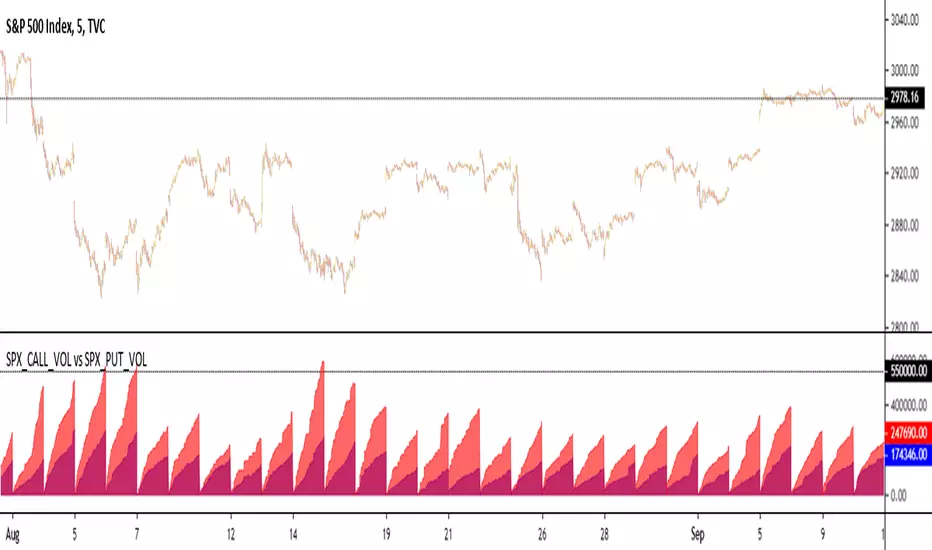

Up Volume vs Down VolumeCalculating NYSE Up Volume (UPVOL.NY) vs NYSE Down Volume (DNVOL.NY). The triangles appear when the ratio exceeds 90% in either direction.

Also has the option to switch to NQ, US, DJ, AM, or AX tickers.

Credit to @MagicEins for the original script:

Pesquisar nos scripts por "乌德勒支+VS+赫拉克勒斯"

ATR vs Day Trading Range and PercentageThis indicator displays the Current Daily ATR vs the current Day Range and displays the percentage.

For example if the Daily ATR is $5 and the current range of the day is $10 this would be 200% the original move.

It is color coded (and can be modified) to change color when the Daily range is over 100% the ATR.

The time frame can be changed from Daily just be aware you must be on a lower timeframe then selected. So if you want to compare the current 30 minute ATR to the current 30 minute range you will need to be showing a 30 min chart or lower for it to calculate correctly.

3GBH BTC DOM vs MCBitcoin Market Cap vs Dominance

- data normalized with RSI

Included in this indicator:

- RSI of BTC Market Cap

- RSI of BTC Dominance

- EMA of BTC Market Cap

- EMA of BTC Domiance

-----

Dominance influences the market. Is money flowing into Bitcoin?

-----

EMA's to help with Technical Analysis.

-----

User-friendly.

You can change all the inputs, they are labelled for ease-of-use.

You can toggle On/Off any or all of the options.

Higher vs Lower Pivots overlayA simple script that I made that draws lines between the high and low pivots. The color of the line define if the pivot is higher or lower than the previous pivot. The main thing to tune is the pivot look back vs look ahead, which are the same params used by the tradingview pivot indicator. There are several other params you can tweaks to get the look you want.

DTR vs ATR w RVolDTR vs ART along with Relative Volume in Percentage. So if you see RVol as 200% with input length of 10 days, today's volume is 2x compared to past 10 days. It helps if today's volume is already reached 20% or 30% within 30mins of market open, etc.

Perp vs Spot Delta (Bybit-CB)Simple script showing the delta of Bybit BTCUSD perp vs Coinbase BTCUSD spot. Orange positive candles show bybit is higher, blue negative candles show Coinbase is higher.

LER - Law of Effort vs ResultsLaw of Effort vs Results is a tool to find the price changes based on volume.

This tool shows that if there is a high volume occur but the price has small difference in one candle, this will trigger a 'spike'. This spike represents that a high activity has occurred but the price did not reflect as the volume changes.

The analogy of this tool can be represented as we drive a car on a steep hill: despite we hit the gas harder, the car just slightly move higher.

NYSE Volume UP FLOW VS Down FLOW ULTIMATE VOLDNYSE Volume UP FLOW VS Down FLOW ULTIMATE StokedStocks

BASED OFF THE VOLD INDEX

The VOLD (also $VOLD) is the difference between the up volume and down volume on the NYSE. i.e. NYSE $UVOL minus $DVOL; the net up volume.

If you consider that VOLD is the net value between UVOL (up volume) and DVOL (down volume) then you need to understand these two to understand VOLD.

UVOL or DVOL are a total of the volume on all stocks that are up or down in price. Up or down is based on the previous session's closing price. The size of the stock's price change is irrelevant.

If the stock is up only $.01, then its volume is grouped into the UVOL total. If that stock's price then drops by $.02 it will be down $.01 and the day's volume for that stock will now be grouped with the DVOL total.

Note that when a stock moves from being an up stock to a down stock its volume will be removed from the UVOL total and added to the DVOL total. Say the stocks volume is 1 million shares when it moves from up to down. The DVOL will increase by 1 million and the UVOL will decrease by 1 million which means that VOLD will decrease by 2 million.

NYSE Up/Down Volume Ratio is often used as a barometer for stocks trading on all U.S. Exchanges even though it is calculated based on stocks listed on the New York Stock Exchange.

NYSE Up/Down ratio represents the volume of NYSE stocks that are advancing divided by the volume of declining stocks.

The volume of advancing stocks or upside volume is the sum of the volume or the number of shares traded associated with stocks that closed higher.

The downside volume is the total number of shares traded that are associated with stocks that closed lower.

The interpretation of the NYSE Up/Down ratio is rather simple. A value higher than one indicates that there is more volume associated with up stocks than with down stocks and it is usually interpreted as a bullish signal.

Obviously, a bearish signal occurs when the NYSE Up/Down ratio is lower than one, which tells us that there are more volume associated with down stocks than with up stocks.

Check out my other indicators and website stokedstocks.wordpress.com for tons of free stock training books and pictures and settings

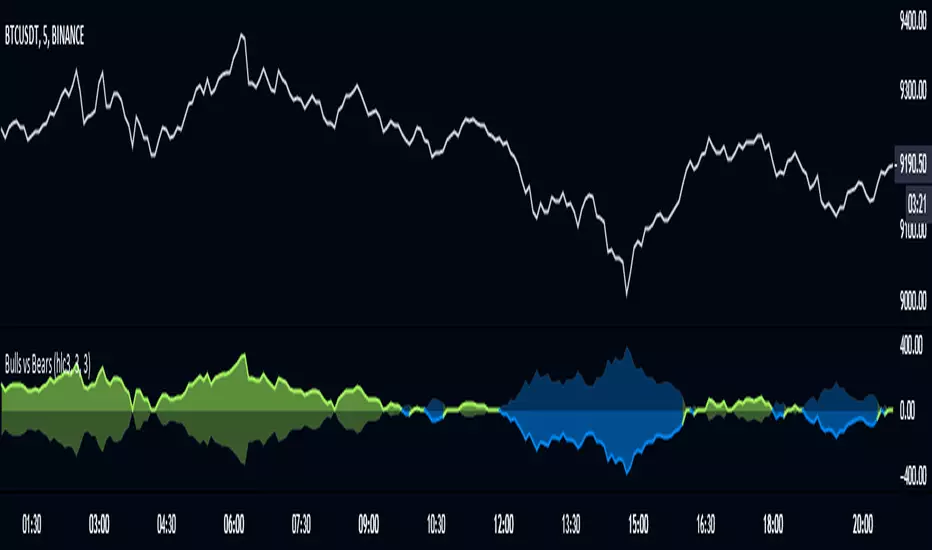

Bulls vs BearsThe script measures relative strenth of bull bars vs bear bars that complete the next rules:

1) rising price with rising volume calculates as bullish only if the next candle is higher

2) falling price with falling volume calculates as bullish only if the next candle is higher

3) rising price with falling volume calculates as bearish only if the next candle is lower

4) falling price with rising volume calculates as bearish only if the next candle is lower

examples

ethusdt

shitperp

bsvusdt

btcusdt

Strategy VS Buy & HoldSUMMARY:

A strategy wrapper that makes a detailed and visual comparison between a given strategy and the buy & hold returns of the traded security.

DESCRIPTION:

TradingView has a "Buy & Hold Return" metric in the strategy tester that is often enough to assess how our strategy compares to a simple buy hold. However, one may want more information on how and when your strategy beats or is beaten by a simple buy & hold strategy. This script aims to show such detail by providing a more comprehensive metrics and charting the profit/loss of the given strategy against buy & hold.

As seen in the script, it plots/draws 4 elements:

1) Strategy P/L: strategy net profit + strategy open profit

2) Buy & Hold P/L: unrealized return

3) Difference: Strategy P/L - Buy & Hold P/L

4) Strategy vs Buy Hold Stats

> Percent of bars strategy P/L is above Buy & Hold

> Percent of bars strategy P/L is below Buy & Hold

> All Time Average Difference

ADJUSTABLE PARAMETERS:

All labels/panels can be disabled by unchecking these two options:

>bnh_info_panel = input(true, title='Enable Info Panel')

>bnh_indicator_panel = input(true, title='Enable Indicator Panel')

Comparison Date Range can be changed to better isolate specific areas:

>From Year, From Month, From Day

default: 1970 01 01

>To Year, To Month, To Day

default: 2050 12 31

Default settings basically covers all historical data.

HOW TO USE:

The default script contains a simple 50-200 SMA cross strategy, just delete and replace it. Those are everything between these lines:

/////////////////////////////////////////////////////////////////////////////////////

//////////////////////////////STRATEGY SCRIPT START//////////////////////////////////

(STRATEGY SCRIPT GOES HERE)

//////////////////////////////STRATEGY SCRIPT END////////////////////////////////////

/////////////////////////////////////////////////////////////////////////////////////

Removing all plots and drawings from your strategy is advisable.

If you are going to use the Comparison Date Range, apply "bnh_timeCond" to your strategy to align the dates. A sample on how it’s applied can be seen on the Placeholder MA cross strategy.

Note: bnh_timeCond returns a boolean series

High and lows round vs full numbersLiterally the name, just checks if a high or low is a full number or decimal (i.e 100.5) then shows the percentage of full number highs vs percentage of full number lows.

I couldn't really find anything useful with it but maybe someone else can

Range: OHLC vs Previous OHLC - Version 2Version 1 here -

This is essentially the same as version 1 with one update. You have the freedom to independently choose OHLC for current candle and prior candle.

To elaborate further, Version 1 had 1 choice. For example, Close; you could only compare the close of prior candle to the current candle.

Version 2; you can compare close of the current candle to the low of the prior candle.

stock gain% vs index gain %This shows the relative strength or weakness of a stock vs an index on any given candle price movement.

Negative stock candle and relative strength shows accumulation

Positive stock candle and relative weakness shows distribution

accumulation will plot an 'A'

distribution will plot a 'D'

Range: OHLC vs Previous OHLCThis will plot your choice of OHLC (or any of the averaging choices) of the current candle compared to the previous candle.

For example if you choose "high" for the input and set the chart to daily, you'll see the currently daily high vs the previous daily high.

Green candle represent a higher high and the length of the candle represents how much higher.

Red candles represent a lower high than the previous day and the length is by how much lower.

This indicator is pretty straight forward, look for me to build on this with something a little more elaborate in the near future.

200/100 vs 190/80 EMA [jarederaj]Track the 200/100 EMA cross Vs the 180/90 EMA cross. Also, see the dates when these periods start on the chart.

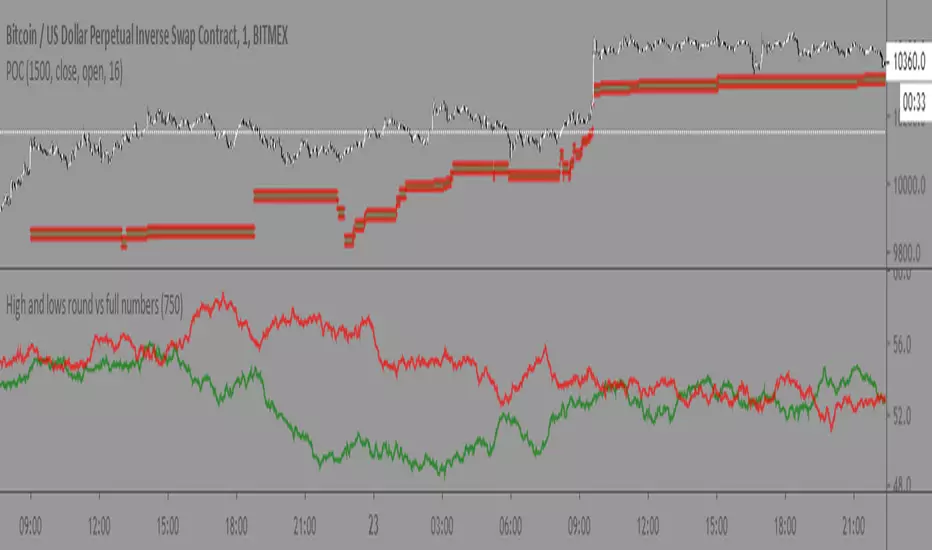

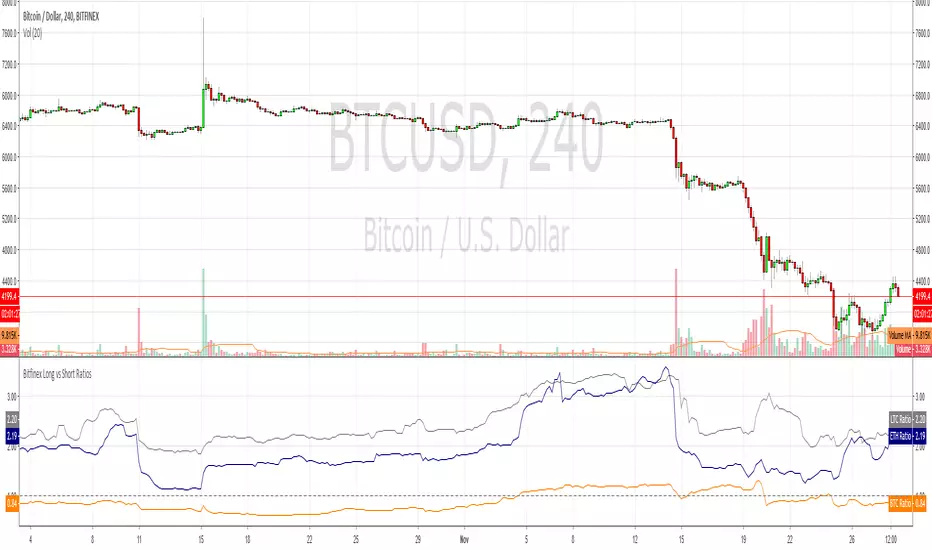

Bitfinex Long vs Short RatiosWas impressed with the 'Longs vs Shorts Ratio' idea from the tweet below so I coded an indicator, enjoy.

twitter.com

Compare - Oscillator vs BTC momentumI've made a simple indicator to compare the momentum of a trading pair against the momentum of BTC to the dollar. I use it to see how a pair is affected by BTC's momentum... I wouldnt use it to trade off alone, but it can be a useful tool alongside other indicators.

The time range can be adjusted, but I wouldnt reccomend setting it to anything over 12M, or under 1W.... as I'm not sure if it would work.

Any feedback is welcome!

This is an idea I had after looking at a wonderful visualisation made by BarclayJames, link below:

www.tradingview.com

비트코인 한국 프리미엄 캔들 차트 (Bithumb vs Bitfinex) by 호재박스 슈퍼스타지표명: 비트코인 한국 프리미엄 캔들 차트 (Bithumb vs Bitfinex)

제작자: 호재박스 슈퍼스타

홈페이지: hozaebox.com