OHLC-TablesENGLISH VERSION

The command shows the opening-high-low-closing-change values of that day based on the previous value in each period.

You can set the clock in any time zone you want.

You can use the indicator by adapting it wherever you want on your screen. You can adjust its position. Top-Left-Middle Left- Bottom Left/ Top Right-Middle Right- Bottom Right.

Although it is not a command with a Buy-Sell indicator, its user-friendliness and convenience were taken into account while developing it.

The purpose of the indicator is to allow you to consider the values while focusing not only on the chart you are watching.

Pesquisar nos scripts por "OHLC"

OHLC - Hourly, Daily,Weekly,Monthly with LabelsOpen, High, Low , close with Labels -- These are professional levels to watch out for active trading

dOP - Day open price

yCL - Yesterday's close Price

yHI - Yesterday's High Price

yLO -- Yesterday's Low Price

OHLC/GAP/EMA/VWAP all in oneThis script will plot the current open and previous high low and close. The overnight gap between the current open and the previous close is highlighted. Also included is the 10 EMA, 20 EMA and the VWAP. This is good for people who are limited on the amount of indicators they can use.

MA CandlesOHLC calculated with a moving average.

You can replace sma with anything. EMA, Hull, sma(sma(sma(sma(close, etc.

You could also make it look clean like Heikin Ashi candlesticks if you include min/max for low/high wicks on candles.

OHLC Volatility Estimators by @Xel_arjonaDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is by Creative-Commons as TradingView's regulations. Any use, copy or re-use of this code should mention it's origin as it's authorship.

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS DEBUGING CODE The models included in the function have been taken from openly sources on the web so they could have some errors as in the calculation scheme and/or in it's programatic scheme. Debugging are welcome.

WHAT'S THIS?

Here's a full collection of candle based (compressed tick) Volatility Estimators given as a function, openly available for free, it can print IMPLIED VOLATILITY by an external symbol ticker like INDEX:VIX.

Models included in the volatility calculation function:

CLOSE TO CLOSE: This is the classic estimator by rule, sometimes referred as HISTORICAL VOLATILITY and is the must common, accepted and widely used out there. Is based on traditional Standard Deviation method derived from the logarithm return of current close from yesterday's.

ELASTIC WEIGHTED MOVING AVERAGE: This estimator has been used by RiskMetriks®. It's calculation is based on an ElasticWeightedMovingAverage Standard Deviation method derived from the logarithm return of current close from yesterday's. It can be viewed or named as an EXPONENTIAL HISTORICAL VOLATILITY model.

PARKINSON'S: The Parkinson number, or High Low Range Volatility, developed by the physicist, Michael Parkinson, in 1980 aims to estimate the Volatility of returns for a random walk using the high and low in any particular period. IVolatility.com calculates daily Parkinson values. Prices are observed on a fixed time interval. n=10, 20, 30, 60, 90, 120, 150, 180 days.

ROGERS-SATCHELL: The Rogers-Satchell function is a volatility estimator that outperforms other estimators when the underlying follows a Geometric Brownian Motion (GBM) with a drift (historical data mean returns different from zero). As a result, it provides a better volatility estimation when the underlying is trending. However, this Rogers-Satchell estimator does not account for jumps in price (Gaps). It assumes no opening jump. The function uses the open, close, high, and low price series in its calculation and it has only one parameter, which is the period to use to estimate the volatility.

YANG-ZHANG: Yang and Zhang were the first to derive an historical volatility estimator that has a minimum estimation error, is independent of the drift, and independent of opening gaps. This estimator is maximally 14 times more efficient than the close-to-close estimator.

LOGARITHMIC GARMAN-KLASS: The former is a pinescript transcript of the model defined as in iVolatility . The metric used is a combination of the overnight, high/low and open/close range. Such a volatility metric is a more efficient measure of the degree of volatility during a given day. This metric is always positive.

Moving Average - TREND POWER v1.1- (AS)0)NOTE:

This is first version of this indicator. It's way more complicated than it should be. Check out Moving Average-TREND POWER v2.1-(AS), its waaaaay less complicated and might be better.Enjoy...

1)INTRODUCTION/MAIN IDEA:

In simpliest form this script is a trend indicator that rises if Moving average if below price or falling if above and going back to zero if there is a crossover with a price. To use this indicator you will have to adjust settings of MAs and choose conditions for calculation.

While using the indicator we might have to define CROSS types or which MAs to use. List of what cross types are defined in the script and Conditiones to choose from.The list will be below.

2) COMPOSITION:

-MA1 can be defined by user in settings, possible types: SMA, EMA, RMA, HMA, TEMA, DEMA, LSMA, WMA.

-MA2 is always ALMA

3) OVERLAY:

Default is false but if you want to see MA1/2 on chart you can change code to true and then turn on overlay in settings. Most plot settings are avalible only in OV=false.

if OV=true possible plots ->MA1/2, plotshape when choosen cross type

if OV=false -> main indicator,TSHs,Cross counter

4)PRESETS :

Indicator has three modes that can be selected in settings. First two are presets and do not require selecting conditions as they set be default.

-SIMPLE - most basic

-ABSOLUTE - shows only positive values when market is trending or zero when in range

-CUSTOM - main and the most advanced form that will require setting conditions to use in calculating trend

4.1)SIMPLE – this is the most basic form of conditions that uses only First MA. If MA1 is below selected source (High/Low(High for Uptrend and Low for DNtrend or OHLC4) on every bar value rises by 0.02. if it above Low or OHLC4 it falls by 0.02 with every bar. If there is a cross of MA with price value is zero. This preset uses CROSS_1_ULT(list of all cross types below)

4.2) ABSOLUTE – does not show direction of the trend unlike others and uses both MA1 and MA2. Uses CROSS type 123_ULT

4.3) CUSTOM – here we define conditions manually. This mode is defined in parts (5-8 of description)

5)SETTINGS:

SOURCE/OVERLAY(line1) – select source of calculation form MA1/MA2, select for overlay true (look point 3)

TRESHOLDS(line2). – set upper and lower THS, turn TSHs on/off

MA1(line3) – Length/type of MA/Offset(only if MA type is LSM)

MA2(line4) – length/offset/sigma -(remember to set ma in the way that in Uptrend MA2MA1 in DNtrend)

Use faster MA types for short term trends and slower types / bigger periods for longer term trends, defval MA1/2 settings

are pretty much random so using them is not recomended.

CROSSshape(line5) – choose which cross type you want to plot on chart(only in OV=true) or what type you want to use in counting via for loops,

CROSScount(line6) – set lookback for type of cross choosen above

BOOLs in lines 5 and 6 - plotshape if OV=true/plot CROSScount histogram (if OV=false)

Lines 7 and 8 – PRESET we want to use /SRC for calculation of indicator/are conditions described below/which MAs to use/Condition for

reducing value t 0 - (if PRESET is ABSOLUTE or SIMPLE only SRC should be set(Line 8 does not matter if not CUSTOM))

5)SOURCE for CONDS:

Here you can choose between H/L and OHLC. If H/L value grow when MAlow. If OHLC MAOHLC. H/L is set by default and recommended. This can be selected for all presets not only CUSTOM

6)CROSS types LIST:

“1 means MA1, 2 is MA2 and 3 I cross of MA1/MA2. L stands for low and H for high so for example 2H means cross of MA2 and high”

NAME -DEFINITION Number of possible crosses

1L - cross of MA1 and low 1

1H - cross of MA1 and high 1

1HL - cross of MA1 and low or MA1 and high 2 -1L/1H

2L - cross of MA2 and low 1

2H - cross of MA2 and high 1

2HL - cross of MA2 and low or MA1 and high 2 -2L/2H

12L - cross of MA1 and low or MA2 and low 2 -1L/2L

12H - cross of MA1 and high or MA2 and high 2 -1H/2H

12HL - MA1/2 and high/low 4 -1H/1L/2H/2L

3 -cross of MA1 and MA2 1

123HL -crosses from 12HL or 3 5 -12HL/3

1_ULT - cross of MA1 with any of price sources(close,low,high,ohlc4 etc…)

2_ULT - cross of MA2 with any of price sources(close,low,high,ohlc4 etc…)

123_ULT – all crosses possible of MA1/2 (all of the above so a lot)

7)CRS CONDS:

“conditions to reduce value back to zero”

>/< - 0 if indicator shows Uptrend and there’s a cross with high of selected MA or 0 if in DNtrend and cross with low. Better for UP/DN trend detection

ALL – 0 if cross of MA with high or low no matter the trend, better for detecting consolidation

ULT – if any cross of selected MA, most crosses so goes to 0 most often

8)MA selection and CONDS:

-MA1: only MA1 is used,if MA1 below price value grows and the other way around

MA1price =-0.02

-MA2 – only MA2 is used, same conditions as MA1 but using MA2

MA2price =-0.02

-BOTH – MA1 and MA2 used, grows when MA1 if below, grows faster if MA1 and MA2 are below and fastest when MA1 and MA2 are below and MA2price=-0.02

-MA1 and MA2 >price=-0.03

-MA1 and MA2 ?price and MA2>MA1=-0.04

9)CONDITIONS SELECTION SUMMARRY:

So when CUSTOM we choose :

1)SOURCE – H/L or OHLC

2)MAs – MA1/MA2/BOTH

3)CRS CONDS (>/<,ALL,ULT)

So for example...

if we take MA1 and ALL value will go to zero if 1HL

if MA1 and >/< - 0 if 1L or 1H (depending if value is positive or negative).(1L or 1H)

If ALL and BOTH zero when 12HL

If BOTH and ULT value goes back to zero if Theres any cross of MA1/MA2 with price or cross of MA1 and MA2.(123_ULT)

If >/< and BOTH – 0 if 12L in DNtrend or 12H if UPtrend

10) OTHERS

-script was created on EURUSD 5M and wasn't tested on different markets

-default values of MA1/MA2 aren't optimalized so do not

-There might be a logical error in the script so let me know if you find it (most probably in 'BOTH')

-thanks to @AlifeToMake for help

-if you have any ideas to improve let me know

-there are also tooltips to help

Volume Sampled Supertrend [BackQuant]Volume Sampled Supertrend

A Supertrend that runs on a volume sampled price series instead of fixed time. New synthetic bars are only created after sufficient traded activity, which filters out low participation noise and makes the trend much easier to read and model.

Original Script Link

This indicator is built on top of my volume sampling engine. See the base implementation here:

Why Volume Sampling

Traditional charts print a bar every N minutes regardless of how active the tape is. During quiet periods you accumulate many small, low information bars that add noise and whipsaws to downstream signals.

Volume sampling replaces the clock with participation. A new synthetic bar is created only when a pre-set amount of volume accumulates (or, in Dollar Bars mode, when pricevolume reaches a dollar threshold). The result is a non-uniform time series that stretches in busy regimes and compresses in quiet regimes. This naturally:

filters dead time by skipping low volume chop;

standardizes the information content per bar, improving comparability across regimes;

stabilizes volatility estimates used inside banded indicators;

gives trend and breakout logic cleaner state transitions with fewer micro flips.

What this tool does

It builds a synthetic OHLCV stream from volume based buckets and then applies a Supertrend to that synthetic price. You are effectively running Supertrend on a participation clock rather than a wall clock.

Core Features

Sampling Engine - Choose Volume buckets or Dollar Bars . Thresholds can be dynamic from a rolling mean or median, or fixed by the user.

Synthetic Candles - Plots the volume sampled OHLC candles so you can visually compare against regular time candles.

Supertrend on Synthetic Price - ATR bands and direction are computed on the sampled series, not on time bars.

Adaptive Coloring - Candle colors can reflect side, intensity by volume, or a neutral scheme.

Research Panels - Table shows total samples, current bucket fill, threshold, bars-per-sample, and synthetic return stats.

Alerts - Long and Short triggers on Supertrend direction flips for the synthetic series.

How it works

Sampling

Pick Sampling Method = Volume or Dollar Bars.

Set the dynamic threshold via Rolling Lookback and Filter (Mean or Median), or enable Use Fixed and type a constant.

The script accumulates volume (or pricevolume) each time bar. When the bucket reaches the threshold, it finalizes one or more synthetic candles and resets accumulation.

Each synthetic candle stores its own OHLCV and is appended to the synthetic series used for all downstream logic.

Supertrend on the sampled stream

Choose Supertrend Source (Open, High, Low, Close, HLC3, HL2, OHLC4, HLCC4) derived from the synthetic candle.

Compute ATR over the synthetic series with ATR Period , then form upperBand = src + factorATR and lowerBand = src - factorATR .

Apply classic trailing band and direction rules to produce Supertrend and trend state.

Because bars only come when there is sufficient participation, band touches and flips tend to align with meaningful pushes, not idle prints.

Reading the display

Synthetic Volume Bars - The non-uniform candles that represent equal information buckets. Expect more candles during active sessions and fewer during lulls.

Volume Sampled Supertrend - The main line. Green when Trend is 1, red when Trend is -1.

Markers - Small dots appear when a new synthetic sample is created, useful for aligning activity cycles.

Time Bars Overlay (optional) - Plot regular time candles to compare how the synthetic stream compresses quiet chop.

Settings you will use most

Data Settings

Sampling Method - Volume or Dollar Bars.

Rolling Lookback and Filter - Controls the dynamic threshold. Median is robust to outliers, Mean is smoother.

Use Fixed and Fixed Threshold - Force a constant bucket size for consistent sampling across regimes.

Max Stored Samples - Ring buffer limit for performance.

Indicator Settings

SMA over last N samples - A moving average computed on the synthetic close series. Can be hidden for a cleaner layout.

Supertrend Source - Price field from the synthetic candle.

ATR Period and Factor - Standard Supertrend controls applied on the synthetic series.

Visuals and UI

Show Synthetic Bars - Turn synthetic candles on or off.

Candle Color Mode - Green/Red, Volume Intensity, Neutral, or Adaptive.

Mark new samples - Puts a dot when a bucket closes.

Show Time Bars - Overlay regular candles for comparison.

Paint candles according to Trend - Colors chart candles using current synthetic Supertrend direction.

Line Width , Colors , and Stats Table toggles.

Some workflow notes:

Trend Following

Set Sampling Method = Volume, Filter = Median, and a reasonable Rolling Lookback so busy regimes produce more samples.

Trade in the direction of the Volume Sampled Supertrend. Because flips require real participation, you tend to avoid micro whipsaws seen on time bars.

Use the synthetic SMA as a bias rail and trailing reference for partials or re-entries.

Breakout and Continuation

Watch for rapid clustering of new sample markers and a clean flip of the synthetic Supertrend.

The compression of quiet time and expansion in busy bursts often makes breakouts more legible than on uniform time charts.

Mean Reversion

In instruments that oscillate, faded moves against the synthetic Supertrend are easier to time when the bucket cadence slows and Supertrend flattens.

Combine with the synthetic SMA and return statistics in the table for sizing and expectation setting.

Stats table (top right)

Method and Total Samples - Sampling regime and current synthetic history length.

Current Vol or Dollar and Threshold - Live bucket fill versus the trigger.

Bars in Bucket and Avg Bars per Sample - How much time data each synthetic bar tends to compress.

Avg Return and Return StdDev - Simple research metrics over synthetic close-to-close changes.

Why this reduces noise

Time based bars treat a 5 minute print with 1 percent of average participation the same as one with 300 percent. Volume sampling equalizes bar information content. By advancing the bar only when sufficient activity occurs, you skip low quality intervals that add variance but little signal. For banded systems like Supertrend, this often means fewer false flips and cleaner runs.

Notes and tips

Use Dollar Bars on assets where nominal price varies widely over time or across symbols.

Median filter can resist single burst outliers when setting dynamic thresholds.

If you need a stable research baseline, set Use Fixed and keep the threshold constant across tests.

Enable Show Time Bars occasionally to sanity check what the synthetic stream is compressing or stretching.

Link again for reference

Original Volume Based Sampling engine:

Bottom line

When you let participation set the clock, your Supertrend reacts to meaningful flow instead of idle prints. The result is a cleaner state machine, fewer micro whipsaws, and a trend read that respects when the market is actually trading.

basechartpatternsLibrary "basechartpatterns"

Library having complete chart pattern implementation

getPatternNameById(id)

Returns pattern name by id

Parameters:

id (int) : pattern id

Returns: Pattern name

method find(points, properties, dProperties, ohlcArray)

Find patterns based on array of points

Namespace types: chart.point

Parameters:

points (chart.point ) : array of chart.point objects

properties (ScanProperties type from Trendoscope/abstractchartpatterns/1) : ScanProperties object

dProperties (DrawingProperties type from Trendoscope/abstractchartpatterns/1) : DrawingProperties object

ohlcArray (OHLC type from Trendoscope/ohlc/1)

Returns: Flag indicating if the pattern is valid, Current Pattern object

method find(this, properties, dProperties, patterns, ohlcArray)

Find patterns based on the currect zigzag object but will not store them in the pattern array.

Namespace types: zg.Zigzag

Parameters:

this (Zigzag type from Trendoscope/ZigzagLite/2) : Zigzag object containing pivots

properties (ScanProperties type from Trendoscope/abstractchartpatterns/1) : ScanProperties object

dProperties (DrawingProperties type from Trendoscope/abstractchartpatterns/1) : DrawingProperties object

patterns (Pattern type from Trendoscope/abstractchartpatterns/1) : Array of Pattern objects

ohlcArray (OHLC type from Trendoscope/ohlc/1)

Returns: Flag indicating if the pattern is valid, Current Pattern object

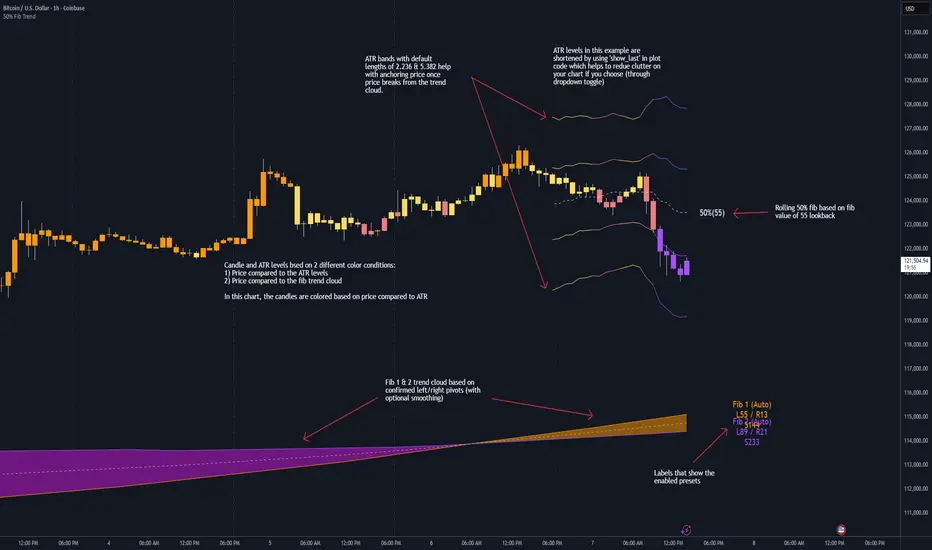

50% Fib Trend Cloud + ATR BandsThis indicator plots two structural 50% fibonacci midpoints from recent confirmed 'left/right' swings that form a *cloud* of equilibrium, then adds a rolling 50% fibonacci range midpoint based on a lookback window that's wrapped in ATR bands. Importantly, it solves a specific trading problem:

Structural midpoints (macro context) are powerful but can lag when price escapes prior ranges. Enter rolling 50% fib + ATR ➡️ which restores real-time balance & tolerance (micro context). Together they show where price is balanced structurally, where it’s balanced right now, and how much volatility to tolerate before acting.

➖➖➖

🔑 Why this is different

Most tools either draw a single midpoint (ex., daily 50%) or ATR bands around a moving average. This script fuses dual swing-based 50% midpoints (structure) + a rolling 50% with ATR (flow), so you don’t lose context when price escapes prior ranges. The cloud tells you who’s in control (fast vs. slow structure). The rolling 50% + ATR tells you how far is “too far” now.

➖➖➖

🧠 What it does (at a glance)

🔸Structural Equilibrium × 2 (Fib1/Fib2)

Two independent 50% midpoints formed from swing pivots (configurable Left/Right bars + optional smoothing). Their gap is the Midpoint Cloud = structural “fair value” zone.

🔸Rolling 50% + ATR Bands

A rolling highest/lowest window computes an always-current 50% rolling midpoint plot; ±ATR × length envelopes define a soft value area and over-stretch boundaries.

🔸Actionable Visuals

Optional fill between Fib1/Fib2, labels, and candle-overlay modes to instantly read regime (above both / below both / between).

🔸Smart Defaults

Timeframe-aware presets for L/R pivots & smoothing; full manual overrides available.

➖➖➖

⚙️ Calculations (plain-English)

🔸Pivot midpoints (Fib1 & Fib2):

1) Detect a swing using `Left/Right` bars

2) Take the swing’s high/low → compute 50%

3) (Optional) Smooth the line (SMA) to stabilize on noisy TFs

4) Repeat with a different sensitivity to get two distinct midpoints

🔸Rolling midpoint:

Highest High / Lowest Low over the last *N* bars → (HH + LL) / 2

🔸ATR levels:

`Upper = Rolling50 + ATR × Mult`, `Lower = Rolling50 − ATR × Mult`

(Typical: ATR length 14–21; Multipliers 2.236 for L1, 5.382 for L2)

➖➖➖

🤖 Auto-Configured Presets (with Manual Override)

💡Goal: make the midpoints “just work” on common timeframes while still letting you dial them in.

💡How Auto Presets work

When Auto Presets = ON, the script picks sensible L/R/S (Left bars / Right bars / Smoothing) for Fib Trend 1 and Fib Trend 2 based on chart timeframe.

🔸Fib 1 (fast) emphasizes *micro-structure* for quicker bias shifts.

🔸Fib 2 (slow) emphasizes *macro-structure* for anchor/bias context.

These defaults keep Fib 1 responsive without jitter and Fib 2 stable without lag.

➡️ Turn Auto Presets = OFF to take full control with the manual inputs described below.

➖➖➖

🛠 Manual Fib Midpoint Settings (when Auto = OFF)

💡Each midpoint uses three knobs:

🔸Pivot Left (L): bars to the left that must be lower/higher to qualify a swing

🔸Pivot Right (R): bars to the right that must be lower/higher to confirm the swing

🔸Smoothing (S): SMA period applied to the raw 50% midpoint (stabilizes noise)

5-Minute optimized defaults

🔸Fib Trend 1: `L21 / R5 / S55` → responsive local structure (entries/exits, re-balancing zones)

🔸Fib Trend 2: `L55 / R13 / S89` → broader structure (trend context, anchors/stops)

Timeframe guidance

🔸1m–3m: may feel a touch laggy → consider ~`L13 / R3 / S34`

🔸15m–1h: defaults remain strong → optionally ~`L34 / R8 / S89`

🔸4h+ : increase span for stability → `L89–144 / R13–21 / S144–233`

➡️ Rule of thumb: shorter L/R = faster detection, longer S = smoother line. Tune until Fib 1 captures the “active swing” and Fib 2 captures the “dominant swing” without whipsaw.

➖➖➖

🎛 Inputs (quick reference)

🔸Fib Trend 1/2: Source (High/Low/Close), Left/Right bars, Smoothing length, Show/Hide, Cloud fill toggle

🔸Rolling 50%: Lookback length, Price basis (Wicks/Close/HLC3/OHLC4), Plot scope (Full / Last N / None)

🔸ATR Bands: ATR length, Multipliers (L1/L2), Plot scope, Line width/colors

🔸Overlay & Labels: Candle overlay mode, Label padding/size, 50% centerline toggle, Plot widths

➖➖➖

🖍️ Candle Coloring & Overlay Modes

💡Purpose: make trend instantly visible on the candles and ATR levels.

1) Color Logic (dropdown)

🔸 Fib Midpoints — Colors by position of price vs. Fib 1 & Fib 2

🔸ATR Zones — Colors by which ATR zone price is in relative to the Rolling 50%

➡️ Price Reference: Choose the input used for the decision (Close, HL2, OHLC3, OHLC4).

➡️Tip: Close is crisp; HL2/OHLC variants are smoother.

2) Overlay Style (dropdown)

🔸 None — No visual change to candles

🔸 Bar Color — Uses `barcolor()` to tint built-in candles (this takes into account your Trading View settings, for instance if you have wicks set to white, they will show up as white with this setting)

🔸 PlotCandles — Draws unified custom candles (body, wick, border) with the same color for maximum clarity

💡Practical use

🔸 Pick Fib Midpoints to read structural bias at a glance (above/below/between the cloud).

🔸 Pick ATR Zones to read value vs. stretch around the Rolling 50% (mean-reversion vs. trend extension).

➖➖➖

📘 How to use

A) Trend confirmation

- Strong bullish bias when price holds above both structural mids; strong bearish when below both.

- Use the Rolling 50% + ATR as a dynamic re-entry zone: pullbacks that respect ATR(L1) often continue the prevailing trend.

B) Transition / mean reversion

- Inside the Cloud (between Fib1 & Fib2) treat behavior as neutralization/re-balancing; range tactics tend to outperform momentum plays.

- In ranges, fades near ±ATR around the rolling 50% can mark short-term edges.

C) Breakout context

- When price leaves the Cloud, the Rolling 50% keeps you anchored so price never feels “floating.” A clean hold outside ATR(L1/L2) suggests regime strength; quick re-entries hint at traps.

➖➖➖

🖼 Chart examples

➡️ Each snapshot shows how the Cloud (structure) and the Rolling 50% + ATR (flow) work together.

1) 1-Minute Downtrend – Cloud as Dynamic Ceiling

- The Cloud slopes down; pullbacks repeatedly fail under the Cloud’s underside.

- Rolling 50% (dashed mid) + ATR(L1) act as a reversion band: rallies stall near upper ATR and rotate lower.

2) 15-Minute Persistent Drift – Structure Guides, Flow Times Entries

- Long drift lower with Cloud overhead.

- Consolidations near the rolling mid resolve in the trend direction; ATR bands frame risk on each attempt.

3) 15-Minute Uptrend (BTC) – From Cloud Escape to Value Stair-Step

- After escaping the prior Cloud, rolling 50% + ATR establish a new higher value area.

- Pullbacks into ATR(L1) produce orderly stair-steps; Cloud remains supportive on deeper dips

4) 5-Minute BTC – Pullback to Value then Rotate

- Strong leg up; retrace tags lower ATR band and rotates back toward the rolling mid.

- Labels (Fib1/Fib2) make the structural context explicit for decision-making.

➖➖➖

🧪 Starter presets

- Intraday (5–15m): Fib1 ~ L21/R5 (smooth 5), Fib2 ~ L55/R13 (smooth 9) • Rolling = 55 • ATR = 14 • L1 = 2.5x, L2 = 5.0x

- Scalping: Shorten lookbacks & smoothing; keep ATR multipliers similar, or tighten L1.

- Swing: Lengthen all lookbacks; consider ATR length 21–28.

➖➖➖

🏁Final Word

This script is not just a visual tool, it’s a complete trend and structure framework. Whether you're looking for clean trend alignment, dynamic support/resistance, or early warning signs of a reversal, this system is tuned to help you react with confidence — not hindsight.

Rembember, no single indicator should be used in isolation. For best results, combine it with price action analysis, higher-timeframe context, and complementary tools like trendlines, moving averages etc Use it as part of a well-rounded trading approach to confirm setups — not to define them alone.

---

💡Turn logic into clarity. Structure into trades. And uncertainty into confidence.

ATR Bands with ATR Cross + InfoTableOverview

This Pine Script™ indicator is designed to enhance traders' ability to analyze market volatility, trend direction, and position sizing directly on their TradingView charts. By plotting Average True Range (ATR) bands anchored at the OHLC4 price, displaying crossover labels, and providing a comprehensive information table, this tool offers a multifaceted approach to technical analysis.

Key Features:

ATR Bands Anchored at OHLC4: Visual representation of short-term and long-term volatility bands centered around the average price.

OHLC4 Dotted Line: A dotted line representing the average of Open, High, Low, and Close prices.

ATR Cross Labels: Visual cues indicating when short-term volatility exceeds long-term volatility and vice versa.

Information Table: Displays real-time data on market volatility, calculated position size based on risk parameters, and trend direction relative to the 20-period Smoothed Moving Average (SMMA).

Purpose

The primary purpose of this indicator is to:

Assess Market Volatility: By comparing short-term and long-term ATR values, traders can gauge the current volatility environment.

Determine Optimal Position Sizing: A calculated position size based on user-defined risk parameters helps in effective risk management.

Identify Trend Direction: Comparing the current price to the 20-period SMMA assists in determining the prevailing market trend.

Enhance Decision-Making: Visual cues and real-time data enable traders to make informed trading decisions with greater confidence.

How It Works

1. ATR Bands Anchored at OHLC4

Average True Range (ATR) Calculations

Short-Term ATR (SA): Calculated over a 9-period using ta.atr(9).

Long-Term ATR (LA): Calculated over a 21-period using ta.atr(21).

Plotting the Bands

OHLC4 Dotted Line: Plotted using small circles to simulate a dotted line due to Pine Script limitations.

ATR(9) Bands: Plotted in blue with semi-transparent shading.

ATR(21) Bands: Plotted in orange with semi-transparent shading.

Overlap: Bands can overlap, providing visual insights into changes in volatility.

2. ATR Cross Labels

Crossover Detection:

SA > LA: Indicates increasing short-term volatility.

Detected using ta.crossover(SA, LA).

A green upward label "SA>LA" is plotted below the bar.

SA < LA: Indicates decreasing short-term volatility.

Detected using ta.crossunder(SA, LA).

A red downward label "SA LA, then the market is considered volatile.

Display: Shows "Yes" or "No" based on the comparison.

b. Position Size Calculation

Risk Total Amount: User-defined input representing the total capital at risk.

Risk per 1 Stock: User-defined input representing the risk associated with one unit of the asset.

Purpose: Helps traders determine the appropriate position size based on their risk tolerance and current market volatility.

c. Is Price > 20 SMMA?

SMMA Calculation:

Calculated using a 20-period Smoothed Moving Average with ta.rma(close, 20).

Logic: If the current close price is above the SMMA, the trend is considered upward.

Display: Shows "Yes" or "No" based on the comparison.

How to Use

Step 1: Add the Indicator to Your Chart

Copy the Script: Copy the entire Pine Script code into the TradingView Pine Editor.

Save and Apply: Save the script and click "Add to Chart."

Step 2: Configure Inputs

Risk Parameters: Adjust the "Risk Total Amount" and "Risk per 1 Stock" in the indicator settings to match your personal risk management strategy.

Step 3: Interpret the Visuals

ATR Bands

Width of Bands: Wider bands indicate higher volatility; narrower bands indicate lower volatility.

Band Overlap: Pay attention to areas where the blue and orange bands diverge or converge.

OHLC4 Dotted Line

Serves as a central reference point for the ATR bands.

Helps visualize the average price around which volatility is measured.

ATR Cross Labels

"SA>LA" Label:

Indicates short-term volatility is increasing relative to long-term volatility.

May signal potential breakout or trend acceleration.

"SA 20 SMMA?

Use this to confirm trend direction before entering or exiting trades.

Practical Example

Imagine you are analyzing a stock and notice the following:

ATR(9) Crosses Above ATR(21):

A green "SA>LA" label appears.

The info table shows "Yes" for "Is ATR-based price volatile."

Position Size:

Based on your risk parameters, the position size is calculated.

Price Above 20 SMMA:

The info table shows "Yes" for "Is price > 20 SMMA."

Interpretation:

The market is experiencing increasing short-term volatility.

The trend is upward, as the price is above the 20 SMMA.

You may consider entering a long position, using the calculated position size to manage risk.

Customization

Colors and Transparency:

Adjust the colors of the bands and labels to suit your preferences.

Risk Parameters:

Modify the default values for risk amounts in the inputs.

Moving Average Period:

Change the SMMA period if desired.

Limitations and Considerations

Lagging Indicators: ATR and SMMA are lagging indicators and may not predict future price movements.

Market Conditions: The effectiveness of this indicator may vary across different assets and market conditions.

Risk of Overfitting: Relying solely on this indicator without considering other factors may lead to suboptimal trading decisions.

Conclusion

This indicator combines essential elements of technical analysis to provide a comprehensive tool for traders. By visualizing ATR bands anchored at the OHLC4, indicating volatility crossovers, and providing real-time data on position sizing and trend direction, it aids in making informed trading decisions.

Whether you're a novice trader looking to understand market volatility or an experienced trader seeking to refine your strategy, this indicator offers valuable insights directly on your TradingView charts.

Code Summary

The script is written in Pine Script™ version 5 and includes:

Calculations for OHLC4, ATRs, Bands, SMMA:

Uses built-in functions like ta.atr() and ta.rma() for calculations.

Plotting Functions:

plotshape() for the OHLC4 dotted line.

plot() and fill() for the ATR bands.

Crossover Detection:

ta.crossover() and ta.crossunder() for detecting ATR crosses.

Labeling Crossovers:

label.new() to place informative labels on the chart.

Information Table Creation:

table.new() to create the table.

table.cell() to populate it with data.

Acknowledgments

ATR and SMMA Concepts: Built upon standard technical analysis concepts widely used in trading.

Pine Script™: Leveraged the capabilities of Pine Script™ version 5 for advanced charting and analysis.

Note: Always test any indicator thoroughly and consider combining it with other forms of analysis before making trading decisions. Trading involves risk, and past performance is not indicative of future results.

Happy Trading!

divergingchartpatternLibrary "divergingchartpattern"

Library having implementation of converging chart patterns

getPatternNameByType(patternType)

Returns pattern name based on type

Parameters:

patternType (int) : integer value representing pattern type

Returns: string name of the pattern

method find(this, sProperties, dProperties, patterns, ohlcArray)

find converging patterns for given zigzag

Namespace types: zg.Zigzag

Parameters:

this (Zigzag type from Trendoscope/ZigzagLite/2) : Current zigzag Object

sProperties (ScanProperties) : ScanProperties Object

dProperties (DrawingProperties type from Trendoscope/abstractchartpatterns/5) : DrawingProperties Object

patterns (array type from Trendoscope/abstractchartpatterns/5) : array of existing patterns to check for duplicates

ohlcArray (array type from Trendoscope/ohlc/1) : array of OHLC values for historical reference

Returns: string name of the pattern

ScanProperties

Object containing properties for pattern scanning

Fields:

baseProperties (ScanProperties type from Trendoscope/abstractchartpatterns/5) : Object of Base Scan Properties

convergingDistanceMultiplier (series float)

convergingpatternsLibrary "convergingpatterns"

Library having implementation of converging chart patterns

getPatternNameByType(patternType)

Returns pattern name based on type

Parameters:

patternType (int) : integer value representing pattern type

Returns: string name of the pattern

method find(this, sProperties, dProperties, patterns, ohlcArray)

find converging patterns for given zigzag

Namespace types: zg.Zigzag

Parameters:

this (Zigzag type from Trendoscope/ZigzagLite/2) : Current zigzag Object

sProperties (ScanProperties) : ScanProperties Object

dProperties (DrawingProperties type from Trendoscope/abstractchartpatterns/5) : DrawingProperties Object

patterns (array type from Trendoscope/abstractchartpatterns/5) : array of existing patterns to check for duplicates

ohlcArray (array type from Trendoscope/ohlc/1) : array of OHLC values for historical reference

Returns: string name of the pattern

ScanProperties

Object containing properties for pattern scanning

Fields:

baseProperties (ScanProperties type from Trendoscope/abstractchartpatterns/5) : Object of Base Scan Properties

convergingDistanceMultiplier (series float) : when multiplied with pattern size gets the max number of bars within which the pattern should converge

abstractchartpatternsLibrary "abstractchartpatterns"

Library having abstract types and methods for chart pattern implementations

checkBarRatio(p1, p2, p3, properties)

checks if three zigzag pivot points are having uniform bar ratios

Parameters:

p1 (chart.point) : First pivot point

p2 (chart.point) : Second pivot point

p3 (chart.point) : Third pivot point

properties (ScanProperties)

Returns: true if points are having uniform bar ratio

getRatioDiff(p1, p2, p3)

gets ratio difference between 3 pivot combinations

Parameters:

p1 (chart.point)

p2 (chart.point)

p3 (chart.point)

Returns: returns the ratio difference between pivot2/pivot1 ratio and pivot3/pivot2 ratio

method inspect(points, stratingBar, endingBar, direction, ohlcArray)

Creates a trend line between 2 or 3 points and validates and selects best combination

Namespace types: chart.point

Parameters:

points (chart.point ) : Array of chart.point objects used for drawing trend line

stratingBar (int) : starting bar of the trend line

endingBar (int) : ending bar of the trend line

direction (float) : direction of the last pivot. Tells whether the line is joining upper pivots or the lower pivots

ohlcArray (OHLC type from Trendoscope/ohlc/1) : Array of OHLC values

Returns: boolean flag indicating if the trend line is valid and the trend line object as tuple

method draw(this)

draws pattern on the chart

Namespace types: Pattern

Parameters:

this (Pattern) : Pattern object that needs to be drawn

Returns: Current Pattern object

method erase(this)

erase the given pattern on the chart

Namespace types: Pattern

Parameters:

this (Pattern) : Pattern object that needs to be erased

Returns: Current Pattern object

method push(this, p, maxItems)

push Pattern object to the array by keeping maxItems limit

Namespace types: Pattern

Parameters:

this (Pattern ) : array of Pattern objects

p (Pattern) : Pattern object to be added to array

@oaram maxItems Max number of items the array can hold

maxItems (int)

Returns: Current Pattern array

method deepcopy(this)

Perform deep copy of a chart point array

Namespace types: chart.point

Parameters:

this (chart.point ) : array of chart.point objects

Returns: deep copy array

DrawingProperties

Object containing properties for pattern drawing

Fields:

patternLineWidth (series int) : Line width of the pattern trend lines

showZigzag (series bool) : show zigzag associated with pattern

zigzagLineWidth (series int) : line width of the zigzag lines. Used only when showZigzag is set to true

zigzagLineColor (series color) : color of the zigzag lines. Used only when showZigzag is set to true

showPatternLabel (series bool) : display pattern label containing the name

patternLabelSize (series string) : size of the pattern label. Used only when showPatternLabel is set to true

showPivotLabels (series bool) : Display pivot labels of the patterns marking 1-6

pivotLabelSize (series string) : size of the pivot label. Used only when showPivotLabels is set to true

pivotLabelColor (series color) : color of the pivot label outline. chart.bg_color or chart.fg_color are the appropriate values.

deleteOnPop (series bool) : delete the pattern when popping out from the array of Patterns.

Pattern

Object containing Individual Pattern data

Fields:

points (chart.point )

originalPoints (chart.point )

trendLine1 (Line type from Trendoscope/LineWrapper/1) : First trend line joining pivots 1, 3, 5

trendLine2 (Line type from Trendoscope/LineWrapper/1) : Second trend line joining pivots 2, 4 (, 6)

properties (DrawingProperties) : DrawingProperties Object carrying common properties

patternColor (series color) : Individual pattern color. Lines and labels will be using this color.

ratioDiff (series float) : Difference between trendLine1 and trendLine2 ratios

zigzagLine (series polyline) : Internal zigzag line drawing Object

pivotLabels (label ) : array containning Pivot labels

patternLabel (series label) : pattern label Object

patternType (series int) : integer representing the pattern type

patternName (series string) : Type of pattern in string

ScanProperties

Object containing properties for pattern scanning

Fields:

offset (series int) : Zigzag pivot offset. Set it to 1 for non repainting scan.

numberOfPivots (series int) : Number of pivots to be used in pattern search. Can be either 5 or 6

errorRatio (series float) : Error Threshold to be considered for comparing the slope of lines

flatRatio (series float) : Retracement ratio threshold used to determine if the lines are flat

checkBarRatio (series bool) : Also check bar ratio are within the limits while scanning the patterns

barRatioLimit (series float) : Bar ratio limit used for checking the bars. Used only when checkBarRatio is set to true

avoidOverlap (series bool) : avoid overlapping patterns.

allowedPatterns (bool ) : array of bool encoding the allowed pattern types.

allowedLastPivotDirections (int ) : array of int representing allowed last pivot direction for each pattern types

themeColors (color ) : color array of themes to be used.

Volume Delta Volume Signals by Claudio [hapharmonic]// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © hapharmonic

//@version=6

FV = format.volume

FP = format.percent

indicator('Volume Delta Volume Signals by Claudio ', format = FV, max_bars_back = 4999, max_labels_count = 500)

//------------------------------------------

// Settings |

//------------------------------------------

bool usecandle = input.bool(true, title = 'Volume on Candles',display=display.none)

color C_Up = input.color(#12cef8, title = 'Volume Buy', inline = ' ', group = 'Style')

color C_Down = input.color(#fe3f00, title = 'Volume Sell', inline = ' ', group = 'Style')

// ✅ Nueva entrada para colores de señales

color buySignalColor = input.color(color.new(color.green, 0), "Buy Signal Color", group = "Signals")

color sellSignalColor = input.color(color.new(color.red, 0), "Sell Signal Color", group = "Signals")

string P_ = input.string(position.top_right,"Position",options = ,

group = "Style",display=display.none)

string sL = input.string(size.small , 'Size Label', options = , group = 'Style',display=display.none)

string sT = input.string(size.normal, 'Size Table', options = , group = 'Style',display=display.none)

bool Label = input.bool(false, inline = 'l')

History = input.bool(true, inline = 'l')

// Inputs for EMA lengths and volume confirmation

bool MAV = input.bool(true, title = 'EMA', group = 'EMA')

string volumeOption = input.string('Use Volume Confirmation', title = 'Volume Option', options = , group = 'EMA',display=display.none)

bool useVolumeConfirmation = volumeOption == 'none' ? false : true

int emaFastLength = input(12, title = 'Fast EMA Length', group = 'EMA',display=display.none)

int emaSlowLength = input(26, title = 'Slow EMA Length', group = 'EMA',display=display.none)

int volumeConfirmationLength = input(6, title = 'Volume Confirmation Length', group = 'EMA',display=display.none)

string alert_freq = input.string(alert.freq_once_per_bar_close, title="Alert Frequency",

options= ,group = "EMA",

tooltip="If you choose once_per_bar, you will receive immediate notifications (but this may cause interference or indicator repainting).

\n However, if you choose once_per_bar_close, it will wait for the candle to confirm the signal before notifying.",display=display.none)

//------------------------------------------

// UDT_identifier |

//------------------------------------------

type OHLCV

float O = open

float H = high

float L = low

float C = close

float V = volume

type VolumeData

float buyVol

float sellVol

float pcBuy

float pcSell

bool isBuyGreater

float higherVol

float lowerVol

color higherCol

color lowerCol

//------------------------------------------

// Calculate volumes and percentages |

//------------------------------------------

calcVolumes(OHLCV ohlcv) =>

var VolumeData data = VolumeData.new()

data.buyVol := ohlcv.V * (ohlcv.C - ohlcv.L) / (ohlcv.H - ohlcv.L)

data.sellVol := ohlcv.V - data.buyVol

data.pcBuy := data.buyVol / ohlcv.V * 100

data.pcSell := 100 - data.pcBuy

data.isBuyGreater := data.buyVol > data.sellVol

data.higherVol := data.isBuyGreater ? data.buyVol : data.sellVol

data.lowerVol := data.isBuyGreater ? data.sellVol : data.buyVol

data.higherCol := data.isBuyGreater ? C_Up : C_Down

data.lowerCol := data.isBuyGreater ? C_Down : C_Up

data

//------------------------------------------

// Get volume data |

//------------------------------------------

ohlcv = OHLCV.new()

volData = calcVolumes(ohlcv)

// Plot volumes and create labels

plot(ohlcv.V, color=color.new(volData.higherCol, 90), style=plot.style_columns, title='Total',display = display.all - display.status_line)

plot(ohlcv.V, color=volData.higherCol, style=plot.style_stepline_diamond, title='Total2', linewidth = 2,display = display.pane)

plot(volData.higherVol, color=volData.higherCol, style=plot.style_columns, title='Higher Volume', display = display.all - display.status_line)

plot(volData.lowerVol , color=volData.lowerCol , style=plot.style_columns, title='Lower Volume',display = display.all - display.status_line)

S(D,F)=>str.tostring(D,F)

volStr = S(math.sign(ta.change(ohlcv.C)) * ohlcv.V, FV)

buyVolStr = S(volData.buyVol , FV )

sellVolStr = S(volData.sellVol , FV )

// ✅ MODIFICACIÓN: Porcentaje sin decimales

buyPercentStr = str.tostring(math.round(volData.pcBuy)) + " %"

sellPercentStr = str.tostring(math.round(volData.pcSell)) + " %"

totalbuyPercentC_ = volData.buyVol / (volData.buyVol + volData.sellVol) * 100

sup = not na(ohlcv.V)

if sup

TC = text.align_center

CW = color.white

var table tb = table.new(P_, 6, 6, bgcolor = na, frame_width = 2, frame_color = chart.fg_color, border_width = 1, border_color = CW)

tb.cell(0, 0, text = 'Volume Candles', text_color = #FFBF00, bgcolor = #0E2841, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 0, 5, 0)

tb.cell(0, 1, text = 'Current Volume', text_color = CW, bgcolor = #0B3040, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 1, 1, 1)

tb.cell(0, 2, text = 'Buy', text_color = #000000, bgcolor = #92D050, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 2, text = 'Sell', text_color = #000000, bgcolor = #FF0000, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(0, 3, text = buyVolStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 3, text = sellVolStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(0, 5, text = 'Net: ' + volStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 5, 1, 5)

tb.cell(0, 4, text = buyPercentStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 4, text = sellPercentStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

cellCount = 20

filledCells = 0

for r = 5 to 1 by 1

for c = 2 to 5 by 1

if filledCells < cellCount * (totalbuyPercentC_ / 100)

tb.cell(c, r, text = '', bgcolor = C_Up)

else

tb.cell(c, r, text = '', bgcolor = C_Down)

filledCells := filledCells + 1

filledCells

if Label

sp = ' '

l = label.new(bar_index, ohlcv.V,

text=str.format('Net: {0}\nBuy: {1} ({2})\nSell: {3} ({4})\n{5}/\\\n {5}l\n {5}l',

volStr, buyVolStr, buyPercentStr, sellVolStr, sellPercentStr, sp),

style=label.style_none, textcolor=volData.higherCol, size=sL, textalign=text.align_left)

if not History

(l ).delete()

//------------------------------------------

// Draw volume levels on the candlesticks |

//------------------------------------------

float base = na,float value = na

bool uc = usecandle and sup

if volData.isBuyGreater

base := math.min(ohlcv.O, ohlcv.C)

value := base + math.abs(ohlcv.O - ohlcv.C) * (volData.pcBuy / 100)

else

base := math.max(ohlcv.O, ohlcv.C)

value := base - math.abs(ohlcv.O - ohlcv.C) * (volData.pcSell / 100)

barcolor(sup ? color.new(na, na) : ohlcv.C < ohlcv.O ? color.red : color.green,display = usecandle? display.all:display.none)

UseC = uc ? volData.higherCol:color.new(na, na)

plotcandle(uc?base:na, uc?base:na, uc?value:na, uc?value:na,

title='Body', color=UseC, bordercolor=na, wickcolor=UseC,

display = usecandle ? display.all - display.status_line : display.none, force_overlay=true,editable=false)

plotcandle(uc?ohlcv.O:na, uc?ohlcv.H:na, uc?ohlcv.L:na, uc?ohlcv.C:na,

title='Fill', color=color.new(UseC,80), bordercolor=UseC, wickcolor=UseC,

display = usecandle ? display.all - display.status_line : display.none, force_overlay=true,editable=false)

//------------------------------------------------------------

// Plot the EMA and filter out the noise with volume control. |

//------------------------------------------------------------

float emaFast = ta.ema(ohlcv.C, emaFastLength)

float emaSlow = ta.ema(ohlcv.C, emaSlowLength)

bool signal = emaFast > emaSlow

color c_signal = signal ? C_Up : C_Down

float volumeMA = ta.sma(ohlcv.V, volumeConfirmationLength)

bool crossover = ta.crossover(emaFast, emaSlow)

bool crossunder = ta.crossunder(emaFast, emaSlow)

isVolumeConfirmed(source, length, ma) =>

math.sum(source > ma ? source : 0, length) >= math.sum(source < ma ? source : 0, length)

bool ISV = isVolumeConfirmed(ohlcv.V, volumeConfirmationLength, volumeMA)

bool crossoverConfirmed = crossover and (not useVolumeConfirmation or ISV)

bool crossunderConfirmed = crossunder and (not useVolumeConfirmation or ISV)

PF = MAV ? emaFast : na

PS = MAV ? emaSlow : na

p1 = plot(PF, color = c_signal, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 80), linewidth = 10, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 90), linewidth = 20, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 95), linewidth = 30, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 98), linewidth = 45, editable = false, force_overlay = true, display = display.pane)

p2 = plot(PS, color = c_signal, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 80), linewidth = 10, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 90), linewidth = 20, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 95), linewidth = 30, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 98), linewidth = 45, editable = false, force_overlay = true, display = display.pane)

fill(p1, p2, top_value=crossover ? emaFast : emaSlow,

bottom_value =crossover ? emaSlow : emaFast,

top_color =color.new(c_signal, 80),

bottom_color =color.new(c_signal, 95)

)

// ✅ Usar colores configurables para señales

plotshape(crossoverConfirmed and MAV, style=shape.triangleup , location=location.belowbar, color=buySignalColor , size=size.small, force_overlay=true,display =display.pane)

plotshape(crossunderConfirmed and MAV, style=shape.triangledown, location=location.abovebar, color=sellSignalColor, size=size.small, force_overlay=true,display =display.pane)

string msg = '---------\n'+"Buy volume ="+buyVolStr+"\nBuy Percent = "+buyPercentStr+"\nSell volume = "+sellVolStr+"\nSell Percent = "+sellPercentStr+"\nNet = "+volStr+'\n---------'

if crossoverConfirmed

alert("Price (" + str.tostring(close) + ") Crossed over MA\n" + msg, alert_freq)

if crossunderConfirmed

alert("Price (" + str.tostring(close) + ") Crossed under MA\n" + msg, alert_freq)

Volume essential parameters overlayVolume EPO – Essential Volume Parameters Overlay

1. Motivation and design philosophy

Volume EPO is designed as a conceptual overlay rather than a self contained trading system. The main idea behind this script is to take complex, foundational market concepts out of heavy, menu driven strategies and express them as lightweight, independent layers that sit on top of any chart or indicator.

In many TradingView scripts, a single strategy tries to handle everything at once: signal logic, risk settings, visual cues, multi timeframe controls, and conceptual explanations. This usually leads to long input menus, performance issues, and difficult maintenance. The architectural approach behind Volume EPO is the opposite: keep the core strategy lean, and move the explanation and measurement of key concepts into dedicated overlays.

In this framework, Volume EPO is the base layer for the concept of volume. It does not decide anything about entries or exits. Instead, it exposes and clarifies how different definitions of volume behave candle by candle. Other layers or strategies can then build on top of this understanding.

2. What Volume EPO does

Volume EPO focuses on four essential volume parameters for each bar:

- Buy volume - Sell volume - Total volume - Delta volume (the difference between buy and sell volume)

The script presents these parameters in a compact heads up display (HUD) table that can be positioned anywhere on the chart. It is designed to be visually minimal, language aware, and usable on top of any other indicator or price action without cluttering the view.

The indicator does not output signals, alerts, arrows, or strategy entries. It is a descriptive and educational tool that shows how volume is distributed, not a prescriptive tool that tells the trader what to do.

3. Two definitions of volume

A central theme of this script is that there is more than one way to define and interpret “volume” inside a single candle. Volume EPO implements and clearly separates two different approaches:

- A geometric, candle based approximation that uses only OHLC and volume of the current bar. - An intrabar, data driven definition that uses lower timeframe up and down volume when it is available.

The user can switch between these modes via the calculation method input. The mode is prominently shown inside the on chart table so that the context is always explicit.

3.1 Geometry mode (Source File, approximate)

In Geometry mode, Volume EPO works only with the current bar’s OHLC values and total volume. No lower timeframe data is required.

The candle’s range is defined as high minus low. If the range is positive, the position of the close inside that range is used as a simple model for how volume might have been distributed between buyers and sellers:

- The closer the close is to the high, the more of the total volume is attributed to the buying side. - The closer the close is to the low, the more of the total volume is attributed to the selling side. - In a rare case where the bar has no price range (for example a flat or doji bar), total volume is split evenly between buy and sell volume.

From this model, the script derives:

- Buy volume (approximated) - Sell volume (approximated) - Total volume (as reported by the bar) - Delta volume as the difference between buy and sell volume

This approach is intentionally labeled as “Geometry (Approx)” in the HUD. It is a theoretical reconstruction based solely on the candle’s geometry and total volume, and it is always available on any market or timeframe that provides OHLCV data.

3.2 Intrabar mode (Precise)

In Intrabar mode, Volume EPO uses the TradingView built in library for up and down volume on a user selected lower timeframe. Instead of inferring volume from the shape of the candle, it reads the underlying lower timeframe data when that data is accessible.

The script requests up and down volume from a lower timeframe such as 15 seconds, using the official TA library functions. The results are then interpreted as follows:

- Buy volume is taken as the absolute value of the up volume. - Sell volume is taken as the absolute value of the down volume. - Total volume is the sum of buy and sell volume. - Delta volume is provided directly by the library as the difference between up and down volume.

If valid lower timeframe data exists for a bar, the bar is counted as covered by Intrabar data. If not, that bar is marked as invalid for this precise calculation and is excluded from the covered count.

This mode is labeled “Precise” in the HUD, together with the selected lower timeframe, because it is anchored in actual intrabar data rather than in a geometric model. It provides a closer view of how buying and selling pressure unfolded inside the bar, at the cost of requiring more data and being dependent on the availability of that data.

4. Coverage, lookback, and what the numbers mean

The top part of the HUD reports not only which volume definition is active, but also an additional line that describes the effective coverage of the data.

In Intrabar (Precise) mode, the script displays:

- “Scanned: N Bars”

Here, N counts how many bars since the indicator was loaded have successfully received valid lower timeframe delta data. It is a measure of how much of the visible history has been truly covered by intrabar information, not a lookback window in the sense of a rolling calculation.

In Geometry mode, the script displays:

- “Lookback: L Bars”

In this extracted layer, the lookback value L is purely descriptive. It does not change how the current bar’s volume is computed, and it is not used in any iterative or statistical calculation inside this script. It is meant as a conceptual label, for example to keep the volume layer consistent with a broader framework where lookback length is a structural parameter.

Summarizing these two fields:

- Scanned tells you how many bars have been processed using real intrabar data. - Lookback is a descriptive parameter in Geometry mode in this specific overlay, not a direct driver of the computations.

5. The HUD layout on the chart

The on chart table is intentionally compact and structured to be read quickly:

- Header: a title identifying the overlay as Volume EPO. - Mode line: explicitly states whether the script is in Precise or Geometry mode, and for Precise mode also shows the lower timeframe used. - Coverage line: - In Precise mode, it shows “Scanned: N Bars”. - In Geometry mode, it shows “Lookback: L Bars”. - Volume block: - A line for buy and sell volume, marked with clear directional symbols. - A line for total volume and the absolute delta, accompanied by the sign of the delta. - Numeric formatting uses human friendly suffixes (for example K, M, B) to keep the display readable. - Footer: the current symbol and a time stamp, adjusted by a user selectable timezone offset so that the HUD can be aligned with the trader’s local time reference.

The table can be positioned anywhere on the chart and resized via inputs, and it supports multiple color themes and languages in order to integrate cleanly into different chart layouts.

6. How to use Volume EPO in practice

Volume EPO is meant to be read together with price action and other tools, not in isolation. Typical uses include:

- Studying how often a strong directional candle is actually supported by dominant buy or sell volume. - Comparing the behavior of delta volume between Geometry and Intrabar definitions. - Building a personal intuition for how intrabar data refines or contradicts the simple candle based approximation. - Feeding these insights into separate, lean strategy scripts that do not need to carry the full explanatory logic of volume inside them.

Because it is an overlay layer, Volume EPO can be stacked with other custom indicators without adding new signals or complexity to their logic. It simply adds a clear and consistent view of volume behavior on top of whatever the trader is already watching.

7. Educational and non signalling nature

Finally, it is important to stress that Volume EPO is not a trading system, not a signal generator, and not financial advice. The script does not tell the user when to enter or exit. It only reports how different definitions of volume describe the current bar.

Deciding whether to trade, how to trade, and which risk parameters to use remains entirely with the user and with their own strategy. Volume EPO provides context and clarity around the concept of volume so that those decisions can be informed by a better understanding of how buying and selling pressure is structured inside each candle.

Note: Even on lower timeframes, every reconstruction of volume remains an approximation, except at the true single tick level. However, the closer the chosen lower timeframe is to a one tick stream, the more accurately it can reflect the underlying order flow and balance between buying and selling pressure.

Candle Info by MontyThis indicator was made to help my friend.

This indicator basically calculates the MOVE in percentage and shows the OHLC of candle in a label.

-> Panel Index: How much index you want the label to be.

-> Show Candle OHLC: Shows Open High Low and Close of the candle in the panel/label

-> % Calculation Mode:

1: Calculated by Candle Wick Low to Candle Wick High for Green candle and Vice Versa for Red Candle

2: Calculated by Open of a candle to the current price.

-> Label Text Color: Used to change the color of the Label Text

-> Label Background Color: Used to change the color of Label background

Join the free Discord: discord.gg/chuffgang

Fair value bands / quantifytools— Overview

Fair value bands, like other band tools, depict dynamic points in price where price behaviour is normal or abnormal, i.e. trading at/around mean (price at fair value) or deviating from mean (price outside fair value). Unlike constantly readjusting standard deviation based bands, fair value bands are designed to be smooth and constant, based on typical historical deviations. The script calculates pivots that take place above/below fair value basis and forms median deviation bands based on this information. These points are then multiplied up to 3, representing more extreme deviations.

By default, the script uses OHLC4 and SMA 20 as basis for the bands. Users can form their preferred fair value basis using following options:

Price source

- Standard OHLC values

- HL2 (High + low / 2)

- OHLC4 (Open + high + low + close / 4)

- HLC3 (High + low + close / 3)

- HLCC4 (High + low + close + close / 4)

Smoothing

- SMA

- EMA

- HMA

- RMA

- WMA

- VWMA

- Median

Once fair value basis is established, some additional customization options can be employed:

Trend mode

Direction based

Cross based

Trend modes affect fair value basis color that indicates trend direction. Direction based trend considers only the direction of the defined fair value basis, i.e. pointing up is considered an uptrend, vice versa for downtrend. Cross based trends activate when selected source (same options as price source) crosses fair value basis. These sources can be set individually for uptrend/downtrend cross conditions. By default, the script uses cross based trend mode with low and high as sources.

Cross based (downtrend not triggered) vs. direction based (downtrend triggered):

Threshold band

Threshold band is calculated using typical deviations when price is trading at fair value basis. In other words, a little bit of "wiggle room" is added around the mean based on expected deviation. This feature is useful for cross based trends, as it allows filtering insignificant crosses that are more likely just noise. By default, threshold band is calculated based on 1x median deviation from mean. Users can increase/decrease threshold band width via input menu for more/less noise filtering, e.g. 2x threshold band width would require price to cross wiggle room that is 2x wider than typical, 0x erases threshold band altogether.

Deviation bands

Width of deviation bands by default is based on 1x median deviations and can be increased/decreased in a similar manner to threshold bands.

Each combination of customization options produces varying behaviour in the bands. To measure the behaviour and finding fairest representation of fair and unfair value, some data is gathered.

— Fair value metrics

Space between each band is considered a lot, named +3, +2, +1, -1, -2, -3. For each lot, time spent and volume relative to volume moving average (SMA 20) is recorded each time price is trading in a given lot:

Depending on the asset, timeframe and chosen fair value basis, shape of the distributions vary. However, practically always time is distributed in a normal bell curve shape, being highest at lots +1 to -1, gradually decreasing the further price is from the mean. This is hardly surprising, but it allows accurately determining dynamic areas of normal and abnormal price behaviour (i.e. low risk area between +1 and -1, high risk area between +-2 to +-3). Volume on the other hand is typically distributed the other way around, being lowest at lots +1 to -1 and highest at +-2 to +-3. When time and volume are distributed like so, we can conclude that 1) price being outside fair value is a rare event and 2) the more price is outside fair value, the more anomaly behaviour in volume we tend to find.

Viewing metric calculations

Metric calculation highlights can be enabled from the input menu, resulting in a lot based coloring and visibility of each lot counter (time, cumulative relative volume and average relative volume) in data window:

— Alerts

Available alerts are the following:

Individual

- High crossing deviation band (bands +1 to +3 )

- Low crossing deviation band (bands -1 to -3 )

- Low at threshold band in an uptrend

- High at threshold band in a downtrend

- New uptrend

- New downtrend

Grouped

- New uptrend or downtrend

- Deviation band cross (+1 or -1)

- Deviation band cross (+2 or -2)

- Deviation band cross (+3 or -3)

— Practical guide

Example #1 : Risk on/risk off trend following

Ideal trend stays inside fair value and provides sufficient cool offs between the moves. When this is the case, fair value bands can be used for sensible entry/exit levels within the trend.

Example #2 : Mean reversions

When price shows exuberance into an extreme deviation, followed by a stall and signs of exhaustion (wicks), an opportunity for mean reversion emerges. The higher the deviation, the more volatility in the move, the more signalling of exhaustion, the better.

Example #3 : Tweaking bands for desired behaviour

The faster the length of fair value basis, the more momentum price needs to hit extreme deviation levels, as bands too are moving faster alongside price. Decreasing fair value basis length typically leads to more quick and aggressive deviations and less steady trends outside fair value.

Weight Gain 4000 - (Adjustable Volume Weighted MA) - [mutantdog]Short Version:

This is a fairly self-contained system based upon a moving average crossover with several unique features. The most significant of these is the adjustable volume weighting system, allowing for transformations between standard and weighted versions of each included MA. With this feature it is possible to apply partial weighting which can help to improve responsiveness without dramatically altering shape. Included types are SMA, EMA, WMA, RMA, hSMA, DEMA and TEMA. Potentially more will be added in future (check updates below).

In addition there are a selection of alternative 'weighted' inputs, a pair of Bollinger-style deviation bands, a separate price tracker and a bunch of alert presets.

This can be used out-of-the-box or tweaked in multiple ways for unusual results. Default settings are a basic 8/21 EMA cross with partial volume weighting. Dev bands apply to MA2 and are based upon the type and the volume weighting. For standard Bollinger bands use SMA with length 20 and try adding a small amount of volume weighting.

A more detailed breakdown of the functionality follows.

Long Version:

ADJUSTABLE VOLUME WEIGHTING

In principle any moving average should have a volume weighted analogue, the standard VWMA is just an SMA with volume weighting for example. Actually, we can consider the SMA to be a special case where volume is a constant 1 per bar (the value is somewhat arbitrary, the important part is that it's constant). Similar principles apply to the 'elastic' EVWMA which is the volume weighted analogue of an RMA. In any case though, where we have standard and weighted variants it is possible to transform one into the other by gradually increasing or decreasing the weighting, which forms the basis of this system. This is not just a simple multiplier however, that would not work due to the relative proportions being the same when set at any non zero value. In order to create a meaningful transformation we need to use an exponent instead, eg: volume^x , where x is a variable determined in this case by the 'volume' parameter. When x=1, the full volume weighting applies and when x=0, the volume will be reduced to a constant 1. Values in between will result in the respective partial weighting, for example 0.5 will give the square root of the volume.

The obvious question here though is why would you want to do this? To answer that really it is best to actually try it. The advantages that volume weighting can bring to a moving average can sometimes come at the cost of unwanted or erratic behaviour. While it can tend towards much closer price tracking which may be desirable, sometimes it needs moderating especially in markets with lower liquidity. Here the adjustability can be useful, in many cases i have found that adding a small amount of volume weighting to a chosen MA can help to improve its responsiveness without overpowering it. Another possible use case would be to have two instances of the same MA with the same length but different weightings, the extent to which these diverge from each other can be a useful indicator of trend strength. Other uses will become apparent with experimentation and can vary from one market to another.

THE INCLUDED MODES

At the time of publication, there are 7 included moving average types with plans to add more in future. For now here is a brief explainer of what's on offer (continuing to use x as shorthand for the volume parameter), starting with the two most common types.

SMA: As mentioned above this is essentially a standard VWMA, calculated here as sma(source*volume^x,length)/sma(volume^x,length). In this case when x=0 then volume=1 and it reduces to a standard SMA.

RMA: Again mentioned above, this is an EVWMA (where E stands for elastic) with constant weighting. Without going into detail, this method takes the 1/length factor of an RMA and replaces it with volume^x/sum(volume^x,length). In this case again we can see that when x=0 then volume=1 and the original 1/length factor is restored.

EMA: This follows the same principle as the RMA where the standard 2/(length+1) factor is replaced with (2*volume^x)/(sum(volume^x,length)+volume^x). As with an RMA, when x=0 then volume=1 and this reduces back to the standard 2/(length+1).

DEMA: Just a standard Double EMA using the above.

TEMA: Likewise, a standard Triple EMA using the above.

hSMA: This is the same as the SMA except it uses harmonic mean calculations instead of arithmetic. In most cases the differences are negligible however they can become more pronounced when volume weighting is introduced. Furthermore, an argument can be made that harmonic mean calculations are better suited to downtrends or bear markets, in principle at least.

WMA: Probably the most contentious one included. Follows the same basic calculations as for the SMA except uses a WMA instead. Honestly, it makes little sense to combine both linear and volume weighting in this manner, included only for completeness and because it can easily be done. It may be the case that a superior composite could be created with some more complex calculations, in which case i may add that later. For now though this will do.

An additional 'volume filter' option is included, which applies a basic filter to the volume prior to calculation. For types based around the SMA/VWMA system, the volume filter is a WMA-4, for types based around the RMA/EVWMA system the filter is a RMA-2.

As and when i add more they will be listed in the updates at the bottom.

WEIGHTED INPUTS

The ohlc method of source calculations is really a leftover from a time when data was far more limited. Nevertheless it is still the method used in charting and for the most part is sufficient. Often the only important value is 'close' although sometimes 'high' and 'low' can be relevant also. Since we are volume weighting however, it can be useful to incorporate as much information as possible. To that end either 'hlc3' or 'hlcc4' tend to be the best of the defaults (in the case of 24/7 charting like crypto or intraday trading, 'ohlc4' should be avoided as it is effectively the same as a lagging version of 'hlcc4'). There are many other (infinitely many, in fact) possible combinations that can be created, i have included a few here.

The premise is fairly straightforward, by subtracting one value from another, the remaining difference can act as a kind of weight. In a simple case consider 'hl2' as simply the midrange ((high+low)/2), instead of this using 'high+low-open' would give more weight to the value furthest from the open, providing a good estimate of the median. An even better estimate can be achieved by combining that with 'high+low-close' to give the included result 'hl-oc2'. Similarly, 'hlc3' can be considered the basic mean of the three significant values, an included weighted version 'hlc2-o2' combines a sum with subtraction of open to give an estimated mean that may be more accurate. Finally we can apply a similar principle to the close, by subtracting the other values, this one potentially gets more complex so the included 'cc-ohlc4' is really the simplest. The result here is an overbias of the close in relation to the open and the midrange, while in most cases not as useful it can provide an estimate for the next bar assuming that the trend continues.

Of the three i've included, hlc2-o2 is in my opinion the most useful especially in this context, although it is perhaps best considered to be experimental in nature. For that reason, i've kept 'hlcc4' as the default for both MAs.

Additionally included is an 'aux input' which is the standard TV source menu and, where possible, can be set as outputs of other indicators.

THE SYSTEM

This one is fairly obvious and straightforward. It's just a moving average crossover with additional deviation (bollinger) bands. Not a lot to explain here as it should be apparent how it works.