Market Open - Relative VolumeThe indicator calculates the Pre-market volume percentage of the current day, relative to the average volume being traded in the trading session (14 days), displayed in Table Row 1, Table Cell 1, as V%. Pre-market volume between 15% & 30% has a orange background color. Pre-market volume percentage above 30% has a green background color.

The indicator calculates the relative volume per candle relative to the average volume being traded in that time period (14 days) (e.g., "1M," "2M," up to "5M"), displayed in a table. Relative volume between 250% & 350% has a orange background color. Relative volume above 350% has a green background color.

FYI >> Indicator calculations are per candle, not time unit (due to pine script restrictions). Meaning, the indicator current table data is only accurate in the 1M chart. If you are using the indicator in a higher timeframe, e.g., on the 5M chart, then the values in table cells >> (1M value == relative volume of the first 5-minute candle) (5M value = relative volume of the first five 5-minute candles) and so on. (Future versions will have a dynamic table).

Pesquisar nos scripts por "ha溢价率"

SMC Structures and FVGThe SMC Structures and FVG indicator allows the user to easily identify trend continuations (Break Of Structure) or trend changes (CHange Of CHaracter) on any time frame. In addition, it display all FVG areas, whether they are bullish, bearish, or even mitigated.

Fair Value Gap :

The FVG process shows every bullish, bearish or even mitigated FVG liquidity area. When a FVG is fully mitigated it will directly be removed of the chart.

There is an history of FVG to show. By selecting specific number of FVG to show in the chart, the user can focus its analysis on lasts liquidity area.

Here's the rules for FVG color :

Green when it's a bullish FVG and has not been mitigated

Red when it's a bearish FVG and has not been mitigated

Gray when the bullish / bearish FVG has been mitigated

Removed when the FVG has been fully mitigated

Structures analysis:

The Structure process show BOS in grey lines and CHoCH in yellow lines. It shows to the user the lasts price action pattern.

The blue lines are the high value and the low value of the current structure.

ICT Institutional Order Flow (fadi)ICT Institutional Order Flow indicator is intended to provide wholistic view to better analyze order flow and where price may go to next. The concept follows ICT principles.

ICT Market Structure

ICT breaks down Pivot points into three categories:

Short Term High/Low (STH/STL) is a 3 candle pattern with a low with higher low on each side (STL), or a high with lower high on each side (STH)

Intermediate Term High/Low (ITH/ITL) uses the calculated STH/STL and marks any STH that has lower or STH on each side, and STL that has higher STL on each side

Long Term High/Low (LTH/LTL) uses the calculated ITH/ITL and marks any ITH that has lower or ITH on each side, and ITL that has higher ITL on each side

Note: ICT also states that if a STH wicks into and closes (almost?) a FVG, he marks it as ITH even if it does not have STH on reach side. This scenario is not covered by this indicator

Liquidity

liquidity is usually present under pivot points. The more prominent the pivot point, the more likely higher values liquidity pools reside under/above it. Liquidity under ITL and LTL as an example, will have better indication of which liquidity the price may seek next.

Displacement

Displacement registers above average move in the price resulting in strong visible move. If requiring a FVG is enabled (in settings), then the displacement could possibly (but never guaranteed) be used to visually recognize a move as it develops.

Full Credit: The calculation for Displacement is derived from TFO's Visualizing Displacement

Imbalances

Imbalances can come in different forms. This indicator identifies three type of imbalances:

1. FVG

2. Volume Imbalance

3. Open Gaps

Imbalances completes the picture by help visualize strong moves, where possible pivot points may develop, and how to enter or manage a trade.

Support and Resistance Backtester [SS]Hey everyone,

Excited to release this indicator I have been working on.

I conceptualized it as an idea a while ago and had to nail down the execution part of it. I think I got it to where I am happy with it, so let me tell you about it!

What it does?

This provides the user with the ability to quantify support and resistance levels. There are plenty of back-test strategies for RSI, stochastics, MFI, any type of technical based indicator. However, in terms of day traders and many swing traders, many of the day traders I know personally do not use or rely on things like RSI, stochastics or MFI. They actually just play the support and resistance levels without attention to anything else. However, there are no tools available to these people who want to, in a way, objectively test their identified support and resistance levels.

For me personally, I use support and resistance levels that are mathematically calculated and I am always curious to see which levels:

a) Have the most touches,

b) Have provided the most support,

c) Have provided the most resistance; and,

d) Are most effective as support/resistance.

And, well, this indicator answers all four of those questions for you! It also attempts to provide some way to support and resistance traders to quantify their levels and back-test the reliability and efficacy of those levels.

How to use:

So this indicator provides a lot of functionality and I think its important to break it down part by part. We can do this as we go over the explanation of how to use it. Here is the step by step guide of how to use it, which will also provide you an opportunity to see the options and functionality.

Step 1: Input your support and resistance levels:

When we open up the settings menu, we will see the section called "Support and Resistance Levels". Here, you have the ability to input up to 5 support and resistance levels. If you have less, no problem, simply leave the S/R level as 0 and the indicator will automatically omit this from the chart and data inclusion.

Step 2: Identify your threshold value:

The threshold parameter extends the range of your support and resistance level by a desired amount. The value you input here should be the value in which you would likely stop out of your position. So, if you are willing to let the stock travel $1 past your support and resistance level, input $1 into this variable. This will extend the range for the assessment and permit the stock to travel +/- your threshold amount before it counts it as a fail or pass.

Step 3: Select your source:

The source will tell the indicator what you want to assess. If you want to assess close, it will look at where the ticker closes in relation to your support and resistance levels. If you want to see how the highs and lows behave around the S/R levels, then change the source to High or Low.

It is recommended to leave at close for optimal results and reliability however.

Step 4: Determine your lookback length:

The lookback length will be the number of candles you want the indicator to lookback to assess the support and resistance level. This is key to get your backtest results.

The recommendation is on timeframes 1 hour or less, to look back 300 candles.

On the daily, 500 candles is recommended.

Step 5: Plot your levels

You will see you have various plot settings available to you. The default settings are to plot your support and resistance levels with labels. This will look as follows:

This will plot your basic support and resistance levels for you, so you do not have to manually plot them.

However, if you want to extend the plotted support and resistance level to visually match your threshold values, you can select the "Plot Threshold Limits" option. This will extend your support and resistance areas to match the designated threshold limits.

In this case on MSFT, I have the threshold limit set at $1. When I select "Plot Threshold Limits", this is the result:

Plotting Passes and Fails:

You will notice at the bottom of the settings menu is an option to plot passes and plot fails. This will identify, via a label overlaid on the chart, where the support and resistance failures and passes resulted. I recommend only selecting one at a time as the screen can get kind of crowded with both on. here is an example on the MSFT chart:

And on the larger timeframe:

The chart

The chart displays all of the results and counts of your support and resistance results. Some things to pay attention to use the chart are:

a) The general success rate as support vs resistance

Rationale: Support levels may act as resistance more often than they do support or vice versa. Let's take a look at MSFT as an example:

The chart above shows the 334.07 level has acted as very strong support. It has been successful as support almost 82% of the time. However, as resistance, it has only been successful 33% of the time. So we could say that 334 is a strong key support level and an area we would be comfortable longing at.

b) The number of touches:

Above you will see the number of touches pointed out by the blue arrow.

Rationale: The number of touches differs from support and resistance. It counts how many times and how frequently a ticker approaches your support and/or resistance area and the duration of time spent in that area. Whereas support and resistance is determined by a candle being either above or below a s/r area, then approaching that area and then either failing or bouncing up/down, the number of touches simply assesses the time spent (in candles) around a support or resistance level. This is key to help you identify if a level has frequent touches/consolidation vs other levels and can help you filter out s/r levels that may not have a lot of touches or are infrequently touched.

Closing comments:

So this is pretty much the indicator in a nutshell. Hopefully you find it helpful and useful and enjoy it.

As always let me know your questions/comments and suggestions below.

As always I appreciate all of you who check out, try out and read about my indicators and ideas. I wish you all the safest trades and good luck!

