RSI with Self-Adjusting Linear Regression Bands (Expo)RSI with Self-Adjusting Linear Regression Bands (Expo) makes use of RSI and Linear Regression to create an RSI that follows the current trend. The indicator has an upper and lower self-adjusting Linear Regression Band that act as RSI boundaries.

HOW TO USE

The indicator can be used in multiple ways, for instance, to find overbought and oversold areas. Or to identify trends as well as pullbacks in trends.

INDICATOR IN ACTION

This indicator is a modification of RafaelZioni's work "Linear Regression Trend bands"

Credit to: RafaelZioni

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

Pesquisar nos scripts por "the script"

Tradingedge Academy REVERSAL CATCHER (RECAT)Core idea behind designing this tool is to CATCH REVERSALS in the live market.

Reversal can be a TREND REVERSAL or a TEMPORARY PULL BACK. This tool works perfectly in both situations.

HOW TO USE:

AFTER YOU APPLY THE SCRIPT.

1. WAIT FOR THE FORMATION BLUE/YELLOW COLOURED BARS AT DAY HIGH/LOW.

Accuracy is highest when the REVERSALS are caught at DAY HIGH/LOW. I would suggest you to work only on DAY HIGH/LOW candles.

Do not jump into the trade. Wait for the candle to close.

2. BLUE represents the start of a BEARISH TREND or simply "SELL SIGNAL".

YELLOW represents the beginning of a BULLISH TREND or simply "BUY SIGNAL".

3. If the BLUE candle is formed at DAY HIGH.

SELL below it's LOW with DAY HIGH as Stoploss. (Keep some BUFFER).

If the YELLOW candle is formed at DAY LOW.

BUY above it's HIGH with DAY LOW as Stoploss. (Keep some BUFFER).

4. TARGET

Risk : Reward = 1:1

Trail Stoploss for 1:2, 1:2.5, 1:3

NOTE:

RECAT can be used in any timeframe. However, lower timeframes tend to have more noise as compared to 15mins and above.

RECAT can be used with all the SCRIPTS. However, high volume scripts give better results.

THERE IS ABSOLUTELY NO REPAINTING AFTER THE CANDLE IS CLOSED.

CONTACT ME FOR ACCESS.

DETAILS IN SIGNATURE.

Average High Traded Volume (Nodes) - Levels/Zones (Expo)Average High Traded Volume (Nodes) - (Expo) automatically identifies and displays High Traded Volume Nodes.

Levels/Zones are displayed where there has been a significant level of trading activity and when there has been both high supply and demand. These levels can leave clues for future price behavior and act as support/resistance zones.

The indicator can be used standalone or as a part of your current trading strategy.

Real-time

No repainting

Works on any market if volume data is provided

HOW TO USE

1. Use the indicator to identify High Traded Volume Nodes.

2. Use the indicator to identify support/resistance zones.

3. Use the indicator to confirm the existence, or a continuation, of a trend or a trend reversal.

INDICATOR IN ACTION

4-hour chart

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

ACCESS THE INDICATOR

• Contact me on TradingView or use the links below

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

On Balance Volume Flow (Expo)On Balance Volume Flow (Expo) identifies buying and selling pressure at extreme points. On Balance Volume Flow (Expo) is primarily used to identify potential turning points and areas of congestion.

Vwap can be enabled as an input source instead of using Volume.

The indicator can be used standalone or as a part of your current trading strategy.

HOW TO USE

1. Use the indicator to identify potential turning points and areas of congestion.

2. Use the indicator to get a feel of how price movements and volume are related.

INDICATOR IN ACTION

1-hour chart

Works on any market

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

ACCESS THE INDICATOR

• Contact me on TradingView or use the links below

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

Auto Support/Resistance Levels (Expo)Auto Support/Resistance Levels (Expo) automatically identifies and displays key support and resistance levels.

The user can enable short- term, medium-term, and long- term Auto SR Levels.

The indicator can be used standalone or as a part of your current trading strategy.

Real-time

No repainting

Works on any market

HOW TO USE

1. Use the indicator to identify key Support and Resistance Levels

INDICATOR IN ACTION

Daily chart

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

ACCESS THE INDICATOR

• Contact me on TradingView or use the links below

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

Fearzone & Greedzone Levels - Contrarian & Breakout (Expo)"Be fearful when others are greedy, and greedy when others are fearful" - Warren Buffett. Fearzone & Greedzone Levels - Contrarian & Breakout (Expo) is a contrarian and breakout indicator that gives us an indication when fear and greed begins to take over in the market. Traders should be prepared for increased volatility and good trading opportunities.

This indicator can both be used to identify potential reversal points and be used to identify breakouts from previous Fear and Greed Levels.

The Fearzone and Greedzone can be visualized with candlesticks or with circles depending on what you prefer.

Alert conditions are added.

HOW TO USE

1. Use the indicator to identify when investors are fearful and greedy.

2. Use the indicator to identify potential reversal points.

3. Use the indicator to identify potential breakouts.

INDICATOR IN ACTION

4 hour chart

4 hour chart

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

GreedZone indicator - Contrarian Indicator"Be fearful when others are greedy, and greedy when others are fearful" - Warren Buffett. Greedzone is a contrarian indicator that gives us an indication when greed begins to take over in the market. Traders should be prepared for increased volatility and good trading opportunities.

The Greedzone is visualized with green candlesticks above the price.

HOW TO USE

1. Use the indicator to identify when investors are greedy.

2. Use the indicator to identify potential reversal points.

INDICATOR IN ACTION

1 hour chart

5 min chart

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

Fearzone (Expo) - Contrarian Indicator"Be fearful when others are greedy, and greedy when others are fearful" - Warren Buffett. Fearzone is a contrarian indicator that gives us an indication when fear begins to take over in the market. Traders should be prepared for increased volatility and good trading opportunities.

The Fearzone is visualized with red candlesticks below the price.

This version of the FearZone indicator is slightly different from the one ©kruskakli has published.

HOW TO USE

1. Use the indicator to identify when investors are fearful.

2. Use the indicator to identify potential reversal points.

INDICATOR IN ACTION

1 hour chart

5 min chart

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

ProfitBee59 v5.0ProfitBee59 v5.0 for TradingView (pb5 ai) helps you do tedious works on your technical charts. It does CC59 counting and prints out positive or negative number on each price bar. When the counting arrives at -9 or +9, it creates respectable support and resistance ( SNR ) levels on the chart. It draws a pair of fast/slow average lines with pink/red colors for corresponding downtrend and yellow/green for uptrend. A yellow cross sign shows a crossing point between these fast/slow average line. It also draws a mega average line in gray to give a mega trend picture. Pb5 ai provides time/price analyseses. Up/Dn arrows are printed out at high probability buy/sell regions. In addition, other auxiliary tools such as Max/Min finder used to find the candlesticks with local max/min prices or Gap finder used to locate discontinuity between candlesticks.

For Forex trading, other intraday parameters are also available including the day opening level, high/low of yesterday and intraday brown background marking time interval for key trading hours in Asian-London-New York markets.

Smart phone/tablet and PC notifications of events occurring in the chart can be sent to you by server-side alerts so that you don't have to stay in front of the screen all the time.

=================================================================

The script ProfitBee59 v5.0 for TradingView (pb5 ai) is locked and protected. Contact the author for your access.

=================================================================

How to install the script:

------------------------------

*Go to the bottom of this page and click on "Add to Favorite Scripts".

*Remove older version of the script by clicking on the "X" button behind the indicator line at the top left corner of the chart window.

*Open a new chart at and click on the "Indicators" tab.

*Click on the "Favorites" tab and choose "ProfitBee59 v5.0".

*Right click anywhere on the graph, choose "Color Theme", the select "Dark".

*Right click anywhere on the graph, choose "Settings".

*In "Symbol" tab, set "Precision" to 1/100 for stock price or 1/100000 for Forex and set "Time Zone" to your local time.

*In "Scales" tab, check "Indicator Last Value Label".

*In "Events" tab, check "Show Dividends on Chart", "Show Splits on Chart" and "Show Earnings on Chart".

*At the bottom of settings window, click on "Template", "Save As...", then name this theme of graph setting for future call up such as "My chart setting".

*Click OK.

ProfitBee59 v4.0ProfitBee59 v4.0 for TradingView helps you do tedious works on your technical charts. It does CC59 counting and prints out positive or negative number on each price bar. When the counting arrives at -9 or +9, it creates respectable support and resistance ( SNR ) levels on the chart. It also analyses the candlesticks for high probability buy/sell regions and draws green/red color on an average line. In addition, other auxiliary tool such as Max/Min finder can be used to find the candlesticks with local max/min prices.

For Forex trading, other intraday parameters are also available including the day opening level, high/low of yesterday, high/low of the day before yesterday and intraday brown background marking time interval for key trading hours in Asian-London-New York markets.

Smart phone/tablet and PC notifications of events occurring in the chart can be sent to you by server-side alerts so that you don't have to stay in front of the screen all the time.

=================================================================

The script ProfitBee59 v4.0 for TradingView is locked and protected. Contact the author for your access.

=================================================================

How to install the script:

------------------------------

*Go to the bottom of this page and click on "Add to Favorite Scripts".

*Remove older version of the script by clicking on the "X" button behind the indicator line at the top left corner of the chart window.

*Open a new chart at and click on the "Indicators" tab.

*Click on the "Favorites" tab and choose "ProfitBee59 v4.0".

*Right click anywhere on the graph, choose "Color Theme", the select "Dark".

*Right click anywhere on the graph, choose "Settings".

*In "Symbol" tab, set "Precision" to 1/100 for stock price or 1/100000 for Forex and set "Time Zone" to your local time.

*In "Status line" tab, uncheck "Indicator Arguments".

*In "Scales" tab, check "Indicator Last Value Label".

*In "Events" tab, check "Show Dividends on Chart", "Show Splits on Chart" and "Show Earnings on Chart".

*At the bottom of settings window, click on "Template", "Save As...", then name this theme of graph setting for future call up such as "My chart setting".

*Click OK.

[Autoview][BackTest]Dual MA Ribbons R0.12 by JustUncleLThis is an implementation of a strategy based on two MA Ribbons, a Fast Ribbon and a Slow Ribbon. This strategy can be used on Normal candlestick charts or Renko charts (if you are familiar with them).

The strategy revolves around a pair of scripts: One to generate alerts signals for Autoview and one for Backtesting, to tune your settings.

The risk management options are performed within the script to set SL(StopLoss), TP(TargetProfit), TSL(Trailing Stop Loss) and TTP (Trailing Target Profit). The only requirement for Autoview is to Buy and Sell as directed by this script, no complicated syntax is required.

The Dual Ribbons are designed to capture the inferred behavior of traders and investors by using two groups of averages:

> Traders MA Ribbon: Lower MA and Upper MA (Aqua=Uptrend, Blue=downtrend, Gray=Neutral), with center line Avg MA (Orange dotted line).

> Investors MAs Ribbon: Lower MA and Upper MA (Green=Uptrend, Red=downtrend, Gray=Neutral), with center line Avg MA (Fuchsia dotted line).

> Anchor time frame (0=current). This is the time frame that the MAs are calculated for. This way 60m MA Ribbons can be viewed on a 15 min chart to establish tighter Stop Loss conditions.

Trade Management options:

Option to specify Backtest start and end time.

Trailing Stop, with Activate Level (as % of price) and Trailing Stop (as % of price)

Target Profit Level, (as % of price)

Stop Loss Level, (as % of price)

BUY green triangles and SELL dark red triangles

Trade Order closed colour coded Label:

>> Dark Red = Stop Loss Hit

>> Green = Target Profit Hit

>> Purple = Trailing Stop Hit

>> Orange = Opposite (Sell) Order Close

Trade Management Indication:

Trailing Stop Activate Price = Blue dotted line

Trailing Stop Price = Fuschia solid stepping line

Target Profit Price = Lime '+' line

Stop Loss Price = Red '+' line

Dealing With Renko Charts:

If you choose to use Renko charts, make sure you have enabled the "IS This a RENKO Chart" option, (I have not so far found a way to Detect the type of chart that is running).

