NWOG with FVGThe New Week Opening Gap (NWOG) and Fair Value Gap (FVG) combined indicator is a trading tool designed to analyze price action and detect potential support, resistance, and trade entry opportunities based on two significant concepts:

New Week Opening Gap (NWOG): The price range between the high and low of the first candle of the new trading week.

Fair Value Gap (FVG): A price imbalance or gap between candlesticks, where price may retrace to fill the gap, indicating potential support or resistance zones.

When combined, these two concepts help traders identify key price levels (from the new week open) and price imbalances (from FVGs), which can act as powerful indicators for potential market reversals, retracements, or continuation trades.

1. New Week Opening Gap (NWOG):

Definition:

The New Week Opening Gap (NWOG) refers to the range between the high and low of the first candle in a new trading week (often, the Monday open in most markets).

Purpose:

NWOG serves as a significant reference point for market behavior throughout the week. Price action relative to this range helps traders identify:

Support and Resistance zones.

Bullish or Bearish sentiment depending on price’s relation to the opening gap levels.

Areas where the market may retrace or reverse before continuing in the primary trend.

How NWOG is Identified:

The high and low of the first candle of the new week are drawn on the chart, and these levels are used to assess the market's behavior relative to this range.

Trading Strategy Using NWOG:

Above the NWOG Range: If price is trading above the NWOG levels, it signals bullish sentiment.

Below the NWOG Range: If price is trading below the NWOG levels, it signals bearish sentiment.

Price Touching the NWOG Levels: If price approaches or breaks through the NWOG levels, it can indicate a potential retracement or reversal.

2. Fair Value Gap (FVG):

Definition:

A Fair Value Gap (FVG) occurs when there is a gap or imbalance between two consecutive candlesticks, where the high of one candle is lower than the low of the next candle (or vice versa), creating a zone that may act as a price imbalance.

Purpose:

FVGs represent an imbalance in price action, often indicating that the market moved too quickly and left behind a price region that was not fully traded.

FVGs can serve as areas where price is likely to retrace to fill the gap, as traders seek to correct the imbalance.

How FVG is Identified:

An FVG is detected if:

Bearish FVG: The high of one candle is less than the low of the next (gap up).

Bullish FVG: The low of one candle is greater than the high of the next (gap down).

The area between the gap is drawn as a shaded region, indicating the FVG zone.

Trading Strategy Using FVG:

Price Filling the FVG: Price is likely to retrace to fill the gap. A reversal candle in the FVG zone can indicate a trade setup.

Support and Resistance: FVG zones can act as support (in a bullish FVG) or resistance (in a bearish FVG) if the price retraces to them.

Combined Strategy: New Week Opening Gap (NWOG) and Fair Value Gap (FVG):

The combined use of NWOG and FVG helps traders pinpoint high-probability price action setups where:

The New Week Opening Gap (NWOG) acts as a major reference level for potential support or resistance.

Fair Value Gaps (FVG) represent market imbalances where price might retrace to, filling the gap before continuing its move.

Signal Logic:

Buy Signal:

Price touches or breaks above the NWOG range (indicating a bullish trend) and there is a bullish FVG present (gap indicating a support area).

Price retraces to fill the bullish FVG, offering a potential buy opportunity.

Sell Signal:

Price touches or breaks below the NWOG range (indicating a bearish trend) and there is a bearish FVG present (gap indicating a resistance area).

Price retraces to fill the bearish FVG, offering a potential sell opportunity.

Example:

Buy Setup:

Price breaks above the NWOG resistance level, and a bullish FVG (gap down) appears below. Traders can wait for price to pull back to fill the gap and then take a long position when confirmation occurs.

Sell Setup:

Price breaks below the NWOG support level, and a bearish FVG (gap up) appears above. Traders can wait for price to retrace and fill the gap before entering a short position.

Key Benefits of the Combined NWOG & FVG Indicator:

Combines Two Key Concepts:

NWOG provides context for the market's overall direction based on the start of the week.

FVG highlights areas where price imbalances exist and where price might retrace to, making it easier to spot entry points.

High-Probability Setups:

By combining these two strategies, the indicator helps traders spot high-probability trades based on major market levels (from NWOG) and price inefficiencies (from FVG).

Helps Identify Reversal and Continuation Opportunities:

FVGs act as potential support and resistance zones, and when combined with the context of the NWOG levels, it gives traders clearer guidance on where price might reverse or continue its trend.

Clear Visual Signals:

The indicator can plot the NWOG levels on the chart, and shade the FVG areas, providing a clean and easy-to-read chart with entry signals marked for buy and sell opportunities.

Conclusion:

The New Week Opening Gap (NWOG) and Fair Value Gap (FVG) combined indicator is a powerful tool for traders who use price action strategies. By incorporating the New Week's opening range and identifying gaps in price action, this indicator helps traders identify potential support and resistance zones, pinpoint entry opportunities, and increase the probability of successful trades.

This combined strategy enhances your analysis by adding layers of confirmation for trades based on significant market levels and price imbalances. Let me know if you'd like more details or modifications!

Pesquisar nos scripts por "gaps"

Multi-Timeframe Stochastic Alert [tradeviZion]# Multi-Timeframe Stochastic Alert : Complete User Guide

## 1. Introduction

### What is the Multi-Timeframe Stochastic Alert?

The Multi-Timeframe Stochastic Alert is an advanced technical analysis tool that helps traders identify potential trading opportunities by analyzing momentum across multiple timeframes. It combines the power of the stochastic oscillator with multi-timeframe analysis to provide more reliable trading signals.

### Key Features and Benefits

- Simultaneous analysis of 6 different timeframes

- Advanced alert system with customizable conditions

- Real-time visual feedback with color-coded signals

- Comprehensive data table with instant market insights

- Motivational trading messages for psychological support

- Flexible theme support for comfortable viewing

### How it Can Help Your Trading

- Identify stronger trends by confirming momentum across multiple timeframes

- Reduce false signals through multi-timeframe confirmation

- Stay informed of market changes with customizable alerts

- Make more informed decisions with comprehensive market data

- Maintain trading discipline with clear visual signals

## 2. Understanding the Display

### The Stochastic Chart

The main chart displays three key components:

1. ** K-Line (Fast) **: The primary stochastic line (default color: green)

2. ** D-Line (Slow) **: The signal line (default color: red)

3. ** Reference Lines **:

- Overbought Level (80): Upper dashed line

- Middle Line (50): Center dashed line

- Oversold Level (20): Lower dashed line

### The Information Table

The table provides a comprehensive view of stochastic readings across all timeframes. Here's what each column means:

#### Column Explanations:

1. ** Timeframe **

- Shows the time period for each row

- Example: "5" = 5 minutes, "15" = 15 minutes, etc.

2. ** K Value **

- The fast stochastic line value (0-100)

- Higher values indicate stronger upward momentum

- Lower values indicate stronger downward momentum

3. ** D Value **

- The slow stochastic line value (0-100)

- Helps confirm momentum direction

- Crossovers with K-line can signal potential trades

4. ** Status **

- Shows current momentum with symbols:

- ▲ = Increasing (bullish)

- ▼ = Decreasing (bearish)

- Color matches the trend direction

5. ** Trend **

- Shows the current market condition:

- "Overbought" (above 80)

- "Bullish" (above 50)

- "Bearish" (below 50)

- "Oversold" (below 20)

#### Row Explanations:

1. ** Title Row **

- Shows "🎯 Multi-Timeframe Stochastic"

- Indicates the indicator is active

2. ** Header Row **

- Contains column titles

- Dark blue background for easy reading

3. ** Timeframe Rows **

- Six rows showing different timeframe analyses

- Each row updates independently

- Color-coded for easy trend identification

4. **Message Row**

- Shows rotating motivational messages

- Updates every 5 bars

- Helps maintain trading discipline

### Visual Indicators and Colors

- ** Green Background **: Indicates bullish conditions

- ** Red Background **: Indicates bearish conditions

- ** Color Intensity **: Shows strength of the signal

- ** Background Highlights **: Appear when alert conditions are met

## 3. Core Settings Groups

### Stochastic Settings

These settings control the core calculation of the stochastic oscillator.

1. ** Length (Default: 14) **

- What it does: Determines the lookback period for calculations

- Higher values (e.g., 21): More stable, fewer signals

- Lower values (e.g., 8): More sensitive, more signals

- Recommended:

* Day Trading: 8-14

* Swing Trading: 14-21

* Position Trading: 21-30

2. ** Smooth K (Default: 3) **

- What it does: Smooths the main stochastic line

- Higher values: Smoother line, fewer false signals

- Lower values: More responsive, but more noise

- Recommended:

* Day Trading: 2-3

* Swing Trading: 3-5

* Position Trading: 5-7

3. ** Smooth D (Default: 3) **

- What it does: Smooths the signal line

- Works in conjunction with Smooth K

- Usually kept equal to or slightly higher than Smooth K

- Recommended: Keep same as Smooth K for consistency

4. ** Source (Default: Close) **

- What it does: Determines price data for calculations

- Options: Close, Open, High, Low, HL2, HLC3, OHLC4

- Recommended: Stick with Close for most reliable signals

### Timeframe Settings

Controls the multiple timeframes analyzed by the indicator.

1. ** Main Timeframes (TF1-TF6) **

- TF1 (Default: 10): Shortest timeframe for quick signals

- TF2 (Default: 15): Short-term trend confirmation

- TF3 (Default: 30): Medium-term trend analysis

- TF4 (Default: 30): Additional medium-term confirmation

- TF5 (Default: 60): Longer-term trend analysis

- TF6 (Default: 240): Major trend confirmation

Recommended Combinations:

* Scalping: 1, 3, 5, 15, 30, 60

* Day Trading: 5, 15, 30, 60, 240, D

* Swing Trading: 15, 60, 240, D, W, M

2. ** Wait for Bar Close (Default: true) **

- What it does: Controls when calculations update

- True: More reliable but slightly delayed signals

- False: Faster signals but may change before bar closes

- Recommended: Keep True for more reliable signals

### Alert Settings

#### Main Alert Settings

1. ** Enable Alerts (Default: true) **

- Master switch for all alert notifications

- Toggle this off when you don't want any alerts

- Useful during testing or when you want to focus on visual signals only

2. ** Alert Condition (Options) **

- "Above Middle": Bullish momentum alerts only

- "Below Middle": Bearish momentum alerts only

- "Both": Alerts for both directions

- Recommended:

* Trending Markets: Choose direction matching the trend

* Ranging Markets: Use "Both" to catch reversals

* New Traders: Start with "Both" until you develop a specific strategy

3. ** Alert Frequency **

- "Once Per Bar": Immediate alerts during the bar

- "Once Per Bar Close": Alerts only after bar closes

- Recommended:

* Day Trading: "Once Per Bar" for quick reactions

* Swing Trading: "Once Per Bar Close" for confirmed signals

* Beginners: "Once Per Bar Close" to reduce false signals

#### Timeframe Check Settings

1. ** First Check (TF1) **

- Purpose: Confirms basic trend direction

- Alert Triggers When:

* For Bullish: Stochastic is above middle line (50)

* For Bearish: Stochastic is below middle line (50)

* For Both: Triggers in either direction based on position relative to middle line

- Settings:

* Enable/Disable: Turn first check on/off

* Timeframe: Default 5 minutes

- Best Used For:

* Quick trend confirmation

* Entry timing

* Scalping setups

2. ** Second Check (TF2) **

- Purpose: Confirms both position and momentum

- Alert Triggers When:

* For Bullish: Stochastic is above middle line AND both K&D lines are increasing

* For Bearish: Stochastic is below middle line AND both K&D lines are decreasing

* For Both: Triggers based on position and direction matching current condition

- Settings:

* Enable/Disable: Turn second check on/off

* Timeframe: Default 15 minutes

- Best Used For:

* Trend strength confirmation

* Avoiding false breakouts

* Day trading setups

3. ** Third Check (TF3) **

- Purpose: Confirms overall momentum direction

- Alert Triggers When:

* For Bullish: Both K&D lines are increasing (momentum confirmation)

* For Bearish: Both K&D lines are decreasing (momentum confirmation)

* For Both: Triggers based on matching momentum direction

- Settings:

* Enable/Disable: Turn third check on/off

* Timeframe: Default 30 minutes

- Best Used For:

* Major trend confirmation

* Swing trading setups

* Avoiding trades against the main trend

Note: All three conditions must be met simultaneously for the alert to trigger. This multi-timeframe confirmation helps reduce false signals and provides stronger trade setups.

#### Alert Combinations Examples

1. ** Conservative Setup **

- Enable all three checks

- Use "Once Per Bar Close"

- Timeframe Selection Example:

* First Check: 15 minutes

* Second Check: 1 hour (60 minutes)

* Third Check: 4 hours (240 minutes)

- Wider gaps between timeframes reduce noise and false signals

- Best for: Swing trading, beginners

2. ** Aggressive Setup **

- Enable first two checks only

- Use "Once Per Bar"

- Timeframe Selection Example:

* First Check: 5 minutes

* Second Check: 15 minutes

- Closer timeframes for quicker signals

- Best for: Day trading, experienced traders

3. ** Balanced Setup **

- Enable all checks

- Use "Once Per Bar"

- Timeframe Selection Example:

* First Check: 5 minutes

* Second Check: 15 minutes

* Third Check: 1 hour (60 minutes)

- Balanced spacing between timeframes

- Best for: All-around trading

### Visual Settings

#### Alert Visual Settings

1. ** Show Background Color (Default: true) **

- What it does: Highlights chart background when alerts trigger

- Benefits:

* Makes signals more visible

* Helps spot opportunities quickly

* Provides visual confirmation of alerts

- When to disable:

* If using multiple indicators

* When preferring a cleaner chart

* During manual backtesting

2. ** Background Transparency (Default: 90) **

- Range: 0 (solid) to 100 (invisible)

- Recommended Settings:

* Clean Charts: 90-95

* Multiple Indicators: 85-90

* Single Indicator: 80-85

- Tip: Adjust based on your chart's overall visibility

3. ** Background Colors **

- Bullish Background:

* Default: Green

* Indicates upward momentum

* Customizable to match your theme

- Bearish Background:

* Default: Red

* Indicates downward momentum

* Customizable to match your theme

#### Level Settings

1. ** Oversold Level (Default: 20) **

- Traditional Setting: 20

- Adjustable Range: 0-100

- Usage:

* Lower values (e.g., 10): More conservative

* Higher values (e.g., 30): More aggressive

- Trading Applications:

* Potential bullish reversal zone

* Support level in uptrends

* Entry point for long positions

2. ** Overbought Level (Default: 80) **

- Traditional Setting: 80

- Adjustable Range: 0-100

- Usage:

* Lower values (e.g., 70): More aggressive

* Higher values (e.g., 90): More conservative

- Trading Applications:

* Potential bearish reversal zone

* Resistance level in downtrends

* Exit point for long positions

3. ** Middle Line (Default: 50) **

- Purpose: Trend direction separator

- Applications:

* Above 50: Bullish territory

* Below 50: Bearish territory

* Crossing 50: Potential trend change

- Trading Uses:

* Trend confirmation

* Entry/exit trigger

* Risk management level

#### Color Settings

1. ** Bullish Color (Default: Green) **

- Used for:

* K-Line (Main stochastic line)

* Status symbols when trending up

* Trend labels for bullish conditions

- Customization:

* Choose colors that stand out

* Match your trading platform theme

* Consider color blindness accessibility

2. ** Bearish Color (Default: Red) **

- Used for:

* D-Line (Signal line)

* Status symbols when trending down

* Trend labels for bearish conditions

- Customization:

* Choose contrasting colors

* Ensure visibility on your chart

* Consider monitor settings

3. ** Neutral Color (Default: Gray) **

- Used for:

* Middle line (50 level)

- Customization:

* Should be less prominent

* Easy on the eyes

* Good background contrast

### Theme Settings

1. **Color Theme Options**

- Dark Theme (Default):

* Dark background with white text

* Optimized for dark chart backgrounds

* Reduces eye strain in low light

- Light Theme:

* Light background with black text

* Better visibility in bright conditions

- Custom Theme:

* Use your own color preferences

2. ** Available Theme Colors **

- Table Background

- Table Text

- Table Headers

Note: The theme affects only the table display colors. The stochastic lines and alert backgrounds use their own color settings.

### Table Settings

#### Position and Size

1. ** Table Position **

- Options:

* Top Right (Default)

* Middle Right

* Bottom Right

* Top Left

* Middle Left

* Bottom Left

- Considerations:

* Chart space utilization

* Personal preference

* Multiple monitor setups

2. ** Text Sizes **

- Title Size Options:

* Tiny: Minimal space usage

* Small: Compact but readable

* Normal (Default): Standard visibility

* Large: Enhanced readability

* Huge: Maximum visibility

- Data Size Options:

* Recommended: One size smaller than title

* Adjust based on screen resolution

* Consider viewing distance

3. ** Empowering Messages **

- Purpose:

* Maintain trading discipline

* Provide psychological support

* Remind of best practices

- Rotation:

* Changes every 5 bars

* Categories include:

- Market Wisdom

- Strategy & Discipline

- Mindset & Growth

- Technical Mastery

- Market Philosophy

## 4. Setting Up for Different Trading Styles

### Day Trading Setup

1. **Timeframes**

- Primary: 5, 15, 30 minutes

- Secondary: 1H, 4H

- Alert Settings: "Once Per Bar"

2. ** Stochastic Settings **

- Length: 8-14

- Smooth K/D: 2-3

- Alert Condition: Match market trend

3. ** Visual Settings **

- Background: Enabled

- Transparency: 85-90

- Theme: Based on trading hours

### Swing Trading Setup

1. ** Timeframes **

- Primary: 1H, 4H, Daily

- Secondary: Weekly

- Alert Settings: "Once Per Bar Close"

2. ** Stochastic Settings **

- Length: 14-21

- Smooth K/D: 3-5

- Alert Condition: "Both"

3. ** Visual Settings **

- Background: Optional

- Transparency: 90-95

- Theme: Personal preference

### Position Trading Setup

1. ** Timeframes **

- Primary: Daily, Weekly

- Secondary: Monthly

- Alert Settings: "Once Per Bar Close"

2. ** Stochastic Settings **

- Length: 21-30

- Smooth K/D: 5-7

- Alert Condition: "Both"

3. ** Visual Settings **

- Background: Disabled

- Focus on table data

- Theme: High contrast

## 5. Troubleshooting Guide

### Common Issues and Solutions

1. ** Too Many Alerts **

- Cause: Settings too sensitive

- Solutions:

* Increase timeframe intervals

* Use "Once Per Bar Close"

* Enable fewer timeframe checks

* Adjust stochastic length higher

2. ** Missed Signals **

- Cause: Settings too conservative

- Solutions:

* Decrease timeframe intervals

* Use "Once Per Bar"

* Enable more timeframe checks

* Adjust stochastic length lower

3. ** False Signals **

- Cause: Insufficient confirmation

- Solutions:

* Enable all three timeframe checks

* Use larger timeframe gaps

* Wait for bar close

* Confirm with price action

4. ** Visual Clarity Issues **

- Cause: Poor contrast or overlap

- Solutions:

* Adjust transparency

* Change theme settings

* Reposition table

* Modify color scheme

### Best Practices

1. ** Getting Started **

- Start with default settings

- Use "Both" alert condition

- Enable all timeframe checks

- Wait for bar close

- Monitor for a few days

2. ** Fine-Tuning **

- Adjust one setting at a time

- Document changes and results

- Test in different market conditions

- Find your optimal timeframe combination

- Balance sensitivity with reliability

3. ** Risk Management **

- Don't trade against major trends

- Confirm signals with price action

- Use appropriate position sizing

- Set clear stop losses

- Follow your trading plan

4. ** Regular Maintenance **

- Review settings weekly

- Adjust for market conditions

- Update color scheme for visibility

- Clean up chart regularly

- Maintain trading journal

## 6. Tips for Success

1. ** Entry Strategies **

- Wait for all timeframes to align

- Confirm with price action

- Use proper position sizing

- Consider market conditions

2. ** Exit Strategies **

- Trail stops using indicator levels

- Take partial profits at targets

- Honor your stop losses

- Don't fight the trend

3. ** Psychology **

- Stay disciplined with settings

- Don't override system signals

- Keep emotions in check

- Learn from each trade

4. ** Continuous Improvement **

- Record your trades

- Review performance regularly

- Adjust settings gradually

- Stay educated on markets

ICT FVG [TheFundedRoad]This indicator shows you all ICT Fair value gaps on chart with midpoint line

Fair value gap is a gap in a set of 3 candles, in a bullish FVG you have 1st candle high being lower than third candle low, and in a bearish FVG you have first candle low higher than third candle high, thats how this indicator finds these fair value gaps

It draws the fair value gap from the 2nd candle forward

You can customize the color and if you want to see the midpoint or not, midpoint is 50% of the gap

Pivotal Point Detection

The indicator highlights price gaps (overnight gaps) with significantly increased volume in the daily chart only. These price jumps can occur after earnings reports or other significant news and often point to an important event (e.g., a new product or business model). According to Jesse Livermore, these are called Pivotal Points.

The price jumps displayed by the indicator are not a guarantee that they represent a true Pivotal Point, but they provide a hint of a significant business development - especially when they occur repeatedly alongside revenue growth. This can help identify potentially strong growth stocks and high-performing investments. However, the underlying events and connections must be investigated through additional research.

make posible to find stocks like:

NYSE:PLTR NASDAQ:ROOT NASDAQ:NVDA NYSE:CVNA NYSE:LRN

A "pivotal price line" is drawn at the opening price of the Pivotal Point. This line is considered a support level. If the price falls below this line, the Pivotal Point loses its validity.

Wick Trend Analysis - AYNETScientific Explanation

1. Wick Trend Lines

Upper Wick Trend Line: The upper_wick_trend is calculated as the Simple Moving Average (SMA) of the upper wick lengths over the user-defined period (trend_length).

pinescript

Kodu kopyala

float upper_wick_trend = ta.sma(upper_wick_length, trend_length)

Lower Wick Trend Line: The lower_wick_trend is similarly calculated for the lower wick lengths.

pinescript

Kodu kopyala

float lower_wick_trend = ta.sma(lower_wick_length, trend_length)

2. Filling Between Lines

fill Function: The fill function colors the area between two plotted lines (plot_upper and plot_lower) based on a defined condition.

pinescript

Kodu kopyala

fill(plot_upper, plot_lower, color=fill_color, title="Wick Trend Area")

Condition for Coloring: The color is determined based on whether the upper wick trend is greater or less than the lower wick trend:

Green Fill: Indicates that the upper wick trend is dominant (i.e., upper_wick_trend > lower_wick_trend).

Red Fill: Indicates that the lower wick trend is dominant (i.e., upper_wick_trend <= lower_wick_trend).

Visualization Features

Trend Lines:

Upper wick trend is plotted as a green line.

Lower wick trend is plotted as a red line.

Filled Area:

The area between the two trend lines is filled:

Green when the upper wick trend is dominant.

Red when the lower wick trend is dominant.

Dynamic Adjustments:

The user can adjust the trend_length to change the sensitivity of the SMA calculations.

Applications

Sentiment Analysis:

Green Fill (Upper Trend Dominance): Indicates stronger rejection at higher prices, suggesting bearish sentiment.

Red Fill (Lower Trend Dominance): Indicates stronger rejection at lower prices, suggesting bullish sentiment.

Signal Generation:

Transitions in the fill color (from green to red or vice versa) can serve as potential trade signals.

Volatility Assessment:

Wider gaps between the trend lines indicate higher market volatility, while narrower gaps suggest lower volatility.

Enhancements

1. Trend Strength Filtering

Add thresholds to filter out minor trends or insignificant wick activity:

pinescript

Kodu kopyala

bool significant_upper_wick = upper_wick_length > 10 // Minimum length for upper wick

bool significant_lower_wick = lower_wick_length > 10

2. Alerts for Trend Changes

Trigger alerts when the dominance of the trend changes:

pinescript

Kodu kopyala

alertcondition(upper_wick_trend > lower_wick_trend, title="Upper Wick Dominance", message="Upper wick trend is now dominant.")

alertcondition(lower_wick_trend > upper_wick_trend, title="Lower Wick Dominance", message="Lower wick trend is now dominant.")

3. Combined Wick Analysis

Incorporate total wick activity (upper + lower wicks) for holistic analysis:

pinescript

Kodu kopyala

float total_wick_trend = ta.sma(upper_wick_length + lower_wick_length, trend_length)

Conclusion

This script provides a robust visualization of wick trends with dynamic color filling to indicate trend dominance. By observing the relative strength of upper and lower wick trends, traders can assess market sentiment, detect potential reversals, and gauge volatility. This method can be further enhanced with additional filters, alerts, and composite indicators to refine trading strategies.

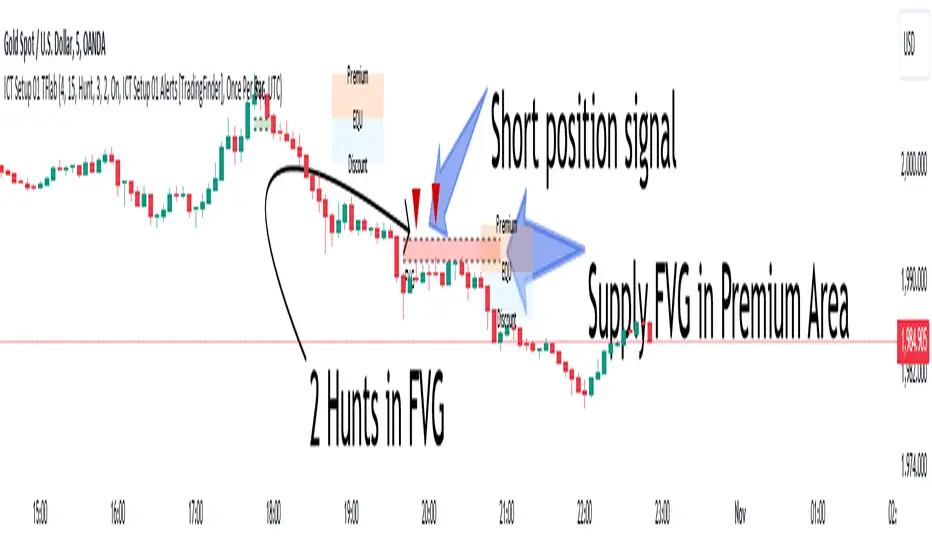

ICT Setup 03 [TradingFinder] Judas Swing NY 9:30am + CHoCH/FVG🔵 Introduction

Judas Swing is an advanced trading setup designed to identify false price movements early in the trading day. This advanced trading strategy operates on the principle that major market players, or "smart money," drive price in a certain direction during the early hours to mislead smaller traders.

This deceptive movement attracts liquidity at specific levels, allowing larger players to execute primary trades in the opposite direction, ultimately causing the price to return to its true path.

The Judas Swing setup functions within two primary time frames, tailored separately for Forex and Stock markets. In the Forex market, the setup uses the 8:15 to 8:30 AM window to identify the high and low points, followed by the 8:30 to 8:45 AM frame to execute the Judas move and identify the CISD Level break, where Order Block and Fair Value Gap (FVG) zones are subsequently detected.

In the Stock market, these time frames shift to 9:15 to 9:30 AM for identifying highs and lows and 9:30 to 9:45 AM for executing the Judas move and CISD Level break.

Concepts such as Order Block and Fair Value Gap (FVG) are crucial in this setup. An Order Block represents a chart region with a high volume of buy or sell orders placed by major financial institutions, marking significant levels where price reacts.

Fair Value Gap (FVG) refers to areas where price has moved rapidly without balance between supply and demand, highlighting zones of potential price action and future liquidity.

Bullish Setup :

Bearish Setup :

🔵 How to Use

The Judas Swing setup enables traders to pinpoint entry and exit points by utilizing Order Block and FVG concepts, helping them align with liquidity-driven moves orchestrated by smart money. This setup applies two distinct time frames for Forex and Stocks to capture early deceptive movements, offering traders optimized entry or exit moments.

🟣 Bullish Setup

In the Bullish Judas Swing setup, the first step is to identify High and Low points within the initial time frame. These levels serve as key points where price may react, forming the basis for analyzing the setup and assisting traders in anticipating future market shifts.

In the second time frame, a critical stage of the bullish setup begins. During this phase, the price may create a false break or Fake Break below the low level, a deceptive move by major players to absorb liquidity. This false move often causes smaller traders to enter positions incorrectly. After this fake-out, the price reverses upward, breaking the CISD Level, a critical point in the market structure, signaling a potential bullish trend.

Upon breaking the CISD Level and reversing upward, the indicator identifies both the Order Block and Fair Value Gap (FVG). The Order Block is an area where major players typically place large buy orders, signaling potential price support. Meanwhile, the FVG marks a region of supply-demand imbalance, signaling areas where price might react.

Ultimately, after these key zones are identified, a trader may open a buy position if the price reaches one of these critical areas—Order Block or FVG—and reacts positively. Trading at these levels enhances the chance of success due to liquidity absorption and support from smart money, marking an opportune time for entering a long position.

🟣 Bearish Setup

In the Bearish Judas Swing setup, analysis begins with marking the High and Low levels in the initial time frame. These levels serve as key zones where price could react, helping to signal possible trend reversals. Identifying these levels is essential for locating significant bearish zones and positioning traders to capitalize on downward movements.

In the second time frame, the primary bearish setup unfolds. During this stage, price may exhibit a Fake Break above the high, causing a brief move upward and misleading smaller traders into incorrect positions. After this false move, the price typically returns downward, breaking the CISD Level—a crucial bearish trend indicator.

With the CISD Level broken and a bearish trend confirmed, the indicator identifies the Order Block and Fair Value Gap (FVG). The Bearish Order Block is a region where smart money places significant sell orders, prompting a negative price reaction. The FVG denotes an area of supply-demand imbalance, signifying potential selling pressure.

When the price reaches one of these critical areas—the Bearish Order Block or FVG—and reacts downward, a trader may initiate a sell position. Entering trades at these levels, due to increased selling pressure and liquidity absorption, offers traders an advantage in profiting from price declines.

🔵 Settings

Market : The indicator allows users to choose between Forex and Stocks, automatically adjusting the time frames for the "Opening Range" and "Trading Permit" accordingly: Forex: 8:15–8:30 AM for identifying High and Low points, and 8:30–8:45 AM for capturing the Judas move and CISD Level break. Stocks: 9:15–9:30 AM for identifying High and Low points, and 9:30–9:45 AM for executing the Judas move and CISD Level break.

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

CISD : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

🔵 Conclusion

The Judas Swing indicator helps traders spot reliable trading opportunities by detecting false price movements and key levels such as Order Block and FVG. With a focus on early market movements, this tool allows traders to align with major market participants, selecting entry and exit points with greater precision, thereby reducing trading risks.

Its extensive customization options enable adjustments for various market types and trading conditions, giving traders the flexibility to optimize their strategies. Based on ICT techniques and liquidity analysis, this indicator can be highly effective for those seeking precision in their entry points.

Overall, Judas Swing empowers traders to capitalize on significant market movements by leveraging price volatility. Offering precise and dependable signals, this tool presents an excellent opportunity for enhancing trading accuracy and improving performance

Average Bullish & Bearish Percentage ChangeAverage Bullish & Bearish Percentage Change

Processes two key aspects of directional market movements relative to price levels. Unlike traditional momentum tools, it separately calculates the average of positive and negative percentage changes in price using user-defined independent counts of actual past bullish and bearish candles. This approach delivers comprehensive and precise view of average percentage changes.

FEATURES:

Count-Based Averages: Separate averaging of bullish and bearish %𝜟 based on their respective number of occurrences ensures reliable and precise momentum calculations.

Customizable Averaging: User-defined number of candle count sets number of past bullish and bearish candles used in independent averaging.

Two Methods of Candle Metrics:

1. Net Move: Focuses on the body range of the candle, emphasizing the net directional movement.

2. Full Capacity: Incorporates wicks and gaps to capture full potential of the bar.

The indicator classifies Doji candles contextually, ensuring they are appropriately factored into the bullish or bearish metrics to avoid mistakes in calculation:

1. Standard Doji - open equals close.

2. Flat Close Doji - Candles where the close matches the previous close.

Timeframe Flexibility:

The indicator can be applied across any desired timeframe, allowing for seamless multi-timeframe analysis.

HOW TO USE

Select Method of Bar Metrics:

Net Move: For analyzing markets where price changes are consistent and bars are close to each other.

Full Capacity: Incorporates wicks and gaps, providing relevant figures for markets like stocks

Set the number of past candles to average:

🟩 Average Past Bullish Candles (Default: 10)

🟥 Average Past Bullish Candles (Default: 10)

Why Percentage Change Is Important

Standardized Measurement Across Assets:

Percentage change normalizes price movements, making it easier to compare different assets with varying price levels. For example, a $1 move in a $10 stock is significant, but the same $1 move in a $1,000 stock is negligible.

Highlights Relative Impact:

By measuring the price change as a percentage of the close, traders can better understand the relative impact of a move on the asset’s overall value.

Volatility Insights:

A high percentage change indicates heightened volatility, which can be a signal of potential opportunities or risks, making it more actionable than raw price changes. Percents directly reflect the strength of buying or selling pressure, providing a clearer view of momentum compared to raw price moves, which may not account for the relative size of the move.

By focusing on percentage change, this indicator provides a normalized, actionable, and insightful measure of market momentum, which is critical for comparing, analyzing, and acting on price movements across various assets and conditions.

ICT Open Range Gap & 1st FVG (fadi)In his 2024 mentorship program, ICT detailed how price action interacts with Open Range Gaps and the initial 1-minute Fair Value Gap following the market open at 9:30 AM.

What is an Open Range Gap?

An Open Range Gap occurs when the market opens at 9:30 AM at a higher or lower level compared to the previous day's close at 4:14 PM, primarily relevant in futures trading. According to ICT, there is a statistical probability of 70% that the price action will close 50% or more of the Open Range Gap within the first 30 minutes of trading (9:30 AM to 10:00 AM).

What is the First 1-Minute Fair Value Gap?

ICT places significant emphasis on the first 1-minute Fair Value Gap (FVG) that forms after the market opens at 9:30 AM. The FVG must occur at 9:31 AM or later to be considered valid. This gap often presents key opportunities for traders, as it represents a temporary imbalance between supply and demand that the market seeks to correct.

Understanding and leveraging these patterns can enhance trading strategies by offering insights into potential price movements shortly after market open.

ICT Open Range Gap & 1st FVG

This indicator is engineered to identify and highlight the Open Range Gaps and the first 1-minute Fair Value Gap. Furthermore, it functions across multiple timeframes, from seconds to hours, catering to various trading preferences. This flexibility is particularly beneficial for traders who favor higher timeframes or wish to observe these patterns' application at broader intervals.

Settings

The Open Range Gap indicator offers flexible display settings. It identifies the quadrants and provides optional color coding to distinguish them. Additionally, it tracks the "fill" level to visualize how far the price action has progressed into the gap, enhancing traders' ability to monitor and analyze price movements effectively. By default, the Open Range Gap will stop extending at 10:00 AM; however, there is an option to continue extending until the end of the trading day.

The 1st Fair Value Gap (FVG) can be viewed on any timeframe the indicator is active on, offering various styling options to match each trader's preferences. While the 1st FVG is particularly relevant to the day it is created, previous 1st FVGs within the same week may provide additional value. This indicator allows traders to extend Monday's 1st FVG, marking the first FVG of the week, or to extend all 1st FVGs throughout the week.

Connors RSI with Down GapThe Connors RSI with Down Gap indicator is a technical tool designed to support Larry Connors' Terror Gap Strategy, which is part of his broader framework outlined in the book "Buy the Fear, Sell the Greed: 7 Behavioral Quant Strategies for Traders." This specific indicator integrates the ConnorsRSI calculation with a focus on detecting down gaps in price, providing insights into moments when panic selling may occur.

The ConnorsRSI

ConnorsRSI is a composite indicator developed by Larry Connors that combines three core components:

RSI: A short-term relative strength index measuring the speed and magnitude of price changes.

Streak RSI: Tracks consecutive up or down closes to assess momentum.

Percent Rank: Evaluates how the current close ranks in relation to past prices.

When combined, these three elements provide a nuanced view of short-term overbought or oversold conditions. ConnorsRSI readings below a certain threshold (commonly 30 or lower) suggest that the asset has been heavily sold, indicating potential exhaustion of selling pressure.

Behavioral Finance Insights

The Terror Gap Strategy is grounded in principles from behavioral finance, which studies how psychological factors affect market participants' decision-making. Specifically, the indicator exploits the fear and irrational behavior that often arise when traders face persistent losses, especially after a down gap. According to behavioral finance theories like prospect theory (Kahneman & Tversky, 1979), people tend to overreact to losses, leading to panic selling. This creates opportunities for contrarian traders who understand the psychology behind these market movements.

The ConnorsRSI with Down Gap indicator works because it identifies:

Overextended selling through the ConnorsRSI, where persistent price declines result in low RSI values (indicating panic).

Gap down days, where the opening price is below the previous day’s close, typically amplifying the sense of loss and fear for traders already in losing positions.

Why This Indicator Works

The psychology of losses makes traders more prone to selling during periods of fear, especially when confronted with a gap down after sustained price declines. This indicator, by combining ConnorsRSI with down gaps, offers a quantitative way to spot these moments of panic. Traders can take advantage of these signals to enter positions when the market is in a state of fear, often when there is potential for a reversion to the mean.

Indicator Mechanics

In the current implementation:

The ConnorsRSI is calculated using three components: a short-term RSI, streak RSI, and percent rank.

When the ConnorsRSI drops below a user-defined lower threshold, the indicator highlights oversold conditions.

If there is a down gap (open price lower than the previous close) and the ConnorsRSI is below the threshold, a label is displayed, signaling a potential opportunity to buy.

Practical Use and Application

For traders looking to implement the Terror Gap Strategy, this indicator provides a clear visual cue (via background coloring and labels) when conditions are ripe for a contrarian trade. It can be particularly useful for traders who thrive on taking advantage of fear-driven sell-offs.

However, to fully understand and apply this strategy effectively, it is recommended to purchase Larry Connors' book "Buy the Fear, Sell the Greed." The book provides detailed explanations of how to execute the strategy with precision, including insights into exit conditions, scaling into positions, and managing risk.

Conclusion

The ConnorsRSI with Down Gap indicator combines quantitative analysis with behavioral finance principles to exploit fear-driven market behavior. By utilizing this tool within a disciplined trading strategy, traders can potentially profit from temporary market inefficiencies caused by panic selling.

References

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Connors, L. (2013). Buy the Fear, Sell the Greed: 7 Behavioral Quant Strategies for Traders.

This indicator can be a valuable asset, but understanding its proper use within a broader strategy framework is essential. Purchasing Connors' book is a recommended step toward mastering the approach.

Volume Analysis - Heatmap and Volume ProfileHello All!

I have a new toy for you! Volume Analysis - Heatmap and Volume Profile . Honestly I started to work to develop Volume Heatmap then I decided to improve it and add more features such Volume profile, volume, difference in Buy/Sell volumes etc. I tried to put my abilities into this script and tried to use some new Pine Language™ features ( method, force_overlay, enum etc features ). I hope the usage of these new features would be an example for Pine Programmers.

Lets talk about how it works:

- It gets number of Rows/Columns from the user for each candle to create heatmap

- It calculates the number of the candles to analyze. Number of the candles may change by number of Rows/columns or if any volume / difference in volumes / volume profile is enabled

- It gets Closing/Opening price, Volume and Time info from lower time frame for each candle ( it can be up to 100K for each candle )

- After getting the data it calculates lower time frame to analyze

- Then it calculates how closing price moves, how much volume on each move and create boxes by the volume/move in each box

- The colors for each box calculated by volume info and closing price movements in the lower time frame

- It shows the boxes on Absolute places or Zero Line optionally

- it shows Volume, Cumulative volume, Difference between Buy/Sell volume for each column

- it changes empty box color by Chart background color, also you can change transparency

- At this time it creates Volume Profile with up to 25 rows

- As a new Pine Language™ feature, it can show Volume Profile in the indicator window or in Main chart, shows Value Area, Value Area High (VAH), Value Area Low (VAL), and draw it and POC (Point Of Control) in the indicator window and/or in the main chart

- Honestly the feature I like is that: For the markets that are not open 24/7, it combines the data from the lower time period without any gaps. For example, if you work for a market that is closed on Saturdays and Sundays, it ensures data integrity by omitting weekends and holidays. so for example if the data is like "ABC---DEF-X---YL-Z" then it makes this data like "ABCDEFXYLZ". In this way, there will be no data breaks in the displayed boxes, there will be no empty colons, and it will appear as if data is coming in at any time.

- Finally it shows Info Panel to give info, its background color automatically changes by the Chart background color

- Important! You should set your "Plan" accordingly, your plan is "Premium or Higher" or "Lower tier". so the script can understand the minimum time frame it can get data!!

I tried to share many screenshots below to explain it much better

How it looks?

it shows Highest Buy/Sell volumes brighter, move volume -> brighter

Volume Profile ( up to 25 row s) ( number of contained candles should be more than 1 )

Volume Profile can be shown in the main chart optionally

How the main chart looks:

Closing price shown and you can enable it, change colors & line width

Can include many candles according to Row&Column number you set

Optionally it can show cumulative volume for each candle

Closing prices from lower time frame

Shows Candle Body by changing background colors

It can shows all included candles on Zero line

You can change the colors of many things

You can set Empty box and border transparency

Table, Empty box Colors adjustment done automatically by chart background color

Sometimes we can not get data from some historical candles if time frame is high such 2days, 1 week etc, and it looks like:

It also checks if Chart time frame and Chart type is suitable

Enjoy!

DP-OCR MTF & MA 2024This script developed is designed for multi-timeframe analysis of previous open, close, and range, with additional signal plots based on various percentage extension levels. It also incorporates EMA calculations for crossover strategies. Here's a quick breakdown of what the script does:

Key Features:

1. Timeframes:

o Two separate timeframes (TF1 and TF2), which can be set by the user (e.g., 15 mins, 30 mins, daily, etc.). The script computes price actions and extensions for both timeframes. For better analysis, use Daily in TF1 and Weekly in TF2

2. Extension Levels:

o Calculates and plots 10%, 21%, 31%, 51%, and 61% extensions (both positive and negative) for each timeframe.

o The most commonly used extension levels are 61%, 31%, -61%, and -21%.

o These extension levels can be turned on or off by the user.

3. Open/Close/Range:

o Tracks the high, low, open, and close for both timeframes.

o Highlights open/close gaps.

o Plots the previous high/low range for both timeframes with a fill and different colors based on price movement.

How to Use:

• You can toggle specific extension levels on or off in the script’s settings.

• For example, when price hits a +61% extension, it could signal a breakout, and when it hits a -61% extension, it may indicate a potential retracement.

• Use these levels in conjunction with your price action analysis to set entry/exit points or stop-loss levels.

4. Today’s Open:

o Plots today’s opening price for both timeframes.

How to Use:

• Use today’s open as a key reference point to determine the day’s price action.

• Compare today’s open with the previous high/low or extension levels to evaluate possible trends or reversals.

5. EMA Calculations:

o The script calculates 5, 15, and 20 period EMAs and plots them on the chart.

o Additional EMA crossover signals can be included for strategy optimization.

How to Use:

• Observe the EMAs for potential crossover signals. For example, a 5-period EMA crossing above a 15-period or 20-period EMA may signal a buy opportunity, while a crossover in the opposite direction may signal a sell.

• Combine the EMA crossovers with extension levels or previous price data to refine your entries and exits.

Customizations Available:

• Users can select whether to display extension levels for either timeframe.

• The script allows automatic adaptation to intraday, daily, weekly, or monthly timeframes based on the current chart settings.

Moreover, the extension levels are calculated based on the previous period’s range, with the most commonly usable extension levels being 61, 31, -61, and -21. These levels are often used for identifying potential price retracements, breakouts, or reversal points in technical analysis.

JordanSwindenLibraryLibrary "JordanSwindenLibrary"

TODO: add library description here

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

getPipSize(multiplier)

Calculates the pip size of the current market

Parameters:

multiplier (int) : The mintick point multiplier (1 by default, 10 for FX/Crypto/CFD but can be used to override when certain markets require)

Returns: The pip size for the current market

truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places

Parameters:

number (float) : The number to truncate

decimalPlaces (simple float) : (default=2) The number of decimal places to truncate to

Returns: The given number truncated to the given decimalPlaces

toWhole(number)

Converts pips into whole numbers

Parameters:

number (float) : The pip number to convert into a whole number

Returns: The converted number

toPips(number)

Converts whole numbers back into pips

Parameters:

number (float) : The whole number to convert into pips

Returns: The converted number

getPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period

Parameters:

value1 (float) : The first value to reference

value2 (float) : The second value to reference

lookback (int) : The lookback period to analyze

Returns: The percent change over the two values and lookback period

random(minRange, maxRange)

Wichmann–Hill Pseudo-Random Number Generator

Parameters:

minRange (float) : The smallest possible number (default: 0)

maxRange (float) : The largest possible number (default: 1)

Returns: A random number between minRange and maxRange

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(length, maType)

Gets a Moving Average based on type (! MUST BE CALLED ON EVERY TICK TO BE ACCURATE, don't place in scopes)

Parameters:

length (simple int) : The MA period

maType (string) : The type of MA

Returns: A moving average with the given parameters

barsAboveMA(lookback, ma)

Counts how many candles are above the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(lookback, ma)

Counts how many candles are below the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently (based on closing prices)

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many times price recently crossed the EMA (based on closing prices)

getPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

lookback (int) : The lookback period to look back over

direction (int) : The color of the bar to count (1 = Green, -1 = Red)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize()

Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize()

Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize()

Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent()

Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(fib, colorMatch)

Checks if the current bar is a hammer candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(fib, colorMatch)

Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(wickSize, bodySize)

Checks if the current bar is a doji candle based on the given parameters

Parameters:

wickSize (float) : (default=2) The maximum top wick size compared to the bottom (and vice versa)

bodySize (float) : (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bullish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bearish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

isInsideBar()

Detects inside bars

Returns: Returns true if the current bar is an inside bar

isOutsideBar()

Detects outside bars

Returns: Returns true if the current bar is an outside bar

barInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls within the given time session

barOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls outside the given time session

dateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range

Parameters:

startTime (int) : The UNIX date timestamp to begin searching from

endTime (int) : the UNIX date timestamp to stop searching from

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze

Parameters:

monday (bool) : Should the script analyze this day? (true/false)

tuesday (bool) : Should the script analyze this day? (true/false)

wednesday (bool) : Should the script analyze this day? (true/false)

thursday (bool) : Should the script analyze this day? (true/false)

friday (bool) : Should the script analyze this day? (true/false)

saturday (bool) : Should the script analyze this day? (true/false)

sunday (bool) : Should the script analyze this day? (true/false)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter(atrValue, maxSize)

Parameters:

atrValue (float)

maxSize (float)

tradeCount()

Calculate total trade count

Returns: Total closed trade count

isLong()

Check if we're currently in a long trade

Returns: True if our position size is positive

isShort()

Check if we're currently in a short trade

Returns: True if our position size is negative

isFlat()

Check if we're currentlyflat

Returns: True if our position size is zero

wonTrade()

Check if this bar falls after a winning trade

Returns: True if we just won a trade

lostTrade()

Check if this bar falls after a losing trade

Returns: True if we just lost a trade

maxDrawdownRealized()

Gets the max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

Returns: The max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

totalPipReturn()

Gets the total amount of pips won/lost (as a whole number)

Returns: Total amount of pips won/lost (as a whole number)

longWinCount()

Count how many winning long trades we've had

Returns: Long win count

shortWinCount()

Count how many winning short trades we've had

Returns: Short win count

longLossCount()

Count how many losing long trades we've had

Returns: Long loss count

shortLossCount()

Count how many losing short trades we've had

Returns: Short loss count

breakEvenCount(allowanceTicks)

Count how many break-even trades we've had

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even count

longCount()

Count how many long trades we've taken

Returns: Long trade count

shortCount()

Count how many short trades we've taken

Returns: Short trade count

longWinPercent()

Calculate win rate of long trades

Returns: Long win rate (0-100)

shortWinPercent()

Calculate win rate of short trades

Returns: Short win rate (0-100)

breakEvenPercent(allowanceTicks)

Calculate break even rate of all trades

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even win rate (0-100)

averageRR()

Calculate average risk:reward

Returns: Average winning trade divided by average losing trade

unitsToLots(units)

(Forex) Convert the given unit count to lots (multiples of 100,000)

Parameters:

units (float) : The units to convert into lots

Returns: Units converted to nearest lot size (as float)

getFxPositionSize(balance, risk, stopLossPips, fxRate, lots)

(Forex) Calculate fixed-fractional position size based on given parameters

Parameters:

balance (float) : The account balance

risk (float) : The % risk (whole number)

stopLossPips (float) : Pip distance to base risk on

fxRate (float) : The conversion currency rate (more info below in library documentation)

lots (bool) : Whether or not to return the position size in lots rather than units (true by default)

Returns: Units/lots to enter into "qty=" parameter of strategy entry function

EXAMPLE USAGE:

string conversionCurrencyPair = (strategy.account_currency == syminfo.currency ? syminfo.tickerid : strategy.account_currency + syminfo.currency)

float fx_rate = request.security(conversionCurrencyPair, timeframe.period, close )

if (longCondition)

strategy.entry("Long", strategy.long, qty=zen.getFxPositionSize(strategy.equity, 1, stopLossPipsWholeNumber, fx_rate, true))

skipTradeMonteCarlo(chance, debug)

Checks to see if trade should be skipped to emulate rudimentary Monte Carlo simulation

Parameters:

chance (float) : The chance to skip a trade (0-1 or 0-100, function will normalize to 0-1)

debug (bool) : Whether or not to display a label informing of the trade skip

Returns: True if the trade is skipped, false if it's not skipped (idea being to include this function in entry condition validation checks)

fillCell(tableID, column, row, title, value, bgcolor, txtcolor, tooltip)

This updates the given table's cell with the given values

Parameters:

tableID (table) : The table ID to update

column (int) : The column to update

row (int) : The row to update

title (string) : The title of this cell

value (string) : The value of this cell

bgcolor (color) : The background color of this cell

txtcolor (color) : The text color of this cell

tooltip (string)

Returns: Nothing.

ICT Unicorn | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ICT Unicorn Indicator! This indicator is built around the ICT's "Unicorn" strategy. The strategy uses Breaker Blocks and Fair Value Gaps for entry confirmation. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new ICT Unicorn Indicator :

Implementation of ICT's Unicorn Strategy

Toggleable Retracement Entry Method

3 Different TP / SL Methods

Customizable Execution Settings

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

The ICT Unicorn entry model merges the concepts of Breaker Blocks and Fair Value Gaps (FVGs), offering a distinct method for identifying trade opportunities. By integrating these two elements, we can have a position entry with stop-loss and take-profit targets on the potential support & resistance zones. This model is particularly reliable for trade entry, as it combines two powerful entry techniques.

An ICT Unicorn Model consists of a FVG which is overlapping with a Breaker Block of the same type. Here is an example :

When a FVG overlaps with a Breaker Block of the same type, the indicator gives a Buy or Sell signal depending on the FVG type (Bullish & Bearish). If the "Require Retracement" option is enabled in the settings, the signals are not given immediately. Instead, the current price of the ticker will need to touch the FVG once more before the signals are given.

After the Buy or Sell signal, the indicator immediately draws the take-profit (TP) and stop-loss (SL) targets. The indicator has three different TP & SL modes, explained in the "Settings" section of this write-up.

You can set up alerts for entry and TP & SL signals, and also check the current performance of the indicator and adjust the settings accordingly to the current ticker using the backtesting dashboard.

🚩 UNIQUENESS

This indicator is an all-in-one suit for the ICT's Unicorn concept. It's capable of plotting the strategy, giving signals, a backtesting dashboard and alerts feature. Different and customizable algorithm modes will help the trader fine-tune the indicator for the asset they are currently trading. Three different TP / SL modes are available to suit your needs. The backtesting dashboard allows you to see how your settings perform in the current ticker. You can also set up alerts to get informed when the strategy is executable for different tickers.

⚙️ SETTINGS

1. General Configuration

FVG Detection Sensitivity -> You may select between Low, Normal, High or Extreme FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivies resulting in spotting bigger FVGs, and higher sensitivies resulting in spotting all sizes of FVGs.

Swing Length -> Swing length is used when finding order block formations. Smaller values will result in finding smaller order & breaker blocks.

Require Retracement ->

a) Disabled : The entry signal is given immediately once a FVG overlaps with a Breaker Block of the same type.

b) Enabled : The current price of the ticker will need to touch the FVG once more before the entry signal is given.

2. TP / SL

TP / SL Method ->

a) Unicorn : This is the default option. The SL will be set to the lowest low of the last 100 bars with an extra offset in a Buy signal. For Sell signals, the SL will be set to the highest high of the last 100 bars with an extra offset. The TP is then set to a value using the SL value and maintaining a risk-reward ratio.

b) Dynamic: The TP / SL zones will be auto-determined by the algorithm based on the Average True Range (ATR) of the current ticker.

c) Fixed : You can adjust the exact TP / SL ratios from the settings below.

Dynamic Risk -> The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails. This setting is has a crucial effect on the performance of the indicator, as different tickers may have different volatility so the indicator may have increased performance when this setting is correctly adjusted.

Simple FVGSimple FVG - Fair Value Gap Indicator

Overview:

The "Simple FVG" script is designed for use with TradingView to identify and visually display Fair Value Gaps (FVG) on a trading chart. This indicator highlights both bullish and bearish imbalances based on specific candlestick patterns, helping traders to quickly identify potential trading opportunities.

Key Features:

Bullish and Bearish Imbalances:

Bullish Imbalances: This script identifies bullish imbalances where the price exhibits a gap upward. The conditions for detecting a bullish imbalance are:

The high of the second candle is greater than the high of the first candle.

The low of the third candle is greater than the high of the first candle.

Bearish Imbalances: This script identifies bearish imbalances where the price exhibits a gap downward. The conditions for detecting a bearish imbalance are:

The low of the second candle is less than the low of the first candle.

The high of the third candle is less than the low of the first candle.

Customizable Display:

Bullish Blocks: Users can toggle the display of bullish imbalance blocks with customizable colors and border settings.

Bearish Blocks: Users can toggle the display of bearish imbalance blocks with customizable colors and border settings.

Color and Border Settings: Adjust the color, border color, and border width of the blocks for both bullish and bearish imbalances according to user preferences.

Visual Representation:

Drawing Blocks: The script draws filled boxes on the chart to represent identified imbalances. These blocks span from the start of the first candlestick to the end of the third candlestick, providing a clear visual indicator of the price gap.

How It Works:

Identification Logic:

The script analyzes three consecutive candles to determine if an imbalance exists.

It compares the highs and lows of these candles to establish bullish or bearish conditions.

Drawing Mechanism:

Once an imbalance condition is met, the script calculates the top and bottom levels of the imbalance block based on the high of the first candle and the low of the third candle for bullish imbalances, and vice versa for bearish imbalances.

It then draws these blocks on the chart using the specified colors and border settings.

Usage Instructions:

Add the Indicator:

Apply the "Simple FVG" indicator to your TradingView chart.

Customize Settings:

Use the input options to enable or disable the display of bullish and bearish blocks.

Adjust the colors and border settings for the imbalance blocks as needed.

Interpret Imbalances:

Look for the drawn blocks to identify potential areas where price imbalances have occurred.

Use this information to inform your trading decisions.

Originality and Value:

The "Simple FVG" script offers a unique approach to visualizing Fair Value Gaps by focusing on specific candlestick patterns. It provides traders with a tool to easily identify and analyze price imbalances, enhancing chart analysis and trading strategy development.

Chart Information:

Ensure to show the complete symbol, timeframe, and script name information on your chart for clarity and reference.

For further details and usage guidelines, refer to the TradingView House Rules.

Note: This script adheres to TradingView's guidelines for originality and usefulness, offering a practical tool for traders seeking to enhance their chart analysis.

This description adheres to TradingView's requirements by providing a detailed explanation of the script's functionality, how it works, and how users can benefit from it.

Support and resistance levels (Day, Week, Month) + EMAs + SMAs(ENG): This Pine 5 script provides various tools for configuring and displaying different support and resistance levels, as well as moving averages (EMA and SMA) on charts. Using these tools is an essential strategy for determining entry and exit points in trades.

Support and Resistance Levels

Daily, weekly, and monthly support and resistance levels play a key role in analyzing price movements:

Daily levels: Represent prices where a cryptocurrency has tended to bounce within the current trading day.

Weekly levels: Reflect strong prices that hold throughout the week.

Monthly levels: Indicate the most significant levels that can influence price movement over the month.

When trading cryptocurrencies, traders use these levels to make decisions about entering or exiting positions. For example, if a cryptocurrency approaches a weekly resistance level and fails to break through it, this may signal a sell opportunity. If the price reaches a daily support level and starts to bounce up, it may indicate a potential long position.

Market context and trading volumes are also important when analyzing support and resistance levels. High volume near a level can confirm its significance and the likelihood of subsequent price movement. Traders often combine analysis across different time frames to get a more complete picture and improve the accuracy of their trading decisions.

Moving Averages

Moving averages (EMA and SMA) are another important tool in the technical analysis of cryptocurrencies:

EMA (Exponential Moving Average): Gives more weight to recent prices, allowing it to respond more quickly to price changes.

SMA (Simple Moving Average): Equally considers all prices over a given period.

Key types of moving averages used by traders:

EMA 50 and 200: Often used to identify trends. The crossing of the 50-day EMA with the 200-day EMA is called a "golden cross" (buy signal) or a "death cross" (sell signal).

SMA 50, 100, 150, and 200: These periods are often used to determine long-term trends and support/resistance levels. Similar to the EMA, the crossings of these averages can signal potential trend changes.

Settings Groups:

EMA Golden Cross & Death Cross: A setting to display the "golden cross" and "death cross" for the EMA.

EMA 50 & 200: A setting to display the 50-day and 200-day EMA.

Support and Resistance Levels: Includes settings for daily, weekly, and monthly levels.

SMA 50, 100, 150, 200: A setting to display the 50, 100, 150, and 200-day SMA.

SMA Golden Cross & Death Cross: A setting to display the "golden cross" and "death cross" for the SMA.

Components:

Enable/disable the display of support and resistance levels.

Show level labels.

Parameters for adjusting offset, display of EMA and SMA, and their time intervals.

Parameters for configuring EMA and SMA Golden Cross & Death Cross.

EMA Parameters:

Enable/disable the display of 50 and 200-day EMA.

Color and style settings for EMA.

Options to use bar gaps and the "LookAhead" function.

SMA Parameters:

Enable/disable the display of 50, 100, 150, and 200-day SMA.

Color and style settings for SMA.

Options to use bar gaps and the "LookAhead" function.

Effective use of support and resistance levels, as well as moving averages, requires an understanding of technical analysis, discipline, and the ability to adapt the strategy according to changing market conditions.

(RUS) Данный Pine 5 скрипт предоставляет разнообразные инструменты для настройки и отображения различных уровней поддержки и сопротивления, а также скользящих средних (EMA и SMA) на графиках. Использование этих инструментов является важной стратегией для определения точек входа и выхода из сделок.

Уровни поддержки и сопротивления