MMI SignalTrend trading strategies filtered by the Market Meanness Index.

This is a port of the experiment described at

www.financial-hacker.com

www.financial-hacker.com

www.financial-hacker.com

www.financial-hacker.com

The Market Meanness Index tells whether the market is currently moving in or out of a "trending" regime. It can this way prevent losses by false signals of trend indicators. It is a purely statistical algorithm and not based on volatility, trends, or cycles of the price curve.

The indicator measures the meanness of the market - its tendency to revert to the mean after pretending to start a trend. If that happens too often, all trend following systems will bite the dust.

Inputs

Price Source: Either open, high, low, close, hl2, hlc3, or ohlc4. The default value is hlc3.

Trend MA Type: Either SMA, EMA, LowPass, Hull MA, Zero-Lag MA, ALMA, Laguerre, Smooth, Decycle. The default value is LowPass.

Trend MA Period: Sets the lookback period of trend MA. The default value is 200.

MMI Period: Sets the lookback period of the Market Meanness Index. The default value is 300.

Pesquisar nos scripts por "curve"

NG [Gaussian Filter Multi-Pole]When smoothing data there is always a trade-off between lag and removal of noise.

Gaussian filter has a consistently low lag and a very smooth curve.

This filter works for poles higher than the 4 (usual usage).

Mathematically maximum poles is 15 after which coefficients are too high to see any difference.

By tuning Lag and number of Poles you can achieve a very smooth MA with least lag possible.

It's just as good as 3rd gen moving averages and can be used as input feed for other indicators.

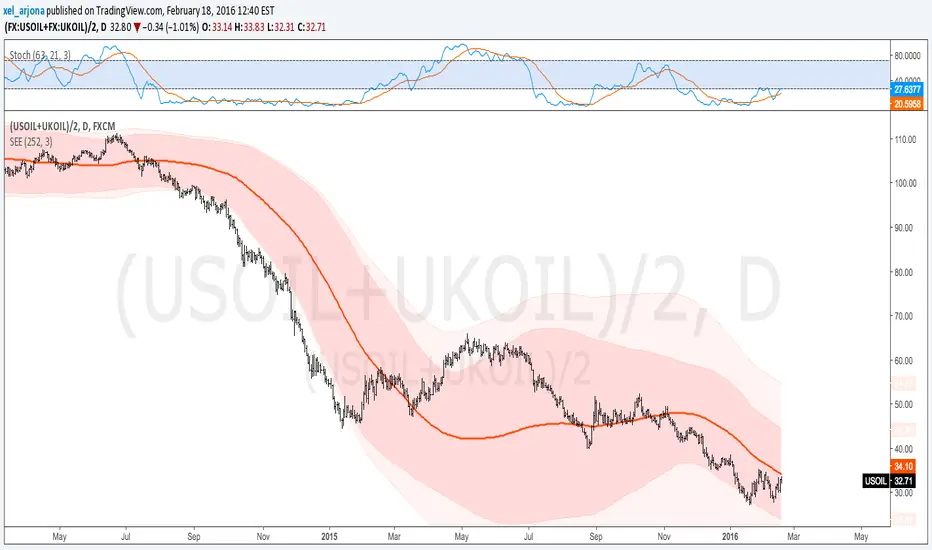

Standard Error of the Estimate -Composite Bands-Standard Error of the Estimate - Code and adaptation by @glaz & @XeL_arjona

Ver. 2.00.a

Original implementation idea of bands by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

This code is a former update to previous "Standard Error Bands" that was wrongly applied given that previous version in reality use the Standard Error OF THE MEAN, not THE ESTIMATE as it should be used by Jon Andersen original idea and corrected in this version.

As always I am very Thankfully with the support at the Pine Script Editor chat room, with special mention to user @glaz in order to help me adequate the alpha-beta (y-y') algorithm, as well to give him full credit to implement the "wide" version of the former bands.

For a quick and publicly open explanation of this truly statistical (regression analysis) indicator, you can refer at Here!

Extract from the former URL:

Standard Error Bands are quite different than Bollinger's. First, they are bands constructed around a linear regression curve. Second, the bands are based on two standard errors above and below this regression line. The error bands measure the standard error of the estimate around the linear regression line. Therefore, as a price series follows the course of the regression line the bands will narrow, showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands.

Standard Error Bands by @XeL_arjonaStandard Error Bands - Code by @XeL_arjona

Original implementation by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Version 1

For a quick and publicly open explanation of this Statistical indicator, you can refer at Here!

Extract from the former URL:

Standard Error bands are quite different than Bollinger's. First, they are bands constructed around a linear regression curve. Second, the bands are based on two standard errors above and below this regression line. The error bands measure the standard error of the estimate around the linear regression line. Therefore, as a price series follows the course of the regression line the bands will narrow, showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands.

Standardized ROC Engine (EMA Version)The purpose of this script is to create a standardized rate‑of‑change engine that compares the momentum of multiple structural anchors, specifically several EMAs, VWAP, price and volume. By converting each ROC stream into a z‑score, the indicator places all components on a common scale, allowing the trader to see when any anchor is accelerating or decelerating relative to its own long‑term distribution. This transforms raw ROC, which is naturally unstable and scale‑dependent, into a normalized momentum map that highlights extremes, clustering and regime shifts with far greater clarity.

The script works by first computing four EMAs of different lengths, along with VWAP, then calculating the percentage rate of change for each series over a user‑defined ROC window. Each ROC stream is then passed through a standardization function that subtracts its rolling mean and divides by its rolling standard deviation, producing a z‑score that expresses how unusual the current momentum is compared to the past. These standardized curves are plotted together, using consistent colors, while horizontal reference lines at one, two and three standard deviations provide visual thresholds for identifying statistically significant momentum events.

The rationale behind this architecture is that raw ROC values are not comparable across different structures because each anchor has its own volatility profile, amplitude and noise characteristics. Standardization solves this by converting every ROC stream into a dimensionless measure of deviation, enabling cross‑anchor comparison without distortion. This approach reveals when short‑term EMAs are accelerating faster than long‑term EMAs, when VWAP momentum diverges from trend momentum, and when volume expansion aligns with or contradicts price acceleration, all expressed in a unified statistical language that is robust across assets and timeframes.

MA Ribbon (Horizontal Levels)📊 MA Ribbon (Horizontal Levels)

MA Ribbon (Horizontal Levels) is a minimalist moving average tool that displays moving averages as horizontal price levels instead of traditional sloping lines.

Rather than showing the historical path of each moving average, this indicator focuses exclusively on where each selected MA is currently located in price, allowing traders to treat moving averages as dynamic support and resistance levels.

The result is a clean, uncluttered chart that preserves moving average structure without visual noise.

🔍 What Makes It Different

No traditional moving average curves

No shading, bands, or fills

Each moving average is represented as a horizontal line at its current value

Lines automatically update as price and the MA value change

Designed to complement price action rather than dominate the chart

This approach makes it easier to see key MA levels at a glance, especially when multiple averages are in use.

⚙️ Key Features

✅ Fully Customizable Moving Averages

Select the moving average type:

SMA

EMA

SMMA (RMA)

WMA

VWMA

Choose the price source (e.g., close)

Configure up to 10 independent moving averages

✅ Per-MA Controls

Each moving average can be customized individually:

Enable or disable any MA (use anywhere from 1 to 10)

Set the MA period (length)

Choose line color

Adjust line thickness

Select line style (solid, dashed, dotted)

✅ Horizontal Level Visualization

Each MA is plotted as a horizontal line extending across the chart, representing the current value of that moving average.

