Top Finder & Dip Hunter [BackQuant]Top Finder & Dip Hunter

A practical tool to map where price is statistically most likely to exhaust or mean-revert. It builds objective support for dips and resistance for tops from multiple methodologies, then filters raw touches with volume, momentum, trend, and price-action context to surface higher-quality reversal opportunities.

What this does

Draws a Dip Support line and a Top Resistance line using the method you select, or a blended hybrid.

Evaluates each touch/penetration against Quality Filters and assigns a 0–100 composite score.

Prints clean DIP and TOP signals only when depth/extension and quality pass your thresholds.

Optionally annotates the chart with the computed quality score at signal time.

Why it’s useful

Objectivity: Converts vague “looks extended” into rules, reduces discretion creep.

Signal hygiene: Filters raw touches using trend, volume, momentum, and candle structure to avoid obvious traps.

Adaptable regimes: Switch methods, sensitivity, and lookbacks to match choppy vs trending conditions.

How support and resistance are built

Pick one per side, or use “Hybrid.”

Dynamic: Anchors to the extreme of a lookback window, padded by recent ATR, so buffers expand in volatile periods and contract when calm.

Fibonacci: Uses the 0.618/0.786 retracement pair inside the current swing window to target common reaction zones.

Volatility: Uses a moving-average basis with standard-deviation bands to capture statistically stretched moves.

Volume-Weighted: Centers off VWAP and penalizes deviations using dispersion of price around VWAP, helpful on intraday instruments.

Hybrid: A weighted average of the above to smooth out single-method biases.

When a touch becomes a signal

Depth/extension test:

Dips must penetrate their support by at least Min Dip Depth % .

Tops must extend above resistance by at least Min Top Rise % .

Quality Score gate: The composite must clear Min Quality Score . Components:

Trend alignment: Favor dips in bullish regimes and tops in bearish regimes using EMAs and RSI.

Volume confirmation: Reward expansion or spikes versus a 20-period baseline.

RSI context: Prefer oversold for dips, overbought for tops.

Momentum shift: Look for short-term momentum turning in the expected direction.

Candle structure: Reward hammer/shooting-star style responses at the level.

How to use it

Pick your regime:

Range/chop, small caps, mean-revert intraday → Volatility or Volume Weighted .

Cleaner swings/trends → Dynamic or Fibonacci .

Unsure or mixed conditions → Hybrid .

Set windows: Start with Lookback = 50 for both sides. Increase in higher timeframes or slow assets, decrease for fast scalps.

Tune sensitivity: Raise Dip/Top Sensitivity to widen buffers and reduce noise. Lower to be more aggressive.

Gate with quality: Begin with Min Quality Score = 60 . Push to 70–80 for cleaner swing entries, relax to 50–60 for scalps.

Act on first prints: The script only fires on new qualified events. Use the score label to prioritize A-setups.

Typical workflows

Intraday futures/crypto: Volume-Weighted or Volatility methods for both sides, higher Sensitivity , require Volume Filter and Momentum Filter on. Look for DIP during opening drive exhaustion and TOP near late-session fatigue.

Swing equities/FX: Dynamic or Fibonacci with moderate sensitivity. Keep Trend Filter on to only take dips above the 200-EMA and tops below it.

Countertrend scouts: Lower Min Dip Depth % / Min Top Rise % slightly, but raise Min Quality Score to compensate.

Reading the chart

Lines: “Dip Support” and “Top Resistance” are the current actionable rails, lightly smoothed to reduce flicker.

Signals: “DIP” prints below bars when a qualified dip appears, “TOP” prints above for qualified tops.

Scores: Optional labels show the composite at signal time. Favor higher numbers, especially when aligned with higher-timeframe trend.

Background hints: Light highlights mark raw touches meeting depth/extension, even if they fail quality. Treat these as early warnings.

Tuning tips

If you get too many false DIP signals in downtrends, raise Min Dip Depth % and keep Trend Filter on.

If tops appear late in squeezes, lower Top Sensitivity slightly or switch top side to Fibonacci .

On assets with erratic volume, prefer Volatility or Dynamic methods and down-weight the Volume Filter .

For strict systems, increase Min Quality Score and require both Volume and Momentum filters.

What this is not

It is not a blind reversal signal. It’s a structured context tool. Combine with your risk plan and higher-timeframe map.

It is not a guarantee of mean reversion. In strong trends, expect fewer, higher-score opportunities and respect invalidation quickly.

Suggested presets

Scalp preset: Lookback 30–40, Sensitivity 1.2–1.5, Quality ≥ 55, Volume & Momentum filters ON.

Swing preset: Lookback 75–100, Sensitivity 1.0–1.2, Quality ≥ 70, Trend & Volume filters ON.

Chop preset: Volatility/Volume-Weighted methods, Quality ≥ 60, Momentum filter ON, RSI emphasis.

Input quick reference

Dip/Top Method: Choose the model for each side or “Hybrid” to blend.

Lookback: Swing window the levels are built from.

Sensitivity: Scales volatility padding around levels.

Min Dip Depth % / Min Top Rise %: Minimum breach/extension to qualify.

Quality Filters: Trend, Volume, Momentum toggles, plus Min Quality Score gate.

Visuals: Colors and whether to print score labels.

Best practices

Map higher-timeframe trend first, then act on lower-timeframe DIP/TOP in the trend’s favor.

Use the score as triage. Skip mediocre prints into news or at session open unless score is exceptional.

Pre-define stop placement relative to the level you used. If a DIP fails, exit on loss of structure rather than waiting for the next print.

Bottom line: Top Finder & Dip Hunter codifies where reversals are most defensible and only flags the ones with supportive context. Tune the method and filters to your market, then let the score keep your playbook disciplined.

Pesquisar nos scripts por "如何用wind搜索股票的发行价和份数"

RightFlow Universal Volume Profile - Any Market Any TimeframeSummary in one paragraph

RightFlow is a right anchored microstructure volume profile for stocks, futures, FX, and liquid crypto on intraday and daily timeframes. It acts only when several conditions align inside a session window and presents the result as a compact right side profile with value area, POC, a bull bear mix by price bin, and a HUD of profile VWAP and pressure shares. It is original because it distributes each bar’s weight into multiple mid price slices, blends bull bear pressure per bin with a CLV based split, and grows the profile to the right so price action stays readable. Add to a clean chart, read the table, and use the visuals. For conservative workflows read on bar close.

Scope and intent

• Markets. Major FX pairs, index futures, large cap equities and ETFs, liquid crypto.

• Timeframes. One minute to daily.

• Default demo used in the publication. SPY on 15 minute.

• Purpose. See where participation concentrates, which side dominated by price level, and how far price sits from VA and POC.

Originality and usefulness

• Unique fusion. Right anchored growth plus per bar slicing and CLV split, with weight modes Raw, Notional, and DeltaProxy.

• Failure mode addressed. False reads from single bar direction and coarse binning.

• Testability. All parts sit in Inputs and the HUD.

• Portable yardstick. Value Area percent and POC are universal across symbols.

• Protected scripts. Not applicable. Method and use are fully disclosed.

Method overview in plain language

Pick a scope Rolling or Today or This Week. Define a window and number of price bins. For each bar, split its range into small slices, assign each slice a weight from the selected mode, and split that weight by CLV or by bar direction. Accumulate totals per bin. Find the bin with the highest total as POC. Expand left and right until the chosen share of total volume is covered to form the value area. Compute profile VWAP for all, buyers, and sellers and show them with pressure shares.

Base measures

Range basis. High minus low and mid price samples across the bar window.

Return basis. Not used. VWAP trio is price weighted by weights.

Components

• RightFlow Bins. Price histogram that grows to the right.

• Bull Bear Split. CLV based 0 to 1 share or pure bar direction.

• Weight Mode. Raw volume, notional volume times close, or DeltaProxy focus.

• Value Area Engine. POC then outward expansion to target share.

• HUD. Profile VWAP, Buy and Sell percent, winner delta, split and weight mode.

• Session windows optional. Scope resets on day or week.

Fusion rule

Color of each bin is the convex blend of bull and bear shares. Value area shading is lighter inside and darker outside.

Signal rule

This is context, not a trade signal. A strong separation between buy and sell percent with price holding inside VA often confirms balance. Price outside VA with skewed pressure often marks initiative moves.

What you will see on the chart

• Right side bins with blended colors.

• A POC line across the profile width.

• Labels for POC, VAH, and VAL.

• A compact HUD table in the top right.

Table fields and quick reading guide

• VWAP. Profile VWAP.

• Buy and Sell. Pressure shares in percent.

• Delta Winner. Winner side and margin in percent.

• Split and Weight. The active modes.

Reading tip. When Session scope is Today or This Week and Buy minus Sell is clearly positive or negative, that side often controls the day’s narrative.

Inputs with guidance

Setup

• Profile scope. Rolling or session reset. Rolling uses window bars.

• Rolling window bars. Typical 100 to 300. Larger is smoother.

Binning

• Price bins. Typical 32 to 128. More bins increase detail.

• Slices per bar. Typical 3 to 7. Raising it smooths distribution.

Weighting

• Weight mode. Raw, Notional, DeltaProxy. Notional emphasizes expensive prints.

• Bull Bear split. CLV or BarDir. CLV is more nuanced.

• Value Area percent. Typical 68 to 75.

View

• Profile width in bars, color split toggle, value area shading, opacities, POC line, VA labels.

Usage recipes

Intraday trend focus

• Scope Today, bins 64, slices 5, Value Area 70.

• Split CLV, Weight Notional.

Intraday mean reversion

• Scope Today, bins 96, Value Area 75.

• Watch fades back to POC after initiative pushes.

Swing continuation

• Scope Rolling 200 bars, bins 48.

• Use Buy Sell skew with price relative to VA.

Realism and responsible publication

No performance claims. Shapes can move while a bar forms and settle on close. Education only.

Honest limitations and failure modes

Thin liquidity and data gaps can distort bin weights. Very quiet regimes reduce contrast. Session time is the chart venue time.

Open source reuse and credits

None.

Legal

Education and research only. Not investment advice. Test on history and simulation before live use.

Lorentzian Harmonic Flow - Temporal Market Dynamic Lorentzian Harmonic Flow - Temporal Market Dynamic (⚡LHF)

By: DskyzInvestments

What this is

LHF Pro is a research‑grade analytical instrument that models market time as a compressible medium , extracts directional flow in curved time using heavy‑tailed kernels, and consults a history‑based memory bank for context before synthesizing a final, bounded probabilistic score . It is not a mashup; each subsystem is mathematically coupled to a single clock (time dilation via gamma) and a single lens (Lorentzian heavy‑tailed weighting). This script is dense in logic (and therefore heavy) because it prioritizes rigor, interpretability, and visual clarity.

Intended use

Education and research. This tool expresses state recognition and regime context—not guarantees. It does not place orders. It is fully functional as published and contains no placeholders. Nothing herein is financial advice.

Why this is original and useful

Curved time: Markets do not move at a constant pace. LHF Pro computes a Lorentz‑style gamma (γ) from relative speed so its analytical windows contract when the tape accelerates and relax when it slows.

Heavy‑tailed lens: Lorentzian kernels weight information with fat tails to respect rare but consequential extremes (unlike Gaussian decay).

Memory of regimes: A K‑nearest‑neighbors engine works in a multi‑feature space using Lorentz kernels per dimension and exponential age fade , returning a memory bias (directional expectation) and assurance (confidence mass).

One ecosystem: Squeeze, TCI, flow, acceleration, and memory live on the same clock and blend into a single final_score —visualized and documented on the dashboard.

Cognitive map: A 2D heat map projects memory resonance by age and flow regime, making “where the past is speaking” visible.

Shadow portfolio metaphor: Neighbor outcomes act like tiny hypothetical positions whose weighted average forms an educational pressure gauge (no execution, purely didactic).

Mathematical framework (full transparency)

1) Returns, volatility, and speed‑of‑market

Log return: rₜ = ln(closeₜ / closeₜ₋₁)

Realized vol: rv = stdev(r, vol_len); vol‑of‑vol: burst = |rv − rv |

Speed‑of‑market (analog to c): c = c_multiplier × (EMA(rv) + 0.5 × EMA(burst) + ε)

2) Trend velocity and Lorentz gamma (time dilation)

Trend velocity: v = |close − close | / (vel_len × ATR)

Relative speed: v_rel = v / c

Gamma: γ = 1 / √(1 − v_rel²), stabilized by caps (e.g., ≤10)

Interpretation: γ > 1 compresses market time → use shorter effective windows.

3) Adaptive temporal scale

Adaptive length: L = base_len / γ^power (bounded for safety)

Harmonic horizons: Lₛ = L × short_ratio, Lₘ = L × mid_ratio, Lₗ = L × long_ratio

4) Lorentzian smoothing and Harmonic Flow

Kernel weight per lag i: wᵢ = 1 / (1 + (d/γ)²), d = i/L

Horizon baselines: lw_h = Σ wᵢ·price / Σ wᵢ

Z‑deviation: z_h = (close − lw_h)/ATR

Harmonic Flow (HFL): HFL = (w_short·zₛ + w_mid·zₘ + w_long·zₗ) / (w_short + w_mid + w_long)

5) Flow kinematics

Velocity: HFL_vel = HFL − HFL

Acceleration (curvature): HFL_acc = HFL − 2·HFL + HFL

6) Squeeze and temporal compression

Bollinger width vs Keltner width using L

Squeeze: BB_width < KC_width × squeeze_mult

Temporal Compression Index: TCI = base_len / L; TCI > 1 ⇒ compressed time

7) Entropy (regime complexity)

Shannon‑inspired proxy on |log returns| with numerical safeguards and smoothing. Higher entropy → more chaotic regime.

8) Memory bank and Lorentzian k‑NN

Feature vector (5D):

Outcomes stored: forward returns at H5, H13, H34

Per‑dimension similarity: k(Δ) = 1 / (1 + Δ²), weighted by user’s feature weights

Age fading: weight_age = mem_fade^age_bars

Neighbor score: sᵢ = similarityᵢ × weight_ageᵢ

Memory bias: mem_bias = Σ sᵢ·outcomeᵢ / Σ sᵢ

Assurance: mem_assurance = Σ sᵢ (confidence mass)

Normalization: mem_bias normalized by ATR and clamped into band

Shadow portfolio metaphor: neighbors behave like micro‑positions; their weighted net forward return becomes a continuous, adaptive expectation.

9) Blended score and breakout proxy

Blend factor: α_mem = 0.45 + 0.15 × (γ − 1)

Final score: final_score = (1−α_mem)·tanh(HFL / (flow_thr·1.5)) + α_mem·tanh(mem_bias_norm)

Breakout probability (bounded): energy = cap(TCI−1) + |HFL_acc|×k + cap(γ−1)×k + cap(mem_assurance)×k; breakout_prob = sigmoid(energy). Caps avoid runaway “100%” readings.

Inputs — every control, purpose, mechanics, and tuning

🔮 Lorentz Core

Auto‑Adapt (Vol/Entropy): On = L responds to γ and entropy (breathes with regime), Off = static testing.

Base Length: Calm‑market anchor horizon. Lower (21–28) for fast tapes; higher (55–89+) for slow.

Velocity Window (vel_len): Bars used in v. Shorter = more reactive γ; longer = steadier.

Volatility Window (vol_len): Bars used for rv/burst (c). Shorter = more sensitive c.

Speed‑of‑Market Multiplier (c_multiplier): Raises/lowers c. Lower values → easier γ spikes (more adaptation). Aim for strong trends to peak around γ ≈ 2–4.

Gamma Compression Power: Exponent of γ in L. <1 softens; >1 amplifies adaptation swings.

Max Kernel Span: Upper bound on smoothing loop (quality vs CPU).

🎼 Harmonic Flow

Short/Mid/Long Horizon Ratios: Partition L into fast/medium/slow views. Smaller short_ratio → faster reaction; larger long_ratio → sturdier bias.

Weights (w_short/w_mid/w_long): Governs HFL blend. Higher w_short → nimble; higher w_long → stable.

📈 Signals

Squeeze Strictness: Threshold for BB1 = compressed (coiled spring); <1 = dilated.

v/c: Relative speed; near 1 denotes extreme pacing. Diagnostic only.

Entropy: Regime complexity; high entropy suggests caution, smaller size, or waiting for order to return.

HFL: Curved‑time directional flow; sign and magnitude are the instantaneous bias.

HFL_acc: Curvature; spikes often accompany regime ignition post‑squeeze.

Mem Bias: Directional expectation from historical analogs (ATR‑normalized, bounded). Aligns or conflicts with HFL.

Assurance: Confidence mass from neighbors; higher → more reliable memory bias.

Squeeze: ON/RELEASE/OFF from BB

VWAP Deviation Oscillator [BackQuant]VWAP Deviation Oscillator

Introduction

The VWAP Deviation Oscillator turns VWAP context into a clean, tradeable oscillator that works across assets and sessions. It adapts to your workflow with four VWAP regimes plus two rolling modes, and three deviation metrics: Percent, Absolute, and Z-Score. Colored zones, optional standard deviation rails, and flexible plot styles make it fast to read for both trend following and mean reversion.

What it does

This tool measures how far price is from a chosen VWAP and expresses that gap as an oscillator. You can view the deviation as raw price units, percent, or standardized Z-Score. The plot can be a histogram or a line with optional fills and sigma bands, so you can quickly spot polarity shifts, overbought and oversold conditions, and strength of extension.

VWAP modes track a session VWAP that resets (4H, Daily, Weekly) or a rolling VWAP that updates continuously over a fixed number of bars or days.

Deviation modes let you choose the lens: Percent, Absolute, or Z-Score. Each highlights different aspects of stretch and mean pressure.

Visual encoding uses a 10-zone color palette to grade the magnitude of deviation on both sides of zero.

Volatility guards compute mode-specific sigma so thresholds are stable even when volatility compresses.

Why this works

VWAP is a high signal anchor used by institutions to gauge fair participation. Deviations around VWAP cluster in regimes: mild oscillations within a band, decisive pushes that signal imbalance, and standardized extremes that often precede either continuation or snapback. Expressing that distance as a single time series adds clarity: bias is the oscillator’s sign, risk context is its magnitude, and regime is the way it behaves around sigma lines.

How to use it

Trend following

Favor the side of the zero line. Bullish when the oscillator is above zero and making higher swing highs. Bearish when below zero and making lower swing lows. Use +1 sigma and +2 sigma in your mode as strength tiers. Pullbacks that hold above zero in uptrends, or below zero in downtrends, are often continuation entries.

Mean reversion

Fade stretched readings when structure supports it. Look for tests of +2 sigma to +3 sigma that fail to progress and roll back toward zero, or the mirror on the downside. Z-Score mode is best when you want standardized gates across assets. Percent mode is intuitive for intraday scalps where a given percent stretch tends to mean revert.

Session playbook

Use Daily or Weekly VWAP for intraday or swing context. Rolling modes help when the asset lacks clean session boundaries or when you want a continuous anchor that adapts to liquidity shifts.

Key settings

VWAP computation

VWAP Mode = 4 Hours, Daily, Weekly, Rolling (Bars), Rolling (Days). Session modes reset the VWAP when a new session begins. Rolling modes compute VWAP over a fixed trailing window.

Rolling (Lookback: Bars) controls the trailing bar count when using Rolling (Bars).

Rolling (Lookback: Days) converts days to bars at runtime and uses that trailing span.

Use Close instead of HLC3 switches the price reference. HLC3 is smoother. Close makes the anchor track settlement more tightly.

Deviation measurement

Deviation Mode

Percent : 100 * (Price / VWAP - 1). Good for uniform scaling across instruments.

Absolute : Price - VWAP. Good when price units themselves matter.

Z-Score : Standardizes the absolute residual by its own mean and standard deviation over Z/Std Window . Ideal for cross-asset comparability and regime studies.

Z/Std Window sets the mean and standard deviation window for Z-Score mode.

Volatility controls

Percent Mode Volatility Lookback estimates sigma for percent deviations.

Absolute Mode Volatility Lookback estimates sigma for absolute deviations.

Minimum Sigma Guard (pct pts) prevents the percent sigma from collapsing to near zero in extremely quiet markets.

Visualization

Plot Type = Histogram or Line. Histogram emphasizes impulse and polarity changes. Line emphasizes trend waves and divergences.

Positive Color / Negative Color define the palette for line mode. Histogram uses a 10-bucket gradient automatically.

Show Standard Deviations plots symmetric rails at ±1, ±2, ±3 sigma in the current mode’s units.

Fill Line Oscillator and Fill Opacity add a soft bias band around zero for line mode.

Line Width affects both the oscillator and the sigma rails.

Reading the zones

The oscillator’s color and height map deviation to nine graded buckets on each side of zero, with deeper greens above and deeper reds below. In Percent and Absolute modes, those buckets are scaled by their mode-specific sigma. In Z-Score mode the bucket edges are fixed at 0.5, 1.0, 2.0, and 2.8.

0 to +1 sigma weak positive bias, usually rotational.

+1 to +2 sigma constructive impulse. Pullbacks that hold above zero often continue.

+2 to +3 sigma strong expansion. Watch for either trend continuation or exhaustion tells.

Beyond +3 sigma statistical extreme. Requires structure to avoid fading too soon.

Mirror logic applies on the negative side.

Suggested workflows

Trend continuation checklist

Pick a session VWAP that matches your timeframe, for example Daily for intraday or Weekly for position trades.

Wait for the oscillator to hold the correct side of zero and for a sequence of higher swing lows in the oscillator (uptrend) or lower swing highs (downtrend).

Buy pullbacks that stabilize between zero and +1 sigma in an uptrend. Sell rallies that stabilize between zero and -1 sigma in a downtrend.

Use the next sigma band or a prior price swing as your target reference.

Mean reversion checklist

Switch to Z-Score mode for standardized thresholds.

Identify tests of ±2 sigma to ±3 sigma that fail to extend while price meets support or resistance.

Enter on a polarity change through the prior histogram bar or a small hook in line mode.

Fade back to zero or to the opposite inner band, then reassess.

Notes on the three modes

Percent is easy to reason about when you care about proportional stretch. It is well suited to intraday and multi-asset dashboards.

Absolute tracks cash distance from VWAP. This is useful when instruments have tight ticks and you plan risk in price units.

Z-Score standardizes the residual and is best for quant studies, cross-asset comparisons, and threshold research that must be scale invariant.

What the alerts can tell you

Polarity changes at zero can mark the start or end of a leg.

Crosses of ±1 sigma identify overbought or oversold in the current mode’s units.

Zone changes signal an upgrade or downgrade in deviation strength.

Troubleshooting and edge cases

If your instrument has long flat periods, keep Minimum Sigma Guard above zero in Percent mode so the rails do not vanish.

In Rolling modes, very short windows will respond quickly but can whip around. Session modes smooth this by resetting at well known boundaries.

If Z-Score looks erratic, increase Z/Std Window to stabilize the estimate of mean and sigma for the residual.

Final thoughts

VWAP is the anchor. The deviation oscillator is the narrative. By separating bias, magnitude, and regime into a simple stream you can execute faster and review cleaner. Pick the VWAP mode that matches your horizon, choose the deviation lens that matches your risk framework, and let the color graded zones guide your decisions.

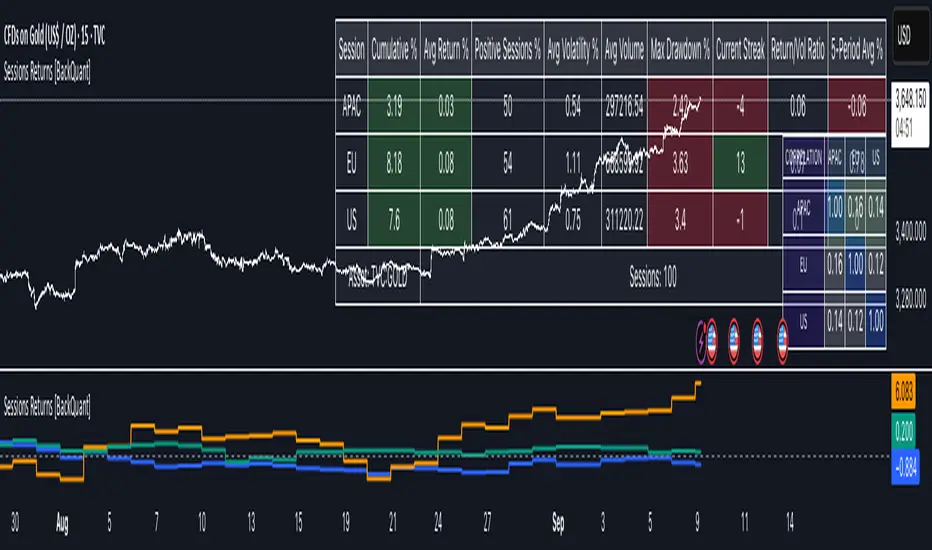

Cumulative Returns by Session [BackQuant]Cumulative Returns by Session

What this is

This tool breaks the trading day into three user-defined sessions and tracks how much each session contributes to return, volatility, and volume. It then aggregates results over a rolling window so you can see which session has been pulling its weight, how streaky each session has been, and how sessions relate to one another through a compact correlation heatmap.

We’ve also given the functionality for the user to use a simplified table, just by switching off all settings they are not interested in.

How it works

1) Session segmentation

You define APAC, EU, and US sessions with explicit hours and time zones. The script detects when each session starts and ends on every intraday bar and records its open, intraday high and low, close, and summed volume.

2) Per-session math

At each session end the script computes:

Return — either Percent: (Close−Open)÷Open×100(Close − Open) ÷ Open × 100(Close−Open)÷Open×100 or Points: (Close−Open)(Close − Open)(Close−Open), based on your selection.

Volatility — either Range: (High−Low)÷Open×100(High − Low) ÷ Open × 100(High−Low)÷Open×100 or ATR scaled by price: ATR÷Open×100ATR ÷ Open × 100ATR÷Open×100.

Volume — total volume transacted during that session.

3) Storage and lookback

Each day’s three session stats are stored as a row. You choose how many recent sessions to keep in memory. The script then:

Builds cumulative returns for APAC, EU, US across the lookback.

Computes averages, win rates, and a Sharpe-like ratio avgreturn÷avgvolatilityavg return ÷ avg volatilityavgreturn÷avgvolatility per session.

Tracks streaks of positive or negative sessions to show momentum.

Tracks drawdowns on cumulative returns to show worst runs from peak.

Computes rolling means over a short window for short-term drift.

4) Correlation heatmap

Using the stored arrays of session returns, the script calculates Pearson correlations between APAC–EU, APAC–US, and EU–US, and colors the matrix by strength and sign so you can spot coupling or decoupling at a glance.

What it plots

Three lines: cumulative return for APAC, EU, US over the chosen lookback.

Zero reference line for orientation.

A statistics table with cumulative %, average %, positive session rate, and optional columns for volatility, average volume, max drawdown, current streak, return-to-vol ratio, and rolling average.

A small correlation heatmap table showing APAC, EU, US cross-session correlations.

How to use it

Pick the asset — leave Custom Instrument empty to use the chart symbol, or point to another symbol for cross-asset studies.

Set your sessions and time zones — defaults approximate APAC, EU, and US hours, but you can align them to exchange times or your workflow.

Choose calculation modes — Percent vs Points for return, Range vs ATR for volatility. Points are convenient for futures and fixed-tick assets, Percent is comparable across symbols.

Decide the lookback — more sessions smooths lines and stats; fewer sessions makes the tool more reactive.

Toggle analytics — add volatility, volume, drawdown, streaks, Sharpe-like ratio, rolling averages, and the correlation table as needed.

Why session attribution helps

Different sessions are driven by different flows. Asia often sets the overnight tone, Europe adds liquidity and direction changes, and the US session can dominate range expansion. Separating contributions by session helps you:

Identify which session has been the main driver of net trend.

Measure whether volatility or volume is concentrated in a specific window.

See if one session’s gains are consistently given back in another.

Adapt tactics: fade during a mean-reverting session, press during a trending session.

Reading the tables

Cumulative % — sum of session returns over the lookback. The sign and slope tell you who is carrying the move.

Avg Return % and Positive Sessions % — direction and hit rate. A low average but high hit rate implies many small moves; the reverse implies occasional big swings.

Avg Volatility % — typical intrabars range for that session. Compare with Avg Return to judge efficiency.

Return/Vol Ratio — return per unit of volatility. Higher is better for stability.

Max Drawdown % — worst cumulative give-back within the lookback. A quick way to spot riskiness by session.

Current Streak — consecutive up or down sessions. Useful for mean-reversion or regime awareness.

Rolling Avg % — short-window drift indicator to catch recent turnarounds.

Correlation matrix — green clusters indicate sessions tending to move together; red indicates offsetting behavior.

Settings overview

Basic

Number of Sessions — how many recent days to include.

Custom Instrument — analyze another ticker while staying on your current chart.

Session Configuration and Times

Enable or hide APAC, EU, US rows.

Set hours per session and the specific time zone for each.

Calculation Methods

Return Calculation — Percent or Points.

Volatility Calculation — Range or ATR; ATR Length when applicable.

Advanced Analytics

Correlation, Drawdown, Momentum, Sharpe-like ratio, Rolling Statistics, Rolling Period.

Display Options and Colors

Show Statistics Table and its position.

Toggle columns for Volatility and Volume.

Pick individual colors for each session line and row accents.

Common applications

Session bias mapping — find which window tends to trend in your market and plan exposure accordingly.

Strategy scheduling — allocate attention or risk to the session with the best return-to-vol ratio.

News and macro awareness — see if correlation rises around central bank cycles or major data releases.

Cross-asset monitoring — set the Custom Instrument to a driver (index future, DXY, yields) to see if your symbol reacts in a particular session.

Notes

This indicator works on intraday charts, since sessions are defined within a day. If you change session clocks or time zones, give the script a few bars to accumulate fresh rows. Percent vs Points and Range vs ATR choices affect comparability across assets, so be consistent when comparing symbols.

Session context is one of the simplest ways to explain a messy tape. By separating the day into three windows and scoring each one on return, volatility, and consistency, this tool shows not just where price ended up but when and how it got there. Use the cumulative lines to spot the steady driver, read the table to judge quality and risk, and glance at the heatmap to learn whether the sessions are amplifying or canceling one another. Adjust the hours to your market and let the data tell you which session deserves your focus.

Time Range Marker By BCB ElevateThe Time Range Marker is a simple yet powerful visual tool for traders who want to focus on specific time intervals within the trading day. This indicator highlights a custom time range on your chart using a background color, helping you visually isolate key trading sessions or event windows such as:

Market open/close hours

News release periods

High-volatility trading zones

Personal strategy testing windows

⚙️ Key Features:

Customizable start and end time (hour & minute)

Works across all intraday timeframes

Adjustable highlight color to match your chart theme

Built using Pine Script v5 for speed and flexibility

🔧 Settings:

Start Hour / Minute – Set the beginning of the time range (in 24-hour format)

End Hour / Minute – Define when the range ends

Highlight Color – Choose the background color for better visibility

🕒 Timezone Note:

The indicator uses UTC time by default to ensure accuracy across markets. If your broker uses a different timezone (like EST, IST, etc.), the script can be adjusted to reflect your local market hours.

✅ How to Use the Time Range Marker Indicator

This indicator is used to visually highlight a specific time window each trading day, such as:

Market open or close sessions (e.g., NYSE, London, Tokyo)

High-impact news release periods

Custom time slots for strategy testing or scalping

🛠️ Installation Steps

Open TradingView and go to any chart.

Click on Pine Editor at the bottom of the screen.

Copy and paste the full Pine Script (shared above) into the editor.

Click the “Add to Chart” ▶️ button.

The indicator will appear on the chart with a highlighted background during the time range you set.

⚙️ How to Customize the Time Range

After adding the indicator:

Click the gear icon ⚙️ next to the indicator’s name on the chart.

Adjust the following settings:

Start Hour / Start Minute: The beginning of your time range (in 24-hour format).

End Hour / End Minute: When the highlight should stop.

Highlight Color: Pick a color and transparency for visual clarity.

Click OK to apply changes.

🕒 Timezone Consideration

By default, the indicator uses UTC (Coordinated Universal Time).

To match your broker’s timezone (e.g., EST, IST, etc.), you'll need to adjust the script by changing:

sessStart = timestamp("Etc/UTC", ...)

sessEnd = timestamp("Etc/UTC", ...)

to your correct timezone, like "Asia/Kolkata" for IST or "America/New_York" for EST.

Let me know your broker or local timezone, and I’ll update it for you.

📈 Tips for Traders

Combine this with volume, price action, or breakout indicators to focus your strategy on high-probability time windows.

Use multiple versions of this script if you want to highlight more than one time range in a day.

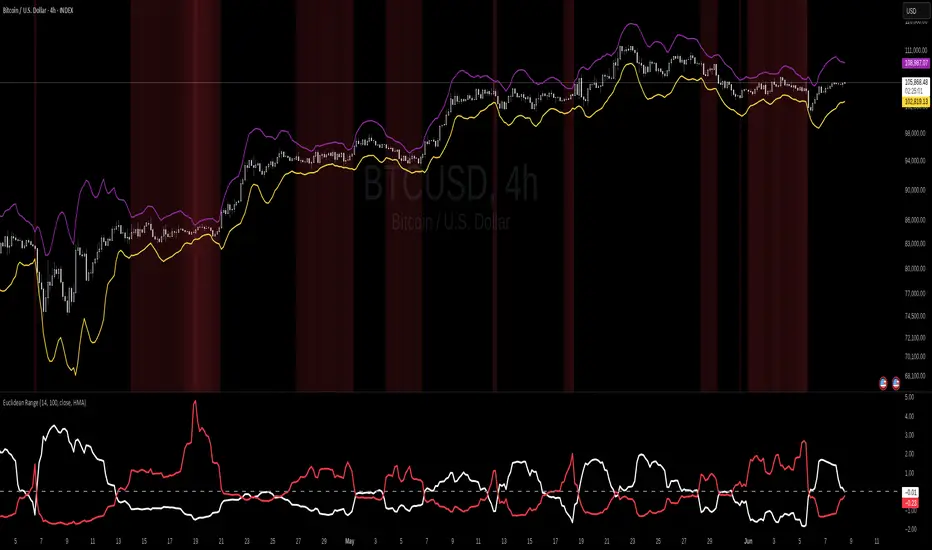

Euclidean Range [InvestorUnknown]The Euclidean Range indicator visualizes price deviation from a moving average using a geometric concept Euclidean distance. It helps traders identify trend strength, volatility shifts, and potential overextensions in price behavior.

Euclidean Distance

Euclidean distance is a fundamental concept in geometry and machine learning. It measures the "straight-line distance" between two points in space. In time series analysis, it can be used to measure how far one sequence deviates from another over a fixed window.

euclidean_distance(src, ref, len) =>

var float sum_sq_diff = na

sum_sq_diff := 0.0

for i = 0 to len - 1

diff = src - ref

sum_sq_diff += diff * diff

math.sqrt(sum_sq_diff)

In this script, we calculate the Euclidean distance between the price (source) and a smoothed average (reference) over a user-defined window. This gives us a single scalar that reflects the overall divergence between price and trend.

How It Works

Moving Average Calculation: You can choose between SMA, EMA, or HMA as your reference line. This becomes the "baseline" against which the actual price is compared.

Distance Band Construction: The Euclidean distance between the price and the reference is calculated over the Window Length. This value is then added to and subtracted from the average to form dynamic upper and lower bands, visually framing the range of deviation.

Distance Ratios and Z-Scores: Two distance ratios are computed: dist_r = distance / price (sensitivity to volatility); dist_v = price / distance (sensitivity to compression or low-volatility states)

Both ratios are normalized using a Z-score to standardize their behavior and allow for easier interpretation across different assets and timeframes.

Z-Score Plots: Z_r (white line) highlights instances of high volatility or strong price deviation; Z_v (red line) highlights low volatility or compressed price ranges.

Background Highlighting (Optional): When Z_v is dominant and increasing, the background is colored using a gradient. This signals a possible build-up in low volatility, which may precede a breakout.

Use Cases

Detect volatile expansions and calm compression zones.

Identify mean reversion setups when price returns to the average.

Anticipate breakout conditions by observing rising Z_v values.

Use dynamic distance bands as adaptive support/resistance zones.

Notes

The indicator is best used with liquid assets and medium-to-long windows.

Background coloring helps visually filter for squeeze setups.

Disclaimer

This indicator is provided for speculative analysis and educational purposes only. It is not financial advice. Always backtest and evaluate in a simulated environment before live trading.

FIR Low Pass Filter Suite (FIR)The FIR Low Pass Filter Suite is an advanced signal processing indicator that applies finite impulse response (FIR) filtering techniques to price data. At its core, the indicator uses windowed-sinc filtering, which provides optimal frequency response characteristics for separating trend from noise in financial data.

The indicator offers multiple window functions including Kaiser, Kaiser-Bessel Derived (KBD), Hann, Hamming, Blackman, Triangular, and Lanczos. Each window type provides different trade-offs between main-lobe width and side-lobe attenuation, allowing users to fine-tune the frequency response characteristics of the filter. The Kaiser and KBD windows provide additional control through an alpha parameter that adjusts the shape of the window function.

A key feature is the ability to operate in either linear or logarithmic space. Logarithmic filtering can be particularly appropriate for financial data due to the multiplicative nature of price movements. The indicator includes an envelope system that can adaptively calculate bands around the filtered price using either arithmetic or geometric deviation, with separate controls for upper and lower bands to account for the asymmetric nature of market movements.

The implementation handles edge effects through proper initialization and offers both centered and forward-only filtering modes. Centered mode provides zero phase distortion but introduces lag, while forward-only mode operates causally with no lag but introduces some phase distortion. All calculations are performed using vectorized operations for efficiency, with carefully designed state management to handle the filter's warm-up period.

Visual feedback is provided through customizable color gradients that can reflect the current trend direction, with optional glow effects and background fills to enhance visibility. The indicator maintains high numerical precision throughout its calculations while providing smooth, artifact-free output suitable for both analysis and visualization.

Time Appliconic Macro | ForTF5m (Fixed)The Time Appliconic Macro (TAMcr) is a custom-built trading indicator designed for the 5-minute time frame (TF5m), providing traders with clear Buy and Sell signals based on precise technical conditions and specific time windows.

Key Features:

Dynamic Moving Average (MA):

The indicator utilizes a Simple Moving Average (SMA) to identify price trends.

Adjustable length for user customization.

Custom STARC Bands:

Upper and lower bands are calculated using the SMA and the Average True Range (ATR).

Includes a user-defined multiplier to adjust the band width for flexibility across different market conditions.

RSI Integration:

Signals are filtered using the Relative Strength Index (RSI), ensuring they align with overbought/oversold conditions.

Time-Based Signal Filtering:

Signals are generated only during specific time windows, allowing traders to focus on high-activity periods or times of personal preference.

Supports multiple custom time ranges with automatic adjustments for UTC-4 or UTC-5 offsets.

Clear Signal Visualization:

Buy Signals: Triggered when the price is below the lower band, RSI indicates oversold conditions, and the time is within the defined range.

Sell Signals: Triggered when the price is above the upper band, RSI indicates overbought conditions, and the time is within the defined range.

Signals are marked directly on the chart for easy identification.

Customizability:

Adjustable parameters for the Moving Average length, ATR length, and ATR multiplier.

Time zone selection and defined trading windows provide a tailored experience for global users.

Who is this Indicator For?

This indicator is perfect for intraday traders who operate in the 5-minute time frame and value clear, filtered signals based on price action, volatility, and momentum indicators. The time window functionality is ideal for traders focusing on specific market sessions or personal schedules.

How to Use:

Adjust the MA and ATR parameters to match your trading style or market conditions.

Set the desired time zone and time ranges to align with your preferred trading hours.

Monitor the chart for Buy (green) and Sell (red) signals, and use them as a guide for entering or exiting trades.

ArrayMovingAveragesLibrary "ArrayMovingAverages"

This library adds several moving average methods to arrays, so you can call, eg.:

myArray.ema(3)

method emaArray(id, length)

Calculate Exponential Moving Average (EMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the EMA

Returns: (array) Array of EMA values

method ema(id, length)

Get the last value of the EMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the EMA

Returns: (float) Last EMA value or na if empty

method rmaArray(id, length)

Calculate Rolling Moving Average (RMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the RMA

Returns: (array) Array of RMA values

method rma(id, length)

Get the last value of the RMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the RMA

Returns: (float) Last RMA value or na if empty

method smaArray(id, windowSize)

Calculate Simple Moving Average (SMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (array) Array of SMA values

method sma(id, windowSize)

Get the last value of the SMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (float) Last SMA value or na if empty

method wmaArray(id, windowSize)

Calculate Weighted Moving Average (WMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (array) Array of WMA values

method wma(id, windowSize)

Get the last value of the WMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (float) Last WMA value or na if empty

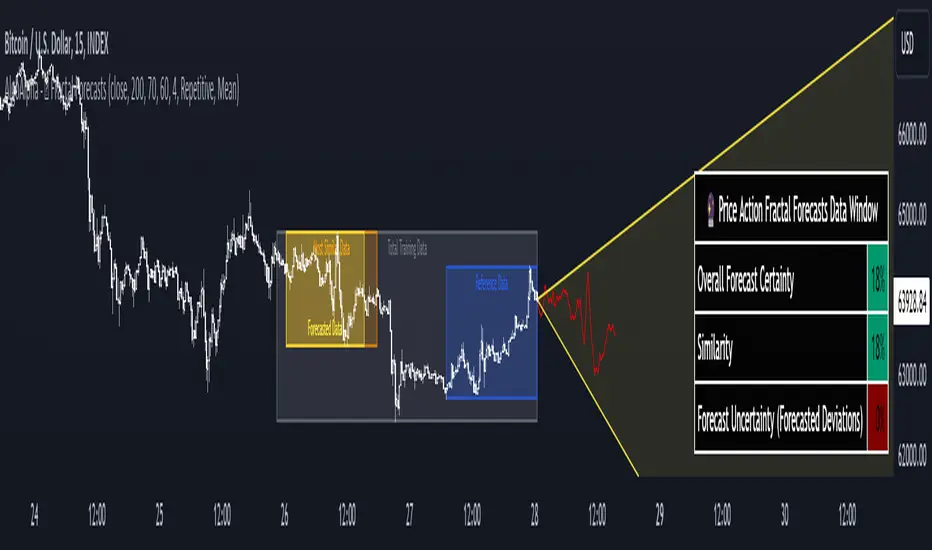

Price Action Fractal Forecasts [AlgoAlpha]🔮 Price Action Fractal Forecasts - Unleash the Power of Historical Patterns! 🌌✨

Dive into the future with AlgoAlpha's Price Action Fractal Forecasts ! This innovative indicator utilizes the mesmerizing complexity of fractals to predict future price movements, offering traders a unique edge in the market. By analyzing historical price action and identifying repeating patterns, this tool forecasts future price trends, providing visually engaging and actionable insights.

Key Features:

🔄 Flexible Data Series Selection: Choose your preferred data series for precise analysis.

🕰 Flexible Training and Reference Data Windows: Customize the length of training data and reference periods to match your trading style.

📈 Custom Forecast Length: Adjust the forecast horizon to suit your strategic objectives.

🌈 Customizable Visual Elements: Tailor the colors of forecast deviation cones, data reference areas, and more for optimal chart readability.

🔄 Anticipatory and Repetitive Forecast Modes: Select between anticipating future trends or identifying repetitive patterns for forecasts.

🔎 Enhanced Similarity Search: Leverages correlation metrics to find the most similar historical data segments.

📊 Forecast Deviation Cone: Visualize potential price range deviations with adjustable multipliers.

🚀 Quick Guide to Maximizing Your Trading with Price Action Fractal Forecasts:

🛠 Add the Indicator: Search for "Price Action Fractal Forecasts" in TradingView's Indicators & Strategies. Customize settings according to your trading strategy.

📊 Strategic Forecasting: Monitor the forecast deviation cone and forecast directional changes for insights into potential future price movements.

🔔 Alerts for Swift Action: Set up notifications based on forecast changes to stay ahead of market movements without constant monitoring.

Behind the Magic: How It Works

The core of the Price Action Fractal Forecasts lies in its ability to compare current market behavior with historical data to unearth similar patterns. It first establishes a training data window to analyze historical prices. Within this window, it then defines a reference length to identify the most recent price action that will serve as the basis for comparison. The indicator searches through the historical data within the training window to find segments that closely match the recent price action in the reference period.

Depending on whether you choose the anticipatory or repetitive forecast mode, the indicator either looks ahead to predict future prices based on past outcomes following similar patterns or focuses on the repeating patterns within the reference period itself for forecasts. The forecast's direction can be configured to reflect the mean average of forecasted prices or the end-point relative to the start-point of the forecast, offering flexibility in how forecasts are interpreted.

To enhance the comprehensiveness and visualization, the indicator features a forecast deviation cone. This cone represents the potential range of price movements, providing a visual cue for volatility and uncertainty in the forecasted prices. The intensity of this cone can be adjusted to suit individual preferences, offering a visual guide to the level of risk and uncertainty associated with the forecasted price path.

Embrace the fractal magic of markets with AlgoAlpha's Price Action Fractal Forecasts and transform your trading today! 🌟🚀

Filtered, N-Order Power-of-Cosine, Sinc FIR Filter [Loxx]Filtered, N-Order Power-of-Cosine, Sinc FIR Filter is a Discrete-Time, FIR Digital Filter that uses Power-of-Cosine Family of FIR filters. This is an N-order algorithm that allows up to 50 values for alpha, orders, of depth. This one differs from previous Power-of-Cosine filters I've published in that it this uses Windowed-Sinc filtering. I've also included a Dual Element Lag Reducer using Kalman velocity, a standard deviation filter, and a clutter filter. You can read about each of these below.

Impulse Response

What are FIR Filters?

In discrete-time signal processing, windowing is a preliminary signal shaping technique, usually applied to improve the appearance and usefulness of a subsequent Discrete Fourier Transform. Several window functions can be defined, based on a constant (rectangular window), B-splines, other polynomials, sinusoids, cosine-sums, adjustable, hybrid, and other types. The windowing operation consists of multipying the given sampled signal by the window function. For trading purposes, these FIR filters act as advanced weighted moving averages.

A finite impulse response (FIR) filter is a filter whose impulse response (or response to any finite length input) is of finite duration, because it settles to zero in finite time. This is in contrast to infinite impulse response (IIR) filters, which may have internal feedback and may continue to respond indefinitely (usually decaying).

The impulse response (that is, the output in response to a Kronecker delta input) of an Nth-order discrete-time FIR filter lasts exactly {\displaystyle N+1}N+1 samples (from first nonzero element through last nonzero element) before it then settles to zero.

FIR filters can be discrete-time or continuous-time, and digital or analog.

A FIR filter is (similar to, or) just a weighted moving average filter, where (unlike a typical equally weighted moving average filter) the weights of each delay tap are not constrained to be identical or even of the same sign. By changing various values in the array of weights (the impulse response, or time shifted and sampled version of the same), the frequency response of a FIR filter can be completely changed.

An FIR filter simply CONVOLVES the input time series (price data) with its IMPULSE RESPONSE. The impulse response is just a set of weights (or "coefficients") that multiply each data point. Then you just add up all the products and divide by the sum of the weights and that is it; e.g., for a 10-bar SMA you just add up 10 bars of price data (each multiplied by 1) and divide by 10. For a weighted-MA you add up the product of the price data with triangular-number weights and divide by the total weight.

What is a Standard Deviation Filter?

If price or output or both don't move more than the (standard deviation) * multiplier then the trend stays the previous bar trend. This will appear on the chart as "stepping" of the moving average line. This works similar to Super Trend or Parabolic SAR but is a more naive technique of filtering.

What is a Clutter Filter?

For our purposes here, this is a filter that compares the slope of the trading filter output to a threshold to determine whether to shift trends. If the slope is up but the slope doesn't exceed the threshold, then the color is gray and this indicates a chop zone. If the slope is down but the slope doesn't exceed the threshold, then the color is gray and this indicates a chop zone. Alternatively if either up or down slope exceeds the threshold then the trend turns green for up and red for down. Fro demonstration purposes, an EMA is used as the moving average. This acts to reduce the noise in the signal.

What is a Dual Element Lag Reducer?

Modifies an array of coefficients to reduce lag by the Lag Reduction Factor uses a generic version of a Kalman velocity component to accomplish this lag reduction is achieved by applying the following to the array:

2 * coeff - coeff

The response time vs noise battle still holds true, high lag reduction means more noise is present in your data! Please note that the beginning coefficients which the modifying matrix cannot be applied to (coef whose indecies are < LagReductionFactor) are simply multiplied by two for additional smoothing .

Whats a Windowed-Sinc Filter?

Windowed-sinc filters are used to separate one band of frequencies from another. They are very stable, produce few surprises, and can be pushed to incredible performance levels. These exceptional frequency domain characteristics are obtained at the expense of poor performance in the time domain, including excessive ripple and overshoot in the step response. When carried out by standard convolution, windowed-sinc filters are easy to program, but slow to execute.

The sinc function sinc (x), also called the "sampling function," is a function that arises frequently in signal processing and the theory of Fourier transforms.

In mathematics, the historical unnormalized sinc function is defined for x ≠ 0 by

sinc x = sinx / x

In digital signal processing and information theory, the normalized sinc function is commonly defined for x ≠ 0 by

sinc x = sin(pi * x) / (pi * x)

For our purposes here, we are used a normalized Sinc function

Included

Bar coloring

Loxx's Expanded Source Types

Signals

Alerts

Related indicators

Variety, Low-Pass, FIR Filter Impulse Response Explorer

STD-Filtered, Variety FIR Digital Filters w/ ATR Bands

STD/C-Filtered, N-Order Power-of-Cosine FIR Filter

STD/C-Filtered, Truncated Taylor Family FIR Filter

STD/Clutter-Filtered, Kaiser Window FIR Digital Filter

STD/Clutter Filtered, One-Sided, N-Sinc-Kernel, EFIR Filt

Granger Causality Flow IndicatorGranger Causality Flow Indicator

█ OVERVIEW

The Granger Causality Flow Indicator is a statistical analysis tool designed to identify predictive relationships between two assets (Symbol X and Symbol Y). In econometrics, "Granger Causality" does not test for actual physical causation (e.g., rain causes mud); rather, it tests for predictive causality .

This script is designed to answer a specific question for traders: "Does the past price action of Asset X provide statistically significant information about the future price of Asset Y, beyond what is already contained in the past prices of Asset Y itself?"

This tool is particularly useful for Pairs Traders , Arbitrageurs , and Macro Analysts looking to identify lead-lag relationships between correlated assets (e.g., BTC vs. ETH, NASDAQ vs. SPY, or Gold vs. Silver).

█ CONCEPTS & CALCULATIONS

To determine if Symbol X "Granger-causes" Symbol Y, this script utilizes a variance-reduction approach based on Auto-Regressive (AR) models. Due to the runtime constraints of Pine Script™, we employ an optimized proxy for the standard Granger test using an AR(1) logic (looking back 1 period).

The calculation performs a comparative test over a rolling window (Default: 50 bars):

The Restricted Model (Baseline):

We attempts to predict the current value of Y using only the previous value of Y (Auto-Regression). We measure the error of this prediction (the "Residuals") and calculate the Variance of the Restricted Model (Var_R) .

The Unrestricted Model (Proxy):

We then test if the past value of X can explain the errors made by the Restricted Model. If X contains predictive power, including it should reduce the error variance. We calculate the remaining Variance of the Unrestricted Model (Var_UR) .

The GC Score:

The script calculates a score based on the ratio of variance reduction:

Score = 1 - (Var_UR / Var_R)

If the Score is High (> 0) : It implies that including X significantly reduced the prediction error for Y. Therefore, X "Granger-causes" Y.

If the Score is Low or 0 : It implies X added no predictive value.

█ HOW TO USE

This indicator is not a simple Buy/Sell signal generator; it is a context filter for cross-asset analysis.

1. Setup

Symbol 1 (X): The potential "Leader" (e.g., BINANCE:BTCUSDT).

Symbol 2 (Y): The potential "Follower" (e.g., BINANCE:ETHUSDT).

Differencing: Enabled by default. This checks the changes in price rather than absolute price, which is crucial for statistical stationarity.

2. Interpreting the Visuals

The script changes the background color and displays a table to indicate the current flow of causality:

Green Background (X → Y): Symbol 1 is leading Symbol 2. Price moves in Symbol 1 are statistically likely to foreshadow moves in Symbol 2.

Orange Background (Y → X): Symbol 2 is leading Symbol 1. The relationship has inverted.

Blue Background (Bidirectional): Both assets are predicting each other (tight coupling or feedback loop).

Gray/No Color: No statistically significant relationship detected.

3. Trading Application

Trend Confirmation: If you trade Symbol Y, wait for the background to turn Green . This indicates that the "Leader" (Symbol X) is currently exerting predictive influence, potentially making trend-following setups on Symbol Y more reliable.

Divergence Warning: If you are trading a correlation pair and the causality breaks (turns Gray), the correlation may be weakening, signaling a higher risk of divergence.

█ SETTINGS

Symbol 1 (X) & Symbol 2 (Y): The two tickers to analyze.

Use Differencing: (Default: True) Converts prices to price-changes. Highly recommended for accurate statistical results to avoid spurious regression.

Calculation Window: The number of bars used to compute the variance and coefficients. Larger windows provide smoother, more stable signals but react slower to regime changes.

Significance Threshold: (0.01 - 0.99) The minimum variance reduction score required to trigger a causal signal.

█ DISCLAIMER

This tool provides statistical analysis of historical price data and does not guarantee future performance. Granger Causality is a measure of predictive capability, not necessarily fundamental causation. Always use appropriate risk management.

TriAnchor Elastic Reversion US Market SPY and QQQ adaptedSummary in one paragraph

Mean-reversion strategy for liquid ETFs, index futures, large-cap equities, and major crypto on intraday to daily timeframes. It waits for three anchored VWAP stretches to become statistically extreme, aligns with bar-shape and breadth, and fades the move. Originality comes from fusing daily, weekly, and monthly AVWAP distances into a single ATR-normalized energy percentile, then gating with a robust Z-score and a session-safe gap filter.

Scope and intent

• Markets: SPY QQQ IWM NDX large caps liquid futures liquid crypto

• Timeframes: 5 min to 1 day

• Default demo: SPY on 60 min

• Purpose: fade stretched moves only when multi-anchor context and breadth agree

• Limits: strategy uses standard candles for signals and orders only

Originality and usefulness

• Unique fusion: tri-anchor AVWAP energy percentile plus robust Z of close plus shape-in-range gate plus breadth Z of SPY QQQ IWM

• Failure mode addressed: chasing extended moves and fading during index-wide thrusts

• Testability: each component is an input and visible in orders list via L and S tags

• Portable yardstick: distances are ATR-normalized so thresholds transfer across symbols

• Open source: method and implementation are disclosed for community review

Method overview in plain language

Base measures

• Range basis: ATR(length = atr_len) as the normalization unit

• Return basis: not used directly; we use rank statistics for stability

Components

• Tri-Anchor Energy: squared distances of price from daily, weekly, monthly AVWAPs, each divided by ATR, then summed and ranked to a percentile over base_len

• Robust Z of Close: median and MAD based Z to avoid outliers

• Shape Gate: position of close inside bar range to require capitulation for longs and exhaustion for shorts

• Breadth Gate: average robust Z of SPY QQQ IWM to avoid fading when the tape is one-sided

• Gap Shock: skip signals after large session gaps

Fusion rule

• All required gates must be true: Energy ≥ energy_trig_prc, |Robust Z| ≥ z_trig, Shape satisfied, Breadth confirmed, Gap filter clear

Signal rule

• Long: energy extreme, Z negative beyond threshold, close near bar low, breadth Z ≤ −breadth_z_ok

• Short: energy extreme, Z positive beyond threshold, close near bar high, breadth Z ≥ +breadth_z_ok

What you will see on the chart

• Standard strategy arrows for entries and exits

• Optional short-side brackets: ATR stop and ATR take profit if enabled

Inputs with guidance

Setup

• Base length: window for percentile ranks and medians. Typical 40 to 80. Longer smooths, shorter reacts.

• ATR length: normalization unit. Typical 10 to 20. Higher reduces noise.

• VWAP band stdev: volatility bands for anchors. Typical 2.0 to 4.0.

• Robust Z window: 40 to 100. Larger for stability.

• Robust Z entry magnitude: 1.2 to 2.2. Higher means stronger extremes only.

• Energy percentile trigger: 90 to 99.5. Higher limits signals to rare stretches.

• Bar close in range gate long: 0.05 to 0.25. Larger requires deeper capitulation for longs.

Regime and Breadth

• Use breadth gate: on when trading indices or broad ETFs.

• Breadth Z confirm magnitude: 0.8 to 1.8. Higher avoids fighting thrusts.

• Gap shock percent: 1.0 to 5.0. Larger allows more gaps to trade.

Risk — Short only

• Enable short SL TP: on to bracket shorts.

• Short ATR stop mult: 1.0 to 3.0.

• Short ATR take profit mult: 1.0 to 6.0.

Properties visible in this publication

• Initial capital: 25000USD

• Default order size: Percent of total equity 3%

• Pyramiding: 0

• Commission: 0.03 percent

• Slippage: 5 ticks

• Process orders on close: OFF

• Bar magnifier: OFF

• Recalculate after order is filled: OFF

• Calc on every tick: OFF

• request.security lookahead off where used

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Fills and slippage vary by venue

• Shapes can move during bar formation and settle on close

• Standard candles only for strategies

Honest limitations and failure modes

• Economic releases or very thin liquidity can overwhelm mean-reversion logic

• Heavy gap regimes may require larger gap filter or TR-based tuning

• Very quiet regimes reduce signal contrast; extend windows or raise thresholds

Open source reuse and credits

• None

Strategy notice

Orders are simulated by TradingView on standard candles. request.security uses lookahead off where applicable. Non-standard charts are not supported for execution.

Entries and exits

• Entry logic: as in Signal rule above

• Exit logic: short side optional ATR stop and ATR take profit via brackets; long side closes on opposite setup

• Risk model: ATR-based brackets on shorts when enabled

• Tie handling: stop first when both could be touched inside one bar

Dataset and sample size

• Test across your visible history. For robust inference prefer 100 plus trades.

Session-Conditioned Regime ATRWhy this exists

Classic ATR is great—until the open. The first few bars often inherit overnight gaps and 24-hour noise that have nothing to do with the intraday regime you actually trade. That inflates early ATR, scrambles thresholds, and invites hyper-recency bias (“today is crazy!”) when it’s just the open being the open.

This tool was built to:

Separate session reality from 24h noise. Measure volatility only inside your defined session (e.g., NYSE 09:30–16:00 ET).

Judge candles against the current regime, not the last 2–3 bars. A rolling statistic from the last N completed sessions defines what “typical” means right now.

Label “large” and “small” objectively. Bars are colored only when True Range meaningfully departs from the session regime—no gut feel, no open-bar distortion (gap inclusion optional).

Overview

Purpose: objectively identify unusually big or small candles within the active trading session, compared to the recent session regime.

Use cases: volatility filters, entry/exit confirmation, session bias detection, adaptive sizing.

This indicator replaces generic ATR with a session-conditioned, regime-aware measure. It colors candles only when their True Range (TR) is abnormally large/small versus the last N completed sessions of the same session window.

How it works

Session gating: Only bars inside the selected session are evaluated (presets for NYSE, CME RTH, FX NY; custom supported).

Per-bar TR: TR = max(high, prevRef) − min(low, prevRef).

prevRef is the prior close for in-session bars.

First bar of the session can include the overnight gap (optional; default off).

Regime statistic: For any bar in session k, aggregate all in-session TRs from the previous N completed sessions (k−N … k−1), then compute Median (default) or Mean.

Today’s anchor: Running statistic from today’s session start → current bar (for context and the on-chart ratio).

Color logic:

Big if TR ≥ bigMult × RegimeStat

Small if TR ≤ smallMult × RegimeStat

Colored states: big bull, big bear, small bull, small bear.

Non-triggering bars retain the chart’s native colors.

Panel (top-right by default)

Regime ATR (Nd): session-conditioned statistic over the past N completed sessions.

Today ATR (anchored): running statistic for the current session.

Ratio (Today/Regime): intraday volatility vs regime.

Sample size n: number of bars used in the regime calculation.

Inputs

Session Preset: NYSE (09:30–16:00 ET), CME RTH (08:30–15:00 CT), FX NY (08:00–17:00 ET), Custom (session + IANA timezone).

Regime Window: number of completed sessions (default 5).

Statistic: Median (robust) or Mean.

Include Open Gap: include overnight gap in the first in-session bar’s TR (default off).

Big/Small thresholds: multipliers relative to RegimeStat (defaults: Big=1.5×, Small=0.67×).

Colors: four independent colors for big/small × bull/bear.

Panel position & text size.

Hidden outputs: expose RegimeStat, TodayStat, Ratio, and Z-score to other scripts.

Alerts

RegimeATR: BIG bar — triggers when a bar meets the “Big” condition.

RegimeATR: SMALL bar — triggers when a bar meets the “Small” condition.

Hidden outputs (for strategies/screeners)

RegimeATR_stat, TodayATR_stat, Today_vs_Regime_Ratio, BarTR_Zscore.

Notes & limitations

No look-ahead: calculations only use information available up to that bar. Historical colors reflect what would have been known then.

Warm-up: colors begin once there are at least N completed sessions; before that, regime is undefined by design.

Changing inputs (session window, multipliers, median/mean, gap toggle) recomputes the full series using the same rolling regime logic per bar.

Designed for standard candles. Styling respects existing chart colors when no condition triggers.

Practical tips

For a broader or tighter notion of “unusual,” adjust Big/Small multipliers.

Prefer Median in markets prone to outliers; use Mean if you want Z-score alignment with the panel’s regime mean/std.

Use the Ratio readout to spot compression/expansion days quickly (e.g., <0.7× = compressed session, >1.3× = expanded).

Roadmap

More session presets:

24h continuous (crypto, index CFDs).

23h/Globex futures (CME ETH with a 60-minute maintenance break).

Regional equities (LSE, Xetra, TSE), Asia/Europe/NY overlaps for FX.

Half-day/holiday templates and dynamic calendars.

Multi-regime comparison: track multiple overlapping regimes (e.g., RTH vs ETH for futures) and show separate stats/ratios.

Robust stats options: trimmed mean, MAD/Huber alternatives; optional percentile thresholds instead of fixed multipliers.

Subpanel visuals: rolling TodayATR and Ratio plots; optional Z-score ribbon.

Screener/strategy hooks: export boolean series for BIG/SMALL, plus a lightweight strategy template for backtesting entries/exits conditioned on regime volatility.

Performance/QOL: per-symbol presets, smarter warm-up, and finer control over sample caps for ultra-low TF charts.

Changelog

v0.9b (Beta)

Session presets (NYSE/CME RTH/FX NY/Custom) with timezone handling.

Panel enhancements: ratio + sample size n.

Four-state bar coloring (big/small × bull/bear).

Alerts for BIG/SMALL bars.

Hidden Z-score stream for downstream use.

Gap-in-TR toggle for the first in-session bar.

Disclaimer

For educational purposes only. Not investment advice. Validate thresholds and session settings across symbols/timeframes before live use.

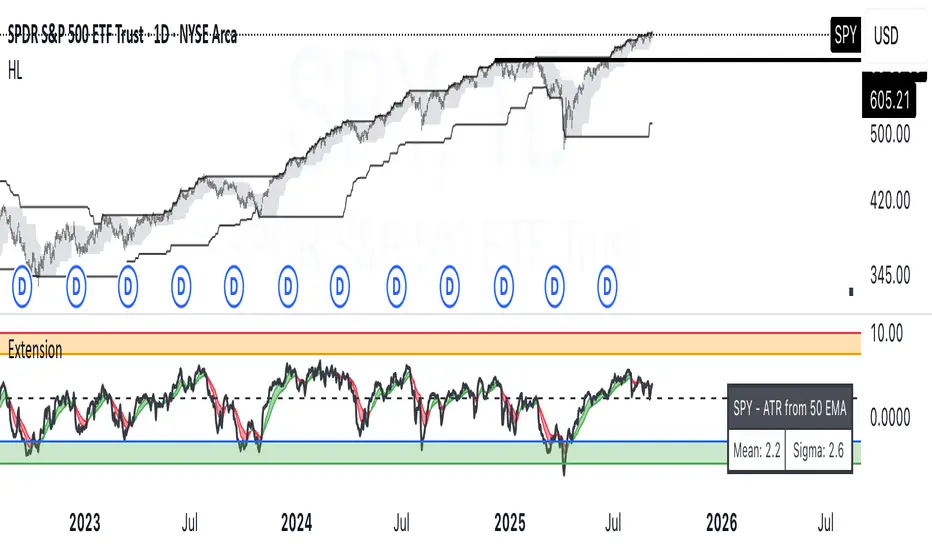

ATR Extension from Moving Average, with Robust Sigma Bands

# ATR Extension from Moving Average, with Robust Sigma Bands

**What it does**

This indicator measures how far price is from a selected moving average, expressed in **ATR multiples**, then overlays **robust sigma bands** around the long run central tendency of that extension. Positive values mean price is extended above the MA, negative values mean price is extended below the MA. The signal adapts to volatility through ATR, which makes comparisons consistent across symbols and regimes.

**Why it can help**

* Normalizes distance to an MA by ATR, which controls for changing volatility

* Uses the **bar’s extreme** against the MA, not just the close, so it captures true stretch

* Computes a **median** and **standard deviation** of the extension over a multi-year window, which yields simple, intuitive bands for trend and mean-reversion decisions

---

## Inputs

* **MA length**: default 50, options 200, 64, 50, 20, 9, 4, 3

* **MA timeframe**: Daily or Weekly. The MA is computed on the chosen higher timeframe through `request.security`.

* **MA type**: EMA or SMA

* **Years lookback**: 1 to 10 years, default 5. This sets the sample for the median and sigma calculation, `years * 365` bars.

* **Line width**: visual width of the plotted extension series

* **Table**: optional on-chart table that displays the current long run **median** and **sigma** of the extension, with selectable text size

**Fixed parameters in this release**

* **ATR length**: 20 on the daily timeframe

* **ATR type**: classic ATR. ADR percent is not enabled in this version.

---

## Plots and colors

* **Main plot**: “Extension from 50d EMA” by default. Value is in **ATR multiples**.

* **Reference lines**:

* `median` line, black dashed

* +2σ orange, +3σ red

* −2σ blue, −3σ green

---

## How it is calculated

1. **Moving average** on the selected higher timeframe: EMA or SMA of `close`.

2. **Extreme-based distance** from MA, as a percent of price:

* If `close > MA`, use `(high − MA) / close * 100`

* Else, use `(low − MA) / close * 100`

3. **ATR percent** on the daily timeframe: `ATR(20) / close * 100`

4. **ATR multiples**: extension percent divided by ATR percent

5. **Robust center and spread** over the chosen lookback window:

* Center: **median** of the ATR-multiple series

* Spread: **standard deviation** of that series

* Bands: center ± 1σ, 2σ, 3σ, with 2σ and 3σ drawn

This design yields an intuitive unit scale. A value of **+2.0** means price is about 2 ATR above the selected MA by the most stretched side of the current bar. A value of **−3.0** means roughly 3 ATR below.

---

## Practical use

* **Trend continuation**

* Sustained readings near or above **+1σ** together with a rising MA often signal healthy momentum.

* **Mean reversion**

* Spikes into **±2σ** or **±3σ** can identify stretched conditions for fade setups in range or late-trend environments.

* **Regime awareness**

* The **median** moves slowly. When median drifts positive for many months, the market spends more time extended above the MA, which often marks bullish regimes. The opposite applies in bearish regimes.

**Notes**

* The MA can be set to Weekly while ATR remains Daily. This is deliberate, it keeps the normalization stable for most symbols.

* On very short intraday charts, the extension remains meaningful since it references the session’s extreme against a higher-timeframe MA and a daily ATR.

* Symbols with short histories may not fill the lookback window. Bands will adapt as data accrues.

---

## Table overlay

Enable **Table → Show** to see:

* “ATR from \”

* Current **median** and **sigma** of the extension series for your lookback

---

## Recommended settings

* **Swing equities**: 50 EMA on Daily, 5 to 7 years

* **Index trend work**: 200 EMA on Daily, 10 years

* **Position trading**: 20 or 50 EMA on Weekly MA, 5 to 10 years

---

## Interpretation examples

* Reading **+2.7** with price above a rising 50 EMA, near prior highs

* Strong trend extension, consider pyramiding in trend systems or waiting for a pullback if you are a mean-reverter.

* Reading **−2.2** into multi-month support with flattening MA

* Stretch to the downside that often mean-reverts, size entries based on your system rules.

---

## Credits

The concept of measuring stretch from a moving average in ATR units has a rich community history. This implementation and its presentation draw on ideas popularized by **Jeff Sun**, **SugarTrader**, and **Steve D Jacobs**. Thanks to each for their contributions to ATR-based extension thinking.

---

## License

This script and description are distributed under **MPL-2.0**, consistent with the header in the source code.

---

## Changelog

* **v1.0**: Initial public release. Daily ATR normalization, EMA or SMA on D or W timeframe, robust median and sigma bands, optional table.

---

## Disclaimer

This tool is for educational use only. It is not financial advice. Always test on your own data and strategies, then manage risk accordingly.

KST Strategy [Skyrexio]Overview

KST Strategy leverages Know Sure Thing (KST) indicator in conjunction with the Williams Alligator and Moving average to obtain the high probability setups. KST is used for for having the high probability to enter in the direction of a current trend when momentum is rising, Alligator is used as a short term trend filter, while Moving average approximates the long term trend and allows trades only in its direction. Also strategy has the additional optional filter on Choppiness Index which does not allow trades if market is choppy, above the user-specified threshold. Strategy has the user specified take profit and stop-loss numbers, but multiplied by Average True Range (ATR) value on the moment when trade is open. The strategy opens only long trades.

Unique Features

ATR based stop-loss and take profit. Instead of fixed take profit and stop-loss percentage strategy utilizes user chosen numbers multiplied by ATR for its calculation.

Configurable Trading Periods. Users can tailor the strategy to specific market windows, adapting to different market conditions.

Optional Choppiness Index filter. Strategy allows to choose if it will use the filter trades with Choppiness Index and set up its threshold.

Methodology

The strategy opens long trade when the following price met the conditions:

Close price is above the Alligator's jaw line

Close price is above the filtering Moving average

KST line of Know Sure Thing indicator shall cross over its signal line (details in justification of methodology)

If the Choppiness Index filter is enabled its value shall be less than user defined threshold

When the long trade is executed algorithm defines the stop-loss level as the low minus user defined number, multiplied by ATR at the trade open candle. Also it defines take profit with close price plus user defined number, multiplied by ATR at the trade open candle. While trade is in progress, if high price on any candle above the calculated take profit level or low price is below the calculated stop loss level, trade is closed.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.5, number of ATRs to calculate stop-loss level)

ATR Take Profit (by default = 3.5, number of ATRs to calculate take profit level)

Filter MA Type (by default = Least Squares MA, type of moving average which is used for filter MA)

Filter MA Length (by default = 200, length for filter MA calculation)

Enable Choppiness Index Filter (by default = true, setting to choose the optional filtering using Choppiness index)

Choppiness Index Threshold (by default = 50, Choppiness Index threshold, its value shall be below it to allow trades execution)

Choppiness Index Length (by default = 14, length used in Choppiness index calculation)

KST ROC Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #2 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #3 (by default = 20, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #4 (by default = 30, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #2 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)