Signal Generator: HTF EMA Momentum + MACDSignal Generator: HTF EMA Momentum + MACD

What this script does

This indicator combines a higher-timeframe EMA trend filter with a MACD crossover on the chart’s timeframe. The goal is to make MACD signals more selective by checking whether they occur in the same direction as the broader trend.

How it works

- On the higher timeframe, two EMAs are calculated (short and long). Their difference is used as a simple momentum measure.

- On the chart timeframe, the MACD is calculated. Crossovers are then filtered with two conditions:

1.They must align with the higher-timeframe EMA trend.

2.They must occur beyond a small “zero band” threshold, with a minimum distance between MACD and signal lines.

- When both conditions are met, the script can plot BUY or SELL labels. ATR is used only to shift labels up or down for visibility.

Visuals and alerts

- Histogram bars show whether higher-timeframe EMA momentum is rising or falling.

- MACD main and signal lines are plotted with optional scaling.

- Dotted lines show the zero band region.

- Optional large BUY/SELL labels appear when conditions are confirmed on the previous bar.

- Alerts can be enabled for these signals; they trigger once per bar close.

Notes and limitations

- Higher-timeframe values are only confirmed once the higher-timeframe candle has closed.

- Scaling factors affect appearance only, not the logic.

- This is an open-source study intended as a learning and charting tool. It does not provide financial advice or guarantee performance.

Pesquisar nos scripts por "crossover债券是什么"

Tzotchev Trend Measure [EdgeTools]Are you still measuring trend strength with moving averages? Here is a better variant at scientific level:

Tzotchev Trend Measure: A Statistical Approach to Trend Following

The Tzotchev Trend Measure represents a sophisticated advancement in quantitative trend analysis, moving beyond traditional moving average-based indicators toward a statistically rigorous framework for measuring trend strength. This indicator implements the methodology developed by Tzotchev et al. (2015) in their seminal J.P. Morgan research paper "Designing robust trend-following system: Behind the scenes of trend-following," which introduced a probabilistic approach to trend measurement that has since become a cornerstone of institutional trading strategies.

Mathematical Foundation and Statistical Theory

The core innovation of the Tzotchev Trend Measure lies in its transformation of price momentum into a probability-based metric through the application of statistical hypothesis testing principles. The indicator employs the fundamental formula ST = 2 × Φ(√T × r̄T / σ̂T) - 1, where ST represents the trend strength score bounded between -1 and +1, Φ(x) denotes the normal cumulative distribution function, T represents the lookback period in trading days, r̄T is the average logarithmic return over the specified period, and σ̂T represents the estimated daily return volatility.

This formulation transforms what is essentially a t-statistic into a probabilistic trend measure, testing the null hypothesis that the mean return equals zero against the alternative hypothesis of non-zero mean return. The use of logarithmic returns rather than simple returns provides several statistical advantages, including symmetry properties where log(P₁/P₀) = -log(P₀/P₁), additivity characteristics that allow for proper compounding analysis, and improved validity of normal distribution assumptions that underpin the statistical framework.

The implementation utilizes the Abramowitz and Stegun (1964) approximation for the normal cumulative distribution function, achieving accuracy within ±1.5 × 10⁻⁷ for all input values. This approximation employs Horner's method for polynomial evaluation to ensure numerical stability, particularly important when processing large datasets or extreme market conditions.

Comparative Analysis with Traditional Trend Measurement Methods

The Tzotchev Trend Measure demonstrates significant theoretical and empirical advantages over conventional trend analysis techniques. Traditional moving average-based systems, including simple moving averages (SMA), exponential moving averages (EMA), and their derivatives such as MACD, suffer from several fundamental limitations that the Tzotchev methodology addresses systematically.

Moving average systems exhibit inherent lag bias, as documented by Kaufman (2013) in "Trading Systems and Methods," where he demonstrates that moving averages inevitably lag price movements by approximately half their period length. This lag creates delayed signal generation that reduces profitability in trending markets and increases false signal frequency during consolidation periods. In contrast, the Tzotchev measure eliminates lag bias by directly analyzing the statistical properties of return distributions rather than smoothing price levels.

The volatility normalization inherent in the Tzotchev formula addresses a critical weakness in traditional momentum indicators. As shown by Bollinger (2001) in "Bollinger on Bollinger Bands," momentum oscillators like RSI and Stochastic fail to account for changing volatility regimes, leading to inconsistent signal interpretation across different market conditions. The Tzotchev measure's incorporation of return volatility in the denominator ensures that trend strength assessments remain consistent regardless of the underlying volatility environment.

Empirical studies by Hurst, Ooi, and Pedersen (2013) in "Demystifying Managed Futures" demonstrate that traditional trend-following indicators suffer from significant drawdowns during whipsaw markets, with Sharpe ratios frequently below 0.5 during challenging periods. The authors attribute these poor performance characteristics to the binary nature of most trend signals and their inability to quantify signal confidence. The Tzotchev measure addresses this limitation by providing continuous probability-based outputs that allow for more sophisticated risk management and position sizing strategies.

The statistical foundation of the Tzotchev approach provides superior robustness compared to technical indicators that lack theoretical grounding. Fama and French (1988) in "Permanent and Temporary Components of Stock Prices" established that price movements contain both permanent and temporary components, with traditional moving averages unable to distinguish between these elements effectively. The Tzotchev methodology's hypothesis testing framework specifically tests for the presence of permanent trend components while filtering out temporary noise, providing a more theoretically sound approach to trend identification.

Research by Moskowitz, Ooi, and Pedersen (2012) in "Time Series Momentum in the Cross Section of Asset Returns" found that traditional momentum indicators exhibit significant variation in effectiveness across asset classes and time periods. Their study of multiple asset classes over decades revealed that simple price-based momentum measures often fail to capture persistent trends in fixed income and commodity markets. The Tzotchev measure's normalization by volatility and its probabilistic interpretation provide consistent performance across diverse asset classes, as demonstrated in the original J.P. Morgan research.

Comparative performance studies conducted by AQR Capital Management (Asness, Moskowitz, and Pedersen, 2013) in "Value and Momentum Everywhere" show that volatility-adjusted momentum measures significantly outperform traditional price momentum across international equity, bond, commodity, and currency markets. The study documents Sharpe ratio improvements of 0.2 to 0.4 when incorporating volatility normalization, consistent with the theoretical advantages of the Tzotchev approach.

The regime detection capabilities of the Tzotchev measure provide additional advantages over binary trend classification systems. Research by Ang and Bekaert (2002) in "Regime Switches in Interest Rates" demonstrates that financial markets exhibit distinct regime characteristics that traditional indicators fail to capture adequately. The Tzotchev measure's five-tier classification system (Strong Bull, Weak Bull, Neutral, Weak Bear, Strong Bear) provides more nuanced market state identification than simple trend/no-trend binary systems.

Statistical testing by Jegadeesh and Titman (2001) in "Profitability of Momentum Strategies" revealed that traditional momentum indicators suffer from significant parameter instability, with optimal lookback periods varying substantially across market conditions and asset classes. The Tzotchev measure's statistical framework provides more stable parameter selection through its grounding in hypothesis testing theory, reducing the need for frequent parameter optimization that can lead to overfitting.

Advanced Noise Filtering and Market Regime Detection

A significant enhancement over the original Tzotchev methodology is the incorporation of a multi-factor noise filtering system designed to reduce false signals during sideways market conditions. The filtering mechanism employs four distinct approaches: adaptive thresholding based on current market regime strength, volatility-based filtering utilizing ATR percentile analysis, trend strength confirmation through momentum alignment, and a comprehensive multi-factor approach that combines all methodologies.

The adaptive filtering system analyzes market microstructure through price change relative to average true range, calculates volatility percentiles over rolling windows, and assesses trend alignment across multiple timeframes using exponential moving averages of varying periods. This approach addresses one of the primary limitations identified in traditional trend-following systems, namely their tendency to generate excessive false signals during periods of low volatility or sideways price action.

The regime detection component classifies market conditions into five distinct categories: Strong Bull (ST > 0.3), Weak Bull (0.1 < ST ≤ 0.3), Neutral (-0.1 ≤ ST ≤ 0.1), Weak Bear (-0.3 ≤ ST < -0.1), and Strong Bear (ST < -0.3). This classification system provides traders with clear, quantitative definitions of market regimes that can inform position sizing, risk management, and strategy selection decisions.

