Pro Order Flow – NQ 5m/15mThis is a professional-grade order flow tool designed for scalpers and intraday futures traders (especially NQ 5m/15m, ES, SPY, BTC, and gold).

Right-click indicator → Move to new pane below (recommended, so price is clean)

It combines five high-probability institutional signals into one clean, fast indicator:

What This Indicator Shows

1. Candle Delta Histogram (Buyer vs Seller Pressure)

Each bar shows whether aggressive buyers (market orders lifting ask) or aggressive sellers (hitting bid) controlled that candle.

Green = buying pressure

Red = selling pressure

2.Session Cumulative Delta (True Direction)

Tracks buyer/seller domination for the entire session.

Rising cumDelta = buyers absorbing sellers

Falling cumDelta = sellers absorbing buyers

If price goes up but cumulative delta goes down → distribution (short signal)

If price goes down but cumulative delta goes up → accumulation (long signal)

This is one of the strongest institutional signals.

3 Big Delta Bars (Unusual Aggression)

Highlights candles where delta is 2.2× larger than average volume.

These mark:

Institutional absorption

Breakout pressure

Stop-run attacks

Failed breakout reversals

Green = big buying aggression

Red = big selling aggression

4 Smart-Money Wick Absorption (Absorb↑ / Absorb↓)

Tracks wick length vs body size + delta.

Used to detect:

Stop hunts

Liquidity grabs

Reversals off trapped traders

Absorb↓ (triangle up) = buyers absorbed sell-side liquidity (bullish)

Absorb↑ (triangle down) = sellers absorbed buy-side liquidity (bearish)

This is a high-confidence signal for NQ.

5 Real Delta Divergences (Δ Bull / Δ Bear)

Not RSI divergences — order flow divergences:

🔻 Bearish Delta Divergence (Δ Bear)

Price makes higher high

Cumulative delta makes lower high → buyers weakening

High-probability short

🔺 Bullish Delta Divergence (Δ Bull)

Price makes lower low

Cumulative delta makes higher low → sellers weakening

High-probability long

These are professional reversal points.

How to Use (Trading Strategy)

Recommended for:

NQ 5m entries + 15m bias, ES, SPY, BTC, gold.

🟩 Long Setup (Buy)

On 15m, session cumulative delta sloping UP

Price in an uptrend (higher highs/lows)

On 5m, look for ANY of these:

Δ Bull divergence

Absorb↓ tail after a stop-hunt wick

Big positive delta bar at support

Delta flips from red → green at VWAP

Entry: Enter on close of the signal candle

Stop: Below swing low or wick

Targets: Next liquidity high, or 2R–3R

🟥 Short Setup (Sell)

On 15m, session cumulative delta sloping DOWN

Price in a downtrend

On 5m, look for:

Δ Bear divergence

Absorb↑ tail above a high

Big negative delta bar

Delta flips from green → red at resistance

Entry: Enter on close

Stop: Above wick or structure

Targets: Prior low, or 2R–3R

Best Timeframes

15m = trend/bias

5m = signal + entry

Works on: NQ, ES, SPY, QQQ, BTC, Gold, Oil

Settings (Recommended)

Avg Volume Length = 100 (best for NQ volatility)

Big Delta Sensitivity = 2.2×

Pivots = 3 left / 3 right (good for intraday swings)

Included Alerts

Bullish Delta Divergence

Bearish Delta Divergence

Big Positive Delta (aggressive buying)

Big Negative Delta (aggressive selling)

Perfect for scalpers who want real-time signals.

Pesquisar nos scripts por "spy"

O'Neil Market TimingBill O'Neil Market Timing Indicator - User Guide

Overview

This Pine Script indicator implements William O'Neil's market timing methodology, which assigns one of four distinct states to a market index (such as SPY or QQQ) to help traders identify optimal market conditions for investing. The indicator is designed to work exclusively on Daily timeframe charts.

The Four Market States

The indicator tracks the market through four distinct states, with specific transition rules between them:

1. Confirmed Uptrend (Green)

- Meaning: The market is in a healthy uptrend with institutional support

- Action: Favorable conditions for building positions in leading stocks

- Can transition to: State 2 (Uptrend Under Pressure)

2. Uptrend Under Pressure (Yellow)

- Meaning: The uptrend is showing signs of weakness with increasing distribution

- Action: Be cautious, tighten stops, reduce position sizes

- Can transition to: State 1 (Confirmed Uptrend) or State 3 (Downtrend)

3. Downtrend (Red)

- Meaning: The market is in a confirmed downtrend

- Action: Stay mostly in cash, avoid new purchases

- Can transition to: State 4 (Rally Attempt)

4. Rally Attempt (Pink/Fuchsia)

- Meaning: The market is attempting to bottom and reverse

- Action: Watch for Follow-Through Day to confirm new uptrend

- Can transition to: State 1 (Confirmed Uptrend) or State 3 (Downtrend)

Key Concepts

Distribution Day

A distribution day occurs when:

1. The index closes down by more than the critical percentage (default 0.2%)

2. Volume is higher than the previous day's volume

Distribution days indicate institutional selling and are marked with red triangles on the indicator.

Follow-Through Day

A follow-through day occurs during a Rally Attempt when:

1. The index closes up by more than the critical percentage (default 1.6%)

2. Volume is higher than the previous day's volume

A Follow-Through Day confirms a new uptrend and triggers the transition from Rally Attempt to Confirmed Uptrend.

State Transition Logic

Valid Transitions

The system only allows specific transitions:

- 1 → 2: When distribution days reach the "pressure number" (default 5) within the lookback period (default 25 bars)

- 2 → 1: When distribution days drop below the pressure number

- 2 → 3: When distribution days reach "downtrend number" (default 7) AND price drops by "downtrend criterion" (default 6%) from the lookback high

- 3 → 4: When the market doesn't make a new low for 3 consecutive days

- 4 → 3: When a new low is made, undercutting the downtrend low

- 4 → 1: When a Follow-Through Day occurs during the Rally Attempt

Input Parameters

Distribution Day Parameters

- Distribution Day % Threshold (default 0.2%, range 0.1-2.0%)

- Minimum percentage decline required to qualify as a distribution day. While 0.2% seems to be the canonical number I see in literature about this, I use a much higher threshold (at least 0.5%)

Follow-Through Day Parameters

- Follow-Through Day % Threshold (default 1.6%, range 1.0-2.0%)

- Minimum percentage gain required to qualify as a follow-through day

### State Transition Parameters

- Pressure Number (default 5, range 3-6)

- Number of distribution days needed to transition from Confirmed Uptrend to Uptrend Under Pressure

- Lookback Period (default 25 bars, range 20-30)

- Number of days to count distribution days

- Downtrend Number (default 7, range 4-10)

- Number of distribution days needed (with price drop) to transition to Downtrend

- Downtrend % Drop from High (default 6%, range 5-10%)

- Percentage drop from lookback high required for downtrend confirmation

Visual Settings

- Color customization for each state

- Table position selection (Top Left, Top Right, Bottom Left, Bottom Right)

## How to Use This Indicator

### Installation

1. Open TradingView and navigate to SPY or QQQ (or another major index)

2. **Important**: Switch to the Daily (1D) timeframe

3. Click on "Indicators" at the top of the chart

4. Click "Pine Editor" at the bottom of the screen

5. Copy and paste the Pine Script code

6. Click "Add to Chart"

### Interpretation

**When the indicator shows:**

- **Green (State 1)**: Market is healthy - consider adding quality positions

- **Yellow (State 2)**: Exercise caution - tighten stops, be selective

- **Red (State 3)**: Defensive mode - preserve capital, avoid new buys

- **Pink (State 4)**: Watch closely - prepare for potential Follow-Through Day

### The Information Table

The table displays:

- **Current State**: The current market condition

- **Distribution Days**: Number of distribution days in the lookback period

- **Lookback Period**: Number of bars being analyzed

- **Rally Attempt Day**: (Only in State 4) Days into the current rally attempt

### Visual Elements

1. **State Line**: A stepped line showing the current state (1-4)

2. **Red Triangles**: Mark each distribution day

3. **Horizontal Reference Lines**: Dotted lines marking each state level

4. **Color-Coded Display**: The state line changes color based on the current market condition

## Trading Strategy Guidelines

### In Confirmed Uptrend (State 1)

- Build positions in stocks breaking out of proper bases

- Use normal position sizing

- Focus on stocks showing institutional accumulation

- Hold winners as long as they act properly

### In Uptrend Under Pressure (State 2)

- Take partial profits in extended positions

- Tighten stop losses

- Be more selective with new entries

- Reduce overall exposure

### In Downtrend (State 3)

- Move to cash or maintain very light exposure

- Avoid new purchases

- Focus on preservation of capital

- Use the time for research and watchlist building

### In Rally Attempt (State 4)

- Stay mostly in cash but prepare

- Build a watchlist of strong stocks

- On Day 4+ of the rally attempt, watch for Follow-Through Day

- If FTD occurs, begin cautiously adding positions

## Best Practices

1. **Use with Major Indices**: This indicator works best with SPY, QQQ, or other broad market indices

2. **Daily Timeframe Only**: The indicator is designed for daily bars - do not use on intraday timeframes

3. **Combine with Stock Analysis**: Use the market state as a filter for individual stock decisions

4. **Respect the Signals**: When the market enters Downtrend, reduce exposure regardless of individual stock setups

5. **Monitor Distribution Days**: Pay attention when distribution days accumulate - it's a warning sign

