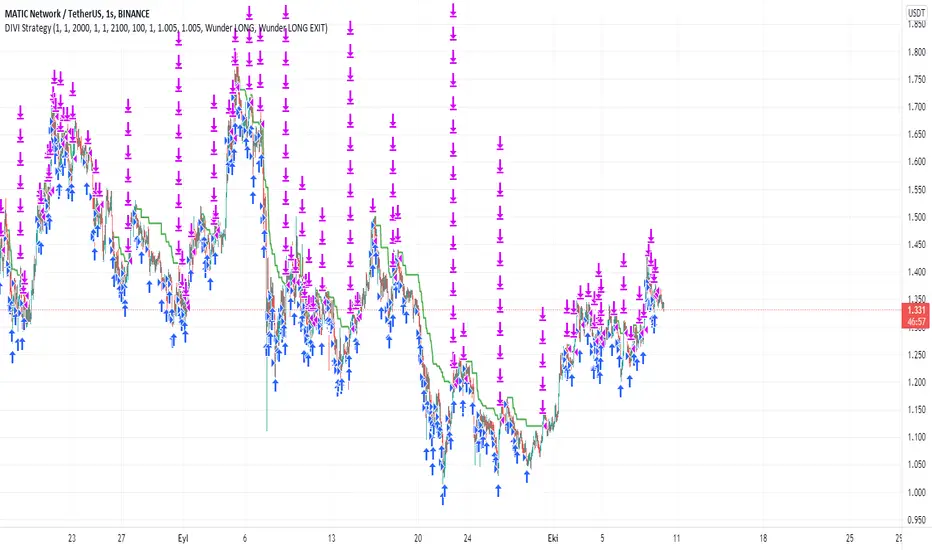

Dollar cost averaging trading system (DCA)As investors, we often face the dilemma of willing high stock prices when we sell, but not when we buy. There are times when this dilemma causes investors to wait for a dip in prices, thereby potentially missing out on a continual rise. This is how investors get lured away from the markets and become tangled in the slippery slope of market timing, which is not advisable to a long-term investment strategy.

Skyrex developed a complex trading system based on dollar-cost averaging in Quick Fingers Luc's interpretation. It is a combinations of strategies which allows to systematically accumulate assets by investing scaled amounts of money at defined market cycle global support levels. Dollar-cost averaging can reduce the overall impact of price volatility and lower the average cost per asset thus even during market slumps only a small bounce is required to reach take profit.

The strategy script monitors a chart price action and identifies bases as they form. When bases are reached the script provides entry actions. During price action development an asset value can go lower and in this way the script will perform safety entries at each subsequent accumulation levels. When weighted average entry price reaches target profit the script will perform a take profit action.

Bases are identified as pivot lows in a fractal pattern and validated by an adjustable decrease/rise percentage to ensure significancy of identified bases. To qualify a pivot low, the indicator will perform the following validation:

Validate the price rate of change on drops and bounces is above a given threshold amount.

Validate the volume at the low pivot point is above the volume moving average (using a given length).

Validate the volume amount is a given factor of magnitude above is above the volume moving average.

Validate the potential new base is not too close to the previous range by using a given price percent difference threshold amount.

A fractal pattern is a recurring pattern on a price chart that can predict reversals among larger, more chaotic price movements.

These basic fractals are composed of five or more bars. The rules for identifying fractals are as follows:

A bearish turning point occurs when there is a pattern with the highest high in the middle and two lower highs on each side.

A bullish turning point occurs when there is a pattern with the lowest low in the middle and two higher lows on each side.

Basic dollar-cost averaging approach is enhances by implementation of adjustable accumulation levels in order to provide opportunity of setting them at defined global support levels and Martingale volume coefficient to increase averaging effect. According to Quick Fingers Luc's principles trading principles we added volume validation of a base because it allows to confirm that the market is resistant to further price decrease.

The strategy supports traditional and cryptocurrency spot, futures, options and marginal trading exchanges. It works accurately with BTC, USD, USDT, ETH and BNB quote currencies. Best to use with 1H timeframe charts and limit orders. The strategy can be and should be configured for each particular asset according to its global support and resistance levels and price action cycles. You can modify levels and risk management settings to receive better performance

Advantages of this script:

Strategy has high net profit of 255% at backtests

Backtests show high accuracy around 75%

Low Drawdowns of around 14% at backtests

Strategy is sustainable to market slumps and can be used for long-term trading

The strategy provides a large number of entries which is good for diversification

Can be applied to any market and quote currency

Easy to configure user interface settings

How to use?

1. Apply strategy to a trading pair your are interested in using 1H timeframe chart

2. Configure the strategy: change layer values, order size multiple and take profit/stop loss values according to current market cycle stage

3. Set up a TradingView alert to trigger when strategy conditions are met

4. Strategy will send alerts when to enter and when to exit positions which can be applied to your portfolio using external trading platforms

5. Update settings once market conditions are changed using backtests on a monthly period

Pesquisar nos scripts por "take profit"

LudovicaLudovica is a trend following strategy that works on intraday timeframes (15 minutes).

The stop loss is decided based on the last price movement, take profits are projected through a Fibonacci extension. Two different extensions are calculated, based on a filter that affects the last price movement it is chosen which one to use for take profits.

Money management is fixed fractional: regardless of the distance between entry point and stop loss, the risk on capital for each trade is decided by the user in the strategy inputs. Take profits from 1 to 4 plan to exit with 15% of the initial size, TPs from 5 to 8 plan to exit with 10% of initial size.

There is a trailing stop system to reduce the drawdown of the strategy (note that stop loss moves as the trade develops).

Take profits are limit orders, stops (loss or trailing) occur at candlestick close (set alerts on the strategy).

Optimized strategies selectable from input panel:

-ETHUSDTPERP 15 min

-CRVUSDTPERP 15 min v1

-CRVUSDTPERP 15 min v2

-SNXUSDTPERP 15 min

Other pairs in development and soon available.

This strategy is in beta stage.

[B_1] 15min Future Based on Pullback Condition

GENERAL INTRODUCTION:

This scripts is a trend catcher strategy, looking for entry points based on pullback condition.

HOW IT WORKS:

Entry Long: when price close above 15m Supertrend and an EMA line trend, MACD (12,26,9) below MACD signal (12,26,9), RSI(14) >50 & <80 and SAR is positive.

Exit Long: when price hit TPs or touch Stoploss.

Entry Short: when price close below 15m Supertrend and an EMA line trend, MACD (12,26,9) above MACD signal (12,26,9), RSI(14) <50 & >25 and SAR is negative.

Exit Short: when price hit TPs or touch Stoploss.

HOW TO USE IT:

1. Setup comment Long/Short: this setting used for auto trading. You can fill text to alert then in alert box of Tradingview, using {{strategy.order.comment}}.

2. Setup Entry

+ EMA Length: the EMA period to filter the trend (default is 30).

+ Buy/Sell ETH follow BTC: open long/short ETHUSDTPERP when BTCUSDT touch and reject SuperTrend 1H/2H/4H.