Lower timeframe chartHi all!

I've made this script to help with my laziness (and to help me (and now you) with efficiency). It's purpose is to, without having to change the chart timeframe, being able to view the lower timeframe bars (and trend) within the last chart bar. The defaults are just my settings (It's based on daily bars), so feel free to change them and maybe share yours! It's also based on stocks, which have limited trading hours, but if you want to view this for forex trading I suggest changing the 'lower time frame' to a higher value since it has more trading hours.

The script prints a label chart (ASCII) based on your chosen timeframe and the trend, based on @KivancOzbilgic script SuperTrend The printed ASCII chart has rows (slots) that are based on ATR (14 bars) and empty gaps are removed. The current trend is decided by a percentage of bars (user defined but defaults to 80%, which is really big but let's you be very conservative in defining a trend to be bullish. Set to 50% to have the trend being decided equally or lower to be more conservative in defining a trend to be bearish) that must have a bullish SuperTrend, it's considered to be bearish otherwise. Big price range (based on the ATR for 14 bars) and big volume (true if the volume is bigger than a user defined simple moving average (defaults to 20 bars)) can be disabled for faster execution.

The chart displayed will consist of bars and thicker bars that has a higher volume than the defined simple moving average. The bars that has a 'big range' (user defined value of ATR (14 days) factor that defaults to 0.5) will also have a wick. The characters used are the following:

Green bar = ┼

Green bar with large volume = ╪

Green bar wick = │

Red bar = ╋

Red bar with large volume = ╬

Red bar wick = ┃

Bar with no range = ─

Bar with no range and high volume = ═

Best of trading!

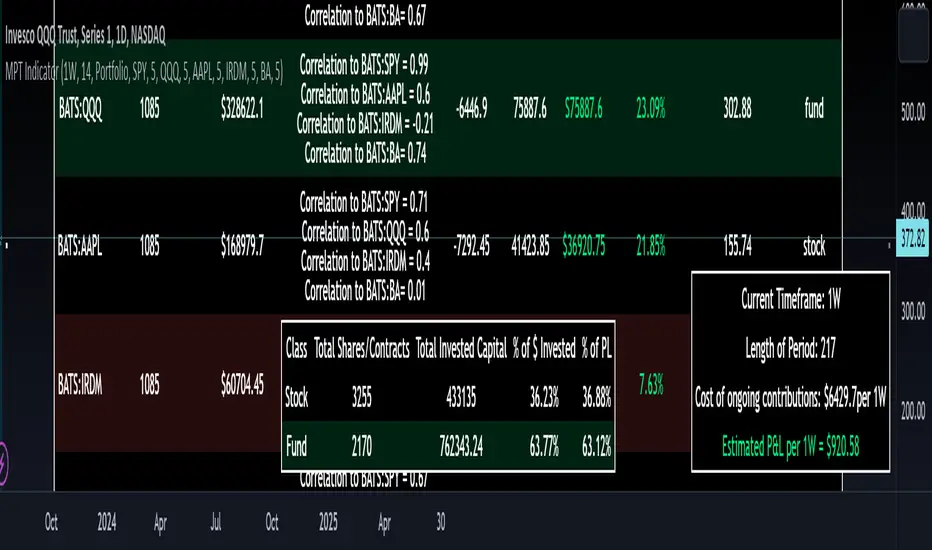

Modern Portfolio Management IndicatorAfter weeks of grueling over this indicator, I am excited to be releasing it!

Intro:

This is not a sexy, technical or math based indicator that will give you buy and sell signals or anything fancy, but it is an indicator that I created in hopes to bridge a gap I have noticed. That gap is the lack of indicators and technical resources for those who also like to plan their investments. This indicator is tailored to those who are either established investors and to those who are looking to get into investing but don't really know where to start.

The premise of this indicator is based on Modern Portfolio Theory (MPT). Before we get into the indicator itself, I think its important to provide a quick synopsis of MPT.

About MPT:

Modern Portfolio Theory (MPT) is an investment framework that was developed by Harry Markowitz in the 1950s. It is based on the idea that an investor can optimize their investment portfolio by considering the trade-off between risk and return. MPT emphasizes diversification and holds that the risk of an individual asset should be assessed in the context of its contribution to the overall portfolio's risk. The theory suggests that by diversifying investments across different asset classes with varying levels of risk, an investor can achieve a more efficient portfolio that maximizes returns for a given level of risk or minimizes risk for a desired level of return. MPT also introduced the concept of the efficient frontier, which represents the set of portfolios that offer the highest expected return for a given level of risk. MPT has been widely adopted and used by investors, financial advisors, and portfolio managers to construct and manage portfolios.

So how does this indicator help with MPT?

The thinking and theory that went behind this indicator was this: I wanted an indicator, or really just a "way" to test and back-test ticker performance over time and under various circumstances and help manage risk.

Over the last 3 years we have seen a massive bull market, followed by a pretty huge bear market, followed by a very unexpected bull market. We have been and continue to be plagued with economic and political uncertainty that seems to constantly be looming over everyone with each waking day. Some people have liquidated their retirement investments, while others are fomoing in to catch this current bull run. But which tickers are sound and how tickers and funds have compared amongst each other remains somewhat difficult to ascertain, absent manually reviewing and calculating each ticker individually.

That is where this indicator comes in. This indicator permits the user to define up to 5 equities that they are potentially interested in investing in, or are already invested in. The user can then select a specific period in time, say from the beginning of 2022 till now. The user can then define how much they want to invest in each company by number of shares, so if they want to buy 1 share a week, or 2 shares a month, they can input these variables into the indicator to draw conclusions. As many brokers are also now permitting fractional share trading, this ability is also integrated into the indicator. So for shares, you can put in, say, 0.25 shares of SPY and the indicator will accept this and account for this fractional share.

The indicator will then show you a portfolio summary of what your earnings and returns would be for the defined period. It will provide a percent return as well as the projected P&L based on your desired investment amount and frequency.

But it goes beyond just that, you can also have the indicator display a simple forecasting projection of the portfolio. It will show the projected P&L and % Return over various periods in time on each of the ticker (see image below):

The indicator will also break down your portfolio allocation, it will show where the majority of your holdings are and where the majority of your P&L in coming from (best performers will show a green fill and worst will show a red fill, see image below):

This colour coding also extends to the portfolio breakdown itself.

Dollar cost averaging (DCA) is incorporated into the indicator itself, by assuming ongoing contributions. If you want to stop contributions at a certain point, you just select your end time for contributions at the point in which you would stop contributing.

The indicator also provides some basic fundamental information about the company tickers (if applicable). Simply select the "Fundamental" chart and it will display a breakdown of the fundamentals, including dividends paid, market cap and earnings yield:

The indicator also provides a correlation assessment of each holding against each other holding. This emphasizes the profound role of diversification on portfolios. The less correlation you have in your portfolio among your holdings, the better diversified you are. As well, if you have holdings that are perfectly inverse other holdings, you have a pseudo hedge against the downturn of one of your holdings. This is even more helpful if the inverse is a company with solid fundamentals.

In the below example you will see NASDAQ:IRDM in the portfolio. You will be able to see that NASDAQ:IRDM has a slight inverse relationship to SPY:

Yet IRDM has solid fundamentals and is performing well fundamentally. Thus, this makes IRDIM a solid addition to your portfolio as it can potentially hedge against a downturn for SPY and is less risky than simply holding an inverse leveraged share on SPY which is most likely just going to cost you money than make you money.

Concluding remarks:

There are many fun and interesting things you can do with this indicator and I encourage you to try it out and have fun with it! The overall objective with the indicator is to help you plan for your portfolio and not necessarily to manage your portfolio. If you have a few stocks you are looking at and contemplating investing in, this will help you run some theoretical scenarios with this stock based on historical performance and also help give you a feel of how it will perform in the future based on past behaviour.

It is important to remember that past behaviour does not indicate future behaviour, but the indicator provides you with tools to get a feel for how a stock has performed under various circumstances and get a general feel of the fundamentals of the company you could potentially be investing in.

Please note, this indicator is not meant to replace full, fundamental analyses of individual companies. It is simply meant to give you a "gist" of how companies are fundamentally and how they have performed historically.

I hope you enjoy it!

Safe trades everyone!

Price & Volume Profile (Expo)█ Overview

The Price & Volume Profile provides a holistic perspective on market dynamics by simultaneously tracking price action and trading volume across a range of price levels. So it is not only a volume-based indicator but also a price-based one. In addition to illustrating volume distribution, it quantifies how frequently the price has fallen within a particular range, thus offering a holistic perspective on market dynamics.

This unique and comprehensive approach to market analysis by considering both price action and trading volume, two crucial dimensions of market activity. Its distinctive methodology offers several advantages:

Holistic Market View: By simultaneously tracking the frequency of specific price ranges (Price Profile) and the volume traded at those ranges (Volume Profile), this indicator provides a more complete picture of market behavior. It shows not only where the market is trading but also how much it's trading, reflecting both price acceptance levels and market participation intensity.

Point of Control (POC): The POC, as highlighted by this indicator, serves as a significant reference point for traders. It identifies the price level with the highest trading activity, thus indicating a strong consensus among market participants about the asset's fair value. Observing how price interacts with the POC can offer valuable insights into market sentiment and potential trend reversals.

Support and Resistance Levels: Price levels with high trading activity often act as support or resistance in future price movements. The indicator visually represents these levels, enabling traders to anticipate potential price reactions.

Price Profile

Price and Volume Profile

█ Calculations

The algorithm analyzes both trade frequency and volume across different price levels. It identifies these levels within the visible chart range, then examines each bar to determine if the selected price falls within these levels. If so, it increases a counter and adds the trading volume. This process repeats across the visible range and is visualized as a horizontal histogram, each bar representing a price level and the bar length reflecting trade frequency and volume. Additionally, it calculates the Point of Control (POC), signifying the price level with the highest activity.

In summary: The histogram presents a dual perspective - not only the traded volume at each price level but also the frequency of the price hitting each range. The longer the bar, the more times the price has frequented that specific range, revealing key insights into price behavior and acceptance levels. These frequently visited areas often emerge as strong support or resistance zones, helping traders navigate market movements.

Please note that the indicator adjusts to the visible price range, making it adaptable to changing market conditions. This dynamic analysis can provide more relevant and timely information than static indicators.

█ How to use

This indicator is beneficial for traders as it offers insights into the distribution of trading activity across different price levels. It helps identify key areas of support and resistance and gives a visual representation of market sentiment and liquidity.

The point of control (POC) , which is the price level with the highest traded volume or frequency count, becomes even more crucial in this context. It marks the price at which the most trading activity occurred, signaling a strong consensus among market participants about the asset's fair value. If the market price deviates significantly from the POC, it could suggest an overbought or oversold condition, potentially leading to a price reversion.

Fair Price Areas/gaps are specific price levels or zones where an asset has spent limited time in the past. These areas are considered interesting or significant because they may have an impact on future price action.

Similar to the concept of fair value gaps, which refers to discrepancies between an asset's market price and its estimated intrinsic value, Fair Price Areas/gaps focus on price levels that have been relatively underutilized in terms of trading activity. When an asset's price reaches a Fair Price Area/gap, traders and investors pay attention because they expect the price to react in some way. The rationale behind this concept is that price tends to gravitate towards areas where it has spent less time in the past, as the market perceives them as significant levels.

█ Settings

The indicator is customizable, allowing users to define the number of price levels (rows), the offset, the data source, and whether to display volume or frequency count. It also adjusts dynamically to the visible price range on the chart, ensuring that the analysis remains relevant and timely with changing market conditions.

Source: The price to use for the calculation. Typically, this is the closing price. By considering the user-selected Source (typically the closing price), the indicator determines the frequency with which the price lands within each designated price level (row) over the selected period. In essence, the indicator provides a count of bars where the Source price falls within each range, essentially creating a "Price Profile."

Row Size: The number of price levels (rows) to divide the visible price range into.

Display: Choose whether to display the number of bars ("Counter") or the total volume ("Volume") for each price level.

Offset: The distance of the histogram from the price chart.

Point of Control (POC): If enabled, the indicator will highlight the price level with the most activity.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Multi Kernel Regression [ChartPrime]The "Multi Kernel Regression" is a versatile trading indicator that provides graphical interpretations of market trends by using different kernel regression methods. It's beneficial because it smoothes out price data, creating a clearer picture of price movements, and can be tailored according to the user's preference with various options.

What makes this indicator uniquely versatile is the 'Kernel Select' feature, which allows you to choose from a variety of regression kernel types, such as Gaussian, Logistic, Cosine, and many more. In fact, you have 17 options in total, making this an adaptable tool for diverse market contexts.

The bandwidth input parameter directly affects the smoothness of the regression line. While a lower value will make the line more sensitive to price changes by sticking closely to the actual prices, a higher value will smooth out the line even further by placing more emphasis on distant prices.

It's worth noting that the indicator's 'Repaint' function, which re-estimates work according to the most recent data, is not a deficiency or a flaw. Instead, it’s a crucial part of its functionality, updating the regression line with the most recent data, ensuring the indicator measurements remain as accurate as possible. We have however included a non-repaint feature that provides fixed calculations, creating a steady line that does not change once it has been plotted, for a different perspective on market trends.

This indicator also allows you to customize the line color, style, and width, allowing you to seamlessly integrate it into your existing chart setup. With labels indicating potential market turn points, you can stay on top of significant price movements.

Repaint : Enabling this allows the estimator to repaint to maintain accuracy as new data comes in.

Kernel Select : This option allows you to select from an array of kernel types such as Triangular, Gaussian, Logistic, etc. Each kernel has a unique weight function which influences how the regression line is calculated.

Bandwidth : This input, a scalar value, controls the regression line's sensitivity towards the price changes. A lower value makes the regression line more sensitive (closer to price) and higher value makes it smoother.

Source : Here you denote which price the indicator should consider for calculation. Traditionally, this is set as the close price.

Deviation : Adjust this to change the distance of the channel from the regression line. Higher values widen the channel, lower values make it smaller.

Line Style : This provides options to adjust the visual style of the regression lines. Options include Solid, Dotted, and Dashed.

Labels : Enabling this introduces markers at points where the market direction switches. Adjust the label size to suit your preference.

Colors : Customize color schemes for bullish and bearish trends along with the text color to match your chart setup.

Kernel regression, the technique behind the Multi Kernel Regression Indicator, has a rich history rooted in the world of statistical analysis and machine learning.

The origins of kernel regression are linked to the work of Emanuel Parzen in the 1960s. He was a pioneer in the development of nonparametric statistics, a domain where kernel regression plays a critical role. Although originally developed for the field of probability, these methods quickly found application in various other scientific disciplines, notably in econometrics and finance.

Kernel regression became really popular in the 1980s and 1990s along with the rise of other nonparametric techniques, like local regression and spline smoothing. It was during this time that kernel regression methods were extensively studied and widely applied in the fields of machine learning and data science.

What makes the kernel regression ideal for various statistical tasks, including financial market analysis, is its flexibility. Unlike linear regression, which assumes a specific functional form for the relationship between the independent and dependent variables, kernel regression makes no such assumptions. It creates a smooth curve fit to the data, which makes it extremely useful in capturing complex relationships in data.

In the context of stock market analysis, kernel regression techniques came into use in the late 20th century as computational power improved and these techniques could be more easily applied. Since then, they have played a fundamental role in financial market modeling, market prediction, and the development of trading indicators, like the Multi Kernel Regression Indicator.

Today, the use of kernel regression has solidified its place in the world of trading and market analysis, being widely recognized as one of the most effective methods for capturing and visualizing market trends.

The Multi Kernel Regression Indicator is built upon kernel regression, a versatile statistical method pioneered by Emanuel Parzen in the 1960s and subsequently refined for financial market analysis. It provides a robust and flexible approach to capturing complex market data relationships.

This indicator is more than just a charting tool; it reflects the power of computational trading methods, combining statistical robustness with visual versatility. It's an invaluable asset for traders, capturing and interpreting complex market trends while integrating seamlessly into diverse trading scenarios.

In summary, the Multi Kernel Regression Indicator stands as a testament to kernel regression's historic legacy, modern computational power, and contemporary trading insight.

Trend Correlation HeatmapHello everyone!

I am excited to release my trend correlation heatmap, or trend heatmap for short.

Per usual, I think its important to explain the theory before we get into the use of the indicator, so let's get into the theory!

The theory:

So what is a correlation?

Correlation is the relationship one variable has to another. Correlations are the basis of everything I do as a quantitative trader. From the correlation between the same variables (i.e. autocorrelation), the correlation between other variables (i.e. VIX and SPY, SPY High and SPY Low, DXY and ES1! close, etc.) and, as well, the correlation between price and time (time series correlation).

This may sound very familiar to you, especially if you are a user, observer or follower of my ideas and/or indicators. Ninety-five percent of my indicators are a function of one of those three things. Whether it be a time series based indicator (i.e.my time series indicator), whether it be autocorrelation (my autoregressive cloud indicator or my autocorrelation oscillator) or whether it be regressive in nature (i.e. my SPY Volume weighted close, or even my expected move which uses averages in lieu of regressive approaches but is foundational in regression principles. Or even my VIX oscillator which relies on the premise of correlations between tickers.) So correlation is extremely important to me and while its true I am more of a regression trader than anything, I would argue that I am more of a correlation trader, because correlations are the backbone of how I develop math models of stocks.

What I am trying to stress here is the importance of correlations. They really truly are foundational to any type of quantitative analysis for stocks. And as such, understanding the current relationship a stock has to time is pivotal for any meaningful analysis to be conducted.

So what is correlation to time and what does it tell us?

Correlation to time, otherwise known and commonly referred to as "Time Series", is the relationship a ticker's price has to the passing of time. It is displayed in the traditional Pearson Correlation Coefficient or R value and can be any value from -1 (strong negative relationship, i.e. a strong downtrend) to + 1 (i.e. a strong positive relationship, i.e. a strong uptrend). The higher or lower the value the stronger the up or downtrend is.

As such, correlation to time tells us two very important things. These are:

a) The direction of the stock; and

b) The strength of the trend.

Let's take a look at an example:

Above we have a chart of QQQ. We can see a trendline that seems to fit well. The questions we ask as traders are:

1. What is the likelihood QQQ breaks down from this trendline?

2. What is the likelihood QQQ continues up?

3. What is the likelihood QQQ does a false breakdown?

There are numerous mathematical approaches we can take to answer these questions. For example, 1 and 2 can be answered by use of a Cumulative Distribution Density analysis (CDDA) or even a linear or loglinear regression analysis and 3 can be answered, more or less, with a linear regression analysis and standard error ascertainment, or even just a general comparison using a data science approach (such as cosine similarity or Manhattan distance).

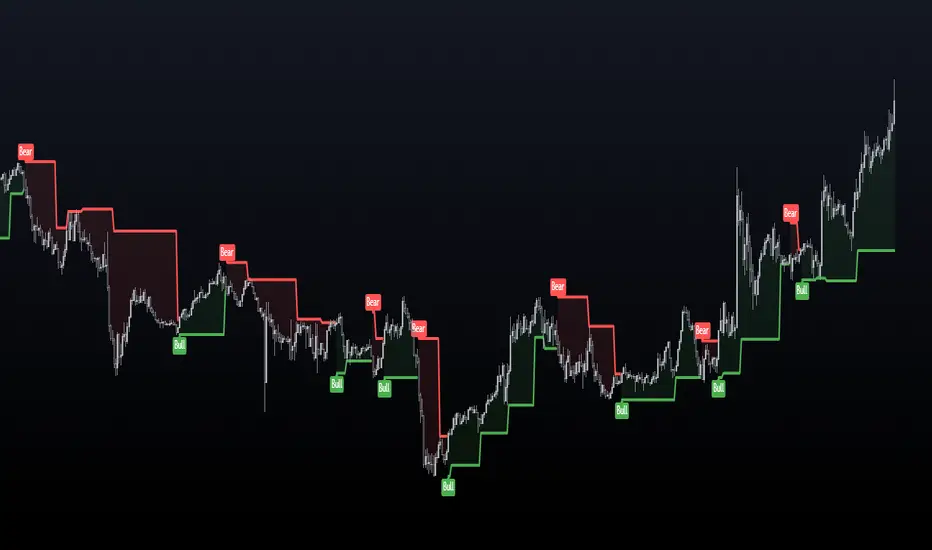

But, the reality is, all 3 of these questions can be visualized, at least in some way, by simply looking at the correlation to time. Let's look at this chart again, this time with the correlation heatmap applied:

If we look at the indicator we can see some pivotal things. These are:

1. We have 4, very strong uptrends that span both higher AND lower timeframes. We have a strong uptrend of 0.96 on the 5 minute, 50 candle period. We have a strong uptrend at the 300 candle lookback period on the 1 minute, we have a strong uptrend on the 100 day lookback on the daily timeframe period and we have a strong uptrend on the 5 minute on the 500 candle lookback period.

2. By comparison, we have 3 downtrends, all of which have correlations less than the 4 uptrends. All of the downtrends have a correlation above -0.8 (which we would want lower than -0.8 to be very strong), and all of the uptrends are greater than + 0.80.

3. We can also see that the uptrends are not confined to the smaller timeframes. We have multiple uptrends on multiple timeframes and both short term (50 to 100 candles) and long term (up to 500 candles).

4. The overall trend is strengthening to the upside manifested by a positive Max Change and a Positive Min change (to be discussed later more in-depth).

With this, we can see that QQQ is actually very strong and likely will continue at least some upside. If we let this play out:

We continued up, had one test and then bounced.

Now, I want to specify, this indicator is not a panacea for all trading. And in relation to the 3 questions posed, they are best answered, at least quantitatively, not only by correlation but also by the aforementioned methods (CDDA, etc.) but correlation will help you get a feel for the strength or weakness present with a stock.

What are some tangible applications of the indicator?

For me, this indicator is used in many ways. Let me outline some ways I generally apply this indicator in my day and swing trading:

1. Gauging the strength of the stock: The indictor tells you the most prevalent behavior of the stock. Are there more downtrends than uptrends present? Are the downtrends present on the larger timeframes vs uptrends on the shorter indicating a possible bullish reversal? or vice versa? Are the trends strengthening or weakening? All of these things can be visualized with the indicator.

2. Setting parameters for other indicators: If you trade EMAs or SMAs, you may have a "one size fits all" approach. However, its actually better to adjust your EMA or SMA length to the actual trend itself. Take a look at this:

This is QQQ on the 1 hour with the 200 EMA with 200 standard deviation bands added. If we look at the heatmap, we can see, yes indeed 200 has a fairly strong uptrend correlation of 0.70. But the strongest hourly uptrend is actually at 400 candles, with a correlation of 0.91. So what happens if we change the EMA length and standard deviation to 400? This:

The exact areas are circled and colour coded. You can see, the 400 offers more of a better reference point of supports and resistances as well as a better overall trend fit. And this is why I never advocate for getting married to a specific EMA. If you are an EMA 200 lover or 21 or 51, know that these are not always the best depending on the trend and situation.

Components of the indicator:

Ah okay, now for the boring stuff. Let's go over the functionality of the indicator. I tried to keep it simple, so it is pretty straight forward. If we open the menu here are our options:

We have the ability to toggle whichever timeframes we want. We also have the ability to toggle on or off the legend that displays the colour codes and the Max and Min highest change.

Max and Min highest change: The max and min highest change simply display the change in correlation over the previous 14 candles. An increasing Max change means that the Max trend is strengthening. If we see an increasing Max change and an increasing Min change (the Min correlation is moving up), this means the stock is bullish. Why? Because the min (i.e. ideally a big negative number) is going up closer to the positives. Therefore, the downtrend is weakening.

