BTC VIP EMA CROSS Buy/Sell (GC & DC)EMA cross 5&10 standard-setting with add on of BUY/SELL signal ( GC & DC) which will make the traders have an indication of buy and sell easily and clearly.

An exponential moving average strategy, or EMA strategy, is used to identify the predominant trend in the market. It can also provide the support and resistance level to execute your trade. Indicators: v4 (default setting), EMA 5 10 Crossover (default setting)

Preferred Time Frame(s):15-Minute, 30-Minute, 1-Hour, 4-Hour, 1-Day

Strategy

Long Entry Rules

Enter a buy in the market if the following indicator or chart pattern takes center stage:

If the blue upward pointing arrow of the EMA 5 10 Crossover custom indicator gets aligned just somewhat below the candlesticks as seen in Fig. 1.0, the market sentiment is said to be bullish, hence a trigger to go long on the pair of interest.

If the light blue line of the custom indicator gets outlined just below price bars as illustrated in Fig. 1.0, price is said to be pushed somewhat higher i.e. a trigger to buy the asset of focus.

Exit Strategy/Take Profit for Buy Entry

Exit or take profit if the following rules or conditions takes precedence:

If the red downward pointing arrow of the EMA 5 10 Crossover custom indicator forms above price bars as depicted in Fig. 1.0 while a buy signal is ongoing in the market, a possible price dip is said to be looming, as such an exit or take profit is advised.

If the red line of the custom indicator forms above the candlestick during a bullish trend, it is a pointer to a possible price dip, hence an exit or take profit is advised.

Pesquisar nos scripts por "中国+10年期美债+购买数据"

Intrinsic value calculation Intrinsic value calculator based on Warren Buffet's and Ben Graham's work

In value investing determing the true value of a COMPANY instead of a stock price is crucial.

This little indicator shows the "Intrinsic value" of the choosen stock meaning the value of the stock in 10 years time. Calculation is based on historical book value's average annual growth rate and dividends paid.

Since this is about long therm investing, use monthly charts.

"Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.”

– Warren Buffett

One way to calculate that is by the growth in per share book value and dividends taken in the forseeable future (10 years) than discount it with the prevailing 10 year note's rate.

In the inputs you have to set 2 variables:

1. How many years back you have the first data for book value per share available?

2. What was the per share book value that year?

(Bookvalue is ploted in olive colour and you can get the oldest one if you move your cursor over the latest data on the left)

CAUTION! You have to reenter it for every stock you analyse as this is stock-specific data!

After setting the input data, you will see the "Intrinsic Value"'s pink curve ploted over the price chart.

If the price is well below the pink line, the company is undervalued and can be a possible applicant for long therm investment.

Margin of safety: when the current price is 50% below the intrinsic value that means a 10% yearly growth potential (100% growth in 10 years) or a 100% margin of safety.

I am a beginer in Pine so please excuse my coding...

If anybody knows hot to extract historical data from 15 years ago, please share it with me, so I can automate the whole calculation without inputs necessary.

M-OscillatorM-Oscillator developed By Mohamed Fawzy, MFTA, CFTe

as Written in IFTA Journal 2018 Edition

more info : ifta.org

Interpretation

• M-Oscillator is a bounded oscillator that moves between (-14) and (+14),

• Movement above 10 is considered overbought, and movement below -10 is oversold.

Overbought/Oversold rule:

• Buy when the M-Oscillator violates the (-10) level to the downside and crosses back to the upside.

• Sell when the M-Oscillator crosses above the (+10) level and crosses back to the downside.

Crossover on Extreme Levels

• Sell signals are triggered when the M-Oscillator crosses its signal line above (13), which indicates an extreme market condition

• Buy signals are triggered when the M-Oscillator crosses its signal line below (- 13)

2-Period RSI strategy (with filter)2-period RSI strategy backtest described in several books of the trader Larry Connors . This strategy uses a 2 periods RSI , one slow arithmetic moving average and one fast arithmetic moving average.

Entry signal:

- RSI 2 value below oversold level (Larry Connors usually sets oversold to be below 5, but other authors prefer to work below 10 due to the higher number of signals).

- Closing above the slow average (200 periods).

- Entry at closing of candle or opening of next candle.

Exit signal:

- Occurs when the candlestick closes above the fast average (the most common fast average is 5 periods, but some traders also suggest the 10 period average).

Entry Filter (modification made by me):

- Applied an RSI2 arithmetic moving average to smooth out oscillations.

- Entered only when RSI2 is below oversold level and RSI2 moving average is below 30.

* NOTE: In the stocks that I evaluate daily the averages of 4 and 6 periods work very well as a filter.

Comments:

This strategy works very well in Daily charts but can be applied in other chart times as well. As this is a strategy to catch market fluctuations, it presents different results with different stocks.

I have been applying this strategy to the stocks of the Brazilian market (BOVESPA) and have enjoyed the result. Every day I evaluate the stocks that are generating entry signals and choose which one to trade based on the stocks with the highest Profit Value.

The RSI 2 averaging filter probably will reduce profit of the backtests because reduces the number of signals, but the Profit Value will usually increase. For me this was a good thing because without the filter, this strategy usually shows more signals than I have capital to allocate.

Before entering a trade I look at which fast average the paper has the highest Profit Value and then I use this average as my output signal for that trade (this change has greatly improved the result of the outputs).

This strategy does not use Stop Loss because normally Stop Loss decreases effectiveness (profit). In any case, the option to apply a percentage Stop Loss if desired is added in the script. As the strategy does not use stop, extra caution with risk management is advisable. I advise not to allocate more than 20% of the trade capital in the same operation.

I'm still studying ways to improve this strategy, but so far this is the best setup I've found. Suggestions are always welcome and we can test to see if they improve the backtest result.

Good luck and good trades.

================================================

Backtest das estratégia do IFR de 2 períodos descrita em varios livros do trader Larry Connors . Esta estratégia usa um IFR de 2 períodos, uma média movel aritmética lenta e uma média movel aritmética rápida.

Sinal de entrada:

- Valor do IFR 2 abaixo do nível de sobrevenda (Larry Connors usualmente define sobrevenda sendo abaixo de 5, mas outros autores preferem trabalhar abaixo de 10 devido ao maior número de sinais).

- Fechamento acima da média lenta (200 períodos).

- Realizado a compra no fechamento do candle ou na abertura do candle seguinte.

Sinal de saída:

- Ocorre quando o candle fecha acima da média rápida (a média rápida mais comum é a de 5 períodos, mas alguns traders sugerem também a média de 10 períodos).

Filtro para entrada (modificação feita por mim):

- Aplicado uma média móvel aritmética do IFR2 para suavisar as oscilações.

- Realizado a entrada apenas quando o IFR2 está abaixo do nível de sobrevenda e a média móvel do IFR2 está abaixo de 30.

*OBS: nos ativos que avalio diariamente as médias de 4 e 6 períodos funcionam muito bem como filtro.

Comentários:

Esta estratégia funciona muito bem no tempo gráfico Diário mas pode ser aplicada tambem em outros tempos gráficos. Como trata-se de uma estratégia para pegar oscilações do mercado, ela apresenta diferentes resultados com diferentes ativos.

Eu venho aplicando esta estratégia nos ativos do mercado brasileiro (BOVESPA) e tenho gostado do resultado. Diariamente eu avalio os papeis que estão gerando entrada e escolho qual irei realizar o trade baseado nos papeis que apresentam maior Profit Value.

O filtro da média do IFR 2 reduz o lucro nos backtests pois reduz também a quantidade de sinais, mas em compensação o Profit Value irá normalmente aumentar. Para mim isto foi algo positivo pois, sem o filtro, normalmente esta estratégia apresenta mais sinais do que possuo capital para alocar.

Antes de entrar em um trade eu olho em qual média rápida o papel apresenta maior Profit Value e então eu utilizo está média como meu sinal de saída para aquele trade (esta mudança tem melhorado bastante o resultado das saídas).

Está estratégia não utiliza Stop Loss pois normalmente o Stop Loss diminui a eficácia (lucro). De qualquer maneira, foi acrescentado no script a opção de aplicar um Stop Loss percentual caso seja desejado. Como a estratégia não utiliza stop é aconselhável um cuidado redobrado com o gerenciamento de risco. Eu aconselho não alocar mais de 20% do capital de trade em uma mesma operação.

Ainda estou estudando formas de melhorar esta estratégia, mas até o momento está é a melhor configuração que encontrei. Sugestões são sempre bem vindas e podemos testar para verificar se melhoram o resultado do backtest.

Boa sorte e bons trades.

Pinescript v3 Compatibility Framework (v4 Migration Tool)Pinescript v3 Compatibility Framework (v4 Migration Tool)

This code makes most v3 scripts work in v4 with only a few minor changes below. Place the framework code before the first input statement.

You can totally delete all comments.

Pros:

- to port to v4 you only need to make a few simple changes, not affecting the core v3 code functionality

Cons:

- without #include - large redundant code block, but can be reduced as needed

- no proper syntax highlighting, intellisence for substitute constant names

Make the following changes in v3 script:

1. standard types can't be var names, color_transp can't be in a function, rename in v3 script:

color() => color.new()

bool => bool_

integer => integer_

float => float_

string => string_

2. init na requires explicit type declaration

float a = na

color col = na

3. persistent var init (optional):

s = na

s := nz(s , s) // or s := na(s ) ? 0 : s

// can be replaced with var s

var s = 0

s := s + 1

___________________________________________________________

Key features of Pinescript v4 (FYI):

1. optional explicit type declaration/conversion (you still can't cast series to int)

float s

2. persistent var modifier

var s

var float s

3. string series - persistent strings now can be used in cond and output to screen dynamically

4. label and line objects

- can be dynamically created, deleted, modified using get/set functions, moved before/after the current bar

- can be in if or a function unlike plot

- max limit: 50-55 label, and 50-55 line drawing objects in addition to already existing plots - both not affected by max plot outputs 64

- can only be used in the main chart

- can serve as the only output function - at least one is required: plot, barcolor, line, label etc.

- dynamic var values (including strings) can be output to screen as text using label.new and to_string

str = close >= open ? "up" : "down"

label.new(bar_index, high, text=str)

col = close >= open ? color.green : color.red

label.new(bar_index, na, "close = " + tostring(close), color=col, textcolor=color.white, style=label.style_labeldown, yloc=yloc.abovebar)

// create new objects, delete old ones

l = line.new(bar_index, high, bar_index , low , width=4)

line.delete(l )

// free object buffer by deleting old objects first, then create new ones

var l = na

line.delete(l)

l = line.new(bar_index, high, bar_index , low , width=4)

Turtle Trade Channels by KıvanÇ fr3762his trend following system was designed by Dennis Gartman and Bill Eckhart, and relies on breakouts of historical highs and lows to take and close trades: it is the complete opposite to the "buy low and sell high" approach. This trend following system was taught to a group of average and normal individuals, and almost everyone turned into a profitable trader.

The main rule is "Trade an N-day breakout and take profits when an M-day high or low is breached (N must me above M)". Examples:

Buy a 10-day breakout and close the trade when price action reaches a 5-day low.

Go short a 20-day breakout and close the trade when price action reaches a 10-day high.

In this indicator, the red line is the trading line, and the dotted blue line is the exit line. Original system is:

Go long when the trading line crosses below close price

Go short when the trading line rosses above close price

Exit long positions when the price touches the exit line

Exit short positions when the price touches the exit line

Recommended initial stop-loss is ATR * 2 from the opening price. Default system parameters were 20,10 and 55,20.

Original Turtle Rules:

To trade exactly like the turtles did, you need to set up two indicators representing the main and the failsafe system.

Set up the main indicator with TradePeriod = 20 and StopPeriod = 10 (A.k.a S1)

Set up the failsafe indicator with TradePeriod = 55 and StopPeriod = 20 using a different color. (A.k.a S2)

The entry strategy using S1 is as follows

Buy 20-day breakouts using S1 only if last signaled trade was a loss.

Sell 20-day breakouts using S1 only if last signaled trade was a loss.

If last signaled trade by S1 was a win, you shouldn't trade -Irregardless of the direction or if you traded last signal it or not-

The entry strategy using S2 is as follows:

Buy 55-day breakouts only if you ignored last S1 signal and the market is rallying without you

Sell 55-day breakouts only if you ignored last S1 signal and the market is pluging without you

The turtles had a progressive position sizing approach that boosted their winnings. Once a trading decision has been made you should...

Developers: Dennis Gartman and Bill Eckhart

İndikatörü geliştiren: Dennis Gartman and Bill Eckhart

Amazing Crossover System - 100+ pips per day!I got the main concept for this system on another site. While I have made one important change, I must stress that the heart of this system was created by someone else! We must give credit where credit is due!

Y'all know baby pips. @ForexPhantom published about this system and did both back and forward test around 10 years ago.

I found it on the sit and now I put it to code to see how it performs. I assume 10 points spread for every trade. I use Renesource or AxiTrader to get the low spreads.

There are 2 mods, the single trades and constant trading on the direction.

Main concept

Indicators

5 EMA -- YELLOW

10 EMA -- RED

RSI (10 - Apply to Median Price: HL/2) -- One level at 50.

TIME FRAME

1 Hour Only (very important!)

PAIRS

Virtually any pair seems to work as this is strictly technical analysis.

I recommend sticking to the main currencies and avoiding cross currencies (just his preference).

WHEN TO ENTER A TRADE

Enter LONG when the Yellow EMA crosses the Red EMA from underneath.

RSI must be approaching 50 from the BOTTOM and cross 50 to warrant entry.

Enter SHORT when the Yellow EMA crosses the Red EMA from the top.

RSI must be approaching 50 from the TOP and cross 50 to warrant entry.

I've attached a picture which demonstrates all these conditions.

That's it!

f.bpcdn.co

Trend Score by KIVANÇ fr3762Trend Score compares close prices between last close with previous closes by a certain period of time.

It's like momentum but gives a score +1 when close price is equal to or above (defaultly) 10 bars ago and gives a score of -1 when below.

calculation continues from default length to the 2 times of length.

Defaultly (for 10 bars length)

If Trend Score converges to 10; that means there's a strong uptrend

conversely if Trend Score converges to -10; that means a strong downtrend market is on.

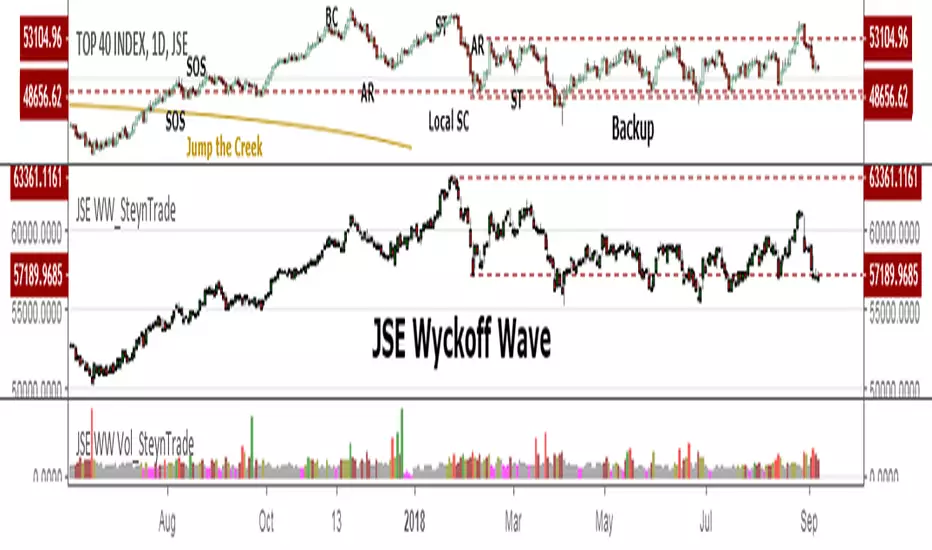

JSE Wyckoff Wave Volume Code// The Stock Market Institute (SMI) describes an propriety indicator the "SMI Wyckoff Wave" for US Stocks. This code is an attempt to make a Wyckoff Wave for the Johannesburg Stock Exchange (JSE).

// The JSE Wyckoff Wave is in a separate code. This is the code for the volume of the wave. Please see code for the JSE Wyckoff Wave which goes with this indicator.

//

// The Wave presents a normalized price for the 10 selected stocks (An Index for the 10 stocks).

// The theory is to select stocks that are widely held, market leaders, actively traded and participate in important market moves.

// This is only my attempt to select 10 stocks and a different selection can be made.

// I am not certain how SMI determine their weightings but what I have done it to equalize the Rand value of the stock volumne so that moves are of equal magnitude.

// The then provides a view of the overall condition of the market and volume flow in the market.

//

// I have used the September 2018 price to normalize the stock price for the 10 selected stocks based. The stocks and weightings can be changed periodically depending on the performance and leadership.

//

// Please, let me know if there is a better work around this.

The stocks and their weightings are:

"JSE:BTI"/0.79

"JSE:SHP"/2.87

"JSE:NPN"/0.18

"JSE:AGL"/1.96

"JSE:SOL"/1.0

"JSE:CFR"/4.42

"JSE:MND"/1.40

"JSE:MTN"/7.63

"JSE:SLM"/7.29

"JSE:FSR"/8.25

JSE Wyckoff WaveThe Stock Market Institute (SMI) describes an propriety indicator the "SMI Wyckoff Wave" for US Stocks. This code is an attempt to make a Wyckoff Wave for the Johannesburg Stock Exchange (JSE). Once the wave has been established the volume can also be calculated. Please see code for the JSE Wyckoff Wave Volume which goes with this indicator.

The Wave presents a normalized price for the 10 selected stocks (An Index for the 10 stocks). The theory is to select stocks that are widely held, market leaders, actively traded and participate in important market moves. This is only my attempt to select 10 stocks and a different selection can be made. I am not certain how SMI determine their weightings but what I have done it to equalize the Rand value of the stock so that moves are of equal magnitude. The then provides a view of the overall condition of the market and volume flow in the market.

I have used the September 2018 price to normalize the stock price for the 10 selected stocks based. The stocks and weightings can be changed periodically depending on the performance and leadership.

Most Indecies when constructed assume that all high prices and all low prices happen at the same time and therefor inflate the wicks of the bars. To make the wave more representatives for the SMI Wyckoff Wave the price is determined on the 5 minute timeframe which removes this bias. However, TradingView does not calculate properly when selecting a lower timeframe than in current period. A work around is to call the sma of the highs and add these which provides more realistic tails. Please, let me know if there is a better work around this.

The stocks and their weightings are:

"JSE:BTI"*0.79

"JSE:SHP"*2.87

"JSE:NPN"*0.18

"JSE:AGL"*1.96

"JSE:SOL"*1.0

"JSE:CFR"*4.42

"JSE:MND"*1.40

"JSE:MTN"*7.63

"JSE:SLM"*7.29

"JSE:FSR"*8.25

OHLC Daily Resolution BandsShout out to nPE- for the idea.

Bands made with stdev from 10 day OHLC.

Keeps resolution to daily, so you can use bands as daily pivots for day trading.

Upper band 1=yesterday close + 0.5 std(ohlc,10)

Upper band 1=yesterday close + 1 std(ohlc,10)

Mid=yesterday close

Lower band 1=yesterday close - 0.5 std(ohlc,10)

Lower band 2=yesterday close - 1 std(ohlc,1

XPloRR MA-Buy ATR-Trailing-Stop Long Term Strategy Beating B&HXPloRR MA-Buy ATR-MA-Trailing-Stop Strategy

Long term MA Trailing Stop strategy to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the EMA(blue) crossing over the SMA curve(orange).

My sell strategy is triggered by another EMA(lime) of the close value crossing the trailing stop(green) value.

The trailing stop value(green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between high and low values.

Every stock has it's own "DNA", so first thing to do is find the right parameters to get the best strategy values voor EMA, SMA and Trailing Stop.

Then keep using these parameter for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Here are the parameters:

Exponential MA: buy trigger when crossing over the SMA value (use values between 11-50)

Simple MA: buy trigger when EMA crosses over the SMA value (use values between 20 and 200)

Stop EMA: sell trigger when Stop EMA of close value crosses under the trailing stop value (use values between 8 and 16)

Trailing Stop #ATR: defines the trailing stop value as a multiple of the ATR(15) value

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now):

BAR(Barco): EMA=11, SMA=82, StopEMA=12, Stop#ATR=9

Buy&HoldProfit: 45.82%, NetProfit: 294.7%, #Trades:8, %Profit:62.5%, ProfitFactor: 12.539

AAPL(Apple): EMA=12, SMA=45, StopEMA=12, Stop#ATR=6

Buy&HoldProfit: 2925.86%, NetProfit: 4035.92%, #Trades:10, %Profit:60%, ProfitFactor: 6.36

BEKB(Bekaert): EMA=12, SMA=42, StopEMA=12, Stop#ATR=7

Buy&HoldProfit: 81.11%, NetProfit: 521.37%, #Trades:10, %Profit:60%, ProfitFactor: 2.617

SOLB(Solvay): EMA=12, SMA=63, StopEMA=11, Stop#ATR=8

Buy&HoldProfit: 43.61%, NetProfit: 151.4%, #Trades:8, %Profit:75%, ProfitFactor: 3.794

PHIA(Philips): EMA=11, SMA=80, StopEMA=8, Stop#ATR=10

Buy&HoldProfit: 56.79%, NetProfit: 198.46%, #Trades:6, %Profit:83.33%, ProfitFactor: 23.07

I am very curious to see the parameters for your stocks and please make suggestions to improve this strategy.

Mattzab ArrowsMattzab Arrows

THE BASICS

Buy and Sell Signal Arrows

Tack Marks to show how close the next opposite arrow might be- showing possible trend reversals

Standard Bollinger Bands

10-Day SMA Line

Configurable

Open Source

THE NITTY GRITTY

For starters, all values listed below can be changed in the settings. Length of time, as well as source, can be changed. For the Hidden EMA, this can be made visible by increasing its transparency.

ARROWS

The buy and sell signal arrows are based on price and MACD histogram.

The MACD settings are as follows: 10 day fast EMA , 20 day slow EMA , 5 day SMA signal smoothing. Instead of close price, we are using the average point of the day's high, low, and close.

For the arrows, current price and yesterday's price are using hl2 for high/low average.

A BUY arrow is created when:

Current Price IS GREATER THAN Previous Price _AND_ Current MACD Histogram IS GREATER THAN Previous MACD Histogram.

Important Note! Because the MACD Histogram repaints, the buy arrows may appear, then disappear later in the day, if the MACD changes. Check on the changelog to see if I've fixed it by the time you're reading this. (TradingView doesn't let you edit the description after it's been posted)

A SELL arrow is created when:

Current Price IS LESS THAN Previous Price _AND_ Current MACD Histogram IS LESS THAN Yesterday's MACD Histogram _AND_ Close Price is below _EITHER_ the Hidden EMA (default set to 4) _OR_ the Visible SMA (Default set to 10, which is the black line).

The hidden EMA can be made visible by increasing it's transparency in the Style tab.

Including the requirement to only sell if the standard conditions are met, PLUS being below one of those moving average lines, helps to prevent false sell arrows and repainting.

TACK MARKS

The Red Tack is the threshold, or barrier, for the next arrow. It will not move. It is based on previous High/Low/Close Price + MACD.

The Blue Tack is the current point in space for our average Price and MACD Delta Values. It will move throughout the day (or hour or minute depending on your resolution). The Blue Tack will give you an indication of how close or how far from the reversal threshold (Red Tack) the ticker is at that point.

While the Blue Tack is ABOVE Red, the most recent signal arrow will be a buy, and we are in a buy/hold period.

While the Blue Tack is BELOW Red, the most recent signal arrow will be a sell, and we are in a sell/wait period.

If the Blue Tack crosses above or below Red, you'll get the next arrow.

MOVING AVERAGE LINES

There are three moving average lines in this indicator.

The first is black, and is by default a 10-Day Simple Moving Average Line.

This black line is a good safeguard against selling too early. This is a good support line and that's how I use it.

The second is invisible, but can be made visible in the Styling, and is by default a 4-Day Exponential Moving Average Line

The third is the blue 20-Day Bollinger Band line.

BOLLINGER BANDS

The Bollinger Bands are unmodified and are just a background indicator for your use. If you prefer not to see the Bollinger Bands , change their transparency to 0% to hide them. I've cleaned up the Bollinger Bands to make the indicator as a whole- easier on the eyes.

Please leave feedback on how the script works for you, if you run into problems, if you have any changes you'd like to see, etc.

MACDouble + RSI (rec. 15min-2hr intrv) Uses two sets of MACD plus an RSI to either long or short. All three indicators trigger buy/sell as one (ie it's not 'IF MACD1 OR MACD2 OR RSI > 1 = buy", its more like "IF 1 AND 2 AND RSI=buy", all 3 match required for trigger)

The MACD inputs should be tweaked depending on timeframe and what you are trading. If you are doing 1, 3, 5 min or real frequent trading then 21/44/20 and 32/66/29 or other high value MACDs should be considered. If you are doing longer intervals like 2, 3, 4hr then consider 9/19/9 and 21/44/20 for MACDs (experiment! I picked these example #s randomly).

Ideal usage for the MACD sets is to have MACD2 inputs at around 1.5x, 2x, or 3x MACD1's inputs.

Other settings to consider: try having fastlength1=macdlength1 and then (fastlength2 = macdlength2 - 2). Like 10/26/10 and 23/48/20. This seems to increase net profit since it is more likely to trigger before major price moves, but may decrease profitable trade %. Conversely, consider FL1=MCDL1 and FL2 = MCDL2 + (FL2 * 0.5). Example: 10/26/10 and 22/48/30 this can increase profitable trade %, though may cost some net profit.

Feel free to message me with suggestions or questions.

Kay_BBandsV3This is the 3rd version of Kay_BBands.

When +DI (Directional Index ) is above -DI , then Upper band will be visible and vice-versa.

This is when the ADX is above the threshold. 28 is the default in this version. I found its more appealing in 5M time frame.

BLUE - ADX under 10

GREEN - Uptrend, ADX over 10

RED - Downtrend, ADX over 10

Use it with another band with setting 20, 0.6 deviation. Prices keeping above or below the 2nd bands upper or lower bounds shows trending conditions.

I didn't know how to update the old script so published it again.

Changes - :

1) Updated default settings for the indicator

2) ADX setting are now DI (28), ADX (10), adx level to check is 10.

3) IMPORTANT one - When DI is up/down, lower/upper band will also have color (more visible that way.)

Play around the settings.. It really eliminates extra indicator checking visually... Please like if you think idea is good.

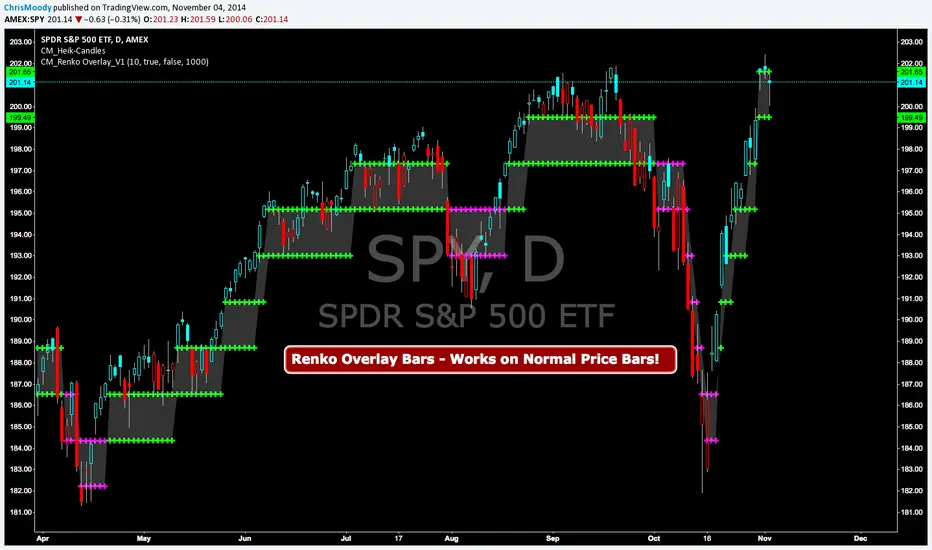

CM Renko Overlay BarsCM_Renko Overlay Bars V1

Overlays Renko Bars on Regular Price Bars.

Default Renko plot is based on Average True Range. Look Back period adjustable in Inputs Tab.

If you Choose to use "Traditional" Renko bars and pick the Size of the Renko Bars the please read below.

Value in Input Tab is multiplied by .001 (To work on Forex)

1 = 10 pips on EURUSD - 1 X .001 = .001 or 10 Pips

10 = .01 or 100 Pips

1000 = 1 point to the left of decimal. 1 Point in Stocks etc.

10000 = 10 Points on Stocks etc.

***V2 will fix this issue.

Custom Indicator - No Trade Zone Warning Back Ground Highlights!Years ago I did an analysis of my trades. Every period of the day was profitable except for two. From 10:00-1030, and 1:00 to 1:30. (I was actively Day Trading Futures) Imagine a vertical graph broken down in to 30 minute time segments. I had nice Green bars in every time slot (Showing Net Profits), and HUGE Red Bars from 10 to 10:30 and 1 to 1:30. After analysis I found I made consistent profits at session open, but then I would enter in to bad setups around 10 to make more money. I also found after I took lunch when I came back at 1:00 I would force trades instead of patiently waiting for a great trade setup. I created an indicator that plotted a red background around those times telling me I was not allowed to enter a trade. Profits went up!!! Details on How to adjust times are in 1st Post. You can adjust times and colors to meet your own trading needs.

Cycle Momentum Filter [JopAlgo]Cycle Momentum Filter (CMF) — spot “when” to engage the market, on any timeframe

Markets breathe in cycles (expansion → contraction) while momentum and trend decide which moves actually travel. CMF is a compact filter that blends those ideas so you can answer two questions before you click:

Is this a good moment to take a trade? (cycle position)

If I take it, is there enough force behind the move to carry it? (momentum + trend)

CMF does not replace your levels—use it with your location tools (e.g., Volume Profile v3.2 and Anchored VWAP). It simply keeps you out of entries taken at the wrong part of the swing or against weak momentum.

(When you add screenshots: image #1 should label each sub-line and the green/yellow/red background; image #2 can show CMF turning green at VAL + AVWAP before a rotation back to POC.)

What you’re seeing (and how to read it at a glance)

CMF draws five sub-lines around a zero line, plus a background color:

Cycle Oscillator (blue): where you are in the swing. Above zero ≈ cycle crest side; below zero ≈ trough side.

ROC % (purple): short-term price acceleration. Above zero = positive momentum; below zero = negative.

MACD Histogram (orange): classic impulse measure (fast–slow EMA gap). Above zero = bullish impulse.

EWO (cyan): Elliott Wave Oscillator (EMA fast – EMA slow). Above zero = trend tilt up.

RSI-MA (gray, plotted as RSI−50): smoothed RSI relative to 50. Above zero = buyers have the relative strength.

Background color = the filter result:

Green → bullish window: cycle favors longs and momentum/trend/RS confirm.

Red → bearish window: mirror logic.

Yellow → neutral: at least one piece disagrees—do less, or wait for alignment.

For new traders: Every sub-line crossing above/below zero is a yes/no vote. Green happens only when all bullish checks are true; red when all bearish checks are true.

How CMF is built (plain-English version)

Cycle (DPO-style): CMF subtracts a displaced SMA from price to remove trend and expose the swing. Below 0 = you’re on the dip side of the cycle; above 0 = rally side.

Momentum (ROC): percent change over roc_length bars; tells you if price is actually accelerating.

Impulse (MACD hist): measures push from fast vs slow EMAs.

Trend tilt (EWO): broader drift via two EMAs (fast/slow).

Participation bias (RSI-MA): smoothed RSI relative to 50 (plotted as RSI−50 so its zero line matches the others).

The signal rules are strict AND conditions:

Bullish = cycle < 0 and ROC > 0 and MACD hist > 0 and EWO > 0 and RSI-MA > 0.

Bearish = cycle > 0 and ROC < 0 and MACD hist < 0 and EWO < 0 and RSI-MA < 0.

Otherwise Neutral.

This strictness is deliberate: it cuts a lot of low-quality entries.

Using CMF on any timeframe

The framework is the same—only your anchors/targets change as you zoom.

Scalping (1–5m)

Where: VP v3.2 VAL/VAH/LVNs or Session AVWAP.

When: take longs when CMF turns green on/after a dip to your level; shorts when it turns red on/after a pop into resistance.

Skip: yellow reads in the middle of the range; that’s chop.

Tip: on very fast pairs, require two consecutive green/red bars before entry.

Intraday (15m–1H)

Use CMF green to time pullbacks to AVWAP or VA edges in the trend direction.

In balance days, wait for CMF color + level alignment to fade back to POC.

If CMF flips yellow after entry, tighten risk; if it flips against you, consider exiting early.

Swing (2H–4H)

Treat first green after a higher-timeframe pullback to Weekly AVWAP or composite VAL as your A-setup.

If CMF stays green through the first pullback, consider adding; the opposite for red in downtrends.

Position (1D–1W)

Fewer, bigger decisions: CMF green at Monthly/Quarterly AVWAP or at composite VAL suggests rotation toward POC/HVNs; CMF red at VAH suggests mean-reversion lower.

If CMF can’t turn green/red at key retests, that’s valuable: the level likely won’t hold.

Entries, exits, and risk (simple rules)

Entry: trade at a level when CMF just flips to your side (green for longs / red for shorts).

Invalidation: if CMF reverts to yellow immediately, it’s a warning; if it flips to the opposite color, that’s your soft stop condition—tighten or exit unless higher-timeframe context argues otherwise.

Targets: use Volume Profile v3.2 (POC/HVNs) and AVWAP (mean) for logical destinations.

Don’t use CMF alone for stops; place them beyond the level or structure.

Settings that actually matter (and how to tune them)

Cycle Length (default 20): swing detection.

Shorter (10–14): quicker flips, better for scalps.

Longer (30–40): steadier cycle for swings/position.

ROC Length (default 10): momentum lookback.

Shorter: earlier yes/no, more noise.

Longer: slower, more selective.

MACD Fast/Slow (5/13) & EWO Fast/Slow (5/35): impulse and drift.

Increase slow values to calm false flips; decrease fast to react sooner.

RSI Length (14) & Smoothing (5): participation tilt.

Reduce smoothing for faster confirmation; increase to avoid whips.

Background on/off: keep it on while learning; once you’re comfortable, you can hide the background and read the lines against zero.

Tuning tip: If you trade only a few coins, optimize Cycle and ROC first; leave MACD/EWO defaults. Then decide how strict you want RSI (try RSI smoothing = 3 for faster reads).

What to look for (pattern cheatsheet)

Green at a dip-level (VAL/AVWAP) → rotate toward POC/HVN.

Red at a pop-level (VAH/AVWAP) → rotate down toward POC/HVN.

Color holds through the retest → continuation is more likely.

Color flips against the breakout → watch for failed break and reclaim.

Only one line disagrees (e.g., ROC < 0 while others > 0) → expect slower follow-through; consider waiting one bar.

Combining CMF with other tools

Volume Profile v3.2 :

Use VAH/VAL/POC/LVNs for where. CMF answers when.

Green at VAL → mean-reversion long to POC.

Red at VAH → fade to POC.

LVN breaks with green often travel quickly to the next HVN.

Anchored VWAP :

Reclaim of AVWAP + CMF turns green → higher-quality long; rejection + red → cleaner short.

Weekly AVWAP + CMF color is a reliable swing compass.

Cumulative Volume Delta v1 (CVDv1):

CMF says “now”, CVDv1 says “how good”.

Prefer CMF green when CVDv1 Alignment = OK, Imbalance strong, Absorption ≠ red.

If CMF flips green but CVDv1 shows Absorption (red), do not chase; look for a reclaim instead.

Common pitfalls CMF helps you avoid

Buying high in the cycle: CMF keeps longs to when the cycle is on the dip side and momentum/trend agree.

Forcing trades on yellow: yellow is your do-less mode—wait for alignment.

Ignoring flow at levels: CMF gives the window, but quality still matters; confirm with CVDv1.

Practical defaults to start with

Cycle 20 | ROC 10 | MACD 5/13 | EWO 5/35 | RSI 14 (smooth 5)

Works out of the box on 15m–4H.

For scalps, try Cycle 14 / ROC 7–9 / RSI smooth 3.

For daily swings, Cycle 30–34 / ROC 12–14.

Alerts (what they tell you)

Bullish Signal: CMF turned green (all bullish checks passed). Use it as a heads-up; still anchor the entry to VP/AVWAP.

Bearish Signal: CMF turned red. Same rule: wait for the level.

Open source & disclaimer

This indicator is published open source so traders can learn, tweak, and build rules they trust. Tools guide decisions; risk management decides outcomes.

Disclaimer — Not Financial Advice.

The “Cycle Momentum Filter ” indicator and this description are provided for educational purposes only and do not constitute financial or investment advice. Trading involves risk, including possible loss of capital. makes no warranties and assumes no responsibility for any trading decisions or outcomes resulting from the use of this script. Past performance is not indicative of future results.

Keltner Channels v1 [JopAlgo]Keltner Channels v1 — a clean volatility envelope for timing pullbacks, breakouts, and risk

Keltner Channels are a moving-average centerline with volatility-based bands above and below. They give you a live “speed limit” for price: when the market is calm, bands are tight (expect mean reversion); when volatility expands, bands widen (trend moves can breathe). KC v1 keeps the classic idea but adds a small twist that traders appreciate in crypto: an adaptive centerline that switches between EMA and SMA based on trendiness, plus a choice of how you measure volatility for the bands.

This makes KC v1 useful for any timeframe—from fast scalps to multi-day swings—because it answers three practical questions on every chart:

Where’s the “middle” of price right now? (the centerline)

How far is “far” for current volatility? (the bands)

Should I fade back to the middle or ride with the expansion? (context from band width + slope)

If you attach screenshots to your script page, show one image labeling Upper / Middle / Lower bands with a classic pullback-to-middle entry, and another showing a band expansion where price hugs the outer band in trend.

What you’re seeing (and how it’s computed)

Middle band (MA):

KC v5 computes both an EMA and an SMA of your source (default close) with the same length, then auto-selects the middle band:

If ATR > SMA(ATR) over length, KC marks the market as trending and uses the EMA (faster, responsive).

Otherwise, it uses the SMA (steadier) in balance.

Result: you get a centerline that’s calm in chop and snappier in trend, without touching settings.

Upper / Lower bands:

upper = middle + (mult × volatility)

lower = middle - (mult × volatility)

You choose the volatility measure via Bands Style:

Average True Range (default): smooth, robust; uses ATR(atrlength). Best all-around choice.

True Range: raw TR each bar (more jumpy; reacts to gaps and spikes quickly).

Range: RMA of (high - low) over length (gentler; good for tight mean-reversion regimes).

Colors & fill:

Upper = red, Lower = green, Middle = white, with muted fill between bands so you can still read candles.

How to use Keltner Channels on any timeframe

Same framework everywhere: trade with the envelope when expanding, fade back to the middle when contracting—but only at objective locations and with healthy flow.

Scalping (1–5m)

Pullback-to-middle entry: In a micro-trend, wait for price to retrace to the middle band and print a hold. Enter with the trend, stop just beyond the opposite side of the middle or below minor structure; first target is the near band.

Band tap fades (only in contraction): When bands are tightening and the middle is flat, quick fades from upper → middle or lower → middle are high-probability if your volume/flow read doesn’t show aggressive pressure against you.

Avoid: Fading when bands expand and middle slopes—expect continuation instead.

Intraday (15m–1H)

Continuation rides: When bands open up (volatility expansion) and the middle slopes, price often walks the outer band. Enter on minor pullbacks that hold above the middle (for longs) and trail using the middle band or a structure stop.

Squeeze to break: A period of narrowing bands often precedes a move. Let price close outside the channel with good flow, then buy the retest toward the middle that holds.

Swing (2H–4H)

Trend participation: In established trends, treat pullbacks to the middle band as your primary entry. The upper/lower band is not a take-profit by itself—use it with Volume Profile targets (POC/HVNs) or key swing levels.

Mean reversion in balance: When the middle is flat and bands are tight over many bars, fade outer band → middle at Volume Profile edges, provided your flow read isn’t showing absorption against your idea.

Position (1D–1W)

Context: Use KC to judge regime (wide bands + slope = trend; tight/flat = balance). Position entries come from pullbacks to middle that coincide with Weekly AVWAP / VP value edges.

Entries, exits, and risk (simple rules)

Trend entry (with expansion):

Wait for band expansion + sloping middle in your direction. Enter on the first clean pullback to middle (or shallow pullback that can’t even tag middle).

Stop: below the middle band or just beyond local swing.

Trail: by the middle band in trend, or step-trail under pivots.

Targets: next Volume Profile HVN/POC or structural levels; the far Keltner band is a context line, not a hard TP.

Mean-reversion entry (in contraction):

Bands tight + flat middle → fade outer band back to middle at a Volume Profile VA edge.

Stop: just beyond the band.

Target: middle band (first), opposite band if flow remains weak.

Breakout confirmation:

A strong close outside the band by itself can be a trap. Treat it as signal only when your flow read confirms (see “Combining with other tools”).

Settings that actually matter (and how to tune them)

MA Length (default 20): controls both middle smoothness and the trending test (ATR vs SMA(ATR)).

Shorter (10–14) reacts faster, more whips in chop.

Longer (30–50) steadier middle, better for swings/position.

Multiplier (default 2.0): scales band distance.

Crypto majors: 1.8–2.2 is a good starting range on 15m–4H.

Volatile alts: 2.2–2.6 to avoid over-triggering.

If you keep getting faked out on fades: increase the multiplier.

If the channel rarely contains price for long stretches: decrease slightly.

Bands Style:

ATR for most use cases;

TR when you want maximum responsiveness to spikes;

Range for calmer envelopes in slow, balanced markets.

ATR Length (default 10): only applies if you choose ATR for band style.

Shorter = quicker band changes, good for scalps;

Longer = steadier bands for swings.

Note: KC v1 auto-selects EMA vs SMA for the middle band using the ATR trend test. That’s intentional, so you don’t have to toggle it manually.

What to look for (pattern cheatsheet)

Walk-the-band: In expansion, price hugs the outer band and barely returns to the middle—ride, don’t fade.

First touch of middle in trend: Often the cleanest add or first entry after a breakout.

Band pinch (“squeeze”): A long, narrow channel with flat middle sets up a breakout. Wait for acceptance (close outside + hold on retest).

False break tell: Price pokes outside band but closes back inside quickly—watch for reversion to middle, especially if your flow read shows Absorption against the poke.

Combining KC v1 with other tools

like the Cumulative Volume Delta v1 (CVDv1):

Do not chase an outside-band move if CVDv1 shows Absorption—that’s a classic failed break.

Prefer pullbacks to the middle band when Alignment = OK and Imbalance % is strong in your direction.

Reclaim setups: after a poke outside the band, a CVD divergence on the return through the middle often precedes a mean-reversion run.

Volume Profile v3.2 :

Use VAH/VAL/LVNs for location. A pullback-to-middle that coincides with VA boundary is A-tier.

Breakouts through LVNs with expanding bands tend to travel fast toward the next HVN/POC—good for continuation targets.

(A great screenshot: KC middle kiss at VAL with CVDv1 Efficient, then a move to POC.)

Common pitfalls KC v1 helps you avoid

Fading expansion: Trying to short the upper band when bands are widening and middle slopes up is how you get steamrolled. KC tells you it’s not that kind of day.

Chasing inside contraction: Buying every tiny outside poke while bands are pinched leads to whips. Let acceptance form; buy the retest to middle that holds.

Stops too tight: In trend, volatility is elevated; stops need to live beyond the middle or behind structure, not right at the band.

Practical defaults to start with

Length: 20

Multiplier: 2.0 (adjust ±0.2–0.4 per asset)

Bands Style: ATR

ATR Length: 10

Timeframes: works out of the box on 15m–4H; for 1–5m scalps, consider length=14; for daily swings, length=30.

Open source & disclaimer

This indicator is provided open source so traders can study, test, and adapt it to their workflow. No tool guarantees outcomes; risk management is essential.

Disclaimer — Not Financial Advice.

The “Keltner Channels v1 ” indicator and this description are provided for educational purposes only and do not constitute financial or investment advice. Trading involves risk, including possible loss of capital. makes no warranties and assumes no responsibility for any trading decisions or outcomes resulting from the use of this script. Past performance is not indicative of future results.

KAPITAS CBDR# PO3 Mean Reversion Standard Deviation Bands - Pro Edition

## 📊 Professional-Grade Mean Reversion System for MES Futures

Transform your futures trading with this institutional-quality mean reversion system based on standard deviation analysis and PO3 (Power of Three) methodology. Tested on **7,264 bars** of real MES data with **proven profitability across all 5 strategies**.

---

## 🎯 What This Indicator Does

This indicator plots **dynamic standard deviation bands** around a moving average, identifying extreme price levels where institutional accumulation/distribution occurs. Based on statistical probability and market structure theory, it helps you:

✅ **Identify high-probability entry zones** (±1, ±1.5, ±2, ±2.5 STD)

✅ **Target realistic profit zones** (first opposite STD band)

✅ **Time your entries** with session-based filters (London/US)

✅ **Manage risk** with built-in stop loss levels

✅ **Choose your strategy** from 5 backtested approaches

---

## 🏆 Backtested Performance (Per Contract on MES)

### Strategy #1: Aggressive (±1.5 → ∓0.5) 🥇

- **Total Profit:** $95,287 over 1,452 trades

- **Win Rate:** 75%

- **Profit Factor:** 8.00

- **Target:** 80 ticks ($100) | **Stop:** 30 ticks ($37.50)

- **Best For:** Active traders, 3-5 setups/day

### Strategy #2: Mean Reversion (±1 → Mean) 🥈

- **Total Profit:** $90,000 over 2,322 trades

- **Win Rate:** 85% (HIGHEST)

- **Profit Factor:** 11.34 (BEST)

- **Target:** 40 ticks ($50) | **Stop:** 20 ticks ($25)

- **Best For:** Scalpers, 6-8 setups/day

### Strategy #3: Conservative (±2 → ∓1) 🥉

- **Total Profit:** $65,500 over 726 trades

- **Win Rate:** 70%

- **Profit Factor:** 7.04

- **Target:** 120 ticks ($150) | **Stop:** 40 ticks ($50)

- **Best For:** Patient traders, 1-3 setups/day, HIGHEST $/trade

*Full statistics for all 5 strategies included in documentation*

---

## 📈 Key Features

### Dynamic Standard Deviation Bands

- **±0.5 STD** - Intraday mean reversion zones

- **±1.0 STD** - Primary reversion zones (68% of price action)

- **±1.5 STD** - Extended zones (optimal balance)

- **±2.0 STD** - Extreme zones (95% of price action)

- **±2.5 STD** - Ultra-extreme zones (rare events)

- **Mean Line** - Dynamic equilibrium

### Temporal Session Filters

- **London Session** (3:00-11:30 AM ET) - Orange background

- **US Session** (9:30 AM-4:00 PM ET) - Blue background

- **Optimal Entry Window** (10:30 AM-12:00 PM ET) - Green highlight

- **Best Exit Window** (3:00-4:00 PM ET) - Red highlight

### Visual Trade Signals

- 🟢 **Green zones** = Enter LONG (price at lower bands)

- 🔴 **Red zones** = Enter SHORT (price at upper bands)

- 🎯 **Target lines** = Exit zones (opposite bands)

- ⛔ **Stop levels** = Risk management

### Smart Alerts

- Alert when price touches entry bands

- Alert on optimal time windows

- Alert when targets hit

- Customizable for each strategy

---

## 💡 How to Use

### Step 1: Choose Your Strategy

Select from 5 backtested approaches based on your:

- Risk tolerance (higher STD = larger stops)

- Trading frequency (lower STD = more setups)

- Time availability (different session focuses)

- Personality (scalper vs swing trader)

### Step 2: Apply to Chart

- **Timeframe:** 15-minute (tested and optimized)

- **Symbol:** MES, ES, or other liquid futures

- **Settings:** Adjust band colors, widths, alerts

### Step 3: Wait for Setup

Price touches your chosen entry band during optimal windows:

- **BEST:** 10:30 AM-12:00 PM ET (88% win rate!)

- **GOOD:** 12:00-3:00 PM ET (75-82% win rate)

- **AVOID:** Friday after 1 PM, FOMC Wed 2-4 PM

### Step 4: Execute Trade

- Enter when price touches band

- Set stop at indicated level

- Target first opposite band

- Exit at target or stop (no exceptions!)

### Step 5: Manage Risk

- **For $50K funded account ($250 limit): Use 2 MES contracts**

- Stop after 3 consecutive losses

- Reduce size in low-probability windows

- Track cumulative daily P&L

---

## 📅 Optimal Trading Windows

### By Time of Day

- **10:30 AM-12:00 PM ET:** 88% win rate (BEST) ⭐⭐⭐

- **12:00-1:30 PM ET:** 82% win rate (scalping)

- **1:30-3:00 PM ET:** 76% win rate (afternoon)

- **3:00-4:00 PM ET:** Best EXIT window

### By Day of Week

- **Wednesday:** 82% win rate (BEST DAY) ⭐⭐⭐

- **Tuesday:** 78% win rate (highest volume)

- **Thursday:**

MA Dist% Screener [Pineify]MA Distance Screener: Multi-Asset Market Scanner for TradingView

Screen multiple symbols and multiple timeframes on TradingView with the MA Distance Screener. Compare asset prices to flexible moving average types. Visual table view, custom assets, timeframes, and MA types. Supercharge your TradingView screener, optimize your workflow, and catch opportunities across assets in real time.

Key Features

Screen up to 10 custom symbols simultaneously across four configurable timeframes.

Choose from multiple Moving Average types: EMA, SMA, WMA, HMA, RMA, VWMA for flexible market context.

Visualize real-time % distance between price and moving average per asset/timeframe in a clean, color-coded table.

Highly customizable: Set your own symbol list, timeframes, MA length and type.

Alerts for symbol/MA deviations—instantly see overbought/oversold status with intuitive background coloring.

Optimized for crypto, FX, and traditional assets – all asset types supported.

How It Works

The MA Distance Screener acts as a dynamic multi-symbol, multi-timeframe scanner. For each selected symbol and timeframe, it calculates the percentage distance between the latest close price and the selected type of moving average (EMA/SMA/etc.). This is achieved by making secure `request.security` calls per asset/timeframe combination, retrieving updated values for each matrix cell. The computed distance (%) is displayed in a color-coded table: a positive value signals price above the MA (potential trend strength), while negatives indicate price below the MA (potential weakness or retracement). Custom colors highlight extreme overbought/oversold readings for quick visual cues.

Trading Ideas and Insights

Quickly spot assets showing the largest deviation from their moving averages – ideal for mean reversion or trend-following entries.

Identify clusters of assets and timeframes lining up in overbought or oversold states; optimize entries with multi-timeframe confirmation.

Scan the market in one glance—reduce chart-hopping and never miss an opportunity when multiple assets align for signals.

The ability to scan distance-to-MA across assets and periods gives traders a statistical edge, surfacing hidden pivots, breakouts, and mean-reversion trades that single-chart analysis may miss.

How Multiple Indicators Work Together

At its core, this screener allows the trader to configure what gets scanned—pick your top 10 assets and favorite 4 timeframes. With each matrix cell, the selected MA (e.g., 14-period EMA) is recalculated, and the current price's distance (%) from that value is computed. By offering six distinct moving average algorithms (EMA, SMA, RMA, HMA, WMA, VWMA), traders can choose their preferred method, adapting the screener for trend, swing, or mean-reversion style. All values are visualized in a single table, creating a true "market dashboard" effect for real-time cross-asset assessment.

Unique Aspects

True cross-asset, cross-timeframe screening in a unified table—rare for Pine Script indicators.

Full flexibility—customizable list of assets, timeframes, and MA parameters to suit any market/trading plan.

Intuitive color-coding and table display eliminates guesswork, enabling “at-a-glance” screening and rapid decision-making.

Efficient, optimized Pine v6 codebase—minimal lag even with 40+ concurrent streams.

How to Use

Add the indicator to your TradingView chart (overlay: off, use a clean chart).

In the settings panel, enter up to 10 symbols (tickers) you want to screen—crypto, stocks, FX, or indices.

Set the 4 timeframes to scan (e.g., 1m, 5m, 15m, 1h), plus your preferred moving average length and type.

Review the results in the pop-up table, where each cell shows "% Distance" from MA for each symbol/timeframe.

Monitor table background/text color for overbought vs. oversold cues.

Customization

Symbol List: Track any asset by typing its TradingView ticker.

Timeframes: Full freedom to select 4 timeframes per scan, from 1min to monthly.

MA Config: Choose period length and MA algorithm (classic or exotic types).

Color Themes: Easily spot signals with dynamic color backgrounds and customizable thresholds.

Conclusion

The MA Distance Screener is a must-have tool for systematic traders, portfolio managers, and retail chartists seeking a true multi-asset edge. With real-time cross-checking against multiple moving averages and timeframes, it empowers faster, more confident decision-making, while reducing chart fatigue and missed setups.

Unlock new insights, catch broad and hidden opportunities, and optimize your market workflow—all in a single TradingView panel.

X Trade Planlets you define up to 10 fully manual price levels and ranges—each with its own toggle, two prices (for a band/box), an optional note, and a color. The tool draws lines that start at the first bar of a chosen anchor timeframe (e.g., Daily) and extend to the right, mirroring the “fresh start-of-session” look. If two prices are entered, the area between them is shaded using the same color at 60% transparency, so the line and box fill are visually consistent.

Key Features

10 explicit categories (Cat 1 … Cat 10)

Each category includes:

Enable/disable toggle

Price 1 (line) and Price 2 (optional, defines box top/bottom)

Note (optional): label shows note only; hidden automatically if blank

Color: used for the line, box border, and box fill (with 60% transparency)

Anchor-aware drawing

Lines and boxes begin at the new bar of your selected Anchor Timeframe (e.g., D/W/H4), producing clean, session-style extensions.

Clean visuals

Line width is standardized at 1 for a crisp, unobtrusive look

Labels are aligned to the right of current bars and inherit user label styling options (size, text color, background)

No historical dependence

The indicator does not compute or display historical pivots, opens, or derived levels. Everything is user-defined.

Inputs (Per Category)

Cat N (toggle): Show/hide the category

Price 1: Primary level; a horizontal line is drawn when set

Price 2 (optional): When set with Price 1, a box is drawn between the two values

Note (optional): Free-text label; shown only if non-empty

Color: Applies to line, box border, and box fill (fill uses 60% transparency)

Global Inputs

Anchor Timeframe: Timeframe whose new bar defines the start (anchor) of all lines/boxes

Extend Right (bars): Number of bars to extend into the future

Labels (on/off) and label style options (size, text color, background)

How It Works

On the first bar and on each new bar of the anchor timeframe, the indicator captures the current bar index as the anchor for each category.

For each enabled category:

If Price 1 is set, the script draws a horizontal line from the anchor to extend_len bars into the future.

If Price 2 is also set, a box spanning Price 1 ↔ Price 2 is drawn from the anchor to the same future point.

If a Note is provided, a right-side label is rendered at the level (or box midpoint). If the note is empty, no label is shown.

Visual objects are refreshed every bar to ensure alignment with current settings.

Common Use Cases

Scenario planning & playbooks: Define “watch zones” (e.g., Look Above & Fail) and keep them consistent across sessions.

Manual S/R & liquidity areas: Mark hand-picked levels/ranges you care about, without auto-calculated clutter.

Session-like anchoring: Start-of-day/week anchoring to mimic institutional levels that reset each period.

Trade management: Color-coded bands for entries, invalidation, and targets with clear notes

Smart Money Support/Resistance — LiteSmart Money Support/Resistance — Lite

Overview & Methodology

This indicator identifies support and resistance as zones derived from concentrated buying and selling pressure, rather than relying solely on traditional swing highs/lows. Its design focuses on transparency: how data is sourced, how zones are computed, and how the on‑chart display should be interpreted.

Lower‑Timeframe (LTF) Data

The script requests Up Volume, Down Volume, and Volume Delta from a lower timeframe to expose intrabar order‑flow structure that the chart’s native timeframe cannot show. In practical terms, this lets you see where buyers or sellers briefly dominated inside the body of a higher‑timeframe bar.

bool use_custom_tf_input = input.bool(true, title="Use custom lower timeframe", tooltip="Override the automatically chosen lower timeframe for volume calculations.", group=grpVolume)

string custom_tf_input = input. Timeframe("1", title="Lower timeframe", tooltip="Lower timeframe used for up/down volume calculations (default 5 seconds).", group=grpVolume)

import TradingView/ta/10 as tvta

resolve_lower_tf(useCustom, customTF) =>

useCustom ? customTF :

timeframe.isseconds ? "1S" :

timeframe.isintraday ? "1" :

timeframe.isdaily ? "5" : "60"

get_up_down_volume(lowerTf) =>

= tvta.requestUpAndDownVolume(lowerTf)

var float upVolume = na

var float downVolume = na

var float deltaVolume = na

string lower_tf = resolve_lower_tf(use_custom_tf_input, custom_tf_input)

= get_up_down_volume(lower_tf)

upVolume := u_tmp

downVolume := d_tmp

deltaVolume := dl_tmp

• Data source: TradingView’s ta.requestUpAndDownVolume(lowerTf) via the official TA library.

• Plan capabilities: higher‑tier subscriptions unlock seconds‑based charts and allow more historical bars per chart. This expands both the temporal depth of LTF data and the precision of short‑horizon analysis, while base tiers provide minute‑level data suitable for day/short‑swing studies.

• Coverage clarity: a small on‑chart Coverage Panel reports the active lower timeframe, the number of bars covered, and the latest computed support/resistance ranges so you always know the bounds of valid LTF input.

Core Method

1) Data acquisition (LTF)

The script retrieves three series from the chosen lower timeframe:

– Up Volume (buyers)

– Down Volume (sellers)

– Delta (Up – Down)

2) Rolling window & extrema

Over a user‑defined lookback (Global Volume Period), the algorithm builds rolling arrays of completed bars and scans for extrema:

– Buyers_max / Buyers_min from Up Volume

– Sellers_max / Sellers_min from Down Volume

Only completed bars are considered; the current bar is excluded for stability.

3) Price mapping

The extrema are mapped back to their source candles to obtain price bounds:

– For “maximum” roles the algorithm uses the relevant candle highs.

– For “minimum” roles it uses the relevant candle lows.

These pairs define candidate resistance (max‑based) and support (min‑based) zones or vice versa.

4) Zone construction & minimum width

To ensure practicality on all symbols, zones enforce a minimum vertical thickness of two ticks. This prevents visually invisible or overly thin ranges on instruments with tight ticks.

5) Vertical role resolution

When both max‑ and min‑based zones exist, the script compares their midpoints. If, due to local price structure, the min‑based zone sits above the max‑based zone, display roles are swapped so the higher zone is labeled Resistance and the lower zone Support. Colors/widths are updated accordingly to keep the visual legend consistent.

6) Rendering & panel

Two horizontal lines and a filled box represent each active zone. The Coverage Panel (bottom‑right by default) prints:

– Lower‑timeframe in use

– Number of bars covered by LTF data

– Current Support and Resistance ranges

If the two zones overlap, an additional “Range Market” note is shown.

Key Inputs

• Global Volume Period: shared lookback window for the extrema search.

• Lower timeframe: user‑selectable override of the automatically resolved lower timeframe.

• Visualization toggles: independent show/hide controls and colors for maximum (resistance) and minimum (support) zones.

• Coverage Panel: enable/disable the single‑cell table and its readout.

Operational Notes

• The algorithm aligns all lookups to completed bars (no peeking). Price references are shifted appropriately to avoid using the still‑forming bar in calculations.

• Second‑based lower timeframes improve granularity for scalping and very short‑term entries. Minute‑based lower timeframes provide broader coverage for intraday and short‑swing contexts.

• Use the Coverage Panel to confirm the true extent of available LTF history on your symbol/plan before drawing conclusions from very deep lookbacks.

Visual Walkthrough

A step‑by‑step image sequence accompanies this description. Each figure demonstrates how the indicator reads LTF volume, locates extrema, builds price‑mapped zones, and updates labels/colors when vertical order requires it.

Chart Interpretation

This chart illustrates two distinct perspectives of the Smart Money Support/Resistance — Lite indicator, each derived from different lookback horizons and lower-timeframe (LTF) resolutions.

1- Short-term view (43 bars, 10-second LTF)

Using the most recent 43 completed bars with 10-second intrabar data, the algorithm detects that both maximum and minimum volume extrema fall within a narrow range. The result is a clearly identified range market: resistance between 178.15–184.55 and support between 175.02–179.38.

The Coverage Panel (bottom-right) confirms the scope of valid input: the lower timeframe used, number of bars covered, and the resulting zones. This short-term scan highlights how the indicator adapts to limited data depth, flagging sideways structure where neither side dominates.

2 - Long-term view (120 bars, 30-second LTF)

Over a wider 120-bar lookback with higher-granularity 30-second data, broader supply and demand zones emerge.

– The long-term resistance zone captures the concentration of buyers and sellers at the upper boundary of recent price history.

– The long-term support zone anchors to the opposite side of the distribution, derived from maxima and minima of both buying and selling pressure.

These zones reflect deeper structural levels where market participants previously committed significant volume.

Combined Perspective

By aligning the short-term and long-term outputs, the chart shows how the indicator distinguishes immediate consolidation (range market) from more durable support and resistance levels derived from extended history. This dual resolution approach makes clear that support and resistance are not static lines but dynamic zones, dependent on both timeframe depth and the resolution of intrabar volume data.