Professional Implementation and Trading Applications

The indicator incorporates three distinct trading profiles designed to accommodate different investment approaches and risk tolerances. The Conservative profile employs longer lookback periods (63 days), higher signal thresholds (0.2), and reduced filter sensitivity (0.5) to minimize false signals and focus on major trend changes. The Balanced profile utilizes standard academic parameters with moderate settings across all dimensions. The Aggressive profile implements shorter lookback periods (14 days), lower signal thresholds (-0.1), and increased filter sensitivity (1.5) to capture shorter-term trend movements.

Signal generation occurs through threshold crossover analysis, where long signals are generated when the trend measure crosses above the specified threshold and short signals when it crosses below. The implementation includes sophisticated signal confirmation mechanisms that consider trend alignment across multiple timeframes and momentum strength percentiles to reduce the likelihood of false breakouts.

The alert system provides real-time notifications for trend threshold crossovers, strong regime changes, and signal generation events, with configurable frequency controls to prevent notification spam. Alert messages are standardized to ensure consistency across different market conditions and timeframes.

Performance Optimization and Computational Efficiency

The implementation incorporates several performance optimization features designed to handle large datasets efficiently. The maximum bars back parameter allows users to control historical calculation depth, with default settings optimized for most trading applications while providing flexibility for extended historical analysis. The system includes automatic performance monitoring that generates warnings when computational limits are approached.

Error handling mechanisms protect against division by zero conditions, infinite values, and other numerical instabilities that can occur during extreme market conditions. The finite value checking system ensures data integrity throughout the calculation process, with fallback mechanisms that maintain indicator functionality even when encountering corrupted or missing price data.

Timeframe validation provides warnings when the indicator is applied to unsuitable timeframes, as the Tzotchev methodology was specifically designed for daily and higher timeframe analysis. This validation helps prevent misapplication of the indicator in contexts where its statistical assumptions may not hold.

Visual Design and User Interface

The indicator features eight professional color schemes designed for different trading environments and user preferences. The EdgeTools theme provides an institutional blue and steel color palette suitable for professional trading environments. The Gold theme offers warm colors optimized for commodities trading. The Behavioral theme incorporates psychology-based color contrasts that align with behavioral finance principles. The Quant theme provides neutral colors suitable for analytical applications.

Additional specialized themes include Ocean, Fire, Matrix, and Arctic variations, each optimized for specific visual preferences and trading contexts. All color schemes include automatic dark and light mode optimization to ensure optimal readability across different chart backgrounds and trading platforms.

The information table provides real-time display of key metrics including current trend measure value, market regime classification, signal strength, Z-score, average returns, volatility measures, filter threshold levels, and filter effectiveness percentages. This comprehensive dashboard allows traders to monitor all relevant indicator components simultaneously.

Theoretical Implications and Research Context

The Tzotchev Trend Measure addresses several theoretical limitations inherent in traditional technical analysis approaches. Unlike moving average-based systems that rely on price level comparisons, this methodology grounds trend analysis in statistical hypothesis testing, providing a more robust theoretical foundation for trading decisions.

The probabilistic interpretation of trend strength offers significant advantages over binary trend classification systems. Rather than simply indicating whether a trend exists, the measure quantifies the statistical confidence level associated with the trend assessment, allowing for more nuanced risk management and position sizing decisions.

The incorporation of volatility normalization addresses the well-documented problem of volatility clustering in financial time series, ensuring that trend strength assessments remain consistent across different market volatility regimes. This normalization is particularly important for portfolio management applications where consistent risk metrics across different assets and time periods are essential.

Practical Applications and Trading Strategy Integration

The Tzotchev Trend Measure can be effectively integrated into various trading strategies and portfolio management frameworks. For trend-following strategies, the indicator provides clear entry and exit signals with quantified confidence levels. For mean reversion strategies, extreme readings can signal potential turning points. For portfolio allocation, the regime classification system can inform dynamic asset allocation decisions.

The indicator's statistical foundation makes it particularly suitable for quantitative trading strategies where systematic, rules-based approaches are preferred over discretionary decision-making. The standardized output range facilitates easy integration with position sizing algorithms and risk management systems.

Risk management applications benefit from the indicator's ability to quantify trend strength and provide early warning signals of potential trend changes. The multi-timeframe analysis capability allows for the construction of robust risk management frameworks that consider both short-term tactical and long-term strategic market conditions.

Implementation Guide and Parameter Configuration

The practical application of the Tzotchev Trend Measure requires careful parameter configuration to optimize performance for specific trading objectives and market conditions. This section provides comprehensive guidance for parameter selection and indicator customization.

Core Calculation Parameters

The Lookback Period parameter controls the statistical window used for trend calculation and represents the most critical setting for the indicator. Default values range from 14 to 63 trading days, with shorter periods (14-21 days) providing more sensitive trend detection suitable for short-term trading strategies, while longer periods (42-63 days) offer more stable trend identification appropriate for position trading and long-term investment strategies. The parameter directly influences the statistical significance of trend measurements, with longer periods requiring stronger underlying trends to generate significant signals but providing greater reliability in trend identification.

The Price Source parameter determines which price series is used for return calculations. The default close price provides standard trend analysis, while alternative selections such as high-low midpoint ((high + low) / 2) can reduce noise in volatile markets, and volume-weighted average price (VWAP) offers superior trend identification in institutional trading environments where volume concentration matters significantly.

The Signal Threshold parameter establishes the minimum trend strength required for signal generation, with values ranging from -0.5 to 0.5. Conservative threshold settings (0.2 to 0.3) reduce false signals but may miss early trend opportunities, while aggressive settings (-0.1 to 0.1) provide earlier signal generation at the cost of increased false positive rates. The optimal threshold depends on the trader's risk tolerance and the volatility characteristics of the traded instrument.

Trading Profile Configuration

The Trading Profile system provides pre-configured parameter sets optimized for different trading approaches. The Conservative profile employs a 63-day lookback period with a 0.2 signal threshold and 0.5 noise sensitivity, designed for long-term position traders seeking high-probability trend signals with minimal false positives. The Balanced profile uses a 21-day lookback with 0.05 signal threshold and 1.0 noise sensitivity, suitable for swing traders requiring moderate signal frequency with acceptable noise levels. The Aggressive profile implements a 14-day lookback with -0.1 signal threshold and 1.5 noise sensitivity, optimized for day traders and scalpers requiring frequent signal generation despite higher noise levels.

Advanced Noise Filtering System

The noise filtering mechanism addresses the challenge of false signals during sideways market conditions through four distinct methodologies. The Adaptive filter adjusts thresholds based on current trend strength, increasing sensitivity during strong trending periods while raising thresholds during consolidation phases. The Volatility-based filter utilizes Average True Range (ATR) percentile analysis to suppress signals during abnormally volatile conditions that typically generate false trend indications.

The Trend Strength filter requires alignment between multiple momentum indicators before confirming signals, reducing the probability of false breakouts from consolidation patterns. The Multi-factor approach combines all filtering methodologies using weighted scoring to provide the most robust noise reduction while maintaining signal responsiveness during genuine trend initiations.

The Noise Sensitivity parameter controls the aggressiveness of the filtering system, with lower values (0.5-1.0) providing conservative filtering suitable for volatile instruments, while higher values (1.5-2.0) allow more signals through but may increase false positive rates during choppy market conditions.

Visual Customization and Display Options

The Color Scheme parameter offers eight professional visualization options designed for different analytical preferences and market conditions. The EdgeTools scheme provides high contrast visualization optimized for trend strength differentiation, while the Gold scheme offers warm tones suitable for commodity analysis. The Behavioral scheme uses psychological color associations to enhance decision-making speed, and the Quant scheme provides neutral colors appropriate for quantitative analysis environments.

The Ocean, Fire, Matrix, and Arctic schemes offer additional aesthetic options while maintaining analytical functionality. Each scheme includes optimized colors for both light and dark chart backgrounds, ensuring visibility across different trading platform configurations.

The Show Glow Effects parameter enhances plot visibility through multiple layered lines with progressive transparency, particularly useful when analyzing multiple timeframes simultaneously or when working with dense price data that might obscure trend signals.

Performance Optimization Settings

The Maximum Bars Back parameter controls the historical data depth available for calculations, with values ranging from 5,000 to 50,000 bars. Higher values enable analysis of longer-term trend patterns but may impact indicator loading speed on slower systems or when applied to multiple instruments simultaneously. The optimal setting depends on the intended analysis timeframe and available computational resources.

The Calculate on Every Tick parameter determines whether the indicator updates with every price change or only at bar close. Real-time calculation provides immediate signal updates suitable for scalping and day trading strategies, while bar-close calculation reduces computational overhead and eliminates signal flickering during bar formation, preferred for swing trading and position management applications.

Alert System Configuration

The Alert Frequency parameter controls notification generation, with options for all signals, bar close only, or once per bar. High-frequency trading strategies benefit from all signals mode, while position traders typically prefer bar close alerts to avoid premature position entries based on intrabar fluctuations.

The alert system generates four distinct notification types: Long Signal alerts when the trend measure crosses above the positive signal threshold, Short Signal alerts for negative threshold crossings, Bull Regime alerts when entering strong bullish conditions, and Bear Regime alerts for strong bearish regime identification.

Table Display and Information Management

The information table provides real-time statistical metrics including current trend value, regime classification, signal status, and filter effectiveness measurements. The table position can be customized for optimal screen real estate utilization, and individual metrics can be toggled based on analytical requirements.

The Language parameter supports both English and German display options for international users, while maintaining consistent calculation methodology regardless of display language selection.

Risk Management Integration

Effective risk management integration requires coordination between the trend measure signals and position sizing algorithms. Strong trend readings (above 0.5 or below -0.5) support larger position sizes due to higher probability of trend continuation, while neutral readings (between -0.2 and 0.2) suggest reduced position sizes or range-trading strategies.

The regime classification system provides additional risk management context, with Strong Bull and Strong Bear regimes supporting trend-following strategies, while Neutral regimes indicate potential for mean reversion approaches. The filter effectiveness metric helps traders assess current market conditions and adjust strategy parameters accordingly.

Timeframe Considerations and Multi-Timeframe Analysis

The indicator's effectiveness varies across different timeframes, with higher timeframes (daily, weekly) providing more reliable trend identification but slower signal generation, while lower timeframes (hourly, 15-minute) offer faster signals with increased noise levels. Multi-timeframe analysis combining trend alignment across multiple periods significantly improves signal quality and reduces false positive rates.

For optimal results, traders should consider trend alignment between the primary trading timeframe and at least one higher timeframe before entering positions. Divergences between timeframes often signal potential trend reversals or consolidation periods requiring strategy adjustment.

Conclusion

The Tzotchev Trend Measure represents a significant advancement in technical analysis methodology, combining rigorous statistical foundations with practical trading applications. Its implementation of the J.P. Morgan research methodology provides institutional-quality trend analysis capabilities previously available only to sophisticated quantitative trading firms.

The comprehensive parameter configuration options enable customization for diverse trading styles and market conditions, while the advanced noise filtering and regime detection capabilities provide superior signal quality compared to traditional trend-following indicators. Proper parameter selection and understanding of the indicator's statistical foundation are essential for achieving optimal trading results and effective risk management.

References

Abramowitz, M. and Stegun, I.A. (1964). Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. Washington: National Bureau of Standards.

Ang, A. and Bekaert, G. (2002). Regime Switches in Interest Rates. Journal of Business and Economic Statistics, 20(2), 163-182.

Asness, C.S., Moskowitz, T.J., and Pedersen, L.H. (2013). Value and Momentum Everywhere. Journal of Finance, 68(3), 929-985.

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Fama, E.F. and French, K.R. (1988). Permanent and Temporary Components of Stock Prices. Journal of Political Economy, 96(2), 246-273.

Hurst, B., Ooi, Y.H., and Pedersen, L.H. (2013). Demystifying Managed Futures. Journal of Investment Management, 11(3), 42-58.

Jegadeesh, N. and Titman, S. (2001). Profitability of Momentum Strategies: An Evaluation of Alternative Explanations. Journal of Finance, 56(2), 699-720.

Kaufman, P.J. (2013). Trading Systems and Methods. 5th Edition. Hoboken: John Wiley & Sons.

Moskowitz, T.J., Ooi, Y.H., and Pedersen, L.H. (2012). Time Series Momentum. Journal of Financial Economics, 104(2), 228-250.

Tzotchev, D., Lo, A.W., and Hasanhodzic, J. (2015). Designing robust trend-following system: Behind the scenes of trend-following. J.P. Morgan Quantitative Research, Asset Management Division.

Deadband Hysteresis Filter [BackQuant]Deadband Hysteresis Filter

What this is

This tool builds a “debounced” price baseline that ignores small fluctuations and only reacts when price meaningfully departs from its recent path. It uses a deadband to define how much deviation matters and a hysteresis scheme to avoid rapid flip-flops around the decision boundary. The baseline’s slope provides a simple trend cue, used to color candles and to trigger up and down alerts.

Why deadband and hysteresis help

They filter micro noise so the baseline does not react to every tiny tick.

They stabilize state changes. Hysteresis means the rule to start moving is stricter than the rule to keep holding, which reduces whipsaw.

They produce a stepped, readable path that advances during sustained moves and stays flat during chop.

How it works (conceptual)

At each bar the script maintains a running baseline dbhf and compares it to the input price p .

Compute a base threshold baseTau using the selected mode (ATR, Percent, Ticks, or Points).

Build an enter band tauEnter = baseTau × Enter Mult and an exit band tauExit = baseTau × Exit Mult where typically Exit Mult < Enter Mult .

Let diff = p − dbhf .

If diff > +tauEnter , raise the baseline by response × (diff − tauEnter) .

If diff < −tauEnter , lower the baseline by response × (diff + tauEnter) .

Otherwise, hold the prior value.

Trend state is derived from slope: dbhf > dbhf → up trend, dbhf < dbhf → down trend.

Inputs and what they control

Threshold mode

ATR — baseTau = ATR(atrLen) × atrMult . Adapts to volatility. Useful when regimes change.

Percent — baseTau = |price| × pctThresh% . Scale-free across symbols of different prices.

Ticks — baseTau = syminfo.mintick × tickThresh . Good for futures where tick size matters.

Points — baseTau = ptsThresh . Fixed distance in price units.

Band multipliers and response

Enter Mult — outer band. Price must travel at least this far from the baseline before an update occurs. Larger values reject more noise but increase lag.

Exit Mult — inner band for hysteresis. Keep this smaller than Enter Mult to create a hold zone that resists small re-entries.

Response — step size when outside the enter band. Higher response tracks faster; lower response is smoother.

UI settings

Show Filtered Price — plots the baseline on price.

Paint candles — colors bars by the filtered slope using your long/short colors.

How it can be used

Trend qualifier — take entries only in the direction of the baseline slope and skip trades against it.

Debounced crossovers — use the baseline as a stabilized surrogate for price in moving-average or channel crossover rules.

Trailing logic — trail stops a small distance beyond the baseline so small pullbacks do not eject the trade.

Session aware filtering — widen Enter Mult or switch to ATR mode for volatile sessions; tighten in quiet sessions.

Parameter interactions and tuning

Enter Mult vs Response — both govern sensitivity. If you see too many flips, increase Enter Mult or reduce Response. If turns feel late, do the opposite.

Exit Mult — widening the gap between Enter and Exit expands the hold zone and reduces oscillation around the threshold.

Mode choice — ATR adapts automatically; Percent keeps behavior consistent across instruments; Ticks or Points are useful when you think in fixed increments.

Timeframe coupling — on higher timeframes you can often lower Enter Mult or raise Response because raw noise is already reduced.

Concrete starter recipes

General purpose — ATR mode, atrLen=14 , atrMult=1.0–1.5 , Enter=1.0 , Exit=0.5 , Response=0.20 . Balanced noise rejection and lag.

Choppy range filter — ATR mode, increase atrMult to 2.0, keep Response≈0.15 . Stronger suppression of micro-moves.

Fast intraday — Percent mode, pctThresh=0.1–0.3 , Enter=1.0 , Exit=0.4–0.6 , Response=0.30–0.40 . Quicker turns for scalping.

Futures ticks — Ticks mode, set tickThresh to a few spreads beyond typical noise; start with Enter=1.0 , Exit=0.5 , Response=0.25 .

Strengths

Clear, explainable logic with an explicit noise budget.

Multiple threshold modes so the same tool fits equities, futures, and crypto.

Built-in hysteresis that reduces flip-flop near the boundary.

Slope-based coloring and alerts that make state changes obvious in real time.

Limitations and notes

All filters add lag. Larger thresholds and smaller response trade faster reaction for fewer false turns.

Fixed Points or Ticks can under- or over-filter when volatility regime shifts. ATR adapts, but will also expand bands during spikes.

On extremely choppy symbols, even a well tuned band will step frequently. Widen Enter Mult or reduce Response if needed.

This is a chart study. It does not include commissions, slippage, funding, or gap risks.

Alerts

DBHF Up Slope — baseline turns from down to up on the latest bar.

DBHF Down Slope — baseline turns from up to down on the latest bar.

Implementation details worth knowing

Initialization sets the baseline to the first observed price to avoid a cold-start jump.

Slope is evaluated bar-to-bar. The up and down alerts check for a change of slope rather than raw price crossings.

Candle colors and the baseline plot share the same long/short palette with transparency applied to the line.

Practical workflow

Pick a mode that matches how you think about distance. ATR for volatility aware, Percent for scale-free, Ticks or Points for fixed increments.

Tune Enter Mult until the number of flips feels appropriate for your timeframe.

Set Exit Mult clearly below Enter Mult to create a real hold zone.

Adjust Response last to control “how fast” the baseline chases price once it decides to move.

Final thoughts

Deadband plus hysteresis gives you a principled way to “only care when it matters.” With a sensible threshold and response, the filter yields a stable, low-chop trend cue you can use directly for bias or plug into your own entries, exits, and risk rules.

EMA Cross Alert V666 [noFuck]EMA Cross Alert — What it does

EMA Cross Alert watches three EMAs (Short, Mid, Long), detects their crossovers, and reports exactly one signal per bar by priority: EARLY > Short/Mid > Mid/Long > Short/Long. Optional EARLY mode pings when Short crosses Long while Mid is still between them—your polite early heads-up.

Why you might like it

Three crossover types: s/m, m/l, s/l

EARLY detection: earlier hints, not hype

One signal per bar: less noise, more focus

Clear visuals: tags, big cross at signal price, EARLY triangles

Alert-ready: dynamic alert text on bar close + static alertconditions for UI

Inputs (plain English)

Short/Mid/Long EMA length — how fast each EMA reacts

Extra EMA length (visual only) — context EMA; does not affect signals

Price source — e.g., Close

Show cross tags / EARLY triangles / large cross — visual toggles

Enable EARLY signals (Short/Long before Mid) — turn early pings on/off

Count Mid EMA as "between" even when equal (inclusive) — ON: Mid counts even if exactly equal to Short or Long; OFF (default): Mid must be strictly between them

Enable dynamic alerts (one per bar close) — master alert switch

Alert on Short/Mid, Mid/Long, Short/Long, EARLY — per-signal alert toggles

Quick tips

Start with defaults; if you want more EARLY on smooth/low-TF markets, turn “inclusive” ON

Bigger lengths = calmer trend-following; smaller = faster but choppier

Combine with volume/structure/risk rules—the indicator is the drummer, not the whole band

Disclaimer

Alerts, labels, and triangles are not trade ideas or financial advice. They are informational signals only. You are responsible for entries, exits, risk, and position sizing. Past performance is yesterday; the future is fashionably late.

Credits

Built with the enthusiastic help of Code Copilot (AI)—massively involved, shamelessly proud, and surprisingly good at breakfasting on exponential moving averages.

XAUUSD Buy/Sell Alerts with SL & TPThis custom TradingView indicator identifies high-probability buy and sell signals on XAUUSD using EMA crossovers combined with RSI confirmation. Designed for precision entries, it automatically calculates optimal Stop Loss (SL) and Take Profit (TP) levels based on user-defined pip distances.

Key Features:

Fast and Slow EMA crossover for trend direction

RSI filter for momentum confirmation

Dynamic SL and TP levels to manage risk and reward

Visual buy/sell signals plotted on chart

Real-time alerts with detailed messages including entry price, SL, and TP

Suitable for multiple timeframes and trading styles

Perfect for traders seeking clear signals with built-in risk management for scalping or swing trading XAUUSD.

CNS - Multi-Timeframe Bollinger Band OscillatorMy hope is to optimize the settings for this indicator and reintroduce it as a "strategy" with suggested position entry and exit points shown in the price pane.

I’ve been having good results setting the “Bollinger Band MA Length” in the Input tab to between 5 and 10. You can use the standard 20 period, but your results will not be as granular.

This indicator has proven very good at finding local tops and bottoms by combining data from multiple timeframes. Use BB timeframes that are lower than the timeframe you are viewing in your price pane.

The default settings work best on the weekly timeframe, but can be adjusted for most timeframes including intraday.

Be cognizant that the indicator, like other oscillators, does occasionally produce divergences at tops and bottoms.

Any feedback is appreciated.

Overview

This indicator is an oscillator that measures the normalized position of the price relative to Bollinger Bands across multiple timeframes. It takes the price's position within the Bollinger Bands (calculated on different timeframes) and averages those positions to create a single value that oscillates between 0 and 1. This value is then plotted as the oscillator, with reference lines and colored regions to help interpret the price's relative strength or weakness.

How It Works

Bollinger Band Calculation:

The indicator uses a custom function f_getBBPosition() to calculate the position of the price within Bollinger Bands for a given timeframe.

Price Position Normalization:

For each timeframe, the function normalizes the price's position between the upper and lower Bollinger Bands.

It calculates three positions based on the high, low, and close prices of the requested timeframe:

pos_high = (High - Lower Band) / (Upper Band - Lower Band)

pos_low = (Low - Lower Band) / (Upper Band - Lower Band)

pos_close = (Close - Lower Band) / (Upper Band - Lower Band)

If the upper band is not greater than the lower band or if the data is invalid (e.g., na), it defaults to 0.5 (the midline).

The average of these three positions (avg_pos) represents the normalized position for that timeframe, ranging from 0 (at the lower band) to 1 (at the upper band).

Multi-Timeframe Averaging:

The indicator fetches Bollinger Band data from four customizable timeframes (default: 30min, 60min, 240min, daily) using request.security() with lookahead=barmerge.lookahead_on to get the latest available data.

It calculates the normalized position (pos1, pos2, pos3, pos4) for each timeframe using f_getBBPosition().

These four positions are then averaged to produce the final avg_position:avg_position = (pos1 + pos2 + pos3 + pos4) / 4

This average is the oscillator value, which is plotted and typically oscillates between 0 and 1.

Moving Averages:

Two optional moving averages (MA1 and MA2) of the avg_position can be enabled, calculated using simple moving averages (ta.sma) with customizable lengths (default: 5 and 10).

These can be potentially used for MA crossover strategies.

What Is Being Averaged?

The oscillator (avg_position) is the average of the normalized price positions within the Bollinger Bands across the four selected timeframes. Specifically:It averages the avg_pos values (pos1, pos2, pos3, pos4) calculated for each timeframe.

Each avg_pos is itself an average of the normalized positions of the high, low, and close prices relative to the Bollinger Bands for that timeframe.

This multi-timeframe averaging smooths out short-term fluctuations and provides a broader perspective on the price's position within the volatility bands.

Interpretation

0.0 The price is at or below the lower Bollinger Band across all timeframes (indicating potential oversold conditions).

0.15: A customizable level (green band) which can be used for exiting short positions or entering long positions.

0.5: The midline, where the price is at the average of the Bollinger Bands (neutral zone).

0.85: A customizable level (orange band) which can be used for exiting long positions or entering short positions.

1.0: The price is at or above the upper Bollinger Band across all timeframes (indicating potential overbought conditions).

The colored regions and moving averages (if enabled) help identify trends or crossovers for trading signals.

Example

If the 30min timeframe shows the close at the upper band (position = 1.0), the 60min at the midline (position = 0.5), the 240min at the lower band (position = 0.0), and the daily at the upper band (position = 1.0), the avg_position would be:(1.0 + 0.5 + 0.0 + 1.0) / 4 = 0.625

This value (0.625) would plot in the orange region (between 0.85 and 0.5), suggesting the price is relatively strong but not at an extreme.

Notes

The use of lookahead=barmerge.lookahead_on ensures the indicator uses the latest available data, making it more real-time, though its effectiveness depends on the chart timeframe and TradingView's data feed.

The indicator’s sensitivity can be adjusted by changing bb_length ("Bollinger Band MA Length" in the Input tab), bb_mult ("Bollinger Band Standard Deviation," also in the Input tab), or the selected timeframes.

Multi-Timeframe Bollinger BandsMy hope is to optimize the settings for this indicator and reintroduce it as a "strategy" with suggested position entry and exit points shown in the price pane.

I’ve been having good results setting the “Bollinger Band MA Length” in the Input tab to between 5 and 10. You can use the standard 20 period, but your results will not be as granular.

This indicator has proven very good at finding local tops and bottoms by combining data from multiple timeframes. Use timeframes that are lower than the timeframe you are viewing in your price pane. Be cognizant that the indicator, like other oscillators, does occasionally produce divergences at tops and bottoms.

Any feedback is appreciated.

Overview

This indicator is an oscillator that measures the normalized position of the price relative to Bollinger Bands across multiple timeframes. It takes the price's position within the Bollinger Bands (calculated on different timeframes) and averages those positions to create a single value that oscillates between 0 and 1. This value is then plotted as the oscillator, with reference lines and colored regions to help interpret the price's relative strength or weakness.

How It Works

Bollinger Band Calculation:

The indicator uses a custom function f_getBBPosition() to calculate the position of the price within Bollinger Bands for a given timeframe.

Price Position Normalization:

For each timeframe, the function normalizes the price's position between the upper and lower Bollinger Bands.

It calculates three positions based on the high, low, and close prices of the requested timeframe:

pos_high = (High - Lower Band) / (Upper Band - Lower Band)

pos_low = (Low - Lower Band) / (Upper Band - Lower Band)

pos_close = (Close - Lower Band) / (Upper Band - Lower Band)

If the upper band is not greater than the lower band or if the data is invalid (e.g., na), it defaults to 0.5 (the midline).

The average of these three positions (avg_pos) represents the normalized position for that timeframe, ranging from 0 (at the lower band) to 1 (at the upper band).

Multi-Timeframe Averaging:

The indicator fetches Bollinger Band data from four customizable timeframes (default: 30min, 60min, 240min, daily) using request.security() with lookahead=barmerge.lookahead_on to get the latest available data.

It calculates the normalized position (pos1, pos2, pos3, pos4) for each timeframe using f_getBBPosition().

These four positions are then averaged to produce the final avg_position:avg_position = (pos1 + pos2 + pos3 + pos4) / 4

This average is the oscillator value, which is plotted and typically oscillates between 0 and 1.

Moving Averages:

Two optional moving averages (MA1 and MA2) of the avg_position can be enabled, calculated using simple moving averages (ta.sma) with customizable lengths (default: 5 and 10).

These can be potentially used for MA crossover strategies.

What Is Being Averaged?

The oscillator (avg_position) is the average of the normalized price positions within the Bollinger Bands across the four selected timeframes. Specifically:It averages the avg_pos values (pos1, pos2, pos3, pos4) calculated for each timeframe.

Each avg_pos is itself an average of the normalized positions of the high, low, and close prices relative to the Bollinger Bands for that timeframe.

This multi-timeframe averaging smooths out short-term fluctuations and provides a broader perspective on the price's position within the volatility bands.

Interpretation

0.0 The price is at or below the lower Bollinger Band across all timeframes (indicating potential oversold conditions).

0.15: A customizable level (green band) which can be used for exiting short positions or entering long positions.

0.5: The midline, where the price is at the average of the Bollinger Bands (neutral zone).

0.85: A customizable level (orange band) which can be used for exiting long positions or entering short positions.

1.0: The price is at or above the upper Bollinger Band across all timeframes (indicating potential overbought conditions).

The colored regions and moving averages (if enabled) help identify trends or crossovers for trading signals.

Example

If the 30min timeframe shows the close at the upper band (position = 1.0), the 60min at the midline (position = 0.5), the 240min at the lower band (position = 0.0), and the daily at the upper band (position = 1.0), the avg_position would be:(1.0 + 0.5 + 0.0 + 1.0) / 4 = 0.625

This value (0.625) would plot in the orange region (between 0.85 and 0.5), suggesting the price is relatively strong but not at an extreme.

Notes

The use of lookahead=barmerge.lookahead_on ensures the indicator uses the latest available data, making it more real-time, though its effectiveness depends on the chart timeframe and TradingView's data feed.

The indicator’s sensitivity can be adjusted by changing bb_length ("Bollinger Band MA Length" in the Input tab), bb_mult ("Bollinger Band Standard Deviation," also in the Input tab), or the selected timeframes.

Multi-Timeframe Bollinger Band PositionBeta version.

My hope is to optimize the settings for this indicator and reintroduce it as a "strategy" with suggested position entry and exit points shown in the price pane.

Any feedback is appreciated.

Overview

This indicator is an oscillator that measures the normalized position of the price relative to Bollinger Bands across multiple timeframes. It takes the price's position within the Bollinger Bands (calculated on different timeframes) and averages those positions to create a single value that oscillates between 0 and 1. This value is then plotted as the oscillator, with reference lines and colored regions to help interpret the price's relative strength or weakness.

How It Works

Bollinger Band Calculation:

The indicator uses a custom function f_getBBPosition() to calculate the position of the price within Bollinger Bands for a given timeframe.

Price Position Normalization:

For each timeframe, the function normalizes the price's position between the upper and lower Bollinger Bands.

It calculates three positions based on the high, low, and close prices of the requested timeframe:

pos_high = (High - Lower Band) / (Upper Band - Lower Band)

pos_low = (Low - Lower Band) / (Upper Band - Lower Band)

pos_close = (Close - Lower Band) / (Upper Band - Lower Band)

If the upper band is not greater than the lower band or if the data is invalid (e.g., na), it defaults to 0.5 (the midline).

The average of these three positions (avg_pos) represents the normalized position for that timeframe, ranging from 0 (at the lower band) to 1 (at the upper band).

Multi-Timeframe Averaging:

The indicator fetches Bollinger Band data from four customizable timeframes (default: 30min, 60min, 240min, daily) using request.security() with lookahead=barmerge.lookahead_on to get the latest available data.

It calculates the normalized position (pos1, pos2, pos3, pos4) for each timeframe using f_getBBPosition().

These four positions are then averaged to produce the final avg_position:avg_position = (pos1 + pos2 + pos3 + pos4) / 4

This average is the oscillator value, which is plotted and typically oscillates between 0 and 1.

Moving Averages:

Two optional moving averages (MA1 and MA2) of the avg_position can be enabled, calculated using simple moving averages (ta.sma) with customizable lengths (default: 5 and 10).

These can be potentially used for MA crossover strategies.

What Is Being Averaged?

The oscillator (avg_position) is the average of the normalized price positions within the Bollinger Bands across the four selected timeframes. Specifically:It averages the avg_pos values (pos1, pos2, pos3, pos4) calculated for each timeframe.

Each avg_pos is itself an average of the normalized positions of the high, low, and close prices relative to the Bollinger Bands for that timeframe.

This multi-timeframe averaging smooths out short-term fluctuations and provides a broader perspective on the price's position within the volatility bands.

Interpretation:

0.0 The price is at or below the lower Bollinger Band across all timeframes (indicating potential oversold conditions).

0.15: A customizable level (green band) which can be used for exiting short positions or entering long positions.

0.5: The midline, where the price is at the average of the Bollinger Bands (neutral zone).

0.85: A customizable level (orange band) which can be used for exiting long positions or entering short positions.

1.0: The price is at or above the upper Bollinger Band across all timeframes (indicating potential overbought conditions).

The colored regions and moving averages (if enabled) help identify trends or crossovers for trading signals.

Example:

If the 30min timeframe shows the close at the upper band (position = 1.0), the 60min at the midline (position = 0.5), the 240min at the lower band (position = 0.0), and the daily at the upper band (position = 1.0), the avg_position would be:(1.0 + 0.5 + 0.0 + 1.0) / 4 = 0.625

This value (0.625) would plot in the orange region (between 0.85 and 0.5), suggesting the price is relatively strong but not at an extreme.

Notes:

The use of lookahead=barmerge.lookahead_on ensures the indicator uses the latest available data, making it more real-time, though its effectiveness depends on the chart timeframe and TradingView's data feed.

The indicator’s sensitivity can be adjusted by changing bb_length ("Bollinger Band MA Length" in the Input tab), bb_mult ("Bollinger Band Standard Deviation," also in the Input tab), or the selected timeframes.

VOID OCULUS MACHINE V8 – ASSASSIN MODEVOID OCULUS MACHINE V8 – ASSASSIN MODE

Version 8.0 | Pine Script v6

Purpose & Originality

VOID OCULUS MACHINE V8 – ASSASSIN MODE brings together four advanced trading filters—EMA crossovers, TRIX momentum, VWAP band positioning, and a proprietary “Predictive Cloud”—into a single, high-precision entry system. Rather than relying on any one signal, it calculates a confidence score combining trend, momentum, volume, and volatility cues, then triggers only the highest-probability setups once a user-defined threshold is met. This multi-layer architecture offers traders laser-focused entries (“Assassin Mode”) with built-in risk (stop) and reward (targets) visualization.

How It Works & Component Rationale

EMA Trend Alignment

Fast EMA (9) vs. Slow EMA (21): Captures short-term versus medium-term trend. A bullish bias requires EMA9 > EMA21, bearish bias EMA9 < EMA21.

TRIX Momentum Filter

A triple-smoothed EMA oscillator over 15 bars, expressed as a percentage change. Positive TRIX confirms upward momentum; negative TRIX confirms downward momentum.

Gaussian Noise Reduction

Dual 5-period EMA smoothing of price removes short-term noise, creating a “cloud base.” Entries only fire when price interacts favorably with this smoothed baseline.

