Sniper EntryThis source code is an implementation of a TradingView indicator called "Sniper Entry". The purpose of this indicator is to identify potential entry points for trades based on certain candlestick patterns and the Stochastic oscillator.

The indicator calculates the Stochastic oscillator based on the close, high, and low prices of the asset over a period of 14 bars. It then uses this oscillator to generate buy and sell signals.

For a buy signal to be generated, the Stochastic oscillator must cross above the oversold level of 20, and the current candle must either be a bullish pin bar or a bullish engulfing pattern. For a sell signal to be generated, the Stochastic oscillator must cross below the overbought level of 80, and the current candle must either be a bearish pin bar or a bearish engulfing pattern.

The indicator also calculates the stop loss and target levels for both buy and sell trades. The stop loss is calculated based on the low or high of the candle that generated the signal, depending on whether it's a buy or sell signal. The target is calculated based on the risk/reward ratio, which is set to 3 in this implementation. The lot size is also set to 0.01, and the starting capital is set to 100.

The indicator then plots the buy and sell signals, the stop loss and target levels, and the Stochastic oscillator on the chart.

It's important to note that this is just one example of a trading indicator, and its effectiveness may vary depending on market conditions and the asset being traded. It's also important to perform your own analysis and use proper risk management techniques when making trades based on any indicator or strategy.

Pesquisar nos scripts por "entry"

VWOP: Volume Weighted & Oscillated PriceWhile playing around with the standard "ta.vwap" I wondered why there was no length input, so I did some research on what the underlying calculation actually is, and did my best to augment it so as to allow for a variable length based on an oscillator value.

Normal VWAP = (Number of Shares Bought x Typical Price) / Total Volume

In my VWOP Calculation, typical price is replaced by selected moving average type or "matype" and then multiplied by the volume.

Then a total value is calculated using math.sum with a length value that changes according to a selected oscillator's value. The total is then divided by

the sum of just volume using the same oscillating length value. Result is then passed through the selected"matype" once more to give the final result.

Indicator designed for use as a entry/exit indicator in conjunction with more traditional moving averages and/or signal filters. Useful for taking volume + an oscillator into account along with price, instead of just the price as with a simple moving average.

The Zig Zag Leveler IndicatorThis indicator is designed to identify potential trade setups in the market using the ZigZag indicator. It uses a combination of the ZigZag indicator and the background fill color to help identify areas of support and resistance. It also uses a pip offset to help with entries and exits. Additionally, it can generate alert conditions when the market direction changes and when a buy or sell signal is generated. This indicator can be used to help identify potential trade setups and can be customized to fit the user's trading strategy.

This indicator takes the guesswork out of trading by providing traders with an array of signals that can help identify entry and exit points. The indicator uses two sets of signals to identify price levels that indicate potential entry and exit points - one set of signals that indicate potential entry points and another set of signals that indicate potential exit points. The indicator also provides traders with a visual representation of the signals that can help them better understand the signals and make informed trading decisions. With this indicator, traders can have a better understanding of the market and have a better chance of making profitable trades.

OTE optimal trade entry (ICT); visible chart only: Dynamic-simple tool based on ICT free YouTube material of many years.

-Highlights a box showing Optimal Trade Entry (OTE): 61.8% - 78.6% retracement

-Auto shifts depending on Bull or Bear move on chart.

--If visible chart is Bullish (low then high): shows OTE box 61.8-78.6% retracement down from the high

--If visible chart is Bearish (high then low): shows OTE box 61.8-78.6% retracement up from the low

-Thanks the use of PineCoders Visible Chart Library, and some of the example code there

SuperTrend Entry(My goal creating this indicator) : Provide a way to enter the market systematically, automatically create Stop Loss Levels and Take Profit Levels, and provide the position size of each entry based on a fix Percentage of the traders account.

The Underlying Concept :

What is Momentum?

The Momentum shown is derived from a Mathematical Formula, SUPERTREND. When price closes above Supertrend Its bullish Momentum when its below Supertrend its Bearish Momentum. This indicator scans for candle closes on the current chart and when there is a shift in momentum (price closes below or above SUPERTREND) it notifies the trader with a Bar Color change.

Technical Inputs

- If you want to optimize the rate of signals to better fit your trading plan you would change the Factor input and ATR Length input. Increase factor and ATR Length to decrease the frequency of signals and decrease the Factor and ATR Length to increase the frequency of signals.

Quick TIP! : You can Sync all VFX SuperTrend Indicators together! All VFX SuperTrend indicators display unique information but its all derived from that same Momentum Formula. Keep the Factor input and ATR Length the same on other VFX SuperTrend indicators to have them operating on the same data.

Display Inputs

- The indicator has a candle overlay option you can toggle ON or OFF. If toggled ON the candles color will represent the momentum of your current chart ( bullish or bearish Momentum)

your able to change the colors that represent bullish or bearish to your preference

- You can toggle on which shows the exact candle momentum switched sides

your able to change the colors that represent a bullish switch or bearish switch to your preference

- The trader can specify which point you would like your stop loss to reference. (Low and High) Which uses the Low of the Momentum signal as the reference for your Stop Loss during buy signals and the High as the reference during sell signals. Or (Lowest Close and Highest Close) which uses the Lowest Close of the Momentum signal as the reference for your Stop Loss during buys and the Highest Close as the reference during sells.

- The colors that represent your Stop Loses and Take Profits can also be changed

Risk Management Inputs

- Your Risk MANAGMENT section is used to set up how your Stop Loss and Take Profit are calculated

- You have the option to take in account Volatility when calculating your Stop Loss. A adjusted ATR formula is used to achieve this. Increase Stop Loss Multiplier from 0 to widen stops.

- Increase Take Profit Multiplier from 0 to access visual Take Profit Levels based on your Stop Loss. This will be important for traders that Prefer trading using risk rewards. For Example: If the the Take Profit Multiplier is 3 a Take Profit level 3 times the size or your stop loss from your entry will be shown and a price number corresponding to that Take Profit Level becomes available.

- Enter your current Account size, Bet Percentage and Fixed Spread to get your Position Size for each trade

-Toggle on the Current Trade Chart and easily get the size of your Position and the exact price of your Take Profit and Stop Loss.

You can increase the Size of the Current Trade Chart= Tiny, Small, Normal, Large, Huge and change the Position of the Current

trade Chart to your preference, (Top- Right, Center, Left) (Middle- Right, Center, Left) (Bottom- Right, Center, Left).

How it can be used ?

- Enter Trades and always know where your stop is going to be

- Eliminate the need to manual calculate Position Size

- Get a consistent view of the current charts momentum

- Systematical enter trades

- Reduce information overload

Smooth OscillatorThis is a an Oscillator based on RSI .

As you can see, entry signal for long is when the indicator and bar color is green and exit when red.

Entry signal for short is when the bar turns red and exit when green.

You should always trade with the trend, this oscillator helps to know where the trend is going, because as the trend is exhausting the plot waves moves to the oversold or overbought area, which can help to know when a reversal is coming.

This is a test version, use under your own discretion and do the proper backtesting.

Please comment your experience.

SuperTrend Entry(My goal creating this indicator) : Provide a way to enter the market systematically, automatically create Stop Loss Levels and Take Profit Levels, and provide the position size of each entry based on a fix Percentage of the traders account.

The Underlying Concept :

What is Momentum?

The Momentum shown is derived from a Mathematical Formula, SUPERTREND. When price closes above Supertrend Its bullish Momentum when its below Supertrend its Bearish Momentum. This indicator scans for candle closes on the current chart and when there is a shift in momentum (price closes below or above SUPERTREND) it notifies the trader with a Bar Color change.

Technical Inputs

- If you want to optimize the rate of signals to better fit your trading plan you would change the Factor input and ATR Length input. Increase factor and ATR Length to decrease the frequency of signals and decrease the Factor and ATR Length to increase the frequency of signals.

Quick TIP! : You can Sync all VFX SuperTrend Indicators together! All VFX SuperTrend indicators display unique information but its all derived from that same Momentum Formula. Keep the Factor input and ATR Length the same on other VFX SuperTrend indicators to have them operating on the same data.

Display Inputs

- The indicator has a candle overlay option you can toggle ON or OFF. If toggled ON the candles color will represent the momentum of your current chart ( bullish or bearish Momentum)

your able to change the colors that represent bullish or bearish to your preference

- You can toggle on which shows the exact candle momentum switched sides

your able to change the colors that represent a bullish switch or bearish switch to your preference

- The trader can specify which point you would like your stop loss to reference. (Low and High) Which uses the Low of the Momentum signal as the reference for your Stop Loss during buy signals and the High as the reference during sell signals. Or (Lowest Close and Highest Close) which uses the Lowest Close of the Momentum signal as the reference for your Stop Loss during buys and the Highest Close as the reference during sells.

- The colors that represent your Stop Loses and Take Profits can also be changed

Risk Management Inputs

- Your Risk MANAGMENT section is used to set up how your Stop Loss and Take Profit are calculated

- You have the option to take in account Volatility when calculating your Stop Loss. A adjusted ATR formula is used to achieve this. Increase Stop Loss Multiplier from 0 to widen stops.

- Increase Take Profit Multiplier from 0 to access visual Take Profit Levels based on your Stop Loss. This will be important for traders that Prefer trading using risk rewards. For Example: If the the Take Profit Multiplier is 3 a Take Profit level 3 times the size or your stop loss from your entry will be shown and a price number corresponding to that Take Profit Level becomes available.

- Enter your current Account size, Bet Percentage and Fixed Spread to get your Position Size for each trade

-Toggle on the Current Trade Chart and easily get the size of your Position and the exact price of your Take Profit and Stop Loss.

You can increase the Size of the Current Trade Chart= Tiny, Small, Normal, Large, Huge and change the Position of the Current

trade Chart to your preference, (Top- Right, Center, Left) (Middle- Right, Center, Left) (Bottom- Right, Center, Left).

How it can be used ?

- Enter Trades and always know where your stop is going to be

- Eliminate the need to manual calculate Position Size

- Get a consistent view of the current charts momentum

- Systematical enter trades

- Reduce information overload

Fractal Potential EntryFractal Potential Entry combine 3 ema and fractal and follow the strategy from Trade Pro on YouTube:

www.youtube.com

with good performance on the 1 minute chart

Feature:

Alert Sell and buy Potential Entry

Happy Trading

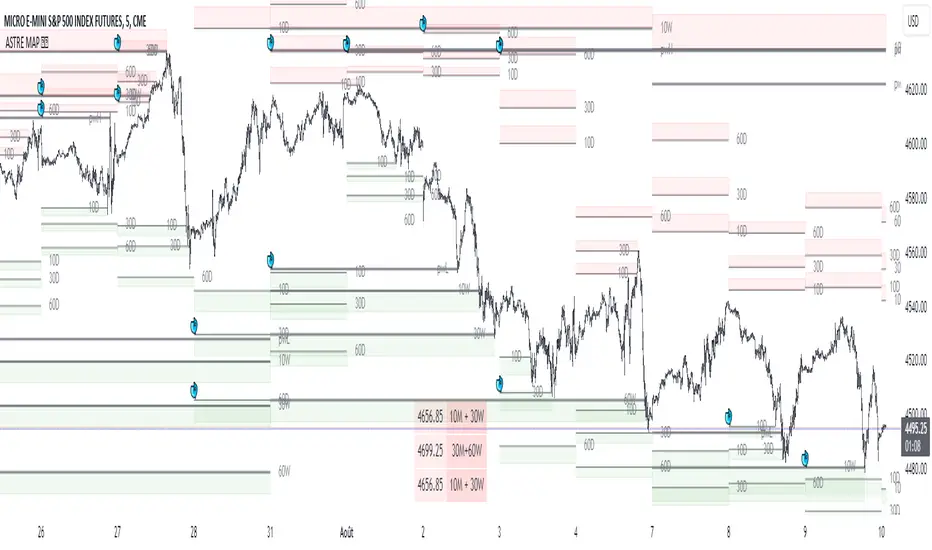

Liquidity mapLocate institutional daily, weekly, and monthly liquidity intervention zones in an innovative format that allows you to fractalize the degree of trend reversal opportunity across multiple lengths!

Far from the traditional formats to tell you "where's the high/low", we display with this map the grab levels relating to the amplitudes of the measured period.

You can check "show old levels" to backtest these potential fractal reversal areas.

Use the levels that interest you according to your working UT (scalping, intraweek, swing, etc.), or take all the elements into consideration for your trading management :

Confluence the information to optimize your entry and shelter your stop loss under strong levels rejections !

Default parameters are: display high/low weekly & monthly, display liquidities levels in daily.

ASTRE Buy/SellWe have designed one of the best buy /sell indicators ! based on our "Reversal score" indicator, a set of strict conditions based on dynamic divergences and fisher's transformation allows to trigger buy signals. The idea is that at a certain level of technical pressure from the indicator, the market has a high probability of changing direction !

(always with the objective of capturing the best top/bottom :) )

Did you miss your trade entry? No problem! The "Barcolor retest" feature allows you to identify a perfect entry on a retest once the structure has been confirmed after a signal:

Exemple on 30s chart :

Using advice :

Use an ATR-type stop loss, or shelter behind bollinger, a short, fixed distance in pips at a minimum below the last local high/low. Your stop loss must be tight and relevant!

For take profit, I recommend that you trail stop part of your position, exit on a contrary signal, or exit part of the position at 5:1 for example.

it is recommended to lower your risk for each identical consecutive signal: 3 buy signals in a row, take a risk for example of $100 on the first, $70 on the second, $40 on the third. The idea is not to be suffocated by the multiple bad signals within the framework of a bad time frame compared to the amplitude of the trend that we seek to take against the trend!

SOON: Easier configuration for 3 commas, backtests. Stay tuned !

astre_ts can in no way be held responsible if your trading account is liquidated after having followed a buy/sell signal and used a large leverage. The signals are reversals: so many are false before having a (very) good trade. Be sure to have strict risk management, or to use a complete strategy so that your results are faithful to the backtests.

BB-RSI-ADX Entry PointsThis is a combination of indicators used to find oversold and overbought entry points for possible reversion.

A Green arrow will appear when all condition are met for an ENTER LONG position.

A Red arow will appear when all condition are met for an ENTER SHORT position.

You can modify all of these condition parameters from the indicator's settings.

How does the indicator work

The signals are using Bollinger Bands , BB %B , RSI and ADX indicators to try and find points of reversal

Enter LONG Conditions

Current candle low is below BB lower band.

The BB %B is more than 0.

RSI > 30

ADX > 25

Enter SHORT Conditions

Current candle high is above BB upper band.

The BB %B is less than 1.

RSI < 70

ADX > 25

Those are the default settings that seem to work for me but you can customize all of these from the indicator settings.

I find this strategy to best work on a 3 minute timeframe

Note: The bb %B is calculated for stDev - 1. This will help you see a change happening faster.

LCDT Trade Entry ToolLCDT Trade Entry Tool

Enter the Offset for the X Axis for the Entry Tool.

Enter the Offset for the Y Axis for the Entry Tool.

Enter the Price for your Stop Loss in $.

Enter your desired Risk Amount in $.

Enter the max amount of of Capital per Trade in $.

There are toggle buttons in the setup to reveal/remove more data in the label that pops up, as well as a toggle to make the text larger.

Volume Entry CandlesIntroduction

For Wyckoff, three things are important in analyzing the market: price, time, and volume . This indicator provides two types of signals:

- linked to large movements of volumes (red and purple circles on top);

- large price movements concerning volatility (green/red triangle up/down);

In the first case, it highlights the volumes that differ from the most common values, allowing us to trace the levels that the market feels.

Two levels highlight the volume peaks and two calculation methods can be chosen: by exponential moving average or by standard deviation.

In the second case, the signal is based on Volatility and highlights the cases in which the high and low of the last three candles exceed the ATR by a certain number of times. This may indicate situations where the market corrects the price after a fairly large move.

in addition, a table will give us statistical information that tells us:

- from how many candles a condition does not occur

- the average of the candles for which it occurs

- the maximum number of candles for which this condition has not occurred

Obviously, like any statistical tool, it is not intended as absolute certainty

Settings

Analyze all / Minutes: By checking the box, we analyze all the candles in the chart, removing the check will only analyze the period set in minutes.

Type of Level: Select the strategy to calculate the critical levels of the volumes, we can choose Ema or Standard Deviation.

Minimum tail in %: here we can exclude candles where tails aren't enough big, for example if we want to exclude candles without a tail. Use a negative value to ignore this control

We then have three groups:

- the first for the EMA ;

- the second for the Standard Deviation;

- the third for the ATR and its multiplier;

each has configuration parameters such as period and multiplier

Period: length for Ema , or Standard Deviation or ATR function

level1 and level2: they are the multipliers for the two levels

ATR multiplier: multiply the ATR value that must be exceeded by ( high-low ) of the last few candles

n candles: set the number of candles

Help

Show Vol Histogram to fine-tuning: if checked show histogram and lines to tune the indicator

Dimension: to set the histogram dimension

Base: set the price level where we want the histogram, in fact, the histogram is not dynamically displayed, it needs a price to appear

How to use

I follow this step for scalping trading:

- Select time frame 1 minute;

- Personally, I deselect "show the first level", and use only the second level;

- In the candles indicated by the purple circle and I draw a horizontal line on the closing of the candle;

- I can use the levels plotted with time frames at 1min also the time frames at 3min and 5 min

the volatility trigger appears as green/red columns in the histogram.

- green colors indicate a bullish reversal;

- red colors indicate a bearish reversal;

Example Bullish reversal

Moderate risk:

Entry point: above high

Stop loss: below low

High risk:

Entry point: a half body of the trigger candle

Stop loss: 1 ATR below the low of the trigger candle

Tips

Pair this indicator with some Moving Average and/or divergence indicator.

This is the twin of an indicator that I made, called "Volume Analysis". It's better if you prefer to analyze levels by yourself and keep the volume values always visible

Bollinger Band Layer Entry (BBLE) The Bollinger Band Layer Entry Indicator uses plenty of Bollinger Bands to create an onion-looking layered indicator to help with layered entries. It is similar to a Ribbon but better. This indicator is best used with any volume-related indicator so you can recede from entering into any position with too much momentum to rebound off of any line. Note that this indicator is best used with another strategy like pair trading. It is not recommended to trade based on this indicator only. Please stay aware of any news about the stock you are trading because some events may have a big impact and force the market to go bullish/bearish by a lot. This indicator can be used with all chart types and works well with many other indicators. It allows for complete customization and offers easy-to-understand settings which can be designated to a certain individual. You can modify every single factor of the BBs which allows for an even more personalized and adapted Indicator that reflects your trading/ investing needs. You also have the option to choose which type of MAs will be used to create the Bollinger Bands , a few of which include: EMA, SMA, WMA, HMA, RMA, DMA, LSMA, VAMA, TMA, MF.

Bollinger Bands are a way to measure and visualize volatility. As volatility increases, the wider the bands become, and the more they deviate from the basis. Vice versa, when volatility decreases, the gap between the bands and basis decreases. Yet a big advantage for not only this but many other indicators is created due to the ample count of different settings that are widely used, it is difficult to view the market through the eyes of all types of investors/traders. This indicator manages to counter exactly this issue, you will be able to see all of these settings on one chart and at one time and enter/exit positions accordingly.

Using this indicator will allow you to visualize entries with ease and make order layering (buying/selling in layers) much more simple. You can choose a certain amount of Bollinger Bands you would like displayed and customize all technical and style-related settings related to each of the BBs separately.

A few of the technical settings you can change for each Bollinger Band are:

Bollinger Band count (Select how many BBs you want to be displayed.)

MA type used to make the Bollinger Bands (EMA, SMA, WMA, etc.)

Source (close, open, high, low.)

BB length (The length of each Bollinger Band, its lookback. How many previous candles should it be based on? Choose each Bollinger Band's lookback length.)

BB deviator (The standard Deviator applied for the BB for both the upper and lower line.)

Offset

A few of the style settings you can change for each Bollinger Band are:

Upper, Lower, Basis line opacity % (separate for each)

Upper, Lower, Basis line color (separate for each)

Fill (the color used to fill from the upper to the lower band) (separate for each)

Fill opacity % (the opacity used when filling the upper line to the lower line) (separate for each)

This indicator is unique because it can be used for all strategies and all trading styles, for example, day trading or long-term investing, really anything if used correctly. The reason it can be used in so many instances is a result of the detailed and in-depth settings tab that allows complete customization of each separate Bollinger Band. This allows the indicator to be used and to be useful in various situations and allows you to dominate the market. Integrated alerts also enhance your efficiency while using this indicator because you can choose to be notified at the crossing of any of the Bollinger Bands.

The technical part of this indicator plots the selected amount of Bollinger Bands using custom-built specified Bollinger Bands accordingly. Then it uses the style settings and styles it as you selected.

Bjorgum MTF MAScope:

Up to 3 MA's can be applied at the users discretion

Choose between 10 different average types including favorites from the Bjorgum series from HEMA to Reversal T3's

Each MA can be independently set

Go Multi-timeframe! Any MA can be set to any timeframe of reference you choose (ex. using 3 different timeframes of higher resolution to your chart reference to establish a multi-time frame trend)

RSI HEATMAP. Use the bar color or the MA color selection toggle to set your color to reference RSI on a gradient. This helps to establish clear visual reference to momentum on top of trend analysis

Assigning RSI bar color to an MA of a higher time frame can allow you to see visual reference of momentum of the greater trend that may be at play.

Example: trying to get short on a 15min while your 1hr and 4hr RSI Heatmap burns deep in oversold.

RSI color can be assigned to the bar color, the MA (1,2 or 3), or both. Alternatively, bar color can be assigned to a more simple rising/ falling MA color and price above/ below the MA for bar color.

ALL MTF FUNCTIONS ARE NON_REPAINTING.

The Idea

The original inspiration behind the script came from an observation of a constant struggle of Pinecoders of both youth or experience to find accurate multi-timeframe indicators that do not repaint, and appear as should on historical bars, while performing reliably in real time. I encourage you to scroll the Pinecoders FAQ on a recent piece explaining the difficulties and caveats of different approaches, but I would like to reference the elimination of the historical bar offset for THIS purpose. MA's are based on closing prices, that is to say they are confirmed and will not change once the bar has closed. There is no need to offset these for historical reference. The purpose of the historical offset is best exemplified, for example, with an intraday strategy involving daily breakouts. Let's entertain going long on a break to a new daily high. We would not know that in real time so we need to reference the previous bars close for BACKTESTING purposes, otherwise we get "lookahead bias". There is no shortage of strategies unintentionally employing this bias out there (I'm sure you have come across them with their unrealistic results).

There is no worry of repainting with the MTF security function included within this script, nor will it offset for something involving lookahead bias. I encourage those that are playing with the code or perhaps writing strategies of their own to borrow the functions within. There is also a function that will return the 10 MA variable selection - yours to keep.

With all that in mind, I wanted a practical script that is easily deployable in everyday trading for the average trader that gives the user a firm grip on their trading steering wheel equipped with the feel of the road. Incorporating several MA's of differing times with the RSI heatmap gives a good visual reference and feel to your trading environment, while offering a level of customization that will fit an individuals personal trading style. The RSI heatmap gradient is per percentage between 30 and 70 and your 2 colors - anything outside of those levels gives you the vibrant bias color

Below I walk through 2 examples of live trades scenarios I made using the mindset the script offers.

The Trade

LONG IZEA

Timeframe: 4hr chart

- 3 Tilson MA's of varying length are deployed at varying intraday time frames

- A bullish pattern in an uptrend offers a possible trade allowing entry from a low risk point from the pattern low

- See the chart for notes and observations using the script

- Notice how the heatmap brightens up as price extends far away from the averages - your risk has elevated for a new position

- Notice the heatmap cool off while price action consolidates sideways

The Trade

SHORT BTCUSDT

Timeframe: 4hr chart

- 3 EMAs are employed - same length (50), with 3 successive timeframe resolutions

- A downtrend is formed with a sharp move to stack the EMAs into layers

- A pull back opportunity presents itself in bearish consolidation

- Notice a Doji star at resistance establishing a swing high as RSI cools off into the EMA dynamic resistance for entry

- An '"equal legs" measured move can be used for a trade target with a stop out above the swing high.

- Again, take note of distance from EMA's, the heatmap in combination with trend development surrounding the MA's

These were just two ideas to show you an example of how to implement some strategy into your trading and to get some interesting use from the indicator. Hope you enjoyed the read and happy trading.

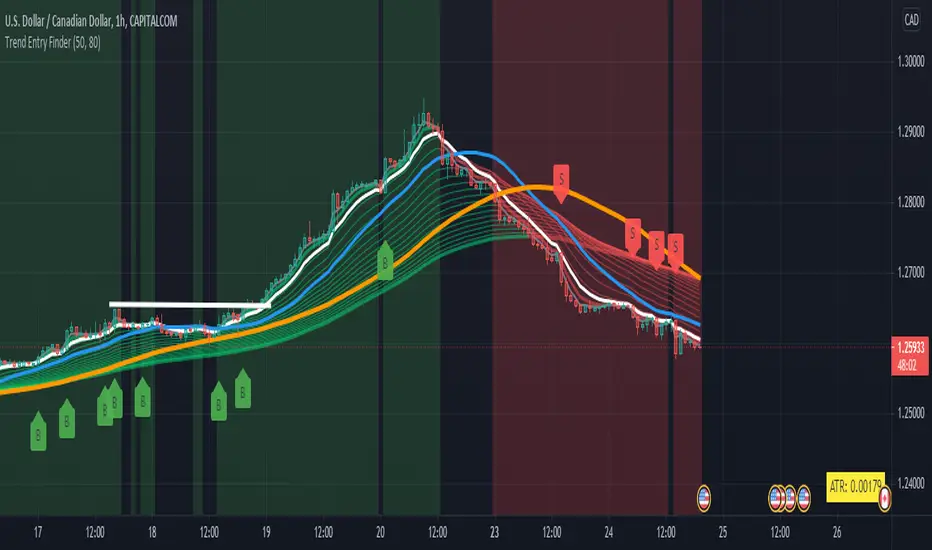

TEF - Trend Entry FinderWith the Trend Entry Finder indicator you can use an EMA ribbon to see if a trend is established (e.g. EMA lines dont intersect and go in one direction). Long and short signals are generated with potential entries into the trade.

Also the 20, 50 and 200 moving averages are displayed that can be used to spot levels of resistance.

CAPITALCOM:US100

Skynet levels + trend + entry/exitThe Skynet levels + trend + entry/exit has the following features.

1>>> The SKYNET LEVELS : There are 3 Skynet levels namely "Upper Pivot" represented by color aqua/blue, "Lower Pivot" represented by the color pink/purple and "Pivot levels" represented by color yellow. The Skynet levels are calculated based on the OHLC data of the past 20 candles.

1.a> The "Upper Pivot" acts as the first resistance for the price and a breakout at the "Upper Pivot" indicates strong upward momentum.

1.b> The "Lower Pivot" acts as the first support for the price and a breakdown at the "Lower Pivot" indicates strong downward momentum.

1.c> The "Pivot level" acts as the median line for the price and the price behavior at the "Pivot level" should be given great significance.

***The "Upper Pivot" and "Lower Pivot" also displays the range of the price action for the past 20 candles. A narrow range indicates volatility suppression and possibility of a big price movement in the future.

Similarly, a wide range indicates volatility expansion which is usually followed by a sideways price movement.

The Skynet levels can be turned ON/OFF from the indicator settings.

2>>> The SKYNET TRENDS : The Skynet trend is a visual trend displayed to make it easy to identify the trend and change in trends.

The trends are identified using the movement of customized exponential moving averages and the price movement itself.

The green/lime color indicates a bullish trend and the red/maroon color indicates a bearish trend.

The darker shade of the green/lime color indicates a stronger bullish momentum and also indicates that the price is too far away from its mean level and there is a likely chance of mean reversion.

Similarly, the darker shade of the red/maroon color indicates a stronger bearish momentum and also indicates that the price is too far away from its mean level and there is a high chance of mean reversion.

3>>> Entry/Exit points : Entry/Exit points are represented by "Green up triangle" and "Red down triangle" respectively.

These labels are generated on the basis of the movement of the price in reference to its "Anchorline". The "Anchorline" is calculated by using the OHLC data of the past 20 candles.

**** This "Anchorline" is different from the earlier mentioned "Pivot level" . Both are derived from OHLC data of the past 20 candles but with different calculations.

Disclaimer: This indicator is not 100% accurate and false signals are generated from time to time. Trading in the markets involves huge risks and one should always do his/her own research before making any trading decisions. This indicator is only designed to help you make a trading decision.

MM Scalper A scalpers Dream just like my other algorithms you have your SL, 2TPs, and entry points to scalp the market based on these two MoneyMoves Moving averages.

can use

Entry

2 TP

ATR x1.5 or x2 Stop Loss auto generated per signal.

BB Bands, TMA Bands, Donchain channels, or volatility cloud

MTF support and resistance

pivot high/low

works on all timeframes for scalpers, intraday, or even swing.

effective on binary as well.

Directions are simple

when one Ma crosses the other you will receive a signal with all your inputs

the signals change based on the length you set on the Baseline and Slop

use market structure and its it a sure winner

Link below or PM us for access to this indicator Happy Trading

LSMA Wave RiderThe LSMA Wave Rider uses Least Squares Moving Average to make a fast oscillator ideal for scalping lower timeframe charts. Upper and lower bands contract during pullback and expand as it "booms". The perfect entry is the first crossover after bands expand. This is a great tool for entering trades.

The above image shows two examples of perfect entries:

1. The upper and lower bands contract getting tighter as it pulls back.

2. The upper and lower bands then begin to expand as it gets ready to fly.

3. The oscillator crosses over showing entry point.

* Please note that this strategy may not work during major downtrends. *

Oscillator 2 is used to detect diversions. Reduce the number to pick up shorter diversions and increase to 200 to pickup larger diversions.

Stochastic RVIBased on the Stochastic RSI but uses RVI (Relative Volatility Index) as source. Another great tool for finding market lows and entry points. This oscillator is also good for finding accurate diversions.

Betelgeuse-Good entry/exit zoneHello everyone and welcome!

This is the my first indicator and also the first version of Betelgeuse script,I hope you will like it.

The indicator was designed to be used on cryptocurrencies

The idea is to be able to identify good entry and exit points in the market, traders often try to identify the minimum or maximum points and this is why Betelgeuse was born.

Betelgeuse should be combined with your analysis and other indicators to find good entry and exit zones and not a precise point.Obviously the more the indicator will be used

over long time frames the more accurate the signals will be.

You can decide to wait for a good signal from the RSI or from the MACD and add up

the Betelegeuse confirmation for a good entry or exit from the market.

The MA based indicator will give you an idea of the direction of the medium term trend.

Direct message me for acces.

Smart Money Entry (Bursa)Calculate any entry price transaction

Red is cumulative of banker money, default value is RM 150,000 entry in every resolution

Orange is cumulative of big money, default value is RM 50,000 entry in every resolution

Green is cumulative of retailer money, default is below RM 50,000 entry in every resolution

All can be set in variable resolution, check in the setting