Adjustable Vertical LinesThe script provides an indicator which will plot lines - 15 min, 30 min and 60 min. You can customize the time intervals and go to as low as one minute, but I found the 15-minute and 30-minute intervals works best for me when trying to find setups, and the lower time-frame intervals, is just pointless to use if you're not scalping on the seconds timeframe.

You can customize inputs for the line style. Line thickness, colour, etc.

I've seen this work using the OBR theory and applying it to the one-minute candle then looking for other confluences like order blocks, or breakers, FVGs, BOS/CHoC for further confirmation for scalping. It's important to backtest though and see for yourself.

Thanks for the boost.

Pesquisar nos scripts por "机械革命无界15+时不时闪屏"

Momentum Fusion v1Momentum Fusion v1

Overview

Momentum Fusion v1 (MFusion) is a multi-oscillator indicator that combines several components to analyze market momentum and trend strength. It incorporates modified versions of classic indicators such as PVI (Positive Volume Index), NVI (Negative Volume Index), MFI (Money Flow Index), RSI, Stochastic, and Bollinger Bands Oscillator. The indicator displays a histogram that changes color based on momentum strength and includes "FUSION🔥" signal labels when extreme values are reached.

Indicator Settings

Parameters:

EMA Length – Smoothing period for the moving average (default: 255).

Smoothing Period – Internal calculation smoothing parameter (default: 15).

BB Multiplier – Standard deviation multiplier for Bollinger Bands (default: 2.0).

Show verde / marron / media lines – Toggles the display of auxiliary lines.

Show FUSION🔥 label – Enables/disables signal labels.

Indicator Components

1. PVI (Positive Volume Index)

Formula:

pvi := volume > volume ? nz(pvi ) + (close - close ) / close * sval : nz(pvi )

Description:

PVI increases when volume rises compared to the previous bar and accounts for price percentage change. The stronger the price movement with increasing volume, the higher the PVI value.

2. NVI (Negative Volume Index)

Formula:

nvi := volume < volume ? nz(nvi ) + (close - close ) / close * sval : nz(nvi )

Description:

NVI tracks price movements during declining volume. If the price rises on low volume, it may indicate a "stealth" trend.

3. Money Flow Index (MFI)

Formula:

100 - 100 / (1 + up / dn)

Description:

An oscillator measuring money flow strength. Values above 80 suggest overbought conditions, while values below 20 indicate oversold conditions.

4. Stochastic Oscillator

Formula:

k = 100 * (close - lowest(low, length)) / (highest(high, length) - lowest(low, length))

Description:

A classic stochastic oscillator showing price position relative to the selected period's range.

5. Bollinger Bands Oscillator

Formula:

(tprice - BB midline) / (upper BB - lower BB) * 100

Description:

Indicates the price position relative to Bollinger Bands in percentage terms.

Key Lines & Histogram

1. Verde (Green Line)

Calculation:

verde = marron + oscp (normalized PVI)

Interpretation:

Higher values indicate stronger bullish momentum. A FUSION🔥 signal appears when the value reaches 750+.

2. Marron (Brown Line)

Calculation:

marron = (RSI + MFI + Bollinger Osc + Stochastic / 3) / 2

Interpretation:

A composite oscillator combining multiple indicators. Higher values suggest overbought conditions.

3. Media (Red Line)

Calculation:

media = EMA of marron with smoothing period

Interpretation:

Acts as a signal line for trend confirmation.

4. Histogram

Calculation:

histo = verde - marron

Colors:

Bright green (>100) – Strong bullish momentum.

Light green (>0) – Moderate bullish momentum.

Orange (<0) – Bearish momentum.

Red (<-100) – Strong bearish momentum.

Signals & Alerts

1. FUSION🔥 (Strong Momentum)

Condition:

verde >= 750

Visualization:

A "FUSION🔥" label appears below the chart.

Alert:

Can be set to trigger notifications when the condition is met.

2. Background Aura

Condition:

verde > 850

Visualization:

The chart background turns teal, indicating extreme momentum.

Usage Recommendations

FUSION🔥 Signal – Can be used as a long entry point when confirmed by other indicators.

Histogram:

1. Green bars – Potential long entry.

2. Red/orange bars – Potential short entry.

3. Media & Marron Crossover – Can serve as an additional trend filter.

4. Suitable for a 5-15 minute time frame

Conclusion

Momentum Fusion v1 is a powerful tool for momentum analysis, combining multiple indicators into a unified system. It is suitable for:

Trend traders (catching strong movements).

Scalpers (identifying short-term impulses).

Swing traders (filtering entry points).

The indicator features customizable settings and visual signals, making it adaptable to various trading styles.

MirPapa_Library_ICTLibrary "MirPapa_Library_ICT"

GetHTFoffsetToLTFoffset(_offset, _chartTf, _htfTf)

GetHTFoffsetToLTFoffset

@description Adjust an HTF offset to an LTF offset by calculating the ratio of timeframes.

Parameters:

_offset (int) : int The HTF bar offset (0 means current HTF bar).

_chartTf (string) : string The current chart’s timeframe (e.g., "5", "15", "1D").

_htfTf (string) : string The High Time Frame string (e.g., "60", "1D").

@return int The corresponding LTF bar index. Returns 0 if the result is negative.

IsConditionState(_type, _isBull, _level, _open, _close, _open1, _close1, _low1, _low2, _low3, _low4, _high1, _high2, _high3, _high4)

IsConditionState

@description Evaluate a condition state based on type for COB, FVG, or FOB.

Overloaded: first signature handles COB, second handles FVG/FOB.

Parameters:

_type (string) : string Condition type ("cob", "fvg", "fob").

_isBull (bool) : bool Direction flag: true for bullish, false for bearish.

_level (int) : int Swing level (only used for COB).

_open (float) : float Current bar open price (only for COB).

_close (float) : float Current bar close price (only for COB).

_open1 (float) : float Previous bar open price (only for COB).

_close1 (float) : float Previous bar close price (only for COB).

_low1 (float) : float Low 1 bar ago (only for COB).

_low2 (float) : float Low 2 bars ago (only for COB).

_low3 (float) : float Low 3 bars ago (only for COB).

_low4 (float) : float Low 4 bars ago (only for COB).

_high1 (float) : float High 1 bar ago (only for COB).

_high2 (float) : float High 2 bars ago (only for COB).

_high3 (float) : float High 3 bars ago (only for COB).

_high4 (float) : float High 4 bars ago (only for COB).

@return bool True if the specified condition is met, false otherwise.

IsConditionState(_type, _isBull, _pricePrev, _priceNow)

IsConditionState

@description Evaluate FVG or FOB condition based on price movement.

Parameters:

_type (string) : string Condition type ("fvg", "fob").

_isBull (bool) : bool Direction flag: true for bullish, false for bearish.

_pricePrev (float) : float Previous price (for FVG/FOB).

_priceNow (float) : float Current price (for FVG/FOB).

@return bool True if the specified condition is met, false otherwise.

IsSwingHighLow(_isBull, _level, _open, _close, _open1, _close1, _low1, _low2, _low3, _low4, _high1, _high2, _high3, _high4)

IsSwingHighLow

@description Public wrapper for isSwingHighLow.

Parameters:

_isBull (bool) : bool Direction flag: true for bullish, false for bearish.

_level (int) : int Swing level (1 or 2).

_open (float) : float Current bar open price.

_close (float) : float Current bar close price.

_open1 (float) : float Previous bar open price.

_close1 (float) : float Previous bar close price.

_low1 (float) : float Low 1 bar ago.

_low2 (float) : float Low 2 bars ago.

_low3 (float) : float Low 3 bars ago.

_low4 (float) : float Low 4 bars ago.

_high1 (float) : float High 1 bar ago.

_high2 (float) : float High 2 bars ago.

_high3 (float) : float High 3 bars ago.

_high4 (float) : float High 4 bars ago.

@return bool True if swing condition is met, false otherwise.

AddBox(_left, _right, _top, _bot, _xloc, _colorBG, _colorBD)

AddBox

@description Draw a rectangular box on the chart with specified coordinates and colors.

Parameters:

_left (int) : int Left bar index for the box.

_right (int) : int Right bar index for the box.

_top (float) : float Top price coordinate for the box.

_bot (float) : float Bottom price coordinate for the box.

_xloc (string) : string X-axis location type (e.g., xloc.bar_index).

_colorBG (color) : color Background color for the box.

_colorBD (color) : color Border color for the box.

@return box Returns the created box object.

Addline(_x, _y, _xloc, _color, _width)

Addline

@description Draw a vertical or horizontal line at specified coordinates.

Parameters:

_x (int) : int X-coordinate for start (bar index).

_y (int) : float Y-coordinate for start (price).

_xloc (string) : string X-axis location type (e.g., xloc.bar_index).

_color (color) : color Line color.

_width (int) : int Line width.

@return line Returns the created line object.

Addline(_x, _y, _xloc, _color, _width)

Parameters:

_x (int)

_y (float)

_xloc (string)

_color (color)

_width (int)

Addline(_x1, _y1, _x2, _y2, _xloc, _color, _width)

Parameters:

_x1 (int)

_y1 (int)

_x2 (int)

_y2 (int)

_xloc (string)

_color (color)

_width (int)

Addline(_x1, _y1, _x2, _y2, _xloc, _color, _width)

Parameters:

_x1 (int)

_y1 (int)

_x2 (int)

_y2 (float)

_xloc (string)

_color (color)

_width (int)

Addline(_x1, _y1, _x2, _y2, _xloc, _color, _width)

Parameters:

_x1 (int)

_y1 (float)

_x2 (int)

_y2 (int)

_xloc (string)

_color (color)

_width (int)

Addline(_x1, _y1, _x2, _y2, _xloc, _color, _width)

Parameters:

_x1 (int)

_y1 (float)

_x2 (int)

_y2 (float)

_xloc (string)

_color (color)

_width (int)

AddlineMid(_type, _left, _right, _top, _bot, _xloc, _color, _width)

AddlineMid

@description Draw a midline between top and bottom for FVG or FOB types.

Parameters:

_type (string) : string Type identifier: "fvg" or "fob".

_left (int) : int Left bar index for midline start.

_right (int) : int Right bar index for midline end.

_top (float) : float Top price of the region.

_bot (float) : float Bottom price of the region.

_xloc (string) : string X-axis location type (e.g., xloc.bar_index).

_color (color) : color Line color.

_width (int) : int Line width.

@return line or na Returns the created line or na if type is not recognized.

GetHtfFromLabel(_label)

GetHtfFromLabel

@description Convert a Korean HTF label into a Pine Script timeframe string via handler library.

Parameters:

_label (string) : string The Korean label (e.g., "5분", "1시간").

@return string Returns the corresponding Pine Script timeframe (e.g., "5", "60").

IsChartTFcomparisonHTF(_chartTf, _htfTf)

IsChartTFcomparisonHTF

@description Determine whether a given HTF is greater than or equal to the current chart timeframe.

Parameters:

_chartTf (string) : string Current chart timeframe (e.g., "5", "15", "1D").

_htfTf (string) : string HTF timeframe (e.g., "60", "1D").

@return bool True if HTF ≥ chartTF, false otherwise.

CreateBoxData(_type, _isBull, _useLine, _top, _bot, _xloc, _colorBG, _colorBD, _offset, _htfTf, htfBarIdx, _basePoint)

CreateBoxData

@description Create and draw a box and optional midline for given type and parameters. Returns success flag and BoxData.

Parameters:

_type (string) : string Type identifier: "fvg", "fob", "cob", or "sweep".

_isBull (bool) : bool Direction flag: true for bullish, false for bearish.

_useLine (bool) : bool Whether to draw a midline inside the box.

_top (float) : float Top price of the box region.

_bot (float) : float Bottom price of the box region.

_xloc (string) : string X-axis location type (e.g., xloc.bar_index).

_colorBG (color) : color Background color for the box.

_colorBD (color) : color Border color for the box.

_offset (int) : int HTF bar offset (0 means current HTF bar).

_htfTf (string) : string HTF timeframe string (e.g., "60", "1D").

htfBarIdx (int) : int HTF bar_index (passed from HTF request).

_basePoint (float) : float Base point for breakout checks.

@return tuple(bool, BoxData) Returns a boolean indicating success and the created BoxData struct.

ProcessBoxDatas(_datas, _useMidLine, _closeCount, _colorClose)

ProcessBoxDatas

@description Process an array of BoxData structs: extend, record volume, update stage, and finalize boxes.

Parameters:

_datas (array) : array Array of BoxData objects to process.

_useMidLine (bool) : bool Whether to update the midline endpoint.

_closeCount (int) : int Number of touches required to close the box.

_colorClose (color) : color Color to apply when a box closes.

@return void No return value; updates are in-place.

BoxData

Fields:

_isActive (series bool)

_isBull (series bool)

_box (series box)

_line (series line)

_basePoint (series float)

_boxTop (series float)

_boxBot (series float)

_stage (series int)

_isStay (series bool)

_volBuy (series float)

_volSell (series float)

_result (series string)

LineData

Fields:

_isActive (series bool)

_isBull (series bool)

_line (series line)

_basePoint (series float)

_stage (series int)

_isStay (series bool)

_result (series string)

MirPapa_Handler_HTFLibrary "MirPapa_Handler_HTF"

High Time Frame Handler Library:

Provides utilities for working with High Time Frame (HTF) and chart (LTF) conversions and data retrieval.

IsChartTFcomparisonHTF(_chartTf, _htfTf)

IsChartTFcomparisonHTF

@description

Determine whether the given High Time Frame (HTF) is greater than or equal to the current chart timeframe.

Parameters:

_chartTf (string) : The current chart’s timeframe string (examples: "5", "15", "1D").

_htfTf (string) : The High Time Frame string to compare (examples: "60", "1D").

@return

Returns true if HTF minutes ≥ chart minutes, false otherwise or na if conversion fails.

GetHTFrevised(_tf, _case)

GetHTFrevised

@description

Retrieve a specific bar value from a Higher Time Frame (HTF) series.

Supports current and historical OHLC values, based on a case identifier.

Parameters:

_tf (string) : The target HTF string (examples: "60", "1D").

_case (string) : A case string determining which OHLC value and bar offset to request:

"b" → HTF bar_index

"o" → HTF open

"h" → HTF high

"l" → HTF low

"c" → HTF close

"o1" → HTF open one bar ago

"h1" → HTF high one bar ago

"l1" → HTF low one bar ago

"c1" → HTF close one bar ago

… up to "o5", "h5", "l5", "c5" for five bars ago.

@return

Returns the requested HTF value or na if _case does not match any condition.

GetHTFfromLabel(_label)

GetHTFfromLabel

@description

Convert a Korean HTF label into a Pine Script-recognizable timeframe string.

Examples:

"5분" → "5"

"1시간" → "60"

"일봉" → "1D"

"주봉" → "1W"

"월봉" → "1M"

"연봉" → "12M"

Parameters:

_label (string) : The Korean HTF label string (examples: "5분", "1시간", "일봉").

@return

Returns the Pine Script timeframe string corresponding to the label, or "1W" if no match is found.

GetHTFoffsetToLTFoffset(_offset, _chartTf, _htfTf)

GetHTFoffsetToLTFoffset

@description

Adjust an HTF bar index and offset so that it aligns with the current chart’s bar index.

Useful for retrieving historical HTF data on an LTF chart.

Parameters:

_offset (int) : The HTF bar offset (0 means current HTF bar, 1 means one bar ago, etc.).

_chartTf (string) : The current chart’s timeframe string (examples: "5", "15", "1D").

_htfTf (string) : The High Time Frame string to align (examples: "60", "1D").

@return

Returns the corresponding LTF bar index after applying HTF offset. If result is negative, returns 0.

NY Opening Range Breakout - MA StopCore Concept

This strategy trades breakouts from the New York opening range (9:30-9:45 AM NY time) on intraday timeframes, designed for scalping and day trading.

Setup Requirements

Timeframe: Works on any timeframe under 15 minutes (1m, 2m, 3m, 5m, 10m)

Session: New York market hours

Range Period: 9:30-9:45 AM NY time (15-minute opening range)

Entry Rules

Long Entries:

Wait for a candle to close above the opening range high

Enter long on the next candle (before 12:00 PM NY time)

Must be above moving average if using MA-based take profit

Short Entries:

Wait for a candle to close below the opening range low

Enter short on the next candle (before 12:00 PM NY time)

Must be below moving average if using MA-based take profit

Risk Management

Stop Loss:

Long trades: Opening range low

Short trades: Opening range high

Take Profit Options:

Fixed Risk Reward: 1.5x the range size (customizable ratio)

Moving Average: Exit when price crosses back through MA

Both: Whichever comes first

Key Features

Trade Direction Options:

Long Only

Short Only

Both directions

Moving Average Filter:

Prevents entries that would immediately hit stop loss

Uses EMA/SMA/WMA/VWMA with customizable length

Acts as dynamic support/resistance

Time Restrictions:

No entries after 12:00 PM NY time (customizable cutoff)

One trade per direction per day

Daily reset of all variables

Visual Elements

Red/green lines showing opening range

Purple line for moving average

Entry and breakout signals with shapes

Take profit and stop loss levels plotted

Information table with current status

Strategy Logic Flow

Morning: Capture 9:30-9:45 range high/low

Wait: Monitor for breakout (previous candle close outside range)

Filter: Check MA condition if using MA-based exits

Enter: Trade on next candle after breakout

Manage: Exit at fixed TP, MA cross, or stop loss

Reset: Start fresh next trading day

This is a momentum-based breakout strategy that capitalizes on early market volatility while using the opening range as natural support/resistance levels.

Consolidation Range [BigBeluga]A hybrid volatility-volume indicator that isolates periods of price equilibrium and reveals the directional force behind each range buildup.

Consolidation Range is a powerful tool designed to detect compression phases in the market using volatility thresholds while visualizing volume imbalance within those phases. By combining low-volatility detection with directional volume delta, it highlights where accumulation or distribution is occurring—giving traders the confidence to act when breakouts follow. This indicator is particularly valuable in choppy or sideways markets where range identification and sentiment context are key.

🔵 CONCEPTS

Volatility Compression: Uses ADX (Average Directional Index) to detect periods of low trend strength—specifically when ADX drops below a configurable threshold.

Range Structure: Upon a low-volatility trigger, the script dynamically anchors horizontal upper and lower bounds based on local highs and lows.

Directional Volume Delta: Inside each active range, it calculates the net difference between buy and sell volume, showing who controlled the range.

Sentiment Bias: A label appears in the center of the zone on breakout, showing the accumulated delta and bias direction (▲ for positive, ▼ for negative).

Range Validity Filter: Only ranges with more than 15 bars are considered valid—short-lived consolidations are auto-filtered.

🔵 KEY FEATURES

Detects low volatility market phases using ADX logic (crosses under "Volatility Threshold Input").

Automatically plots adaptive consolidation zones with upper and lower boundary lines.

Includes dynamic midline to visualize the price average inside the range.

Visual range is filled with a progressive gradient to reflect distance between highs and lows.

When the range is active, the indicator accumulates volume delta (Buy - Sell volume) .

Upon breakout, the total volume delta is displayed at the midpoint , providing insight into market sentiment during the consolidation phase.

Filters out weak or short-lived consolidations under 15 bars.

🔵 HOW TO USE

Spot ranging or compression zones with minimal effort.

Use breakouts with volume delta bias to assess the strength or weakness of moves.

Combine with trend-following tools or volume-based confirmation for stronger setups.

Apply to higher timeframes for macro consolidation tracking .

🔵 CONCLUSION

Consolidation Range now brings together volatility filtering and directional volume delta into one smart module. This hybrid logic allows traders to not only identify balance zones but also understand who was in control during the buildup—offering a sharper edge for breakout and trend continuation strategies.

Anchored VWAP by Time (Math by Thomas)📄 Description

This tool lets you plot an Anchored Volume Weighted Average Price (VWAP) starting from any specific date and time you choose. Unlike standard VWAPs that reset daily or weekly, this version gives you full control to track institutional pricing zones from precise anchor points—such as key swing highs/lows, market open, or news-driven candles.

It’s especially useful for price action and Smart Money Concepts (SMC) traders who track liquidity, fair value gaps (FVGs), and institutional zones.

🇮🇳 For NSE India Traders

You can anchor VWAP to Indian market open (e.g., 9:15 AM IST) or major events like RBI policy, earnings, or breakout candles.

The time input uses UTC by default, so for Indian Standard Time (IST), remember:

9:15 AM IST = 3:45 AM UTC

3:30 PM IST = 10:00 AM UTC

⚙️ How to Use

Add the indicator to your chart.

Open the settings panel.

Under “Anchor Start Time”, choose the date & time to begin the VWAP.

Use UTC format (adjust from IST if needed).

Customize the line color and thickness to suit your chart style.

The VWAP will begin plotting from that time forward.

🔎 Best Use Cases

Track VWAP from intraday range breakouts

Anchor from swing highs/lows to identify mean reversion zones

Combine with your FVGs, Order Blocks, or CHoCHs

Monitor VWAP reactions during key macro events or expiry days

🔧 Clean Design

No labels are used, keeping your chart clean.

Works on all timeframes (1min to Daily).

Designed for serious intraday & positional traders.

Ultimate Scalping Tool[BullByte]Overview

The Ultimate Scalping Tool is an open-source TradingView indicator built for scalpers and short-term traders released under the Mozilla Public License 2.0. It uses a custom Quantum Flux Candle (QFC) oscillator to combine multiple market forces into one visual signal. In plain terms, the script reads momentum, trend strength, volatility, and volume together and plots a special “candlestick” each bar (the QFC) that reflects the overall market bias. This unified view makes it easier to spot entries and exits: the tool labels signals as Strong Buy/Sell, Pullback (a brief retracement in a trend), Early Entry, or Exit Warning . It also provides color-coded alerts and a small dashboard of metrics. In practice, traders see green/red oscillator bars and symbols on the chart when conditions align, helping them scalp or trend-follow without reading multiple separate indicators.

Core Components

Quantum Flux Candle (QFC) Construction

The QFC is the heart of the indicator. Rather than using raw price, it creates a candlestick-like bar from the underlying oscillator values. Each QFC bar has an “open,” “high/low,” and “close” derived from calculated momentum and volatility inputs for that period . In effect, this turns the oscillator into intuitive candle patterns so traders can recognize momentum shifts visually. (For comparison, note that Heikin-Ashi candles “have a smoother look because take an average of the movement”. The QFC instead represents exact oscillator readings, so it reflects true momentum changes without hiding price action.) Colors of QFC bars change dynamically (e.g. green for bullish momentum, red for bearish) to highlight shifts. This is the first open-source QFC oscillator that dynamically weights four non-correlated indicators with moving thresholds, which makes it a unique indicator on its own.

Oscillator Normalization & Adaptive Weights

The script normalizes its oscillator to a fixed scale (for example, a 0–100 range much like the RSI) so that various inputs can be compared fairly. It then applies adaptive weighting: the relative influence of trend, momentum, volatility or volume signals is automatically adjusted based on current market conditions. For instance, in very volatile markets the script might weight volatility more heavily, or in a strong trend it might give extra weight to trend direction. Normalizing data and adjusting weights helps keep the QFC sensitive but stable (normalization ensures all inputs fit a common scale).

Trend/Momentum/Volume/Volatility Fusion

Unlike a typical single-factor oscillator, the QFC oscillator fuses four aspects at once. It may compute, for example, a trend indicator (such as an ADX or moving average slope), a momentum measure (like RSI or Rate-of-Change), a volume-based pressure (similar to MFI/OBV), and a volatility measure (like ATR) . These different values are combined into one composite oscillator. This “multi-dimensional” approach follows best practices of using non-correlated indicators (trend, momentum, volume, volatility) for confirmation. By encoding all these signals in one line, a high QFC reading means that trend, momentum, and volume are all aligned, whereas a neutral reading might mean mixed conditions. This gives traders a comprehensive picture of market strength.

Signal Classification

The script interprets the QFC oscillator to label trades. For example:

• Strong Buy/Sell : Triggered when the oscillator crosses a high-confidence threshold (e.g. breaks clearly above zero with strong slope), indicating a well-confirmed move. This is like seeing a big green/red QFC candle aligned with the trend.

• Pullbacks : Identified when the trend is up but momentum dips briefly. A Pullback Buy appears if the overall trend is bullish but the oscillator has a short retracement – a typical buying opportunity in an uptrend. (A pullback is “a brief decline or pause in a generally upward price trend”.)

• Early Buy/Sell : Marks an initial swing in the oscillator suggesting a possible new trend, before it is fully confirmed. It’s a hint of momentum building (an early-warning signal), not as strong as the confirmed “Strong” signal.

• Exit Warnings : Issued when momentum peaks or reverses. For instance, if the QFC bars reach a high and start turning red/green opposite, the indicator warns that the move may be ending. In other words, a Momentum Peak is the point of maximum strength after which weakness may follow.

These categories correspond to typical trading concepts: Pullback (temporary reversal in an uptrend), Early Buy (an initial bullish cross), Strong Buy (confirmed bullish momentum), and Momentum Peak (peak oscillator value suggesting exhaustion).

Filters (DI Reversal, Dynamic Thresholds, HTF EMA/ADX)

Extra filters help avoid bad trades. A DI Reversal filter uses the +DI/–DI lines (from the ADX system) to require that the trend direction confirms the signal . For example, it might ignore a buy signal if the +DI is still below –DI. Dynamic Thresholds adjust signal levels on-the-fly: rather than fixed “overbought” lines, they move with volatility so signals happen under appropriate market stress. An optional High-Timeframe EMA or ADX filter adds a check against a larger timeframe trend: for instance, only taking a trade if price is above the weekly EMA or if weekly ADX shows a strong trend. (Notably, the ADX is “a technical indicator used by traders to determine the strength of a price trend”, so requiring a high-timeframe ADX avoids trading against the bigger trend.)

Dashboard Metrics & Color Logic

The Dashboard in the Ultimate Scalping Tool (UST) serves as a centralized information hub, providing traders with real-time insights into market conditions, trend strength, momentum, volume pressure, and trade signals. It is highly customizable, allowing users to adjust its appearance and content based on their preferences.

1. Dashboard Layout & Customization

Short vs. Extended Mode : Users can toggle between a compact view (9 rows) and an extended view (13 rows) via the `Short Dashboard` input.

Text Size Options : The dashboard supports three text sizes— Tiny, Small, and Normal —adjustable via the `Dashboard Text Size` input.

Positioning : The dashboard is positioned in the top-right corner by default but can be moved if modified in the script.

2. Key Metrics Displayed

The dashboard presents critical trading metrics in a structured table format:

Trend (TF) : Indicates the current trend direction (Strong Bullish, Moderate Bullish, Sideways, Moderate Bearish, Strong Bearish) based on normalized trend strength (normTrend) .

Momentum (TF) : Displays momentum status (Strong Bullish/Bearish or Neutral) derived from the oscillator's position relative to dynamic thresholds.

Volume (CMF) : Shows buying/selling pressure levels (Very High Buying, High Selling, Neutral, etc.) based on the Chaikin Money Flow (CMF) indicator.

Basic & Advanced Signals:

Basic Signal : Provides simple trade signals (Strong Buy, Strong Sell, Pullback Buy, Pullback Sell, No Trade).

Advanced Signal : Offers nuanced signals (Early Buy/Sell, Momentum Peak, Weakening Momentum, etc.) with color-coded alerts.

RSI : Displays the Relative Strength Index (RSI) value, colored based on overbought (>70), oversold (<30), or neutral conditions.

HTF Filter : Indicates the higher timeframe trend status (Bullish, Bearish, Neutral) when using the Leading HTF Filter.

VWAP : Shows the V olume-Weighted Average Price and whether the current price is above (bullish) or below (bearish) it.

ADX : Displays the Average Directional Index (ADX) value, with color highlighting whether it is rising (green) or falling (red).

Market Mode : Shows the selected market type (Crypto, Stocks, Options, Forex, Custom).

Regime : Indicates volatility conditions (High, Low, Moderate) based on the **ATR ratio**.

3. Filters Status Panel

A secondary panel displays the status of active filters, helping traders quickly assess which conditions are influencing signals:

- DI Reversal Filter: On/Off (confirms reversals before generating signals).

- Dynamic Thresholds: On/Off (adjusts buy/sell thresholds based on volatility).

- Adaptive Weighting: On/Off (auto-adjusts oscillator weights for trend/momentum/volatility).

- Early Signal: On/Off (enables early momentum-based signals).

- Leading HTF Filter: On/Off (applies higher timeframe trend confirmation).

4. Visual Enhancements

Color-Coded Cells : Each metric is color-coded (green for bullish, red for bearish, gray for neutral) for quick interpretation.

Dynamic Background : The dashboard background adapts to market conditions (bullish/bearish/neutral) based on ADX and DI trends.

Customizable Reference Lines : Users can enable/disable fixed reference lines for the oscillator.

How It(QFC) Differs from Traditional Indicators

Quantum Flux Candle (QFC) Versus Heikin-Ashi

Heikin-Ashi candles smooth price by averaging (HA’s open/close use averages) so they show trend clearly but hide true price (the current HA bar’s close is not the real price). QFC candles are different: they are oscillator values, not price averages . A Heikin-Ashi chart “has a smoother look because it is essentially taking an average of the movement”, which can cause lag. The QFC instead shows the raw combined momentum each bar, allowing faster recognition of shifts. In short, HA is a smoothed price chart; QFC is a momentum-based chart.

Versus Standard Oscillators

Common oscillators like RSI or MACD use fixed formulas on price (or price+volume). For example, RSI “compares gains and losses and normalizes this value on a scale from 0 to 100”, reflecting pure price momentum. MFI is similar but adds volume. These indicators each show one dimension: momentum or volume. The Ultimate Scalping Tool’s QFC goes further by integrating trend strength and volatility too. In practice, this means a move that looks strong on RSI might be downplayed by low volume or weak trend in QFC. As one source notes, using multiple non-correlated indicators (trend, momentum, volume, volatility) provides a more complete market picture. The QFC’s multi-factor fusion is unique – it is effectively a multi-dimensional oscillator rather than a traditional single-input one.

Signal Style

Traditional oscillators often use crossovers (RSI crossing 50) or fixed zones (MACD above zero) for signals. The Ultimate Scalping Tool’s signals are custom-classified: it explicitly labels pullbacks, early entries, and strong moves. These terms go beyond a typical indicator’s generic “buy”/“sell.” In other words, it packages a strategy around the oscillator, which traders can backtest or observe without reading code.

Key Term Definitions

• Pullback : A short-term dip or consolidation in an uptrend. In this script, a Pullback Buy appears when price is generally rising but shows a brief retracement. (As defined by Investopedia, a pullback is “a brief decline or pause in a generally upward price trend”.)

• Early Buy/Sell : An initial or tentative entry signal. It means the oscillator first starts turning positive (or negative) before a full trend has developed. It’s an early indication that a trend might be starting.

• Strong Buy/Sell : A confident entry signal when multiple conditions align. This label is used when momentum is already strong and confirmed by trend/volume filters, offering a higher-probability trade.

• Momentum Peak : The point where bullish (or bearish) momentum reaches its maximum before weakening. When the oscillator value stops rising (or falling) and begins to reverse, the script flags it as a peak – signaling that the current move could be overextended.

What is the Flux MA?

The Flux MA (Moving Average) is an Exponential Moving Average (EMA) applied to a normalized oscillator, referred to as FM . Its purpose is to smooth out the fluctuations of the oscillator, providing a clearer picture of the underlying trend direction and strength. Think of it as a dynamic baseline that the oscillator moves above or below, helping you determine whether the market is trending bullish or bearish.

How it’s calculated (Flux MA):

1.The oscillator is normalized (scaled to a range, typically between 0 and 1, using a default scale factor of 100.0).

2.An EMA is applied to this normalized value (FM) over a user-defined period (default is 10 periods).

3.The result is rescaled back to the oscillator’s original range for plotting.

Why it matters : The Flux MA acts like a support or resistance level for the oscillator, making it easier to spot trend shifts.

Color of the Flux Candle

The Quantum Flux Candle visualizes the normalized oscillator (FM) as candlesticks, with colors that indicate specific market conditions based on the relationship between the FM and the Flux MA. Here’s what each color means:

• Green : The FM is above the Flux MA, signaling bullish momentum. This suggests the market is trending upward.

• Red : The FM is below the Flux MA, signaling bearish momentum. This suggests the market is trending downward.

• Yellow : Indicates strong buy conditions (e.g., a "Strong Buy" signal combined with a positive trend). This is a high-confidence signal to go long.

• Purple : Indicates strong sell conditions (e.g., a "Strong Sell" signal combined with a negative trend). This is a high-confidence signal to go short.

The candle mode shows the oscillator’s open, high, low, and close values for each period, similar to price candlesticks, but it’s the color that provides the quick visual cue for trading decisions.

How to Trade the Flux MA with Respect to the Candle

Trading with the Flux MA and Quantum Flux Candle involves using the MA as a trend indicator and the candle colors as entry and exit signals. Here’s a step-by-step guide:

1. Identify the Trend Direction

• Bullish Trend : The Flux Candle is green and positioned above the Flux MA. This indicates upward momentum.

• Bearish Trend : The Flux Candle is red and positioned below the Flux MA. This indicates downward momentum.

The Flux MA serves as the reference line—candles above it suggest buying pressure, while candles below it suggest selling pressure.

2. Interpret Candle Colors for Trade Signals

• Green Candle : General bullish momentum. Consider entering or holding a long position.

• Red Candle : General bearish momentum. Consider entering or holding a short position.

• Yellow Candle : A strong buy signal. This is an ideal time to enter a long trade.

• Purple Candle : A strong sell signal. This is an ideal time to enter a short trade.

3. Enter Trades Based on Crossovers and Colors

• Long Entry : Enter a buy position when the Flux Candle turns green and crosses above the Flux MA. If it turns yellow, this is an even stronger signal to go long.

• Short Entry : Enter a sell position when the Flux Candle turns red and crosses below the Flux MA. If it turns purple, this is an even stronger signal to go short.

4. Exit Trades

• Exit Long : Close your buy position when the Flux Candle turns red or crosses below the Flux MA, indicating the bullish trend may be reversing.

• Exit Short : Close your sell position when the Flux Candle turns green or crosses above the Flux MA, indicating the bearish trend may be reversing.

•You might also exit a long trade if the candle changes from yellow to green (weakening strong buy signal) or a short trade from purple to red (weakening strong sell signal).

5. Use Additional Confirmation

To avoid false signals, combine the Flux MA and candle signals with other indicators or dashboard metrics (e.g., trend strength, momentum, or volume pressure). For example:

•A yellow candle with a " Strong Bullish " trend and high buying volume is a robust long signal.

•A red candle with a " Moderate Bearish " trend and neutral momentum might need more confirmation before shorting.

Practical Example

Imagine you’re scalping a cryptocurrency:

• Long Trade : The Flux Candle turns yellow and is above the Flux MA, with the dashboard showing "Strong Buy" and high buying volume. You enter a long position. You exit when the candle turns red and dips below the Flux MA.

• Short Trade : The Flux Candle turns purple and crosses below the Flux MA, with a "Strong Sell" signal on the dashboard. You enter a short position. You exit when the candle turns green and crosses above the Flux MA.

Market Presets and Adaptation

This indicator is designed to work on any market with candlestick price data (stocks, crypto, forex, indices, etc.). To handle different behavior, it provides presets for major asset classes. Selecting a “Stocks,” “Crypto,” “Forex,” or “Options” preset automatically loads a set of parameter values optimized for that market . For example, a crypto preset might use a shorter lookback or higher sensitivity to account for crypto’s high volatility, while a stocks preset might use slightly longer smoothing since stocks often trend more slowly. In practice, this means the same core QFC logic applies across markets, but the thresholds and smoothing adjust so signals remain relevant for each asset type.

Usage Guidelines

• Recommended Timeframes : Optimized for 1 minute to 15 minute intraday charts. Can also be used on higher timeframes for short term swings.

• Market Types : Select “Crypto,” “Stocks,” “Forex,” or “Options” to auto tune periods, thresholds and weights. Use “Custom” to manually adjust all inputs.

• Interpreting Signals : Always confirm a signal by checking that trend, volume, and VWAP agree on the dashboard. A green “Strong Buy” arrow with green trend, green volume, and price > VWAP is highest probability.

• Adjusting Sensitivity : To reduce false signals in fast markets, enable DI Reversal Confirmation and Dynamic Thresholds. For more frequent entries in trending environments, enable Early Entry Trigger.

• Risk Management : This tool does not plot stop loss or take profit levels. Users should define their own risk parameters based on support/resistance or volatility bands.

Background Shading

To give you an at-a-glance sense of market regime without reading numbers, the indicator automatically tints the chart background in three modes—neutral, bullish and bearish—with two levels of intensity (light vs. dark):

Neutral (Gray)

When ADX is below 20 the market is considered “no trend” or too weak to trade. The background fills with a light gray (high transparency) so you know to sit on your hands.

Bullish (Green)

As soon as ADX rises above 20 and +DI exceeds –DI, the background turns a semi-transparent green, signaling an emerging uptrend. When ADX climbs above 30 (strong trend), the green becomes more opaque—reminding you that trend-following signals (Strong Buy, Pullback) carry extra weight.

Bearish (Red)

Similarly, if –DI exceeds +DI with ADX >20, you get a light red tint for a developing downtrend, and a darker, more solid red once ADX surpasses 30.

By dynamically varying both hue (green vs. red vs. gray) and opacity (light vs. dark), the background instantly communicates trend strength and direction—so you always know whether to favor breakout-style entries (in a strong trend) or stay flat during choppy, low-ADX conditions.

The setup shown in the above chart snapshot is BTCUSD 15 min chart : Binance for reference.

Disclaimer

No indicator guarantees profits. Backtest or paper trade this tool to understand its behavior in your market. Always use proper position sizing and stop loss orders.

Good luck!

- BullByte

Candle % High/Low Bar + HL Order + MA by Barty&PitPapcioWhat does the indicator show?

The "Candle % High/Low Bar + HL Order + MA by Barty&PitPapcio" indicator displays the percentage deviation of each candle’s high and low relative to its open price. The zero line represents the candle’s open — bars above zero show upward movement from the open (to high), bars below zero show downward movement (to low).

Additionally, the indicator plots a dot above or below each bar indicating which came first during the candle — the high or the low — based on data from a lower timeframe two steps below the current chart (for example, on a 1-hour chart it uses 15-minute data).

Finally, the indicator calculates and plots a user-selectable moving average (EMA, SMA, or WMA) of these "first high or low" signals, helping identify trends whether the first move is more often upwards or downwards.

Where do the data come from?

Percentage values are calculated directly from the current chart’s candles:

highPerc=(High−Open)/Open×100%,

lowPerc=(Low−Open)/Open×100%

The timing of the first high or low for each candle is retrieved from a lower timeframe, stepping down two levels from the current timeframe (e.g. from 1H to 15 min), providing better precision in detecting the order of highs and lows that may be blurred on higher timeframes.

Additional features:

Full customization of colors for bars, dots, zero line, grid, and thicknesses.

Background grid with adjustable scale and style.

Safety checks for missing lower timeframe data.

A moving average smoothing the sequence of first high/low signals to reveal directional tendencies.

Suggested strategy for technical analysis support

Identify dominant candle direction: If the dot often appears above the bar (first high), it indicates buying pressure; if below (first low), selling pressure dominates.

Use percentage deviations: Large percent bars indicate heightened volatility and potential reversal points.

Moving average on order signals: The EMA of high/low first signals smooths the noise, showing the dominant trend in the sequence of price moves, useful for filtering other signals.

Combine with other tools: This indicator can act as a directional filter on multiple timeframes, synergizing well with momentum indicators, RSI, or support/resistance levels to confirm move strength.

Lots of love, Bartosz

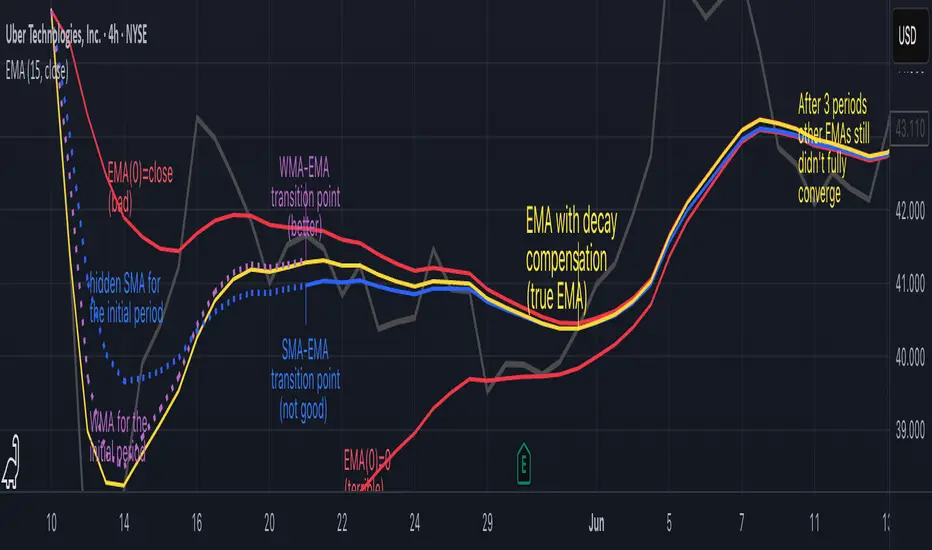

Why EMA Isn't What You Think It IsMany new traders adopt the Exponential Moving Average (EMA) believing it's simply a "better Simple Moving Average (SMA)". This common misconception leads to fundamental misunderstandings about how EMA works and when to use it.

EMA and SMA differ at their core. SMA use a window of finite number of data points, giving equal weight to each data point in the calculation period. This makes SMA a Finite Impulse Response (FIR) filter in signal processing terms. Remember that FIR means that "all that we need is the 'period' number of data points" to calculate the filter value. Anything beyond the given period is not relevant to FIR filters – much like how a security camera with 14-day storage automatically overwrites older footage, making last month's activity completely invisible regardless of how important it might have been.

EMA, however, is an Infinite Impulse Response (IIR) filter. It uses ALL historical data, with each past price having a diminishing - but never zero - influence on the calculated value. This creates an EMA response that extends infinitely into the past—not just for the last N periods. IIR filters cannot be precise if we give them only a 'period' number of data to work on - they will be off-target significantly due to lack of context, like trying to understand Game of Thrones by watching only the final season and wondering why everyone's so upset about that dragon lady going full pyromaniac.

If we only consider a number of data points equal to the EMA's period, we are capturing no more than 86.5% of the total weight of the EMA calculation. Relying on he period window alone (the warm-up period) will provide only 1 - (1 / e^2) weights, which is approximately 1−0.1353 = 0.8647 = 86.5%. That's like claiming you've read a book when you've skipped the first few chapters – technically, you got most of it, but you probably miss some crucial early context.

▶️ What is period in EMA used for?

What does a period parameter really mean for EMA? When we select a 15-period EMA, we're not selecting a window of 15 data points as with an SMA. Instead, we are using that number to calculate a decay factor (α) that determines how quickly older data loses influence in EMA result. Every trader knows EMA calculation: α = 1 / (1+period) – or at least every trader claims to know this while secretly checking the formula when they need it.

Thinking in terms of "period" seriously restricts EMA. The α parameter can be - should be! - any value between 0.0 and 1.0, offering infinite tuning possibilities of the indicator. When we limit ourselves to whole-number periods that we use in FIR indicators, we can only access a small subset of possible IIR calculations – it's like having access to the entire RGB color spectrum with 16.7 million possible colors but stubbornly sticking to the 8 basic crayons in a child's first art set because the coloring book only mentioned those by name.

For example:

Period 10 → alpha = 0.1818

Period 11 → alpha = 0.1667

What about wanting an alpha of 0.17, which might yield superior returns in your strategy that uses EMA? No whole-number period can provide this! Direct α parameterization offers more precision, much like how an analog tuner lets you find the perfect radio frequency while digital presets force you to choose only from predetermined stations, potentially missing the clearest signal sitting right between channels.

Sidenote: the choice of α = 1 / (1+period) is just a convention from 1970s, probably started by J. Welles Wilder, who popularized the use of the 14-day EMA. It was designed to create an approximate equivalence between EMA and SMA over the same number of periods, even thought SMA needs a period window (as it is FIR filter) and EMA doesn't. In reality, the decay factor α in EMA should be allowed any valye between 0.0 and 1.0, not just some discrete values derived from an integer-based period! Algorithmic systems should find the best α decay for EMA directly, allowing the system to fine-tune at will and not through conversion of integer period to float α decay – though this might put a few traditionalist traders into early retirement. Well, to prevent that, most traditionalist implementations of EMA only use period and no alpha at all. Heaven forbid we disturb people who print their charts on paper, draw trendlines with rulers, and insist the market "feels different" since computers do algotrading!

▶️ Calculating EMAs Efficiently

The standard textbook formula for EMA is:

EMA = CurrentPrice × alpha + PreviousEMA × (1 - alpha)

But did you know that a more efficient version exists, once you apply a tiny bit of high school algebra:

EMA = alpha × (CurrentPrice - PreviousEMA) + PreviousEMA

The first one requires three operations: 2 multiplications + 1 addition. The second one also requires three ops: 1 multiplication + 1 addition + 1 subtraction.

That's pathetic, you say? Not worth implementing? In most computational models, multiplications cost much more than additions/subtractions – much like how ordering dessert costs more than asking for a water refill at restaurants.

Relative CPU cost of float operations :

Addition/Subtraction: ~1 cycle

Multiplication: ~5 cycles (depending on precision and architecture)

Now you see the difference? 2 * 5 + 1 = 11 against 5 + 1 + 1 = 7. That is ≈ 36.36% efficiency gain just by swapping formulas around! And making your high school math teacher proud enough to finally put your test on the refrigerator.

▶️ The Warmup Problem: how to start the EMA sequence right

How do we calculate the first EMA value when there's no previous EMA available? Let's see some possible options used throughout the history:

Start with zero : EMA(0) = 0. This creates stupidly large distortion until enough bars pass for the horrible effect to diminish – like starting a trading account with zero balance but backdating a year of missed trades, then watching your balance struggle to climb out of a phantom debt for months.

Start with first price : EMA(0) = first price. This is better than starting with zero, but still causes initial distortion that will be extra-bad if the first price is an outlier – like forming your entire opinion of a stock based solely on its IPO day price, then wondering why your model is tanking for weeks afterward.

Use SMA for warmup : This is the tradition from the pencil-and-paper era of technical analysis – when calculators were luxury items and "algorithmic trading" meant your broker had neat handwriting. We first calculate an SMA over the initial period, then kickstart the EMA with this average value. It's widely used due to tradition, not merit, creating a mathematical Frankenstein that uses an FIR filter (SMA) during the initial period before abruptly switching to an IIR filter (EMA). This methodology is so aesthetically offensive (abrupt kink on the transition from SMA to EMA) that charting platforms hide these early values entirely, pretending EMA simply doesn't exist until the warmup period passes – the technical analysis equivalent of sweeping dust under the rug.

Use WMA for warmup : This one was never popular because it is harder to calculate with a pencil - compared to using simple SMA for warmup. Weighted Moving Average provides a much better approximation of a starting value as its linear descending profile is much closer to the EMA's decay profile.

These methods all share one problem: they produce inaccurate initial values that traders often hide or discard, much like how hedge funds conveniently report awesome performance "since strategy inception" only after their disastrous first quarter has been surgically removed from the track record.

▶️ A Better Way to start EMA: Decaying compensation

Think of it this way: An ideal EMA uses an infinite history of prices, but we only have data starting from a specific point. This creates a problem - our EMA starts with an incorrect assumption that all previous prices were all zero, all close, or all average – like trying to write someone's biography but only having information about their life since last Tuesday.

But there is a better way. It requires more than high school math comprehension and is more computationally intensive, but is mathematically correct and numerically stable. This approach involves compensating calculated EMA values for the "phantom data" that would have existed before our first price point.

Here's how phantom data compensation works:

We start our normal EMA calculation:

EMA_today = EMA_yesterday + α × (Price_today - EMA_yesterday)

But we add a correction factor that adjusts for the missing history:

Correction = 1 at the start

Correction = Correction × (1-α) after each calculation

We then apply this correction:

True_EMA = Raw_EMA / (1-Correction)

This correction factor starts at 1 (full compensation effect) and gets exponentially smaller with each new price bar. After enough data points, the correction becomes so small (i.e., below 0.0000000001) that we can stop applying it as it is no longer relevant.

Let's see how this works in practice:

For the first price bar:

Raw_EMA = 0

Correction = 1

True_EMA = Price (since 0 ÷ (1-1) is undefined, we use the first price)

For the second price bar:

Raw_EMA = α × (Price_2 - 0) + 0 = α × Price_2

Correction = 1 × (1-α) = (1-α)

True_EMA = α × Price_2 ÷ (1-(1-α)) = Price_2

For the third price bar:

Raw_EMA updates using the standard formula

Correction = (1-α) × (1-α) = (1-α)²

True_EMA = Raw_EMA ÷ (1-(1-α)²)

With each new price, the correction factor shrinks exponentially. After about -log₁₀(1e-10)/log₁₀(1-α) bars, the correction becomes negligible, and our EMA calculation matches what we would get if we had infinite historical data.

This approach provides accurate EMA values from the very first calculation. There's no need to use SMA for warmup or discard early values before output converges - EMA is mathematically correct from first value, ready to party without the awkward warmup phase.

Here is Pine Script 6 implementation of EMA that can take alpha parameter directly (or period if desired), returns valid values from the start, is resilient to dirty input values, uses decaying compensator instead of SMA, and uses the least amount of computational cycles possible.

// Enhanced EMA function with proper initialization and efficient calculation

ema(series float source, simple int period=0, simple float alpha=0)=>

// Input validation - one of alpha or period must be provided

if alpha<=0 and period<=0

runtime.error("Alpha or period must be provided")

// Calculate alpha from period if alpha not directly specified

float a = alpha > 0 ? alpha : 2.0 / math.max(period, 1)

// Initialize variables for EMA calculation

var float ema = na // Stores raw EMA value

var float result = na // Stores final corrected EMA

var float e = 1.0 // Decay compensation factor

var bool warmup = true // Flag for warmup phase

if not na(source)

if na(ema)

// First value case - initialize EMA to zero

// (we'll correct this immediately with the compensation)

ema := 0

result := source

else

// Standard EMA calculation (optimized formula)

ema := a * (source - ema) + ema

if warmup

// During warmup phase, apply decay compensation

e *= (1-a) // Update decay factor

float c = 1.0 / (1.0 - e) // Calculate correction multiplier

result := c * ema // Apply correction

// Stop warmup phase when correction becomes negligible

if e <= 1e-10

warmup := false

else

// After warmup, EMA operates without correction

result := ema

result // Return the properly compensated EMA value

▶️ CONCLUSION

EMA isn't just a "better SMA"—it is a fundamentally different tool, like how a submarine differs from a sailboat – both float, but the similarities end there. EMA responds to inputs differently, weighs historical data differently, and requires different initialization techniques.

By understanding these differences, traders can make more informed decisions about when and how to use EMA in trading strategies. And as EMA is embedded in so many other complex and compound indicators and strategies, if system uses tainted and inferior EMA calculatiomn, it is doing a disservice to all derivative indicators too – like building a skyscraper on a foundation of Jell-O.

The next time you add an EMA to your chart, remember: you're not just looking at a "faster moving average." You're using an INFINITE IMPULSE RESPONSE filter that carries the echo of all previous price actions, properly weighted to help make better trading decisions.

EMA done right might significantly improve the quality of all signals, strategies, and trades that rely on EMA somewhere deep in its algorithmic bowels – proving once again that math skills are indeed useful after high school, no matter what your guidance counselor told you.

Elliott Wave Noise FilterElliott Wave Noise Filter

Overview

The Elliott Wave Noise Filter is a specialized indicator for TradingView, designed to solve one of the biggest challenges in Elliott Wave analysis on lower timeframes: the identification of market noise. By combining multiple advanced filtering techniques, this indicator helps distinguish meaningful price action from random fluctuations.

The Problem

On lower timeframes—especially below 15 minutes—Elliott Wave analysis is significantly impacted by excessive market noise. This noise can lead to misinterpretation of wave structures, making it difficult to execute reliable trading decisions.

The Solution

The Elliott Wave Noise Filter utilizes four powerful methods to detect and filter noise:

ATR-Based Volatility Analysis: Identifies price movements too small to be structurally meaningful

Volume Confirmation: Filters out price moves that occur with insufficient volume

Trend Strength Measurement (ADX): Detects periods of weak trend activity, where noise tends to dominate

Fractal Pattern Recognition: Marks significant turning points that could be relevant for Elliott Wave analysis

Features

Visual Indicators

Background Coloring: Red indicates noise; green signifies a clear signal

Hull Moving Average: Smooths price action and highlights the prevailing trend

Fractal Markers: Triangles mark significant highs and lows

Status Panel: Displays current noise status and ADX value

Customization Options

ATR Period: Adjust the lookback period for ATR calculations

Noise Threshold: Defines the percentage of ATR below which a movement is considered noise

Volume Filter: Can be enabled or disabled

Volume Threshold: Sets the ratio to average volume for a move to be deemed significant

Hull MA Display and Length: Configure the moving average settings

ADX Parameters: Adjust trend strength sensitivity

Use Cases

For Elliott Wave Analysis

Eliminate noise to identify cleaner wave structures

Use fractal markers as potential wave endpoints

Reference the Hull MA for determining the broader trend

For General Trading

Identify high-noise periods to avoid low-quality setups

Spot clearer market phases for better entries

Assess price action quality through visual cues

Multi-Timeframe Approach

Apply the indicator across different timeframes for a comprehensive view

Prefer trading when both higher and lower timeframes align with consistent signals

Optimal Settings

For Very Short Timeframes (1–5 minutes)

Higher Noise Threshold (0.4–0.5)

Longer ATR Period (20–30)

Higher Volume Threshold (1.0–1.2)

For Medium Timeframes (15–60 minutes)

Medium Noise Threshold (0.2–0.3)

Standard ATR Period (14)

Standard Volume Threshold (0.8)

For Higher Timeframes (4h and above)

Lower Noise Threshold (0.1–0.2)

Shorter ATR Period (10)

Lower Volume Threshold (0.6–0.7)

Conclusion

The Elliott Wave Noise Filter is an essential tool for any Elliott Wave analyst or trader working on lower timeframes. By reducing noise and emphasizing significant market movements, it enables more precise analysis and potentially more profitable trading decisions.

Note: As with any technical indicator, the Elliott Wave Noise Filter should be used as part of a broader trading strategy and not as a standalone signal for trade execution.

Multi-Timeframe Trend Lines📌 What This Indicator Does

This tool helps you see the direction of the market across different timeframes—all on one chart.

Imagine you're looking at the price of a stock, crypto, or any other asset. You probably know the price can move differently in the short term and the long term. This indicator draws slanted lines to show if the price is generally going up or down over different time periods—like the past 1 minute, 5 minutes, 1 hour, 1 day, or even 1 month.

These lines are colored:

Green if the price is going up (a rising trend).

Red if the price is going down (a falling trend).

You can choose which timeframes you want to see—like 5 minutes or 1 day—by ticking checkboxes.

✅ Why This Is Useful

1. Helps You See the Bigger Picture

Even if you’re trading on a short timeframe (like 5 minutes), this indicator shows you the trend in longer timeframes (like 1 hour or 1 day). This helps you avoid going against the overall direction of the market.

2. Gives You More Confidence

When several timeframes show the same direction (all lines green, for example), it gives you more confidence that the trend is strong.

3. Saves Time

Instead of switching between different charts (like going from a 1-hour chart to a daily chart), you can see all the trends right on your current chart.

4. Easier Decision Making

You can quickly decide if it’s a good idea to buy (when most lines are green) or sell (when most lines are red).

👶 Example for a Beginner

Let’s say you’re looking at a 15-minute chart and thinking of buying.

* The 15-minute line is green (short-term price is going up).

* The 1-hour line is also green (medium-term price is going up).

* The 1-day line is green too (long-term price is going up).

This is a good sign that everything is moving upward, and it may be safer to buy.

But if the 1-day line is red while the shorter ones are green, it might mean the upward move is just temporary. That’s something to be careful about.

Savitzky Flow Bands [ChartPrime]An advanced trend-following tool that applies the Savitzky-Golay smoothing algorithm to price and dynamically adapts trend bands to visualize directional bias and trend strength.

savitzky_golay_filter_w_15_vectors(source) =>

float sum = 0.0

float polynomial = 0.0

float coefficients = array.new(16)

// Predefined 15 coefficients

for i = -4 to 4

coefficients.set(i + 4, i) // from -4 to 5

if i == 4

for j = 5 to -4

for g = 8 to 15

coefficients.set(g, j) // from 5 to -4

// Calculate normalization factor as the sum of absolute values of coefficients

float norm_factor = coefficients.sum()

// Loop through coefficients and calculate the weighted sum

for i = 0 to coefficients.size()-1

sum := sum + coefficients.get(i) * source

// Calculate the smoothed value

for i = 1 to length-1

polynomial := math.sum(sum / norm_factor, i) / i

polynomial

⯁ KEY FEATURES & HOW TO USE

Savitzky-Golay Filtered Line (Basis):

Smooths out price noise using the Savitzky-Golay method, offering a more refined trend path than traditional moving averages. This centerline acts as the trend anchor and visually changes color depending on its slope to reflect the active trend direction.

Dynamic Trend Bands (Upper/Lower):

Constructed from the filtered line with a dynamic offset based on recent price volatility (ATR). These bands shift based on price pressure and are locked once price closes beyond them.

Helpful for identifying breakout moments or exhaustion areas where reversals are likely.

Trend Direction Detection:

A directional signal is confirmed when price breaks and closes above the upper band (uptrend) or below the lower band (downtrend).

Provides a clear and systematic way to identify when a trend begins.

Trend Duration Counter (Visual Decay Line):

A fading overlay line shows how long a trend has been active since the last reversal. The longer the trend persists, the more transparent this extension becomes.

This visual fading effect helps traders anticipate potential trend exhaustion and prepare for reversals or take-profit zones.

Reversal Signals (Diamond Markers):

Diamond shapes are plotted at each market shift, allowing users to visually pinpoint when the trend has flipped.

These markers act as decision zones for entry, exit, or stop-loss adjustments based on directional flow changes.

Color-Based Bar and Candle Painting:

Candles are painted green in uptrends and orange in downtrends, providing an intuitive glance at trend state without needing to interpret numbers.

Helps users stay aligned with the trend visually and avoid counter-trend entries.

⯁ CONCLUSION

The Savitzky Flow Bands indicator offers a modernized, visually rich way to track trend shifts using a scientific smoothing method. With dynamic trend envelopes, color-coded cues, and visual markers, it equips traders with a structured framework to follow the market's flow and make data-driven decisions. Ideal for swing traders, momentum strategists, or any trader looking to trade in sync with the prevailing trend.

5m Gold Strategy - Session Break + Previous Day High/LowHere is your complete Pine Script v5 code for TradingView that:

Implements your 5-minute Gold breakout strategy.

Uses previous day high/low levels.

Confirms entry based on 15-minute SMA trend (SMA 9 > SMA 21).

Marks session time.

Filters news time (pause trading 15 minutes before/after major red news from ForexFactory).

0830-0845 High/Low Marker (Accurate Start + History)This indicator marks the high and low of the 15-minute candle between 08:30 and 08:45 (local time) of the trading session. The high and low are tracked dynamically, with the lines drawn once the 08:45 candle closes.

Key Features:

Session-based Tracking: Automatically tracks and records the high and low of the 15-minute period starting at 08:30 and ending at 08:45.

Excludes 08:45 High : If a high is created exactly at 08:45, the indicator will ignore it and use the highest value before 08:45, ensuring it only references the price action during the specified window.

Line Extension : The high and low lines are drawn and extended to the right for a user-defined number of bars, making them visible beyond the session's close.

Customizable Parameters : Adjust the start and end times of the session, line colors, and line width to fit your preferences.

Use Case :

Ideal for traders who focus on the price action during the early part of the trading session (08:30 to 08:45) and want to track significant levels of support and resistance from that period.

The extended lines help identify potential price zones for the rest of the session or the trading day.

Bitcoin Monthly Seasonality [Alpha Extract]The Bitcoin Monthly Seasonality indicator analyzes historical Bitcoin price performance across different months of the year, enabling traders to identify seasonal patterns and potential trading opportunities. This tool helps traders:

Visualize which months historically perform best and worst for Bitcoin.

Track average returns and win rates for each month of the year.

Identify seasonal patterns to enhance trading strategies.

Compare cumulative or individual monthly performance.

🔶 CALCULATION

The indicator processes historical Bitcoin price data to calculate monthly performance metrics

Monthly Return Calculation

Inputs:

Monthly open and close prices.

User-defined lookback period (1-15 years).

Return Types:

Percentage: (monthEndPrice / monthStartPrice - 1) × 100

Price: monthEndPrice - monthStartPrice

Statistical Measures

Monthly Averages: ◦ Average return for each month calculated from historical data.

Win Rate: ◦ Percentage of positive returns for each month.

Best/Worst Detection: ◦ Identifies months with highest and lowest average returns.

Cumulative Option

Standard View: Shows discrete monthly performance.

Cumulative View: Shows compounding effect of consecutive months.

Example Calculation (Pine Script):

monthReturn = returnType == "Percentage" ?

(monthEndPrice / monthStartPrice - 1) * 100 :

monthEndPrice - monthStartPrice

calcWinRate(arr) =>

winCount = 0

totalCount = array.size(arr)

if totalCount > 0

for i = 0 to totalCount - 1

if array.get(arr, i) > 0

winCount += 1

(winCount / totalCount) * 100

else

0.0

🔶 DETAILS

Visual Features

Monthly Performance Bars: ◦ Color-coded bars (teal for positive, red for negative returns). ◦ Special highlighting for best (yellow) and worst (fuchsia) months.

Optional Trend Line: ◦ Shows continuous performance across months.

Monthly Axis Labels: ◦ Clear month names for easy reference.

Statistics Table: ◦ Comprehensive view of monthly performance metrics. ◦ Color-coded rows based on performance.

Interpretation

Strong Positive Months: Historically bullish periods for Bitcoin.

Strong Negative Months: Historically bearish periods for Bitcoin.

Win Rate Analysis: Higher win rates indicate more consistently positive months.

Pattern Recognition: Identify recurring seasonal patterns across years.

Best/Worst Identification: Quickly spot the historically strongest and weakest months.

🔶 EXAMPLES

The indicator helps identify key seasonal patterns

Bullish Seasons: Visualize historically strong months where Bitcoin tends to perform well, allowing traders to align long positions with favorable seasonality.

Bearish Seasons: Identify historically weak months where Bitcoin tends to underperform, helping traders avoid unfavorable periods or consider short positions.

Seasonal Strategy Development: Create trading strategies that capitalize on recurring monthly patterns, such as entering positions in historically strong months and reducing exposure during weak months.

Year-to-Year Comparison: Assess how current year performance compares to historical seasonal patterns to identify anomalies or confirmation of trends.

🔶 SETTINGS

Customization Options

Lookback Period: Adjust the number of years (1-15) used for historical analysis.

Return Type: Choose between percentage returns or absolute price changes.

Cumulative Option: Toggle between discrete monthly performance or cumulative effect.

Visual Style Options: Bar Display: Enable/disable and customize colors for positive/negative bars, Line Display: Enable/disable and customize colors for trend line, Axes Display: Show/hide reference axes.

Visual Enhancement: Best/Worst Month Highlighting: Toggle special highlighting of extreme months, Custom highlight colors for best and worst performing months.

The Bitcoin Monthly Seasonality indicator provides traders with valuable insights into Bitcoin's historical performance patterns throughout the year, helping to identify potentially favorable and unfavorable trading periods based on seasonal tendencies.

Timeframe StrategyThis is a multi-timeframe trading strategy inspired by Ross Cameron's style, optimized for scalping and trend-following across various timeframes (1m, 5m, 15m, 1h, and 1D). The strategy integrates a comprehensive set of technical indicators, dynamic risk management, and visual tools.

Core Features

Dynamic Take Profit, Stop Loss & Trailing Stop

> Separate settings per timeframe for:

-TP% (Take Profit)

-SL% (Stop Loss)

-Trailing Stop %

-Cooldown bars

> Configurable via UI inputs.

>Smart Entry Conditions

Bullish entry: EMA9 crossover EMA20 and EMA50 > EMA200

Bearish entry: EMA9 crossunder EMA20 and EMA50 < EMA200

>Additional confirmation filters:

-Volume Filter (enabled/disabled via UI)

-Time Filter (e.g., only between 15:00–20:00 UTC)

-Spike Filter: rejects high-volatility candles

-RSI Filter: above/below 50 for trend confirmation

-ADX Filter (only applied on 1m, e.g., ADX > 15)

-Micro-Volatility Filter: minimum range percentage (1m only)

-Trend Filter (1m only): price must be above/below EMA200

>Trailing Stop Logic

-Configurable for each timeframe.

- Optional via toggle (use_trailing).

>Trade Cooldown Logic

-Prevents consecutive trades within X bars, configurable per timeframe.

>Technical Indicators Used

-EMA 9 / 20 / 50 / 200

-VWAP

-RSI (14)

-ATR (14) for volatility-based spike filtering

-Custom-calculated ADX (14) (manually implemented)

>Visual Elements

🔼/🔽 Entry signals (long/short) plotted on the chart.

📉 Table in bottom-left:

Displays current values of EMA/VWAP/volume/ATR/ADX.

> Optional "Tab info" panel in top-right (toggleable):

-Timeframe & strategy settings

-Live status of filters (volume, time, cooldown, spike, RSI, ADX, range, trend)

-Uses emoji (✅ / ❌) for quick diagnostics.

>User Customization

-Inputs per timeframe for all key parameters.

-Toggle switches for:

-Trailing stop

-Volume filter

-Info table visibility

This strategy is designed for active traders seeking a balance between momentum entry, risk control, and adaptability across timeframes. It's ideal for backtesting quick reversals or breakout setups in fast markets, especially at lower timeframes like 1m or 5m.

[TTM] ICT Sessions & Ranges🌟 Overview 🌟

The ICT Sessions & Ranges Indicator helps traders identify key intraday price levels by marking custom session highs/lows and opening ranges.

It helps traders spot potential liquidity grabs, reversals, and breakout zones by tracking price behavior around these key areas

🌟 Session Highs & Lows – Liquidity Zones 🌟

Session highs and lows often attract price due to stop orders resting above or below them. These levels are frequently targeted during high-volatility moves.

🔹 Asia Session

- Usually ranges in low volatility.

- Highs/lows often get swept during early London.

- Price may raid these levels, then reverse.

🔹 London Session

- First major volatility of the day.

- Highs/lows often tested or swept in New York.

- Commonly forms the day’s true high or low.

🌟 Opening Range Concepts 🌟

The Opening Range is the first 15, 30, or 60 minutes of a session (e.g., New York).

The high (ORH) and low (ORL) define the market’s initial balance and key reaction levels.

🔹 Breakout Trade

- Price breaks ORH/ORL with momentum.

- Signals directional intent.

- Traders enter on the breakout, with stops inside the range.

🔹 Liquidity Raid

- Price briefly breaks ORH/ORL to trigger stops.

- Reverses after the sweep.

- Look for structure shift and entry near FVG or OB.

🌟 Customizable Settings 🌟

The indicator includes 3 configurable ranges , each with:

Start & End Time – Set any custom time window.

Display Type – Choose Box (highlight range) or Lines (mark high/low).

Color Settings – Set custom colors for boxes and lines.

🌟 Default Settings 🌟

Range 1 : 19:00–00:00 (Asia Session)

Range 2 : 01:45–05:15 (London Session)

Range 3 : 09:30–10:00 (NY Opening Range – 30m)

ICT Macro H1"H1 Candle Time Box" is a custom TradingView indicator that highlights a configurable time window surrounding the close of each 1-hour (H1) candle. The indicator draws a transparent box 15 minutes before and after each H1 candle close (by default), helping traders visualize time-based reaction zones.

🔍 Features:

Custom time window: Users can set how many minutes before and after the H1 close the box should appear.

Dynamic positioning: Boxes are drawn slightly above the candles to avoid overlap with price bars.