RPS Trading Signals & Backtesting

Overview:

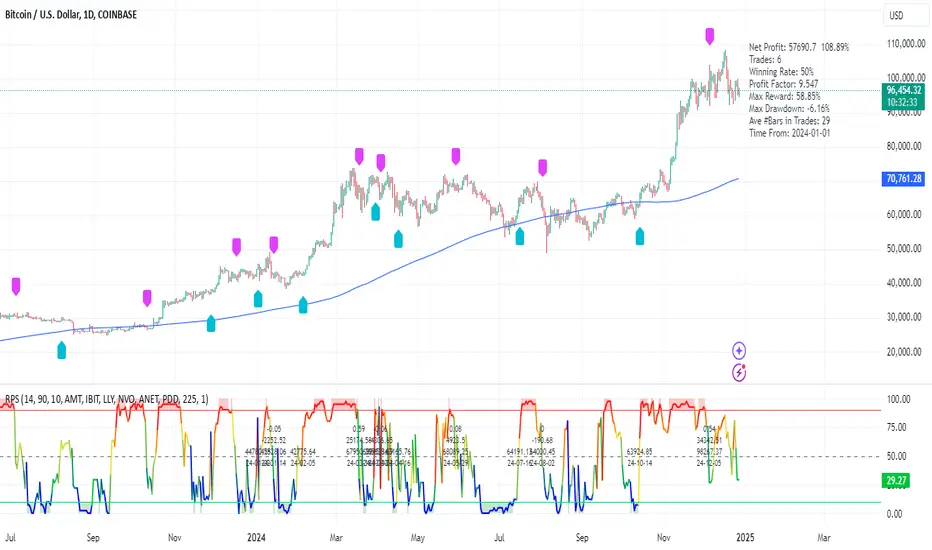

The Enhanced Relative Price Strength (RPS) Indicator is designed for trend traders looking to identify the relative strength of stocks within a select universe. By comparing the price movements of chosen stocks over a specified period, this indicator helps traders make informed decisions about potential buying and selling opportunities.

Key Features:

Relative Strength Ranking: Our RPS indicator ranks the price performance of individual stocks against a curated selection, enabling users to pinpoint which stocks are exhibiting relative strength or weakness.

Customizable Stock Universe: The script evaluates 40 stocks, which include 30 high-weight NDX100 stocks, 4 major index ETFs (SPY, QQQ, DIA, IWM), and allows for the addition of 6 user-defined custom stocks.

Dynamic Color Gradients: The visual representation of the RPS score utilizes a gradient color scheme ranging from purple at low scores to red at high scores, leveraging the color for clear, immediate insight into stock performance.

Threshold Visualization: Users can set specific high (default 85) and low (default 15) thresholds for RPS, highlighted with solid line indicators and area fills. This visual aspect aids traders in quickly spotting entry and exit points.

Trading Signal Generation: The script includes logic for generating buy and sell signals according to defined RPS behaviors relative to the set thresholds, factoring in market conditions based on a long-term moving average.

Backtesting Capabilities: Users can backtest trading signals by inputting desired start and end dates, allowing traders to evaluate the effectiveness of the RPS strategy on historical data for various assets including stocks and cryptocurrencies (e.g., NVDA, LLY, GOOG, BTC, ETH, SOL).

User-Friendly Options: The script allows for adjustments such as moving average lengths, visibility of trading signals, and fills for ease of use and customization according to trading preferences.

How It Works:

The RPS Indicator functions by calculating the performance of stocks relative to each other. Based on the RPS trends, the indicator identifies when to enter or exit trades, providing a framework to capitalize on market movements.

Conclusion:

The Enhanced RPS Indicator aims to empower traders with a powerful analytical tool in their arsenal, tailored to simplify decision-making and bolster trading strategies. As this script evolves, we encourage feedback and collaboration from users to refine and enhance its capabilities further.

Trade Less, Earn More!

Pesquisar nos scripts por "backtest"

PS January Barometer BacktesterPS January Barometer Backtester (PS JBB)

The PS January Barometer Backtester (PS JBB) is a simple strategy designed to test the "January Effect" hypothesis in financial markets. This effect theorizes that stock market performance in January can predict the trend for the rest of the year. The script operates on a monthly timeframe, focusing on capturing and analyzing the price movements in January and their subsequent influence on the market until the end of each year.

