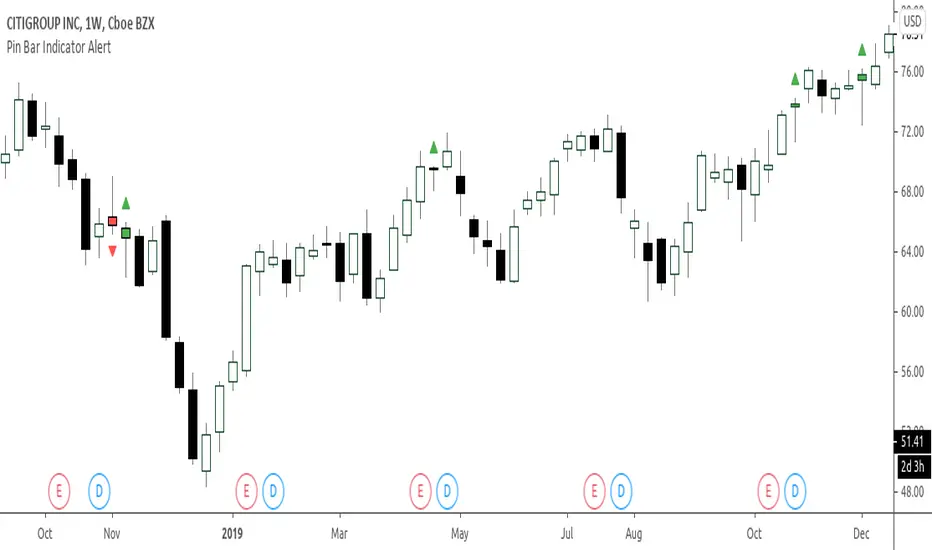

Leledc Exhaustion BarAn mt4 indicator converted to pine,its not always accurate but combined with S/R ,pivots, fibs etc will give an edge.

Dots are the major swings holow circles are the minor swings

more here

www.abundancetradinggroup.com

Indicador Pine Script®