Daily RTH Moving Average On Intraday Timeframes [vnhilton]This indicator is intended for intraday use from the daily timeframe down to the 1 minute. Outside this range, the indicator won't work as intended.

Higher timeframe moving averages are step-lines as they use values from higher timeframes to calculate the moving average. To have a smoother moving average from higher timeframes plotted on lower timeframes, this indicator uses the chart timeframe's candles, allowing for a smooth higher timeframe moving average. This indicator also includes Bollinger Bands. Note that the indicator only uses values from regular trading hours, as to not give weighting to values from extended trading hours.

In the chart above, at October 7th, pre-market price action is bearish due to fundamentals around US employment data. This day led to an all-day-fader, stopping above the June low after attempting to break down the level again (previous breakdown attempts led to the September low). Note that the price is within the Bollinger bands of the 5 day moving average. We can see in the following days that $SPY trended downwards, staying below the anchored VWAP when the October 7th news released, & pay attention to October 10th, where price attempts to make a new low-of-day but ends up outside the 5 day period ma, leading to a reversal. Look at October 13th, where pre-market price action again shows bearish sentiment, but due to fundamentals around CPI data. $SPY opens below the September low, but also ends up outside the daily 5 period MA bands, meaning that the downside extension has extended too far, signalling for a reversion to the mean. This is why October 13th didn't lead to another all-day-fader, & instead trapped sellers trying to short the pre-market low, helping to fuel the relief rally to cause the upsides the June & September lows, & the anchored VWAPs from both significant pre-market events, to be reclaimed, where price pauses at the confluence of the 5 day moving average & the June low.

Pesquisar nos scripts por "daily"

Daily VolumeShows a table in the top right of the chart with a few options:

Only show intraday: By default the table will not be visible on timeframes of 1D or above, but this can be changed to show all the time if desired.

Daily volume: Displays the volume for the day so far, regardless of what timeframe is currently showing.

Yesterday's volume: Displays the volume from the previous day. As with the daily volume , it will show the entire previous day's volume regardless of the current timeframe.

Average Volume: Displays the average volume based on a user-specified number of days. The default value is 30 days.

Text color and table color: Choose the color settings for the table text and background.

Daily/Weekly ExtremesBACKGROUND

This indicator calculates the daily and weekly +-1 standard deviation of the S&P 500 based on 2 methodologies:

1. VIX - Using the market's expectation of forward volatility, one can calculate the daily expectation by dividing the VIX by the square root of 252 (the number of trading days in a year) - also know as the "rule of 16." Similarly, dividing by the square root of 50 will give you the weekly expected range based on the VIX.

2. ATR - We also provide expected weekly and daily ranges based on 5 day/week ATR.

HOW TO USE

- This indicator only has 1 option in the settings: choosing the ATR (default) or the VIX to plot the +-1 standard deviation range.

- This indicator WILL ONLY display these ranges if you are looking at the SPX or ES futures. The ranges will not be displayed if you are looking at any other symbols

- The boundaries displayed on the chart should not be used on their own as bounce/reject levels. They are simply to provide a frame of reference as to where price is trading with respect to the market's implied expectations. It can be used as an indicator to look for signs of reversals on the tape.

- Daily and Weekly extremes are plotted on all time frames (even on lower time frames).

Daily Volume, RVol, RRVol, and RS/RW LabelsHeads-up display of essential Real Day Trading criteria

Daily Volume

Relative Strength/Weakness

ATR 14 and ATR 14 percent of price

Relative Volume (RVol)

Relative Volume to SPY RVol (RRVol)

Daily SMA In Lower Timeframe public versionThis script aims to provide the daily SMAs (50,100,200) in lower time frames, but ONLY if current price is less than 5% away from it (public code version)

Daily Short Volume RatioThe short volume ratio is the number of shares sold short divided by the average daily volume and is used to indicate sentiment. In its most basic form, short volume ratio above 0.5 indicates more folks are shorting the stock while a short volume ratio below 0.5 indicates more folks are buying the stock. Short volume and total volume data is collected daily from FINRA for the NYSE and the NASDAQ exchange and represents lit markets. Daily short and total volume is calculated after the exchanges close so will lag by a day on the chart.