User Input:

January Trifecta Selectors

These are user-selectable options allowing traders to incorporate additional criteria into their market analysis.

The Santa Claus Rally refers to a stock market increase typically seen in the last week of December through the first two trading days in January.

The First Five Days Indicator assesses market performance during the initial five days of the year.

Script Operation:

The script automatically detects the start of each year, tracks January's high, and signals entry and exit points for trades based on the strategy's logic. It's an excellent tool for traders and investors looking to explore the January Effect's validity and its potential impact on their trading decisions.

In essence, the "PS January Barometer Backtester" is designed to exploit specific seasonal market trends, particularly focusing on the early part of the year, by analyzing and acting upon defined market movements. This strategy is ideal for traders who focus on yearly cyclical patterns and seek to incorporate historical trends into their trading decisions.

Note: This script is intended for educational and research purposes and should not be construed as financial advice. Always conduct your own due diligence before making trading/investment decisions.

Support and Resistance Backtester [SS]Hey everyone,

Excited to release this indicator I have been working on.

I conceptualized it as an idea a while ago and had to nail down the execution part of it. I think I got it to where I am happy with it, so let me tell you about it!

What it does?

This provides the user with the ability to quantify support and resistance levels. There are plenty of back-test strategies for RSI, stochastics, MFI, any type of technical based indicator. However, in terms of day traders and many swing traders, many of the day traders I know personally do not use or rely on things like RSI, stochastics or MFI. They actually just play the support and resistance levels without attention to anything else. However, there are no tools available to these people who want to, in a way, objectively test their identified support and resistance levels.

For me personally, I use support and resistance levels that are mathematically calculated and I am always curious to see which levels:

a) Have the most touches,

b) Have provided the most support,

c) Have provided the most resistance; and,

d) Are most effective as support/resistance.

And, well, this indicator answers all four of those questions for you! It also attempts to provide some way to support and resistance traders to quantify their levels and back-test the reliability and efficacy of those levels.

How to use:

So this indicator provides a lot of functionality and I think its important to break it down part by part. We can do this as we go over the explanation of how to use it. Here is the step by step guide of how to use it, which will also provide you an opportunity to see the options and functionality.

Step 1: Input your support and resistance levels:

When we open up the settings menu, we will see the section called "Support and Resistance Levels". Here, you have the ability to input up to 5 support and resistance levels. If you have less, no problem, simply leave the S/R level as 0 and the indicator will automatically omit this from the chart and data inclusion.

Step 2: Identify your threshold value:

The threshold parameter extends the range of your support and resistance level by a desired amount. The value you input here should be the value in which you would likely stop out of your position. So, if you are willing to let the stock travel $1 past your support and resistance level, input $1 into this variable. This will extend the range for the assessment and permit the stock to travel +/- your threshold amount before it counts it as a fail or pass.

Step 3: Select your source:

The source will tell the indicator what you want to assess. If you want to assess close, it will look at where the ticker closes in relation to your support and resistance levels. If you want to see how the highs and lows behave around the S/R levels, then change the source to High or Low.

It is recommended to leave at close for optimal results and reliability however.

Step 4: Determine your lookback length:

The lookback length will be the number of candles you want the indicator to lookback to assess the support and resistance level. This is key to get your backtest results.

The recommendation is on timeframes 1 hour or less, to look back 300 candles.

On the daily, 500 candles is recommended.

Step 5: Plot your levels

You will see you have various plot settings available to you. The default settings are to plot your support and resistance levels with labels. This will look as follows:

This will plot your basic support and resistance levels for you, so you do not have to manually plot them.

However, if you want to extend the plotted support and resistance level to visually match your threshold values, you can select the "Plot Threshold Limits" option. This will extend your support and resistance areas to match the designated threshold limits.

In this case on MSFT, I have the threshold limit set at $1. When I select "Plot Threshold Limits", this is the result:

Plotting Passes and Fails:

You will notice at the bottom of the settings menu is an option to plot passes and plot fails. This will identify, via a label overlaid on the chart, where the support and resistance failures and passes resulted. I recommend only selecting one at a time as the screen can get kind of crowded with both on. here is an example on the MSFT chart:

And on the larger timeframe:

The chart

The chart displays all of the results and counts of your support and resistance results. Some things to pay attention to use the chart are:

a) The general success rate as support vs resistance

Rationale: Support levels may act as resistance more often than they do support or vice versa. Let's take a look at MSFT as an example:

The chart above shows the 334.07 level has acted as very strong support. It has been successful as support almost 82% of the time. However, as resistance, it has only been successful 33% of the time. So we could say that 334 is a strong key support level and an area we would be comfortable longing at.

b) The number of touches:

Above you will see the number of touches pointed out by the blue arrow.

Rationale: The number of touches differs from support and resistance. It counts how many times and how frequently a ticker approaches your support and/or resistance area and the duration of time spent in that area. Whereas support and resistance is determined by a candle being either above or below a s/r area, then approaching that area and then either failing or bouncing up/down, the number of touches simply assesses the time spent (in candles) around a support or resistance level. This is key to help you identify if a level has frequent touches/consolidation vs other levels and can help you filter out s/r levels that may not have a lot of touches or are infrequently touched.

Closing comments:

So this is pretty much the indicator in a nutshell. Hopefully you find it helpful and useful and enjoy it.

As always let me know your questions/comments and suggestions below.

As always I appreciate all of you who check out, try out and read about my indicators and ideas. I wish you all the safest trades and good luck!

Grid Spot Trading Algorithm V2 - The Quant ScienceGrid Spot Trading Algorithm V2 is the last grid trading algorithm made by our developer team.

Grid Spot Trading Algorithm V2 is a fixed 10-level grid trading algorithm. The grid is divided into an accumulation area (red) and a selling area (green).

In the accumulation area, the algorithm will place new buy orders, selling the long positions on the top of the grid.

BUYING AND SELLING LOGIC

The algorithm places up to 5 limit orders on the accumulation section of the grid, each time the price cross through the middle grid. Each single order uses 20% of the equity.

Positions are closed at the top of the grid by default, with the algorithm closing all orders at the first sell level. The exit level can be adjusted using the user interface, from the first level up to the fifth level above.

CONFIGURING THE ALGORITHM

1) Add it to the chart: Add the script to the current chart that you want to analyze.

2) Select the top of the grid: Confirm a price level with the mouse on which to fix the top of the grid.

3) Select the bottom of the grid: Confirm a price level with the mouse on which to fix the bottom of the grid.

4) Wait for the automatic creation of the grid.

USING THE ALGORITHM

Once the grid configuration process is completed, the algorithm will generate automatic backtesting.

You can add a stop loss that destroys the grid by setting the destruction price and activating the feature from the user interface. When the stop loss is activated, you can view it on the chart.

Rocket Grid Algorithm - The Quant ScienceThe Rocket Grid Algorithm is a trading strategy that enables traders to engage in both long and short selling strategies. The script allows traders to backtest their strategies with a date range of their choice, in addition to selecting the desired strategy - either SMA Based Crossunder or SMA Based Crossover.

The script is a combination of trend following and short-term mean reversing strategies. Trend following involves identifying the current market trend and riding it for as long as possible until it changes direction. This type of strategy can be used over a medium- to long-term time horizon, typically several months to a few years.

Short-term mean reversing, on the other hand, involves taking advantage of short-term price movements that deviate from the average price. This type of strategy is usually applied over a much shorter time horizon, such as a few days to a few weeks. By rapidly entering and exiting positions, the strategy seeks to capture small, quick gains in volatile market conditions.

Overall, the script blends the best of both worlds by combining the long-term stability of trend following with the quick gains of short-term mean reversing, allowing traders to potentially benefit from both short-term and long-term market trends.

Traders can configure the start and end dates, months, and years, and choose the length of the data they want to work with. Additionally, they can set the percentage grid and the upper and lower destroyers to manage their trades effectively. The script also calculates the Simple Moving Average of the chosen data length and plots it on the chart.

The trigger for entering a trade is defined as a crossunder or crossover of the close price with the Simple Moving Average. Once the trigger is activated, the script calculates the total percentage of the side and creates a grid range. The grid range is then divided into ten equal parts, with each part representing a unique grid level. The script keeps track of each grid level, and once the close price reaches the grid level, it opens a trade in the specified direction.

The equity management strategy in the script involves a dynamic allocation of equity to each trade. The first order placed uses 10% of the available equity, while each subsequent order uses 1% less of the available equity. This results in the allocation of 9% for the second order, 8% for the third order, and so on, until a maximum of 10 open trades. This approach allows for risk management and can help to limit potential losses.

Overall, the Rocket Grid Algorithm is a flexible and powerful trading strategy that can be customized to meet the specific needs of individual traders. Its user-friendly interface and robust backtesting capabilities make it an excellent tool for traders looking to enhance their trading experience.

Bar Count for BacktestingHello!

Not much special about this script; you can use date & time, or bar count, to ascertain the number of bars in a time period for backtesting.

This script can be used in conjunction with large scripts incorporating complex intricacies that won't load on 20,000+ bar data sets.

If your script's load time transcends the TV allotted load time - use this script to quickly determine the number of bars in the data set.

Through trial & error you should be able to determine the approximate number of bars your script can execute on without exceeding the imposed time limit!

The image above shows a user-defined time window and, consequently, the script returns the number of bars that constitute the time period.

You can drag the white vertical lines to efficiently configure the calculated time period.

The image above shows functionality for the "Bars Back" feature.

Enjoy!

Gann HiLo Activator Strategy█ OVERVIEW

Strategy based on the Gann Hilo Activator . This is a trend following strategy, which means it will go long (and close the previous short position) once the price closes above the high SMA, and go short (and close the previous long position) once the price closes below the low SMA.

█ PARAMETERS

- Length

- Displace (or offset): default is 1

- Begin from start: strategy will run since the beggining

- From year, month, day: Choose an specific date to start backtesting (must disable the parameter above to work)

█ HOW TO USE

After choosing the start date to run the strategy, you can change the length field and look at the backtest results to find the most optimal settings for the current symbol.

This strategy was tested on the stock and crypto market with good results. Hope you enjoy!

200DMA last DOM - ajhImplements and backtests a simple 200 day moving average trend following rules based on last day of month to limits trades to 12 per year.

From the book : 5 BEST Moving Average Strategies (That beat buy and hold) by Steve Burns and Holly Burns

Click on the cog to set the input date range eg; 2000-01-01 to 2016-12-31

The book back tested SP500 returns from 2000-2016 317% using this method vs 125% buy and hold only with less drawdown.

Simple 200 day moving average test and trading on last day of month.

(you may find it trades on next available day close to end of month as not all dates can be traded weekends etc..)

Rules are ;

1. if last day of month and stock over 200 day moving average, then go long 100%

2. if last day of month and stock under 200 day moving average, then close long 100% and goto cash.

Aims to miss market declines and keep you long for upside.

Note: Have found doesn't work well in choppy markets moving sideways like the FTSE100 for same period 2000-2016 and causes losses. Also for many stocks.

Flawless Victory Strategy - 15min BTC Machine Learning StrategyHello everyone, I am a heavy Python programmer bringing machine learning to TradingView. This 15 minute Bitcoin Long strategy was created using a machine learning library and 1 year of historical data in Python. Every parameter is hyper optimized to bring you the most profitable buy and sell signals for Bitcoin on the 15min chart. The historical Bitcoin data was gathered from Binance API, in case you want to know the best exchange to use this long strategy. It is a simple Bollinger Band and RSI strategy with two versions included in the tradingview settings. The first version has a Sharpe Ratio of 7.5 which is amazing, and the second version includes the best stop loss and take profit positions with a Sharpe Ratio of 2.5 . Let me talk a little bit more about how the strategy works. The buy signal is triggered when close price is less than lower Bollinger Band at Std Dev 1, and the RSI is greater than a certain value. The sell signal is triggered when close price is greater than upper Bollinger Band at Std Dev 1, and the RSI is greater than a certain value. What makes this strategy interesting is the parameters the Machine Learning library found when backtesting for the best Sharpe Ratio. I left my computer on for about 28 hours to fully backtest 5000 EPOCHS and get the results. I was able to create a great strategy that might be one of TradingView's best strategies out on the website today. I will continue to apply machine learning to all my strategies from here on forward. Please Let me know if you have any questions or certain strategies you would like me to hyper optimize for you. I'm always willing to create profitable strategies!

P.S. You can always pyramid this strategy for more gains! I just don't add pyramiding when creating my strategies because I want to show you the true win/loss ratio based buying one time and one selling one time. I feel like when creating a strategy that includes pyramiding right off the bat falsifies the win rate. This is my way of being transparent with you all. Have fun trading!

Custom Triple Moving Average Strategy | Auto BacktestingCreate your own MA Strategy set of up to three moving averages!

Auto Backtesting.

Cloud between MA1 and MA2.

Many different MA types to choose from.

Totally Custom!

Happy Trading, and algorithm analysis!

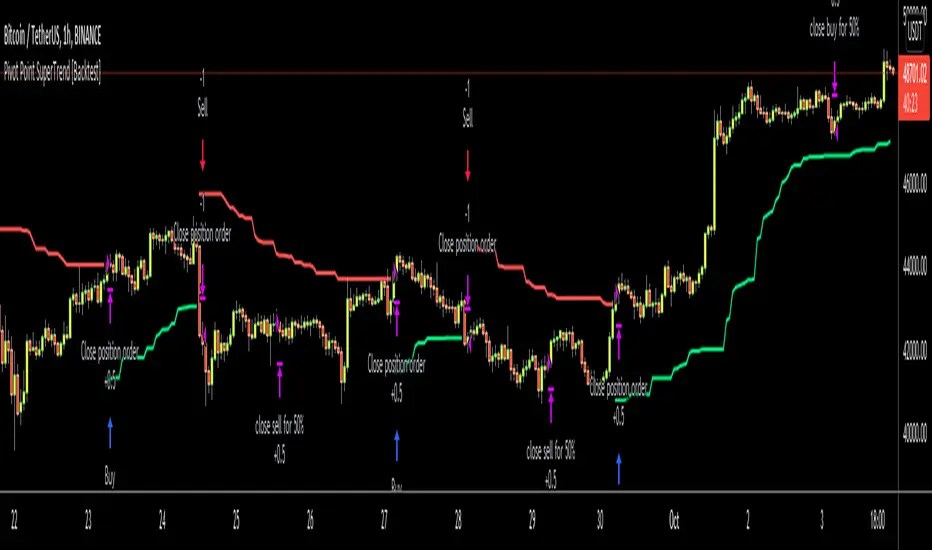

Pivot Point SuperTrend [Backtest]Hello All,

This is backtesting result of following indicator/strategy. I didn't work on adding other indicators. maybe in the future I can try to combine this with other indicators.

You can visit following link to see "Pivot Point SuperTrend" . by using this backtesting tool, you can test&find better options

There is option "Use Center Line to Close Entry for 50%" . by default it's not enabled. if you enable this option, pivot point center line may push you to close your entry for 50% (can be used as early stoploss/take profit line if you think it's risky)

Enjoy!

NVT Signal with RMA and Thresholds (Strategy / Backtest)This is the strategy w/ backtester and trailing-stop / stop-loss for kishin's NVT alerts

Ergotic MACD Strategy [forked from HPotter]Ergotic MACD Strategy forked from HPotter

In addition to this fine script you will find some additional features:

- Backtester

- Alerts

- Filters: RSI, MFI, Price trend

- Trailing Stop Loss

- Other minor adjustments

Strategy Backtester TemplateA template for building a strategy tester:

- date range selector

- stop loss

- take profit

- long and short strategy type selector

Manual Backtest Dashboard (100 Trades)Manual Backtest Dashboard (100 Trades) is a lightweight TradingView indicator designed to help traders manually record and evaluate their trading performance directly on the chart. This tool is built specifically for discretionary traders such as SMC, price action, scalping, and intraday traders who want to analyze their win rate and overall performance without relying on the Strategy Tester.

The indicator works by allowing users to input their trade results manually through the settings panel. Each trade is recorded using simple values: 1 for a winning trade, -1 for a losing trade, and 0 for an empty or uncounted trade. The dashboard automatically calculates the total number of trades entered, the number of wins and losses, and the win rate percentage in real time. Users do not need to fill all 100 trade slots, as only trades with non-zero values are included in the calculations.

This indicator does not place trades or generate buy and sell signals. Instead, it focuses purely on performance evaluation, making it ideal for subjective backtesting, forward testing, and manual trading journals. The dashboard is clean, lightweight, and does not clutter the price chart, ensuring a smooth and distraction-free trading experience. The script is stable, efficient, and does not repaint, making it a reliable tool for traders who want to track and improve their consistency over time.

My Swiftlike Algo Backtest ATR SL/TP HH/HL/LH/LL BOS/CHOCHSwift-Like Algo is a trend-following strategy that trades pullbacks using EMA trend direction, market structure (HH/HL/LH/LL), and ATR-based risk management.

It enters only in the direction of the trend, with automatic Stop-Loss, TP1, and TP2, and supports full strategy backtesting.

Best used on 15m–4H timeframes for crypto, forex, and indices.

⚠️ For educational and testing purposes only.

RSI Signal Backtest Bounce AlertRSI crosses below 5min signal line, bounce above 50 RSI and crosses bullish back above signal line. Once it backtests signal the indicator will fire.

Hilega Milega v6 - Pure EMA/SMA (Nitesh Kumar) + Full BacktestHilega to milega

he Hilega Milega Strategy, inspired by the technique of Nitesh Kumar, is designed for intraday and swing traders who want structured entries and exits with clear demand–supply logic.

🔑 Core Features

Demand & Supply Zones – Automatically plots potential strong buying and selling zones for high-probability trades.

Trend Identification – Uses a blend of EMAs/SMA crossovers to identify bullish and bearish market bias.

Buy & Sell Signals – Generates real-time visual signals based on “Hilega Milega” rules for quick decision-making.

Risk Management – Suggested stop-loss levels are derived from recent demand–supply areas to minimize drawdowns.

Backtesting Enabled – Traders can test the performance across multiple assets (stocks, forex, crypto, commodities).

📊 How It Works

Buy Signal → When price action confirms a bullish zone with supporting trend filters.

Sell Signal → When price action confirms a bearish zone or reversal pattern.

Flat/Exit → Position closed when opposite signal triggers or demand–supply imbalance fades.

⚡ Best Use Cases

Intraday trading (5m, 15m, 1H charts).

Swing trading (4H, Daily charts).

Works across stocks, crypto, commodities, and forex.

⚠️ Disclaimer: This strategy is for educational purposes. Backtest thoroughly and apply proper risk management before live trading.

Multi-MA Strategy Analyzer with BacktestMulti-MA Strategy Analyzer with Backtest

This TradingView Pine Script indicator is designed to analyze multiple moving averages (SMA or EMA) dynamically and identify the most profitable one based on historical performance.

Features

Dynamic MA Range:

Specify a minLength, maxLength, and step size.

Automatically calculates up to 20 MAs.

Custom MA Calculation:

Uses custom SMA and EMA implementations to support dynamic length values.

Buy/Sell Logic:

Buy when price crosses above a MA.

Sell when price crosses below.

Supports both long and short trades.

Performance Tracking:

Tracks PnL, number of trades, win rate, average profit, and drawdown.

Maintains individual stats for each MA.

Best MA Detection:

Automatically highlights the best-performing MA.

Optional showBestOnly toggle to focus only on the best line and its stats.

Visualization:

Up to 20 plot() calls (static) for MAs.

Green highlight for the best MA.

Color-coded result table and chart.

Table View

When showBestOnly = false, the table displays all MAs with stats.

When showBestOnly = true, the table displays only the best MA with a summary row.

Includes:

Best MA length

Total PnL

Number of trades

Win rate

Avg PnL per trade

Max Drawdown

Configuration

minLength (default: 10)

maxLength (default: 200)

step (default: 10)

useEMA: Toggle between EMA and SMA

showBestOnly: Focus on best-performing MA only

Notes

MA plotting is static, limited to 20 total.

Table supports highlighting and is optimized for performance.

Script is structured to run efficiently using arrays and simple int where required.

Potential Extensions

Add visual buy/sell arrows

Export stats to CSV

Strategy tester conversion

Custom date range filtering for backtesting

Author: Muhammad Wasim

Version: 1.0

Ehlers Combo Strategy🚀 Presenting the Enhanced Ehlers Combo Strategy 🚀

Hello Traders! 👋 I'm thrilled to share the latest version of the Ehlers Combo Strategy v2.0. This powerful algorithm combines Ehlers Elegant Oscillator, Decycler, Instantaneous Trendline, Spearman Rank, and introduces the Signal to Noise Ratio for even more precise trading signals.

📊 Strategy Highlights:

Ehlers Elegant Oscillator: Captures market momentum and turning points.

Ehlers Decycler: Filters out market noise for clearer trend signals.

Instantaneous Trendline: Offers a dynamic view of the market trend.

Spearman Rank: Analyzes market rank correlations for enhanced insights.

Signal to Noise Ratio (SNR): Filters out noise for more accurate signals.

💡 Key Features & Customizations:

Adaptive Length: Enable adaptive length based on the market's current conditions.

SNR Threshold: Set your desired SNR threshold for filtering signals.

Exit Length: Define the length for exit signals.

📈 Trading Signals:

Long Entry: Elegant Oscillator and Decycler cross above 0, source crosses above Decycler, source is greater than an increasing Instantaneous Trendline, Spearman Rank is positive, and SNR exceeds the threshold.

Long Exit: Source crosses below the Instantaneous Trendline after entering a long position.

Short Entry: Elegant Oscillator and Decycler cross below 0, source crosses below Decycler, source is less than a decreasing Instantaneous Trendline, Spearman Rank is negative, and SNR exceeds the threshold.

Short Exit: Source crosses above the Instantaneous Trendline after entering a short position.

📊 Insights & Enhancements:

Dynamic Length: The strategy adapts its length dynamically based on market conditions.

Improved SNR: Signal to Noise Ratio ensures better filtering of signals.

Enhanced Visualization: The Elegant Oscillator now features improved color coding for a clearer interpretation.

🚨 Disclaimer:

Trading involves risk, and this script should be used judiciously. It's not a guaranteed profit machine, but with careful use, it can be a valuable addition to your toolkit.

Feel free to backtest, tweak, and make it your own! Let's conquer the markets together! 💪📈

🚀✨ Happy Trading! ✨🚀

---

🙌 Credits:

A big shoutout to the original contributors:

@blackcat1402

@cheatcountry

@DasanC

X48 - Strategy | MA Type Cross + TPSL | Future&Spot | V.2Thank You For Open Source Code, This Strategy Ref. By 1.Simple Strategy Like MA Crossover For Long/Short or Spot Trade, 2. CDC Action Zone V.2 for BarPaint

This Strategy Mixing With MA Crossover Strategy and BarPaint By CDC Action Zone and TP/SL by Varbara

### How To Use Strategy : Setting EMA/SMA Crossover EMA/SMA, Any Value If You Want

For Long Position : Cross Up

For Short Position : Cross Down

Can Use With Spot Trade : Cross Up = Buy, Cross Down = Sell

TP/SL When Your OrderSize Change From any % Of Your TP/SL Value

### In Strategy Setting

Intitial Capital = Ex. 200

Order Size = Should Be Money Management Not Use 100% of Capital Ex. 10% of Capital (200$) = Order Size 20$

StopLoss and Take Profit = If You Run Trend TF 4H+ or 1D+ You Can Change TP% = 1,000% for nonlimit and Stop Loss 5 - 20% from your order size

Ex. Stoploss 15% = OrderSize / 100 x %SL = 20$/100 x 15% = 3$ Loss from order size 20$ (if you not set stop loss.)

Base Currency = (Your Currency) # Ex. USD

Commission = (Your Trading Fee) # Ex. Future Fee Can Check At Binance Fee Rate > www.binance.com > Choose Your Fee Type, Ex. USD M Future (Regular User) = 0.02 (Maker), 0.04 (Taker)

Commission Symbol Type = % # (Ref. By Binance Fee Rate)

### Notice ####

Default Setting It's Realistic From Normal Life Ex. Capital 200$ / Ordersize 20$ (10%)/ Commission 0.1% (Buy+Sell) / Slippage = 2 / TP = 1000% (nonlimit) / SL = 15%/OrderSize

Low Risk But High Return, Good Luck

### Bot Auto Trade by X4815162342 ###

if you wanna try my bot auto trade X48-3in1-bot : Contact My Line ID : x4815x

Full Command Alert For This Strategy If You Wanna See It's

'{"ex":"'+markettype+'","side": "'+longcommand+'", "amount": "@{{strategy.order.contracts}}", "symbol": "{{ticker}}", "passphrase": "'+passphrase+'","leverage":"'+str.tostring(leveragex)+'"}'

'{"ex":"'+markettype+'","side": "'+shortcommand+'", "amount": "@{{strategy.order.contracts}}", "symbol": "{{ticker}}", "passphrase": "'+passphrase+'","leverage":"'+str.tostring(leveragex)+'"}'

But Easy Than Full Command Just Use Thisssssss !! Strategy Be Manage Auto Long and Short or TPSL Position

You Don't Do Anything Just Use This Message to Alerts Message

{{strategy.order.alert_message}}

### If you don't use bot but just looking for strategy test ####

Just Pass Bot Setting Function It's Nothing Effect For Strategy !!!!!!

Let's Enjoy With Your Strategy BackTest 😁

Remember Beware Max drawdown%. I'm Recommend Lower Than 10% It's Very Good.

action zone - ATR stop reverse order strategy v0.1 by 9nckACTION ZONE-ATR MOD v0.1 DOCUMENTATION

Overview

This tradingview pine script strategy is mainly created to enrich my coding skill. It is a combination of “CDC-ACTIONZONE” and my personal studies of trading techniques in various sources e.g.book, course or blog. This strategy purposefully built to connect with my automatic trading bot. However, It will be very useful to aid your trading routine by diminishing mental distraction which possibly leads to bad trades.

How does it work?

This strategy will do a basic simple thing that most traders do by creating entry signals on both sides long/short and also set the stop loss. Furthermore, It will also reverse the order (from long to short and vice versa (if long/short conditions are met). Finally, it will recalculate the stop loss/take profit price in every complete bar to increase the chance of winning and limit our loss.

Entry rules(Long/Short)

If you have no open order, an order will be created when a fast EMA crosses(up(long)/down(short) the slow EMA(It’s as simple as that).

If you have an open order, the current order will be (sold if long, covered if short) and the opposite side order will be created.

Exit and Reverse rules(Long/Short)

If fast EMA cross (DOWN(long), UP(short)), the current order will be closed, THE OPPOSITE SIDE ORDER WILL ALSO BE CREATED.

Risk management

FLEX STOP PRICE : initial value will be set at the bar which order created. It is a fast ema (+/-) MIDDLE ATR value.

If MIDDLE ATR value rises, it will be our new stop price.

If MIDDLE ATR value falls, stop price unchanged

If Price OVERBOUGHT(long)/SOLD(short), LOW of that bar will be a new stop price.

Minimum position hold period

In order to eliminate risk of repeatedly open, close orders in sideway trends. Minimum hold period must be passed to start exit our position. However, It always respects stop loss prices. The value refers to the number of bars.

MUST READ!!!

This strategy uses only MARKET ORDER. If you trade with a bot, make sure you choose only enormous market cap tokens.

This strategy is bi-direction strategy. It will work best in the DERIVATIVE market.

It was initially designed to compete in the cryptocurrency market which has very high volume and volatility.

I only use this strategy in 1HR (acceptable change rate, optimum trade frequency)

How (should) we use it?

Choose crypto future pairs (recommend only top 10-15 market volume pairs in Binance, let’s say 1000M+ trade value)

Choose your time frame (1H is strongly recommended)

Setup your portfolio profile (Setting->Properties) such as Initial cap, order size, commission. DO NOT USE CAL ON EVERY TICK IT WILL CAUSE REPAINTING AND YOUR CAPITAL IS BLEEDING !!!

BACKTEST FIRST!! Back test is a combination of art, math and statis(and a bit of luck). You can apply to train and test methods or whatever you are familiar with. In my opinion, your test period should include UPTREND, SIDEWAY, DOWNTREND. Fine tune fast, slow ema first(my best ema length of 1H timeframe around 7-10, 17-22). Try to eliminate fault breakout trade and use other options only necessary. Hopefully we can use automatic optimization on Pine Script soon.

Don’t forget to turn off using a specific backtest date option to start your strategy.A

THIS IS NOT A PERFECT (OR EVEN PROFITABLE) STRATEGY. USE AT YOUR OWN RISK AND TRADE RESPONSIBLY. DYOR DUDE.