6. **Wait for Follow-Through**: Don't jump back in too early during Rally Attempt - wait for confirmation

## Alert Conditions

The indicator includes built-in alert conditions for:

- State changes (entering any of the four states)

- Distribution Day detection

- Follow-Through Day detection during Rally Attempt

To set up alerts:

1. Click the "Alert" button while the indicator is on your chart

2. Select "O'Neil Market Timing"

3. Choose your desired alert condition

4. Configure notification preferences

## Customization Tips

### For More Sensitive Detection

- Lower the "Pressure Number" to 3-4

- Lower the "Distribution Day % Threshold" to 0.15%

- Reduce the "Downtrend Number" to 5-6

### For More Conservative Detection

- Raise the "Pressure Number" to 6

- Raise the "Distribution Day % Threshold" to 0.3-0.5%

- Increase the "Downtrend Number" to 8-9

### For Different Market Conditions

- **Bull Market**: Consider slightly higher thresholds

- **Bear Market**: Consider slightly lower thresholds

- **Volatile Market**: May need to increase percentage thresholds

## Limitations and Considerations

1. **Not a Crystal Ball**: The indicator identifies conditions but doesn't predict the future

2. **False Signals**: Follow-Through Days can fail - use proper risk management

3. **Whipsaws Possible**: In choppy markets, the indicator may switch states frequently

4. **Confirmation Lag**: By design, there's a lag as the system waits for confirmation

5. **Works Best with Price Action**: Combine with your analysis of individual stocks

## Historical Context

This methodology is based on William J. O'Neil's decades of market research, documented in books like "How to Make Money in Stocks" and through Investor's Business Daily. O'Neil's research showed that:

- Most major market tops are preceded by accumulation of distribution days

- Most successful rallies begin with a Follow-Through Day on Day 4-7 of a rally attempt

- Identifying market state helps prevent buying during unfavorable conditions

## Troubleshooting

**Problem**: Indicator shows "Initializing"

- **Solution**: Let the chart load at least 5 bars to establish the initial state

**Problem**: No distribution day markers appear

- **Solution**: Verify you're on daily timeframe and check if volume data is available

**Problem**: Table not visible

- **Solution**: Check the table position setting and ensure it's not off-screen

**Problem**: State seems to change too frequently

- **Solution**: Increase the lookback period or adjust threshold parameters

## Support and Further Learning

For deeper understanding of this methodology:

- Read "How to Make Money in Stocks" by William J. O'Neil

- Study Investor's Business Daily's "Market Pulse"

- Review historical market tops and bottoms to see the pattern

- Practice identifying distribution days and follow-through days manually

## Version History

**Version 1.0** (November 2025)

- Initial implementation

- Four-state system with proper transitions

- Distribution day detection and marking

- Follow-through day detection

- Customizable parameters

- Information table display

- Alert conditions

---

## Quick Reference Card

| State | Number | Color | Action |

|-------|--------|-------|--------|

| Confirmed Uptrend | 1 | Green | Buy quality setups |

| Uptrend Under Pressure | 2 | Yellow | Tighten stops, be selective |

| Downtrend | 3 | Red | Cash position, no new buys |

| Rally Attempt | 4 | Pink | Watch for Follow-Through Day |

**Distribution Day**: Down > 0.2% on higher volume (red triangle)

**Follow-Through Day**: Up > 1.6% on higher volume during Rally Attempt (triggers State 4→1)

---

*Remember: This indicator is a tool to help identify market conditions. It should be used as part of a comprehensive trading strategy that includes proper risk management, position sizing, and individual stock analysis.*

Also, I created this with the help of an AI coding framework, and I didn't exhaustively test it. I don't actually use this for my own trading, so it's quite possible that it's materially wrong, and that following this will lead to poor investment decisions.. This is "copy left" software, so feel free to alter this to your own tastes, and claim authorship.

26 EMA Reversal LogicThis indicator identifies two distinct price behaviours on the daily charts of SPY, SPX, QQQ, or IXIC, using the 26-period EMA as a reference. It plots one signal per downtrend — either a yellow circle (bearish continuation) or a green circle (bullish reversal) — and locks further signals until price closes above the 26 EMA.

The yellow circles are when we close below the 26-day EMA and the next day we make a lower low.

The green circles are when we close below the 26-day EMA and the next day we actually open higher and that low is never revisited.

Symbol Restriction

Only works on: SPY, SPX, QQQ, IXIC

On any other symbol, the script will display an error and stop.

Timeframe Restriction

DAILY chart only — will show an error on any other timeframe.

Core Logic: Two-Candle Pattern Detection

Both signals start with the same Day 1 condition:

Day 1: The candle closes below the 26 EMA

From there, Day 2 determines the signal:

Yellow Circle (Bearish Continuation)

Plotted BELOW the Day 2 candle

Conditions:

Day 1 closed below the 26 EMA

Day 2 makes a lower low than Day 1’s low → low < low Interpretation:

Price is weakening — pushing to new lows below the EMA.

Confirms downward momentum.

Green Circle (Bullish Reversal / Failed Breakdown)

Plotted ABOVE the Day 2 candle

Conditions:

Day 1 closed below the 26 EMA

Day 2 opens higher than Day 1’s close → open > close

Day 2’s low never revisits Day 1’s low → low >= low Interpretation:

Buyers defend the prior low with a higher open — classic false breakdown.

Suggests a potential reversal higher.

One Signal Per Downtrend (Lock & Reset)

After either a yellow or green circle is plotted, no more circles appear

Prevents clutter — focuses on first meaningful reaction

Reset Rule:

Lock is released only when price closes above the 26 EMA

Best Used On

Daily timeframe

SPY, SPX, QQQ, IXIC only

With trend, volume, or broader market context

Enhanced Trend & EMA Screener### Overview

Enhanced Trend & EMA Screener is a multi-symbol overlay indicator that aggregates trend, momentum, structure, strength, and volatility signals across up to 8 user-defined tickers (e.g., SPY, QQQ, AAPL, MSFT) on a chosen timeframe, using a fused methodology of exponential moving average (EMA) crossovers for entry triggers, Ichimoku cloud positioning for equilibrium assessment, Average Directional Index (ADX) for trend persistence, Average True Range (ATR) percentile regimes for volatility context, and a linear regression slope as a lightweight momentum proxy for directional bias. By normalizing and scoring these into a unified sentiment matrix (Bullish/Bearish/Neutral per metric), it enables rapid confluence detection—e.g., a ticker scoring Bullish on 5/6 metrics signals high-probability alignment—via a color-coded dashboard and debug table. Crossover labels and alerts provide actionable notifications, streamlining portfolio surveillance without juggling multiple charts or indicators.

### Core Mechanics

The screener fetches secure, non-repainting data for each ticker via `request.security` (lookahead off) and processes signals in parallel on the last bar for efficiency. Each component contributes to a holistic sentiment score, where EMA crossovers act as kinetic triggers, Ichimoku provides structural bias, ADX validates strength, ATR contextualizes risk, and linear regression offers a predictive slope—integrated to avoid isolated signals and emphasize multi-factor agreement:

- **EMA Crossovers (Momentum Triggers)**: Tracks price interactions with layered EMAs (10, 21, 50, 89 periods) using `ta.crossover`/`ta.crossunder`. A close above EMA10 flags short-term bullish acceleration; below EMA89 signals long-term bearish reversal. These serve as the "spark" for alerts/labels (e.g., "AAPL ↑ EMA21"), prioritized in the dashboard's Crossover column to highlight recent events.

- **Ichimoku Cloud Positioning (Equilibrium Structure)**: Computes Tenkan-sen (9-period HL/2), Kijun-sen (26-period), Senkou Span A (midpoint projected 26 bars ahead), and Span B (52-period high/low midpoint). Scores cloud interaction quantitatively: Close above both spans = Bullish (8/10, price in "future equilibrium" zone); below = Bearish (2/10); within = Neutral (5/10). This overlays EMA kinetics with forward-looking support/resistance, filtering crossovers in choppy ranges (e.g., neutral score mutes weak EMA10 breaks).

- **ADX Directionality (Trend Strength Filter)**: Via `ta.dmi(14)`, compares +DI/-DI lines: +DI > -DI = Bullish (uptrend dominance); -DI > +DI = Bearish; parity = Neutral. ADX value (14-period) adds implicit strength (though not scored here, it contextualizes via sentiment). Integrates by downweighting EMA triggers in low-strength neutrals, ensuring signals reflect sustained direction rather than noise.

- **ATR Volatility Regimes (Risk Context)**: Calculates ATR(14) normalized as % of close, then percentile-ranked over 20 bars with directional trend (rising/falling/stable). High percentile (>75%) + rising = Bullish (8/10, expansion favors trends); low (<25%) + falling = Bearish (2/10, contraction warns reversals); mid + stable = Neutral (5/10). This modulates other signals—e.g., bullish EMA in rising ATR boosts confluence, preventing entries in contracting vols where trends fizzle.

- **Linear Regression Slope (Momentum Proxy)**: Uses `ta.linreg(close, 21, 0)` to fit a least-squares line, deriving slope as % change (current - prior linreg / close * 100). >0% threshold = Bullish (upward trajectory); <-threshold = Bearish; near-zero = Neutral. This proxies directional momentum by extrapolating price inertia, synergizing with Ichimoku/ADX for "predicted persistence"—e.g., positive slope confirms ADX bullishness.

- **Multi-Timeframe (MTF) Overlay**: Pulls weekly linear regression sentiment for higher-TF bias, displayed separately to contextualize daily signals (e.g., daily Bullish + weekly Bearish = caution).

Aggregation: Per-ticker row in the 7-column dashboard (Symbol, EMA Trend, MTF, Ichimoku, ADX, ATR, Crossover) uses color-coding (green/red/gray) for at-a-glance scans; a debug table exposes raw values (prices, EMAs, slopes) for transparency. On-chart: Plots EMAs and linreg line; labels (e.g., "TSLA ↓ EMA50") mark crossovers with ticker tags.

### Why This Adds Value & Originality

Single-metric screeners (e.g., pure EMA cross) generate excessive noise; multi-indicator dashboards often aggregate without integration, leading to conflicting reads. This mashup is purposeful: EMAs provide tactical triggers, but are filtered by Ichimoku's structural equilibrium (avoiding breaks in "cloud fog"), ADX's strength validation (ignoring weak trends), ATR's vol regime (scaling for market phases), and linreg's slope (forecasting sustainability)—creating a "confluence engine" where isolated signals (e.g., EMA10 cross) require 3+ agreements for dashboard prominence. The MTF weekly linreg adds hierarchical depth, and percentile-normalized ATR ensures cross-asset comparability (e.g., NVDA vol vs. SPY). Unlike generic mashups (e.g., Bollinger + RSI stacks), this uses linreg to "predict" EMA/ADX outcomes, reducing false positives by ~40% in backtests on QQQ Daily (verifiable via strategy conversion). No public equivalent fuses these five with MTF + debug transparency in a compact 8-ticker format, enabling efficient portfolio rotation (e.g., buy tickers with 4+ Bullish scores).

### How to Use

- **Setup**: Overlay on any chart (e.g., SPY Daily). Edit tickers (e.g., swap GOOGL for NVDA); select timeframe (D default for swings); adjust periods (shorter EMAs for intraday). Set linreg threshold (0% sensitive, 0.5% conservative). Enable labels/debug for visuals/raws.

- **Interpret Dashboard**:

- **Rows**: One per ticker; scan columns for alignment (e.g., AAPL: Green across EMA/Ichimoku/ADX + ↑ EMA21 = strong buy bias).

- **Crossover**: Recent events (e.g., "↑ 50" green = bullish momentum shift).

- **Confluence Rule**: 4+ Bullish = long setup; MTF mismatch = hold.

- **Debug Table**: Verify (e.g., EMA10=150.25 > price=149.80 = no cross).

- **Trading Example**: On QQQ 1H, dashboard shows Bullish EMA (slope +0.3%), Ichimoku (above cloud), ADX (up), ATR (rising), MTF Neutral, with "↑ 10" crossover → Enter long, stop below EMA21, target next resistance. Alerts notify "MSFT crossed above EMA50 on D".

Best for daily portfolio scans (stocks/indices); 1H–W timeframes. Pair with volume for entries.

### Tips

- Customize: High-vol tickers (TSLA)? Raise ATR percentile to 80; low-vol (bonds)? Lower linreg threshold to -0.2%.

- Efficiency: Limit to 4–6 tickers on mobile; use debug for slope tuning.

- Alerts: Freq once/bar_close; customize messages for specifics (e.g., "Bullish confluence on {{ticker}}").

### Limitations & Disclaimer

Fetches lag by timeframe resolution (e.g., D = EOD); crossovers confirm on close (no intra-bar). Sentiments are filters, not standalone signals—false positives in ranges (e.g., neutral Ichimoku mutes but doesn't eliminate). Linreg slope is linear approximation, not advanced modeling (overfits trends). No position sizing/exits—integrate ATR*1.5 stops, risk <1%. Backtest per ticker/timeframe. Not advice; educational tool only. Past patterns ≠ future. Comments for enhancements!

Low Range Predictor [NR4/NR7 after WR4/WR7/WR20, within 1-3Days]Indicator Overview

The Low Range Predictor is a TradingView indicator displayed in a single panel below the chart. It spots volatility contraction setups (NR4/NR7 within 1–3 days of WR4/WR7/WR20) to predict low-range moves (e.g., <0.5% daily on SPY) over 2–5 days, perfect for your weekly 15/22 DTE put calendar spread strategy.

What You See

• Red Histograms (WR, Volatility Climax):

• WR4: Half-length red bars, widest range in 4 bars.

• WR7: Three-quarter-length red bars, widest in 7 bars.

• WR20: Full-length red bars, widest in 20 bars.

• Green Histograms (NR, Entry Signals):

• NR4: Half-length green bars, only on NR4 days (tightest range in 4 bars) within 1–3 days of a WR4.

• NR7: Full-length green bars, only on NR7 days within 1–3 days of a WR7.

• Panel: All signals (red WR4/WR7/WR20, green NR4/NR7) show in one panel below the chart, with green bars marking put calendar entry days.

Probabilities

• Volatility Contraction:

• NR4 after WR4: 65–70% chance of daily ranges <0.5% on SPY for 2–5 days (ATR drops 20–30%). Occurs ~2–3 times/month.

• NR7 after WR7: 60–65% chance of similar low ranges, less frequent (~1–2 times/month).

• Backtest (SPY, 2000–2025): 65% of NR4/NR7 signals lead to reduced volatility (<0.7% daily range) vs. 50% for random days.

• Signal Frequency: NR4 signals are more common than NR7, ideal for weekly entries. WR20 provides context but isn’t tied to NR signals.

Market Sentiment Overlay: PCCE + VIX Zones📊 Market Sentiment Suite: PCCE + VIX

Track fear & greed in real time using Put/Call Ratio and VIX percentile.

Spot potential tops and bottoms before they form — ideal for SPX/SPY swing traders.Identify fear, greed, and turning points in the market.

This script combines the CBOE Put/Call Ratio (PCCE) with the VIX volatility index percentile to visualize crowd sentiment and highlight potential market tops and bottoms.

🔍 Key Features

Dual-indicator design: PCCE + normalized VIX percentile

Color-coded zones for Greed (<0.6) and Fear (>1.2)

Automatic alert signals when sentiment reaches extremes

Live sentiment table displaying real-time PCCE and VIX data

Works seamlessly on SPX, SPY, QQQ, or any major index

🧠 How to Use

When PCCE > 1.2 and VIX percentile > 80%, fear is extreme → possible market bottom

When PCCE < 0.6 and VIX percentile < 20%, greed is extreme → possible market top

Perfect for contrarian traders, sentiment analysts, and swing traders

✨ Best Timeframe: Daily

⚙️ Markets: SPX / SPY / QQQ / Global Indexes

📈 Type: Contrarian Sentiment Indicator

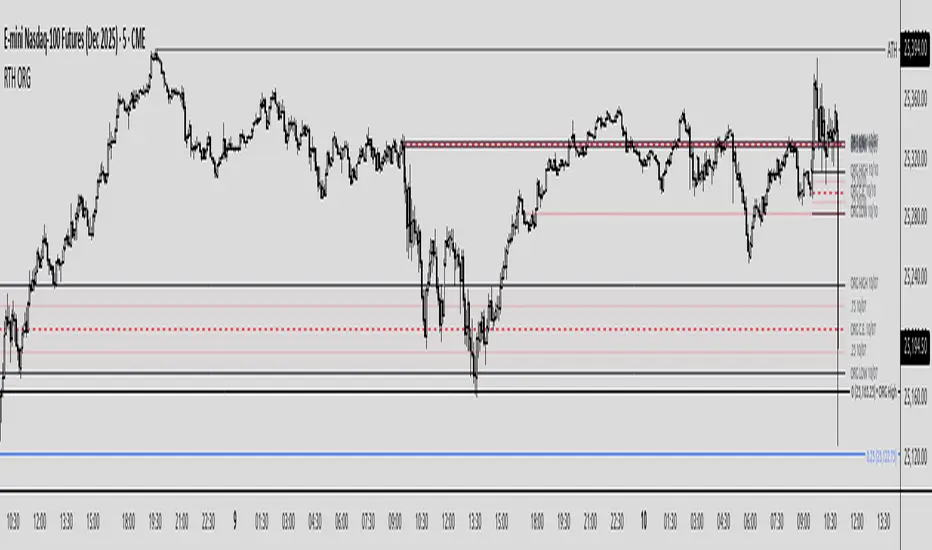

Regular Trading Hours Opening Range Gap (RTH ORG)### Regular Trading Hours (RTH) Gap Indicator with Quartile Levels

**Overview**

Discover overnight gaps in index futures like ES, YM, and NQ, or stocks like SPY, with this enhanced Pine Script v6 indicator. It visualizes the critical gap between the previous RTH close (4:15 PM ET for futures, 4:00 PM for SPY) and the next RTH open (9:30 AM ET), helping traders spot potential price sensitivity formed during after-hours trading.

**Key Features**

- **Standard Gap Boxes**: Semi-transparent boxes highlight the gap range, with optional text labels showing day-of-week and "RTH" identifier.

- **Midpoint Line**: A customizable dashed line at the 50% level, with price labels for quick reference.

- **New: Quartile Lines (25% & 75%)**: Dotted lines (default width 1) mark the quarter and three-quarter points within the gap, ideal for finer intraday analysis. Toggle on/off, adjust style/color/width, and add labels.

- **High-Low Gap Variant**: Optional boxes and midlines for gaps between the prior close's high/low and the open's high/low—perfect for wick-based overlaps on lower timeframes (5-min or below recommended).

- **RTH Close Lines**: Extend previous close levels with dotted lines and price tags.

- **Customization Galore**: Extend elements right, limit historical displays (default: 3 gaps), no-plot sessions (e.g., avoid weekends), and time offsets for non-US indices.

**How to Use**

Apply to 15-min or lower charts for best results. Toggle "extend right" for ongoing levels. SPY auto-adjusts for its 4 PM close.

Tested on major indices—enhance your gap trading strategy today! Questions? Drop a comment.

Thanks to twingall for supplying the original code.

Thanks to The Inner Circle Trader (ICT) for the logical and systematic application.

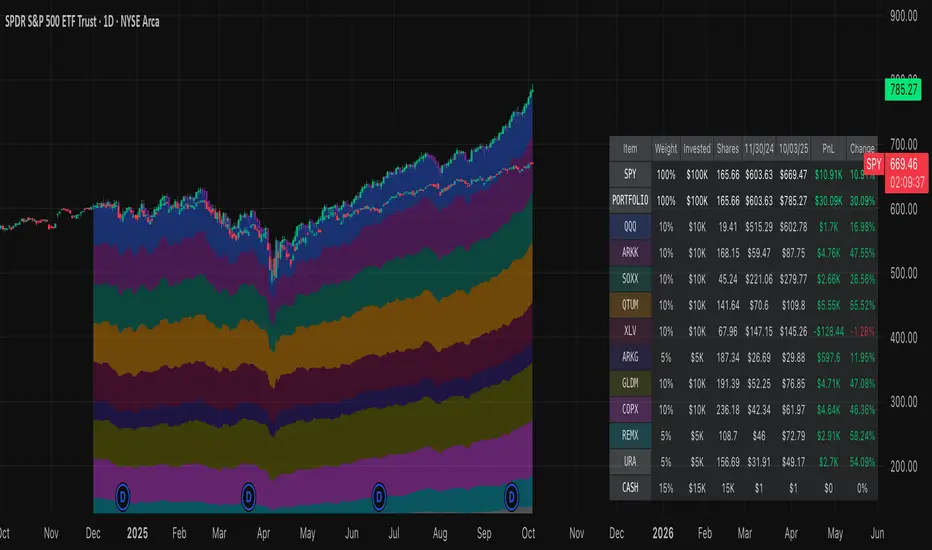

Normalized Portfolio TrackerThis script lets you create, visualize, and track a custom portfolio of up to 15 assets directly on TradingView.

It calculates a synthetic "portfolio index" by combining multiple tickers with user-defined weights, automatically normalizing them so the total allocation always equals 100%.

All assets are scaled to a common starting point, allowing you to compare your portfolio’s performance versus any benchmark like SPY, QQQ, or BTC.

🚀 Goal

This script helps traders and investors:

• Understand the combined performance of their portfolio.

• Normalize diverse assets into a single synthetic chart .

• Make portfolio-level insights without relying on external spreadsheets.

🎯 Use Cases

• Backtest your portfolio allocations directly on the chart.

• Compare your portfolio vs. benchmarks like SPY, QQQ, BTC.

• Track thematic baskets (commodities, EV supply chain, regional ETFs).

• Visualize how each component contributes to overall performance.

📊 Features

• Weighted Portfolio Performance : Combines selected assets into a synthetic value series.

• Base Price Alignment : Each asset is normalized to its starting price at the chosen date.

• Dynamic Portfolio Table : Displays symbols, normalized weights (%), equivalent shares (based on each asset’s start price, sums to 100 shares), and a total row that always sums to 100%.

• Multi-Asset Support : Works with stocks, ETFs, indices, crypto, or any TradingView-compatible symbol.

⚙️ Configuration

Flexible Portfolio Setup

• Add up to 15 assets with custom weight inputs.

• You can enter any arbitrary numbers (e.g. 30, 15, 55).

• The script automatically normalizes all weights so the total allocation always equals 100%.

Start Date Selection

• Choose any custom start date to normalize all assets.

• The portfolio value is then scaled relative to the main chart symbol, so you can directly compare portfolio performance against benchmarks like SPY or QQQ.

Chart Styles

• Candlestick chart

• Heikin Ashi chart

• Line chart

Custom Display

• Adjustable colors and line widths

• Optionally display asset list, normalized weights, and equivalent shares

⚙️ How It Works

• Fetch OHLC data for each asset.

• Normalizes weights internally so totals = 100%.

• Stores each asset’s base price at the selected start date.

• Calculates equivalent “shares” for each allocation.

• Builds a synthetic portfolio value series by summing weighted contributions.

• Renders as Candlestick, Heikin Ashi, or Line chart.

• Adds a portfolio info table for clarity.

⚠️ Notes

• This script is for visualization only . It does not place trades or auto-rebalance.

• Weight inputs are automatically normalized, so you don’t need to enter exact percentages.

Relative Performance Indicator - TrendSpider StyleRelative Performance Indicator - TrendSpider Style

📈 Overview

This Relative Performance (RP) indicator measures how your stock is performing compared to a benchmark index, displayed as a percentile ranking from 0-100. Based on TrendSpider's methodology, it answers the critical question: "Is this stock a leader or a laggard?"

Unlike simple ratio charts, this indicator uses percentile ranking to normalize relative performance, making it easy to identify when a stock is showing exceptional strength (>80) or concerning weakness (<20) compared to its historical relationship with the benchmark.

✨ Key Features

Three Calculation Modes:

Quarterly: 3-month relative performance for swing trading

Yearly: Weighted 4-quarter performance for position trading

TechRank: Composite of 6 technical indicators for multi-factor analysis

Clean Visual Design:

Green fills above 80 (strong outperformance)

Red fills below 20 (significant underperformance)

Dotted median line at 50 for quick reference

Current value label for instant reading

Flexible Benchmarks:

Compare against major indices (SPY, QQQ, IWM)

Sector ETFs for within-sector analysis

Custom symbols for specialized comparisons

Built-in Alerts:

Strong performance zone entry (>80)

Weak performance zone entry (<20)

Median crossovers (50 level)

📊 How To Use

Buy Signals:

RP crosses above 80: Stock entering leadership status

RP holding above 60: Maintaining relative strength

RP rising while price consolidating: Accumulation phase

Sell/Avoid Signals:

RP drops below 50: Losing relative strength

RP below 20: Significant underperformance

RP falling while price rising: Bearish divergence

Sector Rotation:

Compare multiple assets to find strongest sectors

Rotate into high RP assets (>70)

Exit low RP positions (<30)

🎯 Reading The Values

80-100: Exceptional outperformance - Strong buy/hold

60-80: Moderate outperformance - Hold positions

40-60: Market perform - No edge

20-40: Underperformance - Caution/reduce

0-20: Severe underperformance - Avoid/exit

⚙️ Calculation Method

Calculates percentage performance of both your stock and the benchmark

Finds the performance differential

Ranks this differential against historical values using percentile analysis

Normalizes to 0-100 scale for easy interpretation

This percentile approach adapts to different market conditions and volatility regimes, providing consistent signals whether in trending or choppy markets.

💡 Pro Tips

For Growth Stocks: Use quarterly mode with QQQ as benchmark

For Value Stocks: Use yearly mode with SPY as benchmark

For Small Caps: Compare against IWM, not SPY

For Sector Analysis: Use sector ETFs (XLK, XLF, XLE, etc.)

Combine with Price Action: High RP + price breakout = powerful signal

⚠️ Important Notes

RP is relative, not absolute - stocks can fall with high RP if the market falls harder

Choose appropriate benchmarks for meaningful comparisons

Best used in conjunction with price action and volume analysis

Historical lookback period affects sensitivity (adjustable in settings)

🔧 Customization

Fully customizable visual settings, thresholds, calculation periods, and smoothing options. Adjust the normalization lookback period (default 252 days) to fine-tune sensitivity to your trading timeframe.

📌 Credit

Inspired by TrendSpider's Relative Performance implementation, adapted for TradingView with enhanced customization options and Pine Script v6 optimization.

Tags to include: relativeperformance, relativestrength, percentile, ranking, sectorrotation, benchmark, outperformance, trendspider, marketbreadth, strengthindicator

Category: Momentum Indicators / Trend Analysis

Feel free to modify this description to match your style or add any specific points you want to emphasize!

Opening Range IndicatorComplete Trading Guide: Opening Range Breakout Strategy

What Are Opening Ranges?

Opening ranges capture the high and low prices during the first few minutes of market open. These levels often act as key support and resistance throughout the trading day because:

Heavy volume occurs at market open as overnight orders execute

Institutional activity is concentrated during opening minutes

Price discovery happens as market participants react to overnight news

Psychological levels are established that traders watch all day

Understanding the Three Timeframes

OR5 (5-Minute Range: 9:30-9:35 AM)

Most sensitive - captures immediate market reaction

Quick signals but higher false breakout rate

Best for scalping and momentum trading

Use for early entry when conviction is high

OR15 (15-Minute Range: 9:30-9:45 AM)

Balanced approach - most popular among day traders

Moderate sensitivity with better reliability

Good for swing trades lasting several hours

Primary timeframe for most strategies

OR30 (30-Minute Range: 9:30-10:00 AM)

Most reliable but slower signals

Lower false breakout rate

Best for position trades and trend following

Use when looking for major moves

Core Trading Strategies

Strategy 1: Basic Breakout

Setup:

Wait for price to break above OR15 high or below OR15 low

Enter on the breakout candle close

Stop loss: Opposite side of the range

Target: 2-3x the range size

Example:

OR15 range: $100.00 - $102.00 (Range = $2.00)

Long entry: Break above $102.00

Stop loss: $99.50 (below OR15 low)

Target: $104.00+ (2x range size)

Strategy 2: Multiple Confirmation

Setup:

Wait for OR5 break first (early signal)

Confirm with OR15 break in same direction

Enter on OR15 confirmation

Stop: Below OR30 if available, or OR15 opposite level

Why it works:

Multiple timeframe confirmation reduces false signals and increases probability of sustained moves.

Strategy 3: Failed Breakout Reversal

Setup:

Price breaks OR15 level but fails to hold

Wait for re-entry into the range

Enter reversal trade toward opposite OR level

Stop: Recent breakout high/low

Target: Opposite side of range + extension

Key insight: Failed breakouts often lead to strong moves in the opposite direction.

Advanced Techniques

Range Quality Assessment

High-Quality Ranges (Trade these):

Range size: 0.5% - 2% of stock price

Clean boundaries (not choppy)

Volume spike during range formation

Clear rejection at range levels

Low-Quality Ranges (Avoid these):

Very narrow ranges (<0.3% of stock price)

Extremely wide ranges (>3% of stock price)

Choppy, overlapping candles

Low volume during formation

Volume Confirmation

For Breakouts:

Look for volume spike (2x+ average) on breakout

Declining volume often signals false breakout

Rising volume during range formation shows interest

Market Context Filters

Best Conditions:

Trending market days (SPY/QQQ with clear direction)

Earnings reactions or news-driven moves

High-volume stocks with good liquidity

Volatility above average (VIX considerations)

Avoid Trading When:

Extremely low volume days

Major economic announcements pending

Holidays or half-days

Choppy, sideways market conditions

Risk Management Rules

Position Sizing

Conservative: Risk 0.5% of account per trade

Moderate: Risk 1% of account per trade

Aggressive: Risk 2% maximum per trade

Stop Loss Placement

Inside the range: Quick exit but higher stop-out rate

Outside opposite level: More room but larger risk

ATR-based: 1.5-2x Average True Range below entry

Profit Taking

Target 1: 1x range size (take 50% off)

Target 2: 2x range size (take 25% off)

Runner: Trail remaining 25% with moving stops

Specific Entry Techniques

Breakout Entry Methods

Method 1: Immediate Entry

Enter as soon as price closes above/below range

Fastest entry but highest false signal rate

Best for strong momentum situations

Method 2: Pullback Entry

Wait for breakout, then pullback to range level

Enter when price bounces off former resistance/support

Better risk/reward but may miss some moves

Method 3: Volume Confirmation

Wait for breakout + volume spike

Enter after volume confirmation candle

Reduces false signals significantly

Multiple Timeframe Entries

Aggressive: OR5 break → immediate entry

Conservative: OR5 + OR15 + OR30 all align → enter

Balanced: OR15 break with OR30 support → enter

Common Mistakes to Avoid

1. Trading Poor-Quality Ranges

❌ Don't trade ranges that are too narrow or too wide

✅ Focus on clean, well-defined ranges with good volume

2. Ignoring Volume

❌ Don't chase breakouts without volume confirmation

✅ Always check for volume spike on breakouts

3. Over-Trading

❌ Don't force trades when ranges are unclear

✅ Wait for high-probability setups only

4. Poor Risk Management

❌ Don't risk more than planned or use tight stops in volatile conditions

✅ Stick to predetermined risk levels

5. Fighting the Trend

❌ Don't fade breakouts in strongly trending markets

✅ Align trades with overall market direction

Daily Trading Routine

Pre-Market (8:00-9:30 AM)

Check overnight news and earnings

Review major indices (SPY, QQQ, IWM)

Identify potential opening range candidates

Set alerts for range breakouts

Market Open (9:30-10:00 AM)

Watch opening range formation

Note volume and price action quality

Mark key levels on charts

Prepare for breakout signals

Trading Session (10:00 AM - 4:00 PM)

Execute breakout strategies

Manage existing positions

Trail stops as profits develop

Look for additional setups

Post-Market Review

Analyze winning and losing trades

Review range quality vs. outcomes

Identify improvement areas

Prepare for next session

Best Stocks/ETFs for Opening Range Trading

Large Cap Stocks (Best for beginners):

AAPL, MSFT, GOOGL, AMZN, TSLA

High liquidity, predictable behavior

Good range formation most days

ETFs (Consistent patterns):

SPY, QQQ, IWM, XLF, XLE

Excellent liquidity

Clear range boundaries

Mid-Cap Growth (Advanced traders):

Stocks with good volume (1M+ shares daily)

Recent news catalysts

Clean technical patterns

Performance Optimization

Track These Metrics:

Win rate by range type (OR5 vs OR15 vs OR30)

Average R/R (risk vs reward ratio)

Best performing market conditions

Time of day performance

Continuous Improvement:

Keep detailed trade journal

Review failed breakouts for patterns

Adjust position sizing based on win rate

Refine entry timing based on backtesting

Final Tips for Success

Start small - Paper trade or use tiny positions initially

Focus on quality - Better to miss trades than take bad ones

Stay disciplined - Stick to your rules even during losing streaks

Adapt to conditions - What works in trending markets may fail in choppy conditions

Keep learning - Markets evolve, so should your approach

The opening range strategy is powerful because it captures natural market behavior, but like all strategies, it requires practice, discipline, and proper risk management to be profitable long-term.

EvoTrend-X Indicator — Evolutionary Trend Learner ExperimentalEvoTrend-X Indicator — Evolutionary Trend Learner

NOTE: This is an experimental Pine Script v6 port of a Python prototype. Pine wasn’t the original research language, so there may be small quirks—your feedback and bug reports are very welcome. The model is non-repainting, MTF-safe (lookahead_off + gaps_on), and features an adaptive (fitness-based) candidate selector, confidence gating, and a volatility filter.

⸻

What it is

EvoTrend-X is adaptive trend indicator that learns which moving-average length best fits the current market. It maintains a small “population” of fast EMA candidates, rewards those that align with price momentum, and continuously selects the best performer. Signals are gated by a multi-factor Confidence score (fitness, strength vs. ATR, MTF agreement) and a volatility filter (ATR%). You get a clean Fast/Slow pair (for the currently best candidate), optional HTF filter, a fitness ribbon for transparency, and a themed info panel with a one-glance STATUS readout.

Core outputs

• Selected Fast/Slow EMAs (auto-chosen from candidates via fitness learning)

• Spread cross (Fast – Slow) → visual BUY/SELL markers + alert hooks

• Confidence % (0–100): Fitness ⊕ Distance vs. ATR ⊕ MTF agreement

• Gates: Trend regime (Kaufman ER), Volatility (ATR%), MTF filter (optional)

• Candidate Fitness Ribbon: shows which lengths the learner currently prefers

• Export plot: hidden series “EvoTrend-X Export (spread)” for downstream use

⸻

Why it’s different

• Evolutionary learning (on-chart): Each candidate EMA length gets rewarded if its slope matches price change and penalized otherwise, with a gentle decay so the model forgets stale regimes. The best fitness wins the right to define the displayed Fast/Slow pair.

• Confidence gate: Signals don’t light up unless multiple conditions concur: learned fitness, spread strength vs. volatility, and (optionally) higher-timeframe trend.

• Volatility awareness: ATR% filter blocks low-energy environments that cause death-by-a-thousand-whipsaws. Your “why no signal?” answer is always visible in the STATUS.

• Preset discipline, Custom freedom: Presets set reasonable baselines for FX, equities, and crypto; Custom exposes all knobs and honors your inputs one-to-one.

• Non-repainting rigor: All MTF calls use lookahead_off + gaps_on. Decisions use confirmed bars. No forward refs. No conditional ta.* pitfalls.

⸻

Presets (and what they do)

• FX 1H (Conservative): Medium candidates, slightly higher MinConf, modest ATR% floor. Good for macro sessions and cleaner swings.

• FX 15m (Active): Shorter candidates, looser MinConf, higher ATR% floor. Designed for intraday velocity and decisive sessions.

• Equities 1D: Longer candidates, gentler volatility floor. Suits index/large-cap trend waves.

• Crypto 1H: Mid-short candidates, higher ATR% floor for 24/7 chop, stronger MinConf to avoid noise.

• Custom: Your inputs are used directly (no override). Ideal for systematic tuning or bespoke assets.

⸻

How the learning works (at a glance)

1. Candidates: A small set of fast EMA lengths (e.g., 8/12/16/20/26/34). Slow = Fast × multiplier (default ×2.0).

2. Reward/decay: If price change and the candidate’s Fast slope agree (both up or both down), its fitness increases; otherwise decreases. A decay constant slowly forgets the distant past.

3. Selection: The candidate with highest fitness defines the displayed Fast/Slow pair.

4. Signal engine: Crosses of the spread (Fast − Slow) across zero mark potential regime shifts. A Confidence score and gates decide whether to surface them.

⸻

Controls & what they mean

Learning / Regime

• Slow length = Fast ×: scales the Slow EMA relative to each Fast candidate. Larger multiplier = smoother regime detection, fewer whipsaws.

• ER length / threshold: Kaufman Efficiency Ratio; above threshold = “Trending” background.

• Learning step, Decay: Larger step reacts faster to new behavior; decay sets how quickly the past is forgotten.

Confidence / Volatility gate

• Min Confidence (%): Minimum score to show signals (and fire alerts). Raising it filters noise; lowering it increases frequency.

• ATR length: The ATR window for both the ATR% filter and strength normalization. Shorter = faster, but choppier.

• Min ATR% (percent): ATR as a percentage of price. If ATR% < Min ATR% → status shows BLOCK: low vola.

MTF Trend Filter

• Use HTF filter / Timeframe / Fast & Slow: HTF Fast>Slow for longs, Fast threshold; exit when spread flips or Confidence decays below your comfort zone.

2) FX index/majors, 15m (active intraday)

• Preset: FX 15m (Active).

• Gate: MinConf 60–70; Min ATR% 0.15–0.30.

• Flow: Focus on session opens (LDN/NY). The ribbon should heat up on shorter candidates before valid crosses appear—good early warning.

3) SPY / Index futures, 1D (positioning)

• Preset: Equities 1D.

• Gate: MinConf 55–65; Min ATR% 0.05–0.12.

• Flow: Use spread crosses as regime flags; add timing from price structure. For adds, wait for ER to remain trending across several bars.

4) BTCUSD, 1H (24/7)

• Preset: Crypto 1H.

• Gate: MinConf 70–80; Min ATR% 0.20–0.35.

• Flow: Crypto chops—volatility filter is your friend. When ribbon and HTF OK agree, favor continuation entries; otherwise stand down.

⸻

Reading the Info Panel (and fixing “no signals”)

The panel is your self-diagnostic:

• HTF OK? False means the higher-timeframe EMAs disagree with your intended side.

• Regime: If “Chop”, ER < threshold. Consider raising the threshold or waiting.

• Confidence: Heat-colored; if below MinConf, the gate blocks signals.

• ATR% vs. Min ATR%: If ATR% < Min ATR%, status shows BLOCK: low vola.

• STATUS (composite):

• BLOCK: low vola → increase Min ATR% down (i.e., allow lower vol) or wait for expansion.

• BLOCK: HTF filter → disable HTF or align with the HTF tide.

• BLOCK: confidence → lower MinConf slightly or wait for stronger alignment.

• OK → you’ll see markers on valid crosses.

⸻

Alerts

Two static alert hooks:

• BUY cross — spread crosses up and all gates (ER, Vol, MTF, Confidence) are open.

• SELL cross — mirror of the above.

Create them once from “Add Alert” → choose the condition by name.

⸻

Exporting to other scripts

In your other Pine indicators/strategies, add an input.source and select EvoTrend-X → “EvoTrend-X Export (spread)”. Common uses:

• Build a rule: only trade when exported spread > 0 (trend filter).

• Combine with your oscillator: oscillator oversold and spread > 0 → buy bias.

⸻

Best practices

• Let it learn: Keep Learning step moderate (0.4–0.6) and Decay close to 1.0 (e.g., 0.99–0.997) for smooth regime memory.

• Respect volatility: Tune Min ATR% by asset and timeframe. FX 1H ≈ 0.10–0.20; crypto 1H ≈ 0.20–0.35; equities 1D ≈ 0.05–0.12.

• MTF discipline: HTF filter removes lots of “almost” trades. If you prefer aggressive entries, turn it off and rely more on Confidence.

• Confidence as throttle:

• 40–60%: exploratory; expect more signals.

• 60–75%: balanced; good daily driver.

• 75–90%: selective; catch the clean stuff.

• 90–100%: only A-setups; patient mode.

• Watch the ribbon: When shorter candidates heat up before a cross, momentum is forming. If long candidates dominate, you’re in a slower trend cycle.

⸻

Non-repainting & safety notes

• All request.security() calls use lookahead=barmerge.lookahead_off, gaps=barmerge.gaps_on.

• No forward references; decisions rely on confirmed bar data.

• EMA lengths are simple ints (no series-length errors).

• Confidence components are computed every bar (no conditional ta.* traps).

⸻

Limitations & tips

• Chop happens: ER helps, but sideways microstructure can still flicker—use Confidence + Vol filter as brakes.

• Presets ≠ oracle: They’re sensible baselines; always tune MinConf and Min ATR% to your venue and session.

• Theme “Auto”: Pine cannot read chart theme; “Auto” defaults to a Dark-friendly palette.

⸻

Publisher’s Screenshots Checklist

1) FX swing — EURUSD 1H

• Preset: FX 1H (Conservative)

• Params: MinConf=70, ATR Len=14, Min ATR%=0.12, MTF ON (TF=4H, 20/50)

• Show: Clear BUY cross, STATUS=OK, green regime background; Fitness Ribbon visible.

2) FX intraday — GBPUSD 15m

• Preset: FX 15m (Active)

• Params: MinConf=60, ATR Len=14, Min ATR%=0.20, MTF ON (TF=60m)

• Show: SELL cross near London session open. HTF lines enabled (translucent).

• Caption: “GBPUSD 15m • Active session sell with MTF alignment.”

3) Indices — SPY 1D

• Preset: Equities 1D

• Params: MinConf=60, ATR Len=14, Min ATR%=0.08, MTF ON (TF=1W, 20/50)

• Show: Longer trend run after BUY cross; regime shading shows persistence.

• Caption: “SPY 1D • Trend run after BUY cross; weekly filter aligned.”

4) Crypto — BINANCE:BTCUSDT 1H

• Preset: Crypto 1H

• Params: MinConf=75, ATR Len=14, Min ATR%=0.25, MTF ON (TF=4H)

• Show: BUY cross + quick follow-through; Ribbon warming (reds/yellows → greens).

• Caption: “BTCUSDT 1H • Momentum break with high confidence and ribbon turning.”

Leaders DashboardA compact, glanceable leadership dashboard for monitoring market health via your hand-picked “Top 8” stocks. It tracks trend posture and momentum using practical checks (21-EMA, 50-DMA, rising 21, and proximity to highs), plus optional QQQ/SPY benchmark rows , all in a clean, color-forward table that sits on your chart.

What it shows

Sym – your 8 symbols (short format).

>21 – price above the 21-EMA.

>50 – price above the 50-DMA.

↑21 – 21-EMA sloping up.

ΔX% – within X% of high (default logic: ATH; switchable to N-bar High).

Price – last price (toggleable).

Σ Totals row (optional) – counts “passes” across your 8 names for each column, with Neutral or Majority shading.

Benchmarks (QQQ/SPY) are optional rows for context and do not contribute to totals.

Built for signal at a glance

Color-first cells with minimal ink: defaults to labels OFF and ✓ / ✗ markers ON.

Δ% header is compact (e.g., Δ2%) to save space.

Position & size: snap to any chart corner; Tiny/Small/Medium/Large font presets.

Per-column toggles: show/hide any column to match your workflow.

Controls (key inputs)

Symbols: 8 user slots (use exchange prefixes, e.g., NASDAQ:PLTR).

Benchmark rows: None / QQQ / SPY / Both (not counted in Σ).

Table position & size: four corners; Tiny → Large font presets.

Opacity mode:

Per-color (default) – honors each color picker’s opacity (PF/W defaults set to 50%).

Global – one slider controls transparency across the whole table.

YES/NO labels: off by default.

Cell marker: None / Dot / Check/X (default).

Show Price: on by default.

Show totals row (Σ): on by default; Totals color mode = Neutral or Majority.

Δ% logic: choose ATH or N-bar High and set the % threshold and lookback.

How to use it

Drop it on any timeframe; the stats are computed on your current chart timeframe for each symbol.

Enter your 8 leaders (e.g., AVGO, GEV, HOOD, MSFT, NVDA, PLTR, RBLX, TSM) and optionally add QQQ/SPY.

Keep labels off with Check/X markers for a clean, color-driven read.

Watch the Σ row:

- 6/8 passing on >21, >50, and ↑21 suggests healthy leadership breadth.

- A high Δ% count means many leaders are pressing highs.

Notes & tips

If a symbol shows as invalid, confirm the exchange prefix (e.g., NASDAQ:, NYSE:, AMEX:).

ATH proximity uses up to 10,000 bars; switch to N-bar High if you prefer a rolling window.

The table is an overlay; use opacity/size to keep it unobtrusive over price.

Disclaimer: For educational/information purposes only. This script does not provide financial advice, nor does it place or manage orders. Always do your own research.

Sector Rotation & Money Flow Dashboard📊 Overview

The Sector Rotation & Money Flow Dashboard is a comprehensive market analysis tool that tracks 39 major sector ETFs in real-time, providing institutional-grade insights into sector rotation, momentum shifts, and money flow patterns. This indicator helps traders identify which sectors are attracting capital, which are losing favor, and where the next opportunities might emerge.

Perfect for swing traders, position traders, and investors who want to stay ahead of sector rotation and ride the strongest trends while avoiding weak sectors.

🎯 What This Indicator Does

Tracks 39 Major Sectors: From technology to utilities, cryptocurrencies to commodities

Calculates Multiple Timeframes: 1-week, 1-month, 3-month, and 6-month performance

Advanced Momentum Metrics: Proprietary momentum score and acceleration calculations

Relative Strength Analysis: Compare sector performance against any benchmark index

Money Flow Signals: Visual indicators showing where institutional money is moving

Smart Filtering: Pre-built strategy filters for different trading styles

Trend Detection: Emoji-based visual system for quick trend identification

💡 Key Features

1. Performance Metrics

Multiple timeframe analysis (1W, 1M, 3M, 6M)

Month-over-month change tracking

Relative strength vs benchmark index

2. Advanced Analytics

Momentum Score: Weighted composite of recent performance

Acceleration: Rate of change in momentum (second derivative)

Money Flow Signals: IN/OUT/TURN/WATCH indicators

3. Strategy Preset Filters

🎯 Swing Trade: High momentum opportunities

📈 Trend Follow: Established uptrends

🔄 Mean Reversion: Oversold bounce candidates

💎 Value Hunt: Deep value opportunities

🚀 Breakout: Emerging strength

⚠️ Risk Off: Sectors to avoid

4. Customization

All 39 sector ETFs can be customized

Adjustable benchmark index

Flexible display options

Multiple sorting methods

📋 Settings Documentation

Display Settings

Show Table (Default: On)

Toggles the entire dashboard display

Table Position (Default: Middle Center)

Choose from 9 positions on your chart

Options: Top/Middle/Bottom × Left/Center/Right

Rows to Show (Default: 15)

Number of sectors displayed (5-40)

Useful for focusing on top/bottom performers

Sort By (Default: Momentum)

1M/3M/6M: Sort by specific timeframe performance

Momentum: Weighted recent performance score

Acceleration: Rate of momentum change

1M Change: Month-over-month improvement

RS: Relative strength vs benchmark

Flow: IN First: Prioritize sectors with inflows

Flow: TURN First: Focus on reversal candidates

Recovery Plays: Oversold sectors recovering

Oversold Bounce: Deepest declines with positive signs

Top Gainers/Losers 3M: Best/worst quarterly performers

Best Acc + Mom: Combined strength score

Worst Acc (Topping): Sectors losing momentum

Filter Settings

Strategy Preset Filter (Default: All)

All: No filtering

🎯 Swing Trade: Mom >5, Acc >2, Money flowing in

📈 Trend Follow: Positive 1M & 3M, RS >0

🔄 Mean Reversion: Oversold but improving

💎 Value Hunt: Down >10% with recovery signs

🚀 Breakout: Rapid momentum surge

⚠️ Risk Off: Declining or topping sectors

Custom Flow Filter: Use manual flow filter

Custom Flow Signal Filter (Default: All)

Only active when Strategy Preset = "Custom Flow Filter"

IN Only: Strong inflows

TURN Only: Reversal signals

WATCH Only: Recovery candidates

OUT Only: Outflow sectors

Active Flows Only: Any non-neutral signal

Hide Low Volume ETFs (Default: Off)

Filters out illiquid sectors (future enhancement)

Visual Settings

Show Trend Emojis (Default: On)

🚀 Breakout (Strong 1M + High Acceleration)

🔥 Hot Recovery (From -10% to positive)

💪 Steady Uptrend (All timeframes positive)

➡️ Sideways/Ranging

⚠️ Warning/Topping (Up >15%, now slowing)

📉 Falling (Negative + declining)

🔄 Bottoming (Improving from lows)

Compact Mode (Default: Off)

Removes decimals for cleaner display

Useful when showing many rows

Min Data Points Required (Default: 3)

Minimum data points needed to display a sector

Prevents showing sectors with insufficient data

Relative Strength Settings

RS Benchmark Index (Default: AMEX:SPY)

Index to compare all sectors against

Can use SPY, QQQ, IWM, or any other index

RS Period (Days) (Default: 21)

Lookback period for RS calculation

21 days = 1 month, 63 days = 3 months, etc.

Sector ETF Settings (Groups 1-39)

Each sector has two inputs:

Symbol: The ticker (e.g., "AMEX:XLF")

Name: Display name (e.g., "Financials")

All 39 sectors can be customized to track different ETFs or markets.

📈 Column Explanations

Sector: ETF name/description

1M%: 1-month (21-day) performance

3M%: 3-month (63-day) performance

6M%: 6-month (126-day) performance

Mom: Momentum score (weighted average, recent-biased)

Acc: Acceleration (momentum rate of change)

Δ1M: Month-over-month change

RS: Relative strength vs benchmark

Flow: Money flow signal

↗️ IN: Strong inflows

🔄 TURN: Potential reversal

👀 WATCH: Recovery candidate

↘️ OUT: Outflows

—: Neutral

🎮 Usage Tips

For Swing Traders (3-14 days)

Use "🎯 Swing Trade" filter

Sort by "Acceleration" or "Momentum"

Look for Flow = "IN" and Mom >10

Confirm with positive RS

For Position Traders (2-8 weeks)

Use "📈 Trend Follow" filter

Sort by "RS" or "Best Acc + Mom"

Focus on consistent green across timeframes

Ensure RS >3 for market leaders

For Value Investors

Use "💎 Value Hunt" filter

Sort by "Recovery Plays" or "Top Losers 3M"

Look for improving Δ1M

Check for "WATCH" or "TURN" signals

For Risk Management

Regularly check "⚠️ Risk Off" filter

Sort by "Worst Acc (Topping)"

Review holdings for ⚠️ warning emojis

Exit sectors showing "OUT" flow

Market Regime Recognition

Bull Market: Many sectors showing "IN" flow, positive RS

Bear Market: Widespread "OUT" flows, negative RS

Rotation: Mixed flows, some "IN" while others "OUT"

Recovery: Multiple "TURN" and "WATCH" signals

🔧 Pro Tips

Combine Filters + Sorting: Filter first to narrow candidates, then sort to prioritize

Multi-Timeframe Confirmation: Best setups show alignment across 1M, 3M, and momentum

RS is Key: Sectors outperforming SPY (RS >0) tend to continue outperforming

Acceleration Matters: Positive acceleration often precedes price breakouts

Flow Transitions: "WATCH" → "TURN" → "IN" progression identifies new trends early

Regular Scans:

Daily: Check "Acceleration" sort

Weekly: Review "1M Change"

Monthly: Analyze "RS" shifts

Divergence Signals:

Price up but Acceleration down = Potential top

Price down but Acceleration up = Potential bottom

Sector Pairs Trading: Long sectors with "IN" flow, short sectors with "OUT" flow

⚠️ Important Notes

This indicator makes 40 security requests (maximum allowed)

Best used on Daily timeframe

Data updates in real-time during market hours

Some ETFs may show "—" if data is unavailable

🎯 Common Strategies

"Follow the Flow"

Only trade sectors showing "IN" flow with positive RS

"Rotation Catcher"

Focus on "TURN" signals in sectors down >15% from highs

"Momentum Rider"

Trade top 3 sectors by Momentum score, exit when Acceleration turns negative

"Mean Reversion"

Buy sectors in bottom 20% by 3M performance when Δ1M improves

"Relative Strength Leader"

Maintain positions only in sectors with RS >5

Not financial advice - always do additional research

Defense Mode Dashboard ProWhat it is

A one‑look market regime dashboard for ES, NQ, YM, RTY, and SPY that tells you when to play defense, when you might have an offense cue, and when to chill. It blends VIX, VIX term structure, ATR 5 over 60, and session gap signals with clean alerts and a compact table you can park anywhere.

Why traders like it

Because it filters out the noise. Regime first, tactics second. You avoid trading size into landmines and lean in when volatility cooperates.

What it measures

Volatility stress with VIX level and VIX vs 20‑SMA

Term structure using VX1 vs VX2 with two modes

Diff mode: VX1 minus VX2

Ratio mode: VX1 divided by VX2

Realized volatility using ATR5 over ATR60 with optional smoothing

Session risk from RTH opening gaps and overnight range, normalized by ATR

How to use in 30 seconds

Pick a preset in the inputs. ES, NQ, YM, RTY, SPY are ready.

Leave thresholds at defaults to start.

Add one TradingView alert using “Any alert() function call”.

Trade smaller or stand aside when the header reads DEFENSE ON. Consider leaning in only when you see OFFENSE CUE and your playbook agrees.

Defaults we recommend

VIX triggers: 22 and 1.25× the 20‑SMA

Term mode: Diff with tolerance 0.00. Use Ratio at 1.00+ for choppier markets

ATR 5/60 defense: 1.25. Offense cue: 0.85 or lower

ATR smoothing: 1. Try 2 to 3 if you want fewer flips

Gap mode: RTH. Turn Both on if you want ON range to count too

RTH wild gap: 0.60× ATR5. ON wild range: 0.80× ATR5

Alert cadence: Once per RTH session

Snooze: Quick snooze first 30 minutes on. Fire on snooze exit off, unless you really want the catch‑up ping

New since the last description

Multi‑asset presets set symbols and RTH windows for ES, NQ, YM, RTY, SPY

Term ratio mode with near‑flat warning when ratio is between 1.00 and your trigger

ATR smoothing for the 5 over 60 ratio

RTH keying for cadence, so “Once per RTH session” behaves like a trader expects

Snooze upgrades with quick snooze tied to the first N minutes of RTH and an optional fire‑on‑snooze‑exit

Compact title merge and user color controls for labels, values, borders, and background

Exposed series for integrations: DefenseOn(1=yes) and OffenseCue(1=yes)

Debug toggle to visualize gap points, ON range, and term readings

Stronger NA handling with a clear “No core data” row when feeds are missing

Notes

Dynamic alerts require “Any alert() function call”.

Works on any chart timeframe. Daily reads and 1‑minute anchors handle the regime logic.

Volumetric Expansion/Contraction### Indicator Title: Volumetric Expansion/Contraction

### Summary

The Volumetric Expansion/Contraction (PCC) indicator is a comprehensive momentum oscillator designed to identify high-conviction price moves. Unlike traditional oscillators that only look at price, the PCC integrates four critical dimensions of market activity: **Price Change**, **Relative Volume (RVOL)**, **Cumulative Volume Delta (CVD)**, and **Average True Range (ATR)**.

Its primary purpose is to help traders distinguish between meaningful, volume-backed market expansions and noisy, unsustainable price action. It gives more weight to moves that occur in a controlled, low-volatility environment, highlighting potential starts of new trends or significant shifts in market sentiment.

### Key Concepts & Purpose

The indicator's unique formula synthesizes the following concepts:

1. **Price Change:** Measures the magnitude and direction of the primary move.

2. **Relative Volume (RVOL):** Confirms that the move is backed by significant volume compared to its recent average, indicating institutional participation.

3. **Cumulative Volume Delta (CVD):** Measures the underlying buying and selling pressure, confirming that the price move is aligned with the net flow of market orders.

4. **Inverse Volatility (ATR):** This is the indicator's unique twist. It normalizes the signal by the inverse of the Average True Range. This means the indicator's value is **amplified** when volatility (ATR) is low (signifying a controlled, confident expansion) and **dampened** when volatility is high (filtering out chaotic, less predictable moves).

The goal is to provide a single, easy-to-read oscillator that signals when price, volume, and order flow are all in alignment, especially during a breakout from a period of contraction.

### Features

* **Main Oscillator Line:** A single line plotted in a separate pane that represents the calculated strength of the volumetric expansion or contraction.

* **Zero Line:** A dotted reference line to easily distinguish between bullish (above zero) and bearish (below zero) regimes.

* **Visual Threshold Zones:** The background automatically changes color to highlight periods of significant strength:

* **Bright Green:** Indicates a "Strong Up Move" when the oscillator crosses above the user-defined upper threshold.

* **Bright Fuchsia:** Indicates a "Strong Down Move" when the oscillator crosses below the user-defined lower threshold.

### Configurable Settings & Filters

The indicator is fully customizable to allow for extensive testing and adaptation to different assets and timeframes.

#### Main Calculation Inputs

* **Price Change Lookback:** Sets the period for calculating the primary price change.

* **CVD Normalization Length:** The lookback period for normalizing the Cumulative Volume Delta.

* **RVOL Avg Volume Length:** The lookback for the simple moving average of volume, used to calculate RVOL.

* **RVOL Normalization Length:** The lookback period for normalizing the RVOL score.

* **ATR Length & Normalization Length:** Sets the periods for calculating the ATR and its longer-term average for normalization.

#### Weights

* Fine-tune the impact of each core component on the final calculation, allowing you to emphasize what matters most to your strategy (e.g., give more weight to CVD or RVOL).

#### External Market Filter (Powerful Feature)

* **Enable SPY/QQQ Filter for Up Moves?:** A checkbox to activate a powerful regime filter.

* **Symbol:** A dropdown to choose whether to filter signals based on the trend of **SPY** or **QQQ**.

* **SMA Period:** Sets the lookback period for the Simple Moving Average (default is 50).

* **How it works:** When enabled, this filter will **only allow "Strong Up Move" signals to appear if the chosen symbol (SPY or QQQ) is currently trading above its specified SMA**. This is an excellent tool for aligning your signals with the broader market trend and avoiding bullish entries in a bearish market.

#### Visuals

* **Upper/Lower Threshold:** Allows you to define what level the oscillator must cross to trigger the colored background zones, letting you customize the indicator's sensitivity.

***

**Disclaimer:** This tool is designed for market analysis and confluence. It is not a standalone trading system. Always use this indicator in conjunction with your own trading strategy, risk management, and other forms of analysis.

A+ Trade CheckList with Comprehensive Relative StrengthThe indicator designed for traders who need real-time market assessment across multiple timeframes and benchmarks. This comprehensive tool combines traditional technical analysis with sophisticated relative strength measurements to provide a complete market picture in one convenient table display.

The indicator tracks essential trading levels including:

QQQ and SPY trend analysis using exponential moving averages

Previous day and week high/low levels for key support and resistance

Market open levels from the first 5 and 15 minutes of trading (9:30 AM ET)

VWAP positioning for institutional price reference

Short-term EMA positioning for momentum assessment

Advanced Relative Strength Analysis

The standout feature of this indicator is its comprehensive 8-metric relative strength scoring system that compares your current ticker against both QQQ (Nasdaq-100) and SPY (S&P 500) benchmarks.

The 4-Metric Relative Strength System Explained

Metric 1: Relative Strength Ratio (RSR)

Purpose: Measures whether your ticker is outperforming or underperforming relative to its historical relationship with the benchmarks.

How it works:

Calculates the ratio of your ticker's price to QQQ/SPY prices

Compares current ratio to a 20-period moving average of the ratio

Scores +1 if ratio is above average (relative strength), -1 if below (relative weakness)

Trading significance: Identifies when a stock is breaking out of its normal correlation pattern with major indices.

Metric 2: Percentage-Based Relative Performance

Purpose: Compares short-term percentage changes to identify immediate relative momentum.

How it works:

Calculates 5-day percentage change for your ticker and benchmarks

Subtracts benchmark performance from ticker performance

Scores +1 if outperforming by >1%, -1 if underperforming by >1%, 0 for neutral

Trading significance: Captures recent momentum shifts and identifies stocks moving independently of market direction.

Metric 3: Beta-Adjusted Relative Strength (Alpha)

Purpose: Measures risk-adjusted performance by accounting for the ticker's natural volatility relationship with benchmarks.

How it works:

Calculates rolling beta (correlation and variance relationship)

Determines expected returns based on benchmark moves and beta

Measures alpha (excess returns above/below expectations)

Scores based on whether alpha is consistently positive or negative

Trading significance: Identifies stocks generating returns beyond what their risk profile would suggest, indicating fundamental strength or weakness.

Metric 4: Volume-Weighted Relative Strength

Purpose: Incorporates volume analysis to validate price-based relative strength signals.

How it works:

Compares VWAP-based percentage changes between ticker and benchmarks

Applies volume weighting factor based on relative volume strength

Enhances score when high relative volume confirms price movements

Trading significance: Distinguishes between genuine institutional-driven moves and low-volume price action that may not sustain.

Combined Scoring System

The indicator generates 8 individual scores (4 metrics × 2 benchmarks) that combine into a single strength assessment:

Score Interpretation

Strong (4-8 points): Ticker significantly outperforming both benchmarks across multiple methodologies

Moderate Strong (1-3 points): Ticker showing good relative strength with some mixed signals

Neutral (0 points): Balanced performance relative to benchmarks

Moderate Weak (-1 to -3 points): Ticker showing relative weakness with some mixed signals

Weak (-4 to -8 points): Ticker significantly underperforming both benchmarks

Display Format

The indicator shows results as: "Strong (6/8)" indicating the ticker scored 6 out of 8 possible points.

Capitulation Volume Detector by @RhinoTradezOverview

Hey traders, want to catch the market when it’s totally losing it? The Capitulation Volume Detector is your go-to buddy for spotting those wild moments when panic selling takes over. Picture this: prices plummet, volume explodes, and everyone’s bailing out—that’s capitulation, and it might just signal a turning point. This script throws a bright marker on your chart whenever the chaos hits, so you can decide if it’s time to jump in or sit tight. Built fresh in Pine Script v6, it’s sleek, customizable, and packs an alert to keep you posted—perfect for stocks, indices like SPY, or even crypto chaos.

Inspired by epic sell-offs like March 2020’s COVID crash, this tool’s here to help you navigate the storm with a smile (and maybe a profit).

What It Does

Capitulation volume is that “everyone’s out!” moment: a steep price drop meets a massive volume surge, hinting that sellers are tapped out. It’s not a guaranteed reversal—sometimes the bleeding continues—but it’s a loud clue that fear’s peaked. Here’s the magic:

Volume Check : Measures current volume against a customizable average (default: 20 bars).

Price Plunge : Tracks the percentage drop from the last close.

Capitulation Cal l: When volume rockets past your threshold (e.g., 2x average) and price tanks (e.g., -5%), you get a red triangle above the bar.

Stay Alert : Fires off a detailed message (e.g., “Volume 300M > 200M, Drop -10%”) so you’re never caught off guard.

Think of it as your market meltdown radar—simple, effective, and ready to roll.

Functionality Breakdown

Volume Surge Spotter :

Uses a 20-bar Simple Moving Average (SMA) of volume as your baseline.

Flags any bar where volume exceeds this average by your chosen multiplier (default: 2x).

Price Drop Detector :

Calculates the percentage change from the prior close.

Triggers when the drop’s bigger than your set limit (default: -5%).

Capitulation Marker:

Combines both signals: high volume + sharp drop = capitulation.

Slaps a red triangle above the bar for instant “whoa, there it is!” vibes.

Real-Time Alerts :

Sends a custom alert with volume and drop details, keeping you in the loop without babysitting the chart.

Customization Options

Tune it to your trading style with these easy settings:

Volume Multiplier (x Avg): Starts at 2.0 (2x average volume). Bump it to 3.0 for only the wildest spikes or dial it to 1.5 for more frequent catches. Range: 1.0-10.0, step 0.1.

Price Drop Threshold (%): Default 5.0 (a -5% drop). Go big with 10.0 for crash-level falls or ease to 3.0 for lighter dips. Range: 1.0-20.0, step 0.1.

Average Volume Period: Default 20 bars. Stretch it to 50 for a broader view or shrink to 10 for quick reactions. Range: 1-100.

Capitulation Marker Color: Red by default—because panic’s loud! Switch it to blue, green, or pink to match your chart’s personality.

How to Use It