VWAP Band Confirmation (Optional)

Calculates session VWAP ± one standard deviation over 20 bars, plotting upper/lower bands. Traders can require price to sit above/below VWAP mid for trend confirmation.

Predictive Cloud Overlay

A dynamic band (Gaussian ± ATR) forecasts a near-term “value zone.” Pullback and reversal entries can occur as price re-enters or breaks out of this cloud.

Confidence Scoring

Starts at 0 and adds:

+30 for EMA trend alignment (bull or bear)

+20 for volume spike (>20-bar SMA)

+20 for non-zero TRIX slope

+20 for ATR expansion (volatility ramping)

+10 if price is above or below VWAP mid (if VWAP filter is enabled)

Only fires signals when confidence ≥ 60% (configurable), ensuring multi-factor confluence.

Entry Type Differentiation

Breakout: Price pierces prior 10-bar high/low on volume and ATR expansion.

Pullback: Trend bias plus a crossover of price with EMA9.

Reversal: Price crosses back into the Predictive Cloud from outside, confirmed by VWAP cross.

Automated Trade Visualization

On each signal, clears previous objects, plots a “BUY (xx%) – ” or “SELL (xx%) – ” label, four tiered ATR-based targets (1×, 1.5×, 2×, 3.5×), and a stop-loss (ATR × 1.5).

Inputs & Customization

Input Description Default

Fast EMA Length for short-term trend EMA 9

Slow EMA Length for medium-term trend EMA 21

TRIX Length Period for triple-smoothed momentum oscillator 15

Stop Multiplier ATR multiple for stop-loss distance 1.5

Target Multiplier ATR multiple for first profit target 1.5

Enable VWAP Filter Require price alignment above/below VWAP mid On

Minimum Confidence Confidence % threshold to trigger a signal 60

Show Predictive Cloud Toggle the Gaussian ± ATR cloud on/off On

How to Use

Apply to Chart: Suitable on 5 m–1 h timeframes for swing entries.

Adjust Confidence & Filters: Raise the Minimum Confidence to tighten setups; disable VWAP filter for pure price/momentum plays.

Read Signals:

“BUY (75%) – Breakout” label means 75% confluence across filters, triggered by a breakout entry type.

Four colored horizontal lines mark TP1–TP4; a red line marks your stop.

Manage the Trade:

Use the plotted stop-loss line; scale out at targets or trail behind the Predictive Cloud.

Unique Value

VOID OCULUS MACHINE V8 stands out by quantifying multi-dimensional market context into a single confidence score and providing automated trade object plotting—no more manual target calculations or cluttered charts. Its “Assassin Mode” ensures only the most compelling setups trigger, saving traders time and reducing noise.

Disclaimer

This indicator is for educational purposes. Past performance does not guarantee future results. Always backtest across symbols/timeframes, combine with personal discretion, and apply strict risk management before trading live.

Cumulative Volume Delta (SB-1) 2.0

📈 Cumulative Volume Delta (CVD) — Stair-Step + Threshold Alerts

🔍 Overview

This Cumulative Volume Delta (CVD) tool visualizes aggressive buying and selling pressure in the market by plotting candlestick-style bars based on volume delta. It helps traders understand which side — buyers or sellers — is exerting more control on lower timeframes and highlights momentum shifts through stair-step patterns and delta threshold breaks. Resets to zero at EOD

Ideal for futures traders, scalpers, and intraday strategists looking for orderflow-based confirmation.

🧠 What Is CVD?

CVD (Cumulative Volume Delta) measures the difference between market buys and sells over a specific timeframe. When the delta is rising, it suggests buyers are being more aggressive. Falling delta suggests seller dominance.

This script aggregates volume delta from a lower timeframe and plots it in a higher timeframe context, allowing you to track microstructure shifts within larger candles.

📊 Features

✅ CVD Candlesticks

Each bar represents volume delta as an OHLC-style candle using:

Open: Delta at the start of the bar

High/Low: Peak delta range

Close: Final delta value at bar close

Teal candles = Net buying pressure

Red candles = Net selling pressure

✅ Threshold Levels (Key Visual Zones)

The script includes horizontal dashed lines at:

+5,000 and +10,000 → Signify strong buying pressure

-5,000 and -10,000 → Signify strong selling pressure

0 line → Neutrality line (no net pressure)

These levels act as volume-based support/resistance zones and breakout confirmation tools. For example:

A CVD cross above +5,000 shows buyers taking control

A CVD cross above +10,000 implies strong bullish momentum

A CVD cross below -5,000 or -10,000 signals intense selling pressure

📈 Stair-Step Pattern Detection

Detects two specific volume-based continuation setups:

Bullish Stair-Step: Both the high and low of the CVD candle are higher than the previous candle

Bearish Stair-Step: Both the high and low of the CVD candle are lower than the previous candle

These patterns often appear during trending moves and serve as confirmation of strength or continuation.

Visual markers:

🟢 Green triangles below bars = Bullish stair-step

🔴 Red triangles above bars = Bearish stair-step

🔔 Alert Conditions

Get real-time alerts when:

Bullish Stair-Step is detected

Bearish Stair-Step is detected

CVD crosses above +5,000

CVD crosses below -5,000

📢 Alerts only trigger on crossover, not every time CVD remains above or below. This avoids repetitive notifications.

⚙️ Inputs & Customization

Anchor Timeframe: The higher timeframe to which CVD data is applied (default: 1D)

Lower Timeframe: The timeframe used to calculate the CVD delta (default: 5 minutes)

Optional Override: Use custom timeframe toggle to force your own micro timeframe

📌 How to Use This CVD Indicator (Step-by-Step Guide)

✅ 1. Confirm Bias Using the Zero Line

The zero line (0 CVD) represents neutral pressure — neither buyers nor sellers are dominating.

Use it as your first filter:

🔼 If CVD is above 0 and rising → Buyer control

🔽 If CVD is below 0 and falling → Seller control

🧠 Tip: CVD rising while price is consolidating may signal hidden buyer interest.

✅ 2. Watch for Crosses of Key Levels: +5,000 and +10,000

These levels act as momentum thresholds:

Level Signal Type What It Means

+5,000 Buyer breakout Buyers are starting to dominate

+10,000 Strong bull bias Strong institutional or algorithmic buying flow

-5,000 Seller breakout Sellers are taking control

-10,000 Strong bear bias Heavy selling pressure is entering the market

Wait for CVD to cross above +5K or below -5K to confirm the active side.

Use these crossovers as entry triggers, breakout confirmations, or trade filters.

🔔 Alerts fire only when the level is first crossed, not every bar above/below.

✅ 3. Use Stair-Step Patterns for Continuation Confirmation

The indicator shows stair-step patterns using triangle signals:

🟢 Green triangle below bar = Bullish stair-step

Suggests a higher high and higher low in delta → buyers stepping up

🔴 Red triangle above bar = Bearish stair-step

Suggests lower highs and lower lows in delta → selling pressure building

Use stair-step signals:

To confirm a continuation of trend

As an entry or add-on signal

Especially after a threshold breakout

🧠 Example: If CVD breaks above +5K and forms bullish stairs → confirms strong trend, ideal for momentum entries.

✅ 4. Combine with Price Action or Structure

CVD works best when used with price, not in isolation. For example:

📉 Price makes a new low but CVD doesn’t → potential bullish divergence

📈 CVD surges while price lags → buyers are absorbing, breakout likely

Use it with:

VWAP

Orderblocks

Liquidity sweeps

Break of market structure/MSS/BOS

✅ 5.

Set Anchor Timeframe = Daily

Set Lower Timeframe = 5 minutes (default)

This lets you:

See intraday flow inside daily bars

Confirm whether a daily candle is being built on net buying or selling

🧠 You’re essentially seeing intra-bar aggression within a bigger time structure.

🧭 Example Trading Setup

Bullish Scenario:

CVD is rising and above 0

CVD crosses above +5,000 → alert fires

Green stair-step appears

Price breaks local resistance or liquidity sweep completes

✅ Consider long entry with structure and CVD alignment

🎯 Place stops below last stair-step or structural low

📌 Final Notes

This tool does not repaint and is designed to work in real-time across all futures, crypto, and equity instruments that support volume data. If your symbol does not provide volume, the script will notify you.

Use it in confluence with VWAP, liquidity zones, or structure breaks for high-confidence trades.

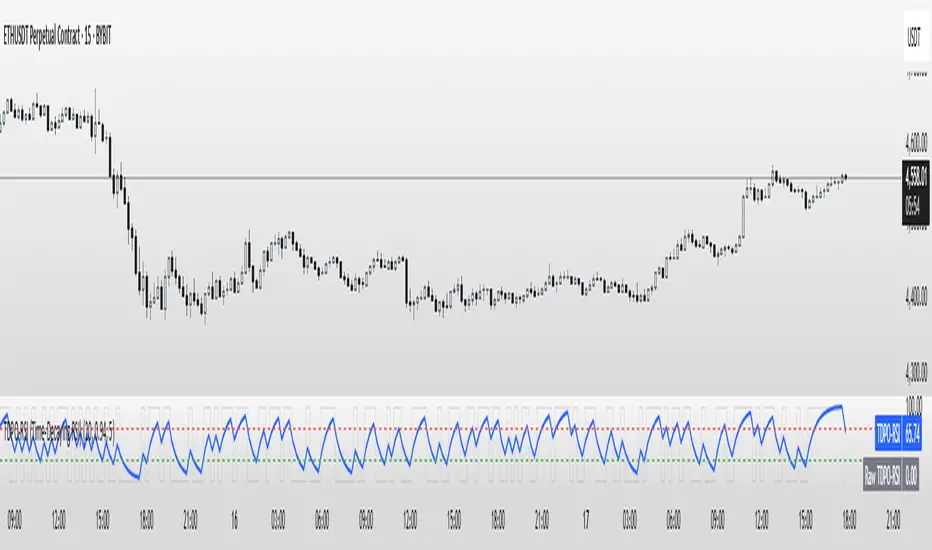

TDPO-RSI (Time-Decaying Percentile RSI)TDPO-RSI (Time-Decaying Percentile RSI)

TDPO-RSI is a modern, statistically-enhanced momentum indicator that improves on traditional RSI by using percentile-based analysis with exponential time decay. Instead of averaging gains and losses equally, this indicator ranks them by size and weights recent data more heavily—resulting in a more responsive and noise-resistant signal.

How it works:

Calculates percentile rank of gains and losses over a lookback window

Applies a decay factor (lambda) to give more weight to recent price action

Outputs a percentile-based RSI value between 0 and 100

Optional smoothing via EMA for clearer crossover signals

Key Uses:

Identify overbought/oversold zones (default: 70/30)

Use raw vs. smoothed RSI crossovers for entries

Detect momentum shifts earlier than traditional RSI

Suitable for scalping, trend continuation, and reversal setups

Inputs:

Lookback Length: Number of bars used for percentile calculation

Decay Factor (lambda): How quickly older data fades in influence (0.80–0.99)

Smoothing EMA: Smooths the final output to reduce noise

Tip: Combine with price structure and volume for best results. Higher timeframes can be used for trend context, while lower timeframes help with precise entries.

This tool is ideal for traders who want adaptive momentum analysis rooted in statistical behavior.

Options Strategy V2.0📈 Options Strategy V2.0 – Intraday Reversal-Resilient Momentum System

Overview:

This strategy is designed specifically for intraday SPY, TSLA, MSFT, etc. options trading (0DTE or 1DTE), using high-probability signals derived from a confluence of technical indicators: EMA crossovers, RSI thresholds, ATR-based risk control, and volume spikes. The strategy aims to capture strong directional moves while avoiding overtrading, thanks to a built-in cooldown logic and optional time/session filters.

⚙️ Core Concept

The strategy executes trades only in the direction of the prevailing trend, determined by short- and long-term Exponential Moving Averages (EMA). Entry signals are generated when the Relative Strength Index (RSI) confirms momentum in the direction of the trend, and volume spikes suggest institutional activity.

To increase adaptability and user control, it includes a highly customizable parameter set for both long and short entries independently.

📌 Key Features

✅ Trend-Following Logic

Long entries are only allowed when EMA(short) > EMA(long)

Short entries are only allowed when EMA(short) < EMA(long)

✅ RSI Confirmation

Long: Requires RSI crossover above a configurable threshold

Short: Requires RSI crossunder below a configurable threshold

Optional rejection filters: Entry blocked above/below specific RSI extremes

✅ Volume Spike Filter

Confirms institutional participation by comparing current volume to an average multiplied by a user-defined factor.

✅ ATR-Based Risk Management

Both Stop Loss (SL) and Take Profit (TP) are dynamically calculated using ATR × a multiplier.

TP/SL ratio is fully configurable.

✅ Cooldown Control

After every trade, the system waits for a set number of bars before allowing new entries.

This prevents overtrading and increases signal quality.

Optionally, cooldown is ignored for reversal trades, ensuring the system can react immediately to a confirmed trend change.

✅ Candle Body Filter (Noise Control)

Avoids trades on candles with too small bodies relative to wicks (often noise or indecision candles).

✅ VWAP Confirmation (Optional)

Ensures price is trading above VWAP for long entries, or below for short entries.

✅ Time & Session Filters

Trades only during regular market hours (09:30–16:00 EST).

No-trade zone (e.g., 14:15–15:45 EST) to avoid low-liquidity traps or late-day whipsaws.

✅ End-of-Day Auto Close

All open positions are force-closed at 15:55 EST, protecting against overnight risk (especially relevant for 0DTE options).

📊 Visual Aids

EMA plots show trend direction

VWAP line provides real-time mean-reversion context

Stop Loss and Take Profit lines appear dynamically with each trade

Alerts notify of entry signals and exit triggers

🔧 Customization Panel

Nearly every element of the strategy can be tailored:

EMA lengths (short and long, for both sides)

RSI thresholds and length

ATR length, SL multiplier, and TP/SL ratio

Volume spike sensitivity

Minimum EMA distance filter

Candle body ratio filter

Session restrictions

Cooldown logic (duration + reversal exception)

This makes the strategy extremely versatile, allowing both conservative and aggressive configurations depending on the trader’s profile and the market context.

📌 Example Use Case: SPY Options (0DTE or 1DTE)

This system was designed and tested specifically for SPY and other intraday options trading, where:

Delta is around 0.50 or higher

Trades are short-lived (often 1–5 candles)

You aim to trade 1–3 signals per day, filtering out weak entries

🚫 Important Notes

It is not a scalping strategy; it relies on confirmed breakouts with trend support

No pyramiding or re-entries without cooldown to preserve risk integrity

Should be used with real-time alerts and manual broker execution

📈 Alerts Included

📈 Long Entry Signal

📉 Short Entry Signal

⚠️ Auto-closed all positions at 15:55 EST

✅ Proven Settings – Real Trades + Backtest Results

The current version of the strategy includes the optimal settings I’ve arrived at through extensive backtesting, as well as 3 months of real trading with consistent profitability. These results reflect real-world execution under live market conditions using 0DTE SPY options, with disciplined trade management and risk control.

🧠 Final Thoughts

Options Strategy V2.0 is a robust, highly tunable intraday strategy that blends momentum, trend-following, and volume confirmation. It is ideal for disciplined traders focused on SPY or other 0DTE/1DTE options, and it includes guardrails to reduce false signals and improve execution timing.

Perfect for those who seek precision, flexibility, and risk-defined setups—not blind automation.

EMA and Dow Theory Strategies🌐 Strategy Description

📘 Overview

This is a hybrid strategy that combines EMA crossovers, Dow Theory swing logic, and multi-timeframe trend overlays. It is suitable for intraday to short-term trading on any asset class: crypto, forex, stocks, and indices.

The strategy provides precise entry/exit signals, dynamic stop-loss and scale-out, and highly visual trade guidance.

🧠 Key Features

・Dual EMA crossover system (applied to both symbol and external index)

・Dow Theory-based swing high/low detection for trend confirmation

・Visual overlay of higher timeframe swing trend (htfTrend)

・RSI filter to avoid overbought/oversold entries

・Dynamic partial take-profit when trend weakens

・Custom stop-loss (%) control

・Visualized trade PnL labels directly on chart

・Alerts for entry, stop-loss, partial exit

・Gradient background zones for swing zones and trend visualization

・Auto-tracked metrics: APR, drawdown, win rate, equity curve

⚙️ Input Parameters

| Parameter | Description |

| ------------------------- | -------------------------------------------------------- |

| Fast EMA / Slow EMA | Periods for detecting local trend via EMAs |

| Index Fast EMA / Slow EMA | EMAs applied to external reference index |

| StopLoss | Maximum loss threshold in % |

| ScaleOut Threshold | Scale-out percentage when trend changes color |

| RSI Period / Levels | RSI period and overbought/oversold levels |

| Swing Detection Length | Number of bars used to detect swing highs/lows |

| Stats Display Options | Toggle PnL labels and position of statistics table |

🧭 About htfTrend (Higher Timeframe Trend)

The script includes a higher timeframe trend (htfTrend) calculated using Dow Theory (pivot highs/lows).

This trend is only used for visual guidance, not for actual entry conditions.

