PowerHouse SwiftEdge AI v2.10 StrategyOverview

The PowerHouse SwiftEdge AI v2.10 Strategy is a sophisticated trading system designed to identify high-probability trade setups in forex, stocks, and cryptocurrencies. By combining multi-timeframe trend analysis, momentum signals, volume confirmation, and smart money concepts (Change of Character and Break of Structure ), this strategy offers traders a robust tool to capitalize on market trends while minimizing false signals. The strategy’s unique “AI” component analyzes trends across multiple timeframes to provide a clear, actionable dashboard, making it accessible for both novice and experienced traders. The strategy is fully customizable, allowing users to tailor its filters to their trading style.

What It Does

This strategy generates Buy and Sell signals based on a confluence of technical indicators and smart money concepts. It uses:

Multi-Timeframe Trend Analysis: Confirms the market’s direction by analyzing trends on the 1-hour (60M), 4-hour (240M), and daily (D) timeframes.

Momentum Filter: Ensures trades align with strong price movements to avoid choppy markets.

Volume Filter: Validates signals with above-average volume to confirm market participation.

Breakout Filter: Requires price to break key levels for added confirmation.

Smart Money Signals (CHoCH/BOS): Identifies reversals (CHoCH) and trend continuations (BOS) based on pivot points.

AI Trend Dashboard: Summarizes trend strength, confidence, and predictions across timeframes, helping traders make informed decisions without needing to analyze complex data manually.

The strategy also plots dynamic support and resistance trendlines, take-profit (TP) levels, and “Get Ready” signals to alert users of potential setups before they fully develop. Trades are executed with predefined take-profit and stop-loss levels for disciplined risk management.

How It Works

The strategy integrates multiple components to create a cohesive trading system:

Multi-Timeframe Trend Analysis:

The strategy evaluates trends on three timeframes (1H, 4H, Daily) using Exponential Moving Averages (EMA) and Volume-Weighted Average Price (VWAP). A trend is considered bullish if the price is above both the EMA and VWAP, bearish if below, or neutral otherwise.

Signals are only generated when the trend on the user-selected higher timeframe aligns with the trade direction (e.g., Buy signals require a bullish higher timeframe trend). This reduces noise and ensures trades follow the broader market context.

Momentum Filter:

Measures the percentage price change between consecutive bars and compares it to a volatility-adjusted threshold (based on the Average True Range ). This ensures trades are taken only during significant price movements, filtering out low-momentum conditions.

Volume Filter (Optional):

Checks if the current volume exceeds a long-term average and shows positive short-term volume change. This confirms strong market participation, reducing the risk of false breakouts.

Breakout Filter (Optional):

Requires the price to break above (for Buy) or below (for Sell) recent highs/lows, ensuring the signal aligns with a structural shift in the market.

Smart Money Concepts (CHoCH/BOS):

Change of Character (CHoCH): Detects potential reversals when the price crosses under a recent pivot high (for Sell) or over a recent pivot low (for Buy) with a bearish or bullish candle, respectively.

Break of Structure (BOS): Confirms trend continuations when the price breaks below a recent pivot low (for Sell) or above a recent pivot high (for Buy) with strong momentum.

These signals are plotted as horizontal lines with labels, making it easy to visualize key levels.

AI Trend Dashboard:

Combines trend direction, momentum, and volatility (ATR) across timeframes to calculate a trend score. Scores above 0.5 indicate an “Up” trend, below -0.5 indicate a “Down” trend, and otherwise “Neutral.”

Displays a table summarizing trend strength (as a percentage), AI confidence (based on trend alignment), and Cumulative Volume Delta (CVD) for market context.

A second table (optional) shows trend predictions for 1H, 4H, and Daily timeframes, helping traders anticipate future market direction.

Dynamic Trendlines:

Plots support and resistance lines based on recent swing lows and highs within user-defined periods (shortTrendPeriod, longTrendPeriod). These lines adapt to market conditions and are colored based on trend strength.

Why This Combination?

The PowerHouse SwiftEdge AI v2.10 Strategy is original because it seamlessly integrates traditional technical analysis (EMA, VWAP, ATR, volume) with smart money concepts (CHoCH, BOS) and a proprietary AI-driven trend analysis. Unlike standalone indicators, this strategy:

Reduces False Signals: By requiring confluence across trend, momentum, volume, and breakout filters, it minimizes trades in choppy or low-conviction markets.

Adapts to Market Context: The ATR-based momentum threshold adjusts dynamically to volatility, ensuring signals remain relevant in both trending and ranging markets.

Simplifies Decision-Making: The AI dashboard distills complex multi-timeframe data into a user-friendly table, eliminating the need for manual analysis.

Leverages Smart Money: CHoCH and BOS signals capture institutional price action patterns, giving traders an edge in identifying reversals and continuations.

The combination of these components creates a balanced system that aligns short-term trade entries with longer-term market trends, offering a unique blend of precision, adaptability, and clarity.

How to Use

Add to Chart:

Apply the strategy to your TradingView chart on a liquid symbol (e.g., EURUSD, BTCUSD, AAPL) with a timeframe of 60 minutes or lower (e.g., 15M, 60M).

Configure Inputs:

Pivot Length: Adjust the number of bars (default: 5) to detect pivot highs/lows for CHoCH/BOS signals. Higher values reduce noise but may delay signals.

Momentum Threshold: Set the base percentage (default: 0.01%) for momentum confirmation. Increase for stricter signals.

Take Profit/Stop Loss: Define TP and SL in points (default: 10 each) for risk management.

Higher/Lower Timeframe: Choose timeframes (60M, 240M, D) for trend filtering. Ensure the chart timeframe is lower than or equal to the higher timeframe.

Filters: Enable/disable momentum, volume, or breakout filters to suit your trading style.

Trend Periods: Set shortTrendPeriod (default: 30) and longTrendPeriod (default: 100) for trendline plotting. Keep below 2000 to avoid buffer errors.

AI Dashboard: Toggle Enable AI Market Analysis to show/hide the prediction table and adjust its position.

Interpret Signals:

Buy/Sell Labels: Green "Buy" or red "Sell" labels indicate trade entries with predefined TP/SL levels plotted.

Get Ready Signals: Yellow "Get Ready BUY" or orange "Get Ready SELL" labels warn of potential setups.

CHoCH/BOS Lines: Aqua (CHoCH Sell), lime (CHoCH Buy), fuchsia (BOS Sell), or teal (BOS Buy) lines mark key levels.

Trendlines: Green/lime (support) or fuchsia/purple (resistance) dashed lines show dynamic support/resistance.

AI Dashboard: Check the top-right table for trend strength, confidence, and CVD. The optional bottom table shows trend predictions (Up, Down, Neutral).

Backtest and Trade:

Use TradingView’s Strategy Tester to evaluate performance. Adjust TP/SL and filters based on results.

Trade manually based on signals or automate with TradingView alerts (set alerts for Buy/Sell labels).

Originality and Value

The PowerHouse SwiftEdge AI v2.10 Strategy stands out by combining multi-timeframe analysis, smart money concepts, and an AI-driven dashboard into a single, user-friendly system. Its adaptive momentum threshold, robust filtering, and clear visualizations empower traders to make confident decisions without needing advanced technical knowledge. Whether you’re a day trader or swing trader, this strategy provides a versatile, data-driven approach to navigating dynamic markets.

Important Notes:

Risk Management: Always use appropriate position sizing and risk management, as the strategy’s TP/SL levels are customizable.

Symbol Compatibility: Test on liquid symbols with sufficient historical data (at least 2000 bars) to avoid buffer errors.

Performance: Backtest thoroughly to optimize settings for your market and timeframe.

Pesquisar nos scripts por "bear"

Dskyz (DAFE) Quantum Sentiment Flux - Beginners Dskyz (DAFE) Quantum Sentiment Flux - Beginners:

Welcome to the Dskyz (DAFE) Quantum Sentiment Flux - Beginners , a strategy and concept that’s your ultimate wingman for trading futures like MNQ, NQ, MES, and ES. This gem combines lightning-fast momentum signals, market sentiment smarts, and bulletproof risk management into a system so intuitive, even newbies can trade like pros. With clean DAFE visuals, preset modes for every vibe, and a revamped dashboard that’s basically a market GPS, this strategy makes futures trading feel like a high-octane sci-fi mission.

Built on the Dskyz (DAFE) legacy of Aurora Divergence, the Quantum Sentiment Flux is designed to empower beginners while giving seasoned traders a lean, sentiment-driven edge. It uses fast/slow EMA crossovers for entries, filters trades with VIX, SPX trends, and sector breadth, and keeps your account safe with adaptive stops and cooldowns. Tuned for more action with faster signals and a slick bottom-left dashboard, this updated version is ready to light up your charts and outsmart institutional traps. Let’s dive into why this strat’s a must-have and break down its brilliance.

Why Traders Need This Strategy

Futures markets are a wild ride—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional games that can wreck unprepared traders. Beginners often get lost in complex systems or burned by impulsive trades. The Quantum Sentiment Flux is the antidote, offering:

Dead-Simple Setup: Preset modes (Aggressive, Balanced, Conservative) auto-tune signals, risk, and sizing, so you can trade without a quant degree.

Sentiment Superpower: VIX filter, SPX trend, and sector breadth visuals keep you aligned with market health, dodging chop and riding trends.

Ironclad Safety: Tighter ATR-based stops, 2:1 take-profits, and preset cooldowns protect your capital, even in chaotic sessions.

Next-Level Visuals: Green/red entry triangles, vibrant EMAs, a sector breadth background, and a beefed-up dashboard make signals and context pop.

DAFE Swagger: The clean aesthetics, sleek dashboard—ties it to Dskyz’s elite brand, making your charts a work of art.

Traders need this because it’s a plug-and-play system that blends beginner-friendly simplicity with pro-level market awareness. Whether you’re just starting or scalping 5min MNQ, this strat’s your key to trading with confidence and style.

Strategy Components

1. Core Signal Logic (High-Speed Momentum)

The strategy’s engine is a momentum-based system using fast and slow Exponential Moving Averages (EMAs), now tuned for faster, more frequent trades.

How It Works:

Fast/Slow EMAs: Fast EMA (Aggressive: 5, Balanced: 7, Conservative: 9 bars) and slow EMA (12/14/18 bars) track short-term vs. longer-term momentum.

Crossover Signals:

Buy: Fast EMA crosses above slow EMA, and trend_dir = 1 (fast EMA > slow EMA + ATR * strength threshold).

Sell: Fast EMA crosses below slow EMA, and trend_dir = -1 (fast EMA < slow EMA - ATR * strength threshold).

Strength Filter: ma_strength = fast EMA - slow EMA must exceed an ATR-scaled threshold (Aggressive: 0.15, Balanced: 0.18, Conservative: 0.25) for robust signals.

Trend Direction: trend_dir confirms momentum, filtering out weak crossovers in choppy markets.

Evolution:

Faster EMAs (down from 7–10/21–50) catch short-term trends, perfect for active futures markets.

Lower strength thresholds (0.15–0.25 vs. 0.3–0.5) make signals more sensitive, boosting trade frequency without sacrificing quality.

Preset tuning ensures beginners get optimized settings, while pros can tweak via mode selection.

2. Market Sentiment Filters

The strategy leans hard into market sentiment with a VIX filter, SPX trend analysis, and sector breadth visuals, keeping trades aligned with the big picture.

VIX Filter:

Logic: Blocks long entries if VIX > threshold (default: 20, can_long = vix_close < vix_limit). Shorts are always allowed (can_short = true).

Impact: Prevents longs during high-fear markets (e.g., VIX spikes in crashes), while allowing shorts to capitalize on downturns.

SPX Trend Filter:

Logic: Compares S&P 500 (SPX) close to its SMA (Aggressive: 5, Balanced: 8, Conservative: 12 bars). spx_trend = 1 (UP) if close > SMA, -1 (DOWN) if < SMA, 0 (FLAT) if neutral.

Impact: Provides dashboard context, encouraging trades that align with market direction (e.g., longs in UP trend).

Sector Breadth (Visual):

Logic: Tracks 10 sector ETFs (XLK, XLF, XLE, etc.) vs. their SMAs (same lengths as SPX). Each sector scores +1 (bullish), -1 (bearish), or 0 (neutral), summed as breadth (-10 to +10).

Display: Green background if breadth > 4, red if breadth < -4, else neutral. Dashboard shows sector trends (↑/↓/-).

Impact: Faster SMA lengths make breadth more responsive, reflecting sector rotations (e.g., tech surging, energy lagging).

Why It’s Brilliant:

- VIX filter adds pro-level volatility awareness, saving beginners from panic-driven losses.

- SPX and sector breadth give a 360° view of market health, boosting signal confidence (e.g., green BG + buy signal = high-probability trade).

- Shorter SMAs make sentiment visuals react faster, perfect for 5min charts.

3. Risk Management

The risk controls are a fortress, now tighter and more dynamic to support frequent trading while keeping accounts safe.

Preset-Based Risk:

Aggressive: Fast EMAs (5/12), tight stops (1.1x ATR), 1-bar cooldown. High trade frequency, higher risk.

Balanced: EMAs (7/14), 1.2x ATR stops, 1-bar cooldown. Versatile for most traders.

Conservative: EMAs (9/18), 1.3x ATR stops, 2-bar cooldown. Safer, fewer trades.

Impact: Auto-scales risk to match style, making it foolproof for beginners.

Adaptive Stops and Take-Profits:

Logic: Stops = entry ± ATR * atr_mult (1.1–1.3x, down from 1.2–2.0x). Take-profits = entry ± ATR * take_mult (2x stop distance, 2:1 reward/risk). Longs: stop below entry, TP above; shorts: vice versa.

Impact: Tighter stops increase trade turnover while maintaining solid risk/reward, adapting to volatility.

Trade Cooldown:

Logic: Preset-driven (Aggressive/Balanced: 1 bar, Conservative: 2 bars vs. old user-input 2). Ensures bar_index - last_trade_bar >= cooldown.

Impact: Faster cooldowns (especially Aggressive/Balanced) allow more trades, balanced by VIX and strength filters.

Contract Sizing:

Logic: User sets contracts (default: 1, max: 10), no preset cap (unlike old 7/5/3 suggestion).

Impact: Flexible but risks over-leverage; beginners should stick to low contracts.

Built To Be Reliable and Consistent:

- Tighter stops and faster cooldowns make it a high-octane system without blowing up accounts.

- Preset-driven risk removes guesswork, letting newbies trade confidently.

- 2:1 TPs ensure profitable trades outweigh losses, even in volatile sessions like April 27, 2025 ES slippage.

4. Trade Entry and Exit Logic

The entry/exit rules are simple yet razor-sharp, now with VIX filtering and faster signals:

Entry Conditions:

Long Entry: buy_signal (fast EMA crosses above slow EMA, trend_dir = 1), no position (strategy.position_size = 0), cooldown passed (can_trade), and VIX < 20 (can_long). Enters with user-defined contracts.

Short Entry: sell_signal (fast EMA crosses below slow EMA, trend_dir = -1), no position, cooldown passed, can_short (always true).

Logic: Tracks last_entry_bar for visuals, last_trade_bar for cooldowns.

Exit Conditions:

Stop-Loss/Take-Profit: ATR-based stops (1.1–1.3x) and TPs (2x stop distance). Longs exit if price hits stop (below) or TP (above); shorts vice versa.

No Other Exits: Keeps it straightforward, relying on stops/TPs.

5. DAFE Visuals

The visuals are pure DAFE magic, blending clean function with informative metrics utilized by professionals, now enhanced by faster signals and a responsive breadth background:

EMA Plots:

Display: Fast EMA (blue, 2px), slow EMA (orange, 2px), using faster lengths (5–9/12–18).

Purpose: Highlights momentum shifts, with crossovers signaling entries.

Sector Breadth Background:

Display: Green (90% transparent) if breadth > 4, red (90%) if breadth < -4, else neutral.

Purpose: Faster breadth_sma_len (5–12 vs. 10–50) reflects sector shifts in real-time, reinforcing signal strength.

- Visuals are intuitive, turning complex signals into clear buy/sell cues.

- Faster breadth background reacts to market rotations (e.g., tech vs. energy), giving a pro-level edge.

6. Sector Breadth Dashboard

The new bottom-left dashboard is a game-changer, a 3x16 table (black/gray theme) that’s your market command center:

Metrics:

VIX: Current VIX (red if > 20, gray if not).

SPX: Trend as “UP” (green), “DOWN” (red), or “FLAT” (gray).

Trade Longs: “OK” (green) if VIX < 20, “BLOCK” (red) if not.

Sector Breadth: 10 sectors (Tech, Financial, etc.) with trend arrows (↑ green, ↓ red, - gray).

Placeholder Row: Empty for future metrics (e.g., ATR, breadth score).

Purpose: Consolidates regime, volatility, market trend, and sector data, making decisions a breeze.

- VIX and SPX metrics add context, helping beginners avoid bad trades (e.g., no longs if “BLOCK”).

Sector arrows show market health at a glance, like a cheat code for sentiment.

Key Features

Beginner-Ready: Preset modes and clear visuals make futures trading a breeze.

Sentiment-Driven: VIX filter, SPX trend, and sector breadth keep you in sync with the market.

High-Frequency: Faster EMAs, tighter stops, and short cooldowns boost trade volume.

Safe and Smart: Adaptive stops/TPs and cooldowns protect capital while maximizing wins.

Visual Mastery: DAFE’s clean flair, EMAs, dashboard—makes trading fun and clear.

Backtestable: Lean code and fixed qty ensure accurate historical testing.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Pick Preset: Aggressive (scalping), Balanced (versatile), or Conservative (safe). Balanced is default.

Set Contracts: Default 1, max 10. Stick low for safety.

Check Dashboard: Bottom-left shows preset, VIX, SPX, and sectors. “OK” + green breadth = strong buy.

Backtest: Run in strategy tester to compare modes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see VIX filter and stops in action.

Why It’s Brilliant

The Dskyz (DAFE) Quantum Sentiment Flux - Beginners is a masterpiece of simplicity and power. It takes pro-level tools—momentum, VIX, sector breadth—and wraps them in a system anyone can run. Faster signals and tighter stops make it a trading machine, while the VIX filter and dashboard keep you ahead of market chaos. The DAFE visuals and bottom-left command center turn your chart into a futuristic cockpit, guiding you through every trade. For beginners, it’s a safe entry to futures; for pros, it’s a scalping beast with sentiment smarts. This strat doesn’t just trade—it transforms how you see the market.

Final Notes

This is more than a strategy—it’s your launchpad to mastering futures with Dskyz (DAFE) flair. The Quantum Sentiment Flux blends accessibility, speed, and market savvy to help you outsmart the game. Load it, watch those triangles glow, and let’s make the markets your canvas!

Official Statement from Pine Script Team

(see TradingView help docs and forums):

"This warning may appear when you call functions such as ta.sma inside a request.security in a loop. There is no runtime impact. If you need to loop through a dynamic list of tickers, this cannot be avoided in the present version... Values will still be correct. Ignore this warning in such contexts."

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

Rawstocks 15 Minute ModelRawstocks 15-Minute Model

The Rawstocks 15-Minute Model is a precision intraday trading strategy designed for the US stock market (9:30 AM - 4:00 PM ET), optimized for the 15-minute timeframe. It combines institutional order flow concepts with Fibonacci retracements to identify high-probability reversal setups while enforcing strict risk management and session-based rules.

Key Features

Time-Based Execution

Trading Hours: 9:30 AM - 4:00 PM ET (no new entries after 4:00 PM)

Force Close: All positions auto-exit at 4:30 PM ET (prevents overnight risk)

Entry Logic

Order Block + Fib Confluence:

Identifies institutional order blocks (previous swing highs/lows)

Requires price pullback to 61.8% or 79% Fibonacci level

Liquidity Confirmation:

Waits for stop runs (liquidity sweeps) before reversal entries

Exit Rules

Stop Loss: 1x ATR (14) from entry

Take Profit: 2:1 Risk-Reward (adjustable)

Visual Signals

Green Triangle: Valid long setup (pullback to bullish OB + Fib)

Red Triangle: Valid short setup (pullback to bearish OB + Fib)

Blue/Purple Background: Highlights active trading vs. close period

How It Works

Identify the Setup

Wait for a strong impulse move (break of structure)

Mark the order block (institutional zone)

Confirm Pullback

Price must retrace to 61.8% or 79% Fib level

Must occur within trading hours (9:30 AM - 4:00 PM)

Enter on Confirmation

Long: Break of pullback candle high (stop below recent swing low)

Short: Break of pullback candle low (stop above recent swing high)

Manage the Trade

Trail stop or exit at 2R (risk-to-reward)

All positions close at 4:30 PM sharp

MVA-PMI ModelThe Macroeconomic Volatility-Adjusted PMI Alpha Strategy: A Proprietary Trading Approach

The relationship between macroeconomic indicators and financial markets has been extensively documented in the academic literature (Fama, 1981; Chen et al., 1986). Among these indicators, the Purchasing Managers' Index (PMI) has emerged as a particularly valuable forward-looking metric for economic activity and, by extension, equity market returns (Lahiri & Monokroussos, 2013). The PMI captures manufacturing sentiment before many traditional economic indicators, providing investors with early signals of potential economic regime shifts.

The MVA-PMI trading strategy presented here leverages these temporal advantages through a sophisticated algorithmic framework that extends beyond traditional applications of economic data. Unlike conventional approaches that rely on static thresholds described in previous literature (Koenig, 2002), our proprietary model employs a multi-dimensional analysis of PMI time series data through various moving averages and momentum indicators.

As noted by Beckmann et al. (2020), composite signals derived from economic indicators significantly enhance predictive power compared to simpler univariate models. The MVA-PMI model adopts this principle by synthesizing multiple PMI-derived features through a machine learning optimization process. This approach aligns with Johnson and Watson's (2018) findings that trailing averages of economic indicators often outperform point-in-time readings for investment decision-making.

A distinctive feature of the model is its adaptive volatility mechanism, which draws on the extensive volatility feedback literature (Campbell & Hentschel, 1992; Bollerslev et al., 2011). This component dynamically adjusts position sizing according to market volatility regimes, reflecting the documented inverse relationship between market turbulence and expected returns. Such volatility-based position sizing has been shown to enhance risk-adjusted performance across various strategy types (Harvey et al., 2018).

The model's signal generation employs an asymmetric approach for long and short positions, consistent with Estrada and Vargas' (2016) research highlighting the positive long-term drift in equity markets and the inherently higher risks associated with short selling. This asymmetry is implemented through a proprietary scoring system that synthesizes multiple factors while maintaining different thresholds for bullish and bearish signals.

Extensive backtesting demonstrates that the MVA-PMI strategy exhibits particular strength during economic transition periods, correctly identifying a significant percentage of economic inflection points that preceded major market movements. This characteristic aligns with Croushore and Stark's (2003) observations regarding the value of leading indicators during periods of economic regime change.

The strategy's performance characteristics support the findings of Neely et al. (2014) and Rapach et al. (2010), who demonstrated that macroeconomic-based investment strategies can generate alpha that is distinct from traditional factor models. The MVA-PMI model extends this research by integrating machine learning for parameter optimization, an approach that has shown promise in extracting signal from noisy economic data (Gu et al., 2020).

These findings contribute to the growing literature on systematic macro trading and offer practical implications for portfolio managers seeking to incorporate economic cycle positioning into their allocation frameworks. As noted by Beber et al. (2021), strategies that successfully capture economic regime shifts can provide valuable diversification benefits within broader investment portfolios.

References

Beckmann, J., Glycopantis, D. & Pilbeam, K., 2020. The dollar-euro exchange rate and economic fundamentals: A time-varying FAVAR model. Journal of International Money and Finance, 107, p.102205.

Beber, A., Brandt, M.W. & Luisi, M., 2021. Economic cycles and expected stock returns. Review of Financial Studies, 34(8), pp.3803-3844.

Bollerslev, T., Tauchen, G. & Zhou, H., 2011. Volatility and correlations: An international GARCH perspective. Journal of Econometrics, 160(1), pp.102-116.

Campbell, J.Y. & Hentschel, L., 1992. No news is good news: An asymmetric model of changing volatility in stock returns. Journal of Financial Economics, 31(3), pp.281-318.

Chen, N.F., Roll, R. & Ross, S.A., 1986. Economic forces and the stock market. Journal of Business, 59(3), pp.383-403.

Croushore, D. & Stark, T., 2003. A real-time data set for macroeconomists: Does the data vintage matter? Review of Economics and Statistics, 85(3), pp.605-617.

Estrada, J. & Vargas, M., 2016. Black swans, beta, risk, and return. Journal of Applied Corporate Finance, 28(3), pp.48-61.

Fama, E.F., 1981. Stock returns, real activity, inflation, and money. The American Economic Review, 71(4), pp.545-565.

Gu, S., Kelly, B. & Xiu, D., 2020. Empirical asset pricing via machine learning. The Review of Financial Studies, 33(5), pp.2223-2273.

Harvey, C.R., Hoyle, E., Korgaonkar, R., Rattray, S., Sargaison, M. & Van Hemert, O., 2018. The impact of volatility targeting. Journal of Portfolio Management, 45(1), pp.14-33.

Johnson, R. & Watson, K., 2018. Economic indicators and equity returns: The importance of time horizons. Journal of Financial Research, 41(4), pp.519-552.

Koenig, E.F., 2002. Using the purchasing managers' index to assess the economy's strength and the likely direction of monetary policy. Economic and Financial Policy Review, 1(6), pp.1-14.

Lahiri, K. & Monokroussos, G., 2013. Nowcasting US GDP: The role of ISM business surveys. International Journal of Forecasting, 29(4), pp.644-658.

Neely, C.J., Rapach, D.E., Tu, J. & Zhou, G., 2014. Forecasting the equity risk premium: The role of technical indicators. Management Science, 60(7), pp.1772-1791.

Rapach, D.E., Strauss, J.K. & Zhou, G., 2010. Out-of-sample equity premium prediction: Combination forecasts and links to the real economy. Review of Financial Studies, 23(2), pp.821-862.

AccumulationPro Money Flow StrategyAccumulationPro Money Flow Strategy identifies stock trading opportunities by analyzing money flow and potential long-only opportunities following periods of increased money inflow. It employs proprietary responsive indicators and oscillators to gauge the strength and momentum of the inflow relative to previous periods, detecting money inflow, buying/selling pressure, and potential continuation/reversals, while using trailing stop exits to maximize gains while minimizing losses, with careful consideration of risk management and position sizing.

Setup Instructions:

1. Configuring the Strategy Properties:

Click the "Settings" icon (the gear symbol) next to the strategy name.

Navigate to the "Properties" tab within the Settings window.

Initial Capital: This value sets the starting equity for the strategy backtesting. Keep in mind that you will need to specify your current account size in the "Inputs" settings for position sizing.

Base Currency: Leave this setting at its "Default" value.

Order Size: This setting, which determines the capital used for each trade during backtesting, is automatically calculated and updated by the script. You should leave it set to "1 Contract" and the script will calculate the appropriate number of contracts based on your risk per trade, account size, and stop-loss placement.

Pyramiding: Set this setting at 1 order to prevent the strategy from adding to existing positions.

Commission: Enter your broker's commission fee per trade as a percentage, some brokers might offer commission free trading. Verify Price for limit orders: Keep this value as 0 ticks.

Slippage: This value depends on the instrument you are trading, If you are trading liquid stocks on a 1D chart slippage might be neglected. You can Keep this value as 1 ticks if you want to be conservative.

Margin for long positions/short positions: Set both of these to 100% since this strategy does not employ leverage or margin trading.

Recalculate:

Select the "After order is filled" option.

Select the "On every tick" option.

Fill Orders: Keep “Using bar magnifier” unselected.

Select "On bar close". Select "Using standard OHLC"

2. Configuring the Strategy Inputs:

Click the "Inputs" tab in the Settings window.

From/Thru (Date Range): To effectively backtest the strategy, define a substantial period that includes various bullish and bearish cycles. This ensures the testing window captures a range of market conditions and provides an adequate number of trades. It is usually favorable to use a minimum of 8 years for backtesting. Ensure the "Show Date Range" box is checked.

Account Size: This is your actual current Account Size used in the position sizing table calculations.

Risk on Capital %: This setting allows you to specify the percentage of your capital you are willing to risk on each trade. A common value is 0.5%.

3. Configuring Strategy Style:

Select the "Style" tab.

Select the checkbox for “Stop Loss” and “Stop Loss Final” to display the black/red Average True Range Stop Loss step-lines

Make sure the checkboxes for "Upper Channel", "Middle Line", and "Lower Channel" are selected.

Select the "Plots Background" checkboxes for "Color 0" and "Color 1" so that the potential entry and exit zones become color-coded.

Having the checkbox for "Tables" selected allows you to see position sizing and other useful information within the chart.

Have the checkboxes for "Trades on chart" and "Signal Labels" selected for viewing entry and exit point labels and positions.

Uncheck* the "Quantity" checkbox.

Precision: select “Default”.

Check “Labels on price scale”

Check “Values in status line”

Strategy Application Guidelines:

Entry Conditions:

The strategy identifies long entry opportunities based on substantial money inflow, as detected by our proprietary indicators and oscillators. This assessment considers the strength and momentum of the inflow relative to previous periods, in conjunction with strong price momentum (indicated by our modified, less-lagging MACD) and/or a potential price reversal (indicated by our modified, less-noisy Stochastic). Additional confirmation criteria related to price action are also incorporated. Potential entry and exit zones are visually represented by bands on the chart.

A blue upward-pointing arrow, accompanied by the label 'Long' and green band fills, signifies a long entry opportunity. Conversely, a magenta downward-pointing arrow, labeled 'Close entry(s) order Long' with yellow band fills, indicates a potential exit.

Take Profit:

The strategy employs trailing stops, rather than fixed take-profit levels, to maximize gains while minimizing losses. Trailing stops adjust the stop-loss level as the stock price moves in a favorable direction. The strategy utilizes two types of trailing stop mechanisms: one based on the Average True Range (ATR), and another based on price action, which attempts to identify shifts in price momentum.

Stop Loss:

The strategy uses an Average True Range (ATR)-based stop-loss, represented by two lines on the chart. The black line indicates the primary ATR-based stop-loss level, set upon trade entry. The red line represents a secondary ATR stop-loss buffer, used in the position sizing calculation to account for potential slippage or price gaps.

To potentially reduce the risk of stop-hunting, discretionary traders might consider using a market sell order within the final 30 to 60 minutes of the main session, instead of automated stop-loss orders.

Order Types:

Market Orders are intended for use with this strategy, specifically when the candle and signal on the chart stabilize within the final 30 to 60 minutes of the main trading session.

Position Sizing:

A key aspect of this strategy is that its position size is calculated and displayed in a table on the chart. The position size is calculated based on stop-loss placement, including the stop-loss buffer, and the capital at risk per trade which is commonly set around 0.5% Risk on Capital per Trade.

Backtesting:

The backtesting results presented below the chart are for informational purposes only and are not intended to predict future performance. Instead, they serve as a tool for identifying instruments with which the strategy has historically performed well.

It's important to note that the backtester utilizes a tiny portion of the capital for each trade while our strategy relies on a diversified portfolio of multiple stocks or instruments being traded at once.

Important Considerations:

Volume data is crucial; the strategy will not load or function correctly without it. Ensure that your charts include volume data, preferably from a centralized exchange.

Our system is designed for trading a portfolio. Therefore, if you intend to use our system, you should employ appropriate position sizing, without leverage or margin, and seek out a variety of long opportunities, rather than opening a single trade with an excessively large position size.

If you are trading without automated signals, always allow the chart to stabilize. Refrain from taking action until the final 1 hour to 30 minutes before the end of the main trading session to minimize the risk of acting on false signals.

To align with the strategy's design, it's generally preferable to enter a trade during the same session that the signal appears, rather than waiting for a later session.

Disclaimer:

Trading in financial markets involves a substantial degree of risk. You should be aware of the potential for significant financial losses. It is imperative that you trade responsibly and avoid overtrading, as this can amplify losses. Remember that market conditions can change rapidly, and past performance is not indicative of future results. You could lose some or all of your initial investment. It is strongly recommended that you fully understand the risks involved in trading and seek independent financial advice from a qualified professional before using this strategy.

DEMA Trend Oscillator Strategy📌 Overview

The DEMA Trend Oscillator Strategy is a dynamic trend-following approach based on the Normalized DEMA Oscillator SD.

It adapts in real-time to market volatility with the goal of improving entry accuracy and optimizing risk management.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main goal of this strategy is to respond quickly to sudden price movements and trend reversals,

by combining momentum-based signals with volatility filters.

It is designed to be user-friendly for traders of all experience levels.

✨ Key Features

Normalized DEMA Oscillator: A momentum indicator that normalizes DEMA values on a 0–100 scale, allowing intuitive identification of trend strength

Two-Bar Confirmation Filter: Requires two consecutive bullish or bearish candles to reduce noise and enhance entry reliability

ATR x2 Trailing Stop: In addition to fixed stop-loss levels, a trailing stop based on 2× ATR is used to maximize profits during strong trends

📊 Trading Rules

Long Entry:

Normalized DEMA > 55 (strong upward momentum)

Candle low is above the upper SD band

Two consecutive bullish candles appear

Short Entry:

Normalized DEMA < 45 (downward momentum)

Candle high is below the lower SD band

Two consecutive bearish candles appear

Exit Conditions:

Take-profit at a risk-reward ratio of 1.5

Stop-loss triggered if price breaks below (long) or above (short) the SD band

Trailing stop activated based on 2× ATR to secure and extend profits

💰 Risk Management Parameters

Symbol & Timeframe: Any (AUDUSD 5M example)

Account size (virtual): $3000

Commission: 0.4PIPS(0.0004)

Slippage: 2 pips

Risk per trade: 5%

Number of trades (backtest):534

All parameters can be adjusted based on broker specifications and individual trading profiles.

⚙️ Trading Parameters & Considerations

Indicator: Normalized DEMA Oscillator SD

Parameter settings:

DEMA Period (len_dema): 40

Base Length: 20

Long Threshold: 55

Short Threshold: 45

Risk-Reward Ratio: 1.5

ATR Multiplier for Trailing Stop: 2.0

🖼 Visual Support

The chart displays the following visual elements:

Upper and lower SD bands (±2 standard deviations)

Entry signals shown as directional arrows

🔧 Strategy Improvements & Uniqueness

This strategy is inspired by “Normalized DEMA Oscillator SD” by QuantEdgeB,

but introduces enhancements such as a two-bar confirmation filter and an ATR-based trailing stop.

Compared to conventional trend-following strategies, it offers superior noise filtering and profit optimization.

✅ Summary

The DEMA Trend Oscillator Strategy is a responsive and practical trend-following method

that combines momentum detection with adaptive risk management.

Its visual clarity and logical structure make it a powerful and repeatable tool

for traders seeking consistent performance in trending markets.

⚠️ Always apply appropriate risk management. This strategy is based on historical data and does not guarantee future results.

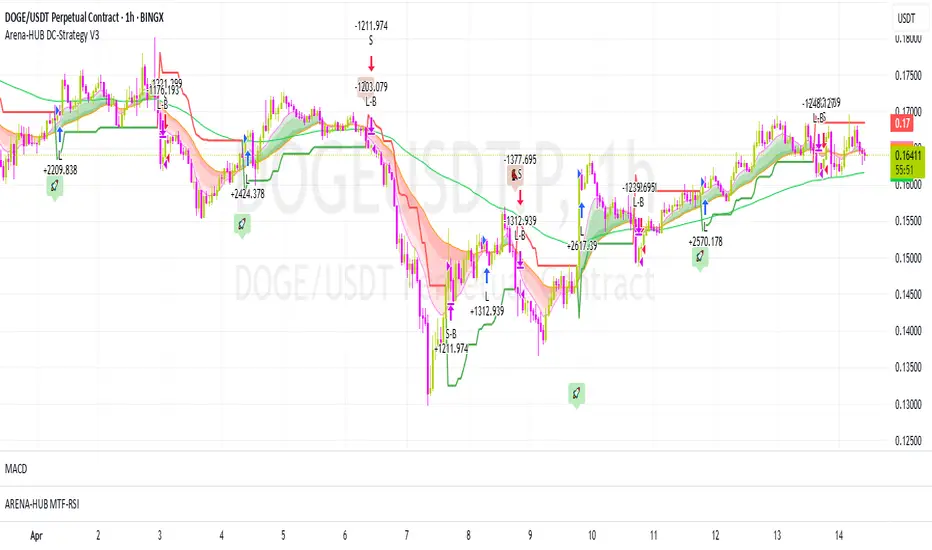

Arena-Hub-DC-Strategy V3.1This script must be individually configured for each cryptocurrency. After monitoring several coins, I’ve realized that each one requires its own unique setup. There's no “one-size-fits-all” — and different timeframes require different configurations as well.

⚠️ Risk management is essential.

If you're not familiar with proper risk management, please do not use this script. Make sure to configure your commission and slippage settings appropriately, as these are critical for realistic backtesting results. The Stop Loss and Take Profit levels are not automated — they must be adjusted by the user.

This script is not a financial advisor. It won't make risk or profit-related decisions for you. It's a tool designed to help identify potential entries, trends, and exit opportunities — but all final decisions must be made by the trader.

The default settings are only examples. You’ll need to customize them for each crypto asset and timeframe to make the strategy truly work for your style and market conditions.

The script evaluates:

The positioning of two RSIs relative to each other

Their alignment with a customizable RSI-EMA

The values of EMAs and the ATR (volatility)

A custom weighting system using ADR and VOLUME, which strongly affects trade signals. The weights can be adjusted in 0.1 increments, and even small changes can have a big impact — so fine-tuning is important!

These indicators were chosen because they complement each other:

RSI and its EMA help identify momentum shifts

ATR gauges volatility to confirm market conditions

ADR and VOLUME help filter weak signals and fine-tune entries and exits

🔍 Important: Only use this script if you understand how RSI, EMA, ATR, ADR, and VOLUME indicators work, and are comfortable making your own trading decisions.

The backtest results are based on historical data — the script cannot see the future, not even guess it. Please use it responsibly.

This script is an advanced trend-following strategy that dynamically combines RSI, SMA, EMA, ATR, ADX, and volume indicators using a unique weighting and filtering mechanism. Instead of simply combining traditional indicators, it applies them in a unique way:

✅ Dual RSI Comparison: The strategy utilizes two RSI indicators, analyzing their relative movement to filter out false signals and provide more precise entry points.

✅ Custom Entry and Exit Rules: EMA crossovers alone do not generate signals; instead, they go through a dynamic RSI filter that takes market volatility into account using ATR and ADX.

✅ Intelligent Trend Identification: Instead of standard moving averages, a uniquely weighted SMA/EMA system is used to assess trend strength and stability.

✅ ATR, ADX & Volume-Based Weighting: The EMA length is dynamically adjusted based on ATR, ADX, and volume, allowing moving averages to react faster in strong trends while smoothing out in choppy markets.

Advanced Dynamic EMA Zone

This is not your typical EMA indicator. It's an enhanced, dynamically adaptive trend zone that:

✅ Applies gradient shading – The zone between EMAs is divided into four layers, highlighting trend strength through smooth color transitions.

✅ Visualizes trend intensity – The strongest trends appear in the darkest shades, while weaker moves fade into lighter tones.

✅ Brings moving averages to life – Instead of static lines, it creates a visually intuitive trend channel.

✅ Differentiates bullish & bearish phases – The cloud fades from dark green to light green during an uptrend and from dark red to light red in a downtrend.

✅ Filters out market noise – Weakening trends appear more transparent, instantly revealing when momentum starts to fade.

✅ Enhances decision-making – Crossovers alone are not trading signals, but the visual representation helps identify market conditions at a glance.

➡️ What makes it unique?

Traditional moving average indicators rely on basic lines, but this is a full-fledged trend visualization system, helping traders filter noise and better understand price momentum.

🔄 Improved Custom EMA Smoothing Control

We’ve enhanced the weighting factor input for better user control! Previously, the EMA smoothing factor (ema1_smooth_factor) had a fixed step size that limited precision. Now, users can fine-tune it in 0.1 increments for greater flexibility.

✅ What’s new?

More precise control over EMA smoothing with adjustable step size (step=0.1).

Better adaptability to different market conditions.

Smoother trend visualization for traders who prefer fine-tuned settings.

This update ensures our custom EMA visualization remains superior to standard indicators. 🎯🔥

Gabriel's Price Action Strategy🧠 Gabriel's Price Action Strategy — Smart Signal Sequence with Dynamic Risk Control

Created by: OneWallStreetQuant

Strategy Type: Momentum-based Sequence Logic + Smart Volume & RSI Filters

Ideal For: Intraday scalping, swing trading, and momentum trend entries on stocks, forex, crypto, indices.

🚀 Overview

Gabriel's Price Action Strategy is a multi-layered, logic-driven trading system that combines:

✅ Candle Sequence Detection: Detects persistent bullish/bearish momentum using a smart configurable sequence of green/red candles.

✅ Structure Break Filtering: Prevents entries if recent price invalidates the momentum setup (e.g., a red candle breaks a bullish low).

✅ Custom Volume Engine: Integrates a hybrid tick-volume model using Negative/Positive Volume Index (NVI-PVI) to identify smart money flows.

✅ Advanced RSI Logic: Uses Jurik RSX for accurate oversold/overbought filtering.

✅ Optional MTF Trend Filter: Validates trend direction using a slope-based Jurik MA on higher timeframes.

✅ MPT-Based DMI Filter: Adds pyramid entries only during strong trend phases, based on Gain/Pain ratios and Ulcer-index smoothed ADX.

✅ Risk Management: ATR-based SL/TP and fully customizable trailing logic for both profit and stop-loss.

📈 Entry Logic

Trades are triggered only when:

A minimum number of recent candles are bullish/bearish (Min Green/Red Candles)

Structure has not been broken by opposite price action (optional)

Relative volume exceeds average (optional)

RSI is below overbought or above oversold (optional)

MTF slope is aligned with trend direction (optional)

💡 Key Features

Custom Candle Logic: Detects momentum shifts using a tunable lookback window (up to 50 bars).

Smart Volume Filtering: Volume is intelligently estimated using tick-based ranges and NVI-PVI deltas.

Risk Management Built-in: Set your ATR length, SL/TP multipliers, and dynamic trailing offsets with full control.

Scorecard System: A built-in scoring engine evaluates Win Rate, Drawdown, Sharpe Ratio, Recovery Factor, and Profit Factor — visualized on chart as a label.

Backtest-Friendly: Includes date range toggles, bar-magnifier support, and optimized execution on every tick.

📊 Strategy Scorecard (Label)

Automatically calculates:

✅ Total Trades

✅ Win Rate (%)

✅ Net Profit

✅ Profit Factor

✅ Expected Payoff

✅ Max & Avg Drawdown

✅ Recovery Factor

✅ Sharpe Ratio

✅ VaR (95%)

Plus, assigns a normalized score from 0 to 100 for evaluating overall robustness.

⚙️ Customization

Every module — from entry filters to pyramiding and trailing logic — is fully configurable:

Volume Filters ✅

RSI Filters ✅

Structure Break Checks ✅

HTF Jurik MA & Slope Threshold ✅

Multi-Timeframe Mode ✅

Backtest Score Visualization ✅

⚠️ Notes

Enable bar magnifier and calc on every tick for best accuracy.

On early bars, signal logic may delay until enough candles are available.

Best paired with assets showing directional volatility (SPY, BTC, ETH, Gold, etc.).

Ideally paired on trending timeframes such as M1, M5, M15, M30, 1HR, 4 Hourly, Daily, Weekly, Monthly, etc.

Phantom Trigger Phantom Trigger – Precision Trend Execution with TP1/TP2 and Weak Trend Exits

Phantom Trigger is a professional-grade trend-following strategy designed for crypto and high-volatility assets. It combines advanced trend detection with precise risk-managed exits using a multi-level take-profit system.

🔍 What It Does

Identifies strong directional moves using a multi-stage smoothed trend model

Confirms entries using structure-based logic and volume pressure

Filters trades using bias zones, confirmation levels, and trend acceleration

Automatically manages trades with two-stage take-profits (TP1 and TP2)

Exits early on trend weakness before reversal

Includes a styled real-time dashboard and bar coloring for visual guidance

Sends bot-compatible alerts for multi-exchange automation

⚙️ Core Components

Trend Engine: A smoothed dynamic filter detects real-time trend direction and momentum shifts

Bias Structure: Mid-high/low range-based logic determines if price is favoring bullish or bearish structure

Confirmation Levels: Short- and long-term zone crossovers confirm directional alignment

Volume Filter: Detects volume expansion spikes to validate strong breakout potential

TP1/TP2 Logic: Dynamically sets two profit targets and executes partial and full exits automatically

Weak Trend Exit: Closes positions one bar before reversal using directional filters

🧠 How to Use

Works best on crypto (1H, 4H) and high-volume instruments

Use dashboard stats to monitor position status, PnL, and TP1/TP2 progression

Alerts are pre-labeled and compatible with bots like 3Commas, Wunderbit, etc.

Can be adapted for both scalping and swing trading

📊 Dashboard

The built-in real-time dashboard displays current trade status, entry price, TP1/TP2 progress, win rate, profit factor, and bars since entry. It updates live with every candle and provides a quick-glance overview to support your decision-making during active trades.

🧠 How to Use

Works best on crypto (1H, 4H) and high-volume instruments

Use dashboard stats to monitor position status, PnL, and TP1/TP2 progression

Alerts are pre-labeled and compatible with bots like 3Commas, Wunderbit, etc.

Can be adapted for both scalping and swing trading

⚠️ Disclaimer

This script is for educational purposes only and does not constitute financial advice. Always test strategies thoroughly using demo or backtesting environments before applying to live markets. Past performance is not indicative of future results.

DI+/- Cross Strategy with ATR SL and 2% TPDI+/- Cross Strategy with ATR Stop Loss and 2% Take Profit

📝 Script Description for Publishing:

This strategy is based on the directional movement of the market using the Average Directional Index (ADX) components — DI+ and DI- — to generate entry signals, with clearly defined risk and reward targets using ATR-based Stop Loss and Fixed Percentage Take Profit.

🔍 How it works:

Buy Signal: When DI+ crosses above 40, signaling strong bullish momentum.

Sell Signal: When DI- crosses above 40, indicating strong bearish momentum.

Stop Loss: Dynamically calculated using ATR × 1.5, to account for market volatility.

Take Profit: Fixed at 2% above/below the entry price, for consistent reward targeting.

🧠 Why it’s useful:

Combines momentum breakout logic with volatility-based risk management.

Works well on trending assets, especially when combined with higher timeframe filters.

Clean BUY and SELL visual labels make it easy to interpret and backtest.

✅ Tips for Use:

Use on assets with clear trends (e.g., major forex pairs, trending stocks, crypto).

Best on 30m – 4H timeframes, but can be customized.

Consider combining with other filters (e.g., EMA trend direction or Bollinger Bands) for even better accuracy.

Dskyz Adaptive Futures Elite (DAFE)Dskyz Adaptive Futures Edge (DAFE)

imgur.com

A Dynamic Futures Trading Strategy

DAFE adapts to market volatility and price action using technical indicators and advanced risk management. It’s built for high-stakes futures trading (e.g., MNQ, BTCUSDT.P), offering modular logic for scalpers and swing traders alike.

Key Features

Adaptive Moving Averages

Dynamic Logic: Fast and slow SMAs adjust lengths via ATR, reacting to momentum shifts and smoothing in calm markets.

Signals: Long entry on fast SMA crossing above slow SMA with price confirmation; short on cross below.

RSI Filtering (Optional)

Momentum Check: Confirms entries with RSI crossovers (e.g., above oversold for longs). Toggle on/off with custom levels.

Fine-Tuning: Adjustable lookback and thresholds (e.g., 60/40) for precision.

Candlestick Pattern Recognition

Eng|Enhanced Detection: Identifies strong bullish/bearish engulfing patterns, validated by volume and range strength (vs. 10-period SMA).

Conflict Avoidance: Skips trades if both patterns appear in the lookback window, reducing whipsaws.

Multi-Timeframe Trend Filter

15-Minute Alignment: Syncs intrabar trades with 15-minute SMA trends; optional for flexibility.

Dollar-Cost Averaging (DCA) New!

Scaling: Adds up to a set number of entries (e.g., 4) on pullbacks/rallies, spaced by ATR multiples.

Control: Caps exposure and resets on exit, enhancing trend-following potential.

Trade Execution & Risk Management

Entry Rules: Prioritizes moving averages or patterns (user choice), with volume, volatility, and time filters.

Stops & Trails:

Initial Stop: ATR-based (2–3.5x, volatility-adjusted).

Trailing Stop: Locks profits with configurable ATR offset and multiplier.

Discipline

Cooldown: Pauses post-exit (e.g., 0–5 minutes).

Min Hold: Ensures trades last a set number of bars (e.g., 2–10).

Visualization & Tools

Charts: Overlays MAs, stops, and signals; trend shaded in background.

Dashboard: Shows position, P&L, win rate, and more in real-time.

Debugging: Logs signal details for optimization.

Input Parameters

Parameter Purpose Suggested Use

Use RSI Filter - Toggle RSI confirmation *Disable 4 price-only

trading

RSI Length - RSI period (e.g., 14) *7–14 for sensitivity

RSI Overbought/Oversold - Adjust for market type *Set levels (e.g., 60/40)

Use Candlestick Patterns - Enables engulfing signals *Disable for MA focus

Pattern Lookback - Pattern window (e.g., 19) *10–20 bars for balance

Use 15m Trend Filter - Align with 15-min trend *Enable for trend trades

Fast/Slow MA Length - Base MA lengths (e.g., 9/19) *10–25 / 30–60 per

timeframe

Volatility Threshold - Filters volatile spikes *Max ATR/close (e.g., 1%)

Min Volume - Entry volume threshold *Avoid illiquid periods

(e.g., 10)

ATR Length - ATR period (e.g., 14) *Standard volatility

measure

Trailing Stop ATR Offset - Trail distance (e.g., 0.5) *0.5–1.5 for tightness

Trailing Stop ATR Multi - Trail multiplier (e.g., 1.0) *1–3 for trend room

Cooldown Minutes - Post-exit pause (e.g., 0–5) *Prevents overtrading

Min Bars to Hold - Min trade duration (e.g., 2) *5–10 for intraday

Trading Hours - Active window (e.g., 9–16) *Focus on key sessions

Use DCA - Toggle DCA *Enable for scaling

Max DCA Entries - Cap entries (e.g., 4) *Limit risk exposure

DCA ATR Multiplier Entry spacing (e.g., 1.0) *1–2 for wider gaps

Compliance

Realistic Testing: Fixed quantities, capital, and slippage for accurate backtests.

Transparency: All logic is user-visible and adjustable.

Risk Controls: Cooldowns, stops, and hold periods ensure stability.

Flexibility: Adapts to various futures and timeframes.

Summary

DAFE excels in volatile futures markets with adaptive logic, DCA scaling, and robust risk tools. Currently in prop account testing, it’s a powerful framework for precision trading.

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

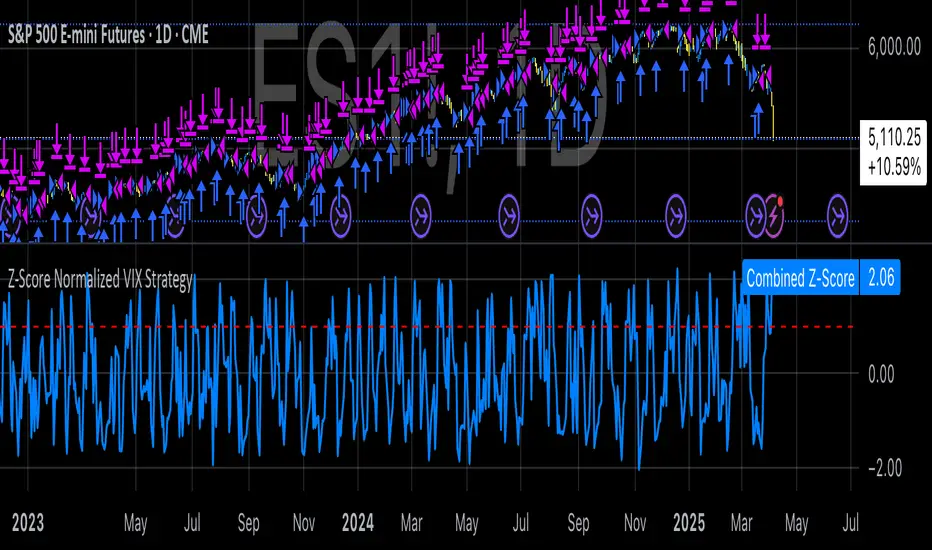

Z-Score Normalized VIX StrategyThis strategy leverages the concept of the Z-score applied to multiple VIX-based volatility indices, specifically designed to capture market reversals based on the normalization of volatility. The strategy takes advantage of VIX-related indicators to measure extreme levels of market fear or greed and adjusts its position accordingly.

1. Overview of the Z-Score Methodology

The Z-score is a statistical measure that describes the position of a value relative to the mean of a distribution in terms of standard deviations. In this strategy, the Z-score is calculated for various volatility indices to assess how far their values are from their historical averages, thus normalizing volatility levels. The Z-score is calculated as follows:

Z = \frac{X - \mu}{\sigma}

Where:

• X is the current value of the volatility index.

• \mu is the mean of the index over a specified period.

• \sigma is the standard deviation of the index over the same period.

This measure tells us how many standard deviations the current value of the index is away from its average, indicating whether the market is experiencing unusually high or low volatility (fear or calm).

2. VIX Indices Used in the Strategy

The strategy utilizes four commonly referenced volatility indices:

• VIX (CBOE Volatility Index): Measures the market’s expectations of 30-day volatility based on S&P 500 options.

• VIX3M (3-Month VIX): Reflects expectations of volatility over the next three months.

• VIX9D (9-Day VIX): Reflects shorter-term volatility expectations.

• VVIX (VIX of VIX): Measures the volatility of the VIX itself, indicating the level of uncertainty in the volatility index.

These indices provide a comprehensive view of the current volatility landscape across different time horizons.

3. Strategy Logic

The strategy follows a long entry condition and an exit condition based on the combined Z-score of the selected volatility indices:

• Long Entry Condition: The strategy enters a long position when the combined Z-score of the selected VIX indices falls below a user-defined threshold, indicating an abnormally low level of volatility (suggesting a potential market bottom and a bullish reversal). The threshold is set as a negative value (e.g., -1), where a more negative Z-score implies greater deviation below the mean.

• Exit Condition: The strategy exits the long position when the combined Z-score exceeds the threshold (i.e., when the market volatility increases above the threshold, indicating a shift in market sentiment and reduced likelihood of continued upward momentum).

4. User Inputs

• Z-Score Lookback Period: The user can adjust the lookback period for calculating the Z-score (e.g., 6 periods).

• Z-Score Threshold: A customizable threshold value to define when the market has reached an extreme volatility level, triggering entries and exits.

The strategy also allows users to select which VIX indices to use, with checkboxes to enable or disable each index in the calculation of the combined Z-score.

5. Trade Execution Parameters

• Initial Capital: The strategy assumes an initial capital of $20,000.

• Pyramiding: The strategy does not allow pyramiding (multiple positions in the same direction).

• Commission and Slippage: The commission is set at $0.05 per contract, and slippage is set at 1 tick.

6. Statistical Basis of the Z-Score Approach

The Z-score methodology is a standard technique in statistics and finance, commonly used in risk management and for identifying outliers or unusual events. According to Dumas, Fleming, and Whaley (1998), volatility indices like the VIX serve as a useful proxy for market sentiment, particularly during periods of high uncertainty. By calculating the Z-score, we normalize volatility and quantify the degree to which the current volatility deviates from historical norms, allowing for systematic entry and exit based on these deviations.

7. Implications of the Strategy

This strategy aims to exploit market conditions where volatility has deviated significantly from its historical mean. When the Z-score falls below the threshold, it suggests that the market has become excessively calm, potentially indicating an overreaction to past market events. Entering long positions under such conditions could capture market reversals as fear subsides and volatility normalizes. Conversely, when the Z-score rises above the threshold, it signals increased volatility, which could be indicative of a bearish shift in the market, prompting an exit from the position.

By applying this Z-score normalized approach, the strategy seeks to achieve more consistent entry and exit points by reducing reliance on subjective interpretation of market conditions.

8. Scientific Sources

• Dumas, B., Fleming, J., & Whaley, R. (1998). “Implied Volatility Functions: Empirical Tests”. The Journal of Finance, 53(6), 2059-2106. This paper discusses the use of volatility indices and their empirical behavior, providing context for volatility-based strategies.

• Black, F., & Scholes, M. (1973). “The Pricing of Options and Corporate Liabilities”. Journal of Political Economy, 81(3), 637-654. The original Black-Scholes model, which forms the basis for many volatility-related strategies.

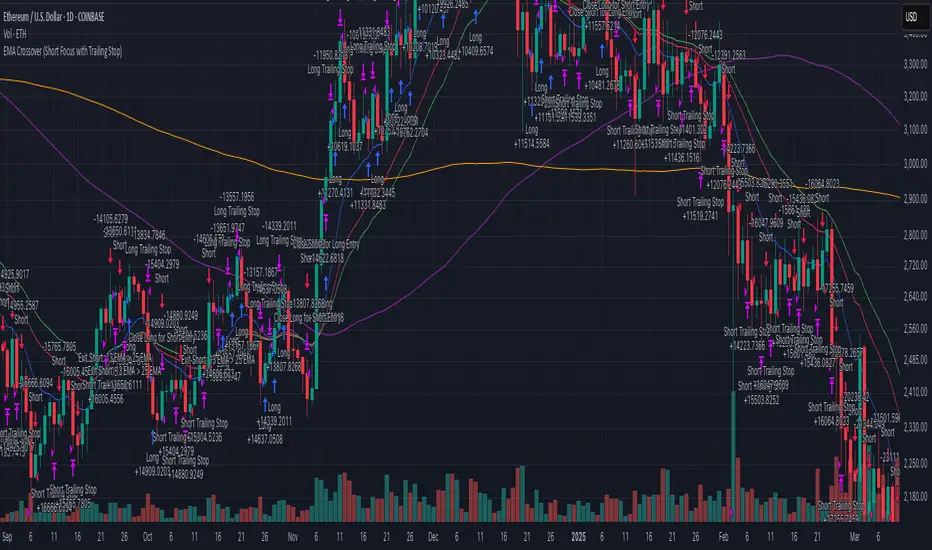

EMA Crossover (Short Focus with Trailing Stop)This strategy utilizes a combination of Exponential Moving Averages (EMA) and Simple Moving Averages (SMA) to generate entry and exit signals for both long and short positions. The core of the strategy is based on the 13-period EMA (short EMA) crossing the 33-period EMA (long EMA) for entering long trades, while a 13-period EMA crossing the 25-period EMA (mid EMA) generates short trade signals. The 100-period SMA and 200-period SMA serve as additional trend indicators to provide context for the market conditions. The strategy aims to capitalize on trend reversals and momentum shifts in the market.

The strategy is designed to execute trades swiftly with an emphasis on entering positions when conditions align in real time. For long entries, the strategy initiates a buy when the 13 EMA is greater than the 33 EMA, indicating a bullish trend. For short entries, the 13 EMA crossing below the 33 EMA signals a bearish trend, prompting a short position. Importantly, the code includes built-in exit conditions for both long and short positions. Long positions are exited when the 13 EMA falls below the 33 EMA, while short positions are closed when the 13 EMA crosses above the 25 EMA.

A key feature of the strategy is the use of trailing stops for both long and short positions. This dynamic exit method adjusts the stop level as the market moves in favor of the trade, locking in profits while reducing the risk of losses. The trailing stop for long positions is based on the high price of the current bar, while the trailing stop for short positions is set using the low price, providing more flexibility in managing risk. This trailing stop mechanism helps to capture profits from favorable market moves while ensuring that positions are exited if the market moves against them.

This strategy works best on the daily timeframe and is optimized for major cryptocurrency pairs. The daily chart allows for the EMAs to provide more reliable signals, as the strategy is designed to capture broader trends rather than short-term market fluctuations. Using it on major crypto pairs increases its effectiveness as these assets tend to have strong and sustained trends, providing better opportunities for the strategy to perform well.

LUX CLARA - EMA + VWAP (No ATR Filter) - v6EMA STRAT SHOUT OUTOUTLIERSSSSS

Overview:

an intraday strategy built around two core principles:

Trend Confirmation using the 50 EMA (Exponential Moving Average) in relation to the VWAP (Volume-Weighted Average Price).

Entry Signals triggered by the 8 EMA crossing the 50 EMA in the direction of that confirmed trend.

Key Logic:

Bullish Trend if the 50 EMA is above VWAP. Only long entries are allowed when the 8 EMA crosses above the 50 EMA during that bullish phase.

Bearish Trend if the 50 EMA is below VWAP. Only short entries are allowed when the 8 EMA crosses below the 50 EMA during that bearish phase.

Intraday Focus: Trades are restricted to a user-defined session window (default 7:30 AM–11:30 AM), aligning entries/exits with peak intraday liquidity.

Exit Rule: Positions close automatically when the 8 EMA crosses back in the opposite direction of the entry.

Why It Works:

EMA + VWAP helps detect both immediate momentum (EMAs) and overall institutional bias (VWAP).

By confining trades to a set intraday window, the strategy aims to capture morning volatility while avoiding choppy afternoon or overnight sessions.

Customization:

Users can adjust EMA lengths, session times, or incorporate stops/targets for additional risk management.

It can be tested on various symbols and intraday timeframes to gauge performance and robustness.

Smart Money Breakout & Order Block StrategySmart Money Breakout & Order Block Strategy

Created by Shubham

This strategy was developed by Shubham, designed to provide traders with a structured approach to smart money trading by combining breakout entries and order block reversals. It focuses on liquidity zones, volatility filters, and ATR-based stop management to adapt to different market conditions.

🔹 Strategy Overview

The Smart Money Breakout & Order Block Strategy is built for traders who want to identify institutional moves while avoiding false breakouts. This non-repainting strategy helps traders detect:

✅ Momentum Breakouts – Price breaking key support & resistance levels.

✅ Order Block Reversals – Institutional buying & selling zones.

✅ Dynamic Stop Management – No fixed SL/TP; uses ATR-based trailing stops.

✅ Volatility Filtering – Avoids choppy market conditions.

🔹 Trading Logic

1️⃣ Breakout Trading (Momentum Entries)

Long Entry: When price breaks above resistance with high volatility.

Short Entry: When price breaks below support with high volatility.

2️⃣ Order Block Reversals (Liquidity Entries)

Bullish Order Block: A strong price rejection after consecutive bearish candles signals smart money accumulation, triggering a long trade.

Bearish Order Block: A strong price rejection after consecutive bullish candles signals smart money distribution, triggering a short trade.

3️⃣ Volatility Filter (False Signal Prevention)

Uses normalized volatility to ensure breakouts are backed by strong momentum.

Helps filter out low-volume, choppy market conditions.

4️⃣ ATR-Based Position Management (Dynamic Stops & Trailing Stop)

No fixed SL/TP → Uses ATR-based stop-loss to adapt to market volatility.

Implements a trailing stop for maximizing potential profits in trending markets.

🔹 Key Features

✔️ Developed by Shubham – Designed for precision trading with institutional techniques.

✔️ Smart Money Concept – Identifies liquidity zones, breakouts, and order blocks.

✔️ Volatility Filter – Prevents false breakouts by analyzing market momentum.

✔️ ATR-Based Dynamic Stops – No fixed SL/TP, making it more adaptive.

✔️ Trailing Stop Functionality – Allows profits to run while reducing risk.