+ Long/Short again: Allow re-entry when price hit all TP or SL.

3. Setup Exit

+ Multi profit: Take profit levels are set according to the fibonacci levels.

+ Auto find TP: If having resistants in higher timeframe near TP1, TP1 will auto set at that resistant.

+ Stoploss: you have two options: Stoploss based on percentage or ATR.

+ When price hit TP1, you have two options: only move Stoploss to entry or active trailing.

4. Custom tools

+ SuperTrend MTF: they used for take multiprofit (you can show or hide them).

+ Table result.

BACKTEST:

Currently, the strategy is optimized for: BINANCE:ETHUSDTPERP . However it can also run on some other coins like: BINANCE:RUNEUSDTPERP , BINANCE:FILUSDTPERP , ...

Parameters for BINANCE:ETHUSDTPERP:

+ 01/01/2022 to present.

+ Order size starting: 01 contract.

+ commission fee: 0.02%

+ No leverage.

=> 475 trades, ratio profit: loss is 5800: 400.

If you want access to this scripts, please inbox to me, you are always welcome.

Miyagi (10 in 1) + DCA StrategyMiyagi: The attempt at mastering something for the best results.

Miyagi indicators combine multiple trigger conditions and place them in one toolbox for traders to easily use, produce alerts, backtest, reduce risk and increase profitability.

Miyagi (10 in 1) + DCA Strategy built for the Miyagi (10 in 1) + Alerts found here:

The DCA Strategy was designed to help visualize, backtest and improve users' DCA strategies and overall profitability.

Users can backtest different trading timeframes using the start and end date inputs.

Users can backtest different take profit and stoploss percents, both long and short.

Users can choose whether or not to use DCA on the backtester via a selectable input.

Input the DCA as you would normally using the Wick Hunter bot.

Happy trading!

Miyagi (4 in 1) + DCA StrategyMiyagi: The attempt at mastering something for the best results.

Miyagi indicators combine multiple trigger conditions and place them in one toolbox for traders to easily use, produce alerts, backtest, reduce risk and increase profitability.

Miyagi (4 in 1) + DCA Strategy built for the Miyagi (4 in 1) + Alerts found here:

The DCA Strategy was designed to help visualize, backtest and improve users' DCA strategies and overall profitability.

Users can backtest different trading timeframes using the start and end date inputs.

Users can backtest different take profit and stoploss percents, both long and short.

Users can choose whether or not to use DCA on the backtester via a selectable input.

Input the DCA as you would normally using the Wick Hunter bot.

Happy trading!

Bjorgum Double Tap█ OVERVIEW

Double Tap is a pattern recognition script aimed at detecting Double Tops and Double Bottoms. Double Tap can be applied to the broker emulator to observe historical results, run as a trading bot for live trade alerts in real time with entry signals, take profit, and stop orders, or to simply detect patterns.

█ CONCEPTS

How Is A Pattern Defined?

Doubles are technical formations that are both reversal patterns and breakout patterns. These formations typically have a distinctive “M” or a “W” shape with price action breaking beyond the neckline formed by the center of the pattern. They can be recognized when a pivot fails to break when tested for a second time and the retracement that follows breaks beyond the key level opposite. This can trap entrants that were playing in the direction of the prior trend. Entries are made on the breakout with a target projected beyond the neckline equal to the height of the pattern.

Pattern Recognition

Patterns are recognized through the use of zig-zag; a method of filtering price action by connecting swing highs and lows in an alternating fashion to establish trend, support and resistance, or derive shapes from price action. The script looks for the highest or lowest point in a given number of bars and updates a list with the values as they form. If the levels are exceeded, the values are updated. If the direction changes and a new significant point is made, a new point is added to the list and the process starts again. Meanwhile, we scan the list of values looking for the distinctive shape to form as previously described.

█ STRATEGY RESULTS

Back Testing

Historical back testing is the most common method to test a strategy due in part to the general ease of gathering quick results. The underlying theory is that any strategy that worked well in the past is likely to work well in the future, and conversely, any strategy that performed poorly in the past is likely to perform poorly in the future. It is easy to poke holes in this theory, however, as for one to accept it as gospel, one would have to assume that future results will match what has come to pass. The randomness of markets may see to it otherwise, so it is important to scrutinize results. Some commonly used methods are to compare to other markets or benchmarks, perform statistical analysis on the results over many iterations and on differing datasets, walk-forward testing, out-of-sample analysis, or a variety of other techniques. There are many ways to interpret the results, so it is important to do research and gain knowledge in the field prior to taking meaningful conclusions from them.

👉 In short, it would be naive to place trust in one good backtest and expect positive results to continue. For this reason, results have been omitted from this publication.

Repainting

Repainting is simply the difference in behaviour of a strategy in real time vs the results calculated on the historical dataset. The strategy, by default, will wait for confirmed signals and is thus designed to not repaint. Waiting for bar close for entires aligns results in the real time data feed to those calculated on historical bars, which contain far less data. By doing this we align the behaviour of the strategy on the 2 data types, which brings significance to the calculated results. To override this behaviour and introduce repainting one can select "Recalculate on every tick" from the properties tab. It is important to note that by doing this alerts may not align with results seen in the strategy tester when the chart is reloaded, and thus to do so is to forgo backtesting and restricts a strategy to forward testing only.

👉 It is possible to use this script as an indicator as opposed to a full strategy by disabling "Use Strategy" in the "Inputs" tab. Basic alerts for detection will be sent when patterns are detected as opposed to complex order syntax. For alerts mid-bar enable "Recalculate on every tick" , and for confirmed signals ensure it is disabled.

█ EXIT ORDERS

Limit and Stop Orders

By default, the strategy will place a stop loss at the invalidation point of the pattern. This point is beyond the pattern high in the case of Double Tops, or beneath the pattern low in the case of Double Bottoms. The target or take profit point is an equal-legs measurement, or 100% of the pattern height in the direction of the pattern bias. Both the stop and the limit level can be adjusted from the user menu as a percentage of the pattern height.

Trailing Stops

Optional from the menu is the implementation of an ATR based trailing stop. The trailing stop is designed to begin when the target projection is reached. From there, the script looks back a user-defined number of bars for the highest or lowest point +/- the ATR value. For tighter stops the user can look back a lesser number of bars, or decrease the ATR multiple. When using either Alertatron or Trading Connector, each change in the trail value will trigger an alert to update the stop order on the exchange to reflect the new trail price. This reduces latency and slippage that can occur when relying on alerts only as real exchange orders fill faster and remain in place in the event of a disruption in communication between your strategy and the exchange, which ensures a higher level of safety.

👉 It is important to note that in the case the trailing stop is enabled, limit orders are excluded from the exit criteria. Rather, the point in time that the limit value is exceeded is the point that the trail begins. As such, this method will exit by stop loss only.

█ ALERTS

Five Built-in 3rd Party Destinations

The following are five options for delivering alerts from Double Tap to live trade execution via third party API solutions or chat bots to share your trades on social media. These destinations can be selected from the input menu and alert syntax will automatically configure in alerts appropriately to manage trades.

Custom JSON

JSON, or JavaScript Object Notation, is a readable format for structuring data. It is used primarily to transmit data between a server and a web application. In regards to this script, this may be a custom intermediary web application designed to catch alerts and interface with an exchange API. The JSON message is a trade map for an application to read equipped with where its been, where its going, targets, stops, quantity; a full diagnostic of the current state and its previous state. A web application could be configured to follow the messages sent in this format and conduct trades in sync with alerts running on the TV server.

Below is an example of a rendered JSON alert:

{

"passphrase": "1234",

"time": "2022-05-01T17:50:05Z",

"ticker": "ETHUSDTPERP",

"plot": {

"stop_price": 2600.15,

"limit_price": 3100.45

},

"strategy": {

"position_size": 0.1,

"order_action": "buy",

"market_position": "long",

"market_position_size": 0,

"prev_market_position": "flat",

"prev_market_position_size": 0

}

}

Trading Connector

Trading Connector is a third party fully autonomous Chrome extension designed to catch alert webhooks from TradingView and interface with MT4/MT5 to execute live trades from your machine. Alerts to Trading Connector are simple; just select the destination from the input drop down menu, set your ticker in the "TC Ticker" box in the "Alert Strings" section and enter your URL in the alert window when configuring your alert.

Alertatron

Alertatron is an automated algo platform for cryptocurrency trading that is designed to automate your trading strategies. Although the platform is currently restricted to crypto, it offers a versatile interface with high flexibility syntax for complex market orders and conditions. To direct alerts to Alertatron, select the platform from the 3rd party drop down, configure your API key in the ”Alertatron Key” box and add your URL in the alert message box when making alerts.

3 Commas

3 Commas is an easy and quick to use click-and-go third party crypto API solution. Alerts are simple without overly complex syntax. Messages are simply pasted into alerts and executed as alerts are triggered. There are 4 boxes at the bottom of the "Inputs" tab where the appropriate messages to be placed. These messages can be copied from 3 Commas after the bots are set up and pasted directly into the settings menu. Remember to select 3 Commas as a destination from the third party drop down and place the appropriate URL in the alert message window.

Discord

Some may wish to share their trades with their friends in a Discord chat via webhook chat bot. Messages are configured to notify of the pattern type with targets and stop values. A bot can be configured through the integration menu in a Discord chat to which you have appropriate access. Select Discord from the 3rd party drop down menu and place your chat bot URL in the alert message window when configuring alerts.

👉 For further information regarding alert setup, refer to the platform specific instructions given by the chosen third party provider.

█ IMPORTANT NOTES

Setting Alerts

For alert messages to be properly delivered on order fills it is necessary to place the following placeholder in the alert message box when creating an alert.

{{strategy.order.alert_message}}

This placeholder will auto-populate the alert message with the appropriate syntax that is designated for the 3rd party selected in the user menu.

Order Sizing and Commissions

The values that are sent in alert messages are populated from live metrics calculated by the strategy. This means that the actual values in the "Properties" tab are used and must be set by the user. The initial capital, order size, commission, etc. are all used in the calculations, so it is important to set these prior to executing live trades. Be sure to set the commission to the values used by the exchange as well.

👉 It is important to understand that the calculations on the account size take place from the beginning of the price history of the strategy. This means that if historical results have inflated or depleted the account size from the beginning of trade history until now, the values sent in alerts will reflect the calculated size based on the inputs in the "Properties" tab. To start fresh, the user must set the date in the "Inputs" tab to the current date as to remove trades from the trade history. Failure to follow this instruction can result in an unexpected order size being sent in the alert.

█ FOR PINECODERS

• With the recent introduction of matrices in Pine, the script utilizes a matrix to track pivot points with the bars they occurred on, while tracking if that pivot has been traded against to prevent duplicate detections after a trade is exited.

• Alert messages are populated with placeholders ; capability that previously was only possible in alertcondition() , but has recently been extended to `strategy.*()` functions for use in the `alert_message` argument. This allows delivery of live trade values to populate in strategy alert messages.

• New arguments have been added to strategy.exit() , which allow differentiated messages to be sent based on whether the exit occurred at the stop or the limit. The new arguments used in this script are `alert_profit` and `alert_loss` to send messages to Discord

Cyatophilum 3Commas DCA Bot BacktesterAn indicator to backtest and automate 3Commas DCA Bots.

═════════════════════════════════════════════════════════════════════════

█ HOW IT WORKS

The indicator allows you to replicate your bot settings and get backtest results from the Strategy Tester and also a backtest panel with additional information on the safety orders.

You can also create alerts for each of the strategy events.

█ HOW TO USE

Choose a symbol that corresponds to your bot pair and exchange.

Pick a chart time frame as small as possible, usually 1 minute. The timeframe should always be smaller or equal to the deal start conditions timeframes.

Always use regular candle type.

Configure your deal start condition . You can combine several technical indicators to trigger an entry using a AND logical gate.

Configure your profit target

Use the Take Profit feature to set a target in percentage of price. You can also make it trail.

There is also a Stop Loss feature that is turned off by default.

Configure your safety orders

Replicate the safety orders from your bot into the indicator inputs.

Check your backtest parameters

Make sure that the initial capital and order size make sense. Since it is a pyramiding strategy with safety orders, the sum of all deals should not be bigger than the initial capital.

In this example: Initial capital is 0.02 BTC, which around 600$. I used 1000$ to be safe.

If you use % equity as order size, please note that it will create compounding.

Check the fees, by default they are set to 0.1%.

I also recommend to set a slippage that corresponds to your exchange's spread.

█ FEATURES

• Strategy direction

Configure wether to go long or short.

• Deal Start Conditions

The current conditions available are:

- Up to 4 MTF Trading View ratings conditions (Buy/Sell, Strong Buy/Sell)

- Up to 4 MTF RSI with configurable start conditions (Less/Greater than, Crossing Up/Down)

- Up to 2 MTF Ultimate Oscillator with configurable start conditions (Less/Greater than, Crossing Up/Down)

- MTF BB%-20-1 (length-deviation) with configurable start conditions (Less/Greater than, Crossing Up/Down)

- MTF BB%-20-2 (length-deviation) with configurable start conditions (Less/Greater than, Crossing Up/Down)

- Up to 2 MTF TA presets with the following options (Bollinger Bands, MFI, CCI, MACD, PSAR, SMA crosses, Heikin Ashi)

• Stop Loss and Take Profit

Configure your stop loss and take profit for long and short trades.

You can also make a trailing take profit.

• DCA (Safety orders)

Create up to 100 safety orders with configurable options for step and volume scaling, take profit from total volume, base and safety order size.

• Backtest Settings

Choose a backtest period, longs or shorts, wether to use limit orders or not.

Graphics

A Configuration panel with all the indicator settings, useful for sharing/saving a strategy.

A Backtest Results panel with additional information from the strategy tester.

█ ALERTS

The indicator is using the alert() calls: it only uses 1 alert slot to send order messages for each event (Long/Short entry, stop loss, take profit, safety order). This means free TV plans can create 1 complete strategy.