If you want non-repainting Renko charts you MUST use TRADITIONAL Renko Bricks. This type of brick is fixed and will not change size.

Also use Renko bricks with WICKS DISABLED. Wicks are not part of Renko, the whole idea of using Renko bricks is not to see the wick noise.

Set you chart Time Frame to the lowest possible one that will build enough bricks to give a reasonable history, start at 1min TimeFrame. Renko bricks are not dependent on time, they represent a movement in price. But the chart candlestick data is used to create the bricks, so lower TF gives more accurate Brick creation.

You want to size your bricks to 2/1000 of the pair price, so for ETHBTC the price is say 0.0805 then your Renko Brick size should be about 2*0.0805/1000 = 0.0002 (round up).

You may find there is some slippage in value, but this can be accounted for in the Backtest by setting your commission a bit higher, for Binance for example I use 0.2%

Special thanks goes to @CryptoRox for providing the initial Risk management Framework in his "How to automate this strategy for free using a chrome extension" example.

VWAP forex Yesterday Hi/Low update fix This script is an updte fix of an earlier script that stopped functioning when TradingView updated Pine script. This script plots Forex (24 hour session) VWAP, yesterday's high, low, open and close (HLOC),

the day before's HLOC -

Also plots higher timeframe 20 emas

1 minute 5, 15, 60 period 20 ema

5 minute 15, 60 period 20 ema

15 minute 60, 120 , 240 period 20 ema

60 minute 120, 240 period 20 ema

120 minute 240, D period 20 ema

240 minute D period 20 ema

Also signals inside bars (high is less than or equal to the previous bar's high and the low is greater than or equal to the previous low) the : true inside bars have a maroon triangle below the bar as well as a ">" above the bar.

If subsequest bars are inside the last bar before the last true inside bar they also are marked with an ">"

This is probably a slight variation from the way Leaf_West plots the inside bars.

It appears that he marks all bars that are inside the original bar until one a bar has a high or low

outside the original bar. But I would need to see an example on his charts.

The Time Session Glitch and the Fix FX_IDC, COINBASE and BITSTAMP:

The script will correctly default to 1700 hrs to 1700hrs EDT/EST session for FXCM.

Strangely some securities appear to erroneously start their session at 1200 hrs ie. My guess is that they are somehow tied to GMT+0 instead of New York time (GMT+5). See this for yourself by selecting EURUSD using the FXCM exchange (FX:EURUSD) and then EURUSD from the IDC exchange (FX_IDC:EURUSD). The FX-IDC session opening range starts 5 hours before it actually should at 1700 hrs EDT/EST. To correct for this I have implemented an automatic fix (default) and a user selected "5 hour time shift adjust. ment needed on some securities".

There is also a 4 hour time shift button which might be necessary when New York reverts from Eastern Standard Time to Eastern Daylight Time (1 hour difference) in March (and then back again in November). In the default auto adjust mode you will need to select the 1 hour time shift. That is if this glitch still exists at that time.

I have looked at other scripts, other than my own and where the script is available, that need to use information about the opening bar and all have the same time shift issue

COINBASE and BITSTAMP open at 0000 hours GMT. Since I use lines instead of circles or crosses I had to make a small adjustment to plot the lines correctly.

If it needs work let me know.

Jayy

alpha Renko intraday wave timeI was asked to share my experimental Renko intraday wave time. So here it is warts and all. The same for the rest - except the Weis cumulative volume.

Renko wave time is in minutes. This script is strictly intraday and has not been played with extensively.

You must use traditional Renko and set the script wave size to the same size as the Renko brick size.

If you click on the sideways wishbone or "V" in the middle upper part of the chart you will get all of the scripts in this particular sandbox. After clicking the sideways wish bone click on "make it mine". You will then have the whole sandbox. The only published script is the Weis cumulative wave.

The "Boys MAs" is supposed to be a script for daily charts and from within some kind of consolidation. In any case I am intrigued by some signals. You have a variety of sandbox options in the format section of the boys MAs.

These codes are pretty rough with lots of abandoned lines of script.

MTF EMA Smooth Indicator By : KaizenotradingPH (Open Source)This indicator script can display three different timeframe MTF EMA indicators simultaneously. The special thing of this script is that it has smoothing feature that can smooth the MTF EMA but only in minutes and hours timeframe (script limitation). You can enable the anti repainting as well which reference the previous bar. These features are useful for customize strategies scripts to avoid repainting. Additionally, this script have customizable length for the three MTF EMA indicators.

This is the open source version of the script.

Lunar calendar day Crypto Trading StrategyLunar calendar day Crypto Trading Strategy

This strategy explores the potential impact of the lunar calendar on cryptocurrency price cycles.

It implements a simple but unconventional rule:

Buy on the 5th day of each lunar month

Sell on the 26th day of the lunar month

No trades between January 1 (solar) and Lunar New Year’s Day (holiday buffer period)

Research background

Several academic studies have investigated the influence of lunar cycles on financial markets. Their findings suggest:

Returns tend to be higher around the full moon compared to the new moon.

Periods between the full moon and the waning phase often show stronger average returns than the waxing phase.

This strategy combines those observations into a practical implementation by testing fixed entry (lunar day 5) and exit (lunar day 26) points, while excluding the transition period from solar New Year to Lunar New Year, effectively capturing mid-month lunar effects.

How it works

The script includes a custom lunar date calculation function, reconstructing lunar months and days for each year (2020–2026).

On lunar day 5, the strategy opens a long position with 100% of equity.

On lunar day 26, the strategy closes the position.

No trades are executed between Jan 1 and Lunar New Year’s Day.

All trades include:

Commission: 0.1%

Slippage: 3 ticks

Position sizing uses the entire equity (100%) for simplicity, but this is not recommended for live trading.

Why this is original

Unlike mashups of built-in indicators, this script:

Implements a full lunar calendar system inside Pine Script.

Translates academic findings on lunar effects into an applied backtest.

Adds a realistic trading filter (holiday gap) based on cultural/seasonal calendar rules.

Provides researchers and traders with a framework to explore non-traditional, time-based signals.

Notes

This is an experimental, research-oriented strategy, not financial advice.

Results are highly dependent on the chosen period (2020–2026).

Using 100% equity per trade is for simplification only and is not a viable money management practice.

The purpose is to investigate whether cyclical patterns linked to lunar time can provide any statistical edge in ETHUSDT.

IU Trailing Stop Loss MethodsThe 'IU Trailing Stop Loss Methods' it's a risk management tool which allows users to apply 12 trailing stop-loss (SL) methods for risk management of their trades and gives live alerts when the trailing Stop loss has hit. Below is a detailed explanation of each input and the working of the Script.

Main Inputs:

- bar_time: Specifies the date from which the trade begins and entry price will be the open of the first candle.

- entry_type: Choose between 'Long' or 'Short' positions.

- trailing_method: Select the trailing stop-loss method. Options include ATR, Parabolic SAR, Supertrend, Point/Pip based, Percentage, EMA, Highest/Lowest, Standard Deviation, and multiple target-based methods.

- exit_after_close: If checked, exits the trade only after the candle closes.

Optional Inputs:

ATR Settings:

- atr_Length: Length for the ATR calculation.

- atr_factor: ATR multiplier for SL calculation.

Parabolic SAR Settings:

- start, increment, maximum: Parameters for the Parabolic SAR indicator.

Supertrend Settings:

- supertrend_Length, supertrend_factor: Length and factor for the Supertrend indicator.

Point/Pip Based:

- point_base: Set trailing SL in points/pips.

Percentage Based:

- percentage_base: Set SL as a percentage of entry price.

EMA Settings:

- ema_Length: Length for EMA calculation.

Standard Deviation Settings:

- std_Length, std_factor: Length and factor for standard deviation calculation.

Highest/Lowest Settings:

- highest_lowest_Length: Length for the highest/lowest SL calculation.

Target-Based Inputs:

- ATR, Point, Percentage, and Standard Deviation based target SL settings with customizable lengths and multipliers.

Entry Logic:

- Trades initiate based on the entry_type selected and the specified bar_time.

- If Long is selected, a long trade is initiated when the conditions match, and vice versa for Short.

Trailing Stop-Loss (SL) Methods Explained:

The strategy dynamically adjusts stop-loss based on the chosen method. Each method has its calculation logic:

- ATR: Stop-loss calculated using ATR multiplied by a user-defined factor.

- Parabolic SAR: Uses the Parabolic SAR indicator for trailing stop-loss.

- Supertrend: Utilizes the Supertrend indicator as the stop-loss line.

- Point/Pip Based: Fixed point-based stop-loss.

- Percentage Based: SL set as a percentage of entry price.

- EMA: SL based on the Exponential Moving Average.

- Highest/Lowest: Uses the highest high or lowest low over a specified period.

- Standard Deviation: SL calculated using standard deviation.

Exit Conditions:

- If exit_after_close is enabled, the position will only close after the candle confirms the stop-loss hit.

- If exit_after_close is disabled, the strategy will close the trade immediately when the SL is breached.

Visualization:

The script plots the chosen trailing stop-loss method on the chart for easy visualization.

Target-Based Trailing SL Logic:

- When a position is opened, the strategy calculates the initial stop-loss and progressively adjusts it as the price moves favorably.

- Each SL adjustment is stored in an array for accurate tracking and visualization.

Alerts and Labels:

- When the Entry or trailing stop loss is hit this scripts draws a label and give alert to the user that trailing stop has been hit for the trade.

Note - on the historical data The Script will show nothing if the entry and the exit has happened on the same candle, because we don't know what was hit first SL or TP (basically how the candle was formed on the lower timeframe).

Summary:

This script offers flexible trailing stop-loss options for traders who want dynamic risk management in their strategies. By offering multiple methods like ATR, SAR, Supertrend, and EMA, it caters to various trading styles and risk preferences.

Systematic Investment Tracker by Ceyhun Gonul### English Description

**Systematic Investment Tracker with Enhanced Features**

This script, titled **Systematic Investment Tracker with Enhanced Features**, is a TradingView tool designed to support systematic investments across different market conditions. It provides traders with two customizable investment strategies — **Continuous Buying** and **Declining Buying** — and includes advanced dynamic investment adjustment features for each.

#### Detailed Explanation of Script Features and Originality

1. **Two Investment Strategies**:

- **Continuous Buying**: This strategy performs purchases consistently at each interval, as set by the user, regardless of market price changes. It follows the principle of dollar-cost averaging, allowing users to build an investment position over time.

- **Declining Buying**: Unlike Continuous Buying, this strategy triggers purchases only when the asset's price has declined from the previous interval's closing price. This approach helps users capitalize on lower price points, potentially improving average costs during downward trends.

2. **Dynamic Investment Adjustment**:

- For both strategies, the script includes a **Dynamic Investment Adjustment** feature. If enabled, this feature increases the purchasing amount by 50% if the current price has fallen by a specific user-defined percentage relative to the previous price. This allows users to accumulate a larger position when the asset is declining, which may benefit long-term cost-averaging strategies.

3. **Customizable Time Frames**:

- Users can specify a **start and end date** for investment, allowing them to restrict or backtest strategies within a specific timeframe. This feature is valuable for evaluating strategy performance over specific market cycles or historical periods.

4. **Graphical Indicators and Labels**:

- The script provides graphical labels on the chart that display purchase points. These indicators help users visualize their investment entries based on the strategy selected.

- A summary **performance label** is also displayed, providing real-time updates on the total amount spent, accumulated quantity, average cost, portfolio value, and profit percentage for each strategy.

5. **Language Support**:

- The script includes English and Turkish language options. Users can toggle between these languages, allowing the summary label text and descriptions to be displayed in their preferred language.

6. **Performance Comparison Table**:

- An optional **Performance Comparison Table** is available, offering a side-by-side analysis of net profit, total investment, and profit percentage for both strategies. This comparison table helps users assess which strategy has yielded better returns, providing clarity on each approach's effectiveness under the chosen parameters.

#### How the Script Works and Its Uniqueness

This closed-source script brings together two established investment strategies in a single, dynamic tool. By integrating continuous and declining purchase strategies with advanced settings for dynamic investment adjustment, the script offers a powerful, flexible tool for both passive and active investors. The design of this script provides unique benefits:

- Enables automated, systematic investment tracking, allowing users to build positions gradually.

- Empowers users to leverage declines through dynamic adjustments to optimize average cost over time.

- Presents an easy-to-read performance label and table, enabling an efficient and transparent performance comparison for informed decision-making.

---

### Türkçe Açıklama

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi**

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi** adlı bu TradingView scripti, çeşitli piyasa koşullarında sistematik yatırım stratejilerini desteklemek üzere tasarlanmış bir araçtır. Script, kullanıcıya iki özelleştirilebilir yatırım stratejisi — **Sürekli Alım** ve **Düşen Alım** — ve her strateji için gelişmiş dinamik yatırım ayarlama seçenekleri sunar.

#### Script Özelliklerinin Detaylı Açıklaması ve Özgünlük

1. **İki Yatırım Stratejisi**:

- **Sürekli Alım**: Bu strateji, fiyat değişimlerine bakılmaksızın kullanıcının belirlediği her aralıkta sabit bir miktar yatırım yapar. Bu yaklaşım, uzun vadede pozisyonu kademeli olarak oluşturmak isteyenler için idealdir.

- **Düşen Alım**: Sürekli Alım’ın aksine, bu strateji yalnızca fiyat bir önceki aralığın kapanış fiyatına göre düştüğünde alım yapar. Bu yöntem, yatırımcıların daha düşük fiyatlardan alım yaparak ortalama maliyeti potansiyel olarak iyileştirmelerine yardımcı olur.

2. **Dinamik Yatırım Ayarlaması**:

- Her iki strateji için de **Dinamik Yatırım Ayarlaması** özelliği bulunmaktadır. Bu özellik aktif edildiğinde, mevcut fiyatın bir önceki fiyata göre kullanıcı tarafından belirlenen bir yüzde oranında düşmesi durumunda alım miktarını %50 artırır. Bu durum, uzun vadede maliyet ortalaması stratejilerine katkıda bulunur.

3. **Özelleştirilebilir Tarih Aralığı**:

- Kullanıcılar, yatırımı belirli bir tarih aralığında sınırlandırmak veya test etmek için bir **başlangıç ve bitiş tarihi** belirleyebilir. Bu özellik, strateji performansını geçmiş piyasa döngüleri veya belirli dönemlerde değerlendirmek için kullanışlıdır.

4. **Grafiksel İşaretleyiciler ve Etiketler**:

- Script, grafik üzerinde alım noktalarını gösteren işaretleyiciler sağlar. Bu görsel göstergeler, kullanıcıların seçilen stratejiye göre yatırım girişlerini görselleştirmesine yardımcı olur.

- Ayrıca, her strateji için harcanan toplam tutar, biriken miktar, ortalama maliyet, portföy değeri ve kâr yüzdesi gibi bilgileri gerçek zamanlı olarak gösteren bir **performans etiketi** sunar.

5. **Dil Desteği**:

- Script, İngilizce ve Türkçe dillerini desteklemektedir. Kullanıcılar, performans etiketi metninin ve açıklamalarının tercih ettikleri dilde görüntülenmesi için dil seçimini yapabilir.

6. **Performans Karşılaştırma Tablosu**:

- İsteğe bağlı olarak kullanılabilen bir **Performans Karşılaştırma Tablosu**, her iki strateji için net kâr, toplam yatırım ve kâr yüzdesi gibi bilgileri yan yana analiz eder. Bu tablo, kullanıcıların hangi stratejinin daha yüksek getiri sağladığını değerlendirmesine yardımcı olur.

#### Scriptin Çalışma Prensibi ve Özgünlüğü

Bu script, iki yatırım stratejisini gelişmiş bir araçta birleştirir. Sürekli ve düşen fiyatlara dayalı alım stratejilerini dinamik yatırım ayarlama özelliğiyle entegre ederek yatırımcılar için güçlü ve esnek bir çözüm sunar. Script’in tasarımı aşağıdaki benzersiz faydaları sağlamaktadır:

- Otomatik, sistematik yatırım takibi yaparak kullanıcıların pozisyonlarını kademeli olarak oluşturmalarına olanak tanır.

- Dinamik ayarlama ile düşüşlerden yararlanarak zaman içinde ortalama maliyeti optimize etme olanağı sağlar.

- Her iki stratejinin performansını basit ve anlaşılır bir şekilde karşılaştıran etiket ve tablo ile verimli bir performans değerlendirmesi sunar.

chrono_utilsLibrary "chrono_utils"

📝 Description

Collection of objects and common functions that are related to datetime windows session days and time ranges. The main purpose of this library is to handle time-related functionality and make it easy to reason about a future bar checking if it will be part of a predefined session and/or inside a datetime window. All existing session functionality I found in the documentation e.g. "not na(time(timeframe, session, timezone))" are not suitable for strategy scripts, since the execution of the orders is delayed by one bar, due to the script execution happening at the bar close. Moreover, a history operator with a negative value that looks forward is not allowed in any pinescript expression. So, a prediction for the next bar using the bars_back argument of "time()"" and "time_close()" was necessary. Thus, I created this library to overcome this small but very important limitation. In the meantime, I added useful functionality to handle session-based behavior. An interesting utility that emerged from this development is data anomaly detection where a comparison between the prediction and the actual value is happening. If those two values are different then a data inconsistency happens between the prediction bar and the actual bar (probably due to a holiday, half session day, a timezone change etc..)

🤔 How to Guide

To use the functionality this library provides in your script you have to import it first!

Copy the import statement of the latest release by pressing the copy button below and then paste it into your script. Give a short name to this library so you can refer to it later on. The import statement should look like this:

import jason5480/chrono_utils/2 as chr

To check if a future bar will be inside a window first of all you have to initialize a DateTimeWindow object.

A code example is the following:

var dateTimeWindow = chr.DateTimeWindow.new().init(fromDateTime = timestamp('01 Jan 2023 00:00'), toDateTime = timestamp('01 Jan 2024 00:00'))

Then you have to "ask" the dateTimeWindow if the future bar defined by an offset (default is 1 that corresponds th the next bar), will be inside that window:

// Filter bars outside of the datetime window

bool dateFilterApproval = dateTimeWindow.is_bar_included()

You can visualize the result by drawing the background of the bars that are outside the given window:

bgcolor(color = dateFilterApproval ? na : color.new(color.fuchsia, 90), offset = 1, title = 'Datetime Window Filter')

In the same way, you can "ask" the Session if the future bar defined by an offset it will be inside that session.

First of all, you should initialize a Session object.

A code example is the following:

var sess = chr.Session.new().from_sess_string(sess = '0800-1700:23456', refTimezone = 'UTC')

Then check if the given bar defined by the offset (default is 1 that corresponds th the next bar), will be inside the session like that:

// Filter bars outside the sessions

bool sessionFilterApproval = view.sess.is_bar_included()

You can visualize the result by drawing the background of the bars that are outside the given session:

bgcolor(color = sessionFilterApproval ? na : color.new(color.red, 90), offset = 1, title = 'Session Filter')

In case you want to visualize multiple session ranges you can create a SessionView object like that:

var view = SessionView.new().init(SessionDays.new().from_sess_string('2345'), array.from(SessionTimeRange.new().from_sess_string('0800-1600'), SessionTimeRange.new().from_sess_string('1300-2200')), array.from('London', 'New York'), array.from(color.blue, color.orange))

and then call the draw method of the SessionView object like that:

view.draw()

🏋️♂️ Please refer to the "EXAMPLE DATETIME WINDOW FILTER" and "EXAMPLE SESSION FILTER" regions of the script for more advanced code examples of how to utilize the full potential of this library, including user input settings and advanced visualization!

⚠️ Caveats

As I mentioned in the description there are some cases that the prediction of the next bar is not accurate. A wrong prediction will affect the outcome of the filtering. The main reasons this could happen are the following:

Public holidays when the market is closed

Half trading days usually before public holidays

Change in the daylight saving time (DST)

A data anomaly of the chart, where there are missing and/or inconsistent data.

A bug in this library (Please report by PM sending the symbol, timeframe, and settings)

Special thanks to @robbatt and @skinra for the constructive feedback 🏆. Without them, the exposed API of this library would be very lengthy and complicated to use. Thanks to them, now the user of this library will be able to get the most, with only a few lines of code!

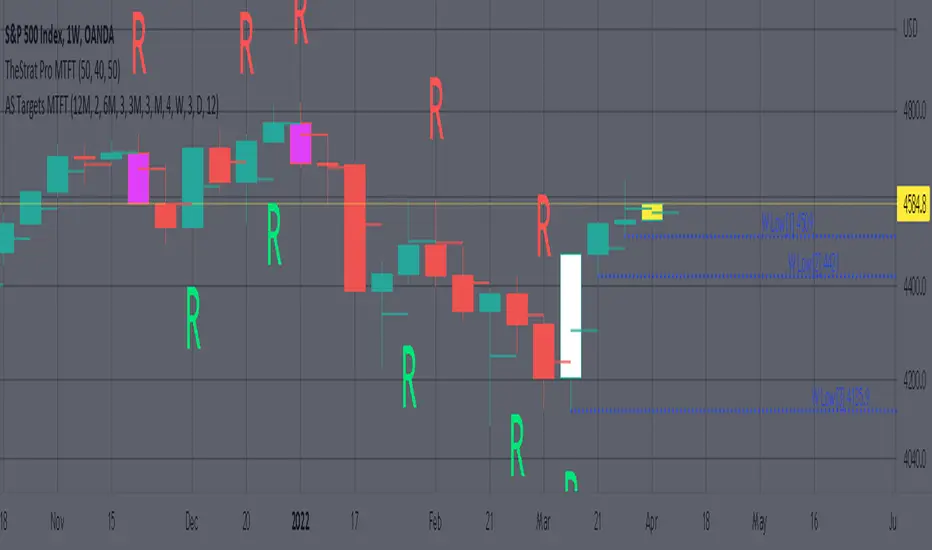

MTFT Reversal Lines, TheStrat Suite (5of5)Multi Time Frame Tools

Multi Time Frame Tools (MTFT) is a suite of scripts aimed to establish a standard timeframe-based color scheme. This can be utilized to overlay different timeframes calculations/values over a single timeframe. As one example, this would allow to observe the 5-month moving average, 5-week moving average, and 5-day moving average overlaid over each other. This would allow to study a chart, get accustomed to the color scheme and study all these at the same time much easier.

All indicators calculated using the below specific timeframes as input, will always use the color scheme outlined below. This is to get you in habit of recognizing the different timeframes overlaid in top of each other. These can be personalized.

Longer TF analysis.

Yearly - Black

Semi-Annual - Yellow

Quarterly - White

Monthly - Maroon

Weekly - Royal Blue

Daily - Lime

Shorter TF analysis.

4 hour - Fuchsia

1 hour - Orange

30 min - Red

15 min - Brown

10 min - Purple

5 min - Lilac

All color coordination is able to be modified in either the “Inputs” or “Style” section. If you need to make changes, make sure to select “Save as Default” on the bottom right of the settings menu.

Recommended Chart Color Layout

I played around with color coordination a lot. The final product was what worked best for me. I personally use the following chart settings to accent all available TF colors.

-> Click on the settings wheel on your chart. -> Click on “Appearance”.

Background - Solid -> On the top row pick the 6th color from the left.

Vert Grid Lines and Horz Grid Lines -> On the top row pick the 7th color from the left.

You may of course change these and the indicator line colors as you like.

Adding indicator to Chart

-> Open the TradingView “Indicators & Strategies” library, the icon has “ƒx”. -> All premium scripts will be located under “Invite-Only Scripts” -> Click indicator to add to your chart.

MTFT TheStrat Suite (5 Scripts)

Rob Smith is the creator of ‘TheStrat’ trading strategy. For ‘TheStrat’ I have put together a suite of 5 premium scripts that combined will offer people interested in learning ‘TheStrat’ a cleaner learning process. For 2 of the 5 scripts specifically, the MTFT approach of overlaying multiple longer timeframes(TF) over a shorter TF selected as a display cannot be utilized. The other 2 scripts will have full MTFT functionality and they are my personal favorite. I will be providing very basic info to utilize this script; it is up to you to dive deep into learning this strategy. I am not an expert with the tool or a financial advisor. As with all aspects of life, I recommend you research, learn, discern and practice extensively in order to become a master.

1. MTFT Patterns Pro/Noob

2. MTFT Full Time Frame Continuity Table

3. MTFT Last HML wOpen

4. MTFT Actionable Signal Targets

*5. MTFT Reversal Lines

MTFT Reversal Lines, TheStrat Suite (5of5)

This script will plot the line at the point that the reversal was formed for multiple timeframes. Often times price retraces to these points before making more explosive moves in continuation of the reversal direction.

The script has the following features.

Six user selected time frames per script instance can be enabled/disabled. Timeframes include: Yearly(Y), Semi-annually(S), Quarterly(Q), Monthly(M), Weekly(W), Daily(D), 4 hour, 1 hour, 30 min, 15 min, 10 min, and 5 min. Image below shows the Weekly TF selected, and only the W, Q, M, and W are enabled. I’ve included some comments on basic observations.

2. Auto hide lower timeframe calculations. Auto Hide feature will hide smaller TF calculations when a larger timeframe is selected as the display TF. Example, when the Daily timeframe candlestick selected the 4 hour and smaller calculations are hidden because they produce irrelevant results relative to the selected timeframe. If a lower TF is selected such as the 30 min candlestick, the previously hidden timeframes are now displayed. This allows easier study as you change between displayed timeframes.

This script works best in conjunction with ‘MTFT Last HML Band wOpen’. In the image below I have the W candlestick selected, along with the Q HML Lines, and the Q Reversal Line shown. It shows you a clearer picture of how price moves on a TheStrat continuation CS and after a TheStrat reversal point is made. This lets you break into the fine details of what happened inside Quarter 1, 2022 and after the reversal point was formed.

IMPORTANT NOTE for TradingView admin: One of the lessons I would consider most important in attaining clarity regarding trading, is “TheStrat” by Rob Smith. His lesson on “actionable signals” is something that can be applied to any strategy. For this reason, I am including “MTFT TheStrat Patterns Pro” script in all images that will depict confluence for a better trade selection.

Example using TheStrat Pro MTFT with this indicator.

Look for a “TheStrat actionable signal” or a “TheStrat Reversal signal” on a smaller timeframe that has an instance of this indicator on a larger timeframe calculation that is in range of the candlestick that formed your actionable signal. This means that the indicators plot you are observing must be above the low and below the high of the candlestick that is the actionable signal/reversal signal. Image below shows what this would look like with this indicator.

The Image below shows what this would look like with this indicator. The selected candlestick is the 3-day, it shows a 2U-1-potential 2D Reversal pattern and the Quarter Reversal Down line in range. This actionable signal is meant to be played for SHORTS. If the low is breached, you would enter a SHORT position from the low of the inside candlestick. For targets you would look at the previous pivots, for this example all targets were hit. This won’t always play out so nice and clean, but given that there is so many stocks and so many signals this is just a thought to improve the quality of the signal as it has extra confluence.

MTFT Actionable Signal Targets, TheStrat Suite (4of5)Multi Time Frame Tools

Multi Time Frame Tools (MTFT) is a suite of scripts aimed to establish a standard timeframe-based color scheme. This can be utilized to overlay different timeframes calculations/values over a single timeframe. As one example, this would allow to observe the 5-month moving average, 5-week moving average, and 5-day moving average overlaid over each other. This would allow to study a chart, get accustomed to the color scheme and study all these at the same time much easier.

All indicators calculated using the below specific timeframes as input, will always use the color scheme outlined below. This is to get you in habit of recognizing the different timeframes overlaid in top of each other. These can be personalized.

Longer TF analysis.

Yearly - Black

Semi-Annual - Yellow

Quarterly - White

Monthly - Maroon

Weekly - Royal Blue

Daily - Lime

Shorter TF analysis.

4 hour - Fuchsia

1 hour - Orange

30 min - Red

15 min - Brown

10 min - Purple

5 min - Lilac

All color coordination is able to be modified in either the “Inputs” or “Style” section. If you need to make changes, make sure to select “Save as Default” on the bottom right of the settings menu.

Recommended Chart Color Layout

I played around with color coordination a lot. The final product was what worked best for me. I personally use the following chart settings to accent all available TF colors.

-> Click on the settings wheel on your chart. -> Click on “Appearance”.

Background - Solid -> On the top row pick the 6th color from the left.

Vert Grid Lines and Horz Grid Lines -> On the top row pick the 7th color from the left.

You may of course change these and the indicator line colors as you like.

Adding indicator to Chart

-> Open the TradingView “Indicators & Strategies” library, the icon has “ƒx”. -> All premium scripts will be located under “Invite-Only Scripts” -> Click indicator to add to your chart.

MTFT TheStrat Suite (5 Scripts)

Rob Smith is the creator of ‘TheStrat’ trading strategy. For ‘TheStrat’ I have put together a suite of 5 premium scripts that combined will offer people interested in learning ‘TheStrat’ a cleaner learning process. For 2 of the 5 scripts specifically, the MTFT approach of overlaying multiple longer timeframes(TF) over a shorter TF selected as a display cannot be utilized. The other 2 scripts will have full MTFT functionality and they are my personal favorite. I will be providing very basic info to utilize this script; it is up to you to dive deep into learning this strategy. I am not an expert with the tool or a financial advisor. As with all aspects of life, I recommend you research, learn, discern and practice extensively in order to become a master.