This indicator displays the short volume ratio for the last 1, 2, 3, 4, and 5 days and includes a smoothing function (def: off) to better visualize trends.

The indicator also includes the ability to view the short volume ratio for the last day for a reference ticker (def: SPY) to compare with total market sentiment.

Thanks to those before me for providing ideas and code.

Daily Short VolumeThis is a script to utilize Quandl (Now Nasdaq Data Link) FINRA Short Volume datasets to see daily volume proportions by short / long activity.

For clarity, long volume does not indicate buying or selling, just that some volume for the day was either buying-to-open or selling-to-close.

Similar but opposite, short volume indicates that some volume for the day was either selling-to-open or buying-to-close.

The decimal value indicates the proportion of Long to Short volume. Example, 0.40 green / 0.60 red would indicate 40% long volume / 60% short volume for that day.

We can take that information as well as the overall outcome of the days session to get an idea for who was drove the market direction for the day.

The four clear outcomes that we can look for are:

If the volume was mostly long (a mostly green bar in the indicator) than an up day would indicate position holders added to long positions.

If the volume was mostly long (a mostly green bar in the indicator) than a down day would indicate position holders reduced from long positions.

If the volume was mostly short (a mostly red bar in the indicator) than a down day would indicate position holders sold short and added to short positions.

If the volume was mostly short (a mostly red bar in the indicator) than an up day would indicate position holders bought to cover long positions.

Those are the clearest possible cases but far more likely the volume will be muddled between short and long making interpreting the net outcome of the day far more difficult.

Unfortunately this data is only published at a daily resolution by FINRA and is usually available at the end of the trading day approximately 3-4 hours following market close.

Please reach out with any questions, suggestions, or recommendations on how to improve this indicator.

Best,

Zero

Daily Scalping Moving AveragesThis is a technical analysis study based on the most fit leading indicators for short timeframes like EMA and SMA.

At the same time we have daily channel made from the last 2 weeks of ATR values, which will give us the daily top and bottom expected values(with 80%+ confidence)

We have 3 groups of lengths for short length, medium length and a bigger length.

At the same time we combine it with the daily vwap values .

In the end we are going to have a total of 7 indicators telling us the direction.

The way we can use it :

The max ratings that we can have are +7 for long and -7 for short

In general once we have at least 5 indicators(fast and medium ones) giving us a direction, there is a high chance that we can scalp that trend and then we can exit either when we will be at +7 or close to neutral point

At the same time is very important to be aware of the current position inside of the TOP/BOTTOM channel that we have.

For example lets assume we are at 40k on BTC and our top channel is around 41-42k while the bottom is around 38k. In this case the margin that we have for long is much smaller than for short, so we should be prepared to exit once we reach the top values and from there wait and see if there is a huge continuation or a reversal. If the top channel was hit and the market started the rebounce going downwards and the moving averages confirms it, then we have a huge advantage using the top points as a STOP LOSS and continue the short movements, giving us an amazing risk/reward ratio .

If you have any questions let me know !

Daily Sun Flares Class XThe classification system for solar flares uses the letters A, B, C, M or X, according to the peak flux as measured at the Earth by the GOES spacecraft.

These are daily Class X sun flares. The data was created by counting daily flares of this class based on the peak time of the flare.

2015-01-01 until 2021-08-25

Daily EMA50 100 200 + BBStandard Bollinger Bands (timeframe dependent), period and standard deviation are configurable.

And standard daily triple EMA (timeframe independent). Short, Medium and Long periods are configurable (50/100/200 by default)

Daily Sun Flares Class MThe classification system for solar flares uses the letters A, B, C, M or X, according to the peak flux as measured at the Earth by the GOES spacecraft.

These are daily Class M sun flares. The data was created by counting daily flares of this class based on the peak time of the flare.

Daily Sun Flares Class CThe classification system for solar flares uses the letters A, B, C, M or X, according to the peak flux as measured at the Earth by the GOES spacecraft.

These are daily Class C sun flares. The data was created by counting daily flares of this class based on the peak time of the flare.

Daily Weekly Monthly Yearly OpensThis indicator draws key level lines such as daily open, weekly open, monthly open, yearly open, previous daily open, previous weekly open, previous monthly open, previous yearly open, monday daily high and monday daily low to chart. This lines can act either support or resistance but it is just possibility. This lines will help you to find buy and sell places.

Daily Settlement (BM&FBOVESPA B3 FUTURES)This script is simple designed to plot the daily settlement to any Securities traded on B3, Brazilian stock exchange.

The daily settlement is an important price where position traders are adjusted every day. This adjustment is defined by the exchange itself every day at approximately 4 pm, with an average of all trades in this window.

We consider that the settlement is a region of "money spent", where every day, some player "woke up" in long or in short at that price. As this is a region of "money spent", traders should give significant attention when traded at this price.

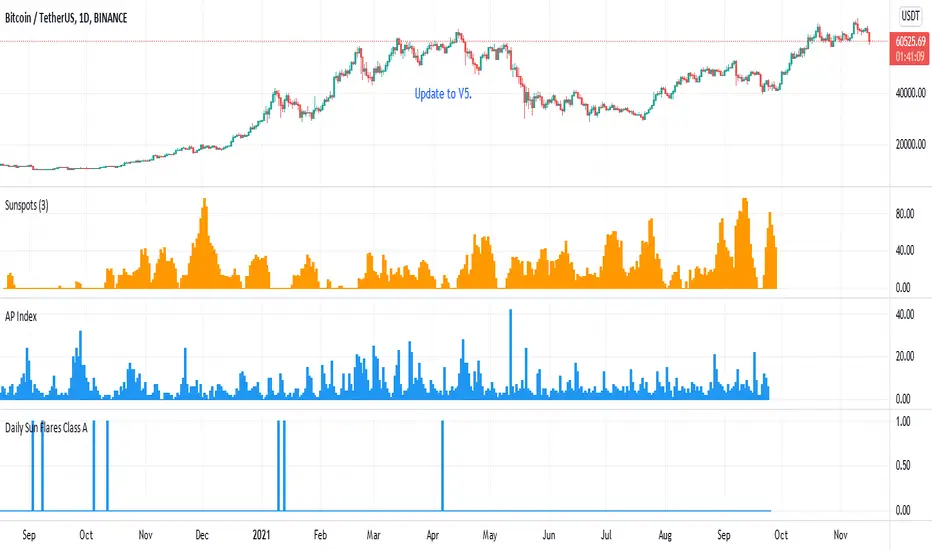

Daily Sun Flares Class AThe classification system for solar flares uses the letters A, B, C, M or X, according to the peak flux as measured at the Earth by the GOES spacecraft.

These are daily Class A sun flares. The data was created by counting daily flares of this class based on the peak time of the flare.

2015-01-01 until 2021-08-25

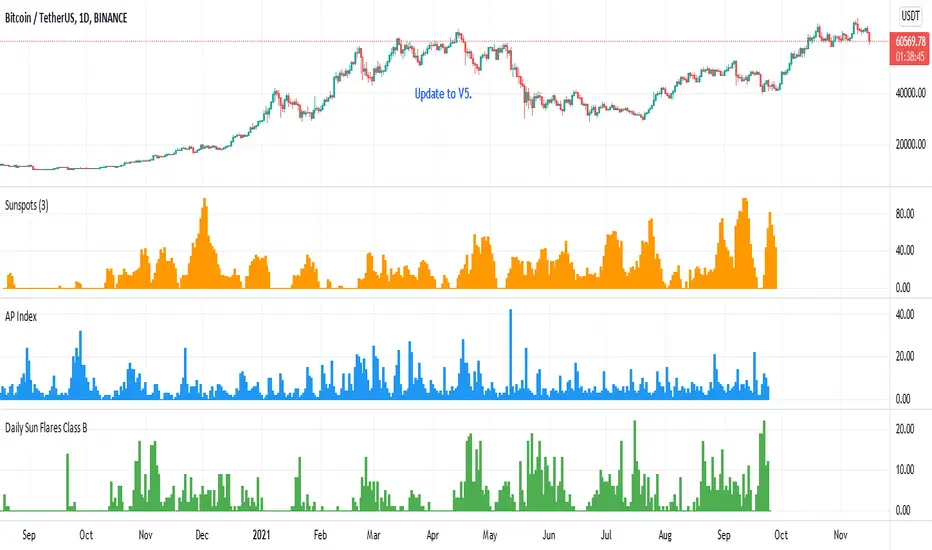

Daily Sun Flares Class BThe classification system for solar flares uses the letters A, B, C, M or X, according to the peak flux as measured at the Earth by the GOES spacecraft.

These are daily Class B sun flares. The data was created by counting daily flares of this class based on the peak time of the flare.

2015-01-01 until 2021-08-25

Daily Open Horizontal LineThis script draws a horizontal line that starts in the daily open (00:00 UTC)

Basically I did this since lots of times price come back down/up to the daily open and then bounces, meaning we can take trades based on this.

Hope you enjoy it.

PD: Took the code from infernix, all the credits to him, I know shit about coding.

Infernix TDV Profile: tradingview.com/u/infernixx

Financial Astrology Indexes ML Daily TrendDaily trend indicator based on financial astrology cycles detected with advanced machine learning techniques for some of the most important market indexes: DJI, UK100, SPX, IBC, IXIC, NI225, BANKNIFTY, NIFTY and GLD fund (not index) for Gold predictions. The daily price trend is forecasted through planets cycles (angular aspects, speed phases, declination zone), fast cycles are based on Moon, Mercury, Venus and Sun and Mid term cycles are based on Mars, Vesta and Ceres . The combination of all this cycles produce a daily price trend prediction that is encoded into a PineScript array using binary format "0 or 1" that represent sell and buy signals respectively. The indicator provides signals since 2021-01-01 to 2022-12-31, the past months signals purpose is to support backtesting of the indicator combined with other technical indicator entries like MAs, RSI or Stochastic . For future predictions besides 2022 a machine learning models re-train phase will be required.

When the signal moving average is increasing from 0 to 1 indicates an increase of buy force, when is decreasing from 1 to 0 indicates an increase in sell force, finally, when is sideways around the 0.4-0.6 area predicts a period of buy/sell forces equilibrium, traders indecision which result in a price congestion within a narrow price range.

We also have published same indicator for Crypto-Currencies research portfolio:

DISCLAIMER: This indicator is experimental and don’t provide financial or investment advice, the main purpose is to demonstrate the predictive power of financial astrology. Any allocation of funds following the documented machine learning model prediction is a high-risk endeavour and it’s the users responsibility to practice healthy risk management according to your situation.

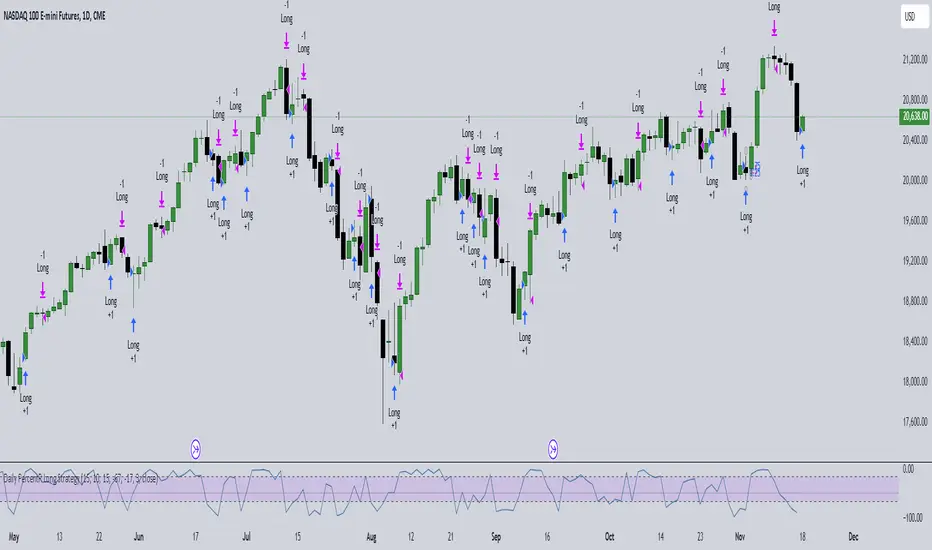

Daily PercentR StrategyThe PercentR strategy from Larry Williams is highly profitable on the daily nasdaq chart

Buy at the open if PercentR Indicator is above –87 and below –20

Exit at the end of the day.

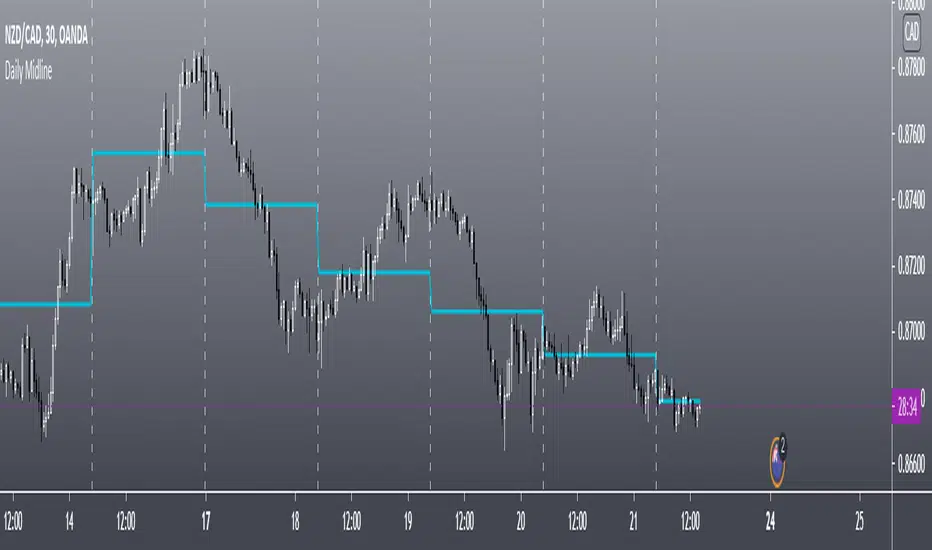

Daily MidlineThis Scripts Shows Daily Midline Levels From Yesterday High/lows.

Credits to rodrigo.aprieto and NorthstarDaytrading

for combined script idea.

Daily and Weekly Moving Averages on Daily ChartFor the long term trend I use the 200 and 150 daily moving averages. The 200-day MA will be plotted as a black line. It is a no-go zone to buy anything trading below that.

The 150-day, or 30-week like Stan Weinstein uses, is plotted in orange.

Than I use the 50 day moving average but also the 10 week moving average. While those look similar there is a small difference which sometimes impacts the choice for selling a stock or holding on to it.

That slight difference is useful in different situations that’s why I want to have them both on my chart.

Both the 50-day and the 10-week are plotted as red lines on the chart. Since there’s only a small difference the same color gives a nicer view.

For shorter term trend I like to use the 20 and 10 day exponential moving averages. I tested these but also the commonly used 21, 9 and some other variations. But came to the conclusion that for me the 20EMA and 10EMA works best.

Both EMA’s are plotted in blue, where the 20EMA has a thicker line to easily see the difference.

Daily Pivot (Fibonacci)Hello All

-

This is Daily Pivot (Fibonacci).

Simple and very useful tool for traders.

Show R5 to S5 levels.

.

Feel free to comment.

Thank you.

Daily Pivot (Traditional)Hello all

-

This code is for daily pivot points, support and resistance with pivot labels and value.

simple code with no bugs.

this code use previous day values on online chat and current day values on offline chat.

pivot values are placed on right side, so no overlapping with other values.

.

.

Thank you Trading View for other educational script to make this possible.