To set your alert messages, open the indicator settings and scroll to the bottom of the "inputs" tab.

Create your alert after you set the messages in the indicator settings, and make sure "Any alert() function call" is set in the alert option.

█ BACKTEST RESULTS

The backtest settings used in this snapshot are the following:

Initial Capital: 1000€

Order size: 0.003 BTC

Commission: 0.1 % per order

Slippage : 1 tick

Please read the author instructions below for access.

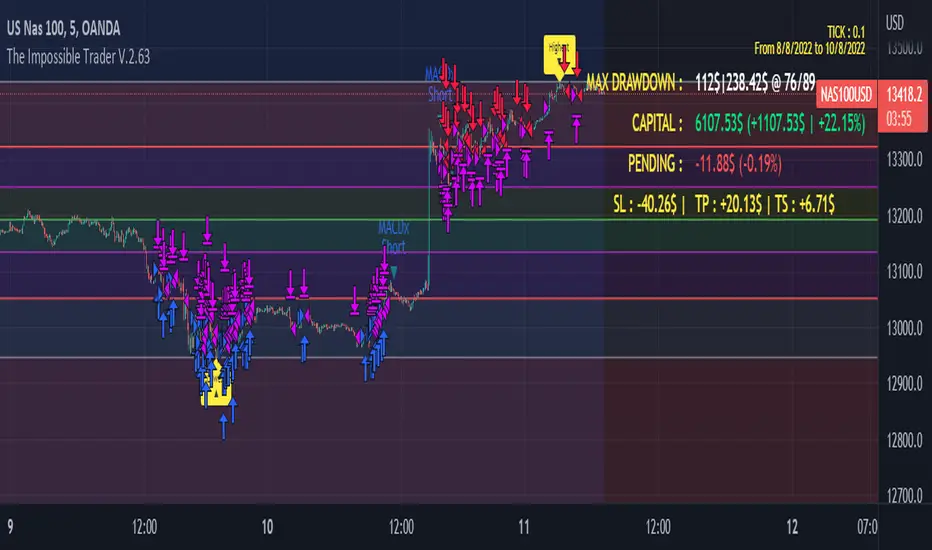

The Impossible TraderTHE IMPOSSIBLE TRADER

A simple, but effective High Freq Strategy script based on MACD or RSI trend, with extra customizable Alert Messages for Bots.

WHAT IT DOES

This script (works best at lower TimeFrames) just follow the trend of MACD or RSI on your asset.

Why it should work? Because in an upper trend, there are more chance of green candles than reds. And in dump trend there are more chance of red candles than greens.

While trend is positive, it will try to open Long orders as fast as possible at market price.

While trend is negative, it will try to open Short orders as fast as possible at market price.

HOW TO SETUP YOUR PREFERENCES

Capital : Insert a % of Margin you want to use for your positions (usually 30% is quite good)

Leverage : Choose leverage based on your plans

Trail Tick @ : This value (in Tick) tell the script "when" the "Trail Stop" order must be activated (from the Entry price)

Offset Tick @ : This is the price (in Tick) from the Trail Stop Price activated. Basically it is a Stop Loss that follow the price at a fixed distance.

SL Tick @ : Set a Stop Loss at amount Tick distance from the Entry Price. (Let's call it a Safety Stop Loss for bad decisions...)

TP Tick @ : Set a Take Profit at amount Tick distance from the Entry Price. Sometimes is better to exit in full Gain than keep positions.

Strategy : You can choose a Only Long, Only Short or Long+Short sametime strategy.

with MACD or RSI : You can try the strategy applied on MACD or applied on customizable RSI EMA

EMA : If you choosed RSI EMA, you can set any value for your testing (usually 80-120 works very nice)

Exit order after bars : Some Exchanges / Brokers apply fixed cost, and a strategy too fast could not be productive. This set will let you to delay the Exit Order on already Opened positions.

Keep Stop Loss active : If you are planning a delay for Exit Orders, sometime could be useful to keep activated Stop Loss.

Strategy Preset : Some preset I've found interesting, with good results.

BackTest Days : If there are too many results and script doesn't work, you can choose a closer range to show results.

EXTRA FEATURES

On Screen Display : OSD will show you some realtime stats about your strategy, like Asset Tick, Trading Period Range, Drawdown, Gains and not closed trade.

Alert Message : You can enter custom Long Entry/Exit and Short Entry/Exit message for your Bots (like AutoView, WunderBit, etc...). When alert is triggered, you can send custom message with {{strategy.order.comment}} in the text field

AutoView Alert Message : If you are user of AutoView, you can generate your calls. Those are tested only on Oanda with index like Sp500, US100, Us30.

TIPS ON USE

Some asset on TradingView require an higher initial capital. Go to this Script Settings -> Properties and rise Initial Capital.

Be aware of commissions and spread when evalutating a strategy. Go to this Script Settings -> Properties and set Commission and Slippage

Trail Stop and Ticks could be difficult to understand, but very profitable. Please take your time and study how it works.

Consider Tick like the minimum movement your asset can do. Ticks occurs "intra-bar", so some of your positions could be closed almost instantly.

Consider Trail Stop like a Stop Loss that keep always the same distance from your positions, but never came back . If you are in gain, say of 10 Ticks, and your Trail have 5 Ticks, this means for sure a close at minimum 5 Ticks from Entry Price.

On Screen Display will show you Ticks for your asset. This will help you on strategy settings, because not all asset responds on the same way.

ONLY LONG EXAMPLE

ONLY SHORT EXAMPLE

AltAlgoHello Traders ,

the AltAlgo is here! – our brand new trading multitool. It is an all-in-one backtesting and alert script based on our proprietary strategy and algorithms. Including many useful customizable features.

About one year ago we published our AltTrader Scalp & Swing indicator. We made a backtester for it named AltTrader BackTester Swing&Scalp. This pair of indicator and strategy turned out to be a great success. After one year of constant development and updates, we are proud to present to you our latest AltAlgo – our newest strategy script with the ability to send alerts! No more copying inputs from strategy to indicator to set alerts. Now you will prepare a strategy and create alerts in one script. We also added some new features.

AltAlgo is a great tool that helps you find the best possible entries for your trades. It's not a limited strategy for only some timeframe periods or assets. You can use it on Crypto, Forex, Stocks, Indices, and basically any chart that is available on TradingView. It is suitable for short-term scalping, mid-term and long-term swing trading, both spot and futures.

AltAlgo combines many algorithms to provide the best possible entry for you. It uses ATR, Supertrend, many different moving averages, and our proprietary system of rules and calculations to plot an ideal BUY or SELL signal for you, across all markets.

The main features/settings of the AltAlgo include :

Specific testing period - you can specify the start and end date to backtest, also the time

Power - the main variable responsible for the AltAlgo sensitivity and the amount of signals

AltFilters - these filters aim to detect the trend and prevent sending signals when the price consolidates

Supertrend - Multi time frame implementation of the famous Supertrend filter to follow the trend direction even more

Only long / only short mode - could be useful for spot trading or to create separate strategies for longs and shorts

COOS (close on opposite signal) - you can choose for the strategy to close open trades when an opposite signal comes in or not

Breakeven - if you want the AltAlgo to move stop loss to BE on chosen take profit level

Trailing stop-loss - it uses the moving target method for trailing from a chosen take profit level

Four levels for taking a profit - separate take profit levels for long and short direction, all calculations can be set in %, pips or ATR

DCA entry - function to improve your entry price and create an entry ZONE in case the price goes in the opposite direction

MultiMA - you can choose one of the 27 moving averages added to filter signals (above MA only BUY, below MA only SELL)

Sessions - we have predefined main trading sessions (America, Europe, Asia) or you can use custom settings based on any day of the week, any hours and time zones

External filter - you can use your own script to filter signals given by the AltAlgo

Miscellaneous - long/short trade background coloring, showing peak profit, etc.

Notice alerts – AltAlgo can send you additional alerts informing you about running trade like take profit or stop loss hits, flips, etc.

External output - you can use the AltAlgo as a signal provider for your other script

Alerts - fully customizable alerts for BUY/SELL signals, supporting entry zone (DCA), automatic ticker renaming (for example BTCUSDTPERP to BTCUSDT), and the option to add top and bottom lines of free text

As you can read, the AltAlgo is packed with lots of useful features, which make it irreplaceable in your trading journey. We put all our knowledge and experience to make this tool and we hope it would be useful for you and you make a lot of profits with it.

We also have a kind, amazing and helpful community of AltAlgo users, which help each other every day and share their knowledge and setups in their trading journey.

Strategy properties used:

Initial capital - 10000

Order size - 10%

Commission - 0.04%

Density & Step Grid Strategies BacktesterThis contains several signals for backtesting strategies only in binance futures assets.

HOW IT WORKS

Grid trading is a trading strategy where an investor creates a so-called "price grid". The basic idea of the strategy is to repeatedly buy at the pre-specified price and then wait for the price to rise above that level and then sell the position (and vice versa with shorting or hedging). We introduce 2 grids trading algorithms "Step" and "Density" .

FEATURES

Grid size: This algorithm has a max of 20 orders.

Take profit: The trader can increase or decrease the distance between the grids from the User Interface panel, is the the distance from average price.

Management: The algorithm distributes the capital for all orders depending on the amount fator, for example 1.1% of amount factor adds 10% over the previus order.

Stop Loss: The algorithm place the stopn using distance from the last lower / upper grid depending on the position side.

USES

Indispensable research and backtesting tool for those using bots for their investments. The algorithm produces a backtesting of the strategy for past history. It is used by professional traders to understand if this strategy has been profitable on a market and what parameters to use for bots using this strategy, only binance futures assets supported.

If you would like to develop your own algorithm with customized conditions based on a grid strategy, please contact us.

If you need help in using this tool, please contact us without hesitation.

TWAP + MA crossover Strategy [Dynamic Signal Lab]Dear TV'ers,

Hereby the strategy script for the TWAP/moving average crossover, with unique taking profit options. moving averages include: EMA , WMA , DEMA , TEMA , VAR, WWMA, ZLEMA , TSF , HULL and TILL.

Use the TWAP as the slow moving average and use another moving average as the faster/more responsive moving average. Finally, you can use a green fill to visualize how much you are in profit from your entry point.

Good strategies always involve gradual taking profit, which is also possible in this script.

You can gradually take profit (and set how much%), using the following criteria:

* minimum consecutive green/red candles

* minimum amount of green/red candles in the last 2-8 candles

* both of the above criteria.

The current default properties should be modified to make this strategy cost-effective, but typically 15minutes and higher timeframes (up to 6hr) seem to work well for larger (top10 cap) crypto projects. Don't use this script for small-caps as it will get you rekt.

Additionally, you'll also be able to continuously take profit, making sure you lock in all those sweet profits. Use this script for backtesting and the indicator compagnon to fire your alerts.

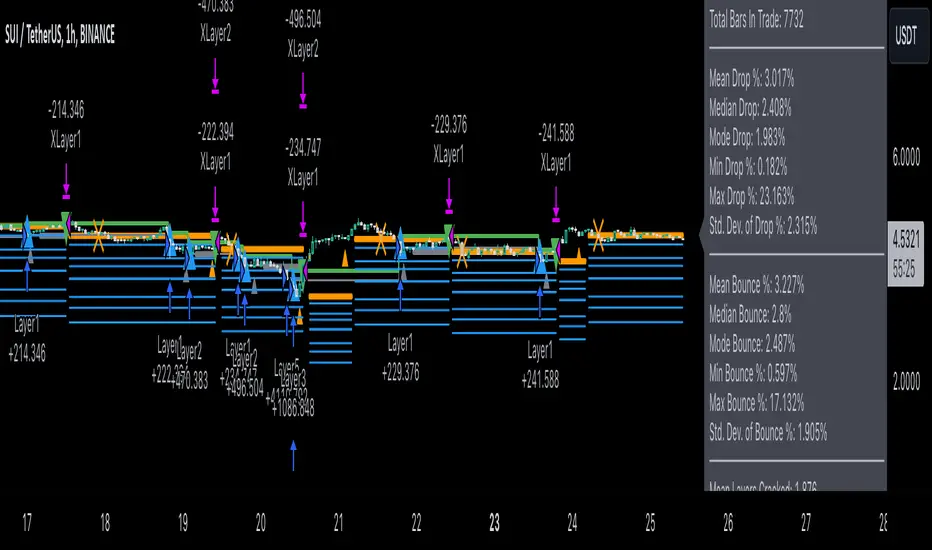

Ranged Volume DCA Strategy - R3c0nTraderUpdate: Republishing this as Public Open-Source script.

Credits:

Thank you "EvoCrypto" for granting me permission to use "Ranged Volume" to create this strategy.

Thank you "junyou0424" for granting me permission to use "DCA Bot with SuperTrend Emulator" which I used for adding bot inputs, calculations, and strategy

What does this do?

This script is mainly used for backtesting a Ranged Volume strategy to see how a 3Commas bot would perform.

I created this script out of necessity and I wanted a way to test a 3Commas DCA bot with a strategy based on “Volume.”

I came across "EvoCrypto’s" "Ranged Volume" study and strategy in TradingView and I liked it. I wanted to configure it so it can be used for DCA bot backtesting. I used parts from "junyou0424’s" "DCA Bot with SuperTrend Emulator" to add the following:

1. The Start Time and End Time

2. Price deviation to open safety orders (%)

3. Target Take Profit (%)

4. Trailing deviation

5. Base Order and Safety Order

6. Safety order volume scale

7. Safety order step scale

8. Max safety orders

In addition to the above, I also added chart indicators for "Take Profit" as well as "Safety Order"

Pre-requisites:

You can use this script without a 3Commas account and see how 3Commas DCA Bot and Ranged Volume strategy would perform vs. a non-DCA strategy. However, I highly recommend signing up for their free account and going through their training. This would give you a base understanding on the settings you will see in this strategy and why you will need to know them.