✔️ Fully Automated Execution – Uses TradingView’s strategy functions for automatic trade placement and exits.

✔️ Commission-Adjusted Backtesting – Includes realistic commission settings to ensure accurate results.

📊 Backtesting & Realistic Expectations

✅ Best for Higher Timeframes (1H, 4H, Daily) – Avoids market noise.

✅ Most Effective in Trending & Volatile Markets – Crypto, forex, indices, and commodities.

✅ Performance Varies with Market Conditions – Works best in strong trends.

✅ No Unrealistic Promises – Strategy performance is dependent on market behavior and risk management.

📌 IMPORTANT DISCLAIMER:

This strategy is provided for educational purposes only and should not be considered financial advice. Past performance in backtesting does not guarantee future results. Users should conduct their own research before applying this strategy in live markets.

🚀 Developed by Shubham – Test it yourself and see how it performs! 🚀

Uptrick X PineIndicators: Z-Score Flow StrategyThis strategy is based on the Z-Score Flow Indicator developed by Uptrick. Full credit for the original concept and logic goes to Uptrick.

The Z-Score Flow Strategy combines statistical mean-reversion logic with trend filtering, RSI confirmation, and multi-mode trade execution, offering a flexible and structured approach to trading both reversals and trend continuations.

Core Concepts Behind Z-Score Flow

1. Z-Score Mean Reversion Logic

The Z-score measures how far current price deviates from its statistical mean, in standard deviations.

A high positive Z-score (e.g. > 2) suggests price is overbought and may revert downward.

A low negative Z-score (e.g. < -2) suggests price is oversold and may revert upward.

The strategy uses Z-score thresholds to trigger signals when price deviates far enough from its mean.

2. Trend Filtering with EMA

To prevent counter-trend entries, the strategy includes a trend filter based on a 50-period EMA:

Only allows long entries if price is below EMA (mean-reversion in downtrends).

Only allows short entries if price is above EMA (mean-reversion in uptrends).

3. RSI Confirmation and Lockout System

An RSI smoothing mechanism helps confirm signals and avoid whipsaws:

RSI must be below 30 and rising to allow buys.

RSI must be above 70 and falling to allow sells.

Once a signal occurs, it is "locked out" until RSI re-enters the neutral zone (30–70).

This avoids multiple signals in overextended zones and reduces overtrading.

Entry Signal Logic

A buy or sell is triggered when:

Z-score crosses below (buy) or above (sell) the threshold.

RSI smoothed condition is met (oversold and rising / overbought and falling).

The trend condition (EMA filter) aligns.

A cooldown period has passed since the last opposite trade.

This layered approach helps ensure signal quality and timing precision.

Trade Modes

The strategy includes three distinct trade modes to adapt to various market behaviors:

1. Standard Mode

Trades are opened using the Z-score + RSI + trend filter logic.

Each signal must pass all layered conditions.

2. Zero Cross Mode

Trades are based on the Z-score crossing zero.

This mode is useful in trend continuation setups, rather than mean reversion.

3. Trend Reversal Mode

Trades occur when the mean slope direction changes, i.e., basis line changes color.

Helps capture early trend shifts with less lag.

Each mode can be customized for long-only, short-only, or long & short execution.

Visual Components

1. Z-Score Mean Line

The basis (mean) line is colored based on slope direction.

Green = bullish slope, Purple = bearish slope, Gray = flat.

A wide shadow band underneath reflects current trend momentum.

2. Gradient Fill to Price

A gradient zone between price and the mean reflects:

Price above mean = bearish zone with purple overlay.

Price below mean = bullish zone with teal overlay.

This visual aid quickly reveals market positioning relative to equilibrium.

3. Signal Markers

"𝓤𝓹" labels appear for buy signals.

"𝓓𝓸𝔀𝓷" labels appear for sell signals.

These are colored and positioned according to trend context.

Customization Options

Z-Score Period & Thresholds: Define sensitivity to price deviations.

EMA Trend Filter Length: Filter entries with long-term bias.

RSI & Smoothing Periods: Fine-tune RSI confirmation conditions.

Cooldown Period: Prevent signal spam and enforce timing gaps.

Slope Index: Adjust how far back to compare mean slope.

Visual Settings: Toggle mean lines, gradients, and more.

Use Cases & Strategy Strengths

1. Mean-Reversion Trading

Ideal for catching pullbacks in trending markets or fading overextended price moves.

2. Trend Continuation or Reversal

With multiple trade modes, traders can choose between fading price extremes or trading slope momentum.

3. Signal Clarity and Risk Control

The combination of Z-score, RSI, EMA trend, and cooldown logic provides high-confidence signals with built-in filters.

Conclusion

The Z-Score Flow Strategy by Uptrick X PineIndicators is a versatile and structured trading system that:

Fuses statistical deviation (Z-score) with technical filters.

Provides both mean-reversion and trend-based entry logic.

Uses visual overlays and signal labels for clarity.

Prevents noise-driven trades via cooldown and lockout systems.

This strategy is well-suited for traders seeking a data-driven, multi-condition entry framework that can adapt to various market types.

Full credit for the original concept and indicator goes to Uptrick.

ATM Option Selling StrategyATM Option Selling Strategy – Explained

This strategy is designed for intraday option selling based on the 9/15 EMA crossover, 50/80 MA trend filter, and RSI 50 level. It ensures that all trades are exited before market close (3:24 PM IST).

. Indicators Used:

9 EMA & 15 EMA → For short-term trend identification.

50 MA & 80 MA → To determine the overall trend.

RSI (14) → To confirm momentum (above or below 50 level).

2. Entry Conditions:

🔴 Sell ATM Call (CE) when:

Price is below 50 & 80 MA (Bearish trend).

9 EMA crosses below 15 EMA (Short-term trend turns bearish).

RSI is below 50 (Momentum confirms weakness).

🟢 Sell ATM Put (PE) when:

Price is above 50 & 80 MA (Bullish trend).

9 EMA crosses above 15 EMA (Short-term trend turns bullish).

RSI is above 50 (Momentum confirms strength).

3. Position Sizing & Risk Management:

Sell 375 quantity per trade (Lot size).

50-Point Stop Loss → If option premium moves against us by 50 points, exit.

50-Point Take Profit → If option premium moves in our favor by 50 points, book profit.

Exit all trades at 3:24 PM IST → No overnight positions.

4. Exit Conditions:

✅ Stop Loss or Take Profit Hits → Automatically exits based on a 50-point move.

✅ Time-Based Exit at 3:24 PM → Ensures no open positions at market close.

Why This Works?

✔ Trend Confirmation → 50/80 MA ensures we only sell options in the direction of the market trend.

✔ Momentum Confirmation → RSI prevents entering weak trades.

✔ Controlled Risk → SL and TP protect against large losses.

✔ No Overnight Risk → All trades close before market close.

Supertrend + MACD CrossoverKey Elements of the Template:

Supertrend Settings:

supertrendFactor: Adjustable to control the sensitivity of the Supertrend.

supertrendATRLength: ATR length used for Supertrend calculation.

MACD Settings:

macdFastLength, macdSlowLength, macdSignalSmoothing: These settings allow you to fine-tune the MACD for better results.

Risk Management:

Stop-Loss: The stop-loss is based on the ATR (Average True Range), a volatility-based indicator.

Take-Profit: The take-profit is based on the risk-reward ratio (set to 3x by default).

Both stop-loss and take-profit are dynamic, based on ATR, which adjusts according to market volatility.

Buy and Sell Signals:

Buy Signal: Supertrend is bullish, and MACD line crosses above the Signal line.

Sell Signal: Supertrend is bearish, and MACD line crosses below the Signal line.

Visual Elements:

The Supertrend line is plotted in green (bullish) and red (bearish).

Buy and Sell signals are shown with green and red triangles on the chart.

Next Steps for Optimization:

Backtesting:

Run backtests on BTC in the 5-minute timeframe and adjust parameters (Supertrend factor, MACD settings, risk-reward ratio) to find the optimal configuration for the 60% win ratio.

Fine-Tuning Parameters:

Adjust supertrendFactor and macdFastLength to find more optimal values based on BTC's market behavior.

Tweak the risk-reward ratio to maximize profitability while maintaining a good win ratio.

Evaluate Market Conditions:

The performance of the strategy can vary based on market volatility. It may be helpful to evaluate performance in different market conditions or pair it with a filter like RSI or volume.

Let me know if you'd like further tweaks or explanations!

Box Chart Overlay StrategyExploring the Box Chart Overlay Strategy with RSI & Bollinger Confirmation

The “Box Chart Overlay Strategy by BD” is a sophisticated TradingView strategy script written in Pine Script (version 5). It combines a box charting method with two widely used technical indicators—Relative Strength Index (RSI) and Bollinger Bands—to generate trade entries. In this article, we break down the strategy’s components, its logic, and how it visually represents trading signals on the chart.

1. Strategy Setup and User Inputs

Strategy Declaration

At the top of the script, the strategy is declared with key parameters:

Overlay: The indicator is plotted directly on the price chart.

Initial Capital & Position Sizing: It uses a simulated trading account with an initial capital of 10,000 and positions sized as a percentage of equity (10% by default).

Commission: A commission of 0.1% is factored into trades.

Input Parameters

The strategy is highly customizable. Users can adjust various inputs such as: