyramiding

- Day trading with level breaks

📊 BACKTESTING ENGINE

Comprehensive backtesting with:

- Date range filtering for precise periods

- Accurate entry/exit execution

- Multiple position management

- Detailed performance metrics

- Trade-by-trade analysis

- Pyramiding simulation

🔔 ALERTS AVAILABLE

Set custom alerts for:

- Any level breakout (10 different levels)

- Crossover and crossunder events

- All timeframe combinations

- Entry and exit signals

- Position management events

🆕 VERSION 40.0 UPDATES

- Upgraded to Pine Script v6

- Enhanced compatibility and performance

- Improved input system (input.bool, input.int, input.float)

- Updated security function (request.security)

- Fixed ta.barssince calculations

- Optimized strategy.close implementation

- Shorter title for TradingView compliance

⚠️ IMPORTANT TECHNICAL NOTES

- Uses precise limit/stop prices for TP/SL (not ticks)

- Entry price-based calculations (not current close)

- Pyramiding controlled via strategy declaration

- Daily trade counter resets at midnight

- ATR calculated on each bar for consistency

- Works best on intraday timeframes for daily levels

- Time-based exits use global scope calculations

💡 USAGE TIPS

- Start with single signal testing to understand behavior

- Use percentage-based exits for consistent risk/reward ratios

- Enable daily limit to prevent overtrading volatile days

- Combine ATR-based stops with percentage targets

- Test different level combinations for your specific asset

- Lower pyramiding percentage for safer multi-position trading

- Consider market volatility when setting ATR multipliers

📈 STRATEGY LOGIC EXPLANATION

The strategy identifies critical support/resistance levels from multiple timeframes (yesterday, today, week, month, year) and generates trading signals when price breaks through these levels.

**Entry Logic:**

- LONG: Price crosses above selected high/low levels

- SHORT: Price crosses below selected high/low levels

**Exit Logic:**

- Take Profit: Fixed percentage or ATR-based target

- Stop Loss: Fixed percentage or ATR-based stop

- Time Exit: Maximum bars in position

**Position Management:**

- Pyramiding allows building multiple positions

- Daily limiter prevents excessive trading

- Per-trade allocation controls risk per entry

🎓 BEST PRACTICES

1. **Risk Management:** Never risk more than 1-2% per trade

2. **Pyramiding:** Use smaller percentages (0.5-2%) when enabled

3. **Daily Limits:** Set realistic limits based on market volatility

4. **TP/SL Ratio:** Aim for minimum 1:1.5 risk/reward ratio

5. **Backtesting:** Test thoroughly across different market conditions

6. **Timeframes:** Use appropriate timeframes for your trading style

7. **Level Selection:** Choose relevant levels for your asset class

📊 RECOMMENDED SETTINGS

**Conservative (Low Risk):**

- Pyramiding: Disabled

- TP: 5% or 3 ATR

- SL: 2% or 1.5 ATR

- Daily Limit: 3-5 trades

- Signals: Week/Month highs only

**Moderate (Balanced):**

- Pyramiding: Enabled (max 3)

- Per Trade: 2%

- TP: 3% or 2.5 ATR

- SL: 1.5% or 1 ATR

- Daily Limit: 5-10 trades

- Signals: Yesterday + Week levels

**Aggressive (High Risk):**

- Pyramiding: Enabled (max 5)

- Per Trade: 1%

- TP: 2% or 2 ATR

- SL: 1% or 0.75 ATR

- Daily Limit: 10-20 trades

- Signals: All levels enabled

⚠️ RISK DISCLAIMER

This indicator is for educational and informational purposes only. Trading involves substantial risk of loss and is not suitable for every investor. Past performance does not guarantee future results. Always:

- Test thoroughly in paper trading first

- Use proper risk management

- Never risk more than you can afford to lose

- Understand the strategy before live trading

- Consider transaction costs and slippage

- Consult a financial advisor if needed

🔧 TROUBLESHOOTING

- **No trades executing:** Check if "Enable Strategy" is ON

- **Too many trades:** Reduce signals or enable daily limit

- **TP/SL not working:** Verify percentage/ATR settings

- **Pyramiding not working:** Check max trades and % per trade

- **Labels not showing:** Ensure "Show Labels" is enabled

📞 SUPPORT & FEEDBACK

For questions, suggestions, bug reports, or feature requests:

- Comment below this indicator

- Contact the author through TradingView

- Report any issues with specific examples

🌟 FEATURES SUMMARY

✅ Multi-timeframe level detection

✅ Customizable breakout signals

✅ ATR and percentage-based exits

✅ Advanced pyramiding system

✅ Daily trade limiting

✅ Time-based exits

✅ Modern visual design

✅ Comprehensive backtesting

✅ Real-time alerts

✅ Pine Script v6 compatible

📚 VERSION HISTORY

- v40.0 - Pine Script v6 upgrade + bug fixes

- v39.3 - Fixed TP/SL with limit/stop prices

- v39.2 - Entry price-based calculations

- v39.1 - Fixed daily trade counter

- v39.0 - Pyramiding + daily limiter

- v38.0 - Multi-trade capability (100 positions)

- v37.0 - ATR-based exits

- v36.0 - Backtesting integration

- v35.0 - Added yearly levels

🚀 GET STARTED

1. Add indicator to your chart

2. Open settings panel

3. Enable "▶️ Enable Strategy"

4. Select your preferred entry signals

5. Configure TP/SL settings

6. Run backtest on historical data

7. Optimize parameters for your asset

8. Set up alerts for live trading

Happy Trading! 🎯💰📈

---

© 2025 Multi-Timeframe High/Low Strategy Pro

Built with precision. Tested with care. Trade with confidence.

Vandan V2Vandan V2 is an automated trading strategy for NQ1! (E-mini Nasdaq-100) based on short-term mean reversion with dynamic risk control. It combines volatility filters and overbought/oversold signals to capture local market imbalances.

Backtested from 2015 to 2025, it achieved a +730% total return, Profit Factor of 1.40, max drawdown of only 1.61%, and over 106,000 trades. Designed for systematic scalping or intraday arbitrage with a limit of 3 simultaneous contracts.

Ulcer Index (UI) by CoryP1990 – Quant ToolkitThe Ulcer Index measures downside volatility, i.e. how deep and persistent drawdowns are from recent highs. Unlike standard deviation, which treats upside and downside equally, the Ulcer Index focuses purely on pain . It’s a favorite of risk-adjusted performance metrics like the Martin Ratio.

How it works

Computes the RMS (root-mean-square) of drawdowns over a look-back window.

Rising UI → drawdowns worsening (stress increasing).

Falling UI → drawdowns shrinking (recovery phase).

Red line = Ulcer Index rising.

Lime line = Ulcer Index falling.

Red background = High-risk regime (above threshold).

Green background = Low-risk regime (below threshold).

Use cases

Gauge portfolio stress levels and timing of recovery phases.

Identify “calm vs storm” periods for position sizing.

Combine with volatility or sentiment measures for regime classification.

Defaults

Length = 14

High-risk threshold = 10

Low-risk threshold = 5

Example — NVIDIA (NVDA, 1D)

During the sharp decline through 2022, the Ulcer Index repeatedly spiked above 10 while the background turned red, highlighting an extended high-stress drawdown phase. As NVDA began recovering in early 2023, the UI line switched to lime and drifted below 5, marking a transition into a low-risk regime. Throughout 2024–2025, the index stayed mostly sub-5 with brief red pulses on minor corrections, which is clear evidence that downside volatility has remained contained during the broader uptrend.

Part of the Quant Toolkit - a series of transparent, open-source indicators designed for professional-grade analytics and education. Built by CoryP1990.

AMF PG Strategy v2.3AMF PG Strategy v2.3

1. Core Philosophy: Filtered and Volatility-Aware Trend Following

"AMF PG Strategy" is an advanced trend-following system designed to adapt to the dynamic nature of modern markets. The strategy's core philosophy is not just to follow the trend but also to wait for the right conditions to enter the market.

This is not a "black box." It is a rules-based framework that gives the user full control over various market filters. By requiring multiple conditions to be met simultaneously, the strategy aims to filter out low-quality signals and focus only on high-probability trend opportunities.

2. Core Engine: AMF PG Trend Following

At the heart of the strategy is a proprietary, volatility-aware trend-following mechanism called AMF PG (Praetorian Guard). This engine operates as follows:

Dynamic Bands: Creates a dynamic upper and lower band around the price that is constantly recalculated. The width of these bands is not fixed; It dynamically adjusts based on recent market volatility, volume flow, and price expansion. This adaptive structure allows the strategy to adapt to both calm and high-volatility markets.

Entry Signals: A buy signal is triggered when the price rises above the upper band. A sell signal is triggered when the price falls below the lower band. However, these signals are executed only when all the active filters described below give the green light.

Trailing Stop-Loss: When a position is entered, the opposite band automatically acts as a trailing stop-loss level. For example, when a buy position is opened, the lower band follows the price as a stop-loss. This allows for profit retention and trend continuation.

3. Multi-Layered Filter System: Understanding the Market

The power of this strategy comes from its modular filter system, which allows the user to filter market conditions based on their own analysis. Each filter can be enabled or disabled individually in the settings:

Filter 1: Trend Strength (ADX Filter): This filter confirms whether there is a strong trend in the market. It uses the ADX (Average Directional Index) indicator and only allows trades if the ADX value is above a certain threshold. This helps avoid trading in weak or directionless markets. It also confirms the direction of the trend by checking the position of the DMI (+DI and -DI) lines.

Filter 2: Sideways Market (Chop Index Filter): This filter determines whether the market is excessively choppy or directionless. Using the Chop Index, this filter aims to protect against fakeouts by blocking trades when the market is highly indecisive.

Filter 3: Market Structure (Hurst Exponent Filter): This is one of the strategy's most advanced filters. It analyzes the current market behavior using the Hurst Exponent. This mathematical tool attempts to determine whether a market tends to trend (permanent), tends to revert to the mean (anti-permanent), or moves randomly. This filter ensures that signals are generated only when market structure supports trending trades.

4. Risk Management: Maximum Drawdown Protection

This strategy includes a built-in capital protection mechanism. Users can specify the percentage of their capital they will tolerate to decline from its peak. If the strategy's capital reaches this set drawdown limit, the protection feature is activated, closing all open positions and preventing new trades from being opened. This acts as an emergency brake to protect capital against unexpected market conditions.

5. Automation Ready: Customizable Webhook Alerts

The strategy is designed for traders who want to automate their signals. From the Settings menu, you can configure custom alert messages in JSON format, compatible with third-party automation services (via Webhooks).

6. Strategy Backtest Information

Please note that past performance is not indicative of future results. The published chart and performance report were generated on the 4-hour timeframe of the BTCUSD pair with the following settings:

Test Period: January 1, 2016 - October 31, 2025

Default Position Size: 15% of Capital

Pyramiding: Closed

Commission: 0.0008

Slippage: 2 ticks (Please enter the slippage you used in your own tests)

Testing Approach: The published test includes 423 trades and is statistically significant. It is strongly recommended that you test on different assets and timeframes for your own analysis. The default settings are a template and should be adjusted by the user for their own analysis.

Bitcoin: Price projection from previous cycles onto 2024 cycleAn indicator for displaying the BITFINEX:BTCUSD price movement pattern from previous cycles onto the 2024–2025 cycle.

Best checked on Bitfinex or the “Brave New Coin – Bitcoin Liquid Index” (though that one has gone offline).

Next time it should be done with embedded constants rather than by copying candles from previous cycles.

Publishing to share the idea.

#1 Vishal Toora Buy Sell Tablecopyright Vishal Toora

**“© 2025 Vishal Toora — counting volumes so you don’t have to. Buy, sell, or just stare at the screen.”**

Or a few more playful options:

1. **“© Vishal Toora — making deltas speak louder than your ex.”**

2. **“© Vishal Toora — one signal to rule them all (Buy/Sell/Neutral).”**

3. **“© Vishal Toora — because guessing markets is so 2024.”**

Disclaimer: This indicator is for educational and informational purposes only. I do not claim 100% accuracy, and you are responsible for your own trading decisions.

Spooky Time (10/31/25) [VTB]Get ready to add some eerie fun to your charts this Halloween! "Spooky Time" is a lighthearted indicator that draws a festive, animated Halloween scene right on your TradingView chart. Perfect for traders who want to celebrate the spooky season without missing a beat on the markets. Whether you're analyzing stocks, crypto, or forex, this overlay brings a touch of holiday spirit to your setup.

#### Key Features:

- **Jack-o'-Lantern Pumpkin**: A detailed, glowing pumpkin with carved eyes, nose, and a jagged mouth. The eyes and mouth cycle through black (off), yellow, and red glows for a subtle animation effect, giving it that classic haunted vibe.

- **Flickering Candle**: A wax candle with a wick and an animated flame that shifts positions slightly across three frames, mimicking a real flickering light. The flame color changes between yellow, red, and orange for added dynamism.

- **Spider Web and Spider**: A spiral web with radial lines, complete with a creepy-crawly spider. The spider's legs animate with small movements, as if it's ready to pounce—perfect for that extra spooky touch!

- **Customization Options**: Toggle the "Desiringmachine" label on/off, choose its position on the chart (e.g., Bottom Center), and select the text color. The entire scene is positioned relative to the chart's open price and ATR for better scaling.

- **Animation Cycle**: The whole setup uses a simple 3-frame animation based on bar_index, making it feel alive without overwhelming your chart.

This indicator is purely visual and non-intrusive—it doesn't plot any trading signals or data, so it won't interfere with your strategies. Just add it to your chart for some Halloween cheer during your trading sessions!

**Date Note**: Timed for Halloween 2025 (10/31/25)—feel the spooky energy!

**Happy Halloween!!!** 🎃👻🕸️

iFVG Strategie by Futures.RobbyiFVG Strategy Checklist by Futures.Robby

Updated: October 27, 2025

Description

This script is a manual checklist designed to help traders evaluate their setups based on the iFVG (Fair Value Gap) strategy. It serves solely as a visual aid and does not perform automatic analysis, signal generation, or trade execution.

How It Works

The script creates an interactive checklist directly on the chart. Traders manually select which criteria are met, and the script calculates a percentage score, displaying it with color coding:

Green (≥ 60%): Good fulfillment of criteria

Orange (40–59%): Partial fulfillment

Red (< 40%): Poor fulfillment

Checklist Criteria

The checklist is divided into two main sections:

1. Trade Criteria (8 Points)

Eight manually selectable criteria to assess setup quality:

Trade im Bias → Trade in Bias: Trade follows the higher timeframe trend (H1/H4/Daily).

BE Level → BE Level: Swing point between entry and target.

Sweep → Sweep: Price hits a key swing before reversing.

Displacement → Displacement: iFVG broken by strong candles.

Leg FVG geschlossen → Leg FVG Closed: No open m1 to m5 FVGs to target.

FVG Reaktion → FVG Reaction: Reaction at FVG during sweep (HTF).

FVG Größe → FVG Size: 6 to 10 points.

Anzahl Kerzen → Number of Candles: Maximum of 6 candles.

2. Goals (1 Point)

Six optional goal conditions, counted together as 1 point:

Equal H / L → Equal High/Low

Session H / L → Session High/Low

News H / L → News High/Low

HTF Swing Point → HTF Swing Point

HTF OB → HTF Order Block

HTF FVG → HTF FVG

Settings and Customization

The script’s settings are translated as follows:

Group: Trade Criteria

Trade im Bias → Trade in Bias

Tooltip: Trendrichtung folgt HTF (H1/H4/Täglich) – Trend follows HTF direction

BE Level → BE Level

Tooltip: Swingpunkt zwischen Einstieg und Ziel – Swing point between entry and target

Sweep → Sweep

Tooltip: Kurs erreicht markanten Swing – Price hits key swing before inverse

Displacement → Displacement

Tooltip: iFVG durch starke Kerzen gebrochen – iFVG broken by strong candles

Leg FVG geschlossen → Leg FVG Closed

Tooltip: Keine offenen m1 bis m5 FVGs bis Ziel – No open m1 to m5 FVGs to target

FVG Reaktion → FVG Reaction

Tooltip: Reaktion an FVG beim Sweep (HTF) – Reaction at FVG during sweep (HTF)

FVG Größe → FVG Size

Tooltip: 6 bis 10 Punkte – 6 to 10 points

Anzahl Kerzen → Number of Candles

Tooltip: Maximal 6 Kerzen – Maximum of 6 candles

Group: Goals

Equal H / L → Equal High/Low

Session H / L → Session High/Low

News H / L → News High/Low

HTF Swing Point → HTF Swing Point

HTF OB → HTF Order Block

HTF FVG → HTF FVG

ℹ️ Ziele zählen gemeinsam als 1 Punkt → ℹ️ Goals count together as 1 point

Window Position & Size

Fensterposition → Window Position

oben rechts → top right

oben links → top left

unten rechts → bottom right

unten links → bottom left

Tabellengröße → Table Size

normal → normal

small → small

tiny → tiny

Translation of Chart Table Contents

The table headers and entries on the chart are translated as follows:

Table Headers:

Trade Checkliste → Trade Checklist

Ziele → Goals

Status Symbols:

✅ → ✅ (Fulfilled)

❌ → ❌ (Not fulfilled)

Individual Criteria (Trade Criteria):

Trade im Bias → Trade in Bias

BE Level → BE Level

Sweep → Sweep

Displacement → Displacement

Leg FVG geschlossen → Leg FVG Closed

FVG Reaktion → FVG Reaction

FVG Größe → FVG Size

Anzahl Kerzen → Number of Candles

Individual Criteria (Goals):

Equal H / L → Equal High/Low

Session H / L → Session High/Low

News H / L → News High/Low

HTF Swing Point → HTF Swing Point

HTF OB → HTF Order Block

HTF FVG → HTF FVG

Note Line:

Ziele zählen gemeinsam als 1 Punkt → Goals count together as 1 point

Important Note

This tool is not an automated indicator, but a visual decision aid for traders who want to apply their strategy in a structured and conscious way.

Flux AI PullBack System (Hybrid Pro)Flux AI PullBack System (Hybrid Pro)

//Session-Aware | Adaptive Confluence | Grace Confirm Logic//

Overview:

The Flux AI PullBack System (Hybrid Pro v5) is an adaptive, session-aware pullback indicator designed to identify high-probability continuation setups within trending markets. It automatically adjusts between “Classic” and “Enhanced” logic modes based on volatility, volume, and ATR slope, allowing it to perform seamlessly across different market sessions (Asian, London, and New York).

Core Features:

Hybrid Auto Mode — Dynamically switches between Classic (fast-moving) and Enhanced (strict) modes.

Session-Aware Context — Optimized for intraday trading in ES, NQ, and SPY.

Grace Confirmation Logic — Validates pullbacks with a follow-through condition to reduce noise.

Adaptive EMA Zone (38/62) — Highlights pullback areas with dynamic aqua fill and transparency linked to trend strength.

Noise Suppression Filter — Prevents false pullbacks during EMA crossovers or unstable transitions.

Weighted Confluence Model — Combines trend, ATR, volume, and swing structure for confirmation strength.

Pine v6 Compliant Alerts — Constant-string safe, ready for webhooks and automation.

Visual Elements:

Aqua EMA Zone: Displays the “breathing” pullback band (tightens during volatility spikes).

PB↑ / PB↓ Markers: Confirmed pullbacks with subtle transparency and fixed label size.

Bar Highlights: Yellow for pullbacks; ice-blue for confirmed continuation.

Use Cases

Perfect for:

Intraday trend traders

0DTE SPX / ES scalpers

Futures traders (NQ, MNQ, MES)

Algorithmic strategy builders using webhooks

Recommended Timeframes:

1–15 minute charts (scalping / intraday)

Higher timeframes for swing confirmations.

Attribution:

This open-source script was inspired by Chris Moody’s “CM Slingshot System” and JustUncleL’s Pullback Tools, but it was built from scratch using AI-assisted code refinement (ChatGPT).

All logic and enhancements are original, not derived from proprietary software.

License: MIT (Open Source)

© 2025 Ken Anderson — You may modify, use, or redistribute with credit.

Keywords:

Pullback, Reversal, AI Trading, EMA Zone, Session Aware, Futures Trading, SPX, ES, NQ, ATR Filter, Volume Confirmation, Flux System, Pine Script v6, Non-Repainting, Adaptive Trading Indicator.

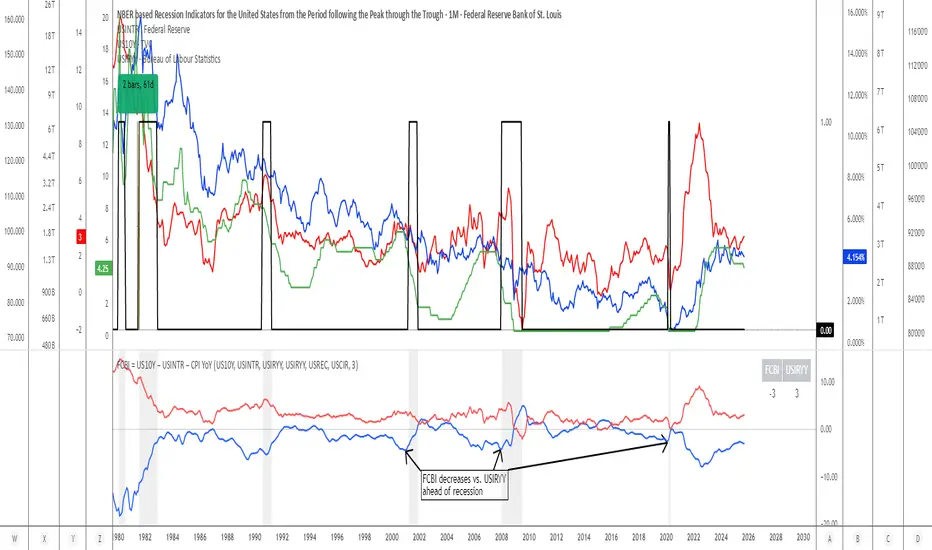

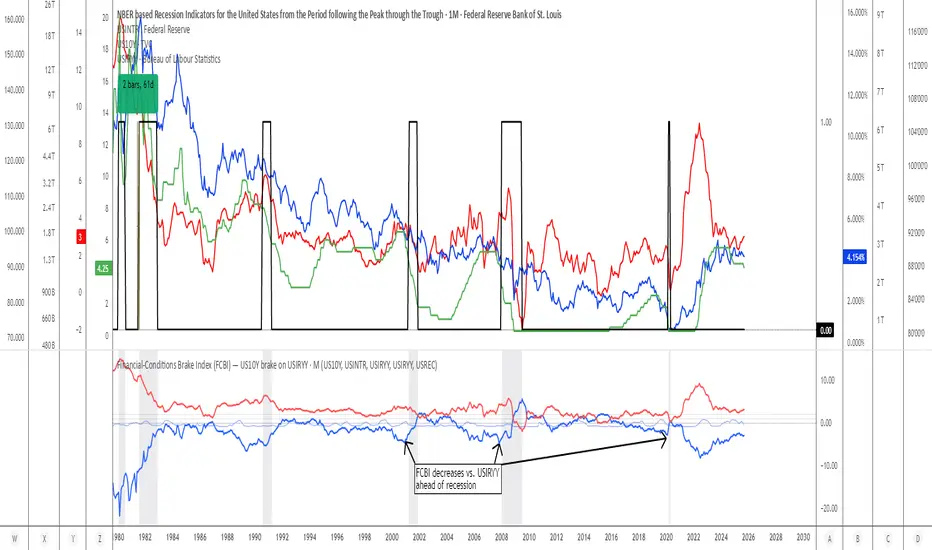

FCBI Brake PressureBrake Pressure (FCBI − USIRYY)

Concept

The Brake Pressure indicator quantifies whether the bond market is braking or releasing liquidity relative to real yields (USIRYY).

It is derived from the Financial-Conditions Brake Index (FCBI) and expresses the balance between long-term yield pressure and real-rate dynamics.

Formula

Brake Pressure = FCBI − USIRYY

where FCBI = (US10Y) − (USINTR) − (CPI YoY)

Purpose

While FCBI measures the intensity of financial-condition pressure, Brake Pressure shows when that brake is being applied or released.

It captures the turning point of liquidity transmission in the financial system.

How to Read

Brake Pressure < 0 (orange) → Brake engaged → financial conditions tighter than real-rate baseline; liquidity constrained.

Brake Pressure ≈ 0 → Neutral zone → transition phase between tightening and easing.

Brake Pressure > 0 (teal) → Brake released → financial conditions looser than real-rate baseline; liquidity flows freely → late-cycle setup before recession.

Zero-Cross Logic

Cross ↑ above 0 → FCBI > USIRYY → brake released → liquidity acceleration → typically 6–18 months before recession.

Cross ↓ below 0 → FCBI < USIRYY → brake re-engaged → tightening resumes.

Historical Behavior

Each major U.S. recession (2001, 2008, 2020) was preceded by a Brake Pressure cross above zero after a negative phase, signaling that long yields had stopped resisting Fed cuts and liquidity was expanding.

Practical Use

• Identify late-cycle turning points and liquidity inflection phases.

• Combine with FCBI for a complete macro transmission picture.

• Watch for sustained positive readings as early macro-recession warnings.

Current Example (Oct 2025)

FCBI ≈ −3.1, USIRYY ≈ +3.0 → Brake Pressure ≈ −6.1 → Brake still engaged. When this crosses above 0, it signals that liquidity is free flowing and the recession countdown has begun.

Summary

FCBI shows how tight the brake is. Brake Pressure shows when the brake releases.

When Brake Pressure > 0, the system has entered the liquidity-expansion phase that historically precedes a U.S. recession.

Financial-Conditions Brake Index (FCBI) — US10Y brake on USIRYYFinancial-Conditions Brake Index (FCBI) – US10Y Brake on USIRYY

Concept

The Financial-Conditions Brake Index (FCBI) measures how U.S. long-term yields (US10Y) interact with the Federal Funds Rate (USINTR) and inflation (CPI YoY) to shape real-rate conditions (USIRYY).

It visualizes whether the bond market is tightening or loosening overall financial conditions relative to the Federal Reserve’s policy stance.

Formula

FCBI = (US10Y) − (USINTR) − (CPI YoY)

How It Works

The FCBI expresses the difference between the long-term yield curve and short-term policy rates, adjusted for inflation. It shows whether the long end of the curve is amplifying or counteracting the Fed’s stance.

FCBI > +2 → Strong brake → Long yields remain elevated despite easing → tight conditions → recession delayed.

FCBI +1 to +2 → Mild brake → Financial transmission slower; lag ≈ 12–18 months.

FCBI 0 to +1 → Neutral → Typical early post-cut environment.

FCBI < 0 → Accelerator → Long yields and inflation expectations falling → liquidity flows freely → recession often follows within 6–14 months.

How to Read the Chart

Blue line (FCBI) shows the strength of the financial brake.

Red line (USIRYY) represents the real yield baseline.

Recession shading (gray) marks NBER recessions for comparison.

FCBI < USIRYY → Brake engaged → financial conditions tighter than real-rate baseline.

FCBI > USIRYY → Brake released → long end easing faster than policy → liquidity surge → late-cycle setup.

Historically, U.S. recessions begin on average about 14 months after the first Fed rate cut, and a decline of the FCBI below zero often precedes that window.

Practical Use

Use the FCBI to identify when policy transmission is blocked (brake engaged) or flowing (brake released).

Cross-check with yield-curve inversions, Fed policy shifts, and inflation expectations to estimate macro timing windows.

Current Example (Oct 2025)

FCBI ≈ −3.1, USIRYY ≈ +3.0 → Brake still engaged.