Why? Strictly filtering trades by higher timeframe often leads to missed opportunities and low frequency.

By keeping htfTrend visual-only, traders can still refer to macro structure but retain trade flexibility.

Use it as a contextual tool, not a constraint.

ストラテジー説明

📘 概要

本ストラテジーは、EMAクロスオーバー、ダウ理論によるスイング判定、**上位足トレンドの視覚表示(htfTrend)**を組み合わせた複合型の短期トレーディング戦略です。

仮想通貨・FX・株式・指数など幅広いアセットに対応し、デイトレード〜スキャルピング用途に適しています。

動的な利確/損切り、視覚的にわかりやすいエントリー/イグジット、統計表示を搭載しています。

🧠 主な機能

・対象銘柄+外部インデックスのEMAクロスによるトレンド判定

・ダウ理論に基づいたスイング高値・安値検出とトレンド判断

・上位足スイングトレンド(htfTrend)の視覚表示

・RSIフィルターによる過熱・売られすぎの回避

・トレンドの弱まりに応じた部分利確(スケールアウト)

・**損切り閾値(%)**をカスタマイズ可能

・チャート上に損益ラベル表示

・アラート完備(エントリー・決済・部分利確)

・トレンドゾーンを可視化する背景グラデーション

・勝率・ドローダウン・APR・資産増加率などの自動表示

| 設定項目名 | 説明内容 |

| --------------------- | -------------------------- |

| Fast EMA / Slow EMA | 銘柄に対して使用するEMAの期間設定 |

| Index Fast / Slow EMA | 外部インデックスのEMA設定 |

| 損切り(StopLoss) | 損切りラインのしきい値(%で指定) |

| 部分利確しきい値 | トレンド弱化時にスケールアウトする割合(%) |

| RSI期間・水準 | RSI計算期間と、過熱・売られすぎレベル設定 |

| スイング検出期間 | スイング高値・安値の検出に使用するバー数 |

| 統計表示の切り替え | 損益ラベルや統計テーブルの表示/非表示選択 |

🧭 上位足トレンド(htfTrend)について

本スクリプトには、上位足でのスイング高値・安値の更新に基づく**htfTrend(トレンド判定)が含まれています。

これは視覚的な参考情報であり、エントリーやイグジットには直接使用されていません。**

その理由は、上位足を厳密にロジックに組み込むと、トレード機会の損失が増えるためです。

このスクリプトでは、**判断の補助材料として「表示のみに留める」**設計を採用しています。

→ 裁量で「利確を早める」「逆張りを避ける」判断に活用可能です。

AZ Dynamic Trend Indicator with Heikin-Ashi### Dynamic Trend Indicator with Heikin-Ashi (v2.7)

**Effortlessly identify trends and reversals** with this versatile tool combining multi-timeframe analysis, adaptive moving averages, and Heikin-Ashi smoothing. Here's what it offers:

#### 🔍 **Core Features**

1. **Dual Timeframe Analysis**:

- Track trends on higher timeframes (e.g., 1H/D) while viewing signals on your current chart.

- Toggle between **Heikin-Ashi** or standard candles for cleaner trend visualization.

2. **8 Customizable MAs**:

- Choose from **ALMA, HMA, SMA, SWMA, VWMA, WMA, ZLEMA, or EMA** with adjustable periods.

- Unique "Trend Strength" metric: `(MA_Close - MA_Open) / (MA_High - MA_Low)` highlights momentum direction.

3. **Smart Signals**:

- **Entry/Exit**: Triangles mark crossovers between MA Close/Open.

- **Reversal Alerts**: Detects counter-trend moves within a user-defined window (default: 3 bars) after signals.

- Color-coded plots: Bullish (🟢), Bearish (🔴), Reversal Bull (🔵), Reversal Bear (🟠).

#### 🎨 **Visual Customization**

- Toggle **High/Low MA lines**, **Close line**, and **fill colors**.

- Adjust colors for all elements to match your chart theme.

- Hide signals or reversal markers as needed.

#### ⚙️ **Practical Use**

- **Trend Following**: Use the MA Close/Open crossover with trend fill colors to confirm direction.

- **Reversal Trading**: Capitalize on pullbacks with reversal signals (e.g., after a bearish signal, watch for Bull Reversal markers).

- **Multi-Timeframe Confirmation**: Avoid false signals by aligning higher-timeframe trends with your entries.

*Ideal for swing traders and trend riders!*

**Note**: Adjust `MA Period`, `Reversal Window`, and `Trend Timeframe` for your strategy. Disable Heikin-Ashi in choppy markets for faster reactions.

---

*Code v2.7 updates: Optimized reversal logic, added ALMA/ZLEMA support, and enhanced visual controls.*

Market Shift Levels [ChartPrime]Market Shift Levels

This indicator detects trend shifts and visualizes key market structure turning points using Hull Moving Average logic. It highlights potential areas of support and resistance where price is likely to react, empowering traders to spot early trend transitions.

Market Shift Levels are horizontal zones that mark the moment of a directional change in market behavior. These shifts are based on crossovers between two smoothed Hull Moving Averages (HMA), allowing the indicator to detect potential reversals with minimal lag.

Once a shift is detected:

A dashed horizontal Market Shift Level is plotted at the low (for bullish shift) or high (for bearish shift) of the candle.

These levels often become key reaction points during pullbacks and trend retests.

Volume or price labels are added when price wicks into these levels, helping traders gauge the strength of rejection or acceptance.

⯁ KEY FEATURES

Uses HMA-based logic to detect when price momentum shifts.

Plots clean Market Shift Levels (MSLs) that act as dynamic support and resistance.

Automatically colors bars and candles based on the price positioning relative to levels.

Labels wick-based retests with either:

Volume data of the 3-bar cluster (default).

Price level if toggled.

⯁ HOW TO USE

Look for trend shifts where the HMA crossover triggers a new level — this marks a possible structural pivot .

Use the horizontal level as a dynamic support or resistance zone — especially when price returns with wick rejections.

Watch for volume labels near the level — higher values signal stronger rejection and potential continuation.

Combine with confluence tools like Smart Money concepts or Fibonacci levels for added edge.

⯁ EXAMPLE SETUPS

After a bullish shift, wait for price to return and wick into the level — if volume spikes and candle closes strong, it’s a retest confirmation entry .

After a bearish shift, bearish wick rejections with volume may signal short re-entry zones .

⯁ CONCLUSION

The Market Shift Levels indicator offers a visual and data-backed approach to spotting trend reversals and critical retest zones. It’s a simple yet powerful tool to structure your trades around objective, repeatable market behavior — all in real-time.

CVD Strength | VTS Pro🔷 CVD Strength | VTS Pro

By Alireza Mossaheb

Description:

CVD Strength is a powerful tool designed to analyze market momentum by visualizing the Cumulative Volume Delta (CVD) using advanced techniques. This indicator provides a multi-timeframe view of volume delta behavior and highlights strong and weak bullish/bearish conditions based on volume spikes, candle size, and optional moving average filters.

Key Features:

Multi-timeframe CVD candle plotting with color-coded strength signals

Optional EMA (21), WMA (30), and SMA (50) overlays for trend filtering

Smart strength detection logic using volume, candle size, and moving average crossovers

Bullish and bearish crossover signals marked on chart

Customizable anchor and lower timeframes for flexible analysis

Alerts users when data vendor does not supply volume information

This script is particularly useful for identifying institutional buying/selling pressure and can be used effectively in both trend-following and mean-reversion strategies.

Trend Flow Trail [AlgoAlpha]OVERVIEW

This script overlays a custom hybrid indicator called the Money Flow Trail which combines a volatility-based trend-following trail with a volume-weighted momentum oscillator. It’s built around two core components: the AlphaTrail—a dynamic band system influenced by Hull MA and volatility—and a smoothed Money Flow Index (MFI) that provides insights into buying or selling pressure. Together, these tools are used to color bars, generate potential reversal markers, and assist traders in identifying trend continuation or exhaustion phases in any market or timeframe.

CONCEPTS

The AlphaTrail calculates a volatility-adjusted channel around price using the Hull Moving Average as the base and an EMA of range as the spread. It adaptively shifts based on price interaction to capture trend reversals while avoiding whipsaws. The direction (bullish or bearish) determines both the band being tracked and how the trail locks in. The Money Flow Index (MFI) is derived from hlc3 and volume, measuring buying vs selling pressure, and is further smoothed with a short Hull MA to reduce noise while preserving structure. These two systems work in tandem: AlphaTrail governs directional context, while MFI refines the timing.

FEATURES

Dynamic AlphaTrail line with regime switching logic that controls directional bias and bar coloring.