ZoneShift+StochZ+LRO + AI Breakout Bands [Combined]This composite Pine Script brings together four powerful trend and momentum tools into a single, easy-to-read overlay:

ZoneShift

Computes a dynamic “zone” around price via an EMA/HMA midpoint ± average high-low range.

Flags flips when price closes convincingly above or below that zone, coloring candles and drawing the zone lines in bullish or bearish hues.

Stochastic Z-Score

Converts your chosen price series into a statistical Z-score, then runs a Stochastic oscillator on it and HMA-smooths the result.

Marks momentum flips in extreme over-sold (below –2) or over-bought (above +2) territory.

Linear Regression Oscillator (LRO)

Builds a bar-indexed linear regression, normalizes it to standard deviations, and shows area-style up/down coloring.

Highlights local reversals when the oscillator crosses its own look-back values, and optionally plots LRO-colored candles on price.

AI Breakout Bands (Kalman + KNN)

Applies a Kalman filter to price, smooths it further with a KNN-weighted average, then measures mean-absolute-error bands around that smoothed line.

Colors the Kalman trend line and bands for bullish/bearish breaks, giving you a data-driven channel to trade.

Composite Signals & Alerts

Whenever the ZoneShift flip, Stoch Z-Score flip, and LRO reversal all agree and price breaks the AI bands in the same direction, the script plots a clear ▲ (bull) or ▼ (bear) on the chart and fires an alert. This triple-confirmation approach helps you zero in on high-probability reversal points, filtering out noise and combining trend, momentum, and statistical breakout criteria into one unified signal.

Pesquisar nos scripts por "ai"

TrendPilot AI v2 — Smart ATR Indicator with ZonesTrendPilot AI v2 is a smart price-action and ATR-based trading system designed for swing and position traders. It combines trend-following logic with adaptive price zones to help users identify high-probability Buy and Sell opportunities — along with intelligent re-entry points, weak signal detection, and visual structure zones.

🔧 Core Features:

✅ ATR-based Buy/Sell signals with confirmation logic

✅ Dynamic 99 EMA Channel for trend context

✅ Re-entry triangles for stacking or retracing setups

✅ 150 EMA Weak Signal Detection for early trend warnings

✅ 🧭 Price Action Zones (Premium, Equilibrium, Discount)

✅ Visual alerts via triangles, labels, and color-coded logic

✅ Designed for 15m, 1H, and 4H charts — also useful on Daily

🧠 How It Works (Logic Breakdown)

1️⃣ Trend Direction — EMA Channel Logic

A 99 EMA Channel determines the dominant market bias.

If price is above the channel → trend is Bullish → Buy signals are valid

If price is below the channel → trend is Bearish → Sell signals are valid

2️⃣ Buy/Sell Signals — ATR Trailing Logic

The system uses custom ATR trailing logic to detect when price momentum shifts.

When a breakout aligns with trend direction, a Buy or Sell label appears.

These are designed to capture the main trend leg or reversal zone.

3️⃣ Re-Entry Signals — Triangle Visual Cues

During a confirmed trend, if price retraces to the EMA channel, a small triangle is shown:

🔼 Green triangle: Buy re-entry during bullish trend

🔽 Red triangle: Sell re-entry during bearish trend

These are not new signals but continuation cues for advanced traders.

4️⃣ Weak Signal Detection — 150 EMA Logic

A secondary 150 EMA helps detect possible trend exhaustion.

If price dips below 150 EMA during a bullish run, an orange triangle appears (⚠️ caution).

If price rises above 150 EMA during a bearish run, a blue triangle appears.

This signals potential weakening of the active trend.

5️⃣ Price Zones — Premium, Equilibrium, Discount

TrendPilot AI v2 draws 3 smart price zones based on ATR & market structure:

🟥 Premium Zone (Top) → Overbought area, caution for long trades

🟨 Equilibrium Zone (Middle) → Fair value, consolidation possible

🟩 Discount Zone (Bottom) → Oversold, better long entries

These zones help filter signals and avoid entries in risky areas.

Example: Avoid Buy signals inside Premium zone.

🧪 Suggested Use:

✅ Timeframes: 15m / 1H / 4H / 1D

✅ Combine signals with zone analysis for optimal entries

✅ Use re-entry triangles to add or confirm during pullbacks

✅ Use weak signal warnings to tighten stops or manage risk

✅ Works best in trending environments or breakout markets

⚠️ Note for Users:

This script is not repainting. All signals are plotted with stable logic.

Past performance does not guarantee future results — always backtest first.

Script does not contain financial advice — use at your own discretion.

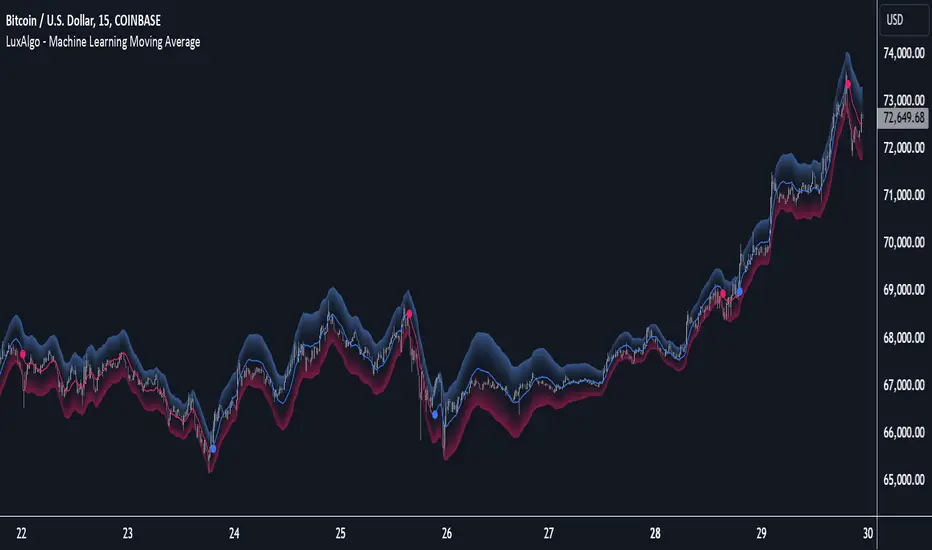

Machine Learning Moving Average [LuxAlgo]The Machine Learning Moving Average (MLMA) is a responsive moving average making use of the weighting function obtained Gaussian Process Regression method. Characteristic such as responsiveness and smoothness can be adjusted by the user from the settings.

The moving average also includes bands, used to highlight possible reversals.

🔶 USAGE

The Machine Learning Moving Average smooths out noisy variations from the price, directly estimating the underlying trend in the price.

A higher "Window" setting will return a longer-term moving average while increasing the "Forecast" setting will affect the responsiveness and smoothness of the moving average, with higher positive values returning a more responsive moving average and negative values returning a smoother but less responsive moving average.

Do note that an excessively high "Forecast" setting will result in overshoots, with the moving average having a poor fit with the price.

The moving average color is determined according to the estimated trend direction based on the bands described below, shifting to blue (default) in an uptrend and fushia (default) in downtrends.

The upper and lower extremities represent the range within which price movements likely fluctuate.

Signals are generated when the price crosses above or below the band extremities, with turning points being highlighted by colored circles on the chart.

🔶 SETTINGS

Window: Calculation period of the moving average. Higher values yield a smoother average, emphasizing long-term trends and filtering out short-term fluctuations.

Forecast: Sets the projection horizon for Gaussian Process Regression. Higher values create a more responsive moving average but will result in more overshoots, potentially worsening the fit with the price. Negative values will result in a smoother moving average.

Sigma: Controls the standard deviation of the Gaussian kernel, influencing weight distribution. Higher Sigma values return a longer-term moving average.

Multiplicative Factor: Adjusts the upper and lower extremity bounds, with higher values widening the bands and lowering the amount of returned turning points.

🔶 RELATED SCRIPTS

Machine-Learning-Gaussian-Process-Regression

SuperTrend-AI-Clustering

Ocs Ai TraderThis script perform predictive analytics from a virtual trader perspective!

It acts as an AI Trade Assistant that helps you decide the optimal times to buy or sell securities, providing you with precise target prices and stop-loss level to optimise your gains and manage risk effectively.

System Components

The trading system is built on 4 fundamental layers :

Time series Processing layer

Signal Processing layer

Machine Learning

Virtual Trade Emulator

Time series Processing layer

This is first component responsible for handling and processing real-time and historical time series data.

In this layer Signals are extracted from

averages such as : volume price mean, adaptive moving average

Estimates such as : relative strength stochastics estimates on supertrend

Signal Processing layer

This second layer processes signals from previous layer using sensitivity filter comprising of an Probability Distribution Confidence Filter

The main purpose here is to predict the trend of the underlying, by converging price, volume signals and deltas over a dominant cycle as dimensions and generate signals of action.

Key terms

Dominant cycle is a time cycle that has a greater influence on the overall behaviour of a system than other cycles.

The system uses Ehlers method to calculate Dominant Cycle/ Period.

Dominant cycle is used to determine the influencing period for the underlying.

Once the dominant cycle/ period is identified, it is treated as a dynamic length for considering further calculations

Predictive Adaptive Filter to generate Signals and define Targets and Stops

An adaptive filter is a system with a linear filter that has a transfer function controlled by variable parameters and a means to adjust those parameters according to an optimisation algorithm. Because of the complexity of the optimisation algorithms, almost all adaptive filters are digital filters. Thus Helping us classify our intent either long side or short side

The indicator use Adaptive Least mean square algorithm, for convergence of the filtered signals into a category of intents, (either buy or sell)

Machine Learning

The third layer of the System performs classifications using KNN K-Nearest Neighbour is one of the simplest Machine Learning algorithms based on Supervised Learning technique.

K-NN algorithm assumes the similarity between the new case/data and available cases and put the new case into the category that is most similar to the available categories.

K-NN algorithm stores all the available data and classifies a new data point based on the similarity. This means when new data appears then it can be easily classified into a well suite category by using K- NN algorithm. K-NN algorithm can be used for Regression as well as for Classification but mostly it is used for the Classification problems.

Virtual Trade Emulator

In this last and fourth layer a trade assistant is coded using trade emulation techniques and the Lines and Labels for Buy / Sell Signals, Targets and Stop are forecasted!

How to use

The system generates Buy and Sell alerts and plots it on charts

Buy signal

Buy signal constitutes of three targets {namely T1, T2, T3} and one stop level

Sell signal

Sell signal constitutes of three targets {namely T1, T2, T3} and one stop level

What Securities will it work upon ?

Volume Informations must be present for the applied security

The indicator works on every liquid security : stocks, future, forex, crypto, options, commodities

What TimeFrames To Use ?

You can use any Timeframe, The indicator is Adaptive in Nature,

I personally use timeframes such as : 1m, 5m 10m, 15m, ..... 1D, 1W

This Script Uses Tradingview Premium features for working on lower timeframes

In case if you are not a Tradingview premium subscriber you should tell the script that after applying on chart, this can be done by going to settings and unchecking "Is your Tradingview Subscription Premium or Above " Option

How To Get Access ?

You will need to privately message me for access mentioning you want access to "Ocs Ai Trader" Use comment box only for constructive comments. Thanks !

Trend Sentinel BarrierEveryone in the market wants to take profits from the trend. It is easy to think but hard to execute. In fact, some callbacks or rebounds may cause you to close the position out of fear and let you miss bigger profits.

Indicator: Trend Sentinel Barri er solves this problem for you! It use AI algorithm to help you seize profits.

It is a trend indicator, using AI algorithm to calculate the cumulative trading volume of bulls and bears, identify trend direction and opportunities, and calculate short-term average cost in combination with changes of turnover ratio in multi-period trends, so as to grasp the profit from the trend more effectively without being cheated.

💠Usage:

Signal: "BUY" means bullish trend, "SELL" means bearish trend.

Support and resistance range: "red area" represents strong support or resistance for long-term fluctuation costs, and "blue area" represents moderate support of resistance for short-term fluctuation costs.

🎈Tip I:

When the BUY and SELL signal appear, it means that the direction of the trend will change, and the color of the candles will also change. Don't care about the color of the candles, let's just focus on the price, support and resistance.

🎈Tip II:

Take the BUY signal as an example. When the signal appears and you hold long position, you need to pay attention to the blue and red support range. If the price returns to this range but there is no SELL signal, you can consider holding the long position for a while.

If the price pump with long candles, and then pulls back to the range, you need to be vigilant. You can consider taking the profit when the price breakthrough the support range, or wait for the SELL signal.

🎈Advanced tip I:

In most cases, the trend market is not smooth, there will be a lot of callbacks or rebounds, but because of this, we have many opportunities to do swing trading.

Continuing to take the BUY signal as an example, when this signal appears, every time the price falls back to the blue or red support area, you can consider adding positions. There are two ways to deal with these newly added positions.

One is to do swing trading. You can consider taking profits near the previous high when the price rises. The advantage of this operation is that you can get more profits in the same trend market.

The second is to continue to hold it as the bottom position until the general trend is completely over, and then close the position after obtaining huge profits.

🎈Advanced tip II:

When using advanced tips I, you can consider adding some momentum indicators to assist you in judging whether pullbacks or rebounds have failed, so as to increase your position. Similarly, the momentum indicator can also help you find a take-profit point for newly added positions

For details, please refer to the momentum indicator: KD Momentum Matrix

*The signals in the indicators are for reference only and not intended as investment advice. Past performance of a strategy is not indicative of future earnings results.

Update-

Optimize the alarm function. If you need to monitor the "Buy" or "Sell" signal, when creating an alarm, set the condition bar to:

Trend Sentinel Barrier --> "Buy" or "Sell" --> Crossing Up --> value --> 1

Intelligent Supertrend (AI) - Buy or Sell SignalIntroduction

This indicator uses machine learning (Artificial Intelligence) to solve a real human problem.

The artificial intelligence that operates this Supertrend was created by an algorithm that tests every single combination of input values across the entire chart history of an instrument for maximum profitability in real-time.

The Supertrend is one of the most popular indicators on the planet, yet no one really knows what input values work best in combination with each other. A reason for this is because not one set of input values is always going to be the best on every instrument, time-frame, and at any given point in time.

The "Intelligent Supertrend" solves this problem by constantly adapting the input values to match the most profitable combination so that no matter what happens, this Supertrend will be the most profitable.

Indicator Utility

The Intelligent Supertrend does not change what has already been plotted and does not repaint in any way which means that it is fully functional for trading in real-time.

Ultimately, there are no limiting factors within the range of combinations that have been programmed. The Supertrend will operate normally but will change input values according to what is currently the most profitable strategy.

Input Values

While a normal Supertrend would include two user-defined input values, the Intelligent Supertrend automates the input values according to what is currently the most profitable combination.

Additional Tools

The Optimised Supertrend is a tool that can be used to visual what input values the Supertrend AI is currently using. Additional tools to back-test this indicator will be added to this product soon.

For more information on how this indicator works, view the documentation here:

www.kenzing.com

For more information on the Supertrend view these fun facts:

www.marketcalls.in

Elite Federal Reserve AIThe Elite Federal Reserve AI indicator provides an analytical framework focused on monitoring economic and market conditions that influence Federal Reserve policy decisions. The indicator examines key relationships and rate-of-change metrics across multiple proxies for monetary policy drivers.

The indicator tracks and analyzes:

• Yield curve dynamics through rate-of-change measurements in short and intermediate-term Treasury yields

• Inflation expectations via TIPS breakeven rate momentum

• Dollar strength and its rate of change over specified periods

• Financial market stress indicators including volatility and sector performance metrics

• Breadth measures through small capitalization stock performance

The indicator calculates momentum and rate-of-change values across these variables to identify shifts in the economic and financial conditions that serve as primary inputs to Federal Reserve decision-making. By monitoring the velocity of change in these key relationships, the indicator provides insight into the changing balance between inflationary pressures, growth expectations, financial stability concerns, and currency dynamics.

This approach focuses on the observable market-based indicators that reflect the underlying economic conditions the Federal Reserve considers in its policy formulation, enabling users to assess the prevailing policy environment through the lens of these critical market relationships and their momentum characteristics.

Elite Correlation Matrix AIThe Elite Correlation Matrix AI indicator provides comprehensive real-time correlation analysis across multiple asset classes, displaying the interrelationships between equities, bonds, commodities, currencies, and volatility instruments.

The indicator calculates and displays correlation coefficients between a predefined set of major market indices and instruments, including:

• Major equity indices (SPY, QQQ, IWM)

• Long-term Treasury bonds (TLT)

• Gold (GLD)

• Crude oil (USO)

• Volatility (VIX)

• US Dollar Index (DXY)

• Bitcoin (BTCUSD)

Key features include:

• Rolling correlation calculations across user-defined periods to identify both short-term and longer-term relationships

• Visual correlation heat map showing the strength and direction of relationships between all tracked instruments

• Detection of correlation breakdowns, which often precede significant market regime shifts

• Dashboard display providing summary metrics of prevailing correlation patterns

The indicator enables users to monitor the current state of market relationships and identify when traditional correlations begin to break down, which frequently serves as an early warning of impending changes in market behavior. By tracking the degree of connectedness between different asset classes, the indicator provides insight into the current risk environment and the potential for diversification effectiveness.

This analysis is particularly valuable for understanding periods of market stress when asset relationships deviate from their normal patterns, as well as identifying environments where traditional correlations hold and where they are undergoing structural changes.

Elite Commodities AIThe Elite Commodities AI indicator provides a comprehensive analytical framework designed specifically for commodities trading. It combines multiple technical components to assess price action within the unique characteristics of commodity markets.

The indicator incorporates the following key elements:

Multi-timeframe RSI analysis across the primary timeframe, 4-hour, and daily periods

Multiple exponential moving averages (fast, slow, and trend) to establish directional context

Volume rate analysis measuring current volume relative to recent average volume

Bollinger Band width analysis to identify periods of volatility contraction

True Range volatility expressed as a percentage of price

The indicator evaluates the interaction between momentum, trend structure, volume participation, and volatility dynamics, which are particularly significant in commodities markets due to their sensitivity to changes in supply-demand fundamentals and large institutional order flow.

By combining these analytical components, the indicator provides a layered assessment of price behavior that captures the interplay between trend development, momentum characteristics, participation levels, and volatility compression—key factors that drive commodity market movements.

This approach enables traders to identify significant price action within the context of prevailing market structure, making it suitable for analyzing both directional trends and consolidation periods that are common in commodity price behavior.2.2s

Elite Bond Market AIDescription:

The Elite Bond Market AI indicator provides a comprehensive analytical framework specifically designed for bond market price action. The indicator combines multiple technical components including multi-timeframe RSI analysis, moving average relationships, volume dynamics, and volatility measurements to identify significant price behavior within the unique characteristics of bond market trading.

The indicator incorporates:

Multi-timeframe RSI evaluation across primary, 4-hour, and daily timeframes

Fast, slow, and trend exponential moving averages for directional context

Volume rate analysis relative to recent average volume

Bollinger Band width measurement for volatility contraction assessment

True Range volatility normalized as a percentage of price

This combination provides a layered analytical approach that captures the interplay between momentum, trend structure, participation levels, and volatility compression—key factors in bond market price discovery and directional moves.

MagiMagi (AI Trend & SMC)exclusively for Bond Team

・50EMA貫きの形を条件に売買シグナル点灯

・AIトレンドを導入しトレンドの方向性を背景色の変化で可視化

・大口のオーダーブロック表示

・ダウ理論における高安を自動水平線にて表示

💰 Aymed55 AI v2 – Para Akışı + RSI + MACD + Alarm→ Para çıkışı + momentum kırılması = SAT ⚠️

📌 What Does This Indicator Do? — Short Summary

The Borsacı AI v2 indicator is designed to detect real money flow in the market.

Its core purpose is simple:

👉 Follow where the money is going — enter early, exit early.

It combines Volume + RSI + MACD to generate highly reliable buy/sell signals.

1) Detects Strong Money Inflow

A BUY condition begins when:

Volume is above 2× the 20-period volume average

Price is moving upward

Volume strength (volume deviation) is positive

→ This means big players are buying.

2) Detects Strong Money Outflow

A SELL condition begins when:

Volume is above 2× the average

Price is falling

→ Means big players are selling.

3) BUY Signal (🚀 AL)

A buy signal is triggered only when ALL of these align:

✔ Strong money inflow

✔ RSI below 70 (not overbought)

✔ MACD bullish crossover (momentum turning up)

→ Result: “Smart money is buying and momentum is shifting upward.”

4) SELL Signal (⚠️ SAT)

A sell signal triggers when:

✔ Money outflow

✔ MACD bearish crossover

→ Result: “Money is leaving and downward momentum is starting.”

5) Background Coloring

Green background = BUY conditions active

Red background = SELL conditions active

6) Alerts Included

TradingView alerts are generated for:

🚀 Buy Signal

⚠️ Sell Signal

🔎 In Summary

This indicator answers one question:

“Where is the money flowing, and when is momentum confirming it?”

It gives early and reliable entry/exit points using a clean, powerful trio:

👉 Volume + RSI + MACD

If you want, I can also write a full English description for TradingView’s description box or a marketing-style product description.

Precision AI Trading ProPrecision AI Trading Pro — TradingView Indicator

EN / 中文雙語說明(No promo, high-level logic, originality stated)

What it does |用途

EN

Trend-aligned entries on 5m/15m (and higher) using multi-layer confirmations. It emphasizes confirmation over prediction, then derives adaptive TP/SL from volatility and recent structure.

中文

在 5/15 分鐘(與更高時框)進行趨勢對齊進場,重確認、不猜轉折;並依波動與近期結構自適應計算 TP/SL。

Why it’s original & useful |原創性與價值

EN

This script implements a custom 11-filter confluence engine and a volatility-aware exit model. Filters are designed to complement each other: HTF context narrows bias, LTF structure checks timing, momentum/volume validate strength, and regime gates avoid chop. Exits use ATR- and swing-based distances with caps to keep results realistic.

中文

本腳本自研 11 重共振濾網 與 隨波動調整的出場模型:HTF 提供方向偏好,LTF 結構掌握時點;動能/量能驗證有效性;型態/趨勢強度門檻過濾震盪;出場以 ATR 與擺動區間計算距離並設上限,使績效更貼近實際。

How it works (high-level) |高層級運作

EN

HTF alignment: EMA(3/8/21) + RSI/MACD on a higher timeframe (confirmed bars only) sets directional bias.

LTF structure: Requires local EMA(3/8/21) alignment, Structure Breakout (recent swing ± ATR buffer), and optional Pullback to EMA8/21.

Regime checks: ADX gate and EMA band width filter out low-trend conditions; Volume confirms pressure.

Risk layer: Peak Guard (overheat/new-high/surge) blocks extended entries.

Trendline/EMA200: Optionally require EMA200 or TL breakout with ATR tolerance.

Exits: SL = max(ATR×k, swing buffer, % floor); TP = min(R×SL, ATR/% caps).

No look-ahead: HTF uses confirmed bars; pivots only annotate context, not used as entry triggers.

中文

HTF 共振:高階時框 EMA(3/8/21)+RSI/MACD(僅採用確認棒)決定方向偏好。

LTF 結構:要求本階 EMA(3/8/21) 一致、結構突破(近期高低點 ± ATR 緩衝),並可選 回踩 EMA8/21。

市況門檻:ADX 閘 與 EMA 帶寬 排除低趨勢環境;量能 驗證推進力。

風險層:Peak Guard(過熱/創高/急漲)避免追價。

趨勢線/EMA200:可選擇要求 EMA200 或趨勢線突破(含 ATR 容忍帶)。

出場:SL = max(ATR×k, 擺動緩衝, % 下限);TP = min(R×SL, ATR/% 上限)。

避免前視:HTF 僅用確認棒;樞紐點僅作標註,不作入場條件。

Filters (11) |濾網(11 項)

HTF Trend / Bright Zone (RSI) / LTF EMA(3/8/21) / MACD / Volume / ADX Gate / Structure Breakout / Pullback to EMA / EMA Band Width / Peak Guard / Trendline or EMA200 Confirmation

(高階趨勢/RSI 亮區/本階 EMA 結構/MACD/量能/ADX 閘/結構突破/回踩 EMA/EMA 窄帶/高位防護/趨勢線或 EMA200 確認)

User can define required passes (default 7).|可自訂需通過的濾網數(預設 7)。

Features |功能

Multi-market presets (Crypto / Gold / US Futures / Forex)|多市場預設

Adaptive TP/SL with labels (dynamic R:R)|自適應 TP/SL(含標註)

Risk-based star rating (0★–5★)|風險星級評分

Signal modes: Conservative / Balanced / Aggressive|訊號模式:保守/平衡/積極

Peak Guard toggle|高位防護可切換

How to use |使用方式

Pick market preset; start with 5m/15m.

Set required filters (default 7) and enable HTF confirmed bars.

Tune TP/SL and risk per symbol/timeframe; use star rating as visual guidance.

In choppy markets, raise ADX min and EMA-band threshold; in trend, relax them slightly.

選擇市場預設(建議 5/15 分鐘起)。

設定需通過的濾網數(預設 7),並啟用 HTF 確認棒。

依商品/時框微調 TP/SL 與風險;以星級作視覺參考。

震盪市提高 ADX 與帶寬門檻;趨勢市可適度放寬。

Notes |注意

Backtest behavior depends on bar resolution and fill rules; intrabar path may differ from live fills.

Educational use only; not financial advice.

No ads/links/contacts.

Changelog |版本紀錄(示例,請用「Update」維護)

2025-09-05: Reversal v2.1 scoring & 2-step confirmation; TL rejection/OB-touch trigger (optional); EMA8 recapture via close; Peak Guard integrated; BTC/ETH/SOL presets refined; alerts expanded; label params cleaned.

2025-08-28: Fixed decimal bug; tuned presets for four markets; kept auto RR/SL logic.

Jarvis Bitcoin Predictor – Advanced AI-Powered TrendJarvis Bitcoin Predictor is an invite-only indicator designed to help traders anticipate market moves with precision.

It combines advanced momentum tracking, volatility analysis, and adaptive trend filters to highlight high-probability trading opportunities.

🔹 Core Features:

- AI-inspired algorithm for Bitcoin price prediction

- Early detection of bullish and bearish trend reversals

- Dynamic support & resistance zones

- Clear buy/sell signal markers

- Built-in alerts to never miss an opportunity

Optimized for Bitcoin, but compatible with other crypto pairs

🔹 How it works (general explanation):

The indicator uses a mix of momentum calculations, volatility filters, and adaptive trend detection to generate signals.

When several market conditions align, Jarvis provides clear entry/exit signals designed to improve decision-making and timing.

🔹 How to use it:

1- Add Jarvis Bitcoin Predictor to your chart.

2- Follow the green signals/zones for bullish opportunities.

3- Follow the red signals/zones for bearish opportunities.

4- Combine with proper risk management and your own strategy.

This tool was built to give traders clarity and confidence in the fast-paced crypto market.

⚠️ Important:

This script is invite-only. To request access, please contact the author directly.

AURA AI - Multi-Layer Signal System# AURA AI - Multi-Layer Signal System

## Originality and Value Proposition

This indicator implements a proprietary multi-layer signal filtering system designed specifically for educational trading analysis. The core value lies in three advanced algorithmic features developed to address common issues in market analysis:

1. **Adaptive Signal Spacing Algorithm**: Dynamically adjusts signal frequency based on real-time volatility calculations using custom ATR multipliers (0.7x to 1.8x)

2. **Hierarchical Signal Filtering**: Three-tier priority system with conflict prevention, cooldown periods, and cross-validation

3. **Progressive Educational Framework**: Contextual learning system with market concept explanations

## Technical Implementation

The system processes market data through multiple validation layers:

- **Primary Signals**: Multi-condition convergence requiring simultaneous confirmation from trend detection, directional strength analysis, momentum indicators, volume validation, and positioning filters

- **Trend Signals**: Direction-following analysis with moving average crossover confirmation and momentum validation

- **Reversal Signals**: Counter-trend opportunity detection with strict distance requirements and timeout filtering

## Algorithm Components and Processing

- **Adaptive Trend Detection**: Custom trailing stop methodology with configurable sensitivity parameters

- **Directional Strength Analysis**: Smoothed momentum indicators with threshold validation

- **Volume-Weighted Confirmation**: Market participation analysis using comparative volume metrics

- **Multi-Timeframe Validation**: Higher timeframe directional bias with hysteresis algorithms for stable detection

- **Custom Filtering Engine**: Proprietary noise reduction and signal prioritization algorithms

## Educational Framework Design

The indicator includes a comprehensive learning system addressing the gap between technical analysis tools and trader education:

- **Progressive Complexity**: Simplified interface for beginners transitioning to professional-grade controls

- **Contextual Explanations**: Real-time tooltips explaining market conditions and signal rationale

- **Risk Management Integration**: Built-in safeguards teaching proper trading practices

- **Signal Classification**: Clear categorization helping users understand different opportunity types

## Justification for Closed-Source Protection

This indicator warrants protection due to:

1. **Proprietary Filtering Algorithms**: Custom-developed signal prioritization and conflict resolution logic

2. **Adaptive Volatility System**: Original methodology for dynamic parameter adjustment

3. **Educational Integration**: Comprehensive learning framework with contextual market education

4. **Risk-Aware Design**: Built-in overtrading prevention and educational safeguards

The combination of these elements creates a unified analytical and educational system that goes beyond standard indicator combinations.

## Configuration and Usage

**Educational Mode**: Simplified interface focusing on high-probability setups with learning tooltips

**Professional Mode**: Full parameter control for experienced traders with advanced filtering options

Key settings include signal type selection, volatility adaptation parameters, multi-timeframe analysis, and day-of-week filtering for backtesting optimization.

## Market Application and Limitations

This system is designed for educational analysis across multiple markets and timeframes. The adaptive algorithms adjust to different volatility environments, though users should understand that no analytical tool can predict future market movements.

The indicator serves as an educational tool to help traders understand market dynamics while providing structured signal analysis. Proper risk management, position sizing, and market knowledge remain essential for successful trading.

## Important Disclosures

- This indicator provides educational analysis tools, not trading advice

- Past signal performance does not guarantee future results

- No claims are made regarding win rates or profitability

- Users must implement proper risk management practices

- Market conditions can change, affecting any analytical system's relevance

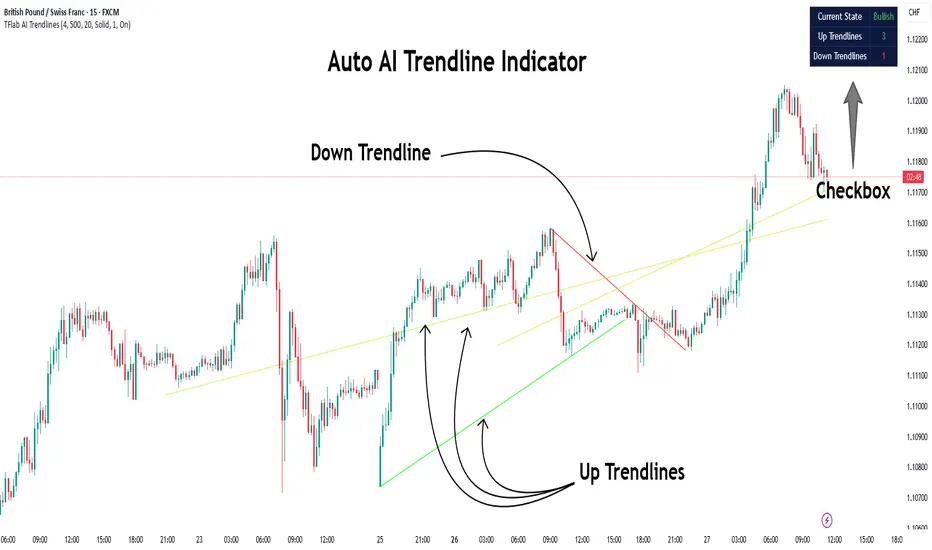

Auto AI Trendlines [TradingFinder] Clustering & Filtering Trends🔵 Introduction

Auto AI trendlines Clustering & Filtering Trends Indicator, draws a variety of trendlines. This auto plotting trendline indicator plots precise trendlines and regression lines, capturing trend dynamics.

Trendline trading is the strongest strategy in the financial market.

Regression lines, unlike trendlines, use statistical fitting to smooth price data, revealing trend slopes. Trendlines connect confirmed pivots, ensuring structural accuracy. Regression lines adapt dynamically.

The indicator’s ascending trendlines mark bullish pivots, while descending ones signal bearish trends. Regression lines extend in steps, reflecting momentum shifts. As the trend is your friend, this tool aligns traders with market flow.

Pivot-based trendlines remain fixed once confirmed, offering reliable support and resistance zones. Regression lines, adjusting to price changes, highlight short-term trend paths. Both are vital for traders across asset classes.

🔵 How to Use

There are four line types that are seen in the image below; Precise uptrend (green) and downtrend (red) lines connect exact price extremes, while Pivot-based uptrend and downtrend lines use significant swing points, both remaining static once formed.

🟣 Precise Trendlines

Trendlines only form after pivot points are confirmed, ensuring reliability. This reduces false signals in choppy markets. Regression lines complement with real-time updates.

The indicator always draws two precise trendlines on confirmed pivot points, one ascending and one descending. These are colored distinctly to mark bullish and bearish trends. They remain fixed, serving as structural anchors.

🟣 Dynamic Regression Lines

Regression lines, adjusting dynamically with price, reflect the latest trend slope for real-time analysis. Use these to identify trend direction and potential reversals.

Regression lines, updated dynamically, reflect real-time price trends and extend in steps. Ascending lines are green, descending ones orange, with shades differing from trendlines. This aids visual distinction.

🟣 Bearish Chart

A Bullish State emerges when uptrend lines outweigh or match downtrend lines, with recent upward momentum signaling a potential rise. Check the trend count in the state table to confirm, using it to plan long positions.

🟣 Bullish Chart

A Bearish State is indicated when downtrend lines dominate or equal uptrend lines, with recent downward moves suggesting a potential drop. Review the state table’s trend count to verify, guiding short position entries. The indicator reflects this shift for strategic planning.

🟣 Alarm

Set alerts for state changes to stay informed of Bullish or Bearish shifts without constant monitoring. For example, a transition to Bullish State may signal a buying opportunity. Toggle alerts On or Off in the settings.

🟣 Market Status

A table summarizes the chart’s status, showing counts of ascending and descending lines. This real-time overview simplifies trend monitoring. Check it to assess market bias instantly.

Monitor the table to track line counts and trend dominance.

A higher count of ascending lines suggests bullish bias. This helps traders align with the prevailing trend.

🔵 Settings

Number of Trendlines : Sets total lines (max 10, min 3), balancing chart clarity and trend coverage.

Max Look Back : Defines historical bars (min 50) for pivot detection, ensuring robust trendlines.

Pivot Range : Sets pivot sensitivity (min 2), adjusting trendline precision to market volatility.

Show Table Checkbox : Toggles display of a table showing ascending/descending line counts.

Alarm : Enable or Disable the alert.

🔵 Conclusion

The multi slopes indicator, blending pivot-based trendlines and dynamic regression lines, maps market trends with precision. Its dual approach captures both structural and short-term momentum.

Customizable settings, like trendline count and pivot range, adapt to diverse trading styles. The real-time table simplifies trend monitoring, enhancing efficiency. It suits forex, stocks, and crypto markets.

While trendlines anchor long-term trends, regression lines track intraday shifts, offering versatility. Contextual analysis, like price action, boosts signal reliability. This indicator empowers data-driven trading decisions.

Nyx-AI Market Intelligence DashboardNyx AI Market Intelligence Dashboard is a non-signal-based environmental analysis tool that provides real-time insight into short-term market behavior. It is designed to help traders understand the quality of current price action, volume dynamics, volatility conditions, and structural behavior. It informs the trader whether the current market environment is supportive or hostile to trading and whether any active signal (from other tools) should be trusted, filtered, or avoided altogether.

Nyx is composed of seven intelligent modules. Each module operates independently but is visually unified through a floating dashboard panel on the chart. This panel renders live diagnostics every few bars, maintaining a low visual footprint without drawing overlays or modifying price.

Market Posture Engine

This module reads individual candlesticks using real-time candle anatomy to interpret directional bias and sentiment. It examines body-to-range ratio, wick imbalances, and compares them to prior bars. If the current candle is a large momentum body with minimal wick, it is interpreted as a directional thrust. If it is a small body with equal wicks, it is considered indecision. Engulfing patterns are used to detect potential liquidity tests. The system outputs a plain-text posture signal such as Building Bullish Intent, Bearish Momentum, Indecision Zone, Testing Liquidity (Up or Down), or Neutral.

Flow Reversal Engine

This module monitors short-term structural shifts and volume contraction to detect early signs of reversal or exhaustion. It looks for lower highs or higher lows paired with weakening volume and closing behavior that implies loss of momentum. It also monitors divergence between price and volume, as well as bar-to-bar momentum stalls (where highs and lows stop expanding). When these conditions are met, it outputs one of several states including Top Forming, Bottom Forming, Flow Divergence, Momentum Stall, or Neutral. This is useful for detecting inflection points before they manifest on trend indicators.

Fractal Context Engine

This engine compares the current bar’s range to its surrounding structural context. It uses a dynamic lookback length based on volatility. It determines whether the market is in expansion (strong directional trend), compression (shrinking range), or a transitional phase. A special case called Flip In Progress is triggered when the current high and low exceed the entire recent range, which often precedes sharp reversals or volatility expansion. The result is one of the following: Trend Expansion, Trend Breakdown, Sideways or Coil, Flip In Progress, or Expansion to Coil.

Candle Behavior Analyzer

This module analyzes the last five candles as a set to detect behavioral traits that a single candle may not reveal. It calculates average body and wick size, and counts how many recent candles show thrust (large body dominance), trap behavior (price returns inside wicks), or weakness (small bodies with high wick ratios). The module outputs one of the following behaviors: Aggressive Buying, Aggressive Selling, Trap Pattern, Trap During Coil, Low Participation, Low Energy, or Fakeout Candle. This helps the trader assess sentiment quality and the reliability of price movement.

Volatility Forecast and Compression Memory

This module predicts whether a breakout is likely based on recent compression behavior. It tracks how many of the last 10 bars had significantly reduced range compared to average. If a certain threshold is met without any recent large expansion bar, the system forecasts that a volatility expansion is likely in the near future. It also records how many bars ago the last high volatility impulse occurred and classifies whether current conditions are compressing. The outputs are Expansion Likely, Active Compression, and Last Burst memory, which provide breakout timing and energy insights.

Entry Filter

This module scores the current bar based on four adaptive criteria: body size relative to range, volume strength relative to average, current volatility versus historical volatility, and price position relative to a 20-period moving average. Each factor is scored as either 1 or 2. The total score is adjusted by a behavioral modifier that adds or subtracts a point if recent candles show aggression or trap behavior. Final scores range from 4 to 8 and are classified into Optimal, Mixed, or Avoid categories. This module is not a trade signal. It is a confluence filter that evaluates whether conditions are favorable for entry. It is particularly effective when layered with other indicators to improve precision.

Liquidity Intent Engine

This engine checks for price behavior around recent swing highs and lows. It uses adaptive pivots based on volatility to determine if price has swept above a recent high or below a recent low. This behavior is often associated with institutional liquidity hunts. If a sweep is detected and price has moved away from the sweep level, the engine infers directional intent and compares current distance to the high and low to determine which liquidity pool is more dominant. The output is Magnet Above, Magnet Below, or Conflict Zone. This is useful for anticipating directional bias driven by smart money activity.

Sticky Memory Tracking

To avoid flickering between states on low volatility or noisy price action, Nyx includes a sticky memory system. Each module’s output is preserved until a meaningful change is detected. For example, if Market Posture is Neutral and remains so for several bars, the previous non-neutral value is retained. This makes the dashboard more stable and easier to interpret without misleading noise.

Dashboard Rendering

All module outputs are displayed in a clean two-column panel anchored to any corner of the chart. Text values are color-coded, tooltips are added for context, and the data refreshes every few bars to maintain speed. The dashboard avoids clutter and blends seamlessly with other chart tools.

This tool is intended for informational and educational purposes only. It does not provide financial advice or trading signals. Nyx analyzes price, volume, structure, and volatility to offer context about the current market environment. It is not designed to predict future price movements or guarantee profitable outcomes. Traders should always use independent judgment and risk management. Past performance of any analysis logic does not guarantee future results.

Helacator Ai ThetaHelacator Ai Theta is a state-of-the-art advanced script. It helps the trader find the possibility of a trend reversal in the market. By finding that point at which the three black crows pattern combines with the three white soldiers pattern, it is the most cherished pattern in technical analysis for its signal of strong bullish or bearish momentum. Therefore, it is a very strong predictive tool in the ability of shifting markets.

Key Highlights: Three White Soldiers and Three Black Crows Patterns

The script identifies these candlestick formations that consist of three consecutive candles, either bullish (Three White Soldiers) or bearish (Three Black Crows). These patterns help the trader identify possible trend reversal points as they provide an early signal of a change in the market direction. It is with great care that the script is written to evaluate the position and relationship between the candlesticks for maintaining the accuracy of pattern recognition. Moving Averages for Trend Filtering:

Two important ones used are moving averages for filtering any signals not in accordance with the general trend. The length of these MAs is variable, allowing the traders to be in a position to adapt the script for use under different market conditions. The moving averages ensure that signals are only taken in the direction that supports the general market flow, so it leads to more reliability within the signals. The MAs are not plotted on the chart for the sake of clarity, but they still perform a crucial function in signal filtering and can be displayed optionally for a more detailed investigation. Cooldown filter to reduce over-trading

This is part of what is implemented in the script to prevent generation of consecutive signals too quickly. All this helps to reduce market noise and not overtrade—only when market conditions are at their best. The cooldown period can be set to be adjusted according to the trader's preference, making the script more versatile in its use. Practical Considerations: Educational Purpose: This script is for educational purposes only and should be part of a comprehensive trading approach. Proper risk management techniques should be observed while at the same time taking into consideration prevailing market conditions before making any trading decision.

No Guaranteed Results: The script is aimed at bringing signal accuracy into improvement to align with the broader market trend and reducing noise, but past performance cannot guarantee future success. Traders should use this script within their broad trading approach. Clean and Simple Chart Display: The primary goal of this script is to have a clear and simple display on the chart. The signals are prominently marked with "BUY" and "SELL," and the color of the bars has changed according to the last signal, thus traders can easily read the output. Community and Open Source Open Source Contribution: This script is open for contribution by the TradingView community. Any suggestions regarding improvements are highly welcomed. Candlestick patterns, moving averages, and the combination of the cooldown filter are presented in such a way as to give traders something special, and any modifications or extra touch by the community is appreciated. Attribution and Transparency: The script is based on standard technical analysis principles and for all parts inspired by or derivated from other available open-source scripts, credit is given where it is due. In this way, transparency ensures that the script adheres to TradingView's standards and promotes a collaborative community environment.

Edge AI Forecast [Edge Terminal]This indicator inputs the previous 150 closing prices in a simple two-layer neural network, normalizes the network inputs using a sigmoid function, uses a feedforward calculation to send it to the second layer, shows the MSE loss curve and uses both automatic and manual backpropagation (user input) to find the most likely forecast values and uses the analog forecasting algorithm to adjust and optimize the data furthermore to display potential prices on the chart.

Here's how it works:

The idea behind this script is to train a simple neural network to predict the future x values based on the sample data. For this, we use 2 types of data, Price and Volume.

The thinking behind this is that price alone can’t be used in this case because it doesn’t provide enough meaningful pattern data for the network but price and volume together can change the game. We’re planning to use more different data sets and expand on this in the future.

To avoid a bad mix of results, we technically have two neural networks, each processing a different data type, one for volume data and one for price data.

The actual prediction is decided by the way price and volume of the closing price relate to each other. Basically, the network passes the price and volume and finds the best relation between the two data set outputs and predicts where the price could be based on the upcoming volume of the latest candle.

The network adjusts the weights and biases using optimization algorithms like gradient descent to minimize the difference between the predicted and actual stock prices, typically measured by a loss function, (in this case, mean squared error) which you can see using the error rate bubble.

This is a good measure to see how well the network is performing and the idea is to adjust the settings inputs such as learning rate, epochs and data source to get the lowest possible error rate. That’s when you’re getting the most accurate prediction results.

For each data set, we use a multi-layer network. In a multi-layer neural network, the outputs of neurons in one layer serve as inputs to neurons in the next layer. Initially, the input layer of the neural network receives the historical data. Each input neuron represents a feature, such as previous stock prices and trading volumes over a specific period.

The hidden layers perform feature extraction and transformation through a series of weighted connections and activation functions. Each neuron in a hidden layer computes a weighted sum of the inputs from the previous layer, applies an activation function to the sum, and passes the result to the next layer using the feedforward (activation) function.

For extraction, we use a normalization function. This function takes a value or data (such as bar price) and divides it up by max scale which is the highest possible value of the bar. The idea is to take a normalized number, which is either below 1 or under 2 for simple use in the neural network layers.

For the activation, after computing the weighted sum, the neuron applies an activation function a(x). To introduce non-linearity into the model to pass it to the next layer. We use sigmoid activation functions in this case. The main reason we use sigmoid function is because the resulting number is between 0 to 1 and is better for models where we have to predict the probability as an output.

The final output of the network is passed as an input to the analog forecasting function. This is an algorithm commonly used in weather prediction systems. In this case, this is used to make predictions by comparing current values and assuming the patterns might repeat in the future.

There are many different ways to build an analog forecasting function but in our case, we’re used similarity measurement model:

X, as the current situation or set of current variables.

Y, as the outcome or variable of interest.

Si as the historical situations or patterns, where i ranges from 1 to n.

Vi as the vector of variables describing historical situation Si.

Oi as the outcome associated with historical situation Si.

First, we define a similarity measure sim(X,Vi) that quantifies the similarity between the current situation X and historical situation Si based on their respective variables Vi.

Then we select the K most similar historical situations (KNN Machine learning) based on the similarity measure sim(X,Vi). We denote the rest of the selected historical situations as {Si1, Si2,...Sik).

Then we examine the outcomes associated with the selected historical situations {Oi1, Oi2,...,Oik}.

Then we use the outcomes of the selected historical situations to forecast the future outcome Y^ using weighted averaging.

Finally, the output value of the analog forecasting is standardized using a standardization function which is the opposite of the normalization function. This function takes a normalized number and turns it back to its original value by multiplying it by the max scale (highest value of the bar). This function is used when the final number is produced by the network output at the end of the analog forecasting to turn the final value back into a price so it can be displayed on the chart with PineScript.

Settings:

Data source: Source of the neural network's input data.

Sample Bars: How many historical bars do you want to input into the neural network

Prediction Bars: How many bars you want the script to forecast

Show Training Rate: This shows the neural network's error rate for the optimization phase

Learning Rate: how many times you want the script to change the model in response to the estimated error (automatic)

Epochs: the network cycle or how many times you want to run the data through the network from the first layer to the last one.

Usage:

The sample bars input determines the number of historical bars to be used as a reference for the network. You need to change the Epochs and Learning Rate inputs for each asset and chart timeframe to get the lowest error rate.

On the surface, the highest possible epoch and learning rate should produce the most effective results but that's not always the case.

If the epochs rate is too high, there is a chance we face overfitting. Essentially, you might be over processing good data which can make it useless.

On the other hand, if the learning rate is too high, the network may overshoot the optimal solution and diverge. This is almost like the same issue I mentioned above with a high epoch rate.

Access:

It took over 4 months to develop this script and we’re constantly improving it so it took a lot of manpower to develop this script. Also when it comes to neural networks, Pine Script isn’t the most optimal language to build a neural network in, so we had to resort to a few proprietary mathematical formulas to ensure this runs smoothly without giving out an error for overprocessing, specially when you have multiple neural networks with many layers.

The optimization done to make this script run on Pine Script is basically state of the art and because of this, we would like to keep the code closed source at the moment.

On the other hand we don’t want to publish the code publicly as we want to keep the trading edge this script gives us in a closed loop, for our own small group of members so we have to keep the code closed. We only accept invites from expert traders who understand how this script and algo trading works and the type of edge it provides.

Additionally, at the moment we don’t want to share the code as some of the parts of this network, specifically the way we hand the data from neural network output into the analog method formula are proprietary code and we’d like to keep it that way.

You can contact us for access and if we believe this works for your trading case, we will provide you with access.

Optimal Moving Average (AI/ML) [wbburgin]Some traders swear by the 200-period moving average. Others, by the 100-period. Others, the 14-period. It depends on your asset, your timeframe, the trend…

The fact of the matter is that no moving average will ever be a consistent indicator for a serious trader - a fixed-length moving average will always need confirmation indicators and tests. When your instrument is trending, you need a faster moving average to better fit the data; when your instrument is ranging, you need a slower moving average that cleans the data. This just is not possible given the way the moving average is traditionally coded, which makes it a lagging indicator.

Thus we need a moving average that:

can project the next prices, and

can change its length depending on what best fits these future prices.

The Optimal Moving Average selects the optimal moving average length for a projected future price. The algorithm classifies moving averages by their effectiveness in predicting future price movement. If a moving average of length n has historically been accurate in predicting the next bar, the moving average will be tested compared to its peers ( n -1, n +5, n -100, etc.) and promoted or demoted depending on its effectiveness. This means that the indicator will not have a length input like other static moving averages or machine-learning moving averages on TradingView- it will select the ideal length for your chart from the average that has the least error and best prediction.

Advantages over other ML Moving Averages on TradingView

The vast majority of AI/ML moving average algorithms classify their moving averages only by if the average is above or below the current price.

This approach is inherently flawed because the model

Is not predictive of future prices (the structural lagging problem still exists),

Is not built on a variable-length MA (cannot select alternating lengths depending on the bar), and

does not classify the scale of difference between the MA and the price.

This indicator solves all those problems. It classifies moving averages by the scale of which their rate predicts the next price. Thus it is quick to catch trend changes but also acts as support or resistance, and models the projected price more accurately than a traditional moving average.

Support & Resistance AI (K means/median) [ThinkLogicAI]█ OVERVIEW

K-means is a clustering algorithm commonly used in machine learning to group data points into distinct clusters based on their similarities. While K-means is not typically used directly for identifying support and resistance levels in financial markets, it can serve as a tool in a broader analysis approach.

Support and resistance levels are price levels in financial markets where the price tends to react or reverse. Support is a level where the price tends to stop falling and might start to rise, while resistance is a level where the price tends to stop rising and might start to fall. Traders and analysts often look for these levels as they can provide insights into potential price movements and trading opportunities.

█ BACKGROUND

The K-means algorithm has been around since the late 1950s, making it more than six decades old. The algorithm was introduced by Stuart Lloyd in his 1957 research paper "Least squares quantization in PCM" for telecommunications applications. However, it wasn't widely known or recognized until James MacQueen's 1967 paper "Some Methods for Classification and Analysis of Multivariate Observations," where he formalized the algorithm and referred to it as the "K-means" clustering method.

So, while K-means has been around for a considerable amount of time, it continues to be a widely used and influential algorithm in the fields of machine learning, data analysis, and pattern recognition due to its simplicity and effectiveness in clustering tasks.

█ COMPARE AND CONTRAST SUPPORT AND RESISTANCE METHODS

1) K-means Approach:

Cluster Formation: After applying the K-means algorithm to historical price change data and visualizing the resulting clusters, traders can identify distinct regions on the price chart where clusters are formed. Each cluster represents a group of similar price change patterns.

Cluster Analysis: Analyze the clusters to identify areas where clusters tend to form. These areas might correspond to regions of price behavior that repeat over time and could be indicative of support and resistance levels.

Potential Support and Resistance Levels: Based on the identified areas of cluster formation, traders can consider these regions as potential support and resistance levels. A cluster forming at a specific price level could suggest that this level has been historically significant, causing similar price behavior in the past.

Cluster Standard Deviation: In addition to looking at the means (centroids) of the clusters, traders can also calculate the standard deviation of price changes within each cluster. Standard deviation is a measure of the dispersion or volatility of data points around the mean. A higher standard deviation indicates greater price volatility within a cluster.

Low Standard Deviation: If a cluster has a low standard deviation, it suggests that prices within that cluster are relatively stable and less likely to exhibit sudden and large price movements. Traders might consider placing tighter stop-loss orders for trades within these clusters.

High Standard Deviation: Conversely, if a cluster has a high standard deviation, it indicates greater price volatility within that cluster. Traders might opt for wider stop-loss orders to allow for potential price fluctuations without getting stopped out prematurely.

Cluster Density: Each data point is assigned to a cluster so a cluster that is more dense will act more like gravity and

2) Traditional Approach:

Trendlines: Draw trendlines connecting significant highs or lows on a price chart to identify potential support and resistance levels.

Chart Patterns: Identify chart patterns like double tops, double bottoms, head and shoulders, and triangles that often indicate potential reversal points.

Moving Averages: Use moving averages to identify levels where the price might find support or resistance based on the average price over a specific period.

Psychological Levels: Identify round numbers or levels that traders often pay attention to, which can act as support and resistance.

Previous Highs and Lows: Identify significant previous price highs and lows that might act as support or resistance.

The key difference lies in the approach and the foundation of these methods. Traditional methods are based on well-established principles of technical analysis and market psychology, while the K-means approach involves clustering price behavior without necessarily incorporating market sentiment or specific price patterns.

It's important to note that while the K-means approach might provide an interesting way to analyze price data, it should be used cautiously and in conjunction with other traditional methods. Financial markets are influenced by a wide range of factors beyond just price behavior, and the effectiveness of any method for identifying support and resistance levels should be thoroughly tested and validated. Additionally, developments in trading strategies and analysis techniques could have occurred since my last update.

█ K MEANS ALGORITHM

The algorithm for K means is as follows:

Initialize cluster centers

assign data to clusters based on minimum distance

calculate cluster center by taking the average or median of the clusters

repeat steps 1-3 until cluster centers stop moving

█ LIMITATIONS OF K MEANS

There are 3 main limitations of this algorithm:

Sensitive to Initializations: K-means is sensitive to the initial placement of centroids. Different initializations can lead to different cluster assignments and final results.

Assumption of Equal Sizes and Variances: K-means assumes that clusters have roughly equal sizes and spherical shapes. This may not hold true for all types of data. It can struggle with identifying clusters with uneven densities, sizes, or shapes.

Impact of Outliers: K-means is sensitive to outliers, as a single outlier can significantly affect the position of cluster centroids. Outliers can lead to the creation of spurious clusters or distortion of the true cluster structure.

█ LIMITATIONS IN APPLICATION OF K MEANS IN TRADING

Trading data often exhibits characteristics that can pose challenges when applying indicators and analysis techniques. Here's how the limitations of outliers, varying scales, and unequal variance can impact the use of indicators in trading:

Outliers are data points that significantly deviate from the rest of the dataset. In trading, outliers can represent extreme price movements caused by rare events, news, or market anomalies. Outliers can have a significant impact on trading indicators and analyses:

Indicator Distortion: Outliers can skew the calculations of indicators, leading to misleading signals. For instance, a single extreme price spike could cause indicators like moving averages or RSI (Relative Strength Index) to give false signals.

Risk Management: Outliers can lead to overly aggressive trading decisions if not properly accounted for. Ignoring outliers might result in unexpected losses or missed opportunities to adjust trading strategies.

Different Scales: Trading data often includes multiple indicators with varying units and scales. For example, prices are typically in dollars, volume in units traded, and oscillators have their own scale. Mixing indicators with different scales can complicate analysis:

Normalization: Indicators on different scales need to be normalized or standardized to ensure they contribute equally to the analysis. Failure to do so can lead to one indicator dominating the analysis due to its larger magnitude.

Comparability: Without normalization, it's challenging to directly compare the significance of indicators. Some indicators might have a larger numerical range and could overshadow others.

Unequal Variance: Unequal variance in trading data refers to the fact that some indicators might exhibit higher volatility than others. This can impact the interpretation of signals and the performance of trading strategies:

Volatility Adjustment: When combining indicators with varying volatility, it's essential to adjust for their relative volatilities. Failure to do so might lead to overemphasizing or underestimating the importance of certain indicators in the trading strategy.

Risk Assessment: Unequal variance can impact risk assessment. Indicators with higher volatility might lead to riskier trading decisions if not properly taken into account.

█ APPLICATION OF THIS INDICATOR

This indicator can be used in 2 ways:

1) Make a directional trade:

If a trader thinks price will go higher or lower and price is within a cluster zone, The trader can take a position and place a stop on the 1 sd band around the cluster. As one can see below, the trader can go long the green arrow and place a stop on the one standard deviation mark for that cluster below it at the red arrow. using this we can calculate a risk to reward ratio.

Calculating risk to reward: targeting a risk reward ratio of 2:1, the trader could clearly make that given that the next resistance area above that in the orange cluster exceeds this risk reward ratio.

2) Take a reversal Trade:

We can use cluster centers (support and resistance levels) to go in the opposite direction that price is currently moving in hopes of price forming a pivot and reversing off this level.

Similar to the directional trade, we can use the standard deviation of the cluster to place a stop just in case we are wrong.

In this example below we can see that shorting on the red arrow and placing a stop at the one standard deviation above this cluster would give us a profitable trade with minimal risk.

Using the cluster density table in the upper right informs the trader just how dense the cluster is. Higher density clusters will give a higher likelihood of a pivot forming at these levels and price being rejected and switching direction with a larger move.

█ FEATURES & SETTINGS

General Settings:

Number of clusters: The user can select from 3 to five clusters. A good rule of thumb is that if you are trading intraday, less is more (Think 3 rather than 5). For daily 4 to 5 clusters is good.

Cluster Method: To get around the outlier limitation of k means clustering, The median was added. This gives the user the ability to choose either k means or k median clustering. K means is the preferred method if the user things there are no large outliers, and if there appears to be large outliers or it is assumed there are then K medians is preferred.

Bars back To train on: This will be the amount of bars to include in the clustering. This number is important so that the user includes bars that are recent but not so far back that they are out of the scope of where price can be. For example the last 2 years we have been in a range on the sp500 so 505 days in this setting would be more relevant than say looking back 5 years ago because price would have to move far to get there.

Show SD Bands: Select this to show the 1 standard deviation bands around the support and resistance level or unselect this to just show the support and resistance level by itself.

Features:

Besides the support and resistance levels and standard deviation bands, this indicator gives a table in the upper right hand corner to show the density of each cluster (support and resistance level) and is color coded to the cluster line on the chart. Higher density clusters mean price has been there previously more than lower density clusters and could mean a higher likelihood of a reversal when price reaches these areas.

█ WORKS CITED

Victor Sim, "Using K-means Clustering to Create Support and Resistance", 2020, towardsdatascience.com

Chris Piech, "K means", stanford.edu

█ ACKNOLWEDGMENTS

@jdehorty- Thanks for the publish template. It made organizing my thoughts and work alot easier.

TCG AI ToolsIntroduction:

This script is a result of an AI recommended created trading strategy that is design to offer new traders’ easy access to trend information and oversold/overbought conditions. Here we have combined commonly used indicators into a single unique visualization that quickly identifies trend changes and both RSI and Bollinger Band based overbought and oversold conditions, and allows all three indicators to be used simultaneously while taking up limited space on the chart.

The value in combining these three indicators is found in the harmony and clarity they are able to provide new traders. Trend changes can be difficult to identify based solely on candlestick analysis, therefore using the moving averages allows the trader to simplify the process of establishing bullish or bearish trends. Once a trend is established it can be very attractive for new traders to establish entries at the wrong time. For this reason, it is useful to include two different overbought and oversold indicators. The Bollinger Bands are included as one of the methods for establishing extreme prices that often result in reversals, and the relative strength index is similarly utilized as a second means to warn traders of extreme conditions.

Using the Indicator

1. MA10 MA20 Trend Indicator

The large red/green horizontal bar located at the 0 line on the X axis is the trend direction indicator. This visualization compares the 10 and 20 period moving averages to establish trend. When the MA10 is above the MA20 the trend is considered bullish and supportive of long positions and indicates such by changing the color of the horizontal bar to green. When the MA10 is below MA20 the trend is considered bearish and indicates such by changing the color of the horizontal bar to red. Color changes occur at the moment of a MA crossover/under.

2. Relative Strength Index.

The vertical red and green bars that make up the background of the panel indicate conditions wherein the RSI is considered overbought or oversold. When the vertical bar is red it indicates that RSI is below 30 suggesting that current conditions are oversold and supportive of long entries. When the vertical bar is green it suggests that the current conditions are overbought and are supportive of short entries.

3. Bollinger Band Extremes

Within the horizontal red/green bar there are red and green arrows. These arrows represent periods where the price is exceeding the upper or lower Bollinger bands and indicate overbought/oversold conditions. When a green arrow appears, it indicates that the price has crossed below the lower BB and is supportive of long entries. If a red arrow appears it indicates that the price has crossed above the upper Bollinger band and conditions are supportive of short entries.

Universal Moving Average Convergence DivergenceI changed MACD formula to divergence of (MA26/MA12 - 1).

And its make it more useful.

Cuz:

1) comparability with all other coins with different prices.

2) fix small numbers in low price coines like shiba

3) making a good indicator like RSI to use it for optimization and ML/AI projects as a variable

Most important thing about this indicator is that its Universal

Now you can compare the UMACD of Shiba with Bitcoin without any problem in matamatics space.No need to use virtuality and its important in Optimization problems that we rediuse the problem from a picture to a number(A plot to a list of numbers)

If we don't care about exagrated pumps and dumps, we can say to it Normalized-MACD too. Cuz in normal situations its MAX ≈ 0.1 and MIN ≈ -0.1