Bitcoin Bitmex volatilityIndicator that shows the volatility of Bitcoin on BitMex in a quantifiable way

Pesquisar nos scripts por "bitcoin"

Bitcoin Shorts and LongsThis indicator shows the volume of shorts and longs for margin trading in Bitfinex.

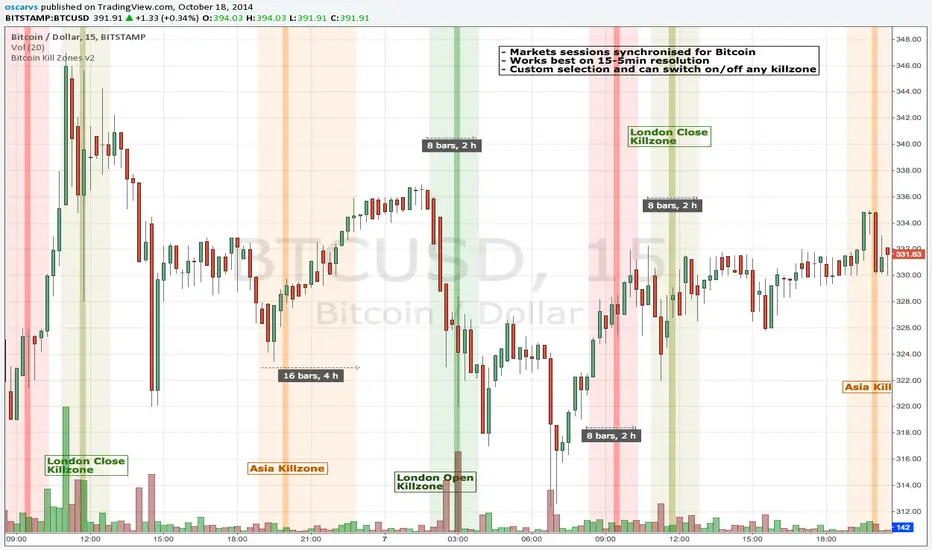

Bitcoin Kill Zones v2.1All I've changed in it from previous version is increased transparency. Makes it easier to observe now imo.

Bitcoin indexsDisplays average high and low, of the combined exchanges: Binance, Bittrex, Poloniex, Bitfinex, Bitmex, so that you can see arbitrage, and smooth out differences of exchanges for more realistic charting.

Bitcoin Futures Expiry/Settlement DatesVersion 0.9 beta:

- Takes heavy performance showing history expiry dates

Bitcoin Exchanges Premiumshows premiums for various bitcoin prices vs bitfinex. not for other cryptos or stocks.

Bitcoin Exchanges PremiumShows premium for international and futures for bitcoin only. Does not with with other charts. Bitcoin Only.

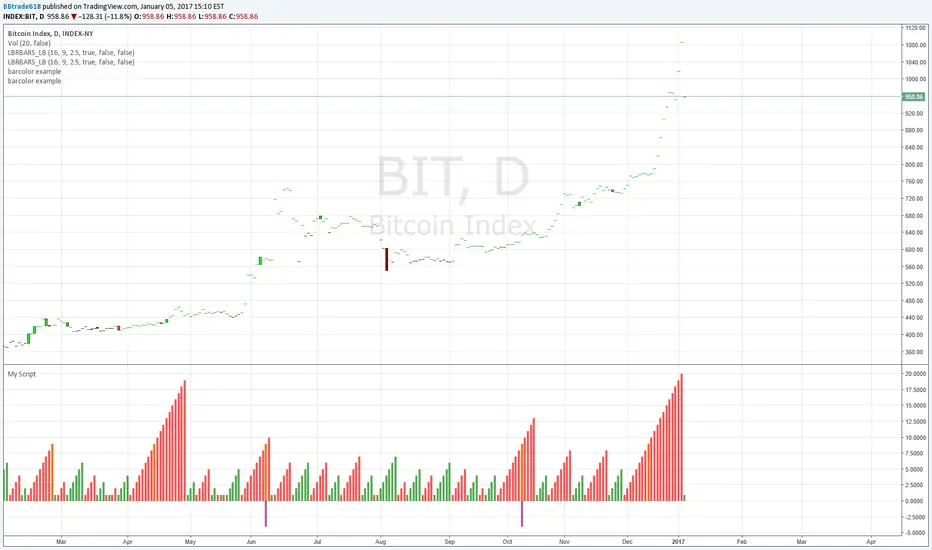

Bitcoin EOD short in Basic Price Action scriptCrash in Bitcoin Index

high to low -22% on bit/usd pair

With a recorded end of day of 20 short value, this was a massive short power building on daily and also weekly timeframe.

