[Pandora] Laguerre Ultimate Explorations MulticatorIt's time to begin demonstrations differentiating the difference between known and actual feasibility beyond imagination... Welcome to my algorithmic twilight zone .

INTRODUCTION:

Hot off my press, I present this Laguerre multicator employing PSv6.0, originally formulated by John Ehlers for TASC - July 2025 Traders Tips. Basically I transcended Ehlers' notions of transversal filtration with an overhaul of his Laguerre design with my "what if" Pandora notions included. Striving beyond John Ehlers' original intended design. This action packed indicator is a radically revamped version of his original filter using novel techniques. My aim was to explore whether providing even more enhanced responsiveness and lesser lag is possible and how. Presented here is my mind warping results to witness.

EHLERS' LAGUERRE EXPLAINED:

First and foremost, the concept of Ehlers' Laguerre-izing method deserves a comprehensive deep dive. Ehlers' Laguerre filter design, as it functions originally, begins with his Ultimate Smoother (US) followed by a gang of four LERP (jargon for Linear intERPolation) filters. Following a myriad of cascading LERPs is a window-like FIR filter tapped into the LERP delay values to provide extra smoothness via the output.

On a side note, damping factor controlled LERP filters resemble EMAs indeed, but aren't exactly "periodic" filters that would have a period/length parameter and their subsequent calculations. I won't go into fine-grained relationship details, but EMA and LERP are indeed related in approach, being cousins of similar pedigree.

EXAMINING LAGUERRE:

I focused firstly on US initialization obstacles at Pine's bar_index==0 with nz() in abundance. The next primary notion of intrigue I mostly wondered about was, why are there four LERP elements instead of fewer or more. Why not three or why not two LERPs, etc... 1-4-6-4-1, I remember seeing those coefficients before in high pass filters.

Gathering my thoughts from that highpass knowledge base, I devised other tapped configuration modes to inspect their behavior out of curiosity. Eureka! There is actually more to Laguerre than Ehlers' mind provided, now that I had formulated additional modes. Each mode exhibits it's own lag/smoothness characteristics better than the quad LERPed version. I narrowed it down to a total of 5 modes for exploration. Mode 0 is just the raw US by itself.

ANALYZING FILTER BEHAVIORS:

Which option might be possibly superior, and how may I determine that? Fortunately, I have a custom-built analyzer allowing me to thoroughly examine transient responses across multiple periodicities simultaneously, providing remarkable visual insights.

While Ehlers has meagerly touched upon presenting general frequency responses in his books, I have excelled far beyond that. This robust filter analysis capability enables me to observe finer aspects hidden to others, ultimately leading to the deprecation of numerous existing filters. Not only this, but inventing entirely new species of filtration whether lowpass, highpass, or bandpass is already possible with a thorough comprehensive evaluation.

Revealing what's quirky with each filter and having the ability to discover what filters may be lacking in performance, is one of it's implications. I'm just going to explain this: For example US has a little too much overshoot to my liking, along with nonconformant cutoff frequency compliance with the period parameter. Perhaps Ehlers should inspect US coefficients a bit closer... I hope stating this is not received in an ill manner, as it's not my intention here.

What this technically eludes to is that UltimateSmoother can be further improved, analogous to my Laguerre alterations described above. I will also state Laguerre can indeed be reformulated to an even greater extent concerning group delay, from what I have already discussed. Another exciting time though... More investigative research is warranted.

LAGUERRE CONCLUSIONS:

After analyzing Laguerre's frequency compliance, transient responses, amplitudes, lag, symmetry across periodicities, noise rejection, and smoothness... I favor mode 3 for a multitude of reasons over the mode 4 configuration, but mostly superb smoothing with less lag, AND I also appreciated mode 1 & 2 for it's lower lag performance options.

Each mode and lag (phase shift) damping value has it's own unique characteristics at extremes, yet they demonstrate additional finesse in it's new hybrid form without adding too much more complexity. This multicator has a bunch of Laguerre filters in the overlay chart over many periodicities so you can easily witness it's differing periodic symmetries on an input signal while adjusting lag and mode.

LAGUERRE OSCILLATOR:

The oscillator is integrated into the laguerreMulti() function for the intention of posterity only. I performed no evaluation on it, only providing the code in Pine. That wasn't part of my intended exploration adventure, as I'm more TREND oriented for the time being, focusing my efforts there.

Market analysis has two primary aspects in my observations, one cyclic while the other is trending dynamics... There's endless oscillators, but my expectations for trend analysis seems a little lesser explored in my opinion, hence my laborious trend endeavors. Ehlers provided both indicator facets this time around, and I hope you find the filtration aspect more intriguing after absorption of this reading.

FUNCTION MODULES EXPLAINED:

The Ultimate Smoother is an advanced IIR lowpass smoothing filter intended to minimize noise in time series data with minimal group delay, similar to a traditional biquad filter. This calculation helps to create a smoother version of the original signal without the distortions of short-term fluctuations and with minimal lag, adjustable by period.

The Modified Laguerre Lowpass Filter (MLLF) enhances the functionality of US by introducing a Laguerre mode parameter along side the lag parameter to refine control over the amount of additional smoothing/lag applied to the signal. By tethering US with this LERPed lag mechanism, MLLF achieves an effective balance between responsiveness and smoothness, allowing for customizable lag adjustments via multiple inputs. This filter ends with selecting from a choice of weighted averages derived from a gang of up to four cascading LERP calculations, resulting with smoother representations of the data.

The Laguerre Oscillator is a momentum-like indicator derived from the output of US and a singular LERPed lowpass filter. It calculates the difference between the US data and Laguerre filter data, normalizing it by the root mean square (RMS). This quasi-normalization technique helps to assess the intensity of the momentum on any timeframe within an expected bound range centered around 0.0. When the Laguerre Oscillator is positive, it suggests that the smoothed data is trending upward, while a negative value indicates a downward trend. Adjustability is controlled with period, lag, Laguerre mode, and RMS period.

Pesquisar nos scripts por "ha溢价率"

Inflection PointInflection Point - The Adaptive Confluence Reversal Engine

This is not just another peak and valley indicator; it is a complete and total reimagining of how market turning points are detected, qualified, and acted upon. Born from the foundational concepts explored in systems like my earlier creation, DAFE - Turning Point, Inflection Point is a ground-up engineering feat designed for the modern trader. It moves beyond static rules and simple pattern recognition into the realm of dynamic, multi-factor confluence analysis and adaptive machine learning.

Where other indicators provide a guess, Inflection Point provides a probability. It meticulously analyzes the market's deepest currents—momentum, exhaustion, and reversal velocity—and fuses them into a single, unified "Confluence Score." This is not a simple combination of indicators; it is an intelligent, weighted system where each component works in concert, creating an analytical engine that is orders of magnitude more sophisticated and reliable than any standard reversal tool.

Furthermore, Inflection Point learns. Through its advanced Adaptive Learning Engine, it constantly monitors its own performance, adjusting its confidence and selectivity in real-time based on its recent success rate. This allows it to adapt its behavior to any security, on any timeframe, with remarkable success.

Theoretical Foundation - Confluence Core

Inflection Point's predictive power does not come from a single, magical formula. It comes from the intelligent synthesis of three critical market phenomena, weighted and scored in real-time to generate a single, high-conviction probability rating.

1. Factor One: Pre-Reversal Momentum State (RSI Analysis)

Instead of reacting to a simple RSI cross, Inflection Point proactively scans for the build-up of momentum that precedes a reversal.

• Formulaic Concept: It measures the highest RSI value over a lookback period for peaks and the lowest RSI for valleys. A signal is only considered valid if significant momentum has been established before the turn, indicating a stretched market condition ripe for reversal.

• Asymmetric Sophistication: The engine uses different, optimized thresholds for bull and bear momentum, recognizing that markets often fall faster than they rise.

2. Factor Two: Volatility Exhaustion (Bollinger Band Analysis)

A true reversal often occurs when price makes a final, exhaustive push into unsustainable territory.

• Formulaic Concept: The engine detects when price has significantly pierced the outer Bollinger Bands. This is not just a touch, but a statistical deviation from the mean that signals volatility exhaustion, where the energy for the current move is likely depleted.

3. Factor Three: Reversal Strength (Rate of Change Analysis)

The character of a reversal matters. A sharp, decisive turn is more significant than a slow, meandering one.

• Formulaic Concept: Using a short-term Rate of Change (ROC), the engine measures the velocity of the reversal itself. A higher ROC score adds significant weight to the final probability, confirming that the new direction has conviction.

4. The Final Calculation: The Adaptive Learning Engine

This is the system's "brain." It maintains a history of its past signals and calculates its real-time win rate. This hitRate is then used to generate an adaptiveMultiplier.

• Self-Correction: In "Quality Control" mode, a high win rate makes the indicator more selective, demanding a higher probability score to issue a signal, thereby protecting streaks. A lower win rate makes it slightly less selective to ensure it continues learning from new market conditions.

• The result is a system that is not static, but a living, breathing tool that adapts its personality to the unique rhythm of any chart.

Why Inflection Point is a Paradigm Shift

Inflection Point is fundamentally different from other reversal indicators for three key reasons:

Confluence Over Isolation: Standard indicators look at one thing (e.g., RSI > 70). Inflection Point simultaneously analyzes momentum, volatility, and velocity, understanding that true reversals are a product of multiple converging factors. It answers not just "if," but "why" a reversal is likely.

Probabilistic Over Binary: Other tools give you a simple "yes" or "no." Inflection Point provides a probability score from 0-100, allowing you to gauge the conviction of every potential signal. This empowers you to differentiate between a weak setup and an A+ opportunity.

Adaptive Over Static: Every other indicator uses the same rules forever. Inflection Point's Adaptive Engine means it is constantly refining its own logic based on what is actually working in the current market, on the specific asset you are trading. It is tailored to the now.

The Inputs Menu - Your Command Center

Every setting is a lever of control, allowing you to tune the engine to your precise trading style and market focus.

🧠 Neural Core Engine

Analysis Depth: This is the primary lookback for the Bollinger Band and other core calculations. A shorter depth makes the indicator faster and more sensitive, ideal for scalping. A longer depth makes it slower and more stable, ideal for swing trading.

Minimum Probability %: This is your master signal filter. It sets the minimum Confluence Score required to plot a signal. Higher values (85-95) will give you only the highest-conviction A+ setups. Lower values (70-80) will show more potential opportunities.

🤖 Adaptive Neural Learning

Enable Adaptive Learning Engine: Toggles the entire learning system. Disabling it will make the indicator's logic static.

Peak/Valley Success Threshold (ATR): This defines what constitutes a "successful" trade for the learning engine. A value of 1.5 means price must move 1.5x the ATR in your favor for the signal to be marked as a win. Adjust this to match your personal take-profit strategy.

Adaptive Mode: This dictates how the engine uses its hitRate. "Quality Control" is recommended for its intelligent filtering. "Aggressive" will always boost signal scores, useful for finding more setups in a known, trending environment.

Asymmetric Balance: Allows you to apply a "boost" to either peak (short) or valley (long) signals. If you find the market you're trading has stronger long reversals, you can increase the "Valley Signal Boost" to catch them more effectively.

🛡️ Elite Filters

Market Noise Filter: An exceptional tool for avoiding choppy markets. It counts the number of directional changes in the last 5 bars. If the market is whipping back and forth too much, it will block the signal. Lower the "Max Direction Changes" to be extremely selective.

Volume Filter: Requires signal confirmation from a significant volume spike. The "Volume Multiplier" dictates how large this spike must be (e.g., 1.2 = 20% above average volume). This is invaluable for filtering out low-conviction moves in stocks and crypto.

The Dashboard - Your Analytical Co-Pilot

The dashboard is not just a set of numbers; it is a holistic overview of the market's health and the engine's current state.

Unified AI Score: This section provides the most critical, at-a-glance information. "Total Score" is the current probability reading, while "Quality" gives you a human-readable interpretation. "Win Rate" shows the real-time performance of the Adaptive Engine.

Order Flow (OFPI): This measures the "weight" of money behind recent price moves by analyzing price change relative to volume. A high positive OFPI suggests strong buying pressure, while a high negative value suggests strong selling pressure. It gives you a peek into the market's underlying flow.

Component Analysis: This allows you to see the individual "Peak" and "Valley" confidence scores before they are filtered, giving you insight into building momentum before a signal forms.

Market Structure: This panel assesses the broader environment. "HTF Trend" tells you the direction of the larger trend (based on EMAs), while "Vol Regime" tells you if the market is in a high, medium, or low volatility state. Use this to align your signals with the broader market context.

Filter & Engine Statistics: Available on the "Large" dashboard, this provides deep insight into how many signals are being blocked by your filters and the current status of the Adaptive Engine's multiplier.

The Visual Interface - A Symphony of Data

Every visual element on the chart is designed for instant interpretation and insight.

Signal Markers: Simple, clean triangles mark the exact bar of a valid signal. A box is drawn around the high/low of the signal bar to highlight the precise point of inflection.

Dynamic Support/Resistance Zones: These are the glowing lines on your chart. They are not static lines; they are dynamic levels that represent the current battlefield between buyers and sellers.

Cyber Cyan (Valley Blue): This is the current Support Zone. This is the price level the market is currently trying to defend.

Neural Pink (Peak Red): This is the current Resistance Zone. This is the price level the market is currently trying to break through.

Grey (Next Level): This line is a projection, based on the current momentum and the size of the S/R range, of where the next major level of conflict will likely be. It acts as a potential price target.

Development & Philosophy

Inflection Point was not assembled; it was engineered. It represents hundreds of hours of research into market dynamics, statistical analysis, and machine learning principles. The goal was to create a tool that moves beyond the limitations of traditional technical analysis, which often fails in modern, algorithm-driven markets. By building a system based on multi-factor confluence and self-adaptive logic, Inflection Point provides a quantifiable, statistical edge that is simply unattainable with simpler tools. This is the result of a relentless pursuit of a better, more intelligent way to trade.

Universal Applicability

The principles of momentum, exhaustion, and velocity are universal to all freely traded markets. Because of its adaptive core and robust filtering options, Inflection Point has proven to be exceptionally effective on any security (stocks, crypto, forex, indices, futures) and on any timeframe (from 1-minute scalping charts to daily swing trading charts).

" Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected. "

— George Soros

Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

Volume Point of Control with Fib Based Profile🍀Description:

This indicator is a comprehensive volume profile analysis tool designed to identify key price levels based on trading activity within user-defined timeframes. It plots the Point of Control (POC), Value Area High (VAH), and Value Area Low (VAL), along with dynamically calculated Fibonacci levels derived from the developing period's range. It offers extensive customization for both historical and developing levels.

🍀Core Features:

Volume Profiling (POC, VAH, VAL):

Calculates and plots the POC (price level with the highest volume), VAH, and VAL for a selected timeframe (e.g., Daily, Weekly).

The Value Area percentage is configurable. 70% is common on normal volume profiles, but this script allows you to configure multiple % levels via the fib levels. I recommend using 2 versions of this indicator on a chart, one has Value Area at 1 (100% - high and low of lookback) and the second is a specified VA area (i.e. 70%) like in the chart snapshot above. See examples at the bottom.

Historical Levels:

Plots POC, VAH, and VAL from previous completed periods.

Optionally displays only "Unbroken" levels – historical levels that price has not yet revisited, which can act as stronger magnets or resistance/support.

The user can manage the number of historical lines displayed to prevent chart clutter.

Developing Levels:

Shows the POC, VAH, and VAL as they form in real-time during the current, incomplete period. This provides insight into intraday/intra-period value migration.

Dynamic Fibonacci Levels:

Calculates and plots Fibonacci retracement/extension levels based dynamically on the range between the developing POC and the developing VAH/VAL.

Offers 8 configurable % levels above and below POC that can be toggled on/off.

Visual Customization:

Extensive options for colors, line styles, and widths for all plotted levels.

Optional gradient fill for the Value Area that visualizes current price distance from POC - option to invert the colors as well.

Labels for developing levels and Fibonacci levels for easy identification.

🍀Characteristics:

Volume-Driven: Levels are derived from actual trading volume, reflecting areas of high participation and price agreement/disagreement.

Timeframe Specific: The results are entirely dependent on the chosen profile timeframe.

Dynamic & Static Elements: Developing levels and Fibs update live, while historical levels remain fixed once their period closes.

Lagging (Historical) & Potentially Leading: Historical levels are based on the past, but are often respected by future price action. Developing levels show current dynamics.

🍀How to Use It:

Identifying Support & Resistance: Historical and developing POCs, VAHs, and VALs are often key areas where price may react. Unbroken levels are particularly noteworthy.

Market Context & Sentiment: Trading above the POC suggests bullish strength/acceptance of higher prices, while trading below suggests bearishness/acceptance of lower prices.

Entry/Exit Zones: Interactions with these levels (rejections, breakouts, tests) can provide potential entry or exit signals, especially when confirming with other analysis methods.

Dynamic Targets: The Fibonacci levels calculated from the developing POC-VA range offer potential intraday/intra-period price targets or areas of interest.

Understanding Value Migration: Observing the movement of the developing POC/VAH/VAL throughout the period reveals where value is currently being established.

🍀Potential Drawbacks:

Input Sensitivity: The choice of timeframe, Value Area percentage, and volume resolution heavily influences the generated levels. Experimentation is needed for optimal settings per instrument/market. (I've found that Range Charts can provide very accurate volume levels on TV since the time element is removed. This helps to refine the accuracy of price levels with high volume.)

Volume Data Dependency: Requires accurate volume data. May be less reliable on instruments with sparse or questionable volume reporting.

Chart Clutter: Enabling all features simultaneously can make the chart busy. Utilize the line management inputs and toggle features as needed.

Not a Standalone Strategy: This indicator provides context and key levels. It should be used alongside other technical analysis tools and price action reading for robust decision-making.

Developing Level Fluctuation: Developing POC/VA/Fib levels can shift considerably, especially early in a new period, before settling down as more volume accumulates and time passes.

🍀Recommendations/Examples:

I recommend have this indicator on your chart twice, one has the VA set at 1 (100%) and has the fib levels plotted. The second has the VA set to 0.7 (70%) to highlight the defined VA.

Here is an example with 3 on a chart. VA of 100%, VA of 80%, and VA of 20%

AWR R & LR Oscillator with plots & tableHello trading viewers !

I'm glad to share with you one of my favorite indicator. It's the aggregate of many things. It is partly based on an indicator designed by gentleman goat. Many thanks to him.

1. Oscillator and Correlation Calculations

Overview and Functionality: This part of the indicator computes up to 10 Pearson correlation coefficients between a chosen source (typically the close price, though this is user-configurable) and the bar index over various periods. Starting with an initial period defined by the startPeriod parameter and increasing by a set increment (periodIncrement), each correlation coefficient is calculated using the built-in ta.correlation function over successive ranges. These coefficients are stored in an array, and the indicator calculates their average (avgPR) to provide a complete view of the market trend strength.

Display Features: Each individual coefficient, as well as the overall average, is plotted on the chart using a specific color. Horizontal lines (both dashed and solid) are drawn at levels 0, ±0.8, and ±1, serving as visual thresholds. Additionally, conditional fills in red or blue highlight when values exceed these thresholds, helping the user quickly identify potential extreme conditions (such as overbought or oversold situations).

2. Visual Signals and Automated Alerts

Graphical Signal Enhancements: To reinforce the analysis, the indicator uses graphical elements like emojis and shape markers. For example:

If all 10 curves drop below -0.79, a 🌋 emoji appears at the bottom of the chart;

When curves 2 through 10 are below -0.79, a ⛰️ emoji is displayed below the bar, potentially serving as a buy signal accompanied by an alert condition;

Likewise, symmetrical conditions for correlations exceeding 0.79 produce corresponding emojis (🤿 and 🏖️) at the top or bottom of the chart.

Alerts and Notifications: Using these visual triggers, several alertcondition statements are defined within the script. This allows users to set up TradingView alerts and receive real-time notifications whenever the market reaches these predefined critical zones identified by the multi-period analysis.

3. Regression Channel Analysis

Principles and Calculations: In addition to the oscillator, the indicator implements an analysis of regression channels. For each of the 8 configurable channels, the user can set a range of periods (for example, min1 to max1, etc.). The function calc_regression_channel iterates through the defined period range to find the optimal period that maximizes a statistical measure derived from a regression parameter calculated by the function r(p). Once this optimal period is identified, the indicator computes two key points (A and B) which define the main regression line, and then creates a channel based on the calculated deviation (an RMSE multiplied by a user-defined factor).

The regression channels are not displayed on the chart but are used to plot shapes & fullfilled a table.

Blue shapes are plotted when 6th channel or 7th channel are lower than 3 deviations

Yellow shapes are plotted when 6th channel or 7th channel are higher than 3 deviations

4. Scores, Conditions, and the Summary Table

Scoring System: The indicator goes further by assigning scores across multiple analytical categories, such as:

1. BigPear Score

What It Represents: This score is based on a longer-term moving average of the Pearson correlation values (SMA 100 of the average of the 10 curves of correlation of Pearson). The BigPear category is designed to capture where this longer-term average falls within specific ranges.

Conditions: The script defines nine boolean conditions (labeled BigPear1up through BigPear9up for the “up” direction).

Here's the rules :

BigPear1up = (bigsma_avgPR <= 0.5 and bigsma_avgPR > 0.25)

BigPear2up = (bigsma_avgPR <= 0.25 and bigsma_avgPR > 0)

BigPear3up = (bigsma_avgPR <= 0 and bigsma_avgPR > -0.25)

BigPear4up = (bigsma_avgPR <= -0.25 and bigsma_avgPR > -0.5)

BigPear5up = (bigsma_avgPR <= -0.5 and bigsma_avgPR > -0.65)

BigPear6up = (bigsma_avgPR <= -0.65 and bigsma_avgPR > -0.7)

BigPear7up = (bigsma_avgPR <= -0.7 and bigsma_avgPR > -0.75)

BigPear8up = (bigsma_avgPR <= -0.75 and bigsma_avgPR > -0.8)

BigPear9up = (bigsma_avgPR <= -0.8)

Conditions: The script defines nine boolean conditions (labeled BigPear1down through BigPear9down for the “down” direction).

BigPear1down = (bigsma_avgPR >= -0.5 and bigsma_avgPR < -0.25)

BigPear2down = (bigsma_avgPR >= -0.25 and bigsma_avgPR < 0)

BigPear3down = (bigsma_avgPR >= 0 and bigsma_avgPR < 0.25)

BigPear4down = (bigsma_avgPR >= 0.25 and bigsma_avgPR < 0.5)

BigPear5down = (bigsma_avgPR >= 0.5 and bigsma_avgPR < 0.65)

BigPear6down = (bigsma_avgPR >= 0.65 and bigsma_avgPR < 0.7)

BigPear7down = (bigsma_avgPR >= 0.7 and bigsma_avgPR < 0.75)

BigPear8down = (bigsma_avgPR >= 0.75 and bigsma_avgPR < 0.8)

BigPear9down = (bigsma_avgPR >= 0.8)

Weighting:

If BigPear1up is true, 1 point is added; if BigPear2up is true, 2 points are added; and so on up to 9 points from BigPear9up.

Total Score:

The positive score (posScoreBigPear) is the sum of these weighted conditions.

Similarly, there is a negative score (negScoreBigPear) that is calculated using a mirrored set of conditions (named BigPear1down to BigPear9down), each contributing a negative weight (from -1 to -9).

In essence, the BigPear score tells you—in a weighted cumulative way—where the longer-term correlation average falls relative to predefined thresholds.

2. Pear Score

What It Represents: This category uses the immediate average of the Pearson correlations (avgPR) rather than a longer-term smoothed version. It reflects a more current picture of the market’s correlation behavior.

How It’s Calculated:

Conditions: There are nine conditions defined for the “up” scenario (named Pear1up through Pear9up), which partition the range of avgPR into intervals. For instance:

Pear1up = (avgPR > -0.2 and avgPR <= 0)

Pear2up = (avgPR > -0.4 and avgPR <= -0.2)

Pear3up = (avgPR > -0.5 and avgPR <= -0.4)

Pear4up = (avgPR > -0.6 and avgPR <= -0.5)

Pear5up = (avgPR > -0.65 and avgPR <= -0.6)

Pear6up = (avgPR > -0.7 and avgPR <= -0.65)

Pear7up = (avgPR > -0.75 and avgPR <= -0.7)

Pear8up = (avgPR > -0.8 and avgPR <= -0.75)

Pear9up = (avgPR > -1 and avgPR <= -0.8)

There are nine conditions defined for the “down” scenario (named Pear1down through Pear9down), which partition the range of avgPR into intervals. For instance:

Pear1down = (avgPR >= 0 and avgPR < 0.2)

Pear2down = (avgPR >= 0.2 and avgPR < 0.4)

Pear3down = (avgPR >= 0.4 and avgPR < 0.5)

Pear4down = (avgPR >= 0.5 and avgPR < 0.6)

Pear5down = (avgPR >= 0.6 and avgPR < 0.65)

Pear6down = (avgPR >= 0.65 and avgPR < 0.7)

Pear7down = (avgPR >= 0.7 and avgPR < 0.75)

Pear8down = (avgPR >= 0.75 and avgPR < 0.8)

Pear9down = (avgPR >= 0.8 and avgPR <= 1)

Weighting:

Each condition has an associated weight, such as 0.9 for Pear1up, 1.9 for Pear2up, and so on, up to 9 for Pear9up.

