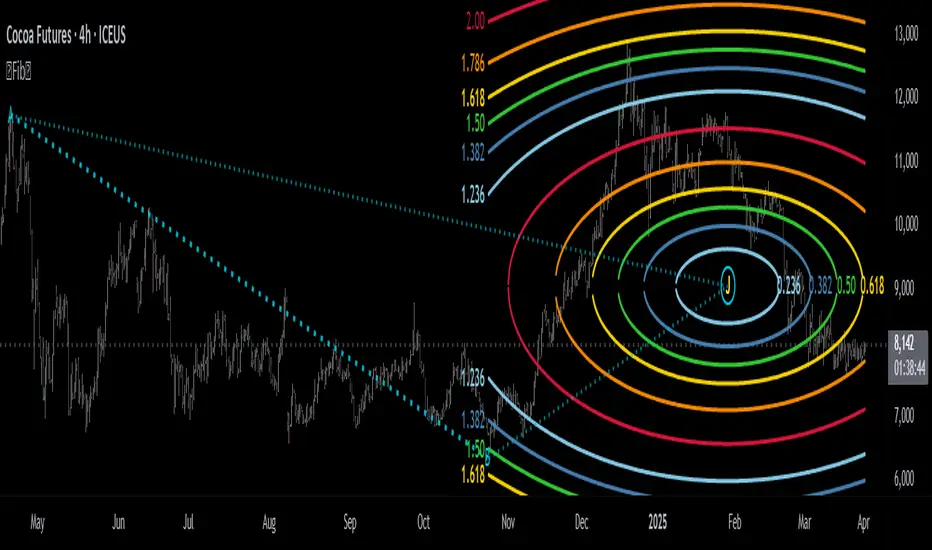

Fibonacci Circle Zones🟩 The Fibonacci Circle Zones indicator is a technical visualization tool, building upon the concept of traditional Fibonacci circles. It provides configurable options for analyzing geometric relationships between price and time, used to identify potential support and resistance zones derived from circle-based projections. The indicator constructs these Fibonacci circles based on two user-selected anchor points (Point A and Point B), which define the foundational price range and time duration for the geometric analysis.

Key features include multiple mathematical Circle Formulas for radius scaling and several options for defining the circle's center point, enabling exploration of complex, non-linear geometric relationships between price and time distinct from traditional linear Fibonacci analysis. Available formulas incorporate various mathematical constants (π, e, φ variants, Silver Ratio) alongside traditional Fibonacci ratios, facilitating investigation into different scaling hypotheses. Furthermore, selecting the Center point relative to the A-B anchors allows these circular time-price patterns to be constructed and analyzed from different geometric perspectives. Analysis can be further tailored through detailed customization of up to 12 Fibonacci levels, including their mathematical values, colors, and visibility..

📚 THEORY and CONCEPT 📚

Fibonacci circles represent an application of Fibonacci principles within technical analysis, extending beyond typical horizontal price levels by incorporating the dimension of time. These geometric constructions traditionally use numerical proportions, often derived from the Fibonacci sequence, to project potential zones of price-time interaction, such as support or resistance. A theoretical understanding of such geometric tools involves considering several core components: the significance of the chosen geometric origin or center point , the mathematical principles governing the proportional scaling of successive radii, and the fundamental calculation considerations (like chart scale adjustments and base radius definitions) that influence the resulting geometry and ensure its accurate representation.

⨀ Circle Center ⨀

The traditional construction methodology for Fibonacci circles begins with the selection of two significant anchor points on the chart, usually representing a key price swing, such as a swing low (Point A) and a subsequent swing high (Point B), or vice versa. This defined segment establishes the primary vector—representing both the price range and the time duration of that specific market move. From these two points, a base distance or radius is derived (this calculation can vary, sometimes using the vertical price distance, the time duration, or the diagonal distance). A center point for the circles is then typically established, often at the midpoint (time and price) between points A and B, or sometimes anchored directly at point B.

Concentric circles are then projected outwards from this center point. The radii of these successive circles are calculated by multiplying the base distance by key Fibonacci ratios and other standard proportions. The underlying concept posits that markets may exhibit harmonic relationships or cyclical behavior that adheres to these proportions, suggesting these expanding geometric zones could highlight areas where future price movements might decelerate, reverse, or find equilibrium, reflecting a potential proportional resonance with the initial defining swing in both price and time.

The Fibonacci Circle Zones indicator enhances traditional Fibonacci circle construction by offering greater analytical depth and flexibility: it addresses the origin point of the circles: instead of being limited to common definitions like the midpoint or endpoint B, this indicator provides a selection of distinct center point calculations relative to the initial A-B swing. The underlying idea is that the geometric source from which harmonic projections emanate might vary depending on the market structure being analyzed. This flexibility allows for experimentation with different center points (derived algorithmically from the A, B, and midpoint coordinates), facilitating exploration of how price interacts with circular zones anchored from various perspectives within the defining swing.

Potential Center Points Setup : This view shows the anchor points A and B , defined by the user, which form the basis of the calculations. The indicator dynamically calculates various potential Center points ( C through N , and X ) based on the A-B structure, representing different geometric origins available for selection in the settings.

Point X holds particular significance as it represents the calculated midpoint (in both time and price) between A and B. This 'X' point corresponds to the default 'Auto' center setting upon initial application of the indicator and aligns with the centering logic used in TradingView's standard Fibonacci Circle tool, offering a familiar starting point.

The other potential center points allow for exploring circles originating from different geometric anchors relative to the A-B structure. While detailing the precise calculation for each is beyond the scope of this overview, they can be broadly categorized: points C through H are derived from relationships primarily within the A-B time/price range, whereas points I through N represent centers projected beyond point B, extrapolating the A-B geometry. Point J, for example, is calculated as a reflection of the A-X midpoint projected beyond B. This variety provides a rich set of options for analyzing circle patterns originating from historical, midpoint, and extrapolated future anchor perspectives.

Default Settings (Center X, FibCircle) : Using the default Center X (calculated midpoint) with the default FibCircle . Although circles begin plotting only after Point B is established, their curvature shows they are geometrically centered on X. This configuration matches the standard TradingView Fib Circle tool, providing a baseline.

Centering on Endpoint B : Using Point B, the user-defined end of the swing, as the Center . This anchors the circular projections directly to the swing's termination point. Unlike centering on the midpoint (X) or start point (A), this focuses the analysis on geometric expansion originating precisely from the conclusion of the measured A-B move.

Projected Center J : Using the projected Point J as the Center . Its position is calculated based on the A-B swing (conceptually, it represents a forward projection related to the A-X midpoint relationship) and is located chronologically beyond Point B. This type of forward projection often allows complete circles to be visualized as price develops into the corresponding time zone.

Time Symmetry Projection (Center L) : Uses the projected Point L as the Center . It is located at the price level of the start point (A), projected forward in time from B by the full duration of the A-B swing . This perspective focuses analysis on temporal symmetry , exploring geometric expansions from a point representing a full time cycle completion anchored back at the swing's origin price level.

