Kelly Position Size CalculatorThis position sizing calculator implements the Kelly Criterion, developed by John L. Kelly Jr. at Bell Laboratories in 1956, to determine mathematically optimal position sizes for maximizing long-term wealth growth. Unlike arbitrary position sizing methods, this tool provides a scientifically solution based on your strategy's actual performance statistics and incorporates modern refinements from over six decades of academic research.

The Kelly Criterion addresses a fundamental question in capital allocation: "What fraction of capital should be allocated to each opportunity to maximize growth while avoiding ruin?" This question has profound implications for financial markets, where traders and investors constantly face decisions about optimal capital allocation (Van Tharp, 2007).

Theoretical Foundation

The Kelly Criterion for binary outcomes is expressed as f* = (bp - q) / b, where f* represents the optimal fraction of capital to allocate, b denotes the risk-reward ratio, p indicates the probability of success, and q represents the probability of loss (Kelly, 1956). This formula maximizes the expected logarithm of wealth, ensuring maximum long-term growth rate while avoiding the risk of ruin.

The mathematical elegance of Kelly's approach lies in its derivation from information theory. Kelly's original work was motivated by Claude Shannon's information theory (Shannon, 1948), recognizing that maximizing the logarithm of wealth is equivalent to maximizing the rate of information transmission. This connection between information theory and wealth accumulation provides a deep theoretical foundation for optimal position sizing.

The logarithmic utility function underlying the Kelly Criterion naturally embodies several desirable properties for capital management. It exhibits decreasing marginal utility, penalizes large losses more severely than it rewards equivalent gains, and focuses on geometric rather than arithmetic mean returns, which is appropriate for compounding scenarios (Thorp, 2006).

Scientific Implementation

This calculator extends beyond basic Kelly implementation by incorporating state of the art refinements from academic research:

Parameter Uncertainty Adjustment: Following Michaud (1989), the implementation applies Bayesian shrinkage to account for parameter estimation error inherent in small sample sizes. The adjustment formula f_adjusted = f_kelly × confidence_factor + f_conservative × (1 - confidence_factor) addresses the overconfidence bias documented by Baker and McHale (2012), where the confidence factor increases with sample size and the conservative estimate equals 0.25 (quarter Kelly).

Sample Size Confidence: The reliability of Kelly calculations depends critically on sample size. Research by Browne and Whitt (1996) provides theoretical guidance on minimum sample requirements, suggesting that at least 30 independent observations are necessary for meaningful parameter estimates, with 100 or more trades providing reliable estimates for most trading strategies.

Universal Asset Compatibility: The calculator employs intelligent asset detection using TradingView's built-in symbol information, automatically adapting calculations for different asset classes without manual configuration.

ASSET SPECIFIC IMPLEMENTATION

Equity Markets: For stocks and ETFs, position sizing follows the calculation Shares = floor(Kelly Fraction × Account Size / Share Price). This straightforward approach reflects whole share constraints while accommodating fractional share trading capabilities.

Foreign Exchange Markets: Forex markets require lot-based calculations following Lot Size = Kelly Fraction × Account Size / (100,000 × Base Currency Value). The calculator automatically handles major currency pairs with appropriate pip value calculations, following industry standards described by Archer (2010).

Futures Markets: Futures position sizing accounts for leverage and margin requirements through Contracts = floor(Kelly Fraction × Account Size / Margin Requirement). The calculator estimates margin requirements as a percentage of contract notional value, with specific adjustments for micro-futures contracts that have smaller sizes and reduced margin requirements (Kaufman, 2013).

Index and Commodity Markets: These markets combine characteristics of both equity and futures markets. The calculator automatically detects whether instruments are cash-settled or futures-based, applying appropriate sizing methodologies with correct point value calculations.

Risk Management Integration

The calculator integrates sophisticated risk assessment through two primary modes:

Stop Loss Integration: When fixed stop-loss levels are defined, risk calculation follows Risk per Trade = Position Size × Stop Loss Distance. This ensures that the Kelly fraction accounts for actual risk exposure rather than theoretical maximum loss, with stop-loss distance measured in appropriate units for each asset class.

Strategy Drawdown Assessment: For discretionary exit strategies, risk estimation uses maximum historical drawdown through Risk per Trade = Position Value × (Maximum Drawdown / 100). This approach assumes that individual trade losses will not exceed the strategy's historical maximum drawdown, providing a reasonable estimate for strategies with well-defined risk characteristics.

Fractional Kelly Approaches

Pure Kelly sizing can produce substantial volatility, leading many practitioners to adopt fractional Kelly approaches. MacLean, Sanegre, Zhao, and Ziemba (2004) analyze the trade-offs between growth rate and volatility, demonstrating that half-Kelly typically reduces volatility by approximately 75% while sacrificing only 25% of the growth rate.

The calculator provides three primary Kelly modes to accommodate different risk preferences and experience levels. Full Kelly maximizes growth rate while accepting higher volatility, making it suitable for experienced practitioners with strong risk tolerance and robust capital bases. Half Kelly offers a balanced approach popular among professional traders, providing optimal risk-return balance by reducing volatility significantly while maintaining substantial growth potential. Quarter Kelly implements a conservative approach with low volatility, recommended for risk-averse traders or those new to Kelly methodology who prefer gradual introduction to optimal position sizing principles.

Empirical Validation and Performance

Extensive academic research supports the theoretical advantages of Kelly sizing. Hakansson and Ziemba (1995) provide a comprehensive review of Kelly applications in finance, documenting superior long-term performance across various market conditions and asset classes. Estrada (2008) analyzes Kelly performance in international equity markets, finding that Kelly-based strategies consistently outperform fixed position sizing approaches over extended periods across 19 developed markets over a 30-year period.

Several prominent investment firms have successfully implemented Kelly-based position sizing. Pabrai (2007) documents the application of Kelly principles at Berkshire Hathaway, noting Warren Buffett's concentrated portfolio approach aligns closely with Kelly optimal sizing for high-conviction investments. Quantitative hedge funds, including Renaissance Technologies and AQR, have incorporated Kelly-based risk management into their systematic trading strategies.

Practical Implementation Guidelines

Successful Kelly implementation requires systematic application with attention to several critical factors:

Parameter Estimation: Accurate parameter estimation represents the greatest challenge in practical Kelly implementation. Brown (1976) notes that small errors in probability estimates can lead to significant deviations from optimal performance. The calculator addresses this through Bayesian adjustments and confidence measures.

Sample Size Requirements: Users should begin with conservative fractional Kelly approaches until achieving sufficient historical data. Strategies with fewer than 30 trades may produce unreliable Kelly estimates, regardless of adjustments. Full confidence typically requires 100 or more independent trade observations.

Market Regime Considerations: Parameters that accurately describe historical performance may not reflect future market conditions. Ziemba (2003) recommends regular parameter updates and conservative adjustments when market conditions change significantly.

Professional Features and Customization

The calculator provides comprehensive customization options for professional applications:

Multiple Color Schemes: Eight professional color themes (Gold, EdgeTools, Behavioral, Quant, Ocean, Fire, Matrix, Arctic) with dark and light theme compatibility ensure optimal visibility across different trading environments.

Flexible Display Options: Adjustable table size and position accommodate various chart layouts and user preferences, while maintaining analytical depth and clarity.

Comprehensive Results: The results table presents essential information including asset specifications, strategy statistics, Kelly calculations, sample confidence measures, position values, risk assessments, and final position sizes in appropriate units for each asset class.

Limitations and Considerations

Like any analytical tool, the Kelly Criterion has important limitations that users must understand:

Stationarity Assumption: The Kelly Criterion assumes that historical strategy statistics represent future performance characteristics. Non-stationary market conditions may invalidate this assumption, as noted by Lo and MacKinlay (1999).

Independence Requirement: Each trade should be independent to avoid correlation effects. Many trading strategies exhibit serial correlation in returns, which can affect optimal position sizing and may require adjustments for portfolio applications.

Parameter Sensitivity: Kelly calculations are sensitive to parameter accuracy. Regular calibration and conservative approaches are essential when parameter uncertainty is high.

Transaction Costs: The implementation incorporates user-defined transaction costs but assumes these remain constant across different position sizes and market conditions, following Ziemba (2003).

Advanced Applications and Extensions

Multi-Asset Portfolio Considerations: While this calculator optimizes individual position sizes, portfolio-level applications require additional considerations for correlation effects and aggregate risk management. Simplified portfolio approaches include treating positions independently with correlation adjustments.

Behavioral Factors: Behavioral finance research reveals systematic biases that can interfere with Kelly implementation. Kahneman and Tversky (1979) document loss aversion, overconfidence, and other cognitive biases that lead traders to deviate from optimal strategies. Successful implementation requires disciplined adherence to calculated recommendations.

Time-Varying Parameters: Advanced implementations may incorporate time-varying parameter models that adjust Kelly recommendations based on changing market conditions, though these require sophisticated econometric techniques and substantial computational resources.

Comprehensive Usage Instructions and Practical Examples

Implementation begins with loading the calculator on your desired trading instrument's chart. The system automatically detects asset type across stocks, forex, futures, and cryptocurrency markets while extracting current price information. Navigation to the indicator settings allows input of your specific strategy parameters.

Strategy statistics configuration requires careful attention to several key metrics. The win rate should be calculated from your backtest results using the formula of winning trades divided by total trades multiplied by 100. Average win represents the sum of all profitable trades divided by the number of winning trades, while average loss calculates the sum of all losing trades divided by the number of losing trades, entered as a positive number. The total historical trades parameter requires the complete number of trades in your backtest, with a minimum of 30 trades recommended for basic functionality and 100 or more trades optimal for statistical reliability. Account size should reflect your available trading capital, specifically the risk capital allocated for trading rather than total net worth.

Risk management configuration adapts to your specific trading approach. The stop loss setting should be enabled if you employ fixed stop-loss exits, with the stop loss distance specified in appropriate units depending on the asset class. For stocks, this distance is measured in dollars, for forex in pips, and for futures in ticks. When stop losses are not used, the maximum strategy drawdown percentage from your backtest provides the risk assessment baseline. Kelly mode selection offers three primary approaches: Full Kelly for aggressive growth with higher volatility suitable for experienced practitioners, Half Kelly for balanced risk-return optimization popular among professional traders, and Quarter Kelly for conservative approaches with reduced volatility.

Display customization ensures optimal integration with your trading environment. Eight professional color themes provide optimization for different chart backgrounds and personal preferences. Table position selection allows optimal placement within your chart layout, while table size adjustment ensures readability across different screen resolutions and viewing preferences.

Detailed Practical Examples

Example 1: SPY Swing Trading Strategy

Consider a professionally developed swing trading strategy for SPY (S&P 500 ETF) with backtesting results spanning 166 total trades. The strategy achieved 110 winning trades, representing a 66.3% win rate, with an average winning trade of $2,200 and average losing trade of $862. The maximum drawdown reached 31.4% during the testing period, and the available trading capital amounts to $25,000. This strategy employs discretionary exits without fixed stop losses.

Implementation requires loading the calculator on the SPY daily chart and configuring the parameters accordingly. The win rate input receives 66.3, while average win and loss inputs receive 2200 and 862 respectively. Total historical trades input requires 166, with account size set to 25000. The stop loss function remains disabled due to the discretionary exit approach, with maximum strategy drawdown set to 31.4%. Half Kelly mode provides the optimal balance between growth and risk management for this application.

The calculator generates several key outputs for this scenario. The risk-reward ratio calculates automatically to 2.55, while the Kelly fraction reaches approximately 53% before scientific adjustments. Sample confidence achieves 100% given the 166 trades providing high statistical confidence. The recommended position settles at approximately 27% after Half Kelly and Bayesian adjustment factors. Position value reaches approximately $6,750, translating to 16 shares at a $420 SPY price. Risk per trade amounts to approximately $2,110, representing 31.4% of position value, with expected value per trade reaching approximately $1,466. This recommendation represents the mathematically optimal balance between growth potential and risk management for this specific strategy profile.

Example 2: EURUSD Day Trading with Stop Losses

A high-frequency EURUSD day trading strategy demonstrates different parameter requirements compared to swing trading approaches. This strategy encompasses 89 total trades with a 58% win rate, generating an average winning trade of $180 and average losing trade of $95. The maximum drawdown reached 12% during testing, with available capital of $10,000. The strategy employs fixed stop losses at 25 pips and take profit targets at 45 pips, providing clear risk-reward parameters.

Implementation begins with loading the calculator on the EURUSD 1-hour chart for appropriate timeframe alignment. Parameter configuration includes win rate at 58, average win at 180, and average loss at 95. Total historical trades input receives 89, with account size set to 10000. The stop loss function is enabled with distance set to 25 pips, reflecting the fixed exit strategy. Quarter Kelly mode provides conservative positioning due to the smaller sample size compared to the previous example.

Results demonstrate the impact of smaller sample sizes on Kelly calculations. The risk-reward ratio calculates to 1.89, while the Kelly fraction reaches approximately 32% before adjustments. Sample confidence achieves 89%, providing moderate statistical confidence given the 89 trades. The recommended position settles at approximately 7% after Quarter Kelly application and Bayesian shrinkage adjustment for the smaller sample. Position value amounts to approximately $700, translating to 0.07 standard lots. Risk per trade reaches approximately $175, calculated as 25 pips multiplied by lot size and pip value, with expected value per trade at approximately $49. This conservative position sizing reflects the smaller sample size, with position sizes expected to increase as trade count surpasses 100 and statistical confidence improves.

Example 3: ES1! Futures Systematic Strategy

Systematic futures trading presents unique considerations for Kelly criterion application, as demonstrated by an E-mini S&P 500 futures strategy encompassing 234 total trades. This systematic approach achieved a 45% win rate with an average winning trade of $1,850 and average losing trade of $720. The maximum drawdown reached 18% during the testing period, with available capital of $50,000. The strategy employs 15-tick stop losses with contract specifications of $50 per tick, providing precise risk control mechanisms.

Implementation involves loading the calculator on the ES1! 15-minute chart to align with the systematic trading timeframe. Parameter configuration includes win rate at 45, average win at 1850, and average loss at 720. Total historical trades receives 234, providing robust statistical foundation, with account size set to 50000. The stop loss function is enabled with distance set to 15 ticks, reflecting the systematic exit methodology. Half Kelly mode balances growth potential with appropriate risk management for futures trading.

Results illustrate how favorable risk-reward ratios can support meaningful position sizing despite lower win rates. The risk-reward ratio calculates to 2.57, while the Kelly fraction reaches approximately 16%, lower than previous examples due to the sub-50% win rate. Sample confidence achieves 100% given the 234 trades providing high statistical confidence. The recommended position settles at approximately 8% after Half Kelly adjustment. Estimated margin per contract amounts to approximately $2,500, resulting in a single contract allocation. Position value reaches approximately $2,500, with risk per trade at $750, calculated as 15 ticks multiplied by $50 per tick. Expected value per trade amounts to approximately $508. Despite the lower win rate, the favorable risk-reward ratio supports meaningful position sizing, with single contract allocation reflecting appropriate leverage management for futures trading.

Example 4: MES1! Micro-Futures for Smaller Accounts

Micro-futures contracts provide enhanced accessibility for smaller trading accounts while maintaining identical strategy characteristics. Using the same systematic strategy statistics from the previous example but with available capital of $15,000 and micro-futures specifications of $5 per tick with reduced margin requirements, the implementation demonstrates improved position sizing granularity.

Kelly calculations remain identical to the full-sized contract example, maintaining the same risk-reward dynamics and statistical foundations. However, estimated margin per contract reduces to approximately $250 for micro-contracts, enabling allocation of 4-5 micro-contracts. Position value reaches approximately $1,200, while risk per trade calculates to $75, derived from 15 ticks multiplied by $5 per tick. This granularity advantage provides better position size precision for smaller accounts, enabling more accurate Kelly implementation without requiring large capital commitments.

Example 5: Bitcoin Swing Trading

Cryptocurrency markets present unique challenges requiring modified Kelly application approaches. A Bitcoin swing trading strategy on BTCUSD encompasses 67 total trades with a 71% win rate, generating average winning trades of $3,200 and average losing trades of $1,400. Maximum drawdown reached 28% during testing, with available capital of $30,000. The strategy employs technical analysis for exits without fixed stop losses, relying on price action and momentum indicators.

Implementation requires conservative approaches due to cryptocurrency volatility characteristics. Quarter Kelly mode is recommended despite the high win rate to account for crypto market unpredictability. Expected position sizing remains reduced due to the limited sample size of 67 trades, requiring additional caution until statistical confidence improves. Regular parameter updates are strongly recommended due to cryptocurrency market evolution and changing volatility patterns that can significantly impact strategy performance characteristics.

Advanced Usage Scenarios

Portfolio position sizing requires sophisticated consideration when running multiple strategies simultaneously. Each strategy should have its Kelly fraction calculated independently to maintain mathematical integrity. However, correlation adjustments become necessary when strategies exhibit related performance patterns. Moderately correlated strategies should receive individual position size reductions of 10-20% to account for overlapping risk exposure. Aggregate portfolio risk monitoring ensures total exposure remains within acceptable limits across all active strategies. Professional practitioners often consider using lower fractional Kelly approaches, such as Quarter Kelly, when running multiple strategies simultaneously to provide additional safety margins.

Parameter sensitivity analysis forms a critical component of professional Kelly implementation. Regular validation procedures should include monthly parameter updates using rolling 100-trade windows to capture evolving market conditions while maintaining statistical relevance. Sensitivity testing involves varying win rates by ±5% and average win/loss ratios by ±10% to assess recommendation stability under different parameter assumptions. Out-of-sample validation reserves 20% of historical data for parameter verification, ensuring that optimization doesn't create curve-fitted results. Regime change detection monitors actual performance against expected metrics, triggering parameter reassessment when significant deviations occur.

Risk management integration requires professional overlay considerations beyond pure Kelly calculations. Daily loss limits should cease trading when daily losses exceed twice the calculated risk per trade, preventing emotional decision-making during adverse periods. Maximum position limits should never exceed 25% of account value in any single position regardless of Kelly recommendations, maintaining diversification principles. Correlation monitoring reduces position sizes when holding multiple correlated positions that move together during market stress. Volatility adjustments consider reducing position sizes during periods of elevated VIX above 25 for equity strategies, adapting to changing market conditions.

Troubleshooting and Optimization

Professional implementation often encounters specific challenges requiring systematic troubleshooting approaches. Zero position size displays typically result from insufficient capital for minimum position sizes, negative expected values, or extremely conservative Kelly calculations. Solutions include increasing account size, verifying strategy statistics for accuracy, considering Quarter Kelly mode for conservative approaches, or reassessing overall strategy viability when fundamental issues exist.

Extremely high Kelly fractions exceeding 50% usually indicate underlying problems with parameter estimation. Common causes include unrealistic win rates, inflated risk-reward ratios, or curve-fitted backtest results that don't reflect genuine trading conditions. Solutions require verifying backtest methodology, including all transaction costs in calculations, testing strategies on out-of-sample data, and using conservative fractional Kelly approaches until parameter reliability improves.

Low sample confidence below 50% reflects insufficient historical trades for reliable parameter estimation. This situation demands gathering additional trading data, using Quarter Kelly approaches until reaching 100 or more trades, applying extra conservatism in position sizing, and considering paper trading to build statistical foundations without capital risk.

Inconsistent results across similar strategies often stem from parameter estimation differences, market regime changes, or strategy degradation over time. Professional solutions include standardizing backtest methodology across all strategies, updating parameters regularly to reflect current conditions, and monitoring live performance against expectations to identify deteriorating strategies.

Position sizes that appear inappropriately large or small require careful validation against traditional risk management principles. Professional standards recommend never risking more than 2-3% per trade regardless of Kelly calculations. Calibration should begin with Quarter Kelly approaches, gradually increasing as comfort and confidence develop. Most institutional traders utilize 25-50% of full Kelly recommendations to balance growth with prudent risk management.

Market condition adjustments require dynamic approaches to Kelly implementation. Trending markets may support full Kelly recommendations when directional momentum provides favorable conditions. Ranging or volatile markets typically warrant reducing to Half or Quarter Kelly to account for increased uncertainty. High correlation periods demand reducing individual position sizes when multiple positions move together, concentrating risk exposure. News and event periods often justify temporary position size reductions during high-impact releases that can create unpredictable market movements.

Performance monitoring requires systematic protocols to ensure Kelly implementation remains effective over time. Weekly reviews should compare actual versus expected win rates and average win/loss ratios to identify parameter drift or strategy degradation. Position size efficiency and execution quality monitoring ensures that calculated recommendations translate effectively into actual trading results. Tracking correlation between calculated and realized risk helps identify discrepancies between theoretical and practical risk exposure.

Monthly calibration provides more comprehensive parameter assessment using the most recent 100 trades to maintain statistical relevance while capturing current market conditions. Kelly mode appropriateness requires reassessment based on recent market volatility and performance characteristics, potentially shifting between Full, Half, and Quarter Kelly approaches as conditions change. Transaction cost evaluation ensures that commission structures, spreads, and slippage estimates remain accurate and current.

Quarterly strategic reviews encompass comprehensive strategy performance analysis comparing long-term results against expectations and identifying trends in effectiveness. Market regime assessment evaluates parameter stability across different market conditions, determining whether strategy characteristics remain consistent or require fundamental adjustments. Strategic modifications to position sizing methodology may become necessary as markets evolve or trading approaches mature, ensuring that Kelly implementation continues supporting optimal capital allocation objectives.

Professional Applications

This calculator serves diverse professional applications across the financial industry. Quantitative hedge funds utilize the implementation for systematic position sizing within algorithmic trading frameworks, where mathematical precision and consistent application prove essential for institutional capital management. Professional discretionary traders benefit from optimized position management that removes emotional bias while maintaining flexibility for market-specific adjustments. Portfolio managers employ the calculator for developing risk-adjusted allocation strategies that enhance returns while maintaining prudent risk controls across diverse asset classes and investment strategies.

Individual traders seeking mathematical optimization of capital allocation find the calculator provides institutional-grade methodology previously available only to professional money managers. The Kelly Criterion establishes theoretical foundation for optimal capital allocation across both single strategies and multiple trading systems, offering significant advantages over arbitrary position sizing methods that rely on intuition or fixed percentage approaches. Professional implementation ensures consistent application of mathematically sound principles while adapting to changing market conditions and strategy performance characteristics.

Conclusion

The Kelly Criterion represents one of the few mathematically optimal solutions to fundamental investment problems. When properly understood and carefully implemented, it provides significant competitive advantage in financial markets. This calculator implements modern refinements to Kelly's original formula while maintaining accessibility for practical trading applications.

Success with Kelly requires ongoing learning, systematic application, and continuous refinement based on market feedback and evolving research. Users who master Kelly principles and implement them systematically can expect superior risk-adjusted returns and more consistent capital growth over extended periods.

The extensive academic literature provides rich resources for deeper study, while practical experience builds the intuition necessary for effective implementation. Regular parameter updates, conservative approaches with limited data, and disciplined adherence to calculated recommendations are essential for optimal results.

References

Archer, M. D. (2010). Getting Started in Currency Trading: Winning in Today's Forex Market (3rd ed.). John Wiley & Sons.

Baker, R. D., & McHale, I. G. (2012). An empirical Bayes approach to optimising betting strategies. Journal of the Royal Statistical Society: Series D (The Statistician), 61(1), 75-92.

Breiman, L. (1961). Optimal gambling systems for favorable games. In J. Neyman (Ed.), Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability (pp. 65-78). University of California Press.

Brown, D. B. (1976). Optimal portfolio growth: Logarithmic utility and the Kelly criterion. In W. T. Ziemba & R. G. Vickson (Eds.), Stochastic Optimization Models in Finance (pp. 1-23). Academic Press.

Browne, S., & Whitt, W. (1996). Portfolio choice and the Bayesian Kelly criterion. Advances in Applied Probability, 28(4), 1145-1176.

Estrada, J. (2008). Geometric mean maximization: An overlooked portfolio approach? The Journal of Investing, 17(4), 134-147.

Hakansson, N. H., & Ziemba, W. T. (1995). Capital growth theory. In R. A. Jarrow, V. Maksimovic, & W. T. Ziemba (Eds.), Handbooks in Operations Research and Management Science (Vol. 9, pp. 65-86). Elsevier.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Kaufman, P. J. (2013). Trading Systems and Methods (5th ed.). John Wiley & Sons.

Kelly Jr, J. L. (1956). A new interpretation of information rate. Bell System Technical Journal, 35(4), 917-926.

Lo, A. W., & MacKinlay, A. C. (1999). A Non-Random Walk Down Wall Street. Princeton University Press.

MacLean, L. C., Sanegre, E. O., Zhao, Y., & Ziemba, W. T. (2004). Capital growth with security. Journal of Economic Dynamics and Control, 28(4), 937-954.

MacLean, L. C., Thorp, E. O., & Ziemba, W. T. (2011). The Kelly Capital Growth Investment Criterion: Theory and Practice. World Scientific.

Michaud, R. O. (1989). The Markowitz optimization enigma: Is 'optimized' optimal? Financial Analysts Journal, 45(1), 31-42.

Pabrai, M. (2007). The Dhandho Investor: The Low-Risk Value Method to High Returns. John Wiley & Sons.

Shannon, C. E. (1948). A mathematical theory of communication. Bell System Technical Journal, 27(3), 379-423.

Tharp, V. K. (2007). Trade Your Way to Financial Freedom (2nd ed.). McGraw-Hill.

Thorp, E. O. (2006). The Kelly criterion in blackjack sports betting, and the stock market. In L. C. MacLean, E. O. Thorp, & W. T. Ziemba (Eds.), The Kelly Capital Growth Investment Criterion: Theory and Practice (pp. 789-832). World Scientific.

Van Tharp, K. (2007). Trade Your Way to Financial Freedom (2nd ed.). McGraw-Hill Education.

Vince, R. (1992). The Mathematics of Money Management: Risk Analysis Techniques for Traders. John Wiley & Sons.

Vince, R., & Zhu, H. (2015). Optimal betting under parameter uncertainty. Journal of Statistical Planning and Inference, 161, 19-31.

Ziemba, W. T. (2003). The Stochastic Programming Approach to Asset, Liability, and Wealth Management. The Research Foundation of AIMR.

Further Reading

For comprehensive understanding of Kelly Criterion applications and advanced implementations:

MacLean, L. C., Thorp, E. O., & Ziemba, W. T. (2011). The Kelly Capital Growth Investment Criterion: Theory and Practice. World Scientific.

Vince, R. (1992). The Mathematics of Money Management: Risk Analysis Techniques for Traders. John Wiley & Sons.

Thorp, E. O. (2017). A Man for All Markets: From Las Vegas to Wall Street. Random House.

Cover, T. M., & Thomas, J. A. (2006). Elements of Information Theory (2nd ed.). John Wiley & Sons.

Ziemba, W. T., & Vickson, R. G. (Eds.). (2006). Stochastic Optimization Models in Finance. World Scientific.

Pesquisar nos scripts por "demand"

VN30 Effort-vs-Result Multi-Scanner — LinhVN30 Effort-vs-Result Multi-Scanner (Pine v5)

Cross-section scanner for Vietnam’s VN30 stocks that surfaces Effort vs Result footprints and related accumulation/distribution and volatility tells. It renders a ranked table (Top-N) with per-ticker signals and key metrics.

What it does

Scans up to 30 tickers (editable input.symbol slots) using one security() call per symbol → stays under Pine’s 40-call limit and runs reliably on any chart.

Scores each ticker by counting active signals, then ranks and lists the top names.

Optional metrics columns: zVol(60), zTR(60), ATR(20), HL/ATR(20).

Signals (toggleable)

Price/Volume – Effort vs Result

EVR Squeeze (stealth): z(Vol,60) > 4 & z(TR,60) < −0.5

5σ Vol, ≤1σ Ret: z(Vol,60) > 5 & |z(Return,60)| < 1

Wide Effort, Opposite Result: z(Vol,60) > 3 & close < open & z(CLV×Vol,60) > 1

Spread Compression, Heavy Tape: (H−L)/ATR(20) < 0.6 & z(Vol,60) > 3

No-Supply / No-Demand: close < close & range < 0.6×ATR(20) & vol < 0.5×SMA(20)

Momentum & Volatility

Vol-of-Vol Kink: z(ATR20,200) rising & z(ATR5,60) falling

BB Squeeze → Expansion: BBWidth(20) in low regime (z<−1.3) then close > upper band & z(Vol,60) > 2

RSI Non-Confirmation: Price LL/HH with RSI HL/LH & z(Vol,60) > 1

Accumulation/Distribution

OBV Divergence w/ Flat Price: OBV slope > 0 & |z(ret20,260)| < 0.3

Accumulation Days Cluster: ≥3/5 bars: up close, higher vol, close near high

Effort-Result Inversion (Down): big vol on down day then next day close > prior high

How to use

Set the timeframe (works best on 1D for EOD scans).

Edit the 30 symbol slots to your VN30 constituents.

Choose Top N, toggle Show metrics/Only matches and enable/disable scenarios.

Read the table: Rank, Ticker, (metrics), Score, and comma-separated Signals fired.

Method notes

Z-scores use a population-std estimate; CLV×Vol is used for effort/location.

Rolling counts avoid ta.sum; OBV is computed manually; all logic is Pine v5-safe.

Intraday-only ideas (true VWAP magnets, auction volume, flows, futures/options) are not included—Pine can’t cross-scan those datasets.

Disclaimer: Educational tool, not financial advice. Always confirm signals on the chart and with your process.

[blackcat] L1 Net Volume DifferenceOVERVIEW

The L1 Net Volume Difference indicator serves as an advanced analytical tool designed to provide traders with deep insights into market sentiment by examining the differential between buying and selling volumes over precise timeframes. By leveraging these volume dynamics, it helps identify trends and potential reversal points more accurately, thereby supporting well-informed decision-making processes. The key focus lies in dissecting intraday changes that reflect short-term market behavior, offering critical input for both swing and day traders alike. 📊

Key benefits encompass:

• Precise calculation of net volume differences grounded in real-time data.

• Interactive visualization elements enhancing interpretability effortlessly.

• Real-time generation of buy/sell signals driven by dynamic volume shifts.

TECHNICAL ANALYSIS COMPONENTS

📉 Volume Accumulation Mechanisms:

Monitors cumulative buy/sell volumes derived from comparative closing prices.

Periodically resets accumulation counters aligning with predefined intervals (e.g., 5-minute bars).

Facilitates identification of directional biases reflecting underlying market forces accurately.

🕵️♂️ Sentiment Detection Algorithms:

Employs proprietary logic distinguishing between bullish/bearish sentiments dynamically.

Ensures consistent adherence to predefined statistical protocols maintaining accuracy.

Supports adaptive thresholds adjusting sensitivities based on changing market conditions flexibly.

🎯 Dynamic Signal Generation:

Detects transitions indicating dominance shifts between buyers/sellers promptly.

Triggers timely alerts enabling swift reactions to evolving market dynamics effectively.

Integrates conditional logic reinforcing signal validity minimizing erroneous activations.

INDICATOR FUNCTIONALITY

🔢 Core Algorithms:

Utilizes moving averages along with standardized deviation formulas generating precise net volume measurements.

Implements Arithmetic Mean Line Algorithm (AMLA) smoothing techniques improving interpretability.

Ensures consistent alignment with established statistical principles preserving fidelity.

🖱️ User Interface Elements:

Dedicated plots displaying real-time net volume markers facilitating swift decision-making.

Context-sensitive color coding distinguishing positive/negative deviations intuitively.

Background shading highlighting proximity to key threshold activations enhancing visibility.

STRATEGY IMPLEMENTATION

✅ Entry Conditions:

Confirm bullish/bearish setups validated through multiple confirmatory signals.

Validate entry decisions considering concurrent market sentiment factors.

Assess alignment between net volume readings and broader trend directions ensuring coherence.

🚫 Exit Mechanisms:

Trigger exits upon hitting predetermined thresholds derived from historical analyses.

Monitor continuous breaches signifying potential trend reversals promptly executing closures.

Execute partial/total closes contingent upon cumulative loss limits preserving capital efficiently.

PARAMETER CONFIGURATIONS

🎯 Optimization Guidelines:

Reset Interval: Governs responsiveness versus stability balancing sensitivity/stability.

Price Source: Dictates primary data series driving volume calculations selecting relevant inputs accurately.

💬 Customization Recommendations:

Commence with baseline defaults; iteratively refine parameters isolating individual impacts.

Evaluate adjustments independently prior to combined modifications minimizing disruptions.

Prioritize minimizing erroneous trigger occurrences first optimizing signal fidelity.

Sustain balanced risk-reward profiles irrespective of chosen settings upholding disciplined approaches.

ADVANCED RISK MANAGEMENT

🛡️ Proactive Risk Mitigation Techniques:

Enforce strict compliance with pre-defined maximum leverage constraints adhering strictly to guidelines.

Mandatorily apply trailing stop-loss orders conforming to script outputs reinforcing discipline.

Allocate positions proportionately relative to available capital reserves managing exposures prudently.

Conduct periodic reviews gauging strategy effectiveness rigorously identifying areas needing refinement.

⚠️ Potential Pitfalls & Solutions:

Address frequent violations arising during heightened volatility phases necessitating manual interventions judiciously.

Manage false alerts warranting immediate attention avoiding adverse consequences systematically.

Prepare contingency plans mitigating margin call possibilities preparing proactive responses effectively.

Continuously assess automated system reliability amidst fluctuating conditions ensuring seamless functionality.

PERFORMANCE AUDITS & REFINEMENTS

🔍 Critical Evaluation Metrics:

Assess win percentages consistently across diverse trading instruments gauging reliability.

Calculate average profit ratios per successful execution measuring profitability efficiency accurately.

Measure peak drawdown durations alongside associated magnitudes evaluating downside risks comprehensively.

Analyze signal generation frequencies revealing hidden patterns potentially skewing outcomes uncovering systematic biases.

📈 Historical Data Analysis Tools:

Maintain comprehensive records capturing every triggered event meticulously documenting results.

Compare realized profits/losses against backtested simulations benchmarking actual vs expected performances accurately.

Identify recurrent systematic errors demanding corrective actions implementing iterative refinements steadily.

Document evolving performance metrics tracking progress dynamically addressing identified shortcomings proactively.

PROBLEM SOLVING ADVICE

🔧 Frequent Encountered Challenges:

Unpredictable behaviors emerging within thinly traded markets requiring filtration processes.

Latency issues manifesting during abrupt price fluctuations causing missed opportunities.

Overfitted models yielding suboptimal results post-extensive tuning demanding recalibrations.

Inaccuracies stemming from incomplete/inaccurate data feeds necessitating verification procedures.

💡 Effective Resolution Pathways:

Exclude low-liquidity assets prone to erratic movements enhancing signal integrity.

Introduce buffer intervals safeguarding major news/event impacts mitigating distortions effectively.

Limit ongoing optimization attempts preventing model degradation maintaining optimal performance levels consistently.

Verify reliable connections ensuring uninterrupted data flows guaranteeing accurate interpretations reliably.

USER ENGAGEMENT SEGMENT

🤝 Community Contributions Welcome

Highly encourage active participation sharing experiences & recommendations!

THANKS

Heartfelt acknowledgment extends to all developers contributing invaluable insights about volume-based trading methodologies! ✨

[blackcat] L2 Z-Score of PriceOVERVIEW

The L2 Z-Score of Price indicator offers traders an insightful perspective into how current prices diverge from their historical norms through advanced statistical measures. By leveraging Z-scores, it provides a robust framework for identifying potential reversals in financial markets. The Z-score quantifies the number of standard deviations that a data point lies away from the mean, thus serving as a critical metric for recognizing overbought or oversold conditions. 🎯

Key benefits encompass:

• Precise calculation of Z-scores reflecting true price deviations.

• Interactive plotting features enhancing visual clarity.

• Real-time generation of buy/sell signals based on crossover events.

STATISTICAL ANALYSIS COMPONENTS

📉 Mean Calculation:

Utilizes Simple Moving Averages (SMAs) to establish baseline price references.

Provides smooth representations filtering short-term noise preserving long-term trends.

Fundamental for deriving subsequent deviation metrics accurately.

📈 Standard Deviation Measurement:

Quantifies dispersion around established means revealing underlying variability.

Crucial for assessing potential volatility levels dynamically adapting strategies accordingly.

Facilitates precise Z-score derivations ensuring statistical rigor.

🕵️♂️ Z-SCORE DETECTION:

Measures standardized distances indicating relative positions within distributions.

Helps pinpoint extreme conditions signaling impending reversals proactively.

Enables early identification of trend exhaustion phases prompting timely actions.

INDICATOR FUNCTIONALITY

🔢 Core Algorithms:

Integrates SMAs along with standardized deviation formulas generating precise Z-scores.

Employs Arithmetic Mean Line Algorithm (AMLA) smoothing techniques improving interpretability.

Ensures consistent adherence to predefined statistical protocols maintaining accuracy.

🖱️ User Interface Elements:

Dedicated plots displaying real-time Z-score markers facilitating swift decision-making.

Context-sensitive color coding distinguishing positive/negative deviations intuitively.

Background shading highlighting proximity to key threshold activations enhancing visibility.

STRATEGY IMPLEMENTATION

✅ Entry Conditions:

Confirm bullish/bearish setups validated through multiple confirmatory signals.

Validate entry decisions considering concurrent market sentiment factors.

Assess alignment between Z-score readings and broader trend directions ensuring coherence.

🚫 Exit Mechanisms:

Trigger exits upon hitting predetermined thresholds derived from historical analyses.

Monitor continuous breaches signifying potential trend reversals promptly executing closures.

Execute partial/total closes contingent upon cumulative loss limits preserving capital efficiently.

PARAMETER CONFIGURATIONS

🎯 Optimization Guidelines:

Length: Governs responsiveness versus smoothing trade-offs balancing sensitivity/stability.

Price Source: Dictates primary data series driving Z-score computations selecting relevant inputs accurately.

💬 Customization Recommendations:

Commence with baseline defaults; iteratively refine parameters isolating individual impacts.

Evaluate adjustments independently prior to combined modifications minimizing disruptions.

Prioritize minimizing erroneous trigger occurrences first optimizing signal fidelity.

Sustain balanced risk-reward profiles irrespective of chosen settings upholding disciplined approaches.

ADVANCED RISK MANAGEMENT

🛡️ Proactive Risk Mitigation Techniques:

Enforce strict compliance with pre-defined maximum leverage constraints adhering strictly to guidelines.

Mandatorily apply trailing stop-loss orders conforming to script outputs reinforcing discipline.

Allocate positions proportionately relative to available capital reserves managing exposures prudently.

Conduct periodic reviews gauging strategy effectiveness rigorously identifying areas needing refinement.

⚠️ Potential Pitfalls & Solutions:

Address frequent violations arising during heightened volatility phases necessitating manual interventions judiciously.

Manage false alerts warranting immediate attention avoiding adverse consequences systematically.

Prepare contingency plans mitigating margin call possibilities preparing proactive responses effectively.

Continuously assess automated system reliability amidst fluctuating conditions ensuring seamless functionality.

PERFORMANCE AUDITS & REFINEMENTS

🔍 Critical Evaluation Metrics:

Assess win percentages consistently across diverse trading instruments gauging reliability.

Calculate average profit ratios per successful execution measuring profitability efficiency accurately.

Measure peak drawdown durations alongside associated magnitudes evaluating downside risks comprehensively.

Analyze signal generation frequencies revealing hidden patterns potentially skewing outcomes uncovering systematic biases.

📈 Historical Data Analysis Tools:

Maintain comprehensive records capturing every triggered event meticulously documenting results.

Compare realized profits/losses against backtested simulations benchmarking actual vs expected performances accurately.

Identify recurrent systematic errors demanding corrective actions implementing iterative refinements steadily.

Document evolving performance metrics tracking progress dynamically addressing identified shortcomings proactively.

PROBLEM SOLVING ADVICE

🔧 Frequent Encountered Challenges:

Unpredictable behaviors emerging within thinly traded markets requiring filtration processes.

Latency issues manifesting during abrupt price fluctuations causing missed opportunities.

Overfitted models yielding suboptimal results post-extensive tuning demanding recalibrations.

Inaccuracies stemming from incomplete/inaccurate data feeds necessitating verification procedures.

💡 Effective Resolution Pathways:

Exclude low-liquidity assets prone to erratic movements enhancing signal integrity.

Introduce buffer intervals safeguarding major news/event impacts mitigating distortions effectively.

Limit ongoing optimization attempts preventing model degradation maintaining optimal performance levels consistently.

Verify reliable connections ensuring uninterrupted data flows guaranteeing accurate interpretations reliably.

USER ENGAGEMENT SEGMENT

🤝 Community Contributions Welcome

Highly encourage active participation sharing experiences & recommendations!

[ AlgoChart ] - Compare MarketIndicator Description:

This indicator allows you to display a second asset, selectable from the input panel, in a separate window. Plotted on the same time scale as the first asset but with a distinct price scale, the indicator enables analysis of the relationships and relative movements of two financial instruments. It’s an ideal tool for understanding whether two assets move in a correlated or divergent manner.

Key Features:

Multi-Asset Comparison: Display two assets simultaneously to compare their trends.

Custom Scale: Each asset uses its own price scale, making comparative analysis easier.

Intuitive Interface: Easily select the second asset through the input panel.

Operational Applications:

Spread Trading: Identify optimal moments to execute spread trades when two highly correlated instruments move in opposite directions.

Supply & Demand: Pinpoint zones of interest on both assets, increasing the validity of support and resistance areas.

Exposure Reduction: Monitor instruments that move similarly to avoid exposing the portfolio in identical directions, thereby reducing the risk of double losses.

Additional Features:

Candle Color Change: When a directional divergence occurs between the two assets, the candles change color to highlight the event.

Customizable Notifications: Receive instant alerts when a divergence occurs, allowing you to act promptly.

CNN Fear and Greed Index JD modified from minusminusCNN Fear and Greed Index - www.cnn.com

Modified from minusminus -

See Documentation from CNN's website

CNN's Fear and Greed index is an attempt to quantitatively score the Fear and Greed in the SPX using 7 factors:

Market Momentum- S&P 500 (SPX) and its 125-day moving average

Stock Price Strength -Net new 52-week highs and lows on the NYSE

Stock Price Breadth - McClellan Volume Summation Index

Put and Call options - 5-day average put/call ratio

Market Volatility - VIX and its 50-day moving average

Safe Haven Demand - Difference in 20-day stock and bond returns

Junk Bond Demand - Yield spread: junk bonds vs. investment grade

Each Factor has a weight input for the final calculation initially set to a weight of 1. The final calculation of the index is a weighted average of each factor.

3 Factors have separate functions for calculation : See Code for Clarity

SPX Momentum : difference between the Daily CBOE:SPX index value and it's 125 Day Simple moving average.

Stock Price Strength : Net New 52-week highs and lows on the NYSE.

Function calculates a measure of Net New 52-week highs by:

NYSE 52-week highs (INDEX:MAHN) - all new NYSE Highs (INDEX:HIGH)

measure of Net New 52-week lows by:

NYSE 52-week lows (INDEX:MALN) - all new NYSE Lows (INDEX:LOWN)

Then calculate a ratio of Net New 52-week Highs and Lows over Total Highs and Lows then takes a 5-day moving average of that ratio-See Code

Stock Price Breadth is the McClellan Volume Summation Index :

First Calculate the McClellan Oscillator

Second Calculate the Summation Index

4 Factors are Straight data requests

5 Day Simple Moving Average of the Put-Call Ratio on SPY

50 Day Simple Moving Average of the SPX VIX

Difference between 20 Day Simple Moving Average of SPX Daily Close and 20 Day Simple Moving Average of 10Y Constant Maturity US Treasury Note

Yield Spread between ICE BofA US High Yield Index and ICE BofA US Investment Grade Corporate Yield Index

The Fear and Greed Index is a weighted average of these factors - which is then normalized to scale from 0 to 100 using the past 25 values - length parameter.

3 Zones are Shaded: Red for Extreme Fear, Grey for normal jitters, Green for Extreme Greed.

Disclaimer: This is not financial advice. These are just my ideas, and I am not an investment advisor or investment professional. This code is for informational purposes only and do your own analysis before making any investment decisions. This is an attempt to replicate in spirt an index CNN publishes on their website and in no way shape or form infringes on their content, calculations or proprietary information.

From CNN: www.cnn.com

FEAR & GREED INDEX FAQs

What is the CNN Business Fear & Greed Index?

The Fear & Greed Index is a way to gauge stock market movements and whether stocks are fairly priced. The theory is based on the logic that excessive fear tends to drive down share prices, and too much greed tends to have the opposite effect.

How is Fear & Greed Calculated?

The Fear & Greed Index is a compilation of seven different indicators that measure some aspect of stock market behavior. They are market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The index tracks how much these individual indicators deviate from their averages compared to how much they normally diverge. The index gives each indicator equal weighting in calculating a score from 0 to 100, with 100 representing maximum greediness and 0 signaling maximum fear.

How often is the Fear & Greed Index calculated?

Every component and the Index are calculated as soon as new data becomes available.

How to use Fear & Greed Index?

The Fear & Greed Index is used to gauge the mood of the market. Many investors are emotional and reactionary, and fear and greed sentiment indicators can alert investors to their own emotions and biases that can influence their decisions. When combined with fundamentals and other analytical tools, the Index can be a helpful way to assess market sentiment.

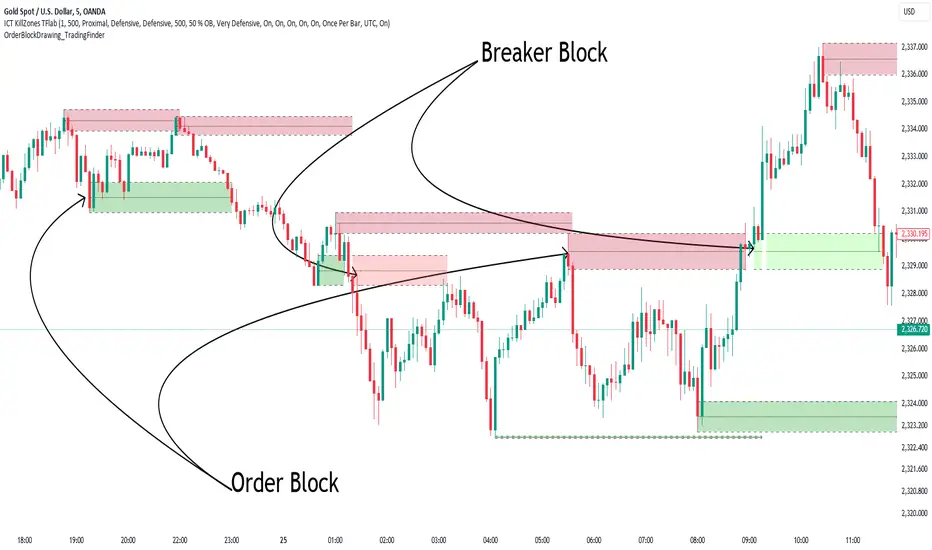

Order Block Drawing [TradingFinder]🔵 Introduction

Perhaps one of the most challenging tasks for Pine script developers (especially beginners) is properly drawing order blocks. While utilizing the latest technical analysis methods for "Price Action," beginners heavily rely on accurately plotting "Supply" and "Demand" zones, following concepts like "Smart Money Concept" and "ICT".

However, drawing "Order Blocks" may pose a challenge for developers. Therefore, to minimize bugs, increase accuracy, and speed up the process of coding order blocks, we have released the "Order Block Drawing" library.

Below, you can read more details about how to use this library.

Important :

This library has direct and indirect outputs. The indirect output includes the ranges of order blocks plotted on the chart. However, the direct output is a "Boolean" value that becomes "true" only when the price touches an order block, colloquially termed as "Mitigate." You can use this output for setting up alerts.

🔵 How to Use

First, you can add the library to your code as shown in the example below.

import TFlab/OrderBlockDrawing_TradingFinder/1

🟣Parameters

OBDrawing(OBType, TriggerCondition, DistalPrice, ProximalPrice, Index, OBValidDis, Show, ColorZone) =>

Parameters:

• OBType (string)

• TriggerCondition (bool)

• DistalPrice (float)

• ProximalPrice (float)

• Index (int)

• OBValidDis (int)

• Show (bool)

• ColorZone (color)

OBType : All order blocks are summarized into two types: "Supply" and "Demand." You should input your order block type in this parameter. Enter "Demand" for drawing demand zones and "Supply" for drawing supply zones.

TriggerCondition : Input the condition under which you want the order block to be drawn in this parameter.

DistalPrice : Generally, if each zone is formed by two lines, the farthest line from the price is termed "Distal." This input receives the price of the "Distal" line.

ProximalPrice : Generally, if each zone is formed by two lines, the nearest line to the price is termed "Proximal" line.

Index : This input receives the value of the "bar_index" at the beginning of the order block. You should store the "bar_index" value at the occurrence of the condition for the order block to be drawn and input it here.

OBValidDis : Order blocks continue to be drawn until a new order block is drawn or the order block is "Mitigate." You can specify how many candles after their initiation order blocks should continue. If you want no limitation, enter the number 4998.

Show : You may need to manage whether to display or hide order blocks. When this input is "On", order blocks are displayed, and when it's "Off", order blocks are not displayed.

ColorZone : You can input your preferred color for drawing order blocks.

🔵 Function Outputs

This function has only one output. This output is of type "Boolean" and becomes "true" only when the price touches an order block. Each order block can be touched only once and then loses its validity. You can use this output for alerts.

= Drawing.OBDrawing('Demand', Condition, Distal, Proximal, Index, 4998, true, Color)

[F][IND] - Time Range HighlighterDescription:

Introducing the Time Range Highlighter script for TradingView – a precision tool designed to enhance your chart analysis experience with a focus on simplicity and functionality. This script caters to traders who find value in isolating specific time intervals for a more detailed market study, akin to the concept of trading "macros".

Key Features:

1. Effortless Customization:

Define and highlight your preferred time ranges effortlessly. Tailor the script to align with your trading strategy by setting specific start and end times for enhanced precision.

2. Multi-Interval Support:

Seamlessly analyze multiple time ranges concurrently. Toggle between highlighted intervals with ease, allowing for a comprehensive examination of various market conditions without cluttering your chart.

3. Enable/Disable On-Demand:

Maintain control over the clutter on your chart. The enable/disable feature lets you activate or deactivate the highlighted time ranges at your discretion, ensuring a clean and unobstructed view when needed.

4. Focused Chart Analysis:

By visually emphasizing chosen time intervals, the script facilitates a focused analysis of critical market movements, enabling traders to identify patterns and trends with efficiency. This feature is particularly beneficial for those employing trading "macros" to filter out noise and concentrate on key periods.

Usage Instructions:

1. Apply the Time Range Highlighter script to your TradingView chart.

2. Customize the script settings to define specific time ranges tailored to your trading preferences.

3. Toggle between enabled and disabled states as needed to maintain clarity on your chart.

4. Leverage the script to streamline your chart analysis process and make more informed trading decisions, especially when employing trading "macros" to focus on specific market intervals.

Disclaimer:

This indicator is provided for educational purposes only. Trading involves risk, and users should consult with a financial professional before making any trading decisions.

Your Feedback Matters!

Please feel free to comment or reach out if you have any improvement suggestions or if you would like to request the development of a specific indicator. Your feedback is invaluable!

BTC bottom top MACRO indicator based on: Cost per transaction(w)Predicting tops and bottoms in any market is a challenging task, and the Bitcoin market is no exception. Many traders and analysts use a combination of various indicators and models to help them make educated guesses about where the market might be heading. One such metric that can provide valuable insights is the Bitcoin cost per transaction indicator.

Here's how it could potentially be superior to just using price action for predicting macro tops and bottoms:

Transaction Cost as an Indicator of Network Activity: The cost per transaction on the Bitcoin network can give an indication of how much activity is taking place. When transaction costs are high, it may signal increased network usage, which often coincides with periods of market enthusiasm or FOMO (Fear of Missing Out) that can precede market tops. Conversely, lower transaction costs might indicate reduced network activity, potentially signaling a lack of investor interest that might precede market bottoms.

Reflects Real-World Use and Demand: Unlike price action, which can be influenced by speculative trading and may not always reflect the underlying fundamentals, the cost per transaction is directly tied to the use of the Bitcoin network. It offers a more fundamental approach to understanding market dynamics.

Complements Price Action Analysis: While price action can give signals about potential tops and bottoms based on historical price patterns and technical analysis, the cost per transaction can add an additional layer of information by reflecting network activity. In this way, the two can be used together to give a more complete picture of the market.

May Precede Price Changes: Changes in transaction costs could potentially precede price changes, giving advanced warning of tops and bottoms. For instance, a sudden increase in transaction costs might indicate a surge in network activity and investor interest, potentially signaling a market top. On the other hand, a decrease in transaction costs might suggest declining network activity and investor interest, potentially signaling a market bottom.

However, it's important to note that while the cost per transaction can provide valuable insights, it's not a foolproof method for predicting market tops and bottoms. Like all indicators, it should be used in conjunction with other tools and analysis methods, and traders should also consider the broader market context. As always, past performance is not indicative of future results, and all trading and investment strategies carry the risk of loss.

HDT CloudsHDT Clouds combines custom clouds such as the 200EMA/MA cloud indicator to create high confluence bounce zones when combined with VWAP. The HDT indicator combines various clouds with the Volume Weighted Average Price indicator and Standard Deviations which allow users to identify areas on the chart where the stock may reverse.

On smaller time frames, like the 5/15/30minute, the 200ema/ma cloud and VWAP (when sitting in the same relative area) creates pockets of supply or demand.

In addition, the various moving average clouds, such as the 8/9ema cloud and the 34/50ema cloud, create areas of supply and demand depending on the overall trend. If the stock is trending very strongly to the upside, the 8/9ema can be used as a potential bounce area. Whereas, if the stock is trending, but not quite as strong, the stock may have demand at the 34-50ema where the stock could see a potential bounce to the upside. What sets this indicator apart from other moving average clouds is the incorporation of VWAP/Standard Deviation and the combining of a 200EMA/MA indicator which creates a strong pocket of demand even on lower time frames such as the 5 or 15 minute time frame.

Dump AlertsNYSE:BRK.B

By popular demand: An inverted version of my first indicator Pump Alerts in Pine Script with two alert conditions for trading bots and automated stock trading setups.

It's originally based on "Pump Catcher" by @joepegler

I modified some parts, hopefully improved the usability and enabled alerts, so you can use it to trigger bots like 3commas via webhooks or stock brokers partnering with TradingView.

Dump Alerts 📉 attempts to detect moments of abnormal and accelerating increase in volume concurrent with falling prices AKA "dumps". Small and big dumps.

I recommend trying different timeframes and tinkering with the lookback period as well as both threshold values.

Other than that it's pretty self-explanatory and beginner-friendly.

Free and Open Source. Let me know how you use it!

Order Blocks Zones with Signals█ OVERVIEW

“Order Blocks Zones with Signals” is a technical analysis tool that automatically identifies Order Blocks (OB) and optionally Fair Value Gaps (FVG) on the chart.

The script visualizes these zones as colored rectangles, offering full customization of style, transparency, and signal display.

It also generates entry and exit signals (Break & Exit) that can serve as confirmations in strategies based on price action and market structure.

Thanks to flexible candle size filters and rich visual options, the indicator maintains chart clarity and readability.

█ CONCEPTS

Order Blocks (OB) are key zones on the chart where significant price movements previously occurred — areas where large market participants (institutions, so-called smart money) initiated or closed positions.

An OB is the last candle that followed the prior trend before the market reversed (e.g., for a Bullish OB: the last bearish candle before a pivot low and a strong upward impulse).

The script detects these levels using local price pivots, analyzing candle direction to filter out less significant movements.

FVG (Fair Value Gaps) represent areas of imbalance between buyers and sellers — price gaps formed by a sharp impulse where full trading did not occur due to one-sided order dominance (e.g., excess buy or sell orders).

Why combine OB and FVG in one indicator?

Combining OB and FVG analysis is essential because these phenomena often occur sequentially in the institutional market cycle:

1. Order Block — institutions enter the market in the OB zone, absorbing orders and building positions.

2. Strong impulse — after smart money entry, a rapid price move creates an FVG (imbalance gap).

3. Retest — price naturally returns to these zones (OB or FVG), drawn by unfilled orders and the search for equilibrium.

Such areas strongly attract price, as they represent not only historical institutional levels but also open “holes” in the order book. Retests of OB and FVG are ideal entry opportunities with high reaction probability (rebound or breakout). The indicator combines these two interconnected elements, enabling comprehensive market structure analysis in a single tool.

Order Blocks are labeled as:

Bullish OB – demand zones, often accumulation areas before an upmove.

Bearish OB – supply zones, signaling potential impulse end or correction start.

█ FEATURES

Order Block Detection (OB Detection):

- Automatic identification of demand and supply zones based on pivots.

- OB is the last candle aligned with the prior trend, just before the market reversal — precisely identified through candle sequence analysis around the pivot.

- OB zones appear with a delay equal to Pivot Length (default 10 bars).

- Break signals trigger when a candle’s body (close) fully pierces the zone, causing the zone to disappear immediately (e.g., close < low of Bullish OB → Break Down and zone deletion).

- Minimum size filtering via OB Size Multiplier.

- Option to create OB without wicks (Include Wicks in OB): when disabled, OB zones are based solely on candle bodies (open/close), ignoring wicks (high/low).

Fair Value Gap Detection (FVG Detection):

- Optional, with enable/disable capability.

- FVG are detected without delay — immediately upon gap occurrence.

- Size filtering via Candle Size Period and FVG Size Multiplier.

Customizable Styling:

- Separate colors and border styles (Solid / Dashed / Dotted) for each zone type.

- Adjustable transparency and border thickness.

- Unified color for box, border, and signal of the same type.

Breakout and Exit Signals:

- Break Up – triggered when a candle’s close breaks above a Bearish OB, causing the zone to disappear.

- Break Down – triggered when a candle’s close breaks below a Bullish OB, causing the zone to disappear.

- Exit Up / Exit Down – temporary exit from the zone without full breakout (price leaves the zone but doesn’t close beyond it). Signal type selection: Break, Exit, or Both.

- Alerts: built-in alerts for all signal types — triggered automatically on candle close confirming breakout or exit from OB.

█ HOW TO USE

Adding to chart: import the code into Pine Editor and run the script on TradingView.

Settings configuration:

- Pivot Length: controls swing detection sensitivity and OB display delay (default 10).

- Include Wicks in OB: enabled (default) – OB includes wicks; disabled – OB uses bodies only.

- Size Filter: adjust Candle Size Period and OB/FVG Size Multiplier to filter out small zones.

- Colors & Styles: set colors, styles, and transparency for each zone type.

- Signal Type: choose which signals to display (Break, Exit, or Both).

Signal interpretation:

- OB Break Up: price closes above Bearish OB → zone disappears → potential bullish continuation.

- OB Break Down: price closes below Bullish OB → zone disappears → potential bearish continuation.

- Exit Signals: price leaves the zone temporarily without breakout — often signals impending reversal or pullback.

Tips:

- Use OB signals alongside other indicators like RSI, MACD, SMI, or trend filters.

- Order Blocks from higher timeframes (e.g., 4H, 1D) carry greater significance and reaction strength.

- Remember: FVG are detected immediately, OB with delay — a complementary approach!

█ APPLICATIONS

- Smart Money Concepts (SMC): use OB zones as dynamic support and resistance levels. In an uptrend, look for buy opportunities in bullish OBs, which price often retests before further gains. Combining with RSI, MACD, or Fibonacci levels enhances zone significance, confirming institutional demand.

- Breakout Trading: trade based on OB breakout signals. A buy signal after breaking a bearish OB may indicate a strong upward impulse, especially if supported by rising MACD or RSI above 50. Similarly for sell signals after Break Down.

- Reversal Zones: Exit signals may indicate the end of a move or correction. Safest to use in alignment with higher-timeframe trend and confirmed by another indicator (e.g., RSI divergence, Fibonacci levels).

- Confluence Analysis: combine OB and FVG for deeper market structure and equilibrium insight. When an Order Block overlaps or borders an FVG, we get confluence of two institutional phenomena — OB (smart money entry) + FVG (imbalance) — making these areas particularly strong price magnets, increasing retest and reaction probability.

█ NOTES

- FVG can be fully disabled for a cleaner chart view.

- In consolidation periods, signals may appear more frequently — always confirm with additional trend filters.

- Works on all markets and timeframes (crypto, forex, indices, stocks).

Support and Resistance levels from Options DataINTRODUCTION

This script is designed to visualize key support and resistance levels derived from options data on TradingView charts. It overlays lines, labels, and boxes to highlight levels such as Put Walls (gamma support), Call Walls (gamma resistance), Gamma Flip points, Vanna levels, and more.

These levels are intended to help traders identify potential areas of price magnetism, reversal, or breakout based on options market dynamics. All calculations and visualizations are based on user-provided data pasted into the input field, as Pine Script cannot directly fetch external options data due to platform limitations (explained below).

For convenience, my website allows users to interact with a bot that will generate the string for up to 30 tickers at once getting nearly real-time data on demand (data is cached for 15min). With the output string pasted into this indicator, it's a bliss to shuffle through your portfolio and see those levels for each ticker.

The script is open-source under TradingView's terms, allowing users to study, modify, and improve it. It draws inspiration from common options-derived metrics like gamma exposure and vanna, which are widely discussed in financial literature. No external code is copied without rights; all logic is original or based on standard mathematical formulas.

How the Options Levels Are Calculated

The levels displayed by this script are not computed within Pine Script itself—instead, they rely on pre-calculated values provided by the user (via a pasted data string). These values are derived from options chain data fetched from financial APIs (e.g., using libraries like yfinance in Python). Here's a step-by-step overview of how these levels are generally calculated externally before being input into the script:

Fetching Options Data:

Historical and current options chain data for a ticker (e.g., strikes, open interest, volume, implied volatility, expirations) is retrieved for near-term expirations (e.g., up to 90 days).

Current stock price is obtained from recent history.

Gamma Support (Put Wall) and Resistance (Call Wall):

Gamma Calculation: For each option, gamma (the rate of change of delta) is computed using the Black-Scholes formula:

gamma = N'(d1) / (S * sigma * sqrt(T))

where S is the stock price, K is the strike, T is time to expiration (in years), sigma is implied volatility, r is the risk-free rate (e.g., 0.0445), and N'(d1) is the normal probability density function.

Weighted gamma is multiplied by open interest and aggregated by strike.

The Put Wall is the strike below the current price with the highest weighted gamma from puts (acting as support).

The Call Wall is the strike above the current price with the highest weighted gamma from calls (acting as resistance).

Short-term versions focus on strikes closer to the money (e.g., within 10-15% of the price).

Gamma Flip Level:

Net dealer gamma exposure (GEX) is calculated across all strikes:

GEX = sum (gamma * OI * 100 * S^2 * sign * decay)

where sign is +1 for calls/-1 for puts, and decay is 1 / sqrt(T).

The flip point is the price where net GEX changes sign (from positive to negative or vice versa), interpolated between strikes.

Vanna Levels:

Vanna (sensitivity of delta to volatility) is calculated:

vanna = -N'(d1) * d2 / sigma

where d2 = d1 - sigma * sqrt(T).

Weighted by open interest, the highest positive and negative vanna strikes are identified.

Other Levels:

S1/R1: Significant strikes with high combined open interest and volume (80% OI + 20% volume), below/above price for support/resistance.

Implied Move: ATM implied volatility scaled by S * sigma * sqrt(d/365) (e.g., for 7 days).

Call/Put Ratio: Total call contracts divided by put contracts (OI + volume).

IV Percentage: Average ATM implied volatility.

Options Activity Level: Average contracts per unique strike, binned into levels (0-4).

Stop Loss: Dynamically set below the lowest support (e.g., Put Wall, Gamma Flip), adjusted by IV (tighter in low IV).

Fib Target: 1.618 extension from Put Wall to Call Wall range.

Previous day levels are stored for comparison (e.g., to detect Call Wall movement >2.5% for alerts).

Effect as Support and Resistance in Technical Trading

Options levels like gamma walls influence price action due to market maker hedging:

Put Wall (Gamma Support): High put gamma below price creates a "magnet" effect—market makers buy stock as price falls, providing support. Traders might look for bounces here as entry points for longs.

Call Wall (Gamma Resistance): High call gamma above price leads to selling pressure from hedging, acting as resistance. Rejections here could signal trims, sells or even shorts.

Gamma Flip: Where gamma exposure flips sign, often a volatility pivot—crossing it can accelerate moves (bullish above, bearish below).

Vanna Levels: Positive/negative vanna indicate volatility sensitivity; crosses may signal regime shifts.

Implied Move: Shows expected range; prices outside suggest overextension.