If you had zoomedin at lower timeframes you would have seen this crash!

Best to your trading!

Feel free to study more inspirations at our facebook page: www.facebook.com

See also my script page for an explenation of this script.

Bitcoin SpreadIt selects the min/max price for btc/usd from a set of exchanges and shows them on the chart. It is possible to add or remove exchanges by editing the source code

BTCCNY premiums over BTCUSD - yuan devaluationBitcoin as an alternative to capital outflows, with a market cap of just 2 billion can easily be up by multiples from the outflow of yuan from mainland China alone.

People simply do not want yuan if their purchasing power is going down over time.

Current methods of taking capital off mainland China via overseas cash withdrawals are quickly being closed out by the communist government.

------------------------------------------------------------

www.zerohedge.com

China has capped the amount of money Chinese holders of bank and credit cards can withdraw outside the country, in its latest effort to discourage people from moving badly needed capital offshore.

China’s foreign-exchange regulator put a new annual cap on overseas cash withdrawals using China UnionPay Co. bank cards, a UnionPay official said on Tuesday. Under the new rules, UnionPay cardholders can withdraw up to 50,000 yuan ($7,854) overseas during the last three months of this year, and the amount will be capped at 100,000 yuan for all of next year, the official said.

State-run UnionPay has a virtual monopoly on processing card transactions in China, meaning the limits extend to nearly all Chinese bank- and credit-card holders. It wasn’t clear when the new cap was issued.

The new cap is in addition to an existing 10,000 yuan daily withdrawal limit, part of China’s curbs on how much money can flow across its borders.

The move by China’s State Administration of Foreign Exchange is the latest by Beijing to scrutinize capital outflows.

The People’s Bank of China, the country’s central bank, said earlier this month that its foreign-exchange reserves fell by $93.9 billion, the biggest monthly drop ever, after it surprised the market on Aug. 11 with its decision to devalue the yuan by around 2%.

Key takeaway from the yuan devaluation and capital control:

The collapse of 2 bubbles: housing and stock market.

Weakness in commodities such as steel, copper and oil are seen which signals a weakening economy of which China are the core driver of that expansion since 2008. I suspect that China's GDP is never 8% as it is reported, but rather near 2~4% right now.

China have spent over 100 billion USD in US treasury proceeds to stabilize the yuan collapsing faster due to speculators. The amount of reserves spent at the current rate is unsustainable, it will take just 2 years for them to be used up completely.

Over time yuan will still be heading downwards.

Volume Weighted Market Mean 3.0 [Dia]150924 - v3.0

This script is a complete rewrite of the previous version here .

It gathers market data from up to 8 different Bitcoin exchange pairs (8 is maximum due to script limitations).The influence of each single exchange can be customized individually, default is 50% for 0-fee exchanges, 10% for futures and 100% for all others. For each single exchange a standard deviation from the composite mean price and a average price range are determined. To make data from exchanges with different liquidity comparable, all single exchange price ranges are normalized to the range of the composite mean price. To make data from exchanges with different fee structure (= exchanges that constantly trade at a premium / discount) comparable, all single exchange prices are corrected by their respective standard deviations. To account for trade volume, all price data is weighted by the current candles volume.

- optional Heikin Ashi candle display

- optional EMAs

- lots of switches to play around with ;-)

BTC Volume Index 1.1 beta [Dia]Indicator calculates total volume across multiple bitcoin exchanges. The influence of each exchange can be adjusted seperately.

0 fee exchanges default to 50%

0 fee futures default to 10%

Define custom lookback periods for price breakout detection.

Look for low-volume price reversals in those candles immediately following high volume peaks. The lower the volume and the greater the open/close price difference of that 2nd candle is compared to the previous one, the higher the likelihood of a local top/bottom being in.

Note:

Bar highlighting is still experimental, future versions will include better filtering options.

Use for confirmation only, not as standalone trading system.

Multi-exchange OBV V2.0This Script takes the average On Balance Volume of 4 bitcoin exchanges.

Bitfinex:BTCUSD

Okcoin:BTCUSD

BTCE:BTCUSD

HUOBI:BTCCNY

KK_Traders Dynamic Index_Bar HighlightingHey guys,

this is one of my favorite scripts as it represents a whole trading system that has given me very good results!

I have only used it on Bitcoin so far but I am sure it will also work for other instruments.

The original code to this was created by LazyBear, so all props to him for this great script!

I have linked his original post down below.

You can find the full rules to the system in this PDF (which has also been taken from LBs post):

www.forexmt4.com

Here is a short summary of the rules:

Go long when (all conditions have to be met):

The green line is above 50

The green line is above the red line

The green line is above the orange line

The close is above the upper Band of the Price Action Channel

The candles close is above its open

(The green line is below 68)

Go short when (all conditions have to be met):

The green line is below 50

The green line is below the red line

The green line is below the orange line

The close is below the lower band of the Price Action Channel

The candles close is below its open

(The green line is above 32)

Close when:

Any of these conditions aren't true anymore.

I have marked two of the rules in brackets as they seem to cut out a lot of the profits this system generates. You can choose to still use these rules by checking the box that says "Use Original Ruleset" in the options.

The system also contains rules regarding the Heiken Ashi bars. However these aren't as specific as the other rules. This is where your personal judgement comes in and this part is hard to explain. Take a look at the PDF I have linked to get a better understanding.

So far, this is just the TDI trading system and LBs script, now what have I changed?

I have incorporated the Price Action Channel to the system and changed it so that it highlights the bars whenever the system is giving a signal. As long as the bars are green the system is giving a long signal, as long as they are red the system is giving a short signal. Keep in mind that this doesn't consider the bar size of the HA bars. I recommend coloring all bars grey via the chart settings in order to be able to see the bar highlighting properly.

I have also published the Price Action Channel seperately in case some of you wish to view the Channel.

I am fairly new to creating scripts so use it with caution and let me know what you think!

LBs original post:

The seperate Price Action Channel script:

BITCOIN KILL ZONES v2Kill Zones

Kill zones are really liquidity events. Many different market participants often come together and act around these events. The activity itself may be event driven (margin calls or options exercise related activity), portfolio management driven (buy-on-close and asset allocation rebalancing orders) or institutionally driven (larger players needing liquidity to get filled in size) or a combination of any/all three. The point is, this intense cross current of activity at a very specific point in time often occurs near significant technical levels and trends established coming out of these events often persist until the next Kill Zone in approached/entered.

Specifically, there are three Kill Zones and each has its own importance/significance.

1. Asian Kill Zone (1900 - 2300 EST) Considered the "institutional" zone, this zone represents both the launch pad for new trends and also too a reloading area from the post American session. It is the start of a new day (or week) for the world and as such it makes sense this zone will often set the tone for the rest of the world's trading day. Since it is very wide (4 hours) one should pay attention to the Tokyo open (2100 EST) the Beijing open (2120 EST) and the Sydney open (0650 EST previous day).

2. London Kill Zone (0200 - 0400 EST) Considered the center of the financial universe for more than 500 years, Europe still carries a lot of influence within the banking world. Many larger players use the Euro session to establish their positions. As such, the London open often sees the most significant trend establishment activity through any given trading day. Indeed, it has been suggested 80% of all weekly trends are established through Tuesday's London Kill Zone.

3. New York Kill Zone (0830 - 1030 EST) The United States is still by far the world's largest economy and so by default New York's open carries a lot of weight and often comes with a big injection of liquidity. Indeed, most of the world's trade-able assets are priced in US dollars which gives even more significance to political and economic activity within this region. Because it comes relatively late in the globe's trading day, this Kill Zone often sees violent price swings within it's first hour leading to the time tested adage "never trust the first hour of North American trading.

Additional notes:

It has become apparent these Kill Zones are evolving over time and the course of world history. Since the end of the second world war, New York has slowly encroached on London's place as the global center for commercial banking. So much so through the later part of the 20th century New York was considered indeed, the new center of the financial universe. With the end of the cold war that leadership seems to have shifted back toward Europe and away from The United States. Additionally, Japan has slowly lost its former predominance within the global economic landscape while Beijing's has risen dramatically.

Only time will tell how these kill zones will evolve given each region's ever changing political, economic and socioeconomic influences.

Trading Notes:

If you have specific levels of interest odds are the bigger players have the same levels too. If it is indeed a solid level, look for price to trade to your level through the kill zone because the zone is a liquidity event where the bigger players can find enough size to get their big orders filled.

Try to avoid taking positions heading into Kill Zones and look for confirmation of your levels coming out of the event. For the more advanced trader, look to take positions on those level hits through the zone but understand higher time frame players often have far deeper pockets then day traders and can endure far more volatility then us little guys.

Thanks for the contribution to @CRInvestor and @ICT_MHuddleston

BAERMThe Bitcoin Auto-correlation Exchange Rate Model: A Novel Two Step Approach

THIS IS NOT FINANCIAL ADVICE. THIS ARTICLE IS FOR EDUCATIONAL AND ENTERTAINMENT PURPOSES ONLY.

If you enjoy this software and information, please consider contributing to my lightning address

Prelude

It has been previously established that the Bitcoin daily USD exchange rate series is extremely auto-correlated

In this article, we will utilise this fact to build a model for Bitcoin/USD exchange rate. But not a model for predicting the exchange rate, but rather a model to understand the fundamental reasons for the Bitcoin to have this exchange rate to begin with.

This is a model of sound money, scarcity and subjective value.

Introduction

Bitcoin, a decentralised peer to peer digital value exchange network, has experienced significant exchange rate fluctuations since its inception in 2009. In this article, we explore a two-step model that reasonably accurately captures both the fundamental drivers of Bitcoin’s value and the cyclical patterns of bull and bear markets. This model, whilst it can produce forecasts, is meant more of a way of understanding past exchange rate changes and understanding the fundamental values driving the ever increasing exchange rate. The forecasts from the model are to be considered inconclusive and speculative only.

Data preparation

To develop the BAERM, we used historical Bitcoin data from Coin Metrics, a leading provider of Bitcoin market data. The dataset includes daily USD exchange rates, block counts, and other relevant information. We pre-processed the data by performing the following steps:

Fixing date formats and setting the dataset’s time index

Generating cumulative sums for blocks and halving periods

Calculating daily rewards and total supply

Computing the log-transformed price

Step 1: Building the Base Model

To build the base model, we analysed data from the first two epochs (time periods between Bitcoin mining reward halvings) and regressed the logarithm of Bitcoin’s exchange rate on the mining reward and epoch. This base model captures the fundamental relationship between Bitcoin’s exchange rate, mining reward, and halving epoch.

where Yt represents the exchange rate at day t, Epochk is the kth epoch (for that t), and epsilont is the error term. The coefficients beta0, beta1, and beta2 are estimated using ordinary least squares regression.

Base Model Regression

We use ordinary least squares regression to estimate the coefficients for the betas in figure 2. In order to reduce the possibility of over-fitting and ensure there is sufficient out of sample for testing accuracy, the base model is only trained on the first two epochs. You will notice in the code we calculate the beta2 variable prior and call it “phaseplus”.

The code below shows the regression for the base model coefficients:

\# Run the regression

mask = df\ < 2 # we only want to use Epoch's 0 and 1 to estimate the coefficients for the base model

reg\_X = df.loc\ [mask, \ \].shift(1).iloc\

reg\_y = df.loc\ .iloc\

reg\_X = sm.add\_constant(reg\_X)

ols = sm.OLS(reg\_y, reg\_X).fit()

coefs = ols.params.values

print(coefs)

The result of this regression gives us the coefficients for the betas of the base model:

\

or in more human readable form: 0.029, 0.996869586, -0.00043. NB that for the auto-correlation/momentum beta, we did NOT round the significant figures at all. Since the momentum is so important in this model, we must use all available significant figures.

Fundamental Insights from the Base Model

Momentum effect: The term 0.997 Y suggests that the exchange rate of Bitcoin on a given day (Yi) is heavily influenced by the exchange rate on the previous day. This indicates a momentum effect, where the price of Bitcoin tends to follow its recent trend.

Momentum effect is a phenomenon observed in various financial markets, including stocks and other commodities. It implies that an asset’s price is more likely to continue moving in its current direction, either upwards or downwards, over the short term.

The momentum effect can be driven by several factors:

Behavioural biases: Investors may exhibit herding behaviour or be subject to cognitive biases such as confirmation bias, which could lead them to buy or sell assets based on recent trends, reinforcing the momentum.

Positive feedback loops: As more investors notice a trend and act on it, the trend may gain even more traction, leading to a self-reinforcing positive feedback loop. This can cause prices to continue moving in the same direction, further amplifying the momentum effect.

Technical analysis: Many traders use technical analysis to make investment decisions, which often involves studying historical exchange rate trends and chart patterns to predict future exchange rate movements. When a large number of traders follow similar strategies, their collective actions can create and reinforce exchange rate momentum.

Impact of halving events: In the Bitcoin network, new bitcoins are created as a reward to miners for validating transactions and adding new blocks to the blockchain. This reward is called the block reward, and it is halved approximately every four years, or every 210,000 blocks. This event is known as a halving.

The primary purpose of halving events is to control the supply of new bitcoins entering the market, ultimately leading to a capped supply of 21 million bitcoins. As the block reward decreases, the rate at which new bitcoins are created slows down, and this can have significant implications for the price of Bitcoin.

The term -0.0004*(50/(2^epochk) — (epochk+1)²) accounts for the impact of the halving events on the Bitcoin exchange rate. The model seems to suggest that the exchange rate of Bitcoin is influenced by a function of the number of halving events that have occurred.

Exponential decay and the decreasing impact of the halvings: The first part of this term, 50/(2^epochk), indicates that the impact of each subsequent halving event decays exponentially, implying that the influence of halving events on the Bitcoin exchange rate diminishes over time. This might be due to the decreasing marginal effect of each halving event on the overall Bitcoin supply as the block reward gets smaller and smaller.

This is antithetical to the wrong and popular stock to flow model, which suggests the opposite. Given the accuracy of the BAERM, this is yet another reason to question the S2F model, from a fundamental perspective.

The second part of the term, (epochk+1)², introduces a non-linear relationship between the halving events and the exchange rate. This non-linear aspect could reflect that the impact of halving events is not constant over time and may be influenced by various factors such as market dynamics, speculation, and changing market conditions.

The combination of these two terms is expressed by the graph of the model line (see figure 3), where it can be seen the step from each halving is decaying, and the step up from each halving event is given by a parabolic curve.

NB - The base model has been trained on the first two halving epochs and then seeded (i.e. the first lag point) with the oldest data available.

Constant term: The constant term 0.03 in the equation represents an inherent baseline level of growth in the Bitcoin exchange rate.

In any linear or linear-like model, the constant term, also known as the intercept or bias, represents the value of the dependent variable (in this case, the log-scaled Bitcoin USD exchange rate) when all the independent variables are set to zero.

The constant term indicates that even without considering the effects of the previous day’s exchange rate or halving events, there is a baseline growth in the exchange rate of Bitcoin. This baseline growth could be due to factors such as the network’s overall growth or increasing adoption, or changes in the market structure (more exchanges, changes to the regulatory environment, improved liquidity, more fiat on-ramps etc).

Base Model Regression Diagnostics

Below is a summary of the model generated by the OLS function

OLS Regression Results

\==============================================================================

Dep. Variable: logprice R-squared: 0.999

Model: OLS Adj. R-squared: 0.999

Method: Least Squares F-statistic: 2.041e+06

Date: Fri, 28 Apr 2023 Prob (F-statistic): 0.00

Time: 11:06:58 Log-Likelihood: 3001.6

No. Observations: 2182 AIC: -5997.

Df Residuals: 2179 BIC: -5980.

Df Model: 2

Covariance Type: nonrobust

\==============================================================================

coef std err t P>|t| \

\------------------------------------------------------------------------------

const 0.0292 0.009 3.081 0.002 0.011 0.048

logprice 0.9969 0.001 1012.724 0.000 0.995 0.999

phaseplus -0.0004 0.000 -2.239 0.025 -0.001 -5.3e-05

\==============================================================================

Omnibus: 674.771 Durbin-Watson: 1.901

Prob(Omnibus): 0.000 Jarque-Bera (JB): 24937.353

Skew: -0.765 Prob(JB): 0.00

Kurtosis: 19.491 Cond. No. 255.

\==============================================================================

Below we see some regression diagnostics along with the regression itself.

Diagnostics: We can see that the residuals are looking a little skewed and there is some heteroskedasticity within the residuals. The coefficient of determination, or r2 is very high, but that is to be expected given the momentum term. A better r2 is manually calculated by the sum square of the difference of the model to the untrained data. This can be achieved by the following code:

\# Calculate the out-of-sample R-squared

oos\_mask = df\ >= 2

oos\_actual = df.loc\

oos\_predicted = df.loc\

residuals\_oos = oos\_actual - oos\_predicted

SSR = np.sum(residuals\_oos \*\* 2)

SST = np.sum((oos\_actual - oos\_actual.mean()) \*\* 2)

R2\_oos = 1 - SSR/SST

print("Out-of-sample R-squared:", R2\_oos)

The result is: 0.84, which indicates a very close fit to the out of sample data for the base model, which goes some way to proving our fundamental assumption around subjective value and sound money to be accurate.

Step 2: Adding the Damping Function

Next, we incorporated a damping function to capture the cyclical nature of bull and bear markets. The optimal parameters for the damping function were determined by regressing on the residuals from the base model. The damping function enhances the model’s ability to identify and predict bull and bear cycles in the Bitcoin market. The addition of the damping function to the base model is expressed as the full model equation.

This brings me to the question — why? Why add the damping function to the base model, which is arguably already performing extremely well out of sample and providing valuable insights into the exchange rate movements of Bitcoin.

Fundamental reasoning behind the addition of a damping function:

Subjective Theory of Value: The cyclical component of the damping function, represented by the cosine function, can be thought of as capturing the periodic fluctuations in market sentiment. These fluctuations may arise from various factors, such as changes in investor risk appetite, macroeconomic conditions, or technological advancements. Mathematically, the cyclical component represents the frequency of these fluctuations, while the phase shift (α and β) allows for adjustments in the alignment of these cycles with historical data. This flexibility enables the damping function to account for the heterogeneity in market participants’ preferences and expectations, which is a key aspect of the subjective theory of value.

Time Preference and Market Cycles: The exponential decay component of the damping function, represented by the term e^(-0.0004t), can be linked to the concept of time preference and its impact on market dynamics. In financial markets, the discounting of future cash flows is a common practice, reflecting the time value of money and the inherent uncertainty of future events. The exponential decay in the damping function serves a similar purpose, diminishing the influence of past market cycles as time progresses. This decay term introduces a time-dependent weight to the cyclical component, capturing the dynamic nature of the Bitcoin market and the changing relevance of past events.

Interactions between Cyclical and Exponential Decay Components: The interplay between the cyclical and exponential decay components in the damping function captures the complex dynamics of the Bitcoin market. The damping function effectively models the attenuation of past cycles while also accounting for their periodic nature. This allows the model to adapt to changing market conditions and to provide accurate predictions even in the face of significant volatility or structural shifts.

Now we have the fundamental reasoning for the addition of the function, we can explore the actual implementation and look to other analogies for guidance —

Financial and physical analogies to the damping function:

Mathematical Aspects: The exponential decay component, e^(-0.0004t), attenuates the amplitude of the cyclical component over time. This attenuation factor is crucial in modelling the diminishing influence of past market cycles. The cyclical component, represented by the cosine function, accounts for the periodic nature of market cycles, with α determining the frequency of these cycles and β representing the phase shift. The constant term (+3) ensures that the function remains positive, which is important for practical applications, as the damping function is added to the rest of the model to obtain the final predictions.

Analogies to Existing Damping Functions: The damping function in the BAERM is similar to damped harmonic oscillators found in physics. In a damped harmonic oscillator, an object in motion experiences a restoring force proportional to its displacement from equilibrium and a damping force proportional to its velocity. The equation of motion for a damped harmonic oscillator is:

x’’(t) + 2γx’(t) + ω₀²x(t) = 0

where x(t) is the displacement, ω₀ is the natural frequency, and γ is the damping coefficient. The damping function in the BAERM shares similarities with the solution to this equation, which is typically a product of an exponential decay term and a sinusoidal term. The exponential decay term in the BAERM captures the attenuation of past market cycles, while the cosine term represents the periodic nature of these cycles.

Comparisons with Financial Models: In finance, damped oscillatory models have been applied to model interest rates, stock prices, and exchange rates. The famous Black-Scholes option pricing model, for instance, assumes that stock prices follow a geometric Brownian motion, which can exhibit oscillatory behavior under certain conditions. In fixed income markets, the Cox-Ingersoll-Ross (CIR) model for interest rates also incorporates mean reversion and stochastic volatility, leading to damped oscillatory dynamics.

By drawing on these analogies, we can better understand the technical aspects of the damping function in the BAERM and appreciate its effectiveness in modelling the complex dynamics of the Bitcoin market. The damping function captures both the periodic nature of market cycles and the attenuation of past events’ influence.

Conclusion

In this article, we explored the Bitcoin Auto-correlation Exchange Rate Model (BAERM), a novel 2-step linear regression model for understanding the Bitcoin USD exchange rate. We discussed the model’s components, their interpretations, and the fundamental insights they provide about Bitcoin exchange rate dynamics.

The BAERM’s ability to capture the fundamental properties of Bitcoin is particularly interesting. The framework underlying the model emphasises the importance of individuals’ subjective valuations and preferences in determining prices. The momentum term, which accounts for auto-correlation, is a testament to this idea, as it shows that historical price trends influence market participants’ expectations and valuations. This observation is consistent with the notion that the price of Bitcoin is determined by individuals’ preferences based on past information.

Furthermore, the BAERM incorporates the impact of Bitcoin’s supply dynamics on its price through the halving epoch terms. By acknowledging the significance of supply-side factors, the model reflects the principles of sound money. A limited supply of money, such as that of Bitcoin, maintains its value and purchasing power over time. The halving events, which reduce the block reward, play a crucial role in making Bitcoin increasingly scarce, thus reinforcing its attractiveness as a store of value and a medium of exchange.

The constant term in the model serves as the baseline for the model’s predictions and can be interpreted as an inherent value attributed to Bitcoin. This value emphasizes the significance of the underlying technology, network effects, and Bitcoin’s role as a medium of exchange, store of value, and unit of account. These aspects are all essential for a sound form of money, and the model’s ability to account for them further showcases its strength in capturing the fundamental properties of Bitcoin.

The BAERM offers a potential robust and well-founded methodology for understanding the Bitcoin USD exchange rate, taking into account the key factors that drive it from both supply and demand perspectives.

In conclusion, the Bitcoin Auto-correlation Exchange Rate Model provides a comprehensive fundamentally grounded and hopefully useful framework for understanding the Bitcoin USD exchange rate.

BTC Arcturus IndicatorBTC Arcturus Indicator: This indicator is designed to create buy and sell signals based on the market value of Bitcoin. It also predicts potential market tops with the Pi Cycle Top indicator.

How Does It Work?

1. MVRVZ (Market Value to Realized Value-Z Score) Calculation:

MC: Bitcoin's market cap (Market Cap) is pulled daily from Glassnode data.

MCR: Realized Market Cap of Bitcoin is taken daily from Coinmetrics data.

MVRVZ: It is calculated by dividing the difference between Bitcoin's market value and realized market value by one standard deviation. This value indicates whether the market is overvalued or undervalued.

2. Reception and Warning Signals:

Buy Signal: When MVRVZ falls below the -0.255 threshold value, the indicator gives a "Buy" signal. This indicates that Bitcoin is undervalued and may be a buying opportunity.

Warning Signal: A warning signal turns on when MVRVZ exceeds the threshold value of 2.765. This indicates that the market is approaching saturation and caution is warranted.

3. Tracking the Highest MVRVZ Value:

The indicator records the highest MVRVZ value in the last 10 candlesticks. This value is used to determine whether the market has reached its highest risk levels.

4. Warning Display:

If the MVRVZ value matches the highest value in the last 10 bars and this warning has not been displayed before, a "Warning" signal is displayed.

Once the warning signal is shown, no further warnings are shown for 10 candles.

5. Pi Cycle Top Indicator:

Pi Cycle Top: This indicator predicts Bitcoin tops by comparing two moving averages (350-day and 111-day). If the short-term moving average falls below the long-term moving average, this is considered a sell signal.

The indicator displays this signal with the label "Sell", indicating a potential market top.

User Guide:

Green Buy Signal: It means Bitcoin is cheap and offers a buying opportunity.

Yellow Warning Signal: Indicates that Bitcoin has reached possible profit taking points and caution should be exercised.

Red Sell Signal: Indicates that Bitcoin has reached market saturation and it may be appropriate to sell.

WAGMI LAB Trend Reversal Indicator HMA-Kahlman (m15)WAGMI HMA-Kahlman Trend Reversal Indicator

This indicator combines the Hull Moving Average (HMA) with the Kahlman filter to provide a dynamic trend reversal signal, perfect for volatile assets like Bitcoin. The strategy works particularly well on lower timeframes, making it ideal for intraday trading and fast-moving markets.

Key Features:

Trend Detection: It uses a blend of HMA and Kahlman filters to detect trend reversals, providing more accurate and timely signals.

Volatility Adaptability: Designed with volatile assets like Bitcoin in mind, this indicator adapts to rapid price movements, offering smoother trend detection during high volatility.

Easy Visualization: Buy (B) and Sell (S) signals are clearly marked with labels, helping traders spot trend shifts quickly and accurately.

Trendlines Module: The indicator plots trendlines based on pivot points, highlighting important support and resistance levels. This helps traders understand the market structure and identify potential breakout or breakdown zones.

Customizable: Adjust the HMA and Kahlman parameters to fit different assets or trading styles, making it flexible for various market conditions.

Usage Tips:

Best Timeframes: The indicator performs exceptionally well on lower timeframes (such as 15-minute to 1-hour charts), making it ideal for scalping and short-term trading strategies.

Ideal for Volatile Assets: This strategy is perfect for highly volatile assets like Bitcoin, but can also be applied to other cryptocurrencies and traditional markets with high price fluctuations.

Signal Confirmation: Use the trend signals (green for uptrend, red for downtrend) along with the buy/sell labels to help you confirm potential entries and exits. It's also recommended to combine the signals with other technical tools like volume analysis or RSI for enhanced confirmation.

Trendline Analysis: The plotted trendlines provide additional visual context to identify key market zones, supporting your trading decisions with a clear view of ongoing trends and possible reversal areas.

Risk Management: As with any strategy, always consider proper risk management techniques, such as stop-loss and take-profit levels, to protect against unforeseen market moves.

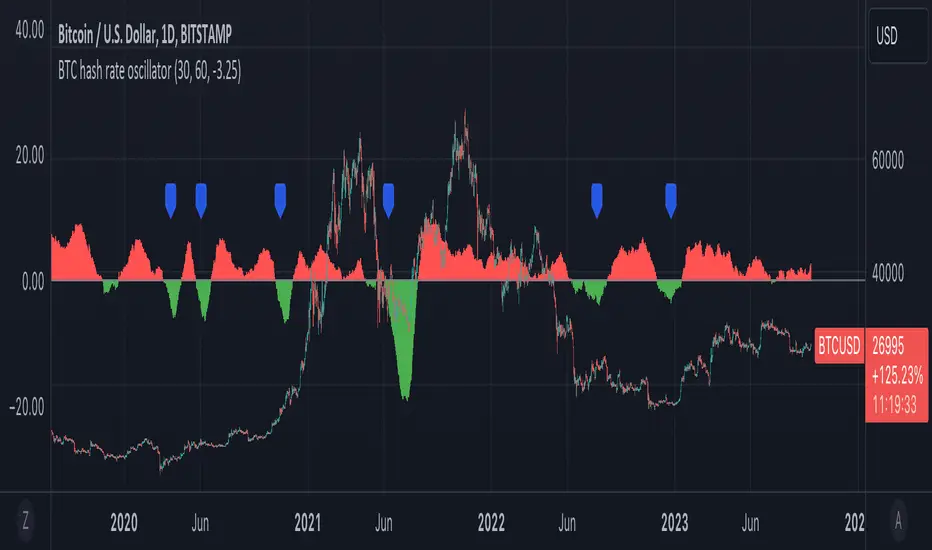

BTC hash rate oscillatorOVERVIEW:

This script looks to identify entry point opportunities when moving averages over Bitcoin's hash rate are indicative of Miner capitulation. The script implements an oscillator based on Charles Capriole's "Hash Ribbons & Bitcoin Bottoms" concept. It analyses the short-term and long-term moving averages of Bitcoin's hash rate and then identifies potential entry opportunities from this.

KEY FEATURES:

Signal Generation: The script identifies entry points when the short-term moving average crosses under the long-term moving average and the rate of change falls below a specified threshold. These conditions suggest potential trading opportunities.

Historical Signals: Optionally the script displays historical signals, indicating past instances where hash rate conditions suggested favourable entry points. Users can also assess the script's historical performance.

USAGE:

The generated opportunities can be used as potential entry points for BTC. The script provides visual cues on the chart (blue labels above the miner capitulation zones) for identification of signals. Customisable moving average lengths and threshold values are supported, which allow adaptation to various strategies.

CONSIDERATIONS:

Validation: It's recommended that careful backtesting over historical data be done before acting on any identified opportunities.

User Discretion: Trading decisions should not rely solely on this script. Users should exercise their judgment and consider market conditions.

Note: This script identifies opportunities based on historical data and should be used with caution, as past performance is not indicative of future results.

RSI Season Tracker by KrisWatersSeason tracker identifies the momentum with tracking dominance and market capitalization data of Bitcoin , Altcoin and USDT .

With this indicator you can able to get know about Bitcoin, Altcoin and USDT dominance and market capitalization easily.

Backgrond Color Definations:

If the background color of indicator is ORANGE means that Bitcoin dominance is the most powerful. It is a good sign for Bitcoin.

If the background color of indicator is BLUE means that Altcoin dominance is the most powerful. It is a good sign for Altcoins.

If the background color of indicator is GREEN means that USDT dominance is the most powerful. It is a good sign for USDT.

Plus Sign (+) Meaning and Color Definations:

If ORANGE plus sign is visible on indicator means that market capitalization of Bitcoin is increasing. It is a good sign for Bitcoin.

If BLUE plus sign is visible on indicator means that market capitalization of Altcoin is increasing. It is a good sign for Altcoins.

If GREEN plus sign is visible on indicator means that market capitalization of Bitcoin and Altcoins are decreasing. It is not a good sign for both.

Light and Dark RSI Line Color Definations:

If the line of Bitcoin color is Orange means that, RSI value was increased compared with previous bar. It is one of the good sign of the momentum strength.

If the line of Bitcoin color is Yellow means that, RSI value was decreased compared with previous bar. It is not a good sign.

If the line of Altcoin color is Navy means that, RSI value was increased compared with previous bar. It is one of the good sign of the momentum strength.

If the line of Altcoin color is Blue means that, RSI value was decreased compared with previous bar. It is not a good sign.

If the line of USDT color is Green means that, RSI value was increased compared with previous bar. It is one of good the sign of the momentum strength.

If the line of USDT color is Lime means that, RSI value was decreased compared with previous bar. It is not a good sign.

Simple RSI rules are valid for this indicator.

RSI value is under 30 indicates that asset is OVERSOLD .

RSI value is upper 70 indicates that asset is OVERBOUGHT .

Important Notice: Dominance data is not correlated with price. For example; sometimes dominance is increasing but the price is not. And that's where the market capitalization comes in.

If the plus sign is not visible , you can get questioning for the movement. It is not a good sign at all.

If the plus sign is visible and RSI is increasing , It is a good sign for the strength of assets movement.

I recommended to use on DAILY timeframe . But you can use different timeframes as well.

Please leave comment below If you have any question or development idea.