1. MTFT Patterns Pro/Noob

2. MTFT Full Time Frame Continuity Table

3. MTFT Last HML wOpen

*4. MTFT Actionable Signal Targets

5. MTFT Reversal Lines

MTFT Actionable Signal Targets, TheStrat Suite (4of5)

Plots the previous highs/lows for the selected timeframe. Will not plot the high/low for a candlestick that is still active/open. You will have to manually Enable/Disable the high/low depending on the type of actionable signal that you are observing. Previous high/low lines will start from the near exact time that it opened so you can see exactly from what previous candlestick you are tracking each target.

Features includes:

1. Six Different Timeframes per script instance. Example below shows a weekly timeframe selected with a Shooting Star as the actionable signal that is being considered along with the past 3 lows for the Week timeframe being enabled. These would be your targets if you were to enter this SHORT trade. Keep in mind that every new week that opens the script will update to the newest 3 lows so if you are still inside a trade you might have to increase the number of past lines in order to keep an eye on the original targets. Which is why I selected 3 in this example, even if there is only 2 targets in mind.

The script will allow you to observe how price moves after an actionable signal is triggered and as it approaches the targets on smaller timeframes. Here is the setup from above on a daily timeframe selected showing how priced moved to the targets. This is all based on Robs teachings, but broken down to better grasp how price moves between pivots.

2. 20 different TF to pick from per slot. Timeframes(TF) include: Yearly(Y), Semi-annually(S), Quarterly(Q), Monthly(M), 2-Week(2W), Weekly(W), 3-Day(3D), Daily(D), 12 hour, 8 hour, 6 hour, 4 hour, 3 hour, 2 hour, 1 hour, 30 min, 15 min, 10 min, 5 min. NOTICE: 2W, 3D, 2D, 12h, 8h, 6h, 3h, and 2h don’t have a supported color scheme as I do not personally use them. They are available to pick from in the timeframe selection and you can set a color for these timeframes under the “Unsupported Color Scheme” section in the settings menu for the script if you would like to use them.

3. Show exact price at the pivots. Since drawing lines vs plots doesn’t show the value in the price bar on the right side this setting will show the value of the targets. Image below shows an example of how this looks.

4. Auto-hide timeframes based on specific timeframes selected. For this script, I look for timeframes smaller than the selected timeframe and auto hide these. This applies to all timeframes. For example, in the above Weekly Shooting Star example. If I were to select the monthly timeframe it would hide this timeframe selected so would not show the weekly targets. In the higher timeframes these targets are irrelevant.

IMPORTANT NOTE: One of the lessons I would consider most important in attaining clarity regarding trading, is “TheStrat” by Rob Smith. His lesson on “actionable signals” is something that can be applied to any strategy. For this reason, I am including “MTFT TheStrat Patterns Pro” script in all images that will depict confluence for a better trade selection.

Example using TheStrat Pro MTFT with this indicator.

Look for a “TheStrat actionable signal” or a “TheStrat Reversal signal” on a smaller timeframe that has an instance of this indicator on a larger timeframe calculation that is in range of the candlestick that formed your actionable signal. This means that the indicators plot you are observing must be above the low and below the high of the candlestick that is the actionable signal/reversal signal. Image below shows what this would look like with this indicator.

The Image below shows what this would look like with this indicator. The selected timeframe is the Weekly, it shows an ‘S’ char above which is an indication of a Shooting Star Actionable signal and the low from 4 months ago in range showing some potential resistance. This actionable signal is meant to be played for SHORTS. If the low is breached than you would enter a short. For targets you would look at the previous pivots, for this example all targets were hit. This wont always play out so nice and clean, but given that there is so many stocks and so many signals this is just a thought to improve the quality of the signal as it has extra confluence.

KISS BOT (Keep It Simple BOT)A very simple script that can be used for Futures and Options Trading - for stocks, crypto, forex etc.

The script includes usage of following public scripts:

1. Super Trend

2. Linear Regression

3. Exponential Moving Average

Concept, we are using three EMA, with source High, Low, and Close. We want to buy or sell when there is a crossover of third EMA (fastest) over first and second respectively.

E.g. the default values are EMA 13 High, EMA 13 Low and EMA 5 Close, we will get Buy signal when EMA 5 crosses over EMA 13 High and we will get Sell signal when EMA 5 crosses under EMA 13 Low.

Super Trend settings are made for Looking for Buy or Looking Sell, so that we focus on the trend. Trend is your friend.

Buy Trigger Line and Sell Trigger Line are just indication of using Trigger Line, buy is when EMA 5 crosses EMA 13 Low and Sell When EMA 5 Crosses EMA 13 High

The Tunnel or Band highlighted is the no trade zone for us and we do not want to trade side ways market.

Inside Bars are shown in Yellow, these candles do not qualify for any trade decision.

Outside Bars are shown in Pink, these candles do not qualify for any trade decision

Trendline Pairs (Deep Search)After getting good response on Wedge-and-Flag-Finder-Multi-zigzag , I thought I will build little bit further into the script.

Main differences

Uses deep search algorithm for patterns instead of just using last 5 pivots

Flag pattern is removed so that we can concentrate mainly on trend line pairs

More number of overall patterns.

Trend Patterns Included

Channel - Rising, Falling, Ranging

Wedge - Rising, Falling + Expanding, Contracting types

Triangle - Expanding, Contracting

Indeterminate - Happens in rare cases where angle calculation results in error. It may still belong to one of the above patterns.

Please note:

This is published as free to use but protected source code indicator. This is because the script contains deep search algorithm which isn't made public yet and is also been used in other invite only scripts.

Will not be adding alerts to this indicator.

Swing Assassin's Consolidated ScriptI put this script together to essentially consolidate a number of scripts that I use on a daily basis into one script. This is an ongoing improvement effort, so there may be some garbage in here right now so keep that in mind if you intend to use this to help in your trading.

There are 5 moving averages (Hull). I use the Fast, Mid and Slow to find entries after I us the Medium Slow and Super Slow to identify a trend. Otherwise, I have those three turned off.

This script also uses Bollinger Bands which I literally cannot trade without.

The script also has anchored VWAP , automated support/resistance lines, and a homebrewed Volume Profile that is a copy from Ildar Akhmetgaleev's indicator "Poor Man's Volume Profile" used under Mozilla Public License Version 2.0.