⭕ Circle Formula

Beyond the center point , the expansion of the projected circles is determined by the selected Circle Formula . This setting provides different mathematical methods, or scaling options , for scaling the circle radii. Each option applies a distinct mathematical constant or relationship to the base radius derived from the A-B swing, allowing for exploration of various geometric proportions.

eScaled

Mathematical Basis: Scales the radius by Euler's number ( e ≈ 2.718), the base of natural logarithms. This constant appears frequently in processes involving continuous growth or decay.

Enables investigation of market geometry scaled by e , exploring relationships potentially based on natural exponential growth applied to time-price circles, potentially relevant for analyzing phases of accelerating momentum or volatility expansion.

FibCircle

Mathematical Basis: Scales the radius to align with TradingView’s built-in Fibonacci Circle Tool.

Provides a baseline circle size, potentially emulating scaling used in standard drawing tools, serving as a reference point for comparison with other options.

GoldenFib

Mathematical Basis: Scales the radius by the Golden Ratio (φ ≈ 1.618).

Explores the fundamental Golden Ratio proportion, central to Fibonacci analysis, applied directly to circular time-price geometry, potentially highlighting zones reflecting harmonic expansion or retracement patterns often associated with φ.

GoldenContour

Mathematical Basis: Scales the radius by a factor derived from Golden Ratio geometry (√(1 + φ²) / 2 ≈ 0.951). It represents a specific geometric relationship derived from φ.

Allows analysis using proportions linked to the geometry of the Golden Rectangle, scaled to produce circles very close to the initial base radius. This explores structural relationships often associated with natural balance or proportionality observed in Golden Ratio constructions.

SilverRatio

Mathematical Basis: Scales the radius by the Silver Ratio (1 + √2 ≈ 2.414). The Silver Ratio governs relationships in specific regular polygons and recursive sequences.

Allows exploration using the proportions of the Silver Ratio, offering a significant expansion factor based on another fundamental metallic mean for comparison with φ-based methods.

PhiDecay

Mathematical Basis: Scales the radius by φ raised to the power of -φ (φ⁻ᵠ ≈ 0.53). This unique exponentiation explores a less common, non-linear transformation involving φ.

Explores market geometry scaled by this specific phi-derived factor which is significantly less than 1.0, offering a distinct contractile proportion for analysis, potentially relevant for identifying zones related to consolidation phases or decaying momentum.

PhiSquared

Mathematical Basis: Scales the radius by φ squared, normalized by dividing by 3 (φ² / 3 ≈ 0.873).

Enables investigation of patterns related to the φ² relationship (a key Fibonacci extension concept), visualized at a scale just below 1.0 due to normalization. This scaling explores projections commonly associated with significant trend extension targets in linear Fibonacci analysis, adapted here for circular geometry.

PiScaled

Mathematical Basis: Scales the radius by Pi (π ≈ 3.141).

Explores direct scaling by the fundamental circle constant (π), investigating proportions inherent to circular geometry within the market's time-price structure, potentially highlighting areas related to natural market cycles, rotational symmetry, or full-cycle completions.

PlasticNumber

Mathematical Basis: Scales the radius by the Plastic Number (approx 1.3247), the third metallic mean. Like φ and the Silver Ratio, it is the solution to a specific cubic equation and relates to certain geometric forms.

Introduces another distinct fundamental mathematical constant for geometric exploration, comparing market proportions to those potentially governed by the Plastic Number.

SilverFib

Mathematical Basis: Scales the radius by the reciprocal Golden Ratio (1/φ ≈ 0.618).

Explores proportions directly related to the core 0.618 Fibonacci ratio, fundamental within Fibonacci-based geometric analysis, often significant for identifying primary retracement levels or corrective wave structures within a trend.

Unscaled

Mathematical Basis: No scaling applied.

Provides the base circle defined by points A/B and the Center setting without any additional mathematical scaling, serving as a pure geometric reference based on the A-B structure.

🧪 Advanced Calculation Settings

Two advanced settings allow further refinement of the circle calculations: matching the chart's scale and defining how the base radius is calculated from the A-B swing.

The Chart Scale setting ensures geometric accuracy by aligning circle calculations with the chart's vertical axis display. Price charts can use either a standard (linear) or logarithmic scale, where vertical distances represent price changes differently. The setting offers two options:

Standard : Select this option when the price chart's vertical axis is set to a standard linear scale.

Logarithmic : It is necessary to select this option if the price chart's vertical axis is set to a logarithmic scale. Doing so ensures the indicator adjusts its calculations to maintain correct geometric proportions relative to the visual price action on the log-scaled chart.

The Radius Calc setting determines how the fundamental base radius is derived from the A-B swing, offering two primary options:

Auto : This is the default setting and represents the traditional method for radius calculation. This method bases the radius calculation on the vertical price range of the A-B swing, focusing the geometry on the price amplitude.

Geometric : This setting provides an alternative calculation method, determining the base radius from the diagonal distance between Point A and Point B. It considers both the price change and the time duration relative to the chart's aspect ratio, defining the radius based on the overall magnitude of the A-B price-time vector.

This choice allows the resulting circle geometry to be based either purely on the swing's vertical price range ( Auto ) or on its combined price-time movement ( Geometric ).

🖼️ CHART EXAMPLES 🖼️

Default Behavior (X Center, FibCircle Formula) : This configuration uses the midpoint ( Center X) and the FibCircle scaling Formula , representing the indicator's effective default setup when 'Auto' is selected for both options initially. This is designed to match the output of the standard TradingView Fibonacci Circle drawing tool.

Center B with Unscaled Formula : This example shows the indicator applied to an uptrend with the Center set to Point B and the Circle Formula set to Unscaled . This configuration projects the defined levels (0.236, 0.382, etc.) as arcs originating directly from the swing's termination point (B) without applying any additional mathematical scaling from the formulas.

Visualization with Projected Center J : Here, circles are centered on the projected point J, calculated from the A-B structure but located forward in time from point B. Notice how using this forward-projected origin allows complete inner circles to be drawn once price action develops into that zone, providing a distinct visual representation of the expanding geometric field compared to using earlier anchor points. ( Unscaled formula used in this example).

PhiSquared Scaling from Endpoint B : The PhiSquared scaling Formula applied from the user-defined swing endpoint (Point B). Radii expand based on a normalized relationship with φ² (the square of the Golden Ratio), creating a unique geometric structure and spacing between the circle levels compared to other formulas like Unscaled or GoldenFib .

Centering on Swing Origin (Point A) : Illustrates using Point A, the user-defined start of the swing, as the circle Center . Note the significantly larger scale and wider spacing of the resulting circles. This difference occurs because centering on the swing's origin (A) typically leads to a larger base radius calculation compared to using the midpoint (X) or endpoint (B). ( Unscaled formula used).

Center Point D : Point D, dynamically calculated from the A-B swing, is used as the origin ( Center =D). It is specifically located at the price level of the swing's start point (A) occurring precisely at the time coordinate of the swing's end point (B). This offers a unique perspective, anchoring the geometric expansion to the initial price level at the exact moment the defining swing concludes. ( Unscaled formula shown).

Center Point G : Point G, also dynamically calculated from the A-B swing, is used as the origin ( Center =G). It is located at the price level of the swing's endpoint (B) occurring at the time coordinate of the start point (A). This provides the complementary perspective to Point D, anchoring the geometric expansion to the final price level achieved but originating from the moment the swing began . As observed in the example, using Point G typically results in very wide circle projections due to its position relative to the core A-B action. ( Unscaled formula shown).