If we see both the Max and Min declining (red), that means the uptrend is weakening and downtrend is strengthening. Here are some examples:

Final Thoughts:

And that is the indicator and the theory behind the indicator.

In a nutshell, to summarize, the indicator simply tracks the correlation of a ticker to time on multiple timeframes. This will allow you to make judgements about strength, sentiment and also help you adjust which tools and timeframes you are using to perform your analyses.

As well, to make the indicator more user friendly, I tried to make the colours distinctively different. I was going to do different shades but it was a little difficult to visualize. As such, I have included a toggle-able legend with a breakdown of the colour codes!

That's it my friends, I hope you find it useful!

Safe trades and leave your questions, comments and feedback below!

Swing Volume Profiles [LuxAlgo]The Swing Volume Profiles indicator aims to calculate and highlight trading activity at specific price levels between two swing points; allowing traders to reveal dominant and/or significant price levels based on volume.

By measuring traded volume at all price levels in the market over a specified time period, the script can also be used to detect some key analysis generally such as supply & demand, buy-side & sell-side liquidity levels, unfilled liquidity voids, and imbalances that can highlight on the chart.

🔶 USAGE

A volume profile is an advanced charting tool that displays the traded volume at different price levels over a specific period. It helps you visualize where the majority of trading activity has occurred.

Key Levels are the areas where the volume is concentrated or where there are significant volume spikes. These levels are known as key support and resistance levels. High-volume nodes indicate areas of high activity and are likely to act as support or resistance in the future.

Volume profile also helps identify value areas, which represent the price levels where the most trading activity has taken place. These levels can act as areas of support or resistance as traders perceive them as fair value.

The Point of Control describes the price level where the most volume was traded. A Naked Point of Control (also called a Virgin Point of Control) is a previous POC that has not been traded. Extending PoC options 'Until Bar Cross' or 'Until Bar Touch' helps in identifying Naked Point of Control Lines.

Previous PoC levels can serve as support and resistance for future price movements. Extending PoC Level 'Until Last Bar' option will help to identify such levels.

🔶 DETAILS

One of the unique features of the script is its ability to detect some other key levels such as levels of acceptance and rejection.

Levels of rejection we may summarize as supply and demand levels, these are also referred to as buy-side and sell-side liquidity levels. They usually occur at extreme highs or lows, where prices may be too high for buyers (high supply, low demand) or too low for sellers (low supply, high demand)

Levels of acceptance are the levels where Liquidity Voids occur, these are also referred to imbalances. Liquidity voids are sudden changes in price when the price jumps from one level to another. The peculiar thing about liquidity voids is that they almost always fill up, so we call them levels of acceptance.

🔶 ALERTS

When an alert is configured, the user will have the ability to be notified in case:

Point Of Control Line is touched/crossed

Value Area High Line is touched/crossed

Value Area Low Line is touched/crossed

🔶 SETTINGS

🔹 Display Options

Mode: Controls the lookback length of detection and visualization, where Present assumes last X bars specifid in '# Bars' option and Historical assumes all data available to the user as well as allowed limits of visiual objects (boxs, lines, labels etc)

# Bars: Controls the lookback length.

🔹 Swing Volume Profiles

The script takes into account user-defined parameters and plots volume profiles. Due to Pine Script™ drwaing objects limit only total volume profiles are presented.

Swing Detection Length: Lookback period

Swing Volume Profiles: Toggles the visibility of the Volume Profiles, with color options to differentiate the Value Area within a profile.

Profile Range Background Fill: Toggles the visibility of the Volume Profiles Range

🔹 Point of Control (PoC)

Point of Control (POC) – The price level for the time period with the highest traded volume

Point of Control (PoC): Toggles the visibility of the Point of Control

Developing PoC: Toggles the visibility of the Developing PoC

Extend PoC: Option that allows detecting virgin PoC levels. Virgin Point of Control (VPoC) is defined as a Point of Control that has never been revisited or touched. The option also allows PoC levels to extend till the last bar aiming to present levels from history where the levels were traded significantly and those levels can be used as support and resistance levels.

🔹 Value Area (VA)

Value Area (VA) – The range of price levels in which the specified percentage of all volume was traded during the time period.

Value Area Volume %: Specifies percentage of the Value Area

Value Area High (VAH): Toggles the visibility of the Value Area High, the highest price level within the Value Area

Value Area Low (VAL): Toggles the visibility of the Value Area Low, the lowest price level within the Value Area

Value Area (VA) Background Fill: Toggles the visibility of the Value Area Range

🔹 Liquidity Levels / Voids

Unfilled Liquidity, Thresh: Enable display of the Unfilled Liquidity Levels and Liquidity Voids, where threshold value defines the significance of the level.

🔹 Profile Stats

Position, Size: Specifies the position and the size of the label presenting Profile Stats, the tooltip of the label includes all related info for each profile.

Price, Price Change, and Cumulative Volume: Enable display of the given options on the chart.

🔹 Volume Profile Others

Number of Rows: Specify how many rows each histogram will have. Caution, having it set to high values will quickly hit Pine Script™ drawing objects limit and may cause fewer historical profiles to be displayed.

Placement: Place profile either left or right.

Profile Width %: Alters the width of the rows in the histogram, relative to the calculated profile length.

🔶 RELATED SCRIPTS

Alternative Liquidity Void Detection script, Buyside-Sellside-Liquidity

5EMA BollingerBand Nifty Stock Scanner

What ?

We all heard about (well: over-heard) 5-EMA strategy. Which falls into the broader category of mean reversal type of trading setup.

What is mean reversal?

Price (or any time series, in fact) tries to follow a mean . Whenever price diverges from the mean it tries to meet it back.

It is empirically observed by some traders (I honestly don't know who first time observed it) that in Indian context specially, 5 Exponential Moving Average (5-EMA) works pretty good as that mean.

So whenever price moves away from that 5-EMA, it ultimately comes back and attain total nirvana :) Means: if price moved way higher than the 5EMA without touching it, then price will correct to meet it's 5-EMA and if price moved way lower, it will be uplifted to meet it's 5-EMA. Funny - but it works !

Now there are already enough social media coverage on this 5-EMA strategy/setup. Even TradingView has some excellent work done on these setups. Kudos to all those great souls.

So when we came to know about this, we were thinking what we should do for the community. Because it is well cover topic (specially in Indian context). Also, there are public indicators.

Then we thought why not come up with a scanner which will scan all the Nifty-50 constituent stocks and find out on the fly, real-time which all stocks are matching this 5-EMA setup and causing a Buy/Sell trade recommendation.

Hence here we are with the first version of our first scanner on the 5EMA setup (well it has some more masala than merely a 5-EMA setup).

Why?

Parts of why is already covered up.

Now instead of blindly following 5-EMA setup, we added the Bollinger band as well. Again: it's also not new. There are enough coverage in social media about the 5-EMA+BB strategy/setup. We mercilessly borrowed from all of these.

Suppose you have an indicator.

Now you apply the indicator in your chart. And then you need to (rock) and roll through your watchlist of Nifty-50 stocks (note: TradingView has no default watchlist of Nifty-50 stock by default - you have to create one custom watchlist to list all manually) to find out which all are matching the setup, need to take a note about the trade recomendations (entry, SL, target) and other stuffs like VWAP, Volume, volatility (Bollinger Band Width).

Not any more.

This scanner will track all the Nifty-50 stocks (technically: 40 stocks other than Banking stocks) and provide which one to Buy or Sell (if any), what's the entry, SL, target, where is the VWAP of the day, what's the picture in volume (high, low, rising, falling) and the implied volatility (using Bolling band width). Also it has a naive alerting mechanism as well.

In fact the code is there to monitor the (Future) OI also and all the OI drama (OI vs price and all the 4 stuffs like long build up, long unwinding, short covering, short buildup). But unfortunately, due to some limitations of the TradingView (that one can not monitor more than 40 `ta.security` call) we have to comment out the code. If you wish you can monitor only 20 stocks and enable the OI monitoring also (20 for stocks + 20 for their OI monitoring .. total 40 `ta.security` call).