As the MA updates, the level shifts vertically, maintaining a clear and consistent reference point.

🧠 How to Use It

This indicator is designed as a context and structure tool, not a signal generator.

Common use cases include:

Identifying dynamic support and resistance zones

Visualizing where short-term and long-term MA levels are stacked

Using MA levels as confluence with price action, VWAP, or volume-based tools

Maintaining a clean chart while still respecting moving average structure

Because the lines are horizontal, the indicator is especially useful for:

Breakout traders

Mean-reversion traders

Market participants who focus on structure and levels rather than indicator signals

🎯 Who It’s For

This indicator is ideal for traders who:

Prefer minimal, uncluttered charts

Think of moving averages as levels, not signals

Want full control over MA appearance and behavior

Use price action and structure first, indicators second

Use this tool in conjunction with standard moving average indicators, treating these horizontal MA levels as complementary reference points rather than replacements

MA Ribbon (Horizontal Levels) is built for traders who want clarity, flexibility, and structural insight — without sacrificing chart readability.

Apex Wallet - Ultimate Trading Suite: All-In-One Overlay & SignaOverview The Apex Wallet All-In-One is a comprehensive professional trading toolkit designed to centralize every essential technical analysis tool directly onto your main price chart. Instead of cluttering your workspace with dozens of separate indicators, this script integrates trend analysis, volatility bands, automated chart patterns, and a multi-indicator signal engine into a single, cohesive interface.

Key Modular Features:

Trend Core: Features dynamic trend curves, cloud fills for momentum visualization, and a multi-timeframe dashboard (1m to 4h) to ensure you are always trading with the higher-timeframe bias.

Automated Chart Structures: Automatically detects and plots Support/Resistance levels, Standard Pivot Points, Market Gaps, and Fair Value Gaps (Imbalances).

Volatility & Volume: Includes professional-grade VWAP with standard deviation bands, Bollinger Bands, and a built-in Volume Delta (Raw/Net) tracker.

Signal Engine: A powerful cross-logic system that generates entry signals based on RSI (QQE), MACD (Zero-cross & Relance), Stochastic, TDI, and the Andean Oscillator.

Predictive Projections: A unique feature that projects current indicator slopes into future candles to help anticipate potential trend continuations or reversals.

Adaptability The script includes three core presets—Scalping, Day-Trading, and Swing-Trading—which automatically adjust all internal periods (Moving Averages, Bollinger, RSI, etc.) to match your specific market speed.

Visual Cleanliness Every feature is toggleable. You can display a "clean" chart with just the Trend Cloud or a "complete" workstation with signals, patterns (Doji, Engulfing), and pivot levels

Fed Balance Sheet (Candles)Fed Balance Sheet (Candles) - TradingView Description

📊 OVERVIEW

Fed Balance Sheet (Candles) transforms the Federal Reserve's total assets into an intuitive candlestick visualization, allowing you to track monetary policy changes with the same visual language you use for price action.

This indicator pulls real-time data directly from FRED (Federal Reserve Economic Data) and displays the Total Assets of All Federal Reserve Banks as dynamic candles on your chart, making it effortless to correlate central bank liquidity with market movements.

🎯 WHY THIS MATTERS

The Federal Reserve's balance sheet is one of the most powerful leading indicators in global markets. When the Fed expands its balance sheet (Quantitative Easing), it injects liquidity into the financial system, historically correlating with:

Rising asset prices (stocks, crypto, commodities)

Lower volatility

Risk-on sentiment

Currency devaluation

When the Fed contracts its balance sheet (Quantitative Tightening), liquidity drains from markets, often leading to:

Asset price pressure

Increased volatility

Risk-off sentiment

Dollar strength

By visualizing this as candles, you can instantly see:

The pace of change (candle size)

The direction (green = expansion, red = contraction)

Acceleration or deceleration (consecutive candles in same direction)

Pivots in monetary policy (color changes from green to red or vice versa)

🔧 HOW IT WORKS

Data Source

Source: Federal Reserve Economic Data (FRED)

Metric: Total Assets of All Federal Reserve Banks

Unit: Displayed in Trillions of USD for easy reading

Frequency: Weekly updates (every Wednesday)

Candlestick Construction

Since balance sheet data is reported as a single number each week (not traditional open-high-low-close), this indicator creates candles by comparing each period to the previous one:

Open = Last week's balance sheet value

Close = This week's balance sheet value

High = The higher of the two values

Low = The lower of the two values

This captures directional movement and magnitude of change, making it intuitive for traders accustomed to candlestick analysis.

Color Scheme

🟢 GREEN CANDLES (Expanding Balance Sheet)

When this week's value is higher than last week's

Interpretation: Fed is adding liquidity (Quantitative Easing)

Historically bullish for risk assets

🔴 RED CANDLES (Contracting Balance Sheet)

When this week's value is lower than last week's

Interpretation: Fed is removing liquidity (Quantitative Tightening)

Historically bearish or neutral for risk assets

Value Label

A floating label displays the current balance sheet value in trillions (e.g., "$8.75T") so you always know the exact figure at a glance.

📈 PRACTICAL APPLICATIONS

1. Market Regime Identification

Strings of green candles = Liquidity-driven bull markets

Strings of red candles = Tightening-induced bear markets or corrections

Color transitions = Potential market inflection points

2. Correlation Analysis

Overlay on stock indices (SPY, QQQ, IWM)

Overlay on crypto (BTC, ETH)

Overlay on commodities (Gold, Silver)

Observe how asset prices react to Fed liquidity changes in real-time

3. Macro Timing

Large green candles = Aggressive easing (crisis response)

Large red candles = Aggressive tightening (inflation fighting)

Small candles = Neutral policy (Fed on hold)

4. Risk Management

Shift portfolio allocation based on liquidity environment

Reduce leverage during red candle trends

Increase exposure during green candle trends

Use as confirmation for other technical signals

5. Multi-Timeframe Context

Daily charts: See how daily price action relates to weekly Fed data

Weekly charts: Perfect alignment with data release frequency

Monthly charts: Visualize long-term monetary cycles spanning years

⚙️ SETTINGS

Zero configuration needed. Simply add the indicator to any chart and it works immediately.

The indicator automatically:

Overlays on your main chart

Uses the left price scale (won't interfere with asset prices)

Updates with the latest Fed data

Displays values in trillions for clean readability

🎨 VISUAL DESIGN PHILOSOPHY

The indicator uses semi-transparent candle bodies with vibrant borders to maintain visibility without obscuring your price action. The color scheme follows universal chart conventions where green represents growth/expansion and red represents decline/contraction.

It's designed to blend seamlessly into any chart theme while providing immediate visual clarity about the Fed's monetary stance.

📚 WHAT YOU NEED TO KNOW

Data Availability

Historical data available from December 2002 (over 20 years of Fed policy)

Updates every Wednesday (Federal Reserve's reporting schedule)

Typically published with a 1-week lag

How the Data Appears

On weekdays: Shows the most recent Wednesday's data

On weekends: Shows Friday's data (which is the prior Wednesday's figure)

Updates automatically when new data is released

Scale Considerations

The Fed's balance sheet is measured in trillions, while most assets are priced much lower. The indicator uses the left price scale by default to avoid conflicts with your main asset's price scale. You can easily move it to a separate pane if you prefer.

🧠 INTERPRETATION GUIDE

Historical QE Phases (Green Candles)

2008-2014: Financial Crisis Response

The Fed's balance sheet expanded from under $1T to ~$4.5T to stabilize markets after the mortgage crisis.

2020: COVID-19 Response

Rapid expansion to ~$7T as the Fed stepped in during pandemic lockdowns.

2020-2022: Extended Support

Balance sheet reached historic peak of ~$9T.

Historical QT Phases (Red Candles)

2017-2019: First Modern QT Attempt

The Fed tried to normalize its balance sheet, reducing it from ~$4.5T to ~$3.8T before pivoting.

2022-Present: Inflation-Fighting QT

The Fed began shrinking its balance sheet to combat inflation, letting bonds mature without replacement.

Key Insights

Size matters, but rate of change matters MORE.

A $9T balance sheet growing slowly has different implications than a $5T balance sheet growing rapidly.

Watch for acceleration.

Increasingly large candles (up or down) signal a policy shift that markets will notice.

Plateaus mean "wait and see."

Tiny candles indicate the Fed is holding steady and watching economic data.

Reversals are major events.

When candles switch from green to red (or vice versa), the Fed has changed course—these are critical market turning points.

🎓 EDUCATIONAL VALUE

This indicator helps you understand:

The mechanics of monetary policy through visual learning

The lag between Fed actions and market reactions by observing temporal correlation

The scale of modern central banking (trillions put into perspective)

The relationship between liquidity and asset prices (cause and effect in action)

Many traders talk about "don't fight the Fed" but never actually track what the Fed is doing. Now you can see it as clearly as you see price action.

🔗 RELATED CONCEPTS

For comprehensive macro analysis, consider also tracking:

Fed Funds Rate (short-term interest rates)

M2 Money Supply (broader measure of money in circulation)

Treasury Yield Curves (bond market expectations)

Dollar Index (DXY) (currency strength)

VIX (market fear/volatility)

The Fed's balance sheet is just one piece of the puzzle, but it's arguably the most important one for understanding liquidity conditions.

⚠️ DISCLAIMER

This indicator displays publicly available economic data from the Federal Reserve. It is for informational and educational purposes only and does not constitute financial advice.

Important considerations:

Past monetary policy does not guarantee future market outcomes

Correlation does not equal causation

Asset prices are influenced by many factors beyond Fed liquidity

Always use proper risk management

Consult with qualified financial professionals before making investment decisions

Trading involves substantial risk of loss and is not suitable for everyone.

📜 VERSION HISTORY

Version 1.0 - Initial Release

Fed balance sheet visualized as candlesticks

Real-time FRED data integration

Automatic display in trillions

Dynamic color coding (green/red)

Current value label with exact figure

💡 WHY CANDLES?

You might wonder: "Why show the Fed's balance sheet as candles instead of a line?"

Because candles tell stories that lines can't.

A line shows you where we are

Candles show you how we got here, how fast we're moving, and what momentum looks like

Candles make the Fed's actions feel immediate and tangible

Candles connect macro data to the chart language you already speak

When you see three big green candles in a row on the Fed balance sheet while your crypto or stock portfolio is rallying, you feel the connection. When you see the candles turn red and shrink, you understand the headwinds forming.

It transforms dry economic data into actionable market intelligence.

📞 SUPPORT & FEEDBACK

If you find this indicator valuable:

⭐ Like and favorite to help others discover it

📝 Comment with your use cases and insights

🔔 Follow for updates and new macro indicators

Your feedback drives improvements and helps build better tools for the trading community.

🚀 THE BOTTOM LINE

The Fed's balance sheet is the tide that lifts or lowers all boats.

Whether you're trading stocks, crypto, forex, or commodities—whether you're a day trader or long-term investor—understanding the Fed's liquidity operations gives you an edge.

This indicator makes that understanding visual, immediate, and actionable.

Stop guessing about macro conditions. Start seeing them.

"Don't fight the Fed" - Wall Street Wisdom

Now you can see exactly what they're doing—in the same language you use to read price action.

May your trades ride the tide of liquidity. 🌊📈

Area per IntervalDescription

This indicator shades the area between 2 curves, an SMA and the nearest open/close to the SMA, and their intersections. The black labels with leader lines describe the calculated area of each shaded section, and the total area accumulated per total number of time intervals for that area. The additional value visible in the status line that is not displayed on the chart is, at any bar index (time interval), the current total area of the incomplete shaded area.

Usage

- The default color of the shaded areas denote the type of momentum being built before the cross. Green for bullish, red for bearish.

- The area value of the shaded areas can be used as a capacity indicator, denoting imbalances between the previous and next crosses.

- The area per interval value of the shaded areas can be used as a momentum indicator, denoting which area is carrying more price movement before the price crosses.

- Similar to indicators that use dynamic price differences between OHLC data, moving averages, etc, confluence with other momentum indicators that use different elements creates additional confirmation.

Conclusion

Simple momentum indicator. Comment for possible updates that can be made.

Multi-Distribution Volume Profile (Zeiierman)█ Overview

Multi-Distribution Volume Profile (Zeiierman) is a flexible, structure-first volume profile tool that lets you reshape how volume is distributed across price, from classic uniform profiles to advanced statistical curves like Gaussian, Lognormal, Student-t, and more.

Instead of forcing every market into a single "one-size-fits-all" profile, this tool lets you model how volume is likely concentrated inside each bar (body vs wicks, midpoint, tails, center bias, right-skew, heavy tails, etc.) and then stacks that behavior across a whole lookback window to build a rich, multi-distribution map of traded activity.

On top of that, it overlays a dynamic Center Band (value area) and a fade/gradient model that can color each price row by volume, hits, recency, volatility, reversals, or even liquidity voids, turning a plain profile into a multi-dimensional context map.

Highlights

Choose from multiple Profile Build Modes , including uniform, body-only, wick-only, midpoint/close/open, center-weighted, and a suite of probability-style distributions (Gaussian, Lognormal, Weibull, Student-t, etc.)

Flexible anchor layout: draw the profile on Right/Left (horizontal) or Bottom/Top (vertical) to fit any chart layout

Value Area / Center Band computed from volume quantiles around the POC.

Gradient-based Fade Metrics: volume, price hits, freshness (time decay), volatility impact, dwell time, reversal density, compression, and liquidity voids

Separate bullish vs bearish volume at each price row for directional structure insights

█ How It Works

⚪ Profile Construction

The script scans a user-defined Bars Included window and finds the full high–low span of that zone. It then divides this range into a user-controlled number of Price Levels (rows).

For each historical bar within the window:

It measures the candle’s price range, body, and wicks.

It assigns volume to rows according to the selected Profile Build Mode, for example:

* Range Uniform – volume spread evenly across the full high–low range.

* Range Body Only / Range Wick Only – concentrate volume inside the body or wicks only.

* Midpoint / Close / Open Only – allocate volume entirely into one price row (pinpoint modeling).

HL2 / Body Center Weighted – center weights around the middle of the range/body.

Recent-Weighted Volume – amplify newer bars using exponential time decay.

Volume Squared (Hard) – aggressively boost bars with large volume.

Up Bars Only / Down Bars Only – filter volume to only bullish or bearish bars.

For more advanced shapes, the script uses continuous distributions across the bar’s span:

Linear, Triangular, Exponential to High

Cosine Centered, PERT

Gaussian, Lognormal, Cauchy, Laplace

Pareto, Weibull, Logistic, Gumbel

Gamma, Beta, Chi-Square, Student-t, F-Shape

Each distribution produces a weight for each row within the bar’s range, normalized so the total volume remains consistent, but the shape of where that volume lands changes.

⚪ POC & Center Band (Value Area)

Once all rows are accumulated:

The row with the highest total volume becomes the Point of Control (POC)

The script computes cumulative volume and finds the band that wraps a user-defined Center of Profile % (e.g., 68%) around the center of distribution.

This range is displayed as a central band, often treated like a value area where price has spent the most “effort” trading.

⚪ Gradient Fade Engine

Each row also gets a fade metric, chosen in Fade Metric:

Volume – opacity based on relative volume.

Price Hits – how frequently that row was touched.

Blended (Vol+Hits) – average of volume & hits.

Freshness – emphasizes recent activity, controlled by Decay.

Volatility Impact – rows that saw larger ranges contribute more.

Dwell Time – where price “camped” the longest.

Reversal Density – where direction changes cluster.

Compression – tight-range compression zones.

Liquidity Void – inverse of volume (thin liquidity zones).

When Apply Gradient is enabled, the row’s bullish/bearish colors are tinted from faint to strong based on this chosen metric, effectively turning the profile into a heatmap of your chosen structural property.

█ How to Use

⚪ Explore Different Distribution Assumptions

Switch between multiple Profile Build Modes to see how your assumptions about intrabar volume affect structure:

Use Range Uniform for classical profile reading.

Deploy Gaussian, Logistic, or Cosine shapes to emphasize central clustering.

Try Pareto, Lognormal, or F-Shape to focus on tail / extremal activity.

Use Recent-Weighted Volume to prioritize the most recent structural behavior.

This is especially useful for traders who want to test how different modeling assumptions change perceived value areas and levels of interest.

⚪ Identify Value, Acceptance & Rejection Zones

Use the POC and Center of Profile (%) band to distinguish:

High-acceptance zones – wide central band, thick rows, strong gradient → fair value areas

Rejection zones & tails – thin extremes, low dwell time, high volatility or reversal density

These regions can be used as:

Targets and origin zones for mean reversion

Context for breakout validation (leaving value)

Bias reference for intraday rotations or swing rotations

⚪ Read Directional Structure Within the Profile

Because each row is split into bullish vs bearish contributions, you can visually read:

Where buyers dominated a price region (large bullish slice)

Where sellers absorbed or defended (large bearish slice)

Combining this with Fade Metrics like Reversal Density, Dwell Time, or Freshness turns the profile into a structural order-flow map, without needing raw tick-by-tick volume data.

⚪ Use Fade Metrics for Contextual Heatmaps

Each Fade Metric can be used for a different analytical lens:

Volume / Blended – emphasize where volume and activity are concentrated.

Freshness – highlight the most recently active zones that still matter.

Volatility Impact & Compression – spot areas of explosive moves vs coiled ranges.

Reversal Density – locate micro turning points and battle zones.

Liquidity Void – visually pop out thin regions that may act as speedways or magnets.

█ Settings

Profile Build Mode – Selects how each bar’s volume is distributed across its price range (uniform, body/wick, midpoint/close/open, center-weighted, or statistical distribution families).

Bars Included – Number of bars used to build the profile from the current bar backward.

Price Levels – Vertical resolution of the profile: more levels = smoother but heavier.

Anchor Side – Where the profile is drawn on the chart: Right, Left, Bottom, or Top.

Offset (bars) – Horizontal offset from the last bar to the profile when using Right/Left modes.

Apply Gradient – Toggles the fade/heatmap coloring based on the selected metric.

Fade Metric – Chooses the property driving row opacity (Volume, Hits, Freshness, Volatility Impact, Dwell Time, Reversal Density, Compression, Liquidity Void).

Decay – Time-decay factor for Freshness (values close to 1 keep older activity relevant for longer).

Profile Thickness – Relative thickness of the profile along the time axis, as a % of the lookback window.

Center of Profile (%) – Volume percentage used to define the central band (value area) around the POC.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Robrechtian Long-Medium Breakout Trend SystemRobrechtian Long–Medium-Term Breakout Trend System

A professional, rule-based trend-following strategy designed to capture large, sustained price movements using pure price action and breakouts.

This system follows long-established trend-following philosophy: no prediction, no volatility targeting, and no profit targets. Only disciplined entries, position additions, and exits driven entirely by trend structure.

Core Principles

Breakout-driven entries: Initial positions are taken only when price breaks above/below the 80-day Donchian channel, confirming a long–medium-term trend shift.

Short-term confirmation: Breakouts must also exceed the 20-day channel, reducing false positives.

Trend-direction filter: A 50-day moving average slope filter ensures alignment with the broader trend.

Explosive bar filter: Entries avoid excessively large, single-candle expansions (>2.5× ATR(20)) to prevent chasing exhaustion spikes.

Pyramiding into strength: Additional units are added only when price makes fresh 20-day breakouts in the direction of the trend. No scaling out. No adding on dips.

Exit only on trend violation: Positions are closed exclusively when price breaks the opposite 80-day channel. This preserves unlimited upside while enforcing disciplined exits.

Pure trend philosophy: No volatility targeting, no smoothing, no discretionary overrides, no optimization for short-term performance.

Intended Use

This system is designed primarily for diversified futures portfolios, where diversification across dozens of globally liquid markets creates robustness and stability. However, it may also be used on individual assets for educational and analytical purposes.

The system embraces the core trend-following logic:

Small losses, big winners, and unlimited upside when trends persist.

⚠️ WARNINGS / DISCLAIMERS

⚠️ Warning 1 — This strategy is not optimized for single stocks

The Robrechtian Trend System is designed for multi-asset futures portfolios, not single equities.

Performance on individual tickers may vary greatly due to lack of diversification.

⚠️ Warning 2 — Trend following includes substantial drawdowns

Deep drawdowns are a normal and expected feature of all long-term trend-following systems.

The strategy does not attempt to smooth returns or manage volatility.

If you seek steady, low-volatility equity curves, this system is not suitable.

⚠️ Warning 3 — No volatility targeting or risk smoothing

This system intentionally avoids volatility-based position sizing.

Trades may experience larger fluctuations than systems using risk parity or vol targeting.

⚠️ Warning 4 — Not financial advice

This script is for educational and research purposes only.

Past performance does not guarantee future results.

Use at your own risk.

⚠️ Warning 5 — TradingView backtests have known limitations

TradingView does not simulate:

futures contract roll logic

slippage

real bid/ask spreads

liquidity conditions

limit-up/limit-down behavior

Results may vary from live market execution.

Kalman Ema Crosses - [JTCAPITAL]Kalman EMA Crosses - is a modified way to use Kalman Filters applied on Exponential Moving Averages (EMA Crosses) for Trend-Following.

Credits for the kalman function itself goes to @BackQuant

The Kalman filter is a recursive smoothing algorithm that reduces noise from raw price or indicator data, and in this script it is applied both directly to price and on top of EMA calculations. The goal is to create cleaner, more reliable crossover signals between two EMAs that are less prone to false triggers caused by volatility or market noise.

The indicator works by calculating in the following steps:

Source Selection

The script starts by selecting the price input (default is Close, but can be adjusted). This chosen source is the foundation for all further smoothing and EMA calculations.

Kalman Filtering on Price

Depending on user settings, the selected source is passed through one of two independent Kalman filters. The filter takes into account process noise (representing expected market randomness) and measurement noise (representing uncertainty in the price data). The Kalman filter outputs a smoothed version of price that minimizes noise and preserves underlying trend structure.

EMA Calculation

Two exponential moving averages (EMA 1 and EMA 2) are then computed on the Kalman-smoothed price. The lengths of these EMAs are fully customizable (default 15 and 25).

Kalman Filtering on EMA Values

Instead of directly using raw EMA curves, the script applies a second layer of Kalman filtering to the EMA values themselves. This step significantly reduces whipsaw behavior, creating smoother crossovers that emphasize real momentum shifts rather than temporary volatility spikes.

Trend Detection via EMA Crossovers

-A bullish trend is detected when EMA 1 (fast) crosses above EMA 2 (slow).

-A bearish trend is detected when EMA 1 crosses below EMA 2.

The detected trend state is stored and used to dynamically color the plots.

Visual Representation

Both EMAs are plotted on the chart. Their colors shift to blue during bullish phases and purple during bearish phases. The area between the two EMAs is filled with a shaded region to clearly highlight trending conditions.

Buy and Sell Conditions:

-Buy Condition: When the Kalman-smoothed EMA 1 crosses above the Kalman-smoothed EMA 2, a bullish crossover is confirmed.

-Sell Condition: When EMA 1 crosses below EMA 2, a bearish crossover is confirmed.

Users may enhance the robustness of these signals by adjusting process noise, measurement noise, or EMA lengths. Lower measurement noise values make the filter react faster (but potentially noisier), while higher values make it smoother (but slower).

Features and Parameters:

-Source: Selectable price input (Close, Open, High, Low, etc.).

-EMA 1 Length: Defines the fast EMA period.

-EMA 2 Length: Defines the slow EMA period.

-Process Noise: Controls how much randomness the Kalman filter assumes in price dynamics.

-Measurement Noise: Controls how much uncertainty is assumed in raw input data.

-Kalman Usage: Option to apply Kalman filtering either before EMA calculation (on price) or after (on EMA values).

Specifications:

Kalman Filter

The Kalman filter is an optimal recursive algorithm that estimates the state of a system from noisy measurements. In trading, it is used to smooth prices or indicator values. By balancing process noise (expected volatility) with measurement noise (data uncertainty), it generates a smoothed signal that reacts adaptively to market conditions.

Exponential Moving Average (EMA)

An EMA is a weighted moving average that emphasizes recent data more heavily than older data. This makes it more responsive than a simple moving average (SMA). EMAs are widely used to identify trends and momentum shifts.

EMA Crossovers

The crossing of a fast EMA above a slow EMA suggests bullish momentum, while the opposite suggests bearish momentum. This is a cornerstone technique in trend-following systems.

Dual Kalman Filtering

Applying Kalman both to raw price and to the EMAs themselves reduces whipsaws further. It creates crossover signals that are not only smoothed but also validated across two levels of noise reduction. This significantly enhances signal reliability compared to traditional EMA crossovers.

Process Noise

Represents the filter’s assumption about how much the underlying market can randomly change between steps. Higher values make the filter adapt faster to sudden changes, while lower values make it more stable.

Measurement Noise

Represents uncertainty in price data. A higher measurement noise value means the filter trusts the model more than the observed data, leading to smoother results. A lower value makes the filter more reactive to observed price fluctuations.

Trend Coloring & Fill

The use of dynamic colors and filled regions provides immediate visual recognition of trend states, helping traders act faster and with greater clarity.

Enjoy!

Super-AO with Risk Management Alerts Template - 11-29-25Super-AO with Risk Management: ALERTS & AUTOMATION Edition

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

This is the Indicator / Alerts companion to the Super-AO Strategy.

While the Strategy version is built for backtesting (verifying profitability and checking historical performance), this Indicator version is built for Live Execution.

We understand the frustration of finding a great strategy, only to realize you can't easily hook it up to your trading bot. This script solves that. It contains the exact same "Super-AO" logic and "Risk Management Engine" as the strategy version, but it is optimized to send signals to automation platforms like Signal Lynx, 3Commas, or any Webhook listener.

2. Quick Action Guide (TL;DR)

Purpose: Live Signal Generation & Automation.

Workflow:

Use the Strategy Version to find profitable settings.

Copy those settings into this Indicator Version.

Set a TradingView Alert using the "Any Alert() function call" condition.

Best Timeframe: 4 Hours (H4) and above.

Compatibility: Works with any webhook-based automation service.

3. Why Two Scripts?

Pine Script operates in two distinct modes:

Strategy Mode: Calculates equity, drawdowns, and simulates orders. Great for research, but sometimes complex to automate.

Indicator Mode: Plots visual data on the chart. This is the preferred method for setting up robust alerts because it is lighter weight and plots specific values that automation services can read easily.

The Golden Rule: Always backtest on the Strategy, but trade on the Indicator. This ensures that what you see in your history matches what you execute in real-time.

4. How to Automate This Script

This script uses a "Visual Spike" method to trigger alerts. Instead of drawing equity curves, it plots numerical values at the bottom of your chart when a trade event occurs.

The Signal Map:

Blue Spike (2 / -2): Entry Signal (Long / Short).

Yellow Spike (1 / -1): Risk Management Close (Stop Loss / Trend Reversal).

Green Spikes (1, 2, 3): Take Profit Levels 1, 2, and 3.

Setup Instructions:

Add this indicator to your chart.

Open your TradingView "Alerts" tab.

Create a new Alert.

Condition: Select SAO - RM Alerts Template.

Trigger: Select Any Alert() function call.

Message: Paste your JSON webhook message (provided by your bot service).

5. The Logic Under the Hood

Just like the Strategy version, this indicator utilizes:

SuperTrend + Awesome Oscillator: High-probability swing trading logic.

Non-Repainting Engine: Calculates signals based on confirmed candle closes to ensure the alert you get matches the chart reality.

Advanced Adaptive Trailing Stop (AATS): Internally calculates volatility to determine when to send a "Close" signal.

6. About Signal Lynx

Automation for the Night-Shift Nation 🌙

We are providing this code open source to help traders bridge the gap between manual backtesting and live automation. This code has been in action since 2022.

If you are looking to automate your strategies, please take a look at Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source). If you make beneficial modifications, please release them back to the community!

Trend BG v2Trend BG v2 colors the chart background based on Directional Movement (DM) and DI strength. It provides an easy visual way to identify trending and non-trending conditions on any timeframe.

How It Works

The script calculates:

Upward Directional Movement (DM+)

Downward Directional Movement (DM–)

True Range smoothed with RMA (14-period)

Positive DI and Negative DI values from classic ADX logic

The trend state is determined by comparing +DI vs –DI:

+DI > –DI → Uptrend

–DI > +DI → Downtrend

Otherwise → Neutral / Sideways

The script then applies a background color based on the detected trend.

Color transparency and theme can be adjusted using the input options.

Why This Script Is Useful

Instead of plotting DI lines or ADX curves, this version presents the trend directly on the background, making it ideal for:

Quick trend recognition

Visual filtering of choppy vs trending markets

Enhancing manual or automated setups

Intraday scalping, positional trend following, and multi-timeframe analysis

The background display is subtle, customizable, and does not interfere with other indicators on the chart.

Key Features

Trend-colored chart background (Up / Down / Neutral)

Adjustable color palette and transparency

Built using classic Directional Movement logic

Works on all markets and all timeframes

Lightweight and efficient (no repainting)

How to Use It

Apply the indicator on your chart and use the background colors to:

Align trades with the market trend

Avoid trading during neutral or low-momentum periods

Confirm trend direction before entries

Improve clarity when using your existing indicators

This indicator does not generate buy/sell signals by itself; instead, it helps visualize the underlying trend environment so traders can make more informed decisions.

Atlas 8 Currency Session Momentum (6H, London)This indicator calculates real-time currency strength for the 8 major currencies (USD, EUR, GBP, JPY, AUD, NZD, CAD, CHF) using a balanced multi-pair engine and a 6-hour momentum reset.

🔍 How it works

The indicator computes the relative strength of each currency by averaging the percentage change of 7 major cross-pairs for each currency.

A currency's value increases when pairs where it is the base appreciate, and decreases when pairs where it is the quote depreciate.

This creates a symmetric and stable strength calculation similar to institutional relative-value models.

🕒 Session-based Momentum Reset

The global trading day is split into 4 × 6-hour blocks:

• 00:00–06:00 Tokyo

• 06:00–12:00 London

• 12:00–18:00 New York

• 18:00–24:00 Late US/Asia pre-open

At each new 6-hour session, all strength lines reset to 0.

This highlights fresh intraday momentum generated by liquidity transitions between sessions.

🎯 What the indicator shows

• Relative strength of all 8 currencies

• Smooth momentum curves using EMA smoothing

• Vertical dividers at each new session

• Background color for each session

• Real intraday build-up of strength/weakness (not cumulative from previous day)

This tool is designed for intraday traders who follow cross-currency momentum during session transitions (Tokyo → London → NY).

🧭 How to use it

• Look for the strongest vs weakest currency after each session reset

• Identify fresh trends during London and NY opens

• Confirm currency-pair bias using strength divergence

• Track momentum exhaustion when lines flatten or converge

Liquidity LayoutLiquidity Layout

The Liquidity Layout is a comprehensive macroeconomic indicator that tracks global liquidity conditions by aggregating multiple financial data streams from major economies (US, EU, China, Japan, UK, Canada, Switzerland). It provides traders with a macro view of market liquidity to help identify favorable conditions for risk assets

⚠️ Important: Timeframe Settings

This indicator is designed for the 1W (weekly) timeframe. If you use other timeframes, you must adjust the offset parameter in the settings to properly align the data with price action. The default offset of 12 is calibrated for weekly charts.

What It Measures

This indicator combines seven key components of global liquidity:

1. Global M2 Money Supply - Tracks broad money supply (M2) plus 10% of narrow money supply (M1) across major economies, weighted by currency strength. This represents the total amount of money circulating in the private sector.

2. Central Bank Balance Sheets (CBBS) - Monitors the combined balance sheets of major central banks (Fed, ECB, BoJ, PBoC, etc.), reflecting quantitative easing and monetary expansion policies.

3. Foreign Exchange Reserves (FER) - Aggregates forex reserves held by central banks, indicating international liquidity buffers and capital flows.

4. Current Account + Capital Flows (CA) - Combines current account balances with capital flows to measure cross-border money movement and trade liquidity.

5. Government Spending (GSP) - Tracks government expenditure minus a portion of federal expenses, representing fiscal stimulus and public sector liquidity injection.

6. World Currency Unit (WCU) - A custom forex composite that weights major and emerging market currencies to capture global currency strength dynamics.

7. Bond Market Conditions - Analyzes yield curves, spreads, and bond indices to assess credit conditions and risk appetite in fixed income markets.

The Formula

The indicator uses two main calculation modes:

ADJ Global Liquidity (Default):

×

This multiplies liquidity components by currency and bond market factors to capture the interactive effects between monetary conditions and market sentiment.

TPI (Trend Power Index) Mode:

A normalized version that combines all components with optimized weights:

Global Liquidity Index: 10%

Bonds: 17.5%

Bond Yields: 25%

Currency Strength: 25%

Government Spending: 5%

Current Account: 5%

M2: 2.5%

Central Bank Balance Sheets: 2.5%

Forex Reserves: 5%

Oil (macro risk indicator): 2.5%

How to Use It

Visualization Modes:

Background Mode (default): Orange background appears when TPI is positive (favorable liquidity conditions)

Line Mode: Displays the indicator as an orange line with customizable offset

Interpreting the Signal:

Positive/Rising = Expanding liquidity, generally bullish for risk assets

Negative/Falling = Contracting liquidity, risk-off environment

TPI > 1 = Extremely favorable conditions (upper threshold)

TPI < -1 = Severe liquidity stress (lower threshold)

Best Practices:

Use on higher timeframes (daily, weekly) for macro trend analysis

Combine with price action - liquidity often leads market moves by weeks or months

Watch for divergences between liquidity and asset prices

Particularly relevant for Bitcoin, equities, and risk assets

Data Sources

The indicator pulls real-time economic data from TradingView's ECONOMICS database and major market indices, including central bank statistics, government reports, and forex rates across G7 and major emerging markets.

Settings

Data Plot: Choose which liquidity component to display

Plot Type: Switch between raw Index values or normalized TPI

Offset: Shift the plot forward/backward for alignment (default: 12 for weekly charts)

Style: Background shading or line plot

Notes

This is a macro-level indicator best suited for understanding the broader liquidity environment rather than short-term trading signals. It helps answer the question: "Is the global financial system expanding or contracting liquidity?"

Filte Ichimoku1. Indicator Name

Filte Ichimoku

2. One-line Introduction

A smoothed and visually enhanced version of the Ichimoku Cloud that highlights trend direction and strength using adaptive color transparency.

3. General Overview

Filte Ichimoku is a modernized take on the classic Ichimoku Kinko Hyo indicator, designed for traders who value clarity and minimalism while retaining core Ichimoku functionality.

It calculates traditional components like Tenkan-sen, Kijun-sen, and the Senkou Span A/B, but focuses primarily on visualizing the Kumo (cloud) with enhanced styling.

Instead of raw plots, Filte Ichimoku applies triple-step smoothing to both Senkou spans, creating a soft, wave-like appearance that reflects trend fluidity.

The color of the cloud dynamically adapts based on whether Span A is above or below Span B (bullish/bearish), and its opacity changes according to the intensity of the trend, which is calculated relative to ATR-based volatility.

By forward-shifting the plots and visually blending the cloud, the indicator helps traders quickly identify dominant trends, potential reversals, and consolidation zones.

Its clean design makes it highly compatible with both traditional Ichimoku strategies and modern price action systems.

4. Key Advantages

🌥 Adaptive Ichimoku Cloud

Cloud color and transparency dynamically change based on real trend strength and direction.

📊 Smoother, Cleaner Display

Triple-smoothing on Senkou A and B creates a less noisy, more readable visual output.

📈 Forward Shift Preserved

Maintains the traditional Ichimoku forward-shift logic, helping project future price zones.

🎨 Customizable Trend Colors

Define your own bullish and bearish cloud colors for easy visual alignment with your strategy.

🚫 Noise Reduction via ATR Normalization

Trend intensity is calculated relative to ATR, reducing false positives in low-volatility zones.

🔒 Lightweight & Secure Design

Optimized script avoids exposure of sensitive logic while remaining fast and reliable in live charts.

📘 Indicator User Guide

📌 Basic Concept

Filte Ichimoku emphasizes cloud dynamics (Kumo) to interpret market structure.

Trend direction is derived from the relationship between Senkou Span A and B, while trend strength is measured by their distance relative to ATR.

The smoother curves make it easier to read while preserving all Ichimoku logic.

⚙️ Settings Explained

Tenkan Sen Length: Fast-moving average calculation period (default: 18)

Kijun Sen Length: Medium trend baseline (default: 52)

Senkou Span Length: Long-term cloud boundary (default: 104)

Bull/Bear Color: Set custom colors for bullish or bearish cloud states

📈 Bullish Timing Example

Senkou Span A > Span B, and the cloud appears green with high opacity

Indicates strong uptrend support, especially when price is above both Tenkan and Kijun

📉 Bearish Timing Example

Span B > Span A, cloud turns red and darkens

Suggests bearish dominance; avoid long entries or prepare for short-side setups

🧪 Recommended Use Cases

Use as a trend background layer for existing Ichimoku or price action systems

Combine with breakouts, support/resistance, and momentum indicators

Great for trend filtering in mid- to long-term strategies

🔒 Precautions

Designed for clarity and filtering—not a standalone entry system

In sideways markets, cloud may compress and color changes may become less meaningful

Adjust smoothing lengths cautiously to avoid lagging during volatile swings

Best results come from combining with price structure analysis

Swing Point PnL PressureThis indicator visualizes the cumulative profit potential of bulls and bears based on recent swing highs and lows — offering a unique lens into trend maturity, sentiment imbalance, and exhaustion risk.

🟢 Bull PnL rises as price moves above prior swing lows — reflecting unrealized gains for long positions

🔴 Bear PnL rises as price drops below prior swing highs — capturing short-side profitability

Over time, these curves diverge during strong trends, revealing which side is in control. But when they converge, it often signals that the dominant side is losing steam — a potential turning point where profit-taking, traps, or reversals may emerge.

This tool doesn’t predict tops or bottoms — it tracks the emotional and financial pressure building on each side of the market. Use it to:

Spot trend exhaustion before price confirms it

Identify profit parity zones where sentiment may flip

Time accumulation or distribution phases with greater confidence

Whether you’re swing trading or analyzing macro structure, this indicator helps you see what price alone can’t: who’s winning, who’s trapped, and who’s about to give up.

Bull/Bear FVG Density RatioThis indicator tracks the directional frequency of Fair Value Gaps (FVGs) over a configurable lookback window, offering a clean, responsive measure of market imbalance.

🔍 What It Does:

Detects bullish and bearish FVGs using a 3-bar displacement logic

Calculates the ratio of FVGs to candles over the last N bars

Plots separate density curves for bullish and bearish FVGs

Includes a threshold line to help identify regime shifts (e.g., drought vs spate)

📈 How to Use:

Use rising density to confirm trend strength or breakout momentum

Watch for crossovers above the threshold to signal active imbalance regimes

Combine with price action or volume overlays for high-confluence setups

⚙️ Inputs:

Lookback Window: Number of candles used to calculate FVG density

Threshold: Visual guide for regime classification (default: 0.2)

This tool is ideal for traders who want to move beyond symptomatic signals and model structural causality. It pairs well with lifecycle scoring, retest velocity, and HTF overlays.

Quantum Fluxtrend [CHE] Quantum Fluxtrend — A dynamic Supertrend variant with integrated breakout event tracking and VWAP-guided risk management for clearer trend decisions.

Summary

The Quantum Fluxtrend builds on traditional Supertrend logic by incorporating a midline derived from smoothed high and low values, creating adaptive bands that respond to market range expansion or contraction. This results in fewer erratic signals during volatile periods and smoother tracking in steady trends, while an overlaid event system highlights breakout confirmations, potential traps, or continuations with visual lines, labels, and percentage deltas from the close. Users benefit from real-time VWAP calculations anchored to events, providing dynamic stop-loss suggestions to help manage exits without manual adjustments. Overall, it layers signal robustness with actionable annotations, reducing noise in fast-moving charts.

Motivation: Why this design?

Standard Supertrend indicators often generate excessive flips in choppy conditions or lag behind in low-volatility drifts, leading to whipsaws that erode confidence in trend direction. This design addresses that by centering bands around a midline that reflects recent price spreads, ensuring adjustments are proportional to observed variability. The added event layer captures regime shifts explicitly, turning abstract crossovers into labeled milestones with trailing VWAP for context, which helps traders distinguish genuine momentum from fleeting noise without over-relying on raw price action.

What’s different vs. standard approaches?

- Baseline reference: Diverges from the classic Supertrend, which uses average true range for fixed offsets from a median price.

- Architecture differences:

- Bands form around a central line averaged from smoothed highs and lows, with offsets scaled by half the range between those smooths.

- Regime direction persists until a clear breach of the prior opposite band, preventing premature reversals.

- Event visualization draws persistent lines from flip points, updating labels based on price sustainment relative to the trigger level.

- VWAP resets at each event, accumulating volume-weighted prices forward for a trailing reference.

- Practical effect: Charts show fewer direction changes overall, with color-coded annotations that evolve from initial breakout to continuation or trap status, making it easier to spot sustained moves early. VWAP lines provide a volume-informed anchor that curves with price, offering visual cues for adverse drifts.

How it works (technical)

The process starts by smoothing high and low prices over a user-defined period to form upper and lower references. A midline sits midway between them, and half the spread acts as a base for band offsets, adjusted by a multiplier to widen or narrow sensitivity. On each bar, the close is checked against the previous bar's opposite band: crossing above expands the lower band downward in uptrends, or below contracts the upper band upward in downtrends, creating a ratcheting effect that locks in direction until breached.

Persistent state tracks the current regime, seeding initial bands from the smoothed values if no prior data exists. Flips trigger new horizontal lines at the breach level, styled by direction, alongside labels that monitor sustainment—price holding above for up-flips or below for down-flips keeps the regime, while reversal flags a trap.

Separately, at each flip, a dashed VWAP line initializes at the breach price and extends forward, accumulating the product of typical prices and volumes divided by total volume. This yields a curving reference that updates bar-by-bar. Warnings activate if price strays adversely from this VWAP, tinting the background for quick alerts.

No higher timeframe data is pulled, so all computations run on the chart's native resolution, avoiding lookahead biases unless repainting is enabled via input.

Parameter Guide

SMA Length — Controls smoothing of highs and lows for midline and range base; longer values dampen noise but increase lag. Default: 20. Trade-offs: Shortens responsiveness in trends (e.g., 10–14) but risks more flips; extend to 30+ for stability in ranging markets.

Multiplier — Scales band offsets from the half-range; higher amplifies to capture bigger swings. Default: 1.0. Trade-offs: Above 1.5 widens for volatile assets, reducing false signals; below 0.8 tightens for precision but may miss subtle shifts.

Show Bands — Toggles visibility of basic and adjusted band lines for reference. Default: false. Tip: Enable briefly to verify alignment with price action.

Show Background Color — Displays red tint on VWAP adverse crosses for visual warnings. Default: false. Trade-offs: Helps in live monitoring but can clutter clean charts.

Line Width — Sets thickness for event and VWAP lines. Default: 2. Tip: Thicker (3–5) for emphasis on key levels.

+Bars after next event — Extends old lines briefly before cleanup on new flips. Default: 20. Trade-offs: Longer preserves history (40+) at resource cost; shorter keeps charts tidy.

Allow Repainting — Permits live-bar updates for smoother real-time view. Default: false. Tip: Disable for backtest accuracy.

Extension 1 Settings (Show, Width, Size, Decimals, Colors, Alpha) — Manages dotted connector from event label to current close, showing percentage change. Defaults: Shown, width 2, normal size, 2 decimals, lime/red for gains/losses, gray line, 90% transparent background. Trade-offs: Fewer decimals for clean display; adjust alpha for readability.

Extension 2 Settings (Show, Method, Stop %, Ticks, Decimals, Size, Color, Inherit, Alpha) — Positions stop label at VWAP end, offset by percent or ticks. Defaults: Shown, percent method, 1.0%, 20 ticks, 4 decimals, normal size, white text, inherit tint, 0% alpha. Trade-offs: Percent for proportional risk; ticks for fixed distance in tick-based assets.

Alert Toggles — Enables notifications for breakouts, continuations, traps, or VWAP warnings. All default: true. Tip: Layer with chart alerts for multi-condition setups.

Reading & Interpretation

The main Supertrend line colors green for up-regimes (price above lower band) and red for down (below upper band), serving as a dynamic support/resistance trail. Flip shapes (up/down triangles) mark regime changes at band breaches.

Event lines extend horizontally from flips: green for bull, red for bear. Labels start blank and update to "Bull/Bear Cont." if price sustains the direction, or "Trap" if it reverses, with colors shifting lime/red/gray accordingly. A dotted vertical links the trailing label to the current close, mid-labeled with the percentage delta (positive green, negative red).

VWAP dashes yellow (bull) or orange (bear) from the event, curving to reflect volume-weighted average. At its end, a left-aligned label shows suggested stop price, annotated with offset details. Background red hints at weakening if price crosses VWAP opposite the regime.

Deltas near zero suggest consolidation; widening extremes signal momentum buildup or exhaustion.

Practical Workflows & Combinations

- Trend following: Enter long on green flip shapes confirmed by higher highs, using the event line as initial stop below. Trail stops to VWAP for bull runs, exiting on trap labels or red background warnings. Filter with volume spikes to avoid low-conviction breaks.

- Exits/Stops: Conservative: Set hard stops at suggested SL labels. Aggressive: Hold through minor traps if delta stays positive, but cut on regime flip. Pair with momentum oscillators for overbought pullbacks.

- Multi-asset/Multi-TF: Defaults suit forex/stocks on 15m–4H; for crypto, bump multiplier to 1.5 for volatility. Scale SMA length proportionally across timeframes (e.g., double for daily). Combine with structure tools like Fibonacci for confluence on event lines.

Behavior, Constraints & Performance

Live bars update lines and labels dynamically if repainting is allowed, but signals confirm on close for stability—flips only trigger post-bar. No higher timeframe calls, so no inherent lookahead, though volume weighting assumes continuous data.

Resources cap at 1000 bars back, 50 lines/labels max; events prune old ones on new flips to stay under budget, with brief extensions for visibility. Arrays or loops absent, keeping it lightweight.

Known limits include lag in extreme gaps (e.g., overnight opens) where bands may not adjust instantly, and VWAP sensitivity to sparse volume in illiquid sessions.

Sensible Defaults & Quick Tuning

Start with SMA 20, multiplier 1.0 for balanced response across majors. For choppy pairs: Lengthen SMA to 30, multiplier 0.8 to tighten bands and cut flips. For trending equities: Shorten to 14, multiplier 1.2 for quicker entries. If traps dominate, enable bands to inspect range compression; for sluggish signals, reduce extension bars to focus on recent events.

What this indicator is—and isn’t

This serves as a visualization and signal layer for trend regimes and breakouts, highlighting sustainment via annotations and risk cues through VWAP—ideal atop price action for confirmation. It is not a standalone system, predictive oracle, or risk calculator; always integrate with broader analysis, position sizing, and stops. Use responsibly as an educational tool.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

CVD Pro – Smart Overlay + Signals (with Persist Mode)What this Indicator Does

CVD Pro visualizes Cumulative Volume Delta (CVD) data directly on your main price chart — helping you detect real buying vs. selling pressure in real time.

Unlike most CVD scripts that run in a separate subwindow, this one overlays price-mapped CVD curves on the candles themselves for better confluence with market structure and FVG zones.

The script dynamically scales normalized CVD values to the price range and uses adaptive smoothing and deviation bands to highlight shifts in trader behavior.

It also includes automatic bullish/bearish crossover signals, displayed as on-chart labels.

⚙️ Main Features

✅ Price-mapped CVD Overlay

CVD is normalized (Z-score) and projected onto the price chart for easy visual correlation with price structure.

✅ Multi-Timeframe Presets

Three sensitivity presets optimized for different chart environments:

Strict (4H) → Best for macro trends and high-timeframe structure.

Balanced (1H / 30m) → Great for active swing setups.

Sensitive (15m) → Captures short-term intraday reversals.

✅ Dynamic Bands & Smoothing

Deviation bands visualize statistical extremes in delta pressure — helping to identify exhaustion and divergence points.

✅ Smart Buy/Sell Signal Logic

Automatic label triggers when the CVD Overlay crosses its smoothed baseline:

🟢 BULL LONG → Rising CVD above the mean (buyers in control).

🔴 BEAR SHORT → Falling CVD below the mean (sellers in control).

✅ Persist Mode

Toggle to keep the last signal visible until a new one forms — ideal for traders who prefer clean chart annotations without noise.

✅ Clean, Minimal Overlay

Everything happens directly on your chart — no extra windows, no clutter. Designed for use with Smart Money Concepts, Fair Value Gaps (FVGs), or volume imbalance setups.

🧩 Use Case

CVD Pro is designed for traders who:

Use Smart Money Concepts (SMC) or ICT-style trading

Watch for FVG reactions, breaker blocks, and liquidity sweeps

Need to confirm order flow direction or momentum strength

Trade intraday or swing setups with precision entries and clear bias confirmation

⚡ Recommended Settings

4H / 1H: Use Strict mode for major structure and confirmation.

1H / 30m: Balanced mode for clear mid-term trend alignment.

15m: Sensitive mode to catch scalps and lower-TF shifts.

🧠 Pro Tips

Combine with RSI or Market Structure Breaks (MSS) for additional confluence.

A strong CVD divergence near a key FVG or 0.5–0.705 Fibonacci zone often signals reversal.

Persistent CVD crossover + price structure break = high-probability entry.

🧩 Credits

Created by Patrick S. ("Nova Labs")

Concept inspired by professional order-flow analytics and adaptive Z-Score normalization.

Would you like me to write a shorter “public summary” paragraph (for the short description at the top of TradingView, the one-liner users see before expanding)?

It’s usually a 2–3 sentence hook like:

“Overlay-based CVD indicator that merges volume delta with price structure. Detect true buying/selling pressure using adaptive normalization, deviation bands, and clean bullish/bearish crossover signals.”

ATR Horizontal Lines from EMA and SMA with TableHow it works:

The script calculates ATR levels (of your choosing)

Instead of plotting curves, it creates horizontal lines

The lines are deleted and recreated on each bar to show current levels

Lines extend to the right or can be limited to a certain width

Customization options:

Line width (1-10 pixels)

Individual colors for each of the 4 lines

All the original parameters (EMA/SMA lengths, ATR length, multipliers)

The horizontal lines will now show the current ATR-based support/resistance levels and move dynamically as the EMAs, SMA, and ATR values change with new price data.

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.