Center Point I: Half-Duration Projection : Using the dynamically calculated Point I as the Center . Located at Point B's price level but projected forward in time by half the A-B swing duration , Point I's calculated time coordinate often falls outside the initially visible chart area. As the chart progresses, this origin point will appear, revealing large, sweeping arcs representing geometric expansions based on a half-cycle temporal projection from the swing's endpoint price. ( Unscaled formula shown).

Center Point M : Point M, also dynamically calculated from the A-B swing, serves as the origin ( Center =M). It combines the midpoint price level (derived from X) with a time coordinate projected forward from Point B by the full duration of the A-B swing . This perspective anchors the geometric expansion to the swing's balance price level but originates from the completion point of a full temporal cycle relative to the A-B move. Like other projected centers, using M allows for complete circles to be visualized as price progresses into its time zone. ( SilverFib formula shown).

Geometric Validation & Functionality : Comparing the indicator (red lines), using its default settings ( Center X, FibCircle Formula ), against TradingView's standard Fib Circle tool (green lines/white background). The precise alignment, particularly visible at the 1.50 and 2.00 levels shown, validates the core geometry calculation.

🛠️ CONFIGURATION AND SETTINGS 🛠️

The Fibonacci Circle Zones indicator offers a range of configurable settings to tailor its functionality and visual representation. These options allow customization of the circle origin, scaling method, level visibility, visual appearance, and input points.

Center and Formula

Settings for selecting the circle origin and scaling method.

Center : Dropdown menu to select the origin point for the circles.

Auto : Automatically uses point X (the calculated midpoint between A and B).

Selectable points including start/end (A, B), midpoint (X), plus various points derived from or projected beyond the A-B swing (C-N).

Circle Formula : Dropdown menu to select the mathematical method for scaling circle radii.

Auto : Automatically selects a default formula ('FibCircle' if Center is 'X', 'Unscaled' otherwise).

Includes standard Fibonacci scaling ( FibCircle, GoldenFib ), other mathematical constants ( PiScaled, eScaled ), metallic means ( SilverRatio ), phi transformations ( PhiDecay, PhiSquared ), and others.

Fib Levels

Configuration options for the 12 individual Fibonacci levels.

Advanced Settings

Settings related to core calculation methods.

Radius Calc : Defines how the base radius is calculated (e.g., 'Auto' for vertical price range, 'Geometric' for diagonal price-time distance).

Chart Scale : Aligns circle calculations with the chart's vertical axis setting ('Standard' or 'Logarithmic') for accurate visual proportions.

Visual Settings

Settings controlling the visual display of the indicator elements.

Plots : Dropdown controlling which parts of the calculated circles are displayed ( Upper , All , or Lower ).

Labels : Dropdown controlling the display of the numerical level value labels ( All , Left , Right , or None ).

Setup : Dropdown controlling the visibility of the initial setup graphics ( Show or Hide ).

Info : Dropdown controlling the visibility of the small information table ( Show or Hide ).

Text Size : Adjusts the font size for all text elements displayed by the indicator (Value ranges from 0 to 36).

Line Width : Adjusts the width of the circle plots (1-10).

Time/Price

Inputs for the anchor points defining the base swing.

These settings define the start (Point A) and end (Point B) of the price swing used for all calculations.

Point A (Time, Price) : Input fields for the exact time coordinate and price level of the swing's starting point (A).

Point B (Time, Price) : Input fields for the exact time coordinate and price level of the swing's ending point (B).

Interactive Adjustment : Points A and B can typically be adjusted directly by clicking and dragging their markers on the chart (if 'Setup' is set to 'Show'). Changes update settings automatically.

📝 NOTES 📝

Fibonacci circles begin plotting only once the time corresponding to Point B has passed and is confirmed on the chart. While potential center locations might be visible earlier (as shown in the setup graphic), the final circle calculations require the complete geometry of the A-B swing. This approach ensures that as new price bars form, the circles are accurately rendered based on the finalized A-B relationship and the chosen center and scaling.

The indicator's calculations are anchored to user-defined start (A) and end (B) points on the chart. When switching between charts with significantly different price scales (e.g., from an index at 5,000 to a crypto asset at $0.50), it is typically necessary to adjust these anchor points to ensure the circle elements are correctly positioned and scaled.

⚠️ DISCLAIMER ⚠️

The Fibonacci Circle Zones indicator is a visual analysis tool designed to illustrate Fibonacci relationships through geometric constructions incorporating curved lines, providing a structured framework for identifying potential areas of price interaction. Like all technical and visual indicators, these visual representations may visually align with key price zones in hindsight, reflecting observed price dynamics. It is not intended as a predictive or standalone trading signal indicator.

The indicator calculates levels and projections using user-defined anchor points and Fibonacci ratios. While it aims to align with TradingView’s standard Fibonacci circle tool by employing mathematical and geometric formulas, no guarantee is made that its calculations are identical to TradingView's proprietary methods.

🧠 BEYOND THE CODE 🧠

The Fibonacci Circle Zones indicator, like other xxattaxx indicators , is designed with education and community collaboration in mind. Its open-source nature encourages exploration, experimentation, and the development of new Fibonacci and grid calculation indicators and tools. We hope this indicator serves as a framework and a starting point for future Innovation and discussions.

Pesquisar nos scripts por "tradingview界面调整"

Buy on 5% dip strategy with time adjustment

This script is a strategy called "Buy on 5% Dip Strategy with Time Adjustment 📉💡," which detects a 5% drop in price and triggers a buy signal 🔔. It also automatically closes the position once the set profit target is reached 💰, and it has additional logic to close the position if the loss exceeds 14% after holding for 230 days ⏳.

Strategy Explanation

Buy Condition: A buy signal is triggered when the price drops 5% from the highest price reached 🔻.

Take Profit: The position is closed when the price hits a 1.22x target from the average entry price 📈.

Forced Sell Condition: If the position is held for more than 230 days and the loss exceeds 14%, the position is automatically closed 🚫.

Leverage & Capital Allocation: Leverage is adjustable ⚖️, and you can set the percentage of capital allocated to each trade 💸.

Time Limits: The strategy allows you to set a start and end time ⏰ for trading, making the strategy active only within that specific period.

Code Credits and References

Credits: This script utilizes ideas and code from @QuantNomad and jangdokang for the profit table and algorithm concepts 🔧.

Sources:

Monthly Performance Table Script by QuantNomad:

ZenAndTheArtOfTrading's Script:

Strategy Performance

This strategy provides risk management through take profit and forced sell conditions and includes a performance table 📊 to track monthly and yearly results. You can compare backtest results with real-time performance to evaluate the strategy's effectiveness.

The performance numbers shown in the backtest reflect what would have happened if you had used this strategy since the launch date of the SOXL (the Direxion Daily Semiconductor Bull 3x Shares ETF) 📅. These results are not hypothetical but based on actual performance from the day of the ETF’s launch 📈.

Caution ⚠️

No Guarantee of Future Results: The results are based on historical performance from the launch of the SOXL ETF, but past performance does not guarantee future results. It’s important to approach with caution when applying it to live trading 🔍.

Risk Management: Leverage and capital allocation settings are crucial for managing risk ⚠️. Make sure to adjust these according to your risk tolerance ⚖️.

Casa_SessionsLibrary "Casa_Sessions"

Advanced trading session management library that enhances TradingView's default functionality:

Key Features:

- Accurate session detection for futures markets

- Custom session hour definitions

- Drop-in replacements for standard TradingView session functions

- Flexible session map customization

- Full control over trading windows and market hours

Perfect for traders who need precise session timing, especially when working

with futures markets or custom trading schedules.

SetSessionTimes(session_type_input, custom_session_times_input, syminfo_type, syminfo_root, syminfo_timezone)

Parameters:

session_type_input (simple string) : Input string for session selection:

- 'Custom': User-defined session times

- 'FX-Tokyo': Tokyo forex session

- 'FX-London': London forex session

- 'FX-New York': NY forex session

- 'Overnight Session (ON)': After-hours trading

- 'Day Session (RTH)': Regular trading hours

custom_session_times_input (simple string) : Session parameter for custom time windows

Only used when session_type_input is 'Custom'

syminfo_type (simple string)

syminfo_root (simple string)

syminfo_timezone (simple string)

Returns:

session_times: Trading hours for selected session

session_timezone: Market timezone (relevant for forex)

getSessionMap()

Get futures trading session hours map

Keys are formatted as 'symbol:session', examples:

- 'ES:market' - Regular trading hours (RTH)

- 'ES:overnight' - Extended trading hours (ETH)

- 'NQ:market' - NASDAQ futures RTH

- 'CL:overnight' - Crude Oil futures ETH

Returns: Map

Key: Symbol:session identifier

Value: Session hours in format "HH:MM-HH:MM"

getSessionString(session, symbol, sessionMap)

Returns a session string representing the session hours (and days) for the requested symbol (or the chart's symbol if the symbol value is not provided). If the session string is not found in the collection, it will return a blank string.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

symbol (string) : The symbol to check. Optional. Defaults to chart symbol.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

inSession(session, sessionMap, barsBack)

Returns true if the current symbol is currently in the session parameters defined by sessionString.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

barsBack (int) : Private. Only used by futures to check islastbar. Optional. The default is 0.

ismarket(sessionMap)

Returns true if the current bar is a part of the regular trading hours (i.e. market hours), false otherwise. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar()

Returns true if the current bar is the first bar of the day's session, false otherwise. If extended session information is used, only returns true on the first bar of the pre-market bars. Works for futures (TradingView's methods do not).

Returns: bool

islastbar()

Returns true if the current bar is the last bar of the day's session, false otherwise. If extended session information is used, only returns true on the last bar of the post-market bars. Works for futures (TradingView's methods do not).

Returns: bool

ispremarket(sessionMap)

Returns true if the current bar is a part of the pre-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

ispostmarket(sessionMap)

Returns true if the current bar is a part of the post-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar_regular(sessionMap)

Returns true on the first regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

islastbar_regular(sessionMap)

Returns true on the last regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isovernight(sessionMap)

Returns true if the current bar is a part of the pre-market or post-market, false otherwise. On non-intraday charts always returns false.

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

getSessionHighAndLow(session, sessionMap)

Returns a tuple containing the high and low print during the specified session.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: A tuple containing

getSessionHigh(session, sessionMap)

Convenience function to return the session high. Necessary if you want to call this function from within a request.security expression where you can't return a tuple.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: The high of the session

getSessionLow(session, sessionMap)

Convenience function to return the session low. Necessary if you want to call this function from within a request.security expression where you can't return a tuple.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: The low of the session

Highs&Lows by HourHighs & Lows by Hour

Description:

Highs & Lows by Hour is a TradingView indicator that helps traders identify the most frequent hours at which daily high and low price points occur. By analyzing historical price data directly from the TradingView chart, this tool provides valuable insights into market timing, allowing traders to optimize their strategies around key price movements.

This indicator is specifically designed for the one-hour (H1) timeframe . It does not display any data on other timeframes , as it relies on analyzing daily highs and lows within hourly periods.

This indicator processes the available data based on the number of historical bars loaded in the TradingView chart. The number of analyzed bars depends on the TradingView subscription plan , which determines how much historical data is accessible.

Key Features:

Works exclusively on the H1 timeframe , ensuring accurate analysis of daily highs and lows

Hourly highs and lows analysis to identify the most frequent hours when the market reaches its daily high and low

Sorted by frequency, displaying the most significant trading hours in descending order based on their recurrence

Customizable table and colors to fit the chart theme and trading style

Useful for scalpers, day traders, and swing traders to anticipate potential price reversals and breakouts

How It Works:

The indicator scans historical price data directly from the TradingView chart to detect the hour at which daily highs and daily lows occur.

It counts the frequency of highs and lows for each hour of the trading day based on the number of available bars in the TradingView chart.

The recorded data is displayed in a structured table, sorted by frequency from highest to lowest.

Users can customize colors to enhance readability and seamlessly integrate the indicator into their analysis.

Why Use This Indicator?

Identify key market patterns by recognizing the most critical hours when price extremes tend to form

Improve timing for trades by aligning entries and exits with high-probability time windows

Enhance market awareness by understanding when market volatility is likely to peak based on historical trends

Important Notes:

This indicator works only on the one-hour (H1) timeframe . It will not display any data on other timeframes

Works well on Forex, stocks, crypto, and futures , especially for intraday traders

The indicator analyzes only the historical bars available on the TradingView chart, which varies depending on the TradingView subscription plan (Free, Pro, Pro+, Premium)

This indicator does not generate buy or sell signals but serves as a data-driven tool for market analysis

How to Use:

Apply the Highs & Lows by Hour indicator to a one-hour (H1) chart on TradingView

Review the table displaying the most frequent hours for daily highs and lows

Adjust colors and settings for better visualization

Use the data to refine trading decisions and align strategy with historical price behavior

Schwarzman Custom ORB with Box DisplayIndicator Overview

The Schwarzman Custom ORB (Opening Range Breakout) Indicator is a fully self-developed script designed for traders who utilize opening range breakout strategies. This indicator allows users to customize their ORB settings, apply them to historical price data, and visually connect multiple ORBs to analyze past performance. The goal is to provide traders with a tool to backtest and refine their breakout strategies based on historical ORB data.

How the Indicator Works

1️⃣ User-Defined ORB Settings

• The user selects a custom start time (hour and minute) for the ORB.

• The user defines a duration (e.g., 15 minutes, 30 minutes, etc.) for the ORB period.

• A timezone offset is included to adjust for different market sessions.

2️⃣ ORB High and Low Calculation

• The script records the highest and lowest prices within the selected ORB time window.

• The recorded values remain static after the ORB period ends, ensuring accurate range plotting.

3️⃣ Historical ORB Visualization

• Instead of only showing a single ORB for the current session, this indicator connects multiple ORBs across past data.

• This allows traders to visually analyze previous breakout performance.

• The plotted ORBs remain fixed and do not repaint, ensuring an accurate backtesting experience.

4️⃣ Stepline Visualization & Range Filling

• The high and low ORB levels are displayed using stepline plots to maintain clear horizontal levels.

• A shaded box is applied between the ORB high and low for better visualization.

Use Cases & Strategy Application

📌 Backtesting Historical ORBs – See how past ORBs performed under different market conditions.

📌 Custom ORB Settings – Adjust the start time and duration for different trading sessions.

📌 Multi-ORB Analysis – Connect ORBs over multiple trading days to study trends and breakouts.

📌 Breakout Strategy Optimization – Use the historical ORB connections to refine entry and exit points.

This indicator is particularly useful for day traders, scalpers, and breakout traders looking for a data-driven approach to trading.

Indicator Development & Transparency Statement

As a trader, I have tested various ORB (Opening Range Breakout) indicators available in the TradingView community. Through these experiences, I aimed to develop a version that best fits my own trading needs and strategy.

This script is a self-developed ORB tool, created from scratch while drawing inspiration from the concept of opening range breakouts, which is widely used in trading. Since I initially coded in Pine Script v4, I used ChatGPT to help refine and migrate the script to Pine Script v6 to ensure compatibility with the latest TradingView features. However, the core logic, structure, and customization were entirely designed and implemented based on my own approach.

I am making this indicator public not to violate any TradingView guidelines but to share my work with the trading community and provide a tool that can help others analyze ORB-based strategies. If there are any compliance concerns, I am open to adjusting the script accordingly, but I want to clarify that this is not a copy of any existing ORB script—it is a custom-built indicator tailored to my own trading preferences.

I appreciate the opportunity to contribute to the community and would welcome any specific feedback from TradingView regarding rule compliance.

Best regards,

Janko S. (Schwarzman)

Appeal to TradingView

Dear TradingView Team,

This script is 100% self-developed and does not copy or replicate any third-party code. It is a customized ORB tool designed for traders who wish to backtest and analyze opening range breakout strategies over multiple sessions. We kindly request specific clarification regarding which exact line(s) of code violate TradingView’s guidelines. If there are any compliance concerns, we are happy to adjust the script accordingly.

Please let us know the precise rules or community guidelines that were violated so we can make the necessary modifications.

🚀 Summary

✔ Fully Custom & Self-Developed – No copied or third-party code.

✔ Innovative Feature – Connects past ORBs for strategy backtesting.

✔ Transparent & Compliant – Requesting exact details on any potential rule violations.

Fibonacci Time-Price Zones🟩 Fibonacci Time-Price Zones is a chart visualization tool that combines Fibonacci ratios with time-based and price-based geometry to analyze market behavior. Unlike typical Fibonacci indicators that focus solely on horizontal price levels, this indicator incorporates time into the analysis, providing a more dynamic perspective on price action.

The indicator offers multiple ways to visualize Fibonacci relationships. Drawing segmented circles creates a unique perspective on price action by incorporating time into the analysis. These segmented circles, similar to TradingView's built-in Fibonacci Circles, are derived from Fibonacci time and price levels, allowing traders to identify potential turning points based on the dynamic interaction between price and time.

As another distinct visualization method, the indicator incorporates orthogonal patterns, created by the intersection of horizontal and vertical Fibonacci levels. These intersections form L-shaped connections on the chart, derived from key Fibonacci price and time intervals, highlighting potential areas of support or resistance at specific points in time.

In addition to these geometric approaches, another option is sloped lines, which project Fibonacci levels that account for both time and price along the trendline. These projections derive their angles from the interplay between Fibonacci price levels and Fibonacci time intervals, creating dynamic zones on the chart. The slope of these lines reflects the direction and angle of the trend, providing a visual representation of price alignment with market direction, while maintaining the time-price relationship unique to this indicator

The indicator also includes horizontal Fibonacci levels similar to traditional retracement and extension tools. However, unlike standard tools, traders can display retracement levels, extension levels, or both simultaneously from a single instance of the indicator. These horizontal levels maintain consistency with the chosen visualization method, automatically scaling and adapting whether used with circles, orthogonal patterns, or slope-based analysis.

By combining these distinct methods—circles, orthogonal patterns, sloped projections, and horizontal levels—the indicator provides a comprehensive approach to Fibonacci analysis based on both time and price relationships. Each visualization method offers a unique perspective on market structure while maintaining the core principle of time-price interaction.

⭕ THEORY AND CONCEPT ⭕

While traditional Fibonacci tools excel at identifying potential support and resistance levels through price-based ratios (0.236, 0.382, 0.618), they do not incorporate the dimension of time in market analysis. Extensions and retracements effectively measure price relationships within trends, yet markets move through both price and time dimensions simultaneously.

Fibonacci circles represent an evolution in technical analysis by incorporating time intervals alongside price levels. Based on the mathematical principle that markets often move in circular patterns proportional to Fibonacci ratios, these circles project potential support and resistance zones as partial circles radiating from significant price points. However, traditional circle-based tools can create visual complexity that obscures key market relationships. The integration of time into Fibonacci analysis reveals how price movements often respect both temporal and price-based ratios, suggesting a deeper geometric structure to market behavior.

The Fibonacci Time-Price Zones indicator advances these concepts by providing multiple geometric approaches to visualize time-price relationships. Each shape option—circles, orthogonal patterns, slopes, and horizontal levels—represents a different mathematical perspective on how Fibonacci ratios manifest across both dimensions. This multi-faceted approach allows traders to observe how price responds to Fibonacci-based zones that account for both time and price movements, potentially revealing market structure that purely price-based tools might miss.

Shape Options

The indicator employs four distinct geometric approaches to analyze Fibonacci relationships across time and price dimensions:

Circular : Represents the cyclical nature of market movements through partial circles, where each radius is scaled by Fibonacci ratios incorporating both time and price components. This geometry suggests market movements may follow proportional circular paths from significant pivot points, reflecting the harmonic relationship between time and price.

Orthogonal : Constructs L-shaped patterns that separate the time and price components of Fibonacci relationships. The horizontal component represents price levels, while the vertical component measures time intervals, allowing analysis of how these dimensions interact independently at key market points.

Sloped : Projects Fibonacci levels along the prevailing trend, incorporating both time and price in the angle of projection. This approach suggests that support and resistance levels may maintain their relationship to price while adjusting to the temporal flow of the market.

Horizontal : Provides traditional static Fibonacci levels that serve as a reference point for comparing price-only analysis with the dynamic time-price relationships shown in the other three shapes. This baseline approach allows traders to evaluate how the incorporation of time dimension enhances or modifies traditional Fibonacci analysis.

By combining these geometric approaches, the Fibonacci Time-Price Zones indicator creates a comprehensive analytical framework that bridges traditional and advanced Fibonacci analysis. The horizontal levels serve as familiar reference points, while the dynamic elements—circular, orthogonal, and sloped projections—reveal how price action responds to temporal relationships. This multi-dimensional approach enables traders to study market structure through various geometric lenses, providing deeper insights into time-price symmetry within technical analysis. Whether applied to retracements, extensions, or trend analysis, the indicator offers a structured methodology for understanding how markets move through both price and time dimensions.

🛠️ CONFIGURATION AND SETTINGS 🛠️

The Fibonacci Time-Price Zones indicator offers a range of configurable settings to tailor its functionality and visual representation to your specific analysis needs. These options allow you to customize zone visibility, structures, horizontal lines, and other features.

Important Note: The indicator's calculations are anchored to user-defined start and end points on the chart. When switching between charts with significantly different price scales (e.g., from Bitcoin at $100,000 to Silver at $30), adjustment of these anchor points is required to ensure correct positioning of the Fibonacci elements.

Fibonacci Levels

The indicator allows users to customize Fibonacci levels for both retracement and extension analysis. Each level can be individually configured with the following options:

Visibility : Toggle the visibility of each level to focus on specific areas of interest.

Level Value : Set the Fibonacci ratio for the level, such as 0.618 or 1.000, to align with your analysis needs.

Color : Customize the color of each level for better visual clarity.

Line Thickness : Adjust the line thickness to emphasize critical levels or maintain a cleaner chart.

Setup

Zone Type : Select which Fibonacci zones to display:

- Retracement : Shows potential pull back levels within the trend

- Extension : Projects levels beyond the trend for potential continuation targets

- Both : Displays both retracement and extension zones simultaneously

Shape : Choose from four visualization methods:

- Circular : Time-price based semicircles centered on point B

- Orthogonal : L-shaped patterns combining time and price levels

- Sloped : Trend-aligned projections of Fibonacci levels

- Horizontal : Traditional horizontal Fibonacci levels

Visual Settings

Fill % : Adjusts the fill intensity of zones:

0% : No fill between levels

100% : Maximum fill between levels

Lines :

Trendline : The base A-B trend with customizable color

Extension : B-C projection line

Retracement : B-D pullback line

Labels :

Points : Show/hide A, B, C, D markers

Levels : Show/hide Fibonacci percentages

Time-Price Points

Set the time and price for the points that define the Fibonacci zones and horizontal levels. These points are defined upon loading the chart. These points can be configured directly in the settings or adjusted interactively on the live chart.

A and B Points : These user-defined time and price points determine the basis for calculating the semicircles and Fibonacci levels. While the settings panel displays their exact values for fine-tuning, the easiest way to modify these points is by dragging them directly on the chart for quick adjustments.

Interactive Adjustments : Any changes made to the points on the chart will automatically synchronize with the settings panel, ensuring consistency and precision.

🖼️ CHART EXAMPLES 🖼️

Fibonacci Time-Price Zones using the 'Circular' Shape option. Note the price interaction at the 0.786 level, which acts as a support zone. Additional points of interest include resistance near the 0.618 level and consolidation around the 0.5 level, highlighting the utility of both horizontal and semicircular Fibonacci projections in identifying key price areas.

Fibonacci Time-Price Zones using the 'Sloped' Shape option. The chart displays price retracing along the sloped Fibonacci levels, with blue arrows highlighting potential support zones at 0.618 and 0.786, and a red arrow indicating potential resistance at the 1.0 level. This visual representation aligns with the prevailing downtrend, suggesting potential selling pressure at the 1.0 Fibonacci level.

Fibonacci Time-Price Zones using the 'Orthogonal' Shape option. The chart demonstrates price action interacting with vertical zones created by the orthogonal lines at the 0.618, 0.786, and 1.0 Fibonacci levels. Blue arrows highlight potential support areas, while red arrows indicate potential resistance areas, revealing how the orthogonal lines can identify distinct points of price interaction.

Fibonacci Time-Price Zones using the 'Circular' Shape option. The chart displays price action in relation to segmented circles emanating from the starting point (point A). The circles represent different Fibonacci ratios (0.382, 0.5, 0.618, 0.786) and their intersections with the price axis create potential zones of support and resistance. This approach offers a visually distinct way to analyze potential turning points based on both price and time.

Fibonacci Time-Price Zones using the 'Sloped' Shape option. The sloped Fibonacci levels (0.786, 0.618, 0.5) create zones of potential support and resistance, with price finding clear interaction within these areas. The ellipses highlight this price action, particularly the support between 0.786 and 0.618, which aligns closely with the trend.

Fibonacci Time-Price Zones using the 'Circular' Shape option. The price action appears to be ‘hugging’ the 0.5 Fibonacci level, suggesting potential resistance. This demonstrates how the circular zones can identify potential turning points and areas of consolidation which might not be seen with linear analysis.

Fibonacci Time-Price Zones using the 'Sloped' Shape option with Point D marker enabled. The chart demonstrates clear price action closely following along the sloped Retracement line until the orthogonal intersection at the 0.618 levels where the trend is broken and price dips throughout the 0.618 to 0.786 horizontal zone. Price jumps back to the retracement slope at the start of the 0.786 horizontal zone and continues to the 1.0 horizontal zone. The aqua-colored retracement line is enabled to further emphasize this retracement slope .

Geometric validation using TradingView's built-in Fibonacci Circle tool (overlaid). The alignment at the 0.5 and 1.0 levels demonstrates the indicator's consistent approximation of Fibonacci Circles.

Comparison of Fibonacci Time-Price Zones (Shape: Horizontal) with TradingView's Built-in Retracement and Extension Tools (overlaid): This example demonstrates how the Horizontal structure aligns with TradingView’s retracement and extension levels, allowing users to integrate multiple tools seamlessly. The Fibonacci circle connects retracement and extension zones, highlighting the potential relationship between past retracements and future extensions.

📐 GEOMETRIC FOUNDATIONS 📐

This indicator integrates circular and straight representations of Fibonacci levels, specifically the Circular , Orthogonal , Sloped , and Horizontal shape options. The geometric principles behind these shapes differ significantly, requiring distinct scaling methods for accurate representation. The Circular shape employs logarithmic scaling with radial expansion, where the distance from a central point determines the level's position, creating partial circles that align with TradingView's built-in Fibonacci Circle tool. The other three shapes utilize geometric progression scaling for linear extension from a starting point, resulting in straight lines that align with TradingView's built-in Fibonacci retracement and extension tools. Due to these distinct geometric foundations and scaling methods, perfectly aligning both the partial circles and straight lines simultaneously is mathematically constrained, though any differences are typically visually imperceptible.

The Circular shape's partial circles are calculated and scaled to align with TradingView's built-in Fibonacci Circles. These circles are plotted from the second swing point onward. This approach ensures consistent and accurate visualization across all market types, including those with gaps or closed sessions, which unlike 24/7 markets, do not have a direct one-to-one correspondence between bar indices and time. To maintain accurate geometric proportions across varying chart scales, the indicator calculates an aspect ratio by normalizing the proportional difference between vertical (price) and horizontal (time) distances of the swing points. This normalization factor ensures geometric shapes maintain their mathematical properties regardless of price scale magnitude or time period span, while maintaining the correct proportions of the geometric constructions at any chart zoom level.

The indicator automatically applies the appropriate scaling factor based on the selected shape option, optimizing either circular proportions and proper radius calculations for each Fibonacci level, or straight-line relationships between Fibonacci levels. These distinct scaling approaches maintain mathematical integrity while preserving the essential characteristics of each geometric representation, ensuring optimal visualization accuracy whether using circular or linear shapes.

⚠️ DISCLAIMER ⚠️

The Fibonacci Time-Price Zones indicator is a visual analysis tool designed to illustrate Fibonacci relationships through geometric constructions incorporating both curved and straight lines, providing a structured framework for identifying potential areas of price interaction. It is not intended as a predictive or standalone trading signal indicator.

The indicator calculates levels and projections using user-defined anchor points and Fibonacci ratios. While it aims to align with TradingView’s Fibonacci extension, retracement, and circle tools by employing mathematical and geometric formulas, no guarantee is made that its calculations are identical to TradingView's proprietary methods.

Like all technical and visual indicators, these visual representations may visually align with key price zones in hindsight, reflecting observed price dynamics. However, these visualizations are not standalone signals for trading decisions and should be interpreted as part of a broader analytical approach.

This indicator is intended for educational and analytical purposes, complementing other tools and methods of market analysis. Users are encouraged to integrate it into a comprehensive trading strategy, customizing its settings to suit their specific needs and market conditions.

🧠 BEYOND THE CODE 🧠

The Fibonacci Time-Price Zones indicator is designed to encourage both education and community engagement. By integrating time-sensitive geometry with Fibonacci-based frameworks, it bridges traditional grid-based analysis with dynamic time-price relationships. The inclusion of semicircles, horizontal levels, orthogonal structures, and sloped trends provides users with versatile tools to explore the interaction between price movements and temporal intervals while maintaining clarity and adaptability.

As an open-source tool, the indicator invites exploration, experimentation, and customization. Whether used as a standalone resource or alongside other technical strategies, it serves as a practical and educational framework for understanding market structure and Fibonacci relationships in greater depth.

Your feedback and contributions are essential to refining and enhancing the Fibonacci Time-Price Zones indicator. We look forward to the creative applications, adaptations, and insights this tool inspires within the trading community.

DCA, Support and Resistance with RSI and Trend FilterThis script is based on

script from Kieranj with added pyramiding and DCA

The buy condition (buyCondition) is triggered when the RSI crosses above the oversold threshold (ta.crossover(rsi, oversoldThreshold)), the trend filter confirms an uptrend (isUptrend is true), and the close price is greater than or equal to the support level (close >= supportLevel).

The partial sell condition (sellCondition) is triggered when the RSI crosses below the overbought threshold (ta.crossunder(rsi, overboughtThreshold)) and profit goal is reached, the trend filter confirms a downtrend (isUptrend is false), and the close price is less than or equal to the resistance level (close <= resistanceLevel).

Full sell will be triggered if trend is broken and profit goal is reached

With this implementation, the signals will only be generated in the direction of the trend on the 4-hour timeframe. The trend is considered up when the 50-period SMA is below the 200-period SMA (ta.sma(trendFilterSource, 50) < ta.sma(trendFilterSource, 200)).

Pyramiding should be activated, values like 100, so every DCA step should be around 1%

i have best results on 5 min charts

SessionLibrary "Session"

Helper functions for trading sessions. TradingView doesn't provide correct data when

calling some of the convenience methods like session.ismarket when you are looking at futures charts. This library corrects those mistakes by providing functions with the same names as the TradingView default properties. that reference a custom defined set of session hours for futures. It also provides a way for consumers to customize the map values by calling getSessionMap() and then overwriting (or adding) custom session definitions.

getSessionMap()

Returns a map of the futures rth & eth session hours. The map is keyed with symbol:session format (eg. ES:market or ES:overnight).

Returns: A map of futures symbols and their associated session hours.

getSessionString(session, symbol, sessionMap)

Returns a session string representing the session hours (and days) for the requested symbol (or the chart's symbol if the symbol value is not provided). If the session string is not found in the collection, it will return a blank string.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

symbol (string) : The symbol to check. Optional. Defaults to chart symbol.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

inSession(session, sessionMap, barsBack)

Returns true if the current symbol is currently in the session parameters defined by sessionString.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

barsBack (int) : Private. Only used by futures to check islastbar. Optional. The default is 0.

ismarket(sessionMap)

Returns true if the current bar is a part of the regular trading hours (i.e. market hours), false otherwise. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar()

Returns true if the current bar is the first bar of the day's session, false otherwise. If extended session information is used, only returns true on the first bar of the pre-market bars. Works for futures (TradingView's methods do not).

Returns: bool

islastbar()

Returns true if the current bar is the last bar of the day's session, false otherwise. If extended session information is used, only returns true on the last bar of the post-market bars. Works for futures (TradingView's methods do not).

Returns: bool

ispremarket(sessionMap)

Returns true if the current bar is a part of the pre-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

ispostmarket(sessionMap)

Returns true if the current bar is a part of the post-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar_regular(sessionMap)

Returns true on the first regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

islastbar_regular(sessionMap)

Returns true on the last regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isovernight(sessionMap)

Returns true if the current bar is a part of the pre-market or post-market, false otherwise. On non-intraday charts always returns false.

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

getSessionHighAndLow(session, sessionMap)

Returns a tuple containing the high and low print during the specified session.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: A tuple containing

GannLSVZO Indicator [Algo Alert]The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Gann Laplace Smoothed Volume Zone Oscillator GannLSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the upgraded Discrete Fourier Transform, the Laplace Stieltjes Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Laplace with Gann Swing Entries and Exits (orange X) and with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

ORIGINALITY & USFULLNESS:

Personal combination of Gann swings and Laplace Stieltjes Transform of a price which results in less noise Volume Zone Oscillator.

The Laplace Stieltjes Transform is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

The Gann swings and the Gan swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Laplace Stieltjes Transform approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Laplace Stieltjes Transform (FLT) and the innovative Double Discrete Fourier Transform (DTF32) soothed price series to suit your analytical needs.

Use dynamic calculation of Laplace coefficient or the static one. You may modify those inputs and Strategy entries with Gann swings.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Trade Exit Calculator [MarketSignalsPro]█ OVERVIEW

This Pine Script calculates a Stop Loss and Take Profit order suggestion based on the Average True Range (ATR). This provides a market generated visual reference for the user to better gauge risk and profit potential for their trades. This is not a trade signal system, it is a tool best used in conjunction with an existing system.

█ FEATURES

Inputs:

stopLossMultiplier and takeProfitMultiplier : These are input parameters that allow the user to adjust the multiplier for calculating stop loss and take profit levels.

longIndicator : This input parameter determines whether the script is calculating levels for a long setup (buy) or a short setup (sell).

Variable Initialization:

Various variables are initialized to manage labels, lines, and calculated stop loss and take profit levels.

ATR (Average True Range) is calculated using a period of 14.

Calculation of Stop Loss and Take Profit:

Depending on the value of longIndicator stop loss and take profit levels are not calculated the same way.

For long setups, stop loss is calculated below the closing price and take profit above, while for short setups, it's the opposite.

The calculation involves multiplying the ATR value by the user-defined multipliers and adding or subtracting from the closing price accordingly.

Plotting Lines:

Lines representing the calculated stop loss, take profit, and entry price are plotted on the chart.

Displaying Labels:

Labels displaying the calculated stop loss, take profit, and entry price are shown on the chart alongside the respective lines.

Updating and Deleting Objects:

Existing lines and labels are updated or deleted to ensure only the most recent levels are displayed on the chart.

Final Output:

The script outputs visual representations of stop loss, take profit, and entry price levels on the chart, providing traders with guidance for risk management and profit-taking strategies based on the volatility of the market.

█ CONCLUSION

In summary, this Pine Script enhances trading strategies by calculating and illustrating stop loss and take profit levels based on the Average True Range indicator, offering traders a structured way to manage risk and profit potential.

█ THANKS

Special thanks to Cryptosnagger for taking the time to build this Pine Script and share it freely with the community.

DiscordWebhooksLibrary🚀 Introduction

Welcome to the TradingView PineScript Library for Discord Webhook Integration! This library is designed for traders and developers who use TradingView for technical analysis and want to integrate their trading strategies with Discord notifications.

Key Features:

* Embed Creation: Easily create rich and informative embeds for your Discord messages, allowing you to send detailed trading alerts and summaries.

* Flexible Webhook Formatting: Customize your Discord messages with options for usernames, avatars, and text content, providing a personalized touch to your notifications.

* Simple Integration: Designed with simplicity in mind, this library can be integrated into your existing Pine Script trading strategies without extensive coding knowledge.

* Real-time Alerts: Utilize TradingView's alert system to send real-time trade signals and market updates to your Discord server.

Compatibility:

This library is compatible with TradingView's Pine Script version 5.

🍃 Code Snippets and Usage Examples

The following examples demonstrate how to use the Discord Webhook Integration Library in your TradingView Pine Scripts. These snippets cover various scenarios, showcasing the flexibility and utility of the library.

Example 1: Simple Alert with Markdown in Embed Description

embedDesc = "This is a **bold** and _italic_ alert message with a (replace_with_your_link)"

embedJson = createEmbedJSON("Simple Alert", embedDesc, 12345)

content = discordWebhookJSON("Alert from Captain Hook", "Captain Hook", na, embedJson)

Example 2: Multiple Embeds with Different Markdown Styles

embedDesc1 = "First alert with **bold** text"

embedDesc2 = "Second alert with _italic_ text"

embedDesc3 = "Third alert with ~~strikethrough~~"

embedJson1 = createEmbedJSON("Alert 1", embedDesc1, 654321)

embedJson2 = createEmbedJSON("Alert 2", embedDesc2, 123456)

embedJson3 = createEmbedJSON("Alert 3", embedDesc3, 111111)

embeds = embedJson1 + "," + embedJson2 + "," + embedJson3

content = discordWebhookJSON("Multiple Alerts", "Captain Hook", na, embeds)

Example 3: Complex Alert with Full Markdown Usage in Embed

embedDesc = "Alert: **Price Breakout!**\\n\\n" +

"*Symbol*: " + syminfo.ticker + "\\n" +

"*Price*: $" + str.tostring(close) + "\\n\\n" +

" (replace_with_your_link)"

embedJson = createEmbedJSON("Complex Alert", embedDesc, 16711680) // Red color

content = discordWebhookJSON("Complex Alert", "Captain Hook", na, embedJson)

Example 4: Advanced Technical Analysis Alert

rsiValue = ta.rsi(close, 14)

= ta.macd(close, 12, 26, 9)

taMessage = "RSI: " + str.tostring(rsiValue) + "\\nMACD: " + str.tostring(macdLine)

embedJson = createEmbedJSON("Technical Analysis Update", taMessage, 255) // Blue color

content = discordWebhookJSON("TA Alert", "Captain Hook", na, embedJson)

Example 5: Market Summary with Multiple Fields

counterTrend = "Your counter trend criterias"

counterTrendEmbed = createEmbedJSON(title = "Counter Trend", description = counterTrend, color = 15258703)

redFlags = "Your red flag criterias"

redFlagsEmbed = createEmbedJSON(title = "Red Flags", description = redFlags, color = 15229263)

embeds = counterTrendEmbed + "," + redFlagsEmbed

content = discordWebhookJSON(contentText = "Example of how a market analysis could look like", username = "Captain Hook", embeds = embeds)

🚨 Error Handling

Use Escape Characters Correctly: In message strings, remember to use \\n for new lines instead of \n. This ensures that the newline character is correctly interpreted in the JSON format.

It can be helpful to plot the json on the last candle

if barstate.islast

label.new(bar_index, high, text=debugMessage, color=color.red, textcolor=color.white, yloc=yloc.abovebar)

🔥 FAQs

Q1: Can I send alerts for multiple conditions?

A: Yes, you can configure multiple conditions in your script. Use separate if statements for each condition and call the discordWebhookJSON function with the relevant message for each alert.

Q2: Why is my alert not triggering?

A: Ensure your alert conditions are correct and that you've properly set up the webhook in both your script and TradingView's alert configuration. Also, check for any syntax errors in your script.

Q3: How many alerts can I send to Discord?

A: While TradingView doesn't limit the number of alerts, Discord has rate limits for webhooks. Be mindful of these limits to avoid your webhook being temporarily blocked.

Q4: Can I customize the appearance of my Discord messages?

A: Yes, the createEmbedJSON function allows you to customize your messages with titles, descriptions, colors, and more. Experiment with different parameters to achieve the desired appearance.

Q5: Is it possible to include real-time data in alerts?

A: Yes, your script can include real-time price data, indicator values, or any other real-time data available in Pine Script.

Q6: How can I contribute to the library or suggest improvements?

A: You can provide feedback, suggest improvements, or contribute to the library's development through the community channels or contact points provided in the "Support and Community" section.

formatTimeframe()

discordWebhookJSON(contentText, username, avatar_url, embeds)

Constructs a JSON string for a Discord webhook message. This string includes optional fields for content, username, avatar URL, and embeds.

Parameters:

contentText (string) : (string, optional): The main text content of the webhook message. Default is 'na'.

username (string) : (string, optional): Overrides the default username of the webhook. Default is 'na'.

avatar_url (string) : (string, optional): Overrides the default avatar URL of the webhook. Default is 'na'.

embeds (string) : (string, optional): A string containing one or more embed JSON objects. This should be formatted correctly as a JSON array. Default is 'na'.

createEmbedJSON(title, description, color, authorName, authorUrl, authorIconUrl, fields)

Creates a JSON string for a single embed object for a Discord webhook.

Parameters:

title (string) : (string, optional): The title of the embed. Default is 'na' (not applicable).

description (string) : (string, optional): The description text of the embed. Supports basic formatting. Default is 'na'.

color (int) : (int, optional): The color code of the embed, typically in decimal format. Default is 'na'.

authorName (string) : (string, optional): The name of the author to display in the embed. Default is 'na'.

authorUrl (string) : (string, optional): The URL linked to the author's name. Default is 'na'.

authorIconUrl (string) : (string, optional): The URL of the icon to display next to the author's name. Default is 'na'.

fields (string) : (string, optional): A string containing one or more field JSON objects. This should be formatted correctly as a JSON array. Default is 'na'. Note: Use the 'createEmbedFieldJSON' function to generate these JSON field strings before adding them to the array.

createEmbedFieldJSON(name, value, inline)

Creates a JSON string representing a single field object within an embed for a Discord webhook message.

Parameters:

name (string) : (string): The name of the field, acting as a title for the field content.