That said these are the pre-requisites I suggest you have:

1. Base Knowledge of 3Commas DCA bots

2. Base knowledge of settings such as “Max safety trades count”, “safety order volume scale” and “safety order step scale”. If these are alien to you, I suggest you read up on these.

3. Knowledge of setting up a Single-pair 3Commas bot for receiving custom TradingView signal.

4. A paper-bot to test your ideas. (Do not use a real money bot until you have tested it sufficiently with a paper-bot. You alone are responsible for your results!)

5. Add the study I created called "R3c0nTrader’s Ranged Volume Study” which adds a separate chart in its own pane showing the volume spikes. It will also generate the “buy” signals for your bot. NOTE: The study also has the same color scheme as this strategy and having the colors in both the strategy and the study will make things easier to see. If you use EvoCrypto’s Ranged Volume Study instead, just keep in mind that the colors won’t match, and you will have to manually match them.

6. Make your buy signals from your strategy are the same as in your study! To do this, use the same “Volume Range Length” you entered in the STRATEGY and enter that value for the “Volume Range Length” in the STUDY. Also ensure you have the same settings for “Heikin Ashi” (On or Off).

Comparisons of Ranged Volume Strategy vs Ranged Volume DCA Strategy

BTCUSD

Beware of Strategies that claim super high profits. This can easily be done by lowering the initial capital to something unrealistic. If I did that with this strategy and set the initial capital $100 and base order size to $100, I get a net profit of 2,864% which is not realistic.

How to Use

1. On the “Inputs” tab:

a. Set your Start and End Time to backtest against.

b. Set your “Volume Range Length” (number of bars to look back)

c. “Heikin Ashi Colors” – Usually I leave this enabled

d. “Show Bar Colors” – Leave enabled

e. “Show Break-Out” – Leave enabled

f. “Show Range” – Leave enabled

g. Set your other inputs which are those settings you would find in your 3Commas bot that you want to test (e.g., Price deviation to open safety orders, Target Take Profit, Base order, Safety order, etc.).

h. Quick Example for BTCUSD on 2hr chart:

i. Price deviation to open safety orders (%) = 6

ii. Target Take Profit (%) = 14

iii. Trailing deviation = 0

iv. Base order = 100

v. Safety order = 200

vi. Safety order volume scale = 2

vii. Safety order step scale = 1.4

viii. Max safety order = 5

2. On the “Properties” tab, set your initial capital, base currency, etc.

a. Initial capital – Default is 10,000 (Please use realistic values here. The amount here should be able to cover ALL your safety orders if they were triggered. Ideally, you should have funds left over and not use all trade capital.)

b. Base currency – Select your currency

c. Order Size - Not used. Use the “Inputs” tab to change your base order size.

d. Leave “Pyramiding” set to 999. This acts as a ceiling to the “Max safety orders” on the “Inputs” tab. It must always be higher than your “Max safety orders.” For example, if you set your “Max safety orders” to “4” and “Pyramiding” to “4” then it effectively means you have “3” “Max safety orders” and not “4” because it is counting each successive entry including the initial order.

e. “Commission” - Optional

f. “Verify price for limit orders” – Leave at zero. This does not change anything that I can tell.

g. Optional - Enter a value for “Commission”

h. Slippage – Optional. Slippage does not occur in backtesting but does occur in real trading but it can be simulated. Example use case for tracking performance of a real money bot: You enter the start date and time of your bot’s trade into this strategy and you notice some values are a little off due to slippage (average price, take profit, safety orders are not lining up) then you would go back here and increase the slippage until those lines up close enough with your actuals.

i. Margin for long positions – I don’t use this honestly.

j. Margin for short positions – I don’t use this honestly.

k. Recalculate “After order is filled” and “On every tick” – I don’t use this honestly.

3. “Style” tab

a. Ranged Volume Bar Coloring - You must disable bar coloring in any studies you added or this may not work properly

i. Color 0 – Default Yellow; appears when a volume breakout occurs

ii. Color 1 – Default Red; appears when a volume breakdown occurs

iii. Color 2 – Light Blue; appears when Close is higher than the Open

iv. Color 3 – Dark Blue; appears when the Close is lower than the Open

b. Take profit – Default Green; take profit line

c. Safety order – Default Light Blue; safety order line

d. No Safety Orders left – Default Red; when a trade runs out of safety orders, the line turns red and there is no safety orders left underneath to catch any further falling price movements.

e. Avg Position Price – Default Orange; your average position price for any given trade.

f. Take Profit Plot Area – Default Green; creates a highlighted area for your take profit

g. SO Plot Area – Default Light Blue; creates a highlighted area for your safety orders

h. Trades on chart – Show or hide your trades on the chart

i. Signal labels – Show or hide the trade signal labels on the chart

j. Quantity – Show or hide the trade quantity on the chart

Explanation of Chart lines and colors on chart

DMT TEMPELTON PECK STRATEGYIntroduction Templeton Peck Strategy Version .

Bring your A-game to the market in A-Team style with DMT Templeton Peck – you’ll love it when this plan comes together!

Using customized standard deviations between historic price action ranges and volume metrics, DMT Templeton Peck enables traders to never miss a change in trend.

In its default state, the DMT Templeton Peck Strategy displays key information, such as:

• Small trend line

• Large trend line

• Position entry prices

• Take profit levels

• Stop levels

• Buy and sell trend signals

In addition to providing core functionality for the indicator’s strategy signals, traders can use this data to enter or exit trades.

When price crosses both trend lines and consolidates there is a high probability that price will continue to move in the same direction. The most profitable results are achieved when trading in the direction of the current large time frame trend.

When small and large trend lines cross a trading signal is generated which can be used to automate trades. Please see the ‘TradingView Alerts’ section of this document for further details.

The Small & Large trend line’s display can be toggled, and their colors modified in the indicator’s style options as shown below.

Basic Strategy

In its simplest form, the strategy is to buy when the price crosses and consolidates above both trend lines and sell when the price crosses and consolidates below both trend lines.

Set amount of first entry to the inputs data.

You can add a commission fee.

Adjust initial capital for your needs.

How to Trade

Confident traders may choose to enter a long position at the point

#1 when the price passes above both trend lines and begins to consolidate.

However, the safer trade is to wait for the trend lines to cross at a point

#2 and then look for an entry in the direction of the local trend.

One price action begins to reverse to the downside the strategy reverses. Confident traders may choose to enter point

#3 when the price passes both trend lines and begins to consolidate once again under the previous price action structure that is now acting as resistance.

A sell signal is generated at the point

#4 which produced a small profit; however, a new short position could have been opened when the price retraced to resistance at a point

#5 and experienced a repeated number of strong rejections.

Do not worry if you miss a trade as there is often more than a single opportunity to enter – like at position #5 when price action retests the previous local price structure as resistance.

The indicator can be used on smaller time frames to scalp or find an entry after a larger time frame has signaled, however smaller time frames will also be “choppy” and should only be traded with a paper-tested strategy.

Traders should take profit on positions at resistance & support levels and look to have fully exited the trade by the time the price crosses back over both trend lines and/or loses a previously established price level.

Indicator Tuning

In its default state, the indicator is tuned for swing trades using 30 minute & 1 hour time frames, however, you are encouraged to experiment with the indicator options.

The input also allows you to set separately longs and shorts for a better view of the trend and to avoid hunts.

Large & Small Length options define how many historic candles are used for the calculation of the relevant trend line.

As a rule of thumb, larger time frames would use smaller values and smaller time frames would use larger values, ie. On a daily chart, a large and small length could be defined as 400 and 100 respectively.

Please be aware that there are limits to the amount of historical data for any intraday level based on your TradingView subscription level:

• Basic – 5000 bars/candles

• Pro & Pro+ - 10000 bars/candles

• Premium – 20000 bars/cables

TradingView Backtest

By utilizing TradingView backtest you can set a specific date for your analysis.

Villa Dinamic Pivot Supertrend StrategyThis strategy works better on AUD/USD in the 15 min timeframe. It uses the Pivot Supertrend to enter trades based on different filters such as:

- Simple EMA filter: that the 3 EMAs should be in order

- DEMA angle: you can choose the DEMA Angle threshold and the look back to check the angle to just trade trades with DEMA at a certain angle

- Simple DEMA filter: just check if close is above or below DEMA

- Take Every Supertrend Signal: this means to take every normal supertrend signal to not just wait for a pivot supertrend signal to enter a trade (specially on long pivot supertrend periods)

- Stop Loss at Supertrend: this means that the stop loss will be at the Normal Supertrend, if false the stop loss will be placed at the ATR level selected.

- 2 Steps Take Profit: this means if you want to close a percentage of position as soon as the normal supertrend crosses the entry price, you can select the % on the "2 Steps TP qty" input

- Stop Loss ATR Multiplier: if Stop Loss at Supertrend is off this will be the stoploss based on the atr

- Take Profit ATR Multiplier: if Stop Loss at Supertrend is off this will be the takeprofit based on the atr (you have to keep in mind that the ratio between this two will make the Risk to reward ratio of the take profit when the Stop Loss at Supertrend)

- Testing: to avoid overfitting, you can select date ranges for backtesting and forwardtesting and select which testing you wanna do

Loft Strategy V4This strategy is an advanced version of the Loft Strategy V1, I shared earlier. (Loft Strategy V1 consists of a kalman filter (by alexgrover ) and a "stop and reverse" line which is following and the kalman filter. If the price goes in the same direction as the position side, the "stop and reverse" line approaches the kalman filter as set on the "Approach Decrease Step" parameter.)

In addition to the previous version, it includes a martingale like deviation and multiple take-profit.

Here it is some parameters definitions of the strategy:

Kalman Filter: The higher this parameter, the faster and more aggressive the filter. Otherwise the filter goes very smoothly

Beginning Approach: First approximation as a percentage of stop-n-reverse line

Final Approach: Minimum approximation of stop-n-reverse line

Approach Decrease Step: If the price moves in the same direction as the strategy, the approach percentage is reduced by this parameter. Otherwise nothing do

Base Order Quantity: Initial capital of position

Max Safe Order Attempt: This parameter determines the maximum number of times the strategy will raise the bet after losing in a row.

Safe Order Deviation: if the last trade is loss, multiply the bet by this parameter (aka. martingale factor)

Profit Deviation: if last trade in loss, multiply the take-profit points

Max Order Quantity: Maximum capital allowed for a position

TP1, TP2, TP3 : Take profit spots in percentage

QT1, QT2, QT3: Amount of take-profit spots

Stop Loss: Maximum stop loss allowed for a trade

Long Entry, Short Entry: Only long side, only short side or both side

Safe Stop After TP2: If the price reaches the TP2 point, move the stop-loss point to the entry price.

Safe Stop After TP1: If the price reaches TP1, move the stop-loss point to the stop-n-reverse line.

SuperTrend Multiple Risk Management SystemThis is an improved SuperTrend strategy that makes use of multiple types of risk management options.

We have for example :

1. Take profit and stop loss levels based on support and resistence created with RSI and Pivot Lines(dynamic)

For example, if we have an oversold level and a pivot low , we can take that low point for support.(or resistence for short)

If instead we have an overbought level and a pivot high, we can take that high point for resistence.(orsupport for short)

2. Take profit and stop loss levels based on swing low and swing high points calculated with highest high and lowest low function(dynamic)

For example we take the lowest point in the last 100 candles. We calculate the distance from the current point to that one, and we apply this value as a take profit point. Same for stop loss

3. Take profit and stop loss levels based on % movements(fixed)

For example we have a tp or sl of 10%. If either of them make a movement of 10% from the entry point, they will get triggered.

4. Break even stop loss once the asset moves certain % in our direction.

For example we have a long breakeven of 5%. If the asset moves 5% in our direction, we move the stop loss on the entry point so if the trade pullback and crosses with this point it will exit from the trade.

Notes:

All the exits from the strategy are happening at the end of the candle close, since we are checking if inside the current candle we cross with either high or low of the candles parts the set prices from any of the above options.

At the same time we can combine multiple of them into one, and we can either exit based on which one was hit first, or use a quantity reduction of the trade and exit multiple times when we hit any of the levels.

This tool is for educational purpose only.

Its main purpose is to show the difference between having a risk management or without.

For example on this scenario of BTC USD 4h, I found out that the drawdawn was reduced by more than half when using different type of risk management, compared to not use one at all, while at the same time increasing the profits by a huge margin.

Trend Follower Strategy v2 [divonn1994]The Trend Follower Strategy that I made classifies red and green candles into tiny, small, and big sizes and will send buy or sell signals depending on if the candle is classified as "big" so you get into and out of a position when there is a big candle. Out during a big green candle to take profit. Out during a big red candle in case the market is turning down. It also won't enter a position unless there is positive EMA momentum.

For the chart there is a Buy and a Sell signal. Buy = 1, Sell = 0, and when the value crosses above or below 0.5 it will trigger a long position or close the long position. The graph isn't necessary to the strategy, but can help with visualizing the trade patterns in the past if you like.

This strategy works best so far with these coins at time of posting (March 4th, 2022):

KCSUSDT (621x profit), HTUSDT (45x profit), LUNAUSDT (45x profit), BNBBTC (1553x profit), ETHBTC (219x profit), KCSBTC (1222x profit), LUNABTC (83x profit), FTMBTC (52x profit).

It can work with other pairings, but I personally like these pairings best. I didn't test it with coins outside of the top 100 coins by market cap. Use it however you want.

Works best on 1 Day charts.

The strategy would rather be in the market than out. It gets out when it see's a red flag, but can immediately go back in in the next bar if the red flags are all gone. So it makes a lot of trades.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Update: This is the same strategy I uploaded before but I made the code Open for anyone to check it out and so it has a similar description as the previous version. Let me know what you think. I'd remove the old version if I could, but I guess it's site policy to not be able to remove scripts that have been uploaded.

Strategy - Cryptosystem NNFX wayFirst script done!

This is my version of the No-Nonsense Forex (NNFX) Strategy

This strategy shows you the entry and exit signal with a standard 1.5 x ATR for Stop Loss and 1 x ATR for Taking Profit. You can adjust the settings to your needs.

This strategy uses 5 indicators:

1. Average True Range for SL and TP placement, there is a nuance where you can add the 1XATR Rule;

2. SMA used to filter longs and shorts;

3. SSL Channel for 1st Confirmation;

4. DPO for 2nd Confirmation;

5. Waddah Attar Explosion as a volume indicator.

There is no exit indicator because I coded 2 trades (2x0.5). TP1 will be at 1xATR and TP2 will automatically trail behind with 1.5XATR. You can see the red trailing line on the charts.

Other exits can be: When SSL gives opposite signal or when price crosses and closes your baseline.

I used this system for 1D timeframe.

Hopefully this can be usefull for your tradingstyle.

Would be great if you guys leave a like.

Thanks!

Titan EMA Averaging Strategy - (DYOR) By MrCryptoTitan EMA Averaging Strategy (VIP Only) Enable Longs or Shorts only Works With Crypto + Forex with correct back tested settings This is not set and forget. This requires you to back test and have relevant Risk Management in place.

The Strategy: The script uses 3EMA with engulfing candle to enter a trade in either short or long direction.

You will need to test the settings and adjust them so there isn't too many - re-entries and make sure you take profit big enough to not trigger on same candle.

When setting alerts you can use once per bar however this may trigger multiple alerts if the candle is moving very fast so this is not recommended. So doing once per bar close will mean entry is confirmed as bar is closed. You will need to select this in drop down menu.

- Max Trade Limit.

- All in one Alert. - Basically add syntax for example- Long/Take Profit/Re-entry/Emergency Stop. Then add one alert and select "Alert() function calls Only" Change Alert name to custom. That's it.

-Built-in Strategy tester.

- Trade Filter - Multi-MA Filters. - MA", "EMA", "WMA", "HullMA", "VWMA", "RMA", "DEMA", "TEMA", VWAP

- ADX Filter based on Level.

Please note when running this strategy you can only trade longs only or shorts only for this setup to be potentially profitable. Also note that setting unrealistic profit targets will make a loss. So it is very important to back test everything.

This Script does not use any Security functions. All indicators which are used part of the strategy are obtained from Trading View indicator Library and have source code has been changed to make this into Strategy.

Please Do Your Own Research before using this.

Anymore information please DM me directly

CryptoGraph Multi Algo StrategyThis is a summary of how this strategy works.

CryptoGraph Multi Algo Strategy is the second profitable real-time trading strategy by the CryptoGraph team, that generates trade signal with exact entires, exits and risk management. The strategy is intended to work nearly every crypto coin pair, stock or index.

Principles behind the strategy

Entry:

Detection of trend direction with the use of an EMA . Default setting is a length of 550.

Detection of shorter term trend direction with the use of multiple Supertrend Indicators.

Detection of an even shorter term direction with the use of a crossover of the Stochastic RSI , below or above certain levels. This would be the final condition for an entry signal.

Exit:

Once an entry signal has fired, the script will look at the current ATR Value. In the script settings there will be an option to adjust the ATR factor. While ATR factor is equal to 1, it means it will use the default ATR value distance from the candle close. When ATR factor is for example 2, it will use two times the ATR distance from the candle close.

This is a simple representation of how this strategy works, in reality there are more underlying factors.

To find the best settings for the crypto coin pair or stock you want the strategy to trade with, simply switch up the EMA , ATR Profit Multiplier and ATR Stop Multiplier and experiment which settings would fit your style best.

What to look for when testing coins or stocks?

EMA, default exponential moving average is set to 550. When above the line, it will only look for longs, when below it will only look for shorts.

The Take Profit and Stop Loss are based on ATR multiplications, adjust these in the inputs interface and you will see the exits change.

Default parameters of the strategy

This is only an example of a profitable combination of all parameters. This would be the 30 minute timeframe Bybit chart on Bitcoin.

ATR take profit at x2, ATR stop loss at x4.1.

In this example we are using an initial capital of $1.000,- while each trade 100% of this capital is used and compounds over time. Meaning every profit or loss will be added to the next trade. Also there is a 0.05% commission used based on Bybit, since we expect most trades to market in and limit out.

Bollinger Bands %B - Belt Holds & Inner CandlesThis is a simple strategy that uses Bollinger Bands %B represented as a histogram combined with Candle Beltholds and Inside candles for entry signals, and combines this with "buy" and "sell" zones of the %B indicator, to buy and sell based on the zones you set.

How to use:

Long when in the green zone and an inside candle (which is highlighted in white) or a bullish belt hold (which is highlighted in yellow), and sell when inside a red zone and has an inside candle or a bearish belt hold (which is highlighted in purple) or the stop loss or take profit is hit.

Short when in the red zone and an inside candle (which is highlighted in white) or a bearish belt hold (which is highlighted in purple), and sell when inside a green zone and has an inside candle or a bullish belt hold (which is highlighted in yellow) or the stop loss or take profit is hit.

Stop loss / take profit selection:

Choose which performs best for you, ATR based uses the average true range, and % based is based on a set percent of loss or profit.

DI Crossing Daily Straregy HulkTradingSimple strategy based on crossing DI+ and DI- and Average True Range.

Long entry when DI+ crossover DI-

Short entry when DI+ crossunder DI-

Stop Loss and Take Profits based on Average True Range.

Default values are 1*ATR(14) for stop loss and 2*ATR(14) for Take Profit.

Risk reward 1 to 2 ratio.

Recommended default values, but you can change it if you want.

Recommended timeframe - 1D.

Script was tested on BTCUSDT pair and have a 2.4 profit factor.

DIVI Wunder StrategyAs it is known, divergence is a situation we encounter very often on graphs. Various divergencies may occur according to many indicators. MACD divergence, RSI divergence... In the strategy I use only positive divergence. What is positive divergence I will explain on MACD positive divergence A MACD positive divergence is a situation in which the MACD does not reach a new low, despite the fact that the price of the stock reached a new low. This is seen as a bullish trading signal—hence, the term “positive divergence.” So I thought of these divergencies and came up with a new strategy. Combining the divergencies with the VOLPIN strategy I wrote earlier, a great strategy has emerged. When the divergence signals are came from MACD,RSI,CCI,OBV,Chaikin Money Flow, VWmacd and Money Flow Index all these indicators I sent a buy signal until the 40 times completed. ThenI sent to sell signal when the price come to take profit level. In this strategy, you divide your principal into as many parts as you want. For example, let's say that you have 1000 dollars of money and you make purchases by dividing this money into 40 equal parts in the default settings of the indicator. $25 per purchase. After each purchase is made as 25 dollars, you can adjust your profit rate from the profit taking settings. When you look at the results of the strategy, your profit rate will be very high. I usually use this strategy in one hour periods. Of course you change it whatever you want. Also change all settings from panel to get more profit. Have fun :)