OBV ATR Strategy (OBV Breakout Channel) bas20230503ผมแก้ไขจาก OBV+SMA อันเดิม ของเดิม ดูที่เส้น SMA สองเส้นตัดกันมั่นห่วยแตกสำหรับที่ผมลองเทรดจริง และหลักการเบรค ได้แรงบันดาลใจ ATR จาก เทพคอย ที่ใช้กับราคา แต่นี้ใช้กับ OBV แทน

และผมใช้เจมินี้ เพื่อแก้ ให้ เป็น strategy เพื่อเช็คย้อนหลังได้ง่ายกว่าเดิม

หลักการง่ายคือถ้ามันขึ้น มันจะขึ้นเรื่อยๆ

เขียน แบบสุภาพ (น่าจะอ่านได้ง่ายกว่าผมเขียน)

สคริปต์นี้ได้รับการพัฒนาต่อยอดจากแนวคิด OBV+SMA Crossover แบบดั้งเดิม ซึ่งจากการทดสอบส่วนตัวพบว่าประสิทธิภาพยังไม่น่าพอใจ กลยุทธ์ใหม่นี้จึงเปลี่ยนมาใช้หลักการ "Breakout" ซึ่งได้รับแรงบันดาลใจมาจากการใช้ ATR สร้างกรอบของราคา แต่เราได้นำมาประยุกต์ใช้กับ On-Balance Volume (OBV) แทน นอกจากนี้ สคริปต์ได้ถูกแปลงเป็น Strategy เต็มรูปแบบ (โดยความช่วยเหลือจาก Gemini AI) เพื่อให้สามารถทดสอบย้อนหลัง (Backtest) และประเมินประสิทธิภาพได้อย่างแม่นยำ

หลักการของกลยุทธ์: กลยุทธ์นี้ทำงานบนแนวคิดโมเมนตัมที่ว่า "เมื่อแนวโน้มได้เกิดขึ้นแล้ว มีโอกาสที่มันจะดำเนินต่อไป" โดยจะมองหาการทะลุของพลังซื้อ-ขาย (OBV) ที่แข็งแกร่งเป็นพิเศษเป็นสัญญาณเข้าเทร

----

สคริปต์นี้เป็นกลยุทธ์ (Strategy) ที่ใช้ On-Balance Volume (OBV) ซึ่งเป็นอินดิเคเตอร์ที่วัดแรงซื้อและแรงขายสะสม แทนที่จะใช้การตัดกันของเส้นค่าเฉลี่ย (SMA Crossover) ที่เป็นแบบพื้นฐาน กลยุทธ์นี้จะมองหาการ "ทะลุ" (Breakout) ของพลัง OBV ออกจากกรอบสูงสุด-ต่ำสุดของตัวเองในรอบที่ผ่านมา

สัญญาณกระทิง (Bull Signal): เกิดขึ้นเมื่อพลังการซื้อ (OBV) แข็งแกร่งจนสามารถทะลุจุดสูงสุดของตัวเองในอดีตได้ บ่งบอกถึงโอกาสที่แนวโน้มจะเปลี่ยนเป็นขาขึ้น

สัญญาณหมี (Bear Signal): เกิดขึ้นเมื่อพลังการขาย (OBV) รุนแรงจนสามารถกดดันให้ OBV ทะลุจุดต่ำสุดของตัวเองในอดีตได้ บ่งบอกถึงโอกาสที่แนวโน้มจะเปลี่ยนเป็นขาลง

ส่วนประกอบบนกราฟ (Indicator Components)

เส้น OBV

เส้นหลัก ที่เปลี่ยนเขียวเป็นแดง เป็นทั้งแนวรับและแนวต้าน และ จุด stop loss

เส้นนี้คือหัวใจของอินดิเคเตอร์ ที่แสดงถึงพลังสะสมของ Volume

เมื่อเส้นเป็นสีเขียว (แนวรับ): จะปรากฏขึ้นเมื่อกลยุทธ์เข้าสู่ "โหมดกระทิง" เส้นนี้คือระดับต่ำสุดของ OBV ในอดีต และทำหน้าที่เป็นแนวรับไดนามิก

เมื่อเส้นกลายเป็นสีแดงสีแดง (แนวต้าน): จะปรากฏขึ้นเมื่อกลยุทธ์เข้าสู่ "โหมดหมี" เส้นนี้คือระดับสูงสุดของ OBV ในอดีต และทำหน้าที่เป็นแนวต้านไดนามิก

สัญลักษณ์สัญญาณ (Signal Markers):

Bull 🔼 (สามเหลี่ยมขึ้นสีเขียว): คือสัญญาณ "เข้าซื้อ" (Long) จะปรากฏขึ้น ณ จุดที่ OBV ทะลุขึ้นไปเหนือกรอบด้านบนเป็นครั้งแรก

Bear 🔽 (สามเหลี่ยมลงสีแดง): คือสัญญาณ "เข้าขาย" (Short) จะปรากฏขึ้น ณ จุดที่ OBV ทะลุลงไปต่ำกว่ากรอบด้านล่างเป็นครั้งแรก

วิธีการใช้งาน (How to Use)

เพิ่มสคริปต์นี้ลงบนกราฟราคาที่คุณสนใจ

ไปที่แท็บ "Strategy Tester" ด้านล่างของ TradingView เพื่อดูผลการทดสอบย้อนหลัง (Backtest) ของกลยุทธ์บนสินทรัพย์และไทม์เฟรมต่างๆ

ใช้สัญลักษณ์ "Bull" และ "Bear" เป็นตัวช่วยในการตัดสินใจเข้าเทรด

ข้อควรจำ: ไม่มีกลยุทธ์ใดที่สมบูรณ์แบบ 100% ควรใช้สคริปต์นี้ร่วมกับการวิเคราะห์ปัจจัยอื่นๆ เช่น โครงสร้างราคา, แนวรับ-แนวต้านของราคา และการบริหารความเสี่ยง (Risk Management) ของตัวคุณเองเสมอ

การตั้งค่า (Inputs)

SMA Length 1 / SMA Length 2: ใช้สำหรับพล็อตเส้นค่าเฉลี่ยของ OBV เพื่อดูเป็นภาพอ้างอิง ไม่มีผลต่อตรรกะการเข้า-ออกของ Strategy อันใหม่ แต่มันเป็นของเก่า ถ้าชอบ ก็ใช้ได้ เมื่อ SMA สองเส้นตัดกัน หรือตัดกับเส้น OBV

High/Low Lookback Length: (ค่าพื้นฐาน30/แก้ตรงนี้ให้เหมาะสมกับ coin หรือหุ้น ตามความผันผวน ) คือระยะเวลาที่ใช้ในการคำนวณกรอบสูงสุด-ต่ำสุดของ OBV

ค่าน้อย: ทำให้กรอบแคบลง สัญญาณจะเกิดไวและบ่อยขึ้น แต่อาจมีสัญญาณหลอก (False Signal) เยอะขึ้น

ค่ามาก: ทำให้กรอบกว้างขึ้น สัญญาณจะเกิดช้าลงและน้อยลง แต่มีแนวโน้มที่จะเป็นสัญญาณที่แข็งแกร่งกว่า

แน่นอนครับ นี่คือคำแปลฉบับภาษาอังกฤษที่สรุปใจความสำคัญ กระชับ และสุภาพ เหมาะสำหรับนำไปใช้ในคำอธิบายสคริปต์ (Description) ของ TradingView ครับ

---Translate to English---

OBV Breakout Channel Strategy

This script is an evolution of a traditional OBV+SMA Crossover concept. Through personal testing, the original crossover method was found to have unsatisfactory performance. This new strategy, therefore, uses a "Breakout" principle. The inspiration comes from using ATR to create price channels, but this concept has been adapted and applied to On-Balance Volume (OBV) instead.

Furthermore, the script has been converted into a full Strategy (with assistance from Gemini AI) to enable precise backtesting and performance evaluation.

The strategy's core principle is momentum-based: "once a trend is established, it is likely to continue." It seeks to enter trades on exceptionally strong breakouts of buying or selling pressure as measured by OBV.

Core Concept

This is a Strategy that uses On-Balance Volume (OBV), an indicator that measures cumulative buying and selling pressure. Instead of relying on a basic Simple Moving Average (SMA) Crossover, this strategy identifies a "Breakout" of the OBV from its own highest-high and lowest-low channel over a recent period.

Bull Signal: Occurs when the buying pressure (OBV) is strong enough to break above its own recent highest high, indicating a potential shift to an upward trend.

Bear Signal: Occurs when the selling pressure (OBV) is intense enough to push the OBV below its own recent lowest low, indicating a potential shift to a downward trend.

On-Screen Components

1. OBV Line

This is the main indicator line, representing the cumulative volume. Its color changes to green when OBV is rising and red when it is falling.

2. Dynamic Support & Resistance Line

This is the thick Green or Red line that appears based on the strategy's current "mode." This line serves as a dynamic support/resistance level and can be used as a reference for stop-loss placement.

Green Line (Support): Appears when the strategy enters "Bull Mode." This line represents the lowest low of the OBV in the recent past and acts as dynamic support.

Red Line (Resistance): Appears when the strategy enters "Bear Mode." This line represents the highest high of the OBV in the recent past and acts as dynamic resistance.

3. Signal Markers

Bull 🔼 (Green Up Triangle): This is the "Long Entry" signal. It appears at the moment the OBV first breaks out above its high-low channel.

Bear 🔽 (Red Down Triangle): This is the "Short Entry" signal. It appears at the moment the OBV first breaks down below its high-low channel.

How to Use

Add this script to the price chart of your choice.

Navigate to the "Strategy Tester" panel at the bottom of TradingView to view the backtesting results for the strategy on different assets and timeframes.

Use the "Bull" and "Bear" signals as aids in your trading decisions.

Disclaimer: No strategy is 100% perfect. This script should always be used in conjunction with other forms of analysis, such as price structure, key price-based support/resistance levels, and your own personal risk management rules.

Inputs

SMA Length 1 / SMA Length 2: These are used to plot moving averages on the OBV for visual reference. They are part of the legacy logic and do not affect the new breakout strategy. However, they are kept for traders who may wish to observe their crossovers for additional confirmation.

High/Low Lookback Length: (Most Important Setting) This determines the period used to calculate the highest-high and lowest-low OBV channel. (Default is 30; adjust this to suit the asset's volatility).

A smaller value: Creates a narrower channel, leading to more frequent and faster signals, but potentially more false signals.

A larger value: Creates a wider channel, leading to fewer and slower signals, which are likely to be more significant.

Pesquisar nos scripts por "backtest"

GannLSVZO Indicator [Algo Alert]The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Gann Laplace Smoothed Volume Zone Oscillator GannLSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the upgraded Discrete Fourier Transform, the Laplace Stieltjes Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Laplace with Gann Swing Entries and Exits (orange X) and with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

ORIGINALITY & USFULLNESS:

Personal combination of Gann swings and Laplace Stieltjes Transform of a price which results in less noise Volume Zone Oscillator.

The Laplace Stieltjes Transform is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

The Gann swings and the Gan swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Laplace Stieltjes Transform approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Laplace Stieltjes Transform (FLT) and the innovative Double Discrete Fourier Transform (DTF32) soothed price series to suit your analytical needs.

Use dynamic calculation of Laplace coefficient or the static one. You may modify those inputs and Strategy entries with Gann swings.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Fine-tune Inputs: Gann + Laplace Smooth Volume Zone OscillatorUse this Strategy to Fine-tune inputs for the GannLSVZ0 Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Gann Laplace Smoothed Volume Zone Oscillator GannLSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the upgraded Discrete Fourier Transform, the Laplace Stieltjes Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Laplace with Gann Swing Entries and with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

When Indicator/Strategy returns 0 or natural trend, Strategy Closes All it's positions.

ORIGINALITY & USFULLNESS:

Personal combination of Gann swings and Laplace Stieltjes Transform of a price which results in less noise Volume Zone Oscillator.

The Laplace Stieltjes Transform is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

The Gann swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Laplace Stieltjes Transform approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Laplace Stieltjes Transform (FLT) and the innovative Double Discrete Fourier Transform (DTF32) soothed price series to suit your analytical needs.

Use dynamic calculation of Laplace coefficient or the static one. You may modify those inputs and Strategy entries with Gann swings.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Retest Confirm Point TibbuCreating a "Retest Confirm Point" indicator that generates buy and sell signals involves defining criteria to confirm that a price retest is valid before issuing a trade signal. This generally requires identifying a key level (such as support, resistance, or a trendline), detecting a retest of this level, and then confirming the validity of the retest.

Here’s a Pine Script example to help you create such an indicator. This script identifies and confirms retests of previous highs and lows, and generates buy and sell signals based on those retests: Explanation:

Recent High and Low:

The script identifies the highest and lowest prices over a specified lookback period.

These levels are plotted on the chart as reference points.

Retest Conditions:

Retest High: The closing price is within a buffer range around the recent high.

Retest Low: The closing price is within a buffer range around the recent low.

Confirmation:

Confirm High: The closing price reaches a new high over a set number of bars after the retest condition.

Confirm Low: The closing price reaches a new low over a set number of bars after the retest condition.

Signals:

Buy Signal: Issued when a confirmed retest of the recent high occurs.

Sell Signal: Issued when a confirmed retest of the recent low occurs.

Customization:

Lookback Period: Adjust to determine the historical range for finding recent highs and lows.

Confirmation Bars: Change the number of bars used to confirm the retest.

Retest Buffer: Adjust the percentage buffer to fine-tune the retest conditions.

Testing and Optimization:

Backtest: Always backtest the strategy on historical data to ensure it behaves as expected.

Adjust Parameters: Modify parameters based on the asset, timeframe, and market conditions.

Feel free to modify this script further based on your specific trading strategy and needs. If you need help with any additional features or further customization, let me know!

ChatGPT can make mistakes. Check important info.

Fine-tune Inputs: Fourier Smoothed Volume zone oscillator WFSVZ0Use this Strategy to Fine-tune inputs for the (W&)FSVZ0 Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Wavelet & Fourier Smoothed Volume Zone Oscillator (W&)FSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the Discrete Fourier Transform . Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Wavalet and Fourier aproximation with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

When I ndicator/Strategy returns 0 or natural trend , Strategy Closes All it's positions.

ORIGINALITY & USFULLNESS:

Personal combination of Fourier and Wavalet aproximation of a price which results in less noise Volume Zone Oscillator.

The Wavelet Transform is a powerful mathematical tool for signal analysis, particularly effective in analyzing signals with varying frequency or non-stationary characteristics. It dissects a signal into wavelets, small waves with varying frequency and limited duration, providing a multi-resolution analysis. This approach captures both frequency and location information, making it especially useful for detecting changes or anomalies in complex signals.

The Discrete Fourier Transform (DFT) is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

In the next Image you can see that trend is negative on 4h, negative on 12h and positive on 1D. That means trend is negative.

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Wavelet approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Fourier Transform (FFT) , the innovative Double Discrete Fourier Transform (DTF32) and Wavelet soothed Fourier soothed price series to suit your analytical needs.

Image of Wavelet transform with FAST settings, Double Fourier transform with FAST settings. Improved noice reduction with SLOW settings, and standard FSVZO with SLOW settings:

Fast setting are setting by default:

VZO length = 2

NoiceR max Length = 2

Slow settings are:

VZO length = 5 or 7

NoiceR max Length = 8

As you can see fast setting are more volatile. I suggest averaging fast setting on 4h 12h 1d 2d 3d 4d W and M Timeframe to get a clear view on market trend.

What if I want long only when VZO is rising and above 15 not 0?

You have set Setting VzoDifference to 15. That reduces the number of trend changes.

Example of W&FSVZO with VzoDifference 15 than 0:

VZO crossed 0 line but not 15 line and that's why Indicator returns 0 in one case an 1 in another.

What is Smooth length setting?

A way of calculating Bullish or Bearish (W&)FSVZO .

If smooth length is 2 the trend is rising if:

rising = VZO > ta.ema(VZO, 2)

Meaning that we check if VZO is higher that exponential average of the last 2 elements.

If smooth length is 1 the trend is rising if:

rising = VZO_ > VZO_

Use this Strategy to fine-tune inputs for the (W&)FSVZO Indicator.

(Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data)

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame . When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame . I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Trend Deviation strategy - BTC [IkkeOmar]Intro:

This is an example if anyone needs a push to get started with making strategies in pine script. This is an example on BTC, obviously it isn't a good strategy, and I wouldn't share my own good strategies because of alpha decay.

This strategy integrates several technical indicators to determine market trends and potential trade setups. These indicators include:

Directional Movement Index (DMI)

Bollinger Bands (BB)

Schaff Trend Cycle (STC)

Moving Average Convergence Divergence (MACD)

Momentum Indicator

Aroon Indicator

Supertrend Indicator

Relative Strength Index (RSI)

Exponential Moving Average (EMA)

Volume Weighted Average Price (VWAP)

It's crucial for you guys to understand the strengths and weaknesses of each indicator and identify synergies between them to improve the strategy's effectiveness.

Indicator Settings:

DMI (Directional Movement Index):

Length: This parameter determines the number of bars used in calculating the DMI. A higher length may provide smoother results but might lag behind the actual price action.

Bollinger Bands:

Length: This parameter specifies the number of bars used to calculate the moving average for the Bollinger Bands. A longer length results in a smoother average but might lag behind the price action.

Multiplier: The multiplier determines the width of the Bollinger Bands. It scales the standard deviation of the price data. A higher multiplier leads to wider bands, indicating increased volatility, while a lower multiplier results in narrower bands, suggesting decreased volatility.

Schaff Trend Cycle (STC):

Length: This parameter defines the length of the STC calculation. A longer length may result in smoother but slower-moving signals.

Fast Length: Specifies the length of the fast moving average component in the STC calculation.

Slow Length: Specifies the length of the slow moving average component in the STC calculation.

MACD (Moving Average Convergence Divergence):

Fast Length: Determines the number of bars used to calculate the fast EMA (Exponential Moving Average) in the MACD.

Slow Length: Specifies the number of bars used to calculate the slow EMA in the MACD.

Signal Length: Defines the number of bars used to calculate the signal line, which is typically an EMA of the MACD line.

Momentum Indicator:

Length: This parameter sets the number of bars over which momentum is calculated. A longer length may provide smoother momentum readings but might lag behind significant price changes.

Aroon Indicator:

Length: Specifies the number of bars over which the Aroon indicator calculates its values. A longer length may result in smoother Aroon readings but might lag behind significant market movements.

Supertrend Indicator:

Trendline Length: Determines the length of the period used in the Supertrend calculation. A longer length results in a smoother trendline but might lag behind recent price changes.

Trendline Factor: Specifies the multiplier used in calculating the trendline. It affects the sensitivity of the indicator to price changes.

RSI (Relative Strength Index):

Length: This parameter sets the number of bars over which RSI calculates its values. A longer length may result in smoother RSI readings but might lag behind significant price changes.

EMA (Exponential Moving Average):

Fast EMA: Specifies the number of bars used to calculate the fast EMA. A shorter period results in a more responsive EMA to recent price changes.

Slow EMA: Determines the number of bars used to calculate the slow EMA. A longer period results in a smoother EMA but might lag behind recent price changes.

VWAP (Volume Weighted Average Price):

Default settings are typically used for VWAP calculations, which consider the volume traded at each price level over a specific period. This indicator provides insights into the average price weighted by trading volume.

backtest range and rules:

You can specify the start date for backtesting purposes.

You can can select the desired trade direction: Long, Short, or Both.

Entry and Exit Conditions:

LONG:

DMI Cross Up: The Directional Movement Index (DMI) indicates a bullish trend when the positive directional movement (+DI) crosses above the negative directional movement (-DI).

Bollinger Bands (BB): The price is below the upper Bollinger Band, indicating a potential reversal from the upper band.

Momentum Indicator: Momentum is positive, suggesting increasing buying pressure.

MACD (Moving Average Convergence Divergence): The MACD line is above the signal line, indicating bullish momentum.

Supertrend Indicator: The Supertrend indicator signals an uptrend.

Schaff Trend Cycle (STC): The STC indicates a bullish trend.

Aroon Indicator: The Aroon indicator signals a bullish trend or crossover.

When all these conditions are met simultaneously, the strategy considers it a favorable opportunity to enter a long trade.

SHORT:

DMI Cross Down: The Directional Movement Index (DMI) indicates a bearish trend when the negative directional movement (-DI) crosses above the positive directional movement (+DI).

Bollinger Bands (BB): The price is above the lower Bollinger Band, suggesting a potential reversal from the lower band.

Momentum Indicator: Momentum is negative, indicating increasing selling pressure.

MACD (Moving Average Convergence Divergence): The MACD line is below the signal line, signaling bearish momentum.

Supertrend Indicator: The Supertrend indicator signals a downtrend.

Schaff Trend Cycle (STC): The STC indicates a bearish trend.

Aroon Indicator: The Aroon indicator signals a bearish trend or crossover.

When all these conditions align, the strategy considers it an opportune moment to enter a short trade.

Disclaimer:

THIS ISN'T AN OPTIMAL STRATEGY AT ALL! It was just an old project from when I started learning pine script!

The backtest doesn't promise the same results in the future, always do both in-sample and out-of-sample testing when backtesting a strategy. And make sure you forward test it as well before implementing it!

Furthermore this strategy uses both trend and mean-reversion systems, that is usually a no-go if you want to build robust trend systems .

Don't hesitate to comment if you have any questions or if you have some good notes for a beginner.

Booz StrategyBooz Backtesting : Booz Backtesting is a method for analyzing the performance of your current trading strategy . Booz Backtesting aims to help you generate results and evaluate risk and return without risking real capital.

The Booz Backtesting is the Booz Super Swing Indicator equivalent but gives you the ability to backtest data on different charts.

This is an Indicator created for the purpose of identifying trends in Multiple Markets, it is based on Moving Average Crossover and extra features.

Swing Trading: This function allows you to navigate the entire trend until it is not strong enough, so you can compare it with fixed parameters such as Take Profit and Stop Loss.

Take Profit and Stop Loss function: With this function you will be able to choose the most optimal parameters and see in real time the results in order to choose the best combination of parameters.

Leverage : We have this function for the futures markets where you can check which is the most appropriate leverage for your operation.

Trend Filter: allows you to take multiple entries in the same direction of the market.

If the market crosses below the 200 moving average, it will take only short entries.

If the market crosses above the 200 moving average, it will take only long entries.

Timeframes

Charting from 1 Hour, 4 Hour, Daily, Weekly, Weekly

Markets :Booz Backtesting can be tested in Cryptocurrency, Stocks and Futures markets.

Background Color : at a glance, you can see what cycle the market is in.

Green background : Shows that the market is in a bullish cycle.

Red background: Shows that the market is in a bearish cycle.

Bozz Strategy

Booz Backtesting : Booz Backtesting is a method for analyzing the performance of your current trading strategy . Booz Backtesting aims to help you generate results and evaluate risk and return without risking real capital.

The Booz Backtesting is the Booz Super Swing Indicator equivalent but gives you the ability to backtest data on different charts.

This is an Indicator created for the purpose of identifying trends in Multiple Markets, it is based on Moving Average Crossover and extra features.

Swing Trading: This function allows you to navigate the entire trend until it is not strong enough, so you can compare it with fixed parameters such as Take Profit and Stop Loss.

Take Profit and Stop Loss function: With this function you will be able to choose the most optimal parameters and see in real time the results in order to choose the best combination of parameters.

Leverage : We have this function for the futures markets where you can check which is the most appropriate leverage for your operation.

Trend Filter: allows you to take multiple entries in the same direction of the market.

If the market crosses below the 200 moving average, it will take only short entries.

If the market crosses above the 200 moving average, it will take only long entries.

Timeframes

Charting from 1 Hour, 4 Hour, Daily, Weekly, Weekly

Markets :Booz Backtesting can be tested in Cryptocurrency, Stocks and Futures markets.

Background Color : at a glance, you can see what cycle the market is in.

Green background : Shows that the market is in a bullish cycle.

Red background: Shows that the market is in a bearish cycle.

Twitter

Website

Configurable Multi MA Crossover Voting SystemThis strategy goes long when all fast moving averages that you have defined are above their counterpart slow moving averages.

Long position is closed when profit or loss target is hit and at least one of the fast moving averages is below its counterpart slow moving average.

The format of the config is simple. The format is : FASTxSLOW,FASTxSLOW,...

Example : If you want 2 moving averages fast=9,slow=14 and fast=20,slow=50 you define it like this : 9x14,20x50

Another example : 5x10,10x15,15x20 => means 3 moving average setups : first wih fast=5/slow=10, second with fast=10/slow=15, last with fast=15/slow=20

You can chose the type of moving average : SMA, WMA, VWMA (i got issues with EMA/RMA so i removed them)

You can chose the source of the moving average : high, close, hl2 etc.

You can chose the period on which ATR is calculated and ATR profit/loss factors.

Profit is calculated like : buy_price + atr_factor*atr

Loss is calculated like : buy_price - atr_factor*atr

Performance in backtest is variable depending on the timeframe, the options and the market.

Performance in backtest suggests it works better for higher timeframes like 1d, 4h etc.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

[astropark] Moon Phases [strategy]Dear Followers,

today I'm glad to present you an indicator which calculates Moon Phases and let's you backtest the simplest strategy over it: buy/sell on full moon and do the opposite on new moon.

This is a public free indicator based on the public one by @paaax:

I added my usual backtesting logic, plus some more customization inputs for easy coloring.

The lower the timeframe you backtest on, the more backtesting data are effective.

Enjoy!

-- astropark

Buy and Hold entry finder StrategyHello everyone!

I proudly present the backtest Strategy Script for my "Buy and Hold entry finder" Script.

It basically shows you the outcome, if you would use my indicator in the past.

The buy signals are limited to 1 order per month.

Order Size: Allows you to choose, how much money you want to invest per month. (Please consider, it will only invest an x amount per Order, but it will not stack the amount you did not invest in an previous month ) (Example in my indicator)

Pyramiding: Just regulates, how often you can open an position.

Commission: Here you can set how much it will cost to open an position at your broker.

I coded a feature that allows you to set a Start Date and an End Date for your backtest. In the end of the backtest the script closes all positions.

If you got any question, feel free to ask in the comments or send me a message.

Sincerely, RS Titan.

Updated TurtlesThis script has been updated to prevent double orders (short/long) from occurring and modifying backtests results.

This is an update to the script that was written a few years ago to prevent double longs/shorts from occurring and skewin backtesting results. Check out the updated indicator here and let me know what you think.

I also added:

- date range inputs if you want to do some backtesting on a particular set of dates.

- the ability to toggle shorting

Line Break StrategyLine Break Strategy

Entry rule:

Long on a bullish line and short on a bearish line.

Backtest:

Profit factors are shown below for three-line break.

Daily time frame, FXCM broker.

EURUSD: 1.267, USDJPY: 1.039, GBPUSD: -0.816, AUDUSD: -0.959

S&P500: -0.783, Nikkei225: 1.099

CrudeOil: 1.03, Gold: 1.196

BTCUSD: -0.883

Reference:

Steve Nison, Beyond Candlesticks - New Japanese Charting Techniques Revealed

Note:

This strategy doesn't work properly on the linebreak chart.

A good example is shown below. The entry prices are not always correct.

If you have signal, but the next candle moves in the opposite direction, the entry price is drawn at the Open of the new candle instead of the Close of the previous candle.

The results of backtest are unreliable due to this reason.

Outsidebar vs Insidebar, Illusion Strategy (by ChartArt)WARNING: This strategy does not work! Please don't trade with this strategy

I'm sharing this strategy for the following three educational reasons:

1. You can easily find 100% strategies, but if they only seem to work 100% on one asset, they actually don't work at all. Therefore never backtest your strategy only on one asset, especially forward testing is useless, because it tends to repeat the old patterns. Your strategy has to work on as many different assets as possible.

2. The pyramiding of orders can have an impact on the strategy. In this case if you manually change the strategy settings by increasing it from 1 to 100 pyramiding orders changes the percent profitable on "UKOIL" monthly from 100% to 90% profitable. On other assets you can see very different results. Allowing much more pyramiding orders in this case results in opening orders where the background color highlights appear.

3. The Tradingview backtest beta version currently does not close the last open trade during the backtest. In this case going long on "UKOIL" near the top in 2011 as this strategy did would result in a big loss in 2015. But since the trade is still open and not canceled out by a new short order it still appears as if this strategy works 100% profitable. Which it doesn't.

Smart Scalper Pro Template + VWAP

📌 Author

Garry Evans

Independent system developer focused on:

Risk-first automation

Market structure & liquidity behavior

Discipline, consistency, and capital preservation

“The edge isn’t the market — it’s the man who survives it.”

⚙️ Risk Management & Position Sizing

The script is built around capital protection, not signal frequency.

Risk logic includes:

Fixed or dynamic risk per trade

Market-adaptive position sizing

Session-based trade limits

Daily trade caps and auto-lockout protection

Volatility-aware sizing (futures & crypto)

⚠️ Profit is pursued only after risk is controlled.

📊 Track Record

Backtested across multiple market environments

Forward-tested and actively used by the author

Real-account trades are logged where platform rules allow

Results vary by market, timeframe, and user-defined risk settings.

🌍 Supported Markets

Designed to work across all liquid markets, including:

Stocks

Crypto (spot & futures)

Options (signal-based framework)

Futures (indices, metals, crypto futures)

The system adapts to volatility and structure — it is not market-specific.

⚖️ Leverage

Leverage is not required

If used, leverage is fully user-controlled

Risk logic scales exposure conservatively

No martingale.

No revenge sizing.

No over-exposure logic.

🧪 Backtesting

✔ Yes

Strategy logic has been backtested

Filters reduce chop, noise, and forced trades

Focus on drawdown control over curve-fitting

🛠 Support

✔ Yes

Direct author support

Ongoing improvements and updates

Feature refinement based on real usage and feedback

👥 Community

✔ Yes

Private user access

High-quality feedback environment

No public signal spam or hype-driven chat rooms

⏳ Trial Period

✔ Yes

Limited trial access available

Designed for evaluation only

Trial users do not receive full feature access

🚫 Who This Script Is NOT For

This system is not for:

Traders looking for guaranteed profits

Users expecting copy-paste “signal calls”

Over-leveraged gamblers

Those unwilling to follow risk rules

Anyone seeking overnight results

This is a discipline and automation tool, not a shortcut.

🧠 Final Positioning

This is not a signal service.

This is a risk-controlled execution framework designed to:

Enforce discipline

Reduce emotional trading

Protect capital during bad market conditions

Scale responsibly during favorable ones

CNN Fear and Greed StrategyAdaptation of the CNN Fear and Greed Index Indicator (Original by EdgeTools)

The following changes have been implemented:

Put/Call Ratio Data Source: The data source for the Put/Call Ratio has been updated.

Bond Data Source: The data sources for the bond components (Safe Haven Demand and Junk Bond Demand) have been updated.

Normalization Adjustment: The normalization method has been adjusted to allow the CNN Fear and Greed Index to display over a longer historical period, optimizing it for backtesting purposes.

Style Modification: The display style has been modified for a simpler and cleaner appearance.

Strategy Logic Addition: Added a new strategy entry condition: index >= 25 AND index crosses over its 5-period Simple Moving Average (SMA), and a corresponding exit condition of holding the position for 252 bars (days).

CNN Fear & Greed Backtest Strategy (Adapted)

This script is an adaptation of the popular CNN Fear & Greed Index, originally created by EdgeTools, with significant modifications to optimize it for long-term backtesting on the TradingView platform.

The core function of the Fear & Greed Index is to measure the current emotional state of the stock market, ranging from 0 (Extreme Fear) to 100 (Extreme Greed). It operates on the principle that excessive fear drives prices too low (a potential buying opportunity), and excessive greed drives them too high (a potential selling opportunity).

Key Components of the Index (7 Factors)

The composite index is calculated as a weighted average of seven market indicators, each normalized to a score between 0 and 100:

Market Momentum: S&P 500's current level vs. its 125-day Moving Average.

Stock Price Strength: Stocks hitting 52-week highs vs. those hitting 52-week lows.

Stock Price Breadth: Measured by the McClellan Volume Summation Index (or similar volume/breadth metric).

Put/Call Ratio: The relationship between volume of put options (bearish bets) and call options (bullish bets).

Market Volatility: The CBOE VIX Index relative to its 50-day Moving Average.

Safe Haven Demand: The relative performance of stocks (S&P 500) vs. bonds.

Junk Bond Demand: The spread between high-yield (junk) bonds and U.S. Treasury yields.

Critical Adaptations for Backtesting

To improve the index's utility for quantitative analysis, the following changes were made:

Long-Term Normalization: The original normalization method (ta.stdev over a short LENGTH) has been replaced or adjusted to use longer historical data. This change ensures the index generates consistent and comparable sentiment scores across decades of market history, which is crucial for reliable backtesting results.

Updated Data Sources: Specific ticker requests for the Put/Call Ratio and Bond components (Safe Haven and Junk Bond Demand) have been updated to use the most reliable and long-running data available on TradingView, reducing data gaps and improving chart continuity.

Simplified Visuals: The chart display is streamlined, focusing only on the final Fear & Greed Index line and key threshold levels (25, 50, 75) for quick visual assessment.

Integrated Trading Strategy

This script also includes a simple, rules-based strategy designed to test the counter-trend philosophy of the index:

Entry Logic (Long Position): A long position is initiated when the market shows increasing fear, specifically when the index score is less than or equal to the configurable FEAR_LEVEL (default 25) and the index crosses above its own short-term 5-period Simple Moving Average (SMA). This crossover acts as a confirmation that sentiment may be starting to turn around from peak fear.

Exit Logic (Time-Based): All positions are subject to a time-based exit after holding for 252 trading days (approximately one year). This fixed holding period aims to capture the typical duration of a cyclical market recovery following a major panic event.

Quasimodo Pattern Strategy Back Test [TradingFinder] QM Trading🔵 Introduction

The QM pattern, also known as the Quasimodo pattern, is one of the popular patterns in price action, and it is often used by technical analysts. The QM pattern is used to identify trend reversals and provides a very good risk-to-reward ratio. One of the advantages of the QM pattern is its high frequency and visibility in charts.

Additionally, due to its strength, it is highly profitable, and as mentioned, its risk-to-reward ratio is very good. The QM pattern is highly popular among traders in supply and demand, and traders also use this pattern.

The Price Action QM pattern, like other Price Action patterns, has two types: Bullish QM and Bearish QM patterns. To identify this pattern, you need to be familiar with its types to recognize it.

🔵 Identifying the QM Pattern

🟣 Bullish QM

In the bullish QM pattern, as you can see in the image below, an LL and HH are formed. As you can see, the neckline is marked as a dashed line. When the price reaches this range, it will start its upward movement.

🟣 Bearish QM

The Price Action QM pattern also has a bearish pattern. As you can see in the image below, initially, an HH and LL are formed. The neckline in this image is the dashed line, and when the LL is formed, the price reaches this neckline. However, it cannot pass it, and the downward trend resumes.

🔵 How to Use

The Quasimodo pattern is one of the clearest structures used to identify market reversals. It is built around the concept of a structural break followed by a pullback into an area of trapped liquidity. Instead of relying on lagging indicators, this pattern focuses purely on price action and how the market reacts after exhausting one side of liquidity. When understood correctly, it provides traders with precise entry points at the transition between trend phases.

🟣 Bullish Quasimodo

A bullish Quasimodo forms after a clear downtrend when sellers start losing control. The market continues to make lower lows until a sudden higher high appears, signaling that buyers are entering with strength. Price then pulls back to retest the previous low, creating what is known as the Quasimodo low.

This area often becomes the final trap for sellers before the market shifts upward. A visible rejection or displacement from this zone confirms bullish momentum. Traders usually place entries near this level, stops below the low, and targets at previous highs or the next resistance zone. Combining the setup with demand zones or Fair Value Gaps increases its accuracy.

🟣 Bearish Quasimodo

A bearish Quasimodo forms near the top of an uptrend when buyers begin to lose strength. The market continues to make higher highs until a sudden lower low breaks the bullish structure, showing that selling pressure is entering the market. Price then retraces upward to retest the previous high, forming the Quasimodo high, where breakout buyers are often trapped.

Once rejection appears at this level, it indicates a likely reversal. Traders can enter short near this area, with stop-losses placed above the high and targets near the next support or previous lows. The setup gains more reliability when aligned with supply zones, SMT divergence, or bearish Fair Value Gaps.

🔵 Setting

Pivot Period : You can use this parameter to use your desired period to identify the QM pattern. By default, this parameter is set to the number 5.

Take Profit Mode : You can choose your desired Take Profit in three ways. Based on the logic of the QM strategy, you can select two Take Profit levels, TP1 and TP2. You can also choose your take profit based on the Reward to Risk ratio. You must enter your desired R/R in the Reward to Risk Ratio parameter.

Stop Loss Refine : The loss limit of the QM strategy is based on its logic on the Head pattern. You can refine it using the ATR Refine option to prevent Stop Hunt. You can enter your desired coefficient in the Stop Loss ATR Adjustment Coefficient parameter.

Reward to Risk Ratio : If you set Take Profit Mode to R/R, you must enter your desired R/R here. For example, if your loss limit is 10 pips and you set R/R to 2, your take profit will be reached when the price is 20 pips away from your entry point.

Stop Loss ATR Adjustment Coefficient : If you set Stop Loss Refine to ATR Refine, you must adjust your loss limit coefficient here. For example, if your buy position's loss limit is at the price of 1000, and your ATR is 10, if you set Stop Loss ATR Adjustment Coefficient to 2, your loss limit will be at the price of 980.

Entry Level Validity : Determines how long the Entry level remains valid. The higher the level, the longer the entry level will remain valid. By default it is 2 and it can be set between 2 and 15.

🔵 Results

The following examples show the backtest results of the Quasimodo (QM) strategy in action. Each image is based on specific settings for the symbol, timeframe, and input parameters, illustrating how the QM logic can generate signals under different market conditions. The detailed configuration for each backtest is also displayed on the image.

⚠ Important Note : Even with identical settings and the same symbol, results may vary slightly across different brokers due to data feed variations and pricing differences.

Default Properties of Backtests :

OANDA:XAUUSD | TimeFrame: 5min | Duration: 1 Year :

BINANCE:BTCUSD | TimeFrame: 5min | Duration: 1 Year :

CAPITALCOM:US30 | TimeFrame: 5min | Duration: 1 Year :

NASDAQ:QQQ | TimeFrame: 5min | Duration: 5 Year :

OANDA:EURUSD | TimeFrame: 5min | Duration: 5 Year :

PEPPERSTONE:US500 | TimeFrame: 5min | Duration: 5 Year :

TMB Invest - Smart Money Concept StrategyEnglish:

**Quick Overview**

The "TMB_SMC_Strategy_v1.1.3" combines a classic trend filter using two EMAs with contrarian RSI entries and simple SMC elements (Fair Value Gaps & Order Blocks). Stop-loss and take-profit orders are volatility-adaptive and controlled via the ATR. An integrated dashboard displays the setup status, stop-loss/take-profit levels, entry reference, and trend, RSI, and ATR values.

---

## Operating Principle

1. **Trend Filter:** A fast EMA (default 50) is compared to a slow EMA (default 200). Trading occurs only in the direction of the trend: long in uptrends, short in downtrends.

2. **Timing via RSI:** Contrarian entries within the trend. Go long when the RSI is below a buy level (default 40); Short when the RSI is above a sell level (standard 60).

3. **Structure Check (SMC Proxy):** An "FVG Touch" serves as additional confirmation that an inefficient price zone has been tested. Order blocks are visualized for guidance but are not a direct entry trigger.

4. **Risk Management via ATR:** Stop-loss and take-profit levels are set as multipliers of the current ATR (e.g., SL = 1×ATR, TP = 2×ATR). This allows target and risk distances to adjust to market volatility.

5. **Simple Position Logic:** Only one position is held at a time (no pyramiding). After entry, stop and limit orders (bracket exit) are automatically placed.

---

## Input Values

* **EMA Fast / EMA Slow:** Lengths of the moving averages for the trend filter.

* **RSI Length / Levels:** Length of the RSI as well as buy and sell thresholds (contra signals within the trend direction).

* **Take Profit (RR) / Stop Loss (RR):** ATR multipliers for TP and SL.

* **Show FVGs & Order Blocks:** Toggles the visual SMC elements (zones/boxes) on or off.

--

## Signals & Execution

* **Long Setup:** Uptrend (fast EMA above slow EMA) **and** RSI below the buy level **and** a current FVG signal in a bullish direction.

* **Short Setup:** Downtrend (fast EMA below slow EMA) **and** RSI above the sell level **and** a current FVG touch in a bearish direction.

* **Entry & Exit:** If the setup is met, the market is entered; stop-loss/take-profit orders are placed immediately according to ATR multiples.

--

## Visualization

* **EMAs:** The fast and slow EMAs are plotted to illustrate the trend.

* **FVGs:** Fair Value Gaps are drawn as semi-transparent boxes in the trend color and projected slightly into the future.

* **Order Blocks:** Potential order block zones from the previous candle are visually highlighted (for informational purposes only).

---

## Integrated Dashboard

A compact table dashboard (bottom left) displays:

* Current **Setup Status** (Long/Short active, Long/Short ready, No Setup),

* **Stop-Loss**, **Take-Profit**, and **Entry Reference**,

* **Trend Status** (Bull/Bear/Sideways),

* **RSI Value**, and **ATR Value**.

Active long/short positions are highlighted in color (green/red).

--

## Practical Guide

1. **Place on Chart** and select the desired timeframe.

2. **Calibrate Parameters** (EMA lengths, RSI levels, ATR multipliers) to match the market and timeframe.

3. **Backtest** across different market phases; prioritize robustness over maximum curve fit.

4. **Fine-Tuning:**

* Shorter EMAs are often useful intraday (e.g., 20/100 or 34/144).

* Adjust RSI levels to market characteristics (45/55 for aggressive trading, 30/70 for conservative trading).

* Increase or decrease ATR multipliers depending on volatility/trading style.

--

## Notes, Limitations & Extensions

* **FVG Definition:** The FVG detection used here is intentionally simplified. Those who prefer a more rigorous approach can switch to a 3-candle definition and fill levels.

* **Order Blocks:** These primarily serve as a guide. Integration into entry/exit logic (e.g., retests) is possible as an extension.

* **Backtest Realism:** Fills may differ from the displayed closing price. For greater accuracy, intrabar backtests or an entry indicator based on the average position price are conceivable.

* **Alerts:** Currently, no alert conditions are defined; these can be added for long/short setups and status messages.

* **Position Management:** By default, no scaling is performed. Partial sales, trailing stops, or multiple entries can be added.

---

## Purpose & Benefits

The strategy offers a clear, modular framework: trend filter (direction), RSI contra timing (entry), SMC proxy via FVG Touch (structure), and ATR-based exits (risk adaptation). This makes it robust, easy to understand, and highly extensible—both for discretionary traders who appreciate visual SMC elements and for systematic testers who prefer a clean, parameterizable foundation.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

EMA inFusion Pro - Multiple SourcesEMA Fusion Pro: Dynamic Trend & Momentum Strategy with Three Exit Modes

EMA Fusion Pro is a highly customizable, multi-exit trend-following strategy designed for traders who value both precision and flexibility. By leveraging exponential moving averages (EMA), average directional index (ADX), and volume analysis, this strategy aims to capture trending market moves while offering three distinct exit modes for optimal risk management across varying market conditions.

Strategy Overview

This strategy systematically identifies potential entry points using a moving average crossover with highly configurable data sources (including price, volume, rate of change, or their Heikin Ashi versions) and filters signal quality with ADX trend strength and volume spikes. Each trade is managed with one of three advanced exit methodologies—reverse signal, ATR-based stop/take profit, or fixed percentage—giving you the control to adapt your risk profile to different market regimes.

Key Features

Customizable EMA Source: Calculate the core trend-filtering EMA from price (default), volume, rate of change, or their Heikin Ashi counterparts for unique market perspectives.

Trend Filter with ADX: Confirm entries only when the trend is strong, as measured by the user-adjustable ADX threshold.

Volume Spike Confirmation: Optional filter to only take trades with above-average volume activity, reducing false signals.

Three Exit Modes:

Reverse Signal: Exit trades when a new, opposite entry signal occurs.

ATR-Based Stop/Take Profit: Dynamic risk management using multiples of the average true range (ATR) for both take profit and stop loss.

Percent-Based Stop/Take Profit: Fixed-percentage risk management with user-defined thresholds.

Visual Annotations: Signal markers, EMA line color-coded by source, trend background coloring, and optional ATR/percent-based TP/SL levels.

Info Panel: Real-time display of all core indicators, current trading mode, exit parameters, and position status for quick oversight.

How It Works

Entry Logic: A crossover signal (above/below the EMA) triggers a new entry, but only if both ADX trend strength and (optionally) volume spike conditions are met.

Exit Logic: Three selectable modes allow you to exit trades on reverse signals, at a dynamic ATR-based profit or loss, or at a fixed percentage gain/loss.

Flexible Data Analysis: The EMA source can be chosen from six options—standard price, volume, rate of change, or their Heikin Ashi variants—allowing experimentation with different market dimensions.

Risk Management: All exits are precisely controlled, either by the next opposing signal, by volatility-adjusted levels, or by fixed risk/reward ratios.

Backtest & Optimization: The strategy is fully backtestable within TradingView’s Strategy Tester, with adjustable parameters for optimization.

Customization & Usage

Indicator Source: Select your preferred data type for EMA calculation, opening the door to creative strategy variations (e.g., volume momentum, pure price trend, rate of change divergence).

Filter Toggles: Enable/disable ADX and volume filters as desired—useful for different market environments.

Exit Mode Selection: Switch between reverse, ATR, or percent-based exits with a single parameter—ideal for adapting to ranging vs. trending markets.

Visual Clarity: The EMA line color reflects its underlying source, and the info panel summarizes all critical values for easy monitoring.

Who Should Use This Strategy?

Trend Followers seeking to ride strong moves with multiple exit options.

Experienced Traders who want to experiment with different data types (volume, momentum, Heikin Ashi) for trend analysis.

Algorithmic Traders looking for a robust, flexible base to build upon with their own ideas.

Getting Started

Apply the script to your chart and review default settings.

Customize parameters—EMA length, ADX threshold, volume settings, exit type—as desired.

Backtest on multiple instruments and timeframes to evaluate performance.

Optimize filters, exit rules, and risk parameters for your preferred trading style.

Monitor with the real-time info panel and trade alerts.

Disclaimer

This script is for educational and entertainment purposes only. It is not financial advice. Past performance is not indicative of future results. Always conduct thorough testing and consider your risk tolerance before trading real capital.

— Happy Trading —

Feel free to adapt, share, and contribute to this open-source strategy!

EMD Trend [InvestorUnknown]EMD Trend is a dynamic trend-following indicator that utilizes Exponential Moving Deviation (EMD) to build adaptive channels around a selected moving average. Designed for traders who value responsive trend signals with built-in volatility sensitivity, this tool highlights directional bias, market regime shifts, and potential breakout opportunities.

How It Works

Instead of using standard deviation, EMD Trend employs the exponential moving average of the absolute deviation from a moving average—producing smoother, faster-reacting upper and lower bounds:

Bullish (Risk-ON Long): Price crosses above the upper EMD band

Bearish (Risk-ON Short): Price crosses below the lower EMD band

Neutral: Price stays within the channel, indicating potential mean reversion or low momentum

Trend direction is defined by price interaction with these bands, and visual cues (color-coded bars and fills) help quickly identify market conditions.

Features

7 Moving Average Types: SMA, EMA, HMA, DEMA, TEMA, RMA, FRAMA

Custom Price Source: Choose close, hl2, ohlc4, or others

EMD Multiplier: Controls the width of the deviation envelope

Bar Coloring: Candles change color based on current trend

Intra-bar Signal Option: Enables faster updates (with optional repainting)

Speculative Zones: Fills highlight aggressive momentum moves beyond EMD bounds

Backtest Mode

Switch to Backtest Mode for performance evaluation over historical data:

Equity Curve Plot: Compare EMD Trend strategy vs. Buy & Hold

Trade Metrics Table: View number of trades, win/loss stats, profits

Performance Metrics Table: Includes CAGR, Sharpe, max drawdown, and more

Custom Start Date: Select from which date the backtest should begin

Trade Sizing: Configure capital and trade percentage per entry

Signal Filters: Choose from Long Only, Short Only, or Both

Alerts

Built-in alerts let you automate entries, exits, and trend transitions:

LONG (EMD Trend) - Trend flips to Long

SHORT (EMD Trend) - Trend flips to Short

RISK-ON LONG - Price crosses above upper EMD band

RISK-OFF LONG - Price crosses back below upper EMD band

RISK-ON SHORT - Price crosses below lower EMD band

RISK-OFF SHORT - Price crosses back above lower EMD band

Use Cases

Trend Confirmation with volatility-sensitive boundaries

Momentum Entry Filtering via breakout zones

Mean Reversion Avoidance in sideways markets

Backtesting & Strategy Building with real-time metrics

Disclaimer

This indicator is intended for informational and educational purposes only. It does not constitute investment advice. Historical performance does not guarantee future results. Always backtest and use in simulation before live trading.

Best SMA FinderThis script, Best SMA Finder, is a tool designed to identify the most robust simple moving average (SMA) length for a given chart, based on historical backtest performance. It evaluates hundreds of SMA values (from 10 to 1000) and selects the one that provides the best balance between profitability, consistency, and trade frequency.

What it does:

The script performs individual backtests for each SMA length using either "Long Only" or "Buy & Sell" logic, as selected by the user. For each tested SMA, it computes:

- Total number of trades

- Profit Factor (total profits / total losses)

- Win Rate

- A composite Robustness Score, which integrates Profit Factor, number of trades (log-scaled), and win rate.

Only SMA configurations that meet the user-defined minimum trade count are considered valid. Among all valid candidates, the script selects the SMA length with the highest robustness score and plots it on the chart.

How to use it:

- Choose the strategy type: "Long Only" or "Buy & Sell"

- Set the minimum trade count to filter out statistically irrelevant results

- Enable or disable the summary stats table (default: enabled)

The selected optimal SMA is plotted on the chart in blue. The optional table in the top-right corner shows the corresponding SMA length, trade count, Profit Factor, Win Rate, and Robustness Score for transparency.

Key Features:

- Exhaustive SMA optimization across 991 values

- Customizable trade direction and minimum trade filters

- In-chart visualization of results via table and plotted optimal SMA

- Uses a custom robustness formula to rank SMA lengths

Use cases:

Ideal for traders who want to backtest and auto-select a historically effective SMA without manual trial-and-error. Useful for swing and trend-following strategies across different timeframes.

📌 Limitations:

- Not a full trading strategy with position sizing or stop-loss logic

- Only one entry per direction at a time is allowed

- Designed for exploration and optimization, not as a ready-to-trade system

This script is open-source and built entirely from original code and logic. It does not replicate any closed-source script or reuse significant external open-source components.

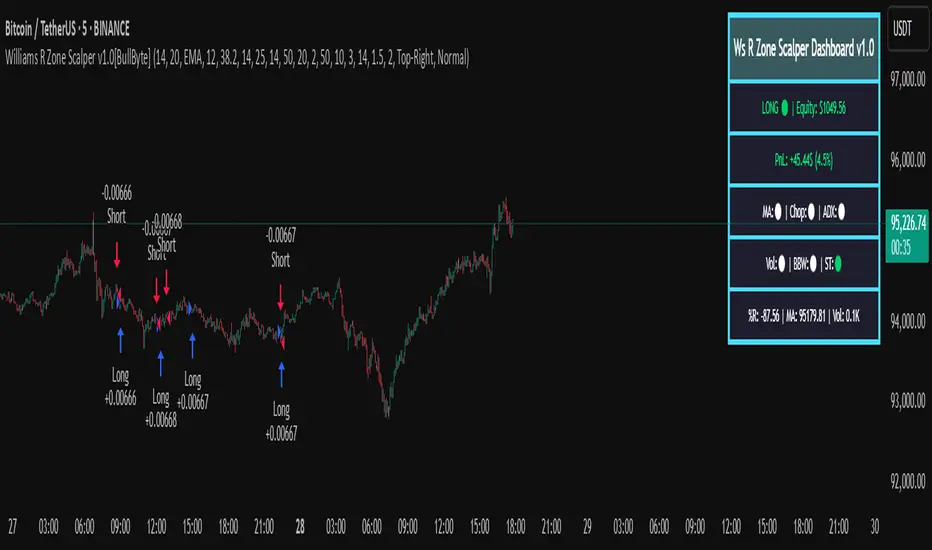

Williams R Zone Scalper v1.0[BullByte]Originality & Usefulness

Unlike standard Williams R cross-over scripts, this strategy layers five dynamic filters—moving-average trend, Supertrend, Choppiness Index, Bollinger Band Width, and volume validation —and presents a real-time dashboard with equity, PnL, filter status, and key indicator values. No other public Pine script combines these elements with toggleable filters and a custom dashboard. In backtests (BTC/USD (Binance), 5 min, 24 Mar 2025 → 28 Apr 2025), adding these filters turned a –2.09 % standalone Williams R into a +5.05 % net winner while cutting maximum drawdown in half.

---

What This Script Does

- Monitors Williams R (length 14) for overbought/oversold reversals.

- Applies up to five dynamic filters to confirm trend strength and volatility direction:

- Moving average (SMA/EMA/WMA/HMA)

- Supertrend line

- Choppiness Index (CI)

- Bollinger Band Width (BBW)

- Volume vs. its 50-period MA

- Plots blue arrows for Long entries (R crosses above –80 + all filters green) and red arrows for Short entries (R crosses below –20 + all filters green).

- Optionally sets dynamic ATR-based stop-loss (1.5×ATR) and take-profit (2×ATR).

- Shows a dashboard box with current position, equity, PnL, filter status, and real-time Williams R / MA/volume values.

---

Backtest Summary (BTC/USD(Binance), 5 min, 24 Mar 2025 → 28 Apr 2025)

• Total P&L : +50.70 USD (+5.05 %)

• Max Drawdown : 31.93 USD (3.11 %)

• Total Trades : 198

• Win Rate : 55.05 % (109/89)

• Profit Factor : 1.288

• Commission : 0.01 % per trade

• Slippage : 0 ticks

Even in choppy March–April, this multi-filter approach nets +5 % with a robust risk profile, compared to –2.09 % and higher drawdown for Williams R alone.

---

Williams R Alone vs. Multi-Filter Version

• Total P&L :

– Williams R alone → –20.83 USD (–2.09 %)

– Multi-Filter → +50.70 USD (+5.05 %)

• Max Drawdown :

– Williams R alone → 62.13 USD (6.00 %)

– Multi-Filter → 31.93 USD (3.11 %)

• Total Trades : 543 vs. 198

• Win Rate : 60.22 % vs. 55.05 %

• Profit Factor : 0.943 vs. 1.288

---

Inputs & What They Control

- wrLen (14): Williams R look-back

- maType (EMA): Trend filter type (SMA, EMA, WMA, HMA)

- maLen (20): Moving-average period

- useChop (true): Toggle Choppiness Index filter

- ciLen (12): CI look-back length

- chopThr (38.2): CI threshold (below = trending)

- useVol (true): Toggle volume-above-average filter

- volMaLen (50): Volume MA period

- useBBW (false): Toggle Bollinger Band Width filter

- bbwMaLen (50): BBW MA period

- useST (false): Toggle Supertrend filter

- stAtrLen (10): Supertrend ATR length

- stFactor (3.0): Supertrend multiplier

- useSL (false): Toggle ATR-based SL/TP

- atrLen (14): ATR period for SL/TP

- slMult (1.5): SL = slMult × ATR

- tpMult (2.0): TP = tpMult × ATR

---

How to Read the Chart

- Blue arrow (Long): Williams R crosses above –80 + all enabled filters green

- Red arrow (Short) : Williams R crosses below –20 + all filters green

- Dashboard box:

- Top : position and equity

- Next : cumulative PnL in USD & %

- Middle : green/white dots for each filter (green=passing, white=disabled)

- Bottom : Williams R, MA, and volume current values

---

Usage Tips

- Add the script : Indicators → My Scripts → Williams R Zone Scalper v1.0 → Add to BTC/USD chart on 5 min.

- Defaults : Optimized for BTC/USD.