Sum up :

Pear1up = 0.9

Pear2up = 1.9

Pear3up = 2.9

Pear4up = 3.9

Pear5up = 4.99

Pear6up = 6

Pear7up = 7

Pear8up = 8

Pear9up = 9

Total Score:

The positive score (posScorePear) is the sum of these values for each condition that returns true.

A corresponding negative score (negScorePear) is calculated using conditions for when avgPR falls on the positive side, with similar weights in the negative direction.

This score quantifies the current correlation reading by translating its relative level into a numeric score through a weighted sum.

3. Trendpear Score

What It Represents: The Trendpear score is more dynamic as it compares the current avgPR with its short-term moving average (sma_avgPR / 14 periods ) and also considers its relationship with an even longer moving average (bigsma_avgPR / 100 periods). It is meant to capture the trend or momentum in the correlation behavior.

How It’s Calculated:

Conditions: Nine conditions (from Trendpear1up to Trendpear9up) are defined to check:

Whether avgPR is below, equal to, or above sma_avgPR by different margins;

Whether it is trending upward (i.e., it is higher than its previous value).

Here are the rules

Trendpear1up = (avgPR <= sma_avgPR -0.2) and (avgPR >= avgPR )

Trendpear2up = (avgPR > sma_avgPR -0.2) and (avgPR <= sma_avgPR -0.07) and (avgPR >= avgPR )

Trendpear3up = (avgPR > sma_avgPR -0.07) and (avgPR <= sma_avgPR -0.03) and (avgPR >= avgPR )

Trendpear4up = (avgPR > sma_avgPR -0.03) and (avgPR <= sma_avgPR -0.02) and (avgPR >= avgPR )

Trendpear5up = (avgPR > sma_avgPR -0.02) and (avgPR <= sma_avgPR -0.01) and (avgPR >= avgPR )

Trendpear6up = (avgPR > sma_avgPR -0.01) and (avgPR <= sma_avgPR -0.001) and (avgPR >= avgPR )

Trendpear7up = (avgPR >= sma_avgPR) and (avgPR >= avgPR ) and (avgPR <= bigsma_avgPR)

Trendpear8up = (avgPR >= sma_avgPR) and (avgPR >= avgPR ) and (avgPR >= bigsma_avgPR -0.03)

Trendpear9up = (avgPR >= sma_avgPR) and (avgPR >= avgPR ) and (avgPR >= bigsma_avgPR)

Weighting:

The weights here are not linear. For example, the lightest condition may add 0.1 point, whereas the most extreme condition (e.g., when avgPR is not only above the moving average but also reaches a high proportion relative to bigsma_avgPR) might add as much as 90 points.

Trendpear1up = 0.1

Trendpear2up = 0.2

Trendpear3up = 0.3

Trendpear4up = 0.4

Trendpear5up = 0.5

Trendpear6up = 0.69

Trendpear7up = 7

Trendpear8up = 8.9

Trendpear9up = 90

Total Score:

The positive score (posScoreTrendpear) is the sum of the weights from all conditions that are satisfied.

A negative counterpart (negScoreTrendpear) exists similarly for when the trend indicates a downward bias.

Trendpear integrates both the level and the direction of change in the correlations, giving a strong numeric indication when the market starts to diverge from its short-term average.

4. Deviation Score

What It Represents: The “Écart” score quantifies how far the asset’s price deviates from the boundaries defined by the regression channels. This metric can indicate if the price is excessively deviating—which might signal an eventual reversion—or confirming a breakout.

How It’s Calculated:

Conditions: For each channel (with at least seven channels contributing to the scoring from the provided code), there are three levels of deviation:

First tier (EcartXup): Checks if the price is below the upper boundary but above a second boundary.

Second tier (EcartXup2): Checks if the price has dropped further, between a lower and a more extreme boundary.

Third tier (EcartXup3): Checks if the price is below the most extreme limit.

Weighting:

Each tier within a channel has a very small weight for the lowest severities (for example, 0.0001 for the first tier, 0.0002 for the second, 0.0003 for the third) with weights increasing with the channel index.

First channel : 0.0001 to 0.0003 (very short term)

Second channel : 0.001 to 0.003 (short term)

Third channel : 0.01 to 0.03 (short mid term)

4th channel : 0.1 to 0.3 ( mid term)

5th channel: 1 to 3 (long mid term)

6th channel : 10 to 30 (long term)

7th channel : 100 to 300 (very long term)

Total Score:

The overall positive score (posScoreEcart) is the sum of all the weights for conditions met among the first, second, and third tiers.

The corresponding negative score (negScoreEcart) is calculated similarly (using conditions when the price is above the channel boundaries), with the weights being the same in magnitude but negative in sign.

This layered scoring method allows the indicator to reflect both minor and major deviations in a gradated and cumulative manner.

Example :

Score + = 321.0001

Score - = -0.111

The asset price is really overextended in long term view, not for mid term & short term expect the in the very short term.

Score + = 0.0033

Score - = -1.11

The asset price is really extended in short term view, not for mid term (even a bit underextended) & long term is neutral

5. Slope Score

What It Represents: The Slope score captures the trend direction and steepness of the regression channels. It reflects whether the regression line (and hence the underlying trend) is sloping upward or downward.

How It’s Calculated:

Conditions:

if the slope has a uptrend = 1

if the slope has a downtrend = -1

Weighting:

First channel : 0.0001 to 0.0003 (very short term)

Second channel : 0.001 to 0.003 (short term)

Third channel : 0.01 to 0.03 (short mid term)

4th channel : 0.1 to 0.3 ( mid term)

5th channel: 1 to 3 (long mid term)

6th channel : 10 to 30 (long term)

7th channel : 100 to 300 (very long term)

The positive slope conditions incrementally add weights from 0.0001 for the smallest positive slopes to 100 for the largest among the seven checks. And negative for the downward slopes.

The positive score (posScoreSlope) is the sum of all the weights from the upward slope conditions that are met.

The negative score (negScoreSlope) sums the negative weights when downward conditions are met.

Example :

Score + = 111

Score - = -0.1111

Trend is up for longterm & down for mid & short term

The slope score therefore emphasizes both the magnitude and the direction of the trend as indicated by the regression channels, with an intentional asymmetry that flags strong downtrends more aggressively.

Summary

For each category—BigPear, Pear, Trendpear, Écart, and Slope—the indicator evaluates a defined set of conditions. Each condition is a binary test (true/false) based on different thresholds or comparisons (for example, comparing the current value to a moving average or a channel boundary). When a condition is true, its assigned weight is added to the cumulative score for that category. These individual scores, both positive and negative, are then displayed in a table, making it easy for the trader to see at a glance where the market stands according to each analytical dimension.

This comprehensive, weighted approach allows the indicator to encapsulate several layers of market information into a single set of scores, aiding in the identification of potential trading opportunities or market reversals.

5. Practical Use and Application

How to Use the Indicator:

Interpreting the Signals:

On your chart, observe the following components:

The individual correlation curves and their average, plotted with visual thresholds;

Visual markers (such as emojis and shape markers) that signal potential oversold or overbought conditions

The summary table that aggregates the scores from each category, offering a quick glance at the market’s state.

Trading Alerts and Decisions: Set your TradingView alerts through the alertcondition functions provided by the indicator. This way, you receive immediate notifications when critical conditions are met, allowing you to react as soon as the market reaches key levels. This tool is especially beneficial for advanced traders who want to combine multiple technical dimensions to optimize entry and exit points with a confluence of signals.

Conclusion and Additional Insights

In summary, this advanced indicator innovatively combines multi-scale Pearson correlation analysis (via multiple linear regressions) with robust regression channel analysis. It offers a deep and nuanced view of market dynamics by delivering clear visual signals and a comprehensive numerical summary through a built-in score table.

Combine this indicator with other tools (e.g., oscillators, moving averages, volume indicators) to enhance overall strategy robustness.

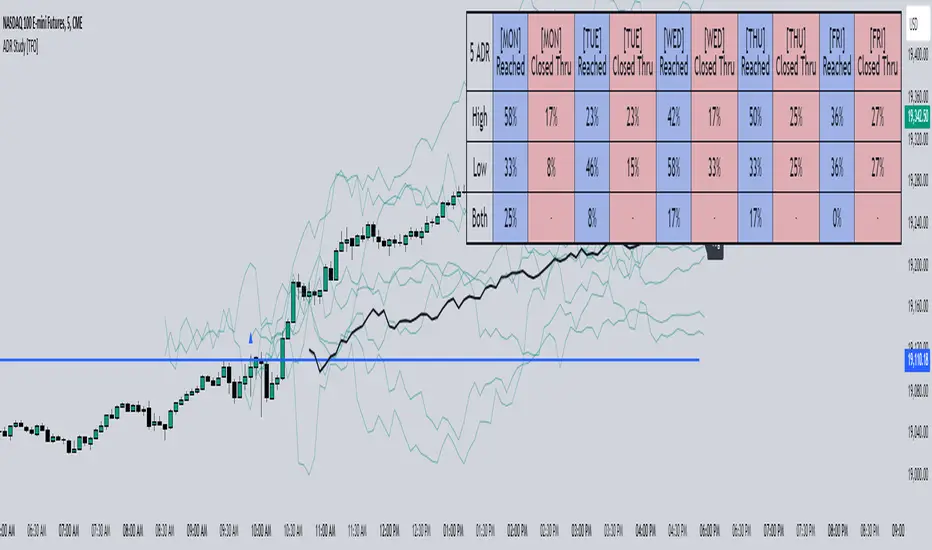

ADR, ATR & VOL OverlayThis is a combined version of 2 of my other indicators:

ADR / ATR Overlay

VOL / AVG Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Custom Session Volume

Average For Selected Session

Volume Percentage Comparison

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Custom Session Volume : User chosen time frame to monitor volume

Average For Selected Session : Average for the custom session volume

Volume Percentage Comparison : Current session compared to the average (calculated at session close)

Options:

ADR/ATR:

Time Frame

Length

Smoothing

Volume:

Set Custom Time Frame For Calculations

Set Custom Time Frame For Average Comparison

Set Custom Time Zone

Table:

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Add/Remove extra row for placement

ADR / ATR Example:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential (coverage) move of 30% in Pre/Post market as suggested by averages.

Custom Volume Session Example:

Set indicator to 30 period average. Set custom time frame to 9:30am to 10:30am Eastern/New York.

When the time frame for the calculation is closed, the indicator will provide a comparison of the current days volume compared to the average of 30 previous days for that same time frame and display it as a percentage in the table.

In this example you could compare how the first hour of the trading day compares to the previous 30 day's average, aiding in evaluating the potential volume for the remainder of the day.

Notes:

Times must be entered in 24 hour format. (1pm = 13:00 etc.)

Volume indicator is for Intra-day time frames, not > Day.

How I use these values:

I use these calculations to determine if a ticker symbol has the necessary range to achieve target gains, to determine if the price oscillation is within "normal" ranges to determine if the trading day will be choppy, and to determine placement of stops and targets within average ranges in combination with support, resistance and retracement levels.

Chart Patterns [ActiveQuants]The Chart Patterns indicator is a comprehensive tool designed to automatically identify a variety of common chart patterns directly on your price chart. By detecting sequences of pivot highs and lows , this indicator helps traders spot potential trend continuations , reversals , and key market structures such as Double Tops and Double Bottoms . Enhance your technical analysis by quickly recognizing these formations as they emerge.

How It Works

The indicator operates in a two-stage process:

Pivot Point Detection: It first identifies significant swing highs and swing lows (pivot points) based on a user-defined Period . These pivots form the fundamental building blocks for pattern recognition.

Pattern Recognition: Using the sequence of these detected pivot points, the script then applies logical rules to identify the following patterns:

Lower Low (LL)

Lower Low & Lower High (LL & LH)

Higher High (HH)

Higher High & Higher Low (HH & HL)

Double Tops

Double Bottoms

Patterns are drawn on the chart with connecting lines and labeled for easy identification. Double Tops and Double Bottoms also feature a status system: " Active " while forming, " Confirmed " upon neckline breakout, or " Invalid " if specific conditions negate the pattern before confirmation.

█ KEY FEATURES

Comprehensive Pattern Detection: Identifies six distinct types of chart patterns, offering insights into both trend continuation and potential reversals.

Pivot-Based Analysis: Uses a robust method of identifying pivot highs and lows as the foundation for pattern formation.

Pattern Status for Double Tops/Bottoms:

- Active: A Double Top or Double Bottom pattern has formed its two peaks/troughs and the intervening neckline point, but the price has not yet broken beyond the neckline. The pattern is developing .

- Confirmed: The price has decisively closed beyond the neckline (below for Double Top, above for Double Bottom), signaling a potential entry or validation of the pattern.

- Invalid: An " Active " Double Top or Double Bottom pattern can be invalidated if, before a neckline breakout occurs, a new pivot point forms that negates the pattern’s structural integrity. For example, if a new pivot low forms above or at the neckline of an Active Double Top, the pattern is considered invalid because the market failed to break down and instead showed relative strength.

Customizable Visuals: Allows users to define colors for bullish and bearish patterns, line widths, and the visibility of pivot points.

Selective Pattern Display: Users can choose to display all patterns or filter by status (Active, Confirmed, Invalid) for Double Tops/Bottoms. Individual pattern types can also be toggled on or off.

Historical Analysis Control: The Show Last History (Bars) input allows users to specify how far back the indicator should plot patterns, optimizing performance and chart readability.

Clear Labeling: Patterns are clearly labeled on the chart, with Double Tops/Bottoms also showing " Top 1 ," " Top 2 ," or " Bottom 1 ," " Bottom 2 " labels.

█ PATTERNS DETECTED

Lower Low (LL): Indicates a potential bearish continuation or the start of a downtrend. Forms when price makes a lower low during an uptrend.

Lower Low & Lower High (LL & LH): A stronger confirmation of a bearish trend, where the market forms a lower low followed by a lower high .

Higher High (HH): Signals a potential bullish continuation or the start of an uptrend. Forms when price makes a higher high during a downtrend.

Higher High & Higher Low (HH & HL): A stronger confirmation of a bullish trend, where the market forms a higher high followed by a higher low .

Double Top: A bearish reversal pattern characterized by two distinct peaks at roughly the same price level, separated by a trough (neckline). Confirmation occurs when price breaks below the neckline.

Double Bottom: A bullish reversal pattern featuring two distinct troughs at roughly the same price level, separated by a peak (neckline). Confirmation occurs when price breaks above the neckline.

█ EXAMPLE: DOUBLE TOP INVALIDATION

Understanding how a Double Top or Double Bottom can be invalidated is crucial. Here's an example for a Double Top:

Formation: The indicator identifies two peaks (Top 1, Top 2) at a similar price level, with a corrective trough (Neckline Pivot P5) in between. The pattern is labeled " Double Top " and is in an " Active " state. ( Imagine points P4 and P6 are the two tops, and P5 is the low point of the neckline between them ).

Pre-Breakout Condition: The price action continues, but before it breaks decisively below the P5 neckline level, a new significant swing low (a new pivot low) forms.

Invalidation Check: The indicator checks the price level of this new pivot low. If this new pivot low occurs at a price equal to or higher than the P5 neckline level, the " Active " Double Top pattern is re-labeled as " Invalid Double Top ". ( See image below for a visual representation of this scenario )

In this example, the Double Top formed with Top 1 (P4) and Top 2 (P6). The neckline is at P5. Before price broke below P5, a new pivot low formed at the red circle. Since this new pivot low is above the P5 neckline, the Double Top is marked " Invalid ".

The logic is that the market failed to break the neckline support and instead established a higher low (or a low at the support level), suggesting that the immediate bearish pressure has waned, thus invalidating the bearish reversal implication of the Double Top before it could confirm. A similar logic applies to Double Bottoms (a new pivot high forming below or at the neckline before an upside breakout).

█ USER INPUTS

Visibility and Common Styling

- Show Last History (Bars):

Specifies the number of recent bars the indicator will analyze and plot patterns on.

Default: 3000 bars. Min: 10.

- Patterns:

Filters which patterns are displayed based on their status.

Options: All, Active, Confirmed, Invalid.

Default: All.

- Pattern Line Width:

Sets the thickness of the lines used to draw the patterns.

Default: 1. Min: 1, Max: 10.

- Bearish Color:

Color for bearish patterns (LL, LL & LH, Double Tops).

Default: Red.

- Bullish Color:

Color for bullish patterns (HH, HH & HL, Double Bottoms).

Default: Green.

Pivot Points

- Period:

The lookback period on either side of a bar to qualify it as a pivot high or low. Higher values detect more significant pivots.

Default: 10 bars. Min: 2.

- Show Pivot Highs:

Toggles the visibility of detected pivot high markers.

Default: Enabled.

- Show Pivot Lows:

Toggles the visibility of detected pivot low markers.

Default: Enabled.

- Pivot Highs Color:

Color for the pivot high markers.

Default: #ff5252 (Reddish).

- Pivot Lows Color:

Color for the pivot low markers.

Default: #089981 (Greenish).

Patterns (Toggles)

- Lower Low:

Enable/disable detection and display of Lower Low patterns.

Default: Enabled.

- Lower Low & Lower High:

Enable/disable detection and display of Lower Low & Lower High patterns.

Default: Enabled.

- Higher High:

Enable/disable detection and display of Higher High patterns.

Default: Enabled.

- Higher High & Higher Low:

Enable/disable detection and display of Higher High & Higher Low patterns.

Default: Enabled.

- Double Tops:

Enable/disable detection and display of Double Top patterns.

Default: Enabled.

- Double Bottoms:

Enable/disable detection and display of Double Bottom patterns.

Default: Enabled.

█ CONCLUSION

The Chart Patterns indicator is a versatile and powerful assistant for traders who utilize classical chart pattern analysis. By automating the detection of key formations and providing clear visual cues along with status updates for patterns like Double Tops and Bottoms, it allows traders to focus on strategy development and execution. With its customizable settings, it can be adapted to various instruments and timeframes, making it a valuable addition to any technical trader's toolkit.

█ IMPORTANT NOTES

⚠ Pivot Period Sensitivity: The Period setting for pivot detection is crucial. A shorter period will identify more frequent, smaller swings, while a longer period will focus on more significant turning points. Adjust this setting based on the asset's volatility, the timeframe you are trading and your trading style.

⚠ Confirmation is Key: While the indicator identifies patterns, always wait for pattern confirmation (e.g., neckline breaks for Double Tops/Bottoms) and consider other factors like volume and market context before making trading decisions.

⚠ Confirmed Bars for Detection: Patterns are identified based on confirmed pivot points, which means a pivot is recognized period bars after it has formed. Status updates for Double Tops/Bottoms (Active, Confirmed, Invalid) also occur on confirmed bars. This approach enhances reliability and reduces the likelihood of repainting based on intra-bar price fluctuations.

⚠ Not a Standalone System: Chart patterns provide valuable insights, but they should be used in conjunction with other technical analysis tools (e.g., trendlines, moving averages, oscillators) and a sound risk management plan.

⚠ Lagging Nature: By their very definition, chart patterns are lagging indicators as they require a sequence of price action and several pivot points to complete their formation.

█ RISK DISCLAIMER

Trading involves a substantial risk of loss and is not suitable for every investor. The information provided by the Chart Patterns indicator is for educational and informational purposes only. It should not be considered as financial advice or a recommendation to buy or sell any security. Chart patterns indicate potential price movements but do not guarantee future results. Always perform your own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.

📈 Happy trading! 🚀

D3m4h GIFVGDescription

D3m4h GIFVG is an indicator designed to automatically detect market imbalances—often referred to as FVGs (Fair Value Gaps)—and potential pivot-based shifts in market structure. It offers a dynamic approach to visualizing supply/demand inefficiencies and pivot-based trend changes. Key features include:

1. Pivot-Based Bullish/Bearish Detection

The indicator identifies higher-high/lower-low pivot logic as well as “outside bar” pivots.

It tracks when the market transitions from bullish to bearish ranges, or vice versa, by using multiple checks:

Pivot low/high detection

Break-of-structure (when price crosses the last pivot)

Opposing FVG detection to confirm an intraday pivot shift

2. FVG (Fair Value Gap) Detection

The script automatically scans for bullish or bearish FVG conditions:

Bullish FVG: Candle at position (bar_index - 2) has a high below the current candle’s low.

Bearish FVG: Candle at position (bar_index - 2) has a low above the current candle’s high.

When it detects an FVG, it draws a box on the chart to highlight the price gap (yellow boxes by default).

3. Pivot Range FVG

If an FVG forms while the market is in a bullish pivot range, the script can paint a special “blue” FVG to underscore its significance. The same logic applies if a newly formed FVG appears in a bearish pivot range.

4. Filled Gap Cleanup

You can optionally hide standard FVG boxes once they’re filled. For example, if the candle’s body (or candle range) covers that gap, the box is removed to keep your chart clean.

5. Pivot-Range FVG “Raided” Cleanup

If the pivot-based FVG is later filled from the opposing direction, it turns green and can optionally remove itself after a set number of bars.

6. Informative Table

A small table on the chart optionally displays whether or not the pivot-based FVG has been “raided”. You can toggle this table on/off in the settings.

How It Works

1. Pivot Shifts

The script tracks the last pivot high/low using a combination of candle-based pivot detection and break-of-structure checks (when price crosses the last pivot in the opposite direction).

When a shift is detected, the pivot range ID increments—this helps the script know when to remove old pivot-based FVGs or draw new ones.

2. FVG Formation

Each new bar checks if a bullish or bearish FVG formed (comparing the high of bar two bars ago to the current low, or the low of bar two bars ago to the current high).

If one is found, a box is drawn to highlight the imbalance. Its color and extension depend on script settings.

3. Imbalance or Pivot FVG

Standard imbalance boxes appear in yellow.

If the new imbalance coincides with a bullish or bearish pivot range, a special “pivot imbalance” box in blue is drawn.

3. Hide Filled

If a newly formed candle’s body fully covers the FVG, the box is considered filled. If Hide Filled Gaps is enabled, the box is deleted once it’s covered.

4. Raid Status

For the pivot-based (blue) FVG, once price invalidates it from the opposite side, it changes color to green and gets removed after a user-defined number of bars.

How to Use

1. Look for FVGs

Observe yellow boxes to identify potential intraday imbalances. Watch for price returning to fill these zones.

If you see a “blue” box, it signifies a pivot-based FVG in line with a recognized shift in structure—arguably a higher-probability zone.

2. “Hide Filled Gaps”

Turn this on if you only want to see currently active or partially filled imbalances. The script cleans up old, fully covered boxes to keep your chart neat.

3. Pivot Shifts

Note the script’s internal pivot logic. Each new pivot re-defines bullish or bearish states. Use these states to gauge the short-term trend shifts.

4. Toggle the Table

You can show or hide the chart table by enabling/disabling “Show Table” from the inputs. This table indicates if the pivot-based “GIFVG” has been “raided” or not.

5. Extend Count

Adjust the extendCount in the code if you want FVG boxes to extend further or shorter in time.

Underlying Concepts

Fair Value Gaps

Market inefficiencies that occur when price jumps, leaving a “gap” from the candle 2 bars ago to the current candle. They can act like mini supply/demand zones where price may revisit for balance.

Pivot Ranges

The script tries to maintain an internal sense of whether the market is in a bullish or bearish pivot range. When it sees a contrary FVG or break-of-structure, it flips the pivot state.

Outside Bars

A candle that has both a higher high and a lower low than the previous bar. The script uses these to mark significant pivot shifts.

By combining pivot-based logic with FVG detection, the D3m4h GIFVG indicator helps highlight potential areas of liquidity or unfilled value. Traders can use these zones to plan entries/exits or to confirm short-term trend shifts.

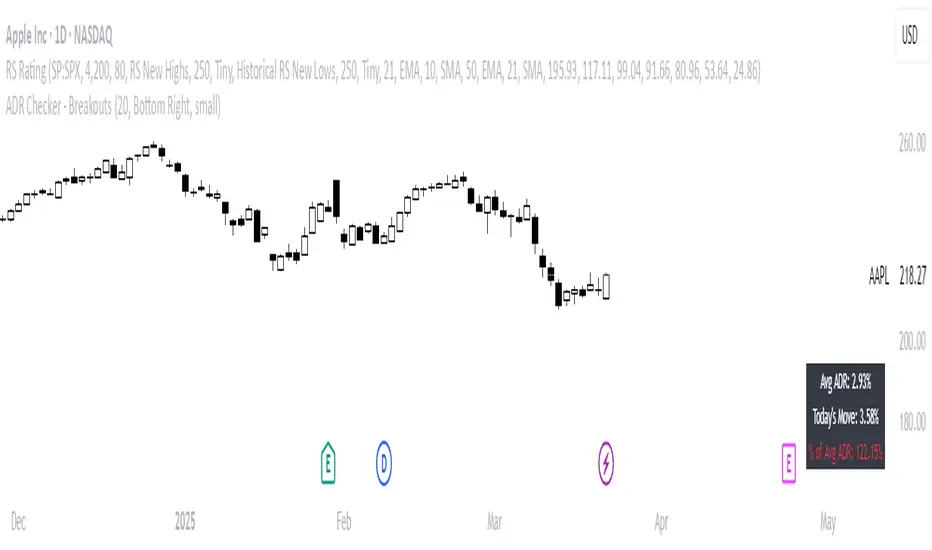

ADR Checker - Breakouts📈 ADR Checker – Breakouts

Gain the edge by knowing when a stock has already made its move.

🚀 What It Does:

The ADR Checker - Breakouts is a powerful yet simple visual tool that helps traders instantly assess whether a stock has already exceeded its Average Daily Range (ADR) for the day — a critical piece of information for momentum traders, swing traders, and especially those following breakout, VCP, or CANSLIM strategies.

Using a customizable on-screen table that always stays in view (regardless of zoom or chart scaling), this script shows:

✅ Average ADR% – 20-day average range, calculated in %.

📊 Today’s Move – how much the stock has moved today.

🔥 % of Avg ADR – today's move relative to its historical average, with live color feedback:

🟥 Over 100% (Overextended – danger!)

🟧 70-100% (Caution zone)

🟩 Below 70% (Room to move)

💡 Why It Matters:

One of the most overlooked mistakes by breakout traders is entering a trade after the move has already happened. If a stock has already moved more than its typical daily range, the odds of further continuation sharply decrease, while the risk of pullback or chop increases.

With this tool, you can:

🚫 Avoid chasing extended breakouts

🎯 Time entries before the real move

⚠️ Quickly assess risk/reward potential intraday

🧠 Example Use Case:

Imagine you're watching a classic VCP setup or flat base breakout. The stock breaks out on volume—but when you check this indicator, you see:

Today’s Move: 7.2%

Avg ADR: 5.3%

% of ADR: 135% 🟥

This tells you the stock is already well beyond its average daily range. While it may continue higher, odds now favor a consolidation, shakeout, or pullback. This is your cue to wait for a better entry or pass entirely.

On the flip side, if the breakout just started and the % of ADR is still under 50%, you have confirmation that there’s room to run — giving you more confidence to enter early.

⚙️ Fully Customizable:

Choose position on screen (top/bottom left/right)

Customize text color, background, and size

🔧 Install This Tool and:

✅ Stop chasing extended moves

✅ Add discipline to your entries

✅ Improve your breakout win rate

Perfect for VCP, CANSLIM, and BREAKOUT traders who want a clean, edge-enhancing visual guide.

Celestial Pair Spread Hello friends, after a very long time!

Today, I tried to put into code an idea that came to my mind spontaneously and suddenly.

Note :

This script is experimental and improvable.

I haven't had a chance to try it yet.

TIMEFRAME : 1D (Daily Bars)

CELESTIAL SPREAD

The spread moves in a very limited area and is consistent within itself, especially on days far from the end of the contract.

That's why there is a reassuring sky atmosphere. That's why this name was given completely improvised.

Basic logic of the script

We enter the name of the CME Futures contract we want to enter:

Ex : CL1! , ES1! , ZC1! , NQ1!

The script creates us a pair trade parity divided into secondary contracts.

Example : ES1!/ES2!

What is pair trading?

I will explain briefly here.

For users who are wondering:

www.investopedia.com

Let's get back to our topic.

Now we have created a parity that does not actually exist.

This parity is the manifestation of the relative movements of two contracts.

When the parity rises, ES1! increased,ES2! has fallen.

In the opposite case, We can say: ES1! Contract has been dropped ES2! has increased.

Pair trading is generally a trade that needs to be kept in mind from time to time.

It is a method preferred by professionals who can process very quickly.

Market risk is minimal, but since 2 contracts are purchased, more money is paid and very low percentage profits are made.

It is very expensive to do pair trading, especially with oil and its derivatives and interest security derivatives.

The contract we are considering has micros. (small-item contracts tied to the same value)

So when we switch to our broker MES1!/MES2! We will trade.

For all CME futures :

www.cmegroup.com

Anyway, let's continue:

The script created the parity showing its relationship with the next contract and plotted it as bars.

Celestial bands are just like Bollinger bands, but they consist of 3 bands based on percentage changes rather than standard deviation.

The middle band is obtained from moving averages.

The upper and lower bands are the middle band subjected to a threshold value.

The threshold value can be changed.

0.15 percent was charged for this script.

CAUTION :

As can be seen in the example below;

The most important thing is not to make any transactions when the contract switch dates are approaching.

Therefore, it is recommended to use it just below the main chart.

The blue bars in the parity are

Values that outside the upper and lower threshold values are colored blue.

For this condition

Alerts has been added.

Don't forget to add alert and edit.

MAIN PURPOSE

It is aimed to start a pair trade when such conditions come and to quickly close the trades when the parity basis reaches the value.

OTHER IMPORTANT POINTS

Other issues are broker related issues.

Difference between initial margins and maintanence margins of contracts (between 1! and 2!)

It shouldn't be too high.

The commission should not be too high.

Leverage must be high because the profit percentage is very low.

To calculate leverage you must divide your contract size by the relevant margin requirement.

Sample margin requirement table:

www.interactivebrokers.com

RISKS

It is an experimental and intellectual script,

the risk of contract price differences (maybe it will not leave a profit except for very extreme values)

I remind you of the quickness risk that comes from a two-legged trade.

Alerts definitely synchronized with an audible alert sent to a smartphone as an e-mail notification and displayed on the locked screen for quick action.

Best regards!

Overextension Oscillator [by DanielM]The Overextension Oscillator is an indicator that detects when a market move has extended significantly beyond its typical range, signaling potential areas for a correction or reversal. Unlike traditional oscillators that rely on fixed overbought/oversold levels, this tool dynamically adjusts its thresholds based on historical swing high and swing low movements.

By analyzing all swing points on the chart, the indicator determines the expected range of price movements and identifies when the price extends beyond normal levels. Since every asset has different price behavior and volatility, swing lengths may vary from asset to asset, ensuring that overextension is measured relative to each market's historical price behavior.

How It Works

1️⃣ Swing Detection & Data Collection

The indicator scans all available swing highs and swing lows on the chart to gather a complete dataset of past price fluctuations.

It records the percentage differences between swings to determine how much price typically moves in a given market.

2️⃣ Overextension Calculation

Using the stored swing data, the indicator calculates:

Average Swing Difference – Measures the average percentage difference between swings.

Average Move Percentage – Determines the typical magnitude of price moves within a trend cycle.

These values are used to create dynamic overextension thresholds that adjust based on historical data.

3️⃣ Price Distance & Overextension Measurement

The indicator calculates the distance between the current price and the closest historical swing point. If this distance exceeds the predefined threshold based on past swings, the move is considered overextended. The greater the deviation, the higher the probability of a pullback or short-term reversal.

4️⃣ Buy/Sell Signal Generation

A Buy signal is generated when the price has dropped below an overextended threshold relative to a past swing low.

A Sell signal is generated when the price has risen beyond an overextended threshold relative to a past swing high.

These signals indicate that the price has reached a level where it historically tends to slow down or reverse.

Accurate Bollinger Bands mcbw_ [True Volatility Distribution]The Bollinger Bands have become a very important technical tool for discretionary and algorithmic traders alike over the last decades. It was designed to give traders an edge on the markets by setting probabilistic values to different levels of volatility. However, some of the assumptions that go into its calculations make it unusable for traders who want to get a correct understanding of the volatility that the bands are trying to be used for. Let's go through what the Bollinger Bands are said to show, how their calculations work, the problems in the calculations, and how the current indicator I am presenting today fixes these.

--> If you just want to know how the settings work then skip straight to the end or click on the little (i) symbol next to the values in the indicator settings window when its on your chart <--

--------------------------- What Are Bollinger Bands ---------------------------

The Bollinger Bands were formed in the 1980's, a time when many retail traders interacted with their symbols via physically printed charts and computer memory for personal computer memory was measured in Kb (about a factor of 1 million smaller than today). Bollinger Bands are designed to help a trader or algorithm see the likelihood of price expanding outside of its typical range, the further the lines are from the current price implies the less often they will get hit. With a hands on understanding many strategies use these levels for designated levels of breakout trades or to assist in defining price ranges.

--------------------------- How Bollinger Bands Work ---------------------------

The calculations that go into Bollinger Bands are rather simple. There is a moving average that centers the indicator and an equidistant top band and bottom band are drawn at a fixed width away. The moving average is just a typical moving average (or common variant) that tracks the price action, while the distance to the top and bottom bands is a direct function of recent price volatility. The way that the distance to the bands is calculated is inspired by formulas from statistics. The standard deviation is taken from the candles that go into the moving average and then this is multiplied by a user defined value to set the bands position, I will call this value 'the multiple'. When discussing Bollinger Bands, that trading community at large normally discusses 'the multiple' as a multiplier of the standard deviation as it applies to a normal distribution (gaußian probability). On a normal distribution the number of standard deviations away (which trades directly use as 'the multiple') you are directly corresponds to how likely/unlikely something is to happen:

1 standard deviation equals 68.3%, meaning that the price should stay inside the 1 standard deviation 68.3% of the time and be outside of it 31.7% of the time;

2 standard deviation equals 95.5%, meaning that the price should stay inside the 2 standard deviation 95.5% of the time and be outside of it 4.5% of the time;

3 standard deviation equals 99.7%, meaning that the price should stay inside the 3 standard deviation 99.7% of the time and be outside of it 0.3% of the time.

Therefore when traders set 'the multiple' to 2, they interpret this as meaning that price will not reach there 95.5% of the time.

---------------- The Problem With The Math of Bollinger Bands ----------------

In and of themselves the Bollinger Bands are a great tool, but they have become misconstrued with some incorrect sense of statistical meaning, when they should really just be taken at face value without any further interpretation or implication.

In order to explain this it is going to get a bit technical so I will give a little math background and try to simplify things. First let's review some statistics topics (distributions, percentiles, standard deviations) and then with that understanding explore the incorrect logic of how Bollinger Bands have been interpreted/employed.

---------------- Quick Stats Review ----------------

.

(If you are comfortable with statistics feel free to skip ahead to the next section)

.

-------- I: Probability distributions --------

When you have a lot of data it is helpful to see how many times different results appear in your dataset. To visualize this people use "histograms", which just shows how many times each element appears in the dataset by stacking each of the same elements on top of each other to form a graph. You may be familiar with the bell curve (also called the "normal distribution", which we will be calling it by). The normal distribution histogram looks like a big hump around zero and then drops off super quickly the further you get from it. This shape (the bell curve) is very nice because it has a lot of very nifty mathematical properties and seems to show up in nature all the time. Since it pops up in so many places, society has developed many different shortcuts related to it that speed up all kinds of calculations, including the shortcut that 1 standard deviation = 68.3%, 2 standard deviations = 95.5%, and 3 standard deviations = 99.7% (these only apply to the normal distribution). Despite how handy the normal distribution is and all the shortcuts we have for it are, and how much it shows up in the natural world, there is nothing that forces your specific dataset to look like it. In fact, your data can actually have any possible shape. As we will explore later, economic and financial datasets *rarely* follow the normal distribution.

-------- II: Percentiles --------

After you have made the histogram of your dataset you have built the "probability distribution" of your own dataset that is specific to all the data you have collected. There is a whole complicated framework for how to accurately calculate percentiles but we will dramatically simplify it for our use. The 'percentile' in our case is just the number of data points we are away from the "middle" of the data set (normally just 0). Lets say I took the difference of the daily close of a symbol for the last two weeks, green candles would be positive and red would be negative. In this example my dataset of day by day closing price difference is:

week 1:

week 2:

sorting all of these value into a single dataset I have:

I can separate the positive and negative returns and explore their distributions separately:

negative return distribution =

positive return distribution =

Taking the 25th% percentile of these would just be taking the value that is 25% towards the end of the end of these returns. Or akin the 100%th percentile would just be taking the vale that is 100% at the end of those:

negative return distribution (50%) = -5

positive return distribution (50%) = +4

negative return distribution (100%) = -10

positive return distribution (100%) = +20

Or instead of separating the positive and negative returns we can also look at all of the differences in the daily close as just pure price movement and not account for the direction, in this case we would pool all of the data together by ignoring the negative signs of the negative reruns

combined return distribution =

In this case the 50%th and 100%th percentile of the combined return distribution would be:

combined return distribution (50%) = 4

combined return distribution (100%) = 10

Sometimes taking the positive and negative distributions separately is better than pooling them into a combined distribution for some purposes. Other times the combined distribution is better.

Most financial data has very different distributions for negative returns and positive returns. This is encapsulated in sayings like "Price takes the stairs up and the elevator down".

-------- III: Standard Deviation --------

The formula for the standard deviation (refereed to here by its shorthand 'STDEV') can be intimidating, but going through each of its elements will illuminate what it does. The formula for STDEV is equal to:

square root ( (sum ) / N )

Going back the the dataset that you might have, the variables in the formula above are:

'mean' is the average of your entire dataset

'x' is just representative of a single point in your dataset (one point at a time)

'N' is the total number of things in your dataset.

Going back to the STDEV formula above we can see how each part of it works. Starting with the '(x - mean)' part. What this does is it takes every single point of the dataset and measure how far away it is from the mean of the entire dataset. Taking this value to the power of two: '(x - mean) ^ 2', means that points that are very far away from the dataset mean get 'penalized' twice as much. Points that are very close to the dataset mean are not impacted as much. In practice, this would mean that if your dataset had a bunch of values that were in a wide range but always stayed in that range, this value ('(x - mean) ^ 2') would end up being small. On the other hand, if your dataset was full of the exact same number, but had a couple outliers very far away, this would have a much larger value since the square par of '(x - mean) ^ 2' make them grow massive. Now including the sum part of 'sum ', this just adds up all the of the squared distanced from the dataset mean. Then this is divided by the number of values in the dataset ('N'), and then the square root of that value is taken.

There is nothing inherently special or definitive about the STDEV formula, it is just a tool with extremely widespread use and adoption. As we saw here, all the STDEV formula is really doing is measuring the intensity of the outliers.

--------------------------- Flaws of Bollinger Bands ---------------------------

The largest problem with Bollinger Bands is the assumption that price has a normal distribution. This is assumption is massively incorrect for many reasons that I will try to encapsulate into two points:

Price return do not follow a normal distribution, every single symbol on every single timeframe has is own unique distribution that is specific to only itself. Therefore all the tools, shortcuts, and ideas that we use for normal distributions do not apply to price returns, and since they do not apply here they should not be used. A more general approach is needed that allows each specific symbol on every specific timeframe to be treated uniquely.

The distributions of price returns on the positive and negative side are almost never the same. A more general approach is needed that allows positive and negative returns to be calculated separately.

In addition to the issues of the normal distribution assumption, the standard deviation formula (as shown above in the quick stats review) is essentially just a tame measurement of outliers (a more aggressive form of outlier measurement might be taking the differences to the power of 3 rather than 2). Despite this being a bit of a philosophical question, does the measurement of outlier intensity as defined by the STDEV formula really measure what we want to know as traders when we're experiencing volatility? Or would adjustments to that formula better reflect what we *experience* as volatility when we are actively trading? This is an open ended question that I will leave here, but I wanted to pose this question because it is a key part of what how the Bollinger Bands work that we all assume as a given.

Circling back on the normal distribution assumption, the standard deviation formula used in the calculation of the bands only encompasses the deviation of the candles that go into the moving average and have no knowledge of the historical price action. Therefore the level of the bands may not really reflect how the price action behaves over a longer period of time.

------------ Delivering Factually Accurate Data That Traders Need------------

In light of the problems identified above, this indicator fixes all of these issue and delivers statistically correct information that discretionary and algorithmic traders can use, with truly accurate probabilities. It takes the price action of the last 2,000 candles and builds a huge dataset of distributions that you can directly select your percentiles from. It also allows you to have the positive and negative distributions calculated separately, or if you would like, you can pool all of them together in a combined distribution. In addition to this, there is a wide selection of moving averages directly available in the indicator to choose from.