How?

To know the divergence from 5-EMA we just check if the high of the candle (on closing) is below the 5-EMA. Then we check if the closing is inside the Bollinger Band (BB). That's a Buy signal. SL: low of the candle, T: middle and higher BB.

Just opposite for selling. 5-EMA low should be above 5-EMA and closing should be inside BB (lesser than BB higher level). That's a Sell signal. SL: high of the candle, T: middle and lower BB.

Along with we compare the current bar's volume with the last-20 bar VWMA (volume weighted moving average) to determine if the volume is high or low.

Present bar's volume is compared with the previous bar's volume to know if it's rising or falling.

VWAP is also determined using `ta.vwap` built-in support of TradingView.

The Bolling Band width is also notified, along with whether it is rising or falling (comparing with previous candle).

Simple, but effective.

Customization

As usual the EMA setup (5 default), the BB setup (20 SMA with 1.5 standard deviation), we provided option wherther to include or exclude BB role in the 5-EMA setup (as we found out there are two schools of thought .. some people use BB some don't. Lets make all happy :))

We also provide options to choose other symbols using Settings if they wish so. We have the default 40 non banking Nifty stocks (why non-banking? - Bank Nifty is in ATH :) .. enough :)). But if user wishes can monitor others too (provided the symbol is there in TradingView).

Although we strongly recommend the timeframe as 30 minutes , you can choose what's fit you most.

The output of the scanner is a table. By default the table is placed in the right-bottom (as we are most comfortable with that). However you can change per your wish. We have the option to choose that.

What is unique in it ?

This is more of an indicator. This is a scanner (of Nifty-50 stocks). So you can apply (our recommendation is in 30m timeframe) it to any chart (does not matter which chart it is) and it will show every 30 mins (which is also configurable) which all stocks (along with trade levels) to Buy and Sell according to the setup.

It will ease your trading activity.

You can concentrate only on the execution, the filtering you can leave it to this one.

Limitations

There is a build in limitation of the TradingView platform is that one can call only upto 40 securities API. Not beyond that. So naturally we are constraint by that. Otherwise we could monitor 190 Nifty F&O stocks itself.

30m is the recommended timeframe. In very lower (say 5m) this script tends to go out of heap (out of memory). Please note that also.

How to trade using this?

Put any chart in 30m (recommended) timeframe.

Apply this screener from Indicators (shortcut to launch indicators is just type / in your keyboard).

This will provide the Buy (shown in green color) or Sell (shown in red color) recommendations in a table, at every 30m candle closing.

Note the volume and BB width as well.

Wait for at least 2 5-minutes candles to close above/below the recommended level .

Take the trade with the SL and target mentioned.

Mentions

@QuantNomad. The whole implementation concept we mercilessly borrowed from him, even some of his code snippet we took it (after asking him through one of his videos comment section and seeking explicit permission which he readily granted within an hour). Thank You sir @QuantNomad. Indebted to you.

Monika (Rawat) ji: for reviewing, correcting, providing real time examples during live market hours, often compromising her own trading activities, about the effectiveness and usefulness of this setup. Thank You madam ji. Indebted to you.

There are innumerable contents in social media about this. Don't even know whom all we checked. Thanks to all of them.

Happy Trading (in stocks - isn't enough of Indices already?)

Disclaimer

This piece of software does not come up with any warrantee or any rights of not changing it over the future course of time.

We are not responsible for any trading/investment decision you are taking out of the outcome of this indicator.

loggerLibrary "logger"

◼ Overview

A dual logging library for developers. Tradingview lacks logging capability. This library provides logging while developing your scripts and is to be used by developers when developing and debugging their scripts.

Using this library would potentially slow down you scripts. Hence, use this for debugging only. Once your code is as you would like it to be, remove the logging code.

◼︎ Usage (Console):

Console = A sleek single cell logging with a limit of 4096 characters. When you dont need a large logging capability.

//@version=5

indicator("demo.Console", overlay=true)

plot(na)

import GETpacman/logger/1 as logger

var console = logger.log.new()

console.init() // init() should be called as first line after variable declaration

console.FrameColor:=color.green

console.log('\n')

console.log('\n')

console.log('Hello World')

console.log('\n')

console.log('\n')

console.ShowStatusBar:=true

console.StatusBarAtBottom:=true

console.FrameColor:=color.blue //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

console.ShowHeader:=false //this wont throw error but is not used for console

console.show(position=position.bottom_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Usage (Logx):

Logx = Multiple columns logging with a limit of 4096 characters each message. When you need to log large number of messages.

//@version=5

indicator("demo.Logx", overlay=true)

plot(na)

import GETpacman/logger/1 as logger

var logx = logger.log.new()

logx.init() // init() should be called as first line after variable declaration

logx.FrameColor:=color.green

logx.log('\n')

logx.log('\n')

logx.log('Hello World')

logx.log('\n')

logx.log('\n')

logx.ShowStatusBar:=true

logx.StatusBarAtBottom:=true

logx.ShowQ3:=false

logx.ShowQ4:=false

logx.ShowQ5:=false

logx.ShowQ6:=false

logx.FrameColor:=color.olive //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

logx.show(position=position.top_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Fields (with default settings)

▶︎ IsConsole = True Log will act as Console if true, otherwise it will act as Logx

▶︎ ShowHeader = True (Log only) Will show a header at top or bottom of logx.

▶︎ HeaderAtTop = True (Log only) Will show the header at the top, or bottom if false, if ShowHeader is true.

▶︎ ShowStatusBar = True Will show a status bar at the bottom

▶︎ StatusBarAtBottom = True Will show the status bar at the bottom, or top if false, if ShowHeader is true.

▶︎ ShowMetaStatus = True Will show the meta info within status bar (Current Bar, characters left in console, Paging On Every Bar, Console dumped data etc)

▶︎ ShowBarIndex = True Logx will show column for Bar Index when the message was logged. Console will add Bar index at the front of logged messages

▶︎ ShowDateTime = True Logx will show column for Date/Time passed with the logged message logged. Console will add Date/Time at the front of logged messages

▶︎ ShowLogLevels = True Logx will show column for Log levels corresponding to error codes. Console will log levels in the status bar

▶︎ ReplaceWithErrorCodes = True (Log only) Logx will show error codes instead of log levels, if ShowLogLevels is switched on

▶︎ RestrictLevelsToKey7 = True Log levels will be restricted to Ley 7 codes - TRACE, DEBUG, INFO, WARNING, ERROR, CRITICAL, FATAL

▶︎ ShowQ1 = True (Log only) Show the column for Q1

▶︎ ShowQ2 = True (Log only) Show the column for Q2

▶︎ ShowQ3 = True (Log only) Show the column for Q3

▶︎ ShowQ4 = True (Log only) Show the column for Q4

▶︎ ShowQ5 = True (Log only) Show the column for Q5

▶︎ ShowQ6 = True (Log only) Show the column for Q6

▶︎ ColorText = True Log/Console will color text as per error codes

▶︎ HighlightText = True Log/Console will highlight text (like denoting) as per error codes

▶︎ AutoMerge = True (Log only) Merge the queues towards the right if there is no data in those queues.

▶︎ PageOnEveryBar = True Clear data from previous bars on each new bar, in conjuction with PageHistory setting.

▶︎ MoveLogUp = True Move log in up direction. Setting to false will push logs down.

▶︎ MarkNewBar = True On each change of bar, add a marker to show the bar has changed

▶︎ PrefixLogLevel = True (Console only) Prefix all messages with the log level corresponding to error code.

▶︎ MinWidth = 40 Set the minimum width needed to be seen. Prevents logx/console shrinking below these number of characters.

▶︎ TabSizeQ1 = 0 If set to more than one, the messages on Q1 or Console messages will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ2 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ3 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ4 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ5 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ6 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ PageHistory = 0 Used with PageOnEveryBar. Determines how many historial pages to keep.

▶︎ HeaderQbarIndex = 'Bar#' (Logx only) The header to show for Bar Index

▶︎ HeaderQdateTime = 'Date' (Logx only) The header to show for Date/Time

▶︎ HeaderQerrorCode = 'eCode' (Logx only) The header to show for Error Codes

▶︎ HeaderQlogLevel = 'State' (Logx only) The header to show for Log Level

▶︎ HeaderQ1 = 'h.Q1' (Logx only) The header to show for Q1

▶︎ HeaderQ2 = 'h.Q2' (Logx only) The header to show for Q2

▶︎ HeaderQ3 = 'h.Q3' (Logx only) The header to show for Q3

▶︎ HeaderQ4 = 'h.Q4' (Logx only) The header to show for Q4

▶︎ HeaderQ5 = 'h.Q5' (Logx only) The header to show for Q5

▶︎ HeaderQ6 = 'h.Q6' (Logx only) The header to show for Q6

▶︎ Status = '' Set the status to this text.

▶︎ HeaderColor Set the color for the header

▶︎ HeaderColorBG Set the background color for the header

▶︎ StatusColor Set the color for the status bar

▶︎ StatusColorBG Set the background color for the status bar

▶︎ TextColor Set the color for the text used without error code or code 0.

▶︎ TextColorBG Set the background color for the text used without error code or code 0.

▶︎ FrameColor Set the color for the frame around Logx/Console

▶︎ FrameSize = 1 Set the size of the frame around Logx/Console

▶︎ CellBorderSize = 0 Set the size of the border around cells.

▶︎ CellBorderColor Set the color for the border around cells within Logx/Console

▶︎ SeparatorColor = gray Set the color of separate in between Console/Logx Attachment

◼︎ Methods (summary)

● init ▶︎ Initialise the log

● log ▶︎ Log the messages. Use method show to display the messages

● page ▶︎ Clear messages from previous bar while logging messages on this bar.

● show ▶︎ Shows a table displaying the logged messages

● clear ▶︎ Clears the log of all messages

● resize ▶︎ Resizes the log. If size is for reduction then oldest messages are lost first.

● turnPage ▶︎ When called, all messages marked with previous page, or from start are cleared

● dateTimeFormat ▶︎ Sets the date time format to be used when displaying date/time info.

● resetTextColor ▶︎ Reset Text Color to library default

● resetTextBGcolor ▶︎ Reset Text BG Color to library default

● resetHeaderColor ▶︎ Reset Header Color to library default

● resetHeaderBGcolor ▶︎ Reset Header BG Color to library default

● resetStatusColor ▶︎ Reset Status Color to library default

● resetStatusBGcolor ▶︎ Reset Status BG Color to library default

● setColors ▶︎ Sets the colors to be used for corresponding error codes

● setColorsBG ▶︎ Sets the background colors to be used for corresponding error codes. If not match of error code, then text color used.

● setColorsHC ▶︎ Sets the highlight colors to be used for corresponding error codes.If not match of error code, then text bg color used.

● resetColors ▶︎ Reset the colors to library default (Total 36, not including error code 0)

● resetColorsBG ▶︎ Reset the background colors to library default

● resetColorsHC ▶︎ Reset the highlight colors to library default

● setLevelNames ▶︎ Set the log level names to be used for corresponding error codes. If not match of error code, then empty string used.

● resetLevelNames ▶︎ Reset the log level names to library default. (Total 36) 1=TRACE, 2=DEBUG, 3=INFO, 4=WARNING, 5=ERROR, 6=CRITICAL, 7=FATAL

● attach ▶︎ Attaches a console to an existing Logx, allowing to have dual logging system independent of each other

● detach ▶︎ Detaches an already attached console from Logx

method clear(this)

Clears all the queue, including bar_index and time queues, of existing messages

Namespace types: log

Parameters:

this (log)

method resize(this, rows)

Resizes the message queues. If size is decreased then removes the oldest messages

Namespace types: log

Parameters:

this (log)

rows (int) : The new size needed for the queues. Default value is 40.

method dateTimeFormat(this, format)

Re/set the date time format used for displaying date and time. Default resets to dd.MMM.yy HH:mm

Namespace types: log

Parameters:

this (log)

format (string)

method resetTextColor(this)

Resets the text color of the log to library default.

Namespace types: log

Parameters:

this (log)

method resetTextColorBG(this)

Resets the background color of the log to library default.

Namespace types: log

Parameters:

this (log)

method resetHeaderColor(this)

Resets the color used for Headers, to library default.

Namespace types: log

Parameters:

this (log)

method resetHeaderColorBG(this)

Resets the background color used for Headers, to library default.

Namespace types: log

Parameters:

this (log)

method resetStatusColor(this)

Resets the text color of the status row, to library default.

Namespace types: log

Parameters:

this (log)

method resetStatusColorBG(this)

Resets the background color of the status row, to library default.

Namespace types: log

Parameters:

this (log)

method resetFrameColor(this)

Resets the color used for the frame around the log table, to library default.

Namespace types: log

Parameters:

this (log)

method resetColorsHC(this)

Resets the color used for the highlighting when Highlight Text option is used, to library default

Namespace types: log

Parameters:

this (log)

method resetColorsBG(this)

Resets the background color used for setting the background color, when the Color Text option is used, to library default

Namespace types: log

Parameters:

this (log)

method resetColors(this)

Resets the color used for respective error codes, when the Color Text option is used, to library default

Namespace types: log

Parameters:

this (log)

method setColors(this, c)

Sets the colors corresponding to error codes

Index 0 of input array c is color is reserved for future use.

Index 1 of input array c is color for debug code 1.

Index 2 of input array c is color for debug code 2.

There are 2 modes of coloring

1 . Using the Foreground color

2 . Using the Foreground color as background color and a white/black/gray color as foreground color

This is denoting or highlighting. Which effectively puts the foreground color as background color

Namespace types: log

Parameters:

this (log)

c (color ) : Array of colors to be used for corresponding error codes. If the corresponding code is not found, then text color is used

method setColorsHC(this, c)

Sets the highlight colors corresponding to error codes

Index 0 of input array c is color is reserved for future use.

Index 1 of input array c is color for debug code 1.

Index 2 of input array c is color for debug code 2.

There are 2 modes of coloring

1 . Using the Foreground color

2 . Using the Foreground color as background color and a white/black/gray color as foreground color

This is denoting or highlighting. Which effectively puts the foreground color as background color

Namespace types: log

Parameters:

this (log)

c (color ) : Array of highlight colors to be used for corresponding error codes. If the corresponding code is not found, then text color BG is used

method setColorsBG(this, c)

Sets the highlight colors corresponding to debug codes

Index 0 of input array c is color is reserved for future use.

Index 1 of input array c is color for debug code 1.

Index 2 of input array c is color for debug code 2.

There are 2 modes of coloring

1 . Using the Foreground color

2 . Using the Foreground color as background color and a white/black/gray color as foreground color

This is denoting or highlighting. Which effectively puts the foreground color as background color

Namespace types: log

Parameters:

this (log)

c (color ) : Array of background colors to be used for corresponding error codes. If the corresponding code is not found, then text color BG is used

method resetLevelNames(this, prefix, suffix)

Resets the log level names used for corresponding error codes

With prefix/suffix, the default Level name will be like => prefix + Code + suffix

Namespace types: log

Parameters:

this (log)

prefix (string) : Prefix to use when resetting level names

suffix (string) : Suffix to use when resetting level names

method setLevelNames(this, names)

Resets the log level names used for corresponding error codes

Index 0 of input array names is reserved for future use.

Index 1 of input array names is name used for error code 1.

Index 2 of input array names is name used for error code 2.

Namespace types: log

Parameters:

this (log)

names (string ) : Array of log level names be used for corresponding error codes. If the corresponding code is not found, then an empty string is used

method init(this, rows, isConsole)

Sets up data for logging. It consists of 6 separate message queues, and 3 additional queues for bar index, time and log level/error code. Do not directly alter the contents, as library could break.

Namespace types: log

Parameters:

this (log)

rows (int) : Log size, excluding the header/status. Default value is 50.

isConsole (bool) : Whether to init the log as console or logx. True= as console, False = as Logx. Default is true, hence init as console.

method log(this, ec, m1, m2, m3, m4, m5, m6, tv, log)

Logs messages to the queues , including, time/date, bar_index, and error code

Namespace types: log

Parameters:

this (log)

ec (int) : Error/Code to be assigned.

m1 (string) : Message needed to be logged to Q1, or for console.

m2 (string) : Message needed to be logged to Q2. Not used/ignored when in console mode

m3 (string) : Message needed to be logged to Q3. Not used/ignored when in console mode

m4 (string) : Message needed to be logged to Q4. Not used/ignored when in console mode

m5 (string) : Message needed to be logged to Q5. Not used/ignored when in console mode

m6 (string) : Message needed to be logged to Q6. Not used/ignored when in console mode

tv (int) : Time to be used. Default value is time, which logs the start time of bar.

log (bool) : Whether to log the message or not. Default is true.

method page(this, ec, m1, m2, m3, m4, m5, m6, tv, page)

Logs messages to the queues , including, time/date, bar_index, and error code. All messages from previous bars are cleared

Namespace types: log

Parameters:

this (log)

ec (int) : Error/Code to be assigned.

m1 (string) : Message needed to be logged to Q1, or for console.

m2 (string) : Message needed to be logged to Q2. Not used/ignored when in console mode

m3 (string) : Message needed to be logged to Q3. Not used/ignored when in console mode

m4 (string) : Message needed to be logged to Q4. Not used/ignored when in console mode

m5 (string) : Message needed to be logged to Q5. Not used/ignored when in console mode

m6 (string) : Message needed to be logged to Q6. Not used/ignored when in console mode

tv (int) : Time to be used. Default value is time, which logs the start time of bar.

page (bool) : Whether to log the message or not. Default is true.

method turnPage(this, turn)

Set the messages to be on a new page, clearing messages from previous page.

This is not dependent on PageHisotry option, as this method simply just clears all the messages, like turning old pages to a new page.

Namespace types: log

Parameters:

this (log)

turn (bool)

method show(this, position, hhalign, hvalign, hsize, thalign, tvalign, tsize, show, attach)

Display Message Q, Index Q, Time Q, and Log Levels

All options for postion/alignment accept TV values, such as position.bottom_right, text.align_left, size.auto etc.

Namespace types: log

Parameters:

this (log)

position (string) : Position of the table used for displaying the messages. Default is Bottom Right.

hhalign (string) : Horizontal alignment of Header columns

hvalign (string) : Vertical alignment of Header columns

hsize (string) : Size of Header text Options

thalign (string) : Horizontal alignment of all messages

tvalign (string) : Vertical alignment of all messages

tsize (string) : Size of text across the table

show (bool) : Whether to display the logs or not. Default is true.

attach (log) : Console that has been attached via attach method. If na then console will not be shown

method attach(this, attach, position)

Attaches a console to Logx, or moves already attached console around Logx

All options for position/alignment accept TV values, such as position.bottom_right, text.align_left, size.auto etc.

Namespace types: log

Parameters:

this (log)

attach (log) : Console object that has been previously attached.

position (string) : Position of Console in relation to Logx. Can be Top, Right, Bottom, Left. Default is Bottom. If unknown specified then defaults to bottom.

method detach(this, attach)

Detaches the attached console from Logx.

All options for position/alignment accept TV values, such as position.bottom_right, text.align_left, size.auto etc.

Namespace types: log

Parameters:

this (log)

attach (log) : Console object that has been previously attached.

Daily Gaps & Trapped PositionsThis script builds substantially upon the default Gaps script provided by Tradingview. Functionality was added to allow users to decide what price from the previous session is used to determine a daily gap, added support for showing gaps across all timeframes up to the daily time frame, and also allow gaps to be shown even with ETH enabled on the chart. This script provides support across normal securities, futures, and also crypto.

Users can decide between the following selections to determine if a daily gap has formed:

- Previous Session Close

- Previous Session High/Low

- Last RTH Candle High/Low

The other larger piece that was added is something called trapped positions or what some folks familiar with Market Profile would call "single prints". They could also be considered FVGs but they are a specific subset of FVGs as these must from above or below the current session's high/low.

Single prints form above or below a current session's high/low and can be considered an area where price has moved too fast in that area and price will most likely return to these areas at a later point in time. In some teachings, these are also looked at as "trapped shorts" (lighter blue box color) or "trapped supply" (yellow orange box color) which creates an area where there will be potential support (trapped shorts) or resistance (trapped supply) when this area is revisited in the future. Adding these to your chart will simply provide additional areas of interest where you may see buying or selling.

Both gaps and trapped positions have the following options:

- Show only active gaps/trapped positions. Selecting this will only show areas where price has not completely traded through the box.

- Close gaps/trapped positions partially. If this is selected, it will reduce the box size as price is traded through the area. If it is not selected, the box will only disappear once price has traded through the entire box completely.

There are some additional settings that allow you to tailor how many boxes show up on the chart. These settings are as follows:

- Max number of boxes. This setting will only plot up to this number of gaps/trapped positions.

- Minimum Deviation. This will prevent gaps/trapped positions from showing if they are too small relative to average across that last 14 periods.

- Limit Max Box Trail Length (bars). If checkbox is selected, the box will stop being extended after X number of bars given in this input.

Multi Time Frame Normalized PriceEnhance Your Trading Experience with the Multi Time Frame Normalized Price Indicator

Introduction

As a trader, having a clear and informative chart is crucial for making informed decisions. In this post, we will introduce the Multi Time Frame Normalized Price (MTFNP) Indicator, an innovative trading tool that offers an insightful perspective on price action. The script creates a symmetric chart, with the time axis going from top to bottom, making it easier to identify potential tops and bottoms in various ranges. Let's dive deeper into this powerful tool to understand how it works and how it can improve your trading experience.

The Multi Time Frame Normalized Price Indicator

The MTFNP Indicator is designed to provide a comprehensive view of price action across multiple time frames. By plotting the normalized price levels for each time frame, traders can easily identify areas of support and resistance, as well as potential tops and bottoms in various ranges.

One of the key features of this indicator is the symmetry of the chart. Instead of the traditional horizontal time axis, the MTFNP Indicator plots the time axis vertically from top to bottom. This innovative approach makes it easier for traders to visualize the price action across different time frames, enabling them to make more informed decisions.

Benefits of a Symmetric Chart

There are several advantages to using a symmetric chart with a vertical time axis, such as:

Easier to read: The unique layout of the chart makes it easier to analyze price action across multiple time frames. The clear separation between each time frame helps traders avoid confusion and identify important price levels more effectively.

Identifying tops and bottoms: The symmetric presentation of price action enables traders to quickly spot potential tops and bottoms in various ranges. This can be particularly useful for identifying potential reversal points or areas of support and resistance.

Improved decision-making: By offering a comprehensive view of price action, the MTFNP Indicator helps traders make better-informed decisions. This can lead to improved trading strategies and ultimately, better results.

The MTFNP Indicator Script

The MTFNP Indicator script leverages several custom functions, including the Chebyshev Type I Moving Average, to provide a smooth and responsive signal. Additionally, the indicator uses the Spider Plot function to create a symmetric chart with the time axis going from top to bottom.

To customize the MTFNP Indicator to your preferences, you can adjust the input parameters, such as the standard deviation length, multiplier, axes color, bottom color, and top color. You can also change the scale to fit your desired chart size.

Exploring the Relationship between Min, Max Values and Time Frames

In the Multi Time Frame Normalized Price (MTFNP) script, it is crucial to understand the relationship between the min and max values across different time frames. By analyzing how these values relate to each other, traders can make more informed decisions about market trends and potential reversals. In this section, we will dive deep into the relationship between the current time frame's min and max values and those of the further-out time frames.

Interpreting Min and Max Values Across Time Frames

When analyzing the min and max values of the current time frame in relation to the further-out time frames, it is essential to keep in mind the following points: