Pesquisar nos scripts por "Volatility"

Standard Deviation Levels with Settlement Price and VolatilityStandard Deviation Levels with Settlement Price and Volatility.

This indicator plots the standard deviation levels based on the settlement price and the implied volatility. It works for all Equity Stocks and Futures.

For Futures

Symbol Volatility Symbol (Implied Volatility)

NQ VXN

ES VIX

YM VXD

RTY RVX

CL OVX

GC GVZ

BTC DVOL

The plot gives you an ideas that the price has what probability staying in the range of 1SD,2SD,3SD ( In normal distribution method)

Please provide the feedback or comments if you find any improvements

UM VIX30/VIX Regime & Volatility Roll Yield

SUMMARY

A front-of-the-curve volatility indicator that compares spot VIX to a synthetic 30-day VIX (VIX30) built from VX1/VX2 futures, revealing early volatility pressure, regime shifts, and roll-yield transitions. Ideal for timing long/short volatility trades in VXX, UVXY, SVIX, and VIX futures.

DESCRIPTION

This indicator compares spot VIX to a synthetic 30-day constant-maturity volatility estimate (“VIX30”) built from VX1 and VX2 futures. The VIX30/VIX Ratio reveals short-term volatility pressure and regime shifts that traditional VX1/VX2 roll-yield alone often misses.

VIX30 is constructed using true calendar-day interpolation between VX1 and VX2, with VX1% and VX2% showing the real-time weights behind the 30-day volatility anchor. The table displays the volatility regime, the VX1/VX2 weights, spot-term roll yield (VIX30/VIX), and futures-term roll yield (VX2/VX1), giving a complete, front-of-the-curve perspective on volatility dynamics.

Use this to spot early volatility expansions, collapsing contango, and regime transitions that influence VXX, UVXY, SVIX, VX options, and VIX futures.

HOW IT WORKS

The script calculates the exact calendar days to expiration for the front two VIX futures. It then applies linear interpolation to blend VX1 and VX2 into a 30-day constant-maturity synthetic volatility measure (“VIX30”). Comparing VIX30 to spot VIX produces the VIX30/VIX Ratio, which highlights short-term volatility pressure and regime direction. A full term-structure table summarizes regime, VX1%/VX2% weights, and both spot-term and futures-term roll yields.

DEFAULT SETTINGS

VX1! and VX2! are used by default for front-month and second-month futures. These may be manually overridden if TradingView rolls contracts early. The default timeframe is 30 minutes, and the VIX30/VIX Ratio uses a 21-period EMA for regime smoothing. The historical threshold is set to 1.08, reflecting the long-run average relationship between VIX30 and VIX.

SUGGESTED USES

• Identify early volatility expansions before they appear in VX1/VX2 roll yield.

• Confirm contango/backwardation shifts with front-of-curve context.

• Time long/short volatility trades in VXX, UVXY, SVIX, and VX options.

• Monitor regime transitions (Low → Cautionary → High) to anticipate trend inflections.

• Combine with price action, Nadaraya-Watson trends, or MA color-flip systems for higher-confidence entries.

• MA red → green flips may signal opportunities to short volatility or increase equity exposure.

• MA green → red flips may signal opportunities to go long volatility, reduce equity exposure, or take short-equity positions.

ALERTS

Alerts trigger when the ratio crosses above or below the historical threshold or when the moving-average slope flips direction. A green flip signals rising volatility pressure; a red flip signals fading or collapsing volatility. These alert conditions can be used to automate long/short volatility bias shifts or trade-entry notifications.

FURTHER HINTS

• Increasing orange/red in the table suggests an emerging higher-volatility environment.

• SVIX (inverse volatility ETF) can trend strongly when volatility decays; on a 6-hour chart, MA green flips often align with attractive short-volatility opportunities.

• For long-volatility trades, consider shrinking to a 30-minute chart and watching for MA green → red flips as early entry cues.

• Experiment with different timeframes and smoothing lengths to match your trading style.

• Higher VIX30/VIX and VX2/VX1 roll yields generally imply faster decay in VXX, UVXY, and UVIX — or stronger upside momentum in SVIX.

• The author likes the 6-hour chart for short vol, and the 30-minute chart for long vol. Long vol trades are fast and furious so you want to be quick.

ATR Volatility and Trend AnalysisATR Volatility and Trend Analysis

Unlock the power of the Average True Range (ATR) with the ATR Volatility and Trend Analysis indicator. This comprehensive tool is designed to provide traders with a multi-faceted view of market dynamics, combining volatility analysis, dynamic support and resistance levels, and trend detection into a single, easy-to-use indicator.

How It Works

The ATR Volatility and Trend Analysis indicator is built upon the core concept of the ATR, a classic measure of market volatility. It expands on this by providing several key features:

Dynamic ATR Bands: The indicator plots three sets of upper and lower bands around the price. These bands are calculated by multiplying the current ATR value by user-defined multipliers. They act as dynamic support and resistance levels, widening during volatile periods and contracting during calm markets.

Volatility Breakout Signals: Identify potential breakouts with precision. The indicator generates a signal when the current ATR value surges above its own moving average by a specified threshold, indicating a significant increase in volatility that could lead to a strong price move.

Trend Detection: The indicator determines the market trend by analyzing both price action and ATR behavior. A bullish trend is signaled when the price is above its moving average and volatility is increasing. Conversely, a bearish trend is signaled when the price is below its moving average and volatility is increasing.

How to Use the ATR Multi-Band Indicator

Identify Support and Resistance: Use the ATR bands as key levels. Price approaching the outer bands may indicate overbought or oversold conditions, while a break of the bands can signal a strong continuation.

Confirm Breakouts: Look for a volatility breakout signal to confirm the strength behind a price move. A breakout from a consolidation range accompanied by a volatility signal is a strong indicator of a new trend.

Trade with the Trend: Use the background coloring and trend signals to align your trades with the dominant market direction. Enter long positions during confirmed bullish trends and short positions during bearish trends.

Set Up Alerts: The indicator includes alerts for band crosses, trend changes, and volatility breakouts, ensuring you never miss a potential trading opportunity.

What makes it different?

While many indicators use ATR, the ATR Volatility and Trend Analysis tool is unique in its integration of multiple ATR-based concepts into a single, cohesive system. It doesn't just show volatility; it interprets it in the context of price action to deliver actionable trend and breakout signals, making it a complete solution for ATR-based analysis.

Disclaimer

This indicator is designed as a technical analysis tool and should be used in conjunction with other forms of analysis and proper risk management.

Past performance does not guarantee future results, and traders should thoroughly test any strategy before implementing it with real capital.

Average VolatilityThis script offers a unique and practical approach to visualizing average volatility by calculating a simple moving average of the daily high-low ranges, directly reflecting price fluctuations over a user-defined period. Unlike standard volatility indicators, it provides customizable options such as adjustable period length, display of absolute and percentage volatility values, and flexible text formatting for clear and tailored insights. This makes it a valuable tool for traders seeking to better understand market volatility trends and manage risk more effectively. Its straightforward visualization supports informed decision-making across various instruments and timeframes.

The indicator displays the average volatility over a configurable period as a bar chart (originally designed for daily intervals). It visualizes the price range (difference between high and low) across a selectable number of periods, as well as its ratio to the closing price, offering various customization options.

For many traders, assets with daily moves of 1% or more may offer greater profit opportunities, especially for short-term trading strategies. Instruments with lower volatility are generally less favored and often not recommended in such approaches due to reduced trading potential. Please note that higher volatility also implies increased risk, and potential losses can be significant. Always use proper risk management.

Detailed description:

The script calculates average volatility as a simple moving average of the high-low ranges (default: 5 periods, intended for daily timeframes). Volatility can be shown as either a bar or line chart. Users can choose to display the absolute volatility values and/or the volatility expressed as a percentage of the closing price. Text size and spacing between labels are adjustable to ensure readability across different instruments. Additionally, the last (unconfirmed) bar can be shown or hidden, since its value depends on the current price. Overall, the script provides a flexible and clear visualization of an instrument’s volatility.

---

Russian:

Индикатор отображает среднюю волатильность как простое скользящее среднее диапазонов «максимум-минимум» (по умолчанию 5 периодов, предназначено для дневных таймфреймов). Волатильность может отображаться в виде столбчатой или линейной диаграммы. Пользователи могут выбрать отображение абсолютных значений волатильности и/или волатильности, выраженной в процентах от цены закрытия. Размер текста и расстояния между надписями регулируются для удобочитаемости на разных инструментах. Кроме того, последний (неподтверждённый) столбец можно показать или скрыть, так как его значение зависит от текущей цены. В общем, скрипт обеспечивает гибкое и наглядное отображение волатильности инструмента.

Активы с волатильностью от 1% и выше дают больше возможностей для краткосрочной торговли, но риск также выше. Инструменты с низкой волатильностью не рекомендуются для таких подходов из-за ограниченного торгового потенциала и сложности в реализации прибыльных сделок. Всегда применяйте риск-менеджмент.

---

Spanish:

El script calcula la volatilidad promedio como un promedio móvil simple de las diferencias entre máximos y mínimos (por defecto 5 periodos, pensado para intervalos diarios). La volatilidad puede mostrarse como gráfico de barras o de líneas. El usuario puede elegir mostrar los valores absolutos de la volatilidad y/o los valores expresados en porcentaje respecto al precio de cierre. El tamaño del texto y el espacio entre las etiquetas son ajustables para garantizar la legibilidad en diferentes instrumentos. Además, se puede mostrar u ocultar la última barra (no confirmada), ya que su valor depende del precio actual. En conjunto, el script proporciona una visualización flexible y clara de la volatilidad del instrumento.

Los activos con una volatilidad del 1% o más ofrecen mayores oportunidades para el trading a corto plazo, pero también conllevan un mayor riesgo. Los instrumentos con baja volatilidad no se recomiendan para este tipo de estrategias debido a su limitado potencial de trading y la dificultad para obtener ganancias. Siempre utilice una gestión de riesgos adecuada.

[NIC] Volatility Anomaly Indicator (Inspired by Jeff Augen)Volatility Anomaly Indicator (Inspired by Jeff Augen)

The Volatility Anomaly Indicator, inspired by Jeff Augen’s The Volatility Edge in Options Trading, helps traders spot price distortions by analyzing volatility imbalances. It compares short-term (10-day) and long-term (30-day) historical volatility (HV), plotting the ratio in a subgraph with clusters of dots to highlight anomalies—red for volatility spikes (potential sells) and green for calm periods (potential buys).

Originality: This indicator uniquely adapts Augen’s volatility concepts into a visual tool, focusing on relative volatility distortions rather than absolute levels, making it ideal for volatile assets like $TQQQ.

Features:

Calculates the ratio of short-term to long-term volatility.

Detects spikes (ratio > 1.5) and calm periods (ratio < 0.67) with customizable thresholds.

Plots volatility ratio as a blue line, with red/green dots for anomalies.

Includes optional buy/sell signals on the main chart (if overlay is enabled).

How It Works

The indicator computes historical volatility using log returns, then calculates the short-term to long-term volatility ratio. Spikes and calm periods are marked with dots in the subgraph, and threshold lines (1.5 and 0.67) provide context. Buy signals (green triangles) trigger during calm periods, and sell signals (red triangles) during spikes.

How to Use

Apply to any chart (e.g., NASDAQ:TQQQ daily).

Adjust inputs: Short Volatility Period (10), Long Volatility Period (30), Volatility Spike Threshold (1.5).

Watch for red dot clusters (spikes, potential sells) and green dot clusters (calm, potential buys).

Combine with price action or RSI for confirmation.

Why Use This Indicator?

Focuses on volatility-driven price inefficiencies.

Clear visualization with dot clusters.

Customizable for different assets and timeframes.

Limitations

Not a standalone system; requires confirmation.

May give false signals in choppy markets.

Uptrick: Momentum-Volatility Composite Signal### Title: Uptrick: Momentum-Volatility Composite Signal

### Overview

The "Uptrick: Momentum-Volatility Composite Signal" is an innovative trading tool designed to offer traders a sophisticated synthesis of momentum, volatility, volume flow, and trend detection into a single comprehensive indicator. This tool stands out by providing an integrated view of market dynamics, which is critical for identifying potential trading opportunities with greater precision and confidence. Its unique approach differentiates it from traditional indicators available on the TradingView platform, making it a valuable asset for traders aiming to enhance their market analysis.

### Unique Features

This indicator integrates multiple crucial elements of market behavior:

- Momentum Analysis : Utilizes Rate of Change (ROC) metrics to assess the speed and strength of market movements.

- Volatility Tracking : Incorporates Average True Range (ATR) metrics to measure market volatility, aiding in risk assessment.

- Volume Flow Analysis : Analyzes shifts in volume to detect buying or selling pressure, adding depth to market understanding.

- Trend Detection : Uses the difference between short-term and long-term Exponential Moving Averages (EMA) to detect market trends, providing insights into potential reversals or confirmations.

Customization and Inputs

The Uptrick indicator offers a variety of user-defined settings tailored to fit different trading styles and strategies, enhancing its adaptability across various market conditions:

Rate of Change Length (rocLength) : This setting defines the period over which momentum is calculated. Shorter periods may be preferred by day traders who need to respond quickly to market changes, while longer periods could be better suited for position traders looking at more extended trends.

ATR Length (atrLength) : Adjusts the timeframe for assessing volatility. A shorter ATR length can help day traders manage the quick shifts in market volatility, whereas longer lengths might be more applicable for swing or position traders who deal with longer-term market movements.

Volume Flow Length (volumeFlowLength): Determines the analysis period for volume flow to identify buying or selling pressure. Day traders might opt for shorter periods to catch rapid volume changes, while longer periods could serve swing traders to understand the accumulation or distribution phases better.

Short EMA Length (shortEmaLength): Specifies the period for the short-term EMA, crucial for trend detection. Shorter lengths can aid day traders in spotting immediate trend shifts, whereas longer lengths might help swing traders in identifying more sustainable trend changes.

Long EMA Length (longEmaLength): Sets the period for the long-term EMA, which is useful for observing longer-term market trends. This setting is particularly valuable for position traders who need to align with the broader market direction.

Composite Signal Moving Average Length (maLength): This parameter sets the smoothing period for the composite signal's moving average, helping to reduce noise in the signal output. A shorter moving average length can be beneficial for day traders reacting to market conditions swiftly, while a longer length might help swing and position traders in smoothing out less significant fluctuations to focus on significant trends.

These customization options ensure that traders can fine-tune the Uptrick indicator to their specific trading needs, whether they are scanning for quick opportunities or analyzing more prolonged market trends.

### Functionality Details

The indicator operates through a sophisticated algorithm that integrates multiple market dimensions:

1. Momentum and Volatility Calculation : Combines ROC and ATR to gauge the market’s momentum and stability.

2. Volume and Trend Analysis : Integrates volume data with EMAs to provide a comprehensive view of current market trends and potential shifts.

3. Signal Composite : Each component is normalized and combined into a composite signal, offering traders a nuanced perspective on when to enter or exit trades.

The indicator performs its calculations as follows:

Momentum and Volatility Calculation:

roc = ta.roc(close, rocLength)

atr = ta.atr(atrLength)

Volume and Trend Analysis:

volumeFlow = ta.cum(volume) - ta.ema(ta.cum(volume), volumeFlowLength)

emaShort = ta.ema(close, shortEmaLength)

emaLong = ta.ema(close, longEmaLength)

emaDifference = emaShort - emaLong

Composite Signal Calculation:

Normalizes each component (ROC, ATR, volume flow, EMA difference) and combines them into a composite signal:

rocNorm = (roc - ta.sma(roc, rocLength)) / ta.stdev(roc, rocLength)

atrNorm = (atr - ta.sma(atr, atrLength)) / ta.stdev(atr, atrLength)

volumeFlowNorm = (volumeFlow - ta.sma(volumeFlow, volumeFlowLength)) / ta.stdev(volumeFlow, volumeFlowLength)

emaDiffNorm = (emaDifference - ta.sma(emaDifference, longEmaLength)) / ta.stdev(emaDifference, longEmaLength)

compositeSignal = (rocNorm + atrNorm + volumeFlowNorm + emaDiffNorm) / 4

### Originality

The originality of the Uptrick indicator lies in its ability to merge diverse market metrics into a unified signal. This multi-faceted approach goes beyond traditional indicators by offering a deeper, more holistic analysis of market conditions, providing traders with insights that are not only based on price movements but also on underlying market dynamics.

### Practical Application

The Uptrick indicator excels in environments where understanding the interplay between volume, momentum, and volatility is crucial. It is especially useful for:

- Day Traders : Can leverage real-time data to make quick decisions based on sudden market changes.

- Swing Traders : Benefit from understanding medium-term trends to optimize entry and exit points.

- Position Traders : Utilize long-term market trend data to align with overall market movements.

### Best Practices

To maximize the effectiveness of the Uptrick indicator, consider the following:

- Combine with Other Indicators : Use alongside other technical tools like RSI or MACD for additional validation.

- Adapt Settings to Market Conditions : Adjust the indicator settings based on the asset and market volatility to improve signal accuracy.

- Risk Management : Implement robust risk management strategies, including setting stop-loss orders based on the volatility measured by the ATR.

### Practical Examples and Demonstrations

- Example for Day Trading : In a volatile market, a trader notices a sharp increase in the momentum score coinciding with a surge in volume but stable volatility, signaling a potential bullish breakout.

- Example for Swing Trading : On a 4-hour chart, the indicator shows a gradual alignment of decreasing volatility and increasing buying volume, suggesting a strengthening upward trend suitable for a long position.

### Alerts and Their Uses

- Alert Configurations : Set alerts for when the composite score crosses predefined thresholds to capture potential buy or sell events.

- Strategic Application : Use alerts to stay informed of significant market moves without the need to continuously monitor the markets, enabling timely and informed trading decisions.

Technical Notes

Efficiency and Compatibility: The indicator is designed for efficiency, running smoothly across different trading platforms including TradingView, and can be easily integrated with existing trading setups. It leverages advanced mathematical models for normalizing and smoothing data, ensuring consistent and reliable signal quality across different market conditions.

Limitations : The effectiveness of the Uptrick indicator can vary significantly across different market conditions and asset classes. It is designed to perform best in liquid markets where data on volume, volatility, and price trends are readily available and reliable. Traders should be aware that in low-liquidity or highly volatile markets, the signals might be less reliable and require additional confirmation.

Usage Recommendations : While the Uptrick indicator is a powerful tool, it is recommended to use it in conjunction with other analysis methods to confirm signals. Traders should also continuously monitor the performance and adjust settings as needed to align with their specific trading strategies and market conditions.

### Conclusion

The "Uptrick: Momentum-Volatility Composite Signal" is a revolutionary tool that offers traders an advanced methodology for analyzing market dynamics. By combining momentum, volatility, volume, and trend detection into a single, cohesive indicator, it provides a powerful, actionable insight into market movements, making it an indispensable tool for traders aiming to optimize their trading strategies.

Sector Rotation Hedging With Volatility Index [TradeDots]The "Sector Rotation Hedging Strategy With Volatility Index" is a comprehensive trading indicator developed to optimally leverage the S&P500 volatility index. It is designed to switch between distinct ETF sectors, strategically hedging to moderate risk exposure during harsh market volatility.

HOW DOES IT WORK

The core of this indicator is grounded on the S&P500 volatility index (VIX) close price and its 60-day moving average. This serves to determine whether the prevailing market volatility is above or below the quarterly average.

In periods of elevated market volatility, risk exposure escalates significantly. Traders retaining stocks in sectors with disproportionately high volatility face increased vulnerability to negative returns. To tackle this, our indicator employs a two-pronged approach utilizing two sequential candlestick close prices to confirm if volatility surpasses the average value.

Upon confirming above-average volatility, a hedging table is deployed to spotlight ETFs with low volatility, such as the Utilities Select Sector SPDR Fund (XLU), to derisk the overall portfolio.

Conversely, in low-volatility conditions, sectors yielding higher returns like the Technology Select Sector SPDR Fund (XLK) are preferred. The hedging table is utilized to earmark high-return sector ETFs.

Thus, during highly volatile market periods, the strategy recommends enhancing portfolio allocation to low-volatility ETFs. During low-volatility windows, the portfolio is calibrated towards high-volatility ETFs for heightened returns.

IMPORTANT CONSIDERATION

In real trading, additional considerations encompassing trading commissions, management fees, and ancillary rotation costs should be factored in. False signals may arise, potentially leading to losses from these fees.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Dynamic Volume-Volatility Adjusted MomentumThis Indicator in a refinement of my earlier script PC*VC Moving average Old with easier to follow color codes, overbought and oversold zones. This script has converted the previous script into a standardized measure by converting it into Z-scores and also incorporated a volatility based dynamic length option. Below is a detailed Explanation.

The "Dynamic Volume-Volatility Adjusted Momentum" or "Nasan Momentum Oscillator" is designed to capture market momentum while accounting for volume and volatility fluctuations. It leverages the Typical Price (TP), calculated as the average of high, low, and close prices, and introduces the Price Coefficient (PC) based on deviations from the simple moving average (SMA) across various time frames. Additionally, the Volume Coefficient (VC) compares current volume to SMA, and calculates Intraday Volatility (IDV) which gauges the daily price range relative to the close. Then intraday volatility ratio is calculated ( IDV Ratio) as the ratio of current Intraday Volatility (IDV) to the average of IDV for three different length periods, which provides a relative measure of current intraday volatility compared to its recent historical average. An inter-day ATR based Relative Volatility (RV) is calculated to adjusts for changing market volatility based on which the dynamic length adjustment adapts the moving average (standard length is 14). The PC *VC/IDV Ratio integrates price, volume, and volatility information which provides a volume and volatility adjusted momentum. This volume and volatility adjusted momentum is converted into a standardized Z-Score. The Z-Score measures deviations from the mean. Color-coded plots visually represent momentum, and thresholds aid in identifying overbought or oversold conditions.

The indicator incorporates a nuanced approach to emphasize the joint impact of price and volume while considering the stabilizing effect of lower intraday volatility. Placing the volume ratio (VC) in the numerator means that higher volume positively contributes to the overall ratio, aligning with the observation that increased volumes often accompany robust price movements. Simultaneously, the decision to include the inverse of intraday volatility (1/IDV) in the denominator acts as a dampener, reducing the impact of extreme intraday volatility on the momentum indicator. This design choice aims to filter out noise, giving more weight to significant price changes supported by substantial trading activity. In essence, the indicator's design seeks to provide a more robust momentum measure that balances the influence of price, volume, and volatility in the analysis of market dynamics.

Change of VolatilityOVERVIEW

The Change of Volatility indicator is a technical indicator that gauges the amount of volatility currently present in the market. The purpose of this indicator is to filter out with-trend signals during ranging/non-trending/consolidating conditions.

CONCEPTS

This indicator assists traders in capitalizing on the assumption that trends are more likely to start during periods of high volatility compared to periods of low volatility . This is because high volatility indicates that there are bigger players currently in the market, which is necessary to begin a sustained trending move.

So, to determine whether the current volatility in the market is low, the indicator will grey out all the areas on the chart whose short term standard deviation of volatility is lower than the long term standard deviation of volatility.

If the short term standard deviation of volatility is above the long term standard deviation of volatility, the current volatility in the market is considered high. This would the ideal time to enter a trending trade due to the assumption that trends are more likely to start during these high-volatility periods.

HOW DO I READ THIS INDICATOR

When the histogram is grey, don't take any trend trades since the current volatility is less than the usual volatility experienced in the market.

When the histogram is green, take all valid with-trend trades since the current volatility is greater than the usual volatility experienced in the market.

Implied Volatility Estimator using Black Scholes [Loxx]Implied Volatility Estimator using Black Scholes derives a estimation of implied volatility using the Black Scholes options pricing model. The Bisection algorithm is used for our purposes here. This includes the ability to adjust for dividends.

Implied Volatility

The implied volatility (IV) of an option contract is that value of the volatility of the underlying instrument which, when input in an option pricing model (such as Black–Scholes), will return a theoretical value equal to the current market price of that option. The VIX , in contrast, is a model-free estimate of Implied Volatility. The latter is viewed as being important because it represents a measure of risk for the underlying asset. Elevated Implied Volatility suggests that risks to underlying are also elevated. Ordinarily, to estimate implied volatility we rely upon Black-Scholes (1973). This implies that we are prepared to accept the assumptions of Black Scholes (1973).

Inputs

Spot price: select from 33 different types of price inputs

Strike Price: the strike price of the option you're wishing to model

Market Price: this is the market price of the option; choose, last, bid, or ask to see different results

Historical Volatility Period: the input period for historical volatility ; historical volatility isn't used in the Bisection algo, this is to serve as a comparison, even though historical volatility is from price movement of the underlying asset where as implied volatility is the volatility of the option

Historical Volatility Type: choose from various types of implied volatility , search my indicators for details on each of these

Option Base Currency: this is to calculate the risk-free rate, this is used if you wish to automatically calculate the risk-free rate instead of using the manual input. this uses the 10 year bold yield of the corresponding country

% Manual Risk-free Rate: here you can manually enter the risk-free rate

Use manual input for Risk-free Rate? : choose manual or automatic for risk-free rate

% Manual Yearly Dividend Yield: here you can manually enter the yearly dividend yield

Adjust for Dividends?: choose if you even want to use use dividends

Automatically Calculate Yearly Dividend Yield? choose if you want to use automatic vs manual dividend yield calculation

Time Now Type: choose how you want to calculate time right now, see the tool tip

Days in Year: choose how many days in the year, 365 for all days, 252 for trading days, etc

Hours Per Day: how many hours per day? 24, 8 working hours, or 6.5 trading hours

Expiry date settings: here you can specify the exact time the option expires

*** the algorithm inputs for low and high aren't to be changed unless you're working through the mathematics of how Bisection works.

Included

Option pricing panel

Loxx's Expanded Source Types

Related Indicators

Cox-Ross-Rubinstein Binomial Tree Options Pricing Model

Volatility Bands Reversal Strategy [Long Only]This strategy based on existng indicator available on TV

If finds the reversals for LONG entries ... I have modified the settings to back test it ...

BUY

====

When the price touches lower band , and tries to close above lower band

some signals are mixed up, you can research and look for a confirmation ...

if the middle band is above EMA50 , you can simply follow the strategy BUY signal

but if the middle band is EMA50 , wait for the price to close above middle band

Sell / Close

==========

wait for the sell signa OR close when price touches the upper band

How do you want to close , you can chose in settings. Chnage these values and see the performance

Please note , sell means just closing the existing LONG position , not short selling

Stop Loss

=========

Stop Loss is defaulted to 6%

This is tested in 1HR, 2HR and 4 HRs chart for SPY and QQQ ETFS ...

for long term investing style , 4 Hrs is the best time frme for this strategy

Warning

========

It is not a financial advise , it is for educational purposes only. Please do your own research before taking any trading decission

Normalized Average True Range (NATR) (Volatility) [cI8DH]As you can see in the chart below, regular ATR is not useful for long term analysis. Normalizing it, fixes the issue. This indicator can be used to measure absolute volatility. It has a built-in stochastic as well for relative volatility. ATR counts high and low in the equation unlike Bolinger Band Width.

Stochastic:

Trend Following Volatility Trail*Script was previously removed by Moderators at 1.8k boosts* - This was out of my control. This script was very popular and seemed to help a lot of traders. I am re uploading to help the community!

Trend Following Volatility Trail

The Trend Following Volatility Trail is a dynamic trend-following tool that adapts its stop, bias, and zones to real-time volatility and trend strength. Instead of using static ATR multiples like a normal Supertrend or Chandelier Stop, it continuously adjusts itself based on how stretched the market is and how persistent the trend has been. This indicator is based on volatility weighted EMAC

This makes the system far more reactive during momentum phases and more conservative during consolidation, helping avoid fake flips and late entries.

How It Works

The indicator builds an adaptive trail around a smoothed price basis:

– It starts with a short EMA as the “core trend line.”

– It measures volatility expansion versus normal volatility.

– It measures trend persistence by reading whether price has been rising or falling consistently.

– These two components combine to adjust the ATR multiplier dynamically.

As volatility expands or the trend becomes more persistent, the bands widen.

When volatility compresses or the trend weakens, the bands tighten.

These adaptive bands form the foundation of the trailing system.

Bull & Bear State Logic

The tool constantly tracks whether price is above or below the adaptive trail:

Price above the upper trail → Bullish regime

Price below the lower trail → Bearish regime

But instead of flipping immediately, it waits for confirmation bars to avoid noise.

This greatly reduces whipsaws and keeps the focus on sustained moves.

Once a new regime is confirmed:

– A coloured cloud appears (bull or bear)

– A label marks the flip point

– Alerts can be triggered automatically

Best Uses

Identifying regime shifts early

Riding sustained trends with confidence

Avoiding choppy markets by requiring confirmation

Using the adaptive cloud as a directional bias layer

Penguin Volatility State StrategyThe Penguin Volatility State Strategy is a comprehensive technical analysis framework designed to identify the underlying "state" or "regime" of the market. Instead of just providing simple buy or sell signals, its primary goal is to classify the market into one of four distinct states by combining trend, momentum, and volatility analysis.

The core idea is to trade only when these three elements align, focusing on periods of volatility expansion (a "squeeze breakout") that occur in the direction of a confirmed trend and are supported by strong momentum.

Key Components

The strategy is built upon two main engines

The Volatility Engine (Bollinger Bands vs. Keltner Channels)

This engine detects periods of rapidly increasing volatility. It measures the percentage difference (diff) between the upper bands of Bollinger Bands (which are based on standard deviation) and Keltner Channels (based on Average True Range). During a volatility "squeeze," both bands are close. When price breaks out, the Bollinger Band expands much faster than the Keltner Channel, causing the diff value to become positive. A positive diff signals a volatility breakout, which is the moment the strategy becomes active.

The Trend & Momentum Engine (Multi-EMA System)

This engine determines the market's direction and strength. It uses:

A Fast EMA (e.g., 12-period) and a Slow EMA (e.g., 26-period): The crossover of these two moving averages defines the primary, underlying trend (similar to a MACD).

An Ultra-Fast EMA (e.g., 2-period of ohlc4): This is used to measure the immediate, short-term momentum of the price.

The Four Market States

By combining the Trend and Momentum engines, the strategy categorizes the market into four visually distinct states, represented by the chart's background color. This is the most crucial aspect of the system.

💚 Green State: Strong Bullish

The primary trend is UP (Fast EMA > Slow EMA) AND the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This represents a healthy, robust uptrend where both the underlying trend and short-term price action are aligned. It is considered the safest condition for taking long positions.

❤️ Red State: Strong Bearish

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) AND the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This represents a strong, confirmed downtrend. It is considered the safest condition for taking short positions.

💛 Yellow State: Weakening Bullish / Pullback

Condition: The primary trend is UP (Fast EMA > Slow EMA) BUT the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This is a critical warning signal for bulls. While the larger trend is still up, the short-term price action is showing weakness. This could be a minor pullback, a period of consolidation, or the very beginning of a trend reversal. Caution is advised.

💙 Blue State: Weakening Bearish / Relief Rally

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) BUT the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This signals that a downtrend is losing steam. It often represents a short-covering rally (a "bear market rally") or the first potential sign of a market bottom. Bears should be cautious and consider taking profits.

How the Strategy Functions

The strategy uses these four states as its foundation for making trading decisions. The entry and exit arrows (Long, Short, Close) are generated based on a set of rules that can be customized by the user. For instance, a trader can configure the strategy to

Only take long trades during the Green State.

Require a confirmed volatility breakout (diff > 0) before entering a trade.

Use the "RSI on Diff" indicator to ensure that the breakout is supported by accelerating momentum.

Summary

In essence, the Penguin Volatility State Strategy provides a powerful "dashboard" for viewing the market. It moves beyond simple indicators to offer a contextual understanding of price action. By waiting for the alignment of Trend (the State), Volatility (the Breakout), and Momentum (the Acceleration), it helps traders to identify higher-probability setups and, just as importantly, to know when it is better to stay out of the market.

License / disclaimer

© waranyu.trkm — MIT License. Educational use only; not financial advice.

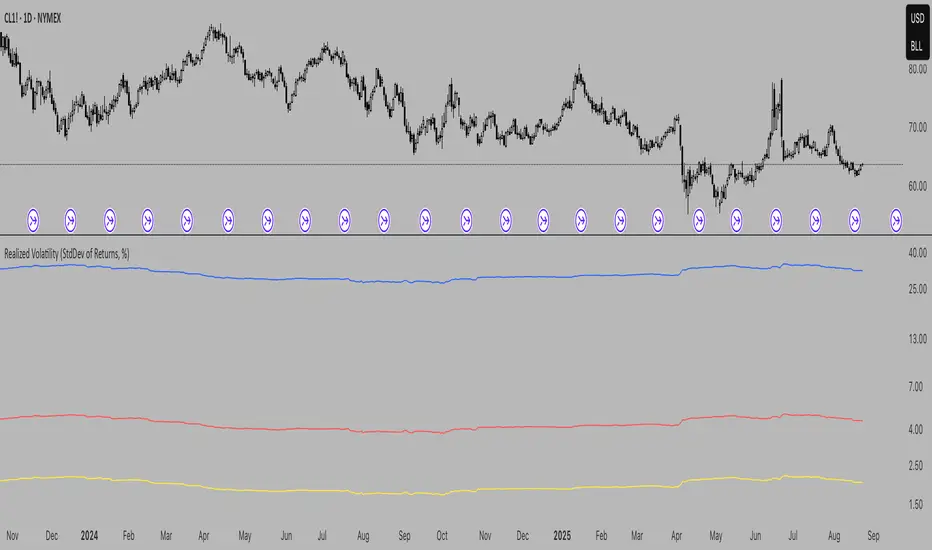

Realized Volatility (StdDev of Returns, %)Realized Volatility (StdDev of Returns, %)

This indicator measures realized (historical) volatility by calculating the standard deviation of log returns over a user-defined lookback period. It helps traders and analysts observe how much the price has varied in the past, expressed as a percentage.

How it works:

Computes close-to-close logarithmic returns.

Calculates the standard deviation of these returns over the selected lookback window.

Provides three volatility measures:

Daily Volatility (%): Standard deviation over the chosen period.

Annualized Volatility (%): Scaled using the square root of the number of trading days per year (default = 250).

Horizon Volatility (%): Scaled to a custom horizon (default = 5 days, useful for short-term views).

Inputs:

Lookback Period: Number of bars used for volatility calculation.

Trading Days per Year: Used for annualizing volatility.

Horizon (days): Adjusts volatility to a shorter or longer time frame.

Notes:

This is a statistical measure of past volatility, not a forecasting tool.

If you change the scale to logarithmic, the indicator readibility improves.

It should be used for analysis in combination with other tools and not as a standalone signal.

Low Volatility Breakout Detector)This indicator is designed to visually identify potential breakouts from consolidation during periods of low volatility. It is based on classic Bollinger Bands and relative volume. Its primary purpose is not to generate buy or sell signals but to assist in spotting moments when the market exits a stagnation phase.

Arrows appear only when the price breaks above the upper or below the lower Bollinger Band, the band width is below a specified threshold (expressed in percentage), and volume is above its moving average multiplied by a chosen multiplier (default is 1). This combination may indicate the start of a new impulse following a period of low activity.

The chart background during low volatility is colored based on volume strength—the lower the volume during stagnation, the less transparent the background. This helps quickly spot unusual market behavior under seemingly calm conditions. The background opacity is dynamically scaled relative to the range of volumes over a selected period, which can be set manually (default is 50 bars).

The indicator works best in classic horizontal consolidations, where price moves within a narrow range and volatility and volume clearly decline. It is not intended to detect breakouts from formations such as triangles or wedges, which may not always exhibit low volatility relative to Bollinger Bands.

Settings allow you to adjust:

Bollinger Band length and multiplier,

Volatility threshold (in %),

Background and arrow colors,

Volume moving average length and multiplier,

Bar range used for background opacity scaling.

Note: For reliable results, it’s advisable to tailor the volatility threshold and volume/background ranges to the specific market and timeframe, as different instruments have distinct dynamics. If you want the background color to closely match the color of breakout arrows, you should set the same volume analysis period as the volume moving average length.

Additional note: To achieve a cleaner chart and focus solely on breakout signals, you can disable the background and Bollinger Bands display in the settings. This will leave only the breakout arrows visible on the chart, providing a clearer and more readable market picture.

Interpolated Median Volatility LSMA | OttoThis indicator combines trend-following and volatility analysis by enhancing traditional LSMA with percentile-based linear interpolation applied to both the Least Squares Moving Average (LSMA) and standard deviation. Rather than relying on raw values, it uses the interpolated median (50th percentile) to smooth out noise while preserving sensitivity to significant price shifts. This approach produces a cleaner trend signal that remains responsive to real market changes, adapts to evolving volatility conditions, and improves the accuracy of breakout detection.

Core Concept

The indicator builds on these core components:

LSMA (Least Squares Moving Average): A linear regression-based moving average that fits line using user selected source over user defined period. It offers a smoother and more reactive trend signal compared to standard moving averages.

Standard Deviation shows how much price varies from the mean. In this indicator, it’s used to measure market volatility.

Volatility Bands: Instead of traditional Bollinger-style bands, this script calculates custom upper and lower bands using percentile-based linear interpolation on both the LSMA and standard deviation. This method produces smoother bands that filter out noise while remaining adaptive to meaningful price movements, making them more aligned with real market behavior and helping reduce false signals.

Percentile interpolation estimates a specific percentile (like the median — the 50th percentile) from a set of values — even when that percentile doesn't fall exactly on one data point. Instead of selecting a single nearest value, it calculates a smoothed value between nearby points. In this script, it’s used to find the median of past LSMA and standard deviation values, reducing the impact of outliers and smoothing the trend and volatility signals for more robust results.

Signal Logic: A long signal is identified when close price goes above the upper band, and a short signal when close price goes below the lower band.

⚙️ Inputs

Source: The price source used in calculations

LSMA Length: Period for calculating LSMA

Standard Deviation Length: Period for calculating volatility

Percentile Length: Period used for interpolating percentile values of LSMA and standard deviation

Multiplier: Controls the width of the bands by scaling the interpolated standard deviation

📈 Visual Output

Colored LSMA Line: Changes color based on signal (green for bullish, purple for bearish)

Upper & Lower Bands: Volatility bands calculated using interpolated values (green for bullish, purple for bearish)

Bar Coloring: Price bars are colored to reflect signal state (green for bullish, purple for bearish)

Optional Candlestick Overlay: Enhances visual context by coloring candles to match the signal state (green for bullish, purple for bearish)

How to Use

Add the indicator to your chart and look for signals when close price goes above or below the bands.

Long Signal: close Price goes above the upper band

Short Signal: close Price goes below the lower band

🔔 Alerts:

This script supports alert conditions for long and short signals. You can set alerts based on band crossovers to be notified of potential entries/exits.

⚠️ Disclaimer:

This indicator is intended for educational and informational purposes only. Trading/investing involves risk, and past performance does not guarantee future results. Always test and evaluate strategies before applying them in live markets. Use at your own risk.

Trend Volatility Index (TVI)Trend Volatility Index (TVI)

A robust nonparametric oscillator for structural trend volatility detection

⸻

What is this?

TVI is a volatility oscillator designed to measure the strength and emergence of price trends using nonparametric statistics.

It calculates a U-statistic based on the Gini mean difference across multiple simple moving averages.

This allows for objective, robust, and unbiased quantification of trend volatility in tick-scale values.

⸻

What can it do?

• Quantify trend strength as a continuous value aligned with tick price scale

• Detect trend breakouts and volatility expansions

• Identify range-bound market states

• Detect early signs of new trends with minimal lag

⸻

What can’t it do?

• Predict future price levels

• Predict trend direction before confirmation

⸻

How it works

TVI computes a nonparametric dispersion metric (Gini mean difference) from multiple SMAs of different lengths.

As this metric shares the same dimension as price ticks, it can be directly interpreted on the chart as a volatility gauge.

The output is plotted using candlestick-style charts to enhance visibility of change rate and trend behavior.

⸻

Disclaimer

TVI does not predict price. It is a structural indicator designed to support discretionary judgment.

Trading carries inherent risk, and this tool does not guarantee profitability. Use at your own discretion.

⸻

Innovation

This indicator introduces a novel approach to trend volatility by applying U-statistics over time series

to produce a nonparametric, unbiased, and robust estimate of structural volatility.

日本語要約

Trend Volatility Index (TVI) は、ノンパラメトリックなU統計量(Gini平均差)を使ってトレンドの強度を客観的に測定することを目的に開発されたボラティリティ・オシレーターです。

ティック単位で連続的に変化し、トレンドのブレイク・レンジ・初動の予兆を定量的に検出します。

未来の価格や方向は予測せず、現在の構造的ばらつきだけをロバストに評価します。

Volume and Volatility Ratio Indicator-WODI该指标名为“交易量与波动率比例指标-WODI”,主要基于交易量和价格波动率构造一个复合指数,帮助识别市场内可能存在的异常或转折信号。具体实现如下:

用户自定义参数

用户可以设置交易量均线长度(vol_length)、指数的短期与长期均线长度(index_short_length、index_long_length)、均线敏感度(index_magnification)、阈值放大因子(index_threshold_magnification)以及检测K线形态的区间(lookback_bars)。这些参数为后续计算提供了灵活性,允许用户根据不同市场环境自定义指标的敏感度和响应速度。

交易量均线与百分比计算

首先通过 ta.sma 计算指定长度的交易量简单均线(vol_ma)。

接下来,将当前交易量与均线进行比较,计算出当前交易量占均线的百分比(vol_percent),这反映了短期内交易量的相对活跃程度。

波动率的衡量

使用当前K线的最高价和最低价计算振幅,再除以收盘价乘以100得到波动率(volatility),从而反映市场价格波动的幅度。

构建交易量/波动率指数

将交易量百分比与波动率相乘,形成了“交易量/波动率指数”(volatility_index)。该指数能够同时反映市场的交易活跃度和价格波动性,两者的联合作用帮助捕捉市场的“热度”。

计算指标均线与阈值

对交易量/波动率指数分别计算短期均线(index_short_ma)和长期均线(index_long_ma),并通过乘以一个敏感度参数(index_magnification)进行调整。

同时,依据长期均线计算一个阈值(index_threshold),起到过滤噪音的作用。当指数突破该阈值时,可能预示着市场的重要变化。

K线形态与反转模式检测

通过遍历最近几根K线(由lookback_bars控制),指标会检测是否符合一系列预定条件(涉及交易量、价格振幅、K线形态等),以判断是否存在反转模式。若符合条件,则标记为反转模式,从而为潜在的转折点提供提示。

图表展示

最终在独立窗口中绘制多个元素:

指数短均线与长均线:经过敏感度调整后显示,用于分析指数趋势。

交易量/波动率指数:采用阶梯线风格绘制,直观展示指数变化。

阈值线:作为参考水平,便于判断指数是否突破常规范围。

交易量柱状图:当当前交易量高于均线时,通过不同颜色显示;当检测到反转模式时,颜色会进一步强化,帮助用户迅速识别潜在信号。

English Description

This indicator, titled “Volume and Volatility Ratio Indicator - WODI”, is designed to construct a composite index based on trading volume and price volatility, aiding in the identification of abnormal market conditions or potential reversal signals. Its functionality is broken down as follows:

User-Defined Parameters

The indicator allows users to set parameters such as the moving average length for volume (vol_length), the short and long moving average lengths for the index (index_short_length and index_long_length), a sensitivity multiplier (index_magnification), a threshold magnification factor (index_threshold_magnification), and the number of bars for pattern detection (lookback_bars). These parameters provide flexibility to adjust the sensitivity and responsiveness of the indicator based on different market conditions.

Volume Moving Average and Percentage Calculation

A simple moving average (SMA) of volume is computed over the specified length (vol_ma) using the ta.sma function.

The current volume is then compared to its moving average to calculate the volume percentage (vol_percent), reflecting the relative trading intensity in the short term.

Measuring Volatility

Volatility is calculated based on the current bar’s high and low prices, normalized by the closing price and multiplied by 100, which provides a measure of the market’s price fluctuation magnitude.

Constructing the Volume/Volatility Index

The index (volatility_index) is derived by multiplying the volume percentage by the calculated volatility. This composite metric reflects both market activity and price movement, effectively capturing the overall “heat” of the market.

Calculating the Index Moving Averages and Threshold

Two moving averages for the volatility_index are computed: one short-term (index_short_ma) and one long-term (index_long_ma). These are then adjusted by the sensitivity multiplier (index_magnification).

A threshold level (index_threshold) is calculated based on the long-term moving average multiplied by the threshold magnification factor, serving to filter out market noise. When the index exceeds this threshold, it may signal significant market shifts.

Detection of Reversal Patterns

The indicator iterates through the recent bars (as determined by lookback_bars) to check whether a set of predetermined conditions (involving trends in the volatility_index, volume comparisons, price closes, and K-line patterns) are met. If these conditions are satisfied, it flags a reversal pattern, which may serve as a warning for a potential market turnaround.

Visualization on the Chart

The final display includes several elements plotted in a separate indicator window:

The short-term and long-term moving averages of the index (after sensitivity adjustment) which help visualize the trend of the composite index.

The volatility index itself is drawn using a step-line style for clarity.

A threshold line is plotted to provide a reference level against which index movements can be compared.

A volume histogram is also displayed, where bars are colored differently when the current volume exceeds the moving average; the color is further enhanced if a reversal pattern is detected, making it easy for users to quickly spot potential signals.

Adaptive Fibonacci Volatility Bands (AFVB)

**Adaptive Fibonacci Volatility Bands (AFVB)**

### **Overview**

The **Adaptive Fibonacci Volatility Bands (AFVB)** indicator enhances standard **Fibonacci retracement levels** by dynamically adjusting them based on market **volatility**. By incorporating **ATR (Average True Range) adjustments**, this indicator refines key **support and resistance zones**, helping traders identify **more reliable entry and exit points**.

**Key Features:**

- **ATR-based adaptive Fibonacci levels** that adjust to changing market volatility.

- **Buy and Sell signals** based on price interactions with dynamic support/resistance.

- **Toggleable confirmation filter** for refining trade signals.

- **Customizable color schemes** and alerts.

---

## **How This Indicator Works**

The **AFVB** operates in three main steps:

### **1️⃣ Detecting Key Fibonacci Levels**

The script calculates **swing highs and swing lows** using a user-defined lookback period. From this, it derives **Fibonacci retracement levels**:

- **0% (High)**

- **23.6%**

- **38.2%**

- **50% (Mid-Level)**

- **61.8%**

- **78.6%**

- **100% (Low)**

### **2️⃣ Adjusting for Market Volatility**

Instead of using **fixed retracement levels**, this indicator incorporates an **ATR-based adjustment**:

- **Resistance levels** shift **upward** based on ATR.

- **Support levels** shift **downward** based on ATR.

- This makes levels more **responsive** to price action.

### **3️⃣ Generating Buy & Sell Signals**

AFVB provides **two types of signals** based on price interactions with key levels:

✔ **Buy Signal**:

Occurs when price **dips below** a support level (78.6% or 100%) and **then closes back above it**.

- **Optionally**, a confirmation buffer can be enabled to require price to close **above an additional threshold** (based on ATR).

✔ **Sell Signal**:

Triggered when price **breaks above a resistance level** (0% or 23.6%) and **then closes below it**.

📌 **Important:**

- The **buy threshold setting** allows traders to **fine-tune** entry conditions.

- Turning this setting **off** generates **more frequent** buy signals.

- Keeping it **on** reduces false signals but may result in **fewer trade opportunities**.

---

## **How to Use This Indicator in Trading**

### 🔹 **Entry Strategy (Buying)**

1️⃣ Look for **buy signals** at the **78.6% or 100% Fibonacci levels**.

2️⃣ Ensure price **closes above** the support level before entering a long trade.

3️⃣ **Enable or disable** the buy threshold filter depending on desired trade strictness.

### 🔹 **Exit Strategy (Selling)**

1️⃣ Watch for **sell signals** at the **0% or 23.6% Fibonacci levels**.

2️⃣ If price **breaks above resistance and then closes below**, consider exiting long positions.

3️⃣ Can be used **alone** or **combined with trend confirmation tools** (e.g., moving averages, RSI).

### 🔹 **Using the Toggleable Buy Threshold**

- **ON**: Buy signal requires **extra confirmation** (reduces false signals but fewer trades).

- **OFF**: Buy triggers as soon as price **closes back above support** (more signals, but may include weaker setups).

---

## **User Inputs**

### **🔧 Customization Options**

- **ATR Length**: Defines the period for **ATR calculation**.

- **Swing Lookback**: Determines how far back to find **swing highs and lows**.

- **ATR Multiplier**: Adjusts the size of **volatility-based modifications**.

- **Buy/Sell Threshold Factor**: Fine-tunes the **entry signal strictness**.

- **Show Level Labels**: Enables/disables **Fibonacci level annotations**.

- **Color Settings**: Customize **support/resistance colors**.

### **📢 Alerts**

AFVB includes built-in **alert conditions** for:

- **Buy Signals** ("AFVB BUY SIGNAL - Possible reversal at support")

- **Sell Signals** ("AFVB SELL SIGNAL - Possible reversal at resistance")

- **Any Signal Triggered** (Useful for automated alerts)

---

## **Who Is This Indicator For?**

✅ **Scalpers & Day Traders** – Helps identify **short-term reversals**.

✅ **Swing Traders** – Useful for **buying dips** and **selling rallies**.

✅ **Trend Traders** – Can be combined with **momentum indicators** for confirmation.

**Best Timeframes:**

⏳ **15-minute, 1-hour, 4-hour, Daily charts** (works across multiple assets).

---

## **Limitations & Considerations**

🚨 **Important Notes**:

- **No indicator guarantees profits**. Always **combine** it with **risk management strategies**.

- Works best **in trending & mean-reverting markets**—may generate false signals in **choppy conditions**.

- Performance may vary across **different assets & timeframes**.

📢 **Backtesting is recommended** before using it for live trading.

Hyperbolic Tangent Volatility Stop [InvestorUnknown]The Hyperbolic Tangent Volatility Stop (HTVS) is an advanced technical analysis tool that combines the smoothing capabilities of the Hyperbolic Tangent Moving Average (HTMA) with a volatility-based stop mechanism. This indicator is designed to identify trends and reversals while accounting for market volatility.

Hyperbolic Tangent Moving Average (HTMA):

The HTMA is at the heart of the HTVS. This custom moving average uses a hyperbolic tangent transformation to smooth out price fluctuations, focusing on significant trends while ignoring minor noise. The transformation reduces the sensitivity to sharp price movements, providing a clearer view of the underlying market direction.

The hyperbolic tangent function (tanh) is commonly used in mathematical fields like calculus, machine learning and signal processing due to its properties of “squashing” inputs into a range between -1 and 1. The function provides a non-linear transformation that can reduce the impact of extreme values while retaining a certain level of smoothness.

tanh(x) =>

e_x = math.exp(x)

e_neg_x = math.exp(-x)

(e_x - e_neg_x) / (e_x + e_neg_x)

The HTMA is calculated by applying a non-linear transformation to the difference between the source price and its simple moving average, then adjusting it using the standard deviation of the price data. The result is a moving average that better tracks the real market direction.

htma(src, len, mul) =>

tanh_src = tanh((src - ta.sma(src, len)) * mul) * ta.stdev(src, len) + ta.sma(src, len)

htma = ta.sma(tanh_src, len)

Important Note: The Hyperbolic Tangent function becomes less accurate with very high prices. For assets priced above 100,000, the results may deteriorate, and for prices exceeding 1 million, the function may stop functioning properly. Therefore, this indicator is better suited for assets with lower prices or lower price ratios.

Volatility Stop (VolStop):

HTVS employs a Volatility Stop mechanism based on the Average True Range (ATR). This stop dynamically adjusts based on market volatility, ensuring that the indicator adapts to changing conditions and avoids false signals in choppy markets.

The VolStop follows the price, with a higher ATR pushing the stop farther away to avoid premature exits during volatile periods. Conversely, when volatility is low, the stop tightens to lock in profits as the trend progresses.

The ATR Length and ATR Multiplier are customizable, allowing traders to control how tightly or loosely the stop follows the price.

pine_volStop(src, atrlen, atrfactor) =>

if not na(src)

var max = src

var min = src

var uptrend = true

var float stop = na

atrM = nz(ta.atr(atrlen) * atrfactor, ta.tr)

max := math.max(max, src)

min := math.min(min, src)

stop := nz(uptrend ? math.max(stop, max - atrM) : math.min(stop, min + atrM), src)

uptrend := src - stop >= 0.0

if uptrend != nz(uptrend , true)

max := src

min := src

stop := uptrend ? max - atrM : min + atrM

Backtest Mode:

HTVS includes a built-in backtest mode, allowing traders to evaluate the indicator's performance on historical data. In backtest mode, it calculates the cumulative equity curve and compares it to a simple buy and hold strategy.

Backtesting features can be adjusted to focus on specific signal types, such as Long Only, Short Only, or Long & Short.

An optional Buy and Hold Equity plot provides insight into how the indicator performs relative to simply holding the asset over time.

The indicator includes a Hints Table, which provides useful recommendations on how to best display the indicator for different use cases. For example, when using the overlay mode, it suggests displaying the indicator in the same pane as price action, while backtest mode is recommended to be used in a separate pane for better clarity.

The Hyperbolic Tangent Volatility Stop offers traders a balanced approach to trend-following, using the robustness of the HTMA for smoothing and the adaptability of the Volatility Stop to avoid whipsaw trades during volatile periods. With its backtesting features and alert system, this indicator provides a comprehensive toolkit for active traders.